Embed Size (px)

Citation preview

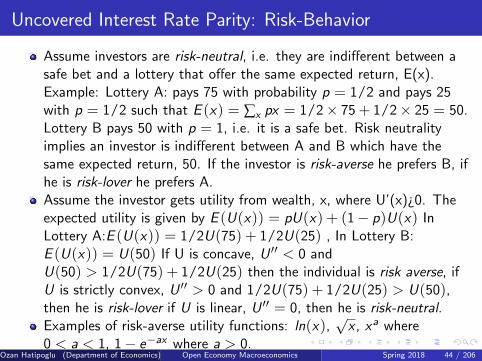

Uncovered Interest Rate Parity: Risk-Behavior

Assume investors are risk-neutral, i.e. they are indifferent between asafe bet and a lottery that offer the same expected return, E(x).Example: Lottery A: pays 75 with probability p = 1/2 and pays 25with p = 1/2 such that E (x) = ∑x px = 1/2× 75 + 1/2× 25 = 50.Lottery B pays 50 with p = 1, i.e. it is a safe bet. Risk neutralityimplies an investor is indifferent between A and B which have thesame expected return, 50. If the investor is risk-averse he prefers B, ifhe is risk-lover he prefers A.

Assume the investor gets utility from wealth, x, where U’(x)¿0. Theexpected utility is given by E (U(x)) = pU(x) + (1− p)U(x) InLottery A:E (U(x)) = 1/2U(75) + 1/2U(25) , In Lottery B:E (U(x)) = U(50) If U is concave, U ′′ < 0 andU(50) > 1/2U(75) + 1/2U(25) then the individual is risk averse, ifU is strictly convex, U ′′ > 0 and 1/2U(75) + 1/2U(25) > U(50),then he is risk-lover if U is linear, U ′′ = 0, then he is risk-neutral.Examples of risk-averse utility functions: ln(x),

√x , xa where

0 < a < 1, 1− e−ax where a > 0.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 44 / 206

Uncovered Interest Rate Parity: Risk-Behavior

Assume investors are risk-neutral, i.e. they are indifferent between asafe bet and a lottery that offer the same expected return, E(x).Example: Lottery A: pays 75 with probability p = 1/2 and pays 25with p = 1/2 such that E (x) = ∑x px = 1/2× 75 + 1/2× 25 = 50.Lottery B pays 50 with p = 1, i.e. it is a safe bet. Risk neutralityimplies an investor is indifferent between A and B which have thesame expected return, 50. If the investor is risk-averse he prefers B, ifhe is risk-lover he prefers A.Assume the investor gets utility from wealth, x, where U’(x)¿0. Theexpected utility is given by E (U(x)) = pU(x) + (1− p)U(x) InLottery A:E (U(x)) = 1/2U(75) + 1/2U(25) , In Lottery B:E (U(x)) = U(50) If U is concave, U ′′ < 0 andU(50) > 1/2U(75) + 1/2U(25) then the individual is risk averse, ifU is strictly convex, U ′′ > 0 and 1/2U(75) + 1/2U(25) > U(50),then he is risk-lover if U is linear, U ′′ = 0, then he is risk-neutral.

Examples of risk-averse utility functions: ln(x),√

x , xa where0 < a < 1, 1− e−ax where a > 0.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 44 / 206

Uncovered Interest Rate Parity: Risk-Behavior

Assume investors are risk-neutral, i.e. they are indifferent between asafe bet and a lottery that offer the same expected return, E(x).Example: Lottery A: pays 75 with probability p = 1/2 and pays 25with p = 1/2 such that E (x) = ∑x px = 1/2× 75 + 1/2× 25 = 50.Lottery B pays 50 with p = 1, i.e. it is a safe bet. Risk neutralityimplies an investor is indifferent between A and B which have thesame expected return, 50. If the investor is risk-averse he prefers B, ifhe is risk-lover he prefers A.Assume the investor gets utility from wealth, x, where U’(x)¿0. Theexpected utility is given by E (U(x)) = pU(x) + (1− p)U(x) InLottery A:E (U(x)) = 1/2U(75) + 1/2U(25) , In Lottery B:E (U(x)) = U(50) If U is concave, U ′′ < 0 andU(50) > 1/2U(75) + 1/2U(25) then the individual is risk averse, ifU is strictly convex, U ′′ > 0 and 1/2U(75) + 1/2U(25) > U(50),then he is risk-lover if U is linear, U ′′ = 0, then he is risk-neutral.Examples of risk-averse utility functions: ln(x),

√x , xa where

0 < a < 1, 1− e−ax where a > 0.Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 44 / 206

Behavioral assumptions

To derive any parity condition we need to have certain assumptionsregarding investor characteristics and behavior. We assume investors arerational and they are risk neutral. Overall the market equilibrium parityconditions will be determined by the rationality and risk-neutralityassumption, but individual traits and decisions might differ. Rationalityimplies agents maximise their utility from wealth when making decisionsand risk neutrality is defined as above.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 45 / 206

Random walk

In empirical work when one tries to estimate the following equation usingexchange rates for Yt ,Yt+1 = aYt + εt+1

where εt is distributed with N(0, 1)and captures unexpected news, shocks, disturbances, etc., the estimate ofa, a, turns out to be 1, i.e. in the statistical test, Ho : a = 1, Ha : a 6= 1,Ho can not be rejected. This means Yt+1 = Yt + εt+1

forming conditional expectations to find a forecast for Yt+1 (see classnotes for the difference between conditional and unconditionalexpectation) ,Et(Yt+1|It) = Et(Yt |It) + Et(εt+1|It)Since Et(εt+1|It) = 0 and Et(Yt |It) = Yt , therefore Et(Yt+1|It) = Yt , i.e.the best forecast one can make is to predict the exchange rates will remainthe same. The link between the market efficiency and the random walkhypothesis will be discussed in class.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 46 / 206

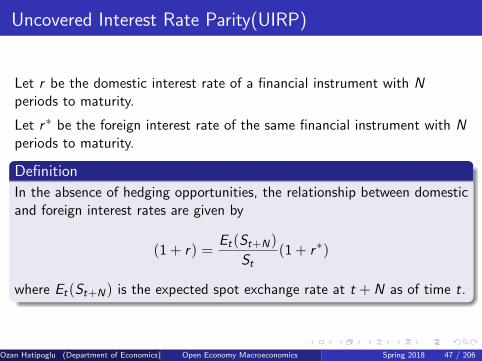

Uncovered Interest Rate Parity(UIRP)

Let r be the domestic interest rate of a financial instrument with Nperiods to maturity.

Let r∗ be the foreign interest rate of the same financial instrument with Nperiods to maturity.

Definition

In the absence of hedging opportunities, the relationship between domesticand foreign interest rates are given by

(1 + r) =Et(St+N)

St(1 + r∗)

where Et(St+N) is the expected spot exchange rate at t + N as of time t.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 47 / 206

UIRP Example

Ayse has 10TL. Let St = 1.6(TL/$), r = 8%, r∗ = 5%(US),Et(St+1) = 1.8. Should Ayse invest in Turkey or US?

If Ayse is risk neutral than she will be indifferent if both bets have thesame expected return otherwise she will pick the bet with higherreturn.

10× (1 + 0.08) = 10. 8TL Return from investing in Turkey

10× 11.6 (1 + 0.05)× 1.8 = 11. 813TL Expected Return from

investing in US.

Should invest in US

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 48 / 206

UIRP Example

Ayse has 10TL. Let St = 1.6(TL/$), r = 8%, r∗ = 5%(US),Et(St+1) = 1.8. Should Ayse invest in Turkey or US?

If Ayse is risk neutral than she will be indifferent if both bets have thesame expected return otherwise she will pick the bet with higherreturn.

10× (1 + 0.08) = 10. 8TL Return from investing in Turkey

10× 11.6 (1 + 0.05)× 1.8 = 11. 813TL Expected Return from

investing in US.

Should invest in US

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 48 / 206

UIRP Example

Ayse has 10TL. Let St = 1.6(TL/$), r = 8%, r∗ = 5%(US),Et(St+1) = 1.8. Should Ayse invest in Turkey or US?

If Ayse is risk neutral than she will be indifferent if both bets have thesame expected return otherwise she will pick the bet with higherreturn.

10× (1 + 0.08) = 10. 8TL Return from investing in Turkey

10× 11.6 (1 + 0.05)× 1.8 = 11. 813TL Expected Return from

investing in US.

Should invest in US

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 48 / 206

UIRP Example

Ayse has 10TL. Let St = 1.6(TL/$), r = 8%, r∗ = 5%(US),Et(St+1) = 1.8. Should Ayse invest in Turkey or US?

If Ayse is risk neutral than she will be indifferent if both bets have thesame expected return otherwise she will pick the bet with higherreturn.

10× (1 + 0.08) = 10. 8TL Return from investing in Turkey

10× 11.6 (1 + 0.05)× 1.8 = 11. 813TL Expected Return from

investing in US.

Should invest in US

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 48 / 206

UIRP Example

Ayse has 10TL. Let St = 1.6(TL/$), r = 8%, r∗ = 5%(US),Et(St+1) = 1.8. Should Ayse invest in Turkey or US?

If Ayse is risk neutral than she will be indifferent if both bets have thesame expected return otherwise she will pick the bet with higherreturn.

10× (1 + 0.08) = 10. 8TL Return from investing in Turkey

10× 11.6 (1 + 0.05)× 1.8 = 11. 813TL Expected Return from

investing in US.

Should invest in US

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 48 / 206

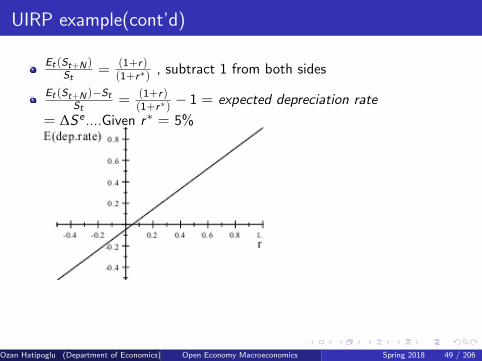

UIRP example(cont’d)

Et (St+N )St

= (1+r)(1+r∗) , subtract 1 from both sides

Et (St+N )−StSt

= (1+r)(1+r∗) − 1 = expected depreciation rate

= ∆Se ....Given r∗ = 5%

An increase in r results in either Et(St+N) ↑ or St ↓ or both. Iflong-run equilibrium is fixed Et(St+N), then only St ↓ .

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 49 / 206

UIRP example(cont’d)

Et (St+N )St

= (1+r)(1+r∗) , subtract 1 from both sides

Et (St+N )−StSt

= (1+r)(1+r∗) − 1 = expected depreciation rate

= ∆Se ....Given r∗ = 5%

An increase in r results in either Et(St+N) ↑ or St ↓ or both. Iflong-run equilibrium is fixed Et(St+N), then only St ↓ .

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 49 / 206

UIRP example(cont’d)

Et (St+N )St

= (1+r)(1+r∗) , subtract 1 from both sides

Et (St+N )−StSt

= (1+r)(1+r∗) − 1 = expected depreciation rate

= ∆Se ....Given r∗ = 5%

An increase in r results in either Et(St+N) ↑ or St ↓ or both. Iflong-run equilibrium is fixed Et(St+N), then only St ↓ .

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 49 / 206

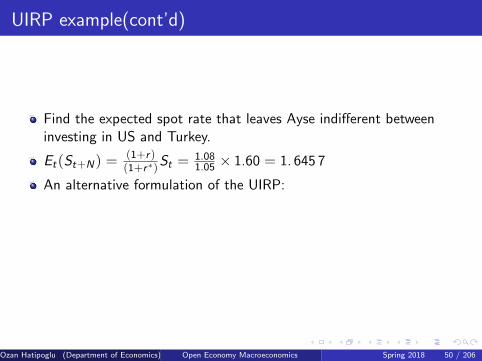

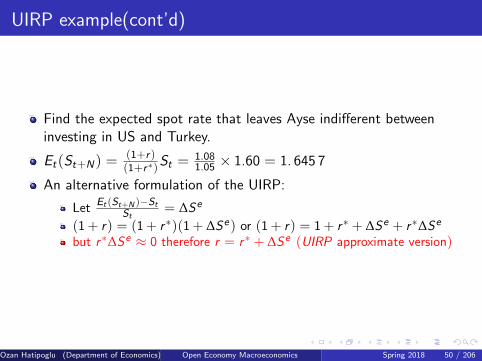

UIRP example(cont’d)

Find the expected spot rate that leaves Ayse indifferent betweeninvesting in US and Turkey.

Et(St+N) =(1+r)(1+r∗)St =

1.081.05 × 1.60 = 1. 645 7

An alternative formulation of the UIRP:

LetEt (St+N )−St

St= ∆Se

(1 + r) = (1 + r∗)(1 + ∆Se) or (1 + r) = 1 + r∗ + ∆Se + r∗∆Se

but r∗∆Se ≈ 0 therefore r = r∗ + ∆Se (UIRP approximate version)

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 50 / 206

UIRP example(cont’d)

Find the expected spot rate that leaves Ayse indifferent betweeninvesting in US and Turkey.

Et(St+N) =(1+r)(1+r∗)St =

1.081.05 × 1.60 = 1. 645 7

An alternative formulation of the UIRP:

LetEt (St+N )−St

St= ∆Se

(1 + r) = (1 + r∗)(1 + ∆Se) or (1 + r) = 1 + r∗ + ∆Se + r∗∆Se

but r∗∆Se ≈ 0 therefore r = r∗ + ∆Se (UIRP approximate version)

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 50 / 206

UIRP example(cont’d)

Find the expected spot rate that leaves Ayse indifferent betweeninvesting in US and Turkey.

Et(St+N) =(1+r)(1+r∗)St =

1.081.05 × 1.60 = 1. 645 7

An alternative formulation of the UIRP:

LetEt (St+N )−St

St= ∆Se

(1 + r) = (1 + r∗)(1 + ∆Se) or (1 + r) = 1 + r∗ + ∆Se + r∗∆Se

but r∗∆Se ≈ 0 therefore r = r∗ + ∆Se (UIRP approximate version)

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 50 / 206

UIRP example(cont’d)

Find the expected spot rate that leaves Ayse indifferent betweeninvesting in US and Turkey.

Et(St+N) =(1+r)(1+r∗)St =

1.081.05 × 1.60 = 1. 645 7

An alternative formulation of the UIRP:

LetEt (St+N )−St

St= ∆Se

(1 + r) = (1 + r∗)(1 + ∆Se) or (1 + r) = 1 + r∗ + ∆Se + r∗∆Se

but r∗∆Se ≈ 0 therefore r = r∗ + ∆Se (UIRP approximate version)

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 50 / 206

UIRP example(cont’d)

Find the expected spot rate that leaves Ayse indifferent betweeninvesting in US and Turkey.

Et(St+N) =(1+r)(1+r∗)St =

1.081.05 × 1.60 = 1. 645 7

An alternative formulation of the UIRP:

LetEt (St+N )−St

St= ∆Se

(1 + r) = (1 + r∗)(1 + ∆Se) or (1 + r) = 1 + r∗ + ∆Se + r∗∆Se

but r∗∆Se ≈ 0 therefore r = r∗ + ∆Se (UIRP approximate version)

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 50 / 206

UIRP example(cont’d)

Find the expected spot rate that leaves Ayse indifferent betweeninvesting in US and Turkey.

Et(St+N) =(1+r)(1+r∗)St =

1.081.05 × 1.60 = 1. 645 7

An alternative formulation of the UIRP:

LetEt (St+N )−St

St= ∆Se

(1 + r) = (1 + r∗)(1 + ∆Se) or (1 + r) = 1 + r∗ + ∆Se + r∗∆Se

but r∗∆Se ≈ 0 therefore r = r∗ + ∆Se (UIRP approximate version)

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 50 / 206

Risk Premium

In general, agents demand a reward (premium) for the risks they take.

Definition

Risk premium is the anticipated excess return agents demand in return fortaking the risk. A risk averter requires positive risk premium. The higherthe risk-averseness the higher the required premium. risk neutral is willingto undertake the risk for zero risk premium. A risk lover is willing to pay apremium in order to take the risk.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 51 / 206

Risk Premium

The above is a simple definition of the risk premium for individualdecisions. In international macroeconomics, the word risk premiumgenerally refers to the excess return risky countries offer to internationalinvestors. It includes several components, some unobservable and othersobservable. Some countries have historically higher nominal rates thanothers due to higher inflation, higher default risk combined with orindependent of high political and economic risk. To explain thisphenomenon in fully efficient markets with risk-neutral and rationalinvestors, one can utilize parity conditions. For example given the expectedinflation and the expected exchange rate depreciation for a risky country Aand for a riskless country B, nominal rates for A might be still higher thanwhat the parity conditions implies, this means there are unobservable orunmeasurable factors such as risk-appetite (or the degree of riskaverseness) of international investors. Heterogeneous investors withdiffering degrees of averseness (a distribution of risk-averseness acrossinvestors) might be one reason, unobserved or mismeasured expectedinflation might be another reason. We will come back to this later.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 52 / 206

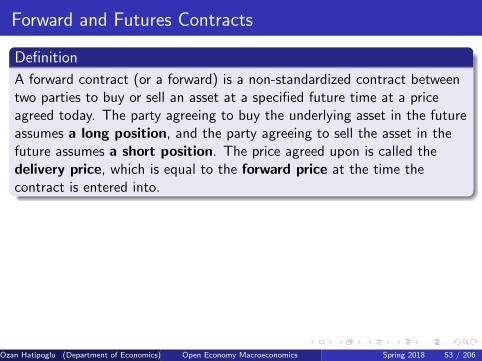

Forward and Futures Contracts

Definition

A forward contract (or a forward) is a non-standardized contract betweentwo parties to buy or sell an asset at a specified future time at a priceagreed today. The party agreeing to buy the underlying asset in the futureassumes a long position, and the party agreeing to sell the asset in thefuture assumes a short position. The price agreed upon is called thedelivery price, which is equal to the forward price at the time thecontract is entered into.

Definition

A futures contract is a standardized financial contract, in which twoparties agree to transact a set of standardized financial instruments orphysical commodities for future delivery at a particular price. In futurescontracts parties can exchange additional property securing the party atgain (margin call) and the entire unrealized gain or loss builds up while thecontract is open.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 53 / 206

Forward and Futures Contracts

Definition

A forward contract (or a forward) is a non-standardized contract betweentwo parties to buy or sell an asset at a specified future time at a priceagreed today. The party agreeing to buy the underlying asset in the futureassumes a long position, and the party agreeing to sell the asset in thefuture assumes a short position. The price agreed upon is called thedelivery price, which is equal to the forward price at the time thecontract is entered into.

Definition

A futures contract is a standardized financial contract, in which twoparties agree to transact a set of standardized financial instruments orphysical commodities for future delivery at a particular price. In futurescontracts parties can exchange additional property securing the party atgain (margin call) and the entire unrealized gain or loss builds up while thecontract is open.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 53 / 206

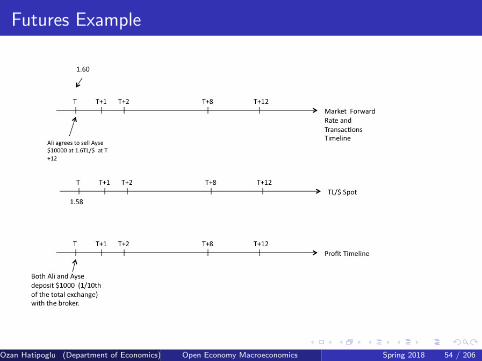

Futures Example

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 54 / 206

Futures Example

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 55 / 206

Futures Example

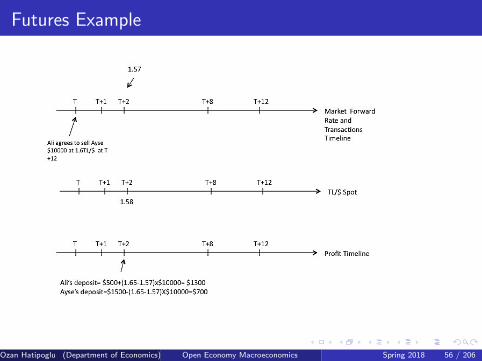

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 56 / 206

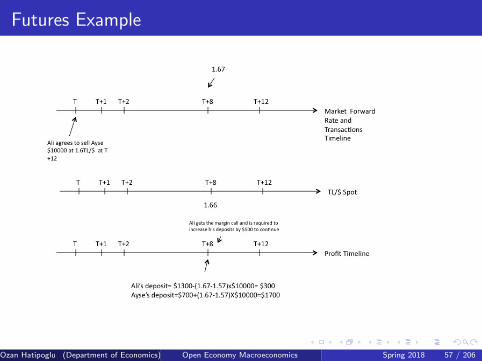

Futures Example

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 57 / 206

Futures Example

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2018 58 / 206

![FM K33 PRENATAL CARE-3.ppt [Read-Only] - ocw.usu.ac.idocw.usu.ac.id/course/download/1110000142-family-medicine/fmd175... · –Risk placenta previa (women high parity) Risk behavior](https://img.pdfslide.net/doc/110x75/5ae57c367f8b9a87048caab3/fm-k33-prenatal-care-3ppt-read-only-ocwusuacidocwusuacidcoursedownload1110000142-family-medicinefmd175risk.jpg)