Embed Size (px)

Citation preview

UOP 7802-1 © 2016 UOP LLC. A Honeywell Company All rights reserved.

Upgrade Bottom of the Barrel to Improve Your Margins

Agafeev Viacheslav

OOO UOP, A Honeywell Company

28-30 November 2016 CIS Downstream Summit 2016 Vienna, Austria

Market Drivers

Key Factors and Considerations

UOP BOTB Technology Portfolio

Uniflex process

Economics

Summary of Presentation

2

1

2

3

4

5

UOP 7802-2

Residual Fuel Oil Demand has Declined Dramatically

150

0

RESIDUAL FUEL OIL DEMAND (1990 to 2012)

MiTPA

1990

50

100

150

0

2012

EUROPE

1990 2012

FSU

Source: BP Statistical Review of World Energy 2012

3

UOP 7802-3

Demand in Europe has fallen to half the level it was 20 years ago FSU RFO demand was higher than in Europe – it is now lower

Combined Impact of Export Duty Change and Declining Demand on Residue Production

RFO market is changing due to:

Russian duty changes impacting export margins

Natural gas usage in power plants

Introduction of tighter specification for marine (bunker) fuels

Upgrading to gasoline and diesel:

Provides margin uplift

Reduces supply gap for gasoline

Supports profitable diesel exports

Forecasts predict that up to 50 million tonnes per annum of residue will be converted to distillates through to 2020,

with the current focus on VGO upgrading

Exports

4

UOP 7802-4

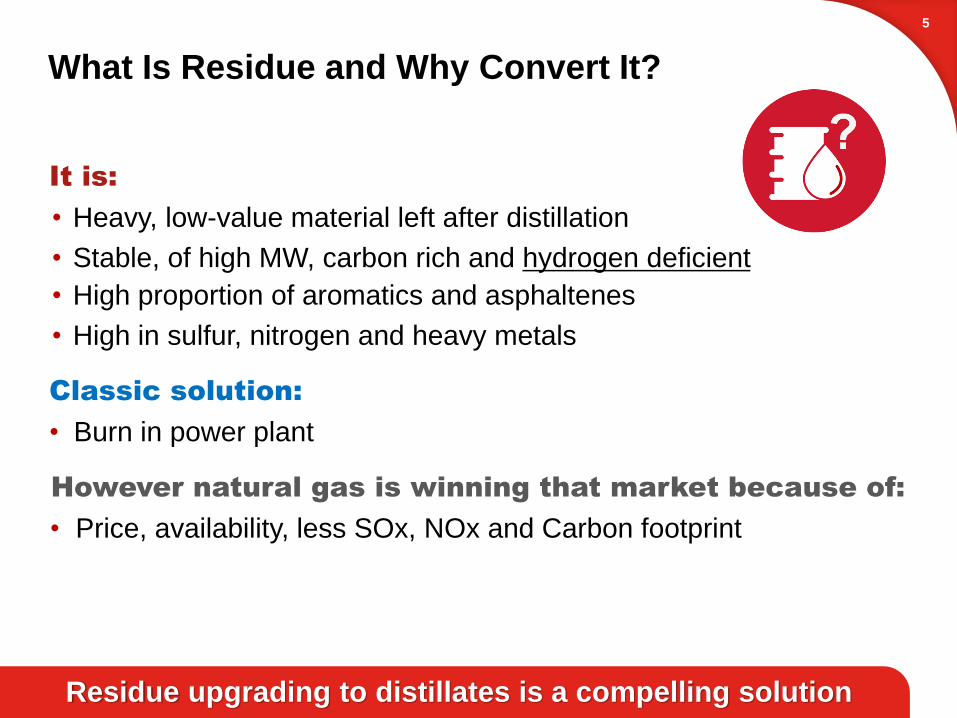

It is:

• Heavy, low-value material left after distillation

• Stable, of high MW, carbon rich and hydrogen deficient

• High proportion of aromatics and asphaltenes

• High in sulfur, nitrogen and heavy metals

Classic solution:

• Burn in power plant

However natural gas is winning that market because of:

• Price, availability, less SOx, NOx and Carbon footprint

What Is Residue and Why Convert It?

Residue upgrading to distillates is a compelling solution

5

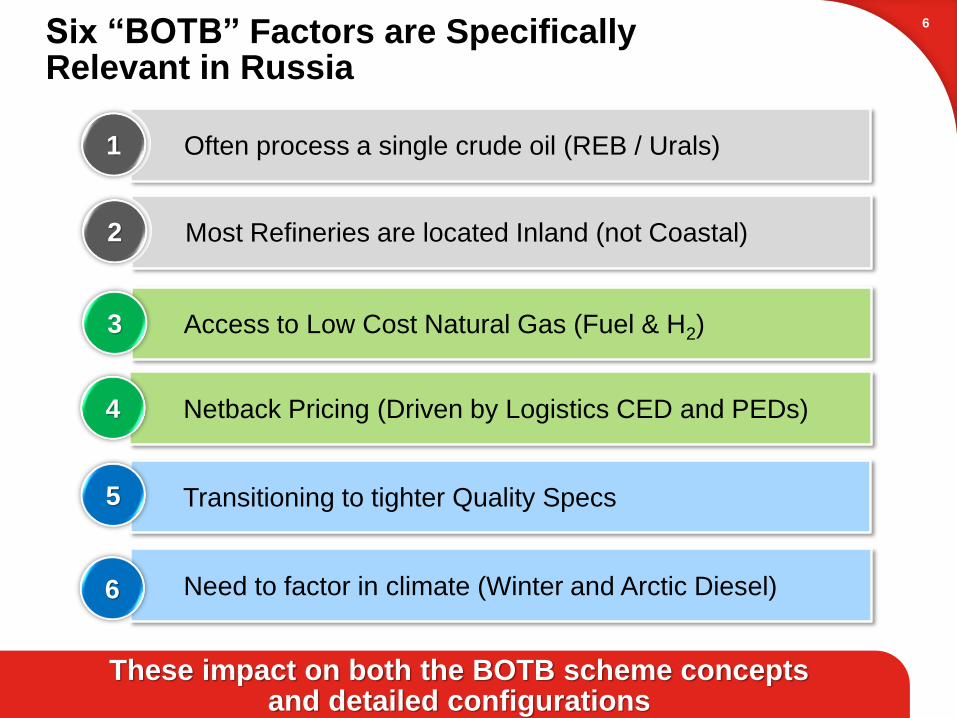

Six “BOTB” Factors are Specifically Relevant in Russia

Often process a single crude oil (REB / Urals)1

Most Refineries are located Inland (not Coastal) 2

Need to factor in climate (Winter and Arctic Diesel)6

Access to Low Cost Natural Gas (Fuel & H2)3

Netback Pricing (Driven by Logistics CED and PEDs) 4

Transitioning to tighter Quality Specs5

6

These impact on both the BOTB scheme concepts and detailed configurations

UOP’s Heavy Oil Upgrading Processes

7

TransportationFuels:

Gasoline, Jet Fuel, Diesel

Dis

tilla

tio

nNaphtha

Crude Oil

Vacuum Residue

Vacuum Gas Oil

Distillates

Residues:Heavy Fuel Oil,

Pitch, Coke

NaphthaHydrotreating & Reforming

FCC orHydrocracking

DistillateHydrotreating

ResidueUpgrading

UOP/FWUSASolvent

Deasphalting

FWUSA SYDEC™Delayed Coking

Process

UOP/FWUSAVisbreaking

UOP RCDUnionfining

Process

UOP Solutions for Residue Upgrading

UOP UniflexProcess

UOP 7802-7

UOP Solutions for Residue Conversion (Low to moderate conversion options)

UOP/FWUSAVisbreaking

UOP RCD Unionfining™Process

Limited conversion

LS fuel oil production or RFCC feed prep

Niche application

Difficult to justify for LS fuel production when natural gas is low cost

Up to 40% conversion with vacuum flasher

Achieves reduction in cutter stock for fuel

Can be a partial fix, not a full solution

Fuel oil outlet needed

FWUSA SYDEC™Delayed Coking Process

Higher conversion -up to 75%

Product require further upgrading to meet finished product specs

Need an outlet for the product pet coke

8

UOP 7802-8

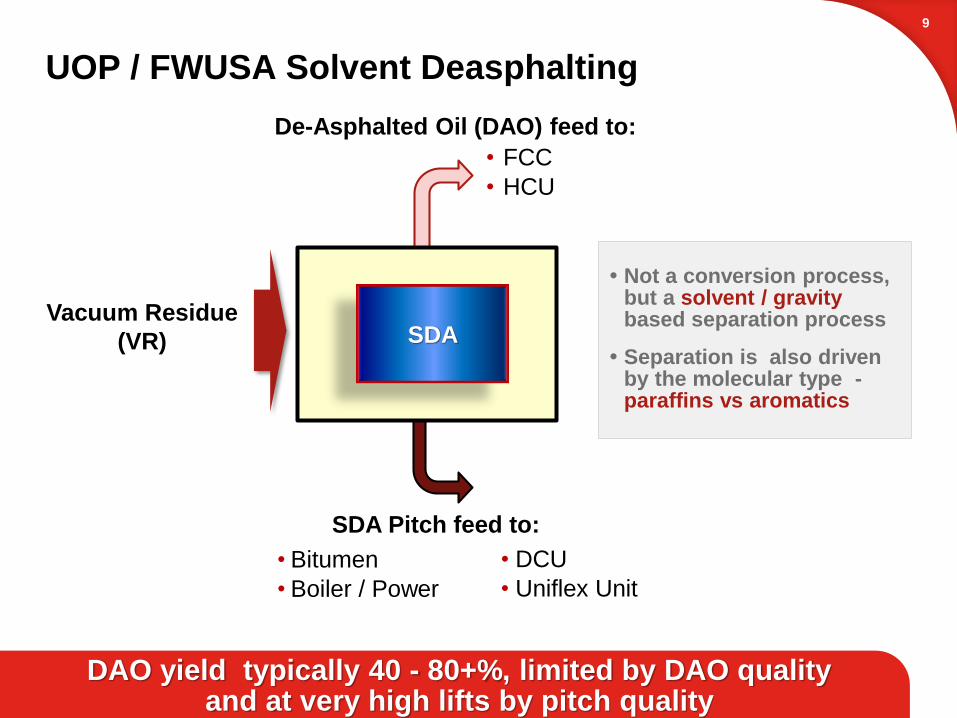

UOP / FWUSA Solvent Deasphalting

De-Asphalted Oil (DAO) feed to:

Not a conversion process, but a solvent / gravity based separation process

Separation is also driven by the molecular type -paraffins vs aromatics

SDAVacuum Residue

(VR)

• Bitumen

• Boiler / Power

SDA Pitch feed to:

• FCC

• HCU

• DCU

• Uniflex Unit

9

DAO yield typically 40 - 80+%, limited by DAO quality and at very high lifts by pitch quality

Visbreaking:

• Over 50 units licensed

Solvent Deasphalting:

• 19 SDA units (after 1994)

Coking:

• Over 70 units licensed

• SYDEC technology is the most successful

Resid Hydrotreating:

• 27 units licensed, 65% of the world’s total

• Wide range of feedstocks and applications

Uniflex Slurry Hydrocracking:

• Acquired by UOP from CANMET

• 5000 bpsd PDU operated for 15 years

UOP’s Residue Upgrading Experience

10

UOP 7802-10

The UOP Uniflex Technology Offering is......

UNIFLEX UNIT(Wt-%)

100

15

50-55

10-15

Vacuum

Residue Feed

Naphtha

Diesel

VGO

HDT

MHC & FCC or

HCU

90-95% Conversion

Maximum Diesel

Minimum VGO

Once through Catalyst

Product streams require further upgrading

CatalystH2

H2S, NH3

Gas, LPG

Pitch

11

UOP 7802-11

UOP Uniflex Process

12

Commercial Experience:

• 5,000 BPD unit operated for 15 years at Petro-Canada Montreal

• Developed excellent design correlations

• Very high reliability demonstrated

UOP Enhancements:

• Completed UOP Schedule A design

• Petro-Canada Montreal Unit experience with improvements

– Single train designs – parallel reactors,

common separation

– High conversion of HVGO

• Integrated pilot plant closely matches commercial performance

UOP 7802-12

Petro-Canada Montreal CANMET Unit Reactor Section

13

UOP 7802-13

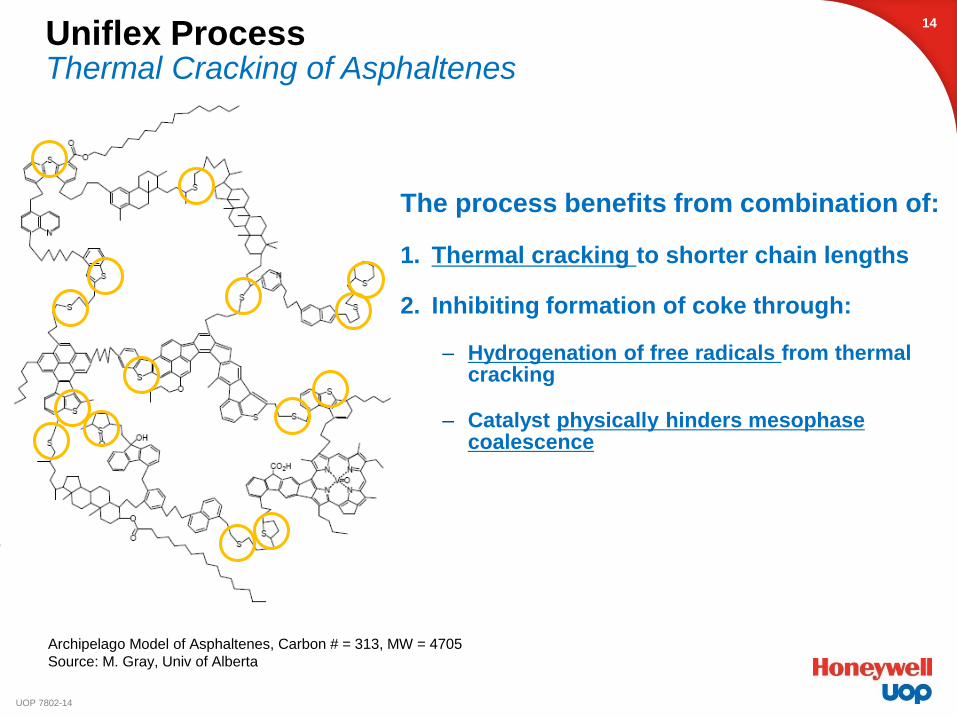

Uniflex ProcessThermal Cracking of Asphaltenes

Archipelago Model of Asphaltenes, Carbon # = 313, MW = 4705

Source: M. Gray, Univ of Alberta

The process benefits from combination of:

1. Thermal cracking to shorter chain lengths

2. Inhibiting formation of coke through:

– Hydrogenation of free radicals from thermal cracking

– Catalyst physically hinders mesophase coalescence

14

UOP 7802-14

• Improved design for higher conversion

– Upflow

– High temperature and moderate pressure

• Efficient utilization of reactor volume

– Reduced gas voidage

– Higher product vaporization

– Near Isothermal

• Asphaltene management

– Inhibit formation of coke pre-cursors

Feed, H2and Catalyst

Productsand Catalyst

15

Simple (no internals) highly effective performance and Commercially proven Reactor design

Uniflex Process Reactor Achieves Higher Conversion

VDU

Uniflex

HDTNaphtha 15 - 18

Gasoil 50 - 55

LVGO 10 - 15

HVGO

Pitch 5 - 10

100

• Light naphtha to gasoline

• Heavy Naphtha, reformer feed quality

• Gasoil, Euro V

• LVGO to existing HCU or FCC

Uniflex Configurations Vacuum Residue Feed

Base Case

No need for new HCU / FCC

16

H2S/ Gas / LPG

UOP 7802-16

VDU

Uniflex

HDT

H2S/ Gas / LPG

Naphtha 9 - 11

Gasoil 30 - 33

LVGO 6 - 9

Pitch 5 - 7

100

Uniflex ConfigurationsSDA Pitch as Feed

SDA

DAO 40

60

17

• Light naphtha to gasoline

• Heavy Naphtha, reformer feed quality

• Gasoil, Euro V

• DAO, LVGO to HCU or FCC

• Pitch to CFB, cement

Smaller Uniflex

Separate new HCU or FCC

HVGO

UOP 7802-17

• UOP global supply of catalyst

• Multiple manufacturing locations

• Simple logistics and storage

Catalyst Supply and Pitch Disposal...

Catalyst

• Cement:

– Often an attractive outlet option

• Boiler/Power:

– Conventional power plants

– CFB

• Solidification:

– Proven technology

– Facilitates transportation and storage

Pitch

18

UOP 7802-18

UOP Uniflex Process - Licensed Units Update

19

Uniflex Commercial Reference List

LocationUnit Capacity

(bpsd)Year

Licensed Project StatusYear ofStart-up

Canada 5,000 N/ADecommissioned

in 20131985

Pakistan 9,000 2011 Completed BEDP 2017/2018

China 18,000 2013Completed BEDP /

Detailed Engineering2017

Russia 7,000 2013 Completed BEDP 2017/2018

China 16,000 2014KO meeting expected

in 20162018

China 18,000 2014KO meeting expected

in 20162018

China 16,000 2014KO meeting expected

in 20162018

UOP 7802-19

Uniflex Process Key Success Factors

Commercially Proven

Low Value Feed

Higher Conversion

Higher Quality Products

Step Change Margin Increase

20

High crude oil prices make an even greater case for Uniflextechnology, offering attractive economic returns

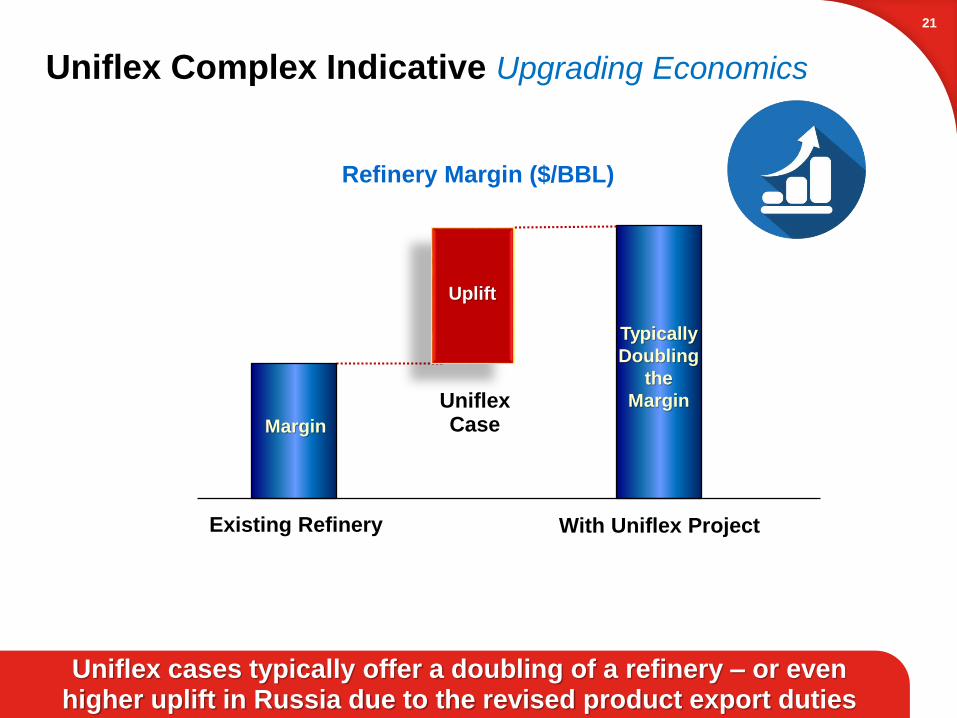

Uniflex Complex Indicative Upgrading Economics

0.9

Existing Refinery With Uniflex Project

UniflexCase

Refinery Margin ($/BBL)

Uplift

1.4

Margin

Typically

Doubling

the

Margin

21

Uniflex cases typically offer a doubling of a refinery – or even higher uplift in Russia due to the revised product export duties

22

Questions & Answers

https://twitter.com/HoneywellUOP https://www.linkedin.com/company/uop

https://www.uop.com/

https://www.youtube.com/user/Honeywell https://www.accessuop.com/

UOP 7802-22