Embed Size (px)

Citation preview

August 23, 2016

Understanding the New

Landscape of Business Lending

Why Do Accountants Need to Understand

the Lender Landscape?

2

Over 250,000 small businesses are expected to take online or

alternative loans this year

The cost of financing varies from lender to lender, it’s confusing,

and the wrong financing can hurt your client’s viability

There are a lot of new loan products available online

You are in an important position to advise and counsel your

small business clients

The World of Small Business Financing

Has Changed

3

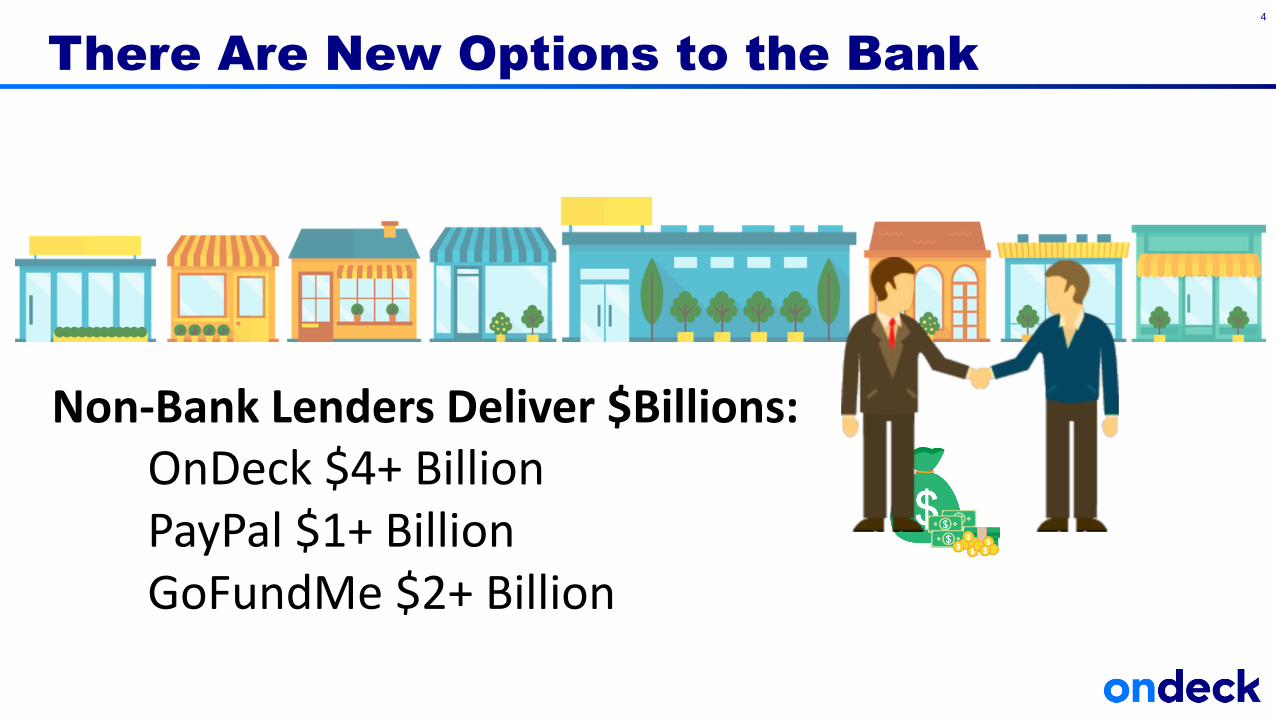

There Are New Options to the Bank

4

Non-Bank Lenders Deliver $Billions:OnDeck $4+ BillionPayPal $1+ BillionGoFundMe $2+ Billion

Why Did This Happen?

5

Searching for capital has

historically been a

challenge for many

business owners

• A time consuming process

• Stringent credit requirements

• Limited credit choices

• Rigid collateral requirements

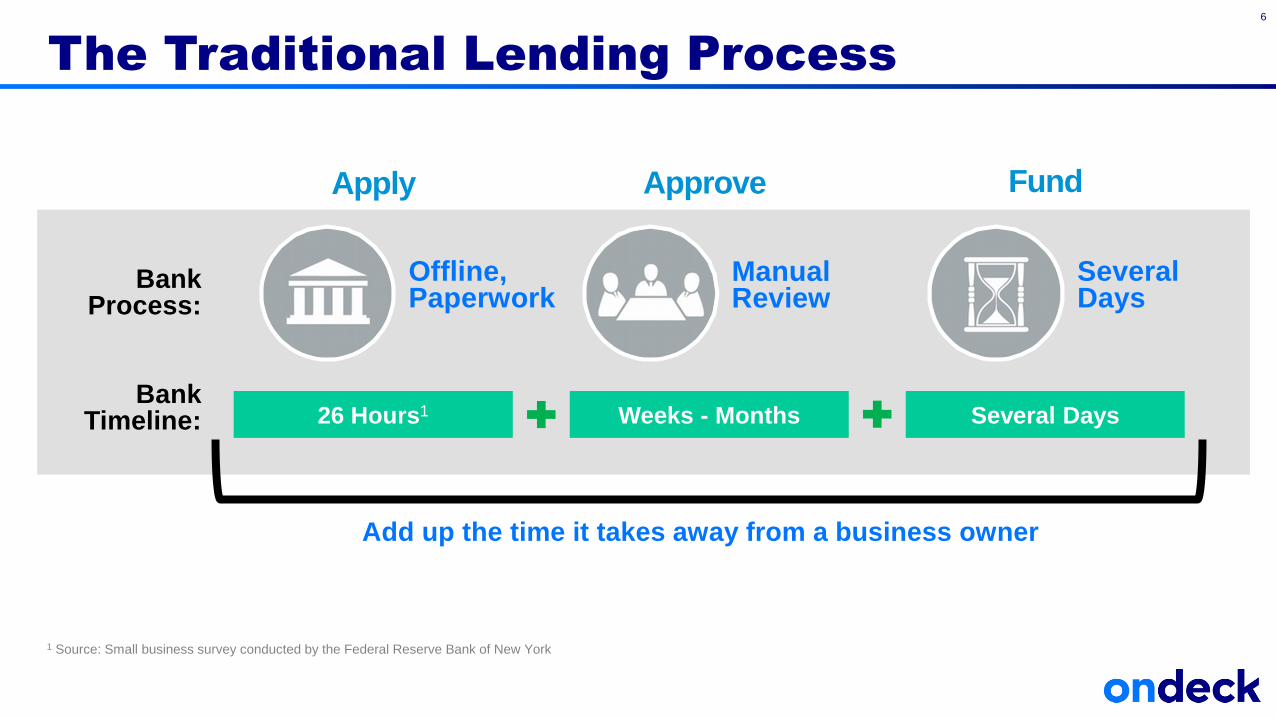

The Traditional Lending Process

6

Offline, Paperwork

Manual Review

Several Days

Bank Process:

1 Source: Small business survey conducted by the Federal Reserve Bank of New York

FundApproveApply

26 Hours1 Weeks - Months Several DaysBank

Timeline:

Add up the time it takes away from a business owner

Traditional Financing Options Just

Don’t Work for Everyone

7

• Banks like to make $5 million loans, not $50,000 loans

• Banks rely on manual, time consuming processes that make it difficult to give business owners quick answers

• Credit criteria focuses on personal credit score and collateral

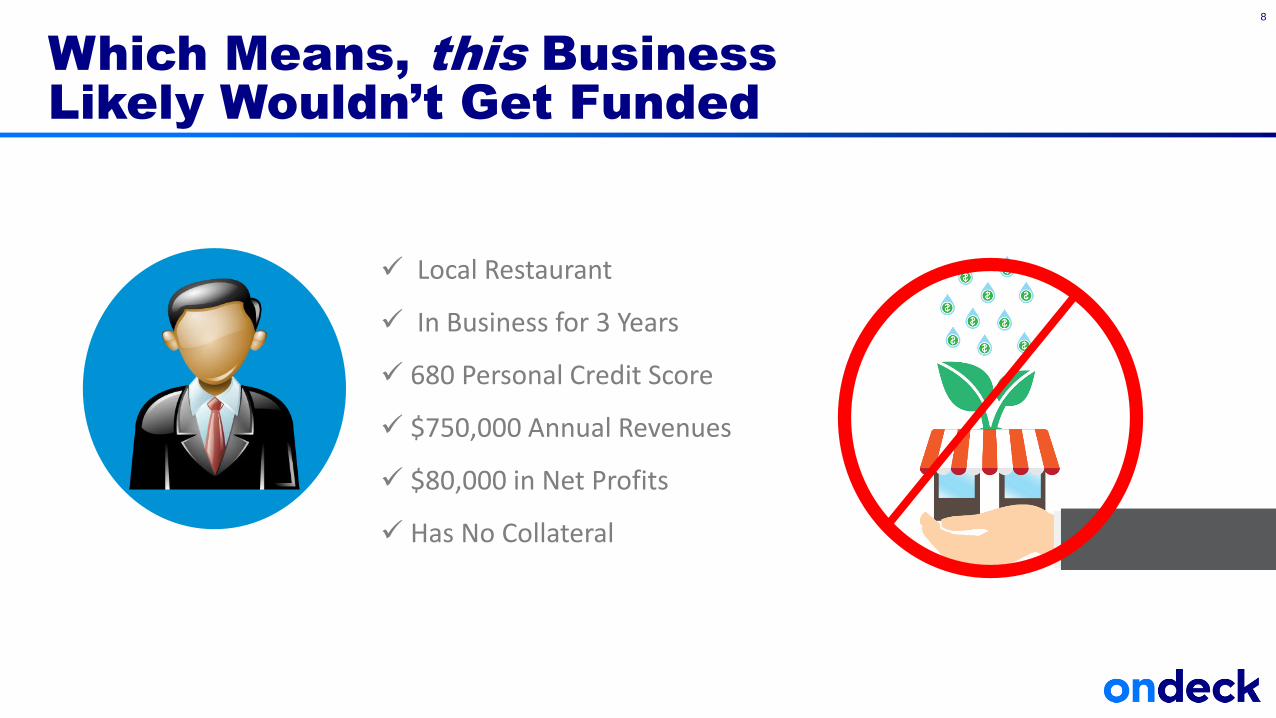

Which Means, this Business

Likely Wouldn’t Get Funded

8

Local Restaurant

In Business for 3 Years

680 Personal Credit Score

$750,000 Annual Revenues

$80,000 in Net Profits

Has No Collateral

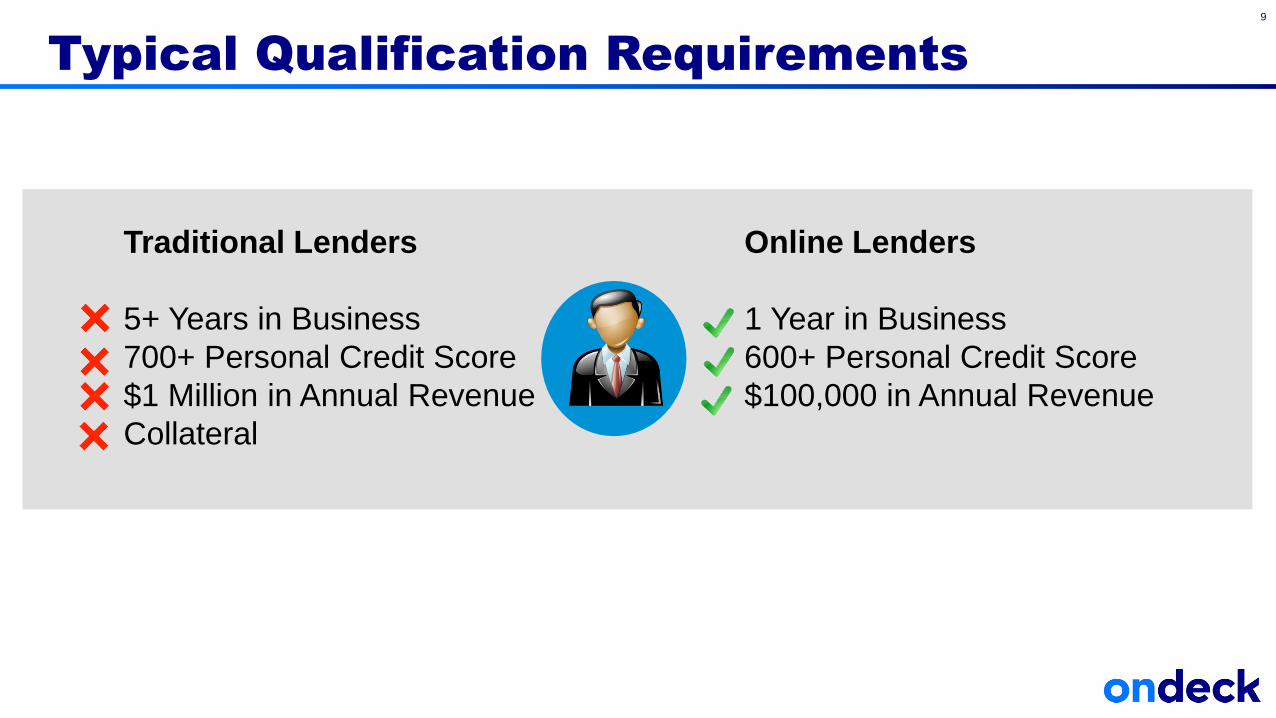

Typical Qualification Requirements

9

Online Lenders

1 Year in Business

600+ Personal Credit Score

$100,000 in Annual Revenue

Traditional Lenders

5+ Years in Business

700+ Personal Credit Score

$1 Million in Annual Revenue

Collateral

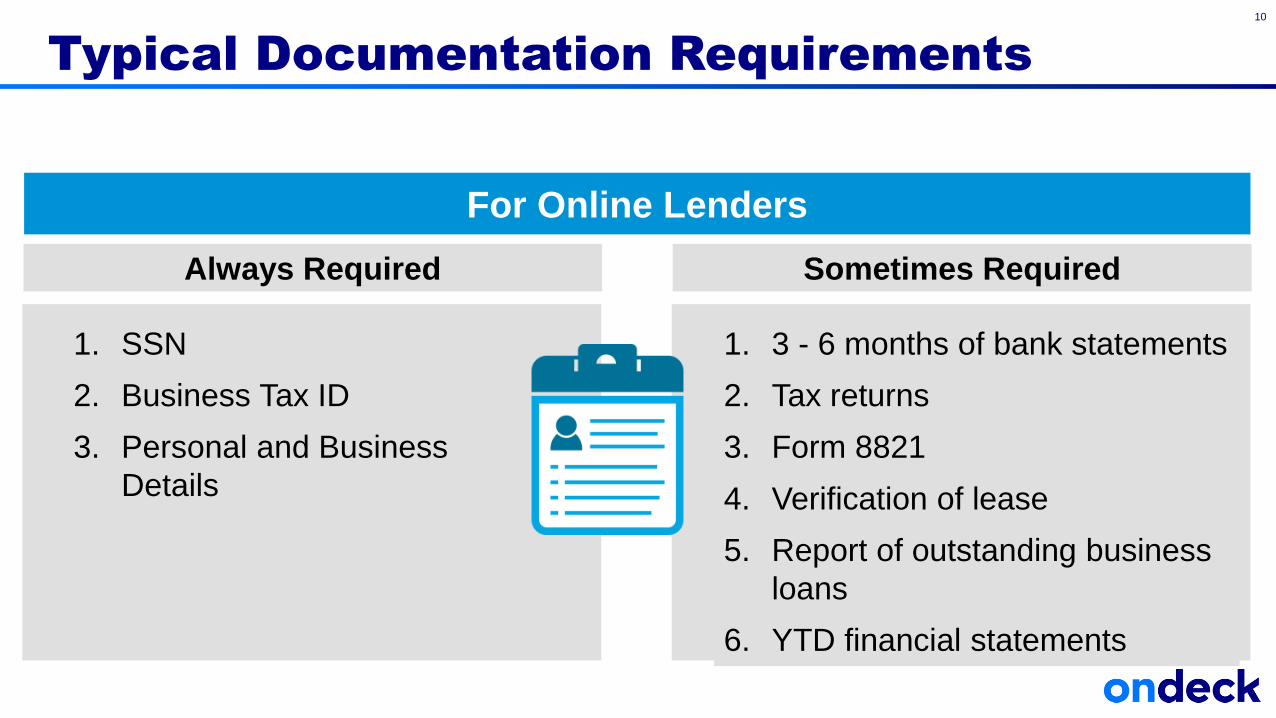

Typical Documentation Requirements

10

1. SSN

2. Business Tax ID

3. Personal and Business

Details

Sometimes RequiredAlways Required

For Online Lenders

1. 3 - 6 months of bank statements

2. Tax returns

3. Form 8821

4. Verification of lease

5. Report of outstanding business

loans

6. YTD financial statements

The Good News…

11

12

are creating new financing options

Business Owner Needs Technology+

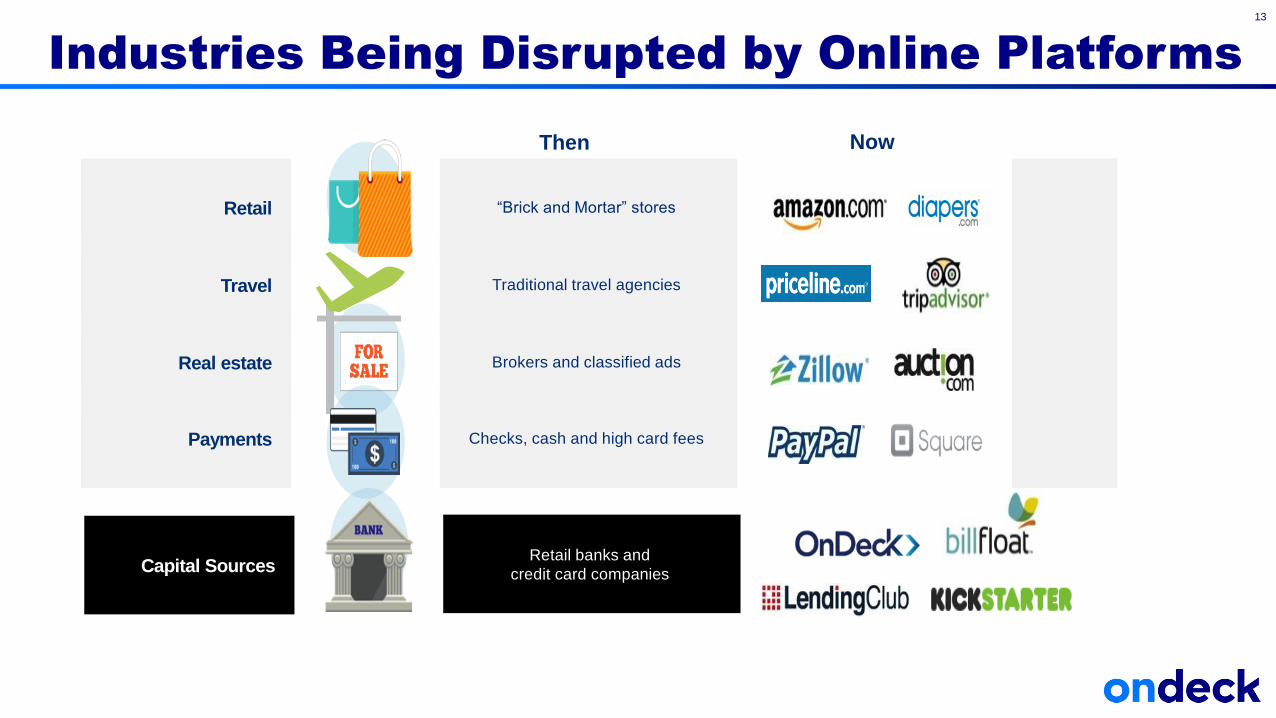

Industries Being Disrupted by Online Platforms

13

Then Now

Retail banks and

credit card companiesCapital Sources

“Brick and Mortar” storesRetail

Brokers and classified adsReal estate

Checks, cash and high card feesPayments

Traditional travel agenciesTravel

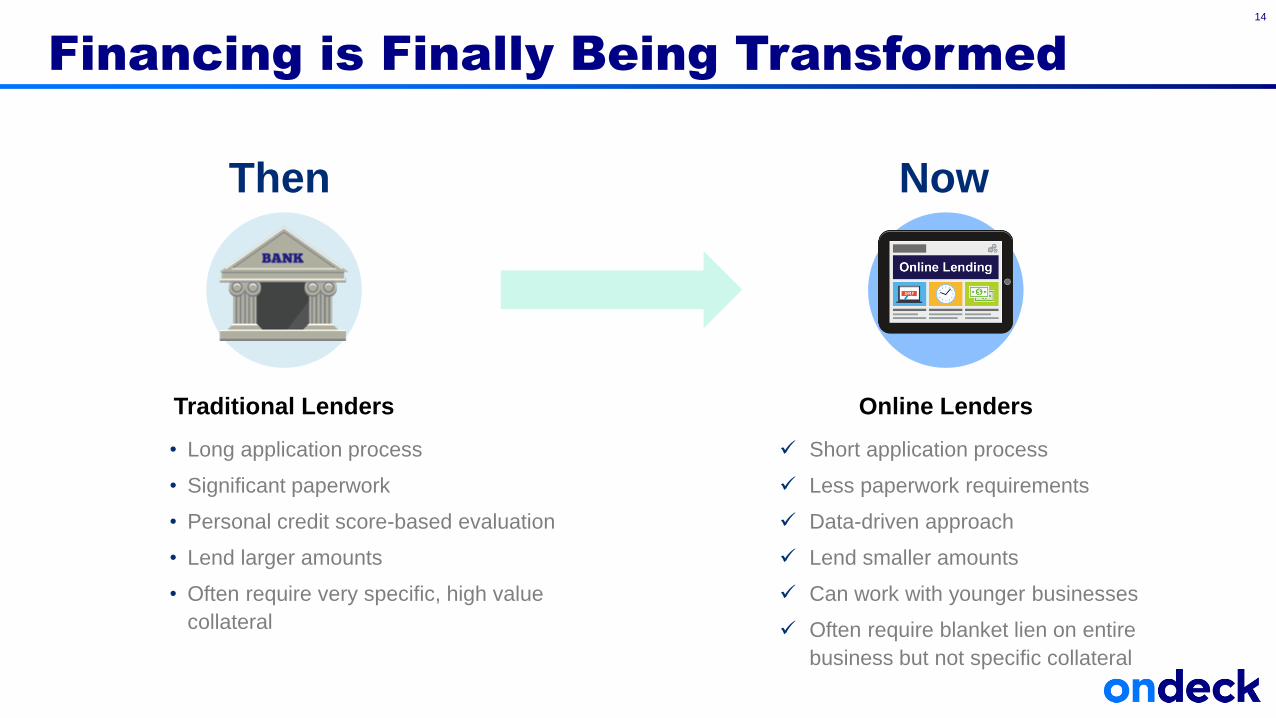

Financing is Finally Being Transformed

14

Then

Traditional Lenders

• Long application process

• Significant paperwork

• Personal credit score-based evaluation

• Lend larger amounts

• Often require very specific, high value

collateral

Now

Online Lenders

Short application process

Less paperwork requirements

Data-driven approach

Lend smaller amounts

Can work with younger businesses

Often require blanket lien on entire

business but not specific collateral

What Our Customers Value

15

Start Funding

1 Day

Speed ServiceAccess Cost

New Financing Options

16

Loan Matching Site

Crowdfunding Invoice Financing

Online Lending

Non-Profit Lenders

17

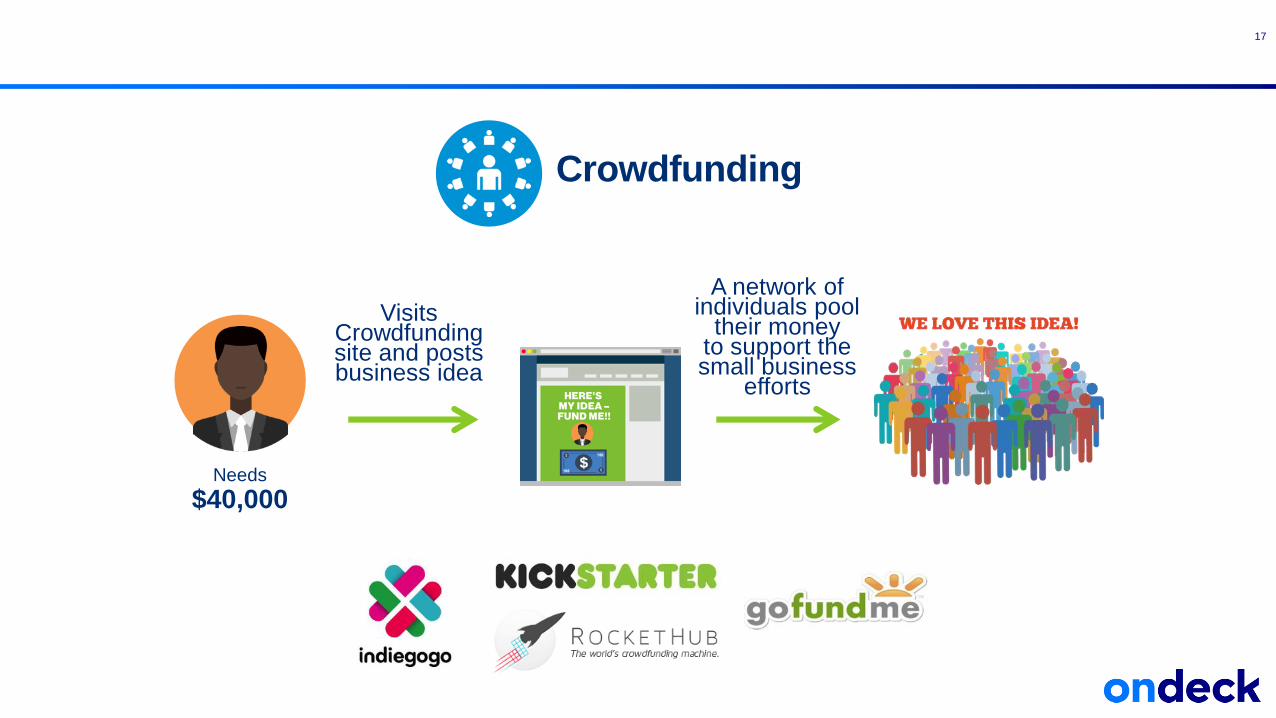

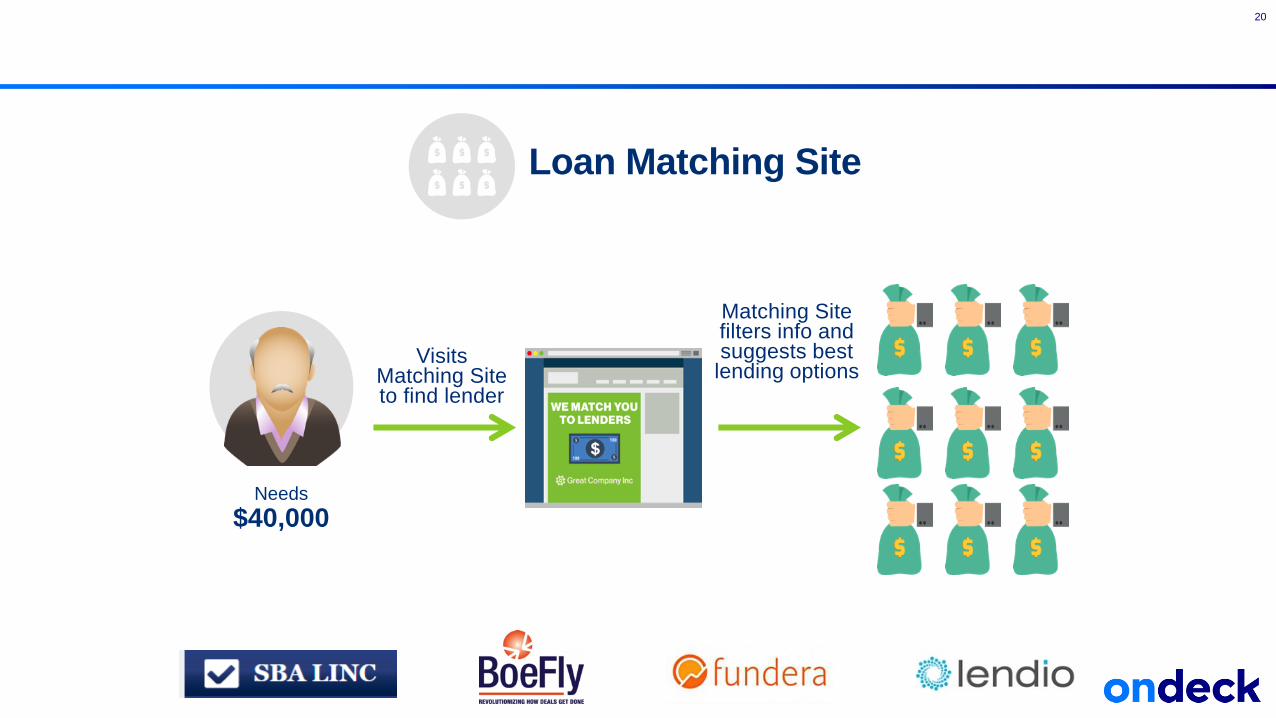

Needs

$40,000

Visits Crowdfundingsite and posts business idea

A network of individuals pool

their moneyto support thesmall business

efforts

Crowdfunding

18

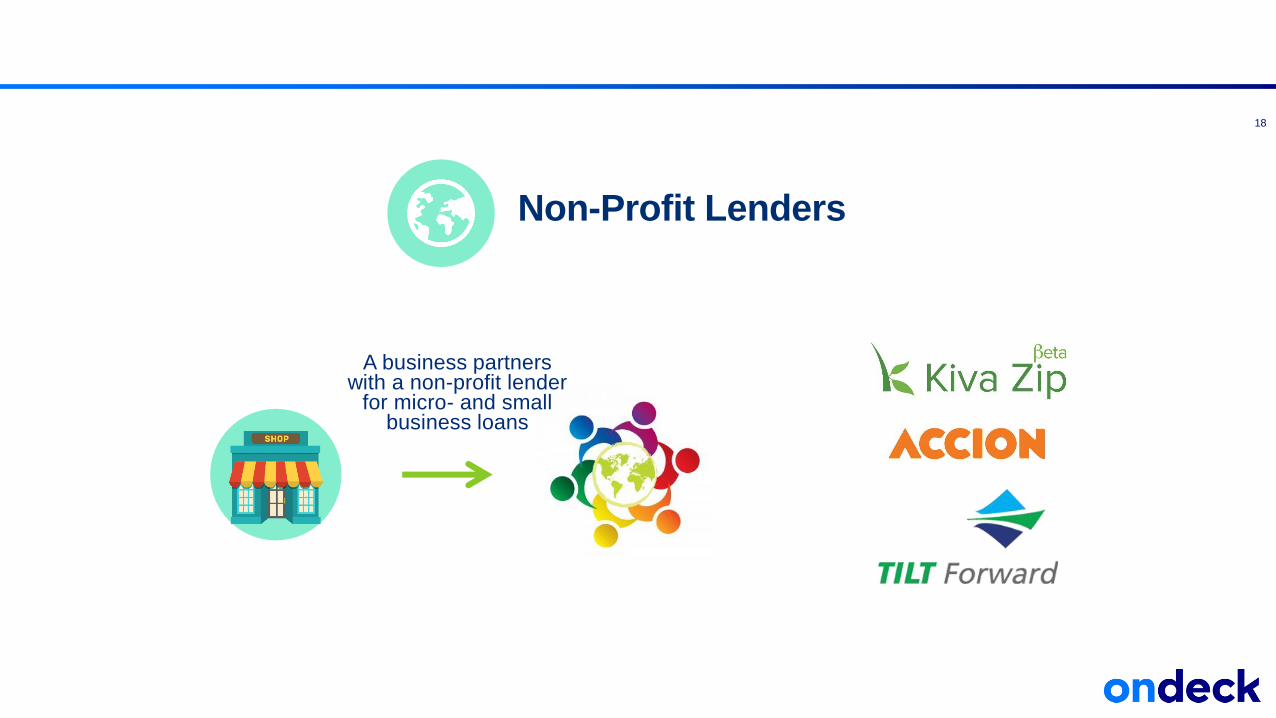

A business partners with a non-profit lender

for micro- and small business loans

Non-Profit Lenders

19

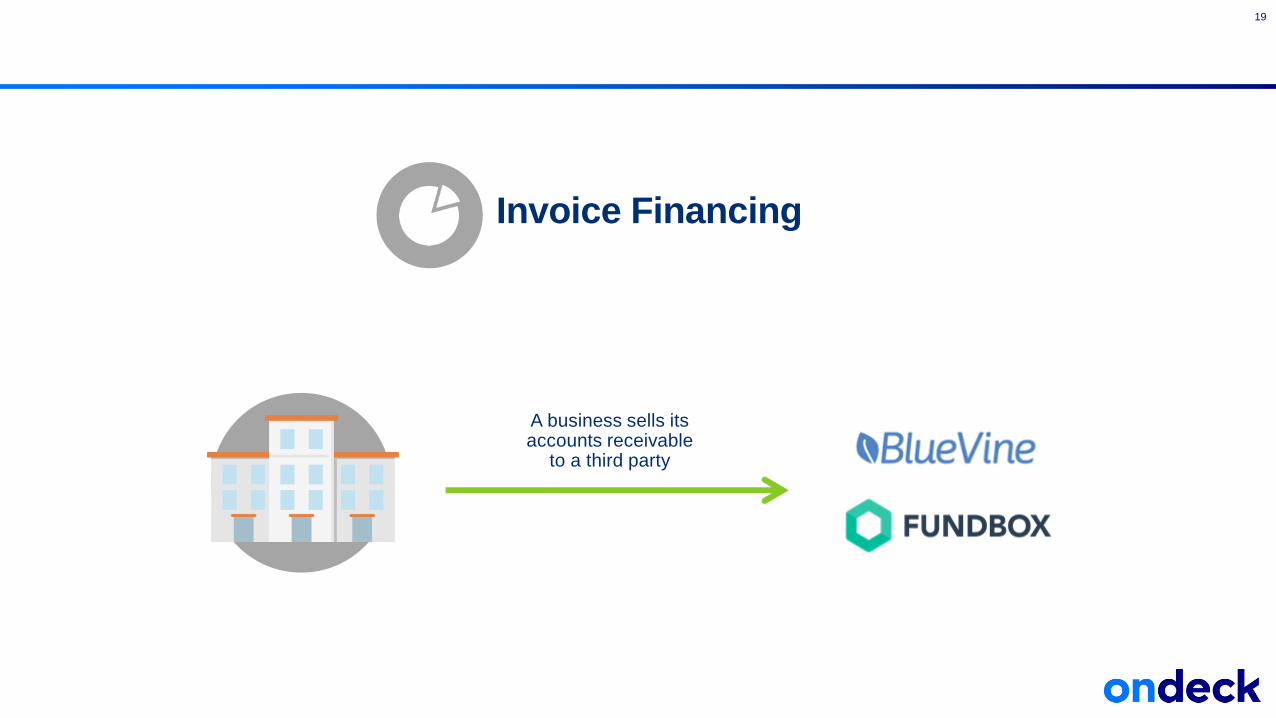

A business sells its accounts receivable

to a third party

Invoice Financing

20

Needs

$40,000

Visits Matching Siteto find lender

Matching Sitefilters info and suggests best

lending options

Loan Matching Site

21

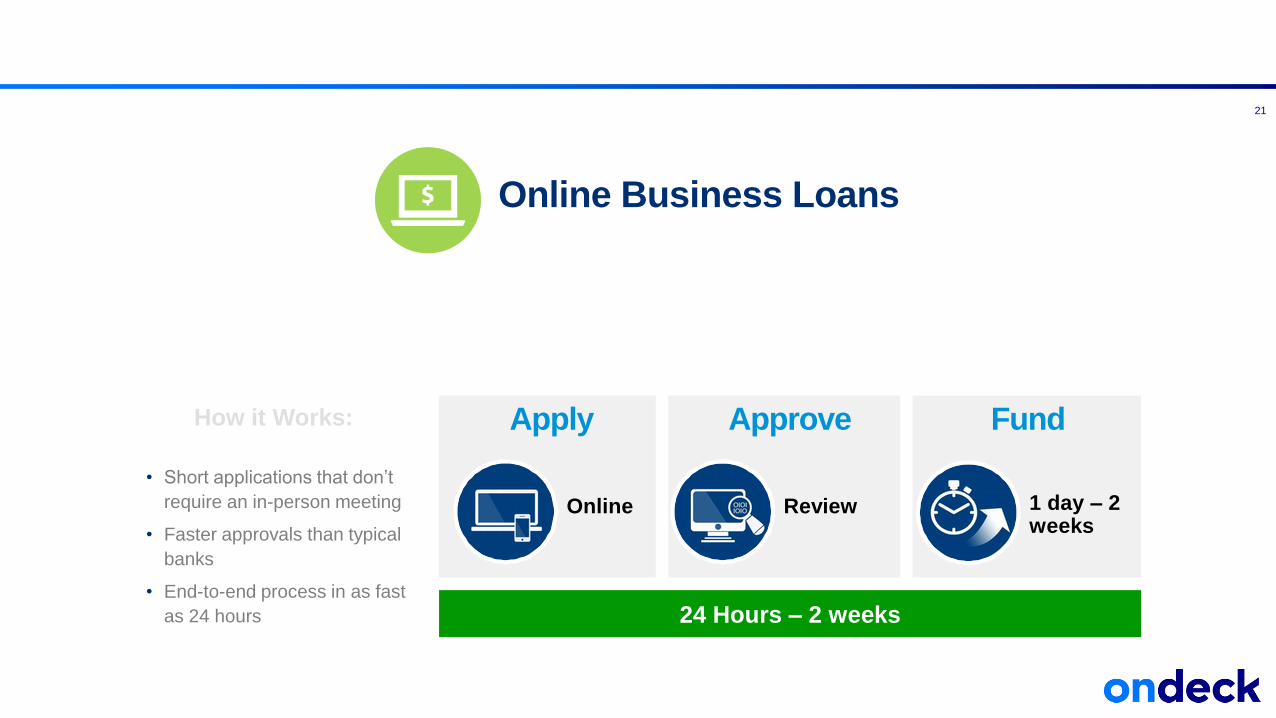

Online Business Loans

• Short applications that don’t

require an in-person meeting

• Faster approvals than typical

banks

• End-to-end process in as fast

as 24 hours

How it Works:

Online

Apply

Review

Approve

1 day – 2 weeks

Fund

24 Hours – 2 weeks

22

Online Business Loans

Short-Term and Long-Term Loans

23

Short Term Needs Long Term Needs

Short-Term Loans

24

Short Term Loans could be a good fit for:

Buying quick-turnaround inventory

Ramping up a new employee

Bridging a seasonal cash flow gap

Short Term Loans allow a borrower to:

Borrow with a term suited for their loan purpose

Meet the need

Pay off the debt quickly

Long-Term Loans

25

Long Term Loans could be a good fit for:

Purchasing a new warehouse or other building

Covering the expense of adding a new location

Purchasing heavy equipment

Long Term Loans allow a borrower to:

Meet a longer-term need with a term suited for

that loan purpose

Spread the cost of expensive purchases over

several years

As a General Rule

26

The longer the term,

the smaller the periodic payment—

but the greater the overall cost of the loan.

Shorter-term loans

typically have a lower overall cost—

but the periodic payments will be higher.

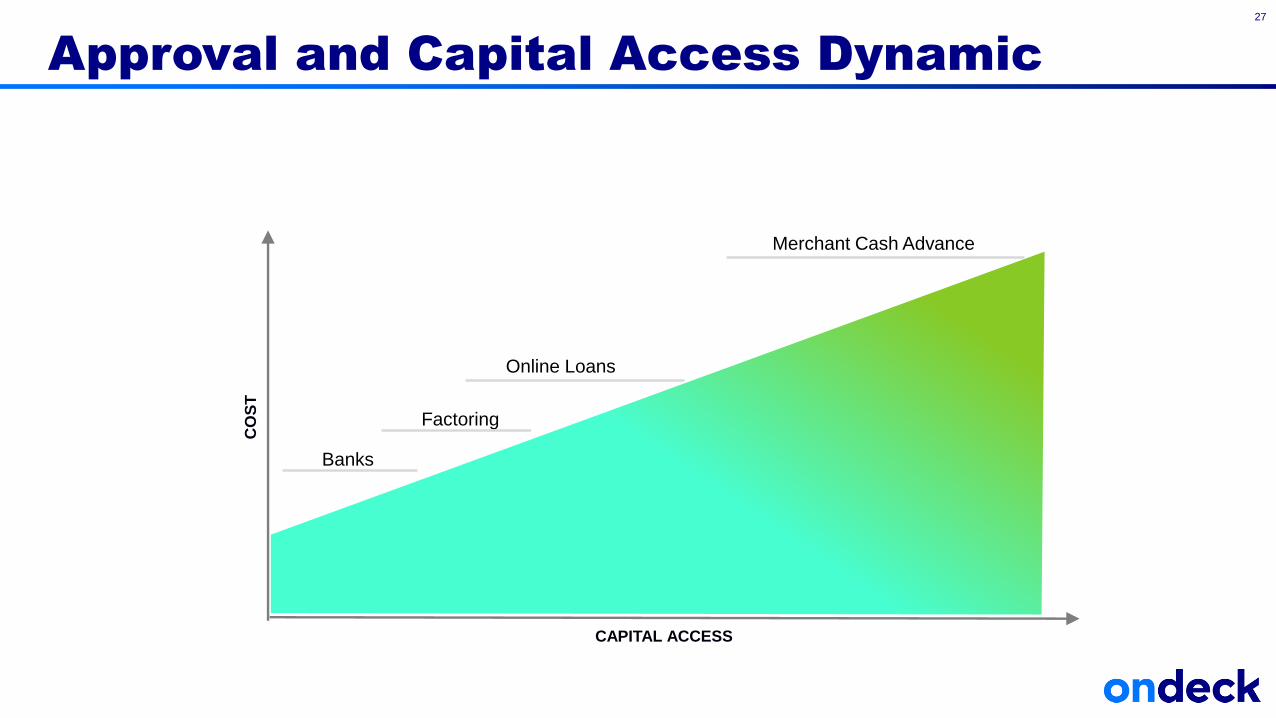

Approval and Capital Access Dynamic

27

CO

ST

CAPITAL ACCESS

Banks

Factoring

Online Loans

Merchant Cash Advance

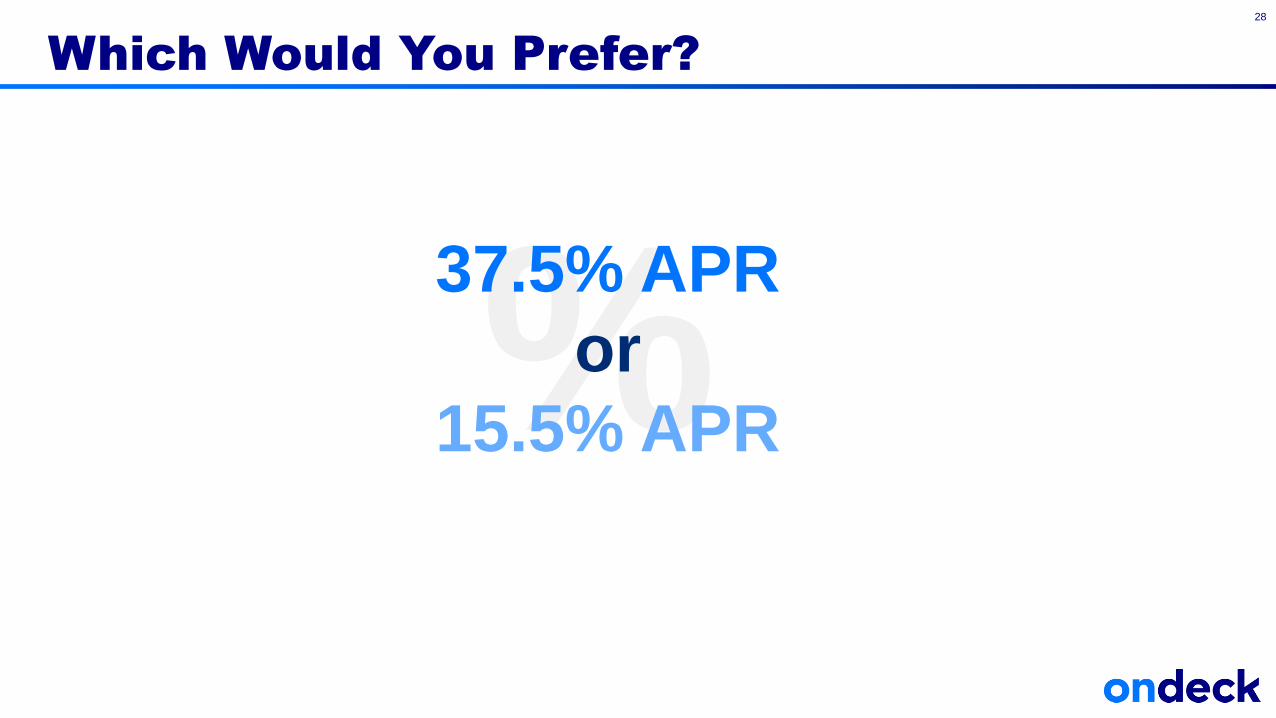

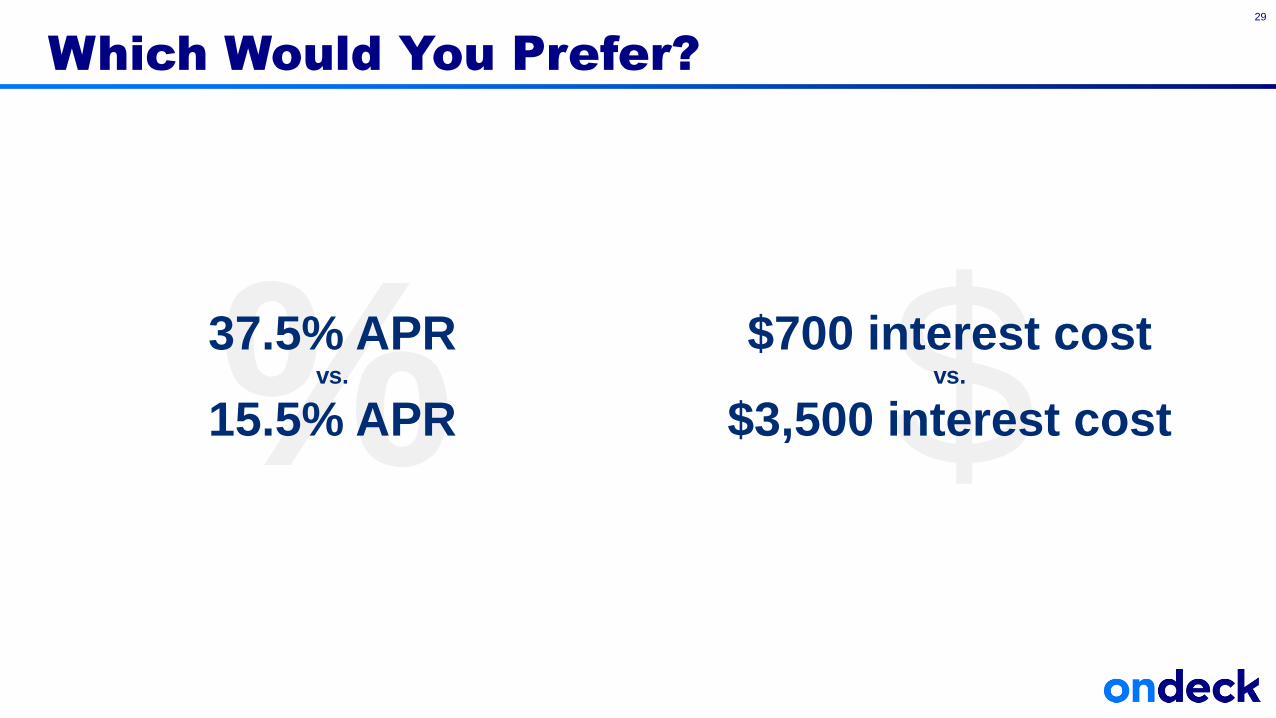

Which Would You Prefer?

28

%37.5% APR

or

15.5% APR

Which Would You Prefer?

29

%37.5% APR vs.

15.5% APR $$700 interest costvs.

$3,500 interest cost

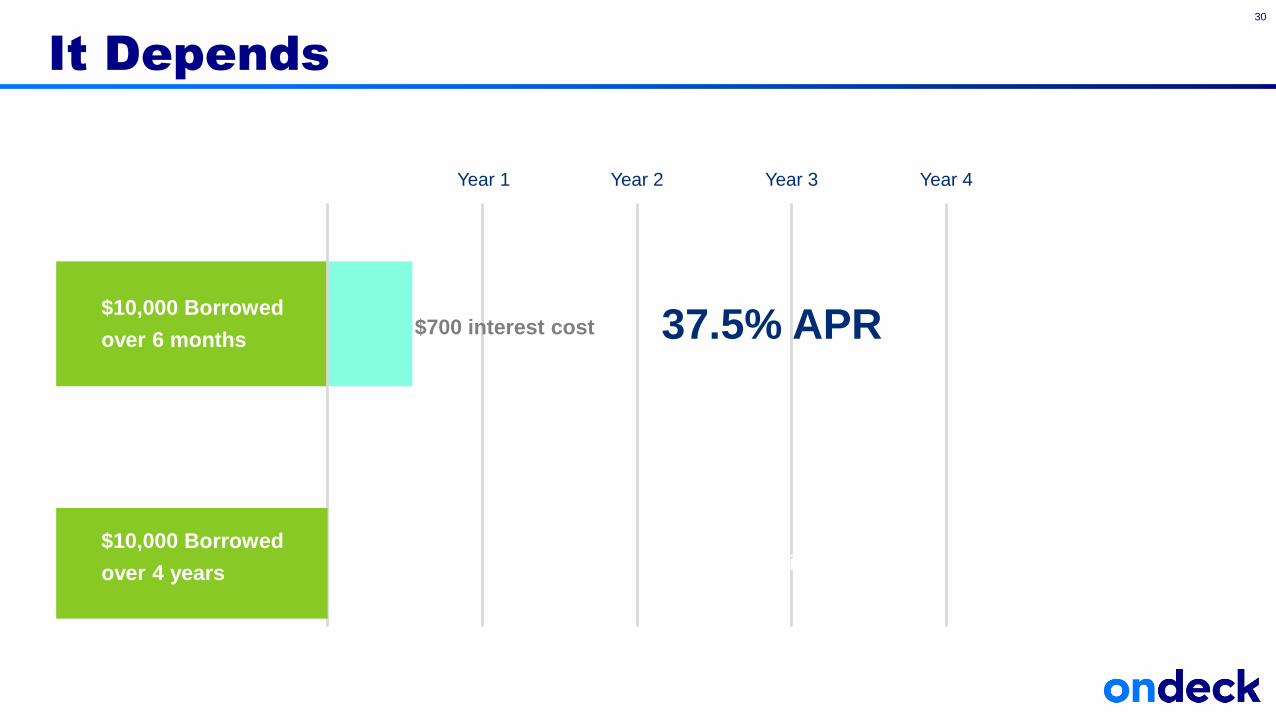

It Depends

30

$10,000 Borrowed

over 6 months

Year 1 Year 2 Year 3 Year 4

$4,800 interest cost

37.5% APR

$10,000 Borrowed

over 4 years

$700 interest cost

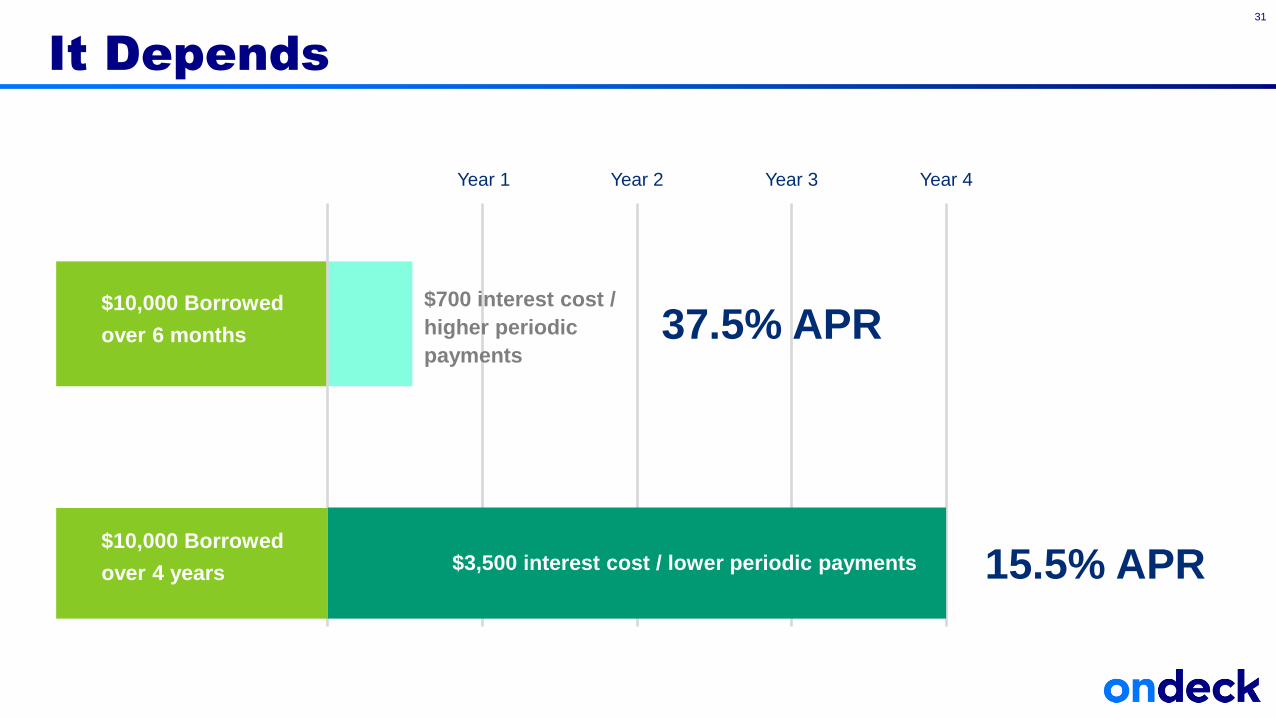

It Depends

31

$10,000 Borrowed

over 6 months

Year 1 Year 2 Year 3 Year 4

$3,500 interest cost / lower periodic payments

37.5% APR

$10,000 Borrowed

over 4 years 15.5% APR

$700 interest cost /

higher periodic

payments

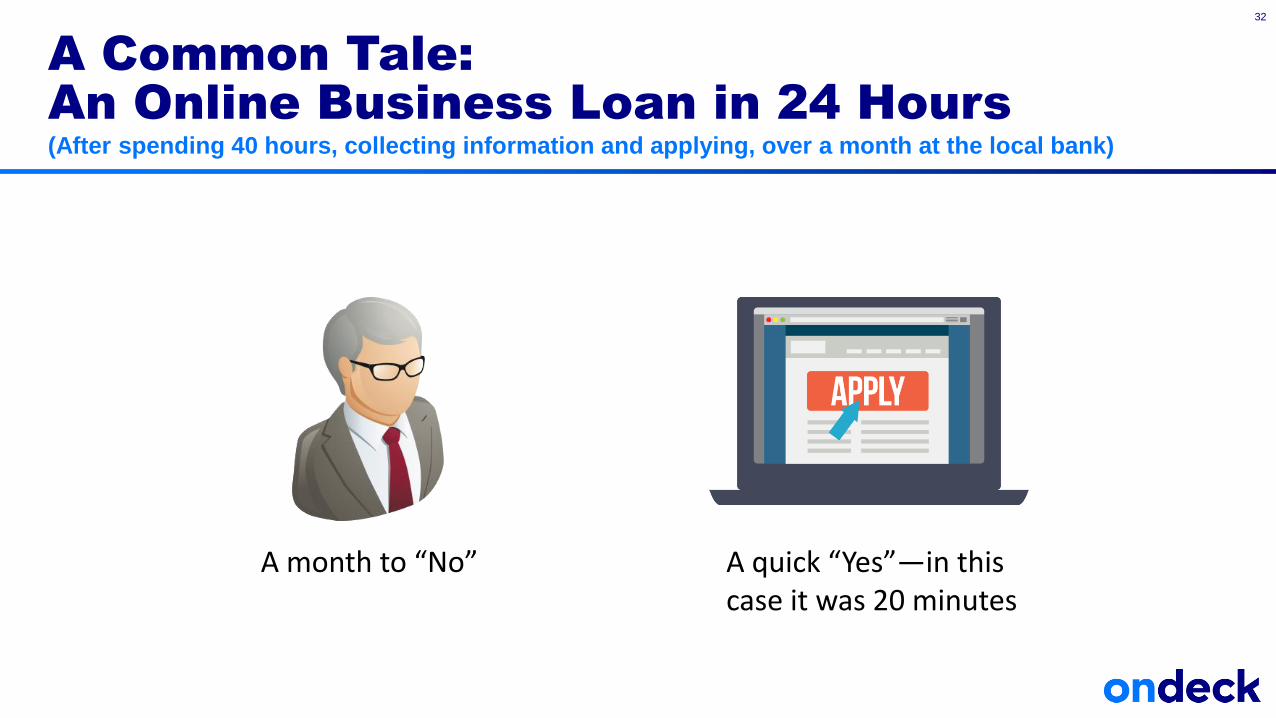

A Common Tale:

An Online Business Loan in 24 Hours

(After spending 40 hours, collecting information and applying, over a month at the local bank)

32

A month to “No” A quick “Yes”—in this case it was 20 minutes

Choosing the Right Loan

33

Loan Matching Site

Crowdfunding Invoice Financing

Online Lending

Non-Profit Lenders

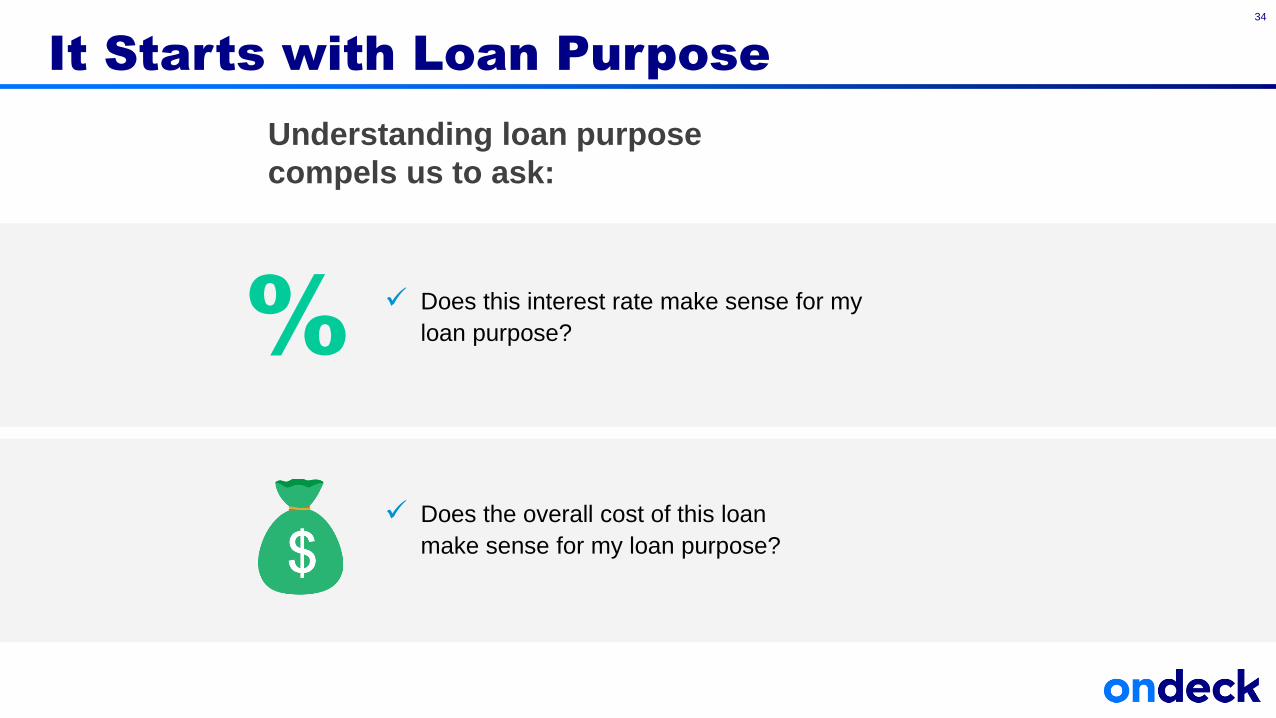

It Starts with Loan Purpose

34

Does this interest rate make sense for my

loan purpose?

Does the overall cost of this loan

make sense for my loan purpose?

%

Understanding loan purpose

compels us to ask:

It Starts with Loan Purpose

35

Nobody would buy a new car with a

30-year home mortgage, regardless of

how low the APR.

It would make the overall cost of the car

too expensive.

Loan Purpose Should Dictate Loan Amount

36

There are costs associated with borrowing—

Borrowing more than needed is

just too expensive

Lenders appreciate borrowers

who know what they really need

Loan Amount Influences Where to Look

37

Non-Profit

Micro-lenders

Loan Matching SitesOnline LendersBanks and

Credit Unions

The SBA

SBA

Good Fit for Online Small Business Loans

38

Pizzeria’s oven breaks down.

Needs to replace ovens

immediately.

Needs $25,000

Florist is gearing up for

Mother’s Day and needs to

stock up on inventory and

supplies.

Needs $15,000

Restaurant needs financing to

remodel and redecorate its

existing space.

Needs $150,000

Good Fit for a Business Loan at the Bank

39

Manufacturer needs to

purchase new heavy

equipment

Needs $400,000

A doctor wants to buy out her

partner’s 50% stake in the

practice.

Needs $700,000

Restaurant is looking to move

to a better location downtown.

Needs $1,000,000

Capital Needs and Considerations

40

Amount

Duration

Return

Cash flow

Buy inventory Purchase equipment

MarketingHiring Open new locations

Cash flow management New business idea

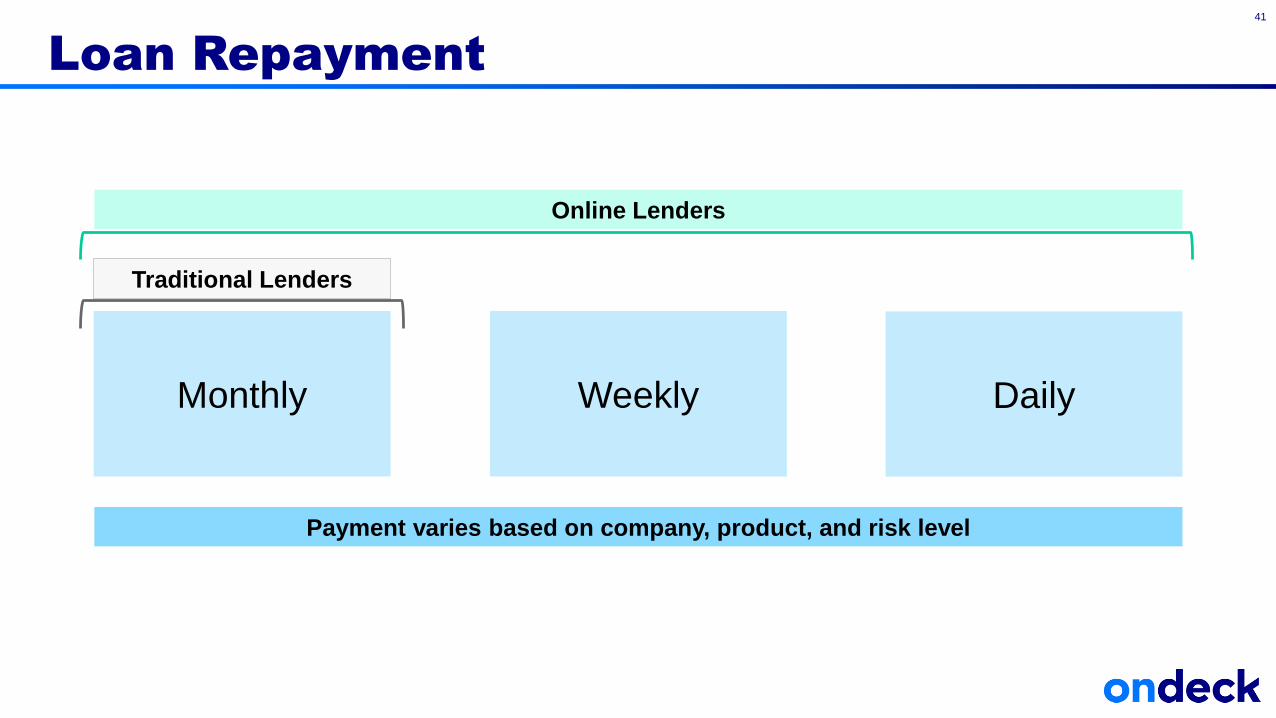

Loan Repayment

41

Monthly

Traditional Lenders

Weekly Daily

Online Lenders

Payment varies based on company, product, and risk level

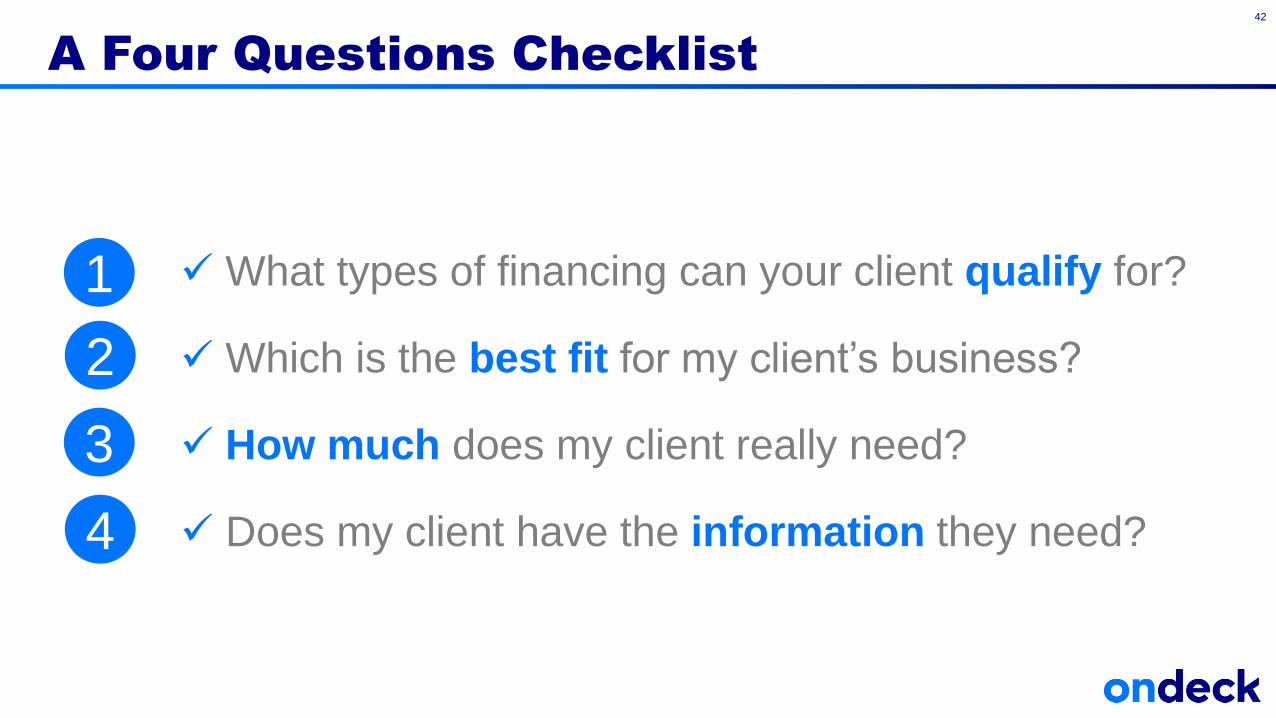

A Four Questions Checklist

42

What types of financing can your client qualify for?

Which is the best fit for my client’s business?

How much does my client really need?

Does my client have the information they need?

1

2

3

4

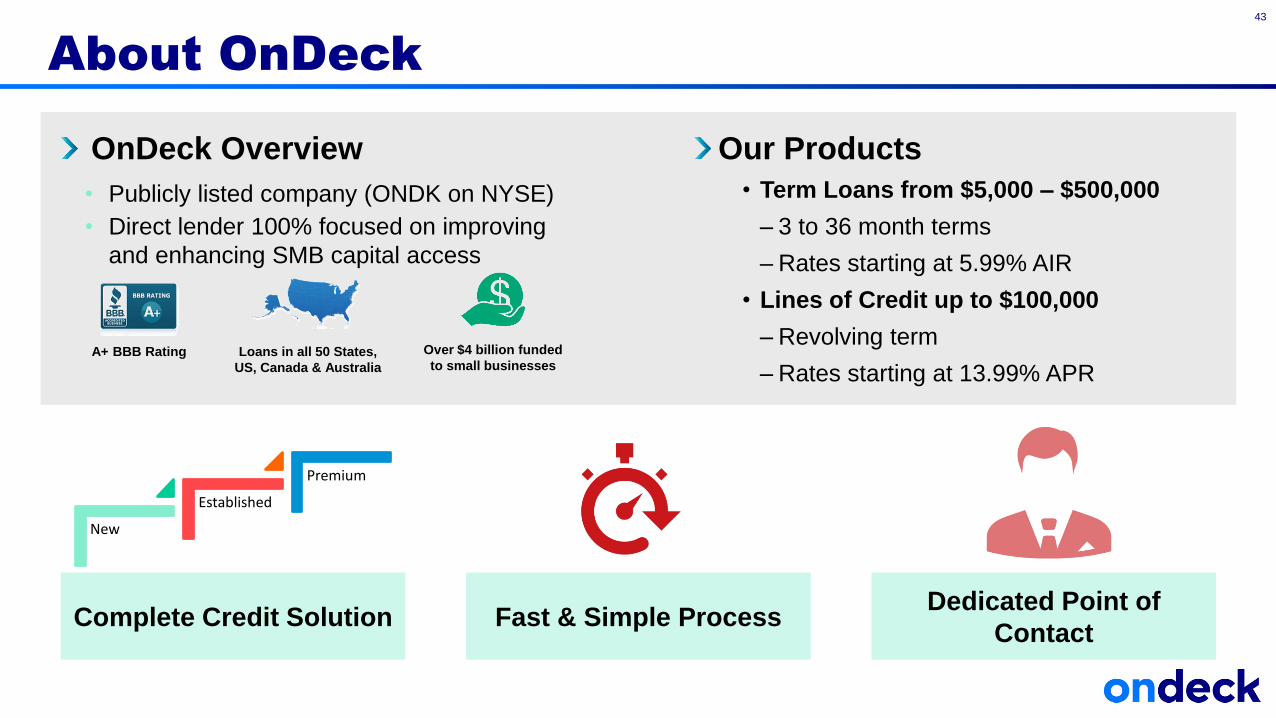

About OnDeck

43

OnDeck Overview

• Publicly listed company (ONDK on NYSE)

• Direct lender 100% focused on improving

and enhancing SMB capital access

Loans in all 50 States,

US, Canada & Australia

A+ BBB Rating

New

Established

Premium

Complete Credit Solution Fast & Simple ProcessDedicated Point of

Contact

Our Products

• Term Loans from $5,000 – $500,000

– 3 to 36 month terms

– Rates starting at 5.99% AIR

• Lines of Credit up to $100,000

– Revolving term

– Rates starting at 13.99% APROver $4 billion funded

to small businesses

44

Questions?

45

OnDeck’s educational website,

dedicated to simplifying small business lending

For more information about the world of online lending, visit: