Embed Size (px)

Citation preview

University of Nigeria Research Publications

OLIOMOGBE, Thompson I

Aut

hor

PG/MBA/00/31124

Title

The Impact Of Inventory Management On Organizational Performance: A Study Of

Nigeria Breweries PLC And Nigeria Bottling Company PLC

Facu

lty

Business Administration

Dep

artm

ent

Management

Dat

e

October, 2002

Sign

atur

e

No. 27 Collcge Road, Ogui New Layout, Enugu MOTTO: YOUR CHOICE IS 01. JR TARGET

PRESENTED B'Y C>I;IOhIOGBE, THOMPSON I.

PGIMBA,~00/3 1 124

b PROJECT REPORT SUBMITTED TO THE

DEPARTMENT OF MANAGEIL?FNT FACULTY OF BUSINESS ADMINISTRATION SCHOOL OF POST - GRADUATE STUDIES

UNlVERSIT'r' OF NIGERIA ENUGU - CAMPUS

TITLE PAGE

"THE lM15r.r.. ,- OF INVENTORY MANAGEMENT ON

ORGAN!r ATIOFl,fl I i2E14FORMANCE".

(A STUDY OF NIGERIA BREWERIESS PLC AND NIGERIA

BOTTLING COMPANY PLC).

CERTIFICATION

Ol~omogbe, Thompson I., a post-graduate student rn the

department of management with r-egistrat~on number

FG/MBA/00/3? 124, has sat~sfactor~ly conipletcd the requ~rement

for the C O L I I S ~ and research work for the Post-graduate Master of

Business Admintstration (MBA) Degree in Management.

Thrs project is an embljdiment of orgnal work and has not . -

been subrn~tted In part or In full for any other D~ploma or Getgee -

of this or any 0th3i Untversity or Polytech~rc.

Y Head of ~epar tm&ht CHUKWU, C . 0 .

Supervisor CHIEF J.A. EZEH.

DEDICATION

T h ~ s project IS ded~cated to my spout; MRS G T

OLIOMOGBE, who dur-mg the perlsd the whole work was bemg

put together exercised a lot of p:~tlence and understandrny for

my not bemg ava~lable a good part of the trme

Above all, I w s h to thank the Lord for seeing me through

the entlre MBA programme

b

ACKNOWLEDGEMENT

I w ~ s h to thank Chief J 4 Eze my project supervisor for his

guldance throughout the per~od that the work was being put

to~~ , i~c r . HIS ~ o r d s of advice and suggest~on were very apt

and found to be very useful.

i also w s h to thank c;tl~zrs, too numerous to mention, who

in one w ~ y or the other contributed to the successful complet~on

of the project. @

Last but not the least, I wish to express my s ~ ~ ~ i e r e thanks

to Lady Justma Odoemenam who took great pains and care In

ensuring that the manuscr~pt was well typed and leglb!e

ABSTRACT

This is a research project carried out to identify and

determine the impact of inventory management and control on

organisationat performance (a study of Nigeria Breweries PLC

and Nigeria Bottling Company PLC).

A sanipie size of 200 respondents all random!y selected

fronl :he staff and management of both Nigeria Breweries PLC

and Nigeria Buttling Company ? L C ail at 9"' Mile. Ngwo. ~ n h g u ,

were used. Both primary and secondary data were collected and

analysed using the Chi-quart : test.

The researcher, based on the data coliecied and analysed,

found out that:

- The respondents from both organizations understand

what inventory management is all about;

- That the organizations go for and use first class raw

materials in the production of their fmished products,

- Inventory management make a great impact on the

organizations mar dactur iny process;

\ 11

7 he pronerly applied princ~ples of cyclrcal order quantrty

model of ~nventory control does not permit continuous flow

of pr-odi.rcts to customers, cont~nuous flow of product~on in

organ~sat~onal prof~ts;

S u ~ t m l y empioyed f~xed order quant~ty systi-m of inventory

control does not assure continuous flow of Input mater~als,

oprrat~ons and ensure opt~rnal lnvzntory levels

Appropr~ate adoptlor-I of the prrnc~ples of the

requirement planning method of ~rlvcntory contro

mate

decrease In overheads, check in abrupt halt rn product~on

b

rmls

not

reduce costs LAdsociatzd w ~ t h holding In overheads arid

checks In halt In product~on schedule

l does

LIST OF FIGURES

Figure 2 .1 : H~present ing thz believe that costs carrying

invzntory vary neal'ly directly with ths size ,f the

order guantity.

Fig: ire 2.2: Representing Economic order quanti~y

Figure 2.3: Representing t k relatinnship betwezn inventory

costs and level of customers services.

Figure 4. I : A pie cnar-t, rzprxent ing the believe that inventory

management has an impact on manufiicturing

process. B

Figure 4 .2 : A t-1istograr.n: r-epresenl,,ig the impact inventory

ma~agernent make in manufacturing process.

Figure 4.3: A Bar chart, representing the believe that there are

problerns encountered in the management of raw

materials invmtory it1 ine orgarii"atior~.

LIST OF TABLES

Table 4.1 :

Table 4.2:

Table 4.3:

Table 4.4:

Tabie 4 .5 :

Tablc 4.6:

Table 4.7:

Table 4.8:

Table 4.9:

Table 4.10:

I ab!? 4. I ' I :

Table 4.12.

Table 4.13:

Sex arid Age D~strtbut~on of Responuents

Total Number of Respcndents

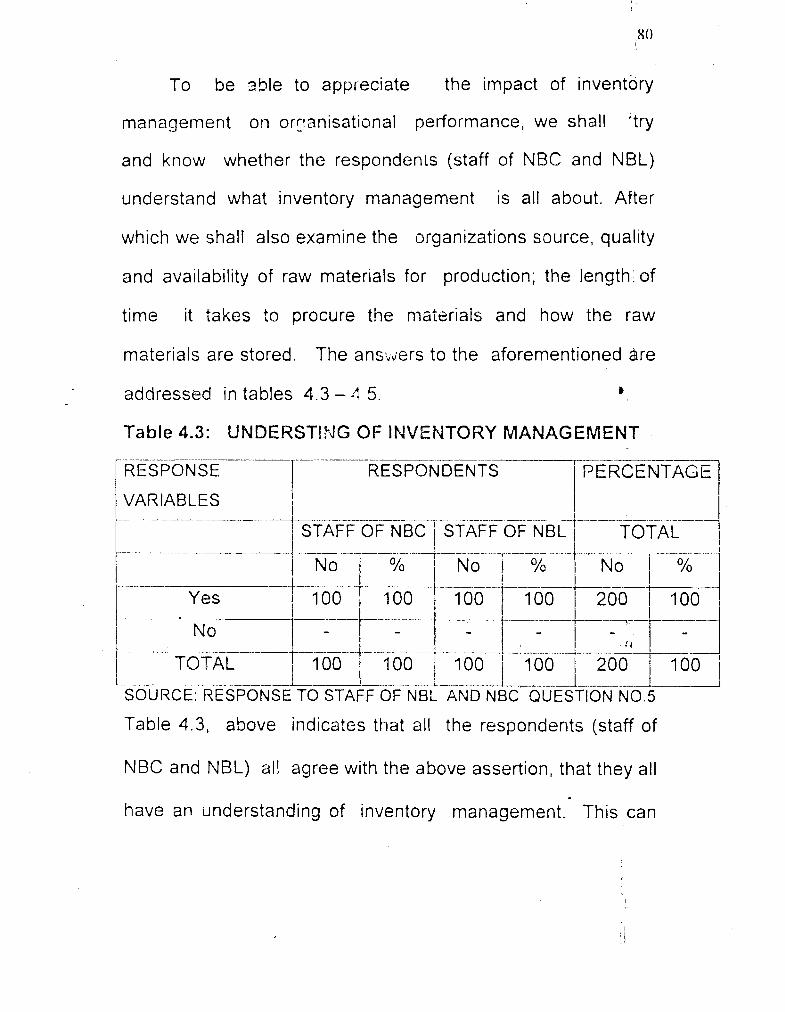

!.lnder 5:mdlng of Inventory Management

Sources of Raw Materials

Quality of Raw rnater~als used in product~on

L e ~ g t h of time it takes to procure the materials

Storage method of the raw materials

Has inventory management any impact on your

manufacturing process? D

What impact does inventory management make in

management process?

Are there prohlems encountered in the inventory

management of raw materials in the organization?

What is the nature of the problem?

Dces principles of cyclical order quality model of

inventory control permit continuous flow of products to

customers, continuous flow of production in the

organisatiotxd profit?

Does the suitable employed fixed order quality system

of inventory assl.!re continuous flow of input material,

decrease in overheads, check in abrupt halt in

production operations and ensure optimal inventory level?

Table 4 .14 Does appropriate adoption of the principles of 'the

materials requirement planning method of inventory

control, reduce costs assc,~ated with holding

resources in inventory reserve, decrease in

overheads and checks in halt in production schedule?

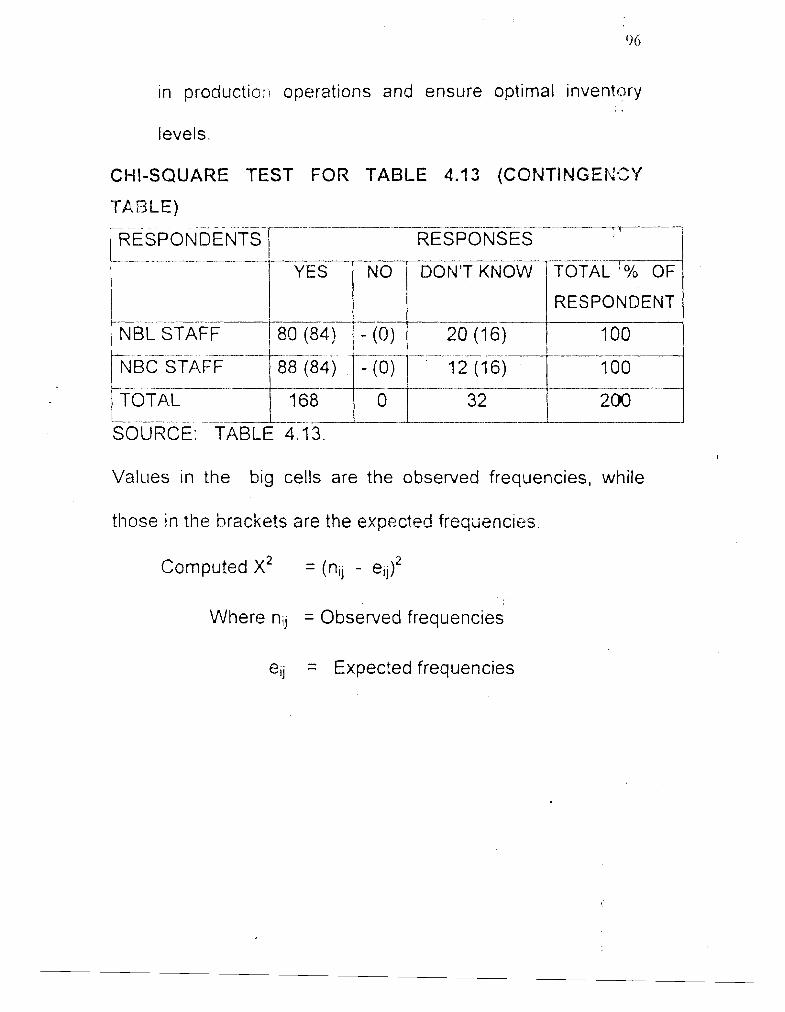

Table 4.15: Chi-square Test:- The principle of cyclical order

quality model af inventory control does not permit

continuous flow of products to customers, continuous

flow of production in the organisational pr'ofit.

Table 4.16: Chi-square 7 est:- Suitable employed fixed order qualrty b

system of inventory control does not assure

continuocrs f lou of input materials, decrease in

overheads, check in abrupt halt in product operatrons

and ensure optimal inventory level.

Table 4.17: Chi-square Test - Appropriate adoption of the

principles of materials requirement planning method of

inventory control does not reduce costs associated

with holding resources in inventory reserve, decrease

in overheads and checks in halt in production

schedule.

TABLE OF CONTENTS

Title page

Certification

Dedication

Acknowlef.:'yement

Abswact

List of figures

Llst of Tables

Table o i contents

CHAPTER ONE

Introduction

Background of the study

Statement of problem

Objectives of the study

Research Questions

Significance of the study

Formulation of research hypotheses

Scope of the study

Limitation of the study

Profde of Nigeria Brewer~es (NB) PLC

Scope of 3peratlons

Profrle of Nigerra Bottling Company (NBC) PLC

Defmrtion of terms

References

CHAPTER TWO

Literature Review

Background to Literature Review 22

Inventory Management Conceptual Overview 23

Types of Inventory Management 25

Factors Influencing Inventory Level 26

l nventory Control Systemrrechniques 27

Reasons for Inventory Control in an Organisation 31

Economic Order Quantity 35

Derivation of Economic Order Quantity 41 B

GainJlmportance of lnventory Control Quantity Discount 47

Problem of Inventory Management 51

Functions of Inventory 53

2.1 1 : Merits of Inventory Management " 54

2.12: Demerits of inventory Management 57

2.13: Inventory Management and Control by Nigeria ~rewer ie 's

(NB) PLC. 60

2.14: lnventory Management and Control by Nigeria Bottling

Company {I'JBC,) PLC. 61

2.15: Summary of related literature 62

References 64

CHAPTER THREE

3.0: Research Design and Ivlethodoiogy 67

Research Method

Method and Source of Data Collection

Questionnaire

Interview Method

Libraries

Population for the study

Procedure for data gathering

Validity and reliability of data instrument

Determination of sample size 72

Method of data analysis

Test of Hypotheses

CHAPTER FOUR

Analysis and Interpretation of Data 77

Part A: Response Rate and Personal data analysis of 77

respondents

Part 8: Analysis of response based on 80

problems/objective

Test of hypotheses 93

References 102

CHAPTER FIVE

Summary of findings, conclusions and recommendations 103

Summary of findings 103

5.2: Conclusions

5.3: Recommendations

5.4: Areas for further research

Bibliography

Appendix I

Appendix I I

Appendix Ill

CHAPTER ONE

I .O INTRODUCTION 8 . i:

1 . BACKGROUND TO THE STUDY

S~irvival of any business concern depends to a very great

extent on the firm's ability to effectively manage and control its

invent.ory. The inability to achieve this feat has caused the failure of

man) industries. Inventory ttlerefore plays a central role in any

business. It is the main reason for the continuous existence of any B I

business organisation mostly those in ma~ufacturmg sector.

Generally, lnventory control, as a management tool, is the

method or methods employed in maintaining detailed lists, showing

quantities and values of raw materials, work - in - process, and

finished goods held in warehouse stock. I

However, many management practiuners and authors have

va r io~~s definitions of inventory control and management. For

instance, Johnson et al. (1 985: 21 2) define inventory management

as the use of various techniques to optimize levels of all types of

stock, raw materials, work -in -progress and finished goods. They

2

observe that inventory management and control take into

consideration such factors as

- Sales forecast,

- Economic batch quantities

- Product~on plann~ng

- Plant and equipment control and so on.

From another perspective, Lewis (1 995: 13) sees inventory

management and control as a science - based art of ensuring b '

that just enough inventory or stock is held by an organisation to

economically meet both its internal and external demand

commitments. As an essential component of any organisational

system, Lucey (1987: 132) observes that the boundary of

inventory management and control should encompass the

various elements which must work harmoniously for.,, the

achievement of the system's objective.

In addition to this, Fedire (1990: 35) notes that the ideology

of material management extends from an integrated approach to

planning, acquisition, conversion, flow and distribution of

production materials from the raw materials stage to the finished

goods stage.

Several statistics clearly point out the current significance of

the inventory control function. A study of corporate balance sheet 1 -

shows that a firm's inventory commonly constitute from 15 to 25

percent of its invented capit;?! Mags, 1996: 419). He emphasizes I

the cost element because the central objective is to ensure that a

minimum of residual stock is maintained while incurring the least

possible cost. He further reports that numerous studies conducted

by consultants and manufacturing firms reveal that a typical

manufacturer incurs inventory carrying cost of from 17% to 20%

of average inventory value.

? .2: STATEMENT OF PROBLEM

Inventory plays an essential role in any organization. The

larger the inventory size, the easier it is to reduce costs of

p~:rchdsing, manufacturing and shipping as well as provide prompt

customers service. However, a larger inventory stock requires a I

higher mvestment of money, higher carrying cost such asdorage.

handling risk of obsolescence# and data processing. These

costs must be balanced off against any advantages in holding

inventory. To what extent have N ~ g e r ~ a Breweries PLC and

Nigeria Bottling company PLC tried to achieve this balance?

What are the techniques of inventory management that are

employed by the companies in the pursuit of this equilibrium?

1.3 OBJECTIVES OF THE STUDY:

The objectives of the study are as follows:

( i ) The study of in rn to ry management practices in Nigenia

Breweries PLC and Nigeria Bottling Company PLC,

Enugu, as they relate to:

Sources, quality and availability of raw materials used in

production; the length of time it takes to procure the

materials and how the rai: materials are stored.

I I I (a) The Optimum inventory level of the organizations

(b ) Inventory control policy or policies

(c) lnventory control of organizations.

(iii) To find out the impact of inventory management on the

company's manufacturing processes.

(iv) To ascertain the problems encountered in the

management of the raw material inventory in the

organisation and make recommendations.

To facilitate the invest~gation of this study, the following

research questions will be addressed. 1

-3 RESEARCH QUESTIONS

( i ) What are the sources and quality of raw materials that

are available to Nigerra Breweries PLC and thg

Nigeria Bottling Company PLC?

(ii) How long does it take to procure the raw materials?

(iii) What storage techniques do the organizations use in

storing their raw materials?

(iv) Identify the inventory management practices and

policies that are being used by the organisation.

(v) What zre the inventory management problems of the

organisation?

1.5 SlGNlFlClANCE OF THE STUDY

The signif~cance of t h ~ s study cannot be over estimated

It IS sgn~f~cant because data so generated from the study IS

suff~cient to expand further f~elds of knowledge of t h ~ s top~c

from many other dimens~ons. The study also, present sufficient

challenges to academ~cs to increase their research interests in

the field of knowledge.

The government will also benefit from this research in

the sense that, they will learn of the eff~cacy of inventory

management and control and how it contributes to the growth

and development of an organization. This will therefore,

make the government to encourage the adequate production

and importation of raw materials and spare parts

It will also help other organizations and even house holds

, . I to appreciate the benefits accruable from the effective and

sufficient application/adoption of inventory management and

control.

1.6: FORMULATION OF RESEARCH HYPOTHESES

Modern researchers agree that research work, when-

ever feasible should proceed from hypotheses because

hypotheses serve as a powerful beacon that light the path for

the research work. Also hypotheses are necessary whenever

causes - and effect relationship are to be discovered. Thus,

formulating hypotheses, as framework for this study becomes

imperative. B

be lo\^ are the null and alternative nypotheses.

1 Ho: The ?ropesly applied principles of Cyclical order

quantity model of inventory control does not permit

continuous flow of products to customers,

continuous flow of production in organisational

profits.

H,: The properly applied principles of Cyclical order

quantity model of inventory control permit

continuous flow of products to customers,

continuous flow of production in organisational

profits.

2. Ho: Suitably employed fixed order quantity system of

mventory control does not assure continuous flow

of input materials, decrease in overheads, check in

abrupt halt in production operation and ensure

optional inventory levels.

HI: Suitably employed fixed order quantity systembof

inventory control assure continuous flow of input

rnateria!~, decrease in overheads, check in abrupt

halt in production operation and ensure optional

inventory levels.

3. Ho: Appropriate adoption of the principles of the materials

requirement planning method of inventory control

does not reduce costs associated with holding

resources in inventory reserve, decrease in

overheads and checks in halt production schedule.

HI: Appropriate adoption of the principles of the

materials requirement planning method of inventony

control certainly reduce costs associated with

holding resources in inventory reserve, decrease in

overheads and checks in halt in production

schedule.

1.7 SCOPE OF THE STUDY

In this study we are concentrating mainly on the

inventory management practices in the Nigeria Breweries PLC

and the Nigeria Bottling Company PLC, Enugu, as they relate

to sources, qmlity and availability of raw materials used in

production; the length of time it takes to procure the materials

and how the raw materials are stored.

1.8 LIMITATION OF THE STUDY I

This study is limited only to the populat~on that will be

sampled in the two organizations. Its research in Nigeria, and

indeed other developing countries. is still in the infant stage,

most of the background data (statistics) that form the bedrock

of research are not readily available. This forms one of the

major bottlenecks the writer encountered in carrying out this

study.

The sludy is also, hindered by time and financial

constraints. In order to meet with the deadline for the

submission of bound copies of this project, and bearing in mind

the lean purse of the researcher, a relatively extensive area of

the country cannot be covered. B

7.9 PROFILE OF NIGERIA BREWERIES (NB) PLC

SCOPE OF OPERATIONS

Nigeria Breweiies PLC, the pioneer and largest brewing

Company in Nigeria, was incorporated in 1946 and recorded a

landmark when the first bottle of STAR larger Beer rolled off the

bottling lines in its Lagos Brewery in June 1949 . This was

followed by Aba Brewery which was Commissioned in 1957 ,

Kaduna Brewery In 1963 and lbadan in 1982 .In September

1993, the fifth company in Enugu was acqulred by the

company. Thus from its humble beginning in 1946, the

cnmpany now has five breweries from which high quality

products are distributed to all parts of this great country.

COMPANY EQUITY

With about 55,000 shareholdersl the authorized share

capital of Nigeria Breweries PLC is N457m, sixty - five per

cent (6596) of the share is held by Nigerians amongst who are

co.i~lpany employees of various categories. The company's

turnover increased from N10.768 billion in 1995 to N12.256

billion in 1996, while a sum of N4.6 billion was paid to the

Federal and State Governments in various forms of taxes as

against N4.0 billion in the previous year.

In 1996, the company paid a dividend of N1.00 per

share, amounting to N915m. This level of dividend is better

appreciated if it is recalled that the company gave a h p t

issue of one for o m in 1995, thus increasing the equity

base of the company from 457.5m ordmdry shares to 915

million ordinary shares. The import of these developments

has been a corresponding growth in the prosperity of

company's shareholders whose funds have appreciated in

value far in excess of their original investments.

BRAND PORTFOLIO

Nigerizl Breweries PLC has a portfolio of six htgh

quality brands; Star larger Beer (1949): Gulder Larger Beer

(1 970); Maltina (1 976); Legend Extra stout (1 992); Amstel

Malta (1994) and the Schweppes range of carbuoated sbft

drinks (Schweppes Soda water) launched in December. 1996.

Together, the brands have facilitated a strong leadership

position in the total brewed products market in Nigeria. Their

outstanding quality and consumer franchise complement other

company values and capabilities to set Nigeria Breweries PLC

apart as the house of quality.

EXPORT

NRC PLC has an Increasing export business that dates back

to I986 Currently, ~t exports to the U K., U S A , Italy,

Netherlands, Germany and Ker \)A.

RESEARCH AND DEVELOPMENT

N~ge r~a Rrewerles PLC has kept pace with key

international development Thus ensurlng that its systems,

processes and operational procedure are always , ' in

conformity with proven best practices in most parts of the

world. It is in line with this policy that the company established

a Research and Development Centre in 1987 to enhance its

research act~vilies 01-1 all aspects of the brew~rlg operation. ;I

ANCILLARY INDUSTRIES I

,*

As a major brewering concern, the company encourages

the establishment of ancillary business Many of these

organ~zations and individuals depend largely on the company

for their m e a x of livelihood. These include manufacturers of

bottles, crown corks, labels, cartons, plastic crates and such

services as Hotels/ Clubs and Direct customers.

SOCIAL RESPONSIBILITY

Nigeria Breweries PLC is a socially responsible

corporate citizen with an enviable record of rendering corporate

philanthropy in the areas of education, sports, and health,

among others. The company recently established an Educatidn

Trust Fund of NlOO million to take more active part in rthe

funding of educational and research facilities in higher

institutions, 311 in an effort to provide and encourage academ'ic

excellence In Nigeria. This is in addition to its secondary

and University Scholarships' programme for children of its

employees.

Nigeria Breweries PLC is the foremcs: sponsor of spoits

by variety in the country with sponsorship covering Table

Tennis, Lawn Tennis, Cyclmg, Chess, Golf, Badminton, Dart,

Boat Race and Ayo. The aim is to develop Nigeria Sports

men and women to partic~pate in national and international

sports. In the health sector, the company is committing funds

to the building of the sickle cell centre in Nigeria, among

other health related and charity activities. I

CONCLUSION

Nigeria Breweries PLC is a model of success in the

private sector. The company's high profile, profitability and

s~~ccessful operations can be traced to good product quality;

efficient management of operations and strategic penetratfon

into market environment. Others are proper understanding

of consumer attitudes and habits and high social responsibility

profile at national and zonal levels (Source: Diary of NB PLC,

2000)

I 1 PROFILE OF NIGERIA BOTTLING COMPANY(NE3C) PLC

An Ice- cold bottle or glass of Coca - cola IS believed t~ I

! the best known taste in the world (source: Coca - cola

annual pamphlet titled "The fact you should know about coca I

cola") Coca - cola was first made in May, 8'". 1886. It was

first made by Dr. John Styth Pemberton, a pharmacist He

made coca - cola in his home in Atlanta, Georgia, USA. The

name Coca - cola was given to the product by frank M.

Robinson, Dr. Pemberton's partner and book keeper;. He also

designed the flowing script that distinguished the famous trade

mark.

Coca - cola contents remain a secret as they have been

for over 100 years. The formula known as MERCHANDISE

7X is kept in a special security vault in a bank in the United

States.

How is coca - cola made?

The first thing is to ~ A x t the bottles (both new and L

returned), and dispose of those with defccts. The bottles ar2

ttlen washed thoroughly. After this, the bottles are closely

scsut~nized to ensure they are hyyienrcaliy clean and not I

cn~pped. In another section of the plant, pure refined sugar

is added to pure drinkable water to produce a solution called

'simple syrup':

In the next stage, the syrup is passed through a filter tp

ensure its purity. This then flows to a poini where it is mixed

with the undiluted coca - cola solution known as concentrate.

Carbon dioxide gas (C02) is now added to give refreshing coca -

cola. At this step, coca - cola is now tr~easured into bottles

mechanically

People got to know about coca - cola t h r i ~ g h Dr. I

Pemberton's Advert~sing and Marketmg activities. Coca - cola b

came into Nigeria in 1953 when the Nigeria Bottling Company

opened its plant in Lagcs. About 7,000,000 bottles of Coca ,-

Cola are iaken in Nigeria annually. Other drinks made by NBC , ,

include; Fanta orange, Fanta Chapman, Sprite, Krest Bitter

Lemon, Schweppes Bitter Lemon, Soda, Tonic and Eva Ta e 81 1

Water.

SOCIAL RESPONSIBILITIES BY NBC FOR A BGTTER

NBC has helped developed other industries such as, Delta

Glass company which produces soft drink bottles; Grown

Products Limited which n~anufacture bottle crowns; Benin

plastic: company which makes plastic cases for bottles. These

are sources of employment for many N~gerians.

(a) NBC employs thousands of Nigerians

(b) NBC has several dealers for its products all over Nigeria,

all of whom are called on once a week.

(d) NBC has the largest privately owned fleet of dellvery

trucks, pick - ups and cars in Nigeria- all working to

bring delicious coca - cola to Nigerians. & I

What does NBC give back to the society ? NBC always

puts something back to the society as a reward for

patronizing its products mainly through Philanthrop~c activities.

For exatnple, the company is n leader in the crusade for

environtnental protect~on. It is conscious of its social

responsibilities. For this reason, it sponsors sporting events I

activities such as:

- Football, where it sponsors the national team and

local competition.

- Table tennis, the Nigeria (closed) championships;

- The conservation movement;

- Activities of thc disabled; and

- Many c~mmuna l events and pr

Pamphlet of NBC PLC, 2001)

A . A - 1 DEFINITION OF TERMS

ojects. (Source:

Econo!,. ic order quantity:

This is calculated ordering qclantity which minimizes the

. balance of costs between inventory holding costs and re8

order costs.

Carrying Costs: hclude such costs as interest on capital

invested in the stock, storage charges, lightening, heating,

refrigeration, rent, handling costs, aud~ting, stock taking or

perpetual inventory costs, insurance and security

deterioration, obsolescence and pilferage etc.

Finished goods: Consists of all stock that is ready for sale.

In a textile company for example: the finished product

comprises different types of textile . . . ..materials that are

already in bundles and can be disposed for sale in the market.

Conipor~ent parts: They are either nianufactured or purchased

units which are carried in stock.

Inventory: Pefers to the quantity of stock that is kept or stored

for m e as the need arises.

Re-order quantity: The quant~ty of the replen~shment order.

Safety stock: Also called buffer stock. A stock allowance to

cover errors in forecasting the lead time or the demand during the

lead time.

b Stock - out Cost: Include such costs as cost contribution through

the lost sale caused by the stock - out, loss of future sales because

customers go elsewhere, loss of customers good will etc.

Supplies: They are items which are not includeci in the

product, except in a way Such things as lubricating oil, r e p i r parts

of machines, cleaning arid polishing materials and similar indirect

cost items.

Work - in process: After the materials have started through the

steps of the process, it is considered as material in process.

2 1

REFERENCES

Fedire, N. (1990): Production, Plannmg and Co-ntrol, New York,

Pergaman press Inc.

Imaga, E. U. L. (1996): Theory and Practice of Production

Manaqement, Enugu, Gostak printing and publishing -

Co. Ltd.

t, al (1 985): Techniques for Production Efficrency,

London, Macniillan press Ltd. b

Lewis, D. (1995): Emerqinq Concepts rn Management, New York,

Macmillan Publishing Company.

Johnson, L

Lucey, T. (1 987)- An Introdi~ctign to CostingA London, EHB and DP

Publicstions.

Lyson, G. (1986): "Purchasing M and E" Handbook in Business

Management, London, Pitman p~~bl ishing Ltd.

Zen?, P. (1985): Basic Prociuctjon Manaclement, New York, John

Willey and Sons Inc.,

Diary of NB PLC, 2tidO.

Pamphet of NSC PLC, 2001.

CHAPTER TWO

2.0: LITERATURE REVIEW

2.1 BACKGROUND TO LITERATURE REVIEW

In any study, such as th~s, it is always imperative to

cr~tically review written opinions, views and statements of other

peqlle, materials and texts that have relevance and reference

to the topics of discussion. This chapter therefore, is aimed

at reviewing some of the most important l~terature OF the

topic - "The impact of inventory management on organisational

performance."

Before this is carried out however, the researcher will

attempt to carry out a conceptual overview, which will enable

us to understand the real concept of inventory management,

before analyzing the various management and control

methods in inventory that are capable of making a great

impact on organisatronal performance.

2.2: INVENTORY MANAGEMENT: CONCEPTUAL

OVERVIEW: I

One of the main functions of management in any system

is the management of inventory, modern business

organizations are increasingly aware :..f the impact of efficient

inventory management in ensuring prompt, effective and

efficient customer's services that result to profitability.

lnventory refers to the quantity of stock that is kept or

stored for use as the need arises. It includes raw materials.

materials - in - process, finished products, component parts, I

suppl~es 1 miscellaneous inventory

Inventory man~gement pertains to the development and ,

administration of policies concerning stock of inventory as well

as the system and procedure by which they are implemented.

The main objective of inventory management is to discover

and maintain the opt~mum level of investment in the inventory.

According to Achison (1 999: 136), "Inventory is the term

for the quantity of stock and lor its value and quality held by

the authority in an organization. It includes the tang~ble

materials /assets of a company other than the f~xed assets; it

comprises raw - materials, all the items to be incorporated into

the finished products, components, work in progress, finished

items or saleable products, that are stored for use as the

need ar~ses". I

Inventory management is synonymous with stock

control, which is a system whereby the levels of supplies in

stock are regulated to maintam quantities requred without

stock excess or stock deficiencies It also involves techniques

used to ensure that stocks are kept at levels that gliarantee

maximum service levels are "stock control coverage analysis" I

This is control technique which aims at maximizing the use of

capital invested In stock. This can be dune by making a

quantitative assessment of likely "carry through" of intakes to

minimize produciion. The techniques serve as a control

mechanism with which the stock balance is continuoilsly up

dated promptly.

2.3 TYPES OF INVENTORIES MANAGED IN AN

ORGANISATION

Before going into detail review of the literature specified

under the above subject heading, we shall first examine types

of invwtory maintained in various organization. I

(a) Raw Material Inventories:

These are those units of inputs which have been

purchased and stored for future prod~lction. They may be

purely extracted materials, half - produced products, or

completely produced ones which the firm does not produce , .

itself.

Their purpose is to differentiate the production function 1

from the purchasing function so as to make the functions

independent of each other. That is, assuming there is a delay

in the shipment of raw materials, ~t does not cause any delay in

the production process. In the event of or delay in procirrement

of raw materials by relying on its inventory.

(b) Work - i:~-proccss Inventory

This consists of partially finished goods requiring

additional work before they become complete finished goods

(c) .'JRO - Inventory Maintenance, Repair and Operating

Supplies

This consists of those consumed in the process of

production, but which do not become part of the product e.g

Lubrication oil, soap, machine repair parts. B

(d) Fio~ished Goods Inventory:

These are completed products ready for shipment as

required by customers. I ,

2.4 FACTORS INFLUENCING INVENTORY LEVEL. 1 '

Many factors combine to influence the level of inventory 'I I

kept i r l every organization. These factors include:- anticipated I

production, seasonality of production; reliability of sources of

supply; efficiency of scheduling purchase and efficiency of

operations. The length of production process determines the

work -in-process inventory while the level of finished - goods

inventories is a matter of coordinatiiig production and sales.

2.5: INVENTORY CONTROL SYSTEMITECHNIQUES ,

The approaches that I: rnanufact~lring firm may employ

for the purposes of inventory control can be grouped into two

broad categories:

a) Stock Replenishment (SR)

b) Material Requirement Plannmg (MRP: B

S t o c k Rep len i shmen t A p , , ~ o a c h

This is a!so called re-order level control method.. In

using this method a level of stock is maintained by setting a

re-order point. As soon as this point is reached it triggers or

\

signals the need for a replenishment of Lie stock of the item.

Orlicky defines stock replenishment as "a set of procedures,

decision rules and records intended to ensure continuous

physical availability of all items comprising an inventory in the

face of uncertain demand".

Material Requirement Planning (MRP)

Materials Requirement Planning is defined by Orlicky ,

In Achison (1999. 137) as "consisting of a set of logically

related procedures, decision rules and records designed to

translate a master production schedule into time - phased net

requirements". Quantities required are specified on the basis

of future demand, and it is precisely determined from the

original producticn schedule for product. Thus, orders for

items are placed when triggered by a time - based signal. The

"Schedule" defines when finished batches and items are *

needed for production. It encompasses scheduling 'and

provisioning activities associated w~ th production resour'ces

(raw materials or parts) to match output needed and supplies

available materials. Requirement Planning is a manufacturing

techriique which is most applicable where the demand for

items is dependent on other items. It is product oriented, and

in most large industries the procedure is computerized

AIMS of FJlatcrial Requirement Planning (MRP).

Thi3 techrlique is usually aimed at:

1 )

ii)

iii)

iv)

Minimizing stock while maintaining delivery schedu

over a period based on market and other information

relating to supply.

To achieve planned and controlled inventories

To promote planning between the purchase and 'the

supplier, and B

To enab!e rapid action to be taken to overcome

shortages in materials and components.

hlanufacturing R e s o u r c e Planning (MRPII)

Manufacturing Resources Plannmg (MRP II) has a

wider impl~cation than MRP I and ~t 1s concerned w ~ t h the

plannmg and scl-~ed;rl~rig of any resources en t~r ing into

prodwtror, includmg machmes, money, and manpower, In

addrtron to materials MRP II has many cleta~led aspects

wh~ch cannot he conveniently covered In this work, but an

Amer~can defrn~t~on can suff~ce to elucidate the meanmg

Manufacturing Resource Planning (MRP 11) was defined

by the ,',merican Product~on inventory control society as:

A systern built around materials requirements planning,

and also including the additional planning function of production

scheduling and capacity requirements planning. Further, once

planning phase is cornplete and the plans have been accepted

as attainable, the execution functions come into play. These

include the shop floor control functions of input - output b

m~asuremeists, detailed scheduling and dispatching, plus

ant~c~pated delay reports from both the shop and the vendors,

pwchasing , follow up and control, e.t c Te term "closed loop"

~rnplies that, not only is each of these elements rncluded in

the overall system, but also there IS feedback from the

execution functions so that planning can be kept valid at all

times.

2.6 REASONS FOR INVENTORY CONTROL IN AN

ORL~.\NISATION

Firm may have various reasons for carrying the

inventory, Levels in his own views slates that the principal

reasons for carrying inventory are: , .

(a) To meet up anticipated demand. In other words to

avoid out of stock syndromes, Inventory control helps

to ensure that customer's demand will more ,often

than ilot be met. This will enable the organization to

satisfy customers demand ~ i ? d it will continue to

enable the organisation have stock of customers

demand.

(b) Price of stocks fluctuates as a result are in high I

demand at a particular period and gets - less demand I -

at other time. Raw materials inventory may be in

high supply at a particular season and scarcely

available at other period. Adequate inventory control

help firms take advantage of seasonal an3 other price

fluctuations.

(c) The advantages derived from discount allowances in

busmess undzrtaking cannot be over emphasized.

F~rms may decide to purchase more supplics than

immediate quantity requirement. This w~ l l earn the filrm

quantity discount a d v a n t a ~ , ~ On me othcr hand, they

will only incur the slightly higher holding and storpge

costs. If those increases in costs are more than offset

by the reduction in the firms unit cost as a result of

large quantity purchases, the firm stands the

chance of having economic gain. I I I

(d) Adequate ~nventory management , acts as an

insurance against longer - than - average supplier

delivery times. Customers demanding their usual

quota of goods are likely to be impressed if they c&n

obtain the same cgcjods elszwhere.

(e) Lack of parts and non - ava~lability of raw materials

bring disappoir-dment In meeting up with customers

order which affects the company's reputat~on and

performance Good inventory control help to mmimize

delay in product~on caused by lack of spare parts and

non-availab~lity of raw matsriais W ~ t h products

comprising many components and sub - assembl~es,

it is administratively nearly impossible to ensure that

one of each of all these parts arrive simultaneously at

a final assembly point. In this situation, stocks of

1 components and sub-assemblies at assembly points

1 act as a buffer within the production system to

1 absorb the demand that the system exerts on itself.

1 Other reasons for inventory control as suggested by

1 Morgan include:- , (i) To forecast against price fluctuation and cost

changes.

( i i ) To avoid under employment (under productivity

machineries and at the same time to keep sto

equipment operational or from shutting down.

( i i i ) To handle production variation

(iv) To hold off increasing capacity

(v) To provide raw material storage

(vi) To assure the customers of the availability of

products. b

(vii) To give customess continuity bf services in the face of

sales fluctuations and break down of machine.

(viii) To take advantage of a favourable raw material price.

(ix) To await shipnient to fill a definite or an expected

order.

(x) To provide goods for customers' order in case of

strike and work stoppages.

(xi) To take advantage of distribution costs or factors.

(xii) To absorb planning errors and unforeseen fluctuations

in supply and demand

(xiii) To facilitate smooth production and marketing

~ p e r a t m .

2.7.1 ECONOMIC ORDER QUANTITY

The carrying of materials in inventory is expensive.

Several studies conducted a number of years age, ,ndicate that

the annual cost of carrying a production inventory average

approximately 35% of value of the inventory.

Wetch (1990:36) notes that five major elements

inventory carrying ... . Costs.. in the following manner

Interest charges on the investment

Insurance costs

Property? Taxes

S i ~ r a g e costs

0; . 4escence and deteriorat~on.

Interest charges on the investment:

comprise

This has to do with the tying down of capital of the company.

When a firm purchases about N150,OOO worth of a production

material and keep its inventory, it simply has this much less

cash to spend for other purposes since money invested i~n

production equipment or in external securities earns a return

for the company. Conceptually, it is logical for the company to

charge all money invested in inventory a rate of interest equal

to that it could earn if invested in something else. That is the

opportunity cost associated with inventory investment.

l n s ~ ~ r a n c e Cost:

Most firlns insure their assets against possible logs

from fire or other firm's damage. Extra deposits worth of

inventory represents an additional assets on which insurance

premiums must be paid property taxes.

Property taxes are levied on the assets values of a firms

assets, the greater the inventory value, the greater the

assets value, and consequently the higher is the firm's tax, bill.

Storage Qist:

The Warehouse in which a firm stores its inventory is

associated by a certain amount of money per year over the

length of its life. The cost of the warehouse is conceptually

charged against inventory occupying the space

obsolescence a n d deterioration:

In most firms a reasonable percentage of a given

inventory stock spo~ls, damage, p~lfered and eventually

become obsolete. Its new product is been introduced

" ,

everyday, a cbrtain percentage of inventory gets obsolete.

Carrying costs rises and falls nearly proportionately w i h

the rise and fall of the inventory level. Furthermore, the

inventory level is directly related to the quantity in which

materials is ordmL;red The larger the order quantity. the higher

is the average inventu-y lwe i during the period covered by the

orders. Costs carrying inventory vary nearly directly with the

size of the order quantity, this is described in

Figure 2.1 :

When considering this group of acql~isition costs, we observe

they behave quite differrntly from carrying costs.

Acquisition cost unlike inventory size are function of the

number of order placed during a given period of time.

EOQ occurs wher: ^C= = AC

IQC = Q

Solving for Q = IQ = IQ' C = ZUA Q" = ZUA ----

IC

ReqLrisition Costs:

These are the actual prlces p a ~ d to suppher usually, total

acqursrt~on cost are not major concern in planning mventory

pol~cy Except where a quality discount IS ava~lable, these

costs do not change with the pattern rn which mventory items

are purchased.

The availability of the fund to be used In acqulrlng

. affects the quantity to be purchased and so influences tlfe

inventory levels.

Carrying Costs:

There are costs incurred because the raw materials are

in company's custody These could be grouped under the

following: 1 ~ 1

Insurance, personal property, taxes, cost of storage space,

breakage, obsolescence and the rate of return on the

investment in inventory des~red by the company. Furthermore,

the cost can be grouped into physical presence of goods and

the coct of capital tied up.

40

Shortage Costs:

These are penalties wh~ch the busmess pay when the

demand exceeds the supply. In other word they don't have

stock to meet the demand of customers.

A shortage of required products niay result In losing

customers apart f rn , rn the losses of the immediate sales.

These costs are the most diff~cult to assess and incorporate in

. mathetnatical inventory models, since they depend upon such

imponderable as loss of customers goodw~ll, reduct~on in future

orders, change In market share and so on.

To prevent cost caused by stock-out, a level of inventory

must be maintained.

Total carrying costs and total ordering , cost vary

inversely The greater the quantity of inventory in hand, the

greater the total carrying costs and the lower the total

orderirig cost.

4 I

Ivventory Costs:

Inventory costs are those variables used in determining

the economic order quantity (EOC!) which is used to

determine the optimum size of mate

rials to order. In most cases, the total costs of an inventory

is the sum of total ordering cost, total carrying costs and

total acqulsltion cost- Shortage cost is a type of inventpry

costs too. b

2.7.2: DERIVATION OF ECONOMIC ORDER QUANTlTY

The deviation of the basic Economic Order Quantity

(EOQ) model is quite easy in a situation where both the

amount of product needed during a grven period and the lead-

time for stock replenishment are known. If the time that

elapse between the placement of an order and its receipt.,,in

inventory is 10 days and daily usage rate is 20 units, the

order point according to Flippo and M~s inger , (1978:489)

should be set at any inventory level of 200 units.

In ordki words, when the stock is reduced to 200 units,

an order should be ,,laced. The unit on hand will meet daily

demand until the order is received. When lead time is nut

known with certainty, it can be treated as random variable and

an appropriate decision rule can be developed to spec~fy the

re-order level of stock.

Economic order Quantity

Source: Management by Flippo and rbl~smger(l978:489)

Let;

D - - Total annual demand

Economic order

Number or orders placed and ieceived during

the year

Average inventory

Cost of placing an order

Carrying cost per Unit of inventory durinpthe

year.

Total inventory cost IS defified as the sum of ordering cost and

carrying cost. To define total inventory cost in terms of the

controllable variables, order quantity (Q), we must express

both types of cost in terms of quantity. Total ordering cost can

be obtein?d by multiplyirlg the number cf orders DIQ by the

cost of placing an order (CO), hence:

Annual ordering Cost = DIQ CO

We can also find annual carrying cost by multiplying the

carrying cost per unit of inventory (CC) by the average number

of units in stock ((212). This exprexion for average rnventory

assumes a constant rate of demand throughout the year.

Annual carrying CoSi = Q/2 CC.

We shall remember that this variable can be manipulated by

management to yield the minimum cost for mventory during a

specific time per~od.

From the figure drawn above, we observed that optimum

solution IS that quantity (Q) that can therefore be obtained by

setting the equat~on for ordering cost equal to the equation

for carrying cost and solving for Q . i.e

Annual carrying cost = Annual ordering c o w

CC Q/2 = DCOIQ

CC ~ ~ 1 2 = DCC)

Q' = 2DCOICC

Q = - +\I2DCO/Cd 1

The optrmum solution is also obtained by differentiating the

total cost function to obtain an ecpatiori tnat expresses the rate

of change in total cost with respect to change in quantity when

the first derivative of the total cost function is set equal to zero, the

ecol?omic order quantity is obtained by solving for Q.

This is the following step order.

Step I: Take the first derivatives of total cost function.

Cost function.

TC = D/QCO + Q/2CC

d ( T C ) dQ = - DCO lQ2 + CCl2

Step 1 1 : b

Set the first derivative equal to zero and solve [or Q.

Q = poco 4 CC

Step Ill:

Test to determine the so l~~t ion in a minimum

dz (TC) dQz 2DC0 JQ30

Given the assumption of a fixed demand, the general

formula can be utilized in finding the economic order quantity

(Q). which iq equal to the square root of 2 times demand (D)

times ordering cost (CO) divided by carrying cost (CC).

For exa dple, assume the following problem:

D = 3000 units per annum

CC = N 2 per Unit per year.

To determine the economic order quantity, evaluzte the

basic equation using the values for the demand, ordering

cost and carryins cost.

QO = \ / 2 ~ 3 0 0 0 ~ 3 0 2 = \/90000

Q = 300 Units.

To obtain the order quantity is 300 units; observe that a

total of ten orders will be placed

For a total cost due to ordering of 300, average

inventory will be 150 units.

average inventory carrying cost will equal N300.

Therefore, total inventory cost will be equal to N600.00.

2.8: GAINIIMPORTANCE OF INVENTORY CONTROL

QUANTITY DISCOUNT: ,

0 : ~ e of the restrictions on the use of the general

economic lot size formula is that, in the case of a purchased

item, the unit purchased price is constant or that, in the case of

a manufactured item, the direct unrt manufacturing cost8 is

constant. When this condition is not satisfied, it becomes

necessary to modify the way in which the formulas are used

to obtain the economic order quantity.

In summary, when quantity discounts are available, the

analysis begin with a determination of the econon-tri lot size

for cash price level. For a given price level, this lot size is

ascertained by first substituting the corresponding carrying

cost in the economic lot size

It IS unan~mously agreed that lnvl n:or~es play a v~tal role

In the life of any organ~zat~on Inventory roles In an

-4 ti

organisation has made it to be considered as the blood bank of

the firms stock. Howard and Baltz (1989:15) supported this fact

when they asserted that inventory is the life blood of

prodc~ction and sales activities; if it were improperly managed,

production process would collapse.

Inventory also influences the working capital needs of

the firm from :he financial stand point. Fund tied up in

inventory are one step further removed from cash in the

working capital cycle. Since inventory is further removed

from cash than receivables are, it needs financial attention if b

the firm's liquidity is to be maintained.

According io Haddley and Whittin, (1963:8) the

fundamental reason for maintaining inventory is that it is

either physically impossible or economically unsound to have

goods arrive in a given system precisely when demnds for

them occur. To Samuel and Wilkes, (1978) there are two

main functions of stock, firstly, to enable production (or

ordering as the case may be) to take place in economic

quantities, and secondly to enable

4 9

oders to be filled promptly from stock. In both C ~ S ~ S ,

production is shielded from the day to day vagaries of demend

and supply and take place at a rate and to a total level which if

not optimum is at least practical. As an ideal, inventory theory

v~ould seek to trade - off these benefit optimally against the

costs.

To Marthin and David, (1982) there are three general

motives for holding inventories:

- the transaction motives which' emphasize the need to 0

maintain inventories to facilitate smooth production

and sales operation.

- The precautionary motive which necessitates holdipg

of 'inventories to gilard against the risk of

unpredictable changes in demand and supply with . I

other forces. 1

- The speculative motives which influences the decision

to increase or decrease inventory levels to take

advantages of price fluctuations.

5 0

Amey and Eggiton (1973) shared the view with Martin

and David when they agreed that firms hold inventories for

transactory, precautionary and speculatory and speculative

motives. They went to assert that management should be

aware that optimum stock level do depend to a certain extent

on expected price movement.

To R~chard et al, (1988) inventories add an operating

flexi biliiy thar wouici not otherw~se exist. b

In manufacturing, work -in-process inventories are an

absolute necessity unless each individual part is to be carried

from machine to machine and those machines set up to

produce that single part. They enumerated the importance of

inventor~es as:-

(a) Filling the gap between supply and demand

(b) Making possible lower production costs

(c) Allo(...linq organisation to cope with perishable

materials.

(d) Storing labor.

2.9: PROBLEM OF INVENTORY MANAGEMENT

According to Kostas, (1 981) the inventory problem

involves the formulation of decision rules that answer to

important question

(i) When is it necessary to place an order (or set up for

production) to repknish inventory

(ii) how much is to be ordered (or produced) for each

replenishment

According to him. the decic:iori rules must aim at satisfying

anticipated demand at a minimum cost or maximum profit.

Haddley and Whitte (1963:B) reasoned along the same line.

To them, the two fundamental questions that must be

answered in controlling the inventory of any physical good are

when to replenish the inventory and how much to order for

replenishment. Essentially every decision which is made in

controlling inventory supply may be, is in one way or the other

associated with the question of when to order and how much

to order. Kim, (1 979:i'I) classified inventory problem into

two:

Deterministic and probabilistic. Suppose that the demand for

an itcni during a specified period is known in advance and the

lead time is either zero or a known constant, then we have

what is called a determin~stic ~nventory management problem.

It is true that those assumed condit~ons do not qu~te obtain in

most actual inventory managemmt problem for which these

assumptionq are quite adequate. For example, when the item

in question in used as raw materials for a stable product~on b

proccss, furthermore, it has been found in practice that

deterministic inventory models are quite helpful in controlling

the stock of many regularly used low va!ue items

In many s i tuatws, our assumptions of known quantity,

and zero or constant lead time do not hold. Often the demand

and lead time are variable quantities, so that we know at best

only their probabil~ty distribution. If we assume that both

demand and lead time are random variables, the analysis of

inventory management problem will become very complex. It

has been found however, that reasonably good situation can

be obtained for many practical inventory management

problems by assuming that the lead time is a known constant.

2.10 FUNCTIONS OF INVENTORY

Inventories at all time require high cost and investment

commitments. Some organizations see inventory cost as an

unnecessary evil but they have not been able to analyse

cr~ticaliy the iota\ situation cjf the costs. Before critics ,can

argue unfavocrrably upon the size and costs of inventory, such

opinion must weigh the gain and contribution inventories

generate to the capital structure of the organisation holding

that inventory.

As a matter of fact, inventories make poss~ble smooth

and effic~ent operation of a manufacturing organisation by

decoupling individual segments of the total operation.

Inventories on the 'purchased parts perm~t activities of

purchasing department personnel to plan and conduct

independently of shop production operations. In doing this,

they allow flexibility for supplier in planning, producing, and

I , : :livering an order for a given part.

In some organizations, inventories of parts and components

are produced "In - House" dxoup le the many individual

machines and production processes from various sub-assembly

and assembly activit~es. This enables management to plan

production.

b

2.1 I: MERITS OF IiWENTORY MANAGEMENT

Inventories are accepted to be carried because

producing and w ing activities of inventories typically take

place at different times, in different rates. Moreso, in

manufacturing outfits, a lot of savings are generated from

holding inventories. Such savings cover the storage costs

over the period required for sales or shipment to take place.

Obviously, it was generally believed that two danger

points exist in inventory investment, carrying too little inventory

and carrying too much inventory. But the major goal of

inventory control is to discover and maintain the optimum level

of inventory investment and this optimal level lies between

these two danger points. P.lso, experiences of the business

managers have shown that kep ing inventories acts as an

insurance against higher than average demand and as well as

against longer than average supply delivery times.

tiowever, these forgone views were shared by Ammer

(1980:275) in his study that inventories are kept in or,der to

achieve advantages of quant~ty discount, seasonal price

fluctuation as well as minimize delay in production caused by

i :k of parts and other inp~l t materrals; He used weighted

average in analysis of the importance of inventory contrd, but

c o ~ ~ l d not properly determine the effect of time factor on the

seasonal and cyclical inventories.

Similarly, Kotier (lWO:l57) in his study opined that the

primary aim of carrying and holding inventories is because of

the fact that it is physically impossible and economically

impracticable for each stock item to arrive where it is needed at

exactly when it is wanted

In the same

inventories are kept

way, many people believe also that

n production w i t to have price advantages.

This is because bulk purchases usually attract quantity discount

thus providing cost advantage of inventories. In line with this,

Cushing (1978: 57) noted that the risk of production shut down

should be over come by holding inventories. He further added b

that inventories are kept for speculative forward buying

purposes. Iri the same manner, savage and small product by

reducing customer's delivery analysis but could not establish

the effects of inventory investment on the performances of the

sample companies. '

Lewi's (1990: 65) in his contribution noted that greater

flexibility to the prcduction department in planning production

runs as an advantage of holdlng inventories. According to him,

production shut downs result to increased costs and delays in

delivery time which leads to loss of customers. He applied

weighted average too in his statistical analysis, but lacked

homogeneit!f in the choice of his studied industries.

lmaga (1995377) noted two major reasons for keeping

inventories namely:- to keep the production operation

flowing smoothly and for prompt customer's services. He used

simple ratio and percentages in his statistical analysis.

Finally, it could be inferred from varlous contr~buttons so

- far that there exists uncertainty in the procurement of industrial

raw materials and this may be delayed because of such

factors as strike, transport disruption, short supply and hence

firms should maintain sufficient stock of raw materials at any

given time to streamline the production.

2.12: DEMERITS OF INVENTORY MANAGEMENT.

Studies had shown that firms need enough inventories

I

especially in the production and maintenance units to avoid

shut down of plants, loss of organisational profits, loss 'of

customers. But there are some perceived pitfalls arising from

keeping excessive inventory. For example, statistics has shown

that the laiyer the inventory carrying costs - interest charged on

capital, insurance, taxes, storage costs, obsolescence,

deterioration, depreciation, record keeping cost, holding and

handling costs, inspection costs ,ar,d distribution costs increases.

In the light of the above, Morgan (1983:57) stressed that

th, higher the value and levels of the iwentories, the greater

the property tax levied on the firm's asskls, and that the dangers

in carrying large inl-entory is that inventories are subject to b

pilferage losses, obsolescence and deterioration. He adopted 2

simple regressional analysis in determination of the relationship

between the inventory related costs and organisational

performance. ? .

AIL, another demerits of holding large stock as expressed

by Kotler (1980:83) co~ l ld be clearly viewed from a cost point of

view with emphasis on customer's servlce. He demonstrated in

fig 3 !. Aow that inventory costs increase at an increasrng rate as

the customers services level approaches 100%.

5 9

Fig. 3: Relationship Between Inventory Costs and Level of

Customers services.

9001

Service Level (percentage of orders that can be filled from

stock)

From the qraph of fig.3 :hove, Kotler (1980:87)

Illustrated that 85% of the total received orders from the existing

stock of the company's inventory is valued at N400,OOO. He

observed that where the firm raises the customer's services

, '

standard by 5 percent to 90 percent, the total value of

inventory investment will be increased by N100,OOO and also

if the standard of service is raised to 95 percent, investment

must be increased by N200,OOO. He conclusively believed

that increase in service indicates increase in inventory costs.

However, it is generally viewed that his argument is faulty. It

tends to ignore the capital basis of the sampled and studied

companies. @

2.13: INVENTORY MANAGEMENT AND CONTROL BY

NlGERlA BREWERIES (NB) PLC.

The following are the type of inventory management in

NB PLC.

(a) Raw material inventories:- They are those units of

input which have been purchased and stored for f

future production. 'They may be purely extracted

materials, half - produced products, or completely

produced ones which the firm does not produce itself.

6 1

Their purpose is to disintegrate the production

function from the pw-chasing function so as to make

the two functions independent of each other.

(b) Work - in --process inventory:- This m-isists of partially

finished goods requiring additional work before they

become complete finished goods.

(c) MRO - inventory maintenance, Repair and operating

supplies:- These are consumed in the proddct

process but which do not become part of the product

e.g lubrication oil, soap, machine repair parts.

(d) Finished Goods inventory:- This is completed products

ready for shipment as request by customers. ( source:

interview with the pr~duction manager)

234: INVENTORY MANAGEMENT AND CONTROL BY

NlGERlA BOTllNG COMPANY (NBC) PLC

In NBC, their sources of raw materials 1s 80% imported.

Thk raw materials order are made from the head office. The

one month. The raw materials storage method is FIFO method

(ie first in -first out).

There are problems encountered in the management of

the raw materials inventory in the NBC. And the nature of this

problem is hazardous and corrosive, as claimed by the

respci idents from the store, distribution and personnel

departments respectively. (Source: Interview with the Personnel

Officer)

2.15: SUMMARY OF LITERATURE REVIEW

b In this chapter (literature review), the background to the

study was carried out, then followed by the conceptual

overview of inventory management. The next that was

x- rayed was the types of inventories managed in an

organization, under this, the following were discussed:- Raw

materials inventories; work - in - process inventory; MRO -

inventory Maintenance, repair and operating supplies, finished

goods inventory.

The next that was discussed was the factors that

influence inventory level. Followed by the inventory control

system1 techniques which includes: stock replenishment (SR)

and Material requirement planning (MRP). Also, not left olut of

disci~ssion was the reasons for inventory control in an

organisation. This was followed by the economic order quantity

and derivation of ecvnomic order Qmrrt~iy, cost formula.

The gainslimportance of inventory control, which include

quantity discount e.t.c problem of inventory managemmt;

functions of inventory; Merits of inventory managemenh and

Demerits of inventory management were all discussed.

Finally in this chapter, was the brref x-ray of the inventory

management and control of both organizations (NBL and

NBC).

REFERENCES

Amey, L R 8. Egginton D N; Manqement Accountinq: a Conceptual Approach. Longman, 1373.

Arrow K J T Harries; "Optimum Inventory Policy", Econorne!rica, XIX '951 . --.-- ...- . -

Buyers, CI & Holmes GA; "Material Control" Principle of Cost Cost Accounting; cassed London; 4'" ed. 1984.

Dvorekzy, AJ Kiefer, and Wolfowitz; "This lnventory problem 1: Case of I .J~kncwn distribution"

b Econometrix XXI (1 95'3).

Edwin, B Flippo & Garry, M blusiilger: "Allocation and Control of resources", Manaqement, Allyn and Bacon, Inc., 1978 .

Hardley,G & T.M. Whitin: "The Nature of Inventory System," Analysis of lnventorv System. Prentice Hall, Eaglewood Cliff N J 1963.

Operation and Ccsts act$^ hilanaqernent Series) Chicago: A WShawCo 1915. 1 1

KIM "Economic order quantity" Quantitative Analysis for Managerial Decision, Addison - Wesely Publisl-mg Co. 1976 .

Kola Folayan, & Modupe Adegun: "The story of Excelling "

History of lever Brothers from - 1983.

Kostas, N. Dervitsiotis: " Inventcry System and Models" Operation Manaqement, McGraw- Hill book 1981.

Lewis, C D

Melnitsky Benjamine;

Scientific Inventory Control, ,Hiffe, London, (Forthcoming).

Manaqement of Industrial Inverltorv. Philadelphia, Chilfon Company, First ed. 195 1.

Pandey I M "Management of inventory". Financial management Vikas publishing House PVT Ltd "79.

Samuel JM&FM Wilkes; "Management of Inventory" Management of Company Finance. - Welson, 2fld ed~tion 1978.

Synder, Arthur: "Principle of Inventory Management". Financial Execitive X X U (April 1964).

Starr, Martin, K & David W Miller; Inventory Control: Theory and Practice. Englewood Cliff, N.J. Prentlce - tlall 1962 p. 17.

Van Hees, RN and N Monhemius; Introduction to Production and Inventory Control: ~heo ' r y and Practice. Macm~llan. 1972. ---.

Whitii-I, T M; The Theory of inventory Ivlanaqernent. Princeton, N J Princeton University Press

CHAPTER THREE

3.0: RESEARCH DESIGN AND METHODOLOGY

Th,is chapter presents the researcher's methodology and

processes involved in carrying out the research project. The

chapter is divided into subsections as presented below:

3.1 RESEARCH METHOD

The type of method to be used in any research

undertaking is determined substantially by the nature of the

research problem and purpose of the study, the use of

descriptive or normative method of research is regarded by the

researcher as logically sound and adequate for getting solution

to the problem posed by the study. i

3.2: METHOD AND SOURCE OF DATA COLLECTt3N

The researcher employed :he use of multiple data

gathering technique in order to adequately cover research

questions and hypotheses and to achieve precise and reliable

result

The exploratory survey method which embraces

quest~onnaire and interview was used as primary data gathering

~ns i run \~ ;-d. Since according to Busha (1986) researchers

consider it to be the most suitable technique for discerning

"the kind of information needed by users as well as i,re source

on which most researchers commonly rely". The researcher

used questionnaires and personal interview for the purpose of

primary data collection.

3.2.1 : QUESTlONNAlRE

The researcher made use of questionnaire to elicit

information from field research.

The questionnaires were admmistered on two categories

of respondents which include:

1. For respondents (i.e the management and staff of

Nigeria Breweries PLC;

2. For responuents (i.e the staff and Management of

Nigeria Bottling Company PLC.)

3.2.2: INTERVIEW METHOD

This .,thod was r~sed to extract responses to questions

that were not included in the questionnaire, but which are vital

to the research. Personal structured and unstructured

interv~ews were conducted wtth the consultants in the area of

management sciences and Business Administration.

3.2.3: L1B2ARIES

Materials from libraries and other research unlts whch

~ncli lde books, journals, weeklies, notes, unpubl~shed projects

leaflets, Pamphlets and dailies were used as the secondary

source of data collection. This was employed essentially to

prov~de a theoretical f ramt3~~~~ t -k for the study. Both private

and public libraries were consulted.

These in addit~on to personal interview compensated for

inherent weakness of the primary data gathering methods,

thereby, enhances research rel~ability.

3.3: THE POPULATION OF THE STUDY

The population for this study was mostly drawn from the t

management and staff of the Nigeria Breweries PI C and

Nigeria Bottling Company PLC, Enugu.

3.4: PROCEDURE FOR THE DATA GATHERING

Research questionnaires were given to the people

scientifically selected for this study. They were requested to

either circle or tick the option that best suited their choick and

also fill the blank spaces, with whatever they felt were the

answers.

In order to avoid delay and at the same time ensure high

percentage return of questionnaires, they were distributed by

hand and collected after they have been duly completed ,py I I h I ; I

the respondents.

3.5: VALIDITY AND RELIABILITY OF DATA INSTRUMENT

Validity as used here is the degree or extent to which an

instrument actually measures what it is intended to measure.

Therefore, an instrument is valid to the extent it is tailored to

achieve research objectives. Thus, the instrument used for

t h ~ s research was validated by ensuring that the questions

were structured in a manner that will enable the research

obtain information relevant to the purpose and objective of the

study. , .

In order to maximize reliability of the instrument used for

the research, the investigator ensured that questions were not I

ambiguously presented to respondents in a manner likely,to

cornniunicate different meaning that could generate inaccurate

and incorxistent responses.

The researcher also maintained objectivity by not fielding

leading questions A pilot survey using ti instrument was

earher carried out to ensure validity and reliability.

For pie-testing, ten (10) members each of the

mmagement and staff of Nigeria Breweries PLC and Nigeria

Bottling Company PLC, Enugu, were selected and had the

questionnaires administered on them. The respondents

answered the questions with ease. Though, in the process,

some errors were identified and suggestions were made.

These were corrected and adjustment effected.

This pre-testing method is for the following:

(a) To identify at the initial stage, any problem that might

be encountered in the course of the research.

(b) To let the responknts make their observations and

criticisms, and

(c) Ensure that further mistakes are eliminated. b

3.6 DETERMINATION OF SAMPLE SIZE

To determine the sample size, the researcher conducted

a pilot survey In wh~cl i 20 of the research questiorinair-e was

administered randomly on the management and staff of both

Nigeria Breweries PLC and N~geria Bottlmg Company PLC,

3u t ~f the number, 17 were correctly filled and returned.

It was therefore, taken as positive response. The remaining

3, represented the ones that were rejected. These were

regarded as ~egative responses. The percentage of response

therefore, is 05 and 15 respectively.

To calculate the optimum sample size, the researcher

applied the Fruend and W~lliams Model of sample size

determination, calculated at 95% confidence level and 5%

standard error, the : . ! w l a is:

N

Where:

N

P

Q

E

7 L

= Sample size

= Percentage of positive response

= Percentage of Negative response

= Percentage of error - - Normal variate for the desired level of

confidence.

Substituting and solving for "N"

With this outcome, the researcher decided, to

approximate the sample to 200 for easy administration. I

3.7 METHOD OF DATA ANALYSIS

Data collected wdl be coded, grouped into frequencies,

computed and arranged into tables for easy references and

analysis. Presentation methods to be used include simple

perceiitages, tables, pie- charts and bar charts and histogram.

b

3.5 TEST OF HYPOTHESES

The main method of analyzing data collected in this study

were the simpie percentage for testing the research questions

and chi - square for testing the hypotheses.

The tormu!a for percentage is given as

Where a = numerator (number of respondents to an item)

b = denominator (total respondents in sample)

100 = Percentage.

The acceptable criterion is 50%. Where the percentage

response is 50% and above, then the statement holds true or

otherv~isie. Where it is less than 50%, it holds as untrue or

otherwise.

The formula for chi - Square is:

WI-ere n,, = Observed frequencies

e,, = Expected frequencies b

The degree of freedom is determined with the following

formula:

df = ( r - l ) ( c - I )

Where r = the number of rows

C = the number of columns

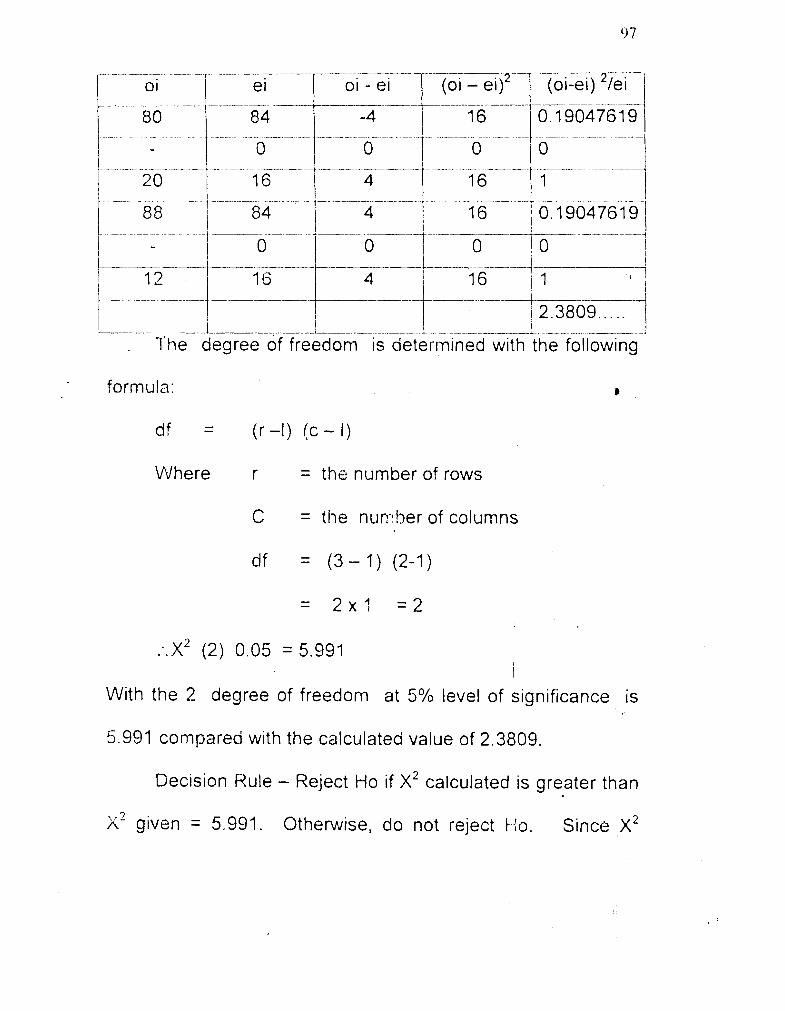

df = ( 3 - 1 ) ( 2 - I ) - - 2 x 1 = 2

:. X' (2) 0.05 = 5.991

OR

df = (2-1) - -.- 1 x 1 = I

:. X' (1) 0.05 = 3.841

YEFERENCES I