Embed Size (px)

Citation preview

e v e r y l i f e h a s a s t o r y .

Universal life ProdUct GUide

Updated march 26, 2012.

ADVISORS PLEASE NOTE: Effective April 23, 2012, the following Designated Indices are being substituted with Designated Indices with similar investment objectives. Accordingly, the names of the corresponding Managed Index Interest Options are updated to reflect the new Designated Indices, as listed below.

Designated Index

imaxx Canadian Equity Value Fund

imaxx U.S. Equity Growth Fund

imaxx U.S. Equity Value Fund

imaxx Global Equity Value Fund

NEW Designated Index

Dynamic Value Fund of Canada

AGF American Growth Class

CI American Value Fund

Dynamic Global Discovery Fund

This material has been prepared for the use of

Transamerica’s advisors in conjunction with other product

information. The intent of this guide is to provide an

overview of the WealthAdvAntAge and EstateAdvAntAge

plans. For a precise understanding of the rights and

obligations of the policyowner and Transamerica, please

refer to the WealthAdvAntAge and EstateAdvAntAge

contracts.

IMPORTANT: This guide is not designed to provide tax,

legal, accounting or other professional advice. If you are

not a qualified tax advisor, we recommend that you advise

your client to seek the advice of a tax professional. It is

the owner’s responsibility to determine the consequences

to him or her under relevant income tax legislation, and

Transamerica assumes no liability to the owner.

The sections that reference tax information provide a

summary only of the current principal Canadian federal

income tax consequences arising under the Income Tax

Act (Canada) and the regulations thereunder to prospective

owners of WealthAdvAntAge and EstateAdvAntAge policies

who are residents of Canada.

The tax information contained in this guide is based

upon the provisions of the Income Tax Act (Canada), the

regulations thereunder currently in effect, all proposed

amendments thereto publicly released by the Department

of Finance (Canada) prior to the date of printing this

guide and upon Transamerica’s understanding of the

administrative practices and policies of the Canada

Revenue Agency (CRA) currently in effect. The tax

About this guideThis guide contains product information for WealthAdvAntAge and EstateAdvAntAge policies. This guide is effective

November 28, 2011, and contains product information for WealthAdvAntAge and EstateAdvAntAge policies.

information, wherever contained in this product guide,

neither anticipates any changes in law, whether by

legislative, governmental or judicial action, nor does it take

into account provincial or foreign income tax legislation or

considerations.

about the guarantees

Transamerica makes certain guarantees with respect to

WealthAdvAntAge and EstateAdvAntAge. These guarantees

do not include:

• The portion of the total fund value attributable to

a particular Index Interest Option. This varies in

accordance with fluctuations in the daily interest rate

formula for each Index Interest Option.

• The interest rate applicable to the Index Interest Options.

In fact, this interest rate may be either positive or

negative, depending on the performance of a particular

index. A negative interest rate will reduce the benefits

and values under this policy, which include but are not

limited to the total fund value, the cash surrender value,

the net cash surrender value, the maximum benefit

amount for a Living Benefit and the death benefit.

Transamerica does not accept responsibility for any errors

or omissions contained in these materials. The information

contained within this document is current as of the date of

publication and is subject to change.

WealthAdvAntAge

EstateAdvAntAge with Accumulation Bonus EstateAdvAntAge – Low-Fee

This product is intended to suit policyholders who plan to invest more aggressively and have longer-term financial goals and investment planning time frames.

These products are intended to suit more conservative policyholders with shorter-term financial goals and investment planning time frames.

Why choose Transamerica’s WealthAdvAntAge and EstateAdvAntAge universal life?

Financial strength and stabilityTransamerica has been helping Canadians achieve

financial security since 1927. Over the years, we’ve

learned that financial peace of mind means different things

to different people. Whether it’s saving for retirement,

protecting family and assets or helping clients achieve

their specific goals, their needs are unique. That’s why

we offer a diverse range of solutions. We want to be there

with the insurance and investment options needed at

every stage of life.

Every life story is unique, and that’s why we offer more than one universal life plan. Each plan addresses different needs, so together with your client, you can choose the plan that is best for now...and for the future.

Transamerica Life Canada is a wholly-owned subsidiary

of AEGON N.V., one of the largest insurers in the

world. Based in the Netherlands, it has major company

operations in Hungary, Spain and the U.K., in addition to

the Netherlands and Americas. Transamerica is one of

Canada’s leading providers of life insurance and investment

products. Its financial strength is complemented by a solid

network of 18,000 accredited advisors located in all major

cities across Canada.

Universal Life Product Guide

Table of contents1. Product Overview 1

2. Insurance coverages 4

Coverage and rider issue ages and amounts 4

Coverage types 5

Death benefit options 5 Increasing death benefit 5 Level death benefit 6 During the COI period 6 After the COI period (varies with the COI option) 6

Cost of Insurance (COI) options 7 Mixing COI options 8 Switching COI options 8 Built-in premium tax 8 COI banding 8

Underwriting programs 8 Non-medical underwriting 9 Medical underwriting 9 Overview of required forms 10 Underwriting risk classifications 10 Summary of underwriting program and applicable

risk classification by age and face amount 11 Underwriting requirement 12 Underwriting materials 12 Ratings 12

Policies with multiple universal life coverages 14 Multiple universal life coverages 14 Base universal life coverage 15 Multiple life special options 15 Severance Option 17 Change of Primary Life Insured Option 17

Joint life coverages 18 Joint last-to-die 18 Joint first-to-die 21 Switching between joint options 23

Riders 24 Level Cost Rider 24 TermSelect Riders 24

3. Investment choices 25

Interest Options 25 Relative risk rating 26

T-Bill Interest Option and Fixed-Rate Interest Options 27

Index Interest Options 28

Asset allocation solutions 32 Investor Profile Questionnaire 32

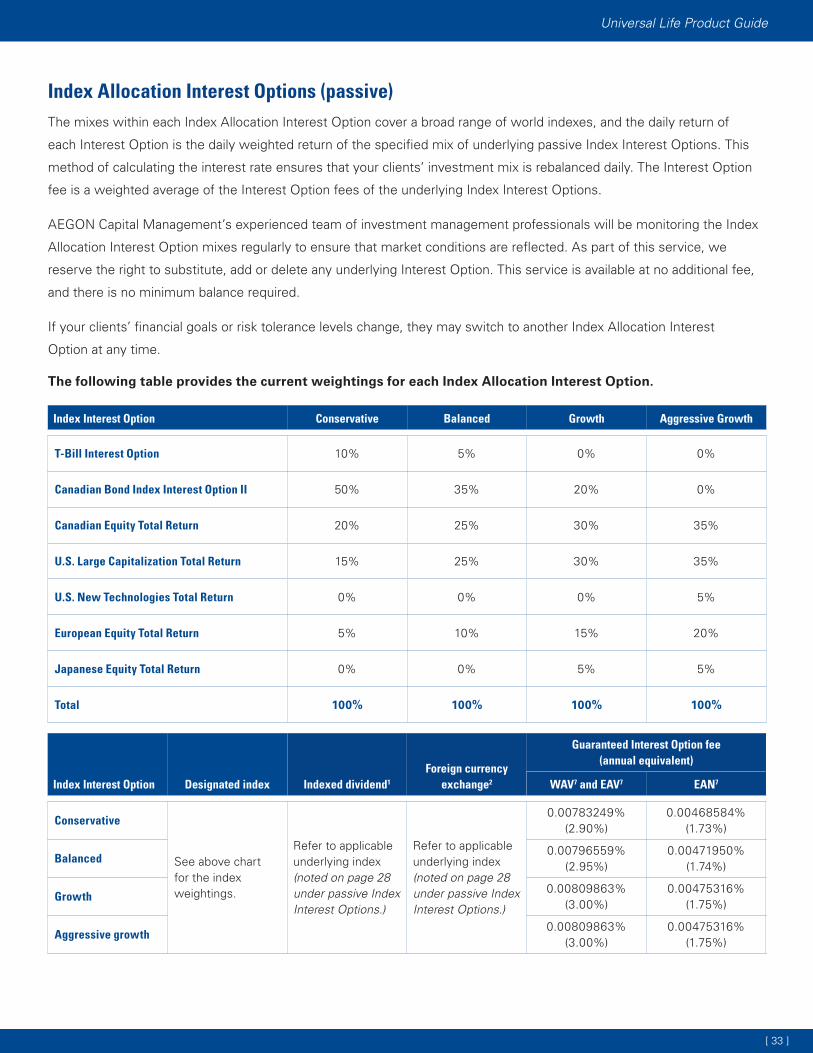

Index Allocation Interest Options (passive) 33

Managed Portfolio Options 34 imaxx TOP Portfolio Index Interest Options 34

Transamerica Interest Option fact sheets 35

Rates of return 35

Interest Option transactions 35 Allocation instructions 35 Interest Option transfers 35

4. Client bonuses 36

Meeting market needs with client bonuses 36

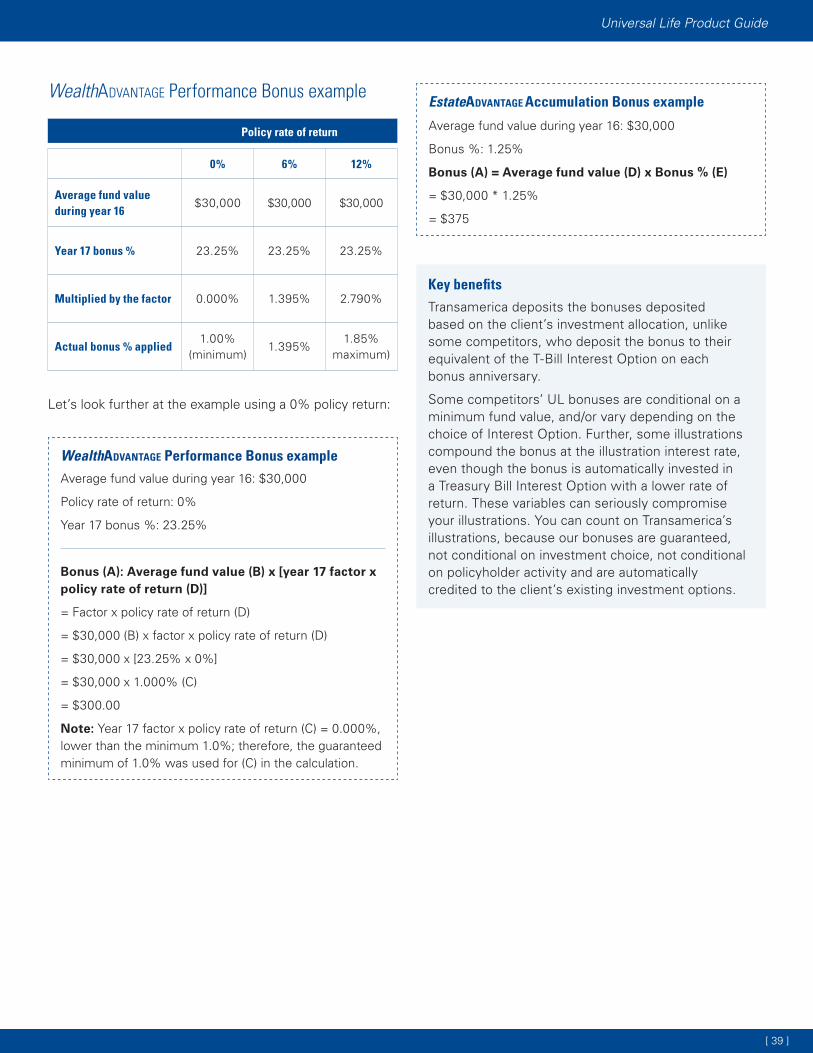

Different bonuses for different needs 36 WealthAdvAnTAge Performance Bonus 36 EstateAdvAnTAge Accumulation Bonus option 36 EstateAdvAnTAge low-fee option 37 A closer look at the universal life client bonuses 38 WealthAdvAnTAge Performance Bonus example 39

5. Optimizing investments while maintaining tax-exempt status 40

Tax-exempt testing and policy anniversary processing 40

Tax-exempt testing 40 If a policy fails a tax-exempt test 41 If a policy passes a tax-exempt test 41 The 250% rule (or “anti-dump-in” rule) 41

Maximum premium estimate 41 Recalculating maximum premium estimates) 42

Optimizer Option 42 Eligibility 42 How Optimizer works 42 Optimizing policies with multiple universal

life coverages 42 Changing the Optimizer option 43 Termination 43 Illustrating Optimizer on LifeView 43

Side Account 44 Side Account as a “safety net” 44

How the Side Account works 44

Universal Life Product Guide

6. Plan flexibility 45

Easy access to funds when needed 45 Policy loans 45 Policy and coverage surrenders 47 Withdrawal order 50 Taxation of loans, withdrawals and surrenders 50

Easy Interest Option changes when needed 51 Allocation instructions for premiums 51 Interest Option transfers 51 Market Value Adjustments (MVAs) 52

Premium flexibility 53 Planned periodic premiums 53 Minimum premiums 53 Maximum premiums 53

Easy insurance coverage adjustments when needed 54

Increasing the face amount 54 Decreasing the face amount 54 Death benefit option changes 54 COI option changes 54

7. Living Benefits 55

Qualification 55

Types of disability 55

Benefit amount 56

Payment of benefit amount 56

Face amount adjustment 56

Claims for Living Benefits 56 Occupational disability claim 56 Critical condition disability claim 56

Continuous disability 57

Living Benefits: Definitions and highlights 57

Exclusions for disability claims 58 General exclusions 58 Exclusions for pre-existing conditions 58

8. Optional Benefits 59

Accidental Death and Dismemberment Rider 59 Schedule of losses 59 Definition of “accident” 59 Termination 59 Exclusions 59

Children’s Insurance Rider 60 Coverage availability 60 Eligibility 61 Paid-up term insurance 61 Conversion 61 Coverage termination 61 Rider termination 61

Payor Waiver Riders 62 Payor Waiver of Monthly Deductions on Death

or Disability (PWMD) Rider 62 Payor Waiver of Planned Premiums on Death

or Total Disability (PWPP) Rider 62 Common terms and conditions for payor

waiver riders 63

Waiver Riders 64 Waiver of Monthly Deductions Rider 64 Waiver of Planned Premiums 65

9. Policy administration 67

Monthly deductions 67

Lapse and reinstatement process 67 Shortage 67 Key benefits 67 Lapse 67 Reinstatements 67

Anniversary statements and eStatement Library 68

Claims processing 68 Payment of death claims 68

Placing an order for marketing material or forms 69 Special note about edition dates 69 Other sources for marketing materials 69 Illustration systems (LifeView) 69

10. How to structure UL insurance for the market you are in 70

Guaranteed UL: Is it possible? 70

Using UL as an investment vehicle 70

Comparing and illustrating UL plans 70

Conclusion 72

Glossary of common terms 73

Index 75

Universal Life Product Guide

[ 1 ]

1. Product overviewFollowing is an overview of the coverages offered and some of the key options and features available with those coverages.

Insurance coverages Issue amounts and ages

Coverage options

• Single • Joint• Multiple Life

Minimum issue amounts

Wealth AdvAntAge

Estate AdvAntAge

Adults: Min. face amount

$100,000 $25,000

Max. face amount

$20,000,000 (ART COI)

$10,000,000 (Level COI)

$20,000,000 (ART COI)

$500,000 (Level COI)

Juveniles: (0 to 15)

Min. face amount

$25,000

(If an additional coverage; otherwise, the minimum face amount of $100,000 applies.)

$25,000

Joint life $100,000

Level COI Rider $100,000 $25,000

TermSelect Riders $50,000

Death benefit options

• Level (with ART COI only).• Increasing (with ART or level COI).

(Only one option can be selected per policy.)

Cost of Insurance (COI) option

• Annual Renewable Term (ART) to age 100.• ART 85/20.• Level COI.

Policy fee $10 per month; no extra charge for extra lives.

Premium tax None: built into cost of insurance.

Joint life

Joint life coverage options

Joint last-to-die

• Deductions to last death (up to 5 lives).• Deductions to first death (maximum 2 lives).• Fund value payout options on each death or last

death allowed on policies rated up to 300%.• Single life insurance option.

Joint first-to-die (up to five lives)

• Single life insurance option.• Survivor Option.• Additional death benefit.• Switch option from joint first-to-die to joint

last-to-die deductions to last death (two lives).

Issue ages (age nearest birthday)

Non-smoker: 0 to 80

Smoker: 16 to 80

(Non-smoker classification for juveniles)

Multiple UL coverages Underwriting

• Up to 15 insurance coverages.• Fund value payout options on each death, last

death or proportionate, allowed with insured rated up to 300%.

• Severance Option allows coverages to be severed from the policy but continue as issued.

• Change of primary life insured.

Underwriting programs

Non-medical underwriting program for face amounts below $250,000 and ages 45 and under.

Preferred underwriting program at $250,000 and above and ages 16+.

* The total face amount for all level cost of insurance coverages and Level Cost Riders for a life insured under all EstateAdvAntAge policies may not exceed $500,000.

Universal Life Product Guide

[ 2 ]

Riders Cost of Insurance bands

termSelect Rider

10-, 20- or 30-year renewable and convertible terms.

Band structure $25,000 to $49,999

$50,000 to $99,999

$100,000 to $249,999

$250,000 to $499,999

$500,000*(For TermSelect Riders only, there are additional COI bands of $500,000 to $999,999, $1,000,000 to $2,499,9999, and $2,500,000+.)

Combined banding combines face amounts of all non-joint universal life and rider coverages to determine underwriting program and requirements for each life insured.

Level COI Rider

Level (to 100)(available with level death benefit option only).

Investment choices

T-Bill Interest Option

Fixed-Rate Interest Options: One-, five- and 10-year terms (minimum $500).

Guaranteed minimum returns:

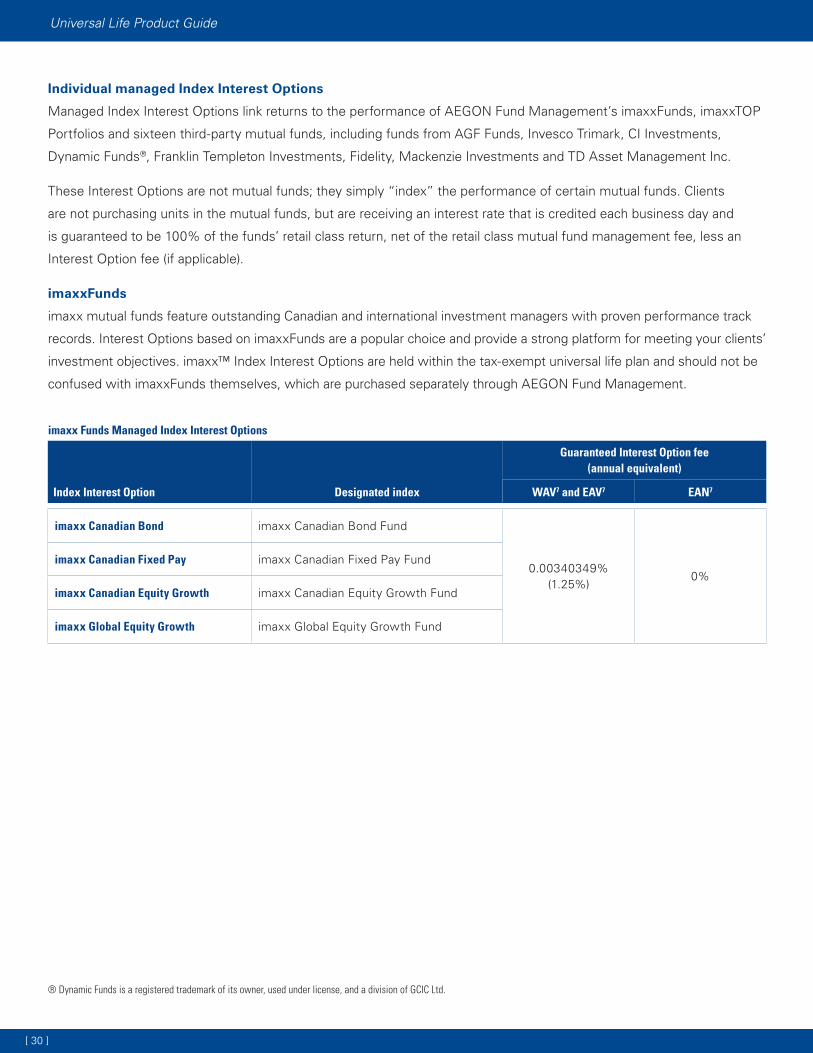

Individual Index Interest Options

Thirty-two Interest Options providing passive and managed solutions, including: • six passive total return Interest Options• four passive currency-neutral Interest Options• sixteen third-party managed options that index historically

consistent, above-average performance from managed investment Canadian mutual funds

• four imaxx mutual funds that feature outstanding Canadian and international investment managers with proven performance

Portfolio Index Interest Options

Eight Interest Options providing both passive and managed solutions, including:• four passive index allocation portfolio options• four managed imaxx TOP asset allocation options indexed to

top-performing Canadian, U.S. and international mutual funds

WealthAdvAntAge and

EstateAdvAntAge with Accumulation Bonus

EstateAdvAntAge with low-fee option

1-year: 0%5-year: 0.5%10-year: 1.5%

1-year: 0%5-year: 1.75%10-year: 2.75%

Client bonuses

WealthAdvAntAge EstateAdvAntAge

Performance Bonus

• Credited in years 2+.• Percentage tied to policy rate of return (with

guaranteed minimums).• Applied to the average fund value in the

previous year, net of loans.

Accumulation Bonus

• Credited in years 2+.• Fixed percentage (1.25%).• Applied to the average fund value in the

previous year, net of loans.

Low Fee • No bonus available.

Plan flexibility

Policy loans • 10% charged annual loan rate.• 8% credited annual interest rate on Security

Account.• Internal loan repayment provision available in

year 16.

Withdrawal order for monthly deductions

• Monthly Deduction Interest Option.• Policyowner picks one Interest Option;

otherwise, the default withdrawal order applies.

* The total face amount for all level cost of insurance coverages and Level Cost Riders for a life insured under all EstateAdvAntAge policies may not exceed $500,000.

Universal Life Product Guide

[ 3 ]

Plan flexibility (continued)

Surrender charges

WealthAdvAnTAge EstateAdvAnTAge

Duration: 10 years Duration: 7 years

Coverage surrender charges (also applies on face amount reductions).

Partial withdrawal surrender charges: a percentage of the withdrawal amount (minimum withdrawal $500).

10% free partial withdrawal

After the second anniversary, the client can withdraw up to 10% of the net fund value. The maximum amount available for a free surrender is equal to the lesser of:

• 10% of the net fund value• the net fund value, minus three monthly

deductions, minus half the total policy coverage surrender charges

Optimizer • Eligible with face amounts of $250,000 or more.• Earliest start is in year 6.• Maximum decrease of 15% over years 6 to 10.

Interest Option transfers

Four free transfers per policy year.

Optional benefits

Accidental Death and Dismemberment Rider

• Pays an additional benefit amount if the life insured dies or loses sight or limbs as a direct result of an accident (not available with joint life coverages).

Children’s Insurance Rider

• Provides low-cost term coverage on the lives of the life insured’s children (including stepchildren or legally adopted children).

• Allows each child to convert his or her coverage for up to five times the initial coverage amount, subject to certain conditions.

• Provides paid-up term insurance if the life insured dies before the children, prior to their 25th birthday (other conditions may apply).

Waiver and Payor Waiver of Monthly Deductions Rider

• Monthly deductions are waived for life if the insured becomes totally disabled before age 60, and between ages 60 and 65, monthly deductions are waived for the later of two years and age 65.

• Payor Waiver of Monthly Deductions Rider is also available to insure the payor on a child’s policy (usually a parent).

Waiver and Payor Waiver of Planned Premium Rider

• Premiums, up to a max. of $1,000 per month, are waived if the insured becomes totally disabled before age 65.

• The amount being waived will be the lesser of the average premiums paid during the 12-month period before disability and $1,000.

• Payor Waiver of Planned Premium Rider is also available to insure the payor on a child’s policy (usually a parent), up to $400 per month.

Built-in, no-cost additional benefits

Living Benefits Living Benefits enable your clients to access their fund value by making a request for a lump sum benefit amount upon disability. The policy definition of “disability” includes both (1) “occupational disability” and (2) “critical condition disability” (see contract for 26 covered conditions). There is no age restriction for this built-in feature, which uses new industry-standardized critical illness definitions.

Compassionate Assistance Program (CAP)

This non-contractual feature currently offered by Transamerica allows an owner to receive a loan against the death benefit of his or her policy if the life insured is suffering from a terminal illness and has a life expectancy of two years or less. Upon the death of the life insured, the death benefit payable to any beneficiaries will be reduced by the loan amount, accrued interest and any premiums waived after the loan was issued. (Living Benefit must first be exhausted.)

Universal Life Product Guide

[ 4 ]

Illustrations with face amounts above the stated maximum must be reviewed by Transamerica’s Head Office.

Any LifeView illustration above the stated maximum will not be valid without Head Office review, and a disclaimer

will be printed on the illustration report pages.

* The total face amount for all level cost of insurance coverages and Level Cost Riders for a life insured under all EstateAdvAntAge policies may not exceed $500,000.

** Preferred underwriting is automatically applied when the underwriting requirement or a life insured is $250,000 and greater and the insured is 16 years of age or older.

2. Insurance coveragesCoverage and rider issue ages and amounts

Coverage options

Minimum face amount Maximum face amountMinimum issue age

Maximum issue ageWealthAdvAntAge EstateAdvAntAge WealthAdvAntAge EstateAdvAntAge

Single life $100,000** $25,000**

$20,000,000 (ART COI)

$10,000,000 (Level COI)

$20,000,000 (ART COI)

$500,000* (Level COI)

0 80

$25,000 juveniles (ages 0 to 15)

Joint life $100,000**

Multiple life Minimum issue amounts apply based on single or joint coverages added as part of the multiple life coverage.

Rider Options

termSelect10Single life: $50,000**

Joint life: $100,000**

$10,000,000 0 70

termSelect20 $20,000,000 0 60

termSelect30 $20,000,000 0 50

Level Cost Rider

Single $100,000**

Joint $100,000**

Single $25,000**

Joint $100,000**$10,000,000 $500,000* 0 80

Universal Life Product Guide

[ 5 ]

Coverage types

Coverage types describe combinations of death benefit

and Cost of Insurance (COI) options, and the type selected

by the client is noted on the data page of each issued

policy and other Transamerica reports.

Only one death benefit option may be selected per policy.

Death benefit options

Both WealthAdvAnTAge and EstateAdvAnTAge provide level

and increasing death benefit options to reflect different

insurance needs and budgets. Regardless of the death

benefit option selected, the total death benefit is the Net

Amount at Risk (NAAR), defined below, plus the fund

value, less any outstanding policy loans, accrued interest

and premiums due.

However, with some of the Fund Value Payout Options,

the fund value may not always be included with each death

benefit. (See “Joint life coverages” or “Multiple universal

life coverages.”)

Only one death benefit option may be selected per policy.

Death benefit option COI options

Level death benefit ART to 85/20 years

Level death benefit ART to 100

Increasing death benefit ART to 85/20 years

Increasing death benefit ART to 100

Increasing death benefit Level to 100

Increasing death benefitThe death benefit includes the face amount (the amount

of insurance coverage selected), plus the fund value, less

any outstanding loans, accrued interest, withdrawals and

premiums due. The NAAR is equal to the face amount

selected at issue and remains constant, subject to tax-

exempt increases. (See “Tax-exempt testing” on page 40

for further details.)

This option is available with all COI options.

The fund value is paid upon death, in addition to the face

amount, unless a different Fund Value Payout Option is

specified. (See “Joint life coverages” or “Multiple universal

life coverages”.)

= NAAR

= Fund value

= Death benefit

Avoiding pitfallsThe death benefit is affected by the performance of the Interest Options. A negative interest rate will reduce the benefits and values under this policy, which include, but are not limited to, the total fund value, the cash surrender value, the net cash surrender value, the maximum benefit amount for a Living Benefit and the death benefit.

Potential marketFund Value Payout Options are available for increasing death benefit policies with multiple universal life coverages and/or joint last-to-die coverages.

Universal Life Product Guide

[ 6 ]

Level death benefitThis option is available only with ART COI.

This option keeps the face amount at a fixed, level amount

of coverage. Therefore, as the investment portion of the

plan grows, the NAAR decreases, which may result in

decreasing the COI over time.

During the COI period (varies with the COI option)The death benefit is equal to the face amount or the

proportionate fund value, whichever is greater. The

NAAR is equal to the face amount less the fund value.

As the fund value increases, the NAAR decreases, which

reduces the amount of insurance risk for which COI is

charged. The fund value is not guaranteed, and may

increase or decrease, depending on market conditions and

the volatility of the Interest Options chosen. The annual

renewable term (ART) COI rates per $1,000 of NAAR will

increase annually until age 100 (for ART to 100 COI) and to

the later of age 85 or 20 coverage years (for ART to 85/20).

Example: If the amount of insurance is $150,000 and the

allocated amount for that coverage is $25,000, the NAAR

is $125,000. The death benefit paid would be $150,000,

but monthly costs would be based on the guaranteed COI

rate, multiplied by the NAAR of $125,000.

After the COI period (varies with the COI option)The death benefit is equal to the NAAR as of the last day

of the COI period, plus the fund value. The face amount

is reset at the NAAR effective on the last day of the COI

period and fixed until the policy terminates. The death

benefit effectively switches to an increasing death benefit

= NAAR

= Fund value

= Death benefit

Avoiding pitfallsUnder the level death benefit option, after the end of the COI period (i.e., at the later of age 85 or 20 years, for ART to 85/20 years, or after reaching age 100), the death benefit effectively switches to an increasing death benefit option. Thereafter, the death benefit is affected by the performance of the Interest Options. A negative interest rate will reduce the total fund value and the death benefit. If the fund value has exceeded the original face amount, there may be no guaranteed face amount, and the death benefit will be entirely a function of the total fund value. Clients in this situation should consider switching to Fixed-Rate Interest Options and other low-risk options to minimize this risk.

On a multiple life policy with a level death benefit option, the proportion of the fund value paid with each death decreases the fund value. Also, the cost of any other coverages that have not yet reached the end of the COI period will continue to be deducted.

The face amount may increase under the level death benefit option where there are exempt-test face increases (page 41).

Potential marketThis plan design is especially efficient when clients have a level need for insurance protection and an increasing need for wealth accumulation.

In general, the level death benefit also makes insurance more affordable as the client ages, since the NAAR, and in many cases the total COI deducted, decreases as the fund value increases. However, this depends on the performance of the fund value and the applicable COI rates in later years.

Those who wish to minimize the COI in later years and who have decreasing insurance needs may consider the Optimizer feature (page 42).

option. The death benefit, thereafter, is affected by the

performance of the Interest Options. However, the death

benefit cannot fall below the reset NAAR.

Example: If the amount of insurance is $150,000 and the

amount allocated to that coverage is $160,000, the NAAR

would be zero. The death benefit paid would be $160,000.

Monthly COI costs would be zero.

Universal Life Product Guide

[ 7 ]

Key benefitsWith either universal life plan, clients may combine coverages with ART and coverages with level COI.

Potential marketART to 100 COI will appeal to clients with level or decreasing protection needs and long-term accumulation needs, especially when combined with the Optimizer Option. It provides them with the lowest COI in early policy years, which allows for faster fund accumulation.

ART to 85/20 COI is attractive for individuals who do not want to worry about the high COI charges after age 85 (or 20 coverage years, if later).

Both ART to 100 and ART to 85/20 COI should be used when the funding level is above the minimum premium and when the insurance need is expected to remain level or decrease over time.

Level COI is attractive for individuals who have a permanent insurance protection need.

Avoiding pitfallsWith ART COI, if the policy is in danger of going into shortage within a 12-month period of the anniversary, then:

• If paying by Pre-Authorized Debit (PAD) and paying minimum premiums, Transamerica will automatically increase the PAD amount each year to reflect the increased COI rates for that policy year. This is done to reduce the risk of the policy lapsing. We plan to inform clients about the increased amounts approximately 30 days prior to their policy anniversary. This automatic increase is explained in the PAD agreement in the Application and our current Request for PAD form. Please ensure your client reviews this component of the Application and understands the implications.

• If paying on a direct billing basis, Transamerica will automatically increase the amount displayed on the billing notice that is sent to clients approximately 20 days prior to their policy anniversary.

Cost of Insurance (COI) options

All of Transamerica’s COI options are fully guaranteed.

The following COI options are available:

• Annual renewable term (ART) COI with rates

increasing yearly on an attained-age basis. Rates for

the applicable coverage will be $0 at the end of the

applicable COI period:

– ART to 85/20: The COI period ends at the later of age

85 or 20 coverage years.

– ART to 100: The COI period ends at age 100.

• Level COI:* term to 100, with rates based on issue age.

Level rates are guaranteed for the COI period, to age

100, providing the insurance coverage does not change.

While the COI period ends at age 100, the coverage

remains in force thereafter until death.

Note that the level COI option is only available with an

increasing death benefit option.

Note that joint last-to-die, with deductions to first death,

is only available with an increasing death benefit with

level COI.

* The total face amount for all level COI coverages and Level Cost Riders for a life insured under all EstateAdvAntAge policies may not exceed $500,000.

Projected values on illustrations using ART are very

sensitive to investment returns. It is critical to illustrate at

conservative interest rates.

Universal Life Product Guide

[ 8 ]

Mixing COI optionsCOI options can be mixed when a policy is issued on

multiple lives. This can be illustrated on LifeView by

beginning with a base universal life coverage and then

adding a new coverage with a different COI option. Note

that level COI is only available with the increasing death

benefit.

Switching COI optionsIn some instances, we allow the COI option for a particular

coverage to be changed in a future year. (Please refer to

“Plan flexibility” in this guide for details.)

The COI factors are guaranteed for the life of the policy

unless there is a material change, such as a change of the

life insured or the total face amount per life insured.

The COI factors are expressed as a rate per $1,000 and

vary by gender, smoking status, preferred underwriting

classification (if applicable), amount of insurance and issue

age (attained age for ART) of the life insured.

The monthly COI is adjusted by any applicable ratings.

Monthly deductions include the monthly COI, rider costs

and the policy fee.

Built-in premium taxWith both WealthAdvAnTAge and EstateAdvAnTAge, the

COI factors include the provincial premium taxes, and we

guarantee that we will not charge your clients an additional

fee to cover any fluctuations in provincial premium tax. This

guarantee is spelled out in the contract and can be found in

Section 7: Monthly Deductions.

COI deductionsThe COI is calculated and deducted on a monthly basis from the tax-deferred fund value, regardless of the mode of premium payment. The monthly COI is calculated as the NAAR multiplied by the applicable annual COI factor (found in the policy data page of the contract), divided by 12. With the level death benefit option, the NAAR fluctuates from month to month; therefore, the COI will fluctuate in tandem.

COI bandingThe COI factor applicable to all coverages for a life insured

on any given month will vary, based on the total face

amount at the beginning of that month for that life insured.

To determine the appropriate COI band for a life insured,

we add the face amount of all coverages (including

TermSelect™ and additional coverage riders) for that life

insured. This “combined banding” approach can result in

a discount at higher face amounts. Please note that this

feature does not apply to joint life coverages.

COI bands

WealthAdvAntAge total face amount

EstateAdvAntAge total face amount

$25,000 to $49,999 juveniles $25,000 to $49,999 all ages

$50,000 to $99,999 juveniles $50,000 to $99,999 all ages

$100,000 to $249,999 $100,000 to $249,999

$250,000 to $499,999 $250,000 to $499,999

$500,000+ $500,000+

(Juveniles = 15 days to 15 years)

Key benefitsCombined banding and built-in premium tax are attractive COI features that are rare in the industry. Most of our competitors charge the provincial premium tax on the full premium, even on the deposits in excess of the COI.

Underwriting programs

(These rules are applicable to all Transamerica life

insurance products.)

Transamerica offers two underwriting programs:

• non-medical

• medical

Universal Life Product Guide

[ 9 ]

Age Face amount

0–16 <$500,000

17–45 <$250,000

46–55 <$100,000

56+ Not available

Age Face amount

0–16 $500,000+

17–45 $250,000+

46–55 $100,000+

56+ All face amounts

In order to qualify for non-medical underwriting, the proposed

insured must have lived in Canada for at least 12 months.

RequirementsThe current Long Form Application (LP257) is required.

Note that Transamerica reserves the right to request

additional medical requirements for any proposed insured

(such as blood and urine testing, physician’s report,

medical examination, etc.) based on the initial assessment

of the application.

If it is determined by the underwriter that any of the above

four medical requirements are necessary, the applicant will

fall under what we call “medical underwriting.”

MisrepresentationIt’s important to ensure that the questions on the

application and any questionnaires are answered truthfully

and completely. Any misrepresentation can lead to voided

contracts and unpaid claims.

Medical underwriting also applies where the underwriter

assesses the need for further information about a client,

based on the information provided on the Long Form

Application for non-medical underwriting.

MisrepresentationIt’s important to ensure that the questions on the

application and any questionnaires are answered truthfully

and completely. Any misrepresentation can lead to voided

contracts and unpaid claims.

RequirementsThe Long Form (LP257) or Short Form (LP411) Application

can be used for medical underwriting. While the Long

Form Application is not required, it can help provide the

underwriter with more complete knowledge about your

client, which can result in faster underwriting and a better

rate for your client.

Tip: Providing complete details for all questions that are

answered with a “yes,” and ensuring that your application

is in good order, can help the underwriter to quickly make a

decision and avoid processing delays.

Medical underwriting“Medical underwriting” means the proposed insured’s

insurability will be assessed by the underwriter based on

the information provided in a Life Insurance Application,

along with specific medical requirements.

Face amount and age availabilityMedical underwriting applies as follows:

Non-medical underwritingOur non-medical approach to underwriting is designed

for ease – making it easier for your clients to get the

protection they need for themselves and their families,

while making it easier for you to do business. Providing

a better experience for your clients, quicker processing

of applications and speedy delivery of policies, our

non-medical approach makes it easy to recommend

Transamerica Life Canada.

Face amount and age availabilityOur convenient non-medical underwriting applies as follows:

Universal Life Product Guide

[ 10 ]

Overview of required formsFor more information on requirements for our underwriting programs, refer to Transamerica’s

Underwriting Handbook (LP1393).

Underwriting risk classificationsWe offer five underwriting risk classifications:

We will offer cigar smokers standard non-smoker rates if the cigar use is limited to 12 cigars per year and the urine test

results are negative for cotinine (nicotine). For those qualifying for non-medical underwriting, a urine test is not needed.

Elite non-smokersPreferred non-smokers

Standard non-smokers Preferred smokers Standard smokers

Tobacco use

Have not used cigarettes, cigarillos (little cigars), cigars, pipe, shisha/hookah (water pipe), nicotine patch, Nicorette® chewing gum or any other smoking cessation products, marijuana, hashish, betel nuts, snuff or tobacco in any other form in the last 24 months.

Have not used cigarettes, cigarillos (little cigars), cigars, pipe, shisha/hookah (water pipe), nicotine patch, Nicorette® chewing gum or any other smoking cessation products, marijuana, hashish, betel nuts, snuff or tobacco in any other form in the last 12 months.

Do not use tobacco products.

Smoke more than 12 cigars per year, use a pipe or chewing tobacco, but do not use any other tobacco products.

Are users of tobacco products.

HealthExcellent medical and non-medical history.

Good medical and non-medical history.

Average medical and non-medical history.

Good medical and non-medical history.

Average medical and non-medical history.

LifestyleStatistically “excellent risks.”

Statistically “good risks.”

Statistically “average” risks.

Statistically “good risks.”

Statistically “average” risks.

Underwriting program Application required Additional requirements

Non-medical

A current Long Form Application (LP257) must be completed.*

Be sure to provide complete details on the application, particularly for any “yes” answers.

Include a cover letter or use the remarks section if you need more room.

Medical

Current Short Form Application (LP411) can be used.*

The Long Form Application (LP257) may also be used, and can help to provide more details to the underwriter, which can result in speedier processing of your application. It could help you manage your client’s expectations with regards to the risk classification the underwriter applies.

Refer to the Underwriting Requirements Chart (LP501).*

* To determine the most current edition of our applications, visit Transamerica’s website at www.transamerica.ca or click on Marketing Materials/Forms and Applications in our LifeView illustration software.

® NICORETTE is a registered trademark of the GlaxoSmithKline Group of Companies.

Universal Life Product Guide

[ 11 ]

Preferred and elite underwriting risk classesPreferred underwriting is automatically applied when the underwriting amount* for a life insured is $250,000 and greater

and the insured is 16 years of age or older.

For preferred underwriting, we consider facts that go beyond the gender and smoking habits of your clients. We look

at other health-related factors, such as physical build, lifestyles and personal and family health history, to consider their

eligibility for an elite, preferred or standard classification. If your clients have a longer life expectancy, based on these

factors, our preferred underwriting program can substantially reduce their life insurance premiums.

Summary of underwriting program and applicable risk classification by age and face amount

Age Face amount Applicable underwriting program Applicable risk classifications

0–16<$500,000 Non-medical

Standard non-smoker$500,000+ Medical

17–45

<$250,000 Non-medicalStandard non-smoker

Standard smoker

$250,000+ Medical

Elite non-smoker

Preferred non-smoker

Standard non-smoker

Preferred smoker

Standard smoker

46–55

<$100,000 Non-medical Standard non-smoker

Standard smoker$100,000–$249,999 Medical

$250,000+ Medical

Elite non-smoker

Preferred non-smoker

Standard non-smoker

Preferred smoker

Standard smoker

56+

<$250,000

Medical

Standard non-smoker

Standard smoker

$250,000+

Elite non-smoker

Preferred non-smoker

Standard non-smoker

Preferred smoker

Standard smoker

* The underwriting requirements and amount are based on the total amount of life insurance for a particular life insured, including single life and joint life coverages and riders (within 6 months).

Universal Life Product Guide

[ 12 ]

INSURED 1 INSURED 2

Coverage 1

Single life universal life for $200,000

Coverage 2

Single life TermSelect

$70,000

Coverage 3Single life

universal life for $180,000

Insured 2 is eligible for a preferred or elite underwriting risk classification, because the total amount of life insurance ($70,000 + $180,000) is $250,000, and therefore qualifies for preferred or elite.

Insured 1 is not eligible for a preferred or elite underwriting risk classification, as the total amount of life insurance is $200,000, and preferred and elite underwriting risk classification begin at $250,000 and greater.

Underwriting requirementThe underwriting requirement is based on the total amount

of life insurance for a particular life insured on one policy,

including single life and joint life coverages, as well as

riders (Level Cost and TermSelect Riders).

Example

Underwriting materialsThe following is a list of underwriting materials that can be

ordered through our icanorder website. Some materials

are only available in PDF format, and are available online

through our Transamerica.ca website or through our

illustration software, LifeView.

Avoiding pitfallsIn this example, if Insured 2 cancelled the TermSelect rider, this would drop the sum insured below the $250,000 amount, and thus the preferred rate classification for the remaining coverage (coverage 3) would no longer apply, and Insured 2 would be paying non-preferred rates from then on.

Avoiding pitfallsAs determining the appropriate class can only be done after all evidence has been submitted and assessed, it is recommended you use care when speaking to your clients about their risk classification, so as best to manage your client’s expectations and to avoid potential disappointments. While it is all right to let them know there’s a possibility that they may qualify for a preferred or elite underwriting risk classification – if you indeed think that they will be eligible – it is still best to provide quotes for only the standard classes. This helps prevent the client from being disappointed if the premium quoted later is higher, because they did not qualify for the better risk classification.

Form numberAvailable for order

or through Transamerica.ca

Long Form Life Application

LP257 Order

Supplement to the Life Insurance Application – also automatically populated in LifeView with illustration.

LP343Website

(PDF only)

Underwriting Age and Amount Requirements Chart

LP501Website

(PDF only)

Underwriting Handbook LP1393 Order

RatingsWhat is a rating?Certain factors such as our gender, age, family history,

current conditions, lifestyle choices and whether or not we

smoke can impact when we are likely to die. Depending

on these factors, one individual may have a greater risk of

dying earlier than another. If there is an increased risk of

an individual dying earlier than normal, then the individual’s

mortality is also considered to be higher than normal. To

offset that risk, an individual who presents a greater than

average risk with regards to mortality, may be charged a

higher premium rate. In the insurance industry, individuals

with a higher mortality are said to have Extra Mortality.

Universal Life Product Guide

[ 13 ]

The increased risk, and thus the extra premium charged,

of an individual is quantified using one of two methods:

• Extra percentage tables; and

• Permanent and temporary flat extra premiums

Extra percentage tablesWhen there are health issues, for example, elevated

blood pressure, the extra percentage tables are used.

The increased risk or Extra Mortality, of an individual is

quantified as a percentage where 100% represents the

normally expected health risk (mortality). This percentage

is then applied to the standard premium or cost of

insurance.

As an example, consider two individuals, Anne and Sally.

Both are female, both age 35 and both are non-smokers.

However, Anne has a health condition, which increases

her risk of dying sooner compared to Sally, who is healthy.

Thus, Anne would receive a rating for elevated mortality.

Say that Anne’s health condition has a rating of 50%, this

would mean Anne’s insurance policy would carry a rating

of 150% (100% Normal Mortality + 50% Extra Mortality).

If Anne’s health condition improves over time, the rating

may be reduced or removed if she applies to have it

reviewed and if the underwriting is favourable with

regard to the entire medical history. An application for a

rating review can be made at least two years after the

rating was applied.

In some cases, when the risk is particularly high (typically

higher than 400%), an insurance company may not be

prepared to assume the risk and the proposed insured

may be declined.

Permanent and temporary flat extra premiumsPermanent

This approach calls for a fixed extra premium per

thousand dollars of sum insured/face amount over and

above the standard premium charge. The additional

mortality risk is likely to be present over a certain

period of time.

For example, Bob has a history of reckless driving and

has received five speeding tickets over the last two years.

Because those who drive recklessly are more likely to die

sooner than those who don’t, Bob will receive a rating.

If Bob changes his driving habits and no longer speeds,

he may apply after two years to have the rating removed

or decreased.

Some avocations such as scuba diving or mountain

climbing could draw an extra premium for the life of the

policy or until the lifestyle of the insured has changed and

an application is made to have it removed.

Temporary

Similar to permanent, this approach also calls for a fixed

extra premium per thousand dollars of sum insured/face

amount over and above the standard premium charge.

However, unlike a permanent flat extra a temporary flat

extra is on a temporary basis or a designated period of

time. The extra premium may only be charged for a fixed

number of years.

For example, Gary is a hobby pilot and does not have

enough experience time according to his record. In two

years, he will have achieved his required number of

experience hours. So, Gary receives a temporary rating for

those two years, which will drop off automatically without

the need for application or review.

Reconsideration of ratings and declinesIf your client receives a rating, he or she may be eligible for

future reconsideration of that rating. Likewise, if your client

has been declined, there may be circumstances under

which we would review that decision. Reconsideration will

only be possible if the overall medical history and lifestyle

has improved.

Universal Life Product Guide

[ 14 ]

Policies with multiple universal life coverages

Multiple universal life coveragesWith WealthAdvAnTAge and EstateAdvAnTAge, more than one

universal life coverage can be included under the same

policy without any additional policy fee.

Each coverage must satisfy the minimum and maximum

face amount requirements. (See “Coverage and rider

issue ages and amounts” on page 4.)

The main difference between multiple universal life

coverages and a Level Cost Rider (see “Riders” on

page 24 for more information) is that when calculating

the death benefit or NAAR, no fund value is attributed

to the face amount payable for the Level Cost Rider.

As well, no surrender charges are applicable for additional

coverage. Since there are no surrender charges associated

with riders, the maximum tax-exempt room is lower than

when using UL coverages.

Within the universal life contracts, a “primary life insured”

is someone who is insured under a universal life coverage.

There may be several “primary life insureds” on a policy

having multiple universal life coverages.

In general, upon the death of any life insured, his or her

death benefit will be paid to the beneficiary specified

for that coverage, and the policy will continue with the

remaining lives insured, provided at least one primary life

insured is surviving.

Under the level death benefit option, the fund value that is

attributed to each coverage in order to calculate the NAAR

and the associated COI is determined proportionately,

based on the face amount for each coverage.

The policy matures when the last universal life coverage

terminates.

Only one death benefit option may be selected per policy.

Good to knowGenerally percentage and permanent extra premiums can only be reviewed after two years and new medical evidence will be required. The change of the rating is subject to the new evidence received and the assessment by the underwriter at that time.

Good to knowFor joint life policies, for the rating of any of the lives to be reviewed, new medical evidence is required on all lives insured. The rating reconsideration may be declined if any of the lives insured are no longer in the same risk class as when the policy was originally issued.

Good to knowFor the review of certain lifestyle ratings, such as those related to an avocation, we will request only the appropriate questionnaires and will not require medical requirements or information. For other ratings, however, we will complete a full review, which can include medical, financial, travelling and lifestyle underwriting.

Reconsideration of medical ratings is not always possible.

Some conditions are unlikely to improve over time. For

example, consider Type 1 diabetes (insulin dependent).

The longer the client has Type 1 diabetes, the greater the

risk of complications and thus the greater the mortality.

As such, Type 1 diabetic ratings are unlikely to be eligible

for reduction in subsequent years.

Knowing that reconsiderations may be a possibility will

help you deliver the rated policy to your client. It will also

provide you with a basis to follow up with your client in

the future with the chance to review the rating or to turn

a declined individual into a client (insured).

Universal Life Product Guide

[ 15 ]

Base universal life coverageThere are certain privileges attributed to the base universal

life coverage. For example, on a multiple life policy, the

Optimizer Option will reduce the face amount for the base

universal life coverage only. As well, some riders and

optional benefits are only available with the base universal

life coverage, such as the Children’s Insurance Rider. The

base universal life coverage is usually indicated as “Life 1”

on the life insurance application or “Base Coverage” on the

LifeView illustration software.

Key benefits• Only one policy fee applies.

• The investment component is conveniently administered through centralized policy Interest Options.

• Premium billing and policy administration are applied to the entire policy, rather than to each life insured.

• Up to 15 coverages (any combination of base coverages and riders) can be included under one policy, including the support of up to five lives on joint first-to-die coverages.

• The policyowner can assign separate beneficiaries for each coverage under the policy.

• If your clients select the increasing death benefit option, they may have either ART or level COI options for different lives.

• Any coverage can be severed from the original policy and continued under a different policy, at any time. (See “Severance Option.”) A policy fee will be added to a severed coverage under its own policy.

• A life insured for a specific coverage can be changed (See “Change of Primary Life Insured Option.”)

Potential marketMultiple life coverages are attractive to both businesses (corporations and partnerships) and families, because they offer great flexibility, without additional policy fees.

Multiple life special optionsFund Value Payout OptionsUnless a different Fund Value Payout Option is specified,

the death benefit will include the applicable proportionate

fund value, based on the total face amount for the life

insured. Proportionate fund value payout is specified in

the contract and does not require a separate contract

endorsement.

Alternate Fund Value Payout Options are available at time of

issue with an increasing death benefit option. Transamerica

offers Fund Value Payout Options for all lives who are

issued without a rating or are rated up to a maximum of

300%. The Fund Value Payout Options must be illustrated

with LifeView and specified on the Supplement to the Life

Insurance Application. These options are added to the

policy as contract endorsements and will be specified on

the data page and policy statement.

Depending on the option selected, in addition to the face

amount for each coverage, the death benefit will be as

follows:

• Proportionate: The proportionate fund value is payable

upon each death (default).

• Each death: The total fund value, less three monthly

deductions, is payable upon each death (minimum

$500 payout).

• Last death: The total fund value is payable at last

death only.

Universal Life Product Guide

[ 16 ]

Insured 1 Insured 2 Insured 3

Face amount $200,000 Face amount $100,000 Face amount $100,000

Total fund value = $80,000 at date of deathMonthly deduction = $1,000

Example of how Fund Value Payout Options work:

Example of proportionate fund value payout

Insured 1 Insured 2 Insured 3

Proportionate fund value $40,000 Proportionate fund value $20,000 Proportionate fund value $20,000

If Insured 1 dies first, the death benefit = $240,000

If Insured 2 dies first, the death benefit = $120,000

If Insured 3 dies first, the death benefit = $120,000

Each death

Insured 1 Insured 2 Insured 3

Death benefit = face amount + total fund value – 3 monthly deductions

If Insured 1 dies first, the death benefit = $277,000

If Insured 2 dies first, the death benefit = $177,000

If Insured 3 dies first, the death benefit = $177,000

Last death

Insured 1 Insured 2 Insured 3

If Insured 1 dies first, the death benefit = $200,000

If Insured 2 dies second, the death benefit = $100,000

If Insured 3 dies last, the death benefit = $100,000 + fund value

Universal Life Product Guide

[ 17 ]

Multiple extras or table ratingsFund Value Payout Options are available for cases rated

with a total mortality equal to 300% or less.

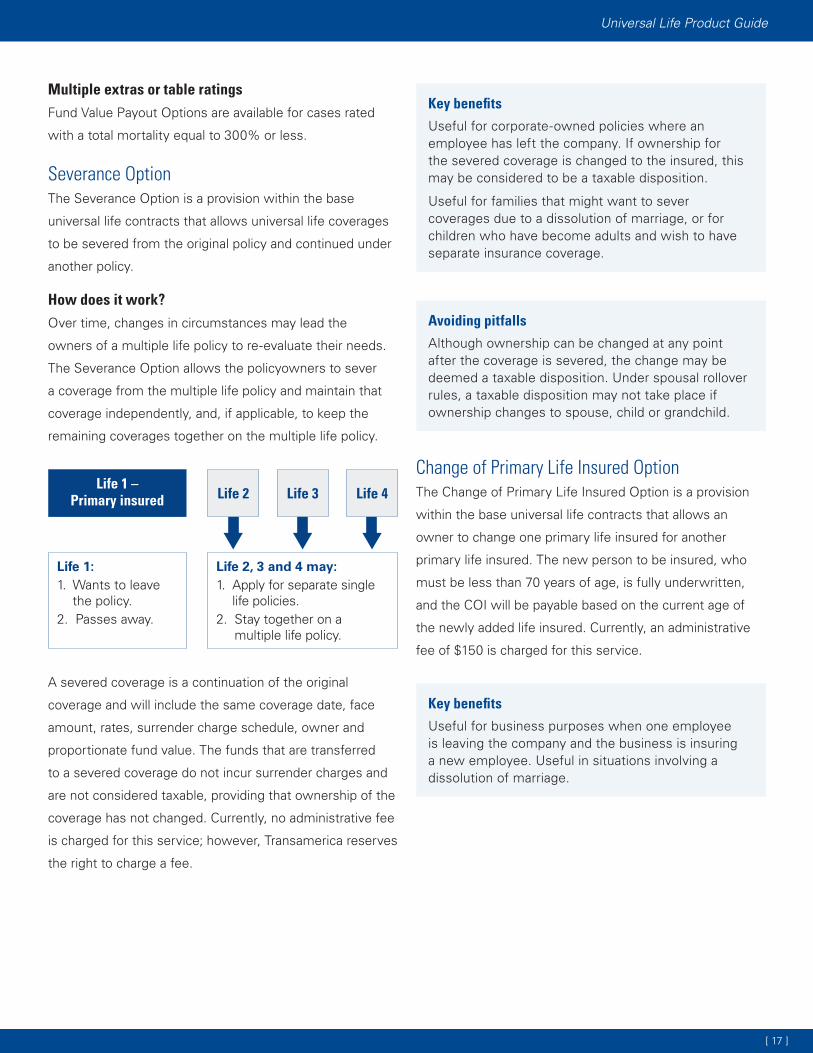

Severance OptionThe Severance Option is a provision within the base

universal life contracts that allows universal life coverages

to be severed from the original policy and continued under

another policy.

How does it work?Over time, changes in circumstances may lead the

owners of a multiple life policy to re-evaluate their needs.

The Severance Option allows the policyowners to sever

a coverage from the multiple life policy and maintain that

coverage independently, and, if applicable, to keep the

remaining coverages together on the multiple life policy.

Change of Primary Life Insured OptionThe Change of Primary Life Insured Option is a provision

within the base universal life contracts that allows an

owner to change one primary life insured for another

primary life insured. The new person to be insured, who

must be less than 70 years of age, is fully underwritten,

and the COI will be payable based on the current age of

the newly added life insured. Currently, an administrative

fee of $150 is charged for this service.

A severed coverage is a continuation of the original

coverage and will include the same coverage date, face

amount, rates, surrender charge schedule, owner and

proportionate fund value. The funds that are transferred

to a severed coverage do not incur surrender charges and

are not considered taxable, providing that ownership of the

coverage has not changed. Currently, no administrative fee

is charged for this service; however, Transamerica reserves

the right to charge a fee.

Life 2 Life 3 Life 4Life 1 –

Primary insured

Life 1:1. Wants to leave

the policy.2. Passes away.

Life 2, 3 and 4 may:1. Apply for separate single

life policies.2. Stay together on a

multiple life policy.

Key benefitsUseful for corporate-owned policies where an employee has left the company. If ownership for the severed coverage is changed to the insured, this may be considered to be a taxable disposition.

Useful for families that might want to sever coverages due to a dissolution of marriage, or for children who have become adults and wish to have separate insurance coverage.

Key benefitsUseful for business purposes when one employee is leaving the company and the business is insuring a new employee. Useful in situations involving a dissolution of marriage.

Avoiding pitfallsAlthough ownership can be changed at any point after the coverage is severed, the change may be deemed a taxable disposition. Under spousal rollover rules, a taxable disposition may not take place if ownership changes to spouse, child or grandchild.

Universal Life Product Guide

[ 18 ]

Key benefitsOn a joint last-to-die basis, there is usually a lower COI, compared with single life coverage on either of the individuals.

On a joint first-to-die basis, there is usually a lower COI, compared to the total cost of separate coverages on each life (e.g., one joint face amount of $500,000, versus having two separate coverages with face amounts of $500,000 each). For example, say a husband and wife ages 35 and 30, respectively, who are both non-smokers, require $500,000 of level life insurance. The cost for separate coverages is $2,995 and $1,950; if they purchase a joint-first-to-die universal life plan, the cost would be $3,875. These costs do no reflect the policy fee.

On each joint coverage, up to five lives can be supported.

Potential marketTraditionally, joint life coverages have been used in family situations: joint first-to-die is used for income protection needs, and joint last-to-die is used for estate planning needs.

There is an increasing trend toward using joint life coverage to insure business interests. For example, joint first-to-die can be used to fund a buy-sell agreement, or for key person insurance.

Joint life coverages

Transamerica’s universal life contracts can also be issued

with joint first-to-die or joint last-to-die coverages. Joint

life coverages are provided as an endorsement to the

contract. The lives insured under a joint life coverage, the

joint insureds, share a single death benefit, and the lives

are combined to produce a Single Equivalent Age (SEA)

and underwriting class for the purpose of calculating the

COI. Joint life coverages may be combined with single

life coverages on one universal life policy. We require

a minimum face amount of $100,000 for each joint life

coverage. In the event of simultaneous deaths, or where

the sequence of deaths cannot be determined, the death

benefit will be divided by the number of the deceased

joint insureds. Joint last-to-die and joint first-to-die

coverages are identified on the contract data page with

the applicable SEA.

Optional benefits, including the Accidental Death and

Dismemberment Rider, the Waiver Rider and the Payor

Waiver Rider, are not available with joint life coverages.

The Children’s Insurance Rider is available on the first

life of a joint first-to-die coverage, providing this coverage

is the base universal life coverage (identified as Life 1 in

the application).

Joint last-to-dieJoint last-to-die universal life coverages are available with

two options for deductions: deductions to first death and

deductions to last death.

The deduction option must be specified on the LifeView

illustration report that is submitted to Transamerica,

as well as on the Supplement to the Life Insurance

Application. This option is added to the policy as a contract

endorsement and is displayed on both the data page and

on the policy statement.

Instead of using different insurance rates for these two

options, different SEA formulas are used. Deductions to

last death is less expensive (based on a younger single

equivalent age) than deductions to first death. The Fund

Value Payout Options and the Single Life Insurance Option

are available with both deductions to first death and

deductions to last death. However, you may not combine

deductions to first death with deductions to last death on

one contract.

Refer to the “Glossary of common terms” for a definition

of SEA.

Universal Life Product Guide

[ 19 ]

Deductions to first deathThis option is only available on a base universal life joint

last-to-die coverage with level COI and an increasing death

benefit. This option is limited to two lives, with each joint

insured being between 18 and 80 years of age; neither of

the joint insureds may be a substandard risk. When this

option is selected and the first joint insured dies, insurance

charges for this joint last-to-die coverage cease.

Deductions to last deathThis option is available for any joint last-to-die coverage and

includes up to five lives, including substandard lives. When

this option is selected, insurance charges are applicable for

this coverage until the death of the last life insured.

Fund Value Payout Options These options are available only at time of issue, on

policies with one joint last-to-die universal life coverage

with an increasing death benefit option, issued without

ratings, or where a joint life insured is rated up to a

maximum of 300%.

The Fund Value Payout Options must be specified on

the LifeView illustration report that is submitted to

Transamerica and specified on the Supplement to the Life

Insurance Application.

These options are added to the policy as contract

endorsements and will be specified on the data page and

policy statement. If the client does not specify an option,

“last death” will be selected automatically as the default.

Avoiding pitfallsIf the policy only includes one joint last-to-die with deductions to first death, upon the death of a joint insured, no further monthly deductions, including the policy fee, will be deducted. However, the deductions to first death option does not cover insurance costs for multiple life coverages, additional coverage riders and optional benefits that are included on the same policy. It only covers the COI for the applicable joint last-to-die coverage. As well, for policies with multiple universal life coverages, the policy fee will continue as long as deductions are taken from the fund value for the other insurance coverages, optional benefits and riders.

If a potential joint insured is rated during the underwriting process, the joint last to-die with deductions to first death coverage will not be available. However, joint last-to-die with deductions to last death may be issued.

* These administrative rules are non-contractual and are subject to change and other criteria based on administrative guidelines in effect on the date of the request.

Potential marketA joint last-to-die policy with deductions to first death is attractive for estate preservation, covering the COI for the surviving insured, and is often purchased in combination with the “each death” Fund Value Payout Option (see following section).

Switching between joint last-to-die deduction options*

From To Administrative rules

Deductions to first death

Deductions to last death

• No underwriting is required.

• Signed illustration with new SEA based on attained ages.

• Up to five lives.

Deductions to last death

Deductions to first death

• Underwriting is required: Part 2 of Policy Change Application (LP386).

• Signed illustration with new SEA based on attained ages.

• Level COI (only after change).

• Available with two lives.

• No substandard risk.

ART to 100 level COI deductions continue to SEA age 100, and ART 85/20 to the later of age 85 of SEA and 20 years.

Universal Life Product Guide

[ 20 ]

Single Life Insurance OptionThis option is included in both joint last-to-die

endorsements (deductions to first death and deductions to

last death), and is available at no extra charge. It allows a

joint last-to-die universal life coverage to be split into two

or more separate coverages (depending on the number

of joint lives insured under the original coverage) without

further evidence of insurability. The split coverage is a

continuation of the original coverage. The proportionate

fund value will be transferred to each of the split coverages

without incurring surrender charges. This transfer should

not trigger taxation, providing that ownership has not

changed. (See “Avoiding pitfalls” under “Multiple Life

Special Options: Severance Option” on page 17.)

Multiple extras or table ratingsFund Value Payout Options are available for insureds rated

with a total mortality equal to 300% or less.

Key benefitsWith each Fund Value Payout Option, a different beneficiary can be specified for the fund value and for the face amount. In this way, for example, the children may be designated as beneficiaries for the face amount to offset estate taxes, and the surviving spouse may be designated as beneficiary for the fund value to help cover funeral expenses and other costs. This can be specified in the general comments section of the Life Insurance Application or provided to Transamerica as a letter from the owner.

Example of “each death” Fund Value Payout Option

Insured 1 Insured 2

Face amount: $500,000Monthly deduction = $500Total fund value = $50,000

Total fund value – 3 monthly deductions = $48,500Remaining policy fund value = $1,500

Insured 1 dies

Example of “last death” Fund Value Payout Option

Insured 1 Insured 2

Face amount: $500,000Monthly deduction = $500Total fund value = $50,000

No fund value is paid out. The face amount and total fund value

are paid at last death.

Insured 1 dies

Life 1 $500,000 Life 2 $500,000

Life 1 – Life 2 (up to five)$1,000,000 payable on first death

Divorce or dissolution of a business partnership

Depending on the option selected, in addition to the face

amount for each coverage, the death benefit is as follows:

• last death: the total fund value at last death (default)

• each death: the total fund value, less three monthly

deductions, upon each death (minimum $500 payout),

with the remaining fund value paid at the last death

Universal Life Product Guide

[ 21 ]

This special option is similar to the Multiple Life Severance

Option and the joint first-to-die Single Life Insurance

Option. The most significant differences are that with the

joint last-to-die version, the split may only occur subject to

the specified contingent events, and the NAAR is allocated

equally among the joint insureds.

Eligibility

• Must be exercised prior to age 70 of the oldest of the

joint life insureds.

• Not available if any of the joint lives are issued as

substandard risks.

• Although no medical evidence of insurability is required,

we reserve the right to financially underwrite any one

of the joint insureds prior to the time the new policy

takes effect. Please refer to a sample contract for the

detailed terms.

Contingent events

• Within 180 days of a Certificate of Divorce being issued

for the joint life insureds.

• On the dissolution of the corporation or partnership,

except in the case of bankruptcy, providing that the

coverage was being used to fund a bona fide purchase

obligation under a written partnership or shareholder’s

agreement, contingent on the death of a joint insured.

Terms of the Single Life Insurance Option

• The current coverage date is used.

• The maximum death benefit is the lesser of the original

face amount divided by the number of joint lives insured

and $1,000,000 (for amounts that exceed $1,000,000,

underwriting is required).

• Original rates apply, based on attained age.

Key benefits

• Provides future flexibility in case of dissolution of

marriage or business dissolution.

Joint first-to-dieSurvivor OptionThis option is included in the joint first-to-die endorsement

and is available at no extra charge. Within 90 days of the death

of the first joint insured, the surviving insured(s) may apply

for single insurance coverage without medical evidence

of insurability. The new insurance coverage is based on

current age and rates and uses the current issue date.

Eligibility for exercising the option

• Not available for substandard risks.

• Not available if any of the surviving joint insureds

have reached age 70.

• Available within 90 days of the date of death of the

first to die.

• Available if the policy was in force and all monthly

deductions have been paid to the date of death of

the first to die.

Terms of new insurance policy

• Same plan of insurance.

• Maximum face amount for each joint insured is the

NAAR applicable for the original coverage immediately

prior to the date of death of the first to die.

• The new policy will take effect on the 90th day following

the date of death of the first to die, providing at least

three monthly deductions have been received.

• An annual policy fee will apply.

Life 1 $1,000,000

Life 3 $1,000,000

Life 4 $1,000,000

Life 1 – Life 2 – Life 3 – Life 4$1,000,000 payable on first death

Death of Life 2

Universal Life Product Guide

[ 22 ]

Additional death benefitThe additional death benefit is included in the joint first-

to-die endorsement and is available at no extra charge.

It provides for an additional death benefit to be paid,

providing that the second death occurs within 90 days

of the first death and is not the result of suicide or self-

inflicted injury. Single Life Insurance OptionThis option is included in the joint first-to-die endorsement

and is available at no extra charge. This option allows

a joint first-to-die universal life coverage to be split into

two or more policies (depending on the number of joint

lives insured under the original coverage) without medical

evidence of insurability.

The split coverage is a continuation of the original

coverage. The proportionate fund value will be transferred

to the split policy without incurring surrender charges.

This transfer should not trigger taxation, provided that

ownership has not changed. (See “Avoiding pitfalls” under

“Multiple Life Special Options: Severance Option.”)

Eligibility for exercising the option

• Not available if any of the joint lives insured under the

applicable coverage are substandard risks or are 70

years of age or older at issue of the original policy.

• Not available if an application for a new life insurance

policy was made for the surviving insureds.

Subject to the terms of the additional death benefit.

• Not available if either death is the result of suicide or

self-inflicted injury.

• The additional death benefit is equal to the NAAR

applicable for the joint first-to-die coverage at the time

of the first death.

• It excludes any additional benefits or riders that may be

attached to the policy.

• The additional death benefit is payable only once,

regardless of the subsequent deaths of other joint

insureds within the same 90-day period.

• The age of the person insured is based on the date of

the new policy (attained age).

• Same class of risk as original coverage.

• Although no medical evidence of insurability is required,

we reserve the right to financially underwrite any one

of the joint insureds prior to the time the new policy

takes effect.

Potential marketAttractive for the income protection market.

Potential marketBeneficial for the income protection market. Provides an additional source of income to a family should both parents die within a short period of time.

Key benefitsA surviving joint insured can purchase new insurance protection without submitting new medical evidence of insurability.

Life 2 passes away – $300,000 death benefit paid.

Life 1 survives – coverage terminates.

Life 3 passes away within 90 days of Life 2: $300,000 additional death benefit.

Life 1 – Life 2 – Life 3$300,000 payable on first death

90 Days

Universal Life Product Guide

[ 23 ]

Life 1 – Life 2 (up to five)$1,000,000 payable on first death

Coverage needs change

Life 1 $1,000,000

Life 2 $1,000,000

This special option is similar to the Multiple Life Severance

Option and the joint last-to-die Single Life Insurance

Option. The most significant differences are that with the

joint first-to-die version, the split is at the discretion of the

owner and is not subject to contingent events, and the

NAAR for each split coverage is equal to the NAAR prior

to the split.

Eligibility for exercising the option

• Must be exercised prior to age 70 of the oldest of the

joint life insureds.

• Transamerica reserves the right to require medical

evidence of insurability for joint insureds classified as

substandard at time of issue.

• Transamerica reserves the right to financially underwrite

any of the joint insureds for whom the split coverage is

requested.

Terms of the Single Life Insurance Option

• The current coverage issue date is used.

• The maximum face amount is as follows:

– with a level death benefit, equal to the original face

amount less the proportionate fund value

– with an increasing death benefit, equal to the original

face amount

• Original rates apply, based on attained age.

• An administrative fee may apply.

Please refer to a sample contract for the detailed terms.

Key benefitsProvides future flexibility in case there is a need to split the insurance coverage.

Key benefitsAdaptable to lifecycle needs as income replacement gives way to estate succession or tax liability coverage.

Switching between joint options The switch option allows clients to change from joint

first-to-die to joint last-to-die, should their insurance

needs change. The SEA will be calculated based on the

individual ages and the original issue date of the joint first-

to-die coverage. In other words, the clients will get the

same SEA had they purchased a joint last-to-die coverage

originally. The issue date is preserved when the switch

option is exercised.

From To Administrative rules

Joint first-to-die

Joint last-to-die (deductions to last death only)

• No underwriting required.

• Available any time after 10th policy anniversary.

• Must be exercised prior to policy anniversary nearest the oldest insured’s 70th birthday.