Embed Size (px)

Citation preview

Understanding the Financial Advocacy

and Problem-Solving (FAPS) Model

United Way Toronto

With the generous support of TD Canada Trust

Researched and written by:

Resources for Results

August 2014

1

Contents

1 Introduction ............................................................................................................................... 2

2 A brief history of FAPS ................................................................................................................ 3

3 Who does FAPS serve? ............................................................................................................... 5

4 What is the context that creates financial exclusion? ............................................................... 6

5 FAPS goal and objectives ............................................................................................................ 7

6 Components of the FAPS model ................................................................................................ 7

6.1 FAPS neighbourhood services ............................................................................................ 7

6.1.1 Community Financial Worker services ........................................................................... 7

6.1.2 Tax clinics ........................................................................................................................ 8

6.1.3 Financial education ......................................................................................................... 9

6.1.4 Community engagement ................................................................................................ 9

6.2 Strategic policy development and advocacy ................................................................... 11

6.2.1 Documenting front-line learning and trends ................................................................ 11

6.2.2 Collaborative policy development and learning ........................................................... 11

6.3 Strategic leadership and coordination ............................................................................. 12

6.3.1 Program planning and coordination ............................................................................. 12

6.3.2 Shared services and accountability .............................................................................. 12

6.3.3 Partner capacity building and knowledge transfer ...................................................... 13

6.3.4 Adaptation and expansion of the model ...................................................................... 14

7 Conclusion ................................................................................................................................ 14

8 Appendix 1 – An overview of the FAPS theory of change ....................................................... 16

9 Appendix 2 – FAPS partnership chronology ............................................................................. 17

10 Appendix 3 – FAPS partners ..................................................................................................... 19

2

1 Introduction

This paper offers an overview of the Financial Advocacy and Problem-Solving (FAPS) model as it has grown and evolved over the past five years of funding by the United Way Toronto Financial Literacy Strategy. The aim is to frame our evaluation efforts and to promote an understanding of the FAPS approach, perhaps inspiring others to pursue similar initiatives.

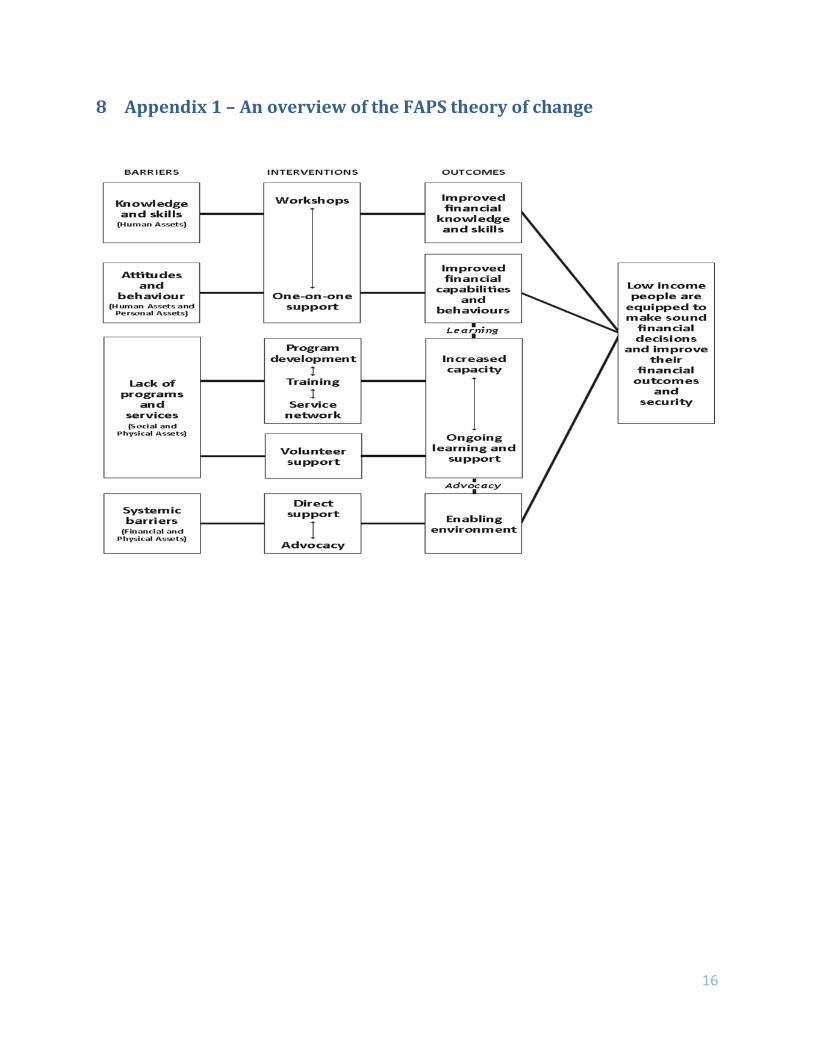

Financial Advocacy and Problem-Solving (FAPS)1 is a multi-faceted community partnership initiative designed to respond to gaps in the services and systems that serve the financial interests of people living in poverty in Toronto’s inner-suburban and inner-city neighbourhoods. The long-term goal of the FAPS model is to increase the income security, stability and life prospects of marginalized people.2 FAPS’ theory of change reflects the layered nature of the work, addressing barriers to financial inclusion at three levels: (1) individuals’ skills, knowledge and behaviour; (2) gaps in programs and services; and (3) systemic and policy issues (see Appendix 1 for a simplified version of the FAPS Theory of Change).

Developed by St. Christopher House (SCH) over ten years ago, the model seeks to provide a cost effective, scalable solution for strengthening the access of individuals, their families and communities to appropriate financial information, supports and services. It consists of a flexible set of specialized interventions to build people’s financial knowledge and empower them to take more control over their financial situation. As its name suggests, the FAPS model also advocates for systemic change; it is grounded in a social justice approach that seeks to promote more equitable and inclusive policies and systems.

In 2010, SCH partnered with Toronto Neighbourhood Centres (TNC) and United Way Toronto (UWT) to adapt and introduce the FAPS model into two additional Toronto neighbourhoods (Jane Finch Community and Family Centre (JFCFC) and the Agincourt Community Services Alliance (ACSA)). The initiative received funding of over $1 million from UWT and TD Bank as a part of the United Way Toronto Financial Literacy Strategy.3

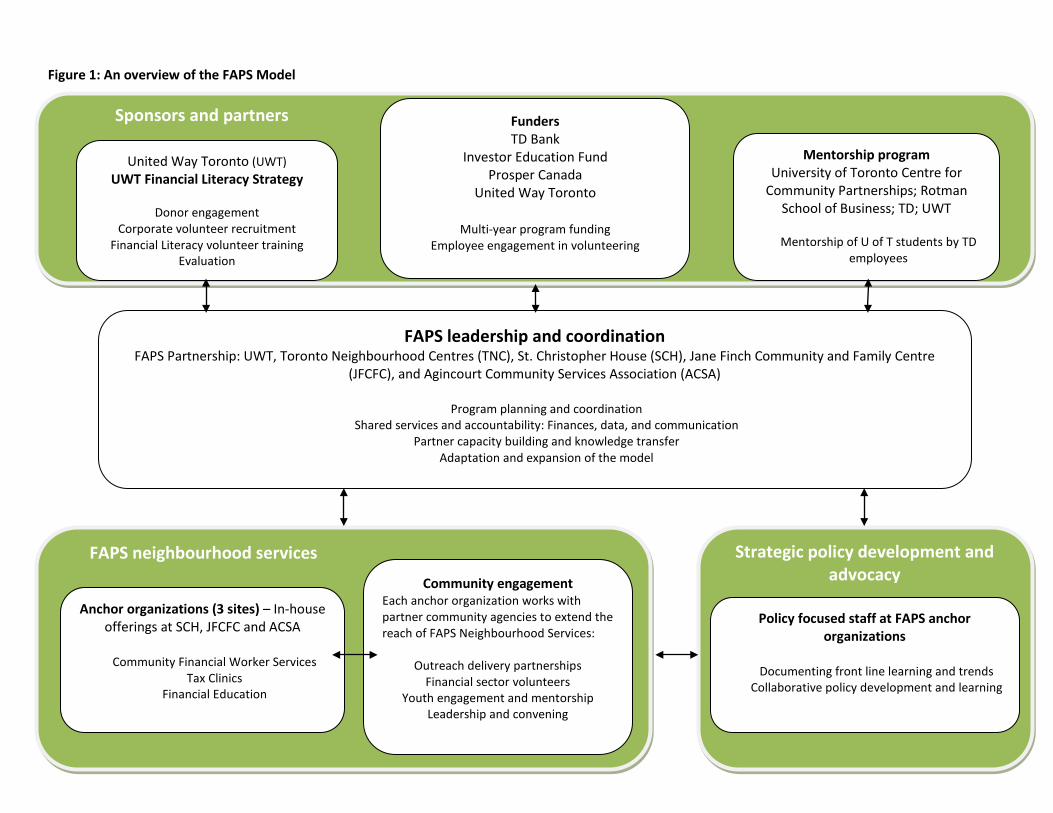

Components of the FAPS model (see Figure 1) include:

• FAPS Neighbourhood Services – Community programming by FAPS anchor organizations:4 The FAPS model is rooted in front-line financial advocacy and problem-solving supports and services provided by Community Financial Workers (CFWs) who assist community participants to access entitlements, make ends meet, be informed about their rights as consumers and begin to break out of a cycle of debt and financial insecurity. In addition, FAPS anchor organizations offer community-based tax clinics,

1 Throughout this paper ‘FAPS’ will refer to the overall initiative, even though the name originally comes from the front-line financial counselling practice of ‘financial advocacy and problem-solving’. 2 FAPS goal is paraphrased from FAPS Logic Model documents (Spring 2012). 3 The following section offers a brief history of the initiative. A full chronology appears in Appendix 2. 4 The FAPS anchor organizations are the three community-based agencies that take the lead in providing neighbourhood services: SCH, JFCFC, and ACSA.

3

financial education and volunteering opportunities. They promote local financial inclusion by working with low-income individuals to avoid and resolve financial pitfalls.

• Strategic Policy Development and Advocacy: FAPS also plays a leadership role in engaging a broad range of community stakeholders to engage civil society in promoting financial inclusion.

• FAPS Leadership and Coordination: FAPS is led by a partnership which seeks to promote the reach, cost-effectiveness and sustainability of the model.

2 A brief history of FAPS

Over a decade ago, through its community development and poverty reduction work in Toronto’s west-end inner-city neighbourhoods, St. Christopher House5 identified a range of money-related systems, policies and issues that limit the progress of low-income consumers towards financial security and well-being. It was apparent that there were few financial services that were both knowledgeable about the myriad social policy guidelines governing the well-being of low-income people and aligned with the financial interests of low-income people. In 2003, SCH developed a new financial problem-solving and advocacy service as a resource to enhance and complement its community programming. Individualized financial problem-solving services were housed alongside adult literacy, employment, computer training, and ESL, as well as settlement, homelessness, seniors and family services.

The program was designed to take a case-based approach, drawing on considerable staff expertise in financial issues (e.g. bank access and services, debt, consumer issues, budgeting, etc. ) and social welfare rules and regulations (e.g. income supports, housing, immigration, etc.). CFWs would meet individually with SCH participants to assess and deconstruct their complex financial problems: offering information, sorting through personal finances, and accessing income entitlements through tax filing or addressing issues with bureaucracies. FAPS immediately met strong demand for these services.

Over the years, SCH has learned a great deal about the financial interests and challenges of a wide range of low-income consumers. The model and its offerings evolved as SCH began to: (1) offer public education in the community; (2) work with banks to promote appropriate new financial products and services; (3) train other service providers in the FAPS knowledge and model; and (4) engage in policy discussions with a range of stakeholders to promote financial inclusion. Front-line delivery experience enabled SCH to identify emerging trends and issues that affect participants, and to collect first-hand evidence to support policy development.

SCH promoted FAPS as a neighbourhood-based model. In 2010, the organization formed a partnership with Toronto Neighbourhood Centres to explore the possibility of scaling up the FAPS program. They sought funding from the United Way Toronto Financial Literacy Strategy, and the FAPS expansion received more than $1 million (over five years) from UWT and TD Bank. Jane Finch Community and Family Centre became the first community partner to

5 See Appendix 1 for more about these organizations.

4

Figure 1: An overview of the FAPS Model

FAPS leadership and coordination FAPS Partnership: UWT, Toronto Neighbourhood Centres (TNC), St. Christopher House (SCH), Jane Finch Community and Family Centre

(JFCFC), and Agincourt Community Services Association (ACSA)

Program planning and coordination Shared services and accountability: Finances, data, and communication

Partner capacity building and knowledge transfer Adaptation and expansion of the model

FAPS neighbourhood services

Funders TD Bank

Investor Education Fund Prosper Canada

United Way Toronto

Multi-year program funding Employee engagement in volunteering

Sponsors and partners United Way Toronto (UWT)

UWT Financial Literacy Strategy

Donor engagement Corporate volunteer recruitment

Financial Literacy volunteer training Evaluation

Mentorship program University of Toronto Centre for

Community Partnerships; Rotman School of Business; TD; UWT

Mentorship of U of T students by TD

employees

Anchor organizations (3 sites) – In-house offerings at SCH, JFCFC and ACSA

Community Financial Worker Services

Tax Clinics Financial Education

Strategic policy development and advocacy

Policy focused staff at FAPS anchor organizations

Documenting front line learning and trends

Collaborative policy development and learning

Community engagement Each anchor organization works with partner community agencies to extend the reach of FAPS Neighbourhood Services:

Outreach delivery partnerships Financial sector volunteers

Youth engagement and mentorship Leadership and convening

5

work with TNC and SCH to expand FAPS outreach and services to neighbourhoods in north-west Toronto and North York. In 2012, the Agincourt Community Service Association joined FAPS to do the same in north-east Toronto/Scarborough.

3 Who does FAPS serve?

FAPS serves marginalized people and those with low-incomes in Toronto’s highly diverse inner-suburban and inner-city neighbourhoods. In 2012/13 FAPS worked with almost 40006 participants through various program offerings at all of its delivery locations.

FAPS often deals with people who have been destabilized by their financial situation. Financial problems cut across all ages, cultures and genders. FAPS programs serve urban neighbourhoods with a high density of newcomers, people receiving Ontario Works (OW) and the Ontario Disability Support Program (ODSP), people who are working poor or seniors on a fixed income. All FAPS locations also work with people who have some combination of health challenges, including serious mental health/addictions issues, disability, and chronic illness. The demographics of each neighbourhood are somewhat different, and FAPS adapts its services to neighbourhood priorities. For example, JFCFC offers Spanish language services to improve the access of the large Latin American population in the area.

What are the financial interests of FAPS participants? While there is no typical FAPS participant, FAPS has begun to identify a continuum of financial interests and needs commonly noted by people living on low-income. These are quite different from the interests of mainstream consumers which seem to determine government policy making and the priorities of financial institutions. FAPS participants’ needs and interests evolve as they are supported to move beyond immediate ‘survival’ and engage in thinking about longer-term issues. These evolving financial interests include: • Increased basic income to make ends meet • Access to basic needs including food security, affordable housing and employment • Access to banking and appropriate financial products and services • Enhanced (and relevant) financial knowledge and skills • Support for tax filing to access income entitlements • Strengthened capacity to navigate and self-advocate within complex bureaucratic systems • Improved ability to research money matters and conduct business using a computer and the

Internet • Resolution of time poverty, which is a significant limiter of social and economic outcomes • Advice to support long-term financial security and retirement • Asset building and saving for investments such as education, retirement, self-employment

6In 2012/13 the overall FAPS initiative served 3992 people. Scope of UWT Financial Literacy Strategy component: “In 2012/13 the Mobile Community Financial Workers supported by United Way Toronto funding were able to provide services to a total of 2443 community members. This included 815 people supported through one-to-one problem-solving and coaching, 1115 in tax clinics, 477 people who participated in specialized workshops delivered by staff and 25 trained as peer support workers to provide outreach in their community about these issues.” Financial Advocacy and Problem-Solving - Year-End Report (Project Year 2: Sept 1 2012 - August 31, 2013) p. 2)

6

4 What is the context that creates financial exclusion?

The FAPS partnership has come to know first-hand, numerous ways in which complex and overlapping government policies and regulations can exclude people from their income entitlements and benefits. An ongoing investment is made in: careful examination of social policy guidelines (e.g. income, tax, housing, and immigration); feedback from the front-line problem-solving work of Community Financial Workers; and, collaborative learning and policy development.7 Through this work, FAPS has identified four key factors that it must address in its work to promote financial inclusion:

Increasing household vulnerability: FAPS is serving growing numbers of individuals and families who report that they are struggling to make ends meet. Day-to-day survival dominates their financial decision-making, limiting their ability to consider their long-term economic security. Many FAPS participants say that they have little money to manage, and that it is almost impossible to save. They do not know where to begin to deal with their problems, and often experience fear, stress and social stigma related to money.

Exclusion from mainstream financial services: People’s financial choices have more impact on their lives and future prospects than ever before. The increasing complexity of money, difficulty in accessing banking services and inappropriateness of financial products results in the exclusion of many from financial decision-making and mainstream financial institutions. It is common for FAPS participants to use pawn shops and cheque cashing operations instead of banks and credit unions. These fringe financial services bring a high cost to low-income consumers. In addition, the easy availability of credit and predatory consumer practices have resulted in high personal debt levels. People cannot afford paid advisors, and often have trouble getting the financial guidance they require.

Lack of a money dimension to community-based human and social services” Front-line community social service agencies do not have the capacity to incorporate the dimension of money into their work to support people with low-incomes to engage in society and the economy. Their staff may not be equipped to understand their clients’ money-related interests and needs. For example, front-line workers must often provide technical support to people who are seeking paid employment while receiving Ontario Works benefits: knowing the rules can prevent the loss of rent subsidies and/or income claw backs. Some staff at community organizations may choose to avoid talking to participants about money matters because they are not confident to do so.

Barriers to accessing entitlements and benefits: Over the years, the FAPS team has developed a picture of how bureaucratic processes often exclude and further marginalize people who are on low-income and face other barriers to participating in Canadian society. Benefits and

7 Here we gratefully recognize the work of specialized researchers John Stapleton, Richard Shillington, and others.

“Many households are vulnerable. Their income bases are so low that any crisis – like the loss of a job, illness, or domestic violence – will immediately push families into financial crisis.”

(FAPS Staff)

7

entitlements must be accessed by navigating a complex, often incoherent, and sometimes conflicting set of programs, regulations, policies, and procedures. As a result, each year, many people with low-incomes miss out on a range of financial benefits and supports to which they are entitled.8 Tax filing has become a critical new entry point for boosting people’s income: the income tax system is now used as a mechanism to redistribute income. Many do not realize that they can only access the Canada Child Tax Benefit, GST/HST Rebates, and Old Age Security (OAS) by filing an annual income tax return, regardless of whether they are employed or not.

5 FAPS goal and objectives

Goal: To improve the financial security, stability and prospects of people with low-income.

Objectives: 1. Financial capability: To equip people with low-incomes to improve their financial

situations and increase their capacity to handle a range of financial decisions 2. Broaden community access to financial advocacy and problem-solving: To expand the

scale and reach of FAPs services to low-income communities, in partnership with other community agencies

3. Systemic change: To promote a financially inclusive environment for people with low-incomes.

6 Components of the FAPS model

The FAPS model is grounded in three core components which are explored in more detail below:

• FAPS neighbourhood services • Strategic policy development and advocacy • FAPS Leadership and Coordination

6.1 FAPS neighbourhood services

6.1.1 Community Financial Worker services FAPS anchor organizations hire and train Community Financial Workers, front-line staff who provide one-to-one problem-solving and financial advocacy supports to community members on low-incomes. CFWs are housed in community-based offices in anchor organizations and work alongside many other front-line staff to serve participants. They also provide outreach services on a periodic, itinerant basis in partnership with other community agencies in surrounding neighbourhoods. The aim is to provide mobile, accessible, community-based financial services that are: free; not-for-profit; independent; private and confidential; professional; high quality; and, accountable to the community (see Appendix 3 for a list of satellite agencies). 8 Richard Shillington in Improved tax filing and benefit take-up, SCH Backgrounder, 2011.

8

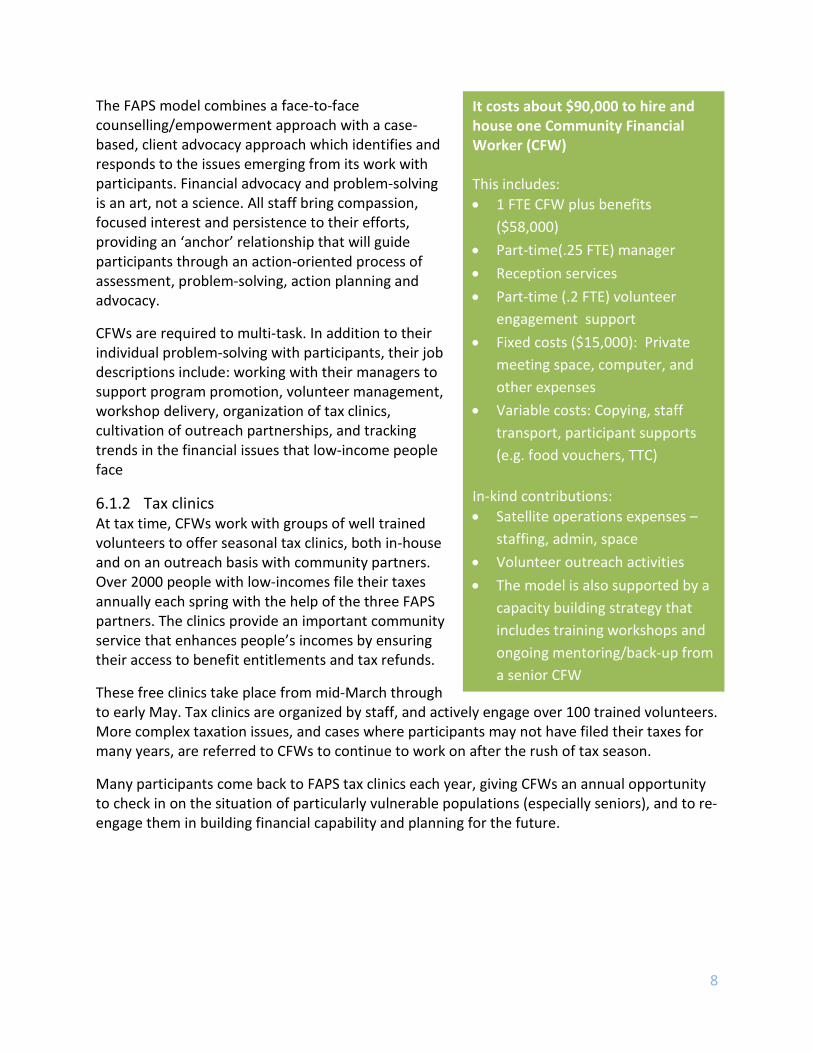

The FAPS model combines a face-to-face counselling/empowerment approach with a case-based, client advocacy approach which identifies and responds to the issues emerging from its work with participants. Financial advocacy and problem-solving is an art, not a science. All staff bring compassion, focused interest and persistence to their efforts, providing an ‘anchor’ relationship that will guide participants through an action-oriented process of assessment, problem-solving, action planning and advocacy.

CFWs are required to multi-task. In addition to their individual problem-solving with participants, their job descriptions include: working with their managers to support program promotion, volunteer management, workshop delivery, organization of tax clinics, cultivation of outreach partnerships, and tracking trends in the financial issues that low-income people face

6.1.2 Tax clinics At tax time, CFWs work with groups of well trained volunteers to offer seasonal tax clinics, both in-house and on an outreach basis with community partners. Over 2000 people with low-incomes file their taxes annually each spring with the help of the three FAPS partners. The clinics provide an important community service that enhances people’s incomes by ensuring their access to benefit entitlements and tax refunds.

These free clinics take place from mid-March through to early May. Tax clinics are organized by staff, and actively engage over 100 trained volunteers. More complex taxation issues, and cases where participants may not have filed their taxes for many years, are referred to CFWs to continue to work on after the rush of tax season.

Many participants come back to FAPS tax clinics each year, giving CFWs an annual opportunity to check in on the situation of particularly vulnerable populations (especially seniors), and to re-engage them in building financial capability and planning for the future.

It costs about $90,000 to hire and house one Community Financial Worker (CFW) This includes: • 1 FTE CFW plus benefits

($58,000) • Part-time(.25 FTE) manager • Reception services • Part-time (.2 FTE) volunteer

engagement support • Fixed costs ($15,000): Private

meeting space, computer, and other expenses

• Variable costs: Copying, staff transport, participant supports (e.g. food vouchers, TTC)

In-kind contributions: • Satellite operations expenses –

staffing, admin, space • Volunteer outreach activities • The model is also supported by a

capacity building strategy that includes training workshops and ongoing mentoring/back-up from a senior CFW

9

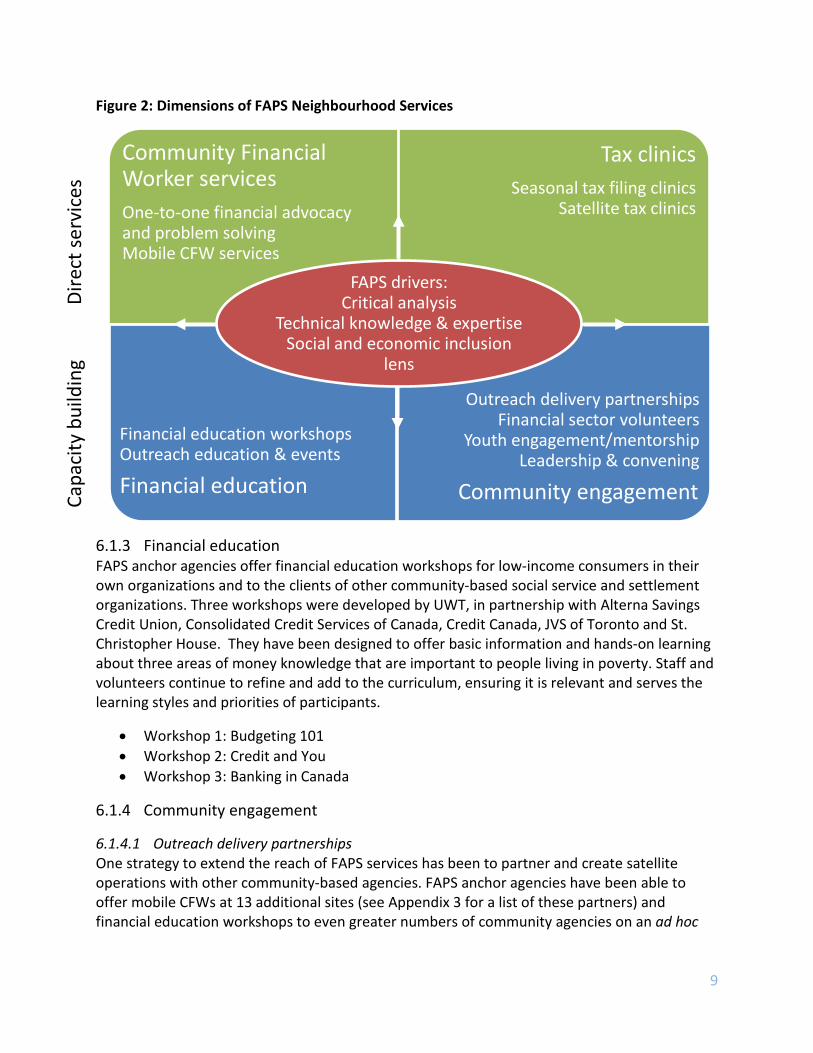

Figure 2: Dimensions of FAPS Neighbourhood Services

6.1.3 Financial education FAPS anchor agencies offer financial education workshops for low-income consumers in their own organizations and to the clients of other community-based social service and settlement organizations. Three workshops were developed by UWT, in partnership with Alterna Savings Credit Union, Consolidated Credit Services of Canada, Credit Canada, JVS of Toronto and St. Christopher House. They have been designed to offer basic information and hands-on learning about three areas of money knowledge that are important to people living in poverty. Staff and volunteers continue to refine and add to the curriculum, ensuring it is relevant and serves the learning styles and priorities of participants.

• Workshop 1: Budgeting 101 • Workshop 2: Credit and You • Workshop 3: Banking in Canada

6.1.4 Community engagement

6.1.4.1 Outreach delivery partnerships One strategy to extend the reach of FAPS services has been to partner and create satellite operations with other community-based agencies. FAPS anchor agencies have been able to offer mobile CFWs at 13 additional sites (see Appendix 3 for a list of these partners) and financial education workshops to even greater numbers of community agencies on an ad hoc

Community Financial Worker services One-to-one financial advocacy and problem solving Mobile CFW services

Tax clinics Seasonal tax filing clinics

Satellite tax clinics

Financial education workshops Outreach education & events

Financial education

Outreach delivery partnerships Financial sector volunteers

Youth engagement/mentorship Leadership & convening

Community engagement

FAPS drivers: Critical analysis

Technical knowledge & expertise Social and economic inclusion

lens

Capa

city

bui

ldin

g Di

rect

serv

ices

10

basis. The FAPS model provides a community resource that augments and enhances the services of other community agencies that lack the expertise and funding to offer such services.

6.1.4.2 Financial sector volunteer engagement to support outreach education In 2010, UWT launched a community financial literacy volunteer strategy that leveraged its corporate partnerships to promote volunteer engagement in financial education within Toronto’s neighbourhoods. In 2011, TD Bank sponsored the initiative and made a commitment to encourage and support its employees to engage in financial education workshops, mentorship and tax filing clinics. Since inception, over 100 corporate volunteers have been trained and actively engaged.

UWT has taken responsibility for volunteer engagement and recruitment, and offers intensive volunteer orientation and training sessions in cooperation with FAPS anchor agencies. Volunteers also attend further orientation and training sessions on-site at FAPS agencies. These sessions are designed to prepare them for work with diverse populations on low-income.

The financial education workshops have been an excellent mechanism for engaging the corporate sector in their communities. At the end of 2013, FAPS staff and volunteers had delivered 244 financial education workshops to low-income consumers at different community-based host organizations across Toronto, since the program’s inception in 2010.

In 2013, FAPS agencies explored new ways of engaging corporate volunteers in their work to promote financial capability. For example, JFCFC is currently cultivating a direct relationship with a local TD bank branch in order to promote financial education and accessibility of banking.

6.1.4.3 Youth engagement and mentorship A complementary financial education mentoring program has been developed by UWT in partnership with the University of Toronto Centre for Community Partnerships and TD Bank to offer a mentorship program within which the students explore their professional options in the financial industry, gain career advice, and engage with their community. TD financial education volunteers and undergraduate students at the Rotman School of Business (University of Toronto) are matched and participate in an orientation process that prepares them for successful mentorship relationships. Mentors and mentees are expected to co-deliver financial education workshops and volunteer at the community level with FAPS agencies. Many have actively continued to volunteer in financial education workshops and tax filing clinics. The program has grown quickly since its inception. To date, over 40 Rotman students have been mentored by financial sector mentors.

6.1.4.4 Leadership and convening FAPS program managers have played leadership roles in their communities, facilitating cross-sectoral collaboration to extend the FAPS’s reach and deepen its impact on financial inclusion. All of the sites participate in Credit Education Week and Financial Literacy Month, offering specialized workshops, community information booths and events.

11

Community convening is also a strategy being employed to promote financial inclusion. The Black Creek Financial Action Network (BCFAN) was established in 2011 with JFCFC as co-founder and Chair, in partnership with the Jane Finch Community Ministry, York University, and TD Community Engagement Centre (CEC). The focus of this network is to support peer learning, share effective practices in delivering financial education, improve referral networks, and build relations with financial institutions in the area. Similarly, ACSA has begun networking in its catchment area, building alliances with other social service agencies and academics. As a part of the UWT Financial Literacy Strategy, the FAPS partners continue to focus on its ambitious agenda of building financial capability networks and agency capacity across the city.

6.2 Strategic policy development and advocacy

6.2.1 Documenting front-line learning and trends The FAPS partnership has assumed a leadership role in encouraging a cycle of policy and advocacy work grounded in its day-to-day activities with participants. It has identified systemic traps that create unintended negative financial consequences for people with low-incomes. These problems are usually caused by the complex, incompatible, intersecting social programs and regulations. CFWs intervene to reduce the harm created by these unexpected effects. The FAPS partnership also coordinates parallel efforts to prevent such cases, by researching and developing practical options for policy and regulatory change and advocating such ideas to government.

Policy-focused staff in partner agencies monitor the policy context on an ongoing basis, identifying new developments and trends affecting the situation of people with low-incomes and lending their expertise to achieving the long term goal of FAPS.

6.2.2 Collaborative policy development and learning The FAPS partnership collaborates with community agencies, funders, academics, philanthropic foundations, national agencies and policy makers to promote policy change. It often engages in what it calls ‘possibility-driven’ advocacy, adopting a practical approach to resolve immediate issues that participants face as a result of the incompatibility of overlapping policies and regulations. This approach offers solutions to specific problems, and urges policy decision makers to adopt the suggested changes.

The partnership has learned that policy work is complicated and requires specialized expertise and a collaborative approach. While policy development is a key priority, not every FAPS anchor agency is expected to engage in policy leadership. Rather, the FAPS partnership provides capacity building for anchor agencies to feed into and support the policy development process led by SCH.

Examples of FAPS policy and advocacy work over the years:

• In 2011-2012, FAPS worked with Policy Analyst in Residence, John Stapleton to research and develop a plain language guide: Planning Retirement on a Low income. (See http://openpolicyontario.com/wordpress/wp-content/uploads/2012/09/alli

12

nonelowincomeretirement.pdf ) • Starting in the late nineties, FAPS worked closely with Royal Bank of Canada (RBC) to

research, design and develop an appropriate, accessible alternative to cheque cashing operations and pay day lenders. Cash & Save was developed in 2002 and operated for two years. It was a service centre of RBC that offered basic financial services in two low-income neighbourhoods of Toronto including cheque-cashing, bill payments, money transfers and money orders. (For a profile of Cash & Save, see Community Banking Projects for Low-income Canadians: A Report Examining Four Projects to Promote Financial Inclusion, by Jerry Buckland)

• In 1999-2001, FAPS worked with Policy Analyst in Residence, Richard Shillington to identify and respond to the low take-up of seniors in accessing their Guaranteed Income Supplement (GIS) benefits. That research revealed that roughly 300,000 low-income seniors in Canada were missing out on $500 million per year in benefits they were entitled to because they hadn’t applied. It took time and media coverage to raise awareness of the issue and then a concerted effort to influence parliamentary hearings in order to ensure that seniors are now informed when they are not accessing their GIS benefits. (See http://www.shillington.ca/)

6.3 Strategic leadership and coordination

6.3.1 Program planning and coordination The FAPS model is led by a collaborative partnership composed of representatives from each partner agency. The overall decision making structure is democratic: UWT, TNC and senior staff from the three lead agencies collaborate closely to guide the project and make decisions. The project has developed a strong collaborative approach to sharing best practices and learning through informal networks to enhance support for and problem-solving with CFWs.

6.3.2 Shared services and accountability The FAPS partnership supports partner agencies to plan and implement FAPS services, while also offering a centralized layer of shared services in order to create core efficiencies and economies of scale. This division of labour is expected to promote the model’s resilience and sustainability.

TNC coordinates umbrella management functions of the FAPS model, including: (1) program planning and decision making with partners; (2) partner relations; (3) communications; (4) funder accountability and reporting; and (5) planning for sustainability. This shared services approach is intended to prevent duplication of effort, to reduce costs and support consistent delivery of programs and services.

13

FAPS anchor agencies are responsible for the day-to-day operations, management, and quality control of their own FAPS services. They are accountable to the partnership for achieving targeted numbers of participants and deliverables.

6.3.3 Partner capacity building and knowledge transfer SCH leads the adaptation process and manages the technical aspects of scaling up and promoting quality assurance in delivery of the model. Over the past several years, SCH has been offering training and technical assistance on an outreach basis to the staff of numerous neighbourhood agencies, in order to share its expertise and knowledge about financial problem-solving and advocacy.

In Toronto, FAPS has partnered with North York Community House, Access Alliance Multi-cultural Health and Social Services, and St. Michael’s Hospital. They are now also working with partners in Winnipeg to adapt the model there. See Appendix 2 for a brief chronology. As a result, additional organizations have built their readiness and ability to deliver FAPS services in their communities and some have accessed funding for this purpose.

In order to facilitate this capacity building and scaling up of the model, the FAPS partnership has developed an eight-workshop staff training series and manual that explain FAPS practice and offer an overview of the technical knowledge required to support people to navigate complex

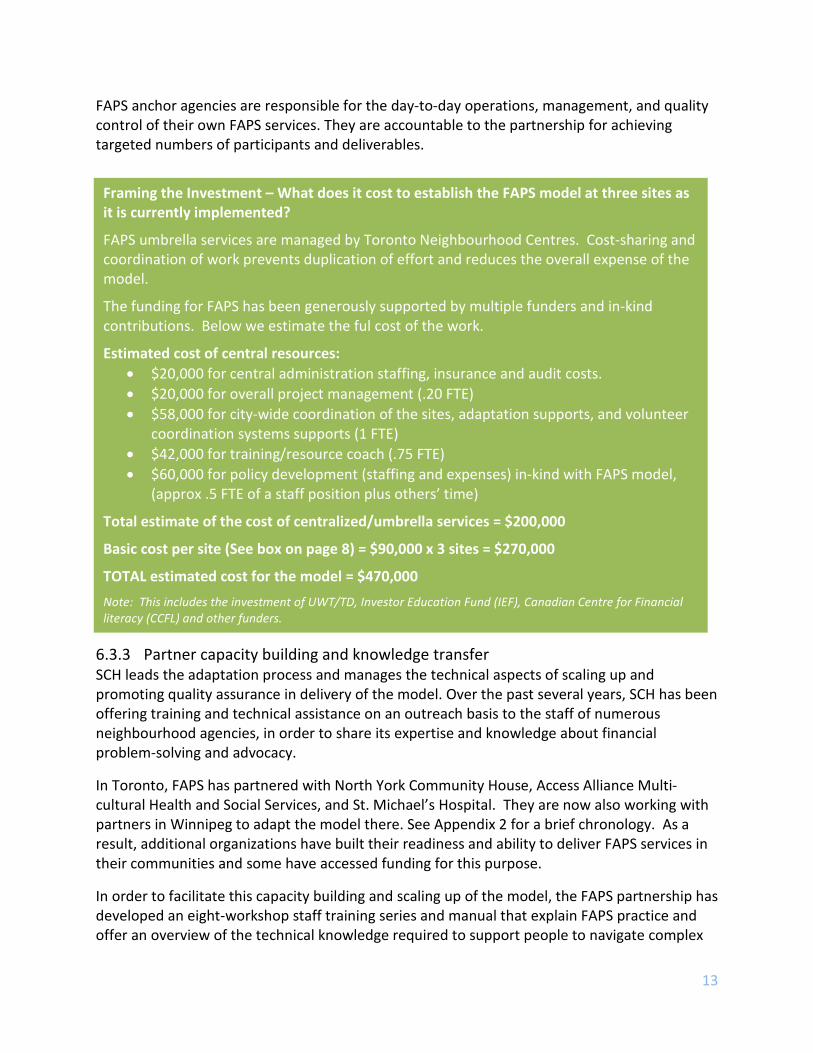

Framing the Investment – What does it cost to establish the FAPS model at three sites as it is currently implemented?

FAPS umbrella services are managed by Toronto Neighbourhood Centres. Cost-sharing and coordination of work prevents duplication of effort and reduces the overall expense of the model.

The funding for FAPS has been generously supported by multiple funders and in-kind contributions. Below we estimate the ful cost of the work.

Estimated cost of central resources: • $20,000 for central administration staffing, insurance and audit costs. • $20,000 for overall project management (.20 FTE) • $58,000 for city-wide coordination of the sites, adaptation supports, and volunteer

coordination systems supports (1 FTE) • $42,000 for training/resource coach (.75 FTE) • $60,000 for policy development (staffing and expenses) in-kind with FAPS model,

(approx .5 FTE of a staff position plus others’ time)

Total estimate of the cost of centralized/umbrella services = $200,000

Basic cost per site (See box on page 8) = $90,000 x 3 sites = $270,000

TOTAL estimated cost for the model = $470,000 Note: This includes the investment of UWT/TD, Investor Education Fund (IEF), Canadian Centre for Financial literacy (CCFL) and other funders.

14

bureaucracies and application processes. The workshops cover a range of issues and subject matter related to the CFWs’ core work of supporting people to access their income entitlements. Workshops include: an overview of the regulatory and benefit ‘landscape’, interpreting participants’ status to determine eligibility for entitlements; understanding social assistance regulations and income calculations; and tax filing.9

The FAPS partnership also works closely with The Canadian Centre for Financial Literacy (CCFL)10 to promote the financial capability of front-line social service staff. CCFL financial literacy training complements FAPS’ workshops and partners are encouraged to attend both workshop series.

6.3.4 Adaptation and expansion of the model As the FAPS partnership seeks to bring its model to scale, it has steered clear of replication, instead looking for like-minded lead community agencies that will have the capacity to adapt the model to their own community. These new potential partners demonstrate the following characteristics:

• Clear local demand for financial supports and services • An anti-poverty orientation and social change mission, with a strong track record of

community convening, leadership and partnership • Senior championship and a strong commitment to integrating a financial dimension into

the overall work of the organization • Excellent operational capacity

As they joined the partnership, FAPS anchor agencies (JFCFC and ACSA) received intensive support from SCH to design their FAPS programs, train staff, and get started. They have been free to develop and deliver services in a way that is tailored to the context and needs of their communities: each has its own unique goals, activities, offerings and partnerships.

7 Conclusion

A recent national scan of financial counselling programs11 found that there are very few Canadian initiatives that specialize in financial problem-solving and coaching/counselling with people with low-incomes. Yet the same study observed that there has been a groundswell of demand for these financial supports and services in communities across Canada.12 The FAPS model offers one approach to integrating expertise and supports in the area of personal finances and social benefit entitlements into the fabric of local social and human development services.

9 Note: Covering some of these subjects requires more than one workshop. 10 See CCFL Website: The Canadian Centre for Financial Literacy (CCFL) 11 Resources for Results, (Forthcoming, 2014) Leveraging Change: Best practices in financial counselling with low-income people. An international best practices scan commissioned by: Prosper Canada, Toronto, Canada. Executive Summary. 12 Leveraging Change, Executive Summary.

15

Indeed, a recent evaluation of FAPS offers new evidence of the effects of financial advocacy and problem-solving with people on low income, identifying effective practices, and providing new insight into how participants change as a result of their participation. The overall finding of the evaluation is that FAPS is much more than financial counselling, financial education, or tax filing. While a financial focus is central to the FAPS intervention, the outcomes can be best understood when viewed through a social and economic inclusion lens.

FAPS fills gaps in community-based poverty-reduction strategies. CFWs use finances as an entry point for creating the conditions and capacity for low-income individuals to build a foundation for social and economic inclusion.

While the FAPS intervention is unique in Canada, it is actually a part of a relatively new wave of interventions internationally, which are working to integrate a financial element into broader social inclusion objectives.13 By enhancing the external conditions for financial stability and promoting participants’ capacity for managing their personal affairs, FAPS is building a solid foundation for broader social participation and well-being, which may ultimately result in more successful poverty reduction outcomes. The evaluation findings suggest that financial advocacy and problem-solving is an important practice that should be integrated into broader poverty reduction and social inclusion processes. It is timely that others across Canada have become interested in adopting and adapting the FAPS model in their communities and we hope this description of the model can help in expanding these services to others.

13 See Backgrounder: Situating FAPS practice and outcomes in the international context, which offers a brief review of international practices connecting financial capability and financial well-being to social inclusion.

16

8 Appendix 1 – An overview of the FAPS theory of change

17

9 Appendix 2 – FAPS partnership chronology

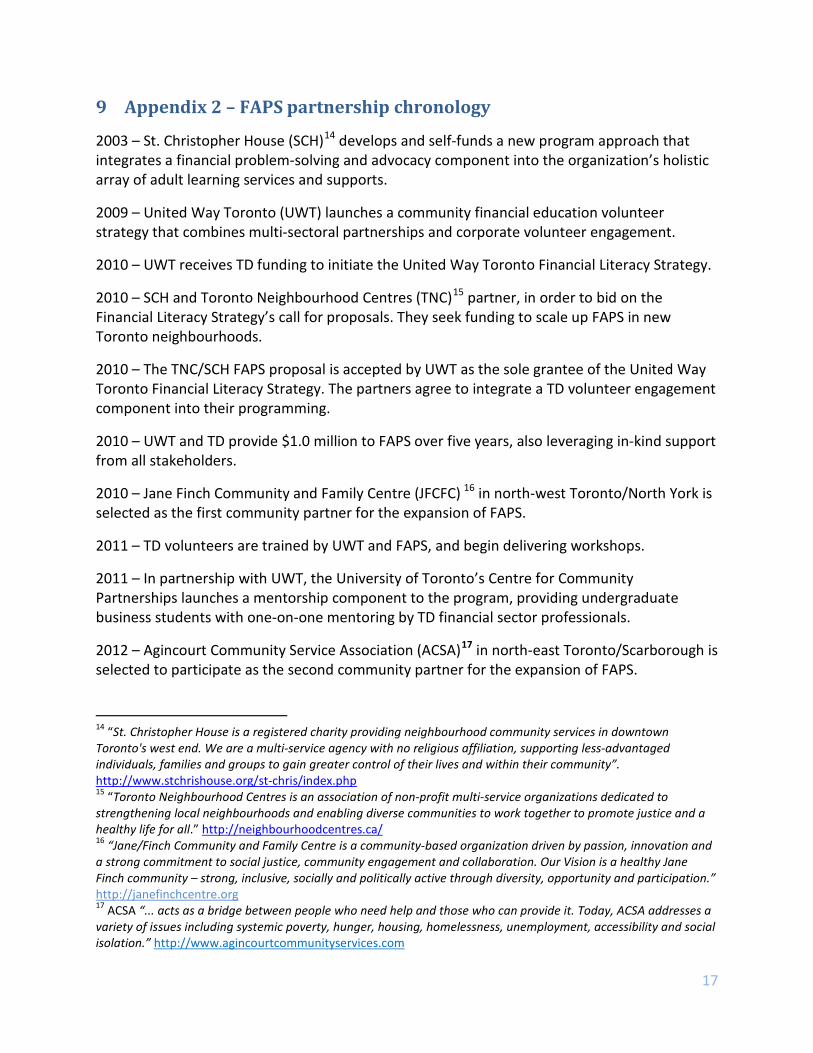

2003 – St. Christopher House (SCH)14 develops and self-funds a new program approach that integrates a financial problem-solving and advocacy component into the organization’s holistic array of adult learning services and supports.

2009 – United Way Toronto (UWT) launches a community financial education volunteer strategy that combines multi-sectoral partnerships and corporate volunteer engagement.

2010 – UWT receives TD funding to initiate the United Way Toronto Financial Literacy Strategy.

2010 – SCH and Toronto Neighbourhood Centres (TNC)15 partner, in order to bid on the Financial Literacy Strategy’s call for proposals. They seek funding to scale up FAPS in new Toronto neighbourhoods.

2010 – The TNC/SCH FAPS proposal is accepted by UWT as the sole grantee of the United Way Toronto Financial Literacy Strategy. The partners agree to integrate a TD volunteer engagement component into their programming.

2010 – UWT and TD provide $1.0 million to FAPS over five years, also leveraging in-kind support from all stakeholders.

2010 – Jane Finch Community and Family Centre (JFCFC) 16 in north-west Toronto/North York is selected as the first community partner for the expansion of FAPS.

2011 – TD volunteers are trained by UWT and FAPS, and begin delivering workshops.

2011 – In partnership with UWT, the University of Toronto’s Centre for Community Partnerships launches a mentorship component to the program, providing undergraduate business students with one-on-one mentoring by TD financial sector professionals.

2012 – Agincourt Community Service Association (ACSA)17 in north-east Toronto/Scarborough is selected to participate as the second community partner for the expansion of FAPS.

14 “St. Christopher House is a registered charity providing neighbourhood community services in downtown Toronto's west end. We are a multi-service agency with no religious affiliation, supporting less-advantaged individuals, families and groups to gain greater control of their lives and within their community”. http://www.stchrishouse.org/st-chris/index.php 15 “Toronto Neighbourhood Centres is an association of non-profit multi-service organizations dedicated to strengthening local neighbourhoods and enabling diverse communities to work together to promote justice and a healthy life for all.” http://neighbourhoodcentres.ca/ 16 “Jane/Finch Community and Family Centre is a community-based organization driven by passion, innovation and a strong commitment to social justice, community engagement and collaboration. Our Vision is a healthy Jane Finch community – strong, inclusive, socially and politically active through diversity, opportunity and participation.” http://janefinchcentre.org 17 ACSA “... acts as a bridge between people who need help and those who can provide it. Today, ACSA addresses a variety of issues including systemic poverty, hunger, housing, homelessness, unemployment, accessibility and social isolation.” http://www.agincourtcommunityservices.com

18

2013 – UWT funds a final-year enhancement of $125,000 to FAPS.

2013 – TNC receives $100,000 from Investor Education Foundation

2013 – JFCFC receives $100,000 from Prosper Canada to enhance the financial literacy knowledge base of low-income people and champion a financial literacy network in the north-west of the Greater Toronto Area.

2013 – JFCFC receives $50,000 from The Counseling Foundation of Canada to enhance the financial capacity and knowledge-base of low-income youth, newcomers and young moms/parents through one-to-one support and workshops.

2013 – St. Christopher House receives $100,000 from Prosper Canada to provide individual and group-based financial literacy programming to low-income self-employed people.

19

10 Appendix 3 – FAPS partners

Satellite partners

Through the support of United Way Toronto and TD Bank volunteers and funding, FAPS financial advocacy and problem-solving is now offered at satellite community agencies on a periodic basis. Below is a list of current partner agencies:

North-West – serviced by JFCFC

• Mount Denis Action for Neighbourhood Change (ANC) • North York Community House • Lotherton ANC • Northwood Neighbourhood Services • Unison Health and Community Services • Bathurst and Finch ANC

Downtown – serviced by SCH

• Central Neighbourhood House Association • Dixon Hall • Ralph Thornton Centre • University Settlement

North-East – serviced by ACSA

• Catholic Cross-Cultural Services • Scarborough Centre for Healthy Communities (hub) • Working Women Community Centre (hub)

Core funding partner

United Way Toronto secured resources from TD Bank Financial to fund the United Way Toronto Financial Literacy Strategy starting in 2010, in order to begin to address some of the root causes of poverty and empower low income individuals to make more informed financial decisions and build towards long term financial stability. The initiative received funding of $1 million from TD Bank Financial Group. That gift enabled the Financial Literacy Strategy to begin implementation and operate fully until August 2014.

Additional funding partners

The UWT Financial Literacy strategy leveraged additional partners and funding. During this phase, the United Way support provided anchor funding which TNC and the participating agencies were able to leverage to secure resources to provide financial literacy supports to low-income people. The following resources were secured in part due to the ongoing support of the United Way’s Financial Literacy Strategy:

20

Investor Education Fund: $100,000 (Feb. 2013 to Jan 30, 2014) for TNC to build financial problem-solving capacity with other agencies as well as extend the MFCW worker position at JFCFC which was to come to an end in August 2013.

SEDI: $100,000 (June 2013 to May 31, 2015) for JFCFC to enhance the financial literacy knowledge base of low-income people, including those who are Spanish-speaking, through one-to-one support, the provision of workshops, training youth and settlement workers, and building the capacity of staff at three partner agencies. This project will include championing a network related to financial literacy in the north-west of the Greater Toronto Area.

The Counseling Foundation of Canada: $50,000 (September 2013 to August 31, 2104) for Jane Finch Community and Family Centre to enhance the financial capacity and knowledge-base of low-income youth, newcomers and young moms/parents through one-to-one support and workshops.

SEDI: $100,000 (June 2013 to May 31, 2015) for St. Christopher House to integrate direct service and capacity development, both in group-based financial literacy programming and in service delivery to low-income self-employed people. Also, a financial literacy lens will be brought to a research project aimed at better understanding and making social policy recommendations about the underground economy, a broader view of the labour market, and financial options for low-income people.

United Way Toronto also provided $125,000 to keep FAPS programming, particularly the front-line delivery of CFW and coordination and program development in the existing three Toronto regions vibrant through to August 2014.

The stability to FAPS financial literacy programming provided by the United Way funds not only resulted in innovation and the program development opportunities outlined above. It also provided a foundation for the delivery of more front-line financial problem-solving supports to low-income people than are directly funded by the United Way. FAPS programming across the three regions served a total of 3992 people. The United Way investment was leveraged to help almost double the amount of people than were funded by the UW dollars alone. These low-income participants accessed over 7.9 million dollars in funds for which they were eligible.