Embed Size (px)

Citation preview

Infor ERP LN 6.1 FP3 Financials

User's Guide for Financial Integration and Reconciliation Transactions

Copyright © 2008 Infor

All rights reserved. The word and design marks set forth herein are trademarks and/or registered trademarks of Infor and/or related affiliates and subsidiaries. All rights reserved. All other trademarks listed herein are the property of their respective owners.

Important Notices

The material contained in this publication (including any supplementary information) constitutes and contains confidential and proprietary information of Infor.

By gaining access to the attached, you acknowledge and agree that the material (including any modification, translation or adaptation of the material) and all copyright, trade secrets and all other right, title and interest therein, are the sole property of Infor and that you shall not gain right, title or interest in the material (including any modification, translation or adaptation of the material) by virtue of your review thereof other than the non-exclusive right to use the material solely in connection with and the furtherance of your license and use of software made available to your company from Infor pursuant to a separate agreement (“Purpose”).

In addition, by accessing the enclosed material, you acknowledge and agree that you are required to maintain such material in strict confidence and that your use of such material is limited to the Purpose described above.

Although Infor has taken due care to ensure that the material included in this publication is accurate and complete, Infor cannot warrant that the information contained in this publication is complete, does not contain typographical or other errors, or will meet your specific requirements. As such, Infor does not assume and hereby disclaims all liability, consequential or otherwise, for any loss or damage to any person or entity which is caused by or relates to errors or omissions in this publication (including any supplementary information), whether such errors or omissions result from negligence, accident or any other cause.

Trademark Acknowledgements

All other company, product, trade or service names referenced may be registered trademarks or trademarks of their respective owners.

Publication Information

Document code: U8967B US

Release: Infor ERP LN 6.1 FP3 Financials

Publication date: July 2008

Table of Contents

Chapter 1 Introduction............................................................................................................. 1-1 Purpose...................................................................................................................................... 1-1 Scope......................................................................................................................................... 1-1 Acronyms ................................................................................................................................... 1-2

Chapter 2 General Information................................................................................................ 2-1 Data used for the examples ....................................................................................................... 2-1

Chapter 3 Purchase Order ....................................................................................................... 3-1 Economic Transactions.............................................................................................................. 3-1

Purchased/Tool/Cost/Service Items and Warehouse........................................................... 3-2 List/manufactured items and warehouse ............................................................................. 3-3 Project / Project Warehouse ................................................................................................ 3-4 No Warehouse/Project ......................................................................................................... 3-4 Return orders ....................................................................................................................... 3-5 Receipts............................................................................................................................... 3-5

Receipts ..................................................................................................................................... 3-5 Purchased item in warehouse.............................................................................................. 3-5 List/manufactured item in warehouse .................................................................................. 3-7 Consignment replenishment ................................................................................................ 3-8 Project.................................................................................................................................. 3-8 Direct delivery for Sales or Service ...................................................................................... 3-9 Production subcontracting ................................................................................................. 3-10 Service subcontracting....................................................................................................... 3-11 Maintenance work subcontracting...................................................................................... 3-12 Assembly ........................................................................................................................... 3-12

ii | Table of Contents

Cost/service/subcontracting/equipment/tool item............................................................... 3-13 Return orders ........................................................................................................................... 3-15

Purchased item from warehouse ....................................................................................... 3-15 List/manufactured item from warehouse ............................................................................ 3-17 Consignment replenishment .............................................................................................. 3-19 Other scenarios.................................................................................................................. 3-19

Rejections in warehouse .......................................................................................................... 3-20 Purchased Item.................................................................................................................. 3-20 List/manufactured item....................................................................................................... 3-22 Consignment replenishment .............................................................................................. 3-22

Receipt correction .................................................................................................................... 3-23 Purchased item.................................................................................................................. 3-23 List/manufactured item....................................................................................................... 3-25 Other scenarios.................................................................................................................. 3-25

Consignment use ..................................................................................................................... 3-25 Invoice Approval/Change Price after Receipt........................................................................... 3-26

Approval / Unapproval ....................................................................................................... 3-26 Expensed tax ..................................................................................................................... 3-27 Purchased/List/Manufactured Item and Warehouse .......................................................... 3-28 Project................................................................................................................................ 3-28 Direct delivery for Sales ..................................................................................................... 3-29 Direct delivery for Service .................................................................................................. 3-35 Production subcontracting ................................................................................................. 3-37 Service subcontracting....................................................................................................... 3-38 Maintenance work subcontracting...................................................................................... 3-39 Assembly ........................................................................................................................... 3-41 Cost/Service/Subcontracting/Equipment/Tool Item............................................................ 3-41

Internal invoices (triangular invoicing direct delivery) ............................................................... 3-43 Sales order......................................................................................................................... 3-43 Service order...................................................................................................................... 3-45

Chapter 4 Purchase Schedule................................................................................................. 4-1 Economic transactions ............................................................................................................... 4-2

Table of Contents | iii

Purchased/manufactured/cost/service items and warehouse .............................................. 4-2 No warehouse...................................................................................................................... 4-3 Receipts............................................................................................................................... 4-3

Receipts ..................................................................................................................................... 4-4 Purchased/manufactured item ............................................................................................. 4-4 Consignment replenishment ................................................................................................ 4-5 Cost/service item ................................................................................................................. 4-6

Rejections in warehouse ............................................................................................................ 4-7 Purchased/manufactured item ............................................................................................. 4-7 Consignment replenishment ................................................................................................ 4-8

Receipt correction ...................................................................................................................... 4-9 Purchased/manufactured item ............................................................................................. 4-9 Consignment replenishment .............................................................................................. 4-10 Consignment use ............................................................................................................... 4-10

Invoice approval ....................................................................................................................... 4-11 Approval / unapproval ........................................................................................................ 4-12 Expensed tax ..................................................................................................................... 4-12 Purchased/Manufactured Item........................................................................................... 4-13 Cost/service item ............................................................................................................... 4-13

Chapter 5 Purchase Contract .................................................................................................. 5-1

Chapter 6 Sales Order.............................................................................................................. 6-1 Economic transactions ............................................................................................................... 6-1

Purchased/Cost/Service Items and Warehouse................................................................... 6-2 List/manufactured items and warehouse ............................................................................. 6-3 No warehouse...................................................................................................................... 6-4 Return orders ....................................................................................................................... 6-4 Issues .................................................................................................................................. 6-4

Issues......................................................................................................................................... 6-5 Purchased item from warehouse ......................................................................................... 6-5 List/manufactured item from warehouse .............................................................................. 6-7 Consignment........................................................................................................................ 6-9

iv | Table of Contents

Direct delivery .................................................................................................................... 6-10 Generic items..................................................................................................................... 6-12 Cost/service/subcontracting/equipment item...................................................................... 6-14

Return orders ........................................................................................................................... 6-16 Purchased item in warehouse............................................................................................ 6-16 List/manufactured item in warehouse ................................................................................ 6-22 Consignment...................................................................................................................... 6-22 Rejected goods .................................................................................................................. 6-23 Other scenarios.................................................................................................................. 6-30

Customer invoices.................................................................................................................... 6-31 Orders related to Issues..................................................................................................... 6-31 Retro billing ........................................................................................................................ 6-32

Internal Invoices....................................................................................................................... 6-32 Purchased/Manufactured/List Item in Warehouse ............................................................. 6-32 Cost/service item in warehouse ......................................................................................... 6-34 Work center........................................................................................................................ 6-35 Direct delivery .................................................................................................................... 6-37

Purchase invoice approval/change price after receipt.............................................................. 6-37 Installment orders..................................................................................................................... 6-38

Advance Installment........................................................................................................... 6-38 Normal Installment ............................................................................................................. 6-39 Goods Invoice .................................................................................................................... 6-39 Settled Guarantee Installment............................................................................................ 6-40

Commissions ........................................................................................................................... 6-41 Rebates.................................................................................................................................... 6-41

Chapter 7 Sales Schedule........................................................................................................ 7-1 Economic transactions ............................................................................................................... 7-1

Purchased/manufactured/cost/service items and warehouse .............................................. 7-2 No warehouse...................................................................................................................... 7-3 Issues .................................................................................................................................. 7-3

Issues......................................................................................................................................... 7-3 Purchased/manufactured item ............................................................................................. 7-3

Table of Contents | v

Cost/service item ................................................................................................................. 7-5 Shipment variances.................................................................................................................... 7-5 Customer invoices...................................................................................................................... 7-6 Internal invoices ......................................................................................................................... 7-7

Purchased/manufactured item ............................................................................................. 7-7 Cost/service item ................................................................................................................. 7-8

Commissions ........................................................................................................................... 7-10 Rebates.................................................................................................................................... 7-10

Chapter 8 Sales Contract......................................................................................................... 8-1

Chapter 9 People ...................................................................................................................... 9-1 Hours ......................................................................................................................................... 9-1

General ................................................................................................................................ 9-1 TP Project ............................................................................................................................ 9-2 PCS Project ......................................................................................................................... 9-2 Production............................................................................................................................ 9-3 Assembly ............................................................................................................................. 9-4 Service................................................................................................................................. 9-5 Maintenance Work ............................................................................................................... 9-6

Expenses ................................................................................................................................... 9-7 General ................................................................................................................................ 9-7 TP Project ............................................................................................................................ 9-7

Chapter 10 Production Order .................................................................................................. 10-1 Materials .................................................................................................................................. 10-1

Issue .................................................................................................................................. 10-1 Return ................................................................................................................................ 10-3

Co-products/By-products ......................................................................................................... 10-7 Receipt............................................................................................................................... 10-7 Return ................................................................................................................................ 10-8

Subcontracting ......................................................................................................................... 10-9 Operation costs........................................................................................................................ 10-9 WIP transfers ........................................................................................................................... 10-9

vi | Table of Contents

Issue ................................................................................................................................ 10-10 Receipt............................................................................................................................. 10-11 Internal invoice................................................................................................................. 10-11

Item surcharge receipt ........................................................................................................... 10-12 Completion............................................................................................................................. 10-13 End items ............................................................................................................................... 10-13

Receipt............................................................................................................................. 10-13 Return .............................................................................................................................. 10-15 Variances......................................................................................................................... 10-16

Chapter 11 Assembly............................................................................................................... 11-1 Materials .................................................................................................................................. 11-1

Issue .................................................................................................................................. 11-1 Return ................................................................................................................................ 11-2

Purchase.................................................................................................................................. 11-6 Operation costs........................................................................................................................ 11-6 WIP transfers ........................................................................................................................... 11-6

Issue .................................................................................................................................. 11-7 Receipt............................................................................................................................... 11-7 Internal invoice................................................................................................................... 11-9

Closing ................................................................................................................................... 11-10 Assembly line................................................................................................................... 11-10 Assembly order ................................................................................................................ 11-11

Issue generic item.................................................................................................................. 11-11

Chapter 12 Maintenance Work Order ..................................................................................... 12-1 Receipt of to be maintained item.............................................................................................. 12-1

No batch repair .................................................................................................................. 12-1 Batch repair........................................................................................................................ 12-3

Material resource lines ............................................................................................................. 12-5 From warehouse ................................................................................................................ 12-5 From Kit ............................................................................................................................. 12-7 Via Purchase...................................................................................................................... 12-7

Table of Contents | vii

To Warehouse ................................................................................................................... 12-7 Location ............................................................................................................................. 12-8 Follow-Up Work Order ....................................................................................................... 12-9 To Scrap ............................................................................................................................ 12-9 From Service Stock............................................................................................................ 12-9 Subcontracting Requirement.............................................................................................. 12-9 Batch repair........................................................................................................................ 12-9

Hour lines................................................................................................................................. 12-9 Other resource lines............................................................................................................... 12-10

Subcontracting ................................................................................................................. 12-10 Tool costs......................................................................................................................... 12-10 General costs................................................................................................................... 12-10 General costs (through Financials) .................................................................................. 12-11

Closing ................................................................................................................................... 12-11 Header (to be maintained item)........................................................................................ 12-11 Material resource lines..................................................................................................... 12-13 Hour Lines........................................................................................................................ 12-17 Other resource lines......................................................................................................... 12-18

Returns .................................................................................................................................. 12-21 Header (to be maintained item)........................................................................................ 12-21 Material resource lines..................................................................................................... 12-24

Chapter 13 Maintenance Sales Order ..................................................................................... 13-1 Part maintenance lines............................................................................................................. 13-1 Part delivery lines..................................................................................................................... 13-2 Part receipt lines ...................................................................................................................... 13-3 Part loan lines .......................................................................................................................... 13-4 General costs........................................................................................................................... 13-7 Freight costs ............................................................................................................................ 13-8 Costing coverage lines............................................................................................................. 13-8 Customer invoices.................................................................................................................. 13-10 Internal invoices ..................................................................................................................... 13-10

viii | Table of Contents

Chapter 14 Service Order ........................................................................................................ 14-1 Material lines............................................................................................................................ 14-1

From Warehouse ............................................................................................................... 14-1 From Warehouse in Car..................................................................................................... 14-2 From Warehouse by Transport .......................................................................................... 14-2 From Service Kit ................................................................................................................ 14-3 From Service Stock............................................................................................................ 14-3 By Purchase Order ............................................................................................................ 14-3 By Field Purchase.............................................................................................................. 14-3 Supplier Direct Delivery ..................................................................................................... 14-4 Supplier Direct Return........................................................................................................ 14-5 To Scrap ............................................................................................................................ 14-8 To Warehouse ................................................................................................................... 14-9 To Warehouse by Transport ............................................................................................ 14-14

Labor lines ............................................................................................................................. 14-14 Other lines.............................................................................................................................. 14-14

Subcontracting ................................................................................................................. 14-14 Tooling ............................................................................................................................. 14-15 Help Desk/ Other ............................................................................................................. 14-15 Travel ............................................................................................................................... 14-15 General costs (through Financials) .................................................................................. 14-15 Freight.............................................................................................................................. 14-16

Costing Service Order Lines .................................................................................................. 14-16 External service order (linked to business partner) .......................................................... 14-16 Internal service order (not linked to Project [TP]) ............................................................. 14-18 Internal service order (linked to Project [TP]) ................................................................... 14-18

Customer invoices.................................................................................................................. 14-18 Internal invoices ..................................................................................................................... 14-19

Warehouse....................................................................................................................... 14-19 Direct Delivery.................................................................................................................. 14-21

Chapter 15 Service Call............................................................................................................ 15-1 General costs........................................................................................................................... 15-1

Table of Contents | ix

Create invoice (costing) ........................................................................................................... 15-1 Customer invoices.................................................................................................................... 15-2

Chapter 16 Service Contract ................................................................................................... 16-1 Actual costs.............................................................................................................................. 16-1 Customer invoices.................................................................................................................... 16-1 Revenues recognition .............................................................................................................. 16-2 Close contract .......................................................................................................................... 16-3

Chapter 17 Warehousing ......................................................................................................... 17-1 Cycle counting ......................................................................................................................... 17-1

Positive quantity................................................................................................................. 17-1 Negative quantity ............................................................................................................... 17-2

Adjustment ............................................................................................................................... 17-3 Positive quantity................................................................................................................. 17-3 Negative quantity ............................................................................................................... 17-4

Issue from warehouse.............................................................................................................. 17-6 Sales order......................................................................................................................... 17-6 Sales schedule................................................................................................................... 17-6 Sales order (manual) ......................................................................................................... 17-6 Service order...................................................................................................................... 17-7 Service order (manual) ...................................................................................................... 17-7 Maintenance sales order.................................................................................................... 17-9 Maintenance sales order (manual)..................................................................................... 17-9 Maintenance work order .................................................................................................... 17-9 Maintenance work order (manual) ..................................................................................... 17-9 SFC production order....................................................................................................... 17-10 SFC production order (manual)........................................................................................ 17-10 ASC production order ...................................................................................................... 17-10 ASC production order (manual) ....................................................................................... 17-10 Production Kanban order ................................................................................................. 17-11 Transfer order / transfer order (manual) / EP distribution order ....................................... 17-11 Project order / project order (manual) .............................................................................. 17-11

x | Table of Contents

Purchase Order................................................................................................................ 17-13 Purchase order (manual) ................................................................................................. 17-13 Warehousing assembly order .......................................................................................... 17-14

Receipt in warehouse............................................................................................................. 17-14 Sales order....................................................................................................................... 17-14 Sales order (manual) ....................................................................................................... 17-15 Service order.................................................................................................................... 17-16 Service order (manual) .................................................................................................... 17-16 Maintenance sales order.................................................................................................. 17-18 Maintenance sales order (manual)................................................................................... 17-18 Maintenance work order .................................................................................................. 17-18 Maintenance work order (manual) ................................................................................... 17-18 SFC production order....................................................................................................... 17-19 SFC production order (manual)........................................................................................ 17-19 ASC production order ...................................................................................................... 17-19 ASC production order (manual) ....................................................................................... 17-19 Production Kanban order ................................................................................................. 17-20 Transfer order / transfer order (manual) / EP distribution order ....................................... 17-20 Project order / project order (manual) .............................................................................. 17-20 Purchase order ................................................................................................................ 17-22 Purchase schedule .......................................................................................................... 17-22 Purchase order (manual) ................................................................................................. 17-22 Warehousing assembly order .......................................................................................... 17-23

Receipt correction .................................................................................................................. 17-23 Inspections............................................................................................................................. 17-23

Rejection purchase order ................................................................................................. 17-23 Rejection purchase schedule ........................................................................................... 17-24 Rejection purchase order (manual).................................................................................. 17-24 Destroying or rejection for other order origins .................................................................. 17-26

Consignment use ................................................................................................................... 17-27 Purchase order ................................................................................................................ 17-27 Purchase schedule .......................................................................................................... 17-27

Table of Contents | xi

Purchase order (manual) ................................................................................................. 17-27 Transfers................................................................................................................................ 17-28

Warehouse transfer – no invoice relation......................................................................... 17-28 Warehouse transfer – invoice relation.............................................................................. 17-34 Floor Stock Item to Shop Floor Warehouse ..................................................................... 17-37 Item transfer..................................................................................................................... 17-38

Warehousing assembly order ................................................................................................ 17-39 Materials .......................................................................................................................... 17-39 End Items......................................................................................................................... 17-40

Internal invoices ..................................................................................................................... 17-41 Bilateral (between two warehouses) ................................................................................ 17-41 Triangular (between warehouse and department) ........................................................... 17-44

Inventory variances................................................................................................................ 17-44 Receipt - purchased item ................................................................................................. 17-44 Receipt - list/manufactured item....................................................................................... 17-46 Receipt - project warehouse ............................................................................................ 17-47 Return - purchased item .................................................................................................. 17-49 Return - list/manufactured item........................................................................................ 17-49 Return – project warehouse............................................................................................. 17-50 Zero quantity .................................................................................................................... 17-50

Revaluation ............................................................................................................................ 17-51 Actualize cost price .......................................................................................................... 17-51 Change valuation method ................................................................................................ 17-52 MAUC correction / actual costs correction ....................................................................... 17-52 Antedating........................................................................................................................ 17-53

Chapter 18 Freight.................................................................................................................... 18-1 Load Planning .......................................................................................................................... 18-1

Complete shipment ............................................................................................................ 18-1 Change estimated costs .................................................................................................... 18-4 Actual Costs....................................................................................................................... 18-9

Freight Order Clusters............................................................................................................ 18-12 Complete cluster line ....................................................................................................... 18-13

xii | Table of Contents

Change estimated costs .................................................................................................. 18-14 Actual Costs..................................................................................................................... 18-15

Freight Order Invoicing........................................................................................................... 18-16 External invoicing by Freight ............................................................................................ 18-16 Costing and External invoicing by Service ....................................................................... 18-17 Internal invoicing .............................................................................................................. 18-17

Chapter 19 Project (TP)............................................................................................................ 19-1 Commitments........................................................................................................................... 19-1

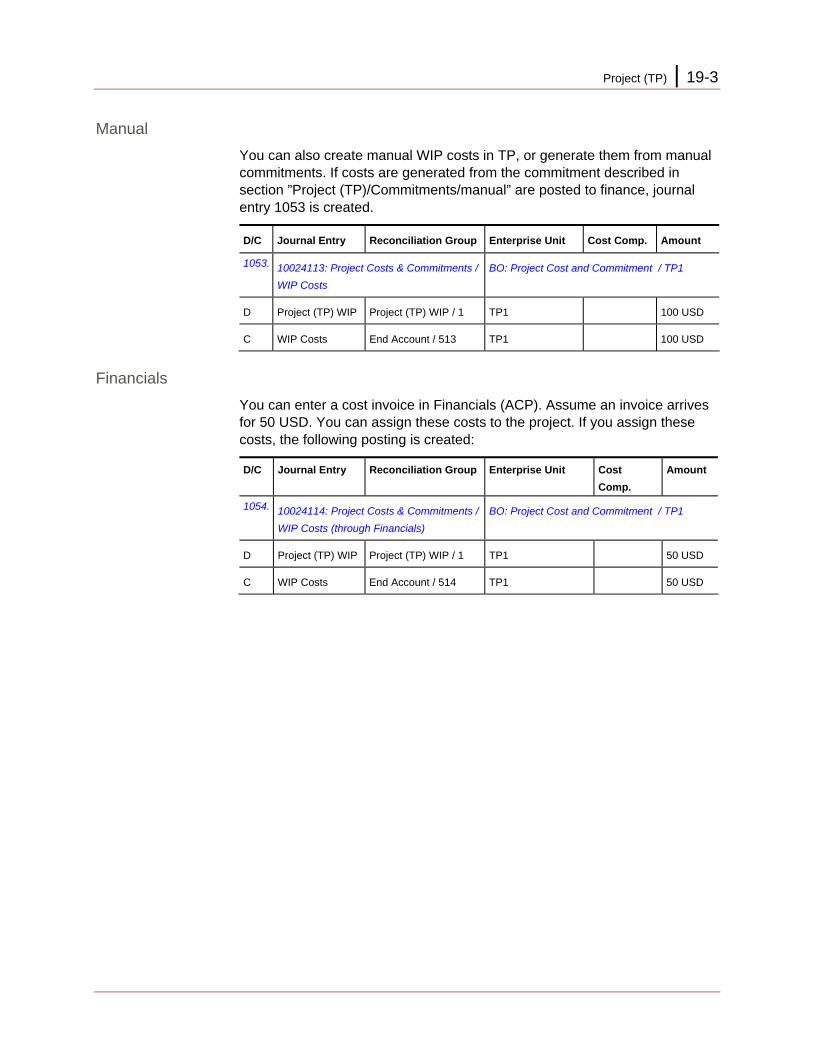

Purchase order .................................................................................................................. 19-1 Purchase schedule ............................................................................................................ 19-1 Manual ............................................................................................................................... 19-1

Costs........................................................................................................................................ 19-2 Direct receipt (purchase).................................................................................................... 19-2 Receipt (warehousing) ....................................................................................................... 19-2 Purchase price variance .................................................................................................... 19-2 Transfer from service ......................................................................................................... 19-2 People................................................................................................................................ 19-2 Manual ............................................................................................................................... 19-3 Financials........................................................................................................................... 19-3

Revenues................................................................................................................................. 19-4 Central invoicing ................................................................................................................ 19-4 Manual ............................................................................................................................... 19-5 Financials........................................................................................................................... 19-6

Interim Results ......................................................................................................................... 19-6 Completion............................................................................................................................... 19-7

Chapter 20 Project (PCS) ......................................................................................................... 20-1 Costs........................................................................................................................................ 20-1

General costs..................................................................................................................... 20-1 General costs (through financials) ..................................................................................... 20-1 General hours .................................................................................................................... 20-2 Project surcharge............................................................................................................... 20-2

Table of Contents | xiii

Other costs......................................................................................................................... 20-2 Revenues................................................................................................................................. 20-3 Revenues recognition .............................................................................................................. 20-3 Close project ............................................................................................................................ 20-4

Post against actual costs ................................................................................................... 20-4 Post against estimated costs ............................................................................................. 20-7

Internal Invoice....................................................................................................................... 20-10

Chapter 21 Central Invoicing................................................................................................... 21-1 Manual sales invoice................................................................................................................ 21-1 Interest invoice......................................................................................................................... 21-1 Invoice from operations management ...................................................................................... 21-2

External.............................................................................................................................. 21-2 Internal ............................................................................................................................... 21-2

Reconciliation interim revenues ............................................................................................... 21-3

Chapter 22 Currency Differences............................................................................................ 22-1 Automatically............................................................................................................................ 22-1 Manually................................................................................................................................... 22-3 Not ........................................................................................................................................... 22-4

Chapter 23 Reconciliation Transactions ................................................................................ 23-1 Integration transaction, reversal, and integration transaction (reversed).................................. 23-1 Approval / unapproval .............................................................................................................. 23-2 Expensed tax ........................................................................................................................... 23-3 Cost transaction ....................................................................................................................... 23-3 Sales invoice............................................................................................................................ 23-3 Advance (Accounts Receivable) .............................................................................................. 23-3 Currency difference.................................................................................................................. 23-3 Opening balance...................................................................................................................... 23-4 Correction (not final)/rounding correction (not final)/correction (final)/rounding difference....... 23-4

Enter corrections manually................................................................................................. 23-4 Post manually entered corrections..................................................................................... 23-5 Calculate rounding currency differences............................................................................ 23-6

xiv | Table of Contents

About this Guide

This document is up to date for SSA ERP LN 6.1 FP3. As a result, all integration transactions and reconciliation transactions are based on FP3. Many of the integration transactions are the same as the integration transactions and reconciliation transactions of earlier versions of SSA ERP LN 6.1, however, with numerous differences as well. For this reason, for earlier versions, use this document with caution.

Chapter 1, “Introduction,” describes the implications for reconciliation.

Chapter 2, “General Information,” provides a general overview of transactions and reconciliation transactions in SSA ERP LN 6.1 FP22. This chapter also describes the data used for the examples in this document.

Chapters 3 through 23 describe the integration transactions and reconciliation transactions.

Send us your comments

We continually review and improve our documentation. Any remarks/requests for information concerning this document or topic are appreciated. Please e-mail your comments to [email protected].

In your e-mail, refer to the document code and title. More specific information will enable us to process feedback efficiently.

xvi | Table of Contents

1 Chapter 1 Introduction

Purpose

This document describes the available integration transactions and reconciliation transactions in SSA ERP LN 6.1 FP3 and provides numerous examples to illustrate the transaction flow.

Scope

This document describes all the integration transactions that originate from Operations Management. In addition, this document also describes some integration transactions that come from Central Invoicing and Financials. For these integration transactions, this chapter describes the implications for reconciliation. In addition, this document describes all specific reconciliation transactions that are not integration transactions.

Note: This document does not describe integration transactions for procurement card purchases, Fixed Asset Management, dimension accounting from Central Invoicing, or disposal from Central Invoicing.

1-2 | Introduction

Acronyms

Term Description

ASC Assembly Control

BO Business Object

C Credit

D Debit

FIFO First In First Out

FITR Financial Transaction

FTP Fixed Transfer Price

IDT Integration Document Type

LIFO Last in First Out

LOT Lot Price

MAUC Moving Average Unit Cost

OM ERP Operations Management

PCS PCS Project (Manufacturing)

SFC Shop Floor Control

TF ERP Financials

TP ERP Project

TROR Transaction Origin

WIP Work in Process

2 Chapter 2 General Information

Data used for the examples

The following data is used in the examples:

Normal Warehouse: NWH1

Normal Warehouse: NWH2

Project Warehouse: PWH1

Consignment Owned Warehouse: COWH1

Shop Floor Warehouse: SFCWH1

TP Project: TP1

PCS Project: PCS1

PCS Calculation Office: PCO1

PCS Cost Component: GEN

Purchase Office: PO1

Purchase Office: PO2

If the Use Tax Number of other Financial Companies check box in the Tax Parameters (tctax0100m000) session is selected, for purchase orders, the purchase office used in the integration transactions can also be an accounting office.

2-2 | General Information

Sales Office: SO1

If the Use Tax Number of other Financial Companies check box in the Tax Parameters (tctax0100m000) session is selected, for sales orders, the sales office used in the integration transactions can also be an accounting office.

SFC Calculation Office: SCO1

Work center: WC1

Work center: WC2

Assembly Line: AL1

Surcharge SUR on assembly line AL1: 10%

Assembly Line: AL2

Line Station: LS1

Line Station: LS2

ASC Calculation Office: ASC1

Service Department: SD1

Service Department: SD2

If the Use Tax Number of other Financial Companies check box in the Tax Parameters (tctax0100m000) session is selected, for service orders, the service department used in the integration transactions can also be an accounting office.

Purchased Item: PI1

Purchase Price 100 USD

Sales Price 200 USD

Item Receipt Surcharge (IRS) of 10%

Warehouse Receipt Surcharge (WRS) of 3 USD for warehouse NWH1

Item Issue Surcharge (IIS) of 20%

Warehouse Issue Surcharge (WIS) of 5 USD for warehouse NWH1

Effective Cost Components:

MAT: aggregated material

OPR: aggregated operational

General Information | 2-3

SUR: aggregated surcharge

WRS: detailed surcharge

Valuation prices, in this case, are:

Receipt 100 (MAT) + 10 (SUR)

Receipt in NWH1 100 (MAT) + 10 (SUR) + 3 (WRS)

Issue 100 (MAT) + 32 (SUR)

Issue from NWH1 100 (MAT) + 37.6 (SUR) + 3 (WRS)

Customized Purchased Item: PCS1 PI1

See data of item PI1

Purchased Item: PI2

Purchase Price 50 USD

Sales Price 150 USD

Effective cost components:

MAT: aggregated material

OPR: aggregated operational

SUR: aggregated surcharge

Manufactured Item: MI1

BOM: Three pieces of PI1 and two pieces of PI2

Item Receipt Surcharge (IRS) of 10 percent

Warehouse Receipt Surcharge (WRS) of 3 USD for warehouse NWH1

Item Issue Surcharge (IIS) of 20 percent

Warehouse Issue Surcharge (WIS) of 5 USD for warehouse NWH1

One hour labor of 20 USD

Effective Cost Components:

MAT: aggregated material

OPR: aggregated operational

SUR: aggregated surcharge

Valuation Prices, in this case, are:

Receipt 400 (MAT) + 20 (OPR) + 147.6 (SUR), if components are not issued from NWH1

Receipt in NWH1 400 (MAT) + 20 (OPR) + 178.98 (SUR), if components are also issued from NWH1

2-4 | General Information

Issue 400 (MAT) + 20 (OPR) + 261.12 (SUR)

Issue from NWH1 400 (MAT) + 20 (OPR) + 303.78 (SUR)

Manufactured Item: MI2

BOM: Two pieces of PI1 and five pieces of PI2

One hour labor of 20 USD

Effective Cost Components:

MAT: aggregated material

OPR: aggregated operational

SUR: aggregated surcharge

Valuation Prices, in this case, are:

Receipt 50 (MAT) + 20 (OPR) - 64 (SUR), if components are not issued from/received in NWH1

Receipt in NWH1 50 (MAT) + 20 (OPR) – 91.2 (SUR), if components are also issue from/received in NWH1

List Item: LI1

Purchase Price 200 USD

Sales Price 500 USD

Consists of three pieces of PI1 and two pieces of PI2

Effective cost component: 100 (from general item data)

Cost Item: CI1

Cost to be Specified has value Yes on the item group

Cost Price is 50 USD

Effective cost component: GEN (aggregated material, type general)

Cost Item: CI2

The Cost to Be Specified parameter has the value No on the item group

Cost Price is 50 USD

Effective cost component: GEN (aggregated material, type general)

Subcontracting Item: SI1

Subcontracting cost component SFC: SUB

Generic Item: GI1 (order system FAS)

Option Based Item Price: 100 USD

General Information | 2-5

Item Receipt Surcharge (IRS) of 10 percent

Item Issue Surcharge (IIS) of 20 percent

Effective cost components:

MAT: aggregated material

OPR: aggregated operational

SUR: aggregated surcharge

Employee: EMP1

Employee Department: ED1

3 Chapter 3 Purchase Order

Economic Transactions

If a purchase order line is approved, you can create integration transactions on the purchase order line. This depends on the value of the purchase parameter Create Financial Economic Stock Transactions.

This parameter can have the following values:

No: No integration transactions are created.

Order Price: Order price is used.

Valuation Price: Valuation price is used.

The parameter value is ignored, for example, in the following situations:

For a consignment replenishment order, or for a consignment payment order, no economic integration transactions are created.

For an equipment item, a subcontracting item or a generic item the order price is also used if the parameter has the value Valuation Price.

For a purchase order of type return rejected goods, no economic integration transactions are created.

3-2 | Purchase Order

Purchased/Tool/Cost/Service Items and Warehouse

Example: Order line for purchase order PUR000001 of two pieces of item PI1 for warehouse NWH1.

The parameter has the value Order Price and the price on the order line is 110 USD.

The following postings are created:

D/C Journal Entry Reconciliation Group

Enterprise Unit

Cost Comp. Amount

1. 10001060: Purchase Order / On Order BO: Purchase Order / PUR000001

D Goods to be Received Commitments / 1 NWH1 MAT 220 USD

C Purchase On Order Commitments / 2 PO1 MAT 220 USD

The parameter has the value Valuation Price.

The following postings are created:

D/C Journal Entry Reconciliation Group

Enterprise Unit

Cost Comp. Amount

2. 10001060: Purchase Order / On Order BO: Purchase Order / PUR000001

D Goods to be Received Commitments / 1 NWH1 MAT 200 USD

C Purchase On Order Commitments / 2 PO1 MAT 200 USD

3. 10001060: Purchase Order / On Order BO: Purchase Order / PUR000001

D Goods to be Received Commitments / 1 NWH1 SUR 20 USD

C Purchase On Order Commitments / 2 PO1 SUR 20 USD

4. 10001060: Purchase Order / On Order BO: Purchase Order / PUR000001

D Goods to be Received Commitments / 1 NWH1 WRS 6 USD

C Purchase On Order Commitments / 2 PO1 WRS 6 USD For tool items, the same postings are created.

For cost items and service items, the same postings are created. Surcharges are not applicable for those items. Therefore, if the parameter has the value Valuation Price, only journal entry 2 is created, with the effective cost component of the cost item or service item.

Purchase Order | 3-3

List/manufactured items and warehouse

Example: The order line for purchase order PUR000002 of two pieces of item LI1 for warehouse NWH1.

The parameter has the value Order Price and the price on the order line is 450 USD.

The following postings are created.

D/C Journal Entry Reconciliation Group

Enterprise Unit

Cost Comp. Amount

5. 10001060: Purchase Order / On Order BO: Purchase Order / PUR000002

D Goods to be Received Commitments / 1 NWH1 100 900 USD

C Purchase On Order Commitments / 2 PO1 100 900 USD

The parameter has the value Valuation Price

In this case, economic transactions are created for the components. List item LI1 consists of three items PI1 and two items PI2. Therefore, if two pieces of item LI1 are bought, this implies six items PI1 and four items PI2.

D/C Journal Entry Reconciliation Group

Enterprise Unit

Cost Comp. Amount

6. 10001060: Purchase Order / On Order BO: Purchase Order / PUR000002

D Goods to be Received Commitments / 1 NWH1 MAT 600 USD

C Purchase On Order Commitments / 2 PO1 MAT 600 USD

7. 10001060: Purchase Order / On Order BO: Purchase Order / PUR000002

D Goods to be Received Commitments / 1 NWH1 SUR 60 USD

C Purchase On Order Commitments / 2 PO1 SUR 60 USD

8. 10001060: Purchase Order / On Order BO: Purchase Order / PUR000002

D Goods to be Received Commitments / 1 NWH1 WRS 18 USD

C Purchase On Order Commitments / 2 PO1 WRS 18 USD

9. 10001060: Purchase Order / On Order BO: Purchase Order / PUR000002

D Goods to be Received Commitments / 1 NWH1 MAT 200 USD

C Purchase On Order Commitments / 2 PO1 MAT 200 USD

Journal entries 6, 7, and 8 are for item PI1, journal entry 9 is for item PI2.

3-4 | Purchase Order

Project / Project Warehouse

Example: order line for purchase order PUR000003 of two pieces of item PI1 for project TP1 of 110 USD each.

In this case, no integration transaction with Purchase Order/On Order is written. Instead of this, a record is written in the financial tables in TP. In TP, this record must be approved and posted. At the moment of posting from TP, a journal entry is created. This journal entry is always against order price:

D/C Journal Entry Reconciliation Group

Enterprise Unit

Cost Comp. Amount

10. 100024060: Project Costs & Commitments / On Order

BO: Project Cost and Commitment / TP1

D Project Soft Commitments

Commitments / 15 TP1 220 USD

C Purchase On Order Commitments / 16 TP1 220 USD

The same journal entry is created when the order is for a delivery to a project warehouse (PWH1).

No Warehouse/Project

In some cases, no warehouse or project is filled on the purchase order line, for example, direct delivery, subcontracting, or receipt of cost and service items without warehouse. In this case, journal entries are equal to the journal entries 1 through 4, with the difference that for the debit side of the transaction, the enterprise unit of the purchase office is used.

Example: Purchase order line for purchase order PUR000004 is a direct delivery for two pieces of item PI1. The value of the parameter is Order Price. The order price is 110 USD.

D/C Journal Entry Reconciliation Group

Enterprise Unit

Cost Comp. Amount

11. 10001060: Purchase Order / On Order BO: Purchase Order / PUR000004

D Goods to be Received Commitments / 1 PO1 MAT 220 USD

C Purchase On Order Commitments / 2 PO1 MAT 220 USD

Purchase Order | 3-5

Return orders

For return orders, journal entries 1 through11 are also created, with the difference that the amounts are negative.

Receipts

When the receipt is made for the order line, or when the issue is made for a return order, journal entries 1 through11 are also are reversed. As a result, the same journal entries are created, but with a negative amount, or with a positive amount for return orders.

Therefore, after receipt, the balance on the ledger accounts for Commitments / 1, Commitments / 2, Commitments / 15, and Commitments / 16 is 0 (zero) USD again. For a partially receipt, a reversal is also made for the full quantity. For the non-received part, new economic transactions are created for the remaining quantity.

Receipts

Purchased item in warehouse

Standard items

Example: Receipt of order line for purchase order PUR000001 of two pieces of item PI1 for warehouse NWH1. The order price is 110 USD each. Inventory transaction ID IT0000001 is created during receipt.

D/C Journal Entry Reconciliation Group

Enterprise Unit

Cost Comp. Amount

12. 10001074: Purchase Order / Receipt BO: Purchase Order / PUR000001

D Interim Transit Interim Transit / 1 NWH1 220 USD

C Invoice Accrual Invoice Accrual / 3 PO1 220 USD

13. 10061074: Warehouse Receipt / Receipt BO: Inventory Transaction / IT0000001

D Inventory Inventory / 1 NWH1 MAT 220 USD

C Interim Transit Interim Transit / 1 NWH1 220 USD

14. 10061056: Warehouse Receipt / Item Surcharge Receipt

BO: Inventory Transaction / IT0000001

D Inventory Inventory / 1 NWH1 SUR 22 USD

3-6 | Purchase Order

C Surcharge Cover End Account / 732 NWH1 IRS 22 USD

15. 10061121: Warehouse Receipt / Warehouse Surcharge Receipt

BO: Inventory Transaction / IT0000001

D Inventory Inventory / 1 NWH1 WRS 6 USD

C Surcharge Cover End Account / 737 NWH1 WRS 6 USD

If the valuation method of item PI1 in warehouse NWH1 is FTP, the following postings are also created:

D/C Journal Entry Reconciliation Group

Enterprise Unit

Cost Comp. Amount

16. 10061067: Warehouse Receipt / FTP Result BO: Inventory Transaction / IT0000001

D Inventory Inventory / 1 NWH1 MAT -20 USD

C FTP Result End Account / 731 NWH1 MAT -20 USD

17. 10061067: Warehouse Receipt / FTP Result BO: Inventory Transaction / IT0000001

D Inventory Inventory / 1 NWH1 SUR -2 USD

C FTP Result End Account / 731 NWH1 SUR -2 USD

If the valuation method of item PI1 in warehouse NWH1 is Lot Price, the following situations can occur:

Lot is not present yet. In that case, lot price is created with amounts 220 (MAT), 22 (SUR) and 6 (WRS), with no integration transactions.

Lot is already present and lot price is 110 (MAT), 11 (SUR) and 3 (WRS). No integration transactions.

Lot is already present and lot price is, for example,110 (MAT), 11 (SUR) and 4 (WRS).

The following integration transaction is created:

D/C Journal Entry Reconciliation Group

Enterprise Unit

Cost Comp. Amount

18. 10061068: Warehouse Receipt / Lot Result BO: Inventory Transaction / IT0000001

D Inventory Inventory / 1 NWH1 WRS 2 USD

C Lot Result End Account / 733 NWH1 WRS 2 USD

Purchase Order | 3-7

List/manufactured item in warehouse

Two scenarios are possible:

Issue by main item: In this case, for manufactured items only, journal entries 12 through 18 are created.

Issue by components (for list items and manufactured items). For this scenario, the following example is valid.

Example: Receipt of order line for purchase order PUR000002 of two pieces of item LI1 for warehouse NWH1. The order price is 450 USD each. Inventory transaction ID IT0000003 is created during receipt.

D/C Journal Entry Reconciliation Group

Enterprise Unit

Cost Comp. Amount

19. 10001074: Purchase Order / Receipt BO: Purchase Order / PUR000002

D Interim Transit Interim Transit / 1 NWH1 900 USD

C Invoice Accrual Invoice Accrual / 3 PO1 900 USD

20. 10061074: Warehouse Receipt / Receipt BO: Inventory Transaction / IT0000003

D Inventory Inventory / 1 NWH1 MAT 675 USD

C Interim Transit Interim Transit / 1 NWH1 675 USD

21. 10061056: Warehouse Receipt / Item Surcharge Receipt

BO: Inventory Transaction / IT0000003

D Inventory Inventory / 1 NWH1 SUR 67.5 USD

C Surcharge Cover End Account / 732 NWH1 IRS 67.5 USD

22. 10061121: Warehouse Receipt / Warehouse Surcharge Receipt

BO: Inventory Transaction / IT0000003

D Inventory Inventory / 1 NWH1 WRS 18 USD

C Surcharge Cover End Account / 737 NWH1 WRS 18 USD

23. 10061074: Warehouse Receipt / Receipt BO: Inventory Transaction / IT0000003

D Inventory Inventory / 1 NWH1 MAT 225 USD

C Interim Transit Interim Transit / 1 NWH1 225 USD

Journal entries 20, 21, and 22 are for the six pieces of PI1. Journal entry 23 is for the four pieces of PI2. The amounts of journal entries 20 and 23 are determined in the following way:

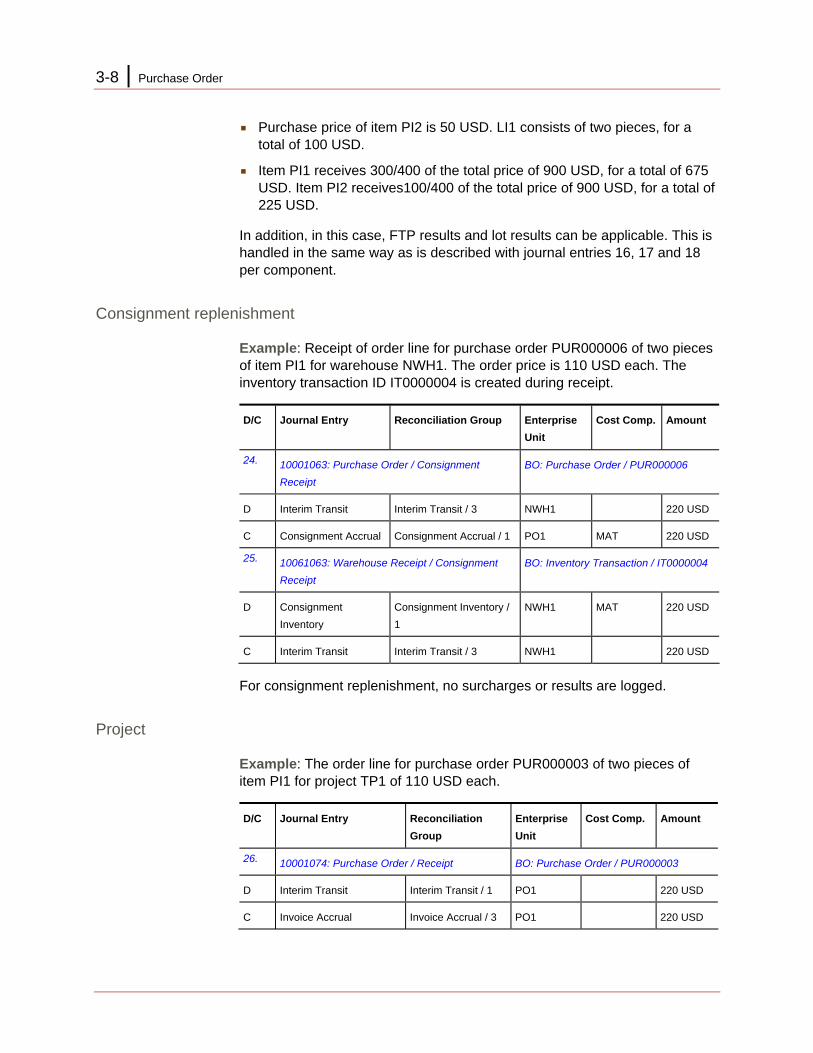

Purchase price of item PI1 is 100 USD. LI1 consists of three pieces, for a total of 300 USD.

3-8 | Purchase Order

Purchase price of item PI2 is 50 USD. LI1 consists of two pieces, for a total of 100 USD.

Item PI1 receives 300/400 of the total price of 900 USD, for a total of 675 USD. Item PI2 receives100/400 of the total price of 900 USD, for a total of 225 USD.

In addition, in this case, FTP results and lot results can be applicable. This is handled in the same way as is described with journal entries 16, 17 and 18 per component.

Consignment replenishment

Example: Receipt of order line for purchase order PUR000006 of two pieces of item PI1 for warehouse NWH1. The order price is 110 USD each. The inventory transaction ID IT0000004 is created during receipt.

D/C Journal Entry Reconciliation Group Enterprise Unit

Cost Comp. Amount

24. 10001063: Purchase Order / Consignment Receipt

BO: Purchase Order / PUR000006

D Interim Transit Interim Transit / 3 NWH1 220 USD

C Consignment Accrual Consignment Accrual / 1 PO1 MAT 220 USD

25. 10061063: Warehouse Receipt / Consignment Receipt

BO: Inventory Transaction / IT0000004

D Consignment Inventory

Consignment Inventory / 1

NWH1 MAT 220 USD

C Interim Transit Interim Transit / 3 NWH1 220 USD

For consignment replenishment, no surcharges or results are logged.

Project

Example: The order line for purchase order PUR000003 of two pieces of item PI1 for project TP1 of 110 USD each.

D/C Journal Entry Reconciliation Group

Enterprise Unit

Cost Comp. Amount

26. 10001074: Purchase Order / Receipt BO: Purchase Order / PUR000003

D Interim Transit Interim Transit / 1 PO1 220 USD

C Invoice Accrual Invoice Accrual / 3 PO1 220 USD

Purchase Order | 3-9

27. 10024029: Project Costs & Commitments / Direct Receipt

BO: Project Cost and Commitment / TP1

D Project (TP) WIP Project (TP) WIP / 1 TP1 220 USD

C Interim Transit Interim Transit / 1 PO1 220 USD

Journal entry 26 is created at the moment the receipt is confirmed. Journal entry 27 is created later on in TP when the transaction is posted. Therefore, the journal entries are not made at the same time.

The journal entries 26 and 27 are created for a direct receipt in project from a cost item, a service item, a subcontracting item, or an equipment item.

For a receipt in a project warehouse, the following journal entries are created:

Purchased/Tool/Cost/Service Items and Warehouse

List/Manufactured Items and Warehouse

However, if a cost item or a service item is received in a project warehouse, journal entries 26 and 27 are created, where the enterprise unit for Interim Transit / 1 is the enterprise unit of the warehouse (PWH1).

Direct delivery for Sales or Service

No invoice relationship between purchase office and sales office or service department

Example: Purchase order line for purchase order PUR000004 is a direct delivery for two pieces of item PI1, linked to sales order SLS000001. The order price is 110 USD. The handling of the sales side of the direct delivery is described in sections “Sales Order/Issues/Direct Delivery” and “Service Order/Material Lines/Direct Delivery.”

D/C Journal Entry Reconciliation Group

Enterprise Unit

Cost Comp. Amount

28. 10001074: Purchase Order / Receipt BO: Purchase Order / PUR000004

D Interim Transit Interim Transit / 1 PO1 220 USD

C Invoice Accrual Invoice Accrual / 3 PO1 220 USD

29. 10001026 Purchase Order / Direct Delivery BO: Purchase Order / PUR000004

D Interim Direct Delivery Interim Transit / 4 PO1 220 USD

C Interim Transit Interim Transit / 1 PO1 220 USD

3-10 | Purchase Order