Embed Size (px)

Citation preview

NAIC Fall Meeting

November 4, 2011

Using Catastrophe Models and Other Tools to

Assess Hurricane Risk

Background

RMS V11 hurricane model was a wake-up call for the industry with respect to Over-reliance on the catastrophe models

Magnitude of the uncertainty underlying the models (if Florida can change by 200 percent, …)

Need for more transparent and robust information for catastrophe risk management

External stakeholders, such as rating agencies, have growing expectations with

respect to

Insurance company understanding of their catastrophe risk and ability to explain it

How companies evaluate the catastrophe models and determine which one(s) to use

Company “ownership” of their risk and their risk management strategies

Catastrophe losses increasing over time and now the largest driver of property

losses, particularly for residential lines of business

© 2011 Karen Clark & Company 2

Goals of the Presentation

Illustrate why the catastrophe models have so much inherent uncertainty and will

never be accurate or precise tools

Demonstrate how other important information and tools can be used to better

understand and manage the risk

Provide insights into how an insurance company can develop a risk

management framework that is Robust (providing consistent information from year to year)

Transparent (providing insight into the risk rather than a simple EP curve)

Operational

Efficient

Flexible

© 2011 Karen Clark & Company 3

Important Theme

“If you can’t explain it simply,

you don’t understand it well enough”

Albert Einstein

© 2011 Karen Clark & Company 4

© 2009 Karen Clark & Company

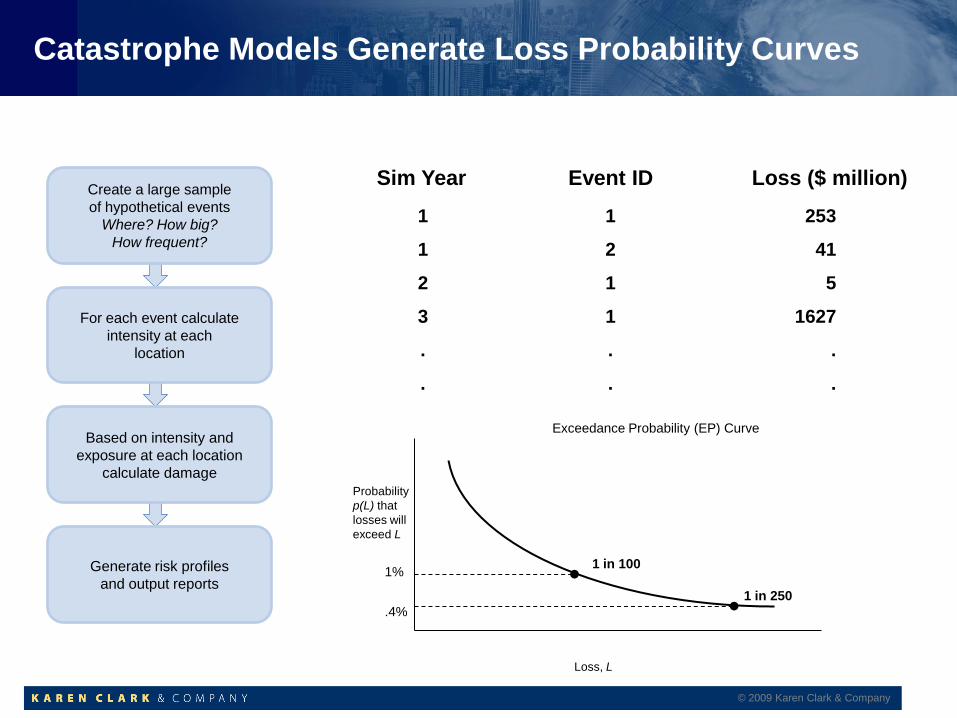

Catastrophe Models Generate Loss Probability Curves

Loss, L

Probability

p(L) that

losses will

exceed L

Exceedance Probability (EP) Curve

1 in 100

1 in 250 •

• .4%

1%

Sim Year

1

1

2

3

.

.

1

2

1

1

.

.

253

41

5

1627

.

.

Event ID Loss ($ million) Create a large sample

of hypothetical events

Where? How big?

How frequent?

For each event calculate

intensity at each

location

Based on intensity and

exposure at each location

calculate damage

Generate risk profiles

and output reports

© 2009 Karen Clark & Company

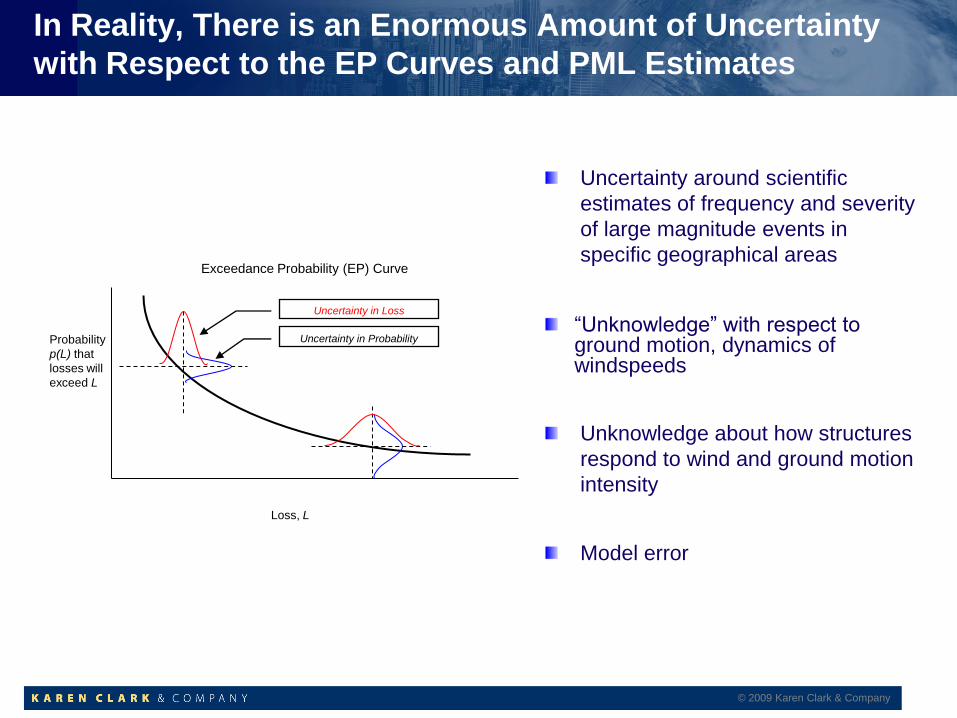

In Reality, There is an Enormous Amount of Uncertainty

with Respect to the EP Curves and PML Estimates

Loss, L

Probability

p(L) that

losses will

exceed L

Exceedance Probability (EP) Curve

Uncertainty in Loss

Uncertainty in Probability

Uncertainty around scientific

estimates of frequency and severity

of large magnitude events in

specific geographical areas

“Unknowledge” with respect to ground motion, dynamics of windspeeds

Unknowledge about how structures

respond to wind and ground motion

intensity

Model error

© 2011 Karen Clark & Company 7

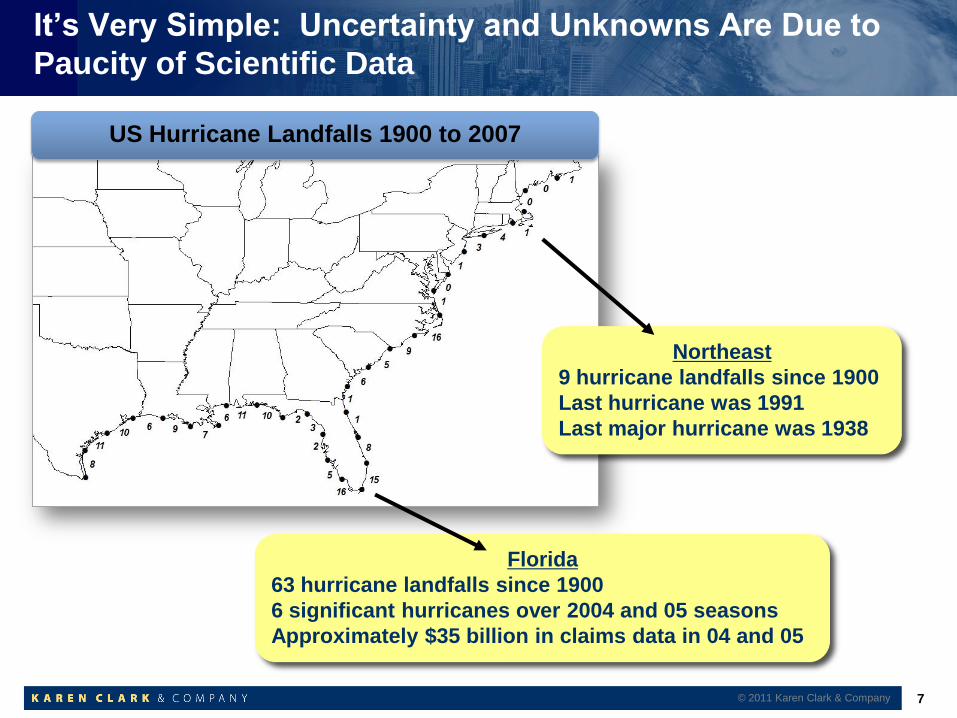

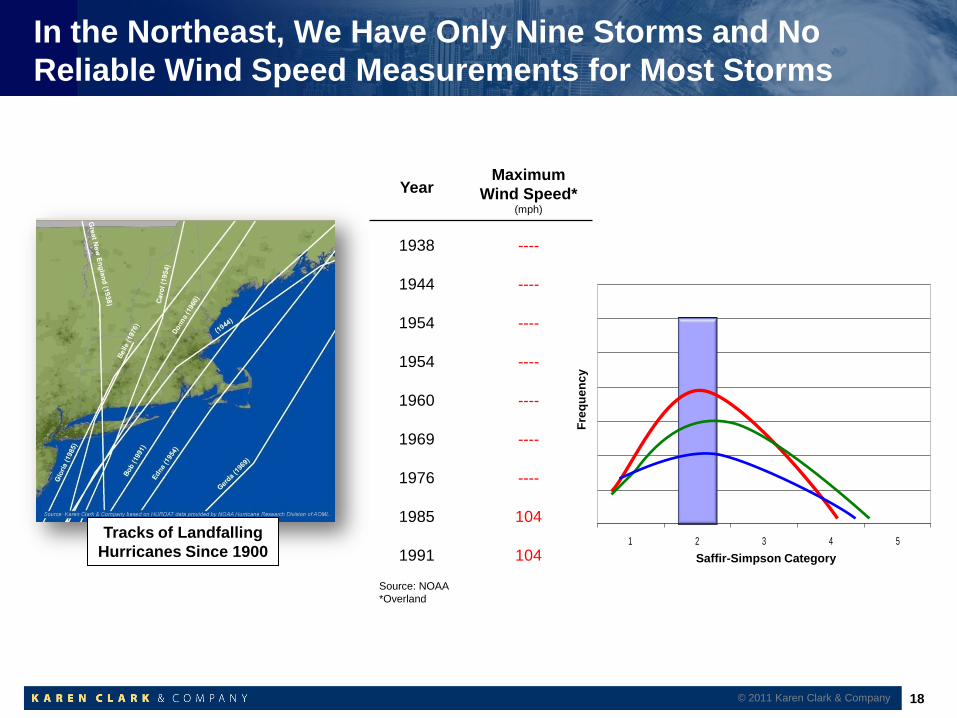

US Hurricane Landfalls 1900 to 2007

Northeast

9 hurricane landfalls since 1900

Last hurricane was 1991

Last major hurricane was 1938

Florida

63 hurricane landfalls since 1900

6 significant hurricanes over 2004 and 05 seasons

Approximately $35 billion in claims data in 04 and 05

It’s Very Simple: Uncertainty and Unknowns Are Due to

Paucity of Scientific Data

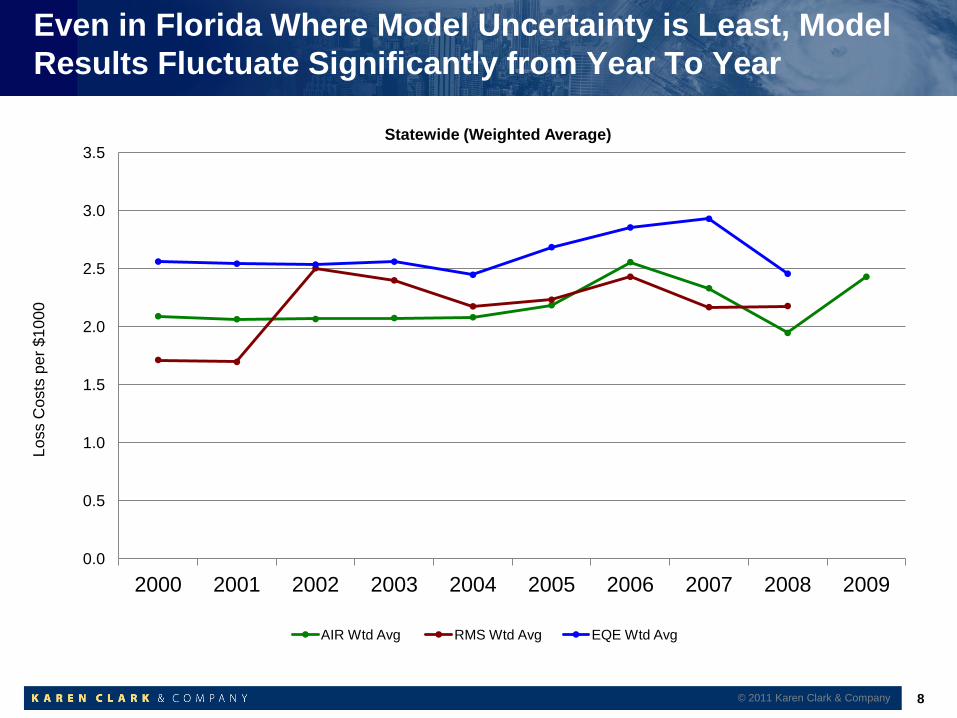

Even in Florida Where Model Uncertainty is Least, Model

Results Fluctuate Significantly from Year To Year

© 2011 Karen Clark & Company 8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

AIR Wtd Avg RMS Wtd Avg EQE Wtd Avg

Lo

ss C

osts

pe

r $

10

00

Statewide (Weighted Average)

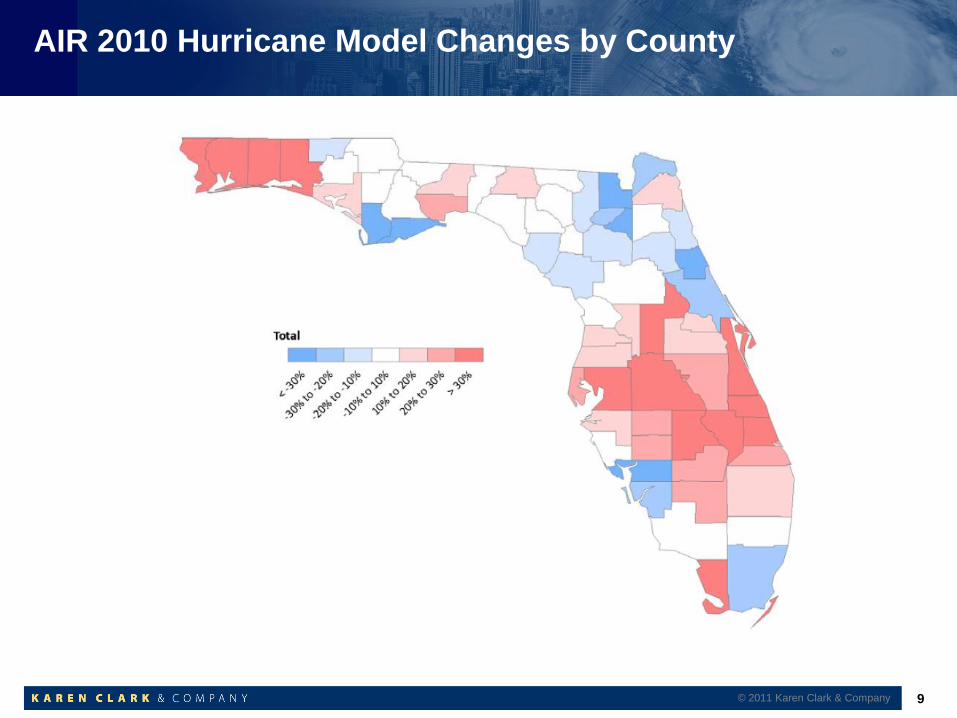

AIR 2010 Hurricane Model Changes by County

© 2011 Karen Clark & Company 9

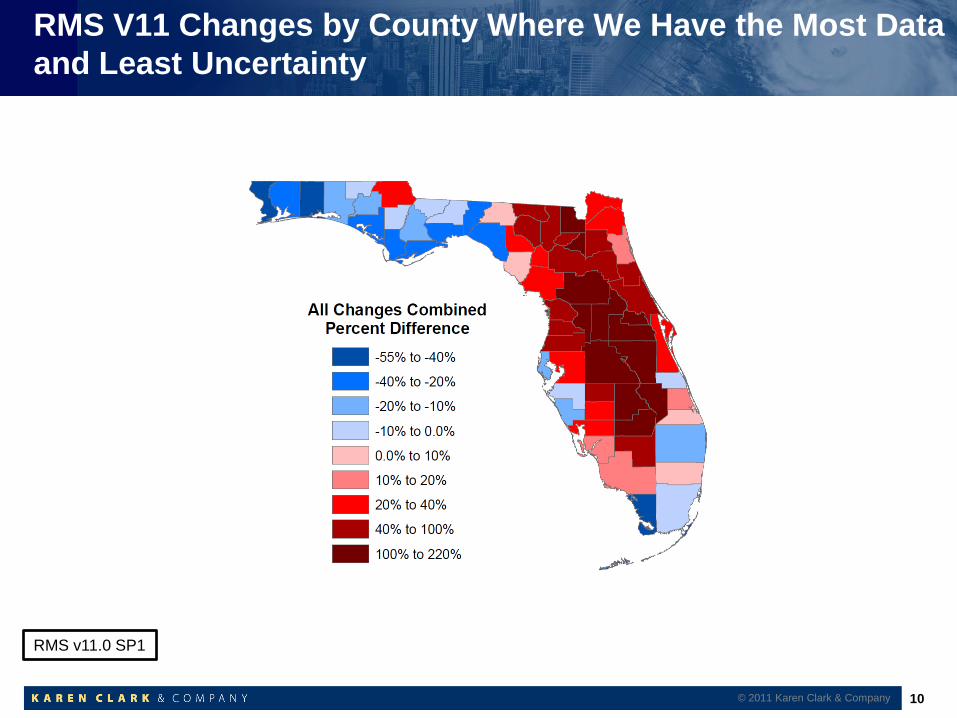

RMS V11 Changes by County Where We Have the Most Data

and Least Uncertainty

© 2011 Karen Clark & Company 10

RMS v11.0 SP1

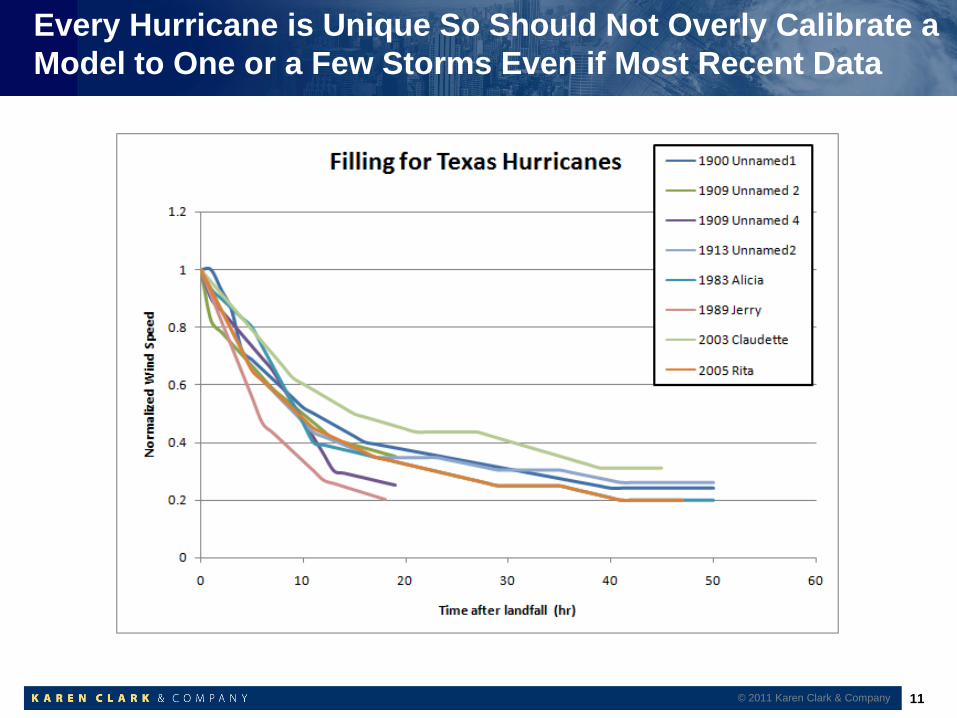

Every Hurricane is Unique So Should Not Overly Calibrate a

Model to One or a Few Storms Even if Most Recent Data

11 © 2011 Karen Clark & Company

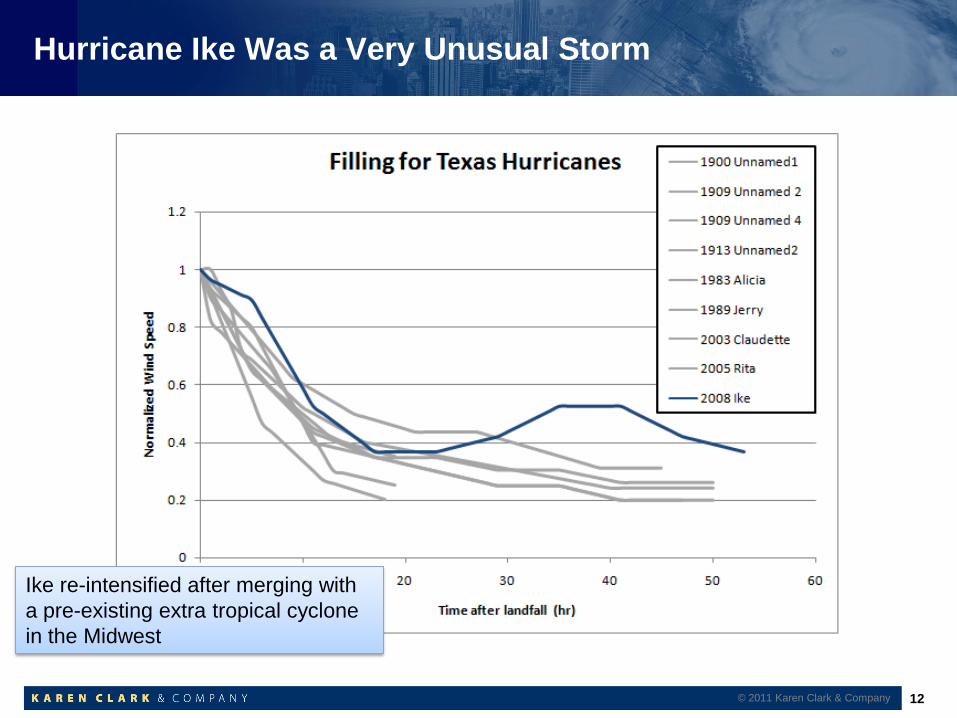

Hurricane Ike Was a Very Unusual Storm

12

Ike re-intensified after merging with

a pre-existing extra tropical cyclone

in the Midwest

© 2011 Karen Clark & Company

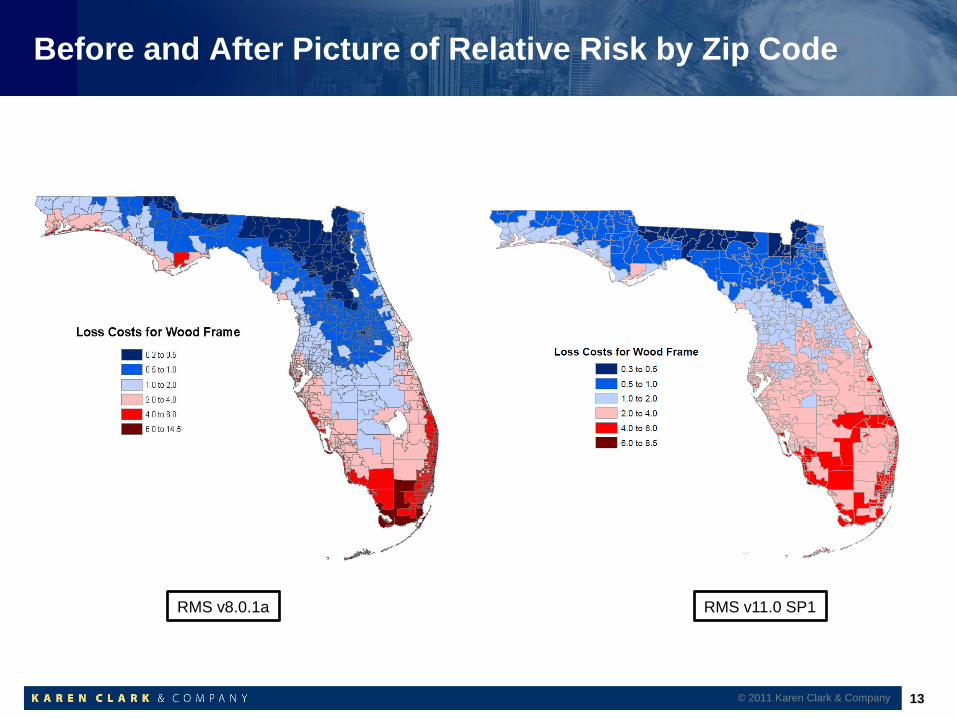

Before and After Picture of Relative Risk by Zip Code

13

RMS v8.0.1a RMS v11.0 SP1

© 2011 Karen Clark & Company

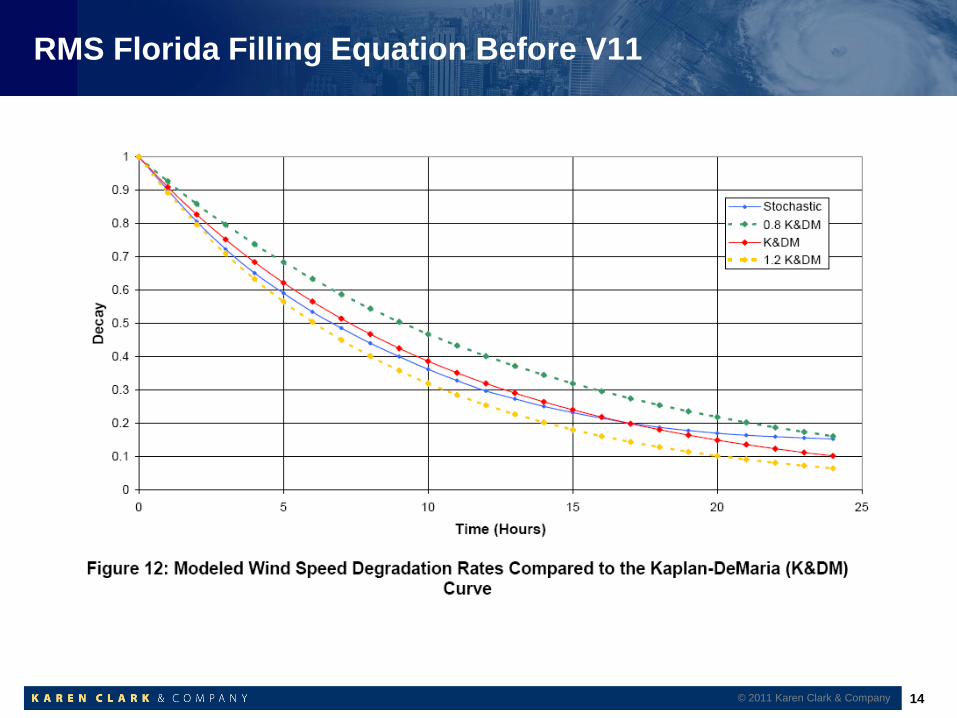

RMS Florida Filling Equation Before V11

14 © 2011 Karen Clark & Company

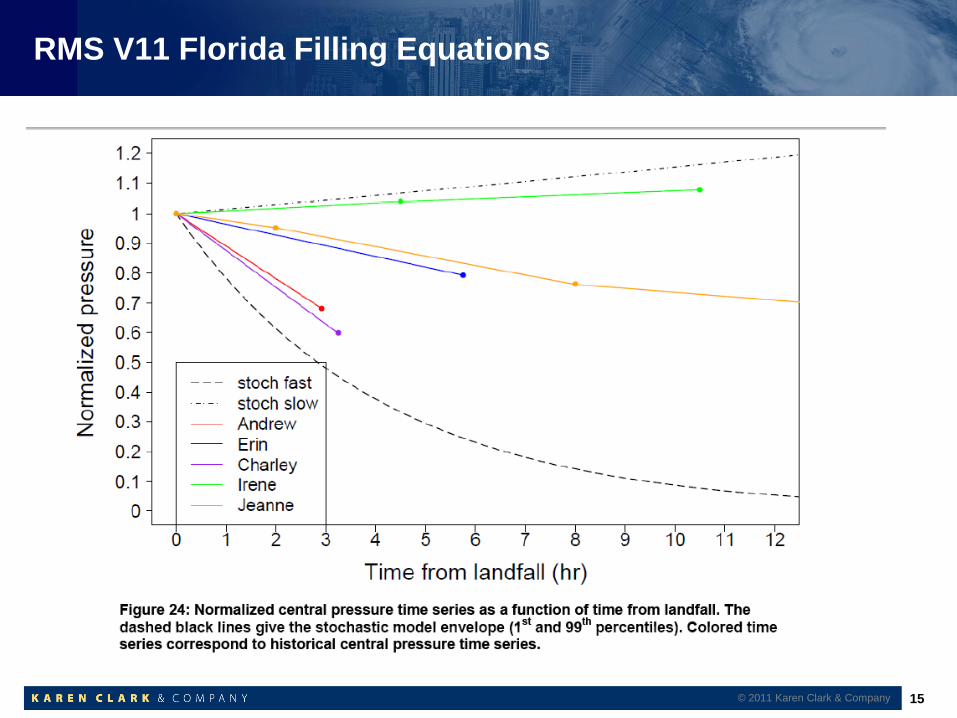

RMS V11 Florida Filling Equations

15 © 2011 Karen Clark & Company

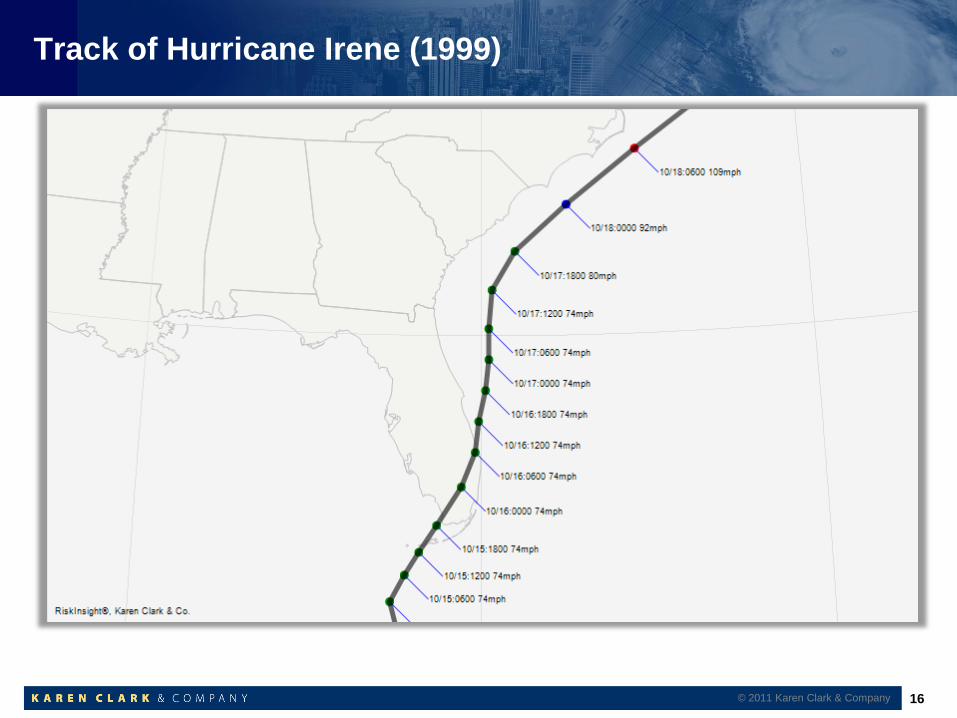

Track of Hurricane Irene (1999)

16 © 2011 Karen Clark & Company

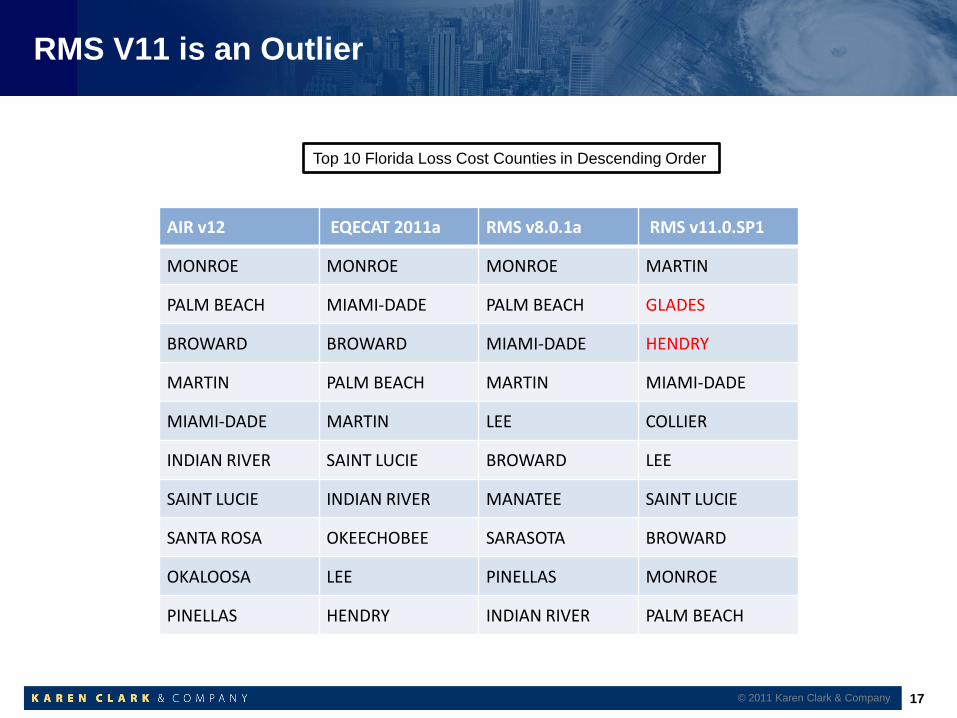

RMS V11 is an Outlier

AIR v12 EQECAT 2011a RMS v8.0.1a RMS v11.0.SP1

MONROE MONROE MONROE MARTIN

PALM BEACH MIAMI-DADE PALM BEACH GLADES

BROWARD BROWARD MIAMI-DADE HENDRY

MARTIN PALM BEACH MARTIN MIAMI-DADE

MIAMI-DADE MARTIN LEE COLLIER

INDIAN RIVER SAINT LUCIE BROWARD LEE

SAINT LUCIE INDIAN RIVER MANATEE SAINT LUCIE

SANTA ROSA OKEECHOBEE SARASOTA BROWARD

OKALOOSA LEE PINELLAS MONROE

PINELLAS HENDRY INDIAN RIVER PALM BEACH

Top 10 Florida Loss Cost Counties in Descending Order

17 © 2011 Karen Clark & Company

In the Northeast, We Have Only Nine Storms and No

Reliable Wind Speed Measurements for Most Storms

© 2011 Karen Clark & Company 18

Tracks of Landfalling

Hurricanes Since 1900

Year

Maximum

Wind Speed* (mph)

1938 ----

1944 ----

1954 ----

1954 ----

1960 ----

1969 ----

1976 ----

1985 104

1991 104

Source: NOAA

*Overland

1 2 3 4 5

Saffir-Simpson Category

Fre

qu

en

cy

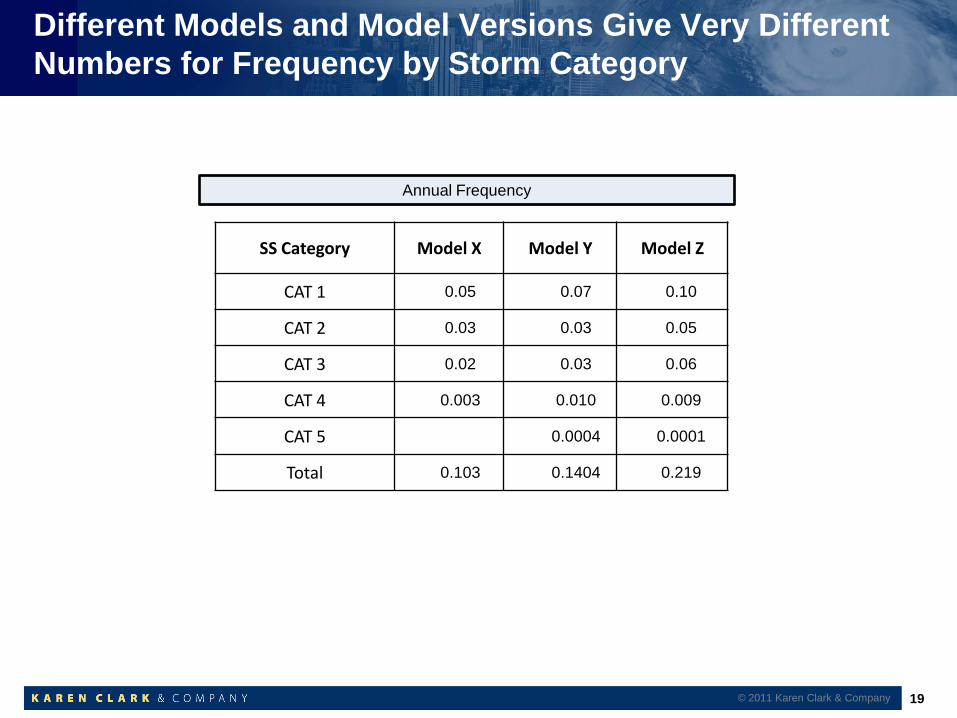

Different Models and Model Versions Give Very Different

Numbers for Frequency by Storm Category

© 2011 Karen Clark & Company 19

SS Category Model X Model Y Model Z

CAT 1 0.05 0.07 0.10

CAT 2 0.03 0.03 0.05

CAT 3 0.02 0.03 0.06

CAT 4 0.003 0.010 0.009

CAT 5 0.0004 0.0001

Total 0.103 0.1404 0.219

Annual Frequency

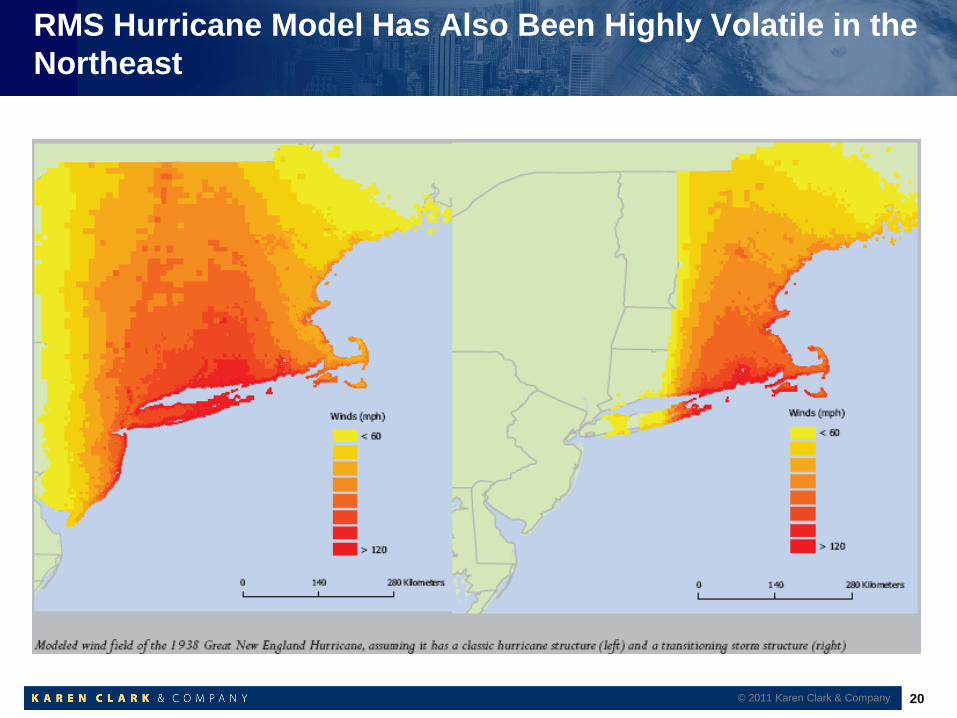

RMS Hurricane Model Has Also Been Highly Volatile in the

Northeast

© 2011 Karen Clark & Company 20

So Why Do We Keep Expecting the Models to Give Accurate

Numbers?

© 2011 Karen Clark & Company 21

Dispelling the Myths Surrounding Catastrophe Models

The models are not getting more accurate over time Not enough reliable data for any degree of accuracy

Much of the volatility in the loss estimates is due to scientific “unknowns” versus new scientific

knowledge

An updated model is not necessarily a better, more credible model Over specification combined with high sensitivity of loss estimates to small changes in model

assumptions

Over calibration to most recent event(s)

The catastrophe models are not objective tools Most model assumptions are based on the subjective judgments of scientists and engineers rather

than objective data

Different scientists have their own opinions and biases

Scientists can change their minds

© 2011 Karen Clark & Company 22

Developing an Effective and Robust Risk Management

Framework

There is no “best” or “right” model

Enlightenment will not come from A set of questions to ask the modelers

Reading hundreds of pages of model documentation

The best way to evaluate a model is to perform detailed tests of the model output How do the simulated frequencies by magnitude compare with the historical data?

How do the vulnerability relativities compare to actual claims experience and engineering

knowledge?

Do the normalized losses at high resolution follow a logical relation to risk?

The most thorough understanding comes from a model-independent view of the

risk in exposed peril regions based on multiple data sources and tools

An effective and robust risk management framework is informed by the models

but not based on the models

© 2011 Karen Clark & Company 23

CONFIDENTIAL

Scientifically-derived, Model-Independent Characteristic

Events (CEs) Provide an Additional Tool

CEs are defined-probability scenario events

CEs are defined for different regions for return periods of interest such as

100, 250, and 500 year

Wind footprints for the CEs are “floated” along the coast to estimate a range

of loss estimates for each return period

CEs are comparable to model-generated events and have additional benefits They are based on same scientific data but eliminate the fluctuations in loss estimates due to

noise in the hazard component of the models

They are transparent and easily peer-reviewed by independent, external experts

They provide a set of scenario losses that can be monitored at the corporate level and drilled

down to individual policies if desired

The average or median CE loss for each region can be compared to model-generated PMLs

24 © 2011 Karen Clark & Company

CONFIDENTIAL

CE Parameters Vary By Region

Texas

Iowa

Kansas

Minnesota

IllinoisOhio

Missouri

Florida

Nebraska

Georgia

Oklahoma

Wisconsin

Maine

Alabama

Arkansas

New York

Virginia

Indiana

Michigan

South Dakota

North Dakota

Louisiana

Kentucky

Mississippi

Tennessee

Pennsylvania

North Carolina

Michigan

South Carolina

West Virginia

Vermont

Maryland

New Jersey

New Hampshire

Massachusetts

Connecticut

Delaware

Rhode Island

25 © 2011 Karen Clark & Company

CONFIDENTIAL

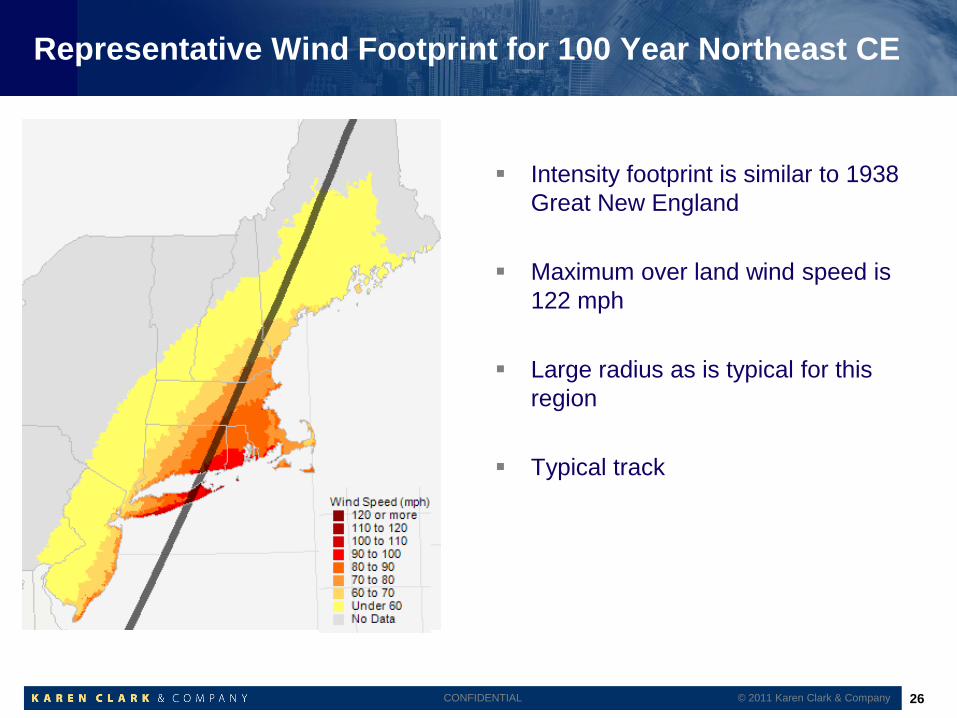

Representative Wind Footprint for 100 Year Northeast CE

Intensity footprint is similar to 1938

Great New England

Maximum over land wind speed is

122 mph

Large radius as is typical for this

region

Typical track

26 © 2011 Karen Clark & Company

CONFIDENTIAL

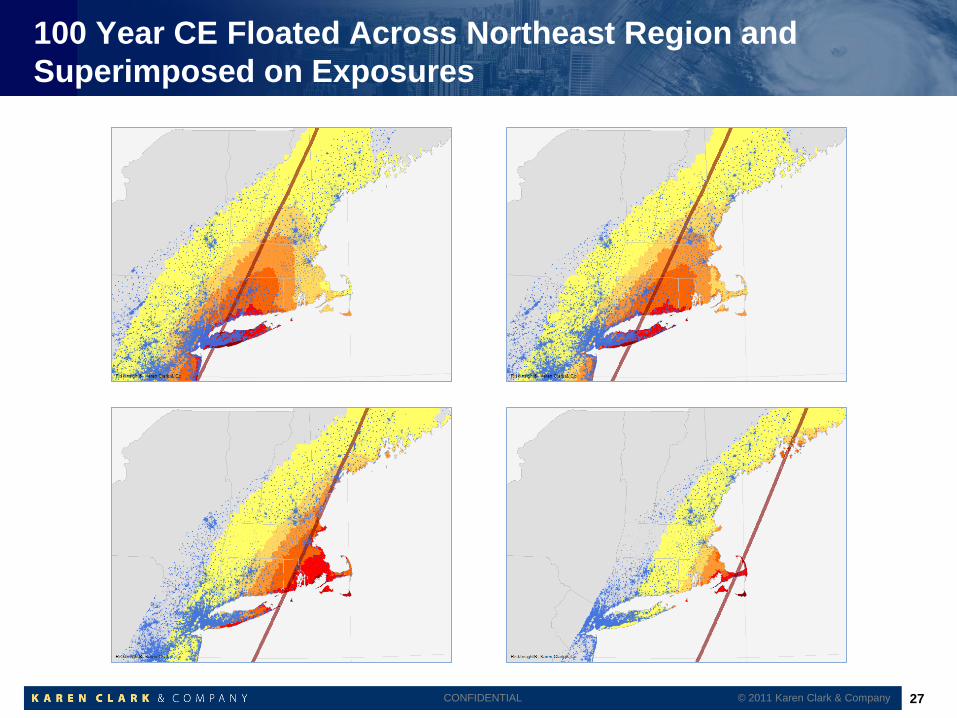

100 Year CE Floated Across Northeast Region and

Superimposed on Exposures

27 © 2011 Karen Clark & Company

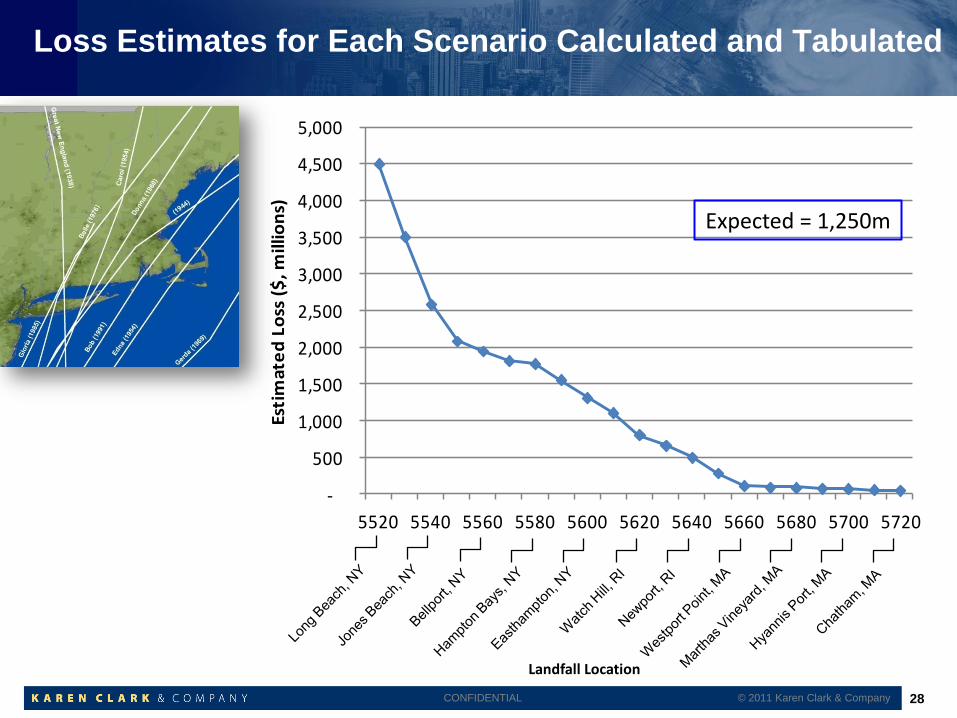

CONFIDENTIAL

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5520 5540 5560 5580 5600 5620 5640 5660 5680 5700 5720

Esti

mat

ed

Lo

ss (

$, m

illio

ns)

Landfall Location

Loss Estimates for Each Scenario Calculated and Tabulated

© 2011 Karen Clark & Company 28

Expected = 1,250m

CONFIDENTIAL

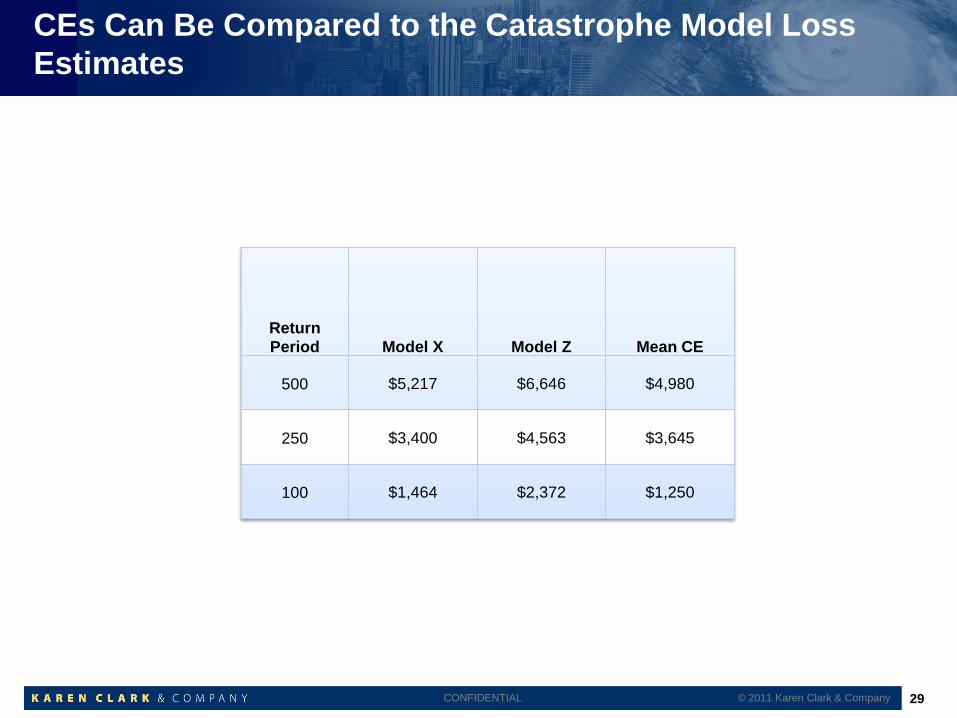

CEs Can Be Compared to the Catastrophe Model Loss

Estimates

© 2011 Karen Clark & Company 29

Return

Period Model X Model Z Mean CE

500 $5,217 $6,646 $4,980

250 $3,400 $4,563 $3,645

100 $1,464 $2,372 $1,250

CONFIDENTIAL

And Provide Additional Information for a Richer Dialog and

Understanding

A reasonable estimate for company’s 1 in 100 year loss is $1 to $1.5 billion

A reasonable estimate for company’s 1 in 250 year loss is $3 to $4 billion

However, company could have a loss in excess of $4 billion from a Cat 3 storm

tracking through NYC and western Long Island (black swan?)

Most scenario losses from 1 in 100 year CE are less than $2 billion

Reducing exposure concentrations and/or re-evaluating underwriting guidelines

can reduce the chances of “black swan” event

© 2011 Karen Clark & Company 30

CONFIDENTIAL

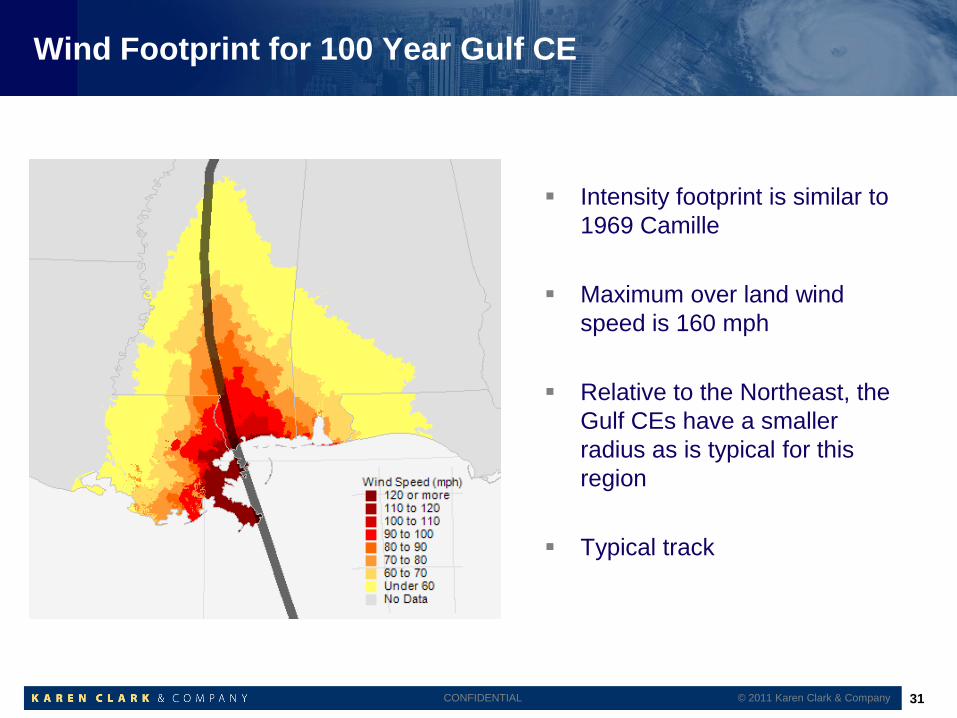

Wind Footprint for 100 Year Gulf CE

Intensity footprint is similar to

1969 Camille

Maximum over land wind

speed is 160 mph

Relative to the Northeast, the

Gulf CEs have a smaller

radius as is typical for this

region

Typical track

31 © 2011 Karen Clark & Company

CONFIDENTIAL

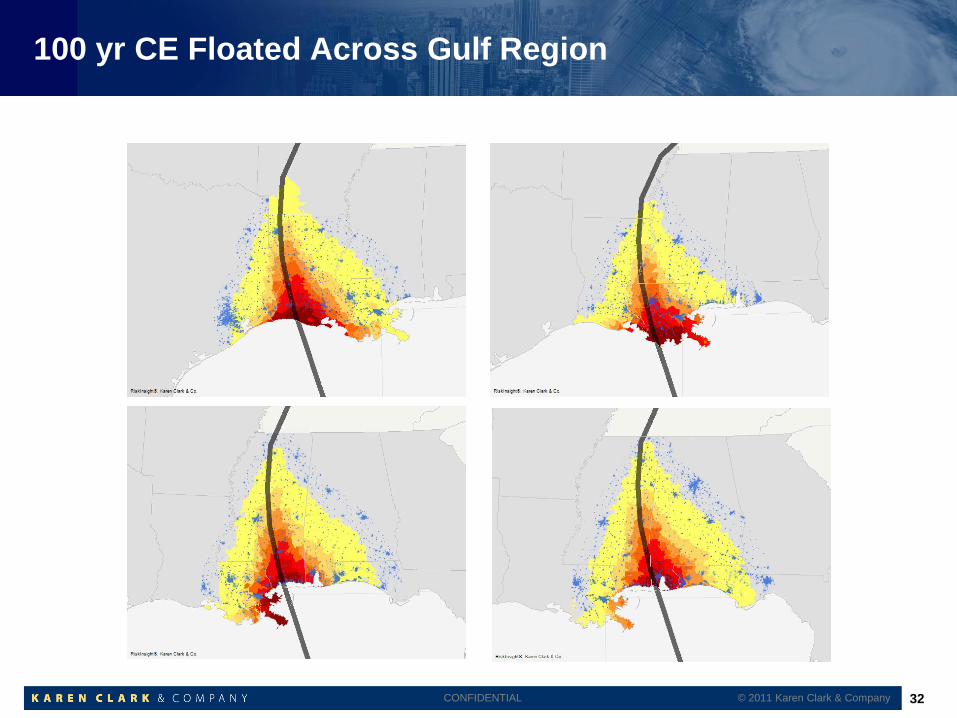

100 yr CE Floated Across Gulf Region

32 © 2011 Karen Clark & Company

CONFIDENTIAL

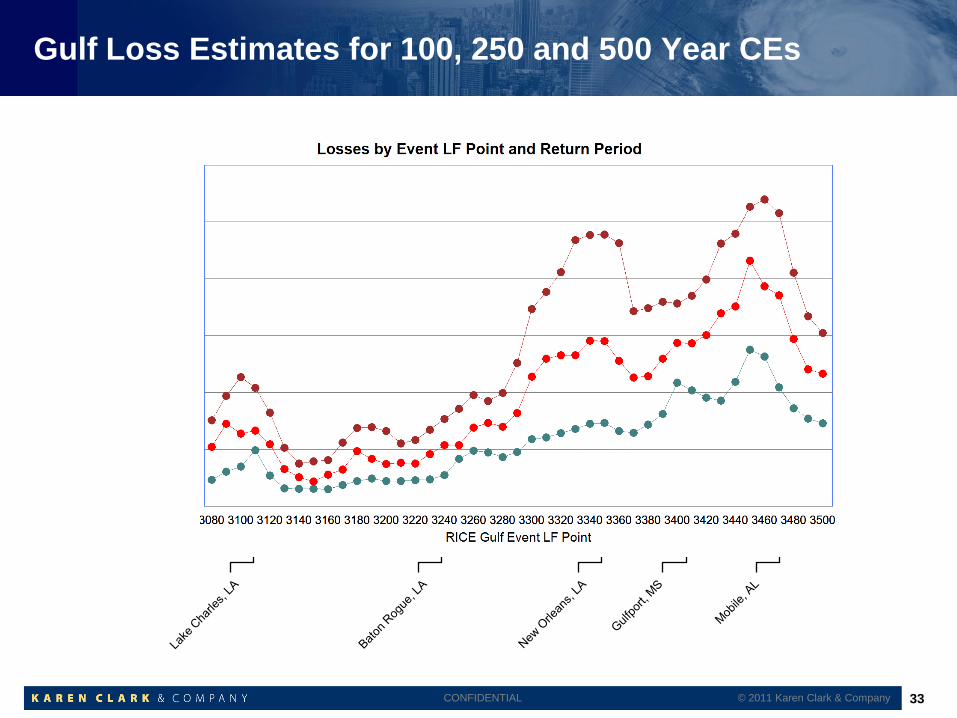

Gulf Loss Estimates for 100, 250 and 500 Year CEs

CE 500

CE 250

CE 100

33 © 2011 Karen Clark & Company

CONFIDENTIAL

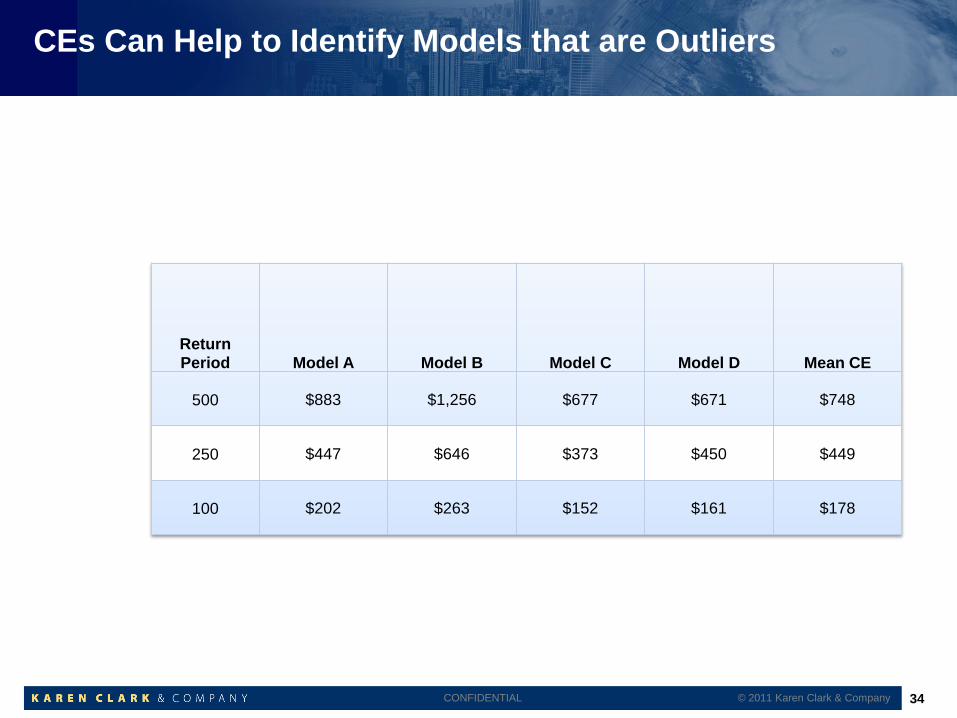

CEs Can Help to Identify Models that are Outliers

© 2011 Karen Clark & Company 34

Return

Period Model A Model B Model C Model D Mean CE

500 $883 $1,256 $677 $671 $748

250 $447 $646 $373 $450 $449

100 $202 $263 $152 $161 $178

CONFIDENTIAL

Benefits of CEs

CEs provide transparent sets of scenario losses for better understanding the risk

Characteristic Event (CE) sets are stable from year to year Will only change if something happens that significantly changes the hazard in a particular region

(e.g. there is a cat 5 hurricane in the Northeast)

Companies can effectively monitor the impacts of pure exposure changes

Companies can plan their risk management strategies and make consistent decisions thereby

serving their policyholders better

CEs are operational risk metrics

Because they provide a fixed set of events, they are fully additive across accounts, lines of

business, etc.

They can be monitored at the corporate level and drilled down to the resolution desired

Underwriters can clearly see the impacts of adding additional accounts

At high resolution, such as zip code, CEs provide a consistent and logical

relation to risk CEs can provide more events in the tail of the distribution

Because they are “floated” to cover all exposure areas, there is less noise at high resolution

© 2011 Karen Clark & Company 35

CONFIDENTIAL

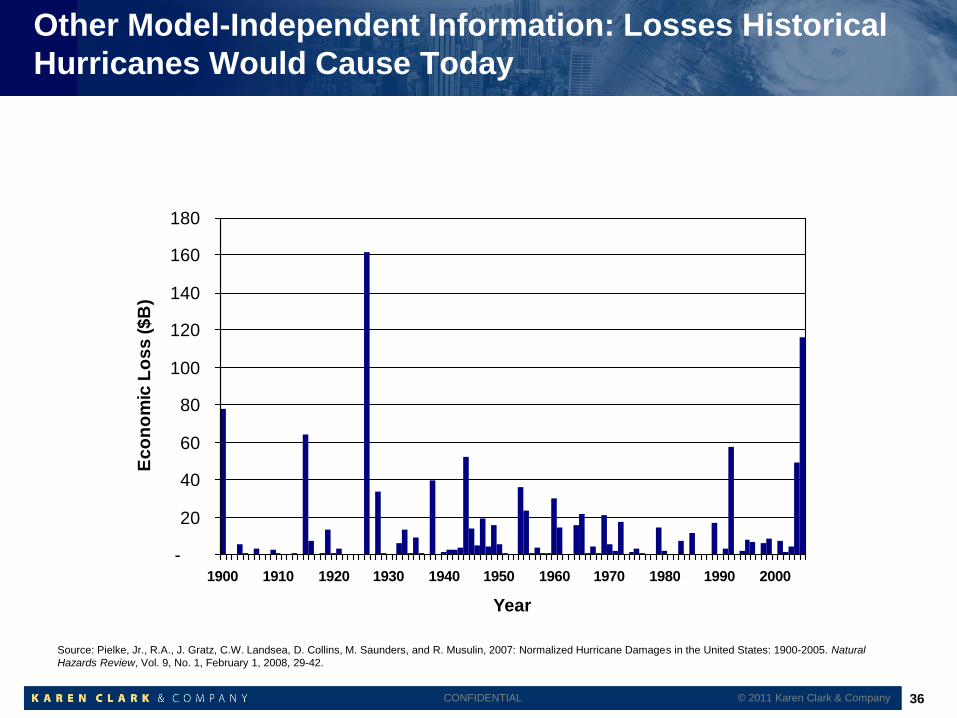

Other Model-Independent Information: Losses Historical

Hurricanes Would Cause Today

-

20

40

60

80

100

120

140

160

180

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

Year

Ec

on

om

ic L

os

s (

$B

)

Source: Pielke, Jr., R.A., J. Gratz, C.W. Landsea, D. Collins, M. Saunders, and R. Musulin, 2007: Normalized Hurricane Damages in the United States: 1900-2005. Natural

Hazards Review, Vol. 9, No. 1, February 1, 2008, 29-42.

© 2011 Karen Clark & Company 36

CONFIDENTIAL

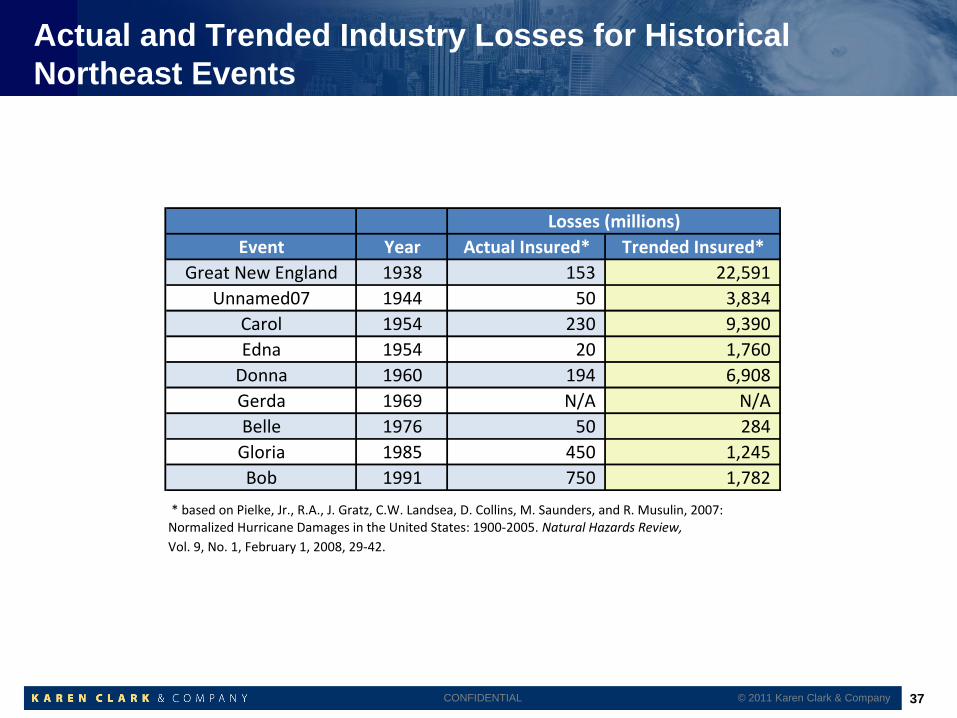

Actual and Trended Industry Losses for Historical

Northeast Events

© 2011 Karen Clark & Company 37

Event Year Actual Insured* Trended Insured*

Great New England 1938 153 22,591

Unnamed07 1944 50 3,834

Carol 1954 230 9,390

Edna 1954 20 1,760

Donna 1960 194 6,908

Gerda 1969 N/A N/A

Belle 1976 50 284

Gloria 1985 450 1,245

Bob 1991 750 1,782

* based on Pielke, Jr., R.A., J. Gratz, C.W. Landsea, D. Collins, M. Saunders, and R. Musulin, 2007:Normalized Hurricane Damages in the United States: 1900-2005. Natural Hazards Review,

Vol. 9, No. 1, February 1, 2008, 29-42.

Losses (millions)

CONFIDENTIAL

Estimated Company Losses for Historical Events versus

Modeled

© 2011 Karen Clark & Company 38

Event Year Est. Historical * Model X Model Z

Great New England 1938 1,018.65 1,792.02 3,614.10

Unnamed07 1944 469.36 N/A N/A

Carol 1954 560.65 830.08 1,693.14

Edna 1954 183.47 N/A N/A

Donna 1960 368.87 1,164.25 1,403.76

Gerda 1969 N/A N/A N/A

Belle 1976 10.10 N/A N/A

Gloria 1985 70.15 228.85 325.99

Bob 1991 161.81 N/A 92.51

Gross Losses (millions)

CONFIDENTIAL

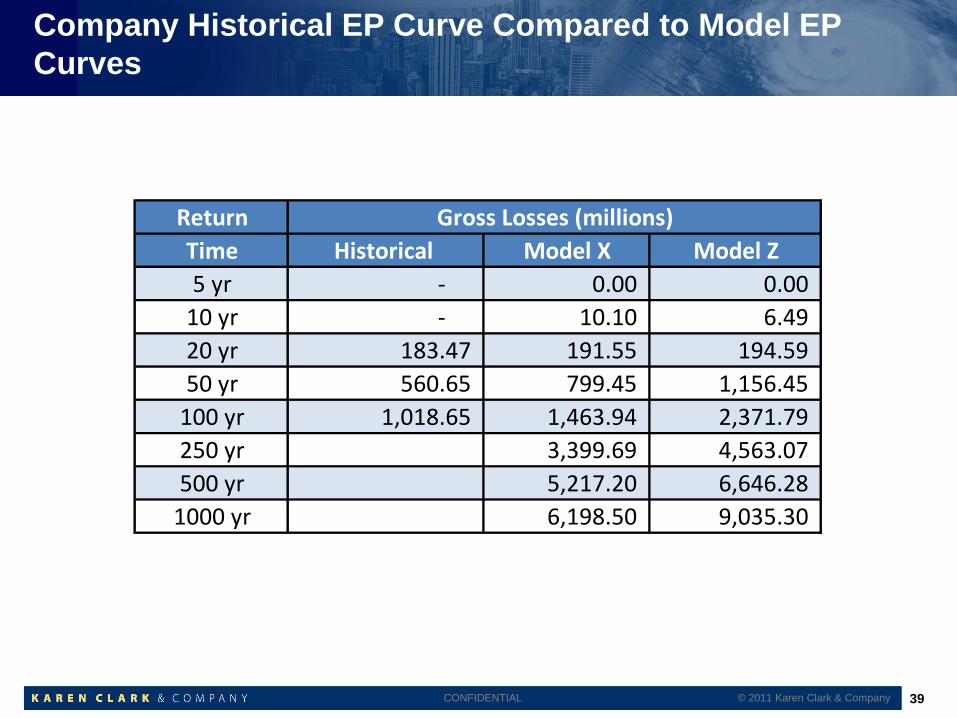

Company Historical EP Curve Compared to Model EP

Curves

© 2011 Karen Clark & Company 39

Return

Time Historical Model X Model Z

5 yr - 0.00 0.00

10 yr - 10.10 6.49

20 yr 183.47 191.55 194.59

50 yr 560.65 799.45 1,156.45

100 yr 1,018.65 1,463.94 2,371.79

250 yr 3,399.69 4,563.07

500 yr 5,217.20 6,646.28

1000 yr 6,198.50 9,035.30

Gross Losses (millions)

CONFIDENTIAL

Conclusions

While the catastrophe models are valuable tools the model-generated loss

estimates are highly volatile due to noise caused by lack of data Disruptive to underwriting and pricing strategies

Disruptive to consumers

Insurance companies and consumers will benefit from other risk metrics and

tools

A more complete toolkit improves the dialog with external stakeholders, such as

rating agencies, who expect companies to take “ownership” of the risk and to be

able to explain what they believe and why

Other sources of information, such as trended historical losses, analyses of

claims data, etc. are also very valuable for understanding the risk

© 2011 Karen Clark & Company 40