Embed Size (px)

Citation preview

Unit 10. Methods of International Settlements

International money transactions refer to the movement of funds from one country to another. The main reason for moving funds from one country to another is the settlement of debts resulting from international trade.

• The methods of payment chiefly include remittance, collection and L/C. If the payment is made by remittance, it is called favorable exchange ( 顺汇 ), by which the buyer makes the payment by bank of his own accord; if by collection or L/C it is adverse exchange ( 逆汇 ), by which the exporter takes the initiative to gather payment from the buyer.

• To choose a method for the payment of the goods, you should consider the credit standing of the buyer. Different methods of payment mean different credits. Bank credit ( 银行信誉 ) is more reliable than commercial credit ( 商业信誉 ). So, we should choose the right method for the safe settlement of the payment.

I. Remittance

A. Definition • Remittance is to deliver the payment of the goods to the seller by bank transfer. In re

mittance, there are four parties involved: the remitter, the beneficiary, the

remitting bank and the paying bank.• The remitter remits the money to the beneficiary as it is required by the contract con

cluded between them. And when the remitter comes to the remitting bank, he fills an application form for the bank to effect the payment, which upon remittance will be binding upon the remitting bank. And the paying bank pays the beneficiary because it is the branch bank or correspondent bank of the remitting bank in the

country of the seller.• Remittance is mainly used for payment in advance ( 预付货款 ) , open account ( 赊销 ) for small quantity of goods, commission, sundry charges, etc.

(a) If it is used for payment in advance or cash with order, it will place the seller in an advantageous position.

(b) If for delivery first and payment afterwards, it will place the buyer in a favorable position.

Note:Remittance uses commercial credit and hence in adopting this method, the parties involved need have trust in each other.

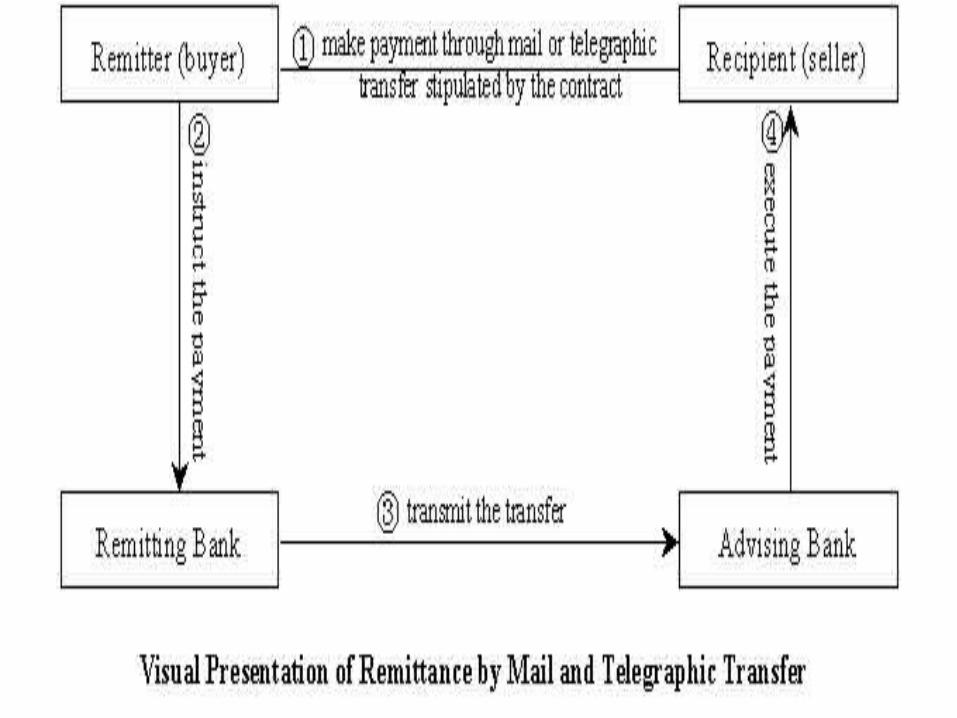

B. Types of Remittance• Money transfer can be channeled through banks by mail transfer

(MT), telegraphic transfer (TT), and demand draft (DD). (a) By mail transfer, the buyer will hand over the payment of the

goods to the remitting bank that will authorize its branch bank or correspondent bank in the country of the beneficiary by mail to make payment to him.

(b) By telegraphic transfer, the buyer will hand over the payment of the goods to the remitting bank which will authorize its branch bank or correspondent bank in the country of the beneficiary by telegraphic means to made the payment to him. Mail transfer is cheap but time-consuming, while telegraphic transfer is more expensive but much faster.

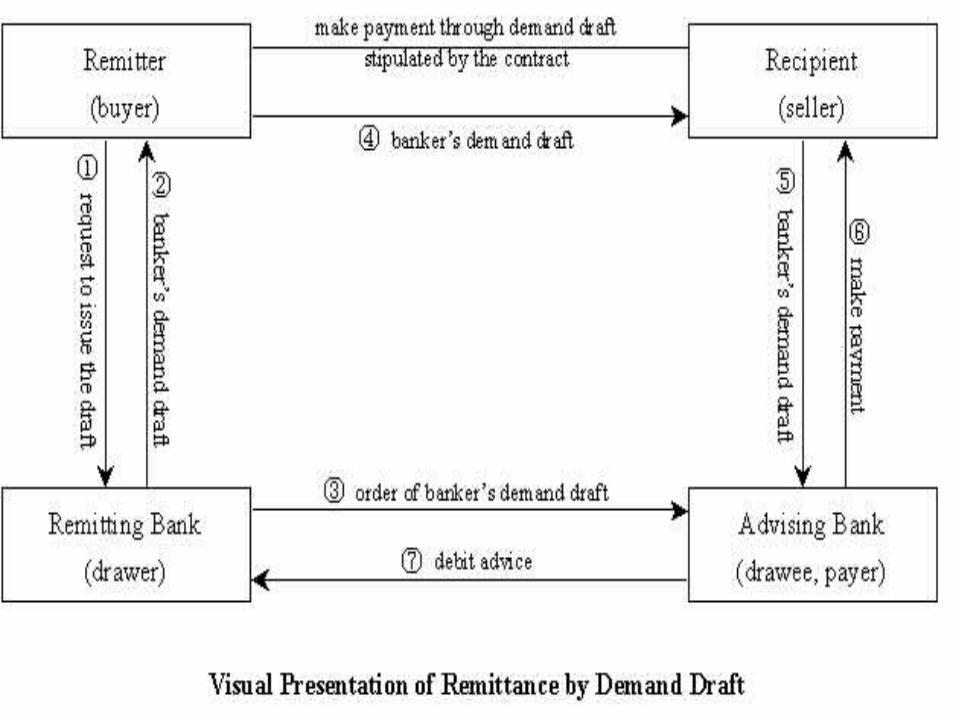

(c) By demand draft, the buyer will come to the local bank to buy a banker’s bill and then deliver it to the seller or beneficiary by mail. When the seller of beneficiary receives it, he will come to the bank designated by the banker’s bill for cash.

II. Collection

A. Definition

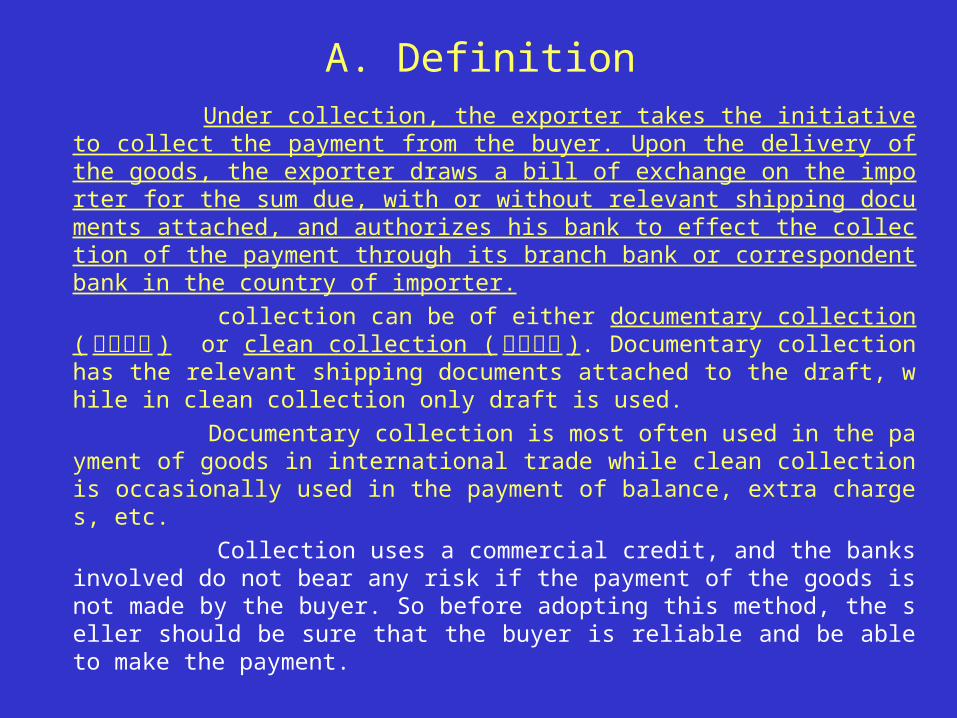

Under collection, the exporter takes the initiative to collect the payment from the buyer. Upon the delivery of the goods, the exporter draws a bill of exchange on the importer for the sum due, with or without relevant shipping documents attached, and authorizes his bank to effect the collection of the payment through its branch bank or correspondent bank in the country of importer.

collection can be of either documentary collection ( 跟单托收 ) or clean collection ( 光票托收 ). Documentary collection has the relevant shipping documents attached to the draft, while in clean collection only draft is used.

Documentary collection is most often used in the payment of goods in international trade while clean collection is occasionally used in the payment of balance, extra charges, etc.

Collection uses a commercial credit, and the banks involved do not bear any risk if the payment of the goods is not made by the buyer. So before adopting this method, the seller should be sure that the buyer is reliable and be able to make the payment.

B. Parties Involved in Collection

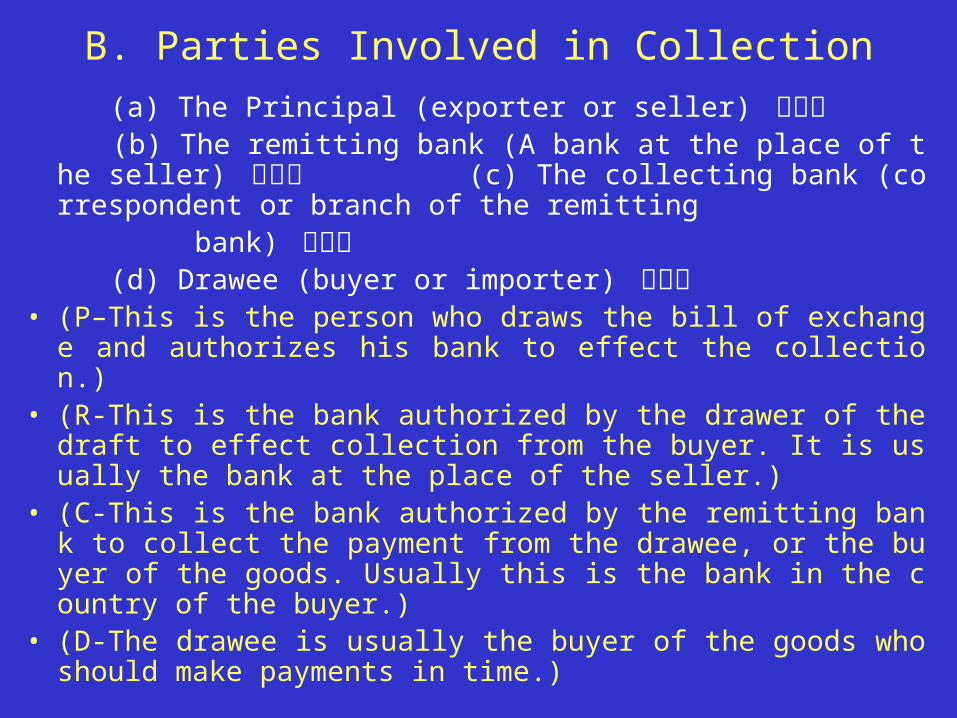

(a) The Principal (exporter or seller) 出票人 (b) The remitting bank (A bank at the place of the seller) 托收行

(c) The collecting bank (correspondent or branch of the remitting

bank) 代收行 (d) Drawee (buyer or importer) 受票人• (P–This is the person who draws the bill of exchange and authorize

s his bank to effect the collection.)• (R-This is the bank authorized by the drawer of the draft to effect c

ollection from the buyer. It is usually the bank at the place of the seller.)

• (C-This is the bank authorized by the remitting bank to collect the payment from the drawee, or the buyer of the goods. Usually this is the bank in the country of the buyer.)

• (D-The drawee is usually the buyer of the goods who should make payments in time.)

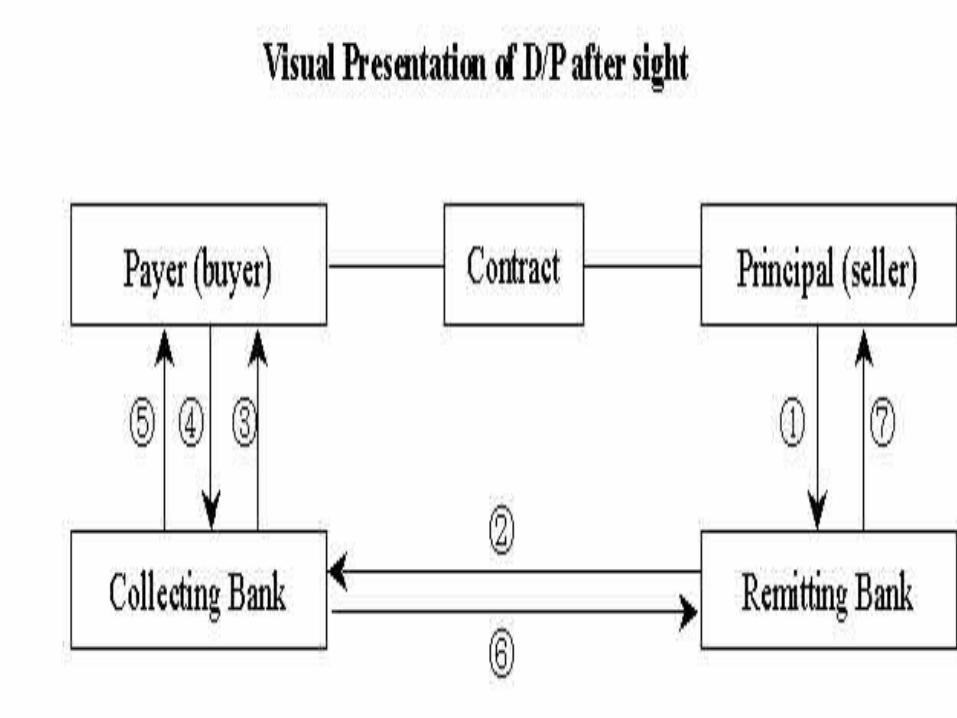

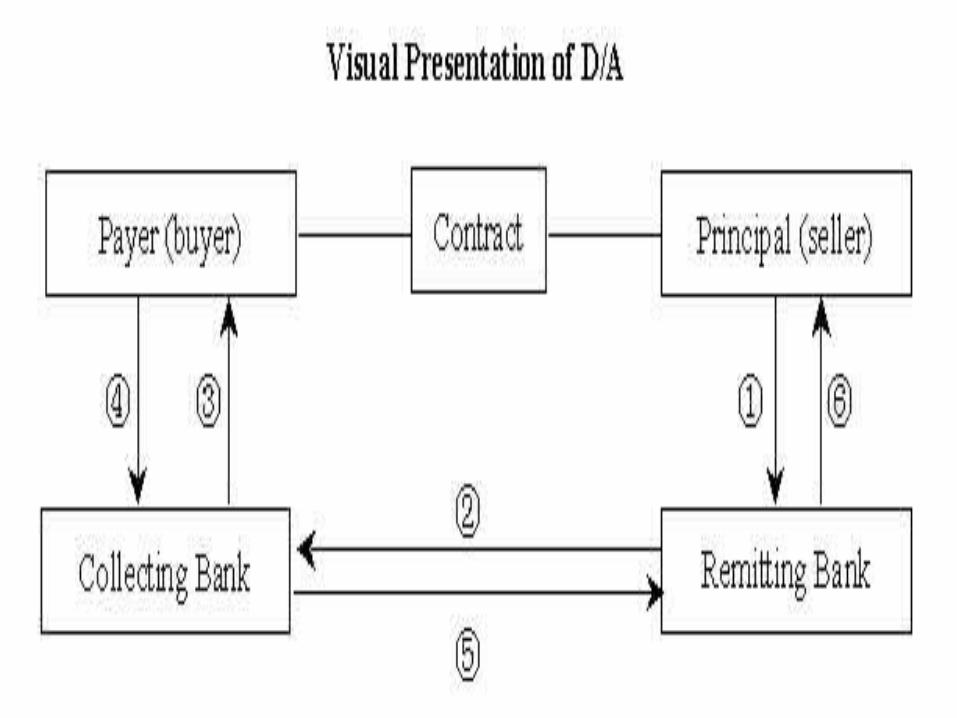

C. Documents Against Payment (D/P)

Under D/P, the buyer can receive the shipping documents only after he has duly made the payment of the goods. It can be further be of 2 types: D/P at sight and D/P at __ days after sight (date).

◆D/P at sight. Under D/P at sight, the seller might draw a draft on the buyer. He hands over the shipping documents together with draft, and the shipping documents and the draft will be transferred to the collecting bank which present them to the buyer and ask him to make the payment at sight. The buyer, upon sight, should then make the payment and obtain the shipping documents. When the collecting bank has finished the collection, it should immediately notify the remitting bank, which will then make the payment to the seller.

◆D/P at __ days after sight (date). Under D/P at __ days after sight (date), the buyer shall duly accept the documentary draft drawn by seller at __ days’ sight upon first presentation and make payment on its maturity. The shipping documents are to be delivered against payment only.

Note:

Under D/P, the buyer can not obtain the shipping documents if he does not make the payment, should this happen, the seller need first negotiate with the buyer, and at the same time, he may consider if he can sell the goods to others or to ship the goods back, usually at his own cost.

D. Documents Against Acceptance (D/A)

Under the D/A, the buyer can get the shipping documents from the collecting bank after he has duly accepted the draft. This is only applicable to time draft. This is greatly convenience to the buyer, but it means much more risk for the seller, for once he has delivered the shipping documents, he will have lost his title over the goods.

D/A means more risks for the seller, for the buyer might refuse to pay after he has accepted the draft and taken the delivery of the goods. Certainly the seller might sue the buyer, but as is often the case, the buyer claims bankruptcy and then the seller can do nothing to remedy the situation.

III. Letter of Credit(L/C)

As we can see, neither remittance nor collection is a safe means for the settlement of payment in international trade as both of them rely on commercial credit. With the development of international trade, bank credit gets involved in the settlement of payment which provides it with more secure means. L/C is the major means thus developed is now most often used in the settlement of payment in international trade.

A. Definition

• In international trade practice, a L/C can be seen as a document by which a bank, upon the request of an importer, promises to effect the payment of the goods to the exporter.

• Function of L/C: The L/C solves the possible problems arising from

the distrust between the seller and the buyer. Under L/C, the seller can feel assured that so long as he has made the delivery of the goods and got the required documents he can get the payment of the goods in time and the buyer can also feel at ease that he can get the shipping documents at the same time when he effects the payment of the goods.

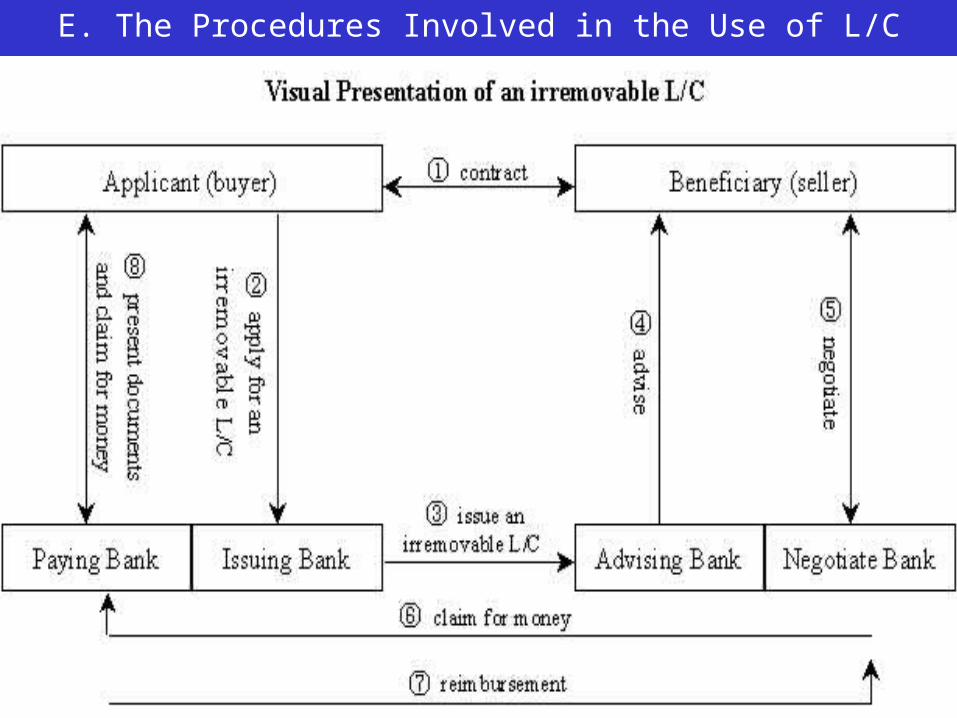

B. Parties Involved in L/C

• The applicant, who is usually the importer that applies to the bank for the L/C.

• Issuing bank, which opens the L/C upon the request of the importer.

• Advising bank, or notifying bank, which is authorized by the issuing bank to transfer the L/C to the exporter’s bank.

• Beneficiary, who is usually the exporter and is entitled to use the L/C for the payment of the goods.

• Negotiating bank, which is willing to buy on discount the documentary draft drawn by the beneficiary.

• Paying bank, which is designated by the L/C to pay the draft.

• Confirming bank, which is asked by the issuing bank to confirm the L/C. If a bank has confirmed the L/C, it holds itself responsible for the negotiation or payment of the L/C.

C. The Main Contents of L/C • (a) The parties involved, including the applicant, the issuing bank, negotiatin

g bank, the paying bank, etc.• (b) Remarks about the L/C: such as the No. of the L/C, its type, the issuing d

ate, etc.• (c) The amount of the L/C• (d) The clauses of the bill of exchange, such as the amount of the bill, drawer

and drawee, the paying date, etc.• (e) The clauses about the documents, what documents are required, such as th

e invoice, the bill of lading, the insurance policy, the packing list (装箱单) , the certificate of origin, and inspection certificate, etc. Also, the required member of copies of the documents, description of the goods, specifications, quantity, packing, unit price, total amount, mode of transport, place of unloading, etc.

• (f) Particular clauses, such as the special provisions about the deal in accordance with the particular business or political situations of the importing country.

• (g) Guarantee clauses of the issuing bank, which testifies that the issuing bank will hold itself responsible for the payment to the beneficiary or the holder of the draft.

D. Revocable L/C & Irrevocable L/C

• Revocable L/C (可撤消信用证) is the one that can be withdrawn or amended by the issuing bank any time before the negotiation, or acceptance, or payment is effected. In doing so, the issuing bank does not need to have the agreement or even notify the beneficiary. This is rarely used in the settlement of payment in international trade.

• Irrevocable L/C (不可撤消信用证) is the one that cannot be withdrawn or amended by the opening bank without the agreement of the beneficiary. This hind of L/C is more secure and hence is most often used.

We should note that, according to Uniform Customs and Practice of Commercial Documentary Credits 500, if a L/C is not marked as being irrevocable, it should be taken as irrevocable.

E. The Procedures Involved in the Use of L/C