Embed Size (px)

Citation preview

Group-based incentive systems such as gain-sharing, employee stock ownership plans(ESOPs), and profit sharing have been thesubject of numerous studies (see Cooke,1994; Kim, 1999; McKersie, 1986; andHammer, 1988 for differences between gain-sharing and profit sharing and Klein, 1987,and Klein & Hall, 1988, for differences be-tween ESOPs and profit sharing). Profitsharing, simply put, occurs when a portion oforganizational profits is distributed to em-ployees as part of their compensation (Kruse,1993). Research on profit sharing has gener-ally entailed case study examinations (Bartol& Durham, 2000) or adopted a micro-eco-nomic perspective (e.g., Weitzman, 1995).The latter type of research has typically ad-dressed the issue of whether profit sharing

has any effect on such outcomes as prof-itability, productivity, absenteeism, and laborturnover, by using survey data to compare or-ganizations with and without profit sharing(e.g., Blasi, Conte, & Kruse, 1996; Kruse,1996). For a variety of reasons that will beaddressed later, there is little consensus re-garding the effectiveness of profit sharing.The ambiguity surrounding if, how, andwhen profit sharing is successful leaveshuman resource professionals uncertain asto whether to recommend the implementa-tion of profit sharing in their firms. We striveto shed light on this important issue by ex-panding the set of outcomes profit sharingshould influence to include more proximalresults (e.g., more favorable employee atti-tudes, more supportive employee behaviors).

USING PROFIT SHARING TO ENHANCEEMPLOYEE ATTITUDES: A LONGITUDINALEXAMINATION OF THE EFFECTS ON TRUSTAND COMMITMENT

Human Resource Management, Winter 2002, Vol. 41, No. 4, Pp. 423–439© 2002 Wiley Periodicals, Inc. Published online in Wiley InterScience (www.interscience.wiley.com). DOI: 10.1002/hrm.10052

Jacqueline A-M. Coyle-Shapiro, Paula C. Morrow, RayRichardson, and Stephen R. Dunn

The ability of profit sharing to increase organizational performance via positive changes in em-ployee attitudes has yielded mixed results. Drawing on principal agent, expectancy, and organi-zational justice theories, we assess how perceptions of profit sharing (capacity for individual con-tribution and organizational reciprocity) alter organizational commitment and trust inmanagement using longitudinal data provided by 141 engineering employees. Favorable per-ceptions of profit sharing served to increase organizational commitment while only organiza-tional reciprocity predicted trust in management. The relationship between organizational rec-iprocity and commitment was partially mediated by trust in management. Implications for thedesign of profit sharing initiatives are noted. © 2002 Wiley Periodicals, Inc.

Correspondence to: Jacqueline A-M. Coyle-Shapiro, Department of Industrial Relations, London School ofEconomics, Houghton Street, London WC2A 2AE, United Kingdom; telephone: +44 207-955-7035; fax:+44 207-955-7424; e-mail: [email protected]

424 • HUMAN RESOURCE MANAGEMENT, Winter 2002

Co-existing with case-oriented andmacro-economic profit sharing research is amuch smaller body of inquiry that examinesthe effects of profit sharing on employee atti-tudes and behavior. As noted by Florkowskiand Schuster (1992), this research creditsprofit sharing with improving a range of atti-tudes and behaviors. Ogden (1995) andSchwochau, Delaney, Jarley, and Fiorito(1997), for example, have demonstrated howprofit sharing facilitates employee support forpolicy changes. At the same time, the mecha-nisms by which profit-sharing affects hypoth-esized outcomes remain under-explored(Florkowski & Schuster, 1992; Ogden, 1995).Furthermore, the predominant research de-sign employed in these empirical studies iscross-sectional, which limits causal infer-ences. Our focus complements this work byassessing the effects of profit sharing on trustin management and affective organizationalcommitment. Specifically, we address the fol-lowing two questions. First, to what extentdoes profit sharing enhance employees’ trustin management and organizational commit-ment? Second, if profit sharing does enhancetrust and commitment, what are the keymechanisms by which this effect occurs?

Literature Review and Hypotheses

There is a very large literature, both theoreticaland empirical, on profit sharing (sometimestermed profit-related pay). Lawler, Mohrman,and Ledford (1995) report that two-thirds ofthe U.S. Fortune 1000 firms have some sort ofprofit sharing plan and there is good evidenceto suggest that firms that adopt profit sharingexperience lower absenteeism and quit rates(Azfar & Danninger, 2001; Brown, Fakhfakh,& Sessions, 1999; Wilson & Peel, 1991).However, the evidence demonstrating the abil-ity of profit sharing to have a positive impacton organizational performance is supportive,but not universal. In the UK, for example,Blanchflower and Oswald (1988) found no as-sociation between profit sharing and a mea-sure of financial performance among a largesample of establishments, while Wadhwaniand Wall (1990), based on an analysis of 219manufacturing firms, concluded that profitsharing was “much ado about nothing.”

On the other hand, Weitzman and Kruse(1990) and Schulz (1998) found that profitsharing increased productivity by an average of7.4% and 9.1% respectively. Much of this liter-ature presupposes that these schemes generatehigher productivity or profits by inducinggreater worker effort, providing incentives toinvest in skill enhancements, or increasing in-formation flows between employees and man-agers (Kruse, 1992, 1996). The success ofprofit sharing can also be explained as an ap-plication of principal-agent theory (Eisen-hardt, 1988, 1989) since it is a performance-based form of compensation that serves tobetter align the interests of employees, man-agers, and shareholders. Nevertheless, there isgeneral recognition that the processes bywhich profit sharing affects firm performanceare not well understood (Bartol & Durham,2000; Weitzman & Kruse, 1990). Morebroadly, Moynihan, Gardner, and Wright(2002) note that strategic human resourcemanagement has been criticized for its lack oftheoretical specification of the mediatingprocesses through which human resourcepractices may influence organizational out-comes. The authors argue that organizationalcommitment may represent an important me-diating mechanism in the relationship be-tween HR practices (e.g., profit sharing) andorganizational performance.

Florkowski and Schuster (1992) arguethat the diversity of empirical results associ-ated with profit sharing may reflect a failure toconsider employee perceptions of profit shar-ing. Thus, it would seem that the identifica-tion of mediating variables could help explainwhy some profit sharing initiatives are suc-cessful while others are not. Using a cross-sectional survey of 160 employees, the au-thors’ study demonstrates a positiverelationship between perceptions of profitsharing and organizational commitment.While the results of this single, cross-sectionalstudy must necessarily be regarded as tenta-tive, they suggest a fruitful line of inquiry. Inthis study we build upon the Florkowski andSchuster framework by examining the rela-tionship between perceptions of profit sharingand employee attitudes using a longitudinalresearch design. Two complementary percep-tual bases of explanation are proposed: indi-

…two-thirds ofthe U.S. For-tune 1000 firmshave some sortof profit sharingplan and thereis good evidenceto suggest thatfirms that adoptprofit sharingexperiencelower absen-teeism and quitrates.

Profit Sharing to Enhance Employee Attitudes • 425

Consequently,the extent towhich employ-ees perceivethat they can beinstrumental inaffecting theprofitability ofthe organiza-tion, the morepsychologicalownership theywill experience,and the greaterdegree to whichtheir attitudeswill be favor-ably enhanced.

vidual capacity for contribution and organiza-tional reciprocity. The first draws on ex-pectancy theory as a basis for explanation bysuggesting that employees think rationallyabout the connections among effort, perfor-mance, and rewards and that the degree towhich an organization supports these link-ages will have a major bearing on subsequentemployee attitudes. Profit sharing may serveas such a support mechanism. The secondbasis asserts that organizational reciprocity isderived from theories of organizational jus-tice, specifically perceptions of proceduraljustice. The establishment of profit sharingsystems implies the intent of returning to em-ployees a portion of the fruits of their collec-tive labor (i.e., an organizational-level mani-festation of the norms of reciprocity).Employees perceiving high levels of such rec-iprocity attributable to profit sharing arelikely to rate procedural justice highly. Suchassessments, in turn, are asserted to affectsubsequent employee attitudes.

Capacity for Individual Contribution

An underlying assumption of profit sharing isthat employees understand the pay systemand perceive that their collective efforts willhave a bearing on company profitability. Sev-eral studies have documented that under-standing a pay system is strongly related tosatisfaction with the pay system (Brown &Huber, 1992; Judge, 1994). To the extent thatemployees understand how a plan works (in-strumentality perceptions) and can forecasthow it might benefit them (expectancy per-ceptions), employee attitudes may be en-hanced. If, on the other hand, too many fac-tors beyond employees’ control are thought toaffect company profitability (e.g., economicconditions, accounting procedures), theprospects for the plan to have desirable con-sequences are diminished. In addition, em-ployees must perceive that the company willalso engage in whatever actions are necessaryto make the firm competitive and thereforeprofitable. Cable and Wilson (1989), for ex-ample, strongly emphasize the context withinwhich profit sharing is introduced, whichsuggests that the effects of profit sharingmight be highly sensitive to the precise cir-

cumstances where it is deployed. Similarly,Florkowski and Schuster (1992, p. 510) state,“most fundamental, participants must believethat they can significantly affect corporate fi-nancial performance.” In short, how employ-ees perceive the link between their effort andperformance may influence how profit shar-ing affects employee attitudes.

The capacity for individual contribution isalso likely to enhance employee attitudes be-cause it facilitates perceptions of “psychologi-cally experienced ownership.” Psychologicallyexperienced ownership is a state of mindwhere employees feel a target of ownership(e.g., a job, product, employing organization)is “theirs” (Pierce, Kostova, & Dirks, 2001).Following a review of the employee ownershipliterature, Pierce, Rubenfeld, and Morgan(1991) concluded that ownership ties (e.g.,profit sharing) might yield desirable attitudi-nal and behavioral effects through psycholog-ically experienced ownership. More recently,Pierce et al. (2001) identified determinants ofpsychological ownership. A key determinantin their analysis is an innate human desire toexperience causal efficacy in the work envi-ronment (which they term efficacy and ef-fectance). Hence, the capacity to make an in-dividual contribution to the organization is atthe heart of efficacy and effectance. Conse-quently, the extent to which employees per-ceive that they can be instrumental in affect-ing the profitability of the organization, themore psychological ownership they will expe-rience, and the greater degree to which theirattitudes will be favorably enhanced.

Perceptions of Organizational Reciprocity

Profit sharing may also enhance employee at-titudes through mechanisms related to orga-nizational justice (Greenberg, 1996) and no-tions of “fair exchange.” We assert that profitsharing can facilitate perceptions of proce-dural justice (fairness) among all employeegroups within an organization. Even in theface of free-rider problems, the institution ofprofit sharing implies an organization’s intentto share rewards broadly with employees, asopposed to distributing profits solely to man-agers or shareholders. Moreover, proceduraljustice has been shown to affect employees’

426 • HUMAN RESOURCE MANAGEMENT, Winter 2002

trust in leadership and organizationalcommitment (Korsgaard, Schweiger, &Sapienza, 1995; McFarlin & Sweeney, 1992).Profit sharing may also be advantageous be-cause of its symbolic value; that is, it maydemonstrate to employees that managementhas their best interests at heart. Furthermore,Rousseau and Shperling (2000) argue that thedissemination of financial information tolower level employees can increase employees’trust in management. It also suggests thepresence of a corporate culture where em-ployee contributions are valued, setting thestage for the evolution of norms of reciprocity.

This idea has been captured by perceivedorganizational support (POS) developed byEisenberger and his colleagues (1986) to rep-resent employees’ beliefs about “the extent towhich the organization values their contribu-tions and cares about their well-being” (Eisen-berger, Huntington, & Sowa, 1986, p. 501).Adopting a social exchange framework, Eisen-berger et al. (1986) argue that high levels ofPOS create feelings of obligation to recipro-cate through more positive attitudes. As such,employees seek a balance in their exchange re-lationships with organizations by having atti-tudes that are commensurate with the organi-zation’s orientation toward them. Relying onthe norm of reciprocity (Gouldner, 1960),studies support a positive relationship betweenperceived organizational support and organiza-tional commitment (Allen, Shore, & Griffeth,2000; Coyle-Shapiro & Kessler, 2000; Eisen-berger et al., 1986; Meyer & Allen, 1997).

Shore and Shore (1995) note that thepremise of research on antecedents of POS isthat organizational actions are interpreted byan employee as information about the degreeof employer commitment to them, as individ-uals. Therefore, POS is strengthened by fa-vorable work experiences that employees be-lieve reflect discretionary decisions made bythe organization (Rhoades, Eisenberger, &Armeli, 2000). Specifically, opportunities forrewards have been found to be positively as-sociated with POS (Eisenberger, Cummings,Armeli, & Lynch, 1997; Eisenberger,Rhoades, & Cameron, 1999; Guzzo, Noonan,& Elron, 1994). Shore and Shore (1995)identify two types of human resource prac-tices that are positively related to POS: (1)

discretionary practices that imply investmentby the organization and (2) organizationalrecognition. An important aspect of perceivedorganizational support is the degree to whichorganizational actions are viewed as voluntaryrather than the result of external constraints(Shore & Shore, 1995). Eisenberger et al.(1997) found that practices such as rewardsystems, fringe benefits, and training oppor-tunities have a stronger relationship with per-ceived organizational support when employ-ees believed they represented discretionaryactions by the organization. Therefore, theextent to which employees view profit sharingas organizational reciprocity, the more likelythey will reciprocate the organization throughpositive attitudes.

Applebaum, Bailey, Berg, and Kalleberg(2000) note that a major weakness of priorempirical work on high-performance worksystems (HPWSs) is its neglect of worker at-titudes that may help our understanding ofwhy HPWSs might be related to organiza-tional performance. We focus on two atti-tudes—trust in management and organiza-tional commitment—that researchers havehighlighted as important outcomes of humanresource practices (Applebaum et al., 2000).

Trust in Management

Interpersonal trust is gaining prominence asorganizational researchers uncover its bene-ficial impact on numerous outcomes. Trusthas been found to be positively associatedwith organizational citizenship behavior(Podsakoff, MacKenzie, & Bommer, 1996),employee productivity (Mishra & Morrisey,1990) and cooperation (Axelrod, 1984;Deutsch, 1962). The conceptualization oftrust is subject to disciplinary differences(Rousseau, Sitkin, Burt, & Camerer, 1998)with psychologists viewing trust in terms ofattributes of trustors and trustees. Some ac-ademics treat trust as a positive attitude heldby the trustor toward the trustee (Robinson,1996; Whitener, Brodt, Korsgaard, &Werner, 1998). Others adopt more specificdefinitions to include “willingness to be vul-nerable” (Mayer, Davis, & Schoorman,1995), “willingness to rely on another”(Doney, Cannon, & Mullen, 1998) and

Interpersonaltrust is gainingprominence asorganizationalresearchers uncover itsbeneficial impact on numerous outcomes.

Profit Sharing to Enhance Employee Attitudes • 427

Therefore, thedegree to whichemployees perceive profitsharing as reflecting managerialbenevolence(albeit with the existence oftax incentives),their trust inmanagementshould be enhanced.

“confident, positive expectations” (Lewicki,McAllister, & Bies, 1998). Mishra (1996, p.265) presents four dimensions of trust asreflecting the content domain of the trustliterature and defines trust as “one party’swillingness to be vulnerable to anotherparty based on the belief that the latterparty is (a) competent, (b) open, (c) con-cerned, and (d) reliable.”

In view of the importance of trust for in-traorganizational relationships, attention hasfocused on the antecedents of trustworthybehavior. Whitener et al. (1998) argue thatmanagers have considerable impact on build-ing trust and, furthermore, managerial ac-tions and behaviors provide the foundationof trust. The authors present five categoriesof behavior that influence the degree towhich employees perceive managers to betrustworthy among which is benevolence, de-fined as the demonstration of a concern forthe welfare of others (Mayer et al., 1995)and which consists of three managerial ac-tions: showing consideration for employees’needs, acting in ways that protect employeeinterests, and not exploiting employees forthe benefit of managers (Whitener et al.,1998). Applebaum et al. (2000) argue andprovide empirical support for the impact ofhigh-performance work systems (HPWSs) onemployee trust in management. Specifically,they argue that “incentives to enhance moti-vation should increase trust. This is espe-cially true for incentives such as evidence ofthe organization’s commitment to theworker” (p. 175). This draws on the demon-stration of concern for the employee as amanagerial trust enhancing behavior. Profitsharing is included as one practice that re-flects managerial benevolence, which in turnaffects the degree to which employees trusttheir managers (Applebaum et al., 2000).Therefore, the degree to which employeesperceive profit sharing as reflecting manage-rial benevolence (albeit with the existence oftax incentives), their trust in managementshould be enhanced. We examine this withthe following hypothesis:

Hypothesis 1: Employee perceptions oftheir capacity to contribute and organiza-tional reciprocity will be positively associ-

ated with trust in management controllingfor employees’ prior trust in management.

Organizational Commitment

Achieving high levels of organizational com-mitment among employees is frequently men-tioned as an indicator of supportive humanresource management practices and as amechanism for enhancing organizational per-formance (Arthur, 1994; Guest, 1987). Affec-tive commitment, for example, has consis-tently been found to be negatively associatedwith turnover intentions and actual turnover(Cropanzano, James, & Konovsky, 1993;Meyer, Allen, & Smith, 1993; Rhoades et al.,2000; Somers, 1995). However, studies in-vestigating the relationship between affectivecommitment and in-role performance haveyielded mixed results, with meta-analyticfindings supporting only a positive weak cor-relation between organizational commitmentand in-role (i.e., individual level) perfor-mance (Meyer, 1997). Meyer (1997) suggeststhat a potential explanation for the weak linkbetween organizational commitment and per-formance is that the measure of individualperformance may not capture the unique be-haviors that contribute to the performance ofthe overall unit. Two studies conducted at theorganizational level support this assertion(i.e., a stronger positive relationship betweenthe average commitment levels among em-ployees and organizational performance).Benkhoff (1997) reports significant linkagesbetween several measures of organizationalcommitment and branch bank performance(i.e., achieving higher sales targets, increasedprofits). Ostroff (1992) investigated the linkbetween the commitment of teachers andschool performance and found that commit-ment was significantly related to most in-dices of performance in the predicted direc-tion. Thus, there is growing recognition ofthe importance of organizational commit-ment at both individual and organizationallevels of analysis.

Emerging empirical research suggeststhat organizations can influence their em-ployees’ commitment through the adoptionof progressive human resource practicessuch as profit sharing (Huselid, 1995; Poole

428 • HUMAN RESOURCE MANAGEMENT, Winter 2002

& Jenkins, 1998; Meyer, 1997; Wood & deMenzes, 1998). Some researchers view therelationship between human resource prac-tices and organizational commitment as a di-rect one. For example, Florkowski (1987)was among the first to propose such a con-nection as he identified organizational com-mitment as the most immediate determinantof organizational performance in his concep-tual model of the effectiveness of profit shar-ing plans. Similarly, there is empirical sup-port for the positive relationship betweenemployee ownership schemes and organiza-tional commitment (Florkowski & Schuster,1992; Klein, 1987; Klein & Hall, 1988; Wet-zel & Gallagher, 1990). Other researchersview trust as an important intermediary out-come in the relationship between progressivehuman resource practices and organizationalcommitment (Applebaum et al., 2000). Theauthors propose that HPWSs lead to greatertrust in management that in turn leads tohigher organizational commitment. In otherwords, enhanced trust as a result of HPWSsprovides the explanatory mechanism under-lying higher organizational commitment. Weexamine both views by exploring whethertrust in management fully mediates the rela-tionship between perceptions of profit shar-ing and organizational commitment. If thisrelationship is supported, it suggests thattrust in management is an important expla-nation for the effects of perceptions of profitsharing on organizational commitment. Ifnot, it indicates that profit sharing may affectorganizational commitment directly andtrust in management is not necessary for thiseffect to occur.

Hypothesis 2: Employees’ trust in manage-ment will mediate the effects of percep-tions of capacity to contribute and organi-zational reciprocity on organizationalcommitment controlling for employees’prior commitment.

Method

Setting and Participants

Data for this study were obtained from asample of employees in a UK multinational

supplier of aerospace components to theaerospace industry. In the late 1980s, theplant introduced TQM, which attempted toinculcate the values of continuous improve-ment, customer satisfaction, and teamworkthrough a flexible cellular manufacturingstructure. Practices such as communicationsand team briefings, as well as the display ofcell performance measures, served to rein-force the operation of cells as “mini-busi-nesses.” Subsequently, an opportunity arosefor a management buy-out that separated thesite from its multinational owner. This pavedthe way for management to introduce aprofit-related pay scheme, an opportunitythat was not previously available.

The profit sharing scheme introducedby the organization had three central fea-tures: the organization required agreementfrom 80% of the employees; a specifiedfraction of employees’ wage had to be ex-plicitly linked to the profit outcome in ad-vance; and the actual profit-linked pay-ments made to employees were subject totax relief. At the time of this study, full in-come tax relief was available to the individ-ual employee on the lower of 20% of totalpay or the absolute sum of £4000 per year.Profit-linked payments in excess of theseamounts were taxed normally. The obviousbenefit of the tax break to the employee wasthat, even from an unchanged level of grosspay, net pay would be increased. Againstthis was the prospect that the element oftotal pay that was linked to profits wouldturn out to be volatile. If profits fell, so toowould the profit allocation to employees.Total net pay, therefore, became less cer-tain. The organization did not automaticallybenefit in a direct way from the scheme.

Accordingly, management canvassed em-ployees to assess their desire to join thescheme. This canvas was not done well. Itwas preceded by hasty communication aboutthe scheme in which managers, themselvesnot fully understanding it, attempted to ex-plain it to employees. Not surprisingly, the80% participation rate was not attained. Amore considered attempt was subsequentlymade to communicate the benefits of thescheme (i.e., profit sharing represented apossible supplement to their base pay), and

Data for thisstudy were obtained from asample of employees in aUK multina-tional supplierof aerospacecomponents tothe aerospace industry.

Profit Sharing to Enhance Employee Attitudes • 429

Surveys wereadministered on two measurementoccasions: 10months prior toand 20 monthssubsequent tothe introductionof profit sharing.

employees were given time to digest theintricacies of how it would operate. Sixmonths later, the scheme was re-launchedwith a participation rate of virtually 100%(two individuals opted out of the scheme). Atthe time of the second survey, the profit shar-ing scheme was midway through its secondyear of operation. Employees were thereforeaccustomed to its workings and had receivedinterim payments and a final pay out of about4% of their annual salaries seven monthsprior to completing the second survey.

Procedure

Prior to the commencement of this study, thefirst researcher met with management andtrade union representatives separately togain their support for the research. Employ-ees were informed that their participation inthe survey was voluntary and their responseswould remain confidential. Employees com-pleted the surveys during work away fromtheir work area. Surveys were administeredon two measurement occasions: 10 monthsprior to and 20 months subsequent to the in-troduction of profit sharing. At the time ofthe first survey was conducted, none of therespondents was aware of the pending intro-duction of profit sharing. Therefore, the sur-vey responses were not influenced by indi-viduals’ knowledge of the forthcomingintervention.

At Time 1, of the 246 employees asked tocomplete the survey, 206 did so, whichyielded a response rate of 84%. Of the 206who completed the first survey, 141 com-pleted the second survey 2 1/2 years later,yielding a response rate of 68%. The subse-quent analysis is confined to those employ-ees who completed the two surveys. At Time2, the participant group was 91% male, witha mean age of 41.9 years, a mean job tenureand tenure at the site of 6.9 years and 12.1years, respectively. The sample consisted of44% manufacturers, 22% engineers, 13% ad-ministrative/clerical, 12% supervisors/man-agers, 3% research, and 6% in a number ofproduction-related positions. Overall, theparticipant sample was representative of thepopulation on the basis of job type, organiza-tional tenure, and age.

Dependent Variables

Trust in management. This six-item scale wastaken from Cook and Wall (1980, p. 39) whodefined trust in terms of “the extent to whichone is willing to ascribe good intentions toand have confidence in the words and actionsof other people.” This scale captures the twocomponents: faith in the trustworthy inten-tions of others and confidence in the abilityof others. The alpha coefficient for this scalewas .89 and .86 at Time 1 and Time 2, re-spectively. A 7-point scale was used rangingfrom “strongly agree” to “strongly disagree.”

Organizational commitment. Organizationalcommitment was measured at Time 1 andTime 2 using the six positively worded itemsfrom the nine-item scale developed by Cookand Wall (1980) for use in samples of blue-collar employees in the UK. The developmentof the scale draws upon the work of Buchanan(1974) and Porter, Steers, Mowday, and Boul-lian (1974) whereby commitment is viewed ascomprising three interrelated components:identification, involvement, and loyalty. Theauthors report alpha coefficients of .87 and.80 for two independent samples. Other in-vestigators report alpha coefficients of .82(Peccei & Guest, 1993) and .86 (Peccei &Rosenthal, 1997). In this study, organizationalcommitment exhibited an internal consis-tency reliability of .81 at Time 1 and .77 atTime 2. A 7-point scale was used ranging from“strongly agree” to “strongly disagree.”

Independent Variables

Capacity for individual contribution. Thisfive-item scale was developed specifically forthis study to capture the extent to which in-dividuals perceive that they can contribute tothe profitability of the organization. Respon-dents used a 7-point Likert scale. The alphacoefficient of this scale is .73.

Organizational reciprocity. This three-itemscale measures the extent to which respon-dents perceive profit sharing as reflecting aninvestment by the organization in its employ-ees using a 7-point Likert scale. This scalehas an alpha coefficient of .71.

430 • HUMAN RESOURCE MANAGEMENT, Winter 2002

Analysis

Hierarchical regression analysis was used totest the hypotheses using the Time 1 andTime 2 data. Prior research has demon-strated that attitudes and behaviors at workcan be influenced by demographic character-istics (Mowday, Porter, & Steers, 1982).Therefore, we included three demographicvariables (gender, age, and organizationaltenure) to reduce the possibility of spuriousrelationships based on these types of per-sonal characteristics. In all equations, wecontrol for the dependent variable at Time 1.To test Hypothesis 1, we entered the demo-graphic variables and trust in management atTime 1 in step 1. In step 2, we entered theprofit sharing factors: capacity for individualcontribution and organizational reciprocity.By entering the profit sharing factors in asubsequent step, this allows us to examinethe unique, if any, contribution made by theprofit sharing factors to explaining variancein trust in management at Time 2.

To test Hypothesis 2, we followed theprocedures recommended by Baron andKenny (1986) for testing mediation. First,the mediator (trust in management) is re-gressed on the independent variables (capac-ity to contribute and organizational reciproc-ity); second, the dependent variable(organizational commitment) is regressed onthe independent variables (capacity to con-tribute and organizational reciprocity); andthird, the dependent variable (organizational

commitment) is regressed simultaneously onthe independent (capacity to contribute andorganizational reciprocity) and mediator(trust in management) variables. Mediationis present if the following conditions holdtrue: the independent variable affects themediator in the first equation; the inde-pendent variable affects the dependent vari-able in the second equation; and the media-tor affects the dependent variable in thethird equation. The effect of the independ-ent variable on the dependent variable mustbe less in the third equation than in the sec-ond. Full mediation occurs if the independ-ent variable has no significant effect whenthe mediator is controlled and partial medi-ation occurs if the effect of the independentvariable is smaller but significant when themediator is controlled.

Results

Table I presents the means, standard devia-tions, and intercorrelations of the scales. Thestandard deviations of the main study vari-ables ranged from .85 to 1.30, suggestingthat none of the variables are excessively re-strictive in range. The results of paired sam-ple t-tests indicate that trust in management(T1 = 3.61, T2 = 4.25) and organizationalcommitment (T1 = 4.96, T2 = 5.46) signifi-cantly increased (p < .01) between Time 1and Time 2. The two dependent variableshad a correlation of .62 suggesting that theywere moderately related. Similar correlations

Descriptive Statistics and Correlations.

Mean SD 1 2 3 4 5 6 7 8 9

1. Gender T1 0.09 (0.21)2. Age T1 39.32 (9.84) –.173. Organizational tenure T1 9.05 (6.40) .03 .334. Trust in management T1 3.61 (1.30) .19 .20 .105. Organizational commitment T1 4.96 (0.99) .12 .19 .11 .656. Trust in management T2 4.25 (1.01) .12 .08 –.04 .50 .357. Organizational commitment T2 5.46 (0.85) .17 .07 .00 .29 .39 .628. Capacity for individual 3.89 (1.05) .13 –.08 .04 .17 .20 .27 .36

contribution T2

9. Organizational reciprocity T2 3.61 (1.27) .16 .06 –.07 .28 .51 .54 .46 .25 —

Correlations > .28 are statistically significant at p < .01. Correlations > .16 are statistically significant at p < .05.

TABLE I

Profit Sharing to Enhance Employee Attitudes • 431

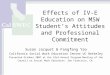

have been found between organizationalcommitment and perceived organizationalsupport (Rhoades et al., 2000) and Cook andWall (1980) report a correlation of .58 be-tween organizational commitment and trust.Consequently, we conducted a factor analy-sis to determine the factorial independenceof the two constructs. The results (principalcomponents with varimax rotation) are pre-sented in Table II and show a two-factor so-lution with eigenvalues greater than 1.0. Allof the items loaded above .50 on the appro-priate factor and demonstrated a differenceof at least .20 between this loading and thenext highest loading, thus supporting the in-dependence of the two attitudes. We alsofactor analyzed the profit sharing items sincethey were designed explicitly for this study. Atwo-factor solution emerged (Table III); thefirst factor reflected “capacity for individualcontribution: and the second reflected “orga-nizational reciprocity.”

Hypothesis 1 predicted that there wouldbe a positive relationship between percep-tions of profit sharing and employees’ trustin management. The results presented inTable IV (column 2) provide partial supportfor hypothesis 1. Controlling for prior trustand the demographic variables, perceptions

of organizational reciprocity is positively as-sociated with trust in management (β = .41,p < .01) but no significant effect was foundfor capacity for individual contribution.Overall, the inclusion of perceptions ofprofit sharing explains unique variance intrust in management (∆F = 21.42, ∆R2 =.18, p < .01).

As capacity for individual contributionis not significantly related to trust in man-agement, condition 1 of mediation is notfulfilled so trust cannot mediate the effectsof capacity to contribute on organizationalcommitment. However, an individual’s per-ception of their capacity to contribute is di-rectly and significantly related to organiza-tional commitment (β = .18, p < .01) aftercontrolling for trust in management. Turningto the mediating role of trust in manage-ment, the results of Hypothesis 1 fulfill con-dition 1 for organizational reciprocity. TableIV (column 4) shows the fulfillment of con-dition 2 in establishing a relationship be-tween perceptions of organizational reciproc-ity and organizational commitment. Theinclusion of perceptions of profit sharing ex-plains additional variance in organizationalcommitment at Time 2 (∆F = 20.96, ∆R2 =.20, p < .01). When trust in management

Results of Factor Analysis of Dependent Variable Items (Trust in Management and Organizational Commitment)

Factor Items 1 2

Management is sincere in its attempts to meet the workers’ point of view. .79 .31Management at work seems to do an efficient job. .75 .21Management can be trusted to make sensible decisions for the firm’s future. .75 .24Management would be quite prepared to gain advantage by deceiving the workers. ‡ .70 .18I feel confident that __ will always try to treat me fairly. .70 .31Our __ has a poor future unless it can attract better managers. ‡ .64 .14

Even if __ were not doing too well financially, I would be reluctant to change to another employer. .13 .79The offer of a bit more money with another employer would not seriously make me think of changing my job. .12 .77In my work, I like to feel I am making some effort, not just for myself but for __ as well. .33 .73I feel myself to be part of __. .40 .73To know that my own work had made a contribution to the good of __ would please me. .25 .70I am quite proud to tell people I work for __. .34 .64

Eigenvalue 5.90 1.37Percentage of variance explained 49.2 11.4

‡ reversed scored __ name of organization

TABLE II

432 • HUMAN RESOURCE MANAGEMENT, Winter 2002

and organizational reciprocity are simulta-neously included in the equation (Table IV,column 5), the results suggest that trust inmanagement partially mediates the effectof organizational reciprocity on organiza-tional commitment (the beta coefficient of

organizational reciprocity reduces from.34, p < .01 to .15, p < .05 when trust is inthe equation). Therefore, Hypothesis 2 ispartially supported in relation to the effectof organizational reciprocity but not to ca-pacity to contribute.

Results of Factor Analysis of Profit-Sharing Items

Factor Items 1 2

The problem with profit sharing is that we never know how much we are going to make out of it.a .72 –.21 Profits are a bad basis for pay because they are affected by factors outside the control of the workforce.a .68 –.26 Profit sharing is really too complicated to be an effective incentive.a .68 –.39 It is hard to see how my work alone can affect ___’s profits.a .62 .11 Under profit sharing, there is no point in me making more effort if other people do not do the same.a .61 .03

Profit sharing shows that management is looking after employee interests. –.12 .86 Profit sharing is a way of ___ saying “thank you” for all my hard work. .03 .78 Profit sharing does not fairly reward employees for their contribution to the profits of ___.a –.17 .69

Eigenvalue 2.91 1.46 Percentage of variance explained 36.4 18.3

aReverse-scored.

TABLE III

Results of Hierarchical Regression Analysis Predicting Trust in Management andOrganizational Commitment

Trust in management T2 Organizational commitment T2

Variable Step 1 Step 2 Step 1 Step 2 Step 3

Step 1—Controls Gender T1 .03 –.02 .13 .06 .06 Age T1 .01 .00 .04 .04 .02 Organizational tenure T1 –.10 –.06 –.06 –.03 –.01 Dependent variable T1 .51** .37** .37** .29** .18**

Step 2—Profit SharingCapacity for individual contribution T2 – .10 – .22** .18** Organizational reciprocity T2 – .41** – .34** .15*

Step 3—Trust in management T2 – – – – .41**

F 12.02** 17.56** 7.08** 13.09** 17.40** Change in F 12.02** 21.42** 7.08** 20.96** 27.61** Change in R2 .26 .18 .17 .20 .11 Adjusted R2 .24 .42 .14 .34 .45

*p < .05. **p < .01.

TABLE IV

Profit Sharing to Enhance Employee Attitudes • 433

The results ofthis study helpexplain whyprofit sharing, acompensation-related humanresource practice, generates favorable outcomes.

Discussion

Our findings confirm and extend empiricalresearch (Florkowski & Schuster, 1992) sup-porting the importance of employee percep-tions of profit sharing in achieving desiredattitudinal outcomes. Against the backdropof a paucity of research on employee’s reac-tions to innovative pay plans (Dulebohn &Martocchio, 1998), our results confirm thatplans that engender positive perceptions leadto higher levels of trust and organizationalcommitment.

Perhaps more importantly, this researchsheds light on the underlying mechanismsthrough which profit sharing can affect em-ployee attitudes. Our findings suggest thatperceptions of profit sharing have a differ-ential effect on our attitudinal outcomes.First, capacity to contribute is significantlyrelated to organizational commitment but isunrelated to trust in management. Second,if employees view profit sharing as an act ofreciprocity, their trust in management andorganizational commitment will both be en-hanced. Finally, trust in management is nota necessary precondition for perceptions oforganizational reciprocity to enhance orga-nizational commitment. In other words, aprofit sharing perception grounded in orga-nizational reciprocity is a powerful an-tecedent because it affects organizationalcommitment independently and/or throughits ability to enhance trust (i.e., the impactof organizational reciprocity on organiza-tional commitment is not simply an artifactof its ability to increase trust). Our findingsparallel those of Applebaum et al. (2000) inthat human resource practices (in this case,profit sharing) can enhance employees’ trustin management and organizational commit-ment. However, our point of departure isthat trust in management does not fully ex-plain the effects of profit sharing on organi-zational commitment.

The results of this study help explain whyprofit sharing, a compensation-relatedhuman resource practice, generates favor-able outcomes. Moreover, the study findingsare consistent with several well-establishedmanagement theories. Drawing on the tenetsof principal–agent theory (Eisenhardt, 1988,

1989), profit sharing can be seen as a way toalign the goals of management and employ-ees. When employees perceive profit sharingfavorably, commitment and trust increase,encouraging employees to exert maximum ef-fort, share information, and invest in firm-specific training that may not be valued out-side of the firm. Turning to the specificcomponents of profit sharing studied here,the results further explain why profit sharingcan be beneficial by drawing on core ideasfrom expectancy theory (i.e., individual ca-pacity for contribution) and organizationaljustice theory (i.e., organizational reciproc-ity). It is perhaps the joint use of these well-established models that accounts for thestrength of the findings.

The results associated with capacity forcontribution were not as strong in that a sig-nificant positive relationship was detectedonly for organizational commitment and notfor trust in management. It may be that anindividual’s belief that he/she has the capac-ity to contribute to the profitability of the or-ganization is related to commitment and nottrust because the attitudinal targets are dif-ferent. Perceptions of ability to contribute tothe bottom line of the organization and orga-nizational commitment are more closelybound because they share a common refer-ent, “the organization.” The organizationalreferent also embraces the entire employeemembership and is based on a historical timespan of some duration (i.e., the employee’stenure). Trust in management refers to per-ceptions of a narrower range of individuals(i.e., those identified as “management”) andwho may be more transient in organizationalmembership than rank-and-file employees.The perception of an ability to contributemay also be more stable or enduring andthus linked more closely to organizationalcommitment, than an attitude like trust inmanagement which may be more susceptibleto change associated with day-to-day interac-tions with managerial personnel. Finally, athird factor that might account for the dif-ferent findings in trust and commitment isthat employees may simply see their personalinterests, as reflected in capacity for individ-ual contribution to profitability, and the or-ganization’s interests as more closely aligned

434 • HUMAN RESOURCE MANAGEMENT, Winter 2002

than personal interests and management in-terests. Future research is needed to explorethese possibilities, along with a broader con-sideration of other employee attitudes.

Implications

These findings have implications for practi-tioners charged with implementing profitsharing programs. Our findings suggest thatwhen profit sharing is perceived as both anopportunity for individual input to the orga-nization’s success and a reflection of the or-ganization’s desire to treat employees fairly,higher levels of commitment follow. Struc-turing profit sharing systems to enhance per-ceptions of input (e.g., some portion of theprofit sharing based on individual contribu-tion to performance) and reciprocity (e.g.,some portion based on years of service)would seem advantageous. Drawing on theexpectancy basis of the capacity for individ-ual contribution findings, practitionersshould expect more positive attitudes amongemployees if they distribute profit sharingproceeds as often as possible, as opposed toplacing such funds in a deferred retirementplan, since the deferred approach entails agreater time lag between effort and rewards.Similarly, explicitly “rolling out” profit shar-ing as a desire on the part of management todistribute rewards more fairly shouldheighten trust in management.

Moreover, employee perceptions of profitsharing may prove useful in understandingthe extent to which a genuine change in em-ployee attitudes is occurring. Stated differ-ently, change initiatives ought to be intro-duced and implemented so as to maximizefavorable employee perceptions of the initia-tive. For some time, academics have arguedthat employee participation in organizationalchange is fundamental to their acceptance ofchange. Jenkins and Lawler (1981), for ex-ample, argue that employees’ participation inthe decision to implement a pay systemchange will enhance their commitment tothe new system. Similarly, McClurg’s (2001)recent findings and recommendations forimplementing team-based pay underscorethe importance of extensive and ongoingcommunication in garnering support for

group-based reward systems. Kim’s (1999)empirical work, illustrating that gainsharingprograms implemented through an employeemajority vote are more likely to survive thanthose programs implemented without a vote,is especially relevant to this research. In ourstudy, employee participation in the decisionto implement profit sharing may not onlyhave influenced the acceptance of the pro-gram but also how employees interpreted theunderlying organizational motives. Conse-quently, an early assessment of employee re-actions provides an opportunity to gaugewhether desired perceptual changes are oc-curring and perhaps to discover unantici-pated problems (e.g., an overall resistance tochange, perceived lack of support from topmanagement, or so-called free-rider prob-lems where employees perceive that othersmay not contribute their fair share of effortunder a group-based reward system).

Limitations

As with the majority of studies, this study hasits limitations. First, because this study wasconducted in only one organization, replica-tions in other organizations over longer timespans will be required before any firm con-clusions can be drawn. Second, the absenceof a control group (nearly 100% of employeesvoted to adopt the plan) makes it difficult toeliminate alternative explanations for thefindings. Our respondents may have useddifferent frames of reference to complete thesurveys over the 2 1/2-year period. Therewere no other readily discernible, concur-rent factors that might account for these re-sults. Given that our results were consistentwith prior research examining human re-source practices on employee attitudes, andprofit sharing was the most notable changeduring the period of investigation, our confi-dence in attributing these results to profitsharing is bolstered.

Another possible limitation is that all thevariables were measured with self-report sur-vey measures. Consequently, the observedrelationships may have been artificially in-flated as a result of respondents’ tendenciesto respond in a consistent manner. However,more recent meta-analytic research on the

Our findingssuggest thatwhen profitsharing is per-ceived as bothan opportunityfor individualinput to the or-ganization’ssuccess and areflection of theorganization’sdesire to treatemployeesfairly, higherlevels of com-mitment follow.

Profit Sharing to Enhance Employee Attitudes • 435

This studysought to address these issues by relating profitsharing to established theories ofhuman behavior(i.e., principal–agent, expectancy,and organiza-tional justicemodels) and bypositioningprofit sharingin the contextof attitudechange.

percept-percept inflation issue indicates thatwhile this problem continues to be com-monly cited, the magnitude of the inflationof relationships may be over-estimated(Crampton & Wagner, 1994). In addition,the measures used to assess perceptions ofprofit sharing were expressly designed forthis study and do not have establishedrecords of reliability and validity. Further-more, this study did not include possiblenegative reactions to the profit sharingscheme. Nor, unfortunately, did the researchsetting allow us to assess whether profit shar-ing and/or enhanced employee attitudes re-sulted in higher levels of performance asmeasured by objective means. Future re-search efforts should seek to include suchmeasures. Finally, despite the demonstrationof the positive effects of profit sharing shownhere, profit sharing may have inherent limi-tations. The implementation of profit sharingand accompanying alterations in human re-source management systems tend to increaselabor costs, and there is some evidence thatthese increased costs can outweigh produc-tivity and profitability gains (Kim, 1998).

Future research could pursue several av-enues of investigation. Further research ex-ploring potential antecedents of employeereactions to profit sharing plans may provideinsight into the manageability of perceptionsof organizational change. These types of an-tecedents may include specific features ofthe plan, contextual factors, and individualdifferences. For example, Dulebohn andMarticchio (1998) have shown, albeit in across-sectional research design, that under-standing of a work group pay plan is linkedto perceptions of fairness of the plan.Specifically, they advocate managerial inter-ventions to explain and verify employee un-derstanding of group-based pay plans. Ourresults support the importance of early as-sessment of employee perceptions ofchanges in compensation plans but clearlymuch more research is needed. Contextualfeatures might include how informationrelated to profit sharing is disseminated toemployees. More frequent and detailedcommunication to employees about organi-zational performance might serve tostrengthen individuals’ perceptions of their

personal contribution, and in the case of lowperformance, lead to changes in work-re-lated behavior. Individual differences rele-vant to managing organizational changemight include personality traits such asopenness to experience. Selection and re-tention of employees who seek and appreci-ate new experiences may facilitate adoptionof change. Another research opportunitymight be to study the role of self-efficacy.Based on the results of this study, we wouldhypothesize that individuals high in need forself-efficacy will embrace profit sharingwhen they perceive their capacity for contri-bution to be high, but will reject profit shar-ing when they perceive their capacity forcontribution to be low.

Conclusions

Interest in profit sharing and other forms ofgroup-based compensation continues todraw considerable attention from practition-ers and deserves more consideration from ac-ademic scholars. Employees and managerspersist in reporting enhanced satisfactionwith profit sharing compensation systems(Florkowski & Schuster, 1992) yet, empiricalevidence of the impact of profit sharing isrelatively scarce and mixed. The underlyingcausal mechanisms as to why profit sharingshould enhance employee attitudes have notbeen adequately specified (i.e., profit sharingresearch is seldom tied to theoretical modelsseeking to explain why profit sharing shouldbe beneficial). This study sought to addressthese issues by relating profit sharing to es-tablished theories of human behavior (i.e.,principal–agent, expectancy, and organiza-tional justice models) and by positioningprofit sharing in the context of attitudechange. Stated differently, hypotheses de-rived from established theoretical modelsand previous empirical work guided the re-search, thereby contributing to both explana-tion and prediction. In addition, this studysought to strengthen the causal inferencesregarding the effects of profit sharing by as-sessing its effects on attitude change longitu-dinally. Pretest attitude data (i.e., trust inmanagement and organizational commit-ment at Time 1) have rarely been incorpo-

436 • HUMAN RESOURCE MANAGEMENT, Winter 2002

rated in compensation studies (Dulebohn &Marticchio, 1998). This approach, coupledwith the results obtained here, revealed agreat deal about the interplay among profitsharing, how it is perceived, and subsequent

impact on employee attitudes. We are hope-ful that these results will stimulate others toengage in further research to discover addi-tional circumstances under which profitsharing systems can be advantageous.

Jacqueline A-M. Coyle-Shapiro is a Lecturer in Industrial Relations at the Lon-don School of Economics. Dr. Coyle-Shapiro’s research interests include psychologi-cal contracts, the employment relationship, organizational citizenship behavior, andorganizational change. Her published work has appeared in such journals as the Jour-nal of Applied Behavioral Science, Journal of Management Studies, European Journalof Work and Organizational Psychology, and the Journal of Vocational Behavior.

Paula C. Morrow is a University Professor of Management at Iowa State Universityin Ames, Iowa. Her research has focused on understanding employee attitudes andbehaviors, especially work commitment and employee loyalty. She has published over50 management-related publications in outlets that include the Journal of Applied Psy-chology, the Journal of Organizational Behavior, and the Journal of Vocational Behav-ior. She recently co-completed a major project for the U.S. Department of Trans-portation on the relationship between driver work scheduling practices and safetyperformance among commercial motor vehicle firms.

Ray Richardson is currently Deputy Director at the London School of Economics(where he has a joint appointment in the Interdisciplinary Institute of Managementand the Department of Industrial Relations); he is also a part-time Professor at Eras-mus University in Rotterdam. He has worked as a special advisor for the UK Govern-ment and as a consultant for international organizations, private firms, and tradeunions. His principal research focuses recently have been HR Strategies and the eval-uation of different forms of contingent pay (employee share ownership schemes,profit related pay, merit pay, etc.).

Stephen R. Dunn is a Lecturer in Industrial Relations at the London School of Eco-nomics. His current research interests include the impact of employment law, man-agement of employment relations, and public policy issues. He has published a streamof articles in journals such as the British Journal of Industrial Relations and HumanResource Management Journal.

REFERENCES

Allen, D.G., Shore, L.M., & Griffeth, R.W. (2000).The role of perceived organizational support inthe voluntary turnover process. Manuscriptunder review.

Applebaum, E., Bailey, T., Berg, P., & Kelleberg,A.L. (2000). Manufacturing advantage: Whyhigh-performance work systems pay off. Ithaca,NY: Cornell University Press.

Arthur, J.B. (1994). Effects of human resource sys-tems on manufacturing performance and

turnover. Academy of Management Journal, 37,670–687.

Axelrod, R. (1984). The evolution of cooperation.New York: Basic Books.

Azfar, O., & Danninger, S. (2001). Profit-sharing,employment stability, and wage growth. Indus-trial and Labor Relations Review, 54, 619–630.

Baron, R.M., & Kenny, D.A. (1986). The modera-tor-mediator distinction in social psychologicalresearch: Conceptual, strategic and statisticalconsiderations. Journal of Personality and So-cial Psychology, 51, 1173–1182.

Profit Sharing to Enhance Employee Attitudes • 437

Bartol, K.M., & Durham, C.C. (2000). Incentives:Theory and practice. In C.L. Cooper & E.A.Locke (Eds.), Industrial and organizational psy-chology (pp. 1–33). Oxford, UK: Blackwell.

Benkhoff, B. (1997). Ignoring commitment is costly:New approaches establish the missing link be-tween commitment and performance. HumanRelations, 50, 701–726.

Blanchflower, D.G., & Oswald, A.J. (1988). Profit-related pay: Prose discovered. Economic Jour-nal, 98, 720–730.

Blasi, J., Conte, M., & Kruse, D. (1996). Employeestock ownership and corporate performanceamong public companies. Industrial and LaborRelations Review, 50, 60–79.

Brown, K.A., & Huber, V.L. (1992). Lowering floorand raising ceilings: A longitudinal assessment ofthe effects of an earnings at-risk plan on pay sat-isfaction. Personnel Psychology, 45, 279–311.

Brown, S., Fakhfakh, F., & Sessions, J.G. (1999).Absenteeism and employee sharing: An empiri-cal analysis based on French panel data,1981–1991. Industrial and Labor Relations Re-view, 52, 234–251.

Buchanan, B. (1974). Building organizational com-mitment: The socialization of managers in workorganizations. Administrative Science Quar-terly, 19, 533–546.

Cable, J., & Wilson, N. (1989). Profit-sharing andproductivity: An analysis of U.K. engineeringfirms. Economic Journal, 99, 366–375.

Cook, J., & Wall, T. (1980). New work attitude mea-sures of trust, organizational commitment andpersonal need non-fulfillment. Journal of Occu-pational Psychology, 53, 39–52.

Cooke, W.N. (1994). Employee participation pro-grams, group-based incentives, and companyperformance: A union-nonunion comparison.Industrial and Labor Relations Review, 47,594–609.

Coyle-Shapiro, J., & Kessler, I. (2000). Conse-quences of the psychological contract for theemployment relationship: A large scale survey.Journal of Management Studies, 37, 903–930.

Crampton, S.M., & Wagner, J.A. (1994). Percept-percept inflation in microorganizational re-search: An investigation of prevalence and ef-fect. Journal of Applied Psychology, 79, 67–76.

Cropanzano, R., James, K., & Konovsky, M.A.(1993). Dispositional affectivity as a predictorof work attitude and job performance. Journalof Organizational Behavior, 14, 595–606.

Deutsch, M. (1962). Cooperation and trust: Sometheoretical notes. In M.R. Jones (Ed.) NebraskaSymposium on Motivation (pp. 275–317). Lin-coln: University of Nebraska Press.

Doney, P.M., Cannon, J.P., & Mullen, M.R. (1998).Understanding the influence of national cultureon the development of trust. Academy of Man-agement Review, 23, 601–620.

Dulebohn, J.H., & Martocchio, J.J. (1998). Em-ployee perceptions of the fairness of work groupincentive pay plans. Journal of Management,24, 469–488.

Eisenberger, R., Cummings, J., Armeli, S., & Lynch,P. (1997). Perceived organizational support, dis-cretionary treatment, and job satisfaction. Jour-nal of Applied Psychology, 82, 812–820.

Eisenberger, R.R., Huntington, S.H., & Sowa, D.(1986). Perceived organizational support. Jour-nal of Applied Psychology, 71, 500–507.

Eisenberger, R., Rhoades, L., & Cameron, J. (1999).Does pay for performance increase or decreaseperceived self-determination and intrinsic moti-vation? Journal of Personality and Social Psy-chology, 77, 1026–1040.

Eisenhardt, K.M. (1988). Agency- and institutional-theory explanations: The case of retail salescompensation. Academy of Management Jour-nal, 31, 488–511.

Eisenhardt, K.M. (1989). Agency theory: An assess-ment and review. Academy of Management Re-view, 14, 57–74.

Florkowski, G.W. (1987). The organizational impactof profit sharing. Academy of Management Re-view, 12, 622–636.

Florkowski, G.W., & Schuster, M.H. (1992). Sup-port for profit sharing and organizational com-mitment: A path analysis. Human Relations, 45,507–523.

Gouldner, A.W. (1960). The norm of reciprocity.American Sociological Review, 25, 161–178.

Greenberg, J. (1996). The quest for justice on thejob. Thousand Oaks, CA: Sage.

Guest, D. (1987). Human resource managementand industrial relations. Journal of Manage-ment Studies, 24, 503–521.

Guzzo, R.A., Noonan, K.A., & Elron, E. (1994). Expa-triate managers and the psychological contract.Journal of Applied Psychology 79, 617–626.

Hammer, T. (1988). New developments in profitsharing. In J. Campbell, R. Campbell & Associ-ates (Eds.), Productivity in organizations (pp.328–366). San Francisco: Jossey-Bass.

438 • HUMAN RESOURCE MANAGEMENT, Winter 2002

Huselid, M. (1995). The impact of human resourcemanagement practices on turnover, productiv-ity, and corporate financial performance. Acad-emy of Management Journal, 38, 635–672.

Jenkins, D.G., & Lawler, E.E. (1981). Impact of em-ployee participation on pay plan development.Organizational Behavior and Human Perfor-mance, 28, 111–128.

Judge, T.A. (1994). Validity of the dimensions of thepay satisfaction questionnaire: Evidence of dif-ferential prediction. Personnel Psychology, 46,331–355.

Kim, Dong-One. (1999). Determinants of the sur-vival of gainsharing programs. Industrial &Labor Relations Review, 53, 21–42.

Kim, S. (1998). Does profit sharing increase firms’profits? Journal of Labor Research, 19, 351–371.

Klein, K.J. (1987). Employee stock ownership andemployee attitudes: A test of three models. Jour-nal of Applied Psychology, 72, 319–332.

Klein, K.J., & Hall, R.J. (1988). Correlates of em-ployee satisfaction with stock ownership: Wholikes an ESOP most? Journal of Applied Psy-chology, 73, 630–638.

Korsgaard, M.A., Schweiger, D.M., & Sapienza, H.J.(1995). Building commitment, attachment, andtrust in strategic decision-making teams: Therole of procedural justice. Academy of Manage-ment Journal, 38, 60–84.

Kruse, D. L. (1992). Profit-sharing and productivity:Microeconomic evidence from the UnitedStates. Economic Journal, 102, 24–36.

Kruse, D. (1993). Profit sharing: Does it make a dif-ference?. Kalamazoo, Michigan: W.E. UpjohnInstitute for Employment Research.

Kruse, D. (1996). Why do firms adopt profit-sharingand employee ownership plans? British Journalof Industrial Relations, 34, 515–538.

Lawler, E., Mohrman, S., & Ledford, G.R. (1995).Creating high performance organizations. SanFrancisco: Jossey-Bass.

Lewicki, R.J., McAllister, D.J., & Bies, R.J. (1998).Trust and distrust: New relationships and reali-ties. Academy of Management Review, 23,438–458.

Mayer, R.C., Davis, J.H., & Schoorman, F.D.(1995). An integrative model of organizationaltrust. Academy of Management Review, 20,709–734.

McClurg, L.N. (2001). Team rewards: How far havewe come? Human Resource Management, 40,73–86.

McFarlin, D.B., & Sweeney, P.D. (1992). Distribu-tive and procedural justice as predictors of sat-isfaction with personal and organizational out-comes. Academy of Management Journal, 35,626–637.

McKersie, R.B. (1986). The promise of gainsharing.ILR Report, 24, 7–11.

Meyer, J.P. (1997). Organizational commitment. InC.L. Cooper & I. T. Robertson (Eds.), Interna-tional review of industrial and organizationalpsychology (Vol. 12, 175–228). New York: Wiley.

Meyer, J.P., & Allen, N.J. (1997). Commitment inthe workplace: Theory, research and applica-tion. Thousand Oaks, CA: Sage.

Meyer, J.P., Allen, N.J., & Smith, C.A. (1993). Com-mitment to organizations and occupations: Ex-tension and test of a three-component concep-tualization. Journal of Applied Psychology, 75,710–720.

Mishra, A.K. (1996). Organizational responses tocrisis: The centrality of trust. In R.M. Kramer &T.R. Tyler, (Eds.) Trust in organizations: Fron-tiers of theory and research (pp. 261–287).Thousand Oaks, CA: Sage.

Mishra, J., & Morrissey, M A. (1990). Trust in em-ployee/employer relationships: A survey of WestMichigan managers. Public Personnel Manage-ment, 19, 443–485.

Mowday, R.T., Porter, L.W., & Steers, R.M (1982).Employee-organizational linkages: The psychol-ogy of commitment, absenteeism, and turnover.New York: Academic Press.

Moynihan, L.M. Gardner, T.M., & Wright, P.M.(2002). High performance HR practices andcustomer satisfaction: Employee process mech-anisms. Working paper, Center for AdvancedHuman Resource Studies, Cornell University.

Ogden, S.G. (1995). Profit sharing and organiza-tional change. Accounting, Auditing & Account-ability Journal, 8, 23–47.

Ostroff, C. (1992). The relationship between satis-faction, attitudes, and performance: An organi-zational level analysis. Journal of Applied Psy-chology, 77, 963–974.

Peccei, R., & Guest, D. (1993). The dimensionalityand stability of organizational commitment.Discussion Paper No. 149, Centre for Eco-nomic Performance, London School of Eco-nomics: London.

Peccei, R., & Rosenthal, P. (1997). The antecedentsof commitment to customer service: Evidencefrom the UK service context. International

Profit Sharing to Enhance Employee Attitudes • 439

Journal of Human Resource Management, 8,66–86.

Pierce, J.L., Kostova, T., & Dirks, K.T. (2001). To-ward a theory of psychological ownership in or-ganizations. Academy of Management Review,26, 298–310.

Pierce, J.L., Rubenfeld, S.A., & Morgan, S. (1991).Employee ownership: A conceptual model ofprocess and effects. Academy of ManagementReview, 16, 121–144.

Podsakoff, P.M., MacKenzie, S.B., & Bommer, W.H.(1996). Transformational leadership behaviorsand substitutes for leadership as determinantsof employee satisfaction, commitment, trust,and organizational citizenship behavior. Journalof Management, 22, 259–298.

Poole, M., & Jenkins, G. (1998). Human resourcemanagement and the theory of rewards: Evi-dence from a national survey. British Journal ofIndustrial Relations, 36, 227–247.

Porter, L.W., Steers, R.M., Mowday, R.T., & Boul-lian, P.V. (1974). Organizational commitment,job satisfaction, and turnover among psychiatrictechnicians. Journal of Applied Psychology, 59,603–609.

Rhoades, L., Eisenbereger, R., & Armeli, S. (2000).Employee commitment to the organization: Thecontribution of perceived organizational sup-port. Paper presented at the Annual Meeting ofthe Academy of Management, Toronto.

Robinson, S.L. (1996). Trust and breach of the psy-chological contract. Administrative ScienceQuarterly, 41, 574–599.

Rousseau, D.M., & Shperling, Z. (2000). Pieces ofaction: Ownership, power and the psychologicalcontract. Paper presented at the Annual Meet-ing of the Academy of Management, Toronto.

Rousseau, D.M, Sitkin, S.B., Burt, R.B., & Camerer,C. (1998). Not so different after all: A cross dis-cipline view of trust. Academy of ManagementReview, 23, 393–404.

Schulz, E.R. (1998). The influence of group incen-tives, training, and other human resource prac-tices on firm performance and productivity. Dis-sertation Abstracts International, 58(11-A), 4459.

Schwochau, S., Delaney, J., Jarley, P., & Fiorito, J.(1997). Employee participation and assess-ments of support for organizational policychanges. Journal of Labor Research, 18(3),379–402.

Shore, L.M., & Shore, T.H. (1995). Perceived orga-nizational support and organizational justice. In

R.S. Cropanzano & K.M. Kacmar (Eds.), Orga-nizational politics, justice and support: Manag-ing the social climate of the workplace (pp.149–164). Westport, CT: Quorum Books.

Somers, M.J. (1995). Organizational commitment,turnover and absenteeism: An examination ofdirect and interaction effects. Journal of Orga-nizational Behavior, 16, 49–58.

Wadhwani, S., & Wall, M. (1990). The effects ofprofit-sharing on employment, wages, stock re-turns and productivity: Evidence from micro-data. Economic Journal, 100, 1–17.

Weitzman, M.L. (1995). Incentive effects of profitsharing. In H. Siebert (Ed.), Trends in businessorganization: Do participation and cooperationincrease competitiveness? (pp. 51–87). Interna-tional workshop/Institut für Weltwirtschaft ander Universität Kiel. Tubingen: J.C.B. Mohr.

Weitzman, M., & Kruse, D. (1990). Profit sharingand productivity. In A. Blinder (Ed.), Paying forproductivity (pp. 95–142). Washington, DC:Brookings Institute.

Wetzel, K.W., & Gallagher, D.G. (1990). A compar-ative analysis of organizational commitmentamong workers in the cooperative and privatesectors. Economic and Industrial Democracy,11, 93–109.

Whitener, E.M., Brodt, S.E., Korsgaard, M.A., &Werner, J.M. (1998). Managers as initiators oftrust: An exchange relationship framework forunderstanding managerial trustworthy behavior.Academy of Management Review, 23, 513–530.

Wilson, N., & Peel, M.J. (1991). The impact of ab-senteeism and quits of profit-sharing and otherforms of employee participation. Industrial andLabor Relations Review, 44, 454–468.

Wood, S., & de Menezes, L. (1998). High commit-ment management in the UK: Evidence fromthe Workplace Industrial Relations Survey, andEmployers’ Manpower and Skills Practices Sur-vey. Human Relations, 51, 485–515.

ENDNOTES

The authors wish to thank John Kellyand Donald Verry for their comments on aprevious draft of this article. We also thankthe three anonymous reviewers whose com-ments greatly improved this paper. The assis-tance of Dawn Fell, Tamara Tennekoon, andSophia Virji in the collection of the surveydata is gratefully acknowledged.