Embed Size (px)

Citation preview

Updates on HDMF

Housing Loan Program

Juanito V. Eje

Task Force Head

Business Development Sector 24 November 2015

Presentation Outline

I. Pag-IBIG at a Glance

II. Updates on Existing Housing Loan

Guidelines

III. Approved Housing Loan Guidelines for

Implementation in 2016

IV. Updates on Government-to-Government

(G-to-G) arrangement

Your Pag-IBIG today

115.765.76 MillionMillion MembersMembers

₱₱11.3411.34 BillionBillion

DividendsDividends

Highest in the Fund’sHighest in the Fund’s 3434--year Historyyear History

Net IncomeNet Income

₱₱ 16.2216.22 BillionBillion

₱₱376.09 B376.09 B Total AssetsTotal Assets

20142014

20142014 ₱₱28.07 B28.07 B Membership SavingsMembership Savings

20142014

Target by 2015:Target by 2015:

117 Branches117 Branches NationwideNationwide

7777 BranchesBranches

NationwideNationwide

2222 PostsPosts

WorldwideWorldwide

Membership Breakdown

Employed Pvt9,096,047

58%

Employed Govt

1,989,41213%

OFW4,314,009

27%

Employed Pvt HH

24,8930.2%

Other Working

Groups340,061

2%

Total Active Membership Distribution

Total = 15,764,422

Target

2010

38

2014

77

2015

117

Current

More Branches and Satellite Offices

to reach more members

22 Posts Worldwide

Overseas Posts

Asia

Pacific

Europ

e

Middle

East

Korea

Macau

Japan

Hong

Kong

Taiwan

Brunei

Malaysia

Singapor

e

London

Rome

Greece

Milan

Dubai

Riyadh

Qatar

Abu

Dhabi

Bahrain

Al

Khobar

Kuwait

Oman

Jeddah

United States of America

New York (New)

Europe Remittance Partners: 77 North America

Remittance Partners: 103

Middle East Remittance Partners: 278

Asia Pacific

Remittance Partners: 300

Overseas Desks Remittance Partners Concentration of OFWs

and expanding

Housing Loan Borrowers Per Membership Category

From January 2010 to September 2015

2%

16%

20%

62%

Employed Private Employed Government

OFW Self-Employed

Corporate-Wide PLR*

Updates on Programs

Performing Loans Ratio (PLR)

79.02%79.02%

80.23%80.23%

81.77%81.77%

80.89%80.89% 80.69%80.69%

83.27%83.27%

87%87%

*Mortgage/ Sales Contracts Receivables only

10% INCREASE

2015 Developers Application

for Funding Allocation

Pag-IBIG

Housing Hub

No. of

Developers

Approved

Amount

Utilization

%

Utilization

NCR 164 P 19.547 B P 11.621 B 59.45%

North Luzon 96 5.206 B 2.758 B 52.98%

South Luzon 60 5.477 B 4.293 B 78.38%

Visayas 48 4.053 B 1.640 B 59.51%

One Mindanao 74 4.248 B 2.559 B 66.88%

Total 442 P 38.531 B P 23.644 B 61.36%

Note: Actual take out Jan to Oct 2015 : P 33.616 B

End-User Home Financing Program

Affordable Housing Program

Institutional Loan Programs

Part II – Updates on Existing Housing Loan Guidelines

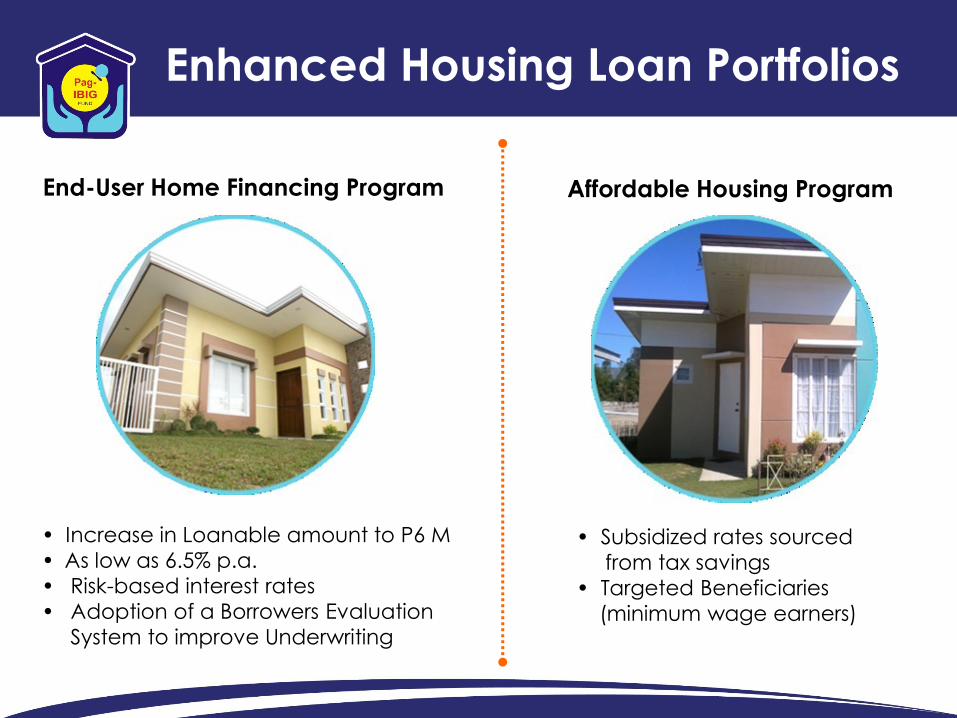

Enhanced Housing Loan Portfolios

End-User Home Financing Program

• Increase in Loanable amount to P6 M

• As low as 6.5% p.a.

• Risk-based interest rates

• Adoption of a Borrowers Evaluation

System to improve Underwriting

Affordable Housing Program

• Subsidized rates sourced

from tax savings

• Targeted Beneficiaries

(minimum wage earners)

End-User Home Financing Program

Interest Rates* adopting of risk-based pricing

(Cir. 310)

3 year-fixing

5 year-fixing

10 year-fixing

15 year-fixing

20 year-fixing

25 year-fixing

30 year-fixing

6.500%

7.270%

8.025%

8.585%

8.800%

9.050%

10.000%

Risk-Based Pricing Framework

* Effective June 2015

Before

• Borrower Evaluation

System (BES) determines

applicable LTV:

– LTV varies from a high 90%

to a low of 70% depending

on BES result (Good, Fair,

Poor)

Now

• Fixed LTV for developer-

assisted accounts

– 100% for loans up to P450K,

provided property under a

socialized housing project.

– 90% for loans up to P 1.700 M

– 85% for loans over P 1.700 M

End-User Home Financing Program

Loan-to-Value (LTV) Ratio

Amounts NCR & OFWs Outside NCR GROSS MONTHLY

INCOME

(Maximum) P 15,000 P 17,500 P 12,000 P 14,000

LOAN AMOUNT

(Maximum) P50,000 P 750,000 P 450,000 P 750,000

INTEREST RATE* 4.5% 6.5% 4.5% 6.5%

Affordable Housing Program (AHP)

Loan Take-out

No. of Units

20,218 Loan Value

P 7.4B

Designed for minimum wage earners,

the AHP caters to the actual need of the

borrower based on his capacity to pay.

Loan amount up to P750K

Interest rate as low as 4.5%*

Direct Developmental Loan

Program Developmental financing for developers under

easier terms and conditions

Loan may be used for the development of

residential subdivision or medium-rise buildings

or for the construction of housing units

Wholesale Loan Rates

1-Year Fixing 6.125%

2-Year Fixing 6.750%

3-Year Fixing 7.875% as of January 1, 2015

Institutional Loan Programs

Part III – Approved Housing Loan Guidelines for

Implementation in 2016

The borrower may avail of two or more Housing Loans

at the same time;

The resulting amortization payments for all loans are

within his capacity to pay;

The aggregate loan value should not exceed

P6,000,000.00; and·

Cross-default provision

Updates on Housing Loan Programs

I. Availment of Multiple Housing Loans (Cir. 353)

Acquisition/installation of solar panels as part of home

improvement or as a component of the housing unit to

be purchased

The loan shall be secured by a collateral that shall

consist of the same residential property to which the

loan proceeds are applied.

Updates on Housing Loan Programs

II.Availment of Pag-IBIG Housing Loans for

the Acquisition/ Installation of Solar Panels

Particulars Cir. 259

(Existing)

Cir. 344

(Approved,

For Implementation)

Documentation

(Buyer & Developers) Contract To Sell -

Documentation

(Developers & HDMF) - Deed of Absolute Sale

Documentation

(Buyer & HDMF)

Deed of Assignment with

SPA

Deed of Conditional Sale

Property Title

TCT in the name of the

Developer with

Annotated DOA with SPA

TCT in the name of HDMF

General Loan Documentation

Updates on Housing Loan Programs

III. Take Out Mechanism for Developer Assisted Housing Programs

Particulars Cir. 259

(Existing)

Cir. 344

(Approved,

For Implementation)

Delivery of Folders to

HDMF

Window 1 and 2

Classification

One Window (All accounts to

be delivered are covered with

NOA)

Borrower’s Validation Borrower’s CI and

Validation upon delivery of

individual loan folders

All accounts must undergo

advance borrower’s CI &

validation

Inspection of individual

units

Upon delivery of individual

loan folders

All properties subject of the

loan must undergo advance

inspection

Pre-approval Activities

Updates on Housing Loan Programs

III. Take Out Mechanism for Developer Assisted Housing Programs

Updates on Housing Loan Programs

III. Take Out Mechanism for Developer Assisted Housing Programs

Particulars Cir. 259

(Existing)

Cir. 344

(Approved,

For Implementation)

Documents For

Loan Release

Contract To Sell

(Between Developer & Buyer)

Deed of Absolute Sale

(Between Developer & HDMF)

- Deed of Conditional Sale

•Promissory Note

•Disclosure Statement

•Loan & Mortgage Agreement

Promissory Note

-

-

Tax Dec & Receipt in the name of

the Developer (H& L)

Tax Dec & Receipt in the name

of HDMF (H& L)

TCT in the name of the Developer

with Annotated DOA with SPA

TCT in the name of HDMF

Post Approval/ For take Out

REGULAR PRIME RETAIL WINDOW

Available for new developers and

previously accredited

developers

ONLY for previously accredited

developers that

passed the

performance

criteria

For developer whose accreditation is

suspended

Updates on Housing Loan Programs

IV. Classification of Developers and Grant of Incentives (Cir 345)

Approved. For Implementation

CRITERIA REGULAR PRIME

Complete

DOCUMENTATION

compliance ratio

CDCR 95% 95%

UNIT

specifications

compliance ratio

USCR 90% 95%

CONVERSION

performance CP 90% 95%

BUYBACK (for breach of warranties)

BB No BB No BB

PERFORMING

ACCOUNTS

ratio

PAR 85% 95%

Updates on Housing Loan Programs

IV. Classification of Developers and Grant of Incentives (Cir 345)

Particulars REGULAR PRIME

Requirement For

take Out

TCT in the name of

HDMF

Title in the name of

the developer

Certificate

Authorizing

Registration

Updates on Housing Loan Programs

IV. Classification of Developers and Grant of Incentives (Cir 345)

Cir. 247 – repealed last July 1, 2015

Cir. 349 – existing (Interim Guidelines)

Cir. 344 – approved. For 2016 implementation

Updates on Housing Loan Programs

V. Implementation of various Housing Loan Guidelines/Circulars

Transitory Provision

Circular 349 shall continue to be in force for six (6) months from

the date of implementation of Cir. 344

Part IV – Updates on Government-to-Government (G-to-G)

arrangement

Bureau of Internal Revenue

Finalization of the requirements for the issuance of E-CAR

Finalization in the procedure on the G to G arrangement

System testing completed for pilot areas (Calamba and

Marikina)

For system testing Trece Martires

Timeline - 1st quarter of 2016

Government-to-Government (G- to-G) Transactions

Thank you