Embed Size (px)

Citation preview

BBS042

UNIVERSITY OF BOLTON

BOLTON BUSINESS SCHOOL

MSc ACCOUNTANCY & FINANCIAL MANAGEMENT

TRIMESTER 1 EXAMINATIONS 2016/17

ADVANCED TAXATION

MODULE NO: ACC7506 Date: 28 November 2016 Time: 13:00 to 16:00 INSTRUCTIONS TO CANDIDATES: There are four questions on this

paper. This examination is 3 hours Answer question in section A, and

Two from Three in section B. This is a closed book examination

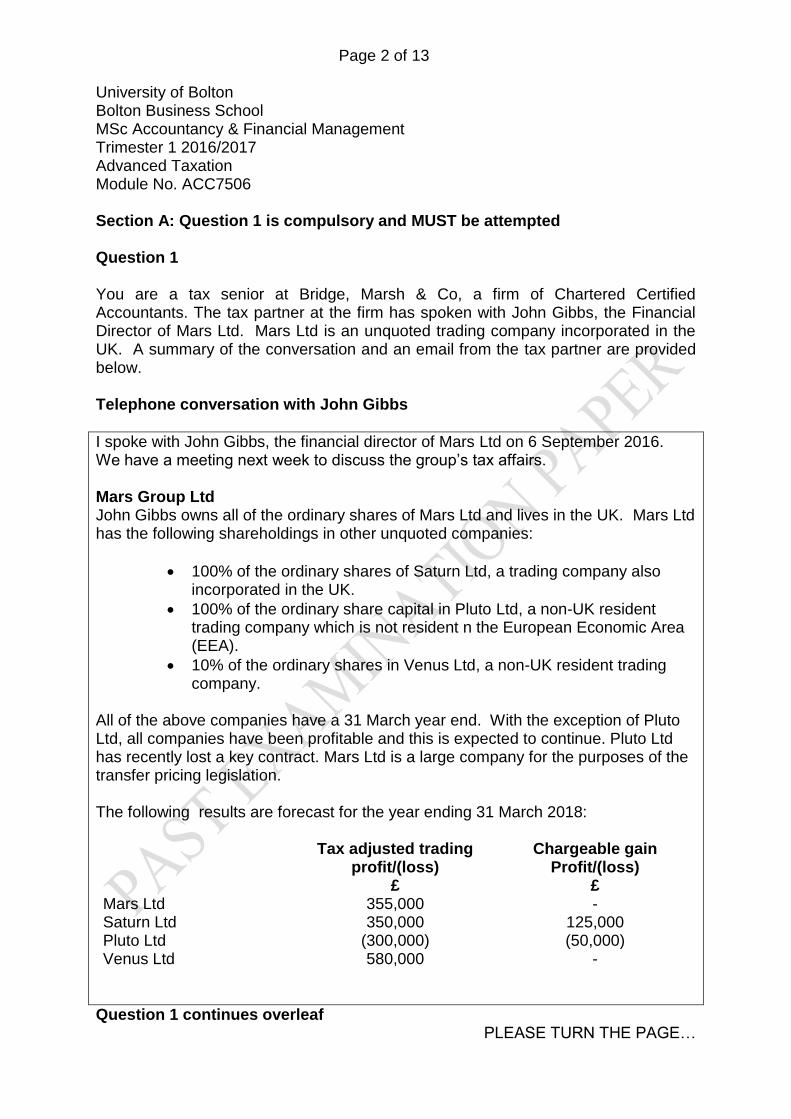

Page 2 of 13 University of Bolton Bolton Business School MSc Accountancy & Financial Management Trimester 1 2016/2017 Advanced Taxation Module No. ACC7506

Section A: Question 1 is compulsory and MUST be attempted Question 1 You are a tax senior at Bridge, Marsh & Co, a firm of Chartered Certified Accountants. The tax partner at the firm has spoken with John Gibbs, the Financial Director of Mars Ltd. Mars Ltd is an unquoted trading company incorporated in the UK. A summary of the conversation and an email from the tax partner are provided below. Telephone conversation with John Gibbs

I spoke with John Gibbs, the financial director of Mars Ltd on 6 September 2016. We have a meeting next week to discuss the group’s tax affairs. Mars Group Ltd John Gibbs owns all of the ordinary shares of Mars Ltd and lives in the UK. Mars Ltd has the following shareholdings in other unquoted companies:

100% of the ordinary shares of Saturn Ltd, a trading company also incorporated in the UK.

100% of the ordinary share capital in Pluto Ltd, a non-UK resident trading company which is not resident n the European Economic Area (EEA).

10% of the ordinary shares in Venus Ltd, a non-UK resident trading company.

All of the above companies have a 31 March year end. With the exception of Pluto Ltd, all companies have been profitable and this is expected to continue. Pluto Ltd has recently lost a key contract. Mars Ltd is a large company for the purposes of the transfer pricing legislation. The following results are forecast for the year ending 31 March 2018: Tax adjusted trading

profit/(loss) Chargeable gain

Profit/(loss) £ £ Mars Ltd 355,000 - Saturn Ltd 350,000 125,000 Pluto Ltd (300,000) (50,000) Venus Ltd 580,000 -

Question 1 continues overleaf PLEASE TURN THE PAGE…

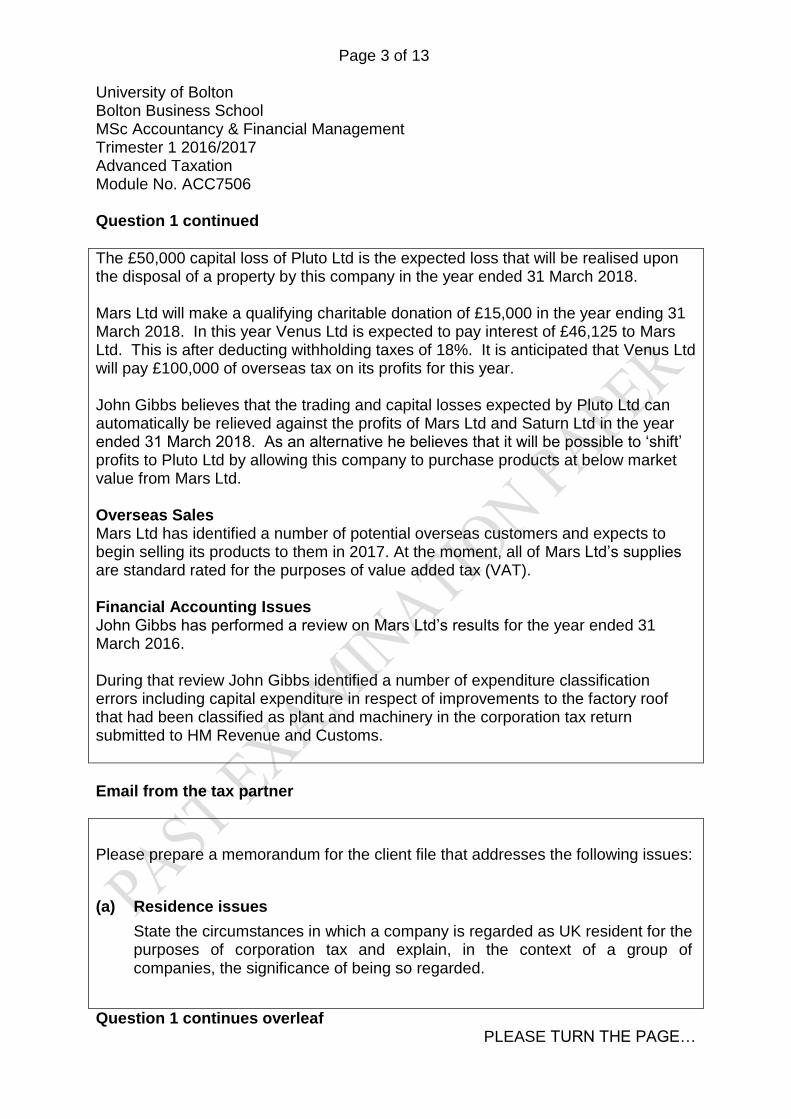

Page 3 of 13 University of Bolton Bolton Business School MSc Accountancy & Financial Management Trimester 1 2016/2017 Advanced Taxation Module No. ACC7506

Question 1 continued

The £50,000 capital loss of Pluto Ltd is the expected loss that will be realised upon the disposal of a property by this company in the year ended 31 March 2018. Mars Ltd will make a qualifying charitable donation of £15,000 in the year ending 31 March 2018. In this year Venus Ltd is expected to pay interest of £46,125 to Mars Ltd. This is after deducting withholding taxes of 18%. It is anticipated that Venus Ltd will pay £100,000 of overseas tax on its profits for this year. John Gibbs believes that the trading and capital losses expected by Pluto Ltd can automatically be relieved against the profits of Mars Ltd and Saturn Ltd in the year ended 31 March 2018. As an alternative he believes that it will be possible to ‘shift’ profits to Pluto Ltd by allowing this company to purchase products at below market value from Mars Ltd. Overseas Sales Mars Ltd has identified a number of potential overseas customers and expects to begin selling its products to them in 2017. At the moment, all of Mars Ltd’s supplies are standard rated for the purposes of value added tax (VAT). Financial Accounting Issues John Gibbs has performed a review on Mars Ltd’s results for the year ended 31 March 2016. During that review John Gibbs identified a number of expenditure classification errors including capital expenditure in respect of improvements to the factory roof that had been classified as plant and machinery in the corporation tax return submitted to HM Revenue and Customs.

Email from the tax partner

Please prepare a memorandum for the client file that addresses the following issues:

(a) Residence issues

State the circumstances in which a company is regarded as UK resident for the purposes of corporation tax and explain, in the context of a group of companies, the significance of being so regarded.

Question 1 continues overleaf PLEASE TURN THE PAGE…

Page 4 of 13 University of Bolton Bolton Business School MSc Accountancy & Financial Management Trimester 1 2016/2017 Advanced Taxation Module No. ACC7506

Question 1 continued

(b) Offset of losses and profit shifting

Explain, giving reasons, whether John Gibbs is correct in believing that:

(i) Pluto Ltd’s losses can be automatically offset; and/or

(ii) profits may be shifted to Pluto Ltd in the manner he has suggested in the year ending 31 March 2018.

(c) Actions to allow loss relief

Advise John Gibbs of the actions that could be taken to allow relief for Pluto Ltd losses within the Mars group of companies for the year ending 31 March 2018.

(d) Corporation tax liabilities

Assuming that the trading and capital losses of Pluto Ltd can now be relieved and will be used either by Mars Ltd or Saturn Ltd, calculate the forecast corporation tax liabilities of Mars Ltd and Saturn Ltd for the year ending 31 March 2018.

Please explain the allocation of any reliefs within and between the companies and give details and time limits for any elections or claims that would need to be submitted.

(e) Potential sales by Hereford Ltd to overseas customers

Explain the VAT implications for Mars Ltd of the sales to overseas customers.

(f) Financial accounting issues

Set out the further action required by the company and, potentially, ourselves in respect of the classification errors.

Required:

Prepare the memorandum requested by the tax partner.

The following marks are available:

(i) Residence issues. (5 marks)

(ii) Offset of losses and profit shifting. (6 marks)

Question continues overleaf

PLEASE TURN THE PAGE…

Page 5 of 13 University of Bolton Bolton Business School MSc Accountancy & Financial Management Trimester 1 2016/2017 Advanced Taxation Module No. ACC7506

Question 1 continued

(iii) Actions to allow loss relief.

(3 marks)

(iv) Corporation tax liabilities.

You should assume that the rates and allowances for the Financial Year

2015 apply throughout this part of the question.

(9 marks)

(v) Potential sales by Mars Ltd to overseas customers.

(4 marks)

(vi) Financial accounting issues.

(4 marks)

Professional marks will be awarded for adopting a logical approach to problem

solving, the clarity of the calculations, effectiveness with which the

Information is communicated and the overall presentation of the

memorandum.

(4 marks)

(Total: 35 marks)

End of Question 1

End of Section A

PLEASE TURN THE PAGE…

Page 6 of 13 University of Bolton Bolton Business School MSc Accountancy & Financial Management Trimester 1 2016/2017 Advanced Taxation Module No. ACC7506

Section B: TWO questions ONLY to be attempted

Question 2 Your client, Margaret Smith, requires some advice on the inheritance tax and capital

gains tax implications of making gifts to her daughter Joan.

Margaret

– Does not expect to live past her eightieth birthday, which will be on 31

December 2021.

– Has left her entire estate to her daughter, Joan.

Gift to Joan

– This will be made on 30 June 2017, and will consist of two assets; shares in

Strictly Ltd and an antique painting.

Shares in Strictly Ltd

– 50,000 £1 ordinary shares in Strictly Ltd, an unquoted trading company, to be

gifted to Joan.

– Margaret owns 100,000 shares in Strictly Ltd, and her husband also owns

100,000 shares.

– Issued share capital is 400,000 £1 ordinary shares.

– Current values of Strictly Ltd’s shares are as follows:

Shareholding Value per share £

50% 4.50

37.5% 3.55

25% 2.95

12.5% 2.50

– By 31 December 2021 these values are likely to have increased by 40%.

– Strictly Ltd owns investments in quoted shares that represent 12% of the

value of its total assets.

Question 2 continues overleaf

PLEASE TURN THE PAGE…

Page 7 of 13 University of Bolton Bolton Business School MSc Accountancy & Financial Management Trimester 1 2016/2017 Advanced Taxation Module No. ACC7506

Question 2 continued

Acquisition of Strictly shares

– Margaret originally acquired 50,000 £1 ordinary shares in Dancing Ltd in March

2003 for £96,000.

– Dancing Ltd was taken over by Strictly Ltd on 15 October 2014, at which time

Margaret received two £1 ordinary shares in Strictly Ltd and £0.80 in cash for

each share held in Dancing Ltd.

– On 15 October 2014 a 25% holding of Strictly Ltd’s ordinary shares was worth

£1.20 per share.

– Margaret has never been a director or employee of either Dancing Ltd or

Strictly Ltd.

Antique painting

– Currently worth £108,000.

– Acquired in June 1995 for £98,000.

– Value not likely to change before 31 December 2021.

Joan

– Joan is a risk-averse investor, and would therefore sell the shares in Strictly

Ltd soon after receiving them. She would keep the painting.

Margaret’s other assets

– Margaret has other assets worth £350,000, has not made any previous

lifetime transfers of assets and will not dispose of any other assets during the

tax year 2017/18.

Capital loss and CGT rates

– Margaret has a capital loss brought forward of £15,000, from the sale of a

holiday cottage in 2012.

– Margaret has annual taxable income of £11,865.

Question 2 continues overleaf

PLEASE TURN THE PAGE…

Page 8 of 13 University of Bolton Bolton Business School MSc Accountancy & Financial Management Trimester 1 2016/2017 Advanced Taxation Module No. ACC7506

Question 2 continued

Required:

(i) Advise Margaret of the inheritance tax (IHT) and capital gains tax (CGT)

implications of the proposed gifts to Joan on 30 June 2017 and calculate the

total tax due, assuming that Margaret dies on 31 December 2021.

You should consider any claims, elections or alternatives available.

(12 marks)

(ii) Show the IHT and CGT position if Margaret does not make the proposed

gift to Joan on 30 June 2017 but retains the assets until her death on 31

December 2021.

(3 marks)

(iii) Compare the total tax liability for the alternative courses of action and give

any appropriate recommendations based on your findings.

(5 marks)

(Total: 20 marks)

End of Question 2

PLEASE TURN THE PAGE…

Page 9 of 13 University of Bolton Bolton Business School MSc Accountancy & Financial Management Trimester 1 2016/2017 Advanced Taxation Module No. ACC7506

Question 3

You should assume today’s date is 1 March 2016.

Your client Jack is planning to start a TV repair and sale business on 6 April 2016.

A limited company has been formed for this purpose. Jack needs your advice on

the acquisition of a vehicle to use in his business.

The following information has been obtained from a meeting with Jack.

Proposed acquisition of vehicle

Jack is considering whether the vehicle should be:

i. acquired by himself personally or by the limited company

ii. a car or a van.

Car

– Jack is considering buying a petrol engine car with a list price of £18,000

including VAT and CO2 emissions of 132 g/kilometre.

Van

– Alternatively, Jack would buy a petrol engine van with the same list price

and CO2 emission level.

Hire purchase

– Irrespective of who buys the vehicle it will be acquired under a 0% finance

hire purchase contract with the cost being £3,000 per year.

Running costs

– All running costs, including fuel will be paid for by the limited company in the

event that it acquires the vehicle.

– If Jack acquires the vehicle he will pay all running costs but he will receive a

mileage allowance from the company.

Question 3 continues overleaf

PLEASE TURN THE PAGE…

Page 10 of 13 University of Bolton Bolton Business School MSc Accountancy & Financial Management Trimester 1 2016/2017 Advanced Taxation Module No. ACC7506

Question 3 continued

– The running costs per year for each of the vehicles will be:

£ Insurance 500 Repairs/servicing 500 Road fund licence 100 Fuel £3 for each

40 miles

Mileage

– Jack anticipates that he will drive 22,000 miles in the 2016/17 tax year of

which 20,000 will be for business purposes.

Other information

– All figures include VAT where appropriate.

– Assume that Jack will be a higher rate tax payer in 2016/17 by virtue of the

salary that he will draw from the business.

– The company will be registered for VAT from 6 April 2016.

Required:

a) Assuming the vehicle acquired is a car advise Jack of the income tax,

corporation tax, VAT and national insurance implications for both the

limited company and himself of acquiring the vehicle, either:

i. personally; or

ii. by the limited company.

Detailed calculations are not required for this part of the question.

(8 marks)

b) Advise Jack how your answer to (a) would be different if the vehicle acquired was a van.

(3 marks)

Question 3 continues overleaf

PLEASE TURN THE PAGE…

Page 11 of 13 University of Bolton Bolton Business School MSc Accountancy & Financial Management Trimester 1 2016/2017 Advanced Taxation Module No. ACC7506

Question 3 continued

c) Assuming that the vehicle acquired is a car and that the mileage

allowances are paid at the authorised rates for business mileage only,

advise which of the two alternatives (acquisition by Jack personally or

by the limited company) would be the most tax efficient.

For both alternatives your answer should take account of the aggregate net

after tax cash position for both Jack personally and the limited company.

For this part of the question you can ignore the effect of VAT.

(9 marks)

You should assume that the rates and allowances for the tax year 2015/16

apply throughout this question.

(Total: 20 marks)

Question 4 You should assume today’s date is 6 April 2016.

Your client Sandy Hunt requires you to calculate her income tax liability for

2015/16. She also requires a calculation of her potential inheritance tax liability.

Personal information

- Sandy Hunt is a pensioner who has been made a widow as a result of the

death of her husband on 7 April 2015.

- Sandy’s husband had made no lifetime gifts. He left an estate worth £500,000

of which £100,000 was left to the couple’s children and the balance to Sandy.

- Sandy owns a large number of investments as well as the assets inherited from her husband. These are set out below (including the assets she inherited) as at today’s date.

Question 4 continues overleaf

PLEASE TURN THE PAGE…

Page 12 of 13 University of Bolton Bolton Business School MSc Accountancy & Financial Management Trimester 1 2016/2017 Advanced Taxation Module No. ACC7506

Question 4 continued

Shares in Selwyn Ltd

- 45,000 £1 ordinary shares in Selwyn Ltd, an unquoted trading company with

a share capital of 200,000 ordinary shares. Sandy’s three children hold the

other shares in the company equally.

- Sandy inherited these shares from her husband, who had originally acquired

them at their par value in March 1993.

- The shares were valued at £160,000 on 7 April 2015, and are currently worth

£236,250. Selwyn Ltd has assets worth £1,050,000, of which £500,000 are

investments in quoted shares.

- Selwyn Ltd paid a dividend of 10p per share during 2015/16.

Other stocks and shares

- 20,000 ordinary shares, par value 50p each, in Rhubarb plc, a ‘blue chip’ UK

company quoted at 410p – 426p. Rhubarb plc regularly pays a dividend of

27p per share each year.

- 25,000 units in Union Trust, a unit trust quoted in the UK at 210p – 218p. The

trust is aimed at capital growth, and therefore only paid a dividend of £450

(net) during 2015/16.

Interest yielding investments

- UK government stocks with an interest rate of 4% and a nominal value of

£100,000. These are currently quoted at 90 − 94p.

- Deposits of £150,000 in an ‘instant access’ account with the Brat and Bong

Building Society. This is a building society paying a high rate of interest of

5.50% per annum (gross) on this account.

- £10,000 in the NS&I Pensioners Guaranteed Income Bonds, which pay a

gross interest rate of 7%.

- Sandy invested £23,000 in an ISA account with the Scotman Building Society

on 1 December 2015. This is her first ISA investment but her late husband

had £28,000 of ISA investments at his death. Sandy received £210 of gross

interest during 2015/16 which was reinvested in the ISA making a current

balance of £23,210.

Question 4 continues overleaf

PLEASE TURN THE PAGE…

Page 13 of 13 University of Bolton Bolton Business School MSc Accountancy & Financial Management Trimester 1 2016/2017 Advanced Taxation Module No. ACC7506

Question 4 continued

Other assets

- Her main residence, which is currently valued at £225,000.

- Chattels, cash and other assets of £165,000.

- Sandy invested £10,000 in a venture capital trust during 2015/16.

Other income

- During 2015/16, Sandy received income of £1,650 (net) as a beneficiary of a

discretionary trust. The trust holds cash of £65,200 held in a money market

deposit account.

- Sandy receives a UK state retirement pension of £113 weekly and a private

pension of £12,200 per annum (gross).

Other information

- Under the terms of her will, Sandy has left £60,000 to Oxfam, a registered

charity, and the rest of her estate to her family. Her only previous lifetime gift

of assets was a gift of £160,000 to a discretionary trust for the benefit of her

children in June 2010.

Required:

(a) Calculate Sandy’s income tax payable/repayable for 2015/16.

(9 marks)

(b) Calculate the IHT liability that would arise if Sandy were to die during

April 2016.

Your answer should indicate who is liable for the tax and by what date.

(11 marks)

(Total: 20 marks)

END OF QUESTIONS