Embed Size (px)

Citation preview

UNITED STATES DISTRICT COURT NORTHERN DISTRICT ILLINOIS

EASTERN DIVISION

SHAUN HOUSE, On Behalf of Himself and All Others Similarly Situated,

Plaintiff,

v.

AKORN, INC., JOHN N. KAPOOR, KENNETH S. ABRAMOWITZ, ADRIENNE L. GRAVES, RONALD M. JOHNSON, STEVEN J. MEYER, TERRY A. RAPPUHN, BRIAN TAMBI, and ALAN WEINSTEIN,

Defendants.

Case No. 1:17-cv-05018

CLASS ACTION

Hon. Thomas M. Durkin

CERTAIN PLAINTIFFS’ MEMORANDUM OF LAW IN OPPOSITION TO THEODORE H. FRANK’S RENEWED MOTION TO INTERVENE

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 1 of 41 PageID #:657

i

TABLE OF CONTENTS INTRODUCTION……………………………………………………………………………… 1 RELEVANT FACTUAL AND PROCEDURAL BACKGROUND ………………………….. 5 ARGUMENT…………………………………………………………………………………… 8 I. FRANK HAS NO DIRECT INTEREST TO SUPPORT INTERVENTION .................. 8

A. Frank’s Alleged Breach of Fiduciary Duty Arguments Are Without Merit …………………………………………………………………………..... 9

1. No Fiduciary Duties Are Owed to a Putative, Uncertified Class ……… 9

2. Voluntary Dismissal Prior to Class Certification Cannot Constitute a Breach of Fiduciary Duty…………………………………. 10 3. Bringing Suit Cannot Constitute a Breach of Fiduciary Duty …………. 13

B. Frank Has No Standing To Pursue A Direct Claim ……………………………. 13

1. Plaintiffs Complied with Trulia and Walgreens ……………………….. 13

2. The Supplemental Disclosures Were More Than Sufficient To Support The Mootness Fee Even If Court Approval Was Required ……………………………………………………………….. 15

a. “Plainly Material” Is Not the Applicable Standard ……………. 17 b. The Disclosures Were Nonetheless “Plainly Material” ……….. 17

i. Earlier Set of Projections Revised Downward During the Process …………………………………….. 19

ii. GAAP Reconciliations and Non-GAAP Line Items …… 20

iii. Fresenius’ Offers of Continuing Equity to Dr. Kapoor …………………………………………….. 22

iv. The Value of Derivative Claims Pending Against the Board ………………………………………………. 23

v. Issues Regarding JPM’s Potential Conflicts …………… 24

II. FRANK ALSO HAS NOT STATED A CLAIM FOR UNJUST ENRICHMENT ………………………………………………………………………… 25

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 2 of 41 PageID #:658

ii

III. FRANK DOES NOT HAVE STANDING TO INTERVENE UNDER RULE 24 ……. 26

A. Intervention of Right Under Rule 24(a)(2) …………………………………….. 26

1. Frank Lacks a Direct and Significant Interest …………………………. 26

2. Frank’s Interests Were Adequately Represented by the Parties ……………………………………………………………… 28

3. Frank’s “Interests” Will Not be Impaired ……………………………… 28

B. Permissive Intervention Under Rule 24(b) …………………………………….. 29

CONCLUSION ………………………………………………………………………………… 30

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 3 of 41 PageID #:659

iii

TABLE OF AUTHORITIES Adams v. USAA Cas. Ins. Co., 863 F.3d 1069 (8th Cir. 2017) ………………………………… 11 Altier v. Worley Catastrophe Response, LLC, No. 11-241c, 2012 U.S. Dist. LEXIS 6391 (E.D. La. Jan. 18, 2012) …………………………………….. 30 Armstrong v. Bd. of Sch. Dirs. of City of Milwaukee, 616 F.2d 305 (7th Cir. 1980) ………………………………………………………………. 17 Aron v. Crestwood Midstream Partners LP, No. 4:15-CV-1367, 2016 U.S. Dist. LEXIS 152427 (S.D. Tex. Oct. 14, 2016) ………………………………… 15 In re Atheros Communs., Inc. S’holder Litig., C.A. No. 6124-VCN, 2011 Del. Ch. LEXIS 36 (Del. Ch. Mar. 4, 2011) …………………………………………. 25 Back Doctors Ltd. v. Metro. Prop. & Cas. Ins. Co., 637 F.3d 827 (7th Cir. 2011) ………………………………………………………………. 11 Bond v. Utreras, 585 F.3d 1061 (7th Cir. 2009) ……………………………………….……. 8, 29 Boyer v. BNSF Ry. Co., 832 F.3d 699 (7th Cir. 2016) ………………………………………… 26 Bray v. Simon & Schuster, Inc., No. 4:14-CV-00258-NKL, 2014 U.S. Dist. LEXIS 86278 (W.D. Mo. June 25, 2014) ………………………………… 11 Buckhannon Board & Care Home, Inc. v. West Virginia Dep't of Health & Human Res., 532 U.S. 598 (2001) ………………………………………………………. 15 Buller v. Owner Operator Indep. Driver Risk Retention Group, Inc., 461 F. Supp. 2d 757 (S.D. Ill. 2006) ………………………………………………………. 11 Campbell-Ewald Co. v. Gomez, 136 S. Ct. 663 (2016) ……………………………………….. 12 CE Design Ltd. v. King Supply Co., 791 F.3d 722 (7th Cir. 2015) ……………………………. 30 In re Celera Corp. S’holder Litig., No. 6304-VCP, 2012 Del. Ch. LEXIS 66 (Del. Ch. Mar. 23, 2012) rev’d in part on other grounds, 2012 Del. LEXIS 658 (Del. Dec. 27, 2012) ……………… 22 Chambers v. NASCO, Inc., 501 U.S. 32 (1991) ……………………………………………….. 26 Cisneros v. Taco Burrito King 4, Inc., No. 13 CV 6968, 2014 U.S. Dist. LEXIS 33234 (N.D. Ill. Mar. 14, 2014) ………………………………….. 10

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 4 of 41 PageID #:660

iv

City of Livonia Emps.’ Ret. Sys. v. Wyeth, No. 07 Civ. 10329 (RJS), 2013 U.S. Dist. LEXIS 113658 (S.D.N.Y. Aug. 7, 2013) ………………..……………… 5, 16 Cruz-Bernal v. Keefe, No. 14 C 50178, 2015 U.S. Dist. LEXIS 90180 (N.D. Ill. July 13, 2015) …………………………………... 12 Culver v. City of Milwaukee, 277 F.3d 908 (7th Cir. 2002)…….……………………………… 11 Cummins v. Bickel & Brewer, No. 00 C 3703, 2001 U.S. Dist. LEXIS 12738 (N.D. Ill. Aug. 16, 2001) ………………………………….. 26 Dale M. v. Bd. of Educ. of Bradley-Bourbonnais High Sch. Dist. No. 307, 282 F.3d 984 (7th Cir. 2002) ………………………………………………………………. 26 Damasco v. Clearwire Corp., 662 F.3d 891 (7th Cir. 2011) ………………………………….. 12 Davis v. Cent. Vt. Pub. Serv. Corp., No. 5:11-cv-181, 2012 U.S. Dist. LEXIS 139186 (D. Vt. Sep. 27, 2012) ……………………………………. 15 In re Direxion ETF Tr., 279 F.R.D. 221 (S.D.N.Y. 2012) …………………….……………. 29, 30 In re El Paso S’holder Litig., 41 A.3d 432 (Del. Ch. 2012) …………………………………… 18 Felzen v. Andreas, 134 F.3d 873 (7th Cir. 1998) ………………………………………………. 17 In re First Cap. Holdings Corp. Fin. Prods. Sec. Litig., 33 F.3d 29 (9th. Cir. 1994)……………………………………………………………………………… 14 Flying J, Inc. v. Van Hollen, 578 F.3d 569 (7th Cir. 2009) ……………………………………. 30 Glasser v. Volkswagen of Am., Inc., 645 F.3d 1084 (9th Cir. 2011)…………………………… 14 In re GMC Pick-Up Truck Fuel Tank Prods. Liab. Litig., 55 F.3d 768 (3d Cir. 1995) ………………………………………………………………… 11 Goodyear v. Estes Exp. Lines, Inc., No. 1:06-CV-863, JDT-TAB, 2008 U.S. Dist. LEXIS 18694 (S.D. Ind. Mar. 10, 2008) ………………………………….. 14 In re Google Referrer Header Privacy Litig., 87 F. Supp. 3d 1122 (N.D. Cal. 2015) ……………………………………………………… 4 Grok Lines, Inc. v. Paschall Truck Lines, Inc., No. 14 C 08033, 2015 U.S. Dist. LEXIS 124812 (N.D. Ill. Sep. 18, 2015) …………………………………. 12 Hammond v. City of Junction City, 126 F. App’x 886 (10th Cir. 2005) ………………………. 10

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 5 of 41 PageID #:661

v

Heartwood, Inc. v. United States Forest Serv., 316 F.3d 694 (7th Cir. 2003) ………………… 26 Hickman v. Wells Fargo Bank N.A., 683 F. Supp. 2d 779 (N.D. Ill. 2010) …………………… 26 Hill v. State St. Corp., 794 F.3d 227 (1st Cir. 2015)…………………………………………… 30 Hinds Cty., Miss. v. Wachovia Bank N.A., 790 F. Supp. 2d 125 (S.D.N.Y. 2011) …………...... 11 Houseman v. Sagerman, Civil Action No. 8897-VCG, 2014 Del. Ch. LEXIS 55 (Ch. Apr. 16, 2014) ……………………………………………... 23 Howell v. Mgmt. Assistance, Inc., 519 F.3d 83 (S.D.N.Y. 1981) ……………………………… 15 J. I. Case Co. v. Borak, 377 U.S. 426 (1964) ………………………………………………….. 16 Jackson v. United States, 881 F.2d 707 (9th Cir. 1989) ……………………………………….. 26 In re Johnson & Johnson Derivative Litig., 900 F. Supp. 2d 467 (D.N.J. 2012) ……………… 27 Knisley v. Network Assocs., 312 F.3d 1123 (9th Cir. 2002) …………………………………… 16 Kopet v. Esquire Realty Co., 523 F.2d 1005 (2d Cir. 1975) …………………………………… 15 Kurz v. Fidelity Mgmt. & Res. Co., No. 07-CV-592-JPG, 2007 U.S. Dist. LEXIS 74267 (S.D. Ill. Oct. 4, 2007) …………………………………….. 11 Lantern Bus. Credit v. Alianza Trinity Dev. Grp., No. 1:16cv107, 2016 U.S. Dist. LEXIS 153462 (W.D.N.C. Oct. 8, 2016) …………………………………. 27 League of United Latin Am. Citizens v. Wilson, 131 F.3d 1297 (9th Cir. 1997) ………………. 30 In re Lear Corp. S’holder Litig., 926 A.2d 94 (Del. Ch. 2007) ……………………………….. 18 Lewis v. Anderson, 477 A.2d 1040 (Del. 1984) ……………………………………………….. 23 Ligas v. Maram, 478 F.3d 771 (7th Cir. 2007) ………………………………………………… 29 Maric Capital Master Fund, Ltd. v. Plato Learning, Inc., 11 A.3d 1175 (Del. Ch. 2010)……………………………………………………………… 20 In re Massey Energy Co. Derivative & Class Action Litig., No. 5430-VCS, 2011 Del. Ch. LEXIS 83 (Ch. May 31, 2011) ……………………………. 24 Meridian Homes Corp. v. Nicholas W. Prassas & Co., 683 F.2d 201 (7th Cir. 1982)………… 27

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 6 of 41 PageID #:662

vi

Merritt v. Colonial Foods, Inc., 505 A.2d 757 (Del. Ch. 1986) ……………………………….. 23 Mills v. Elec. Auto-Lite Co., 396 U.S. 375 (1970) …………………………………………. 15, 17 Moore v. Verizon Commc’ns Inc., No. C 09-1823 SBA, 2013 U.S. Dist. LEXIS 15609 (N.D. Cal. Feb. 5, 2013)…………………………………… 28 In re Motor Fuel Temperature Sales Practices Litig., MDL No. 1840, 2016 U.S. Dist. LEXIS 113406 (D. Kan. Aug. 24, 2016) …………………………………. 4 In re Netsmart Techs. Inc. S’holders Litig., 924 A.2d 171 (Del. Ch. 2007) …………………… 19 In re Orchard Enters., Inc., 88 A.3d 1 (Del. Ch. 2014) ……………………………………….. 23 Ougle v. Boehringer Ingelheim Pharm., Inc., No. MDL No. 2385, 2015 U.S. Dist. LEXIS 137699 (S.D. Ill. Oct. 8, 2015) …………………………………… 29 Parshall v. Stonegate Mortg. Corp., No. 1:17-cv-00711-JMS-DML, 2017 U.S. Dist. LEXIS 129977 (S.D. Ind. Aug. 11, 2017)………………………………… 15 Pearson v. NBTY, Inc., No. 11 C 7972, 2015 U.S. Dist. LEXIS 133706 (N.D. Ill. Oct. 1, 2015) …………………………………………………………………….. 30 Pharm. Research & Mfrs. Of Am. v. Comm'r, 201 F.R.D. 12 (D. Me. 2001) …………………. 28 Pitts v. Terrible Herbst, Inc., 653 F.3d 1081 (9th Cir. 2011) ………………………………….. 12 In re PNB Holding Co. S’holders Litig., No. 28-N, 2006 Del. Ch. LEXIS 158 (Del. Ch. Aug. 18, 2006)…………………………………………………………………… 20 Poertner v. Gillette Co., 618 F. App’x 624 (11th Cir. 2015) ………………………………….. 4 Primax Recoveries, Inc. v. Sevilla, 324 F.3d 544 (7th Cir. 2003)……………………………… 12 RBC Capital Mkts., LLC v. Jervis,129 A.3d 816 (Del. 2015) …………………………………. 2 Retiree Support Grp. v. Contra Costa Cty., 315 F.R.D. 318 (N.D. Cal. 2016)………………… 29 Revlon, Inc. v. MacAndrews & Forbes Holdings, Inc., 506 A.2d 173 (Del. 1985) ……………. 23 Reynolds v. Ben. Nat'l Bank, 288 F.3d 277 (7th Cir. 2002) ……………………………………. 15 Robert F. Booth Tr. v. Crowley, 687 F.3d 314 (7th Cir. 2012)………………………………… 27 In re Rural Metro Corp. S'holder Litig., 88 A.3d 54 (Del. Ch. 2014) …………………………. 25

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 7 of 41 PageID #:663

vii

In re Schering-Plough/Merck Merger Litig., No. 09-1099, 2010 U.S. Dist. LEXIS 29121 (D.N.J. Mar. 26, 2010) ……………………………………. 15 Silverman v. Motorola Sols., Inc., 739 F.3d 956 (7th Cir. 2013) ……………………………… 30 Smith v. Kerry Chevrolet, Inc., No. 06-180-JGW, 2008 U.S. Dist. LEXIS 46380 (E.D. Ky. June 13, 2008) ………………………………….. 11 Spangler v. Pasadena City Bd. of Educ., 552 F.2d 1326 (9th Cir. 1977)………………………. 29 Standard Fire Ins. Co. v. Knowles, 568 U.S. 558 (2013) ……………………………………… 12 Stilz v. Standard Bank & Tr. Co., No. 10 C 1996, 2010 U.S. Dist. LEXIS 131968 (N.D. Ill. Dec. 14, 2010) ………………………………… 11 In re Sw. Airlines Voucher Litig., 799 F.3d 701 (7th Cir. 2015) ………………………………. 4 Tellabs, Inc. v. Makor Issues & Rights, Ltd., 551 U.S. 308 (2007) ……………………………. 4 In re TIBCO Software Inc. S’holder Litig., No. 10319, 2015 Del. Ch. LEXIS 265 (Del. Ch. Oct. 20, 2015) …………………………………………………………………… 25 In re Trulia, Inc. Stockholder Litig., 129 A.3d 884 (Del. Ch. 2016) …………….………… passim Vollmer v. Publrs. Clearing House, 248 F.3d 698 (7th Cir. 2001) …………………………….. 29 In re Walgreen Co. Stockholder Litig., 832 F.3d 718 (7th Cir. 2016)……………………… passim White v. Nat’l Football League, 756 F.3d 585 (8th Cir. 2014) ………………………………… 11 Wis. Educ. Ass'n Council v. Walker, 705 F.3d 640 (7th Cir. 2013) ……………………………. 26 Wolschlager v. Law Offices of Mitchell D. Bluhm & Assocs., LLC, No. 1:17-CV-00033, 2017 U.S. Dist. LEXIS 83448 (W.D. Mich. May 18, 2017)………… 12 In re Xoom Corp. S’holder Litig., No. 11263-VCG, 2016 Del. Ch. LEXIS 117 (Aug. 4, 2016) ……………………………………………………………………………… 17

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 8 of 41 PageID #:664

viii

STATUTES, RULES AND MISCELLANEOUS 15 U.S.C. §78u-4(a) ……………………………………………………………………………. 15 17 C.F.R. §244.100 …………………………………………………………………………….. 21 FED. R. CIV. P. 23…………………………………………………………………………… passim FED. R. CIV. P. 23.1 ……………………………………………………………………………. 1 FED. R. CIV. P. 24 ………………………………………………………………………….. passim Ill. R. Prof’l Conduct R. 5.6 …………………………………………………………………… 1 Restatement (Third) of the Law Governing Lawyers §99 cmt. l (Am. Law Inst. 2000) ……… 10 Hall v. Berry Petroleum Co., No. 8476-VCG, Tr. at 13:7-10 (Del. Ch. Dec. 4, 2014) ……….. 19 Ted Frank – Biography, CEI.org https://cei.org/content/ted-frank (last visited May 16, 2018) ………………………………. 4 What We Do, SEC.gov (2013), https://www.sec.gov/Article/whatwedo.html#laws (last visited May 16, 2018) ………………………………………………………………… 21

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 9 of 41 PageID #:665

Plaintiffs Shaun House, Demetrios Pullos and Robert Carlyle1 submit this memorandum in

opposition to Theodore H. Frank’s (“Frank”) Renewed Motion To Intervene.

INTRODUCTION

Putative intervenor, Frank, previously argued that, as a shareholder of Akorn, Inc. (“Akorn”),

he has the right to come into this case to protect Akorn. This Court correctly rejected that argument

because the claim Frank sought to assert belongs only to the corporation, Akorn, and not its

shareholders directly. As such, any alleged claim for waste or the like can only be brought by Frank

in a shareholder derivative action, which this Court further found Frank had neither brought nor

could likely pursue due to the demand requirement of FED. R. CIV. P. 23.1 and the Illinois business

judgment rule. See, generally, Memorandum Opinion and Order (N.D. Ill. Nov. 21, 2017), Dkt. No.

81 (“Order”).2 Given another chance by this Court, Frank nevertheless initially made the same

arguments previously overruled by the Court. Plaintiffs noted this in their opposition, and made clear

that the arguments had not improved with age. In his reply, Frank seemingly abandoned his attempt

to side-step the law that a shareholder has no right to pursue a claim belonging to a corporation in

which he is a shareholder.3 Instead, Frank offered new theories to justify his intervention to object to

Plaintiffs’ counsel being compensated for pressing for, and obtaining, certain additional disclosures

1 There were seven actions filed by Plaintiffs Robert Berg, Jorge Alcarez, House, Carlyle, Sean Harris, and Pullos, respectively. Defendants agreed to provide all of the Plaintiffs’ counsel with a payment of $322,500 in attorneys’ fees and expenses. Dkt. No. 56 at 6. On January 3, 2018, Levy & Korsinsky, LLP, counsel for plaintiff Alcarez, withdrew and disclaimed all rights to attorneys’ fees. Dkt. No. 86. Similar withdrawals were filed by Rigrodsky & Long, P.A., counsel for plaintiff Berg, Dkt. No. 92, and DiTommaso Lubin Austermuehle, P.C., local counsel for several plaintiffs. Dkt. No. 89. Faruqi & Faruqi LLP, counsel for plaintiff Harris, also disclaimed their fee. Thus, this opposition is only being filed on behalf of Plaintiffs House, Pullos and Carlyle and their counsel, Kahn Swick & Foti, LLC, Monteverde & Associates PC, and Brower Piven, A Professional Corporation, who seek the right to the agreed-upon fees. 2 Unless otherwise noted, references to “Dkt. No. _” refer to Berg v. Akorn, Inc., No. 1:17-cv-05016, because the relevant documents have been filed there, and all citations and quotation marks are omitted. 3 Frank has also clearly abandoned his other overreaching earlier request for an injunction against Plaintiffs’ counsel filing any future class action cases here or elsewhere, a request for relief that, among other things, likely runs afoul of Illinois Rule of Professional Conduct 5.6.

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 10 of 41 PageID #:666

2

from Defendants in connection with the Akorn/Fresenius Kabi AG (“Fresenius”) merger (the

“Merger”).

This time, Frank claims Plaintiffs and their counsel owed fiduciary duties to the putative class

on whose behalf certain of the complaints in the actions were brought and that by dismissing those

claims, they have breached those fiduciary duties and/or been unjustly enriched. Based on these

theories, Frank claims he is entitled to intervene under FED. R. CIV. P. 24 (“Rule 24”). These

arguments, however, are, as a matter of law and fact, as meritless as his attempt to usurp Akorn’s

claim that he cannot assert. As demonstrated below, Plaintiffs’ counsel’s successful effort to compel

additional disclosures by Akorn resulted in Akorn mooting their claims. Following the guidelines

adopted by the Seventh Circuit, Plaintiffs voluntarily dismissed their actions and then negotiated a

reasonable attorneys’ fee from Akorn as recompense for their efforts. Akorn, in its business

judgment, concluded that payment was appropriate and the amount commensurate with the result

achieved. Importantly, the result achieved did not necessitate certification of a class, no releases –

class or individual – were exchanged, and no plaintiff or putative class member relinquished any

rights in connection with the dismissal of the actions or the payment of the agreed-upon fee.

Plaintiffs and their counsel’s conduct were completely consistent with the roadmap set forth in In re

Trulia, Inc. Stockholder Litig., 129 A.3d 884, 898 (Del. Ch. 2016), which was adopted in this Circuit

in In re Walgreen Co. Stockholder Litig., 832 F.3d 718 (7th Cir. 2016). This Frank concedes.

Frank’s argument that by dismissing the actions, Plaintiffs and their counsel breached their

fiduciary duties to absent class members that they undertook by filing the actions as putative class

actions is wrong. Because the claims asserted by Plaintiffs were mooted by the disclosures Akorn

voluntarily agreed to make, there was nothing left to litigate. Presumably, Frank would not have

Plaintiffs continue litigation after their complaints have been voluntarily satisfied by Defendants.

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 11 of 41 PageID #:667

3

This is the reason that the Federal Rules of Civil Procedure were amended in 2003 to permit

dismissals of putative class actions without notice to class members as required by FED. R. CIV. P.

23(e) (“Rule 23(e)”) where the class was not yet certified and the dismissal would not bind or release

any absent class members’ claims. Frank ignores this rule change and the Advisory Committee

comments on the reasons for the amendment, and cites cases preceding the 2003 amendment or that

are factually distinguishable. Because Plaintiffs and their counsel scrupulously followed the Federal

Rules and Seventh Circuit case law, Frank’s attempt to argue non-existent Rule 23 jurisprudence

must fail, and the Court should decline his invitation to ignore those controlling authorities.

Moreover, Frank argues, on the one hand, that Plaintiffs breached their fiduciary duties

because there were valuable claims that Plaintiffs abandoned, but then, on the other hand, that the

claims Plaintiffs alleged should never have been asserted at all and, accordingly, the result Plaintiffs

achieved had no value. Frank, however, cannot have it both ways, and here, he cannot have it either

way. If some valuable claim was abandoned that was not satisfied by Akorn’s mooting disclosures,

Frank has failed to identify what claim was left to vindicate. If the claims asserted had no value in

the first place and, accordingly, Akorn mooting those claims had no value, then Frank has no

personal right or interest in the dismissal of the actions. For the same reasons as this Court

previously held, he has no direct interest or injury resulting from Akorn’s additional disclosures or

payment by Akorn of the agreed-upon fee.

Finally, Frank offers a new “unjust enrichment” theory based on the payment of the agreed-

upon attorneys’ fee. This theory as a basis for his intervention is unsupportable by fact or law. First,

Akorn chose to pay the mootness fee in its broad business judgment after the actions were dismissed,

so Akorn made a determination of the value of the additional disclosures on account of Plaintiffs’

actions, which is entitled to great deference. Second, even if Akorn had not made its own business

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 12 of 41 PageID #:668

4

judgment that the agreed-upon mootness fee was appropriate, the disclosures were material and

provided value to Akorn’s shareholders that would have supported such a fee in a litigated setting.

Third, Frank cannot even approach meeting the elements for a claim by him for unjust enrichment.

Rather, even if a claim for unjust enrichment lay, that claim would belong solely to Akorn. Frank’s

attempt to use his new unjust enrichment theory as a vehicle to intervene is no more than a disguised

effort to, once again, usurp a right that belongs only to Akorn, not its shareholders, that can only be

brought by Akorn or by a shareholder through a shareholder derivative action. Thus, Frank’s new

theories simply bring us full circle.

Frank and his supporters’ dislike of the plaintiffs’ securities bar and his speculation

concerning Plaintiffs and their counsel’s motives and societal value is simply irrelevant to the issues

before this Court.4 The issues before this Court must turn on cognizable evidence and applicable law.

Putting aside Frank’s bellicose unsupported and entirely irrelevant (and untrue) ad hominin attacks

on Plaintiffs and their counsel, which reflect a political and philosophical agenda appropriately

addressed to Congress and not this Court,5 Frank has offered no facts or law to support any of his

4 Frank’s dislike for the plaintiffs’ securities bar and its efforts are not shared by the Supreme Court, which has long and repeatedly “recognized that meritorious private actions to enforce federal antifraud securities laws are an essential supplement to criminal prosecutions and civil enforcement actions brought … by the [DOJ] and the [SEC].” Tellabs, Inc. v. Makor Issues & Rights, Ltd., 551 U.S. 308, 313 (2007). 5 Indeed, Frank is part of, and supported by, a Libertarian political action organization, the Competitive Enterprise Institute. See https://cei.org/content/ted-frank. Ironically, or perhaps tellingly, Frank, who claims here to be protecting absent Akorn investors, works for an organization whose webpage states that one of its main goals is to mount “court challenges to . . . the Dodd-Frank Act,” a statute adopted in the wake of the 2007-08 financial crisis to protect investors through, inter alia, enhanced public disclosure. It may then not be surprising that Frank’s view is additional disclosures to assist investors in exercising their corporate franchise are of no value since his organization’s goals are to reduce (or even eliminate) the amount of disclosure to shareholders. Frank’s cause, however, has understandably been met with little enthusiasm by the courts. See, e.g., Poertner v. Gillette Co., 618 F. App’x 624, 629 (11th Cir. 2015) (rejecting Frank’s contention that “nonmonetary relief was illusory.”); In re Sw. Airlines Voucher Litig., 799 F.3d 701, 704 (7th Cir. 2015) (affirming approval despite objection by Frank that settlement is “too generous to class counsel.”); In re Motor Fuel Temperature Sales Practices Litig., MDL No. 1840, 2016 U.S. Dist. LEXIS 113406, at *77 (D. Kan. Aug. 24, 2016) (rejecting Frank’s objection that court failed to “focus on lack of benefit to the class[.]”); In re Google Referrer Header Privacy Litig., 87 F. Supp. 3d 1122, 1128 (N.D. Cal. 2015) (overruling Frank’s objection that “only acceptable benefit is some form of monetary

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 13 of 41 PageID #:669

5

arguments and, indeed, as demonstrated, the facts and law here defeat every argument he has made.6

RELEVANT FACTUAL AND PROCEDURAL BACKGROUND

On April 24, 2017, Akorn and Fresenius announced that they had entered into an agreement

(the “Merger Agreement”), pursuant to which Akorn would be acquired by affiliates of Fresenius.

On May 22, 2017, Akorn filed a preliminary proxy statement (the “Preliminary Proxy”) in

connection with the Merger. Thereafter, five putative class actions were filed in federal court in New

Orleans and one individual action in federal court in Illinois7 challenging the disclosures made in the

Preliminary Proxy under §§14(a) and 20(a) of the Securities Exchange Act of 1934 against, among

others, Akorn and its Board of Directors (the “Board”).

On June 14, 2017, certain plaintiffs sent a letter to Akorn demanding that it remedy certain

disclosure deficiencies in the Preliminary Proxy. On June 15, 2017, Akorn filed a definitive proxy

statement (the “Definitive Proxy”), which addressed several of the major disclosure deficiencies

identified in the various complaints and in the demand letter. On June 20, 2017, Frank purchased

1000 shares of Akorn. See Dkt. No. 82-1 at ¶14. On June 26, 2017, Plaintiffs filed a targeted motion

for preliminary injunction that raised two narrow disclosure issues that were not addressed in the

Definitive Proxy. On June 27, 2017, Plaintiffs’ counsel received and reviewed confidential

discovery from Akorn, including Board meeting minutes and financial analyses performed by J.P.

Morgan (“JPM”), the Board’s financial advisor. On June 28, 2017, Plaintiffs sent a second demand

letter to Akorn identifying disclosure deficiencies either not addressed in the Definitive Proxy or that

compensation.”); City of Livonia Emps.’ Ret. Sys. v. Wyeth, No. 07 Civ. 10329 (RJS), 2013 U.S. Dist. LEXIS 113658, at *15 (S.D.N.Y. Aug. 7, 2013) (objection led by Frank “does not seem grounded in the facts of this case, but in [objector’s] and [Frank’s] objection to class actions generally.”). 6 Given that Frank has repeatedly changed the focus of his arguments after Plaintiffs have demonstrated they lacked merit, Plaintiffs reserve the right to file a surreply memorandum if Frank once again offers new theories in his reply papers. 7 The individual, Carlyle case, was subsequently voluntarily dismissed in Illinois and re-filed in Louisiana, but still as an individual action.

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 14 of 41 PageID #:670

6

had arisen in discovery.

In response, Defendants sought to transfer the actions to this Court. After a flurry of briefing,

on or about July 5, 2017, Akorn agreed to make two of the material disclosures identified in

Plaintiffs’ motion for preliminary injunction and/or second demand letter, and Plaintiffs agreed to

withdraw that motion. On the same day, the Louisiana court transferred the actions to this Court. On

July 10, 2017, Akorn filed a Form 8-K (the “8-K”) that included the agreed-upon supplemental

disclosures (together with the disclosures included in the Definitive Proxy, the “Supplemental

Disclosures”). Having secured the information that they considered most material, pursuant to the

procedure outlined in Trulia and Walgreens, on July 14, 2017, Plaintiffs dismissed their cases

without prejudice to themselves or the putative class. No settlement – individual or class – was

reached. No claims – individual or class – were released or relinquished. Plaintiffs’ counsel only

reserved this Court’s jurisdiction for seeking a mootness fee under the caption of the Berg case –

again, as contemplated by Trulia/Walgreens.

Although all such voluntary dismissals were self-executing, the parties nonetheless waited

until after this Court entered the stipulated dismissal of the last case on July 25, 2017 before

broaching the subject of a mootness fee with Defendants. Almost six weeks later, on September 7,

2017, after arms’-length negotiations between sophisticated parties – and, as Frank admits, in a

rational exercise of its corporate business judgment, see Dkt. No. 83 at 1 – Akorn agreed to pay,

without the need for court-intervention, the fee. On September 15, 2017, the remaining parties

submitted a public stipulation and proposed order closing the Berg matter that disclosed both the

agreement and the amount of the fee and expense reimbursement. Dkt. No. 56. Frank admits Trulia

is the law of this Circuit under Walgreens, see Dkt. No. 82-1 at ¶62, and Trulia lays out a clear

roadmap for non-settlement, mootness dismissals of uncertified putative class actions. Although

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 15 of 41 PageID #:671

7

Plaintiffs scrupulously followed Trulia, three days later, on September 18, 2017, Frank moved to

intervene. Dkt. No. 57.

On November 21, 2017, after briefing on the motion, the Court issued its Order, stating:

Thus, the court in Trulia favorably contemplated the very scenario that has arisen in this case. And Plaintiffs’ counsel have taken the advice of the court in Trulia and dismissed this case without prejudice, such that the class claims are no longer at issue. The court in Trulia also contemplated that an objecting shareholder like Frank would bring a “separate litigation” to challenge the reasonableness of any settlement payment. Instead, Frank seeks to intervene in a case that has settled.

Order at 6. The Court also found that Rule 24 “requires that a potential intervenor demonstrate his

‘interest’ in the case,” Order at 6, and Frank “has not, and – it appears to the Court – cannot, identify

such an interest.” Id. First, “Frank’s injury from Akorn’s payment of the settlement [ ] can only be

derivative of Akorn’s” and “Berg’s case was not filed as a derivative suit, and Frank does not claim

to have complied with any of the[ ] procedures” of a derivative suit. Id. at 7. Second, Frank’s claim

would be “barred by the business judgement rule” as he admits that “Akorn’s decision to settle” was

“‘rational.’” Id. Further, if Frank claims his interest is because he was a class member, the Court

found that is not sufficient because the “class claims have been dismissed without prejudice.” Id. The

Court also noted that “the fact that Plaintiffs[ ] have dismissed their class claims without prejudice,

and that Defendants have already reached an agreement with Plaintiffs’ counsel, makes it difficult (if

not impossible) to see how this case remains within the ambit of Rule 23, or any other authority of

the Court.” Id. at 9. Further, the Court found that disgorgement of the fee would not be appropriate

because the claims were not “meritless.” Id. at 10. Although denying Frank’s motion, the Court

granted leave to refile it, but ordered that he “focus on the issues identified by the Court … regarding

his interest.” Id.

Frank refiled his motion on December 8, 2017, Dkt. No 82, but notwithstanding the Court

generously granting him a second bite at the apple, Frank’s opening brief on his Renewed Motion to

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 16 of 41 PageID #:672

8

Intervene and supporting papers simply rehashed the same shareholder derivative claims that the

Court had already rejected in its Order. Counsel for Plaintiffs filed their opposition to his motion on

December 22, 2018, Dkt. No. 84, pointing out that Frank failed to address any of the shortcomings

identified by the Order.

Upon reviewing the arguments made in the opposition, Frank refocused his reply brief on

new arguments, Dkt. No. 88, which are equally meritless in fact and in law. Frank now argues he has

a direct claim, and therefore, standing to intervene, because Plaintiffs and/or their counsel breached

fiduciary duties to absent members of the uncertified class by dismissing their actions and

abandoning some unidentified claims they should have pursued, see Renewed Motion, at 3, or, in the

alternative, by filing their actions in the first place. See id. at 2. To support this argument, he again,

resorts to a misapplication of Trulia and unsupported, incorrect and, indeed, irrelevant arguments

about the quality of the Supplemental Disclosures obtained by Plaintiffs and their counsel. Id. at 8-

12. He also argues that Plaintiffs’ counsel are unjustly enriched by the payment of the mootness fee,

see id. at 2-3, a claim, if it even exists, belongs to Akorn, and must be pursued by Akorn through a

shareholder derivative action. Thus, Frank’s third round of new arguments for intervention fair no

better than his prior rounds of arguments.

ARGUMENT

I. FRANK HAS NO DIRECT INTEREST TO SUPPORT INTERVENTION Regardless of whether intervention is under Rule 24(a) or Rule 24(b), the Seventh Circuit

requires that, “at some fundamental level[,] the proposed intervenor must have a stake in the

litigation.” Bond v. Utreras, 585 F.3d 1061, 1070 (7th Cir. 2009). Frank simply does not possess a

direct cause of action against Plaintiffs or their counsel and, thus, he has no “stake” in this litigation.

Under Trulia, Mr. Frank’s sole recourse to object to the mootness fee here is to bring a derivative

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 17 of 41 PageID #:673

9

action in a separate proceeding – one that this Court has already determined he does not have

standing to bring. Nor can Frank create a Rule 24 “stake” in this litigation by inventing a direct

cause of action for breach of fiduciary duty where none exists. No direct fiduciary duties are owed to

a putative, uncertified class that bars dismissal of an action based on the mootness of the claims

asserted or a pre-certification individual settlement that does not bind class members, and there is no

fiduciary duty to not bring a suit on behalf of a class. Similarly, Frank cannot state a direct claim for

unjust enrichment for the same reasons that his initial motion to intervene was denied. If anyone has

been unjustly enriched, they were enriched only at the expense of Akorn, not its shareholders, and

that claim can only be brought derivatively.

A. Frank’s Alleged Breach of Fiduciary Duty Arguments Are Without Merit

As this Court previously found that Frank’s arguments for intervention were based on claims

belonging to Akorn, and that he had failed to demonstrate standing to bring the derivative claims, in

his renewed motion, Frank attempts to rebrand his derivative claims as direct causes of action against

Plaintiffs and their counsel for breach of fiduciary duty. That attempt fails.

1. No Fiduciary Duties Are Owed to a Putative, Uncertified Class

As an initial matter, Frank neglects to mention that the action brought by plaintiff Carlyle

was brought as an individual action and always remained so. This conveniently omitted fact, which

does not fit with Frank’s overarching political agenda, defeats Frank’s breach of fiduciary duty

arguments ab initio. Because plaintiff Carlyle never sought to represent any class, but only his own

interests, neither he nor his counsel could possibly have owed any duties to any class. Indeed, in the

context of alleged inadequate disclosures, remedying those deficiencies for any individual

complaining shareholder has the effect of remedying them for all shareholders without resort to the

class action device. For this reason alone, Frank’s entire fiduciary duty argument fails, as Defendants

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 18 of 41 PageID #:674

10

could have issued the Supplemental Disclosures in response to, and agreed to pay the same mootness

fee, to plaintiff Carlyle alone.

Putting aside Frank’s convenient omission, the remaining Plaintiffs and their counsel, who

brought putative class actions, also owed no fiduciary duties to any putative, uncertified class

because of its uncertified nature. As Judge Zagel explained in Cisneros v. Taco Burrito King 4, Inc.,

No. 13 CV 6968, 2014 U.S. Dist. LEXIS 33234 (N.D. Ill. Mar. 14, 2014):

While Plaintiffs attorneys[ ] may have intended to include Plaintiffs[’] claim in[ ] a larger class action, they, first and foremost, have a fiduciary duty to act in the best interests of Plaintiff-not a potential class of plaintiffs. That remains true even when Plaintiff[’]s best interests are satisfied by a complete offer of settlement, removing controversy from the case and possibly preventing an action from moving forward as a class action.

Id., at *11. See also Restatement (Third) of the Law Governing Lawyers §99 cmt. l (Am. Law Inst.

2000) (“[P]rior to certification, only those class members with whom the lawyer maintains a personal

client-lawyer relationship are clients.”); Hammond v. City of Junction City, 126 F. App’x 886, 889

(10th Cir. 2005) (“no attorney-client relationship between the attorney and [prospective class

member] until the class was certified”).

2. Voluntary Dismissal Prior to Class Certification Cannot Constitute a Breach of Fiduciary Duty

Whether or not Plaintiffs or their counsel owed fiduciary duties to members of the putative,

uncertified class at the time the cases were filed, they could not have breached those duties by

dismissing their mooted, individual claims without prejudice, as the 2003 amendment to Rule 23(e)

specifically changed the law to require court approval of the voluntary dismissal or settlement of a

certified class action only. The Advisory Committee comment to the 2003 amendment explains:

Rule 23(e)(1)(A) resolves the ambiguity in former Rule 23(e)’s reference to dismissal or compromise of a “class action.” That language . . . was [ ] read to require court approval of settlements with putative class representatives that resolved only individual claims. The new rule requires approval only if the claims, issues, or

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 19 of 41 PageID #:675

11

defenses of a certified class are resolved by a settlement, voluntary dismissal, or compromise. Since the 2003 amendment, courts have consistently recognized that settlements and

voluntary dismissals that occur before class certification, as here, are plainly permissible and because

of this, no breach of any claimed duty to absent class members could occur when plaintiffs

voluntarily dismiss their mooted actions. See, e.g., Order at 9-10 (“Walgreens applied a standard for

approval of class settlements under Rule 23, which is not at issue here”); White v. Nat’l Football

League, 756 F.3d 585, 591 (8th Cir. 2014) (Rule 23(e) does not apply if the claims are not of a

certified class).8 Accordingly, neither Plaintiffs nor their counsel could have violated any alleged

duty by exercising their statutory right to dismiss their mooted claims without prejudice in uncertified

actions, and any argument to the contrary conflicts with Rule 23(e)’s plain language.9

8 See also Adams v. USAA Cas. Ins. Co., 863 F.3d 1069, 1081-83 (8th Cir. 2017) (“the overwhelming majority of courts have held that when no class has been certified, voluntary dismissal of a putative class action is governed not by Rule 23 but by Rule 41”); Kurz v. Fidelity Mgmt. & Res. Co., No. 07-CV-592-JPG, 2007 U.S. Dist. LEXIS 74267, at *4 (S.D. Ill. Oct. 4, 2007) (same); Stilz v. Standard Bank & Tr. Co., No. 10-1996, 2010 U.S. Dist. LEXIS 131968, at *16 (N.D. Ill. Dec. 14, 2010) (quoting Advisory Committee note to Rule 23(e)(1)(A)); Buller v. Owner Operator Indep. Driver Risk Retention Group, Inc., 461 F. Supp. 2d 757, 764 (S.D. Ill. 2006) (settlements or voluntary dismissals before class certification are outside of Rule 23); Bray v. Simon & Schuster, Inc., No. 4:14-CV-00258-NKL, 2014 U.S. Dist. LEXIS 86278, at *7 (W.D. Mo. June 25, 2014) (“putative class will not be harmed by dismissal of the class claims without prejudice, and notice … is not necessary”); Smith v. Kerry Chevrolet, Inc., No. 06-180-JGW, 2008 U.S. Dist. LEXIS 46380, at *4 (E.D. Ky. June 13, 2008) (same); Hinds Cty., Miss. v. Wachovia Bank N.A., 790 F. Supp. 2d 125, 132-33 (S.D.N.Y. 2011) (prior to certification, court approval is not required to compromise individual claims of potential class members); 7B Wright, Miller, & Kane, Federal Practice & Procedure §1797 (3d ed. 2017) (“[S]ettlements or voluntary dismissals that occur before class certification are outside the scope of subdivision [Rule 23](e)”). 9 In contrast, two of the cases Frank cites for his proposition that some fiduciary duty is owed to an uncertified class once a complaint is filed both preceded the 2003 amendment, which specifically provides for the dismissal of pre-certification class actions without court approval, and are, therefore, no longer good law. See In re GMC Pick-Up Truck Fuel Tank Prods. Liab. Litig., 55 F.3d 768, 777 (3d Cir. 1995); Culver v. City of Milwaukee, 277 F.3d 908, 911, 913-14 (7th Cir. 2002). Back Doctors Ltd. v. Metro. Prop. & Cas. Ins. Co., 637 F.3d 827, 831 (7th Cir. 2011), dealt with the irrelevant standard to evaluate the amount in controversy under CAFA. Moreover, even if the 2003 amendment had not resolved any previous uncertainty regarding the permissibility of dismissing without court approval an uncertified class action where class members’ claims were not prejudiced, all of the cases Frank cites can be easily distinguished because they dealt with claims for monetary damages where no such monetary relief was obtained for the other putative class members, whereas Plaintiffs here primarily sought injunctive relief, which was mooted,

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 20 of 41 PageID #:676

12

Dismissal was the only appropriate action, both under Trulia and under prevailing federal

law, because Plaintiffs’ claims were mooted. See, e.g., Damasco v. Clearwire Corp., 662 F.3d 891,

896 (7th Cir. 2011) (“To allow a case, not certified as a class action and with no motion for class

certification … pending, to continue in … court when the sole plaintiff no longer maintains a

personal stake defies the limits on federal jurisdiction …”); Cruz-Bernal v. Keefe, No. 14-50178,

2015 U.S. Dist. LEXIS 90180, at *8-*9 (N.D. Ill. July 13, 2015) (same); Wolschlager v. Law Offices

of Mitchell D. Bluhm & Assocs., LLC, No. 1:17-CV-00033, 2017 U.S. Dist. LEXIS 83448, at *9

(W.D. Mich. May 18, 2017) (noting “well-established circuit rule that voluntary settlement of a

named plaintiffs’ claims prior to class certification moots the entire action”).

Importantly, Plaintiffs’ dismissals did not release any individual or class claims, did not

relinquish any individual or class rights, and, thus, could not possibly have prejudiced the putative

class or Frank.10 Accordingly, members of the putative class, including Frank, remain free to pursue

any of the now-mooted claims that Plaintiffs raised or any other claims they may believe they have

against Defendants should they so desire. In short, no putative class was ever certified. Pursuant to

black letter law, Plaintiffs and their counsel had the statutory right to voluntarily dismiss their mooted

but which relief all putative class members shared through the Supplemental Disclosures. 10 The cases Frank cites in support of his argument that Plaintiffs somehow breached a duty they did not owe even though they did not release any class members’ claims do not support his position. In Grok Lines, Inc. v. Paschall Truck Lines, Inc., No. 14 C 08033, 2015 U.S. Dist. LEXIS 124812, at *9 (N.D. Ill. Sep. 18, 2015), the attorneys sought to settle the case as a class action (unlike here) and is, thus, entirely inapposite. Pitts v. Terrible Herbst, Inc., 653 F.3d 1081, 1091-92 (9th Cir. 2011), dealt with an unaccepted Rule 68 offer of judgment (again, unlike here). But see Campbell-Ewald Co. v. Gomez, 136 S. Ct. 663, 672 (2016) (“[A]n unaccepted settlement offer or offer of judgment does not moot a plaintiff’s case . . . We need not, and do not, now decide whether the result would be different if a defendant deposits the full amount of the plaintiff’s individual claim in an account . . . and the court then enters judgment for the plaintiff in that amount.”); id. at 882 (“If the defendant is willing to give the plaintiff everything he asks for, there is no case or controversy to adjudicate, and the lawsuit is moot.”) (Roberts, J., dissenting). In Primax Recoveries, Inc. v. Sevilla, 324 F.3d 544, 546-47 (7th Cir. 2003), a motion for class certification had been filed and the mootness discussion is dicta regarding a related state court matter. Finally, Standard Fire Ins. Co. v. Knowles, 568 U.S. 558 (2013), simply states the correct proposition that a “plaintiff who files a proposed class action cannot legally bind members of the proposed class before the class is certified.” Id. at 588.

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 21 of 41 PageID #:677

13

actions. A decision to avail oneself of a statutory right under federal law cannot be a breach of

fiduciary duty, and Frank cites no current authority for his position or any current authority contrary

to Plaintiffs’ and their counsel’s position.

3. Bringing Suit Cannot Constitute a Breach of Fiduciary Duty

Because the plain language of Rule 23(e) is fatal to Frank’s attempts to conjure a direct claim

for a breach of fiduciary duty on account of Plaintiffs’ dismissal without prejudice of their mooted,

uncertified actions, Frank argues that Plaintiffs and their counsel breached this nonexistent duty by

simply filing suit because, in his factually unsupported, layman’s opinion, Plaintiffs’ claims

constituted “worthless claims” for disclosures that were not “plainly material.” But see Order at 10

(“[E]ven if Berg’s claims are ‘worthless,’ they are not necessarily meritless”). Thus, Frank argues

that the very act that gave rise to the alleged fiduciary duty – the filing of a putative class action –

also breached that purported duty. Dkt. No. 88 at 2. This argument relies, not just on hopelessly

circular logic, but on the wrong standard. Trulia’s “plainly material” standard only applies to

settlements of certified class actions where absent class members are bound by the settlement. That

is not the situation here. Even if this Court reviewed the Supplemental Disclosures under that rubric

– which is not relevant to whether Frank is entitlement to intervention – the disclosures easily meet

that standard.

B. Frank Has No Standing To Pursue A Direct Claim

As Frank repeatedly admits, Walgreens/Trulia is the law of this Circuit. Accordingly, Frank’s

sole recourse is by way of derivative action – an action that this Court has already found he cannot

bring. For this reason alone, his motion must again be denied.

1. Plaintiffs Complied with Trulia and Walgreens In Trulia, the Delaware Court of Chancery addressed the proper way to litigate and resolve

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 22 of 41 PageID #:678

14

disputes regarding disclosure claims in connection with merger transactions like that here.

Specifically, Trulia laid out two permissible paths that any such litigation could take. Unlike the

circumstances here, Trulia holds that any court-approved settlement of class action litigation

involving the release of class claims for disclosures would require the disclosures be “plainly

material” and a release that is narrowly tailored. 129 A.3d at 898. In contrast, in the precise

procedural posture of the actions here, in what the Trulia court characterized as the “preferred

scenario,” the matter can be resolved without a class settlement where the “disclosure claims have

been mooted by defendants electing to supplement their proxy materials, plaintiffs dismiss their

actions without prejudice to the other members of the putative class (which has not yet been certified)

and the Court reserves jurisdiction solely to hear a mootness fee application.” Id. at 897. In those

instances, the Trulia court held that “the parties also have the option to resolve the fee application

privately without obtaining Court approval” – consistent with “the right of a corporation’s directors

to exercise business judgment to expend corporate funds, with the caveat that notice must be

provided to the stockholders.” Id. at 897-98 (emphasis added). In this instance, “an interested person

[may] object to the use of corporate funds … by ‘challeng[ing] the fee payment as waste in a

separate litigation,’ if the circumstances warrant.” Id. at 898 (emphasis added).

As this Court has already found, this latter, “preferred” scenario – a non-settlement,

mootness dismissal reached after discovery – is exactly what happened here. Order at 6, 10 n.1.11

11 Notably, even if there had been a certified class here and a formal Rule 23(e) settlement subject to Court approval, Frank would still lack standing to object to the fee Akorn agreed to pay. In federal court, an attorneys’ fee request by agreement of the parties that does not diminish the class members’ award is “presumptively reasonable.” Goodyear v. Estes Exp. Lines, Inc., No. 1:06-CV-863, JDT-TAB, 2008 U.S. Dist. LEXIS 18694, at *13-*14 (S.D. Ind. Mar. 10, 2008). And “[s]imply being a member of a class is not enough to establish standing. One must be an aggrieved class member.” In re First Cap. Holdings Corp. Fin. Prods. Sec. Litig., 33 F.3d 29, 30 (9th Cir. 1994). “If modifying the fee award would not ‘actually benefit the objecting class member,’ the class member lacks standing because his challenge to the fee award cannot result in redressing any injury.” Glasser v. Volkswagen of Am., Inc., 645 F.3d 1084, 1088 (9th Cir. 2011). Further, Frank’s argument that “mootness fees appear premised on a catalyst theory of an equitable

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 23 of 41 PageID #:679

15

These actions reflect a model application of Trulia. And, pursuant to Trulia, which even Frank

acknowledges “is now the law of this circuit,” Dkt. No. 82-1 at ¶62, Frank’s only avenue to complain

about the mootness fee Akorn agreed to pay is by “object[ing] to the use of corporate funds, such as

by ‘challeng[ing] the fee payment as waste in a separate litigation,’” Trulia, 129 A.3d at 898

(emphasis added); see also Order at 6.12

2. The Supplemental Disclosures Were More Than Sufficient To Support The Mootness Fee Even If Court Approval Was Required

As explained, under Rule 23(e)(1)(A) and Trulia/Walgreens, no court approval was required

to dismiss the actions or obtain a voluntary payment of a mootness fee by Akorn because there was award, which does not exist under federal law,” is not supported by these factually distinguishable cases. Parshall v. Stonegate Mortg. Corp., No. 1:17-cv-00711-JMS-DML, 2017 U.S. Dist. LEXIS 129977, at *3 (S.D. Ind. Aug. 11, 2017), relied on Buckhannon Board & Care Home, Inc. v. West Virginia Dep’t of Health & Human Res., 532 U.S. 598 (2001), and dealt with the definition of prevailing party under certain fee-shifting statutes. Id. at 604. Reynolds v. Ben. Nat’l Bank, 288 F.3d 277, 288 (7th Cir. 2002), dealt with whether the court properly approved a class action settlement and attorneys’ fees related to the settlement. There is no class action settlement here. And the term “catalyst theory” does not even appear in the case. In Howell v. Mgmt. Assistance, Inc., 519 F.3d 83, 91 (S.D.N.Y. 1981), the court did not allow an award of attorneys’ fees because the action was “devoid of merit” and it found the case to be “a compelling case for the imposition of sanctions” on the plaintiffs’ attorneys. Here, the Court found that the claims were not meritless. See Order at 10. 12 Unable to overcome the preclusive effect of Walgreens and Trulia, Frank attempts to invoke the limitation of attorneys’ fees to a “reasonable percentage” of the relief recovered for the class provision of the Private Securities Litigation Reform Act of 1995, 15 U.S.C. §78u-4(a)(6) (“PSLRA”), arguing Plaintiffs have to prove how the payment of a mootness fee is not prohibited under the PSLRA, which he claims only allows attorneys’ fees for monetary recoveries. See Dkt. No. 83 at 7-8. The PSLRA, however, speaks only to “fees and expenses awarded by the court to counsel for the plaintiff class ….” 15 U.S.C. §78u-4(a)(6) (emphasis added). No class was certified here, no counsel were appointed class counsel, and Plaintiffs’ counsel did not, and are not, seeking an award from the Court. That is precisely why Trulia controls. “The fact that this suit has not yet produced, and may never produce, a monetary recovery from which the fees could be paid does not preclude an award based on this rationale.” See Mills v. Elec. Auto-Lite Co., 396 U.S. 375, 392 (1970); Kopet v. Esq. Realty Co., 523 F.2d 1005, 1008-09 (2d Cir. 1975) (finding fee award warranted where litigation caused disclosure of financial statements). Moreover, nothing in the PSLRA precludes fees when the recovery is not monetary. See, e.g., Aron v. Crestwood Midstream Partners LP, No. 4:15-CV-1367, 2016 U.S. Dist. LEXIS 152427, at *26 (S.D. Tex. Oct. 14, 2016) (“Even where the common fund is zero, attorneys’ fees may still be awarded”); Davis v. Cent. Vt. Pub. Serv. Corp., No. 5:11-181, 2012 U.S. Dist. LEXIS 139186, at *39-*40 (D. Vt. Sep. 27, 2012) (awarding fee where there was no common fund); In re Schering-Plough/Merck Merger Litig., No. 09-1099, 2010 U.S. Dist. LEXIS 29121, at *48-*50 (D.N.J. Mar. 26, 2010) (awarding $3.5 million attorneys’ fee in disclosure-based settlement). Frank acknowledges that Walgreens and Trulia are the law of this Circuit, and those cases set out a roadmap for the payment of mootness fees. Frank cannot embrace those decisions while simultaneously alleging that their very framework is illegal under the PSLRA.

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 24 of 41 PageID #:680

16

no certified class, no class settlement and class members were not bound by the dismissals. It is only

where a settlement for a certified class is presented to a court for approval that a court needs to

analyze the value of the disclosures obtained in such a settlement to demonstrate the entitlement to a

mootness fee. Nevertheless, Frank devotes much of his efforts to the incorrect arguments that to earn

a mootness fee, the disclosures in question must be “plainly material” and that the disclosures

obtained by Plaintiffs here were not. Although Plaintiffs have no obligation pursuant to the proper

procedure they followed under Trulia to show that the Supplemental Disclosures were “plainly

material” or bestowed any value on the members of the uncertified class, they can readily do so.13

According to Frank, disclosures are “worthless,” and class actions aimed at securing

disclosure are a “scourge.” Dkt. No. 83 at 12-13.14 Irrespective of Frank’s view of class actions

seeking enhanced disclosures, Congress and the Supreme Court long ago recognized that complete

and accurate disclosure is the touchstone of the federal securities law protections of investors faced

with significant corporate decisions. See, e.g., J. I. Case Co. v. Borak, 377 U.S. 426, 431 (1964)

(“The purpose of § 14(a) is to prevent management or others from obtaining authorization for

corporate action by means of deceptive or inadequate disclosure in proxy solicitation. The section

stemmed from the congressional belief that fair corporate suffrage is an important right …”)

(emphasis added). To this end, the Supreme Court has recognized that private enforcement of the

proxy disclosure laws are a necessary supplement to government action and that equitable relief

13 Frank also contends that Plaintiffs’ counsel must prove that they caused the Supplemental Disclosures in the Definitive Proxy, Dkt. No. 88 at 7, but he is wrong. At issue here is a private mootness fee resolution and the parties thereto bear no burden of proof in that agreement. Akorn entered into that agreement based on its business judgment of the value of Plaintiffs’ counsel’s contribution. 14 As other courts have noted, Frank’s argument “does not seem grounded in the facts of this case, but in … [his] objection to class actions generally.” City of Livonia, 2013 U.S. Dist. LEXIS 113658, at *15 (Frank’s briefs are “long on ideology and short on law.”). However, as the Ninth Circuit noted, federal courts “deal in cases, not crusades,” and “licensing self-appointed Samaritans to rove the legal campagna, appealing fee awards that no party with an actual stake in the outcome cares to dispute . . . seems as likely a recipe for strike suits as one for reform.” Knisley v. Network Assocs., 312 F.3d 1123, 1128 (9th Cir. 2002).

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 25 of 41 PageID #:681

17

would most often result from such litigation. See id. at 432, 435; Mills, 396 U.S. at 396. Frank

disagrees with this established jurisprudence, and wants this Court to ignore it or change it. While

everyone is entitled to their opinion, his position has understandably been consistently rejected by

courts across this country. See supra notes 5, 14.

a. “Plainly Material” Is Not the Applicable Standard

As outlined above, and as this Court has already concluded, Trulia’s “plainly material”

standard is specifically limited to court-approved, disclosure-only settlements of certified class

actions that involve the release of class claims and, thus, does not apply here. Order at 9-10; Trulia,

129 A.3d at 898. Rather, this Court has already found that before it is a non-settlement, mootness

dismissal in compliance with Trulia. See Order at 6. Accordingly, any of Frank’s theories based on

his argument that the Supplemental Disclosures lack “plain materiality” is a false postulate

inapplicable to the procedural history of this case. Here, Plaintiffs’ counsel are not required to

“prove” their entitlement to a fee by demonstrating the materiality of the disclosures obtained.15 For

this reason alone, Frank has failed to plead any direct claim based on his view of the value of the

Supplemental Disclosures.16

b. The Disclosures Were Nonetheless “Plainly Material”

Even if Plaintiffs had obtained certification of a class, entered a settlement based on the

15 In the context of a disputed mootness fee application where there was an individual release by the plaintiffs, but none by the class, the Delaware Court of Chancery recently held that “a fee can be awarded if the disclosure provides some benefit to stockholders, whether or not material to the vote. In other words, a helpful disclosure may support a fee award . . . .” In re Xoom Corp. S’holder Litig., No. 11263-VCG, 2016 Del. Ch. LEXIS 117, at *10 (Aug. 4, 2016) (emphasis added). Frank admits that a Supplemental Disclosure was “helpful.” Dkt. No. 88 at 11. 16 The “correct” standard, of course, is the long-standing deference given by federal courts to the private resolution of disputes, and Frank cites no law that gives him standing to challenge Akorn’s business judgment decision to pay Plaintiffs’ counsel a mootness fee. See, e.g., Armstrong v. Bd. of Sch. Dirs. of City of Milwaukee, 616 F.2d 305, 312-13 (7th Cir. 1980), overruled on other grounds, Felzen v. Andreas, 134 F.3d 873 (7th Cir. 1998) (“[i]t is axiomatic that the federal courts look with great favor upon the voluntary resolution of litigation through settlement.”).

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 26 of 41 PageID #:682

18

Supplemental Disclosures, and sought Court approval under Rule 23(e) of that settlement, and the

“plainly material” standard did apply (which it does not), the disclosures pleaded and secured by

Plaintiffs would easily satisfy that standard.17 At the time of the announcement of the Merger

Agreement on April 24, 2017 – two months before Frank became an Akorn shareholder – Akorn

was, by all accounts, a healthy company on the brink of significant profitability. On March 2, 2017,

Akorn announced that it has received critical FDA approval for one of its New Drug Applications.

As a result of these announcements, financial analysts increased their price targets and upgraded

Akorn’s future outlook. Accordingly, many stockholders were surprised to learn on May 22, 2017,

when Akorn filed its Preliminary Proxy, that it had lowered its projected financial performance

during the sales process – a time period that coincided with its release of positive 2016 financial

results. Further concerning was the fact that Fresenius offered Akorn’s Chairman, Dr. Kapoor,

continuing equity in the surviving company at the same time that the Merger consideration was being

negotiated and Akorn was lowering its projections.18 Accordingly, when Plaintiffs filed suit, they

sought, primarily, to remedy the Preliminary Proxy’s failure to disclose: (i) the earlier sets of

projections that the Board lowered during the sales process; (ii) a GAAP (or “generally accepted

accounting principles”) reconciliation of the final set of lowered projections that it did disclose or, at

17 In addition to the discussion of the materiality of the Supplemental Disclosures contained herein, Plaintiffs submit herewith the Affidavit of M. Travis Keath, CFA, CPA/ABV, dated May 15, 2018 (Ex. A), which discusses the importance to investors of the Supplemental Disclosures from a financial standpoint. 18 In situations such as this, the potential for a conflict of interest is high and the possibility that a corporate insider may accept lower consideration for public shareholders in exchange for greater personal value (through continuing equity) is significant. See, e.g., In re Lear Corp. S’holder Litig., 926 A.2d 94, 114, 116 (Del. Ch. 2007) (“the failure to get the [optimal] price for [the company] now would not hurt him as much as the public stockholders”; such an economic motivation “could rationally lead [him] to favor a deal at a less than optimal price, because the procession of a deal was more important to him, given his overall economic interest, than only doing a deal at the right price”); RBC Capital Mkts., LLC v. Jervis, 129 A.3d 816, 860 n.157 (Del. 2015) (in private equity buyout, CEO would be able to cash out current equity early and also keep job and receive more equity in private company); In re El Paso S’holder Litig., 41 A.3d 432, 444-45 (Del. Ch. 2012) (finding reasonable likelihood that CEO who stood to retain an equity interest in the surviving company was conflicted).

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 27 of 41 PageID #:683

19

least, the line items that went into calculating the non-GAAP metrics that it disclosed; (iii) specifics

regarding Fresenius’ offers of continuing equity while negotiating the Merger consideration for

public stockholders; (iv) the Board’s evaluation of the merit and value to Akorn of a pending

derivative litigation; and (v) JPM’s certain potential conflicts of interest.

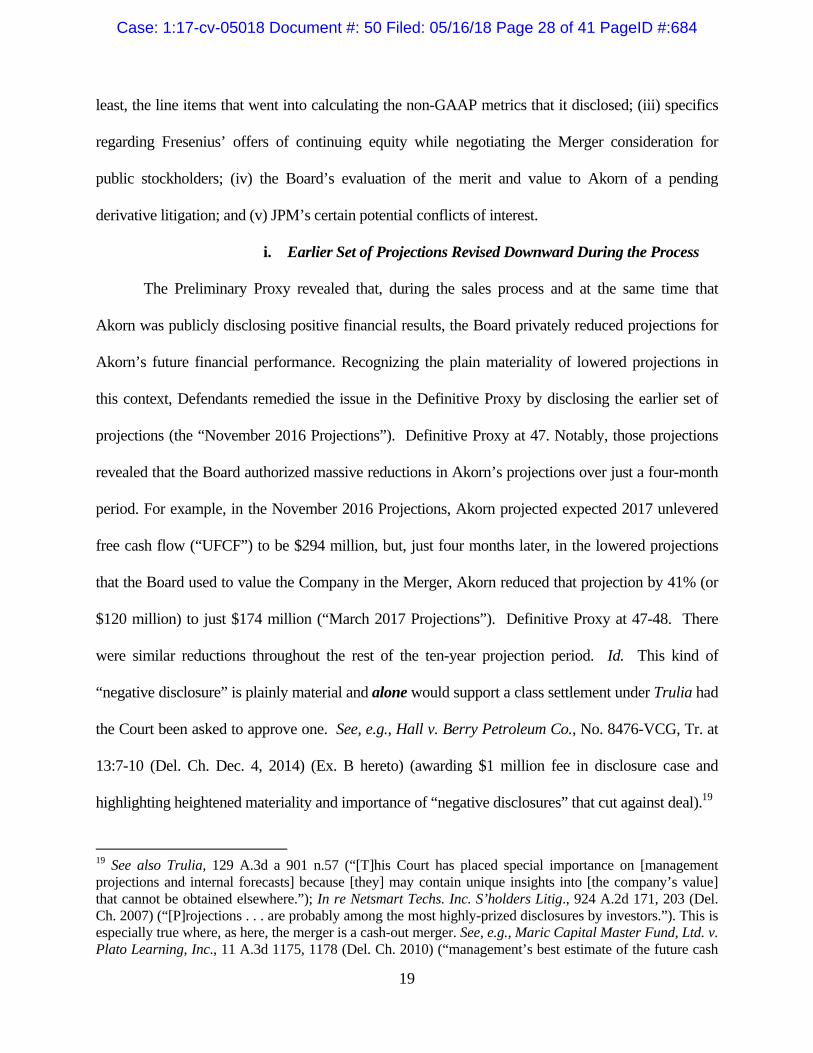

i. Earlier Set of Projections Revised Downward During the Process

The Preliminary Proxy revealed that, during the sales process and at the same time that

Akorn was publicly disclosing positive financial results, the Board privately reduced projections for

Akorn’s future financial performance. Recognizing the plain materiality of lowered projections in

this context, Defendants remedied the issue in the Definitive Proxy by disclosing the earlier set of

projections (the “November 2016 Projections”). Definitive Proxy at 47. Notably, those projections

revealed that the Board authorized massive reductions in Akorn’s projections over just a four-month

period. For example, in the November 2016 Projections, Akorn projected expected 2017 unlevered

free cash flow (“UFCF”) to be $294 million, but, just four months later, in the lowered projections

that the Board used to value the Company in the Merger, Akorn reduced that projection by 41% (or

$120 million) to just $174 million (“March 2017 Projections”). Definitive Proxy at 47-48. There

were similar reductions throughout the rest of the ten-year projection period. Id. This kind of

“negative disclosure” is plainly material and alone would support a class settlement under Trulia had

the Court been asked to approve one. See, e.g., Hall v. Berry Petroleum Co., No. 8476-VCG, Tr. at

13:7-10 (Del. Ch. Dec. 4, 2014) (Ex. B hereto) (awarding $1 million fee in disclosure case and

highlighting heightened materiality and importance of “negative disclosures” that cut against deal).19

19 See also Trulia, 129 A.3d a 901 n.57 (“[T]his Court has placed special importance on [management projections and internal forecasts] because [they] may contain unique insights into [the company’s value] that cannot be obtained elsewhere.”); In re Netsmart Techs. Inc. S’holders Litig., 924 A.2d 171, 203 (Del. Ch. 2007) (“[P]rojections . . . are probably among the most highly-prized disclosures by investors.”). This is especially true where, as here, the merger is a cash-out merger. See, e.g., Maric Capital Master Fund, Ltd. v. Plato Learning, Inc., 11 A.3d 1175, 1178 (Del. Ch. 2010) (“management’s best estimate of the future cash

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 28 of 41 PageID #:684

20

ii. GAAP Reconciliations and Non-GAAP Line Items

While UFCF are generally considered the holy grail of projections, as they allow

sophisticated investors to project a company’s future profitability and performance and discount that

projection to the present day, Plaintiffs believed it was necessary for Akorn to disclose both sets of

projections in a format that its shareholders were accustomed to seeing. In its regular quarterly

reports, Akorn traditionally disclosed its financial results in GAAP format – with net income being

the ultimate, bottom-line GAAP metric provided. GAAP format is important because GAAP metrics

– like revenue and net income – are universally defined terms that all investors can understand. And

it was in this format that Akorn stockholders were accustomed to receiving Akorn’s financial results

for years.

By Akorn chosing to provide non-GAAP metrics for its future projections, two problems

arose. First, non-GAAP metrics (like EBITDA and UFCF) are not universally defined terms, and

companies can (and do) use their own definitions, with their own adjustments, not all of which are

always disclosed.20 For this reason, pursuant to then-prevailing SEC rules, when a company

disclosed non-GAAP financial measures in a proxy, the company was also generally required to

flow of a corporation that is proposed to be sold in a cash merger is clearly material”); In re PNB Holding Co. S’holders Litig., No. 28-N, 2006 Del. Ch. LEXIS 158, at *59 (Del. Ch. Aug. 18, 2006) (“[R]eliable management projections of the company’s future prospects are of obvious materiality to the electorate[, as] the key issue for the stockholders is whether accepting the merger price is a good deal in comparison with remaining a shareholder and receiving the future expected returns . . .”). 20 As outlined in depth in Plaintiff House’s complaint: (1) this problem had been specifically recognized by the former SEC Chairwoman, who noted a number of “troublesome practices which can make non-GAAP disclosures misleading”; (2) at the time Plaintiffs filed their suits, the SEC had been emphasizing that disclosure of non-GAAP projections can be inherently misleading and had heightened its scrutiny of the use of such projections; and (3) on May 17, 2016, just before Plaintiffs filed suit, the SEC released new and updated Compliance and Disclosure Interpretations on the use of non-GAAP financial measures that demonstrated it tightening policy, one of which regarded forward-looking information, such as financial projections, and required companies to provide any reconciling metrics that are available without unreasonable efforts. See, e.g., House Dkt. No 1 at ¶¶37-39. While Frank is correct that the SEC has since changed its regulations, that change occurred on October 18, 2017, after Plaintiffs filed suit, after the Supplemental Disclosures were issued, and after these cases were dismissed without prejudice.

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 29 of 41 PageID #:685

21

disclose all projections and information necessary to make the non-GAAP measures not misleading

and to provide a reconciliation of the differences between the non-GAAP financial measure disclosed

or released with the most comparable financial measure or measures calculated and presented in

accordance with GAAP. 17 C.F.R. §244.100.

Second, because Akorn investors had received GAAP metrics (like net income) for years in

quarterly reports, receiving only non-GAAP metrics made it difficult for them to compare past

financial performance with what was projected to be its future financial performance. Accordingly,

regardless of SEC rule,21 based on the specific facts of this case, Akorn’s use of non-GAAP metrics

alone was materially misleading. Ultimately, there are two ways to cure this problem. The first – but

lesser – is to secure the individual line items that go into the calculation of UFCF. The Definitive

Proxy disclosed the individual line items that went into management’s calculation of that non-GAAP

metric for both the November 2016 and March 2017 Projections. Id. at 47-48. The second – and

superior – method is to secure a GAAP reconciliation of the non-GAAP metric to a GAAP

equivalent metric. This Defendants refused to do in the Definitive Proxy. Accordingly, Plaintiffs

filed their narrowly tailored motion for preliminary injunction and this was one of the two issues

raised there. In response, Defendants produced a full GAAP reconciliation of all relevant non-

GAAP metrics to their GAAP equivalents. See 8-K, at 8-11.

This disclosure revealed that the November 2016 Projections assumed steady increases in its

net income consistent with Akorn’s past performance, while Akorn’s March 2017 Projections

assumed a sudden drop in Akorn’s near term performance inconsistent with its recent financial

results.22 The “negative disclosure” of projected financial information that cuts against the

21 The SEC notes that its rules and review of proxy statements do not guarantee their accuracy and that investors have important rights of recovery against those disseminating inaccurate proxies, even if the SEC cleared a proxy. See “What We Do,” available at https://www.sec.gov/Article/whatwedo.html#laws. 22 The disclosure of the line item projections and GAAP reconciliation also resolved the uncertainty as to

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 30 of 41 PageID #:686

22

sufficiency of a merger like this is plainly material and would alone support a class settlement.

iii. Fresenius’ Offers of Continuing Equity to Dr. Kapoor

During discovery, Plaintiffs uncovered a third major disclosure issue regarding the offers of

continuing equity that Fresenius offered Dr. Kapoor while his management team was lowering

projections and negotiating the Merger consideration. The Definitive Proxy’s entire disclosure

regarding these discussions was that: (1) on March 30, 2017, Fresenius requested that “Dr. Kapoor

agree to invest 20% of any proceeds that Dr. Kapoor would receive in [the Merger] in ordinary

shares of Fresenius Parent [the surviving company]” and (2) “[t]here were no other substantive

discussions with respect to such an investment by Dr. Kapoor and no agreement with respect to such

an investment was ever entered into.” Definitive Proxy at 34. That was not true.

As Plaintiffs learned in discovery, there were other offers by Fresenius tied to Dr. Kapoor’s

continuing equity. The Definitive Proxy revealed to stockholders only that Fresenius had made a

$34.00 bid on April 2, 2017. See Definitive Proxy at 34. Through the Supplemental Disclosures,

stockholders learned that Fresenius had actually offered three alternative bids on that date: (1) one for

$34.00, which was disclosed; (2) one for $33.00 plus a $2.00 CVR, which was not previously

disclosed; and (3) one for $34.50 that included an equity investment by Dr. Kapoor, which also was

not disclosed, and which rendered the statement in the Definitive Proxy that no further

communications regarding such an investment occurred false. See 8-K, at 4-5.

Information regarding firm bids are always material – especially when they are for more than

the bid disclosed in the Definitive Proxy. See, e.g., In re Orchard Enters., Inc., 88 A.3d 1, 23 (Del.

whether stock-based compensation was treated as a cash or non-cash expense in calculating Akorn’s UFCF. Courts have held that treating it as a cash expense (as Akorn and JPM did) is “unusual” and “uncommon.” See, e.g., In re Celera Corp. S’holder Litig., No. 6304-VCP, 2012 Del. Ch. LEXIS 66, at *87-*88 (Del. Ch. Mar. 23, 2012), rev’d in part on other grounds, 2012 Del. LEXIS 658 (Del. Dec. 27, 2012). By treating stock-based compensation as a cash expense, Defendants lowered Akorn’s UFCF projections, which, in turn, lowered the valuation range for the Company in JPM’s Discounted Cash Flow Analysis.

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 31 of 41 PageID #:687

23

Ch. 2014) (“[T]he omission of key information about a competing bid is material – even if the bid is

‘highly speculative and contingent’ – where a proxy statement contains partial and incomplete

disclosures about the bidding history.”). So too is information regarding potential conflicts that affect

key members of the Board and/or management, like the undisclosed offer of continuing equity in a

company to its chairman of the board.

iv. The Value of Derivative Claims Pending Against the Board

Plaintiffs also delved into the valuation of certain pending derivative litigation which sought

to recover damages from the Board suffered by Akorn as a result of then-pending securities

litigation.23 This was relevant to Akorn shareholders for two reasons. First, the derivative claims

were assets of Akorn and, as such, the Board had a fiduciary obligation to value them as part of the

Merger. See Houseman v. Sagerman, No. 8897-VCG, 2014 Del. Ch. LEXIS 55, at *40 (Del. Ch.

Apr. 16, 2014) (“prior to a merger, stockholders own as an asset the value of any derivative claim

that could be asserted; after a merger, ‘the right to bring a derivative action passes via merger to the

surviving corporation,’ and the stockholders are entitled to receive consideration for the transfer of

that asset”). Second, and more important, upon the consummation of the Merger, the derivative

plaintiffs would lose standing to continue pursuing the derivative actions, such that the members of

the Board were deciding on whether to relieve themselves of million of dollars in potential derivative

liability. See, e.g., Lewis v. Anderson, 477 A.2d 1040, 1047 (Del. 1984) (merger eliminates standing

of former stockholders to pursue pre-merger derivative claims).

These claims – much less whether the Board considered and valued them – were not even

mentioned in the Preliminary or Definitive Proxies. The Supplemental Disclosures remedied that, 23 See, e.g., Merritt v. Colonial Foods, Inc., 505 A.2d 757, 766 (Del. Ch. 1986) (denying summary judgment, in part, because one possible motivation to enter into merger was to extinguish pending derivative claims); Revlon, Inc. v. MacAndrews & Forbes Holdings, Inc., 506 A.2d 173, 184 (Del. 1985) (conflict where a “significant by-product” of entering into merger was “to protect the directors against a perceived threat of personal liability”).

Case: 1:17-cv-05018 Document #: 50 Filed: 05/16/18 Page 32 of 41 PageID #:688

24

revealing, critically: (1) that, while the Board was considering the Merger, they were specifically

“aware of and considered the likely effect of the proposed merger . . . on the . . . derivative claims” –

namely, that they would likely be dismissed; and (2) that the Board assigned no value to the

derivative claims. See 8-K, at 4-5. This information is again plainly material. See In re Massey

Energy Co. Deriv. & Class Action Litig., No. 5430-VCS, 2011 Del. Ch. LEXIS 83, at *8 (Ch. May

31, 2011) (noting importance of proxy fairly and accurately describing a board’s weighing of the

value of derivative claims in connection with merger and the disclosure that a derivative claim was

not valued allowed shareholders to vote on an informed basis).24

v. Issues Regarding JPM’s Potential Conflicts

Plaintiffs also took issue with Akorn’s failure to disclose certain potential conflicts faced by

JPM. Notably, the Preliminary Proxy failed to disclose whether JPM’s $47 million fee was

contingent on the consummation of the Merger and, if so, how much. See Preliminary Proxy at 45.25

Delaware courts have long recognized that, where a banker is paid a large fee contingent on the

consummation of a merger, conflicts of interest can arise because “the interests of the agent [banker]