Embed Size (px)

Citation preview

Untangling Property Dispositions:The Partnership Tangle

NCSHAJune 2015Los Angeles CA

2

The Y15 Landscape

Most Year 15 events do not involve sale of the property Instead, the Property GP (the Developer) buys out the LP (the

investor or syndicator) Most LPs want an exit Untangling the tax credit partnerships can be complex

and contentious – and take a long time Two key factors in the unwind negotiations:

Level of equity value in the property Level of ambiguity and complexity in the partnership

documents

3

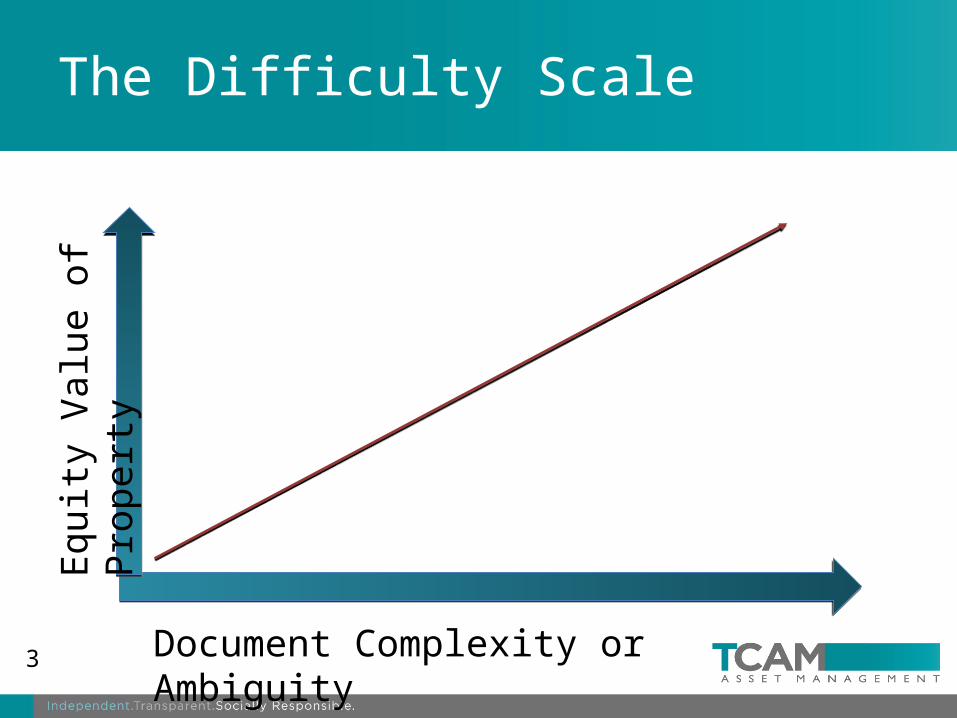

The Difficulty Scale

Document Complexity or Ambiguity

Equi

ty V

alue

of P

rope

rty

4

The Easy Deals

Either: There is limited equity value in the property OR Partnership documents are very clear about exit

Limited Equity Value Very low rent/income restrictions Weak markets High levels of soft debt Mortgage prepayment restrictions or penalties

Clear Documents Usually means a clear Right of First Refusal or option at Debt +

LP Taxes

5

Non-Profit Right of First Refusal

Practically speaking, usually treated like an option LPs do want their exit tax paid

Non-profit GPs now working with LP during years 10-15 to manage tax capital accounts to zero

When exit tax is high, negotiations can get trickier and/or the exit can be slowed

6

Low Equity Value

GP makes offer

LP confirms GP estimate of value with internal analysis or Broker Opinion of Value

LP will want to be caught up on any unpaid priorities

LP may want transaction expenses covered

GP handles all third-party approvals

If prior to Year 15, LP will want assurances about continued compliance

7

The Tough Deals

Lots of value to fight over In many deals, GP has an

option to purchase the property or the LP’s interest at fair market value

In the absence of a real market sale, fair market value can be debated endlessly Dueling appraisals is an

expensive way to address this problem

8

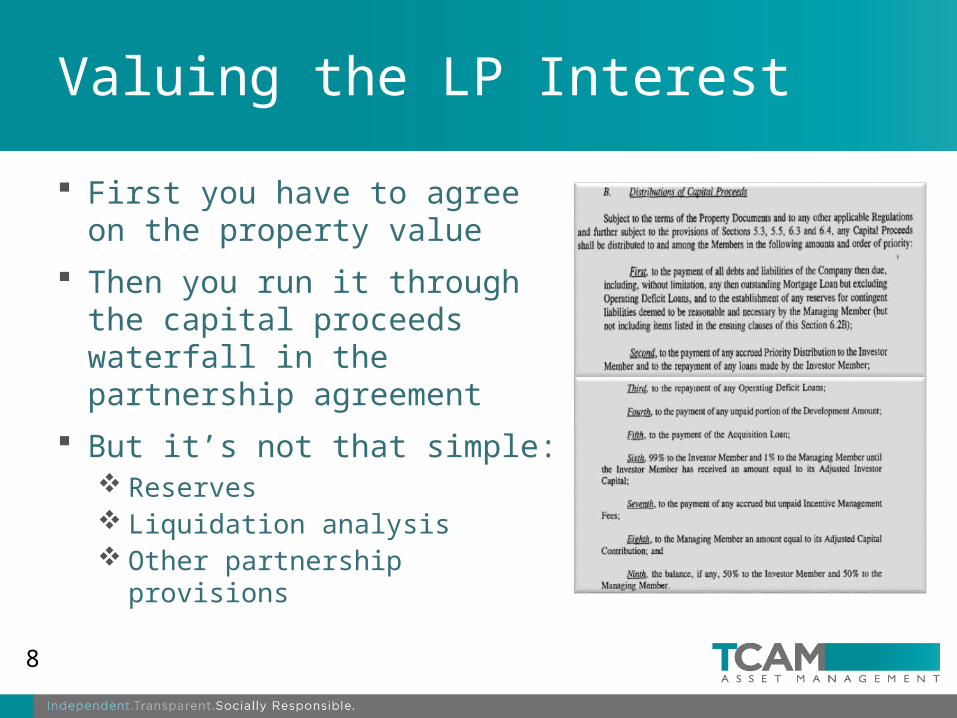

Valuing the LP Interest

First you have to agree on the property value

Then you run it through the capital proceeds waterfall in the partnership agreement

But it’s not that simple: Reserves Liquidation analysis Other partnership provisions

9

Liquidation Analysis Issue

Virtually all partnership agreements have provisions about the distribution of in the event of a liquidation The provisions can differ from the capital transactions

waterfall They tend to favor the Investor Limited Partner

The provisions do not apply if the GP is buying out the LP, but the LP can and often does argue that the hypothetical sale on which the buy-out is based would in fact be a liquidation

Buy-outs can get stuck on this issue

10

Other Complicating Factors in the Buy-Out LP has no right to force a sale of the property LP has a right to force a sale but cannot really

enforce its right without removing the GP LP’s ability to transfer its interest without the GP’s

consent The GP gets the majority of the cash flow but very

little of the residual proceeds There are conditions to the exercise of the Right of

First Refusal

11

The Good News

Significant equity value is a happy surprise Most GPs and third-party buyers are not planning QCP

or market rate conversion Planning to operate for cash flow and/or Redevelop with a new round of tax credits, extending

affordability New deals are structured with more thought about

back-end Track record of cash flow and residual proceeds

helps keep investors interested in further investment

Untangling Property Dispositions:The Partnership Tangle

NCSHAJune 2015Los Angeles CA