Embed Size (px)

Citation preview

CC SS BB AA GG

Budgeting for equity

Understanding the Public Finance Management Act, 2015A simplified Version of the PFMA, 2015

Understanding the Public Finance Management Act, 2015 was produced by the Civil Society Budget Advocacy Group (CSBAG) with support from the Democratic Governance Facility, and the USAID Uganda and UKaid Governance and Accountability Participation Programme. The contents of this publication are the responsibility of CSBAG and not of our development partners.

© July 2016

Civil Society Budget Advocacy Group (CSBAG)P.O. Box 660, NtindaPlot 11 Vubya Close, Ntinda Nakawa Rd Fixed Line: +256-755-202-154E-mail: [email protected] Web www.csbag.org

| @CSBAGUGANDA CSBAG/Facebook.com

All rights reserved. No part of this publication may be reproduced, or reprinted in any form by any means without the prior permission of the copyright holder. CSBAG encourages its use and will be happy if excerpts are copied and used. When doing so, however please acknowledge CSBAG.

Table of Contents

Foreword 2

INTRODUCTION 4

WHY THE PUBLIC FINANCE MANAGEMENT ACT, 2015? 5

WHAT IS THE ROLE OF PARLIAMENT IN PFMA, 2015? 7

MACROECONOMIC AND FISCAL POLICIES 12

BUDGETING PREPARATION, APPROVAL AND MANAGEMENT 14

CONTINGENCIES FUND 19

CASH AND ASSET MANAGEMENT 20

PUBLIC DEBT MANAGEMENT 21

ACCOUNTING AND AUDIT 22

PETROLEUM REVENUE MANAGEMENT 24

MISCELLANEOUS 25

REFERENCES 26

Figure 1: PURPOSE OF THE PFM ACT 2015 5

Figure 2: BUDGET REPORTING CYCLE 14

Figure 3: FINANCIAL REPORTING TIMELINES 23

Introduction

The PFMA 2015 (as amended) addresses key gaps identified in PFM legislation leading to a repeal of the Public Finance and Accountability Act 2003. Specifically, the new law strengthened accountability and transparency in the use of public resources through increased Parliamentary oversight over the Executive, restored credibility and predictability of the national budget given a new financial reporting calendar and alignment of budget preparation, implementation and oversight, operationalised the Contingencies Fund as per Article 157 of the Constitution and regulated all government revenues including Petroleum Revenue Management.

As a result of pro-activeness of the Civil Society Budget Advocacy Group (CSBAG) to improve PFM and government’s efforts to consult stakeholders on the development of this omnibus law, CSBAG made contribution into the PFMA 2015 (as amended) to advocate for a people centered law that promotes inclusive planning, equitable budgeting and accountability.

Why the GuideThis simplified version of the Public Finance Management Act 2015 provides an overview of the Public Finance Management Act 2015 as amended. It is intended to be used as a quick reference guide for the Members of Parliament, Civil Society Organisations and other

stakeholders to ease their applicability of the law in the day to day conduct of public finance monitoring and advocacy at both National and Local Government Level.

The guide provides key highlights of the PFMA, 2015 as amended. It covers macroeconomic and fiscal policies, budget preparation, approval and management, contingencies fund, cash and asset, public debt, grants and guarantees, accounting and audit, petroleum revenue management and miscellaneous parts of the PFMA 2015 as amended. The detailed requirements and implementation guide are set out in Public Finance Management Regulations 2016, related guidelines and instructions.

The information in this guide is for general information only and should not be treated or relied on as a substitute for legal interpretation of the PFMA 2015 (as amended) or its application to particular circumstances or entities.

Target Audience: The simplified version of the Public Finance Management Act 2015 is intended to be used by Members of Parliament, Civil Society Organisations and other stakeholders to ease their applicability of the law in the day to day conduct of public finance monitoring and advocacy at both National and Local Government Level.

The Public Finance Management Act, (PFMA) 2015 (as amended), is aligned to the Constitution of the Republic of Uganda and Public Financial Management Reform Strategy (2014/15 - 2017/18). The PFMA includes robust planning, budgeting and accountability processes that are intended to promote stakeholder involvement and effective service delivery taking into account recent developments in oil sector.

Why the Public Finance Management Act, 2015?

UShs

Figure 1: PURPOSE OF

THE PFM ACT 2015

A comprehensive and sound legal and regulatory framework is a foundation of accountability systems for public resources entrusted to Government to administer on behalf of its citizens. Therefore, the PFMA 2015, under Section 2 of the Act, provides for public financial management in Uganda by establishing:

Table 1: KEY TERMS USED IN THE PFM ACT, 2015

Term Definition

Appropriation An authorization made under an Appropriation Act permitting payment out of the Consolidated Fund or the Petroleum Fund under specified conditions or for a specified purpose.

Appropriation in Aid

This refers to the category of expenditure that is non-tax and collected by institutions that spend at source.

Budget The Government Plan of Revenue and Expenditure for a financial year.

Consolidated Fund

The Consolidated Fund of Uganda established under Article 153 of the Constitution.

Classified expenditure

The expenses and commitments incurred by an authorized agency for the collection and dissemination of information related to national security interests and include the cost of procurement and maintenance of related assets.

Government Refers to the Central Government.

Government debt A financial claim on the Government that requires payment by Government, of the principal, or the principal and the interest, to a creditor.

Inventories means

(a) Assets in the form of materials or supplies to be consumed in the production process,

(b) Assets in the form of materials or supplies to be consumed or distributed in the rendering of services; and

(c) Assets held for sale or distribution in the ordinary course of operation.

Public corporation

(a) An authority established by an Act of Parliament other than a local government, which receives a contribution from public funds, or the operations of which may, under the Act establishing it or any Act relating to it, impose or create a liability upon public funds; and

(b) Any public body which in a financial year receives any income from public funds.

Public debt Includes the interest on that debt, sinking fund payments in respect of that debt and the costs, charges and expenses incidental to the management of that debt.

Sector A group of institutions or votes that have common functions, objectives and mandates.

Statutory expenditure

Expenditure charged on the Consolidated Fund by the Constitution or by an Act of Parliament, but does not include the expenditure of moneys appropriated or granted by an Appropriation Act or a Supplementary Appropriation Act.

Treasury memoranda

An action report by the minister responsible for finance detailing the actions taken on the recommendations of Parliament arising out of the report of the Auditor General.

Virement The reallocation of funds within the budget of a vote, from a budget line to another budget line.

Votes An entity for which an appropriation is made by an Appropriation Act or Supplementary Appropriation Act.

What is the role of parliament in PFMA, 2015?

Chapter nine of the Constitution under Articles 152, 153,154 and 159 requires Government to seek authority by or under an Act of Parliamentary to levy tax, receive or retain revenue, borrow or spend public money. The PFMA, 2015 is the prime legislative framework for Parliamentary authorization and scrutiny of Government’s revenue and expenditure proposals and management of Government’s assets and liabilities.

Government is required to effectively and efficiently manage the public resources and provide timely accountability to Parliament. Below is a key highlight of the role of Parliament outlined in the PFMA, 2015 as amended.

Table 2: KEY HIGHLIGHTS OF THE ROLE OF PARLIAMENT AS STIPULATED IN THE PFM ACT, 2015

Part Name Policy Objectives Role of Parliament PFMA, 2015 Reference

PART II Macroeconomic and Fiscal Policies

Principles and objectives to guide government spending and revenue mobilisation for economic stabilization and long term sustainability of public finances in a prudent and transparent manner.

Approve the Charter for Fiscal Responsibility and any deviations from its objectives

Sec.5(5)

Approve the Budget Framework Paper by 1st February for each financial year

Sec.9(8)

Analyze and make recommendations where necessary in government policies and programmes affecting the economy

Sec. 12(1)

Ensure public resources are held and utilized in a transparent, accountable, efficient, effective and sustainable manner and in accordance with the Charter and Budget Framework Paper

Sec.12(2)

PART III Budget Preparation, Approval and Management

Procedures for optimal resource allocation and efficiency based on government policy and national strategic objectives. To enable the budget to be implemented as intended.

Approve annual budget, work plan of government for the next financial year and the Appropriation Bill and any other bills that may be necessary to implement the national budget by 31st May of each year

Sec.14(1)

Consider a report on fiscal performance

Sec.18(1)

Authorise a reallocation of funds from a vote

Sec.20

Authorise a vote to enter into a commitment of more than one financial year as part of the Annual Budget

Sec.23 (2)

Scrutinize classified expenditure 24 (2)

Approve Supplementary Appropriation Bill (Refer to PFMA Amendment Act) which is over 3% of the approved budget

Sec.25(1)

Receive supplementary estimates of amounts spent within 4 months of spending (Refer to PFMA Amendment Act)

Sec.25(2)

PART IV Contingencies Fund

Provides for financing responses to natural disasters that is in the public interest

Appropriate money to Contingencies Fund up to 0.5 % of the total approved budget for that financial year (Refer to PFMA Amendment Act)

Sec.26

May Invalidate a withdrawal from the Contingencies Fund where Parliament determines that the requirements of the law are not complied with

Sec.26(13)

Consider Auditor General’s report on accounts of the Contingencies Fund

Sec.26(16)

PART V Cash and Asset Management

Prudent and safe custody in management of Government resources and investments

Authorize votes, state enterprises or public corporation through an Act of Parliament to collect, receive or retain revenue

Sec.29

Approve abandonment of claims and write off of public money and stores

Sec.35(1)

Consider a report for losses authorized by the Minister

Sec.35(5)

PART VI Public Debt, Grants and Guarantees

Sustainable debt financing and comprehensive capture of all finances of government

Approve loans raised by the Minister

Sec.36(5)

Approve authority to guarantee loans & consider report on existing guarantees

Sec.39 (4)

Consider Minister’s report on Government debt

Sec.42(2)

Appropriate expenditure to be incurred on donor funded projects

Sec.43(1)

Consider Minister’s report on grants received by Government or a vote

Sec.44(5)

PART VII Accounting and Audit

Accountability and transparency in the use of public resources

Hold Accounting Officers personally and accountable for the activities of a vote

Sec.45(5)

Receive from the Minister the Treasury Memorandum within 6months from the date of Parliament’s consideration of the report of the Auditor General

Sec.53

PART VIII Petroleum Revenue Management

Prescribes framework for prudent management of petroleum revenue

Authorise by an Appropriation Act any withdraws from the Petroleum Fund

Sec.58

Appropriate money from the Petroleum Fund to the Consolidated Fund and Petroleum Revenue Investment Reserve

62 (1)

Consider Minister’s reports on the Petroleum Fund on estimated revenue and accounts by 30th SeptemberSemiannual (1st April) and annual reports (31st December) of the fund

Sec.61 (1) (a) & (b)

Consider Minister’s policy guidance to Bank of Uganda regarding Government’s expectation on the performance of the Petroleum Revenue Investment Reserve including risk and return

Sec.65 (2)

Approve the Annual Plan of the Petroleum Revenue Investment Reserve

Sec.71(3)

Consider Minister’s Annual report on the Petroleum Revenue Investment Reserve

Sec.72(3)

Consider Audit report on Petroleum Fund and Petroleum Revenue Investment Reserve

Sec.73(2)

PART IX Miscellaneous Consider Certificate of financial implications issued by Minister to accompany every Bill introduced in Parliament,

Sec.76 (1)

Consider report on exemption of tax

Sec.77 (1)

Liability on failure to meet requirements, Offences and Surcharges, Amendments, Repeals, Transitional provisions

Sec.78-85

SCHEDULES Schedules 1 -6 Currency points, formats for the CFR& BFPs, terms and conditions for raising loans, provisions for submission of accounts & formula for revenue sharing from royalties among local governments

Sch.1-6

Table 3: REPORTS TO PARLIAMENT UNDER THE PFM ACT,2015

Part Name Policy Objectives Role of Parliament PFMA, 2015 Reference

PART II Macroeconomic and Fiscal Policies

Principles and objectives to guide government spending and revenue mobilisation for economic stabilization and long term sustainability of public finances in a prudent and transparent manner.

Approve the Charter for Fiscal Responsibility and any deviations from its objectives

Sec.5(5)

Approve the Budget Framework Paper by 1st February for each financial year

Sec.9(8)

Analyze and make recommendations where necessary in government policies and programmes affecting the economy

Sec. 12(1)

Ensure public resources are held and utilized in a transparent, accountable, efficient, effective and sustainable manner and in accordance with the Charter and Budget Framework Paper

Sec.12(2)

PART III Budget Preparation, Approval and Management

Procedures for optimal resource allocation and efficiency based on government policy and national strategic objectives. To enable the budget to be implemented as intended.

Approve annual budget, work plan of government for the next financial year and the Appropriation Bill and any other bills that may be necessary to implement the national budget by 31st May of each year

Sec.14(1)

Consider a report on fiscal performance

Sec.18(1)

Authorise a reallocation of funds from a vote

Sec.20

Authorise a vote to enter into a commitment of more than one financial year as part of the Annual Budget

Sec.23 (2)

Scrutinize classified expenditure 24 (2)

Approve Supplementary Appropriation Bill (Refer to PFMA Amendment Act) which is over 3% of the approved budget

Sec.25(1)

Receive supplementary estimates of amounts spent within 4 months of spending (Refer to PFMA Amendment Act)

Sec.25(2)

PART IV Contingencies Fund

Provides for financing responses to natural disasters that is in the public interest

Appropriate money to Contingencies Fund up to 0.5 % of the total approved budget for that financial year (Refer to PFMA Amendment Act)

Sec.26

May Invalidate a withdrawal from the Contingencies Fund where Parliament determines that the requirements of the law are not complied with

Sec.26(13)

Consider Auditor General’s report on accounts of the Contingencies Fund

Sec.26(16)

PART V Cash and Asset Management

Prudent and safe custody in management of Government resources and investments

Authorize votes, state enterprises or public corporation through an Act of Parliament to collect, receive or retain revenue

Sec.29

Approve abandonment of claims and write off of public money and stores

Sec.35(1)

Consider a report for losses authorized by the Minister

Sec.35(5)

PART VI Public Debt, Grants and Guarantees

Sustainable debt financing and comprehensive capture of all finances of government

Approve loans raised by the Minister

Sec.36(5)

Approve authority to guarantee loans & consider report on existing guarantees

Sec.39 (4)

Consider Minister’s report on Government debt

Sec.42(2)

Appropriate expenditure to be incurred on donor funded projects

Sec.43(1)

Consider Minister’s report on grants received by Government or a vote

Sec.44(5)

PART VII Accounting and Audit

Accountability and transparency in the use of public resources

Hold Accounting Officers personally and accountable for the activities of a vote

Sec.45(5)

Receive from the Minister the Treasury Memorandum within 6months from the date of Parliament’s consideration of the report of the Auditor General

Sec.53

PART VIII Petroleum Revenue Management

Prescribes framework for prudent management of petroleum revenue

Authorise by an Appropriation Act any withdraws from the Petroleum Fund

Sec.58

Appropriate money from the Petroleum Fund to the Consolidated Fund and Petroleum Revenue Investment Reserve

62 (1)

Consider Minister’s reports on the Petroleum Fund on estimated revenue and accounts by 30th SeptemberSemiannual (1st April) and annual reports (31st December) of the fund

Sec.61 (1) (a) & (b)

Consider Minister’s policy guidance to Bank of Uganda regarding Government’s expectation on the performance of the Petroleum Revenue Investment Reserve including risk and return

Sec.65 (2)

Approve the Annual Plan of the Petroleum Revenue Investment Reserve

Sec.71(3)

Consider Minister’s Annual report on the Petroleum Revenue Investment Reserve

Sec.72(3)

Consider Audit report on Petroleum Fund and Petroleum Revenue Investment Reserve

Sec.73(2)

PART IX Miscellaneous Consider Certificate of financial implications issued by Minister to accompany every Bill introduced in Parliament,

Sec.76 (1)

Consider report on exemption of tax

Sec.77 (1)

Liability on failure to meet requirements, Offences and Surcharges, Amendments, Repeals, Transitional provisions

Sec.78-85

SCHEDULES Schedules 1 -6 Currency points, formats for the CFR& BFPs, terms and conditions for raising loans, provisions for submission of accounts & formula for revenue sharing from royalties among local governments

Sch.1-6

Table 3: REPORTS TO PARLIAMENT UNDER THE PFM ACT,2015

REPORT DATES

The Minister Reports on Fiscal Performance to Parliament (section 18)

28th February and 31st October

The Minister reports to Parliament the reasons for non-utilization of grants to Local Governments (section 17(5)) By 1st April

The Minister reports to Parliament the performance of the Multiyear commitments made (section 23(4)). By 1st April

The Auditor General reports to Parliament on the accounts of the Contingencies Fund (section 26(16)) 31st December

The Minister reports to Parliament on abandonment of claims and write off of public money and stores (section 35(5)) By 30th September

The Minister reports to Parliament on Management of Government Debt, guaranteed loans and the other financial liabilities of Government and analysis of associated risks (section 42(2)) and (section 39(4))

1st April

The Minister report to Parliament on Grants received by Government or received by Vote (section 44(5)). 1st April

A Person or Authority granted power to exempt the payment or to vary any tax under an Act of Parliament shall make report to Parliament on exemption of Tax (section 77(1))

By 30th Sept, 31st Dec, 31st March and 30th June

The Minister tables to Parliament the Estimated Petroleum Revenue for the FY (section 61(1)(a)) 30th Sept

The Minister tables to Parliament Semi-annual and Annual reports on the performance of the Petroleum Fund (section 61(1)(b))

1st April and 31st Dec

The Minister tables to Parliament an annual plan and performance report of the Petroleum Revenue Investment Reserve (section 71(3)) and (section 72(3))

1st April

The Auditor General submits an audit report to Parliament on the Petroleum Revenue Investment Reserve (section 73(2))

30th June and 31st December

The Minister submits to Parliament a Treasury Memoranda (section 53(1))

Within six months from the date of Parliament’s consideration of AG report

Mandate of key offices in Public Financial Management

The PFMA 2015 establishes clear lines of responsibility in the management of public resources.

Macro Economic and Fiscal Policies

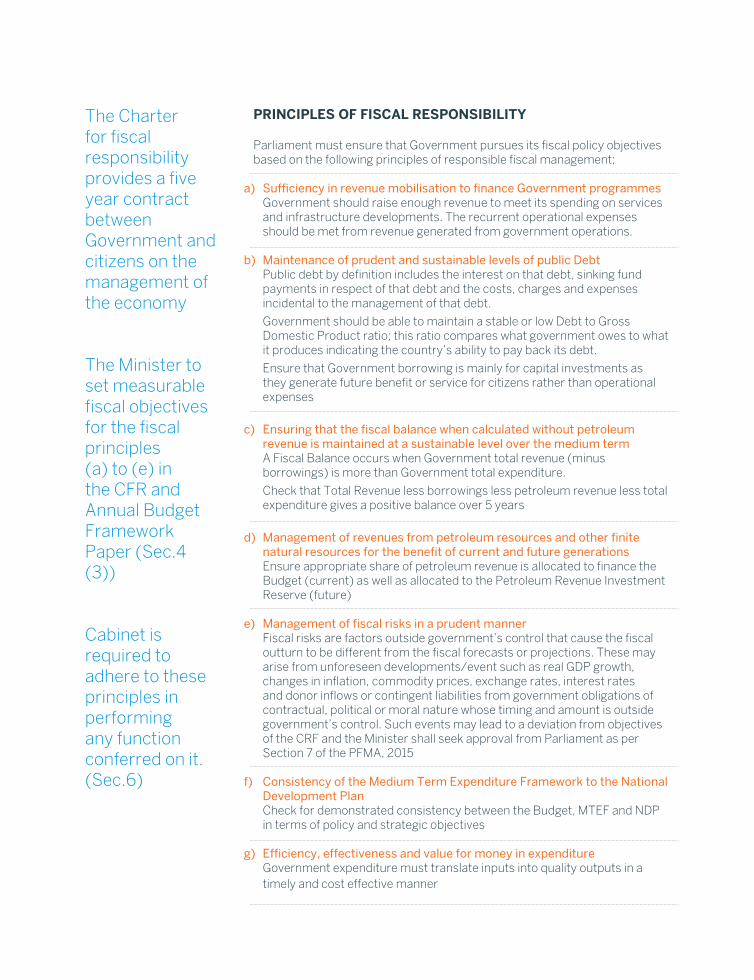

The Charter for fiscal responsibility provides a five year contract between Government and citizens on the management of the economy

The Minister to set measurable fiscal objectives for the fiscal principles (a) to (e) in the CFR and Annual Budget Framework Paper (Sec.4 (3))

Cabinet is required to adhere to these principles in performing any function conferred on it. (Sec.6)

PRINCIPLES OF FISCAL RESPONSIBILITY

Parliament must ensure that Government pursues its fiscal policy objectives based on the following principles of responsible fiscal management;

a) Sufficiency in revenue mobilisation to finance Government programmesGovernment should raise enough revenue to meet its spending on services and infrastructure developments. The recurrent operational expenses should be met from revenue generated from government operations.

b) Maintenance of prudent and sustainable levels of public DebtPublic debt by definition includes the interest on that debt, sinking fund payments in respect of that debt and the costs, charges and expenses incidental to the management of that debt.

Government should be able to maintain a stable or low Debt to Gross Domestic Product ratio; this ratio compares what government owes to what it produces indicating the country’s ability to pay back its debt.

Ensure that Government borrowing is mainly for capital investments as they generate future benefit or service for citizens rather than operational expenses

c) Ensuring that the fiscal balance when calculated without petroleum revenue is maintained at a sustainable level over the medium termA Fiscal Balance occurs when Government total revenue (minus borrowings) is more than Government total expenditure.

Check that Total Revenue less borrowings less petroleum revenue less total expenditure gives a positive balance over 5 years

d) Management of revenues from petroleum resources and other finite natural resources for the benefit of current and future generationsEnsure appropriate share of petroleum revenue is allocated to finance the Budget (current) as well as allocated to the Petroleum Revenue Investment Reserve (future)

e) Management of fiscal risks in a prudent mannerFiscal risks are factors outside government’s control that cause the fiscal outturn to be different from the fiscal forecasts or projections. These may arise from unforeseen developments/event such as real GDP growth, changes in inflation, commodity prices, exchange rates, interest rates and donor inflows or contingent liabilities from government obligations of contractual, political or moral nature whose timing and amount is outside government’s control. Such events may lead to a deviation from objectives of the CRF and the Minister shall seek approval from Parliament as per Section 7 of the PFMA, 2015

f) Consistency of the Medium Term Expenditure Framework to the National Development Plan Check for demonstrated consistency between the Budget, MTEF and NDP in terms of policy and strategic objectives

g) Efficiency, effectiveness and value for money in expenditureGovernment expenditure must translate inputs into quality outputs in a timely and cost effective manner

Development of the Fiscal StrategyFiscal policy is how the actions of government for spending and taxation impact on the economy and aggregate demand. As part of fiscal responsibility, Parliament ensures that Government makes credible and prudent decisions about its spending and taxation in a transparent manner. The PFMA 2015(as amended) therefore requires the Minister responsible for finance to submit to Parliament a Charter for Fiscal Responsibility not later than three months after the first sitting of Parliament after a general election. Government is also expected to provide regular macroeconomic and fiscal updates to Parliament.

Budgeting Preparation, Approval and Management

Parliament is the supreme law-making authority that scrutinizes and controls government activity

AppropriationIt provides legal authority to government to spend public resources through an Appropriation. It is therefore unlawful to spend government money unless authorized through appropriation by an Act of Parliament or statutory expenditure.

The PFMA, 2015 requires appropriation of ALL government resources including donor funds (loans & grants) and Petroleum Fund.

The Appropriation limit expires by 30th June.

Sec. 17 of the PFMA, 2015

Budgeting and Reporting CycleThe key stages in the budgeting and reporting cycle include:

Table 4: STEPS IN THE BUDGET ENACTMENT/APPROVAL STAGE (PFMA 2015)

Requirements (PFMA 2015) Timelines

Submission of National Budget Framework Paper (NBFP) Parliament [Section 9 (5)]

By 31st

December

Approval of the National Budget Framework Paper by Parliament [Section 9 (8)]

By 1st

February

Presentation of the Ministerial Policy Statements to Parliament [Section 13 (13)]

By 15th

March

Presentation of the Annual Budget and Tax Bills to Parliament [(Section 13 (3)]

By 1st

April

Approval of Annual Budget [Section 14 (1)] By 31st

May

Budget comes into operation [Section 13 (5)] 1st

July

Budget DocumentationThe PFMA 2015 (as amended) specifies key documents that are to be presented by the Minister to Parliament at the time the Budget is presented. These include the following:

National Budget Framework Paper:

• Prepared in consultation with stakeholders

• Taking into consideration balanced development, gender and equity responsiveness

• Shall be consistent with the Charter of Fiscal responsibility

• Shall be in a format prescribed under schedule 3

• Shall be reviewed and approved by Parliament

Ministerial Policy Statement:

• Achievements of the vote for the previous financial year

• Annual and three months’ work plans and outcomes, objectives, outputs, targets and performance indicators

• Annual procurement and recruitment plans of the vote- ensure accuracy and completeness

• Statement of actions taken by the vote on Parliaments recommendation of Auditor General’s reports

• The cash flow projections of the vote in line with the work plans

• Certificate issued by Minister responsible for Finance in consultation with Equal Opportunities Commission on gender and equity responsiveness

• Vehicle utilization report

• Asset register of the vote

National Annual Budget:

• Section13(6)ofthePFMArequiresthattheAnnualBudget shall be consistent with the NDP, the Charter for Fiscal Responsibility (CFR) and the Budget Framework Paper (BFP).

• Section13(6)ofPFMA,Section13(7)requiresaCertificate of Compliance for the Annual Budget of the previous financial year to accompany the Annual Budget for next financial year issued by the NPA.

Therefore, ensure that the annual budget is accompanied by a certificate of compliance of the annual budget of the previous financial year issued by the National Planning Authority

Check that the annual budget includes:• Financingestimatesforthefinancialyear

including:• FinancingtobetransferedfromthePetroleum

Fund to the Consolidated Fund• Plansfordomesticandexternalfinancing• Plansforgovernmentdebt,guaranteestobe

issued and divestment of government assets• moneyrecoveredasaresultofthe

recommendations of the Auditor General’s report

• aplanfordivestmentofgovernmentassets• Expenditureestimates–preceding,current&

proceeding FY• Multi-yearcommitmentstobemadeintheFY• TaxexpendituresofGovernment• Budgetsofself-accountingdepartments,

commissions and organization set up under the Constitution

• GrantstoLocalGovernmentsandanysubventionsfor the FY

The Minister shall also present with the Annual budget the following:

• AppropriationBill,• TreasuryMemorandum,• Statementattestingtoreliabilityandcompleteness,• ListofappointedordesignatedAOs,• CertificateofGenderandequityresponsivenessand• Budgetsofpubliccorporationsandstateenterprises

PARLIAMENT TO ANALYSE POLICY ISSUESSec 12 of the PFMA 2015 provides for Parliament to analyse policies and programmes that affect the economy and where possible make recommendations on alternative approaches to policy or programme.

BUDGETS FOR PUBLIC CORPORATIONS AND STATE ENTERPRISES Section 13 (11)(f) of the Public Finance Management Act, 2015 requires the Minister responsible for Finance to lay before Parliament the budgets for Public Corporations and State Enterprises at the time of laying the Annual Budget as per section 13(3).

APPROVAL AND SCRUTINY OF THE BUDGET The PFMA 2015 (as amended) advances the budget preparation process so that the national budget is presented to Parliament by 1st April (Sec.13 (3)) and approved by 31st May (Sec. 14(1)). This provides Parliament with sufficient time to scrutinize the budget and have the budget effective by 1st July in line with good budgeting practice.

THE ROLE OF THE BUDGET COMMITTEE Under Sec.9 (7) and Sec. 13 (4) the Speaker commits the National Budget Framework paper and the proposed annual budget to the relevant Budget Committee of Parliament and to each sectoral Committee of Parliament for scrutiny of the part of the annual budget that falls within the jurisdiction of that sectoral committee.

Parliament scrutinizes the Executive’s spending proposals by way of debate and sectoral committee scrutiny in accordance with the rules of procedures.

The Constitution under Article 154(4) and Sec 14 (3) of the PFMA 2015 provides for the President to authorize issuance from the Consolidated Fund where the Appropriation Act will not or has not come into operation by the start of the financial year. This is referred to as a vote on account and runs for four months from the beginning of the financial year.

However the PFMA 2015 (as amended), brought forward the process for appropriation and approval of the budget prior to the beginning of the financial year, so the vote on account is no longer used though it remains a Constitutional provision.

COMMITMENT AND EXPIRY OF APPROPRIATIONCommitment Control: The Act, under Sec.15, provides for expenditure control mechanism by requiring any cash release for settling a commitment of Government to be made based on a programmed Annual Cash flow plan issued by the Secretary to the Treasury. This plan is based on the procurement, work and recruitment plans approved by Parliament. This was intended to avoid accumulation of domestic arrears.

Expiry of appropriation: Under Sec. 17 of the PFMA, 2015, any appropriation by Parliament shall expire by 30th June and cease to have any effect at the close of the financial year for which it is made. Therefore, any funds not spent at year end are required to be repaid to the Consolidated Fund by close of the financial year.

Any appropriation by a Local Council shall also be returned to the Council to be authorised as a supplementary appropriation for the next year’s budget. The Accounting Officer of a local Government is required to explain to the Minister responsible for finance in writing, when they fail to utilize at least 60% of the unconditional or equalization grant by 31st July of the following financial years (Sec 17(4)).

Budget execution: Under Sec. 21, of the PFMA, 2015, an Accounting Officer is required to implement activities of the budget in accordance with the approved policy statement and within the cash projections as issued by the Secretary to the Treasury. For effective monitoring of budget implementation, an Accounting Officer shall submit a budget execution report to the Secretary to the Treasury every three months of the financial year.

Multi-year expenditure commitments: Under Sec. 23 of the PFMA, 2015, any contract, transaction or agreement that binds Government to a future financial obligation of more than one financial year must be authorized by Parliament and a report made by the Minister on the performance of that commitment.

REPORTING ON FISCAL PERFORMANCE As part of monitoring implementation of the Annual budget in line with the Charter for fiscal responsibility, the Minister is required to make reports on key fiscal performance parameters under Sec. 18 of PFMA, 2015.

Ensure that fiscal performance reports made to Parliament by end of February and October include:

• Thecurrentandprojectedstateofthe economy

• TheperformanceofGovernmentagainstthe fiscal objectives of the CRF

• Thefinancialandnon-financialperformance of the annual budget

• TheContingenciesFund

• Virementsmade

• Performanceofthepetroleumfund

• Donationsmadetoavote

In addition, Sec 19 requires the Minister to publish pre and post election economic and fiscal updates detailing all the election related spending accompanied by a statement signed by the Secretary to the Treasury policy decisions made by government and other circumstances with implications on the contents of the economic and fiscal updates.

Reallocation and VirementsParliament may authorise by resolution, any reallocation of funds from one vote to another in circumstances only where the functions of a vote are transferred to that other vote (Sec.20).

The Act allows the Minister to reallocate funds from one budget item or Activity to another within the appropriated budget of a vote but caps this at 10% variation (Sec 22).

Classified ExpenditureIn accordance with Sec 24 of the PFMA 215, Classified Expenditure budget shall be scrutinised in a closed session by three member committees of Parliament which include: chairperson of the committee responsible for budget, the chairperson of the committee responsible for defence and internal affairs and another member appointed by the Speaker.

Supplementary ExpenditureThe PFM Amendment Act 2015 under Sec.25 limits additional resources over and above what is approved by Parliament. The Minister responsible for finance may, upon request by an Accounting Officer, approve a supplementary expenditure of up to 3% of the total approved budget for that financial year. The Minister must lay before Parliament the supplementary estimates within four months after the money is spent. Any supplementary expenditure above 3% should be authorised by Parliament.

A supplementary expenditure is an expenditure which cannot be funded through virements, it cannot be postponed to the next financial year and it was not foreseen by the vote at the time of budget preparation or should have been included in the budget of the vote.

Contingencies Fund

Government may, in public interest, need to respond quickly when there is a natural disaster and no resources are available from the annual budget or other sources to finance responses to the natural disaster. Part IV of the PFMA 2015 gives effect to Article 157 of the Constitution by establishing a Contingencies Fund. An amount equivalent to 0.5% of appropriated annual budget of the previous financial year shall be used to provide financing respond to natural disasters.

A natural disaster is an event that causes severe human suffering or material, economic or environmental damage and which results in or is likely to result in the loss of essential services required to meet basic human needs.

CASH AND ASSET MANAGEMENTRevenue Collection and retention: The PFMA 2015 under Section 29 provides Parliamentary oversight over all public resources by requiring authorization through an Act of Parliament for a vote, state enterprise or public corporation to collect or receive revenue. All government entities including those that internally generate revenue are required to submit their budget estimates to Parliament for appropriation. Any retention of any revenues shall be appropriated by Parliament in accordance with Sec.29 (3) of the PFMA, 2015.

Consolidated Fund: In order to ensure safe custody and control over the cash resources of Government, all revenue collected or money raised or received for the purpose of Government shall form part of the Consolidated Fund or public fund established for that special purpose by an Act of Parliament.

Bank Account Management: The PFMA 2015, under Section 33, centralizes management of bank accounts within Treasury. The Secretary to the Treasury is required to prescribe the framework for banking and cash management. A written authorization of the Accountant General is required for opening of any bank account to receive or spend public money at both Local and Central government.

Asset Management: Accounting Officers are responsible for asset and inventory management of the vote. The Act provides Parliamentary oversight by requiring permission of Parliament for any pledge or encumbering of the land or any other asset of a vote.

Any abandonment of claims and write off of public money and stores requires the Minister, under Sec 35, to seek approval of Parliament by resolution specifying the amount authorized to be written off or abandoned. However, the Minister is given a limit of up to ten million shillings and any sums written off or abandoned included in a Supplementary Appropriation Bill.

Public Debt Management

Subject to the Constitution under Article 159, the authority to raise money by loan and issue guarantee for and on behalf of the Government is solely vested in the Minister and no other person, public corporation, state enterprise or local government council take any action resulting into a liability being incurred by Government. Sec 36 of the PFMA, 2015

Article 195 provides that Local Government borrowing is subject to approval by Government

The Minister is required to seek Parliamentary approval for• Loans(Sec36):

• Tofinanceabudgetdeficitorshortfall• Toobtainforeigncurrency• Foron-lendingtoanapprovedinstitutions

• Anyrepayment,conversionandconsolidation of loans.(Sec.37)

• Guaranteetherepaymentoftheprincipalmoney, interest and other charges on the loan (Sec.39)

The Minister is required to prepare and submit a detailed report on public debt management to Parliament by 1st April (Sec.42)

The Minster may also raise loans for the management of monetary policy and treasury operations (PFM Amendment Act S.4) and for defraying an expenditure which may lawfully be defrayed or treasury operations (Sec.36 (2)(b)(e))

Government is tasked to maintain prudent levels of debt in a sustainable manner. This is a potential area of fiscal risk that must be controlled and managed by Government. Parliament plays a critical role in oversight over public debt management.

The PFM Amendment Act, 2015, under 36 (5a) of the Principal Act, caps the borrowing for treasury operations to 10% of the domestic revenue of Government for the financial year. It requires automatic repayment of the loan from Uganda Revenue Authority collections account held at Bank of Uganda , within the financial year.

Treasury operations are the day to day management of the cash needs of Government , by undertaking annual, quarterly and daily cash forecasts for ensuring through investments and temporary borrowing, that Government has sufficient liquidity to meet its obligations on time in line with the Parliamentary appropriations.

Monetary Policy is the actions of a Central bank to influence the demand and supply of money to create economic growth through interest rates and other monetary tools

Treasury operations are the day to day management of the cash needs of Government , by undertaking annual, quarterly and daily cash forecasts for ensuring through investments and temporary borrowing, that Government has sufficient liquidity to meet its obligations on time in line with the Parliamentary appropriations.

Monetary Policy is the actions of a Central bank to influence the demand and supply of money to create economic growth through interest rates and other monetary tools

Management of projects funded by Loans and Grants: The Act under Sec.43 provides for comprehensiveness in budget information to capture projects funded by loans and grants. All expenditure to be incurred by Government on externally financed projects in a financial year is required to be appropriated by Parliament.

The Minister is authorized under Sec.44 to receive monetary grants made to Government or a vote by a foreign government, international organisation or any other person and the funds received shall be paid into the Consolidated fund. The Minster is required to table before Parliament a report of the grants received every financial year.

Accounting and Audit

Government is accountable to Parliament for the use of public resources and the exercise of powers conferred by Parliament. As part of its accountability requirements, Parliament seeks independent assurance that Accounting Officers are operating, and accounting for their performance, in accordance with Parliament’s intentions. In pursuit of the above policy objective, Government is required to produce half year and annual consolidated financial statements.

These financial statements provide information on the Government’s assets and liabilities, revenue and expenses and cash flows. The Auditor-General is responsible for expressing an independent opinion on the annual financial statements of the Government thereby giving assurance to government’s activity.

The PFM Act under Part VII provides the key function and responsibility for Accounting Officers (Sec.45) and Accountant General (Sec 46) in the public financial management.

Sec 45(5) provides that an Accounting Officer shall be responsible and personally accountable to Parliament.

Section 47 of the Act establishes the position of the Internal Auditor General and strengthens its independence with direct reporting to the Secretary to Treasury.

The Act establishes an Audit Committee for each sector of Government and for a number of votes in Local Government under Sec.49. The audit committees assist Accounting Officers to oversee the effectiveness and efficiency of internal controls within a vote.

The Act requires full reporting on performance of entire Government. Entities are required to prepare both half year and annual financial statements. Consolidated Accounts of government include Central Government, Local Governments, public corporations, Contingencies Fund and Petroleum Fund. (Sec.52)

Figure 3: FINANCIAL REPORTING TIMELINES

The Act introduced in-year reporting as a statutory requirement under Section 50, which was previously administrative. Accounting Officers are therefore required to submit half year accounts to the Accountant General by 15th February. The Accountant General consolidates the accounts from votes and makes a submission to Secretary to Treasury by 15th March. (Sec. 50(3))

Accounting Officers of a vote including Local Government are required to submit Annual Accounts within two months after the end of the financial year to the Auditor General to conduct an audit and to the Accountant General for consolidation. Accounting Officers of a public corporation are required to submit a summary statement of financial performance of Public Corporations to the Accountant General and Secretary to the Treasury within 2 months after year end. (Sec 51)

The annual financial statements includes a statement on actions taken by the vote on the recommendations of Parliament on the report of the Auditor General

Treasury memorandum: Accounting officers of Central and Local Government votes are required to submit, together with their Ministerial statements and financial statements, updates on actions taken on Parliamentary recommendations on the report of the Auditor General. (Sec 53) This process completes the accountability cycle of Government.

Petroleum Revenue Management

The PFMA 2015 establishes the Petroleum Fund under Section 56 to:

a) Receive all petroleum revenue accruing to Government

b) Finance the National Budget (UCF)

c) Finance investment for the benefit of current and future generations

Uganda Revenue Authority shall be responsible for collection and receipt of all Petroleum revenue due to Government as provided under Sec.57. The Act encourages timely payment of revenues due to Government. Any default of payment attracts a penalty of 7% of the amount in default for each day of default.

Withdrawals from the Petroleum Fund shall only be by Appropriation and Warrant issued by Auditor General as provided under Sec 58.

The Accountant General is required to prepare accounts for the Petroleum Fund and submit semi-annual financial statements by 15th February and annual financial statements by 31st August to the Minister, Secretary to the Treasury and the Auditor General. (Sec.60)

The Minister is responsible for the Petroleum Fund and an Investment Advisory Committee is established to tender technical advice to the Minister. The Minister shall report to Parliament:

a) Petroleum Revenue estimates by 30th September to facilitate the next budget cycle (Sec 61(1)(a))

b) Semi-annual and annual reports by 1st April and 31st December (Sec 61 (1)(b) & Sec 71(3))

c) Qualifying Instruments issued for investment of Petroleum Revenue (Sec 63(3))

SHARING OF REVENUE FROM ROYALTIESSec 75 of the PFMA 2015 provides for sharing of petroleum revenues as follows:

• Central Government shall retain 94% of revenue from royalties out of which one (1) percentage point is be shared by gazetted cultural institutions (where oil is located).

• 6 % to be shared amongst Local Governments within petroleum exploration and production areas.

• 50% of all loyalties due to Local Governments to be allocated to only oil producing districts

• The other 50% to be shared amongst all Local Governments based on population size, geographical area, and terrain.

• Royalties will be appropriated to beneficiary districts as unconditional grants as part of the annual budget.

Royalty allocations shall be part of revenue of the district and shall be utilised for the development of the local government in question.

Bank of Uganda shall be responsible for managing the Petroleum Revenue Investment Reserve as provided under Sec 64 in accordance with the principles of portfolio management and petroleum investment policy issued by the Minister responsible for finance in consultation with the Secretary to the Treasury and on advice of the Investment Advisory Committee.

Bank of Uganda is required to prepare accounts of the Petroleum Revenue Investment Reserve and submit semi-annual financial statements by 15th February and annual financial statements by 31st August to the Minister copying the Auditor General, Secretary to the Treasury, Accountant General. (Sec.69)

The Auditor General is required to provide independent assurance to the management of the Petroleum Fund and Petroleum Revenue Investment Reserve in accordance with the National Audit Act, 2008. The Audit General is required to submit audit reports to Parliament by 30th June for the semi-annual accounts and 31st December for the annual accounts.

Miscellaneous

Under Sec 76, Every Bill introduced in Parliament shall be accompanied by a Certificate of financial implications issued by the Minister indicating the impact of the Bill on the economy.

Report on exemption of Tax: Under Sec 77, any person or an authority granted power to exempt the payment or to vary any tax under an Act of parliament shall every financial year make a report to Parliament

Liability on failure to meet requirementsUnder Sec 78, Parliament may request the Minister responsible for the insititution to make a report where the insititution has not met the requirements of this Act.

OffencesSec 79 provides for punitive measures against a person who commits an offence and shall be liable on conviction too a fine not exceeding five hundred currency points or a term of imprisonement not exceeding four years or both. This law therefore bites when enforced by those responsible including Parliament.

RegulationsIt is importnat that the law is read together with the PFM Regulations 2016 as provided for under Sec. 81. The regulations have been issued by the Minister effective 29th April 2016.

References1. The Constitution of the Republic of Uganda

1995 as amended.

2. The Public Finance Management Act, 2015

3. The Public Finance Management Amended Act, 2015