-

8/7/2019 US Wealth Management Survey

1/20

U.S. Wealth Management SurveyTrends and Emerging Business

Models

Leading Research John Rolander Gauthier Vincent

Chuck LymanSofia Graniello

-

8/7/2019 US Wealth Management Survey

2/20

1

Executive Summary The U.S. wealth management industry is in the

midst of a series of dramatic changes, resulting from the

recent crisis as well as long-term trends in the industry

Full-service firms have been losing share of advisors and assets

to independent and self-directed

channelsa trend that preceded the crisis and has accelerated The

financial crisis has created new challenges: Client satisfaction

has approached historic lows, and

client focus on transparency and lower-risk/return products has

resulted in lower revenue yield

In addition, consolidation of banks and brokerages has led to

the challenge of creating a truly integratedexperience and

realizing the potential economic rewards

Going forward, we expect the industry to focus on three key

strategic challenges:

1. How can advisors and firms regain client trust?

2. What is the the role of the advisor in a world of integrated

financial institutions?

3. How can wealth management operating models deliver

specialization and scale to enable competitive

advantage and profitable growth?

Answering these questions will be key to positioning evolving

wealth management firms for a new phaseof growth and

profitability

-

8/7/2019 US Wealth Management Survey

3/20

2

North America Shows Continued Growth Prospects for High Net

Worth (HNW) Markets

12.7

9.1

11.711.3

10.2

3.3

2.7

3.33.2

2.9

0

5

10

15

20

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

HNW Population(in millions)

HNW Wealth(in US$ trillions)

*****

**

North American HNW1 Population and Wealth,2

2005-2013eNorth American HNW and Ultra HNW Population

and Wealth,3 2008

9.1

3.2

Wealth (in US$ trillions)Population (in thousands)

*

*

*

*

1. High net worth is defined as individuals with more than US$1M

in investable assets, ultra high net worth as those with more than

$30M in investable assets.2. Wealth is defined as investable

assets, excluding primary residence, collectibles, consumables, and

consumer durables.3. The estimate of ultra HNW wealth in North

America is based on the global contribution rate of ultra HNW to

total HNW wealth = 34.7%.Note: 2013 population growth is an

estimate based on Booz & Company analysis.

Source: Capgemini/Merrill Lynch World Wealth Report 2009; IHS

research; Booz & Company analysis and research

4.2%CAGR

7%CAGR

-

8/7/2019 US Wealth Management Survey

4/20

3

North American HNW Growth Is Outpacing Other Global HNW

Markets

GDP 6.1%HNW 10.8%

Multiple 1.8x

Middle East & Africa

GDP 5.2%

HNW 8.1%

Multiple 1.6x

Asia/Pacific

GDP 4.5%HNW 5.9%

Multiple 1.3x

Latin America

GDP 2.8%

HNW 8.4%

Multiple 3.0x

North America

GDP 2.5%

HNW 4.4%

Multiple 1.7x

Europe

GDP 3.6%

HNW 7.0%

Multiple2 1.9x

Global

1. 2002-2007 sample used to avoid distortions from market

conditions in 2008 and 2009.2. Multiple represents the number of

times that HNW markets are growing above GDP; a higher multiple

represents a HNW market growing much faster than the rest of the

economy.

Source: IHS research; Booz & Company analysis and

research

Key Takeaways

Rapid growth of HNW globally at7% CAGR, with North

Americagrowing faster at 8.4%

Higher HNW to GDP multiple in

North America attributed tounique market characteristics:

Wealth distribution andconcentration

Stability and maturity of

capital markets

Global Wealth Management Market Growth(CAGR 2002-20071)

-

8/7/2019 US Wealth Management Survey

5/20

4

Recent Trends Have Posed Important Challenges to Firms in

the U.S. Wealth Management Marketplace

ClientBehavior

AdvisorMovement

Pressure onProfitability

Key Trends

Asset allocation shifts toward safer products,

and demand for transparency increases

Post-crisis, client satisfaction levels are at anall-time

low

Advisor migration toward independent channelscontinues

Advisors are increasingly making trade-offsbetween compensation

and services received(issue resolution, portfolio management

tools)

Battle for HNW clients continues, resulting inexpanding war for

advisor talent

Implications

Business Models

1

2

3

4

As a response to shifts in the marketand profit pressure, firms

are adaptingtheir business models

New formats in the independent space

have emerged to offer new valuepropositions for firms and

advisors

New players have entered the marketand are attracting breakaway

advisors

Consolidation is driving scale in bankbrokerage and resulting in

integratedinstitutions

Team coverage models dominate theultra HNW space

Innovations have emerged in the onlinespace

Changes in asset levels and pricing, along withincreasing

regulatory oversight, are puttingpressure on wealth managers

profitability

Source: Booz & Company

-

8/7/2019 US Wealth Management Survey

6/20

5

Globally, the Downturn Has Engendered More Pragmatic Client

Behaviors

* Based on responses of 140 private banking executives, senior

financial advisors, and leaders of regulatory authorities in 15

markets worldwide to Booz & Companys 2009 private banking

survey.

Source: Booz & Company research and analysis

35%

20%

16%11%

*

*

*

*

*

*

*

*

*

*

Shift in Asset Allocation(% of client assets invested, per

product)

Changing Requirements of HNW Investors

Sustainability of RecentTrend Toward Lower Risk*

(% of responses)

26%

6%*

*

*

*

1 Client Behavior

95% of survey respondents rated price transparency as being of

high importance when asked about new pricing structures

Assets shifting away from equities and alternatives

Increasing preference for safer, more transparentproducts such

as fixed income and cash related

Despite the recent shift in asset allocation, the majority

ofrespondents expect a return to traditional allocation

-

8/7/2019 US Wealth Management Survey

7/20

6

0.7

0.8

0.9

1.0

***

Investment Returns During the Crisis Have Resulted in

Plummeting Client Satisfaction Levels

1 Client Behavior

HNW Client Satisfaction Index*

Key Takeaways Client satisfaction levels decreased to

all-time lows during the financial crisisas investment

performancedecreased

Driven by this decline, clientsexperienced decreased loyalty to

theiradvisors and firms, fueling themigration trend

Advisors are facing challenges in howto best address client

dissatisfaction

Wealth management firms areresponding by adopting a more

client-

focused perspective

* Calculated from percentage of satisfied customers, with 1

being the highest number of satisfied customers.

Source: Booz & Company

CLIENT EXAMPLE

-

8/7/2019 US Wealth Management Survey

8/20

7

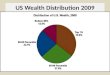

The $10.8T U.S. Wealth Market Is Served by Multiple

Providers

with Distinct Formats but Overlapping Value Propositions

U.S. Retail Wealth Management Market

Source: Capgemini/Merrill Lynch; Aite Group; Financial Plannings

FP 50; press releases; 10-K forms; Booz & Company analysis

EndClientWealthSpectrum

Firm Asset Size

MassAffluent

Ultr

aHNW

Wire Houses$4.2T

$50 Billion

HNW

Discount Brokers$1.8T

Independents and Regionals$1.9T

Bank Brokersand Insurance

$0.6T

Wire House

PrivateBanksBank Private Banks

$1.1T

$1 Trillion$1 Billion

RegisteredInvestmentAdvisors

(RIAs)$1.2T

Total Assets: $10.8T

2 Advisor Movement

-

8/7/2019 US Wealth Management Survey

9/20

8

Advisor Head Count by Channel(2004-2008 CAGR and Number of

Advisors)

The Shift of Advisors and Assets from Full-Service to

Independent

Models Is Expected to Continue

Key Takeaways

Driven by the desire for independenceand higher payouts,

financial advisorshave been migrating from wire housesto more

independent channels

The hybrid channel has benefited fromthis trend, as breakaway

advisorstypically have a mix of commission andfee businesses

Independent segments shouldcontinue to benefit from investor

andadvisor preference for independence

Independents, RIAs, and hybridadvisors have increased share

and

now account for about 40% of assetscombined

* Broker/dealer.

Source: Cerulli Associates publicly available data, Market

Update: RIA Channel Sizing and Assessment,; Booz & Company

analysis

2 Advisor Movement

1.8%

15

19

16

70

99

36

55

310

-5 0 5 10 15 20

* *

* *

* *

* *

* *

* *

* *

* *

Advisor Head Count (CAGR)

2008Advisors

(in thousands)Channel

-

8/7/2019 US Wealth Management Survey

10/20

9

Increasingly, Advisors Are Choosing a Sales Format Based on

Trade-Offs Between Compensation, Flexibility, and Risk

60%

50%

40%

25%

* ** *

Inherited book

Advisor notresponsible foroverhead or teamcosts

Broad product setand team of experts

HNW / ultra HNW

Creates a brandand marketpresence

Self-sourced clientbase

Responsible for alloverhead andbusiness risks

Advisor Compensation Structures*

2 Advisor Movement

Lead Flow / Franchise Value

Business RiskLow

Large / Valuable

High

Small / Weak

* Percentages represent portion of gross revenues generated per

advisor paid out as advisor compensation.

Source: Booz & Company

Private Bank Model

Characteristics

Independent Model

Characteristics

-

8/7/2019 US Wealth Management Survey

11/20

10

Winning in Talent Acquisition Is Key; the Battle to Win the

HNW

Client Is the Battle for the Advisor Who Owns the

Relationship

Source: Booz & Company

Upgrading the Talent Pool

Few firms are recruiting actively (and those thatare recruiting

are being very selective)

Primarily growth-oriented banks

Severe constraints on head count at most firms

Internal levers increasingly important

Focus on increasing advisor productivity

Accelerating growth in performance of youngeradvisors

Creating incentives (bonus, deferredcompensation) to encourage

long-term retention

Opportunities to hire experienced talentare increasing

More talent on the market due to layoffsat brokerage firms /

investment bank

Salary levels are normalizing

However

Many experienced advisors are lockedin by retention deals

Many have concerns about cultural /

business model mismatch if they move

2 Advisor Movement

-

8/7/2019 US Wealth Management Survey

12/20

1111

Profitability Will Remain Under Pressure and Firms Will Need

to

Continue Managing Costs Tightly

TrendsProfitability Driver Impact on Profitability

Assets Lower asset values have decreased earnings

Preference for simple, less risky, and transparent products

Mandates

Simplicity and transparency reduce clients willingness to

delegate wealth management (fewer discretionary mandates)

Regulation Increasing requirements regarding operations, IT,

reporting,

data security, regulation, etc.

Source: Booz & Company

1. Right-size thecost base

2. Upgrade organicgrowthcapabilities

3. Explore newsales formatsand business

models

HolisticAdvice

Offering integrated advisory services (e.g., insurance,financial

planning, risk management) with higher margins

Pricing Greater price sensitivity in low return environment

Pressure on management fees

Priorities

3 Pressure on Profitability

TailoredOfferings

Can be addressed via modular product architecture Complex

products will return, but with lower margins

-

8/7/2019 US Wealth Management Survey

13/20

12

Ultra HNW

HNW

Affluent

Need to Balance Revenue with Cost to Serve Is Driving

Specialization and Standardization Strategies

Source: Booz & Company

Creating New Business Models

Operations /Infrastructure

Product /Portfolio

Management

Marketing /Sales /AdviceSegment

Value Chain

StandardizationStrategies

SpecializationStrategies Depends on

segment and

focus of player

4 Business Models

Observed Models Disintegration of value chain by

segments

Focus on scale in lower segments

Specialization in upper segments

Niche players / RIAs

Focus on upper segments and advice;product specialization

Emphasize conflict-free platform; nocommissions; no product

push

Large, integrated players

Team-based sales and service

Increased cross-selling, cost synergies Separate branding (in

upper

segments) to increase credibilityStandardization

Customization

?

-

8/7/2019 US Wealth Management Survey

14/20

13

Consolidation Has Driven Scale in Bank Brokerage and the

Emergence of Integrated Institutions

Wire House / Bank Brokerage Trends and Implications

1. Combined 2009 and 2007 estimates; includes $1.4T in assets at

Merrill Lynch Global Wealth Management (2009) and ~$100B at U.S.

Trust (2007 figures; updated AUM estimates not available).

2. 2009 estimates; includes $1.1T assets at Wells Fargo Advisors

and ~$100B at Wells Fargo Private Bank and Wells Fargo Family

Wealth.

Source: Press releases; Booz & Company analysis

Bank and Wire House Consolidation

$1.2T client assets2

$1.5T client assets1

Acquirer Bank Acquired

Increasing Scale Due to Consolidation

$167B total assets

4 Business Models: Bank Brokerage

Bank ofAmerica

Merrill Lynch

Wells Fargo Wachovia

Capital OneChevy Chase

Bank

Fifth Third Bank First Charter

PNC National City

Emergence of Bankerage

Increased perception of bankssecurity in comparison to

non-bankB/Ds

Increased penetration of B/D servicesin banks retail

branches

Increased legitimacy of bank B/Dmodel, as larger retail banks

mergewith brokerage firms

Acquirer Bank Acquired

$111B total assets

$270B total assets

-

8/7/2019 US Wealth Management Survey

15/20

14

Hybrid Formats Offer Flexibility for Firms and Advisors That

Have a Mix of Fee-Based and Commission-Based Business

Hybrid Firms Operating Models

RIA OnlyB/D onlyB/D Offering

Corporate RIARIA with B/D

Affiliation

B/D SupportingCorporate RIA and

Advisor-Owned RIA

4 Business Models: Hybrids

Holdingcompany

(B/D)

B/DCorporate

RIA

B/D

Advisor-owned RIA

firm

RIA

Advisor Affiliated B/DAdvisor

Typically, firms that support advisor-

owned RIA offer corporate RIA as well

Advisor

Typically offercorporate RIA

ModelBenefit

s

Firm/A

dvisor

Regulatory

Structure

Source: Booz & Company

Firm

Broader options for advisor recruiting and

fulfillment of investor needs Highest percentage of revenues

generated

by fee business

Ability to recruit/retain advisors desiring

additional independence Higher percentage of revenues

generated

by fee business

RIA with ability to support B/D product

set and revenue model RIA with ability to recruit new

advisors

with commission business

Advisor

Flexibility to serve broad range of clientneeds

Higher level of support / lower investment

Maintenance of independent business inthe context of an

independent B/D

Higher payout, offset by higher costs andinitial investments

Ability to join or found an independentfirm while still serving

a broad range ofclient needs

-

8/7/2019 US Wealth Management Survey

16/20

15

WealthSpectrum

Mass

Affluent

UltraHNW

Team Coverage Models Dominate in the Ultra HNW Market

Competitor Map: Coverage Models

Coverage Spectrum

Advisor Team

PrivateBanks

Business Models: Private Banks

Morgan StanleySmith Barney

Merrill Lynch

Wells FargoAdvisors

UBS

Citi (PWM*)Harris

Full Service andBank Brokerage

Credit Suisse

Goldman Sachs

Morgan Stanley(PWM*)

Merrill Lynch(PBIG**)

High-EndBrokerage

Harris(myCFO)

HighTower

Bessemer Trust

J.P. MorganPrivate Bank

CitiPrivate Bank

HarrisPrivate Bank

* Private Wealth Management** Private Bank Investment Group

Source: Booz & Company

4

-

8/7/2019 US Wealth Management Survey

17/20

16

An Integrated Model Positions Wealth Managers to Serve

Entrepreneurs Better Through Wealth Creation Strategies

* Percentages represent composition of the Forbes 400, 2008.

Source: Booz & Company analysis

Sources of Ultra HNW Wealth*

Business Models: Private Banks

100%

21%

*

*

*

*

*

*

*

*

******

Entrepreneurial Wealth

Wealth Creation: The PrivateInvestment Banking Model

Broad range of private banking,commercial banking, andinvestment

banking capabilities

Team-based, multidisciplinary

sales and service coveragemodel

Referral protocols to accessproducts within a

diversifiedfinancial services firm

4

-

8/7/2019 US Wealth Management Survey

18/20

17

Conclusions

The wealth management industry is undergoing a number of

changes, from new client behaviorsand shifts in sources of

profitability to new sales formats and emerging business models

Wealth management firms can take advantage of these changes. To

capture continued growthprospects, they will need to:

Focus on client experience

Revisit market segmentation and refine their customer value

proposition by segment

Upgrade or build new capabilities (e.g., product solutions,

advice, client knowledgemanagement) to deliver customer value

-

8/7/2019 US Wealth Management Survey

19/20

18

Booz & Company is a leading global management

consultingfirm, helping the worlds top businesses, governments,

andorganizations.

Our founder, Edwin Booz, defined the profession when

heestablished the first management consulting firm in 1914.

Today, with more than 3,300 people in 61 offices around

theworld, we bring foresight and knowledge, deep

functionalexpertise, and a practical approach to building

capabilitiesand delivering real impact. We work closely with our

clientsto create and deliver essential advantage.

For our management magazine strategy+business,

visitwww.strategy-business.com.

Visit www.booz.com to learn more about Booz & Company.

2010 Booz & Company Inc.

The most recentlist of our officesand affiliates, withaddresses

andtelephone numbers,can be found onour website,www.booz.com

WorldwideOffices

AsiaBeijingDelhiHong KongMumbaiSeoulShanghaiTaipeiTokyo

Australia,New Zealand &Southeast

AsiaAdelaideAucklandBangkokBrisbaneCanberraJakartaKuala Lumpur

MelbourneSydney

EuropeAmsterdamBerlinCopenhagenDohaDublinDsseldorfFrankfurtHelsinkiIstanbulLondonMadridMilanMoscowMunichOsloParisRomeStockholmStuttgartViennaWarsawZurich

Middle EastAbu DhabiBeirutDohaCairoDubaiRiyadh

North AmericaAtlantaChicagoClevelandDallasDCDetroitFlorham

ParkHoustonLos AngelesMexico CityNew York CityParsippanySan

Francisco

South AmericaBuenos AiresRio de JaneiroSantiagoSo Paulo

-

8/7/2019 US Wealth Management Survey

20/20

19

Contact Information

New YorkJohn RolanderPartner+1-212-551-6069

[email protected]

Gauthier VincentSenior Executive

[email protected]

Chuck [email protected]

Sofia GranielloSenior

[email protected]