Embed Size (px)

Citation preview

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

1

UNITED NATIONS “ROYALTY”: Potential Impacts on Future Deep Water Investments from Article 82 of The United Nations Convention on the Law of the Sea

Prepared by: RODGERS OIL & GAS CONSULTING

February, 2015

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

2

1. PURPOSE

The purpose of this report is to describe the UN Levy, identify relevant issues around its

interpretation, and provide estimates of the potential impacts on investors and the host

jurisdiction, both taxpayers and resource owners.

2. INTRODUCTION & PURPOSE

The oil and gas industry is currently reeling from a precipitous decline in prices. This

decline affects high cost producers and projects, including, in particular, those projects

in the deep water offshore. British Petroleum, for example, suggests that low prices

could last for perhaps the next three years.1 Nobody expects prices to remain at current

levels (below $ 50/bbl) for the long term. The period of lower prices may be long

enough to play a role in positioning the global economy for renewed growth, and in

helping to ease some of the cost pressure facing the industry. In the longer term,

growing demand, particularly in Asia and Africa, is seen as underpinning higher prices.

From a supply perspective, the deep water offshore has been playing an increasing role

in meeting future demand.

Global [deep water] investment has soared from $16 billion in 2003 to more than

$70 billion in 2013, and production has more than doubled over the past ten

years to almost 6 million barrels per day, or 7 percent of the world’s total oil

supply. …

The major oil companies have seen deep-water as an attractive business that can

deliver large volumes at high margins, more than offsetting its handicaps of tying

up immense amounts of capital and technical challenges. They have doubled

down, betting on deep-water across the globe: the average number of countries

in which the super-majors participate in deep-water projects has increased from

three to seven over the past decade. 2

Deep water developments are tending to be located further offshore, often beyond 200

nautical miles (nm) – for example, the Bay du Nord discovery offshore Newfoundland &

Labrador (NL) is beyond Canada’s exclusive economic zone (EEZ) in 3,600 feet of water.

1 BBC News, January 21, 2015, http://www.bbc.com/news/business-30913321 2 Navigating in Deep Water: Greater rewards through narrower focus, Thomas Seitz & Kassia Yanosek,

McKinsey and Company, 2014.

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

3

In an already challenged cost environment, developments beyond the EEZ face even

higher costs due to a new, or additional, fiscal levy. This levy results from Coastal

States’ obligations under the United Nations Convention on the Law of the Sea

(UNCLOS).3

Article 82 of the convention requires Coastal States to make payments for the benefit of

other, land-locked states. These payments4 relate only to production from a coastal

state’s jurisdiction beyond 200 nm. Developing states that are net importers of the

mineral resource produced on their continental shelves are exempt from this obligation.

The English text of Article 82, states that: 1. The coastal State shall make payments or contributions in kind in respect of the

exploitation of the non-living resources of the continental shelf beyond 200

nautical miles from the baselines from which the breadth of the territorial sea is

measured.

2. The payments and contributions shall be made annually with respect to all

production at a site after the first five years of production at that site. For the sixth

year, the rate of payment or contribution shall be 1 per cent of the value or

volume of production at the site. The rate shall increase by 1 per cent for each

subsequent year until the twelfth year and shall remain at 7 per cent thereafter.

Production does not include resources used in connection with exploitation.

3. A developing State which is a net importer of a mineral resource produced from

its continental shelf is exempt from making such payments or contributions in

respect of that mineral resource.

4. The payments or contributions shall be made through the Authority, which shall

distribute them to States Parties to this Convention, on the basis of equitable

sharing criteria, taking into account the interests and needs of developing States,

particularly the least developed and the land-locked amongst them.

No payments are currently being made under this article.

3 The United Nations Convention on the Law of the Sea (UNCLOS) is an international agreement between

166 countries that establishes a framework for a range of ocean activities such as navigation, fisheries, and seabed resource exploration and exploitation.

http://www.un.org/depts/los/convention_agreements/convention_overview_convention.htm 4 While “payment” under Article 82 is seen as a royalty, levy is used in this report to distinguish it from

domestic or more traditional royalties applied by a coastal state. In addition, the Article permits “contributions in kind”. This adds its own set of complications. These are not discussed in this report except to say that states are being encouraged to drop the contributions in kind option.

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

4

The rational for these payments is the “common heritage of mankind” (CHM). The

convention recognizes that resources beyond 200 NM are not the exclusive property of

any single nation; that all nations have an inherent right to take part in their exploitation,

and that they cannot exercise their rights without due regard for the rights of others. 5 In

this context, an important understanding is that the obligation is not so much a cost as it

is part of the benefits afforded coastal states for the privilege of enjoying extended rights

beyond the EEZ.

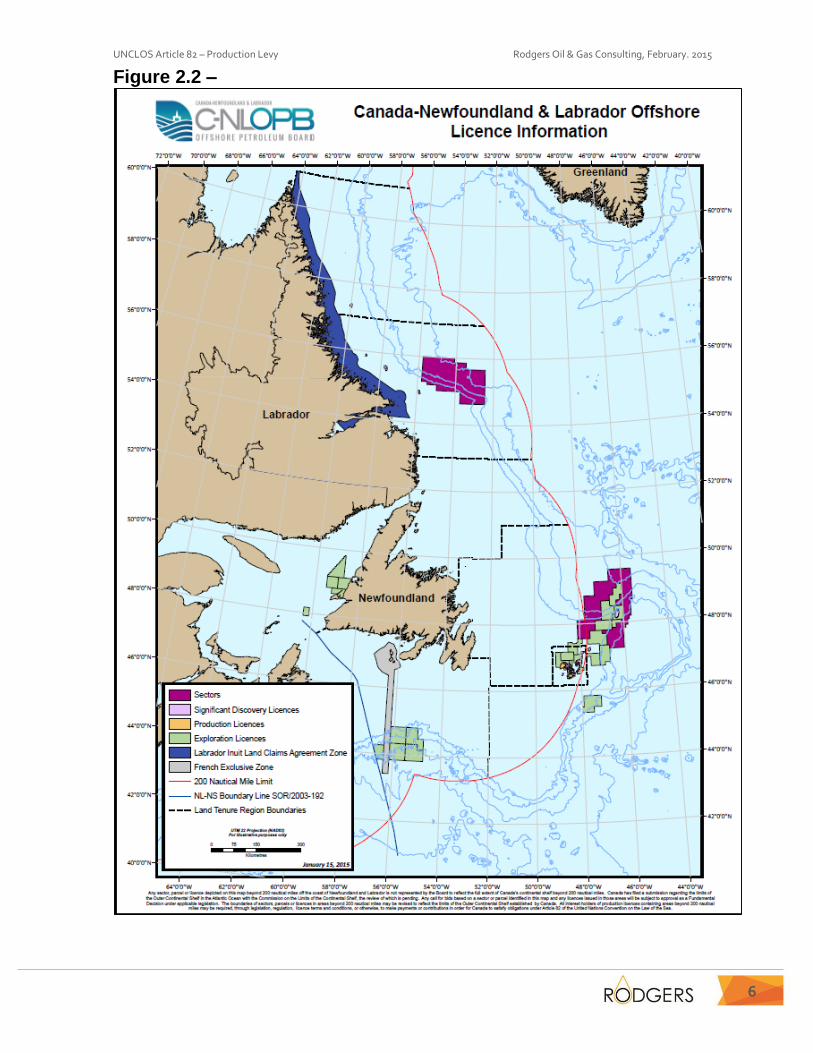

Figure 2.1 provides a conceptual illustration of the Article 82 area from which payments

would be required. Figure 2.2 provides further illustration, identifying the area under

management off Canada’s East coast and showing the sectors and exploration licenses

within and beyond the 200 nm red line.6

5 Legal discussion of common heritage of mankind (GHM) generally begins with the speech of the Maltese

ambassador Arvid Pardo (1914–1999) to the United Nations in 1967. In this speech he proposed that the seabed and ocean floor beyond national jurisdiction be considered CHM. See Prue Taylor, The Common Heritage of Mankind: A Bold Doctrine Kept Within Strict Boundaries, 2011.

http://wealthofthecommons.org/essay/common-heritage-mankind-bold-doctrine-kept-within-strict-boundaries

6 Geologically the widths of the continental shelves vary, from less than I nautical mile (nm) along parts of the US state of California to 800 nm along parts of the northern coast of Siberia. The world-wide average is 40 nm. See Natural Geographic, http://education.nationalgeographic.com/education/encyclopedia/continental-shelf/?ar_a=1

The average water depth is about 200 feet, 400 feet at the shelf/slope break point. See Science Clarified, http://www.scienceclarified.com/landforms/Basins-to-Dunes/Continental-Margin.html

The EEZ represents an area of 85 million (MM) square kilometers (sq km) world-wide. The Article 82 area adds 15 MM sq km. For comparison, the size of the in-land portion of the United States (Lower 48) is 8 MM sq km. See National Oceanic and Atmospheric Administration (NOAA) of the U.S. Department of Commerce, http://www.gc.noaa.gov/gcil_maritime.html

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

5

Figure 2.1 -

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

6

Figure 2.2 –

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

7

3. DEFINITIONS & FISCAL PRINCIPALS: Article 82 contains a number of important terms that are not defined. For example:

“payment” - is this a royalty or a tax;

“production” – is this gross or net production;

“site” – does this refer to a licence, a well, a platform, or a project (e.g., multiple

wells/platforms linked by storage, gathering and offloading infrastructure)?

“value” - is this monetary value on the day of sale, monetary value on the day of

extraction? Is value to be measured at the site, or at some other location?

An excellent discussion of these and related matters is contained in the International

Seabed Authority’s Technical Report No. 4.7

The first observation in considering Article 82 is to recognize that the obligation to pay is

on the coastal state not producers. It is therefore not necessary that the obligation be

passed on to producers. This said, it would appear that producers will be required to pay

on the basis that the levy is a cost of doing business and enjoying the right to profit.

Whether there would then be some method of offset is a different matter.

It is the sovereign state’s jurisdiction to decide on how the UN levy will interact with other

fiscal instruments. If it decides that the levy will interact with other instruments the

details of such interaction will have to be worked out. Issues such as whether the levy is

a royalty or a tax and whether it is based on gross or net production then become

important. Some of the discussion around these and related issues is presented below.

Royalty or Tax: In day-to-day usage royalties are often referred to as taxes – to connote

a fiscal burden irrespective of how it is labeled. Petroleum fiscal system design

principals refer to the fiscal burden as the resource owner share, the government share

(GS), or government take. While the latter term is most commonly used, it does reflect

one perspective where the government is seen as taking something. Resource owners

don’t see a royalty as taking anything, rather they see it as sharing in the benefits of

development, since the resource ultimately belongs to the State.

7 Issues Associated With The Implementation Of Article 82 Of The United Nations Convention On The

Law Of The Sea, ISA Technical Study, No: 4, Kingston Jamaica, 2009.

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

8

The GS has two broad conceptual components – royalties and taxes. This distinction is

important as taxes ultimately find their justification in costs whereas royalties are based

on the notion of “excess” profits - economic rent. 8

Taxes are levies of general application, typically applying to all companies and company

activities; e.g., corporate income tax (CIT), value added tax (VAT), and import duties.

Economic rent however is a site-specific concept.

Taxes are conceptually linked to costs through the state’s sovereign right to impose

levies to support public services; e.g., the military, police protection, transportation,

education, and health care.

It is customary for CIT systems to treat royalties as a deduction in determining a

company’s tax obligation. This is essentially no different than recognizing other input

costs such as the cost of constructing production facilities or drilling wells. From a cost

perspective the price charged by the drilling contractor is no different than the price

charged by the resource owner for granting access to the state’s resources.

While the term “royalty” has a specific historical interpretation as a levy on the gross

value of production it is often used to refer to any fiscal instrument, however defined,

that is not a tax. The fiscal system applicable to production from the United States outer

continental shelf consists of a bonus bid from the competitive bidding process for the

allocation of petroleum rights, a fixed percentage royalty, and normal CIT. Other

jurisdictions may have no bonus requirement but have a somewhat higher royalty. In

Canada the distinction may not be so clear. In addition to CIT, the fiscal system

applicable in the Newfoundland & Labrador offshore consists of a royalty with two

components – one based on gross revenue and the other based on net revenue. To

reinforce the notion that this is essentially a single royalty the gross component is always

payable and creditable against the net component when the latter is payable. The gross

8 Economic Rent is the price that the owner of a resource charges for access to this resource. This price

is seen as an “excess” profit in that it is the share remaining after investors have earned a competitive return and all costs have been recovered, including exploration investment, risk, and uncertainty.

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

9

component however does allow the deduction of costs, including prior royalty paid and a

return allowance to be consistent with the notion of economic rent.

Relating royalties or otherwise non-tax fiscal levies to economic rent would imply a net

basis for these levies as Economic Rent is an after-cost concept. This said, it is again

common practice in designing fiscal levies to find a balance between simplicity and

complexity. Complexity is often introduced as a consequence of enabling the fiscal

instrument to accommodate the widest possible range of potential economic outcomes.

For some projects a 1% royalty might be appropriate while for other a more appropriate

rate might be 25%. Jurisdictions that, for example, opt for an 18.75% royalty would

under-value their share in some cases and over-value it in others. Profit sharing or net

revenue-based royalties might come closer to the appropriate share across the full

range of situations.

While profit sharing systems might be more flexible in fine tuning the rate to differing

economic situations, this flexibility comes with increased complexity, increased

administrative costs and risks, and decreased transparency. This is why many

jurisdictions, the United States in particular, opt for the simpler more straight forward

approach. The fixed rate does not mean that these jurisdictions ignore costs and thus

the principal of economic rent. Policy makers respond to situations where the fixed

royalty might be too high with a view that it is in fact the market signaling that prices are

not yet high enough to bring on projects with this cost structure. Similarly, situations

where the rate might be seen as too low are seen as recognizing the importance of

upside potential to investors, thereby allowing the fixed rate to be higher than it would be

otherwise.

Newfoundland & Labrador’s approach is representative of that adopted by many

jurisdictions. Most jurisdictions provide a mechanism or basis to effectively graduate

the royalty rate up as costs are recovered. In NL’s case this is primarily accomplished

through the net royalty component. It is possible to think of the whole net component

apparatus as nothing more than the basis for an increase in the royalty rate.

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

10

Another approach (one that balances the recognition of cost recovery with fiscal

simplicity) is to offer a fixed royalty structure that graduates over time. This is the

approach taken by Article 82 where a royalty-free period is allowed for 5 years thereby

facilitating cost recovery after which the rate gradually increases from 1% to the

maximum 7% over 7 years.

Royalty - Gross or Net - What did the Article 82 drafter intend? Did drafters intend the

levy to be based on gross production or determined on a net basis? If on a net basis, it

might mean that other fiscal levies can be deducted in determining the levy. It would be

hard to imagine the drafters choosing a net approach that would be applied, potentially

differently, across 166 different jurisdictions. “During negotiations of Article 82 at

UNCLOS III the possibility of using the net was considered, but it was thought that it was

simpler to consider the gross because of the diversity of accounting systems.” 9

Production: With the net approach rejected, the reference to all production in Article 82

Is being seen as meaning commercial production as this would be consistent with

accepted industry practice. The phrase Production does not include resources used in

connection with exploitation is similarly seen as excluding, for example, water or gas re-

injected to enhance resource recovery or gas flared due to necessity.

Valuation: Another question relates to where the production is to be valued. The

definition refers to a “site”, but offers no further explicit guidance. It would be common

practice to value production at or near where it is produced – the wellhead or lease

boundary. Thus, in most situations the fiscal rules permit reduction of the sales price for

transportation costs from the lease boundary to the point of sale.

Implicit in the issue of valuation is the consideration of currency. Since this is an

international levy it is assumed that valuation would be in terms of some commonly

9 Implementation of Article 82 of the United Nations Convention on the Law of the Sea - ISA Technical

Study: No. 12 – Report of the International Workshop convened by the International Seabed Authority in collaboration with the China Institute for Marine Affairs in Beijing, the People’s Republic of China, 26 – 30 November 2012.

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

11

accepted currency. Industry practice would be to use United States dollars (USD’s).

The euro is another possibility.

Interaction with Other Fiscal Instruments: The United States has adopted the position

that producers would pay but would see no, or minimal, additional fiscal burden. Under

US Federal OCS leases in the Gulf of Mexico (GoM), the producer must pay both

domestic royalty and the UN levy, however the levy would be a credit against the royalty.

To illustrate: the current royalty rate is 18.75%; if the Levy were 7%, the producer would

effectively pay 7% levy + 11.75% (18.75% - 7.0%) royalty. If the federal royalty were

less than the levy, say 5%, the producer would pay a total of 2%, as the credit would not

permit the royalty to be reduced below zero. See note for a brief description of the NL

royalty terms.10

Corporate Income Tax: Presumably the levy would be deductible in determining

corporate income tax. This again would be accepted practice in seeing other fiscal costs

as necessary in earning income and thus recognized in determining profits.

With respect to the interaction with other fiscal instruments, individual states will have to

decide what is most appropriate. There will probably be complications stemming from

domestic circumstances. For example, the UN levy is a commitment made by Canada

(by the national level of government); at the same time, the Canadian Federal

government and the Government of Newfoundland & Labrador have agreed, for royalty

purposes, that the offshore is to be treated as if it were provincial jurisdiction.11 This

means that NL effectively owns the resources on which these royalties would be based.

This, in turn, might suggest that NL would support the position adopted by Canada and

other coastal states in adopting the UNCLOS. Alternatively, the NL Government might

take the position that the Federal, not the Provincial, government undertook the

10 Newfoundland & Labrador’s royalty structure has a gross rate component that ranges from 1% - 7.5%,

based on cumulative production, and simple payout, and a net component with incremental rates of 20% and 30% based on payout return allowance levels of 5% and 15%, plus the long term bond rate. Analysis for this report also includes a supplemental after payout net rate of 6.50% based on price.

11 “The purposes of this Accord are … to provide that the Government of Newfoundland and Labrador can establish and collect resource revenues as if these resources were on land, within the province”, Article 2(e), The Atlantic Accord.

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

12

obligation to pay under Article 82 and that, therefore, Newfoundland & Labrador should

not be disadvantaged.

NL’s “ownership” right, in the context of Canada’s commitment to pay under the UN

Convention and the benefits enjoyed from the extension of rights beyond the EEZ, is

clearly a matter that remains to be worked out.

There are a multitude of issues still to be finalized respecting the meaning of key terms,

the implementation procedures to be put in place, and the response of individual

jurisdictions as they decide how the Article will interact with domestic fiscal structures.

To provide a sense of the magnitude of the economic impacts analysis below in section

4 is provided under two sets of fiscal terms – those for the United States Gulf of Mexico

and those for the Newfoundland & Labrador offshore, off Canada’s East Coast. For each

fiscal system the UN levy is assumed to be payable by the producer with two

alternatives – no credit and full credit – against domestic royalties. In all cases the levy is

assumed to be an allowed deduction for CIT.12

With respect to the “no credit” vs the “full credit” alternative, the full range and

everywhere in between are still real possibilities. For a jurisdiction that believes that it is

already capturing the full value of the economic rent, an offsetting credit could be

expected. An offset would also be expected where the levy is not viewed in isolation, but

rather is seen as a cost of doing business and earning income. If, however, the

jurisdiction perceived the levy solely as an erosion of the economic rent or believed that

it is currently not capturing the full economic rent, the levy might be applied on top of, or

in conjunction with an increase in, existing domestic levies. In deciding how to

accommodate the levy, a jurisdiction will be considering a balance between the

economic rent that is available for capture and the proportion of this rent that it wishes to

capture directly through royalties and indirectly through enhanced industry investment

activity and employment.

12 It would be highly unusual if this deductibility were not permitted. In jurisdictions where, for example, CIT

is not applied or where it is part of a production sharing agreement, one would still expect some sort of offsetting of costs as reflected in normal tax policy.

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

13

4. MODELING APPROACH: Analysis is based on the following assumptions in respect of Article 82. That: (a) the

levy is a royalty, not a tax; (b) the levy would be paid by producers, (c) production is

gross commercial production, (d) valuation excludes production used in connection with

extraction, such as re-injected water or gas; (e) site means the lease boundary; and (f)

value is measured in USD’s at the lease boundary.13

The impact of the levy ultimately depends on the success of exploration efforts and the

economic characteristics of individual projects, and on the fiscal systems of the

individual jurisdictions. The approach adopted for this report is to express these impacts

in terms of relative change from a reference case. The reference case incorporates

seven deep water oil fields. No gas fields are considered. Costs and field sizes for

shallow water fields are included in the table to illustrate the significance of the generally

higher cost of deep water developments. Frontier developments can experience even

higher costs.

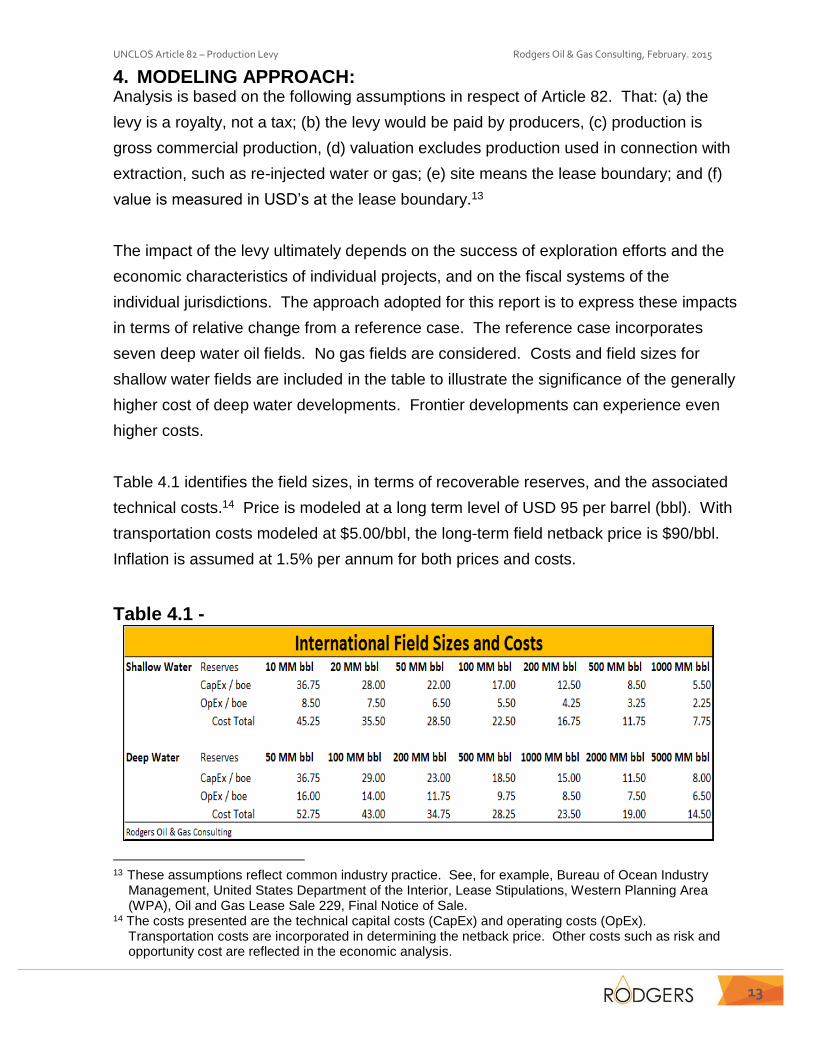

Table 4.1 identifies the field sizes, in terms of recoverable reserves, and the associated

technical costs.14 Price is modeled at a long term level of USD 95 per barrel (bbl). With

transportation costs modeled at $5.00/bbl, the long-term field netback price is $90/bbl.

Inflation is assumed at 1.5% per annum for both prices and costs.

Table 4.1 -

13 These assumptions reflect common industry practice. See, for example, Bureau of Ocean Industry

Management, United States Department of the Interior, Lease Stipulations, Western Planning Area (WPA), Oil and Gas Lease Sale 229, Final Notice of Sale.

14 The costs presented are the technical capital costs (CapEx) and operating costs (OpEx). Transportation costs are incorporated in determining the netback price. Other costs such as risk and opportunity cost are reflected in the economic analysis.

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

14

5. FISCAL IMPACTS: United States Gulf of Mexico Fiscal Terms:

Figures 5.1a.and 5.1b provide impact estimates of the levy on both investor ROR and

discounted NPV. Figure 5.1c breaks down the range of impacts in terms of the

government share.

Figure 5.1a -

Figure 5.1b –

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

15

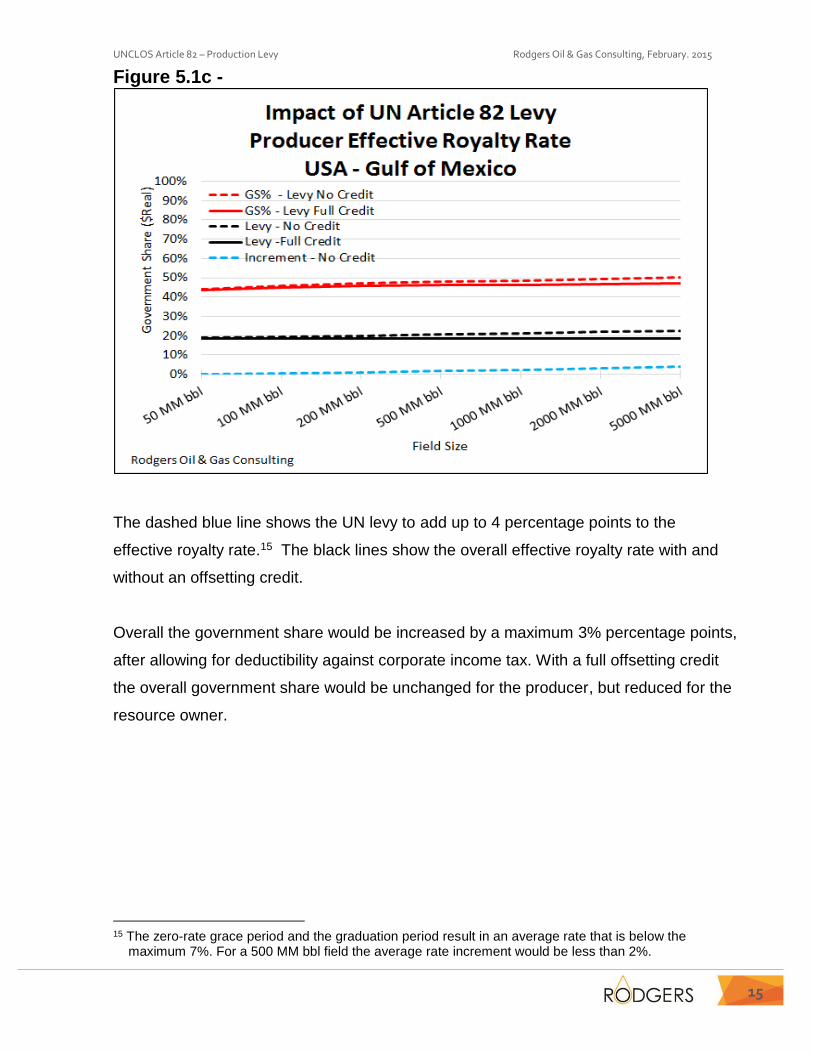

Figure 5.1c -

The dashed blue line shows the UN levy to add up to 4 percentage points to the

effective royalty rate.15 The black lines show the overall effective royalty rate with and

without an offsetting credit.

Overall the government share would be increased by a maximum 3% percentage points,

after allowing for deductibility against corporate income tax. With a full offsetting credit

the overall government share would be unchanged for the producer, but reduced for the

resource owner.

15 The zero-rate grace period and the graduation period result in an average rate that is below the

maximum 7%. For a 500 MM bbl field the average rate increment would be less than 2%.

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

16

Canada – Newfoundland & Labrador Fiscal Terms:

When compared to Figures 5.1a – 5.1c, Figures 5.2a - 5.2c show the impacts under the

Newfoundland & Labrador fiscal terms to be similar to those under the Gulf of Mexico

terms.

Figure 5.2a -

Figure 5.2b –

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

17

Figure 5.2c -

Compared with the GoM, the government share would be an average 5 percentage

points higher (53% vs. 48%) with the NL offshore fiscal terms. The average effective

royalty rate is 20.60% for NL and 18.78% for the GoM. The UN levy adds an average

effective royalty rate of 1.85%. The CIT rate offshore NL is 29%, compared to 35% in

the GoM.

For the oil field sizes considered, NL’s GS% would range from 45% - 58%, including the

levy. This compares to 44% to 50% under the GoM terms.

In terms of royalties, NL’s share would range from 8.5% to 33.6%. The comparable

range under the GoM terms is 19.00% to 22.6%.

Impact on Producer Net Cash Flow NCF): The average impact of the UN Article 82 levy

on producer NCF is in the order of $1 per bbl. The range under the NL terms is $0.09 -

$2.44. This compares to $0.08 - $2.24 with the GoM fiscal terms.

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

18

6. CONCLUDING COMMENTS: Analysis for this report shows the impact of the UN levy to be rather minimal, particularly

in the context of the risks and technical costs involved in offshore deep water oil and gas

development. This point of course is mute in the case where the levy is creditable

against other fiscal instruments.

It is important to keep in mind that $1/bbl - $2.50/bbl may not appear particularly

significant when compared to a price that is in the order of $90 - $100 per barrel.

However, $1/bbl represents $500 million in producer NCF for a 500 MM bbl

development and $2.50/bbl represents a NCF impact of $12 billion for a 5 billion barrel

development. This is certainly not insignificant!

It is the net cash flow that is most important. It is the net cash flow that represents the

return to investors and, at the same time, it is the net cash flow that is the ultimate

source of funds for future investments and production growth.

In conclusion, it is not difficult to see how resource owners might be reluctant to see a

reduction in their earnings if the UN levy were to be credited against domestic royalties.

Looked at in perspective however it appears that the UN levy ought to be seen as a cost

of doing business. Without Article 82, domestic royalties and other fiscal instruments

could not be applied beyond the 200 nautical mile zone. The levy therefore represents

the price that all parties agreed as reasonable for the right to benefit from extending the

coastal states’ jurisdiction beyond their exclusive economic zone into otherwise

international waters.

UNCLOS Article 82 – Production Levy Rodgers Oil & Gas Consulting, February. 2015

19

ABOUT RODGERS OIL & GAS CONSULTING

Rodgers Oil & Gas Consulting is a consultancy firm based in Edmonton

Alberta. The firm’s principal, Barry Rodgers, is an economist specializing

in upstream oil and gas fiscal system design and evaluation, including

international and inter-jurisdictional fiscal comparison. Rodgers Oil & Gas

maintains an extensive up-to-date data base containing fiscal

descriptions and related fiscal and economic assessments for some 500

fiscal regimes representing over 150 countries. More information can be

found at: http://www.bgrodgers.com/

Contact Information

Barry Rodgers 10409 – 134th St. Edmonton, Alberta, Canada Office: (780) 634 – 3405 Cell: (780) 905 – 3622 Email: [email protected] Website: http://www.bgrodgers.com/