Embed Size (px)

Citation preview

Università degli studi di PaviaUniversità degli studi di PaviaUniversità degli studi di PaviaUniversità degli studi di PaviaFacoltà di EconomiaFacoltà di Economia

a.a.a.a. 20142014--20152015

Lesson 4 International Accounting

Lelio Bigogno, Stefano Santucci

1

IAS/IFRS: IAS 16 PROPERTY, IAS/IFRS: IAS 16 PROPERTY, PLANT AND EQUIPMENTPLANT AND EQUIPMENT

2

HistoryHistory of IAS16of IAS16

� August 1980 Exposure Draft E18 Accounting for Property, Plant and Equipment in the Context of the Historical Cost System

� March 1982 IAS 16 Accounting for Property, Plant and Equipment

� 1 January 1983 Effective date of IAS 16 (1982)

� May 1992 Exposure Draft E43 Property, Plant and Equipment� May 1992 Exposure Draft E43 Property, Plant and Equipment

� December 1993 IAS 16 Accounting for Property, Plant and Equipment (revised as part of the 'Comparability of Financial Statements' project) ù

� 1 January 1995 Effective date of IAS 16 (1993) Property, Plant and Equipment1998 IAS 16 was revised by IAS 36 Impairment of Assets

� 1 July 1999 IAS 16 (1998) effective date of 1998 revisions to IAS 16

3

HistoryHistory of IAS16of IAS16

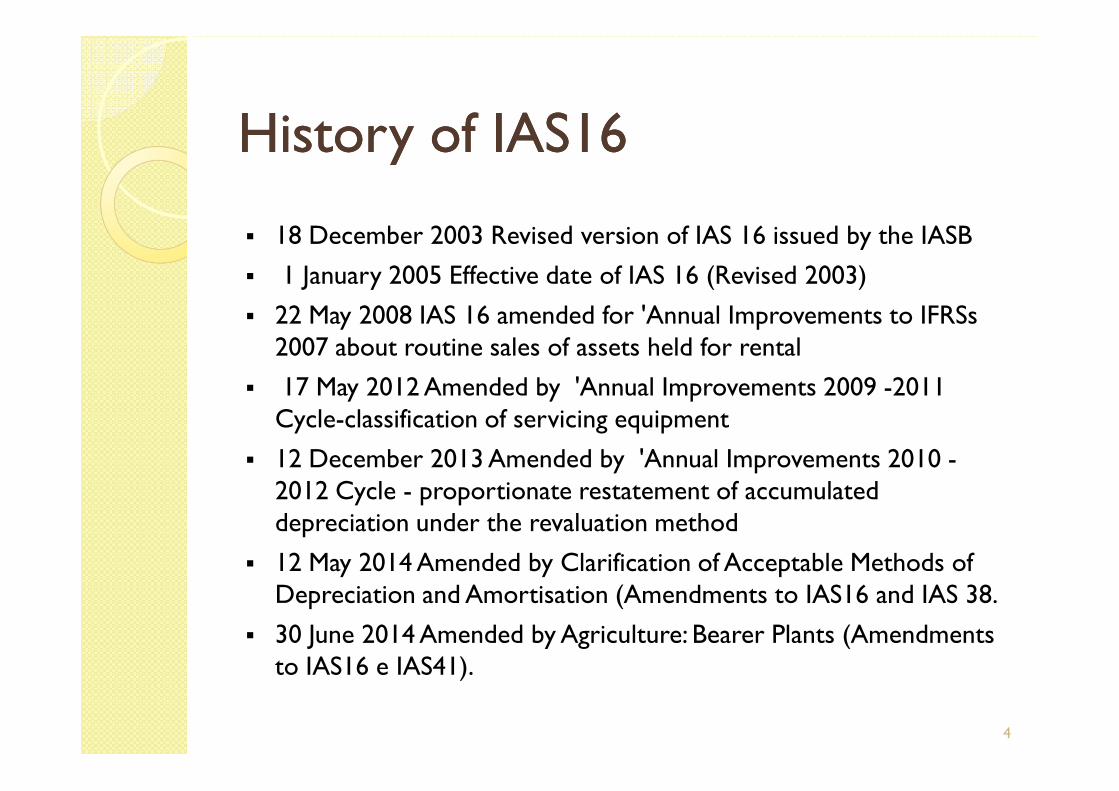

� 18 December 2003 Revised version of IAS 16 issued by the IASB

� 1 January 2005 Effective date of IAS 16 (Revised 2003)

� 22 May 2008 IAS 16 amended for 'Annual Improvements to IFRSs 2007 about routine sales of assets held for rental

� 17 May 2012 Amended by 'Annual Improvements 2009 -2011 � 17 May 2012 Amended by 'Annual Improvements 2009 -2011 Cycle-classification of servicing equipment

� 12 December 2013 Amended by 'Annual Improvements 2010 -2012 Cycle - proportionate restatement of accumulated depreciation under the revaluation method

� 12 May 2014 Amended by Clarification of Acceptable Methods of Depreciation and Amortisation (Amendments to IAS16 and IAS 38.

� 30 June 2014 Amended by Agriculture: Bearer Plants (Amendments to IAS16 e IAS41).

4

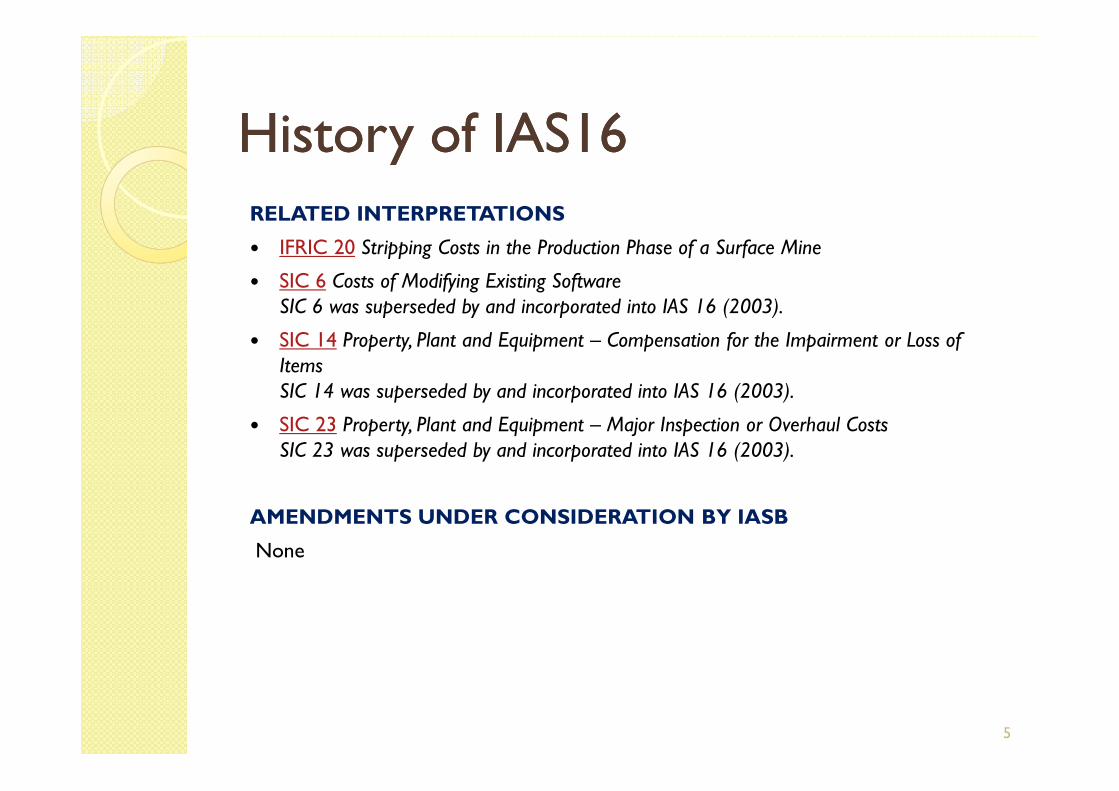

HistoryHistory of IAS16of IAS16RELATED INTERPRETATIONS

� IFRIC 20 Stripping Costs in the Production Phase of a Surface Mine

� SIC 6 Costs of Modifying Existing SoftwareSIC 6 was superseded by and incorporated into IAS 16 (2003).

� SIC 14 Property, Plant and Equipment – Compensation for the Impairment or Loss of ItemsSIC 14 was superseded by and incorporated into IAS 16 (2003).SIC 14 was superseded by and incorporated into IAS 16 (2003).

� SIC 23 Property, Plant and Equipment – Major Inspection or Overhaul CostsSIC 23 was superseded by and incorporated into IAS 16 (2003).

AMENDMENTS UNDER CONSIDERATION BY IASB

None

5

ObjectiveObjective

To prescribe the accountingtreatment for property, plant, andequipment.equipment.

6

ObjectiveObjective

The principal issues are:

� the recognition of assets,

the determination of their carrying amounts,� the determination of their carrying amounts,

� the depreciation charges and impairmentlosses to be recognised in relation to them.

7

ScopeScope

Applies to the accounting for property, plantand equipment,

except except

where another standards requires or permits differing accounting treatment

8

ScopeScope

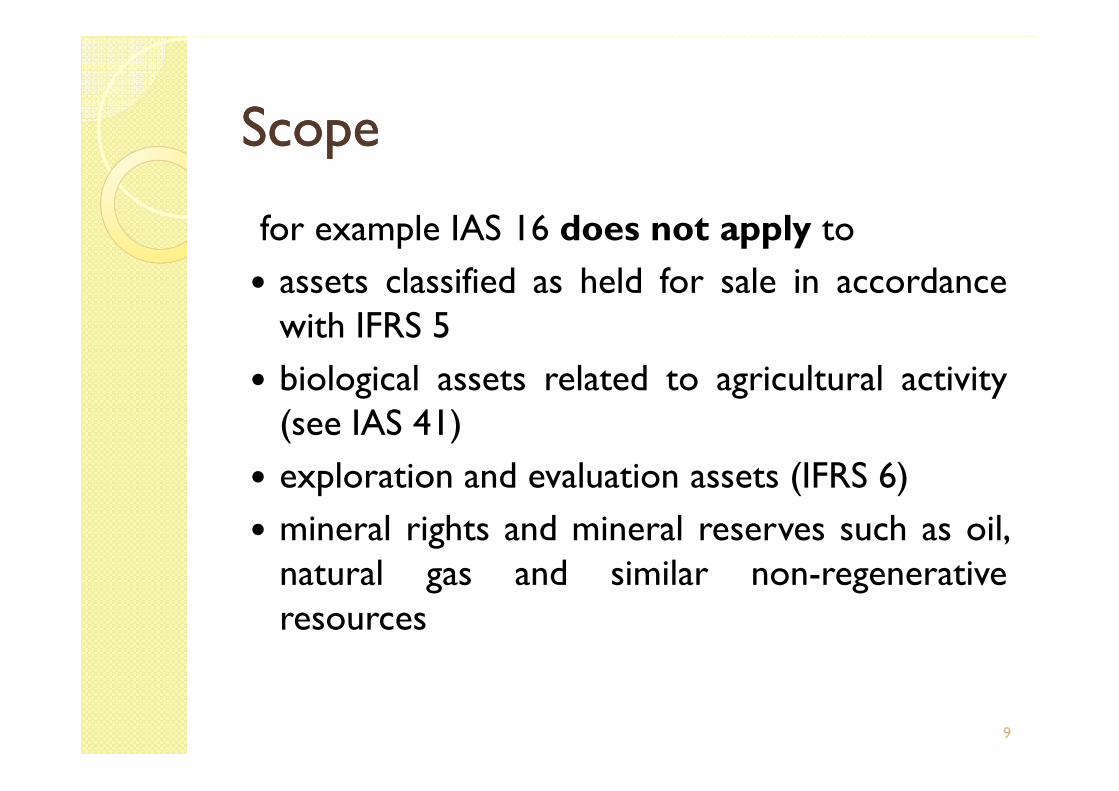

for example IAS 16 does not apply to

� assets classified as held for sale in accordancewith IFRS 5

� biological assets related to agricultural activity� biological assets related to agricultural activity(see IAS 41)

� exploration and evaluation assets (IFRS 6)

� mineral rights and mineral reserves such as oil,natural gas and similar non-regenerativeresources

9

ScopeScope

The standard does apply to property,plant, and equipment used to develop ormaintain the last three categories ofmaintain the last three categories ofassets.

10

RecognitionRecognition

Items of property, plant, and equipment should be recognised as assets when it is probable that:

� the future economic benefits associated with the � the future economic benefits associated with the asset will flow to the entity,

and

� the cost of the asset can be measured reliably.

11

RecognitionRecognition

� This recognition principle is applied to all property,plant, and equipment costs at the time they areincurred.

� These costs include costs incurred initially to acquireor construct an item of property, plant and equipmentand costs incurred subsequently to add to, replacepart of, or service it.

12

RecognitionRecognition

� IAS 16 does not prescribe the unit of measure forrecognition – what constitutes an item of property,plant, and equipment. Note, however, that if the costmodel is used (see below) each part of an item ofproperty, plant, and equipment with a cost that isproperty, plant, and equipment with a cost that issignificant in relation to the total cost of the item mustbe depreciated separately.

13

RecognitionRecognition

� IAS 16 recognises that parts of some items of property,plant, and equipment may require replacement atregular intervals. The carrying amount of an item ofproperty, plant, and equipment will include the cost ofreplacing the part of such an item when that cost isreplacing the part of such an item when that cost isincurred if the recognition criteria (future benefits andmeasurement reliability) are met.

The carrying amount of those parts that are replaced isderecognised in accordance with the derecognitionprovisions of IAS

14

RecognitionRecognition

� Also, continued operation of an item of property, plant,and equipment (for example, an aircraft) may requireregular major inspections for faults regardless ofwhether parts of the item are replaced. When eachmajor inspection is performed, its cost is recognised inmajor inspection is performed, its cost is recognised inthe carrying amount of the item of property, plant, andequipment as a replacement if the recognition criteriaare satisfied.

15

RecognitionRecognition

If necessary, the estimated cost of a future similarinspection may be used as an indication of what the costof the existing inspection component was when theitem was acquired or constructed.

16

InitialInitial MeasurementMeasurement

An item of property, plant and equipmentshould initially be recorded at cost.

17

InitialInitial MeasurementMeasurement

Cost includes all costs necessary to bring the asset toworking condition for its intended use. This wouldinclude not only its original purchase price but alsocosts of site preparation, delivery and handling,installation, related professional fees for architects andinstallation, related professional fees for architects andengineers, and the estimated cost of dismantling andremoving the asset and restoring the site (see IAS 37,Provisions, Contingent Liabilities and ContingentAssets).

18

InitialInitial MeasurementMeasurement

If payment for an item of property, plant, andequipment is deferred, interest at amarket rate must be recognised orimputedimputed

19

InitialInitial MeasurementMeasurement

If an asset is acquired in exchange for another asset(whether similar or dissimilar in nature), the cost will bemeasured at the fair value unless

(a) the exchange transaction lacks commercial substanceoror

(b) the fair value of neither the asset received nor theasset given up is reliably measurable.

If the acquired item is not measured at fair value, itscost is measured at the carrying amount of theasset given up.

20

MeasurementMeasurement SubsequentSubsequent toto InitialInitialRecognitionRecognition

IAS 16 permits two accounting models:

�Cost Model. The asset is carried at cost lessaccumulated depreciation and impairment.

�Revaluation Model. The asset is carried at a�Revaluation Model. The asset is carried at arevalued amount, being its fair value at the dateof revaluation less subsequent depreciation andimpairment, provided that fair value can bemeasured reliably

21

RevaluationRevaluation modelmodel

�Under the revaluation model, revaluationsshould be carried out regularly, so that thecarrying amount of an asset does not differmaterially from its fair value at the balancematerially from its fair value at the balancesheet date.

� If an item is revalued, the entire class of assetsto which that asset belongs should be revalued

22

RevaluationRevaluation modelmodel

� Revalued assets are depreciated in the same way asunder the cost model

� If a revaluation results in an increase in value, itshould be credited to equity under the heading"revaluation surplus" unless it represents the reversal of"revaluation surplus" unless it represents the reversal ofa revaluation decrease of the same asset previouslyrecognised as an expense, in which case it should berecognised in profit orloss.

23

RevaluationRevaluation modelmodel

� A decrease arising as a result of a revaluation should berecognised as an expense to the extent that it exceedsany amount previously credited to the revaluationsurplus relating to the same asset.

24

RevaluationRevaluation modelmodel

� When a revalued asset is disposed of, any revaluationsurplus may be transferred directly to retained earnings,or it may be left in equity under the heading revaluationsurplus. The transfer to retained earnings should notbe made through profit or loss.be made through profit or loss.

25

DepreciationDepreciation ((CostCost and and RevaluationRevaluationModelsModels))

For all depreciable assets:

� The depreciable amount (cost less residual value)should be allocated on a systematic basis over theasset's useful life;asset's useful life;

� The residual value and the useful life of an asset shouldbe reviewed at least at each financial year-end and, ifexpectations differ from previous estimates, any changeis accounted for prospectively as a change in estimateunder IAS 8.

26

DepreciationDepreciation ((CostCost and and RevaluationRevaluationModelsModels))

� The depreciation method used should reflect thepattern in which the asset's economic benefits areconsumed by the entity;

� a depreciation method that is based on revenue that is� a depreciation method that is based on revenue that isgenerated by an activity that includes the use of an assetis not appropriate)

27

DepreciationDepreciation ((CostCost and and RevaluationRevaluationModelsModels))

� The depreciation method should be reviewed at leastannually and, if the pattern of consumption of benefitshas changed, the depreciation method should bechanged prospectively as a change in estimate under IASchanged prospectively as a change in estimate under IAS8;

� Expected future reductions in selling prices could beindicative of a higher rate of consumption of the futureeconomic benefits embodied in an asset.

28

DepreciationDepreciation ((CostCost and and RevaluationRevaluationModelsModels))

� Depreciation should be charged to profit or loss,unless it is included in the carrying amount of anotherasset;asset;

� Depreciation begins when the asset is available for useand continues until the asset is derecognised, even if it isidle.

29

RecoverabilityRecoverability of the of the CarryingCarryingAmountAmount

IAS 36 requires impairment testing and, ifnecessary, recognition for property, plant, andequipment.equipment.

30

RecoverabilityRecoverability of the of the CarryingCarryingAmountAmount

An item of property, plant, or equipment shallnot be carried at more than recoverableamount, that is the higher of an asset's fairvalue less costs to sell and its value in use.amount, that is the higher of an asset's fairvalue less costs to sell and its value in use.

31

RecoverabilityRecoverability of the of the CarryingCarryingAmountAmount

Any claim for compensation from thirdparties for impairment is included in profit orloss when the claim becomes receivable.loss when the claim becomes receivable.

32

DerecognitonDerecogniton ((RetirementsRetirements and and DisposalsDisposals) )

An asset should be removed from the balancesheet on disposal or when it is withdrawn from useand no future economic benefits are expected from itsdisposal.disposal.

The gain or loss on disposal is the differencebetween the proceeds and the carrying amount andshould be recognised in profit or loss.

33

DerecognitonDerecogniton ((RetirementsRetirements and and DisposalsDisposals) )

If an entity rents some assets and then ceases torent them, the assets should be transferred toinventories at their carrying amounts as they becomeheld for sale in the ordinary course of business.

34

DisclosureDisclosure

For each class of property, plant, and equipment, disclose:

� basis for measuring carrying amount basis for measuring carrying amount

� depreciation method(s) used

� useful lives or depreciation rates

� gross carrying amount and accumulated depreciation and impairment losses

35

DisclosureDisclosure

� reconciliation of the carrying amount at the beginning and the end of the period, showing:

◦ additions

◦ disposals

◦ acquisitions through business combinations ◦ acquisitions through business combinations

◦ revaluation increases or decreases

◦ impairment losses

◦ reversals of impairment losses

◦ depreciation

◦ net foreign exchange differences on translation

◦ other movements

36

DisclosureDisclosure

Additional disclosures:

o restrictions on title

� expenditures to construct property, plant, and equipment during the period

� contractual commitments to acquire property, plant, and � contractual commitments to acquire property, plant, and equipment

� compensation from third parties for items of property, plant, and equipment that were impaired, lost or given up that is included in profit or loss

37

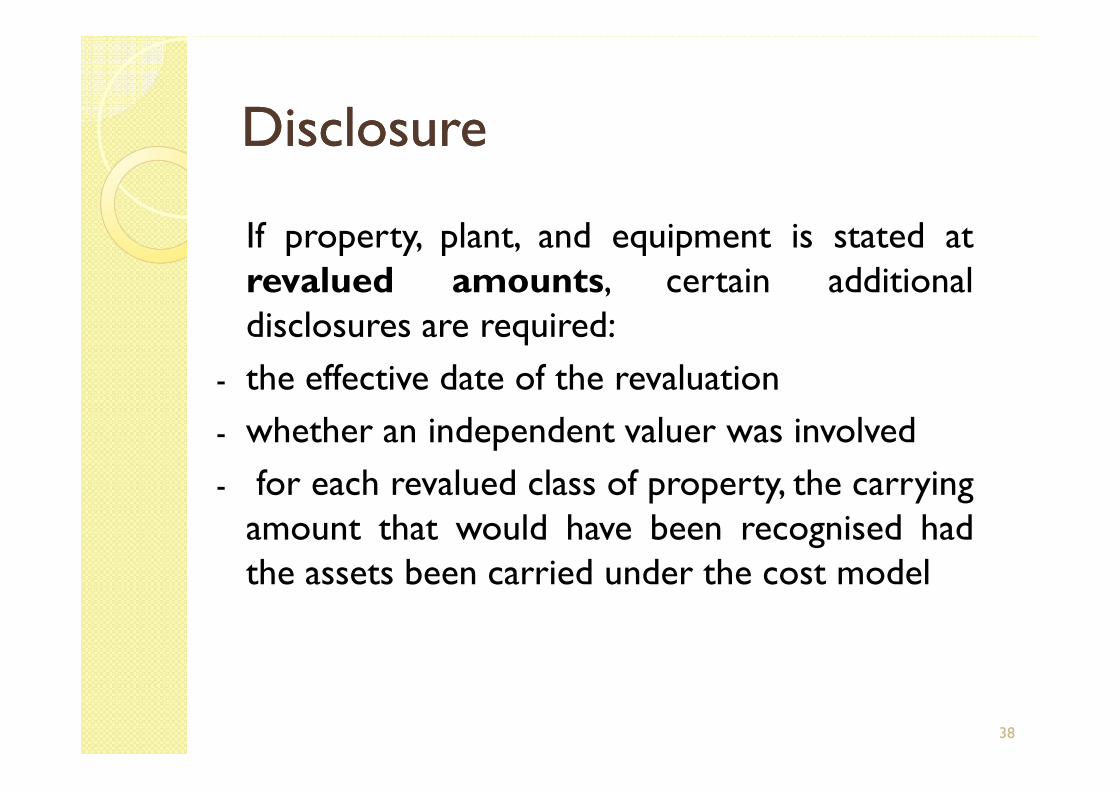

DisclosureDisclosure

If property, plant, and equipment is stated atrevalued amounts, certain additionaldisclosures are required:

- the effective date of the revaluation- the effective date of the revaluation

- whether an independent valuer was involved

- for each revalued class of property, the carryingamount that would have been recognised hadthe assets been carried under the cost model

38

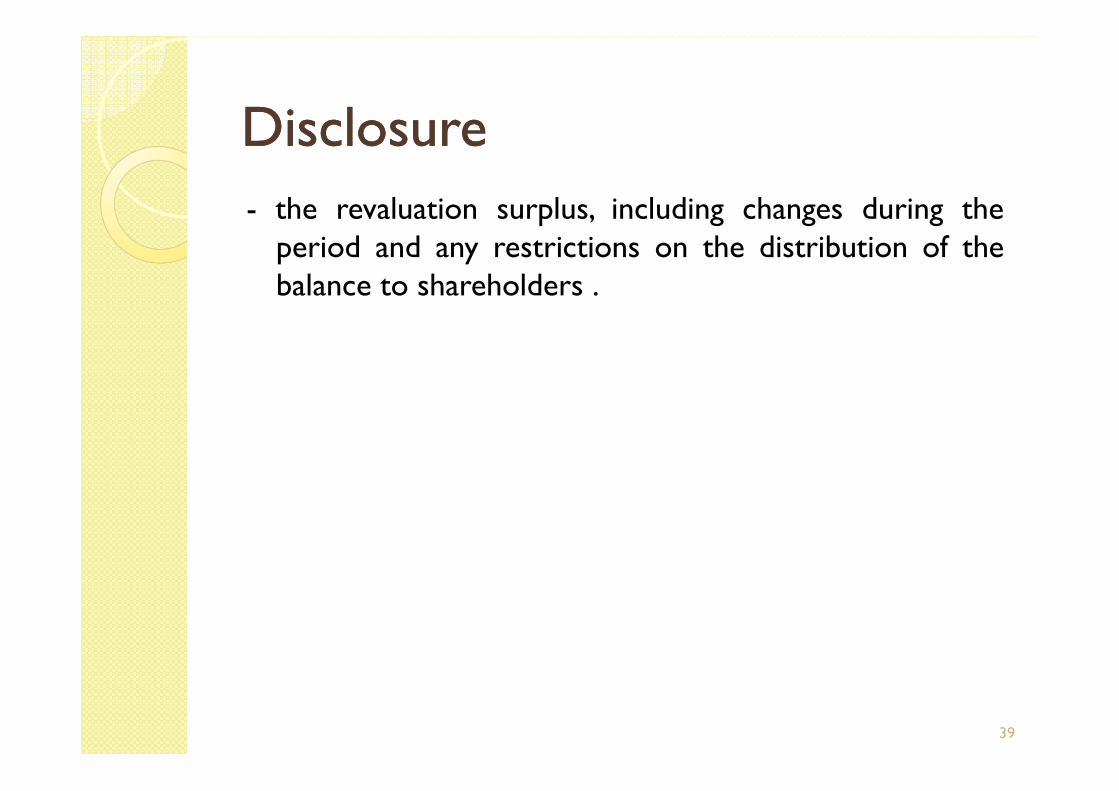

DisclosureDisclosure

- the revaluation surplus, including changes during theperiod and any restrictions on the distribution of thebalance to shareholders .

39

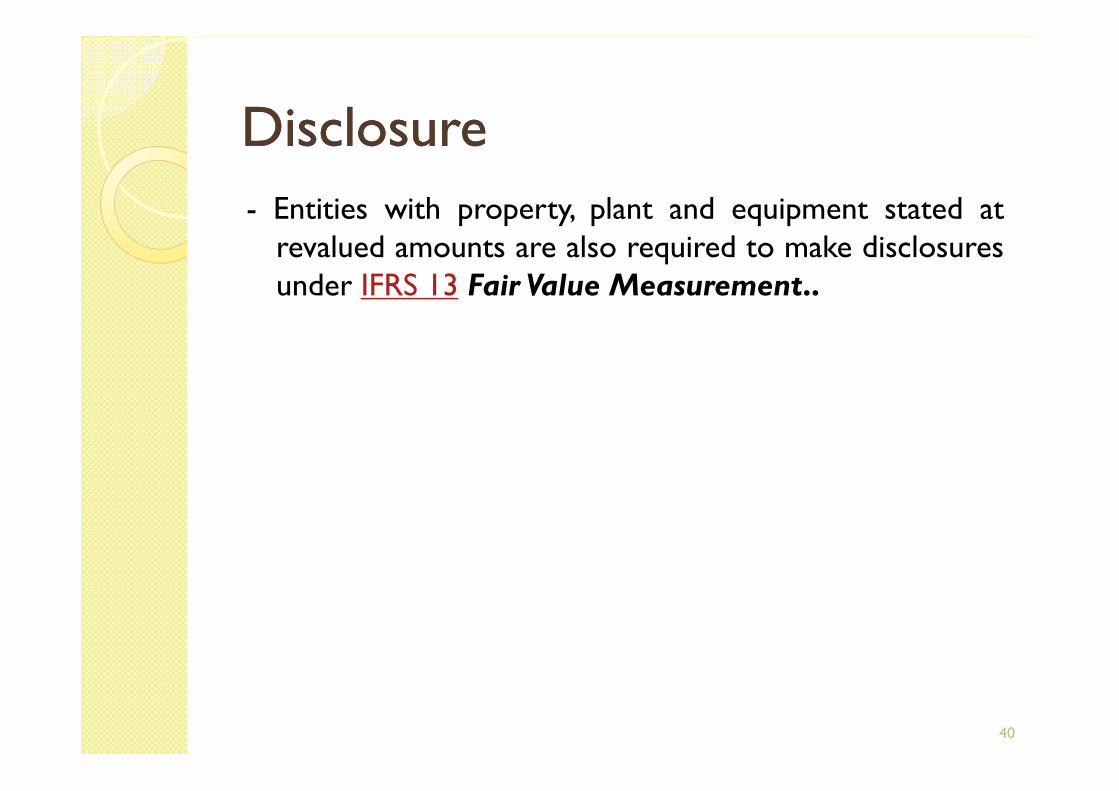

DisclosureDisclosure

- Entities with property, plant and equipment stated atrevalued amounts are also required to make disclosuresunder IFRS 13 Fair Value Measurement..

40

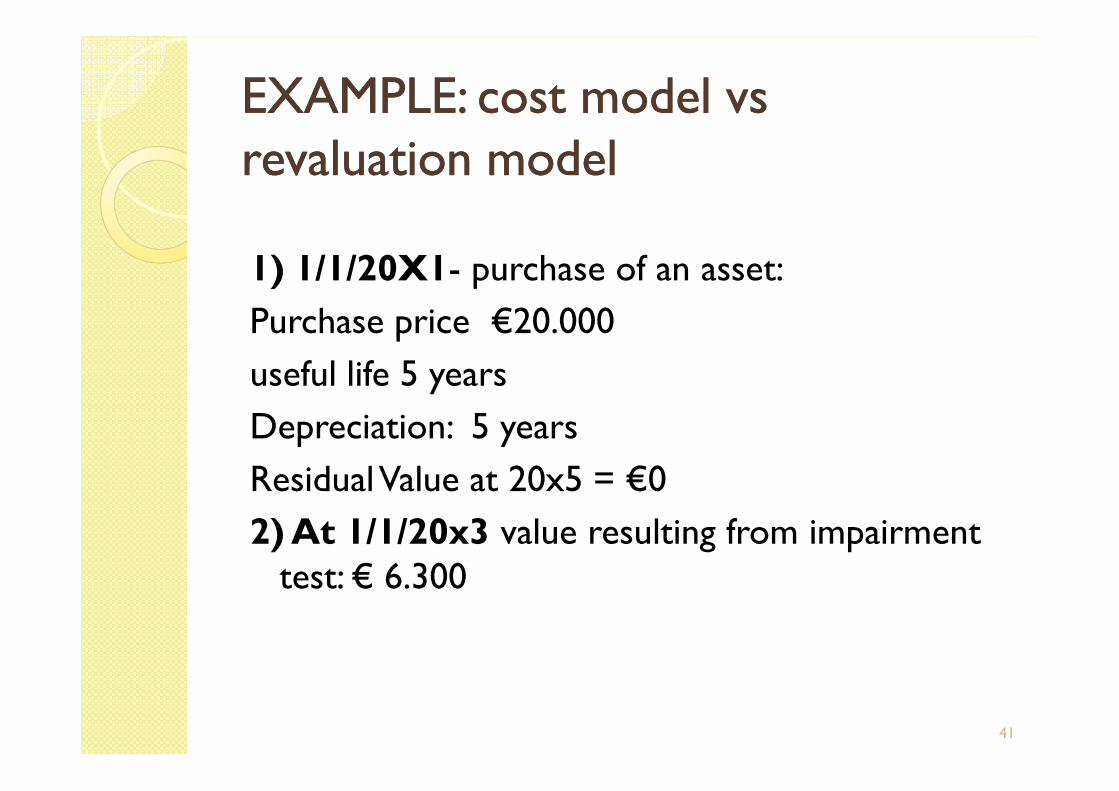

EXAMPLE: EXAMPLE: costcost modelmodel vs vs revaluationrevaluation modelmodel

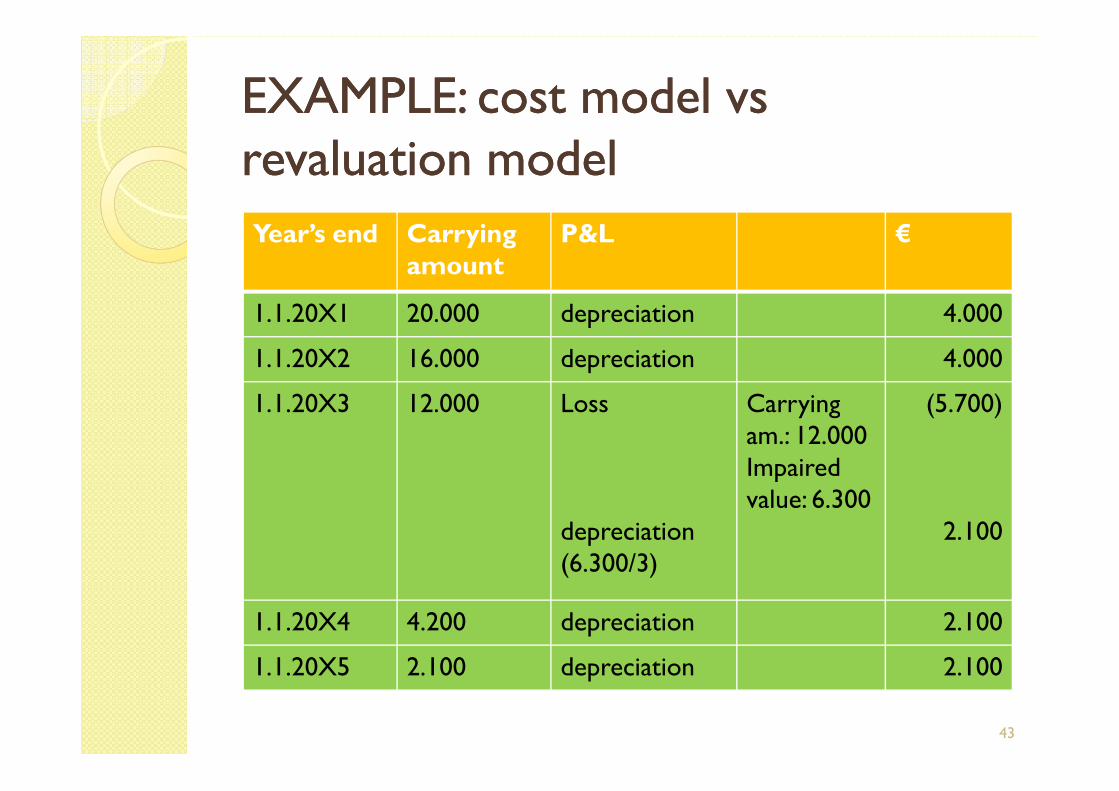

1) 1/1/20X1- purchase of an asset:

Purchase price €20.000

useful life 5 yearsuseful life 5 years

Depreciation: 5 years

ResidualValue at 20x5 = €0

2) At 1/1/20x3 value resulting from impairmenttest: € 6.300

41

EXAMPLE: EXAMPLE: costcost modelmodel vs vs revaluationrevaluation modelmodel

?

Depreciations Schedule

And effect of impairment test accordingAnd effect of impairment test accordingto cost model

42

EXAMPLE: EXAMPLE: costcost modelmodel vs vs revaluationrevaluation modelmodel

Year’s end Carryingamount

P&L €

1.1.20X1 20.000 depreciation 4.000

1.1.20X2 16.000 depreciation 4.000

1.1.20X3 12.000 Loss Carrying (5.700)

43

1.1.20X3 12.000 Loss

depreciation(6.300/3)

Carryingam.: 12.000Impairedvalue: 6.300

(5.700)

2.100

1.1.20X4 4.200 depreciation 2.100

1.1.20X5 2.100 depreciation 2.100

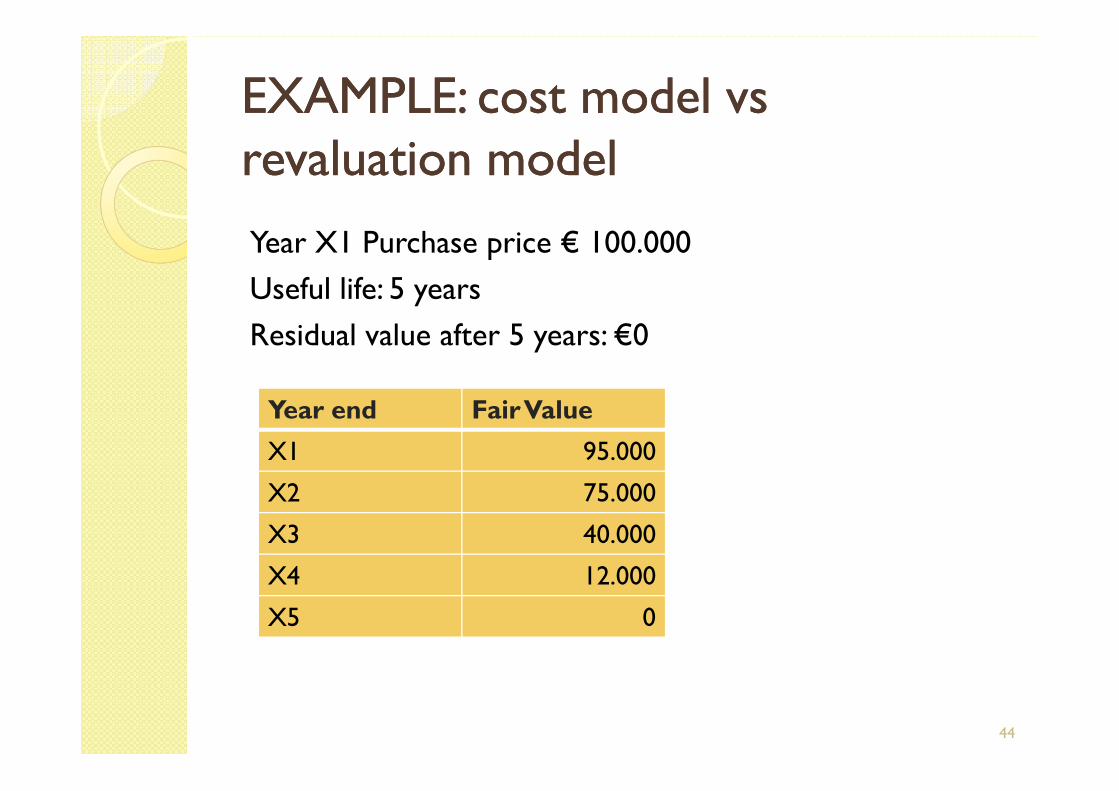

EXAMPLE: EXAMPLE: costcost modelmodel vs vs revaluationrevaluation modelmodel

Year X1 Purchase price € 100.000

Useful life: 5 years

Residual value after 5 years: €0

Year end Fair Value

44

Year end Fair Value

X1 95.000

X2 75.000

X3 40.000

X4 12.000

X5 0

EXAMPLE: EXAMPLE: costcost modelmodel vs vs revaluationrevaluation modelmodel

??

Accounting method accordingAccounting method accordingto revaluation model

45

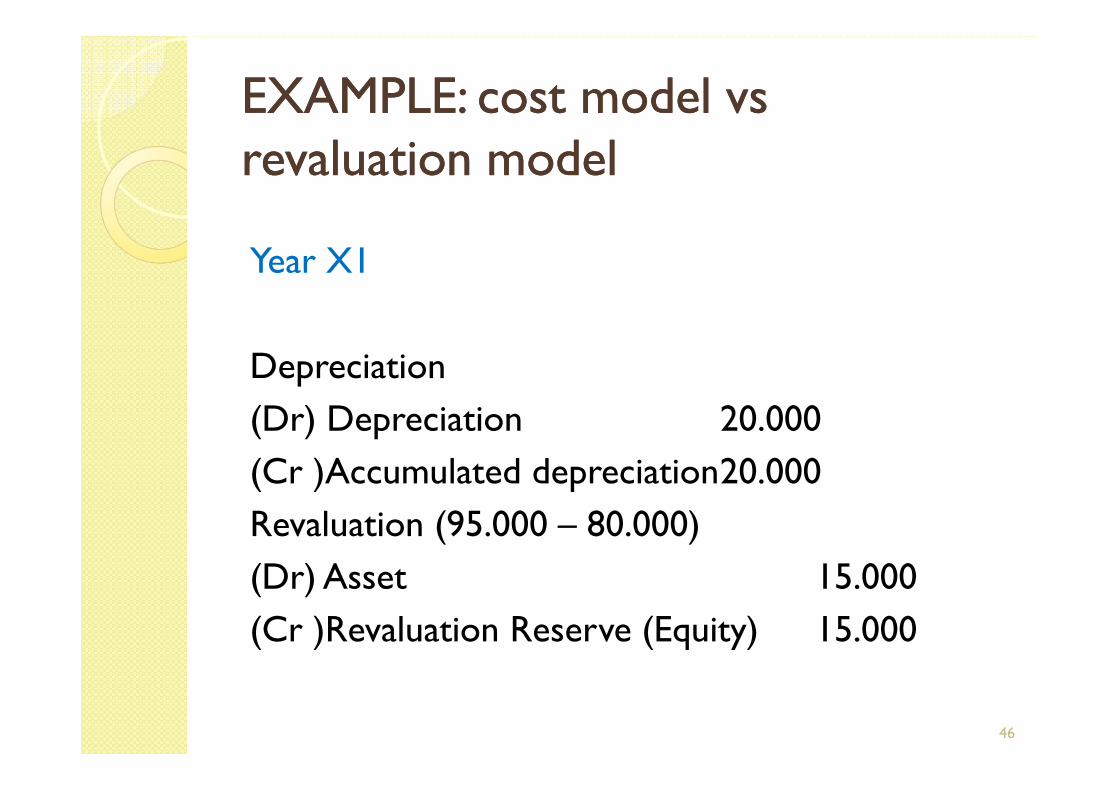

EXAMPLE: EXAMPLE: costcost modelmodel vs vs revaluationrevaluation modelmodel

Year X1

Depreciation

(Dr) Depreciation 20.000(Dr) Depreciation 20.000

(Cr )Accumulated depreciation20.000

Revaluation (95.000 – 80.000)

(Dr) Asset 15.000

(Cr )Revaluation Reserve (Equity) 15.000

46

EXAMPLE: EXAMPLE: costcost modelmodel vs vs revaluationrevaluation modelmodel

Year X2

Depreciation (95.000/4)

(Dr) Depreciation 23.750(Dr) Depreciation 23.750

(Cr )Accumulated depreciation 23.750

Revaluation (75.000 – 71.250)

(Dr) Asset 3.750

(Cr )Revaluation Reserve (Equity) 3.750

47

EXAMPLE: EXAMPLE: costcost modelmodel vs vs revaluationrevaluation modelmodel

Year X3

Depreciation (75.000/3)

(Dr) Depreciation 25.000

(Cr )Accumulated depreciation 25.000(Cr )Accumulated depreciation 25.000

devaluation (50.000 – 40.000)

(Dr) Revaluation Reserve (Equity) 10.000

(Cr ) Asset 10.000

48

EXAMPLE: EXAMPLE: costcost modelmodel vs vs revaluationrevaluation modelmodel

Year X4

Depreciation (40.000/2)

(Dr) Depreciation 20.000(Dr) Depreciation 20.000

(Cr )Accumulated depreciation 20.000

devaluation (20.000-12.000)

(Dr) Revaluation Reserve (Equity) 8.000

(Cr ) Asset 8.000

49

EXAMPLE: EXAMPLE: costcost modelmodel vs vs revaluationrevaluation modelmodel

Year X5

DepreciationDepreciation

(Dr) Depreciation 12.000

(Cr )Accumulated depreciation 12.000

50

EXAMPLE: EXAMPLE: costcost modelmodel vs vs revaluationrevaluation modelmodel

year Asset depreciation

Net Book Value

Fair Value Equity

X1 100.000 20.000 80.000 95.000 15.000

X2 95.000 23.750 71.250 75.000 3.750

51

X2 95.000 23.750 71.250 75.000 3.750

X3 75.000 25.000 50.000 40.000 (10.000)

X4 40.000 20.000 20.000 12.000 (8.000)

X5 12.000 12.000 0 0 0

750

![Deliberation on IFRS IAS-16, IAS-17, IAS-20 by CA. D.S. … · Deliberation on IFRS IAS-16, IAS-17, IAS-20 by CA. D.S. Rawat Partner, Bansal & Co. Property Plant & Equipment [PPE]](https://img.pdfslide.net/doc/110x75/5b16e1ed7f8b9a726d8e6199/deliberation-on-ifrs-ias-16-ias-17-ias-20-by-ca-ds-deliberation-on-ifrs.jpg)