Embed Size (px)

Citation preview

UNDERSTANDING

MARKET CONNECTEDNESS:

A MARKOV CHAIN APPROACH∗

Harald Schmidbauer†/ Angi Rosch‡/ Erhan Uluceviz§

c© 2012 Harald Schmidbauer / Angi Rosch / Erhan Uluceviz

Abstract

The degree of connectedness of equity markets on a given day can be assessed by decom-

posing the forecast error variance resulting from a vector autoregressive model, applied to

daily returns on stock indices. This well-known procedure leads, for each day, to a spillover

matrix quantifying the contribution of a shock, to which one return series is exposed, to

future variability of other return series. A spillover matrix can be readily interpreted as a

network structure and summarized into the so-called spillover index, to which much recent

research work has been devoted.

Taking a sequence of spillover matrices as starting point, we show how the scope of

this concept can be broadened in several ways. Firstly, we demonstrate how the eigenvalue

structure of spillover matrices contributes to assessing market interaction in the form of in-

formation propagation. Secondly, adopting a Markov chain perspective, we obtain a dynamic

description of market connectedness which can be analyzed in terms of various entropy mea-

sures. Both suggestions are supported by theoretical arguments as well as empirical evidence,

using data from Dow Jones Industrial Average, CAC 40, DAX and Nikkei 225 stock indices.

It turns out that the spillover index is only one, and limited, summary measure of market

connectedness and its manifold aspects.

Key words: Connectedness of equity markets; spillovers; eigenvalue structure; Markov

chains; entropy; transmission of shocks

1 Introduction

There is overwhelming evidence that economic entities are becoming more and more intercon-

nected with each other under ever increasing activities in the fields of trade-credit relationships,

portfolios built on sophisticated derivatives, cross-border mergers and acquisitions, just to name

a few. However, quantifying the extent and intensity of the connectedness and understanding

its dynamics is still a daunting task to be accomplished.

The events leading to the eruption of the recent global financial crisis have fallen into a

period of elevated interconnectedness, but the course of actions may well have contributed to

boosting market connectedness even further, and the developments exemplify the interlockings

of financial institutions and products.

∗This research was presented on the 32nd International Symposium on Forecasting ISF 2012, held in Boston,

MA (USA), June 24-27, 2012. The paper is published in: The International Institute of Forecasters (ed.),

Proceedings of the 32nd International Symposium on Forecasting ISF 2012 , Boston, MA (USA), June 24-27,

2012. ISSN: 1997-4124.†Istanbul Bilgi University, Istanbul, Turkey; e-mail: [email protected]‡FOM University of Applied Sciences, Munich, Germany; e-mail: [email protected]§Istanbul Bilgi University, Istanbul, Turkey; e-mail: [email protected]

1

Following reviews by Mishkin [14] and Baba and Packer [1], the first and more limited phase

from July 2007 to August 2008 arose from losses in one relatively small segment of the U.S. finan-

cial system, namely, the subprime residential mortgages sector which, however, quickly spread to

other markets, especially those of credit and securitized products, sowing the seeds for the global

financial crisis in 2008. Following the decline in real estate prices, losses in mortgage-backed

financial securities (MBS) had to be covered by what turned out to be insufficient collaterals.

The subsequent sale of assets by banks to raise money for the collaterals drove MBS prices fur-

ther down, leading to a vicious circle. Bear Stearns, spiraling from being healthy to practically

insolvent in about 72 hours1, became the first major casualty of the financial crisis. It was

rescued from impending bankruptcy by a deal with JPMorgan Chase & Co. in March of 2008.

As a result of the deal, the Federal Reserve (FED) guaranteed USD 29 billion for toxic assets

in Bear Stearns’ portfolio.

The second phase was mainly triggered by the bankruptcy of Lehman Brothers in September

of 2008. Unlike the Bear Stearns case, the regulators did not step in to bail out the bank. With

the collapse of Lehman Brothers, credit default swaps (CDS) written on subprime mortgage

securities caused huge losses for American International Group, Inc. (AIG) — with bond markets

becoming more sophisticated, investors found it more convenient to trade CDSs than to buy

and to sell actual bonds. One day after the collapse of Lehman Brothers, the FED stepped in

with a USD 85 billion (eventually rising to more than USD 170 billion) loan to keep AIG afloat.

The events leading to rescue operations made a term very popular: too-big-to-fail , referring to

financial institutions that would supposedly block the functioning of the world financial system

if allowed to collapse. However, as Mishkin [14] maintains, too-big-to-fail is a misnomer: “A

financial firm can be systemically important, that is, its failure can threaten the health of the

financial system, either because it is so large or its activities are so interconnected with the rest

of the financial system,” concluding that a more accurate term would be “too-interconnected-

to-fail” or “too-systemically-important-to-fail.”

The goal of the present paper is to quantify dynamically the amount of connectedness of

markets with a focus on the flow of information (e.g. “shocks” hitting one of the markets) across

markets.

In a series of papers about market connectedness, Diebold and Yilmaz (see, for example,

[4, 5]) demonstrate that decompositions of error variances of joint asset return forecasts, obtained

from vector autoregressive (VAR) models, can be interpreted to represent a network with assets

as nodes, the strength of links between nodes determined by shares of forecast error variance

spillovers. The point in their approach is not actually to forecast future returns, but rather to

assess the degree of market connectedness, operationalized as spillover of shocks occurring in

one market to other markets in the form of forecast error variance for that market, constructing

the so-called spillover index as a summary measure. In [5] they analyze how connectedness of

the major U.S. banks measured by the spillover index capture network effects. They track both

average and daily time-varying connectedness of major U.S. financial institutions’ stock return

volatilities in recent years, including the time period of the financial crisis of 2007 and 2008.

They apply this methodology to a selection of global equity markets in Diebold and Yilmaz [4].

In the present paper, we understand the term “market connectedness” (or connectedness

for short) as the general phenomenon that markets do not operate in isolation. Building on

the framework established by Diebold and Yilmaz [4, 5], we construct alternative measures of

connectedness which are able to capture features of connectedness neglected by the spillover

index. Concepts borrowed from population dynamics and information theory constitute an

important foundation in our methodology.

The methodology developed in the present paper is illustrated using data from four stock

1The Wall Street Journal, 2009-05-09.

2

01

23

45

67

8

rela

tive

valu

e

djifchigdaxin225

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Figure 1: The level series (with 1988-05-23 ≡ 1)

markets: New York Stock Exchange, Euronext Paris, Frankfurt Stock Exchange and Tokyo

Stock Exchange. Overall, these four markets comprise on average 62% of the world market

capitalization (for the time period from 1997 through 2010) and represent the main economic

centers of the world for the time period in question, namely the U.S., the EU, and East Asia.

This paper is organized as follows. Section 2 describes some properties of the data on which

the study is based. Section 3 reviews the methodology developed by Diebold and Yilmaz [4, 5]

and points out some limitations of their concepts. Section 4 extends the perspective by asking

how repercussions of a shock to one of the markets would ultimately distribute among markets

under the existing spillover scheme, using concepts from population dynamics. In Section 5,

we adopt a Markov Chain perspective to further elucidate dynamic aspects of information flow

between markets. Empirical results are presented in Section 6. Section 7 concludes and discusses

suggestions for further research.

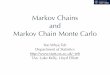

2 Data

The empirical starting point of the present study consists of four time series of daily closing

quotations of the stock indices Dow Jones Industrial Average (New York Stock Exchange, in

the following called dji), the CAC 40 (fchi, Euronext Paris), DAX (gdaxi, Frankfurt Stock Ex-

change), and Nikkei 225 (n225, Tokyo Stock Exchange) in the time period beginning 1988-01-05

(the first day for which all four series were available) and ending 2012-01-24 (6255 observations).

The level series, normed such that 1988-05-23 ≡ 1, are shown in Figure 1. Directly used are

daily simple returns in percent, which are plotted in Figure 2.

A visual inspection of the return series in Figure 2 suggests a simultaneous occurrence of

periods of high volatility in the four markets considered, and the impression that returns are

somehow “connected” is reinforced in Figure 3. However, it appears that n255 is detached from

the other three stock indices in the sense of lower correlation of daily returns. The main tool to

measure the amount of connectedness is based on a decomposition of the forecast error variance

(fevd stands for forecast error variance decomposition), which will be briefly described next.

3

−10

010

dji

−10

010

fchi

−10

010

gdax

i

−10

010

n225

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Figure 2: The series of daily returns

Figure 3: Scatterplots of daily returns

4

3 Measuring spillovers using fevds

3.1 Spillover index and directional spillovers

Given a multivariate (here: 4-dimensional) empirical time series, the fevd results from the

following steps:

1. Fit a standard VAR (vector autoregressive) model to the series.

2. Using series data up to, and including, time t, establish an n period ahead forecast (up to

time t+ n).

3. Decompose the error variance of the forecast for each component with respect to shocks

from the same or other components at time t.

Diebold and Yilmaz [4] propose several connectedness measures derived from variance de-

compositions, and they argue that these measures are intimately related to key measures of

connectedness as used in the network literature. The decomposition of forecast error variance

is given in terms of the structural VAR. This needs to be identified on the basis of the standard

VAR by imposing suitable restrictions in the form of an ordering of the variables. To circumvent

the undesirable dependence on the ordering, following Diebold and Yilmaz [5], we revert to the

so-called generalized fevd, proposed by Pesaran and Shin [15], which remedies the dependence

on the ordering by giving each component of the series in question first priority. For example,

the forecast error variance (fev) for returns on dji is given as

fev(dji) = var

n−1∑i=0

(Φdji

dji(i), Φfchidji (i), Φgdaxi

dji (i), Φn225dji (i)

)×

εdji ,t+n−iεfchi ,t+n−iεgdaxi,t+n−iεn225,t+n−i

, (1)

which can be decomposed into

fev(dji) = σ2dji ·∑n−1

i=0 (Φdjidji)

2(i) + σ2fchi ·∑n−1

i=0 (Φfchidji )2(i) +

σ2gdaxi ·∑n−1

i=0 (Φgdaxidji )2(i) + σ2n225 ·

∑n−1i=0 (Φn225

dji )2(i),(2)

where each Φkl designates an impulse response function from series k to series l. The four terms

in this sum are then divided by fev(dji) to obtain the fevd. This procedure is carried out for each

stock index, and the resulting terms are arranged in the so-called spillover matrix as follows:

from (time t)

dji fchi gdaxi n225

dji � � � �fchi � � � �

to (time t+ n)gdaxi � � � �n225 � � � �

(3)

Each row thus sums up to 1 (or 100%) and provides a breakdown of the forecast error variance

of the corresponding stock index with respect to its origin in terms of percentages. Each entry

in the spillover table is called a directional spillover. Schematically, the spillover index is then

obtained as ∑�∑

� +∑

�. (4)

5

010

2030

4050

6070

spill

over

inde

x (p

erce

nt)

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Figure 4: The spillover index series

3.2 Rolling estimation

A spillover index series was obtained by proceeding along the steps outlined above, where a

moving window of 50 days was used for fitting a sequence of VARs, resulting in a spillover table

for every day, which leads to the spillover index according to equation (4). The result of this

operation is shown in Figure 4, together with a smoothed version (obtained by local polynomial

regression fitting) of the series. This series, and hence market connectedness, has been strongly

increasing since 1994, with intermittent shorter periods of decline. Similar findings were made

by Diebold and Yilmaz [4].

3.3 Limitations of the spillover index

A diagonal entry of 1 in the spillover matrix, and otherwise zeros in the row, indicates that the

respective market is entirely exogenous, as its forecast error variance can only be explained by

market-internal shocks. An entirely endogenous market, on the other hand, features a diagonal

entry of 0 as its forecast error variance is completely due to shocks from other markets (off-

diagonal entries in the row summing up to 1).

Table 1 displays four patterns of spillovers; they are particularly different with respect to

the involvement of market 1. 1 0 0

0 0.4 0.6

0 0.6 0.4

0.6 0.2 0.2

0.1 0.6 0.3

0.1 0.3 0.6

0 0.5 0.5

0.1 0.9 0

0.1 0 0.9

0.7 0 0.3

0.4 0.6 0

0.3 0.2 0.5

(a) (b) (c) (d)

Table 1: Four hypothetical examples: different spillover patterns, but equal spillover index values

While spillover pattern (a) distinguishes market 1 as being not only exogenous, but entirely

isolated, in patterns (b) and (c) the market’s integration and involvement into interactions with

the two other markets is established to a increasing extent, up to being entirely endogenous in

(c). Pattern (d) characterizes market 1 as the one with the highest own contribution share, but

also the highest spillover activity to others. In all four cases, however, the spillover index is

40%. The spillover index alone is not capable to capture the diversity of spillover patterns; it is

a summary measure assessing the “average” amount of spillovers in a system irrespective of its

particular network structure.

6

In the following two sections, we broaden the scope of spillover discussion in two directions:

In Section 4, we start from a static perspective into the eigenvalue structure of the spillover

table. Building on this, we introduces a dynamic, viz. Markov chain perspective in Section 5 .

4 Broadening the perspective I: eigenvectors

The starting point is the spillover matrix on a given day. It refers to a forecast horizon which

produces stable fevd results (5 days were found adequate in our application). While the row

entries characterize the markets’ exposition to shocks, broken down by origin of shock, the

propagation of a shock needs to be read and tracked column-wise. In this sense, a market is

actively interacting with other markets if the respective column contains at least one non-zero

off-diagonal entry.

4.1 Propagation of shocks

The network structure of the spillover matrix, in particular its directional conception with

respect to the propagation of shocks, leads us to broaden the perspective using concepts which

are borrowed from population theory.2 A shock originating from one market and propagating

further in time may be compared to a spark of infection (in a neutral sense), entering, and

spreading in, a system of more or less effective routes of transmission. An entirely exogenous

market will never get “infected” by other markets, but may be able to transmit an “infection”

coming from itself. The column entries in the spillover matrix may be interpreted as (average)

amounts of direct transmission between markets in one time unit. For example, in the case of

spillover table (b) in Table 1, an initial shock of unit size to market 2 will result in a shock of

size 0.2 to market 1 and a shock of size 0.3 to market 3, while diminishing to size 0.6 in market 2

itself; this can be written as M · (0, 1, 0)T = (0.2, 0.6, 0.3)T . To further exploit and develop this

idea, we make the following assumptions:

1. The propagation of a shock across markets can be modeled by the transmission equation

n1 = M ·n0, where M denotes the spillover matrix of a certain day and n0 is a unit vector

indicating the market from which the shock comes. This concept of shock transmission

(or propagation) dynamics is analogous to matrix population models.

2. The propagation of a shock (or of “information” in this sense) can take place in a short time

interval of unspecified length. The subsequent shock propagation (or the “repercussions”

of the shock) can be modeled recursively as

ns+1 = M · ns, s = 0, 1, 2, . . . (5)

(step s = 0 initializes the recursion). The index s in equation (5) therefore denotes a

hypothetical step in information flow. Moreover, assuming that information flow across

markets can proceed instantly, with spillover conditions persisting throughout the day in

question, it makes sense to investigate steady-state properties (as s → ∞) of the model

defined by equation (5).

The four hypothetical examples from Table 1 will serve to illustrate the dynamics of shock

propagation, and its relation to where a shock comes from; see Table 2.

Under spillover conditions (a), the shock propagation ultimately (as s→∞) depends heavily

on where the shock originates. This peculiarity is due to the limited connectedness of markets

in this example. In examples (b), (c) and (d), however, the shock distribution will become

2A detailed review of matrix population models can be found in the book by Caswell [2].

7

Spillover Shock comes from market

matrix 1 2 3

number of steps number of steps number of steps

1 2 ∞ 1 2 ∞ 1 2 ∞1 1 1 0 0 0 0 0 0

(a) 0 0 0 0.4 0.52 0.5 0.6 0.48 0.5

0 0 0 0.6 0.48 0.5 0.4 0.52 0.5

0.6 0.40 0.20 0.2 0.30 0.40 0.2 0.30 0.40

(b) 0.1 0.15 0.20 0.6 0.47 0.40 0.3 0.38 0.40

0.1 0.15 0.20 0.3 0.38 0.40 0.6 0.47 0.40

0 0.10 0.09 0.5 0.45 0.45 0.5 0.45 0.45

(c) 0.1 0.09 0.09 0.9 0.86 0.45 0 0.05 0.45

0.1 0.09 0.09 0 0.05 0.45 0.9 0.86 0.45

0.7 0.58 0.53 0 0.06 0.16 0.3 0.36 0.32

(d) 0.4 0.52 0.53 0.6 0.36 0.16 0 0.12 0.32

0.3 0.44 0.53 0.2 0.22 0.16 0.5 0.34 0.32

Table 2: Four hypothetical examples: courses of shock propagation

stationary in the long run, which means that shock repercussions ultimately settle equally among

the three markets, irrespective of the initial shock’s origin. Here, all markets in the system are

at least indirectly connected. However, the ultimate relative impact level does depend on the

shock’s origin: In examples (b) and (c), a shock coming from market 1 produces the lowest

impact level as compared to other origins, while example (d) draws a different picture. The

following ratios of impact levels result from the hypothetical spillover matrices (b), (c) and (d):

1: 2 : 2, 1 : 5 : 5, and 1 : 0.3 : 0.6, respectively. In real markets, tracing impact level ratios can

provide valuable insight into the relative time-dependent dynamics of shock propagation, and

hence vulnerability, of connected markets; see Section 6 below. We shall see in the following

how these ratios can be related to the eigenvalue structure of the spillover matrix.

4.2 Eigenvalue structure of the spillover table

In analogy to life cycle concepts in population theory, the network structure of the spillover

matrix can be translated into a “shock cycle graph”. If the graph is strongly connected in

the sense that each pair of markets is connected within a finite number of transitions, Perron-

Frobenius theory carries over (see e.g. Seneta [18] and Caswell [2]). Then, the spillover matrix is

irreducible and primitive, and its right eigenvector N corresponding to the dominant eigenvalue 1

(a consequence of the row-stochasticity of the matrix), satisfying

N = M · N, (6)

is unique up to a scalar, and describes the stable relative impact structure in the long run.

Further insight into the spillover pattern can be derived from the corresponding left eigen-

vector v:

vT = vT ·M (7)

It permits a discussion of “propagation values” of markets in analogy to the notion of “reproduc-

tive values” for population age groups: The propagation value of a market renders the value of

a shock which comes from the market as seed for future impact variability. (The interpretation

8

of propagation values in terms of the stationary distributions of a Markov chain, defined on the

basis of a spillover table, will be one of the topics of Section 5.)

Recalling the hypothetical spillover patterns of Table 1, it is obvious that example (a) does

not meet the condition of strong connectedness, while examples (b), (c) and (d) do. The corre-

sponding shock propagation dynamics are displayed in Table 2; the associated eigenvectors are

given in Table 3.

left right

n.a. not

n.a. unique

n.a.

left right

1 1/3

2 1/3

2 1/3

left right

1 1/3

5 1/3

5 1/3

left right

1 1/3

0.3 1/3

0.6 1/3

(a) (b) (c) (d)

Table 3: Four hypothetical examples: left and right eigenvectors (corresponding to eigenvalue

1)

The long-run “spread” given by the right eigenvector is the same whenever markets are

strongly connected, indicating an even shock propagation in the long run. However, the mar-

kets’ “propagation values”, which are the left eigenvector components, can be different: In

example (c), a shock coming from market 2 (or 3) has five times the power of a shock from mar-

ket 1, while market 1 stands out as the most powerful one with respect to shock propagation in

example (d). — Remember that the spillover index equals 40% for all examples (a) through (d).

Two further examples may illustrate that the notion of a market’s “propagation value” does

not simply mirror its direct spillover to other markets; cf. Table 4. 0.6 0.2 0.2

0.2 0.6 0.2

0.2 0.2 0.6

0.7 0 0.3

0.4 0.5 0.1

0 0.4 0.6

left right

1 1/3

1 1/3

1 1/3

left right

1 1/3

0.75 1/3

0.9375 1/3

Table 4: Two examples with equal aggregate spillovers (and equal spillover index values)

These examples again share a spillover index of 40%, as well as aggregate spillovers to other

markets of 0.4. However, there is a fundamental difference in the system’s behavior which would

be disregarded when confining the interest to a single propagation step only. This difference

is — to some extent — captured by means of “propagation values”.

5 Broadening the perspective II: Markov chains

Exposing one among several connected markets to a shock can be seen as injecting information

into a system of markets, with the market in question as initial transformation channel. As

shown in Section 4, newly injected information will ultimately distribute evenly among the

markets, provided they are connected. How fast is this information (this shock) “digested” by

the system of markets? This question can be discussed in terms of the speed of convergence of

a distribution of a Markov chain, determined by the shock, to the stationary distribution. We

9

shall see that there may be markets from which a shock is harder to digest (in the sense of slower

convergence to stationarity) than for others. The amount of information given by a shock that

is retained in the memory of the system of markets depends on how the market is connected

to other markets, how these are connected among each other, and on the number of time steps

covered in information flow. The amount of information retained in the long run is proportional

to the “propagation value” of the market from where the shock emanated. The momentum of

initial information can be discussed in terms of the distance of the distribution of a Markov

chain, determined by the shock, to the stationary distribution. Entropy measures, applied to

Markov chains, will provide the framework to discuss these questions. The perspective provided

by the Markov chain approach to spillover analysis is also appealing insofar as it permits a new

interpretation of propagation values, defined in Section 4.2. The mathematical theory of Markov

chains from a non-negative matrix standpoint is presented by Seneta [18].

5.1 A Markov chain perspective

The most important ingredient of a discrete-time Markov chain, the transition matrix, is essen-

tially a collection of conditional distributions in the form of a row- or column-stochastic matrix,

the layout depending on the formalism adopted to update state probabilities. The condition

is expressed in the current state of the process. It is thus clear that a spillover table, as given

by equations (3) and (4), does not constitute the transition matrix of a Markov chain: Col-

umn sums of a spillover table need not equal 1. (Columns constitute the “from” part, i.e. they

specify the condition.) Coerced into the Markov chain scheme, spillover tables would make the

Markov chain run in reverse time (“from” followed by “to”). However, it is again a concept from

population dynamics that provides the necessary means to define a Markov chain properly.

The shock propagation equation (5) transforms into a Markov chain running forward in time

along the following steps (cf. Tuljapurkar [20]): First, it holds that

nTs+1 ·V = nT

s ·V ·V−1 ·MT ·V, s = 0, 1, 2, . . . ,

where the diagonal matrix V is made up by the left eigenvector v of matrix M (corresponding

to eigenvalue 1). Now, the Markov transition matrix can be identified (we use the notation of

Tuljapurkar [20]; subscript “F” means “forward”):

PF = V−1 ·MT ·V, (8)

and after some scaling

πTs =nTs ·V

nT0 · v

,

the Markov chain equation emerges:

πTs+1 = πTs ·PF , s = 0, 1, 2, . . . , (9)

with probability vectors πs.3

In analogy to Tuljapurkar’s [20] application of Markov chain transformation in a population

context, the Markov chain in Equation (9) can be used as a basis for the sequence space descrip-

tion of histories (or genealogies) of shocks, as the realizations of the Markov chain constitute

these histories. In our context, histories would be sequences of integers describing the line of

propagation of a shock by specifying the number of the market to which the shock has been

3The Markov chain transformation running backward in time would employ the matrix M itself as transition

matrix, cf. Tuljapurkar [20], and our introductory remarks.

10

transmitted recently. The conditional one-step transmission probabilities, the condition specify-

ing which market is the transmitting one, are provided by the the rows of the Markov transition

matrix.

Table 5 shows the Markov chain transition matrices we obtain for the hypothetical examples

with spillover matrices introduced in Table 1 of Section 3.3. On the basis of the transition matrix,

one-step, two-step, and long-term transmission probabilities for a shock originally coming from

one particular market can be computed. Results are provided in Table 6.

n.a.

0.6 0.2 0.2

0.1 0.6 0.3

0.1 0.3 0.6

0 0.5 0.5

0.1 0.9 0

0.1 0 0.9

0.7 0.12 0.18

0 0.6 0.4

0.5 0 0.5

(a) (b) (c) (d)

Table 5: Four hypothetical examples: the Markov chain transition matrix (running forward in

time)

Spillover Shock comes from market

matrix 1 2 3

number of steps number of steps number of steps

1 2 ∞ 1 2 ∞ 1 2 ∞

(a) n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

0.6 0.4 0.2 0.1 0.15 0.2 0.1 0.15 0.2

(b) 0.2 0.3 0.4 0.6 0.47 0.4 0.3 0.38 0.4

0.2 0.3 0.4 0.3 0.38 0.4 0.6 0.47 0.4

0 0.10 0.09 0.1 0.09 0.09 0.1 0.09 0.09

(c) 0.5 0.45 0.45 0.9 0.86 0.45 0 0.05 0.45

0.5 0.45 0.45 0 0.05 0.45 0.9 0.86 0.45

0.7 0.58 0.53 0 0.20 0.53 0.5 0.60 0.53

(d) 0.12 0.16 0.16 0.6 0.36 0.16 0 0.06 0.16

0.18 0.26 0.32 0.4 0.44 0.32 0.5 0.34 0.32

Table 6: Four hypothetical examples: transient and stationary distributions of the Markov chain

A comparison of Markov chain results in Table 6 with results from the propagation equa-

tion (5) in Table 2 reveals a general relationship with respect to long-run behavior.

In fact, the Markov chain in Equation (9) becomes stationary in the long run if the spillover

matrix M is irreducible and primitive; cf. Tuljapurkar [20]. According to arguments in Sec-

tion 4.2, this translates into the condition of strongly connected markets. Then, from Equa-

tion (9), it is obvious that the stationary distribution of the Markov chain must equal the

left eigenvector of the Markov transition matrix PF (corresponding to eigenvalue 1). Indeed,

what turns out in particular is that the stationary distribution and the — scaled — vector of

propagation values, introduced as left eigenvector v of M in Section 4.2, are the same:

π =V · uvT · u

=v

|v|. (10)

11

(Recall from Section 4.2 that the vector u denoting the right eigenvector of M corresponding to

eigenvalue 1, has equal components if M is irreducible and primitive.)

Whichever market generates the shock initially, if the system is strongly connected, the

Markov chain will move towards the equilibrium which is governed by the left eigenvector of

the spillover matrix, or, in other words, by the markets’ propagation values. The vector of

propagation values represents the “news balance” of markets in the long run. The origin of

shocks is “forgotten” as shocks are “digested” by the system.

The question of speed of convergence (speed of “digestion” of the shock) and the question

of distance to equilibrium (information momentum) will be addressed in the following section.

5.2 Entropy

Although convergence to the equilibrium is a complex process, concepts from information theory

can be adopted to obtain consistent answers to the above questions.

Kullback-Leibler distance (KLIC)

The Kullback-Leibler distance, or Kullback-Leibler information criterion (KLIC), measures the

relative variability of one probability distribution πa with respect to the variability of a second

distribution πb:4

KLIC =∑i

πa(i) · ln(πa(i)

πb(i)

)(11)

KLIC provides a measure of “information gain” of knowing distribution πa as compared to

distribution πb. If, for example, πa denotes any initial distribution of a Markov chain and πbits stationary distribution, KLIC provides a measure of how distant the initial distribution is

from equilibrium. Translated into the context of shock propagation, it measures the initial

information content of a shock (news) with respect to the news balance between markets in the

long run. Schoen and Kim [17], in a population theoretical context, relate the Kullback-Leibler

distance to the momentum of a population. This idea suggests an analogy to the momentum of

the “injection” of news to the market.

Kolmogorov-Sinai entropy (KS)

The Kolmogorov-Sinai entropy characterizes the dynamical randomness that accompanies the

paths of a stochastic process. Given a set of initial states of the process, it is the exponential rate

at which the number of most probable paths will increase with time, thus measures the rate of

convergence to equilibrium.5 Demetrius [3] introduced this entropy measure to population theory

as “population entropy”; Tuljapurkar [20] relates it to the rate of convergence of a population,

respectively its corresponding Markov chain, to equilibrium:

KS = −∑i,j

π(i) · ln(ppijij

)(12)

Here, pij denote the entries in the transition matrix of the Markov chain, π(i) are the stationary

probabilities. In our application, KS determines the speed at which a shock (news) coming from

a market is being “digested” by the system of markets, in the sense that the system will settle

at its intrinsic “news balance” determined by the properties of the spillover matrix.

Table 7 shows KLIC values and the value of KS which we obtain in our hypothetical examples

introduced in Table 1 of Section 3.3.

4Discrimination information was the original term used by Kullback and Leibler themselves, cf. [11], [12], [13].5In information theory, it is known under the name “Shannon entropy” since the work of Shannon [16];

cf. Kolmogorov [10], and Sinai [19].

12

KLIC (a) (b) (c) (d)

shock comes from

market 1 n.a. 1.609 2.398 0.642

market 2 n.a. 0.916 0.788 1.846

market 3 n.a. 0.916 0.788 1.153

KS n.a. 0.908 0.359 0.753

Table 7: Four hypothetical examples: KLIC under different shock scenarios, and KS

The highest values of KLIC in examples (b) and (c), relate to the extent to which a news

balance between markets is being distorted by shocks (news) coming from market 1. It is the

market with the least aggregate direct spillover to other markets. A comparison of (b) an (c),

however, reveals that heavy back-spillovers from other markets can generate a higher level of

distortion and an extended cycle of “infection”. Consequently, the speed of convergence to a

news balance between markets measured by KS is low in example (c), while the market system

in (b) will recover rather quickly. Remember that these examples share a spillover index of 40%.

6 Empirical findings

The empirical basis of our study of interaction between Dow Jones Industrial Average, CAC

40, DAX and Nikkei 225 stock indices is a daily sequence of return spillover matrices which

resulted from fitting a sequence of VARs along the the steps outlined in Section 3. It was

collapsed into the series of return spillover indices in Figure 4, which indicates an upward trend

in market integration during the past two decades. The spillover index is an appealing summary

measure, however, the network structure of spillovers may differ widely at the same value as

was pointed out in Section 3.3. We will now proceed and apply the theoretical framework which

we established in Sections 4 and 5 to obtain insights into the particularly underlying network

structure, and how it evolved across time.

Can the eigenvalue structure of the spillover matrix contribute to characterizing market

interaction on that day in isolation? To identifying the major player in the sense of news dis-

seminator? The secret lies in the left eigenvector corresponding to eigenvalue 1. It represents

the markets’ propagation values in the long run, assuming that spillover conditions persist. Fur-

thermore, an interpretation as stationary distribution of a Markov chain holds as well, rendering

the probability that an initial single shock will finally be encountered in a certain market on the

day in question. In other words, the left eigenvector of the spillover matrix mirrors the news

balance that can be reached between markets on a given day. Figure 5 displays the sequence

of results for each day in our dataset and for each market. Odds ratios of the probability that

a given market will be affected in the long run as compared to the other markets can serve to

carve out distinct structures in the series. An impression of the scale of results is provided in

Figure 6.

As a matter of fact, the news balance between the four markets is in a continuous process

of relocation in response to economic and geopolitical events. However, there is evidence for

a lasting structural change since the turn of the millennium, if not initiated with the official

launch of Euro on January 1, 1999 which was established in Maastricht by the European Union

in 1992.

It is since then that the CAC 40 and, most pronouncedly, the DAX experienced an up-

grade in the level of long-term propagation values, which, furthermore, started to move rather

synchronously, as if they were under a stabilizing force. In return, the Dow Jones Industrial

13

0.0

0.4

0.8

dji

0.0

0.4

0.8

fchi

0.0

0.4

0.8

gdax

i

0.0

0.4

0.8

n225

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Figure 5: The series of relative propagation values / the stationary probabilities of a Markov

chain

Average appears to have taken over a less prominent role as news disseminator and to gradually

descend to the level of European markets. In contrast, the preceding decade bears wild swings

with respect to the stakes which the four markets had in news propagation.

Distinct peaks on the side of Dow Jones Industrial Average may be related to the early 1990s

recession, the subsequent bull acceleration and emergence of technology-driven “new economy”,

and the crash of the “dot-com bubble” in early 2000. “. . . The technology-heavy Nasdaq reached

its pinnacle of 5,048.62 on March 10, [2000]. Then the Internet bubble burst and the index

plummeted nearly 40 percent, dropping below 3,000 in December [2010] in its worst annual

loss”.6 The Nasdaq crossed the 3,000 mark on 2012-02-29 morning for the first time since

December 2000.7 The FED’s reversal of its loose-interest stance in June 2004, and the “dollar

crisis” of 2005 matches the resurgence of propagation potential for the DJIA in 2004 and 2005.

Gourinchas [7] argues that “. . . As deflationary risks started to fade and the economy’s recovery

took hold, the FOMC [Federal Open Market Committee] shifted towards tightening its monetary

stance. Starting in June 2004, the FOMC increased interest rates gradually and measurably until

June 29, 2006 when they reached a plateau of 5.25%.” Diebold and Yilmaz [4] refer to the “dollar

crisis” of March 2005 as “. . . associated with remarks from policy makers in several emerging

and industrialized countries (South Korea, Russia, China, India and Japan) indicating that they

were considering central bank reserve diversification away from the US dollar.”

The prominent role of the German market as news disseminator in 1989 appears to be

linked to the reunification process and expectations of a strengthening of ties with the Soviet

economy which were raised on the occasion of Gorbachev’s visit to Germany in June of that

year.8 When a “reinforcement of positive mood” towards the Economic and Monetary Union

(EMU) was triggered in March 1998 by the declaration of 11 European Union nations being “fit

6The New York Times, 2012-03-13.7CNNMoney, 2012-02-29.8The Wall Street Journal, 1989-06-09.

14

02

46

810

12dj

i

0.0

1.0

fchi

0.0

1.0

gdax

i

0.0

1.0

n225

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Figure 6: The series of odds ratios of stationary probabilities (one market vs. other markets)

15

to join in” at its start, the news balance again appears to have been shifted towards European

markets.9 Wild swings of propagation values can be observed for the Nikkei 225 during the 1990s

“Lost Decade” of collapse of the Japanese asset price bubble (cf. Hayashia and Prescott [9]).

The subsequent decade, however, shows rather damped propagation values at the lowest level

among the four markets. A “massif” emerging on March 11, 2011 discontinues this flow. It was

supposedly triggered by the Fukushima Daiichi nuclear disaster following an earthquake and

tsunami on that day.10

Figure 7 displays a detail from Figure 6, meant to facilitate a closer view on the span of

years dominated by the U.S. subprime mortgage crisis, the subsequent global financial turmoil,

and the European debt crisis. The period from July 2007 to August 2008 is marked with events

converting problems in a niche of the financial markets, namely subprime residential mortgages,

to global financial crisis, as set out in the Introduction. In early 2010, the main focus of the

financial centers of the world was on news coming from Greece and the financially troubled

members of the EU.11

The observation that propagation values have recently tended to stabilize at similar levels, in

spite of severe crises arising in one market and spilling over to others, give rise to the following

hypothesis:

The news propagation balance in periods of global financial turmoil tends to be close

to a uniform distribution. News from one market are digested rapidly by the other

markets.

Figure 8 supports this hypothesis. It shows the information content which can be attributed to

the stationary distribution on a given day as compared to the uniform information, measured

in terms of the Kullback-Leibler divergence (KLIC) of the stationary distribution of the Markov

chain from the uniform distribution. As time proceeds, the range of results is narrowing with

an average closer to zero.

“What if” scenarios are finally sketched out in Figure 9. It shows the amount of information

which would be generated by a singular shock as compared to the news balance on a given day,

if the shock originates from one particular of the four markets. It reveals that the information

gain (in terms of KLIC) has decreased for shocks from the two European markets with the start

of EMU, and at least stabilized for the U.S. market. The Japanese market is different in this

respect: a shock from Japan would hit the news balance rather heavily. This is obviously due

to the less pronounced role of Nikkei 225 in the past decade’s news propagation process.

Figure 10 shows the time series of the Kolmogorov-Sinai entropy measure, that is, how the

speed of convergence to a news balance between markets if the system is distorted by a shock

(news) changed across time. A sustained increase could be observed since the mid-1990s, and it

seems that KS (at least when smoothed) has reached a plateau during the recent crisis.

7 Summary and conclusions

The goal of the present study was to add to the methodology concerned with measuring and

interpreting spillovers between equity markets, based on forecast error variance decomposition

(fevd), which was developed by Diebold and Yilmaz [4, 5]. Our reading of the spillover table

suggests to focus on intraday information propagation. Applying tools and concepts from popu-

lation dynamics and information theory, we developed eigenvector- and entropy-based measures,

9The Wall Street Journal, 1998-03-26.10Financial Times, 2011-04-12.11BBC News, 2012-06-13.

16

0.0

0.4

0.8

dji

0.0

0.4

0.8

fchi

0.0

0.4

0.8

gdax

i

0.0

0.4

0.8

n225

2002 2004 2006 2008 2010 2012

Figure 7: The series of odds ratios of stationary probabilities from 2002 onwards

0.0

0.2

0.4

0.6

0.8

1.0

KLI

C, s

tatio

nary

w.r.

t. un

iform

dis

trib

utio

n

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Figure 8: Kullback-Leibler divergence (KLIC), stationary w.r.t. uniform distribution

17

02

46

8dj

i

02

46

8fc

hi

02

46

8gd

axi

02

46

8n2

25

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Figure 9: Kullback-Leibler divergence (KLIC), impact w.r.t. stationary distribution

0.2

0.4

0.6

0.8

1.0

1.2

KS

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Figure 10: Kolmogorov-Sinai entropy (KS)

18

derived from Markov chain transformations, which are able to measure the information prop-

agation value of a market on a given day, permitting an assessment of the vulnerability of a

system of markets to unforeseen shocks from outside, as well as the dynamics of market impact

as information is transmitted among markets.

Among our empirical findings, using daily data from four major stock markets from 1988

through 2012, is that markets have converged with respect to their importance in passing on

information, that the origin of news is no longer important when considering its ultimate impact,

and that information exchange during times of crisis is high and uniform.

References

[1] Baba N., and Packer F., 2009. From Turmoil to Crisis: Dislocations in The FX Swap

Market Before and After The Failure of Lehman Brothers. BIS Working Papers , No. 285,

Bank For International Settlements.

[2] Caswell H., 2001. Matrix Population Models: Construction, Analysis, and Interpretation.

2nd ed. Sinauer Associates, Sunderland, MA.

[3] Demetrius L., 1974. Demographic parameters and natural selection. Proc. Natl. Acad. Sci.

USA 71, 4645–4647.

[4] Diebold F.X., and Yilmaz K., 2009. Measuring Financial Asset Return and Volatility

Spillovers with Application to Global Equity Markets. Economic Journal 119, 158–171.

[5] Diebold F.X., and Yilmaz K., 2011. On the Network Topology of Variance Decompositions:

Measuring the Connectedness of Financial Firms. NBER Working Paper 17490, National

Bureau of Economic Research.

[6] Gaspard P., 2004. Time-reversed dynamical entropy and irreversibility in Markovian ran-

dom processes. Journal of Statistical Physics 117, 599–615.

[7] Gourinchas P.O., 2010. U.S. Monetary Policy, Imbalances and the Financial Crisis . Re-

marks prepared for the Financial Crisis Inquiry Commission Forum Washington DC,

February 26-27, 2010.

[8] Gorton G.B., and Metrick A., 2009. Securitized Banking and The Run On Repo. NBER

Working Paper 15223, National Bureau of Economic Research.

[9] Hayashia F., and Prescott E.C., 2002. The 1990s in Japan: A Lost Decade. Review of

Economic Dynamics 5, 206–235.

[10] Kolmogorov A.N., 1959. Entropy per unit time as a metric invariant of automorphism.

Doklady of Russian Academy of Sciences 124, 754–755.

[11] Kullback S., and Leibler R.A., 1951. On Information and Sufficiency. Annals of Mathe-

matical Statistics 22, 79–86.

[12] Kullback S., 1959. Information theory and statistics. Wiley, New York.

[13] Kullback, S., 1987. Letter to the Editor: The Kullback-Leibler distance. The American

Statistician 41, 340–341.

[14] Mishkin F.S, 2010. Over The Cliff: From The Subprime To The Global Financial Crisis

NBER Working Paper 16609, National Bureau of Economic Research.

19

[15] Pesaran H.H., and Shin Y., 1998. Generalized Impulse Response Analysis in Linear Mul-

tivariate Models. Economics Letters 58, 17–29.

[16] Shannon C., 1948. A Mathematical Theory of Communication. Bell System Technical

Journal 27, 379–423.

[17] Schoen R., and Kim Y.J., 1991. Movement toward stability as a fundamental principle of

population dynamics. Demography 28, 455–466.

[18] Seneta E., 1981. Non-negative Matrices and Markov Chains. Revised Printing. Springer,

New York.

[19] Sinai Y.G., 1959. On the Notion of Entropy of a Dynamical System. Doklady of Russian

Academy of Sciences 124, 768–771.

[20] Tuljapurkar S.D., 1982. Why use population entropy? It determines the rate of conver-

gence. J. Math. Biology 13, 325–337.

20