Embed Size (px)

Citation preview

Understanding the Drivers of Value and Valuation in Today’s Agency Environment

Bruce Biegel Senior Managing Director

Mirren Live New York: 2015 New Business Conference May 5, 2015

New York, NY

About Winterberry Group

• Corporate Growth Strategy

• Marketing System Engineering

• M&A Strategy and Due Diligence

• Market Intelligence

• Investment Banking, through

Factors Driving and Inhibiting Agency Value

A Look at Agency Valuations Today

Considerations for Maximizing Agency Value

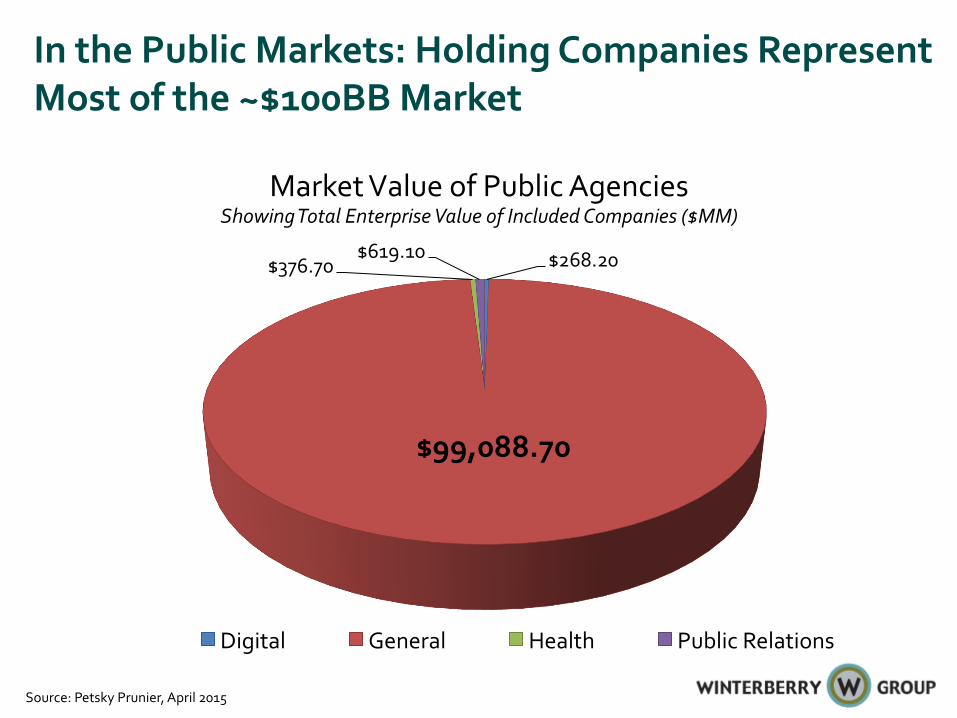

In the Public Markets: Holding Companies Represent Most of the ~$100BB Market

Source: Petsky Prunier, April 2015

$268.20

$99,088.70

$376.70 $619.10

Digital General Health Public Relations

Market Value of Public Agencies Showing Total Enterprise Value of Included Companies ($MM)

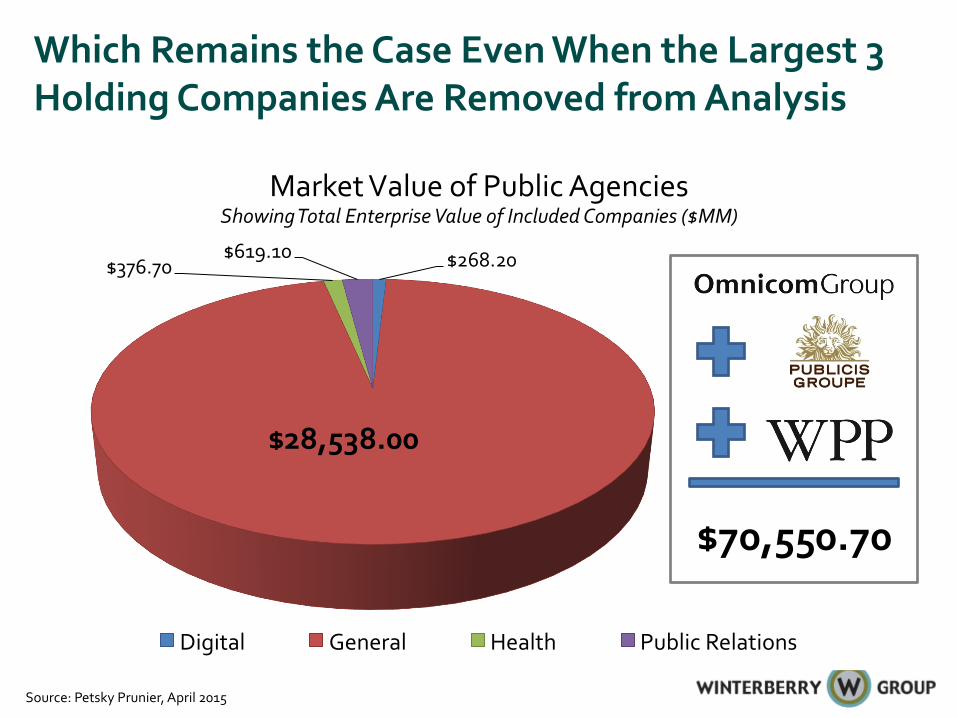

$268.20

$28,538.00

$376.70 $619.10

Digital General Health Public Relations

Which Remains the Case Even When the Largest 3 Holding Companies Are Removed from Analysis

Source: Petsky Prunier, April 2015

Market Value of Public Agencies Showing Total Enterprise Value of Included Companies ($MM)

$70,550.70

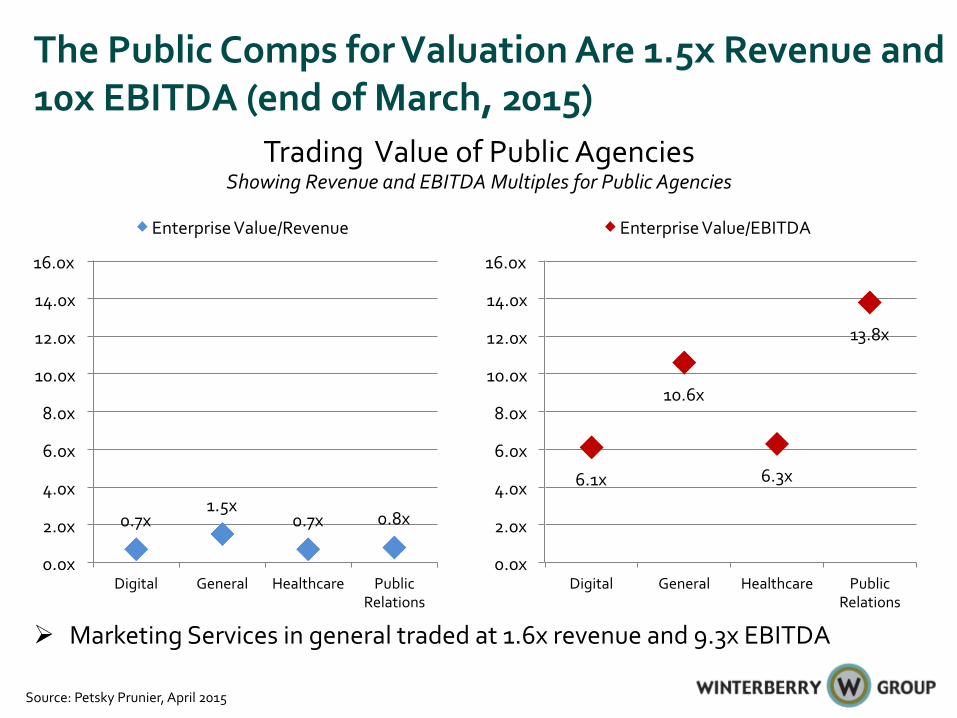

6.1x

10.6x

6.3x

13.8x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

Digital General Healthcare Public Relations

Enterprise Value/EBITDA

The Public Comps for Valuation Are 1.5x Revenue and 10x EBITDA (end of March, 2015)

Source: Petsky Prunier, April 2015

Trading Value of Public Agencies Showing Revenue and EBITDA Multiples for Public Agencies

Ø Marketing Services in general traded at 1.6x revenue and 9.3x EBITDA

0.7x 1.5x

0.7x 0.8x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

Digital General Healthcare Public Relations

Enterprise Value/Revenue

However, in the Private Market, Companies Are Most Often Valued Based on Deal Comps

Source: Cornerstone Funds

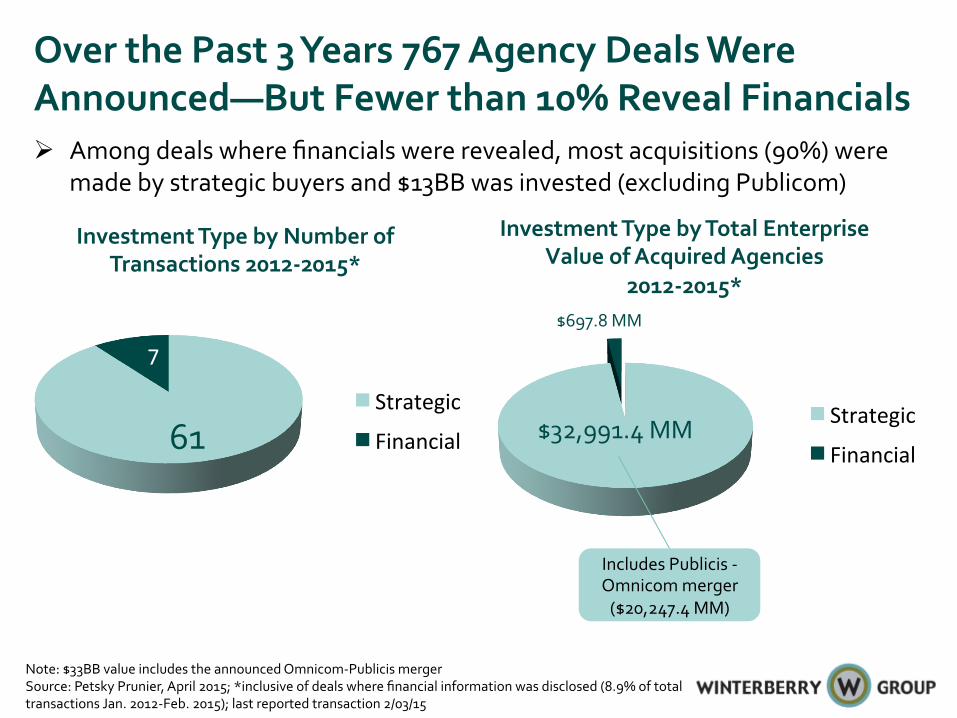

Over the Past 3 Years 767 Agency Deals Were Announced—But Fewer than 10% Reveal Financials

7

Investment Type by Number of Transactions 2012-‐2015*

Strategic

Financial

Investment Type by Total Enterprise Value of Acquired Agencies

2012-‐2015*

Strategic

Financial 61

$697.8 MM

$32,991.4 MM

Includes Publicis -‐ Omnicom merger ($20,247.4 MM)

Note: $33BB value includes the announced Omnicom-‐Publicis merger Source: Petsky Prunier, April 2015; *inclusive of deals where financial information was disclosed (8.9% of total transactions Jan. 2012-‐Feb. 2015); last reported transaction 2/03/15

Ø Among deals where financials were revealed, most acquisitions (90%) were made by strategic buyers and $13BB was invested (excluding Publicom)

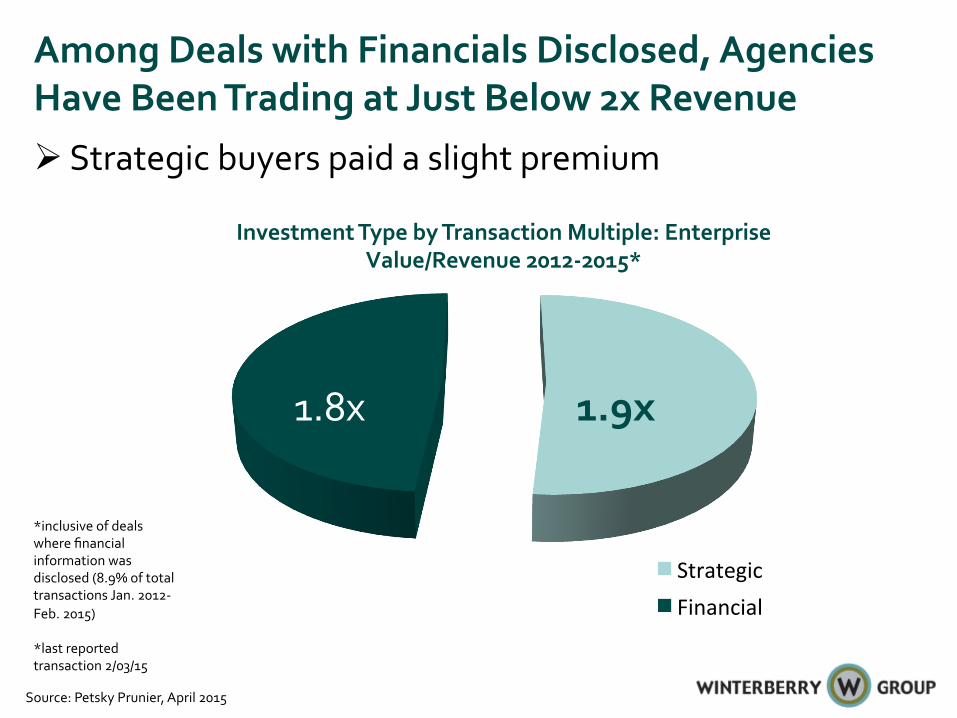

Investment Type by Transaction Multiple: Enterprise Value/Revenue 2012-‐2015*

Strategic Financial

1.8x 1.9x

Source: Petsky Prunier, April 2015

Among Deals with Financials Disclosed, Agencies Have Been Trading at Just Below 2x Revenue Ø Strategic buyers paid a slight premium

*inclusive of deals where financial information was disclosed (8.9% of total transactions Jan. 2012-‐Feb. 2015) *last reported transaction 2/03/15

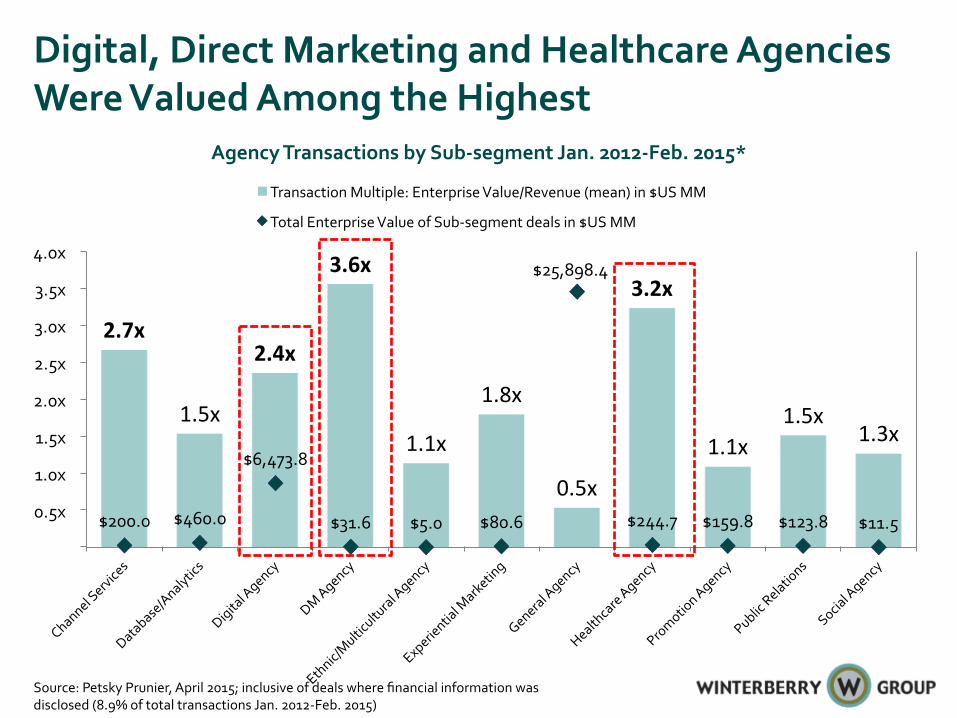

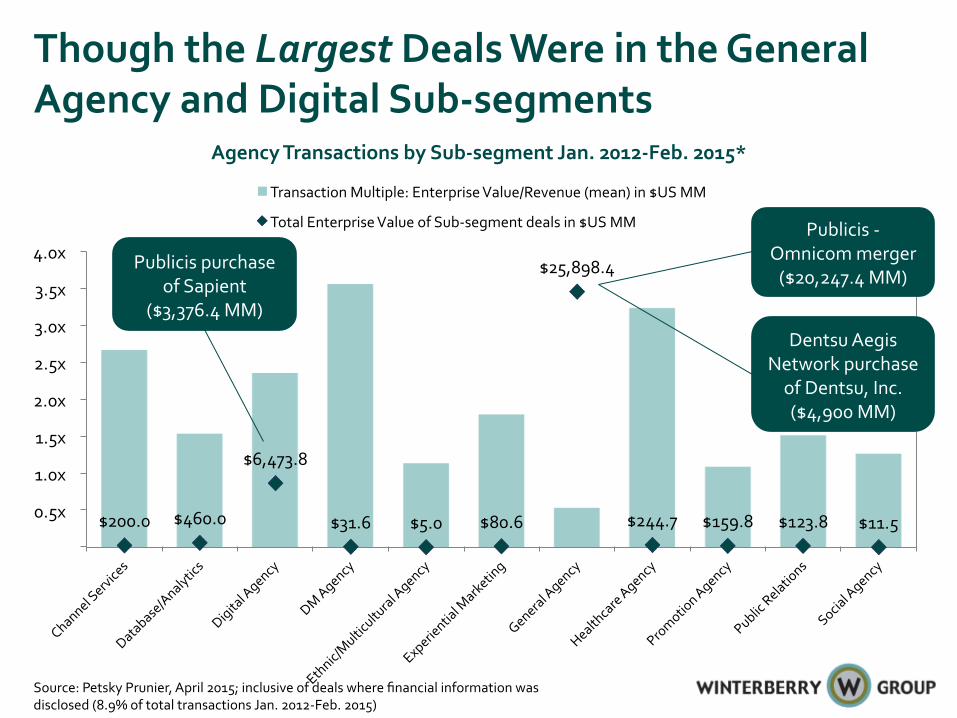

Digital, Direct Marketing and Healthcare Agencies Were Valued Among the Highest

Source: Petsky Prunier, April 2015; inclusive of deals where financial information was disclosed (8.9% of total transactions Jan. 2012-‐Feb. 2015)

2.7x

1.5x

2.4x

3.6x

1.1x

1.8x

0.5x

3.2x

1.1x 1.5x

1.3x

$200.0 $460.0

$6,473.8

$31.6 $5.0 $80.6

$25,898.4

$244.7 $159.8 $123.8 $11.5 0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

Agency Transactions by Sub-‐segment Jan. 2012-‐Feb. 2015*

Transaction Multiple: Enterprise Value/Revenue (mean) in $US MM

Total Enterprise Value of Sub-‐segment deals in $US MM

$200.0 $460.0

$6,473.8

$31.6 $5.0 $80.6

$25,898.4

$244.7 $159.8 $123.8 $11.5 0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

Agency Transactions by Sub-‐segment Jan. 2012-‐Feb. 2015*

Transaction Multiple: Enterprise Value/Revenue (mean) in $US MM

Total Enterprise Value of Sub-‐segment deals in $US MM

Though the Largest Deals Were in the General Agency and Digital Sub-‐segments

Publicis -‐ Omnicom merger ($20,247.4 MM)

Dentsu Aegis Network purchase of Dentsu, Inc. ($4,900 MM)

Publicis purchase of Sapient

($3,376.4 MM)

Source: Petsky Prunier, April 2015; inclusive of deals where financial information was disclosed (8.9% of total transactions Jan. 2012-‐Feb. 2015)

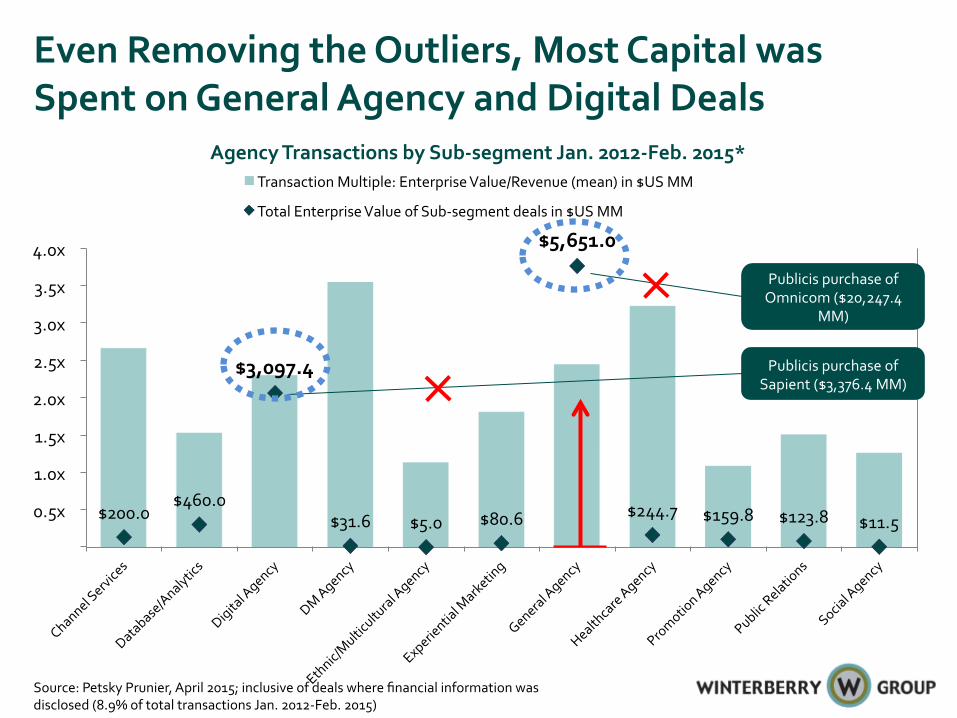

$200.0 $460.0

$3,097.4

$31.6 $5.0 $80.6

$5,651.0

$244.7 $159.8 $123.8 $11.5 0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

Agency Transactions by Sub-‐segment Jan. 2012-‐Feb. 2015* Transaction Multiple: Enterprise Value/Revenue (mean) in $US MM

Total Enterprise Value of Sub-‐segment deals in $US MM

Even Removing the Outliers, Most Capital was Spent on General Agency and Digital Deals

Publicis purchase of Omnicom ($20,247.4

MM)

Publicis purchase of Sapient ($3,376.4 MM)

Source: Petsky Prunier, April 2015; inclusive of deals where financial information was disclosed (8.9% of total transactions Jan. 2012-‐Feb. 2015)

The Good News: No Near Term Pause in Agency Consolidation Expected; Even Large Deals

—John Wren, President-‐CEO,

Omnicom

"I think it'll be a very long =me before I try to do a merger of

equals again… [though] we've just formed a new dedicated

acquisi;on group… so I expect over =me we will be doing more, but no

big bang type things. Sensible acquisi;ons, mid-‐size that fit what we see as our strategic growth

areas.”

Factors Driving and Inhibiting Agency Value

A Look at Agency Valuations Today

Considerations for Maximizing Agency Value

A Series of Trends Are Creating Opportunities—as Well as Challenges—for Agency Growth

• Growth of overall marketing spend • Complex and dynamic marketing

technology landscape • Demand from marketing leadership to

execute “big data” strategies

• Demand for marketers to become omnichannel

• Desire to leverage cross-‐channel insights and campaign measurement/attribution

• Ad-‐tech companies disintermediating agencies with DIY/SaaS offerings

• Consulting firms emerging as digital agency competitors

• Trend towards project-‐based work rather than AOR relationships—threatens recurring revenue and challenges planning efforts (talent/resources)

• Tarnished reputations resulting from lack of fee transparency and scrutiny around rebates/kickbacks

Strong Macroeconomic Gains in the U.S. Have Been Mirrored By Continued Agency Growth

• The U.S. unemployment rate continues to drop, (down to 5.5% in February) and is now at its lowest level since the 2009 recession

• Ad agency employment levels are at highest point since 2001 and digital media firms added over 50,000 jobs in the past three years

• The S&P 500 has grown 13.5% in the past year, and 54.5% over three years

• In April several publicly traded agency stock prices hit all-‐time highs (including for Dentsu, Publicis and WPP (Interpublic traded at its highest price in February since 2002))

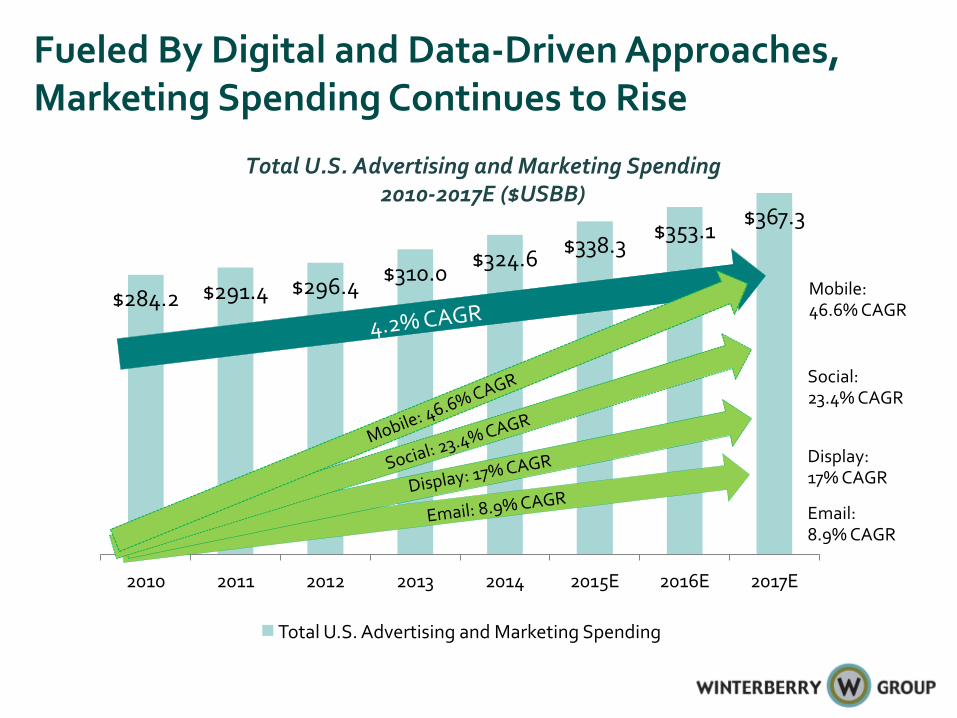

$284.2 $291.4 $296.4 $310.0 $324.6 $338.3

$353.1 $367.3

2010 2011 2012 2013 2014 2015E 2016E 2017E

Total U.S. Advertising and Marketing Spending 2010-‐2017E ($USBB)

Total U.S. Advertising and Marketing Spending

Fueled By Digital and Data-‐Driven Approaches, Marketing Spending Continues to Rise

Email: 8.9% CAGR

Display: 17% CAGR

Social: 23.4% CAGR

Mobile: 46.6% CAGR

4.2% CAGR

Social: 23.4

% CAGR

Display: 17% CAGR

Email: 8.9% CAGR

Source: GDMA/Winterberry Group, “The Global Review,” October 2014

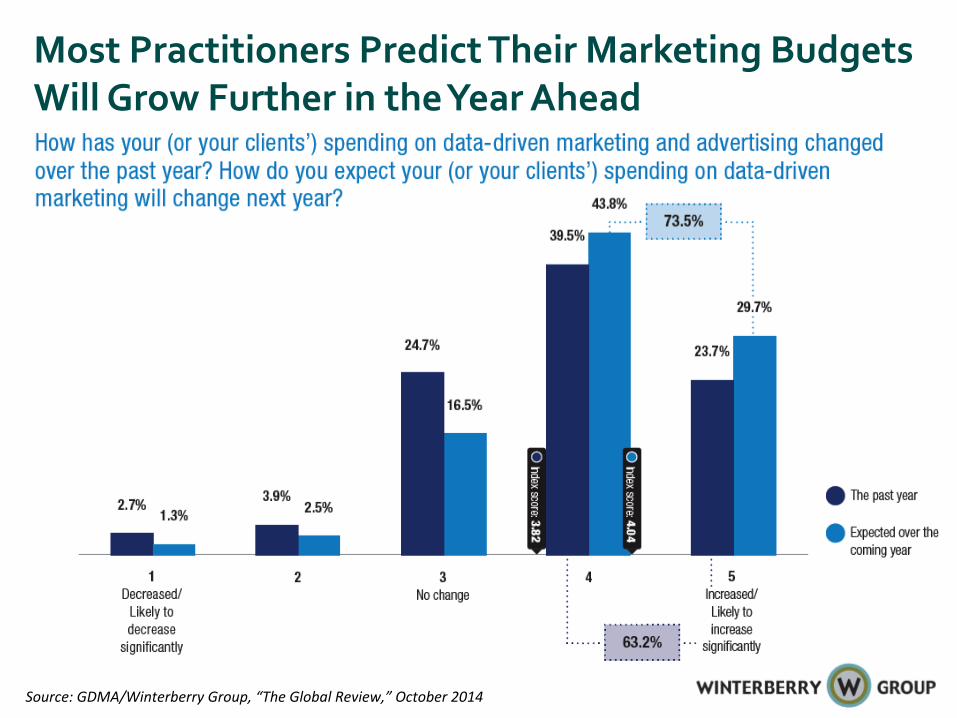

Most Practitioners Predict Their Marketing Budgets Will Grow Further in the Year Ahead

1.3% 1.7%

15.8%

23.3%

57.1%

1 2 3 4 5

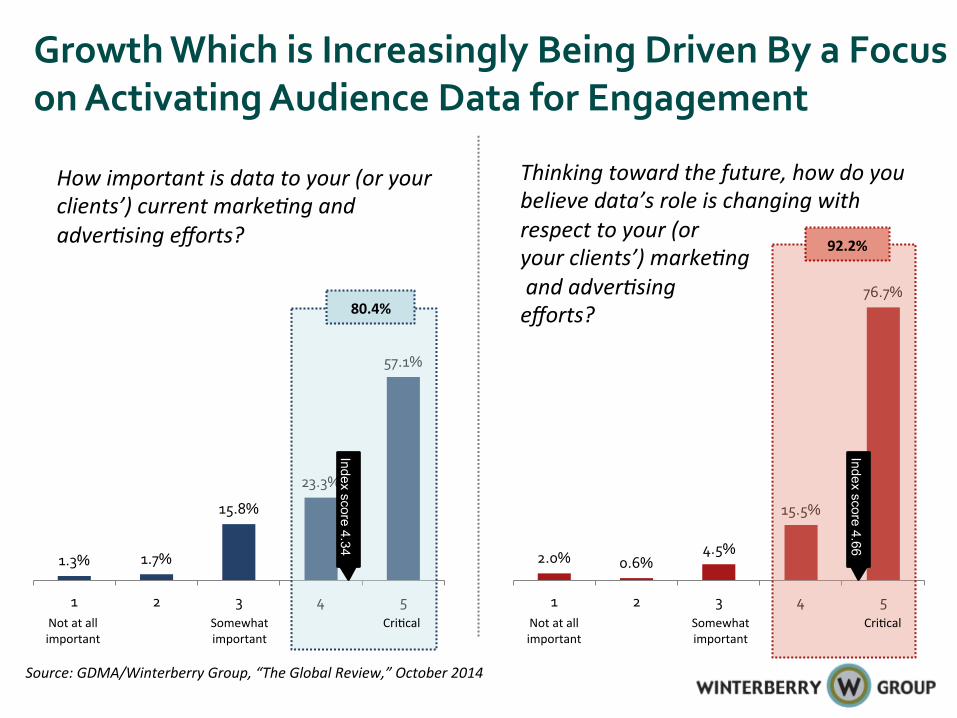

80.4%

Not at all important

Cri=cal Somewhat important

Source: GDMA/Winterberry Group, “The Global Review,” October 2014

How important is data to your (or your clients’) current markeLng and adverLsing efforts?

Thinking toward the future, how do you believe data’s role is changing with respect to your (or your clients’) markeLng and adverLsing efforts?

Index score 4.34 2.0% 0.6% 4.5%

15.5%

76.7%

1 2 3 4 5

92.2%

Not at all important

Cri=cal Somewhat important

Index score 4.66

Growth Which is Increasingly Being Driven By a Focus on Activating Audience Data for Engagement

With a Corresponding Adoption and Expansion of Marketing Tech / Data Tech

And All Marketers Need Help Leveraging These Tools

Source: Winterberry Group, “Marketing Data Technology” white paper, January 2015

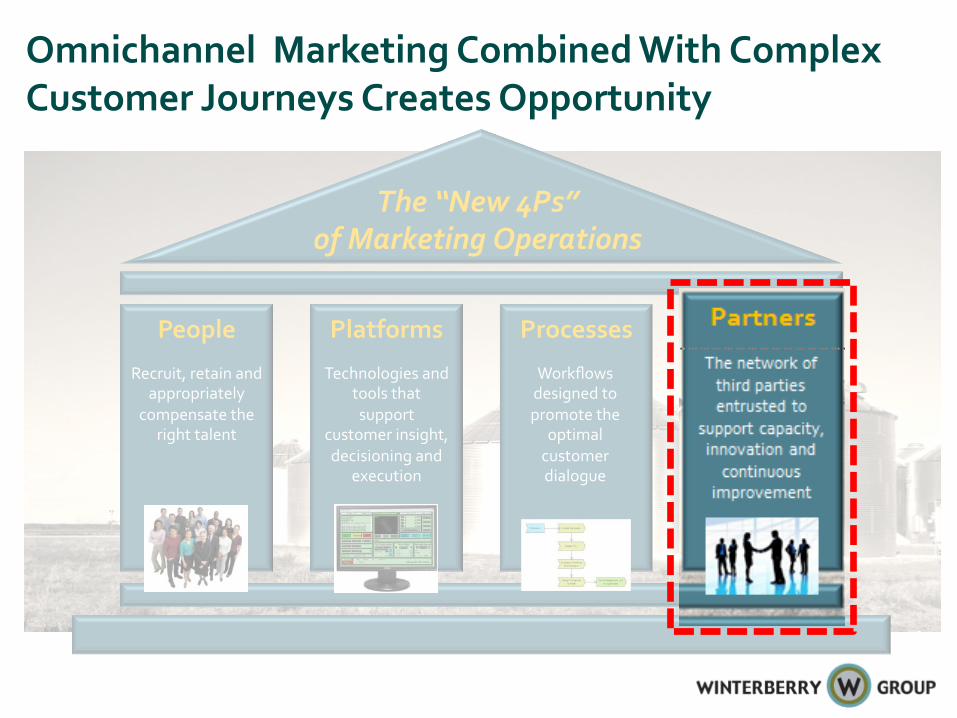

Omnichannel Marketing Combined With Complex Customer Journeys Creates Opportunity

Holistic Marketing Process

Management

Effe

ctiv

e Pe

ople

M

anag

emen

t

The “New 4Ps” of Marketing Operations

People

Recruit, retain and appropriately

compensate the right talent

Partners

The network of third parties entrusted to

support capacity, innovation and continuous

improvement

Platforms

Technologies and tools that support

customer insight, decisioning and

execution

Processes

Workflows designed to promote the

optimal customer dialogue

Yet, Alongside Opportunities Are Several Threats, Starting With Technology Disintermediation

Ø Marketing technology increasingly offered as SaaS with improved UI on web-‐based portals (easing self-‐service for clients)

Ø Prevalence of turn-‐key data management and activation solutions

Ø Marketers may prefer to eventually “in source” campaign management tasks, as internal resources know unique business needs best

Plus New Competition from Integrators and Enablers from Technology and Digital Consultancies

"There's no ques=on that we're compe;ng against companies that we never competed

against before: DeloiOe Consul=ng, Accenture, IBM… It's a very difficult

compe==ve market out there, and we just have to be on our game.”

—Michael Roth, Chairman-‐CEO,

Interpublic Group

And a Shift to Project-‐Based Work, Challenging the More Predictive (Stable) AOR Approach

Ø Clients are cherry-‐picking agencies based on campaign-‐specific requirements, particularly as digital needs become more acute

Ø For agencies, project-‐based work threatens recurring revenue—making forward-‐looking projections (and valuation) more murky

Ø Short term agency projects creates greater potential for client conflict issues

Will This Shift Last? Strategy and Messaging Across the Journey Benefit From Consistency

"I think we're going to get back to some kind of [long-‐term] partnership with big brands… In order to be able to think long term, you

need relationships.”

—Susan Credle, Chief Creative Officer,

Leo Burnett

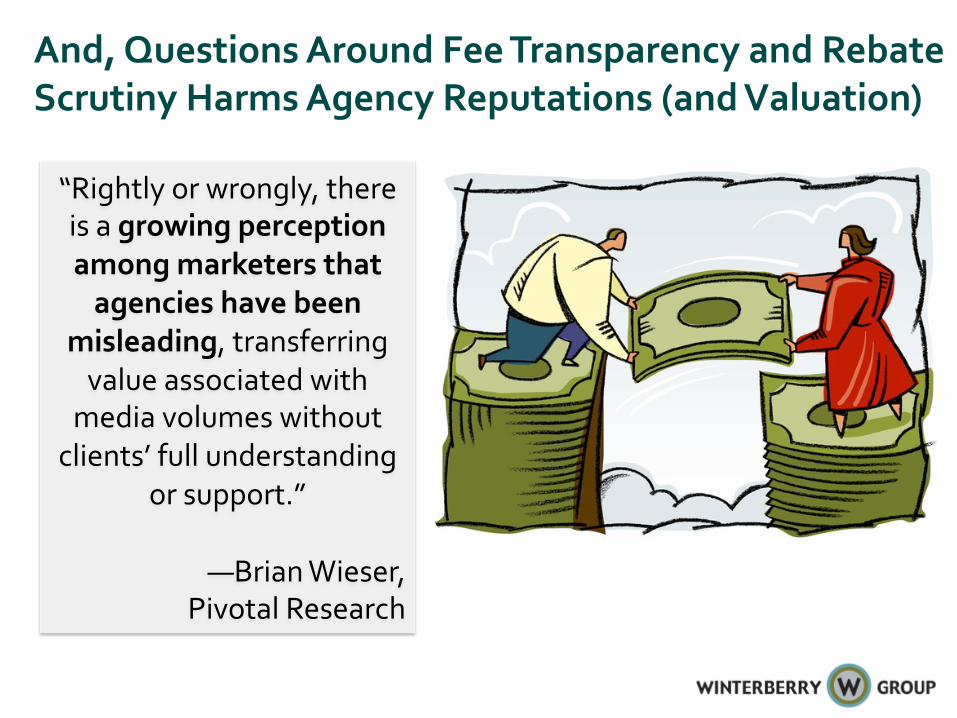

And, Questions Around Fee Transparency and Rebate Scrutiny Harms Agency Reputations (and Valuation)

“Rightly or wrongly, there is a growing perception among marketers that agencies have been

misleading, transferring value associated with media volumes without clients’ full understanding

or support.” —Brian Wieser,

Pivotal Research

Factors Driving and Inhibiting Agency Value

A Look at Agency Valuations Today

Considerations for Maximizing Agency Value

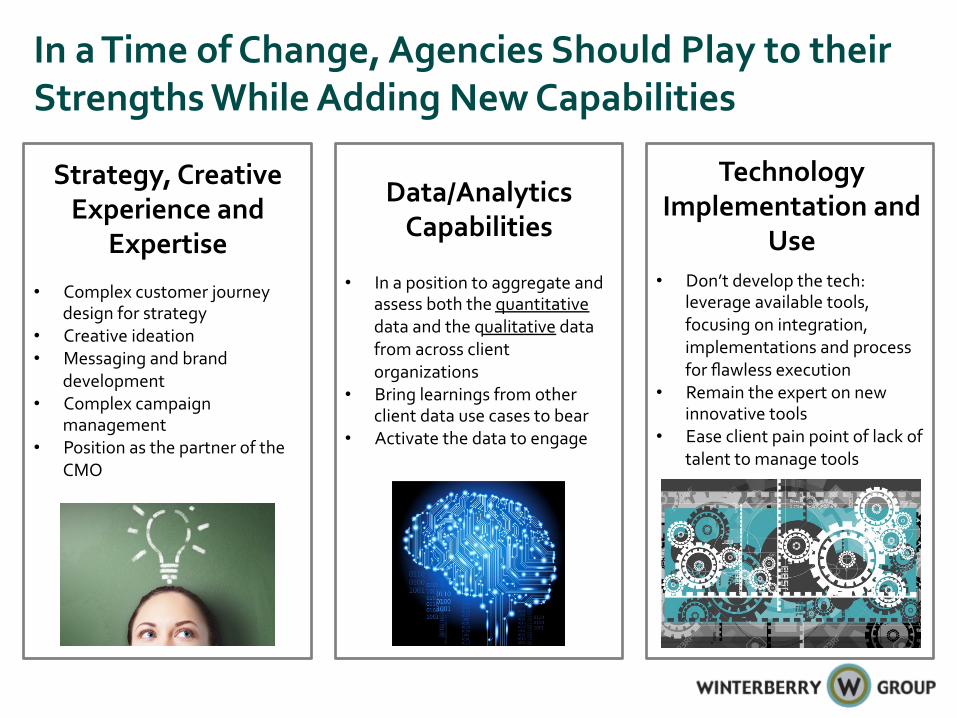

In a Time of Change, Agencies Should Play to their Strengths While Adding New Capabilities

Data/Analytics Capabilities

Technology Implementation and

Use

Strategy, Creative Experience and

Expertise

• Complex customer journey design for strategy

• Creative ideation • Messaging and brand

development • Complex campaign

management • Position as the partner of the

CMO

• In a position to aggregate and assess both the quantitative data and the qualitative data from across client organizations

• Bring learnings from other client data use cases to bear

• Activate the data to engage

• Don’t develop the tech: leverage available tools, focusing on integration, implementations and process for flawless execution

• Remain the expert on new innovative tools

• Ease client pain point of lack of talent to manage tools

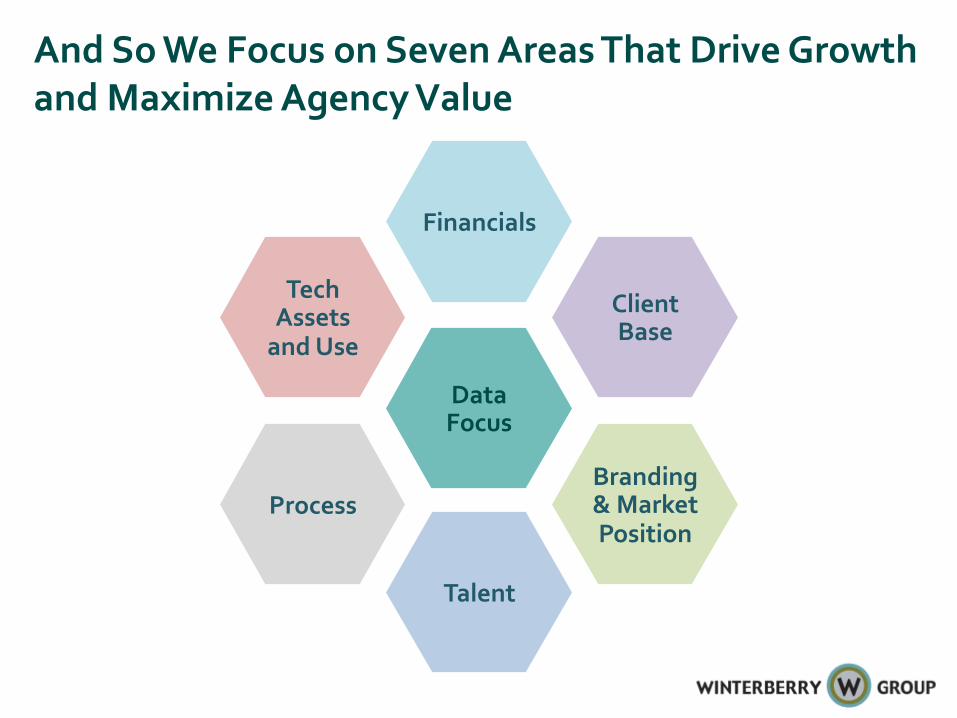

And So We Focus on Seven Areas That Drive Growth and Maximize Agency Value

Data Focus

Financials

Client Base

Branding & Market Position

Talent

Process

Tech Assets and Use

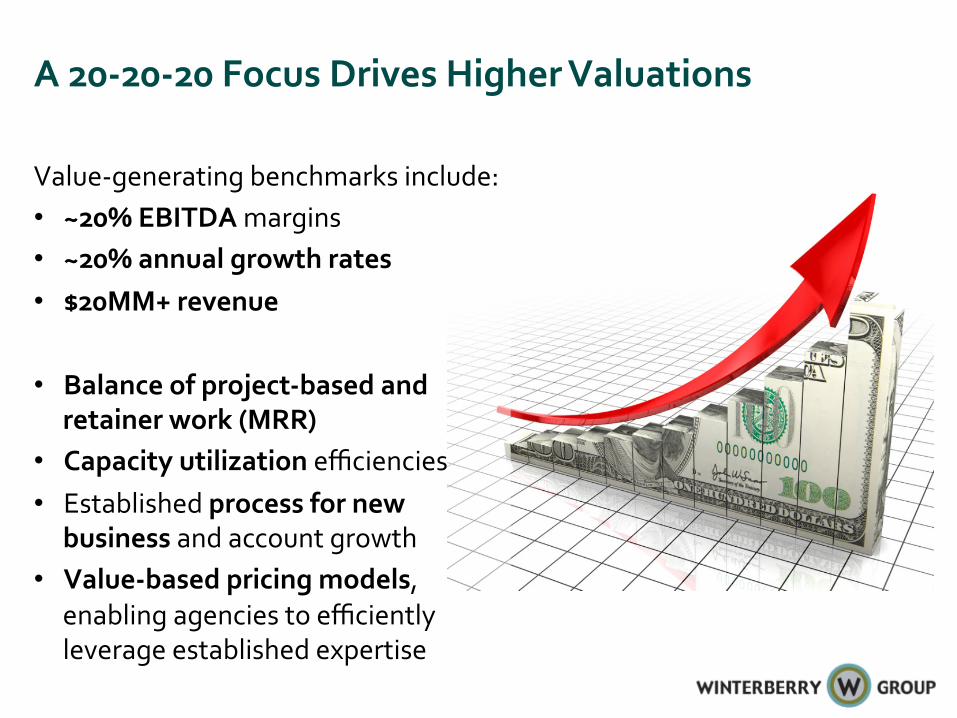

A 20-‐20-‐20 Focus Drives Higher Valuations

Value-‐generating benchmarks include: • ~20% EBITDA margins • ~20% annual growth rates • $20MM+ revenue

• Balance of project-‐based and retainer work (MRR)

• Capacity utilization efficiencies • Established process for new

business and account growth • Value-‐based pricing models,

enabling agencies to efficiently leverage established expertise

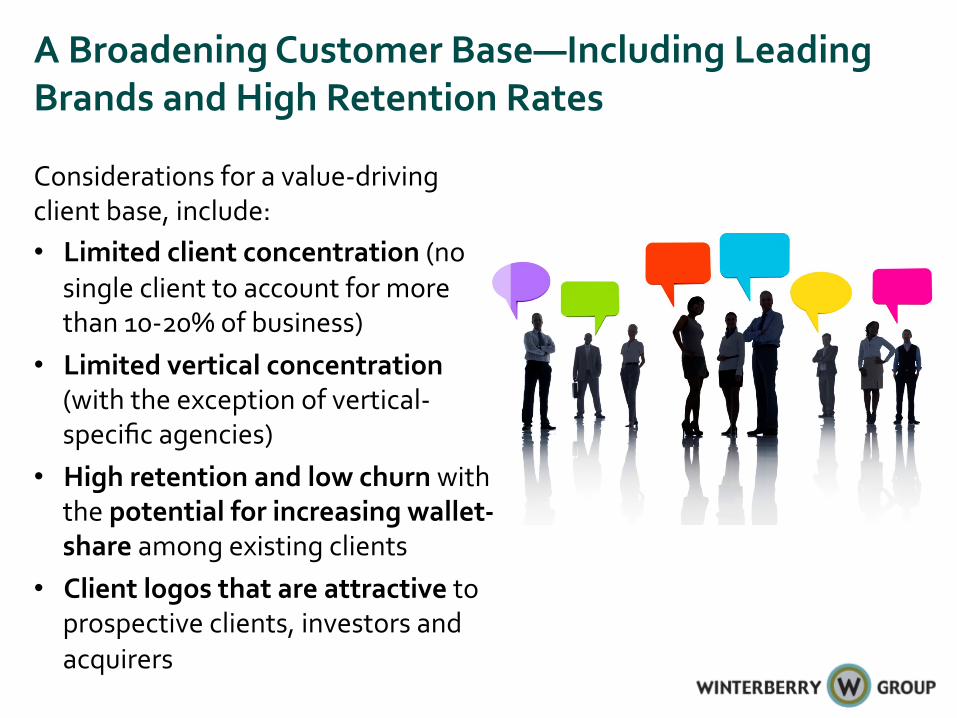

A Broadening Customer Base—Including Leading Brands and High Retention Rates

Considerations for a value-‐driving client base, include: • Limited client concentration (no

single client to account for more than 10-‐20% of business)

• Limited vertical concentration (with the exception of vertical-‐specific agencies)

• High retention and low churn with the potential for increasing wallet-‐share among existing clients

• Client logos that are attractive to prospective clients, investors and acquirers

Strategists

Creatives

Data Scientists

Account Managers

Design Agency

Loyalty Specialty

Media Focus

CEA – Digital Focus

The Right Balance of Talent Resources and Expertise Across Core Agency Disciplines

Balance of Talent Integrated

Focus Areas

Organizations structured for success include: • A balance of strategists and

Creatives • Account management with clear

purpose • Data science and analytics teams

to interpret, model and optimize results at the program and campaign level

• Operations and advanced project management

• Digital and technology expertise

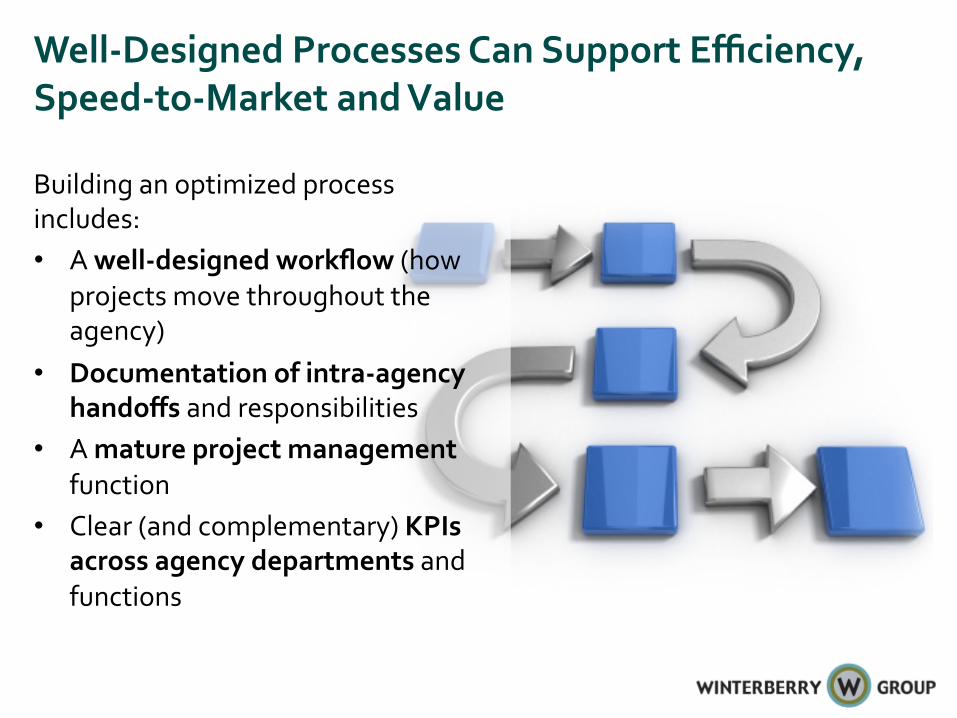

Well-‐Designed Processes Can Support Efficiency, Speed-‐to-‐Market and Value

Building an optimized process includes: • A well-‐designed workflow (how

projects move throughout the agency)

• Documentation of intra-‐agency handoffs and responsibilities

• A mature project management function

• Clear (and complementary) KPIs across agency departments and functions

Leadership Requires a Rigorous Focus on Audience Data as the Primary Insight-‐Generator

Marketing best-‐practice has evolved from leveraging primarily market research data, to using primarily audience data to inform efforts. Agencies well positioned to drive value will use both: • Declared data (e.g., registration data

including age and gender) as well as • Inferred data (e.g., online behavioral,

purchase history, inferred interests) And will enhance audience data-‐driven insights with market research and other information, to build targeted campaigns and audience engagement strategies.

A Platform Strategy and Use of Preferred Vendors Supports Agency Tech Leadership

Agency technology leadership relies on: • An established technology strategy

• Including buy vs. build and perspective on stacks

• A continuous process for tech evaluation and sourcing

• Integration resources to leverage a range of vendors for client use cases

• A set of preferred and secondary platform providers

• Expertise to leverage available tools to integrate, activate and measure audience behaviors across the customer journey

Agencies That Focus on Thought Leadership and Innovation Will Be Well Regarded

To encourage innova=ve thinking, Grey presents a

“Heroic Failure Award,”

emphasizing the value in crea=vity, tes=ng and learning

Considerations for fostering thought leadership: • Produce or publish research for

industry benefit • Productize IP • Speaking engagements • Prioritize education and training • Create a culture of innovation—

encouraging testing, learning (and failing)

Bruce Biegel Senior Managing Director [email protected] @WinterberryGrp

www.winterberrygroup.com

Questions?