Embed Size (px)

Citation preview

University of Nigeria Research Publications

OKETAH, Ifeoma M.

Aut

hor

PG/MBA/93/17519

Title

Risk Analysis and Control In Banks Credit Portfolio Management

Facu

lty

Business Administration

Dep

artm

ent

Banking and Finance

Dat

e

August, 1995

Sign

atur

e

RISK ANALYSIS AND CONTROL IN BANKS

CREDIT PORTFOLIO MANAGEMENT

OKETAH IFEOMA MARY PG/MBA/93/17519

SUBMITTED TO THE FA~S&+Y-'O~F BUSINESS ADMINISTRATION IN PARTIAL FULFILLMENT

OF REQUIREMENTS FOR THE DEGREE MBA FINANCE

UNIVERSITY OF NIGERIA ENUGU CAMPUS

AUGUST 1995.

CERTIFICATION

Oketah Ifeorna Mary, a Postgraduate ti dent in the Department of Banking and

Finance and with Registration NP PG/MBA/93/17519 has satisfactorily completed

the requirements for course and research work for the degree of M. B. A. in

Banking and Finance.

The work embodied in this thesis/dissertation project/report is original and has

not been submitted in part or in full for any other Diploma or degree of this or

any other University.

I

Dr. A. M. 0. Anyafo Dr. 3 E. Chikeleze Head, Desprtmenl of Ranking & Finance, Supervisor, University of Nigeria, Departmcnt of Banking & Finance Enugu Campus. University of Nigeria,

Enugu Campus.

DEDICATION 1 (

This work is dedicated to my husband,

Dr. M. 0. Okwor and my Son, Master Chikeluh Okwo.

iii

1

ACKNOWLEDGEMENT This research could not have been completed'without the

assistance of so many people.

First and foremost, my profound gratitude goes to my super-

visor, Dr. Chikeleze, who developed special interest in his work and

monitored its progress to completion.

My sincere gratitude also goes to my mother-in-law, Mrs. B.

Okwo and my mother, Chief Mrs. R. Oketah for their motherly

love and their moral support.

I also express my gratitude to my brothers-in-law, Dr. Fred.

Okwo for his worthy contribution and guidance which has made

the successfulcompletion of the project a reality and to Mr. Marcy

Okwor and Mr. Charles Okwo for their moral and financia! support.

My gratitude also goes to my brother, Engr. Festus Oketah,

and to my uncle, Mr. Lawrence eneje for their contribution to the

successful completion of this academic programme.

I am equally indebted to the following people who have in

one way or the other contributed toward the attainment of this aca-

demic goal. They are: Mrs. P. Ugwu; Mr. E. Echiegu; Joe Ezeh;

Esther Ugwu Ebere Okwor; Ann Eze; Mr. and Mrs. Diyoke; Mr. and

Mrs. M. Oke; Mr. Osy Oke; Mr. Paddy Ugwuoju; Mr. Paddy Okwor;

Mr. and Mrs. A. Odoh and others whose names are not written

I

down due to space.

Last but not the least, to my hr;sbai?d Di-. M. 0. Okwo and my

5211 ChilieIuba Okwo for contributing in many ways to the atiain-

;-:lent of this goal. And finally, to Almighty God for His protection

,:i:;d guidance over me.

Oketah, Bfeoma M. August 1995.

CERTiFICATION

iIEDICATION

ACKNOWLEDGEMENT

TABLE OF CONTENTS

LIST OF TABLES

LIST OF FIGURES

ABST2.:b*r3T

CHAPEX ONE

INYRODUCTION

1.1 Background of the Study

? Statement of the Problem

i .3 Objectives of the Study

i 4 Formulation of Hypothesis -. - yificance of the Study

S c o p a d Limitation of the Study

Page No.

iii

iv

iv

ix

X

xi

X

1

1

2

3

4

5

6

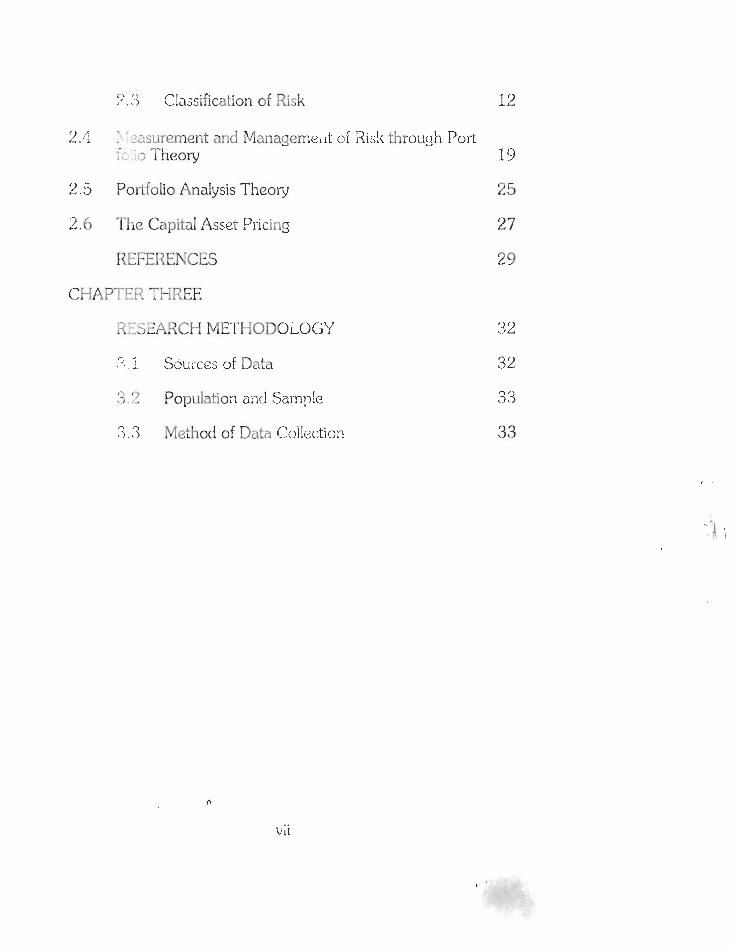

LITERATURE REVIEW 7

2. i The Concept of Risk, Uncertainty and Bank 7

2.2 Distinction between Risk and Uncertainty 9

vi

'7 . \ 3 ) Classification of Risk

2.11 ~xurement and Manayerneht oi Rls!i through Port I _ \i Theory 19

2 5 Portfolio Analysis Theo y 25

2.6 The Capital Asset Pricing 27

REFERENCES 29

CHAPTEi? THREE

33EARCH METHODOLOGY 32

C - < J i Sowces of Data 32

S '2 Population ax! Sampie 33

3.3 Method of Data Collection 33

n

vii

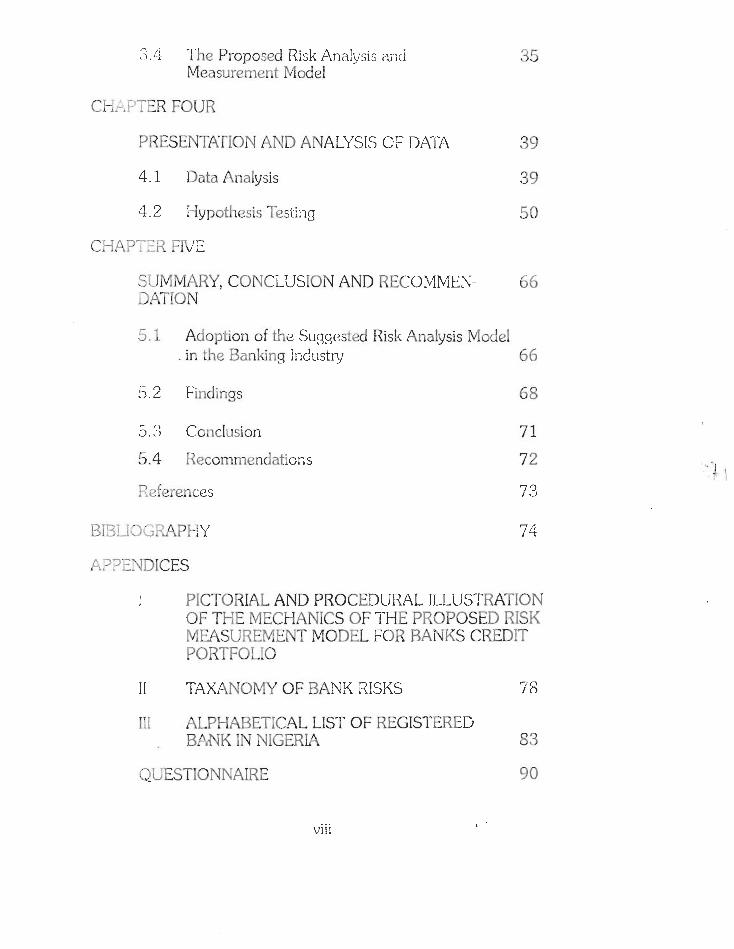

5.4 The Proposed Risk Analysis aid

Measure.mcnt Model

CFI-. '-'TER FOUR

PRESENTATION AND ANALYSIS CF D,

4.1 Data Analysis

3.2 Hypothesis Testing

SLJMMARY, CONCLUSION AND RECOMMEN- 65 DATION

5.1 Adoption of the Suggested Risk Analysis Model . in the Banlcing Industry 66

5.2 Findings G S

5.3 Co~~clusion

5.4 Recommendations

References

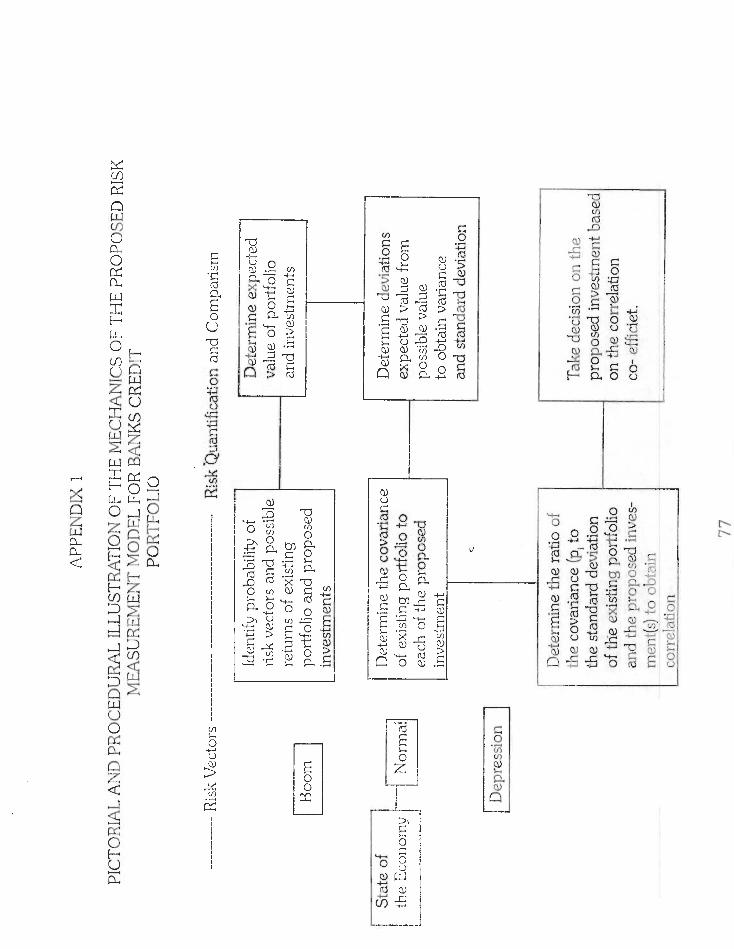

PICTORIAL AND PROCEDURAL ILLUSTRATION OF TEE MECHANICS OF THE PROPOSED RISK MEASUIIEMENT MODEL FOR BANKS CREDIT PORTFOLIO

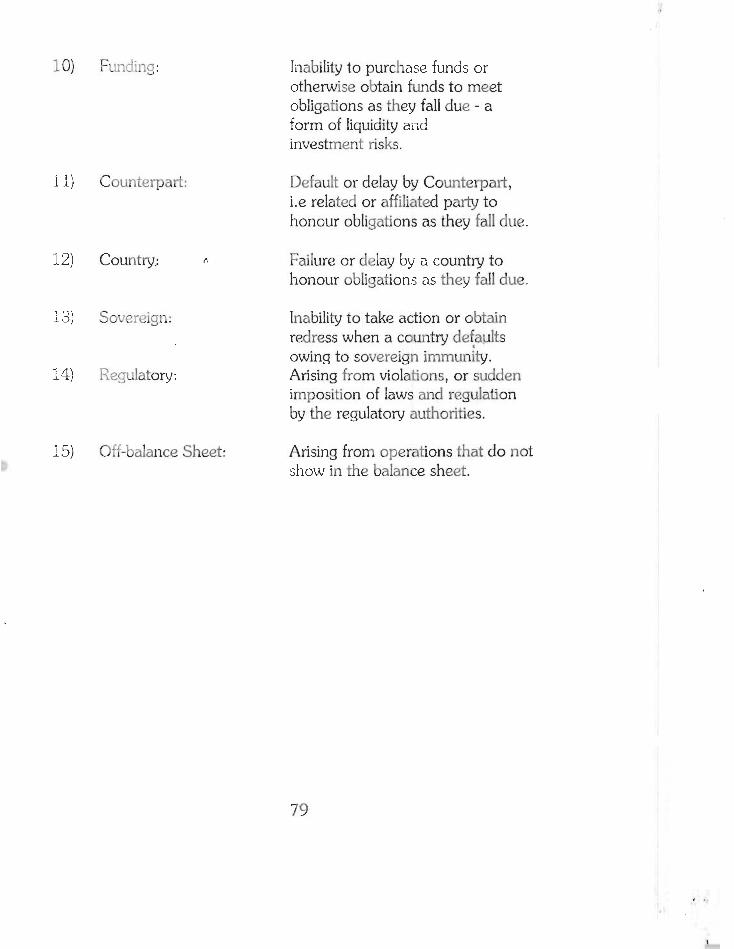

I1 TAXANOMY OF BANK RISKS 78

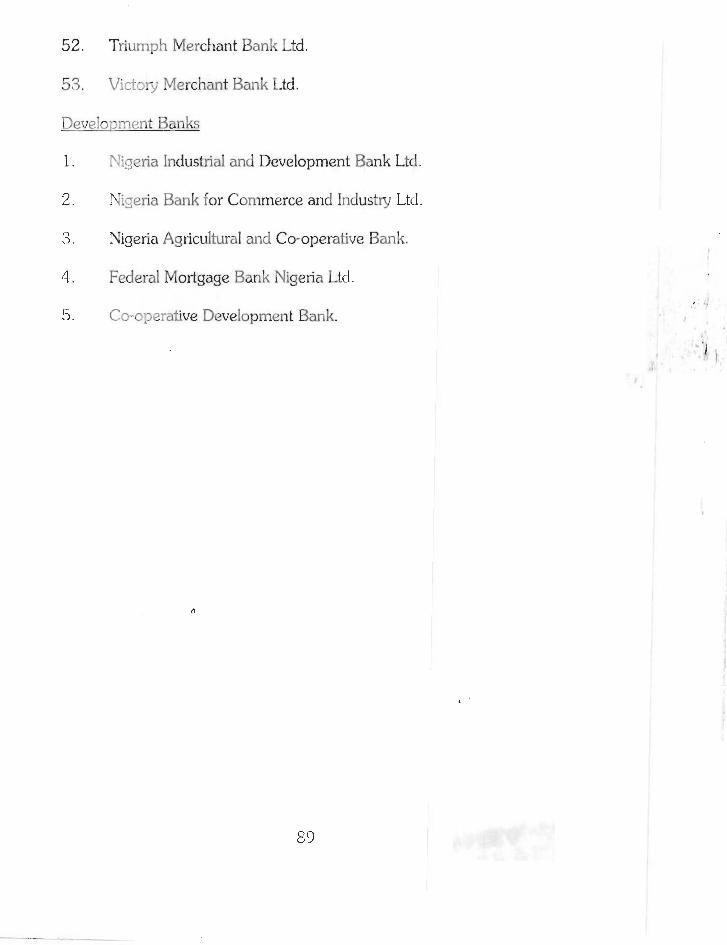

III ALPHABETCAL LIST OF REGISTEREG BAlYK IN NIGERIA 83

QUESTIONNAIRE 90

viii

Table LIST OF TABLES

Page No.

Classification of Respondents Bank by their Areas of Banking Operation 40

Opinion on Risk Analysis of Credit Applications 41

Techniques or Credit Application's Risk Analysis 41

Causes of State Government Banks hsolvency 43 0

Opinion on. the Necessity for Diversification of loan Portfolio 44

Respondents View on the Enhancement of Banks Loan '

PortfoIio through Effective Risk Diversification 45

Opinion on the Employment of Correlation Analysis for Effective Risk Diversification 45

Clas<ification of Banks Provision or Bad and Doubtful Debts 47

CE.'"s Sectoral Loan Allocation Guidelines Effect on versification 48

Opinion on whether the CBN's Sectoral Loan Allocation Guidelines should be Scrapped 49

Hypothesis 1 Table 52

Hypothesis 2 Table 57

Pse!iminary Calculation for Applying Variance AnaIysis Test 58

ix

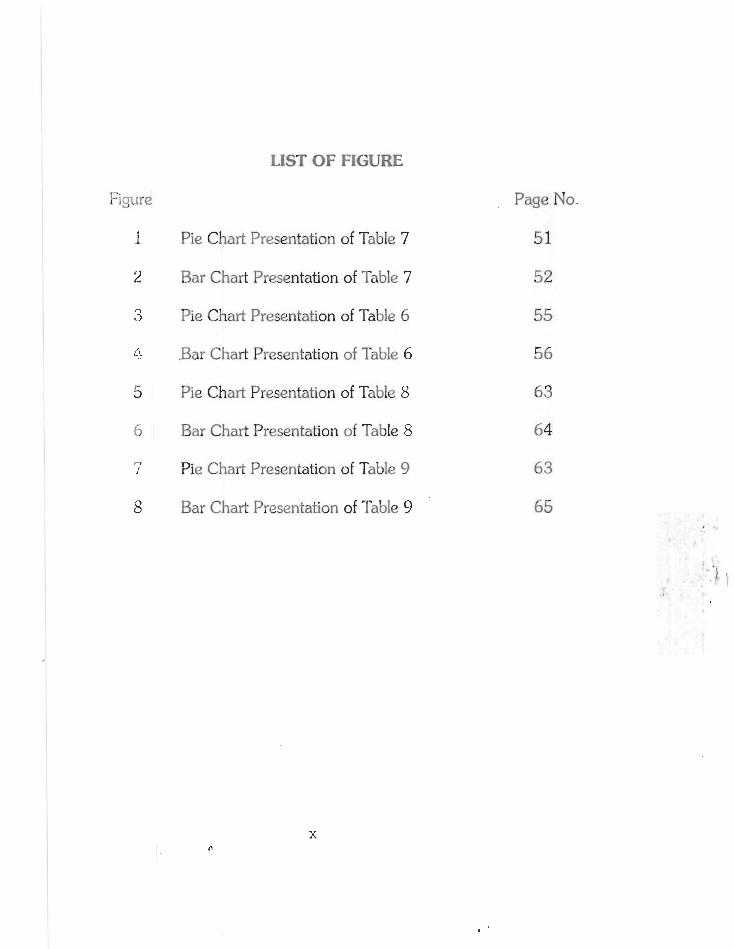

LIST OF FIGURE

Figure

1

2

3

6:

5

6

Pie Chart Presentation of Table 7

Bar Chart Presentation of Table 7

Pie Chart Presentation of Table 6

.Bar Chart Presentation of Table 6

Pie Chart Presentation of Table 8

Bar Chart Presentation of Table 8

Pie Chart Presentation of Table 9

Bar Chart Presentation of Table 9

Page No.

51

52

55

56

63

64

63

65

ABSTRACT

This study is about Risk Analysis and Control in Banks Credit

Portfolio Management. The study Involved ascertaining opinions of

bank managers on risk analysis and control technique in the Nigerian

banking industry. The fundamental objectives of the study, among

others were:

1. To determine the existing tools of risk analysis and control in

banks lending portfolio management.

2. To construct a m d e I far risk analysis and control in credit

portfolio. *l t

The researcher, therefore, developed a risk measurement model

for banks credit portfolio management. The model identifies risk

vectors in the economy; proposes that diversification should be based

on riskcorrelationship; and determines the correIationship in terms

of correlation coefficient of the risk of the existing portfolio with that

of the additional investment. This model formed the basis of our

appraisal of risk analysis and control technique in practice in Nigeria

banking industry. n

The entire commercial, merchant and development banks in

Nigeria were the study population, from which a sample of 56 were

selected. A set of structured questionnaire was administered to the 4

sample, out of which 42 responded.

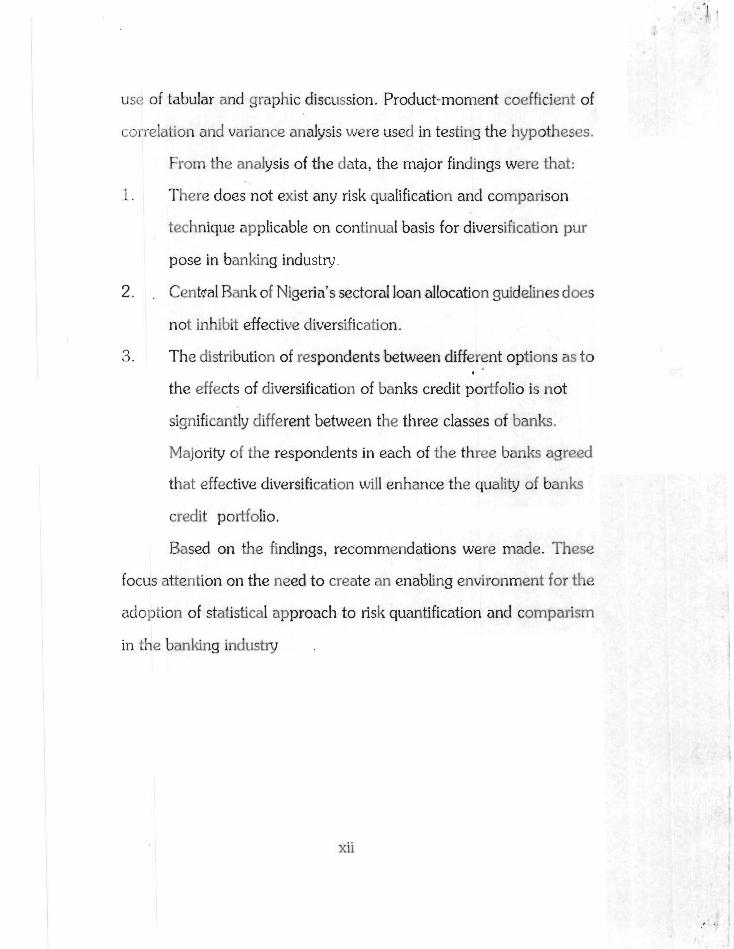

The collected data were classified, analysed and interpreted by

use of tabular and graphic discussion. Product-moment coefficient of

correlation and variance analysis were used in testing the hypotheses.

From the analysis of the data, the major findings were that:

1. There does not exist any risk qualification and comparison

technique applicable on continual basis for diversification pur

pose in banking industry.

2. . CentlraI Bank of Nigeria's sectoral loan aIlocation guidelines does

not inhibit effective diversification.

3. The distribution of respondents between different options as to I

the effects of diversification of banks credit portfolio is not

significantly different between the three classes of banks.

Majority of the respondents in each of the three banks agreed

that effective diversification will enhance the quality of banks

credit portfolio.

Based on the findings, recommendations were made. These

focus attention on the need to create an enabling environment for the

adoption of statistical approach to risk quantification and comparism

in the banking industry .

xii

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study

Banks perform a very important service t o all sectors of.the

~xonomy, by providing facilities fur the mobilization of savings, and

making the funds available for investment purposes by the process of

granting credit facilities to other customers. Thus, these funds are

made available to businesses t o enable them to expand their produc-

tive capacity, and to individuals and household to facilitate consump-

tion. Commercial banks thereby create money by granting credit

through overdraft, loans and advances.

The problem these banks encounter is that most of theses

loan granted are not repaid, leading to making provision for bad

debts. Since the introduction of Central Bank of Nigeria's Prudential

Guidelines in November 1990, huge sum of money are written of the

books of banks as bad and doubtful debts. The trend of the lending

risk actor which is the percentage of provision for bad and doubtful

debts to total loan and advances is increasing.

Bank have, in place, standard practice for appraising and ap-

proving individual credit applications. In spite of this, bad and doubt-

ful debts still claim bulk charge on banks performance; and in some

cases threatens the collapse of the affected banks, classified distressed

by (Nigeria deposit Insurance Corporation NDIC). 1

0

This study premised upon the fact that most loan defaulters

do so due to the economic circumstances affecting the industry in

which they operate; which we believe that a credit portfolio can

diversify holdings of loans as to achieve simultaneously low risk and

high returns.

1 .2 Statement of the Problem

That banks ensure the individual appraisal and ratings of credit

applications through their credit analysis departments is not in doubt.

However, as a result of non-effective diversification of portfolio

effect, negative pressure on a sector of the economy adversely af-

fect the value of banks overall credit portfolio as they are basically

positively correlated.

For instance, governments all over the world are rated as

highly credit-worthy and are preferred for bank lending. The reverse

appears to be the case in Nigeria, as state governments appear un-

able to meet their debt obligations. This plunged most banks neck-

deep into troubled water because of the prudential guidelines. Most

State banks concentrate their loan portfolio on government and gov-

ernment related institutions; which its default leads to the banks Ii-

abilities exceeding their assets basically resulting from provisions for

bad and doubtful debts.

The volume and value of bank loan which have become clas-

sified have continued to increase even at a faster rate than the in-

creases in bank lending. This has adverse effect on banks since it

affects their cash flow. It is beIieved that most debts go bad because

of the inadequacy of loan management and recovery procedure of

banks.

Central Bank's sectoral allocation affects bank lending and

increases risk in bank lending. For instance, agriculture is considered

a high risk and low yield venture for bank financing. As a result of

this, low yield high risk situation banks have used a11 sorts of strate-

gies known to them to circumvent lending to farmers. Although the

banks agree to the existence of risk in agricultural lending, none of

them knows the rate of defauh or any indicator of risk. There is,

therefore, no knowledge of which institutions record more risk and

why they do so.

This lack of knowledge and obvious ignorance to a ve y im-

pol-tant fact to the business of banks has led to questions such as:

What could be done to eliminate or at least reduce the magni-

tude of the risk and uncertainly in bank lending portfolio and hence

assist in creating an easy and undistributed investment cycle in bank

lending?

Why does lending risk exist? What are the causes of the re-

ported high risk in bank Iending?

1.3 Objectives of the Study

The study is meant to -

1. Determine the existing tools of risk analysis and control in

banks lc~nding portfolio management; 3

2. Determine the effectiveness of lending diversification through

portfolio theory in checking the incidence of bad doubtful

debts in bank management;

3. Construct a model for risk analysis and control in credit

portfolio;

4. Determine the effect of Central Bank of Nigeria's sectoral

credit allocation guidelines on banks lendings;

5 . Make recommendations based on the findings.

1.4 Formulation of Hvpothesis

Hypothesis 1

Null -Hypothesis IH ): Effective loan diversification through risk 0 -

and correlation analysis of banks credit investments is not in prac-

tice.

Alternative Hvpothesis (Hi): Effective loan diversification credit

investment is in practice.

Hypothesis 2

Null Hypothesis: The distribution of respondents between differ-

ent optiqns as to the effects of diversification of banks credit

portfolio is not significantly different between the three classes of

banks.

Alternative Hwothesis: The distribution of respbndents between

different options as to the effects of diversification of banks credit

portfolio is significantly different between the three classes of banks.

Null Hvpothesis: CBN's sectoral loan allocation guidelines do not 4

ink7.it effective diversification in banks lending.

Ahernative Hypothesis: Central Bank of Nigeria's (CBN) sectoral

loans allocation guidelines do inhibit effective diversification in banks

lending.

1.5 Sisnificance of the Study

The relevance of this study can readily be seen in its contribu-

' d m towards enhancing fending practices; thereby improving the quality

of banks loan portfolio through achieving effective diversification.

It is not an exaggeration to say that the difference between

success and failure in the banking industry is in the effetfive manage-

ment of the banks loans and advances. Efficient loan management is

vital to the protection of assets and the achievement of adequate

returns to investments. Though much work abound in the literature

on the techniques of lending, the methods of securing such lending

and the pitfalls that await the unwary banker; by cornparism, there

appears to be ve y little in print on the subject of loan management

and recovery. A study of this will therefore be an addition to the

existing volumes of banking literature.

For loan management to be effective, it must know when a

loan begins to look doubtful and take appropriate action. This will

enable the bank to at best obtain full repayment including accrued

interest or at worst to mitigate the eventual capital loss. In the face of

increased competition among banks, future profits are likely to be

harder to come by.

The study will show the effect of Central Bank's sectoral loan

allocation guidelines on bank lending, and suggest possible solution,

if necessary. The economy as a whole will benefit from the study

because if the level of bad debts is reduced, banks will be left with

more profits t o enable them make the expected contribution to the

development of the economy. The study will also be a guide to fu-

ture researchers who may like to research more on the topic.

1.6 Scope and Limitation of the Study

The study was restricted to risk analysis and control in bank's

credit portfolio management. The researcher assumed the existence

of an effective credit analysis and department in the banks in study.

The study is therefore concern with risk comparism instead of riskness

of individual loan investments.

The researcher intends to cover all the banks in Nigeria, but

due to the three main constraints of research namely: Time, money

and energy, she can only study some selected commercial. The study does not include mortgage, people and community banks.

CHAPTER TWO

LITERATURE REVIEW

It is important to consider the work of other people who have

written on related topics to achieve the theoretical framework of this

study. It is therefore in realization of this objective that the researcher

critically reviewed the works of different people under these sub-

headings, namely:

1. The concept of risk, uncertainty and bank.

2. Distinction between risk and uncertainty.

3. Classification of Risk.

4. Measurement and management of risk through portfolio

the0 y.

5. Portfolio analysis and selection.

6. Capital asset pricing model.

2.1 The Concept of Risk, Uncertaintv and Bank

The word "Risk" means different things to different people.

h economics, risk is defined as the chance that a particular deci-

sion oraction can give rise to as variety of outcomes for which one

can calculate the mathematical probability. In investment, it is the

probability of loosing money or making profit on one's invest-

ments. In insurance, it is a general term for any possibility of loss. It

is also the person or property covered by an insurance policy.

Okafor argued that risk is used as a surrogate for the likeli-

hood of loss or the potential size of such a loss. He also explained

that risk implies exposure to danger for economic adversity. He

used risk to denote exposure to loss arising from variations between

the expected, and the actual outcome of investment activities. Ac-

cording to him, condition of risk is incomplete knowledge and at

the same time, incomplete ignorance.'

Also, yandey defined risk as the variability that is likely to

occur in the future returns from a project. "The greater the variabil-

ity of the expected returns, the riskier the p r o j e ~ t . " ~ He gave three

different techniques to handle risk: The payback p'ei-iod, risk ad-

justed discount rate and certainty-equivalent techniques. His defini-

tion of risk is associated with projects.

Weston and Brigham also defined the riskiness of an asset in

terms of the likely variability off future returns from the assets. In

their word The concept of probability is a fundamental element in both the definition and the measurement of risk. A probability distribution shows the probability off occurrence of each possible outcome, assuming a given investment is undertaken.

Also Irukwu argued that no one is exempt from risk. He

insisted that risk in the sense of chance of loss has been the bane of

human existence from time immemorial. According to him, whether

we like it or not, and however careful we may be, we are exposed to

the risks of, for instance, fire, earthquake, storm, flood, burglary at-

tack by an armed robber, injury from the tortuous acts of others and

several other hazards. The above situations gave birth to many defi-

nitions of risk depending on the context it has been used.

In the same way, Pappas and Brigham argued that risk is "a

hazard or peril; exposure to harm; and risk to mean the possibility

that some unfavourable events wil[ occur.Wardy opined that risk is

uncertainty in regard to cost, loss or damage. According to him where

destruction or loss of capital is certain in connection with a business

process, it not a risk, it can be charged up in advance as a cost.

The above definitions though in line with most literature defi-

nitions, are narrow in the sense that they are simply looking at risk

as a negative variance. In view of the above, a further consideration,

of other definitions is necessary.

Political risk was defined by Ting "as the the non-market un-

certainks or variations surrounding the desired business outcome

(revenues, cost, profit, market share, continuation off the business

and so on), for an international project or venture that may stem

from instabilities in the host country's political policy and/or foreign 7

exchange system", Higgins simply defined risk "as the dispersion in

possible o u t ~ o m e " . ~ Also sharpe defined risk as the extent to which

the actual outcome is likely to diverge from the expected value.9

2.2 Distinction between Risk and Uncertainty 1

The definitions made in 2.1 above lack clarity as to distinction

beheen risk and uncertainty. In attempt to distinguish the two, Ruth

argued that "uncertainty is the compliment of knowledge" and went

further to define it as "the gap between what is known and what

needs to be known to make correct decision.'O Also in his attempt t o

distinguish between risk and uncertainty Willett contended that: Risk is the object corrective of the subjective uncertainty. It is the uncertainty considered as embodied in

0 the course of events in the external would of which the subjective uncertainty is a more or less faithfd interpretation."

In his own distinction Preffer contended that risk is a combi- I

nation of hazards and is measured by probability while uncertainty is

veasured by a degree of belief. Risk is a state of the world, uncer-

tainty is a state of the mind.

Willett's and Prefers definitions were analysed by Houston.

According to him, Willett's definition was seen to comprise of two

major aspects: the first is the objective - subjective distinction risk is

seen as an objective phenomenon which can be measured empiri-

cally in the real world and is independent of the individual observer.

The second aspect denfined risk as "a concept of variation and is

not identified with the degree of probability. While in Preffer's defi-

nitions, Houston notes his emphasis on the objective - subjective

dichotomy of risk and uncertainty, is that in the former the distribu-

tion of the outcome in a group of instances is known (either through

calculations a prior or from statistics of past experiences) while in

the case cf uncertain@, this is not true, the reason being in general

that it is impossible to form a group of instances because the situa-

tion dealt with, is in a high degree unique.15

In an attempt to distinguish risk and uncertainty, 0kafor ex-

plained that condition of risk implies incomplete knowledge as well

as incompleteignorance. The condition of uncertainty, on the other

hand, implies a near complete ignorance of the future outcome of

present clzcision .I6

Although, Weston and Brighan used the two words synony-

mously, they made distinction between risk and uncertainty. In their

words: Risk is associated with those situations in which a probability distribution of the returns on a given project can be estimated; uncertainty is associated with those situations in which insufficient evidence is available even to estimate a probability

di~tribution.'~

They argued that probability distributions of expected returns

can themselves by estimated with greater or lesser precision. They

explained that when statistical procedures can be used to estimate

probability distribution, then risk is said to be measured by objective

probability distributions. However, if statistical data cannot be used to

estimate probability distribution, then the estimate will be determined

subjectivdy, hence, subjective probability distributions.

Dzspite the above definitions, for purposes of our study, we

should regard an investment risky if its actual outcome has the prob-

11

;.':i;ity of varying, positively or negatively, from the expected out-

come and that there exist techniques to measure this dispersion,

.- - : ~ e l y the average (or mean) absolute deviation and the standard

dct iation.

2.3 Classification of Risk

There exist distinctions in risk types. Monray distinguished

between two types of risk According to him, risk could be pure or

speculative in nature Barauch et al. explained that pure risk holds

our the prospect of a loss or no loss (insurable risk) whik a specula-

tive risk holds out the prospect of a gain as well as 1 0 ~ s . ~ ~

However, Kulp, adopts a different dimension to the categori-

zation of risks based on the origin or cause of the risk situation.

Risk, according to him, could be "fundamental" or particular in na-

ture. His explanations of the two terms are that:

Fundamental risks are essentially group risks, the conditions which cause them have no relation to any particular individual . . . Particular risks affect each individual separately .. . They are usually personal in their application, because they are so largely personal in their nature . .. , the individual has a certain degree of control over their causes .20

In line with portfolio risk analysis, Higgins classified risk as "non- diversifiable" and "diversifiable."

He explained that the non-diverslfiable

?-is:-; is the risk remaining after the rest has been diversified away in

the portfolio.

The part that is diversified away is Imownas the diversifiable risk.21

In addition to the above, Fabozzi, et a. distinguished between

a security's unsystematic risk and its systematic risk. They described

unsystematic risks as the risks whjch can be washed away by mixing

the security with other securities in a diversified portfolio; whereas

sy;lcmatic risk are those which cannot be eliminated by diversifica-

tion. He further explained that the unsystematic risk depends on fac-

tors that are unique or specific to the company that issued the secu-

rity, such as labor difficulties, unexpectedly high or low sales, mana-

gerial issues, and so on. Thus, the unsystematic component is not

linked tc: the overall market or economic system.

Osubor grouped risk into four classes: Market risk, purchasing

power risk, money rate risk and credit risk. According to him, market

ris!.. :s risk that a failure or impairment of market would cause the

market instruments to be unsaleable, at less that their fair prices;

purchasing power risk that ?ype of risk that a prolonged inflation

would cause repayment of money in future of reduced buying power;

money rate risk is the risk that a future rise in interest rate would

Iocver the value of debt; and finally credit risk which is the risk of

deiault in repayment. It is the risk associated with the fear that those

who owe you might default in their regular payments.23

Okafor also grouped risk into six classes: Business risk, mar-

ket risk, purchasing power risk political risk, risk ~ f q unplanned

obsolence and management and union risks. He explained that busi-

13

ness risk does arise from changes in genera! economic conditions

Lhat lead to unexpected declines in the earning power of most in-

wstments. It therefore follows that period of unanticipated deprcs-

sion are characterized by a high rate of business; market risk origi-

:-ates from adverse market (Mob) reactionto unanticipated events.

Depressed returns could arise from fundamental changes in earn-

ings power or simply from outright pessimism on the part of capital

market participants. There are many things that can cause this type

of risk for instance, an unpopular election result could cause de-

przssed stock market prices. Similarly, the death of a president or a

surprise sign of war could cause tremendous pessimism in the mar-

ket; purchasing power risk, according to him is the risk that arises

from afall in the reaI value of investment outcomes due to an unan-

ticipated increase in the rate of inflation. Investors in fixed income

financial assets are exposed to a great deal of inflation or purchasing n

power risk; political risk come from non-predictability of political

forces, which affect investment outcomes. Many political measures

such as nationalization, indigenisation programmes,, could cause an

unanticipated decline in the return on investment; risk of unplanned

obsolence occurs when unanticipated economic and/or technologi-

cal factors cause a premature abandonment of a product Iine or of a

entire project. For example, when a radical change in consumer

taste eliminates the effective demand for a product, thus rendering

it obsolete,^ or when a drastic change in technology causes the un-

planned abandonment of a manufacturing process. This risk often

arixs from less revolutiona y forces, e.g when a manufacturing plant

is forced to close down due to tempora y or permanent disruption of

raw materials supplies, and finally management and union risks, this

according to him arises from unanticipated variations in profit perfor-

mance caused by management. Similarly, unexpected changes in per-

formance could arise from union risks. Union risks are disruptions t o

corporate performance caused by unfavourable union actions such

as strikes, sit-ins and outright sabotage. He also explained that man-

ageinent and union risk is due to errors of judgement, inefficiency or

fraud on the.part of management and union leaders.24

Also Johmson et aI. mentioned specific sources of risk that

causedvariability in banks return; These include liquidity risk, interest

rate risk, credit risk and capital risk. He explained that some ele-

ments of these source of risk are controllabIe and cari 'be limited

through managerial action, whereas other elements remain uncon-

trdlable. According to them, Banks must meet demand for liquidity

when customers demand loanable funds. In order t o meet potential

demands for liquidity, banks must maintain liquidity in assets or must

rely on creating liquidity by borrowing funds. In their words.

Liquidity risk refers to the variability in earnings that results from satisfying a demand for liquidity.

They also explained that interest rate risk is the risk of mak-

ing a loan that is financed at a known rate but that during the loan life

may be referred to be refinanced at a higher interest rate. The net

yield to the bank is reduced whenever loan rate is fixed and funding

rate rises. A bank is therefore, subject to certain degree of earnings

variabiiity as interest rate fluctuates. Management can control the

degree of interest rate risk that a bank is subject to, to some extent.

Credit risk refers to the variability in earning that could result from loan losses and security defaults.

,They further explained that banks can control credit risk

through conservative lending practices, although they may pass up

potentially profitable loans by restrictive credit policies. Credit risk

is difficult to assess. without thoroughly examining the loan portfo-

1;:). ~ci~)iial risk, according to him, reflects the degree of leverage

cxpioyed by the bank. Capital, the owner's equity serves to protect

cxditors (depositors) against losses a bank may incur. The amount

of capital required to protect creditors is related to the quality, or

riskness of a bank's assets.25

Bank management is simply seen by Nwankwo as being

coterranous with risk management. In his opinion, the main source

of ~i.vesilble funds is bank deposits while loans and investments are

L?.C main outlets. Similarly, the main source of income and profit-

?bility of banking is the spread or difference between the rate at

w.-kh funds are borrowed and the rate they are invested, or loan

out, and also in maturity transformation, that is, borrowing short

and \en&ng long .2''

Rose stated:

While the 1950s focused on techniques for the management of bank assets, and the 1960s and 1970s emphasized liability management, ban king in 1980's is concerned with risk-how to measure risk and how to control it for the betterment of industry and it's

Also Guth in his address to the international Banking Summer

ScImol in Cambridge as quoted by Nwankwo, commented pointedly

that:

The subject of risk today occupies a

central position in the business policy csnsideration bank management, and it is not surprising that every institution is assessed and appreciated by customers, investors and the general public to a large extent by ihe way it presents itself with respect to volume and allocation of ' '

risks as well as provision against them.28

From the foregoing, it is not surprising that the present over-

riding consideration of bank management is the necessity to mini-

mize risks and maximize returns consistent .with prudential constraints

and regulations.

The crux of our study is the "credit r isk defined and explained

by >-\':.' clnkwo as The risk that the interest or the principal or both on loan nd securities will not be paid as agreed. When some loans become uncollectible and are written off, the bank loses both earning assets and some portion of its expected revenues. If loan losses continue to mount and persist for several

years, the bank's cushion for capital eventually becomes eroded and unless additional funds are injected, the bank may be forced to liquidation.

As can be deduced from Nwankwo's definition and explana-

tion, credit risk can be very disastrous to the banking industry. He

also mentioned some factors that contributes to credit risk. These

factors include: The range of interest rate in the portfolio and the

proportion of the portfolio at the various ranges. The higher the

dispersion, the greater the credit risk; competence of the loan ad-

ministrators, this include the managerial and the technical compe-

tence of the administrators; the proportion of the portfolio effec-

tivcly collaterised - the higher the effective collaterisation the lower

the credit risk. Last but not least is the degree of the correlationship

of the risks in the portfolio - the higher (positive) correlation the

greater the credit risk.

In general, management and control of risks in the banking

industvy take the path or risk avoidance and minimization, risk trans-

fer < i?d risk retention. 6

Risk minimization and avoidance is a technique whereby in

Q:.~' 31. to control risk, banks specifically restrain from lending got cer-

tain sectors or projects perceived to be very risky. This is.particularly

emphasized in their strong preference for self-liquidating short-term

lending strategy; risk transfer entails sharing risk with external i n -

stitutions, e. insurance company. This becomes necessary because

all risks of bank cannot be completely avoided. Banks assume those

risks, in their operations, that are not and cannot be transferred and

those that are not and cannot be self insurance. The insurance fund is

the networth and incomes earned on current operation serve as the

insurance premium required to keep the networth at an adequate

The importance of diversification was explained by Nwankwo.

In his words.

It is for instance, the heavy concentration in property lending that partly contributed to the faiIure of some banks in the U.K. during the fring bank crisis. In the U.S the collapse of the Penn square bank and 'many Texas and Oklahoma banks was attributed largely to the banks heavy concentration of investments in energy sector; v~hile in West Germany, over exposure to a single borrower, IBH Holdings AG, and its subsidiary companies was responsible for SMH's difficulties and near collapse. When SMH got into trouble its exposure to IBH Holdings was equivalent to 800% of the bank's capital and 40% of its assets. While a certain degree of concen tration is inevitable and may be necessary in certain circumstance, and while a fool proof diversification policy may be difficult to implement, the p;ecept nevertheless still remain that the more diversified, the less the risk.2'

2.4 Measurement and Management of Risk Throuqh Portfolio Theory

Diversification, according to Tewles and Bradley is to spread

out o m ' s investment as a protection against risk. This, they further

explained, is based on the age-old axion "Don't put a11 your eggs in

one basket." They argued that diversification gives protection against:

CycIical movement of business; long-term or secular changes in in-

dusty; losses in the position of individual companies; and that within

reasonable limits proper diversification is a sound way of reducing

or ei~~ninating all bui market (systematic) risk""

The American Investment Company act of 1940 as quoted

by Sharpe defined a diversified investment company as:

One that invests at least 75% of

its funds in a diversified manner.?'

Sharpe also argued that "diversification typically reduces non-

market risk. .. As more and more securities are included in a portfo-

lio, total risk should fall, reaching the lower limit represented by

market risk: ." He went further to argue that diversification provides

substantial risk reduction if the components of a portfolio are

uncorrelated. In fact, if enough are included, the overall risk of the

poltiolio will be almost (but not quite) zero.33

The above definitions and explanations, therefore, point to

the fact that when a risky security or portfolio is combined with a

riskless one, the risk of the combination is proportional to the amount

inveskcl in the risky components. The ebove is corroborated by

Higgins who opined that when a decision rnaker owns a portfolio of

asset, the relevant measure of risk is not an asset's risk in isolation ut

rai.1er its risk as part of the portfolio,34

Higgins opinion is based upon the principle of portfolio theory

20

as first enunciated by I-I. M. Markwortz as quoted by Frear who went further

to argce that effective diversification would require estimates off three fac-

tors, namely:

Expected future return of each candidate security.

The expected risk of each candidate security.

The extent to which each security risk correlates with

each other security.

$.nd that based on the above actors, the best portfolio for an investor

will be:

if: two portfolios have the same risk but different returns, the investor

will prefer the portfolio with the higher return.

If two portfolio have the same expected returns but difference degree of risk, the investor will prefer the portfolio with the lower risk.

If one portfolio has both a higher return and a lower risk than an o t b , the investor will prefer the first portfolio.

- h e above assumption gave rise to the "efficient portfolio" concept

descr?c.d by Sharpe. According to him, a portfolio is said to be efficient, if it

has less. risk than others with comparable expected return and more return

than others with comparable risk.35 a

According to Okafor, Measurement Problems arise from the fact that

risk represents an index of the variability of the realized from the expected

rates of retwn. He also emphasized that the degree of risk cannot be as-

sessed with absolute certainty until the final outcome of a investment is known.

He further explained that any of the statistical measure of dispersion, such

21

;s the range, the variance or the standard deviation or its square (the vari-

ance) is the best indicator of investment risk, just as the expected rate of

return is the most widely used measure of investment return. He also ex-

plained that unlike returns, the risk of an investment portfoIio is not neces-

sarily the weighted average of the risk of component securities. Inter-rela-

tionship among the risks of individual securities in the portfolio must be

considered. The interactive risk of securities in a portfolio is measured

either by the covariance or by the correlation coefficient of their returns.36

lie also gave example of how to measure co-variance of returns in a two

assets portfolio. He defined the covariance of returns as:

where: Covxy = Covariance of returns of securi

ties X and Y

X - - Series of observed returns

on security X.

Y - - Series of observed returns

on security Y.

Rx = Mean (expected value)

return on X.

R - - Y

Mean (expected value)

22

return on Y.

n = number of returns

observed.

Similarly, the correlation co-efficient of security in a two as-

set por~ol io is obtained by dividing their covariance by the product

of the standard deviation of their individual returns.

Thus:

where rxy = Co-efficient of correlation

between returns on X and Y.

Sx = risk of security x, i.e

standard deviation of its

return.

S Y

= risk of security y, i.e

standard deviation of its

return.

Weston and Brighams (1979) used the equation below for

the calculation of the riskness of a portfolio, but under the assump-

tion that the distributions are normal.

According to then, the co-variance (COV) between two securities

depends upon:

1. The correlation between the two securities; and

2. The standard deviation of each security's returns. It

23

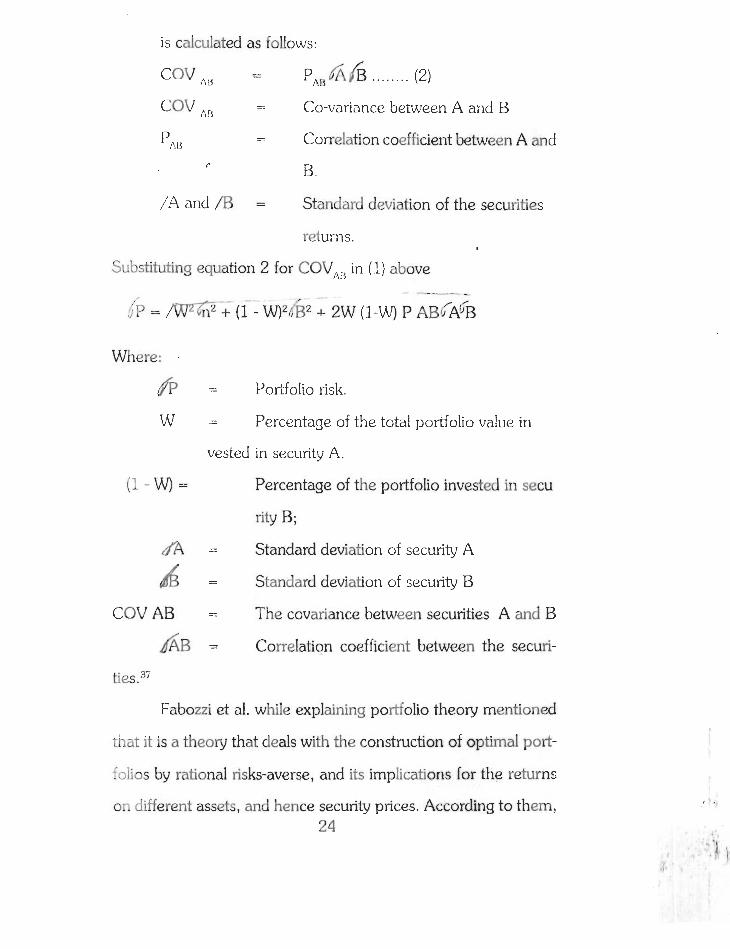

is calculated as follows:

Cov A,, = p,,GAIrB ........ (2)

Cov A:, - - Co-variance between A and B

PAL3 - - Correlation coefficient between A and

0 B.

/'A and /B = Standard deviation of the securities

returns.

Substituting equation 2 for COV,,, in (1) above

Where:

[P = PortfoIio risk.

W = Percentage of the total portfolio value in

vested in security A.

(I-W)= Percentage of the portfolio invested in secu

rity B;

/A = Standard deviation of security A

= Standard deviation of security B

COVAB = The covariance between securities A and E

~ A B = Correlation coefficient between the securi-

ties. 37

Fabozzi et al. while explaining portfolio theory mentioned

that it is a the0 y that deals with the construction of optimal port-

foiios by rational risks-averse, and its implications for the returns

on different assets, and hence security prices. According to them, 24

one way to evaluate the risk of a portfolio is by estimating the extent to

which future portfolio values are likely to deviate from expected portfolio

return. This is measured by the variance of the portfolio's return and is

called the total portfolio risk Total portfolio risk can be decomposed into

two types of risk: Systematic risk and unsystematic risk. They went further

to explain that systematic risk, also called market risk, is the risk that af-

fects all securities. The beta of any security or portfolio is the relative sys-

terrdic risk of the asset and is measured statistically (using historical return

data) by the slope of the repression between the assets and the market's

returns. The repression line estimated is called the market model Unsys-

tematic risk.is the risk that is unique to a company and it can be eliminated

by diversifying the portfolio. Thus, systematic risk and unsystematic risk

are referred to as non diversifiabIe and diversifiable risk respec t i~e ly .~~

Thus they have developed two measures of risk: One is a measure

of total risk (standard deviation), the other, a relative index of systematic or

noil-diversifiable risk (beta).

The totality of portfolio theory is simply a technique of risk

measurement through standard deviation and risk management by diversi-

fication through correlation analysis of securities returns. This study de-

veloped a model for bank's credit risk measurement and management in

line with portfolio theory.

2.5 Portfolio Analysis and SeIection

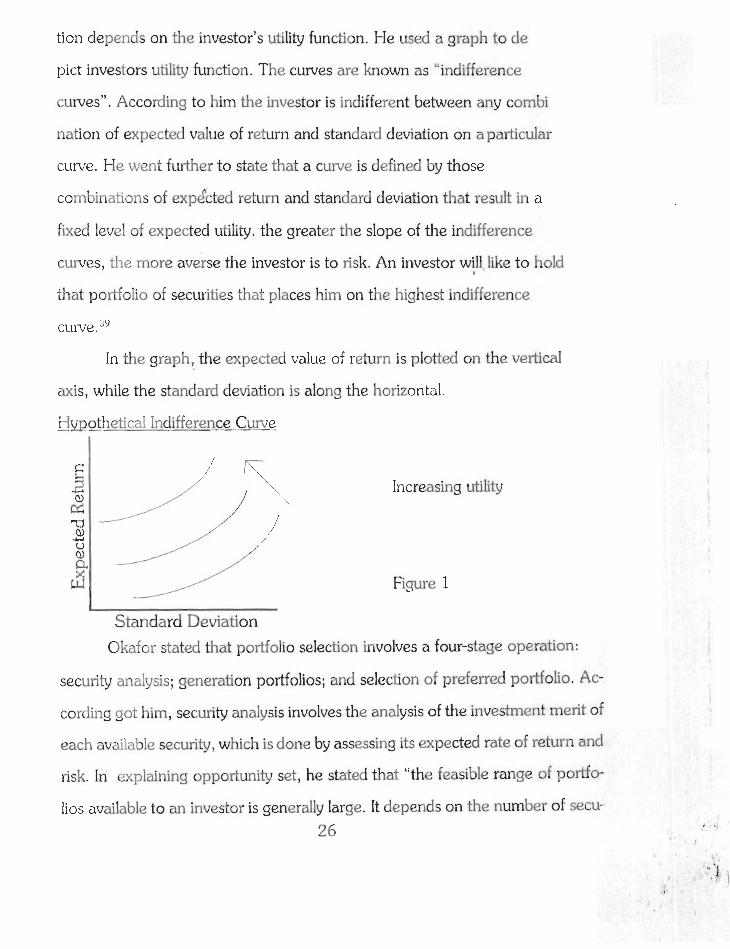

Van Horne in his book, financial management and policy, argued

that the best combination of expected value of return and standard devia

tion depends on the investor's utility function. He used a graph to de

pict investors utility function. The curves are known as "indifference

curves". According to him the investor is indifferent between any combi

nation of expected value of return and standard deviation on aparticular

curve. He went further to state that a cuwe is defined by those

combinations of expe"cted return and standard deviation that result in a

fixed level of expected utility. the greater the slope of the indifference

curves, the more averse the investor is to risk. An investor will, like to hold

that portfoIio of securities that places him on the highest indifference

curve .3c)

In the graph, the expected value of return is plotted on the vertical

axis, while the standard deviation is along the horizontal.

Hypothetical Indifference Curve

I

Increasing utility

Standard Deviation

Okafor stated that portfolio selection involves a four-stage operation:

security analysis; generation portfoiios; and selection of preferred portfolio. Ac-

cording got him, security analysis involves the analysis of the investment merit of

each avdable security, which is done by assessing its expected rate of return and

risk. In explaining opportunity set, he stated that "the feasible range of porifo-

lios available t o an investor is generally large. It depends on the number of sew- 26

rities avai!abIe on the market. For a set of securities, the opportunity set would

be a maximum number of n = C,, portfolios where n is the number of single-

asset portfolio and C,, is the maximum number of portfolios t o be constructed

irom all possible combinations among them."('

He also describe how to identify an efficient portfolio. According to

him, "A pclrtfolio is efficient if it has less risk that any other with a similar

return; 0:- a higher return than any other in its risk class. When efficient port-

folios have been identified, then selection of preferred portfolio will take place.

2.6 The Capital Asset Pricing

Fabozzi et al described the capital asset pricing model as a form of

relationship between risk and return. According to him, it is based on elemen-

tary logic and simple economic principles. Asset with the same systematic risk

should have the same expected rate of return; that is, the price of assets in the

capital markets should adjust until equivalent risk asset have identical expected

returns.";

Van home explained that there is implied an equilibrium relationship

betweer: risk and expected return for each security. He further explained that

a security will be expected to provide a return commensurate with its unavoid-

able risk. This is simple the risk that cannot be avoided by diversification. The

greater the unavoidable risk of a security, the greater the return that investors

will expect from the security. The relationship between expected return and

unavoidal' isk, and the valuation of securities that follows, is the essence of

capita1 z ;w pricing mode. This model was developed by Sharpe and Lintner

in the 1960's and it has had important implication for finance ever since.42

For proper risk analysis, projects must be properly analysed and evalu-

ated. Betterley wrote that the objective of risk management is proper protec-

tion of company assets and profitability against loss from pure risk. This pro-

tection is accomplished by systematic analysis of risks and the employment of

various techniques aimed at reducing potential loss from these risks. He rec-

ommended the following steps to project analysts and financiers or proper

evaluation of projects.

Make actual visits to project sites.

Interview heads of departments and operating divisions regularly to

learn their problem area. Maintain close communication to keep

abreast of changes.

Educate the people processing orders (and loan application) t o be

alert for indications of new exposures to risk.

Establish a routine or reviewing agreements with clients.

Study inspection reports submitted by project monitoring team.

Read house journals, news releases, etc. of clients.

Learn from the misfortune of others.

Be guided more by potential severity that probability in performing

risk analysis.

Risk analysis is a never encling process; so repeat t h e s ~ steps over

and over again.""

In conclusion, the totality of portfolio theory is simply a technique of

risk measurements. This study, developed a m d e l for banks credit risk

measurement and management in line with portfolio theory.

REFRENCES

Okafor, F. 0. Investment decisions. (Southampton: The Camelot Press, 1983), p. 28.

Pandey, I. M. Financial Management. (New DeIhi: Vikas Publishing House PVT Ltd., 1991), p. 573 .

Weston & Brighams, Managerial Finance. (New York: The Dyden Press, 1978), p. 247.

Irukwu, J. 0. Accident and motor Insurance in Africa. (Ibadan, the Gaxton Press, 1974), p. 4

Pappas, J . L. and Brigham, E. F., Managerial Economic. 3rd ed., (Illinois: The Dyden Press, 1979, p. 74.

Pardy, C. 0. Readings in risk and risk bearinq. (Chicago: University of Chicago Press, 1924), p. 1

Tings, W. Multinational risk Assessment and Manaqement. (Quorum Books, 1958), p. 22.

Higgins, R. C. Evaluatins investment osportunity. (New Jersey: Prentice-Hall Inc., 1 9 8 1 , p . 22.

Sharpe, W. F. Investments. 3rd ed. (New Jersey: Prentice-Hall, Inc., 1978), p. 579.

Ruth, P. M., Planning on uncertainty (John Wiley and Sons, Inc., 1971), p. 1.

Willet, A. H., The economic theory of risk and insurance. .(~hila$elphia: University off Pennsylvania Press, 195f), p. 6.

Pfeffer, I. Insurance and economic theow. (Illinois: Richard D. Irvin, Inc., 19561, p. 42. ,

Ho~xton, D. B. "Risk insurance and sampling". In J . D. Hammond,

Essays in the Theory of Risk and Insurance, (Illinois: Scott, foreman and Co., 1968), p. 152.

14. Ibid.

15. Kngiht, F. H. Risk, uncertaintv and profit. Bonston: Houghton Mufflin, 1921), p. 233.

17. Weston & Brigham, Op.' cit., p. 251.

18. Monbray, A. H. Insurance : Its theorv and practice in the United States. 1st ed. (New York: McGraw-Hall Book Co., Inc., 1930), pp. 4-5.

19. Balauch, F., et aI. Acceptable risk. (Cambridge University Press, 1983), p. 6.

20. Kulp, C. A. Casualtv insurance. (New York: Ronald Press, 1928), pp. 4-7.

21. Huggins, R. C., Op. cit., p. 272.

22. Fabozzi, et al. Foundation of financial markets and institutions. , .

(Englewood Cliffs: Prentice-Hall International Inc., 1994), p. 265. .: '1

23. Osubor, J. U. Business finance and bankinq in Nigeria. (Owerri: New Africa Publishing Co. Ltd., 1954), pp. 178-179.

24. Okafor, F. O., Op. cit., pp. 32-33

25. Johnson, et a]., Commercial bank management. (New York: The dryden Press, 1985), pp. 46-48

26. Nwankwo, G. 0 . Bank manaqement principles and practice. (Lagos: Malhouse Press Ltd., 1991), p. 138.

27. Rose, P. S. (1987), p. 54.

29. Ibid.

Teweles and E. S. Bradley, The stock market. (New Jersey: John Wiley and Sons, Inc., 1982), p. 345.

Higgins, R. C., Op. cit., p. 271

Sharpe, W. F. Op. cit., p. 580.

Ibid .

Higgins, Op. cit., p. 271.

Frear, J., The manasement of business finance. London: Pitman publishing Ltd., 1980), p. 233.

Okafor, F. O., Op. cit., p. 189.

Weston & Brigham Op. cit., pp. 257-258.

Fabozzi, et aI. Op. cit., p. 232.

Van Horne, J. C., Financial Manaqement and ~ol icy. (Englewood Cliffs: Prentice-HalI, Inc., 1989), p. 58.

Okafor, F. O., Op. cit., p. 192.

Fabozzi, et aI. Op. cit., p. 273.

Van Horne, J . C., Op. cit., p. 61.

Betterley, G. M., "Risk management." In Mayrard, H, B. (ed.) Handbook of business Administration, (New York: McGraw-Hill Book Co., 1970), p. 78.

CHAPTER THREE

RESEARCH METHODOLOGY

This chapter is concerned with methods with which data were col-

lected, their sources, determjnation of sample size, method of analysis of

data and test of hypothesis. Included in the chapter, is a model suggested

for :isk measurement and analysis.

3.1 Sources of Data

Two main sources of data were used to calIect information by the

researcher. The sources were prima y data and seconda y data.

In gathering the primary data, the researcher used sample survey of

selected commercial, merchant and development banks in Nigeria. The

study excluded mortgage banks which in the banking industy are relatively

new and established specifically to cater for a segment of the economy -

estate development. Also the study excludes, the community banks which

like the Mortgage banks are relatively new to allow for operational assess-

ment.

The s a m ~ l e survey of the banks was considered necessary because it

is t h r o ~ g h it that data required to test the stated hypotheses are to be gener-

ated.

In addition to the primary data collected, secondaQ data are ob-

tained from research literature and conceptual literature. From research

Iiterature, past research related projects and research work are consulted,

while in the conceptual literature, data were obtained from textbooks and

journals, etc. 32

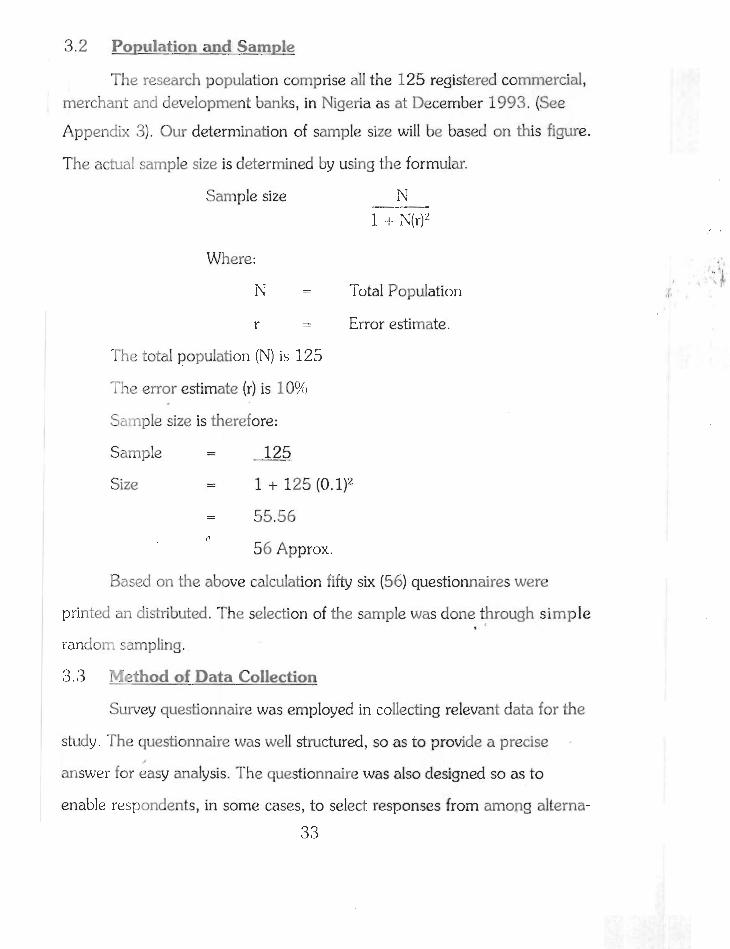

3.2 Population and Sample

The research population comprise all the 125 registered commercial, merchant and development banks, in Nigeria as at December 1993. (See

Appendix 3). Our determination of sample size will be based on this figure.

The actual sample size is determined by using the formular.

Sample size N 1 + N(r)"

Where:

N - - Total Population

r - - Error estimate.

The total population (N) is 125

The error estimate (r) is 10%)

Sz-nple size is therefore:

Sample - - 125

Size - - 1 + 125 (0.1)2

f l

56 Approx,

Based on the above calculation fifty six (56) questionnaires were

printed an distributed. The selection of the sample was done through s imple I

randolr. sampling.

3.3 Vethod of Data Collection

Survey questionnaire was employed in collecting relevant data for the

study. The questionnaire was well structured, so as t o provide a precise

answer for easy analysis. The questionnaire was also designed so as to

enable respondents, in some cases, to select responses from among alterna-

33

tive answers supplied, and in others, to supply the answers themselves when

the questions involved are unstructured. The survey questionnaire was per-

sonally administered to the respondents ostensibly to minimize the low re-

sponse and in most cases, non-response syndrome characteristics of most

research survey in Nigeria. Despite this, the researcher was not able to collect

the fifty-six (56) questionnaire administered, only forty-two (42) were collected,

which represents about 75% of the sample size Data analysis will be based on

the collected questionnaires.

3.4 :Jethod used for Data Analysis

The raw data collected from the selected commercial, merchant and

development banks are translated into percentages so as to enable the

researcher draw a reasonable conclusion based on the information collected. 0

Tables were used to analyse the responses derived from the question-

naire. Analysis of data also include test of hypothesis, which is to determine:

1. Whether effective loan diversification through risk and correlation

analysis of banks credit investments is not in practice.

2 . Whether the distribution of respondents between different options

as to the effects of diversification of banks credit portfolio is

not significantly different between the three classes of banks.

3. Whether Central Bank of Nigeria's (CRN) sectoral loans allocation

guidelines do not inhibit effective diversification of banks

lending.

In order to reach conclusion on those issues, answers supplied by

respondents to the relevant survey questionnaire were quantified and sub-

jeded to appropriate statistical test namely, product-moment co-efficient of

correlation and variance analysis test using ANOVA table. Different statistical

charts will also be used for clearer presentation.

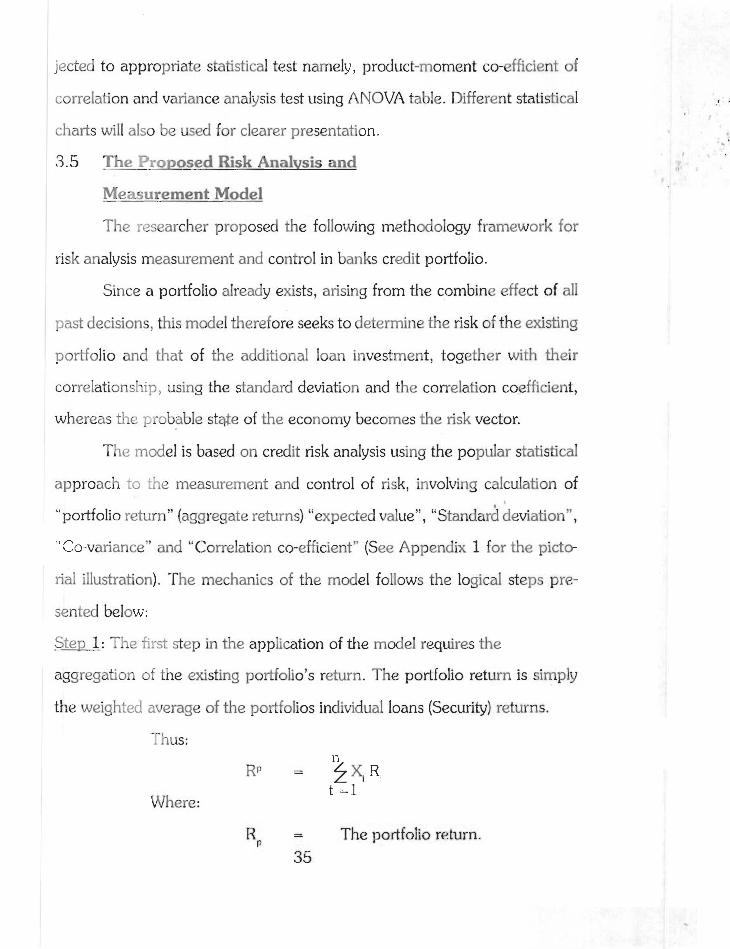

3.5 The "roposed Risk Analvsis and

Measurement Model

The researcher proposed the following methodology framework for

risk analysis measurement and control in banks credit portfolio.

Since a portfolio already exists, arising from the combine effect of all

past decisions, this model therefore seeks to determine the risk of the existing

portfolio and that of the additional loan investment, together with their

correlationship, using the standard deviation and the correlation coefficient,

whereas the isrobable st@e of the economy becomes the risk vector.

The model is based on credit risk analysis using the popular statistical

approach to 'he measurement and control of risk, involving calculation of

"portfolio return" (aggregate returns) "expected value", ''standard deviation",

"Co-variance" and "Correlation co-efficient" (See Appendix I for the picto-

rial iIlustrakion). The mechanics of the m d e l follows the logical steps pre-

sented below:

Sten 1: The first step in the application of the model requires the

aggregation of the existing portfolio's return. The portfolio return is simply

the weighted average of the portfolios individual loans (Security) returns.

-r A hus:

R C

- The portfolio return. 35

Xi = Weight of security i

R, = Return of security i

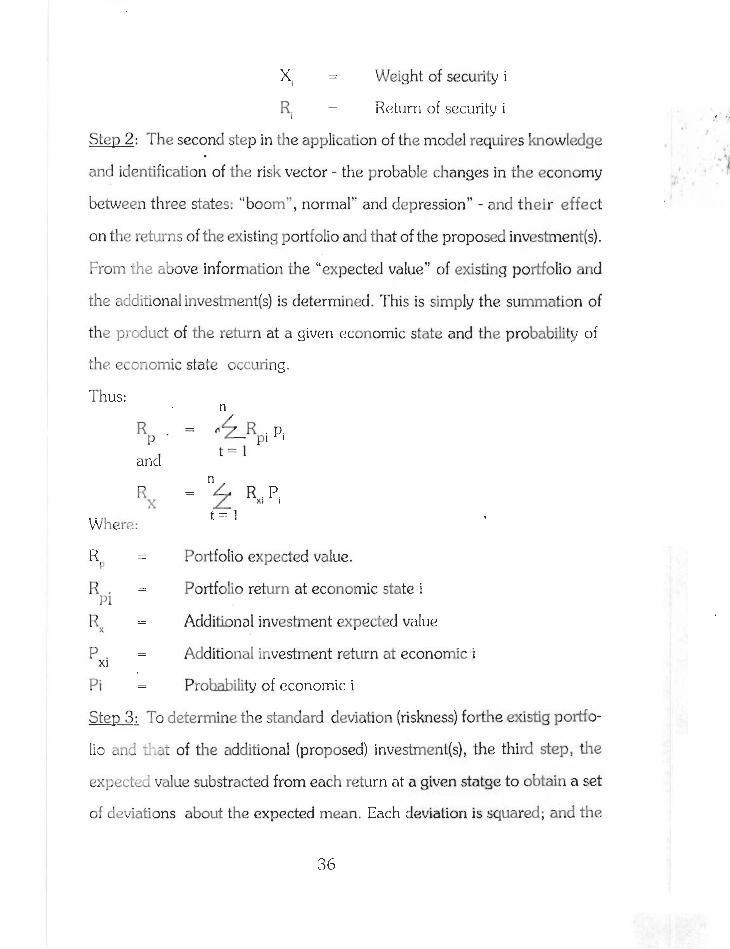

Step 2: The second step in the application of the model requires knowledge

and identification of the risk vector - the probable changes in the economy

between three states: "boom", normal" and depression" - and their effect

on the retuns of the existing portfolio and that of the proposed investrnent(s).

From the above information the "expected value" of existing portfolio and

the additional investment(s) is determined. This is simply the summation of

the p r~duc t of the return at a given economic state and the probability of

the eco:-iomic state occuring.

Thus: n

R P .

= "R p i P '

t = l and

R s = "4 Rxi Pi

Where: t = 1

R P

= Portfolio expected value.

R - .- Portfolio return at economic state i pi

R .- - X

Additional investment expected value

P - - xi Additional investment return at economic i

Pi = Probability of economic i

Step 3: To determine the standard deviation (riskness) forthe existig portfo-

lio and ?;at of the additional (proposed) investment(s), the third step, the

expectec; value substracted from each return at a given statge to obtain a set

of deviations about the expected mean. Each deviation is squared; and the

squared deviation is multiplied by the probability of the occurence of the given . economic state; the products are then summed to obtain the variance of the

probability distribution, the square root of which give the standard deviation:

Standard Deviation = P /'% ( Rp, - fip = j2 Pi t= 1

and

Standard Deviation

of additional investment x= /-

t = l

Step 4: Having worked independently with the two investments, the first

attempt at risk comparison is step 4; where the covariance of the existing

portfolio's return with that of the additional investment is analysed by the

summation of the product of the set of deviations of the two investments and

their probabilities at the given economic states.

Thus:

Step 5: Finally in order t o determine the degree of association of the risk

of the exist!:.: portfolio with the additional investments, their correlation co-

efficient 51; ;Jd be determined by the quotient of the co-variance of the port-

folio and additional investment to the product of the portfolio standard devia-

tion and that of the additional investment.

Thus:

Correlation co-efficient - - r = Covariance PA

Interpretation of Correlation Co-efficient (r)

The value for correlation coefficient ranges from + I (perfectlyposi-

tive correIation) to - 1 (perfectly negative correlation). Diversification in lend-

ing therefore, will be effective; if additional loan investment are in loans which

are nqatively correlated with the existing loan portfolio,

CHAPTER FOUR

PRESENTATION AND ANALYSIS OF DATA

The data collected from the survey questionnaire are presented and

analysed in this chapter. Raw scores are converted into percentages for

easy analysis. The three hypotheses made in Chapter one are tested in

this chapter. Product-moment coefficient of correlation and variance analysis

are the methods used to test the hypotheses. Diiferent statistical charts are also

used for ck-mr presentation.

Du,:~g the research, a total of fifty-six questionnaires were distributed.

The figure was determined by sample formular.

N

1 + N (r2)

When N is the total population

r is the error estimate

Out of the fifty-six (56) questionnaire administered, forty-two (42)

were collected. This figure is regarded as data producing sample. Theanaly-

sis will be based on the forty-two questionnaire collected.

4.1 Fata Analysis

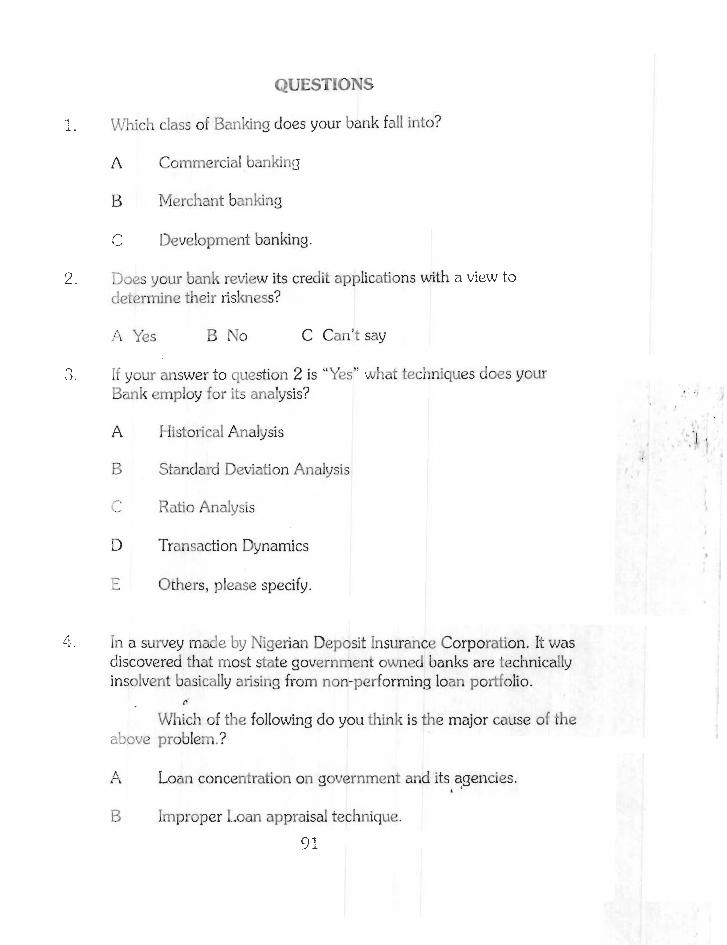

Question 1: Which class of Banking does your bank fall into? The study

attempted to classify the respondent banks according to their business areas. They were asked to indicate which of the foIlowings: Commercial, merchant and development - class of banlung operations their banks are engaged. Since the classification was distinct the respondent answered as shown in Table 1.

Table 1

Classification of Respondents Bank by their

P,rer.s of Banking Operation

Option No. of Respondents Percentage

Commercial 18 43

Merchant 21 50

Development 3 7

I Total 42 1 0 0 1 The above table shows that 18 respondents representing 43% specifi-

caily chose commercial banking as their operational area; 21 respondents

being 50% indicated merchant banking while 3 (7%) chose development bank-

ing. Majority of the respondents are merchant bankers. The result shows

that the research covers different classes of banks. This will make the result

from the analysis of data more acceptable, though there are other

classes of banking that are not mentioned. ' ' 1 , I

Q~iestion 2: Does your Bank review its credit application with a view to

determine their riskness?

Table 2

Opinion on Risk AnaIvsis of Credit A~pIications

Optim No. of Respondents Percentages

1 Total 42 100 1

In line with the view expressed by the researcher in Chapter one, all

the respondents agreed to reviewing credit applications by their banks with a

view to determining their riskness prior to its approval. Forty-two (42) respon-

dents representing 100% agreed that they review their credit application be-

fore approval.

Question 3: If your answer to question 2 is yes? what techniques do your

bank employ for its analysis?

Table 3

Techniques for ~rGdi t Application's Risk Analvsis

I

Options

Historical Analysis

Standard deviation

Ratio analysis

Transaction dynamic

41

No. of Respondent

33

-

35

26

Percentage

79

0

83

62

4

Although all the respondents agreed (in the last question) to review-

i r , ~ credit applications by their bank with a view to determining their riskness,

there exists divergent views as to the method adopted for risk anaIysis. Table

3 shows that 33 of the respondents which represents 79% adopt historical

analysis, 35 (83%) adopt ratio analysis,; 26 respondent being 6296, chose

future transactions, commencing from the time of loan approval to loan re-

payment with a view to identifying risky areas of the transactions as to make

adeqrmte provision for their control. None of the respondents chose stan- fl

d a d deviation technique of risk analysis. This is an indication that this tech-

nique of risk analysis and quantification is not in practice, despite acclaimed

usekhess in theory. With the above result we can generalize that no bank

use standard deviation as a technique for calculating theriskness of a portfo-

lio 01- investment.

Question 4:

In a survey by Nigeria Deposit Insurance Corporation (NDIC), it was

discovered that most state governments owned banks are technically

insoIvent, basically arising from non-performing loan portfolio. Which

af the following do you think is the major cause of the above problem?

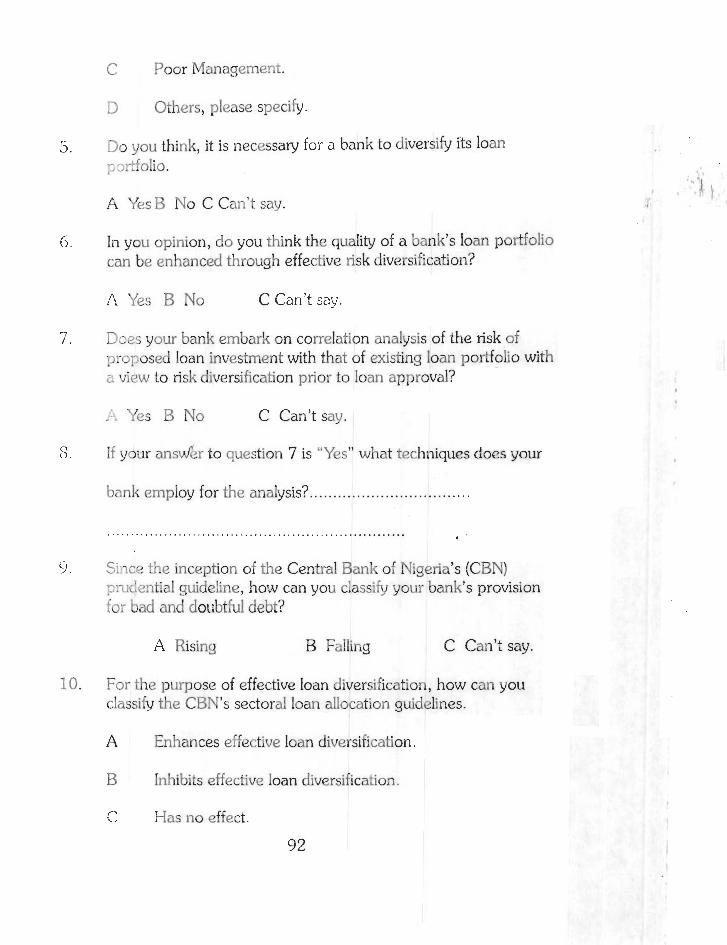

Table 4

Causes of State Government Banks Insolvency

1 Options No. of Respondents Percentaqe

Loan concentration on government and its ar,r-cies fl 10

Improper loan appraisal techniques

Poo:- Management

1 Others 2 5 I I Total 42 100

In answering the question above, as Table 4 shows, 1 Oresponden(249b)

are of the opinion that the cause of insolvency of stategovernment owned

banks is Icm concentration on government and its agencies, 22 respondents

(52%) chose improper loan appraisal technique as the cause of banks insol-

vency. Eqht (8) respondents (19%) suggested poor management and two re-

spondent (5% give other reascns, these reasons indude poor collatarisation of

loans. This table reveals that the bane of State Government owned banks is

not necessarily its loan concentration in government sector, but basically that

of improper loan appraisal techniques.

This table can also be used to answer the questions stated in Chapter 1

under Statement of Problem. The questions go like this:

'kvhat could be done to eliminate or at least reduce the magnitude of

the risk and uncertainty in bank lending portfolio and hence assist increating

43

an easy and undistributed investment cycle in bank lending.

Why does lending risk exist? What are the causes of the reported high risk in bank lending?

n' Question 5:

Do you think it is necessary for a bank to diversity its loan portfolio?

Table 5 ,

Opinion on the Necessity for Diversification of Loan Portfolio

Option No. of Respondents Percentage

Can't Say - -

I Total 42 100 I Pi1 the 42 (100%) respondents agreed that it is necessary for a bank

to diversify its loan portfolio (See Table 5).

Question 6:

In your opinion, do you think the quality of a bank's loan portfolio can be enhanced through effective risk diversification.

Table 6

Respondents view on the Enhancement of Banks Loan Portfolio throush Effective Risk Diversification

Options No, of Respondents Percentage

i Yes n

34 81 I I No 6 14

1 Can't Say 2 5

1 Total 42 1 0 0

It was the opinion of 34 (18%) respondents that effective risk

diversification can enhance the quality of bank's ioan Portfolio, 6 respondents

(14%)) objected the view that effective risk diversification enhances the quaZity

of bank's ioan portfolio, while two respondents (5%) could not express opin-

ion on rke issue.

Question 7:

h e s your bank embark on Correlation analysis of the risk of proposed

loan invesiment with that of the existing loan portfolio with a view to risk di-

versification prior to loan approval?

Table 7

Opinion on the Employment of Correlation

Analvsis for Effective Risk Diversification

Options No. of Respondents Percentage -

Yes

No

Can't Say

Total 42 100

Only three (7%) respondents agreed that their banks employ corre-

lation analysis. 36 (86%) Respondents agreed to the absence of a formal

correlation risk analysis technique, white the remaining (7%) respondents

couiL not give their opinion on the issue. This can be interpreted to mean

that the respondents who do not give an opinion on the issue d o not under-

stand what correlation analysis means. Most banks do not carry out the

analysis.

Question 8:

i: your answer to question 7 is "yes" what technique does your bank

em>loy for the analysis.

In the proceeding question: Question No. 7, only 3 respondents

were of the opinion that their banks embark on correlation analysis of the

risk of proposed load investment with that of the existing loan portfolio

with a view to risk diversification prior to loan approval. Although, these

respondents agreed that their banks employ correlation analysis, they do

not mention the technique they adopt in the analysis. This could be inter-

pretcd to mean that the respondents either do not know the technique in

use by their banks, which is not likely, given the status of the respondents,

or rfiey provided wrong answers.

A discussional interview with some of the respondents shows that in

practice, diversification is achieved through budgetary limits for different

sectors, and government securities subject to regulational requirements of

CentraI Bank of Nigeria (CBN); pointing to the absenceof the use of port-

46

folio theory in banks credit portfolio management.

Que'stion 9:

Since the inception of the Central Bank of Nigeria's (CBN) prudential

yuide;incs, how can you classify your banks provision for bad and

doubtful debts?

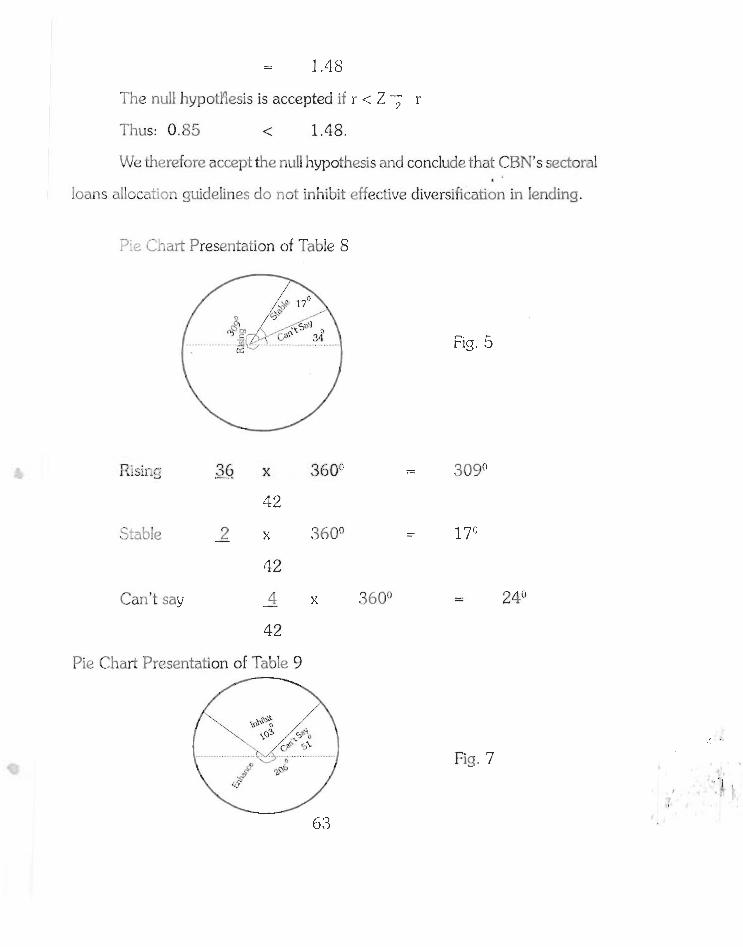

Table 8

Classification of Banks Provision for

Bad and Doubtful Debts

Options

Rising .

Fdling

.%able

Can't Say

No. of Respondents

36

Percentage

The above table reveals that most of the respondents 36 representing

Total

86% bclieve that since the inception of the prudential guideline of CBN,

their ~rovision or bad and doubtful debts have been rising. Their reason for

the above, they believe, arises from the stringent requirements of the guide-

line and the increase in volume of their loan portfolio, and not necessarily a

42

decline in quality of their loan portfolio since most of the provisions are usu-

100

ally recovered.

Question 10:

For the purpose of effective loan diversification, how can you clas-

sify the central bank of Nigeria's sectoral loan allocation guidelines. 47

CBW: Sectoral Loan Allocation Guidelines Effect on Diversification

Options

Enhance

Inhibit

Has no effect

Can't Say

No. of Res~ondents 1 ~ercen ta se

Twenty four (24) respondents representing 57% were of the opin-

I

ion that the CBN's sectoral allocation guidelines enhance effective loan

diversification, respondents (29%) believe that it inhibits effective diversifi-

I

catica, while 6 respondents (14%) could not express opinion on the issue.

Many of the respondents would think that effective loan diversifications is

w k n loans are given to different sectors of the economy, according to

CBN's guideIines without looking at the correlation of their loan portfolio.

In actual sense, effective diversification of loan portfolio is deemed to

exist, if the loan are negatively correlated.

Question I 1 :

Would you wish to see the scrapping of the CBN's sectoral loan

allocation guidelines?

Total 42 100

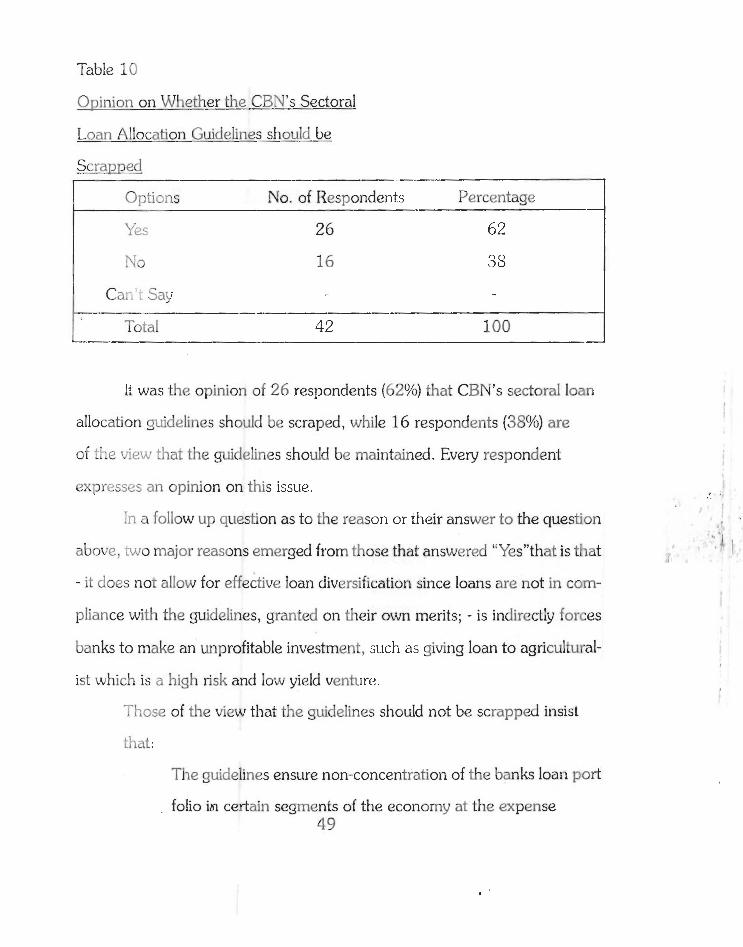

Table 10

Opinion on Whether the CBN's Sectoral

Loan Allocation Guidelines should be

Scrapped

Optims No. of Respondents Percentage

1 Total 42 100 1

It was the opinion of 26 respondents (62%) that CBN's sectoral loan

allocation guidelines should be scraped, while 16 respondents (38%) are

of the view that the guidelines should be maintained. Every respondent

expresses an opinion on this issue.

In a follow up question as t o the reason or their answer to the question

above, two major reasons emerged from those that answered "Yeswthat is that

- it does not allow for effective loan diversification since loans are not in com-

pliance with the guideIines, granted on their own merits; - is indirectly forces

banks to make an unprofitable investment, such as giving loan to agricultural-

ist which is a high risk and low yield venture. - 1 hose of the view that the guidelines should not be scrapped insist

that :

The guidelines ensure non-concentration of the banks loan port

folio in certain segments of the economy at the expense 49

of the others;

- the guidelines also have a favourabte impact on economic

development, since most of the sectors of the economy were

considered.

They argued further that the problem is not with the guidelines but

with its implementation and monitoring which they hope the Central Bank

o; 5i;cria will intensify to ensure the attainment of the objective of the

guidelines.

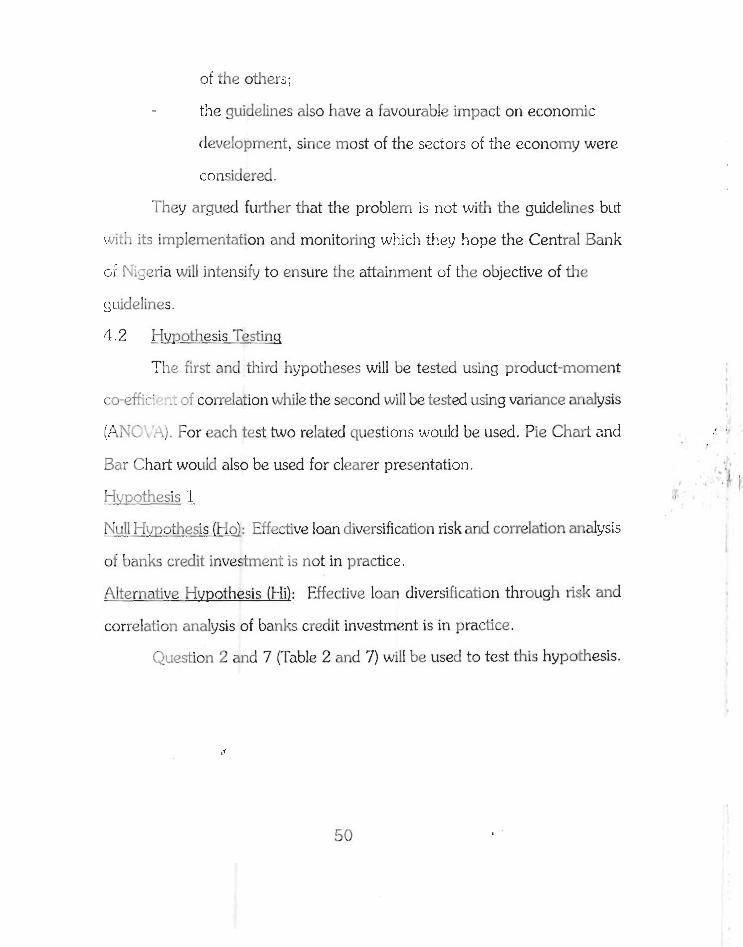

4.2 Hypothesis Testinq

The first and third hypotheses will be tested using product-moment

co-effi::' - -. cf correlation while the second will be tested using variance analysis

(ANC . . :). For each test two related questions would be used. Pie Chart and

Bar Chart would also be used for clearer presentation.

hkothesis 1

Null Hmothesis (Hol: Effective loan diversification risk and correlation analysis

of banks credit investment is not in practice.

Alternative Hy~othesis (Hi): Effective loan diversification through risk and

correlation anaIysis of banks credit investment is in practice.

Question 2 and 7 (Table 2 and 7) will be used to test this hypothesis.

Table 2

Opinion on Risk Analysis of Credit Applicatjon

I Options No. of Respondents Percentaqe

Yes

No

Can't S2y

Table 7

Opinion or, the Ern~loyment of Correlation

Analysis for Effective Risk Diversification

Options No. of Respondents Percentage

Yes

No

Can't Say

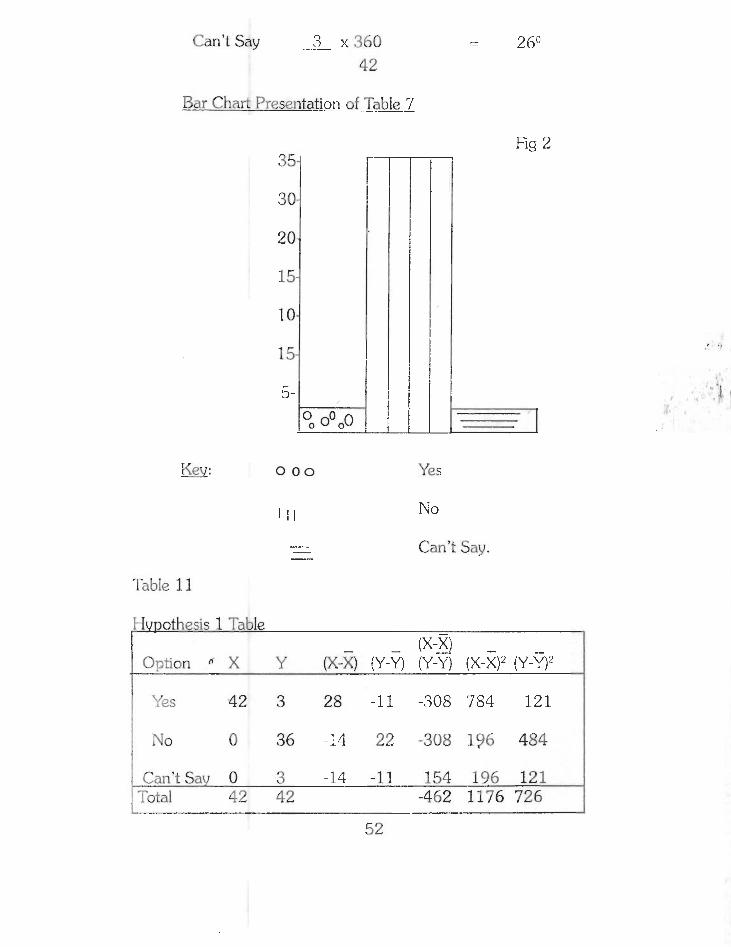

Pie Chart Representation of Table 7

Fig. 1

Can't Say - 3 x 360 42

Bar Chart Presentation of Table 1

Fig 2

TabIe 1 f

Yes

No

Can't Say.

,Hvnothesis 1 Table (x-X)

Option x Y D(-X) (Y-Y) (Y-Y) (x-X)"-T)Y)' 'I

Yes 42 3 28 -11 -308 784 121

I i Can't Say 0 3 -14 -11 154 196 121 1 Total 42 42 -462 1176 726

Note: X data are extracted from Table 2.

Y data are extracted from Table 7.

G/ '7

Where ZT = Critical value from the Standard

normal table.

- - Standard Error.

Using 1% level of significance

' n - 1 / 3 - 1

- - 1.82 I

Ho is accepted if r < Z 56; n - i

Thus, - 0.5 c 1.82. We therefore accept the null hypothesis and

conclude that effective loan diversification through risk and correlation

analysis of banks credit investments is not in practice.

Hypothesis 2

Null Hrlpothesis (Ho): The distribution of respondents between different

options as to the effects of diversification of banks credit portfolio is not

significantly different, between the three classes of banks.

Alternative Hwothesis: The distribution of respondents between different

options as to the effects of diversification of banks credit podfolio is signifi- n

cantly different, between the three classes of banks.

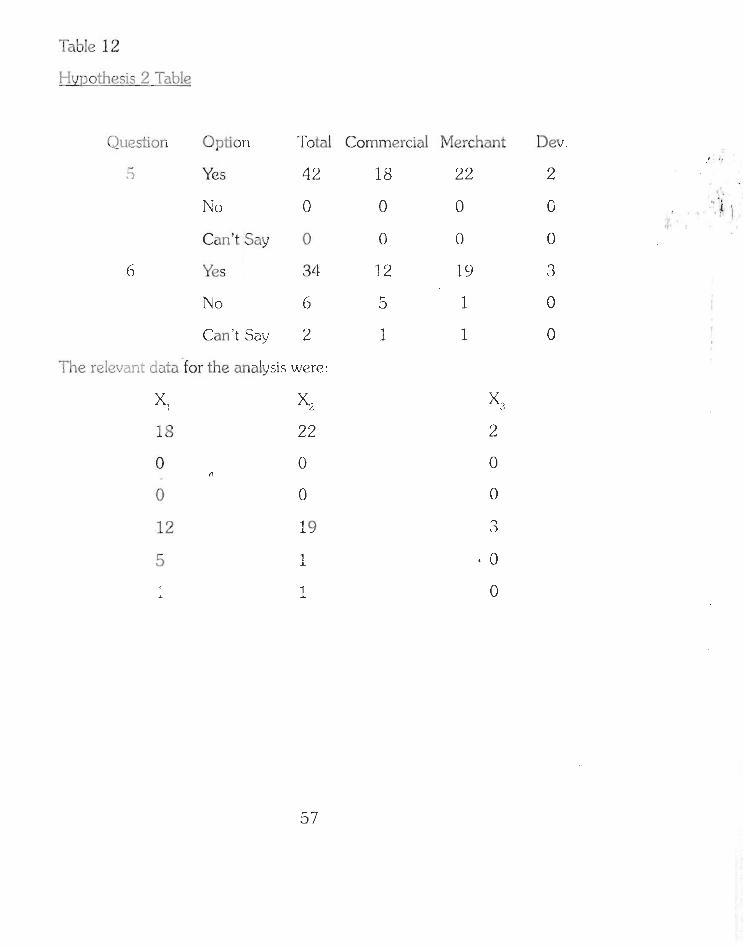

This hypothesis will be tested using variance analysis test. The ANOVA

table for the test will be extracted from TabIe 5 and 6. , ~

Table 5

Opinion on the Necessity for Diversification

of Loan P d o l i o

Table 6

respond en:^ View on the Enhancement of

Banks Loan Portfolio throush Effective

Risk Diversification

Option 1 %s

I No i 1 Can't Say

No. of Respondents

42

-

-

aption I Yes

NO n

Can't Say

Percentage - 100

-

-

No. of Respondents

34

6

U 3

Percentage

81

14

5

Key:

Yes

Ns

Can't Say

Fig 4

i I I Yes

0 0 0 Can't Say.

Table 12

Hvnothesis 2 TabIe

Question Option

5 Yes

No