Embed Size (px)

Citation preview

Use of the New Markets Use of the New Markets T C dit b TT C dit b T E tE tTax Credit by TaxTax Credit by Tax--Exempt Exempt

EntitiesEntitiesMichael I. Sanders and Megan Christensen

Blank Rome LLPBlank Rome LLPSeptember 20, 2013

ABA Tax Section Exempt Organizations MeetingSan Francisco, CA

NMTC Overview:

● Opportunity to subsidize or provide gap financing in a qualified census tract.● Benefits to developers, businesses and charities.● Major investors such as Goldman Sachs● Major investors such as Goldman Sachs, US Bank, JPMorgan Chase, or PNC buy the credits and provide cash infusion to the development which may not be paid back at the end of the 7-year compliance period.

New Markets Tax Credit New Markets Tax Credit –– A Government Sponsored A Government Sponsored Joint Venture VehicleJoint Venture Vehicle

-- $36.5 billion in NMTC allocated through 2013; subject to renewal by Congress.

Purpose: The new markets tax credit (NMTC) serves as a way to provide subsidy or gap financing to real estate developments business activities or charitable operationsfinancing to real estate developments, business activities, or charitable operations planned in qualified census tracts (high poverty rate or low median family income).

What does it provide? 39% tax credit on the capital invested in a community development entity (CDE), over 7 years (5% in yrs 1-3; 6% in yrs 4-7).

Who benefits from the credit? The investor (typically national banks, insurance companies) making an investment in a CDE gets a tax credit of $0.39 for every $1 invested and CRA credit, which under a “leveraged” structure yields in excess of a 10% after-tax return. The CDE directs capital into qualified projects or businesses. The investor is not repaid its equity investmentis not repaid its equity investment.

Eligible Investments: • Community businesses, including e.g. hospitals, charter schools.• Commercial or mixed-use real estate projects (at least 20% of gross income from commercial component).

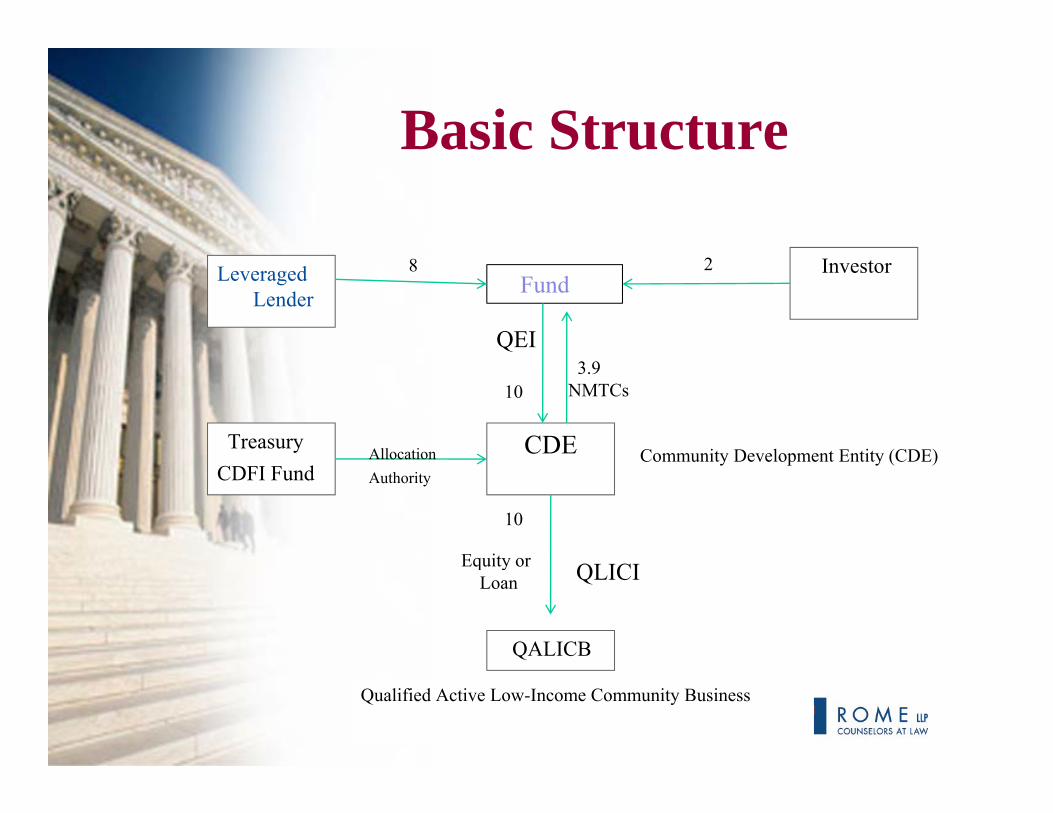

Basic Structure

Leveraged Lender Fund

Investor28

QEI

CDETreasuryAllocation

103.9

NMTCs

Community Development Entity (CDE)CDFI Fund

AllocationAuthority

Community Development Entity (CDE)

10

Equity or

QALICB

Equity or Loan QLICI

Qualified Active Low-Income Community Business

NMTC Basics - Requirements• Low-Income Community - §45D(e)

– Qualified Census Tract:P t t ≥ 20%• Poverty rate ≥ 20%; or

• Median Family Income (“MFI”) ≤ 80% of applicable area MFI.– Preferred if “severely distressed” (Poverty rate > 30%, MFI ≤ 60%

of applicable area MFI, or unemployment ≥ 1.5x national average)of applicable area MFI, or unemployment ≥ 1.5x national average) or otherwise underserved communities (15 potential criteria) (NMTC Application Q.24)

– Targeted Population (Treas. Reg. §1.45D-1(d)(9))• Qualified Business - §45D(d)(3); §1397C(d); §1.45D-1(d)(5)

– Generally any business, except no “Sin” businesses, no farming, no intangibles.

– If business is rental of real property, must have gross rental income from commercial rents ≥ 20% (i.e., < 80% residential rental income).

NMTC Basics - Allocations

• Congress authorizes Treasury to allocate the credits to entities certified as Communitycredits to entities certified as Community Development Entities (“CDEs”) (§45D(c)(1)):(§45D(c)(1)):– Partnership or corporation;– Primary mission to serve low-income y

communities/persons;– Maintain accountability to residents of low-income

iticommunities

• Competitive process through CDFI Fund to i ll tireceive an allocation.

NMTC Basics - Investor• Investor makes equity investment

(“QEI”) in CDE (§45D(b); §1 45D 1(c))( QEI ) in CDE. (§45D(b); §1.45D-1(c))

• Investor receives tax credits = 39% of i t t 7 (5% i fi t 3investment over 7 years (5% in first 3 years; 6% in last 4 years). (§45D(a); §1 45D 1(b))§1.45D-1(b))

• QEI may not be redeemed in 7–year period (§45D( )(1) (3)(C) §1 45D 1( ))period. (§45D(g)(1), (3)(C); §1.45D-1(e))

• Typically uses a leveraged structure.

NMTC Basics - CDE

• CDE receives QEI, which triggers tax di Icredit to Investor. (§45D(a); §1.45D-1(b))

• CDE uses at least 85% of QEI to make loans or equity investments (“QLICIs”) in qualified project. (§45D(b)(1)(B); §1.45D-1(c)(1) (5))1(c)(1),(5))– At least 85% of QEI must remain outstanding

for 7 years. (§45D(g)(3); §1.45D-1(c)(5)(i); §1.45D-y (§ (g)( ) § ( )( )( ) §1(e)(2)(ii))

– Only receives payments of interest or distributions of incomedistributions of income.

NMTC Basics - QALICB• Project developer = Qualified Active Low-Income

Community Business (“QALICB”). (§45D(d)(2); §1.45D-1(d)(4))

• QALICB uses proceeds of QLICIs to operate business or construct property for rent (non-residential). (§§45D(d)(3), 1397C(d), 168(e)(2); §1.45D-1(d)(5)(ii))

• Interest-only/income-only payments made. (§1.45D-1(d)(2))• 5 requirements for QALICB:

– 50% Gross Income (§45D(2)(A)(i); §1.45D-1(d)(4)(i)(A));50% Gross Income (§45D(2)(A)(i); §1.45D 1(d)(4)(i)(A));– 40% Use of Tangible Property (§45D(2)(A)(ii); §1.45D-

1(d)(4)(i)(B));– 40% Employee Services Performed (§45D(2)(A)(iii); §1.45D-p y (§ ( )( )( ); §

1(d)(4)(i)(C));– <5% Collectibles (§45D(2)(A)(iv); §1.45D-1(d)(4)(i)(D)); and– <5% Nonqualified Financial Property (§45D(2)(A)(v); §1.45D-

1(d)(4)(i)(E)).

NMTC - Recapturep• Recapture events (§45D(g);

§1 45D 1(e)):§1.45D-1(e)):– No longer CDE;

h f d i– Less than 85% of QEI used in QLICI; orQEI i d d– QEI is redeemed.

All i l l i d dit• All previously claimed credits recaptured plus interest.

Opportunities for Nonprofitspp p

A Section 501(c)(3) organization (consistent with its charitable purpose), or other nonprofit, may play various roles in NMTC transactions:● As CDE● As QALICB● As QALICB● As Leverage Lender

The Bradford

The BradfordThe Bradford• Mixed-Use, Mixed-Income• 105 Units in Bedford-Stuyvesant, Brooklyn.

– Ground floor retail of 9,700 s.f. for small businesses– 21 units: families with ≤30% AMI ($23,760 for family of 4)( , y )– 32 units: rents set at 125% AMI ($99,000 for family of 4)– 51 units: rents set at 130% AMI ($102,960 for family of 4)

• “affordable sustainable and transit-oriented• affordable, sustainable and transit-oriented development”

• Green elements– On-site co-generation plant– LEED Silver certification

The BradfordThe Bradford

• Bedford Stuyvesant Restoration• Bedford-Stuyvesant Restoration CorporationBRP D l• BRP Development

• Goldman Sachs (NMTC equity)• 2 CDEs

The BradfordCondition Prior to Closing and Demo: Fully vacant retail and under-improved residentialvacant retail and under improved residential

The BradfordThe Bradford• Work in Progress

KIPP NYC College Prep Hi h S h lHigh School

KIPP NYC College Prep High School

• School forced to move twice in 2 years andSchool forced to move twice in 2 years and lacking a permanent home.

• 125,000 s.f. school facility• Annual education of 1,000 students in grades 9-

1280% t d t f l i• 80% expected to come from low-income communities

• 245 construction jobsj• 90 permanent faculty and staff jobs• LEED Certified

KIPP NYC College Prep High School

NYC D t t f Ed ti• NYC Department of Education

• JPMorgan Chase

• Robin Hood Foundation

• Multiple CDEs

CURRENT HOT ISSUESCURRENT HOT ISSUES

• Construction Safe Harbor (NQFP)Construction Safe Harbor (NQFP)• Issuance of Tax Opinion• Planning Opportunities to Mitigate COD• Planning Opportunities to Mitigate COD

income tax consequences at exit (less of an issue for tax-exempt QALICBs)p Q )

• Exit Strategies & Use of Put-Call Options

• Workouts of Old Transactions

NMTCs & Tax-ExemptNMTCs & Tax-Exempt Entities

QUESTIONSQ

Contact UsContact Us

Blank Rome LLP600 New Hampshire Ave., NWp ,

Washington, DC 20037• Michael I. SandersMichael I. Sanders

– [email protected]– 202.772.5808

• Megan Christensen– [email protected]– 202 772 5897202.772.5897