Embed Size (px)

Citation preview

1

UNIT -1

(A)Banker and customer relationship

(B) Customers and Account holders

Meaning of Banker :

An institution which trades in money, establishment for the deposit, custody and

issue of money as also for making loans and discount and facilitating the

transmission of remittance from one place to another

As per sec 3 of the Indian Negotiable Instruments Act 1881, the work

“ banker includes any person acting as banker and any post office saving bank”

Sec 5 ( c) of Banking Regulation Act defines “ banking company” as a company

that transacts the business of banking in India. Since a banker or a banking

company undertakes banking related activities we can derive the meaning of

banker or a banking company from Sec 5(b)as a body corporate that :

Accept deposits from public

Lends or

Invests the money so collected by way of deposits

Allows withdrawals of deposits on demand or by any other means.

Meaning of customer:

A customer is one who has an account with a banker or for whom a banker

habitually undertakes to act as such “

In order to constitute a customer, a person should satisfy the following

conditions :

person should have a bank account in his own name

The dealing between banker and the customer should be related to banking

business

A human being, firm, joint stock company, society or any separate legal

entity may be a customer of a banker

VVN

DEGR

EE C

OLLE

GE

2

Features of bank

Bank should deals with money : Bank is a financial institution and which deals

with money which belongs to public and its own . Here bank utilizes public

deposit in maximum extent to gain profit

Acceptance of deposit : Acceptance of deposit is another main features of the

bank, it should accept the deposit from the public through various schemes

Lending loan: Lending loan is another feature of the bank. It has to properly

allocate the available resources i,e. Money, in order to gain profit and ensure

returns to its customers, bank must lend loans to needy people for the return

called interest

Name identity : Bank should add the word “ Bank” to its name to enable it as

bank

Banking business: Banking business should be the main activity of the bank, it

should accept money and lends to needy people along with that it should

perform certain agency functions to its customer. These are the main banking

business activities

Bridge between savers and borrowers :Bank creates bridge between savers and

borrowers. It pools money from the public and lends it to needy group. Hence

bank connects link between savers and borrowers

Profit motives through services : Banking is a profit motive institution which

earns profit through various financial services.

Functions of Bank:

Primary functions : Are the basic or fundamental functions executing by a

commercial bank which give birth to all other additional or modern functions.

These are primarily dealt with accepting the public deposits, advancing loans

and cash credits.

Accepting deposits : Commercial bank accepts various types of deposits from

public especially from its clients. These deposits are payable after a certain time

period.

Public deposits are classified into two-

Time / Term deposits : These are repayable after a certain fixed period .

The deposits cannot be withdrawn by the customer by cheque, draft or by

other means. The Time deposits are- Fixed deposits, Recurring deposits ,

Cash certificates

VVN

DEGR

EE C

OLLE

GE

3

Demand deposits : These are the deposits which can be withdrawn by the

customer at any time by means of cheques, draft or any other specified

mode. Demand deposits are- Savings bank deposits , current account

deposits

Advancing of loans : The commercial banks provide loans and advances of

various forms. These are sanctioned to the approached customers on certain

conditions and provisions. The loans offered by commercial banks are:

Overdraft : This is one of cash credit facility offered to current account

holders. It is an arrangement with the bankers thereby the customer is

allowed to draw money over and above the balance in his/ her account. It

is a short term temporary fund facility with interest charge over the

amount overdrawn.

Cash credit: Cash credit is a form of working capital credit given to the

business firms. Under this arrangement, the customer opens an account

and the sanctioned amount is credited with that account . It is made

against security of goods, personal security etc. The advantage of this

mode is that bank charges interest only on the amount utilized and not on

total amount sanctioned or credited to the account.

Discounting bills: It is one of the primary operation of a bank where the

bank purchases inland and foreign bills before these are due for payment

by the drawer debtors, at discounted values i.e, values a little lower than

the face values

Loans and advances: It includes both demand and term loan, direct loans

and advances given to all types of customer mainly to businessmen and

investors against personal security or goods of movable or immovable in

nature. The loan amount is paid in cash or by credit to customer account

which the customer can draw at any time. The interest is charged against

full amount whether the customer utilizes the amount sanctioned or not.

Credit creation : Credit creation is also one of primary function. It appears when

a bank sanctions a loan to a customer, it does not give cash to him, but, a

deposit account is opened in his name and the amount is credited to his account.

He can withdraw the money whenever he needs. Thus, whenever the bank

sanctions a loan it creates a deposit. In this way the bank increases the money

supply of the economy. Such functions are known as “ Credit creation “.

Secondary functions: Along with the primary functions, each commercial bank

has to perform several secondary functions too. It includes many agency

functions or general utility functions. They are :

VVN

DEGR

EE C

OLLE

GE

4

Agency functions . These are the functions served by a commercial bank on

behalf of its customers for a consideration. The various agency services are:

To collect and clear cheque, dividends and interest warrant

To make payment of rent, insurance premium etc

To deal in foreign exchange transactions

To purchase and sell securities

To act as trust , attorney, executor

To accept tax proceeds and tax returns.

General/ public utility functions : These are the functions met by the

commercial bank which are generally utilized by bank customers or general

public for some amount of fee. These are

To provide safety locker facility to customers

To provide money transfer facility

To issue traveler’s cheque

To accept various bills for payment ( phone bill, water bill)

To provide various cards such as credit, debit cards

Relationship between a Banker and Customer:

The general relationship between banker and customer includes :

Debtor and creditor relationship : The real relationship between banker and

customer is that of a debtor and creditor. When a person deposits some money

to open an account, the banker assumes the positions of a debtor and customer

becomes a creditor. But on other hand, when a customer avails the facility of

overdraft and loan , the relationship of debtor creditor is reversed , banker takes

the position of a creditor and customer becomes a debtor

Special features of debtor and creditor relationship :

Demand for payment is necessary : In case of a deposit in a bank, banker

the debtor is not needed to repay the amount of his own. Customer the

creditor must make a demand for the repayment of deposit in proper

manner. But in commercial debts, debtors is liable to pay the amount due

on a specified date or earlier and demand for payment is not needed. In

other words, the customer must demand from the banker to pay his

money. Demand for payment is essential in case of debt due from a

banker.

Demand must be made only at proper place: Demand to repay the amount

made by customer must be at proper place at the branch of the bank

where the customer has the account. The credit balance of customers

VVN

DEGR

EE C

OLLE

GE

5

account is payable only at a branch where the account is kept. Customer

has only option to make a demand on specified branch of a bank. In an

ordinary commercial debt, debtor can pay the money to creditor at any

place.

Demand must be made only at proper time: The demand to repay the

amount must be made by customer only within banking hours. Bankers

undertake to pay amount in banking hours. Section 65 of the Negotiable

Instruments Act , 1881 specified that presentation for repayment must be

made within banking hours on a working day at bank. A banker is not

liable to pay a cheque if not presented in banking hours on a working day

of bank.

Demand should be made in proper manner: The demand to repay the

amount must be made in proper manner by the customer by a way of

cheque or an order, drafts or otherwise. The oral instructions or a

telephonic demand is not sufficient to withdraw money from a bank.

Trustee and Beneficiary : When the banker accepts securities and other

valuables for safe custody, he acts as a trustee for his customer. Banker as a

trustee retains money or other assets and performs for the benefit of his

customer called beneficiary. Customer continues to be the owner of his assets

deposited with banker. As a trustee, it is the duty of banker to take care of the

lockers and their contents.

Principal and Agents : Banker also acts as an agent of his customer. It performs

a number of agency functions like buying and selling of securities on behalf of

customers, collection of cheques and makes payment of various dues on behalf

of his customer. There are large number of agency functions performed by

banker in the recent time. Hence , a banker performs as agent of his customer

who becomes principal while rendering an agency function.

Mortgagee and Mortgager: When the customer effects a mortgage deed of his

immovable property in favour of bank or deposits the title deed of his property

with banker as security for a loan, the mortgage and mortgager relationship is

established between customer and banker. Banker become mortgagee and

customer becomes mortgager.

Bailee and Bailor relationship : When customer takes safe locker facility of gold

jewellery or any other ornament with bank bailee and bailor relationship lies

between banker and customer. Here banker becomes bailee and get the

possession of customer ornament and not the ownership. Here bank should

VVN

DEGR

EE C

OLLE

GE

6

safeguard the customer belongings but should not use it. Bank has right to

charge certain fee for this service.

Banker has no right to close the accounts: A banker as debtor has no right to

close the accounts of his creditor at any time without prior permission from

customer

A banker as a creditor: If a banker disburses loan and overdraft, it assumes the

role of a creditor and the customer assumes the role of a debtor.

Special relationship between Banks and Customer :

The special features of banker customer relationship are grouped into obligations

and rights

Obligations of a banker :

Obligation to honour customer’s cheques : The bank has an obligation to honour

customer’s cheque as and when they are presented as long as sufficient funds

are available at credit in customer’s account . According to the bank primary

contract is to repay the money received for his customer’s account usually by

honouring his cheques.

This obligation arises out of two implied situations between the parties:

The banker should repay the borrowed fund whenever the customer demands it

in writing at the branch where he holds the current account

The customer’s credit should not be damaged by the banker by dishonouring the

cheques except on reasonable grounds.

Section 31 of the Negotiable Instruments Act,1881 , states that , “ the drawee of

a cheque having sufficient funds of the drawer in his hands, properly applicable

to the payment of such cheque , must pay the cheque when duly required to do

so, in default of such payment, must compensate the drawer for any loss or

damage caused by such a default.”

Thus , a banker must honour the customer’s cheques drawn on him provided:

Sufficient funds of the customer in his hand: The obligation of a bank to

honour customers’ cheque arises only when it has sufficient fund in

customer’s account at least equal to or more than the amount of cheque.

A bank’s obligation to pay a cheque is subject to the amount available in

the deposit account. If there is no sufficient balance , the bank is justified

in overriding his obligation.

Correctness of the cheque: The obligation to pay a cheque depends upon

the correctness of the cheque. All the required particulars like date, name

VVN

DEGR

EE C

OLLE

GE

7

of the payee , amount in words and figures and the signature of the

drawer ought to have been correctly filled in .

Proper drawing of the cheque: The cheque will be honoured only when it

is drawn according to the requirement of the law. It must be drawn on a

printed form supplied by the bank and it should not contain any ‘ request’

to pay the amount.

Proper application of the fund: The fund must be available for the cheque

drawn. In case a customer has drawn a cheque one account, having

insufficient funds, the banker cannot debit it to his other account where

he has sufficient funds unless the customer asks for it. For instance , a

customer having insufficient funds in his current account cannot presume

that the cheque drawn by him will be honoured by the banker because he

has fixed deposit with the bank.

Proper presentation : The bank will undertake to honour cheques

provided they are presented at the branch where the account is kept and

during the banking hours. If the cheques are presented after six months

from the date of issue, they will be regarded as stale cheques and they

will not be honoured.

Reasonable time for collection : A customer cannot impose on the bank a

condition that the bank should pay his cheques blindly even when they

are drawn against cheques sent for collection before they are collected

Existence of legal bar: A bank is relieved from his statutory duty of

honouring his customer’s cheques if there is any legal bar like Garnishee

order attaching the customer’s account.

Wrongful dishonour of cheque : Wrongful dishonour of cheque means a

dishonour committed by mistake or by negligence on the part of the bank or any

of its employees. If a bank, without any justification , dishonours his customers’

cheque, it makes bank liable to compensate the customer for injury to his credit.

According to section 31 of the Negotiable Instrument Act, 1881, the words “

loss or damage” do not mean only pecuniary loss but also loss of credit or injury

to reputation. The loss can be of two types:

Nominal loss

Special or substantial loss

VVN

DEGR

EE C

OLLE

GE

8

Banker’s obligation to maintain secrecy of accounts: A bank is under

obligation to maintain strict secrecy as regard the state of his customer’s

accounts even after the account are closed. The banker has an implied

obligation to maintain secrecy of the customer’s account. He should not disclose

matters relating to the customer’s financial positions since it may adversely

affect the customer’s credit and business. This obligation continues even after

the account of the customer is closed.

Under the following circumstances a banker may disclose the relevant

information about the customer as a banking practice :

Disclosure of information under compulsion of law: Banker has to obey the law

and it has to disclose the customer’s account information when law compelled

to furnish and it is bank’s obligation to disclose information to the extent of

asked by the law and not more than that .

Disclosure of information under banking practice : The banker can disclose the

account information of the customer in his own interest. Suppose if the

customer fails to repay the debt amount, usually the bank ask the guarantor and

the bank disclose the accounting information of the customer to guarantor with

his own interest.

Disclosure by the instruction of customer : Banker must disclose the customer

accounting information with the prior permission and will of the customer. The

customer may himself direct the banker to disclose the state of his accounts to

his employer or messenger or any person acting as his agent. In such a case the

consent is said to be expressed. Where, the customer furnishes the bankers name

to the third person for reference or where the customer takes loans from the

banker on the basis of a guarantee given, it is implied that the customer has

authorized the banker to furnish the necessary information to such third party on

his request.

Disclosure as common courtesy : Banker can share a piece of accounting

information of customer with the fellow banker as common courtesy. Fellow

banker asks details of customer under few circumstances like issuing letter of

credit, discounting bills etc by these circumstances banker will disclose the

information .

Disclose for the interest of the nation : If the customer is dealing with any

illegal activity it is dangerous for the nation and to safeguard the public and

nation, it is banker duty to disclose the customer information to concerned

authority

VVN

DEGR

EE C

OLLE

GE

9

Consequence of wrongful disclosure :

If the banker wrongfully discloses information and financial data of the

customer, banker is liable to the third parties and also to the customer. If it is

proved that due to false information provided by the bankers, third party

suffered loss, the banker is liable for damages. Thus banker should be very

careful in providing facts about the customers. Even by mistake or by

negligence he should not reveal facts about customers state of account

unnecessarily .

Rights of a Banker:

Bank’s Right to General Lien: Lien is a term used to identify the right to

retain a property belonging to a debtor till such time he discharges the debt due

to the retainer of the property. Lien is simply a right to possess a property. Lien

will be lost when the possession of the property is lost.

Types of Lien:

Particular lien : This lien refers to the particular property which is retained by

the lender or creditor against the specific or particular loan. The particular

property will be retained until the particular debt is cleared by the debtor.

Particular lien is one under which the creditor can retain the goods of debtor

relating to particular amount due only.

General lien : General lien states creditor’s right to retain all the goods and

assets against general amount due that is all amount due by the debtor. Under

general lien creditor can retain all the goods of debtor against total amount .

Banker can enjoy the lien on all the goods pledged by the customer against all

the amount irrespective of agreement. There are some implied situation under

that bank can exercise general lien with the absent of agreement. It confers the

right to retain goods not only in respect of debt incurred in connection with a

particular transaction but also in respect of any general balance arising out of the

general dealing between the two parties.

The banker should satisfy certain conditions to exercise lien:

The assets should be under possession of bank

The assets which is there with the banker as security should belongs to

customer( debtor only)

VVN

DEGR

EE C

OLLE

GE

10

When bank holds possession of property the banker must acts his

capacity as banker only

The deposit of property should not be for specific purpose and there must

be expressed or implied agreement between banker and customer to exercise

lien right

The possession of goods must be lawful

There should be amount due by the customer to the banker to get the right

of lien.

The right of lien does not confer on the creditor, the right of sale but only

the right to retain the goods till the loan is repaid. In case of pledge , the creditor

enjoys the right of sale

The right of lien is conferred upon by Indian Contract Act: No separate

agreement or contract is therefore, necessary any for this purpose. However ,

the banker takes a letter of lien from customer, mentioning that the goods are

entrusted to the banker as security for a loan

The right of lien can be exercised on goods or other securities standing on

the name of the borrower. The right of lien can only be exercised on the goods

owned by borrower only not on the goods jointly owned by people along with

the borrower

Exception to the right of general lien:

The banker cannot exercise the right of lien on following circumstances :

Safe custody deposit : Banker cannot holds the right of lien on safe custody

deposits. Under these circumstances banker acts as a bailee to customer and not

as the capacity of banker, so as per law banker cannot exercise the lien on safe

custody deposits.

Bills or instruments deposited for collection or any other specific purpose:

When customer deposit any bills or instruments for collection purpose or any

other specific purpose like purchase of securities then bank cannot exercise the

right of lien because here it is implied agreement between banker and customer

that the fund must be utilized for specific purpose and banker acts as agent of

customer not in the capacity of banker.

Trust amount or property : Banker should not possess the right of lien on trust

amount which lays certain instructions for the banker to usage of fund regarding

specific manner and as per expressed consent banker must utilize the same for

mentioned purpose and moreover here bank never acts in the capacity of banker

but acts as trustee.

VVN

DEGR

EE C

OLLE

GE

11

Illegal possession of goods : Illegal possession of goods do not entrust banker’s

right of lien, if customer left the securities by mistake or properties come to the

banker without awareness of customer then banker cannot exercise the lien

because the banker must have legal possession of article.

Prior due date of loan : Bank can exercise lien after the completion of loan’s

due date that when bank lends it fixes the time period to return the loan. In this

circumstances banker can exercise the lien on customer goods only after the due

date of loan but not prior to the due date of loan.

Bonds and coupons : Lien is not applicable for bonds and coupons which are

received for collection. Here banker merely acts as an agent of customer but not

in the capacity of banker so as per law, if bank acts as an agent lien is not

applicable .

Stolen goods : If customer pledge any assets which is stolen and has been

granted loan by the bank, in such circumstances banker cannot has the right of

lien on those goods even though transactions have taken place in the ordinary

course of business. Since the customer is not the real owner of the assets and

lien is not exercised on those assets.

No simultaneous right to bank: When right of set off is available to bank then

bank cannot possess the right of lien. Generally at a time bank cannot possess

both the right.

Right of set off:

A banker possess the right of set off which enables him to combine two

accounts in the name of same customer and to adjust the debit balance in one

account with credit balance in the other. Banker’s right to set off is a statutory

right of banker to combine two or more accounts of customer which has debit

and credit balance and it is being done to know the net balance due from

customer or by banker .

The following conditions are essential to exercise right of set off:

The debt must be a sum certain and due immediately

The debt must be due by and to the same parties

The both the parties bank and customer are should be in the same

capacity of debtor and creditor

There should be no specific agreement relating account and fund

The accounts must be in the same name in the same right

VVN

DEGR

EE C

OLLE

GE

12

The right can be exercised in respects of debts due only not in respects of

future debts or contingent debts

Right to exercise before the garnishee order is effective

Under following situation banker can automatically set of customer’s

account :

When customer dies

When customer becomes mental incapacity

When customer declared as insolvent

On the receipt of garnishee order

At the time of winding up of company

Fraud by the customer by pledging asset with another bank which is

already kept with one bank

The right of set off cannot applicable for the following circumstance :

The right of set off is not applicable for trust account that is fund deposited for

specific purpose

The right of set off is not applicable for partnership account and account of one

partner that is it is not possible to combine debit and credit balance of

partnership account and debit or credit balance of one partner account

Right of set off is not applicable for dividend account of company and loan

account of the same company

Joint account and single account cannot be combined and right of set off is not

applicable

Account of guardian and minor account cannot be combined and set off is not

applicable because of different parties

Right of set off is not applicable for the same party’s account but acting as

different capacity

Distinction between Lien and Set off

Sl No Lien Set Off

1 Banker lien is recognized under

section 171 of the contract act

Set off is a right under customery law of

banker

2 Lien is related to goods and

security of customer

Set off is related to money claims

3 Lien is right of banker to retain

customer goods and security

Set of is right of banker to combine more

than one account of customer to ascertain

final balance due to him or due by him

VVN

DEGR

EE C

OLLE

GE

13

4 Notice is not required to

exercise lien

Notice is required in some of the cases of

set off

5 Lien precedes set off Set –off follows lien

Right of appropriation – Rule in Clayton’s case: The need of appropriation

arises in case a customer raises more than one loan account. The payment made

by the customer may not be sufficient to clear all debts due to the customer.

Similarly, when a customer holds more than one current account and regularly

operates these accounts by depositing funds and making withdrawals

simultaneously in all the accounts he holds, it creates a problem for the bank to

appropriate which fund to which account. In such circumstances , he has to

follow the rules of governing the appropriation . The general rule is that the

debtor ( customer) has the first choice and he can appropriate the funds

according to his desire. If the customer does not take any decision regarding

appropriation at the time of payment, then the creditor( bank) has the choice.

The right of appropriation is made should be informed to the customer. The

right of appropriation can be exercised at anytime. If the choice of appropriation

is not made by the customer as well as banker then Clayton’s law will come into

existence. Clayton’s law is applicable when there is no implied and expressed

instructions on discharge of debt by the customer and even no action by the

banker to discharge various debt of customer. Clayton’s law states on

apportionment of debt, as per law the apportionment of debt should be

chronological one that is first side of the debt should be cleared by the first side

of the credit amount.

Right to charge interest : The bank has the implied right to charge interest on

loans and advances , and also to charge commission for services rendered by the

bank. The bank can debit such charges to the customer’s account. It is implied

right of banker to charge interest on outstanding balances due by the customer

when customer is awarded loan from banker, it charges interest on loan amount

and if customer has not paid the previous loan instalment the banker has right to

charge compound interest that is interest on interest .

Right to charge commission : The banker has an implied right to charge

commission for the services provided to the customer . Bank not only functions

as acceptance of deposit and lends it to needy group besides it provides many

banking services to customer and others also. Nowadays banks provide many

VVN

DEGR

EE C

OLLE

GE

14

banking services to customer because of increased competition and to retain and

gain more customers. At the same time when bank provides any services it

possess right to charge commission on the services. The various service

provided by the banks are safe custody facility , purchase and sale of shares ,

debentures , factoring etc and it charges commission on these services.

Right to charge incidental charges : Incidental charge is a levy imposed by

the bank on unremunerative current accounts. Normally, it is not charged on the

current accounts whose balances can be profitably employed by the bank. These

charges need not be paid in cash but will be debited to the customer’s current

account.

Right to charge commitment charges : It is a charge made by the banker on

overdrafts and cash credit accounts. The commitment charge is charged on the

un used part of the sanctioned limit which does not earn any profit to the bank

besides charging interest on the used part of overdraft. Banker incorporates

‘commitment clause’ in overdraft and commitment charges agreements. This

protects the bank from the loss incurred on the un used part of the commitment

charges accounts and overdrafts.

Garnishee order

A garnishee order is an order issued by a court addressed to banker instructing

to stop or withhold payment of money belonging to a specified person who has

an account with the banker and who has committed a default in satisfying the

claim of his creditors .

It is a legal procedure by which creditor can receive the debts owed by the

debtor through the debtor bankers. In the relationship between debtor and

creditor, in case a debtor fails to pay the money due to his creditor, the creditor

may apply to the court to issue a Garnishee order, on the debtor banker. As a

result of this order the debtor account with the bank is frozen and the bank

cannot make any payment out of the account

On receiving the order, the account of customer becomes suspended. Banker is

under an obligation not to make any payment from the account attached to

Garnishee order

VVN

DEGR

EE C

OLLE

GE

15

The creditor who seeks for attachment of Garnishee order is called a

Judgment creditor

The debtor whose money is frozen is called judgment debtor

The banker with whom the debtor has his account is called Garnishee

There are two stages of Garnishee order:

Order – Nisi : It is an order issued by competent court of law addressed to a

banker not to make any payment from the account of garnishee debtor until

further orders are issued

Order- Absolute : In this order , court specifies how much amount from the

account is to be kept separate

Cases where Garnishee order is not Applicable:

The garnishee order served on the banks does not apply when:

Debt is not actually due to customer

Account is in the joint names of customer and other persons whereas

order is in the name of the customer only

Banker is entitled to set-off the balance against debt due to it from the

judgement debtor ( customer )

Money in account is held by customer as a trustee or is impressed with

trust

Name of customer as appearing on garnishee order is wrong or inaccurate

Account is overdrawn.

Garnishee order is applicable :

Where there is a credit balance

Attaches the amount drawn by a cheque but payment not yet effected

All bank branches of a bank are treated as one entity

Attaches future maturing term deposits also

Attaches joint account if issued so

Attaches personal account of partners if an order is served on a partnership

account

Types of Bank Account

Savings bank account: The saving accounts are one of the most popular

deposits for individual accounts. Savings account meant for savings purposes.

VVN

DEGR

EE C

OLLE

GE

16

Any individual either single or jointly can open a savings account. Most of the

salaried persons, pensioners and students use savings account. The advantage

of having savings account is banks pay interest for the savings. The saving

account holder is allowed to withdraw money from the account as and when

required

Features of savings bank account :

Savings bank account are meant for promoting saving habit among people

These accounts can be opened by individuals singly, two or more individuals

jointly, certain organisations as permitted by RBI. Minors’ accounts can be

opened by their guardians

Business organisations engaged in profit generating activities are generally not

permitted to open SB accounts

Minor above the age of 10 are also allowed to open

Self –operated SB accounts under certain conditions as per SBI directions. This

is basically to inculcate savings habit in them

Government departments, municipal authorities, political parties,

trade/professional / business entities or associations are not allowed to open

these accounts

Cheque book facility is offered in these accounts. Due to electronic banking

ATM/Debit card also offered. Internet banking facility is also offered to

customers subject to conditions stipulated by banks in this regard. Upon request,

credit card facility is also offered

Cheques can be used for withdrawals or for making any payments. Since the

advent of electronic banking there are several online payment options available

for transfer of money which can be made use of

The number of withdrawals in these accounts is restricted as per RBI directions/

banks discretion as these accounts are not meant for business or trading.

However there is no restriction on the number of deposit transactions

Current account : Current account are basically meant for businessmen and are

never used for the purpose of investment or savings. These deposits are the most

liquid deposits and there are no limit for number of transactions or the amount

of transactions in a day. Most of the current account are opened in the names of

firm/company accounts. Cheque book facility is provided and the account

holder can deposit all types of the cheques and drafts in their name of endorsed

VVN

DEGR

EE C

OLLE

GE

17

in their favour by third parties. No interest is paid by banks on these accounts.

Bank charges certain service charges, on such accounts

Features of current account :

The main objective of current account holders in opening these account is to

enable them ( mostly businessmen) to conduct their business transactions

smoothly.

There are no restrictions on the number of times deposit in cash/ cheque can be

made or the amount of such deposits

Usually banks do not pay any interest on such current account

The current accounts do not have any fixed maturity as these are on continuous

basis accounts

Cheque book facility is provided and the account holder can deposit all types of

the cheques and drafts in their names or endorsed in their favour by third parties

These accounts are meant for customers who have large number of transactions

of credit and debit everyday basis

Current accounts can be opened by individuals , proprietary concerns,

partnership concerns, public and private limited companies, trusts, associations ,

societies and other institutions

Customers are expected to maintain the minimum balances in their accounts as

per the rules of business of the bank concerned

There are no restrictions on the number of withdrawals or deposit transactions

that can be routed through a current account

Withdrawals from these account normally are to be done through cheque leaves

issued to the customer

ATM cards / Debit cards, internet banking facility are also provided to the

account holders

If any overdraft arrangements are made this will be as per rules stipulated by the

bank including period, interest rate, quantum and validity of such facility

Nomination facility is available only in the account of proprietary concerns

among current accounts

Fixed accounts: The account which is opened for a particular fixed period (

time) by depositing particular amount is known as Fixed ( Term) deposit

account. The term ‘ fixed deposit ‘ means that the deposits is fixed and is

repayable only after a specific period is over. Under fixed deposit account

money is deposited for a fixed period say six months , one year , five year or

VVN

DEGR

EE C

OLLE

GE

18

even ten years. The money deposited in this account can not be withdrawn

before the expiry of period.

Features of fixed deposit account:

The main purpose of fixed deposit account is to enable the individuals to earn a

higher rate of interest on their surplus funds

The amount can be deposited only once. For further such deposits, separate

accounts need to be opened

Fixed deposit account may be opened for a minimum period of 7 days and

maximum period of 10 years. Accordingly , bank offer interest rate for different

periods. These rates can change periodically in tune with RBI’s Monetary

policy

The minimum amount required to open o fixed deposit is Rs 1000

As per RBI directive interest is paid on fixed deposits on a quarterly basis or

half yearly basis. However monthly interest can be paid at a discounted rate as

per RBI directives

Deposit holders can avail loan against pledge of fixed deposits receipts, banks

offer up to 90% of the principal as loan amount at 1 or 2 % higher interest rate

than the rate of interest offered on the deposit.

Tax deducted at source ( TDS) is applicable on the interest paid by banks as per

prevailing Income Tax rules . Exemption from TDS is also granted to General

public/ senior citizens against submission of Form 15G or 15H.

Recurring deposit account : Recurring deposit is a special kind of Term

deposit offered by banks in India popularly known as RD accounts which help

people with regular incomes to deposit a fixed amount every month into their

recurring deposit account and earn interest at the rate applicable to fixed deposit

Features of Recurring deposit accounts :

Recurring deposit accounts are normally allowed for maturities ranging from 6

months to 12 months

These accounts can be opened in single or joint names. Nomination facility is

also available

Rate of interest offered is similar to that in Fixed deposits

Interest is compounded on quarterly basis in recurring deposits

VVN

DEGR

EE C

OLLE

GE

19

Non – Resident External ( NRE) Account : The Indian government has

created specific banking guidelines for non-residents Indians living around the

world. As per the Income Tax Act, person is considered a Non Resident Indian

( NRI) if they are an Indian citizen but are physically in India for 182 days or

less a year

The Reserve Bank of India (RBI) has created two primary instruments that fall

under the term NRI accounts –

Non –Resident External ( NRE)

Non-Resident Ordinary ( NRO)

Both options were created to provide Indians who primarily reside outside of

the country with ways to send and house money back to India. This can include

money to support their families, manage properties , make investment , deposit

earned income in India or a combination of these activities

NRI accounts differ from Indian resident bank accounts as they are able to

accept foreign currency deposits. For both NRO and NRE accounts, we can

open a current , savings or fixed deposit account , with specific interest rates

determined by the banks

A Non – Resident External ( N RE) account is a specific account with banks,

cooperative banks, and authorised dealers by the RBI that can be opened and

maintained by NRIs using foreign funds. The accounts can be held as a savings

account, current , recurring or fixed deposits. The account is held in India and is

maintained in rupees.

With an NRE account, people can easily deposit foreign earnings into this

account. The amount that is deposited from the foreign currency is converted

into Indian Rupees as per the prevailing exchange rate.

With a savings or current the account holder can utilize the account to pay bills

or issue cheque for payments in India. Account holder can appoint an Indian

resident as a Power Of Attorney ( POA). With an NRE deposit , we can park

foreign earnings in a fixed term deposit of 1-3 years that is held in Indian

Rupees.

In all cases , the account holder earn Indian Interest rates on the converted rupee

amounts that they send over, and both the principal and interest are tax-free in

India. The rates of interest on the accounts will be as per the guidelines issued

by the Department of Banking Regulations

Overall , NRE account provide a tax-free space for remittances, ample liquidity,

an easy way to pay for expenses in Indian , and a medium to invest in India as

well.

VVN

DEGR

EE C

OLLE

GE

20

Non Resident Ordinary ( NRO) Account :

A NRO account can be in the form of a savings account, current, recurring or

fixed deposits. The account accepts foreign currency as well as Indian Rupees

to open an account, with the balance being held in Indian rupees. It can be held

jointly by two NRI’s or can be held jointly with an Indian resident

The account can also be used for local payments, so for example to pay water,

electricity or phone bill. The NRO account can take remittances from outside

India, certain cash amounts and transfers from other NRO accounts

The NRO account is subject to all applicable taxes in India. Due to the taxable

event that would occur under repatriation, an NRO account is considered a

convenient way for NRIs to deposit both their earned income in India while also

accepting foreign deposits

Due to its restricted repatriation and tax implications, the NRO account is best

suited if we are not intending to send balances out of India. It can be seen as a

vehicle to deposit our income in India such as rent or dividends. It is also more

conducive if we want to open an account jointly with a person resident in India.

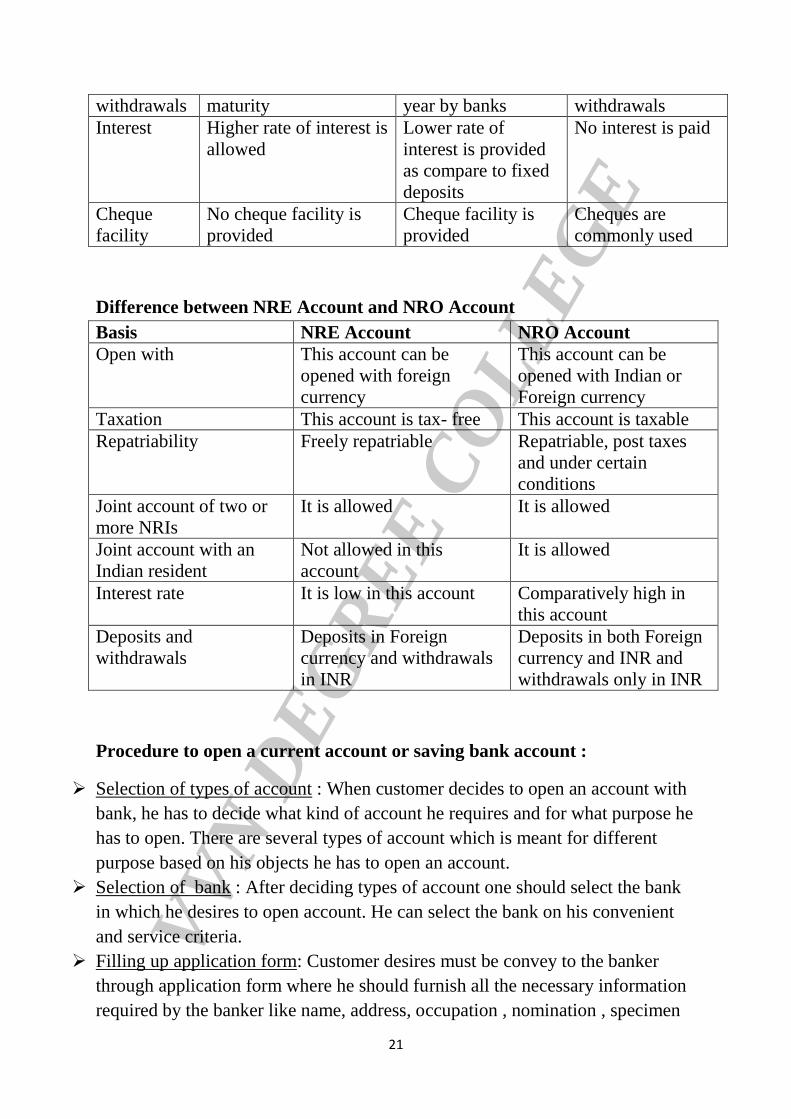

Difference between Fixed deposit account , savings deposit account and

current account :

Basis of

difference

Fixed Deposit Account Savings Deposit

Account

Current Deposit

Account

Object The object of fixed

deposit account is to

earn interest

The main aim of

savings deposit

account is to

cultivate the habit of

savings among the

public

The main aim of

current deposit

account is to assist

the business

Period of

deposit

Deposits are made for a

pre decided and

predetermined period of

time

No predetermined

period for deposits

in saving deposit

account

There is no fixed

period of deposits

as it is an open and

running account

Frequency

of deposits

Deposit is made once in

time

Deposit can be made

large number of

times

No restriction on

depository money

Restrictions

on

The deposit amount can

be withdrawn at

50 withdrawals are

permitted in half

There is no

restriction on

VVN

DEGR

EE C

OLLE

GE

21

withdrawals maturity year by banks withdrawals

Interest Higher rate of interest is

allowed

Lower rate of

interest is provided

as compare to fixed

deposits

No interest is paid

Cheque

facility

No cheque facility is

provided

Cheque facility is

provided

Cheques are

commonly used

Difference between NRE Account and NRO Account

Basis NRE Account NRO Account

Open with This account can be

opened with foreign

currency

This account can be

opened with Indian or

Foreign currency

Taxation This account is tax- free This account is taxable

Repatriability Freely repatriable Repatriable, post taxes

and under certain

conditions

Joint account of two or

more NRIs

It is allowed It is allowed

Joint account with an

Indian resident

Not allowed in this

account

It is allowed

Interest rate It is low in this account Comparatively high in

this account

Deposits and

withdrawals

Deposits in Foreign

currency and withdrawals

in INR

Deposits in both Foreign

currency and INR and

withdrawals only in INR

Procedure to open a current account or saving bank account :

Selection of types of account : When customer decides to open an account with

bank, he has to decide what kind of account he requires and for what purpose he

has to open. There are several types of account which is meant for different

purpose based on his objects he has to open an account.

Selection of bank : After deciding types of account one should select the bank

in which he desires to open account. He can select the bank on his convenient

and service criteria.

Filling up application form: Customer desires must be convey to the banker

through application form where he should furnish all the necessary information

required by the banker like name, address, occupation , nomination , specimen

VVN

DEGR

EE C

OLLE

GE

22

signature etc., account can be opened in his name or by jointly , if he wants to

open current account he can open in the name of his business.

Introducer to open an account : While opening bank account he has to provide

any person’s reference who is customer of the bank and having more than six

month or long relationship with the bank. Introducer has to make sure about

familiarity of the person and has to sign in the application form .

Specimen signatures : When the bank is satisfied with the introductory

reference it proceeds with the opening of the account. The applicant is asked to

give his two or three specimen signature on a prescribed form , generally card,

for the purpose of bank’s record.

Photographs : Banks require four copies of photographs of the account holders.

These photographs are required for all types of account opening. If a customer

has a savings account or current with a bank’s branch , he may open fixed

deposit account without photographs. When a customer comes to a branch he

can be easily identified. The identity of the customers is very clearly established

with the help of photographs .

Submission of application form : After filling of application it has to be

submitted to concerned person along with required documents for legal purpose.

While opening an account one has to submit various documents like address

proof, identity proof incase of individual and article and memorandum , board

resolution in case of joint stock company

Verification of the application by officer : Officer will verify the filled

information and documents which is submitted by the person and confirms the

correctness of the details and allow prospective customers to go ahead.

Initial deposit : When everything set right he has to deposit initial nominal

amount with bank. He should fill the slip and submit the slip along with cash to

cashier, later the transactions, account number will be issued to that person and

he will become customer of the bank.

Advantages of a Bank account :

The following are the advantages of opening an account with bank:

Safety of money: The money with the bank remains in safe custody. There is

always a risk in keeping cash with one’s own self. It may be lost or stolen

Cultivate habit of savings : Banks cultivate the habit of savings in the public.

Savings in the bank on the one hand are safe and on the other earn interest for

its depositors who are promoted to save and deposit some money in their bank

account .

VVN

DEGR

EE C

OLLE

GE

23

Avail loans facilities : Banks allow loans and overdraft facilities to their

customers. This provides financial help to the customers

Collection of cheques etc: The bank collects on behalf of the customers the

amount of cheques, drafts, bills of exchange etc, deposited in the bank.

Facility in making payments: It is always easy to make payment through bank

accounts. Payments are greatly facilitated by means of cheques. The cheques

serve as proof of payment in case of disputes

Safe custody of valuable articles : Valuable articles, deeds, securities etc. can

also be deposited in the bank for safe custody . safe vaults are provided by

banks for storing these valuables.

Providing credit information : Banks provide information relating to the credit

worthiness of the customer. Banks also issue letter of credit for their customers

which are very useful in foreign trade.

Types of customer And account holders

Minor :

A minor is not capable of entering into a valid contract and a contract entered

into by a minor is void – Indian contract act , 1872

A minor is a person who has not completed 18 years of age. If a guardian is

appointed by a court before a person completes 18 years, he remain minor till he

completes his 21 years.

Guardians are classified into three types

Natural guardian : Father is natural guardian after him mother will be the

natural guardian of minor and after marriage husband is considered as guardian.

Testamentary guardian : Testamentary guardian is a person who is

appointed by the will of minor’s father or mother by the will of natural guardian

Guardian appointed by a court under the Guardians and wards act ,1890

Opening of Minor’s Account

The account of minor can be opened in any one of the following modes:

By natural guardian , father or mother on behalf of the minor

By a natural guardian , father or mother in the joint names of

himself/herself and the minor , payable to either or survivor

By a person in the name of any minor of whom he or she is the guardian

appointed by a competent court under any enactment for the time being in force

VVN

DEGR

EE C

OLLE

GE

24

Essential requirements for opening Minor’s account:

For opening the account of a minor bank requires :

Minor’s date of birth . The birth date of is ascertained and verified from

the municipal birth certificate or birth certificated issued by the school authority

where the minor is studying

Recording the date of birth and date of maturity in the account opening

form

Specimen signature card

Date of birth to be recorded in the pass book and in all types of account

Relationship proof will be required as per bank’s recommendation in case

the guardian is not the parent

Name added in the ration card or any other address proof of the minor

PAN card for the parent or guardian who would operate the account on

behalf of the minor

Precautions to be taken at the time of Opening Minor account

Precaution while opening bank account:

Bank prefers to open saving account and fixed deposit account in the name of

the minor and should not allow minor to open current account

Bank can open account in the name of minor or joint name of minor and

guardian . Bank opens account in the name of minor only, he should be at least

14 years or more and should able to read and write regional languages

Precaution for date of birth : While opening bank account for a minor bank

should collect the proof for date of birth and should retain with the bank, when

minor attains his majority on that date bank should close the minor account and

opens new account where the minor ( who has become a major now) can

operate the account alone and at the time bank should get his specimen

signature and should not allow guardian to operate account.

Granting loans to minor: When bank grants any loans to minor, it cannot be

recovered because minor is not a competent party and if there is any agreement

between bank and minor pertaining to loan is not possible to recover amount

from the bank. Even bank cannot recover the loan after minor becomes major

and even if minor represents himself as major, if takes loan in that situation also

bank cannot recover the loan amount. If minor unintentionally overdraw money

from his account then also bank will not get any legal right and power to

VVN

DEGR

EE C

OLLE

GE

25

recover the same. Hence bank should be very careful while operating minor

account.

Guarantees : While accepting guarantee against loan bank should not accept the

guarantee of a minor and bank should not grant loan to minor against the

guarantee of others. Minor is not a principal and not accepted as guarantee. The

law does not permit minor to give guarantee for others and even not to get loan

against others guarantee.

Minor as an agent : Minor can be permitted to acts as an agent on behalf of the

principal , for that bank should get prior written consent from the original

principal. The written consent given by the principal should contain the powers

of agent and banker should allow agent that is minor to perform function upto

the limit of that power not beyond the power. Minor agent can draw amount

through cheque and sign the draft as per the power given by the principal and

any loss or damages occurs by the operation of agent, principal will become

liable for that loss and damages not the agent

Minor as a partner : As per Indian partnership Act Minor can enter into

partnership with the permission of all the other partner. He can enter into

contract and operates bank account and he will not liable for personal asset

against the loss or damages. He only gets benefits from the partnership. After

his majority he should inform whether continue in partnership or not , in the

absent of information it is implied that he will continue in that partnership as a

general partner and then he will become liable for damages and losses and his

personal assets also will become claim against the loss or damages

Risks in a contract with Minor

If any contract is entered into or by any money is advanced to the minor, the

other party runs the following risks:

Any money advanced to the minor cannot be recovered by compulsion as

the contract with the minor is void

As the contract entered with a minor is void right from the beginning,

any money given to him as loan when he was minor cannot be recovered after

he attains majority

Even if surety is given for the money obtained by the minor, the surety

cannot be sued in court, if the principal debtor, who is a minor, refuses to pay

back the loan. VVN

DEGR

EE C

OLLE

GE

26

Minor cannot even pledge or mortgage the property and hence the

securities held by a creditor in the form of pledge or mortgage will not give a

real title and cannot be availed in case a minor debtor refuses to pay the loan.

Even the security belonging to a third party who is a minor is offered

against the loan by a minor in his own capacity, cannot be executed

Even the negotiable instruments drawn or endorsed by the minor are not

valid except in case when it is drawn for the supply of necessities of life.

Joint account

Joint account is a bank account shared by two or more persons, any one of the

individual who is a member of the account can withdraw from the account and

deposit to it. Normally family members or close relatives or business partners

prefers joint account for their convenient transactions

It is an bank account registered in the name of two or more person and any one

of the holder can operate it.

When an account is opened in the name of two or more persons it is known as a

joint account

Features of Joint account

When two or more persons jointly open an account, it is called a joint

account.

As far as possible a joint account should be opened only among close

relatives

Account opening form should be signed jointly by all

A clear operational mandate from the account holders should be obtained

, as to who could operated the account

Photographs , ID and address proof of all individuals as a part of KYC

process are to be obtained

All joint account holders should jointly nominate a nominee

Precautions to be taken at the time of opening joint account

The application for opening of a joint account must be signed by all the

persons desiring to open joint account

The banker should get clear –cut instruction about operation of the

account. The names of person or persons who will sign withdrawals or cheques

VVN

DEGR

EE C

OLLE

GE

27

should be specifically mentioned. In absence of such instructions, the banker

should honour only those cheques which are signed by all joint account holders

The bank should get clear directions about the balance amount to be paid

in the event of death of one or more account holders.

In case the bank allows overdraft from this account then a concurrence

from all the joint account holders should be obtained. The bank should make all

the parties liable jointly and severally for all the amounts due to the bank.

In the event of insolvency or death the operations of this account should

be stopped. The solvent or surviving account holders be advised to transfer the

balance to a fresh account by issuing a cheque

In the event of any party to the account giving a notice of revocation of

authority , the bank should suspend the operation of this account

Any joint account holder, even if he is not authorised to operate the

account, can stop payment of a cheque issued on the joint account. The bank

should follow these directions and stop the operations.

A joint account holder who is authorised to operate the account cannot

appoint an agent or attorney to operate the account on his behalf. Such an agent

or attorney can be appointed by the consent of all the joint account holders

Partnership Firms

Partnership is the relation between persons who have agreed to share the profit

of business carried on by all or any one of them acting for all”

Features of partnership firm

A partnership is a relation between persons who have agreed to share the

profit of a business carried on by all or any one of them acting for all. The

relationship is spelt out in a document called deed of partnership

The minimum number of partners in a partnership should be 2.

A partnership can be either registered or un-registered

A minor cannot be admitted to a partnership, but he can be admitted to

the benefits of a partnership , with the consent from other partners.

When a minor attains majority, he should within 6 months of attaining

majority, has the option to exit the partnership. If he fails to do so, he is deemed

as a partner from the date of his admission to the partnership and will be

responsible for any liabilities and loss too.

Every single partner can bind a partnership by his action

VVN

DEGR

EE C

OLLE

GE

28

If the partnership has applied for registration at the time of opening the

account obtain the provisional receipt from the partners as a proof.

Clear instruction regarding as to who will operate the account, should be

obtained at the time of opening an account

If a new partner is admitted, operations in the account can be allowed

subject to making changes in the account opening forms and banks data base

If a partner retires from a partnership, all other remaining partners have to

authenticate the transaction .

When a partnership is dissolved, the operations in the account are to be

stopped if the account is in debit balance

In a partnership account any one partner can stop the operations. The

bank needs to inform all the other partners about the stopping of operations in

the account through a specific letter

The bank will allow any further transactions only after all partners jointly

authorize the bank to do so, through a letter

Cheques drawn in favour of the firm should not be allowed to be

collected in the individual account of a partner.

Opening of account

A partnership firm can open all types of accounts except saving account. Bank

opens account of a partnership firm in the name of the firm and not in the names

of partners individually or jointly . The account opening form is signed by all

the partners in their individual capacity as well as in the capacity of a partner to

ensure joint and several liabilities. While opening the account banks verify the

partnership deed to examine whether any clause of the deed is detrimental to the

interest of bank. Since bank would not like to be bound by the terms of the

partnership deed, banks do not accept the partnership deed even if offered

In case of registered firm, banks obtains registration certificate. The account is

opened in the name of the firm and all the partners are required to sign account

opening form

Documentation to be obtained while opening an account

Bank’s account opening form duly completed and signed by all partners

ID and address proof of the firm

Photographs and address proof of all the partners; partnership deed copy

Rubber stamp of the firm should be impressed on the application form

and partners signature should be affixed under it

VVN

DEGR

EE C

OLLE

GE

29

Mandate regarding operation of the account

Operations of account

Bank obtains operational instructions that who will operate the account and how

it is to be operated. In case a minor is also a partner in the firm his birth

certificate is obtained to ascertain the date of birth, which is recorded in the

account opening form

All partners jointly one of the named partner two/ three of the named

partners. A third party under a mandate letter or a power of attorney signed by

all the partners

A partner authorised to operate the firm’s account cannot delegate his

authority to another person unless all other partners agree

The authority given to operate the account can be withdrawn by any of

the other partners including dormant or sleeping partner by giving notice to the

bank

Each partner, whether he/she is operating the account or not , has powers

to countermand payment of the cheques

Precautions to be considered for partnership firm :

Number of partners: While opening partnership account bank must consider

partnership deed which is the article of partnership firm. Bank should make sure

whether the number of partners are according to legality or not. As per legal, in

case of banking firm there is maximum limit of partner 10 and any other firm

maximum is 20. Partnership firm need minimum two partner to open

partnership firm

Name of bank account : In case of partnership account bank should open

account in the name of firm but not in the name of any individual partner

Opening of an account : Bank can open the account in the name of partnership

firm and at the time of opening account banker should get specimen signature of

all the partners and all the partners should agree to open the account in the name

of firm if there is any objection to open account by any of the partner, bank

should not open the account until all the parties agree. Hence bank should

obtain the authority letter signed by all partners

Cancellation of authority to operate the accounts : When partnership account is

opened any one or more partner will gain the authority to operate the account

VVN

DEGR

EE C

OLLE

GE

30

that is who can withdraw and deposit amount from and to the account. In such

case when bank receives any notice regarding cancellation of the authority of

the partner, bank must stop the payment and operation of the account. Any

partner including sleeping partner can give notice to bank regarding to stop

payment or cancellation authority

Delegation of authority : Delegation of authority refers to transferring power

and right from one person to another person when he is not available or absent.

Partner cannot delegate his authority to any other person without written

consent of all the partners. If he has to appoint any person to work on behalf of

him he should take permission from all the partners and prepare power of

attorney to transfer powers from authorized partner to any other person by the

signature of all the partners

Admission of new partner : On admission of any new partner to the partnership

account bank must close the account , if there is any overdraft facility and

should open new account from the consent from all the partner including new

partner. In case if the bank account shows debit balance at the time of admission

of new partner, bank no need to close the account but written consent from all

the partner should be obtained

Retirement of partner : At the time of retirement of any partner , a notice is to be

served to banker. With the absent of notice, retired partner will becomes liable

for further transactions. When partner retires and bank balance show credit

amount, in such case no need to close bank account and when any debit balance

at the time of retirement, bank must close the account to avoid the applicability

of clayton’s rule and new account has to be opened by the consent of all the

existing partner

In case of death of partner : When partner dies the partnership firm may be

dissolved or may not be dissolved. If it is dissolved then bank must close the

account and if not bank can allow partners to operate account based on

conditions. When partnership is not dissolved and account balance shows credit

balance then banker no need to close the bank account and asks remaining

partner to settle deceased partner’s net balance to his executors. In case if bank

account shows any debit balance bank must close the account to avoid

applicability of clayton’s case

Insolvency of partner : In the event of insolvency of any partner , the remaining

partner can be allowed to operate the account. If there is any cheque which is

drawing by insolvent partner it must be stopped by the banker without paying

VVN

DEGR

EE C

OLLE

GE

31

the amount but if the cheque drawn prior to judgment of insolvent on that even

bank can honour the cheque with prior permission by the remaining partners

Joint Stock Company

A joint stock company is constituted under company act. Company is a artificial

person with perpetual succession. It is voluntary association of persons formed

for some common purpose with capital divisible into parts known as share. It

has separate legal entity and corporate personality. It is separate from the

shareholders constituting it.

Features

Companies are artificial persons which have legal existence. Companies

which are incorporated under companies Act 2013 can open account with bank

Company can be broadly divided into private limited and public limited

companies

Private limited companies cannot issue shares to public and the minimum

number of shareholders is 2 and the maximum number of shareholders is

restricted to 200

Public limited company can issue shares to public. The minimum

numbers of shareholders are 7 and there is no ceiling of maximum number of

shareholders

Formalities relating to opening accounts of companies will include

obtaining the following documents namely

Memorandum Of Association and Articles Of Association

Certificate of incorporation issued by the Registrar of companies in

whose jurisdiction the company is registered

Certificate of commencement of business

Copy of Board resolution certified by the chairman to open an account

with the bank. Operating instruction regarding execution of documents, the

name/s of director/s other executive authorized to sign etc.

Copy of latest audited balance sheet and profit and loss account. List of

present directors duly certified by the chairman, address of the registered office

along with the KYC documents pertaining to the company should also be

obtained along with KYC documents in respect of authorised signatories

VVN

DEGR

EE C

OLLE

GE

32

All account opening forms should be signed by authorised signatories.

Photographs of authorised signatories as per KYC norms should be obtained

All documents should contain the company’s seal

In case of change of constitution, the company has to inform to the bank.

In case of death of director , as a company is a legal entity having perpetual

existence, its account should not be stopped

A fresh resolution by the board of directors, authorizing the new directors

and their specimen signatures should be submitted to the bank.

Precautions to be taken by the Banker for joint stock company account

Study of documents: Banker should properly and carefully study the

important documents like certificate of incorporation and certificate of

commencement of business, Memorandum of association , article of association

and prospectus . banker should also obtain the printed and certified copies of all

these important document for his own record

Copy of Board’s resolution: banker should get certified copy of resolution

passed by Board of directors along with the application to open the account. The

resolution should contain the information relating to:

Appointment of banker of company

Authorised persons to operate the bank account on behalf of company

Authorised persons to execute the documents on behalf of company

Authorised persons to deposit the title deeds in case of equitable

mortgage

Bank should observe while borrowing amount, whether the borrowing is

done under the delegation of power and is it done under the provision of article

and should examine the document produced during the borrowing

Bank should examine the purpose of borrowing and the purpose should

be under the provision of memorandum.

At the time of closing down of the company, powers of the director are

canceled except to the extent permitted by the company and director cannot

borrow funds without permission of liquidator and permissible limits given by

the liqudiator

At the time of providing any loan to company against the mortgage of the

property, bank should verify whether the security will come under the purview

of any charge if it is so, then bank should consider second charge applicability

Clubs and Associations

VVN

DEGR

EE C

OLLE

GE

33

Clubs , societies , charitable and religious institutions, libraries, schools ,

colleges etc not engaged in trading activities maintain their account with the

banks.

Features

Clubs, societies and associations are bodies of members, who come

together for a common cause. Generally , a non- trading clubs, societies and

associations approach banks to open account. Such bodies do not share profits

with members

Clubs can be registered or unregistered . Accounts of unregistered clubs,

societies and associations cannot be opened as individual members are not

liable for debts of the body, hence suits can’t be enforced

While opening of accounts of clubs and associations obtain the account

opening form along with photos of the office bearers, address proof of all the

office bearers, certified true copy of the original certificate of registration,

certified true copy of MOA , certified true copy of the rules, regulations, bye-

laws, resolution of managing committee appointing the authorized persons to

operate the account

Bank should take the following precautions in case of clubs and association

account :

Incorporated club and Non incorporated club: Normally there are two types of

clubs that is registered and unregistered club. While opening bank account for

clubs and society bank must see whether it is incorporated or not, if it is

incorporated , bank should obtain incorporation certificate and then allow club

to open account. If the club is not incorporated it is problem for bank to recover

amount due by the clubs because bank can not able sue on unregistered club. If

banks allows unregistered club, if it do so it is on own risk of the bank

Rules and laws of club: If the club is registered one, it must formulate rule and

regulation on its own. It will have its own constitution and own rules and laws.

Bank has to obtain the copy of the same and retain with bank for further

reference

A resolution from managing committee : Managing committee should pass a

resolution to open bank account and bank should receive a copy of the

resolution. The resolution should include the following information

Appointment of the bank concerned as a banker of the club

VVN

DEGR

EE C

OLLE

GE

34

Information regarding the name of authorised person who operate the

account and who can withdraw and deposit fund

Borrowings : While borrowing bank should confirm whether the club is eligible

to borrow or not and clearly note the borrowing limit. Bank should get a copy of

special resolution from the managing committee or board regarding borrowing

fund until and unless bank should not allow club to borrow