Embed Size (px)

DESCRIPTION

U.S. Department of Justice Office of the Inspector General Fraud Detection Office. Grant Fraud Prevention National Grants Management Association January 18, 2012 Senior Special Agent Ken Dieffenbach 202-616-9844. What is Grant Fraud?. - PowerPoint PPT Presentation

Citation preview

Grant Fraud Prevention

National Grants Management Association

January 18, 2012January 18, 2012

Senior Special AgentKen Dieffenbach

202-616-9844

U.S. Department of JusticeOffice of the Inspector General

Fraud Detection Office

What is Grant Fraud?

Source: GAO Report 11-773T, June 23, 2011

Federal Outlays for grants to state and local governments (in billions)

1990 1995 2000 2005 2010

Fraud Assumptions

It Happens / It’s Not Good

Prevent / Detect it Early

Fraud Consequences

Organizational Reputation /

Survival / Program Impairment

Administrative

Civil

Criminal

Suspension & Debarment

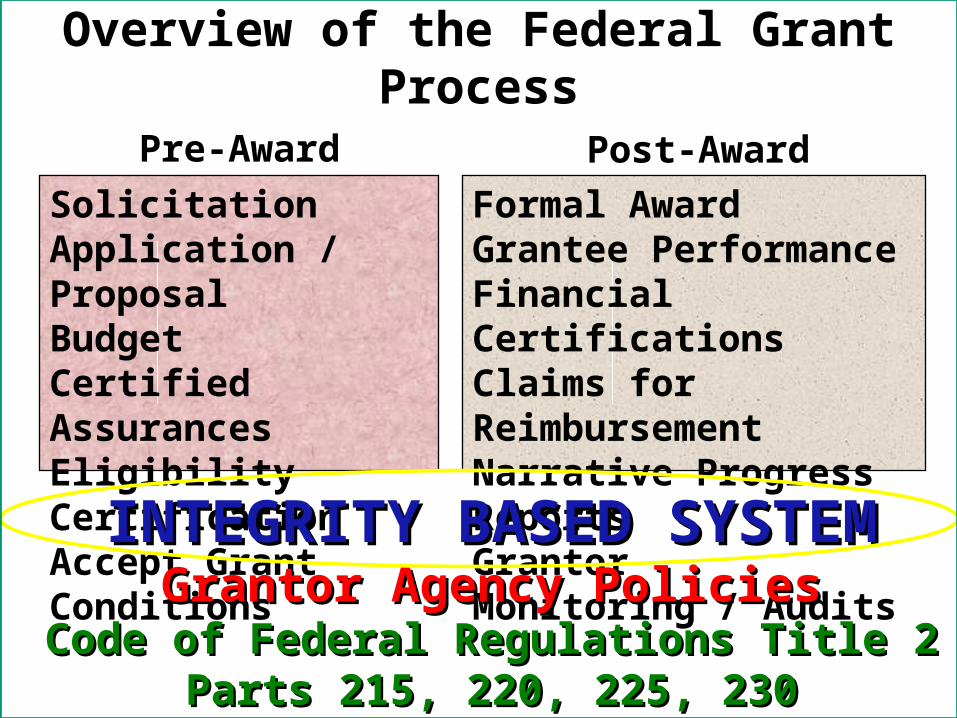

Overview of the Federal Grant Process

SolicitationApplication / ProposalBudgetCertified AssurancesEligibility CertificationAccept Grant Conditions

Formal AwardGrantee PerformanceFinancial CertificationsClaims for ReimbursementNarrative Progress ReportsGrantor Monitoring / Audits

INTEGRITY BASED SYSTEMINTEGRITY BASED SYSTEMGrantor Agency PoliciesGrantor Agency Policies

Code of Federal Regulations Title 2Code of Federal Regulations Title 2Parts 215, 220, 225, 230Parts 215, 220, 225, 230

Pre-Award Post-Award

Common Grant Fraud Risks

Conflicts of Interest /

Procurement Process Issues

“Lying”/ Failing to Support

Theft

Conflicts of Interest / Procurement Process Issues

Grantees are required to use federal funds in the best interest of their program and these decisions must be free of undisclosed personal or organizational conflicts of interest– both in appearance and fact.

The typical issues in this area include: Less than Arms-Length Transactions: purchasing goods or services

or hiring an individual from a related party such as a family member or a business associated with an employee of a grantee.

Sub grant award decisions and vendor selections must be accomplished using a fair and transparent process free of undue influence. Most procurements require full & open competition.

Consultants can play an important role in programs, however, their use requires a fair selection process, reasonable pay rates, and specific verifiable work product.

Former Member of Virginia House of Delegates Sentenced to 114 Months in Prison for Bribery

and Extortion

Philip A. Hamilton was elected to the Virginia House of Delegates in 1988

In January 2007, he introduced a budget amendment to appropriate $1 million for a “Center for Teacher Quality and Educational leadership” at Old Dominion University

Prior to, and after, offering this amendment, Hamilton negotiated with ODU for a $40,000 per year position as the Director of the new program.

ODU advertised the new position, received three applicants, interviewed none and hired Hamilton for the position which he held for two years.

Source: Excerpted from August 12, 2011 Press Release, U.S. Attorney’s Office for the Eastern District of Virginia

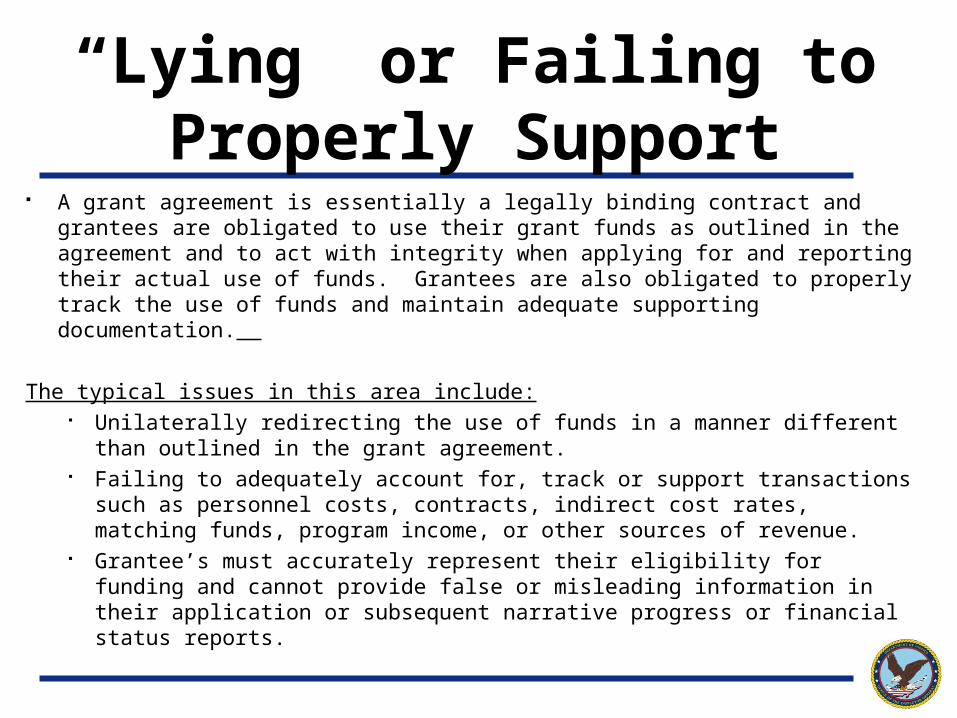

“Lying” or Failing to Properly Support

A grant agreement is essentially a legally binding contract and grantees are obligated to use their grant funds as outlined in the agreement and to act with integrity when applying for and reporting their actual use of funds. Grantees are also obligated to properly track the use of funds and maintain adequate supporting documentation.

The typical issues in this area include: Unilaterally redirecting the use of funds in a manner different than outlined in

the grant agreement. Failing to adequately account for, track or support transactions such as

personnel costs, contracts, indirect cost rates, matching funds, program income, or other sources of revenue.

Grantee’s must accurately represent their eligibility for funding and cannot provide false or misleading information in their application or subsequent narrative progress or financial status reports.

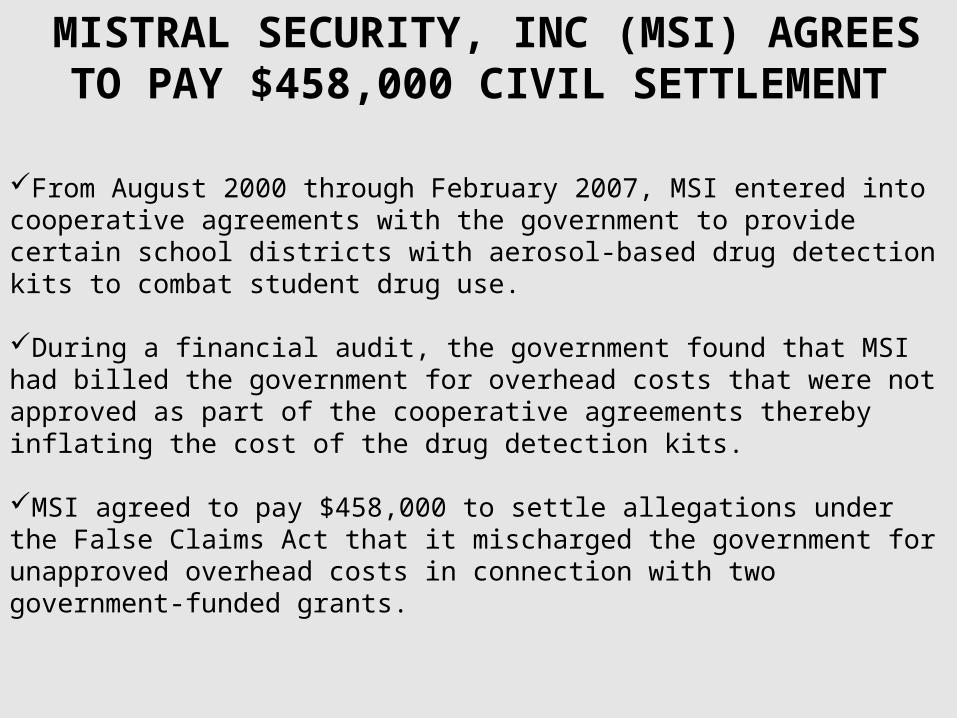

MISTRAL SECURITY, INC (MSI) AGREES TO PAY $458,000 CIVIL SETTLEMENT

From August 2000 through February 2007, MSI entered into cooperative agreements with the government to provide certain school districts with aerosol-based drug detection kits to combat student drug use.

During a financial audit, the government found that MSI had billed the government for overhead costs that were not approved as part of the cooperative agreements thereby inflating the cost of the drug detection kits.

MSI agreed to pay $458,000 to settle allegations under the False Claims Act that it mischarged the government for unapproved overhead costs in connection with two government-funded grants.

Source: Excerpted from September 30, 2011 Press Release, U.S. Attorney’s Office for the District of Maryland

Theft

Theft is the most common issue in almost all organizations–

including those that receive federal grant funding.

People that embezzle funds can be extremely creative and appear

very trustworthy– precisely why they can do so much damage to an

organization and remain undetected for extended periods of time.

Poor or no internal controls equals virtually inevitable theft. A lack of

appropriate separation of duties is one of the most common

weaknesses.

Checks routinely written to employees as “reimbursement” of

expenses and the use of ATM / Debit / Gift / Credit Cards must be

carefully controlled and require robust oversight.

KINLOCH MAYOR KEITH CONWAY SENTENCED FOR FRAUD, EMBEZZLEMENT, & WITNESS TAMPERING

Between January 2009 and March 31, 2011, Mayor Keith Conway of Kinloch, Missouri, stole, diverted and embezzled city funds to pay for several personal Bahamas vacation cruises, airline tickets to Las Vegas and Ft. Lauderdale for himself and friends, the down payment and loan payments on a time share condominium in South Florida, personal credit card bills, personal federal income taxes, as well as Ameren electric bills for a city owned residence where he was living rent free.

Conway was originally indicted on the fraud charges in May, 2011 and was charged in a superseding indictment June 2, 2011 with the additional witness tampering charge related to his efforts to persuade the Board of Alderman to provide false information to federal law enforcement about the criminal charges pending against him.

Conway was sentenced to 21 months in prison, and ordered to pay restitution of $62,429.

Source: Excerpted from November 18, 2011 Press Release, US Attorney’s Office for the Eastern District of Missouri

Risk Mitigation

1. Read & Understand the Grant Agreement; Know the rules: Agency Guidance;

CFR’s; Mandatory Disclosure, etc…

2. Examine your programs to identify fraud vulnerabilities: time & effort records;

indirect and G&A rates; consultants; control of “cash”

3. Consider developing a compliance plan.

4. Implement specific fraud prevention strategies including educating others about

the risks– the more people are aware of the issues, the more they can help

prevent problems or detect them as early as possible.

5. Maintain a well designed and tested system of internal controls.

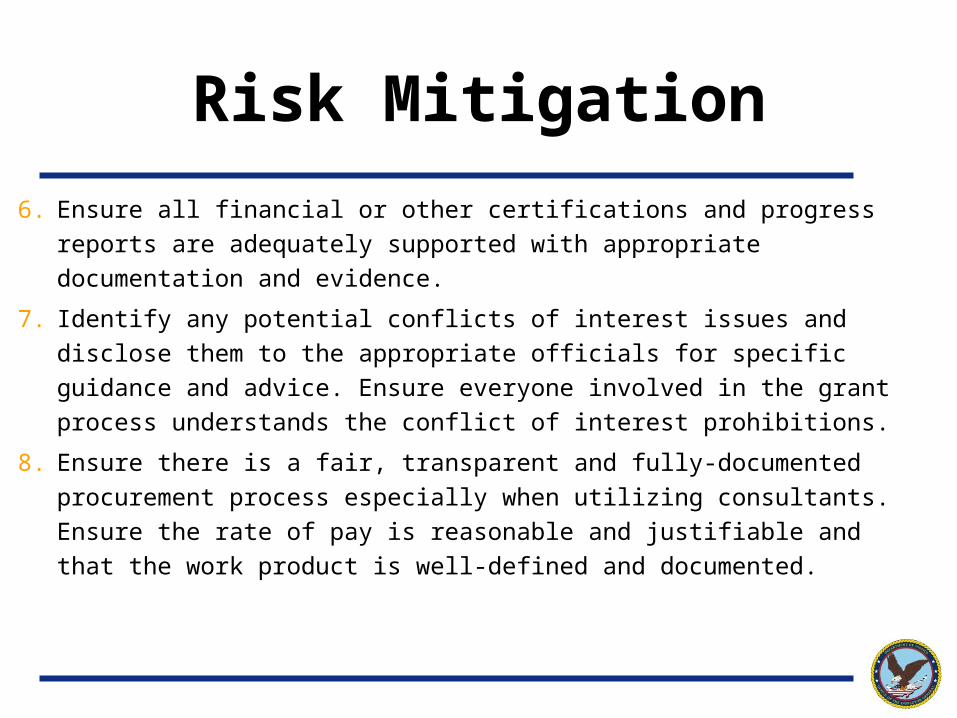

6. Ensure all financial or other certifications and progress reports are

adequately supported with appropriate documentation and evidence.

7. Identify any potential conflicts of interest issues and disclose them to the

appropriate officials for specific guidance and advice. Ensure everyone

involved in the grant process understands the conflict of interest

prohibitions.

8. Ensure there is a fair, transparent and fully-documented procurement

process especially when utilizing consultants. Ensure the rate of pay is

reasonable and justifiable and that the work product is well-defined and

documented.

Risk Mitigation

Questions?Ken Dieffenbach

202-616-9844