Embed Size (px)

Citation preview

Using R in Academic Finance

Sanjiv R. Das Professor, Santa Clara University

Department of Finance h?p://algo.scu.edu/~sanjivdas/

Outline • High-‐performance compuGng for Finance • Modeling the opGmal modificaGon of home loans using R

• IdenGfying systemically risky financial insGtuGons using R network models.

• Goal-‐based porOolio opGmizaGon with R

• Using R to deliver funcGons/models on the web, and for pedagogical purposes.

R works well with Python and C.

h?p://www.rinfinance.com/RinFinance2010/agenda/

h?p://cran.r-‐project.org/web/views/Finance.html

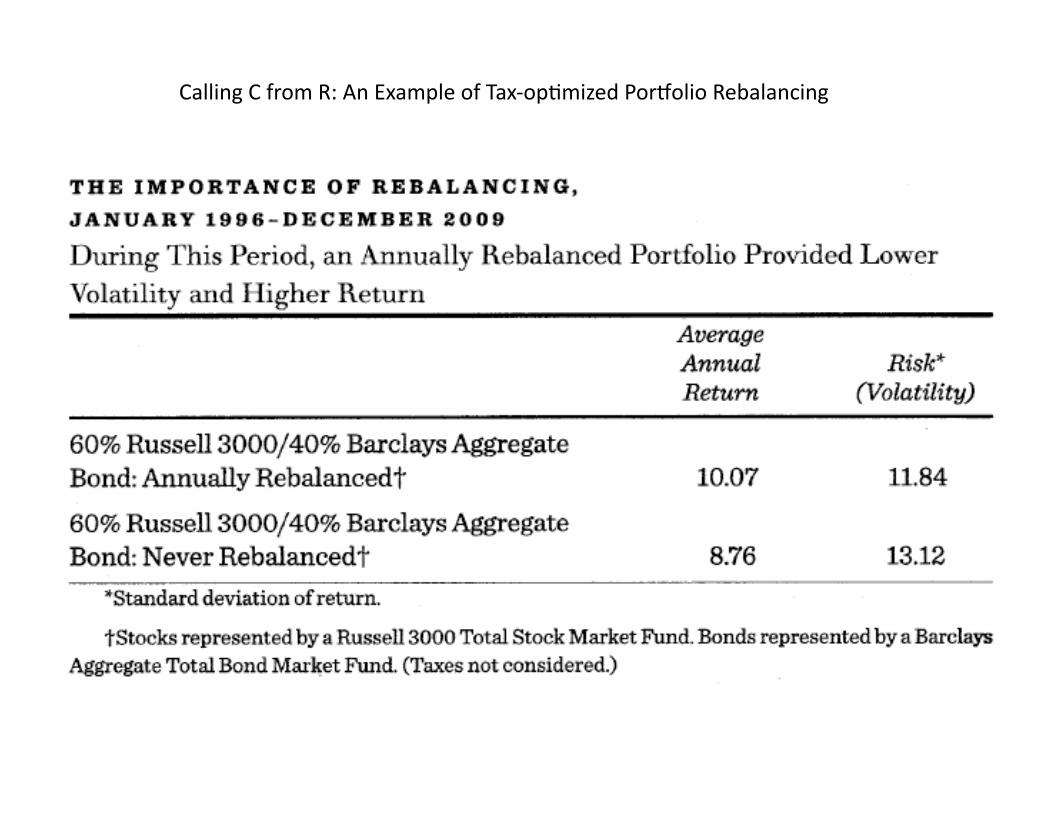

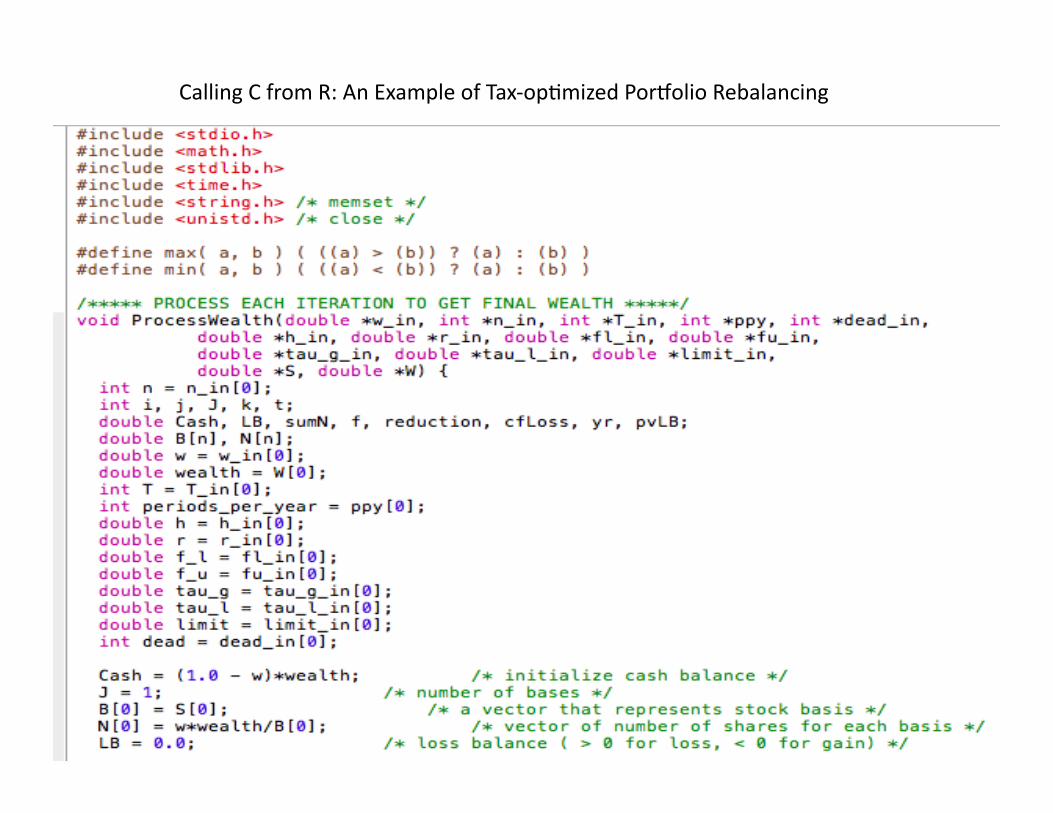

Calling C from R: An Example of Tax-‐opGmized PorOolio Rebalancing

Calling C from R: An Example of Tax-‐opGmized PorOolio Rebalancing

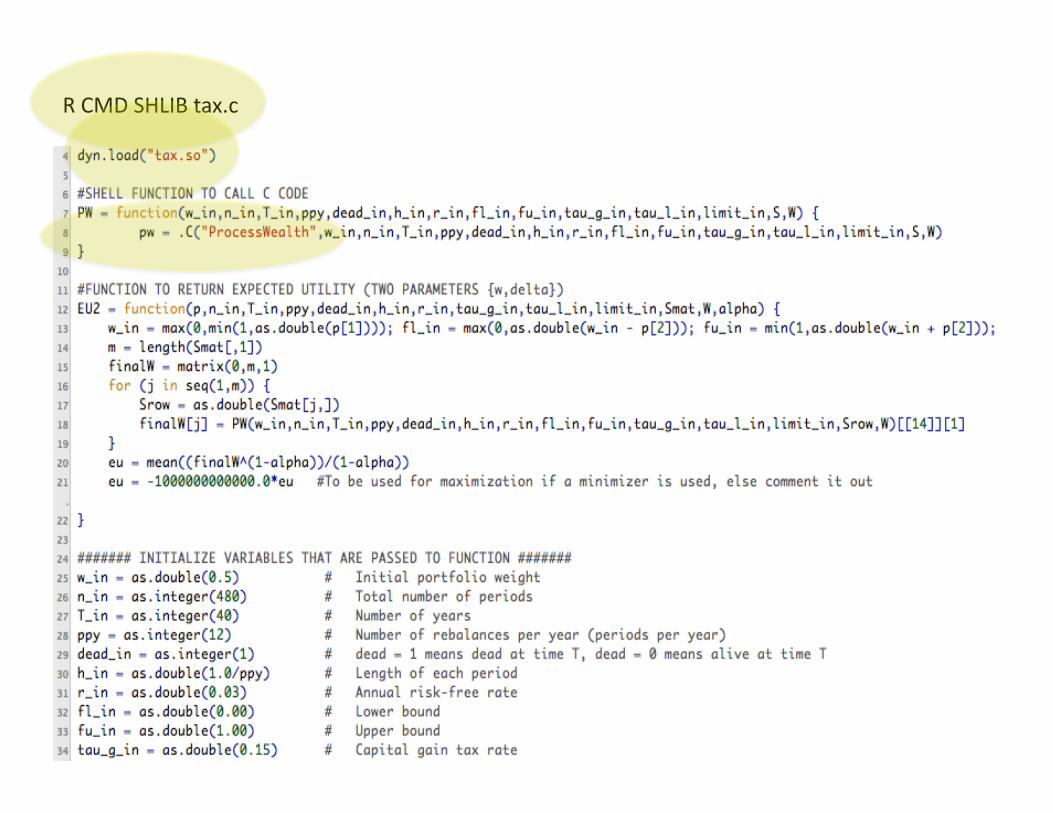

R CMD SHLIB tax.c

MODIFYING HOME LOANS WITH R MODELS

Topic 1

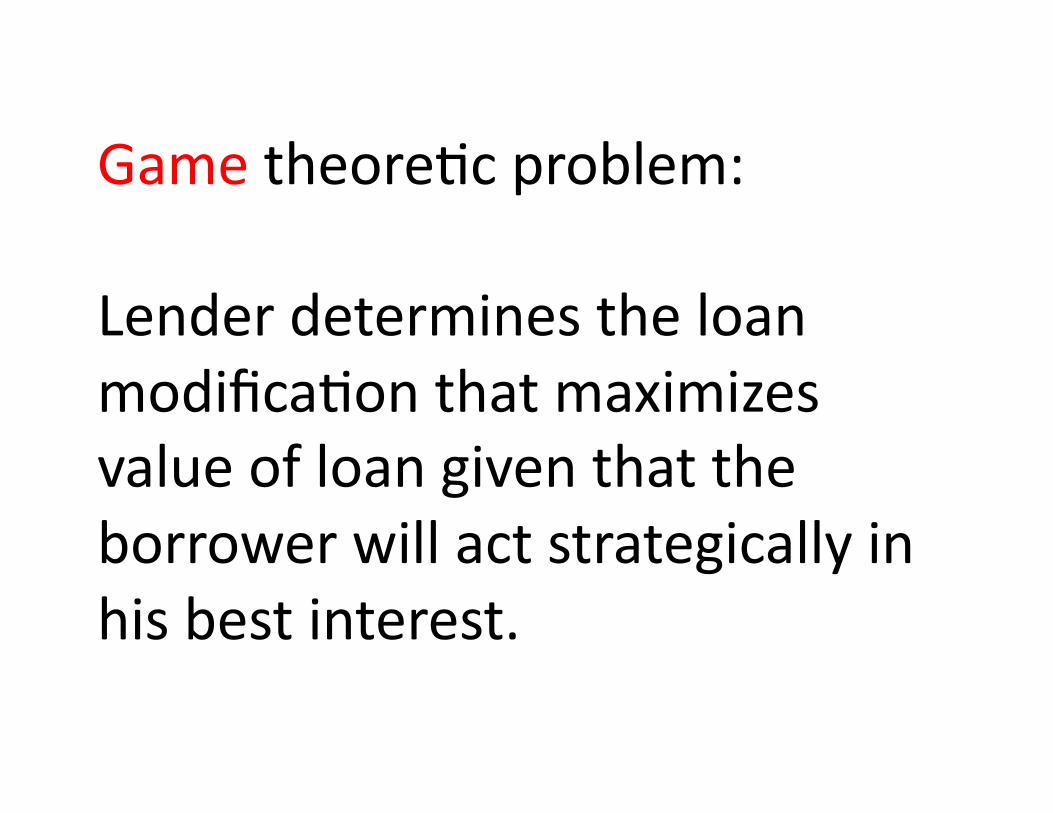

THE PRINCIPAL PRINCIPLE: OpGmal ModificaGon of Distressed Home Loans (Why Lenders should Forgive, not Foresake Mortgages)

STRATEGIC LOAN MODIFICATION: An OpGons based response to strategic default (joint work with Ray Meadows)

Game theoreGc problem:

Lender determines the loan modificaGon that maximizes value of loan given that the borrower will act strategically in his best interest.

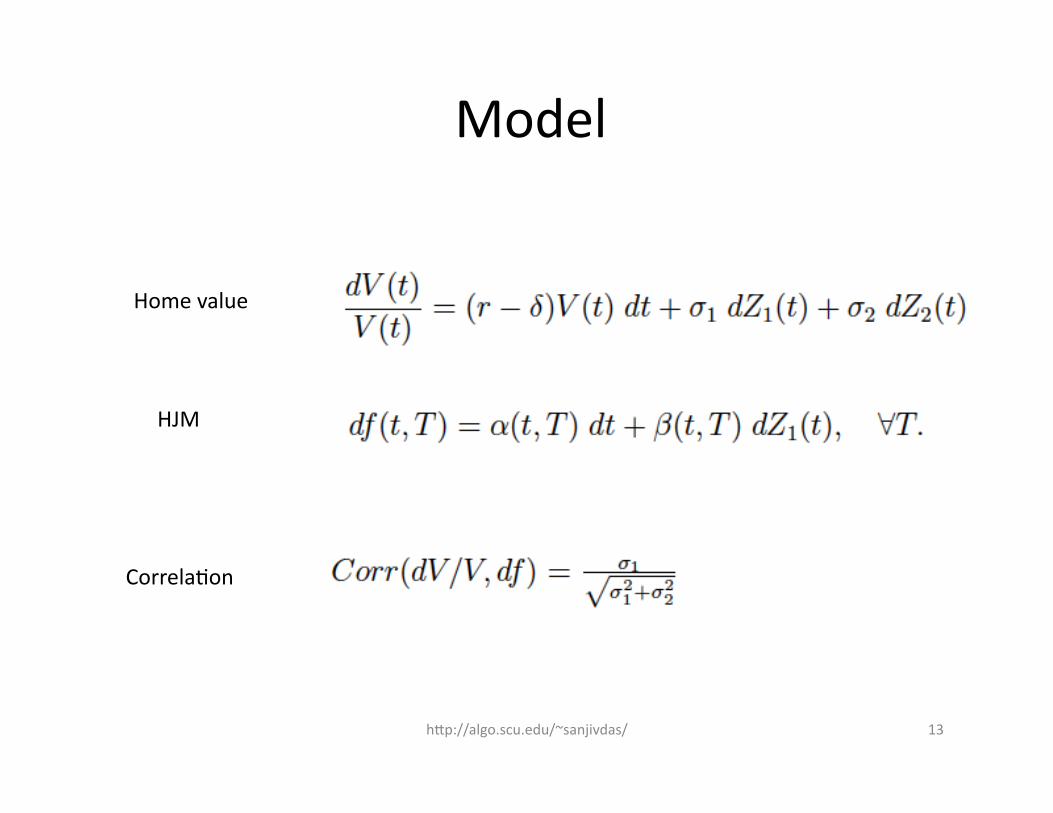

Model

h?p://algo.scu.edu/~sanjivdas/ 13

Home value

HJM

CorrelaGon

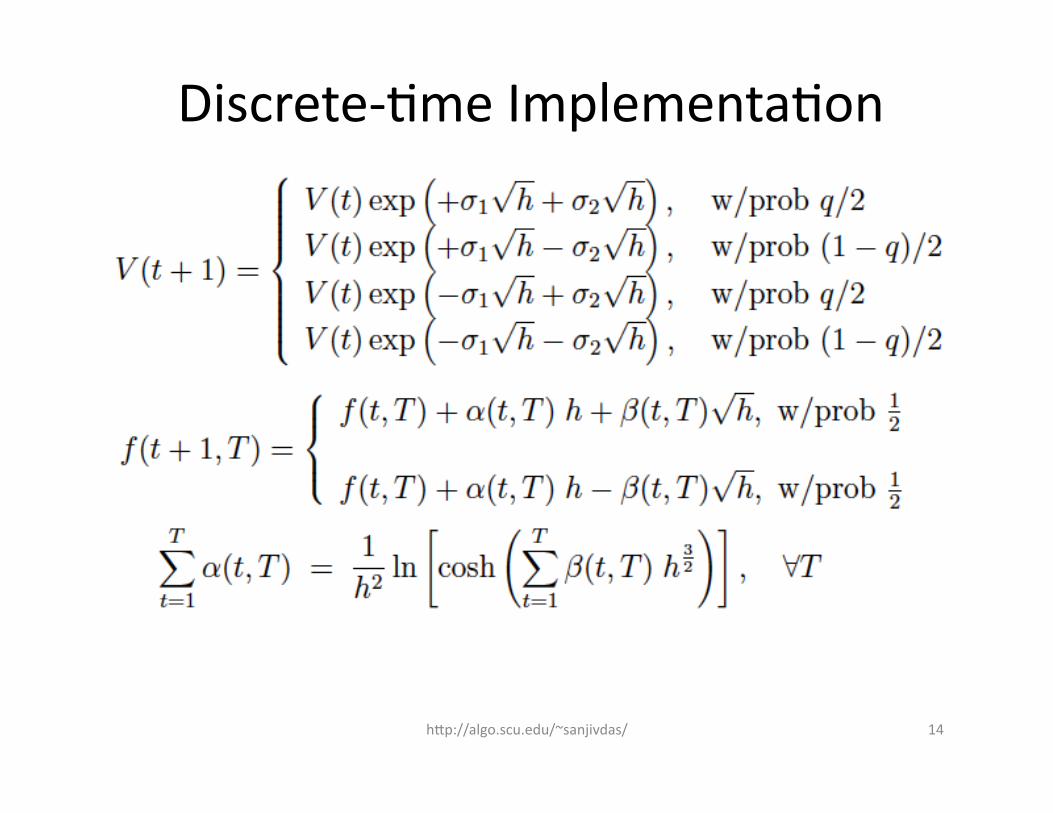

Discrete-‐Gme ImplementaGon

h?p://algo.scu.edu/~sanjivdas/ 14

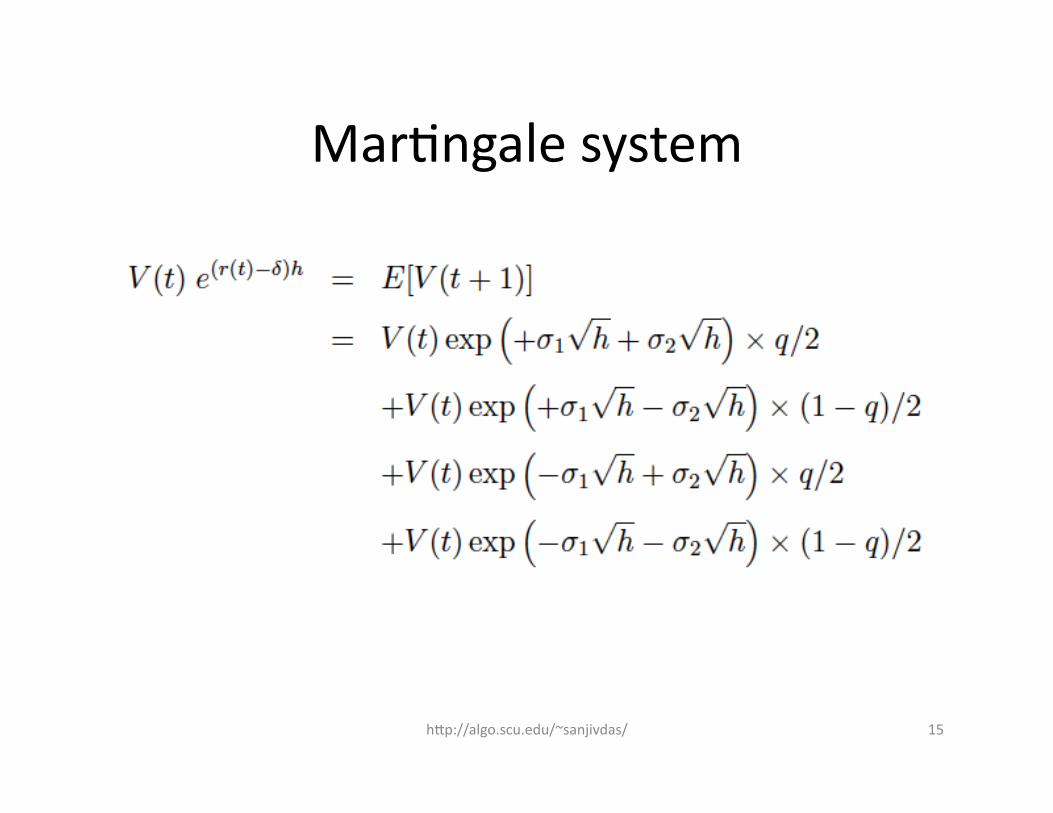

MarGngale system

h?p://algo.scu.edu/~sanjivdas/ 15

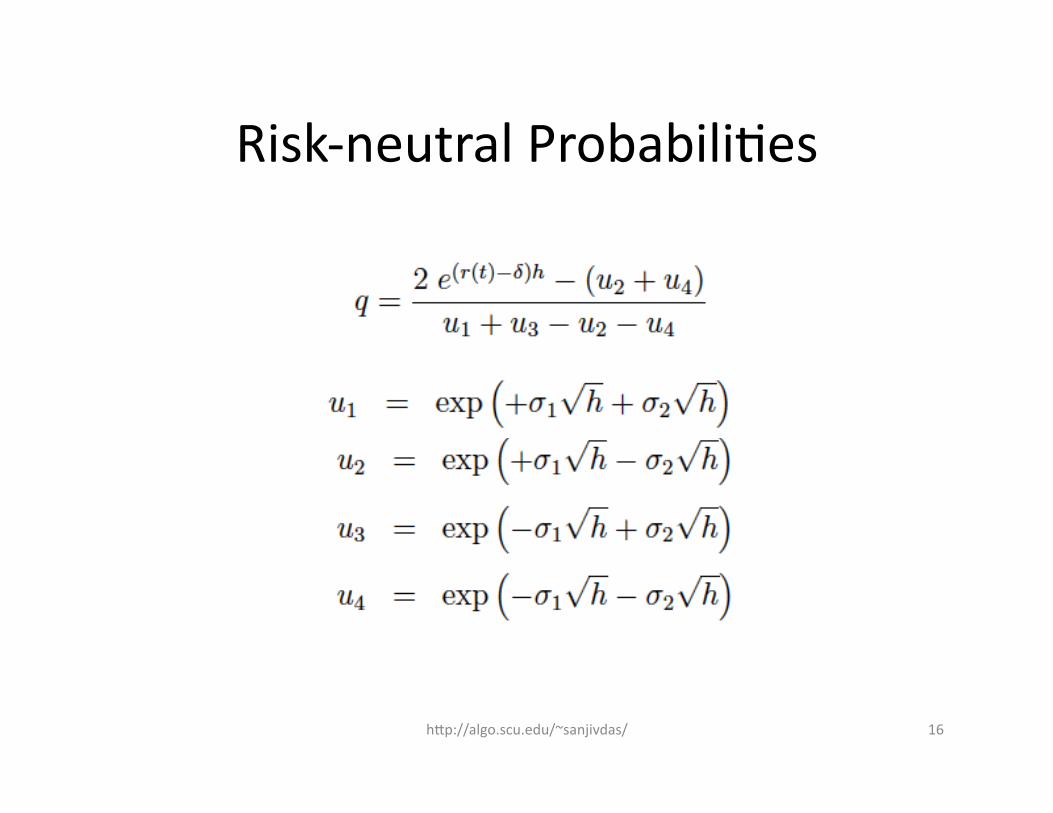

Risk-‐neutral ProbabiliGes

h?p://algo.scu.edu/~sanjivdas/ 16

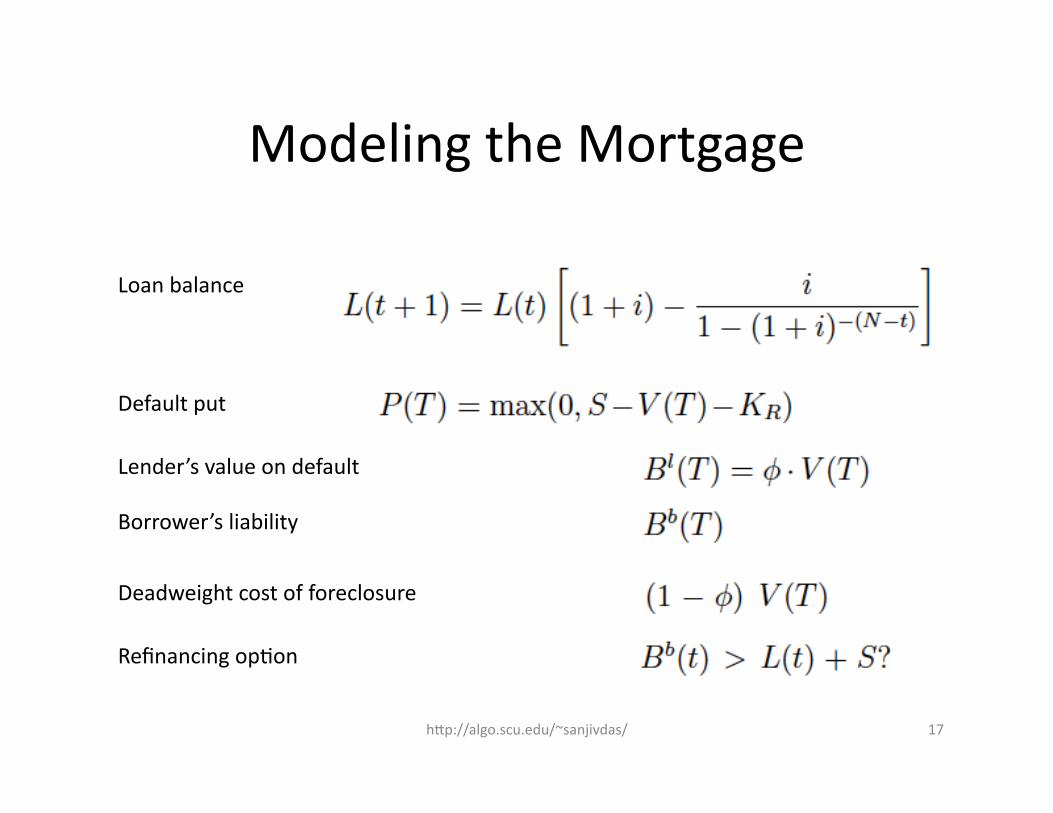

Modeling the Mortgage

h?p://algo.scu.edu/~sanjivdas/ 17

Loan balance

Default put

Lender’s value on default

Borrower’s liability

Deadweight cost of foreclosure

Refinancing opGon

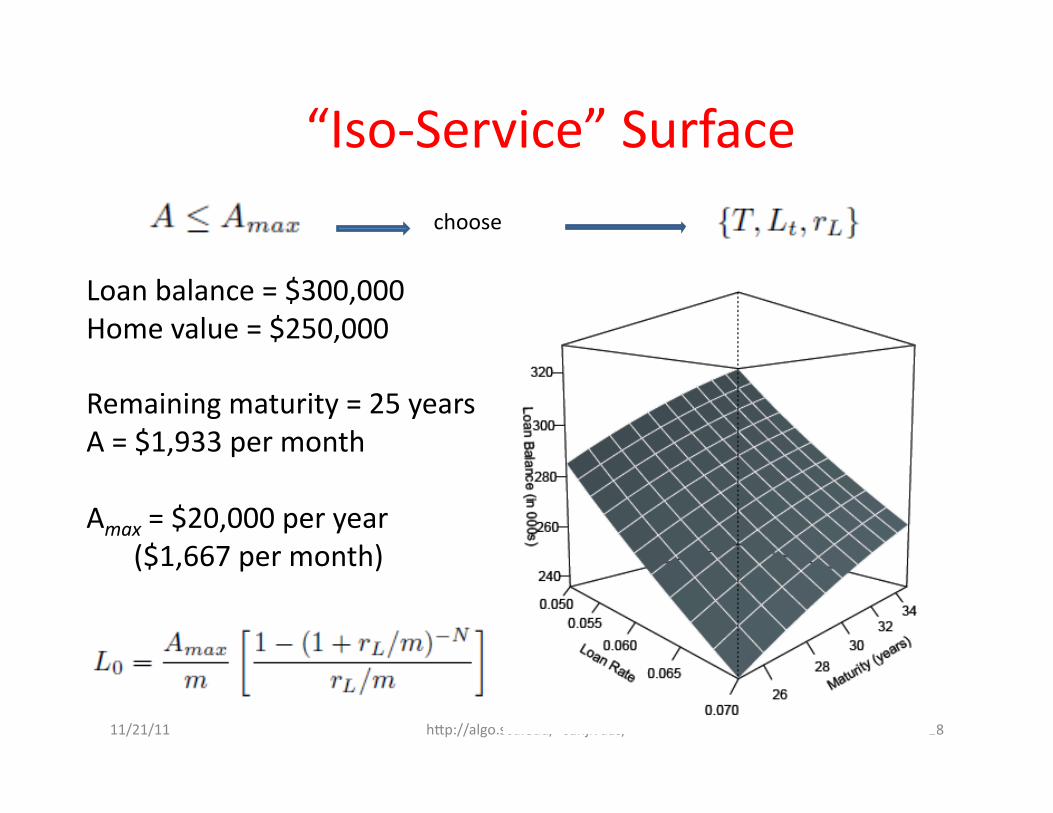

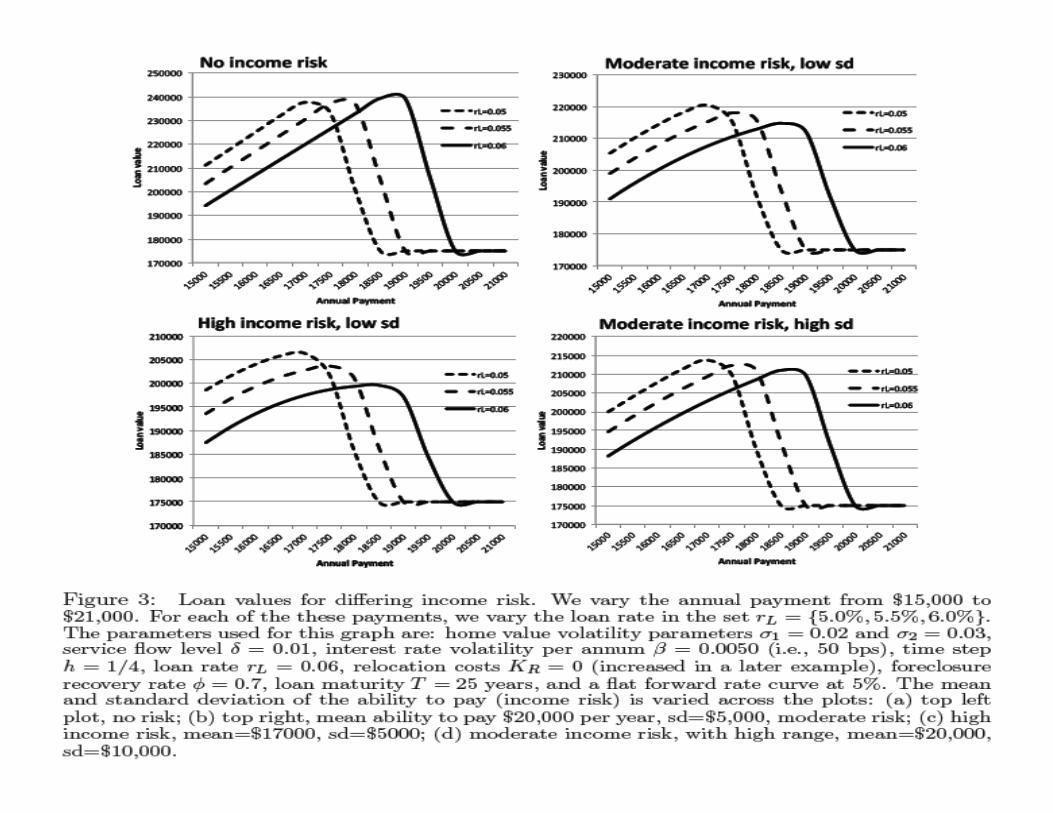

“Iso-‐Service” Surface

11/21/11 h?p://algo.scu.edu/~sanjivdas/ 18

Loan balance = $300,000 Home value = $250,000

Remaining maturity = 25 years A = $1,933 per month

Amax = $20,000 per year ($1,667 per month)

choose

Some R

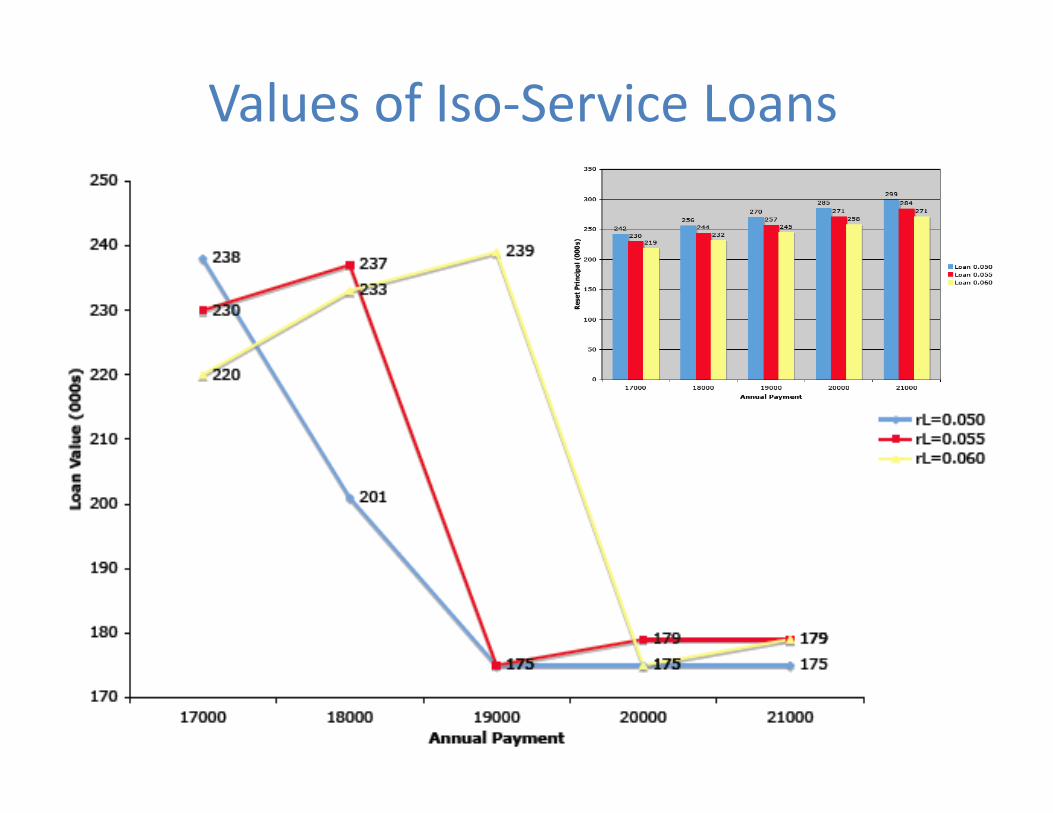

Values of Iso-‐Service Loans

h?p://algo.scu.edu/~sanjivdas/ 20

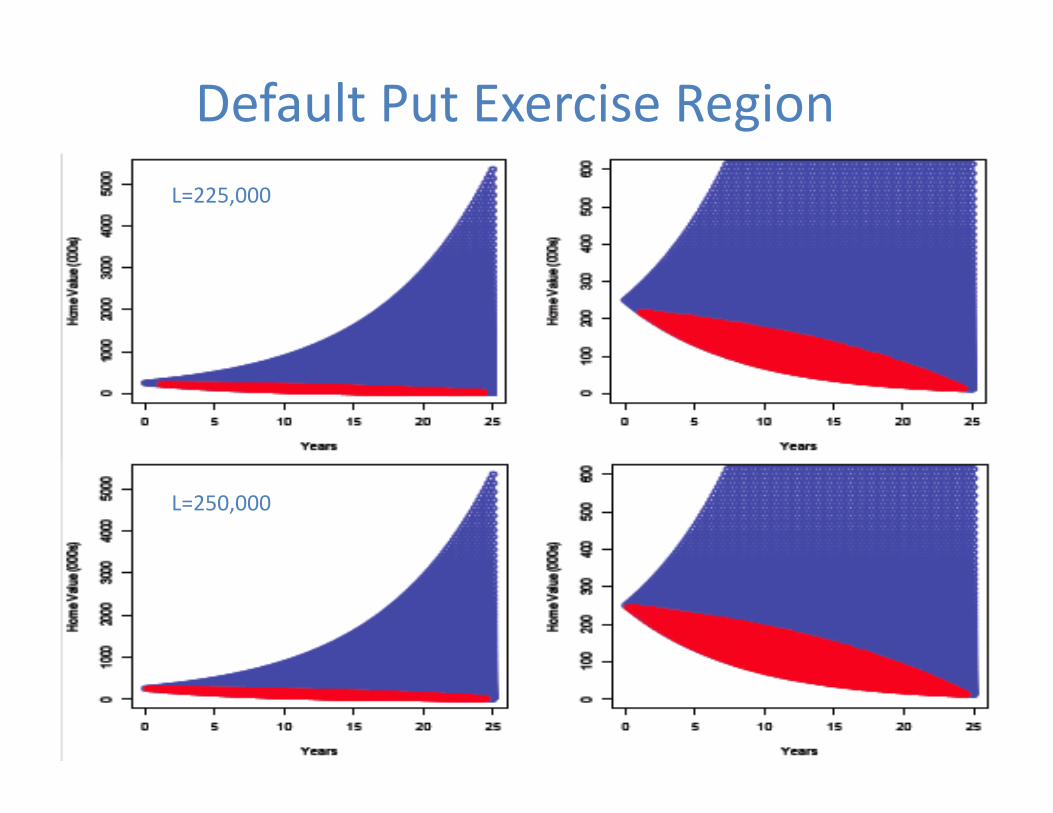

Default Put Exercise Region

h?p://algo.scu.edu/~sanjivdas/ 21

L=225,000

L=250,000

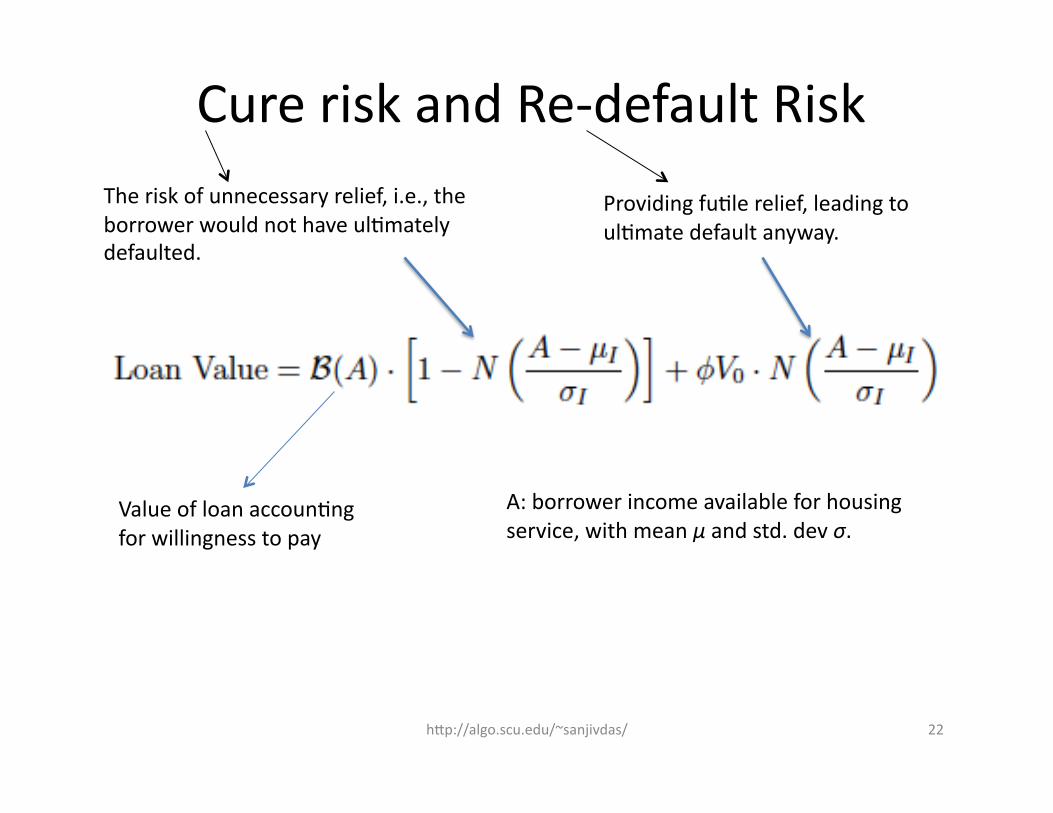

Cure risk and Re-‐default Risk

h?p://algo.scu.edu/~sanjivdas/ 22

The risk of unnecessary relief, i.e., the borrower would not have ulGmately defaulted.

Providing fuGle relief, leading to ulGmate default anyway.

Value of loan accounGng for willingness to pay

A: borrower income available for housing service, with mean μ and std. dev σ.

h?p://algo.scu.edu/~sanjivdas/ 23

h?p://algo.scu.edu/~sanjivdas/

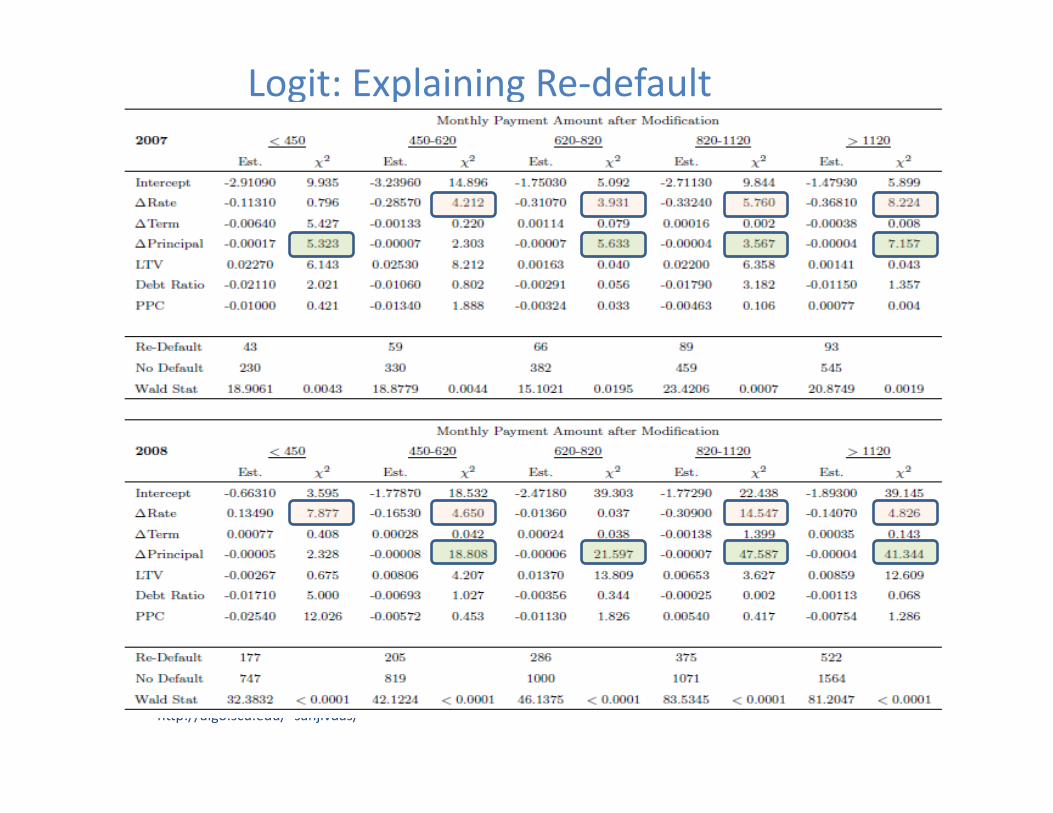

Logit: Explaining Re-‐default

h?p://algo.scu.edu/~sanjivdas/ 25

Reduced-‐Form Analysis of SAMs

Home values

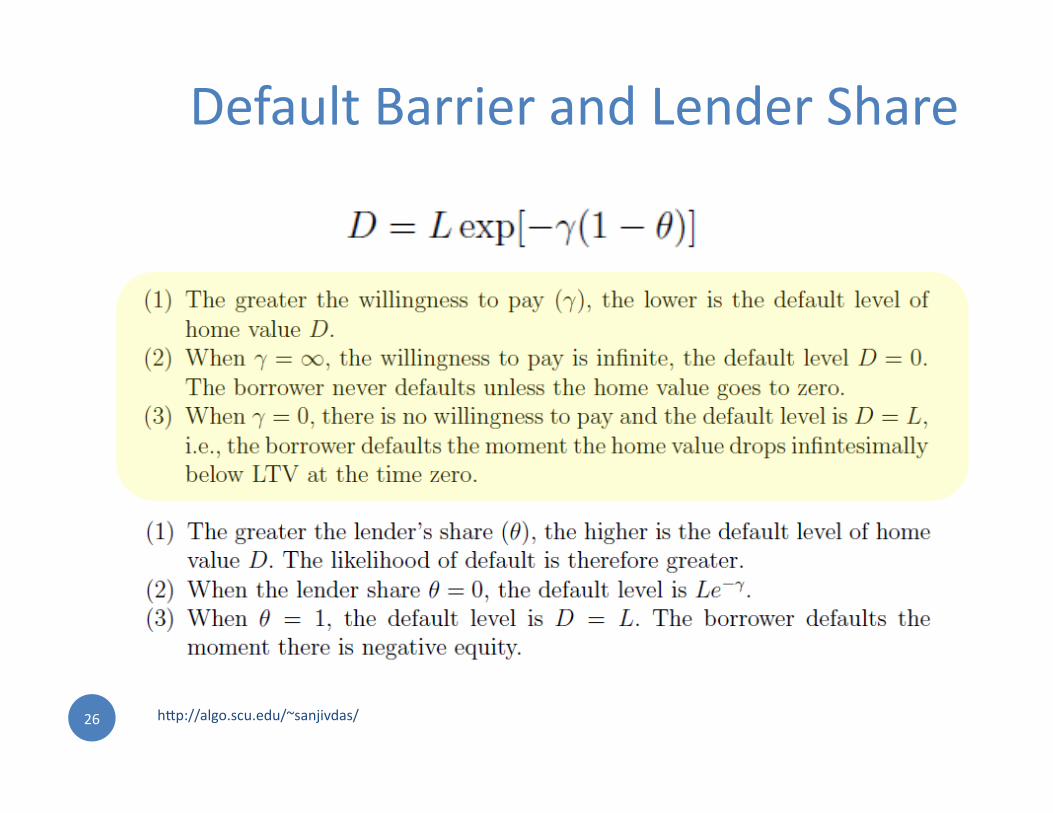

Normalize iniGal home value to 1. The opGon to default is ITM when (H > L).

There is a home value D at which the borrower will default. D is a “default level” or default exercise barrier.

D is a funcGon of the lender share θ, we write it as D(L, θ).

D increases in L and in θ.

Foreclosure recovery as a fracGon of H is ϕ.

h?p://algo.scu.edu/~sanjivdas/ 26

Default Barrier and Lender Share

h?p://algo.scu.edu/~sanjivdas/ 27

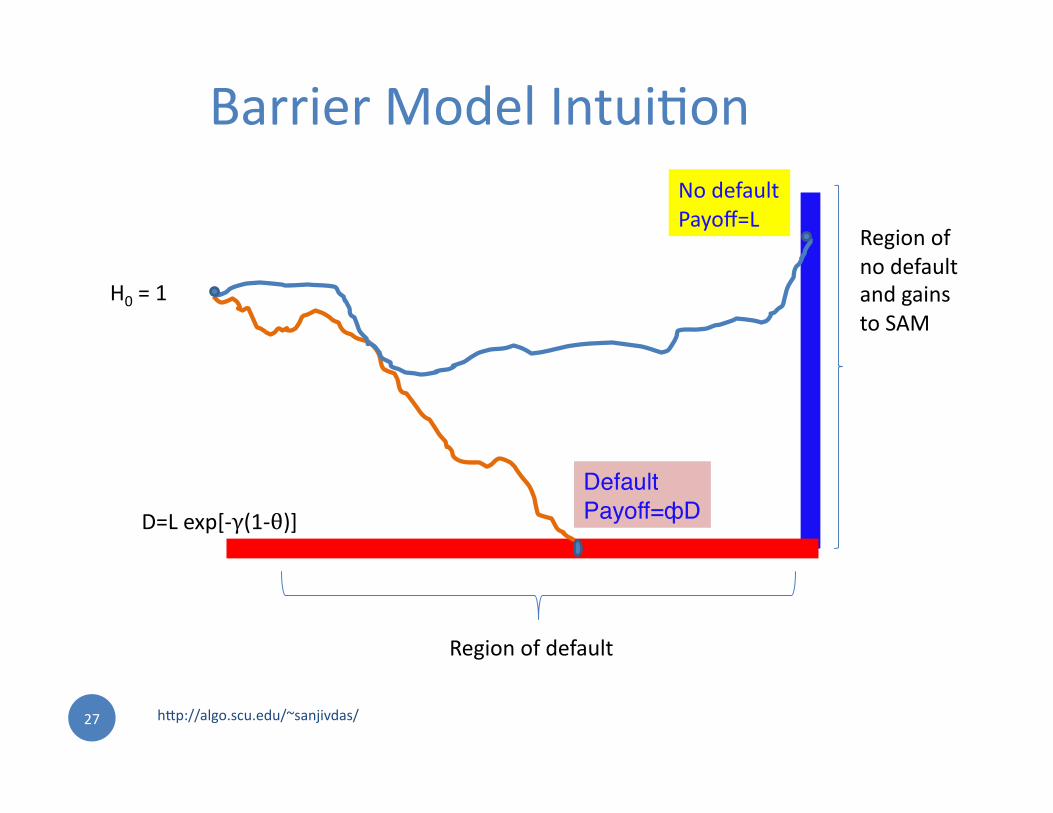

Barrier Model IntuiGon

D=L exp[-‐γ(1-‐θ)]

Region of no default and gains to SAM

Region of default

H0 = 1

Default"Payoff=фD"

No default Payoff=L

h?p://algo.scu.edu/~sanjivdas/ 28

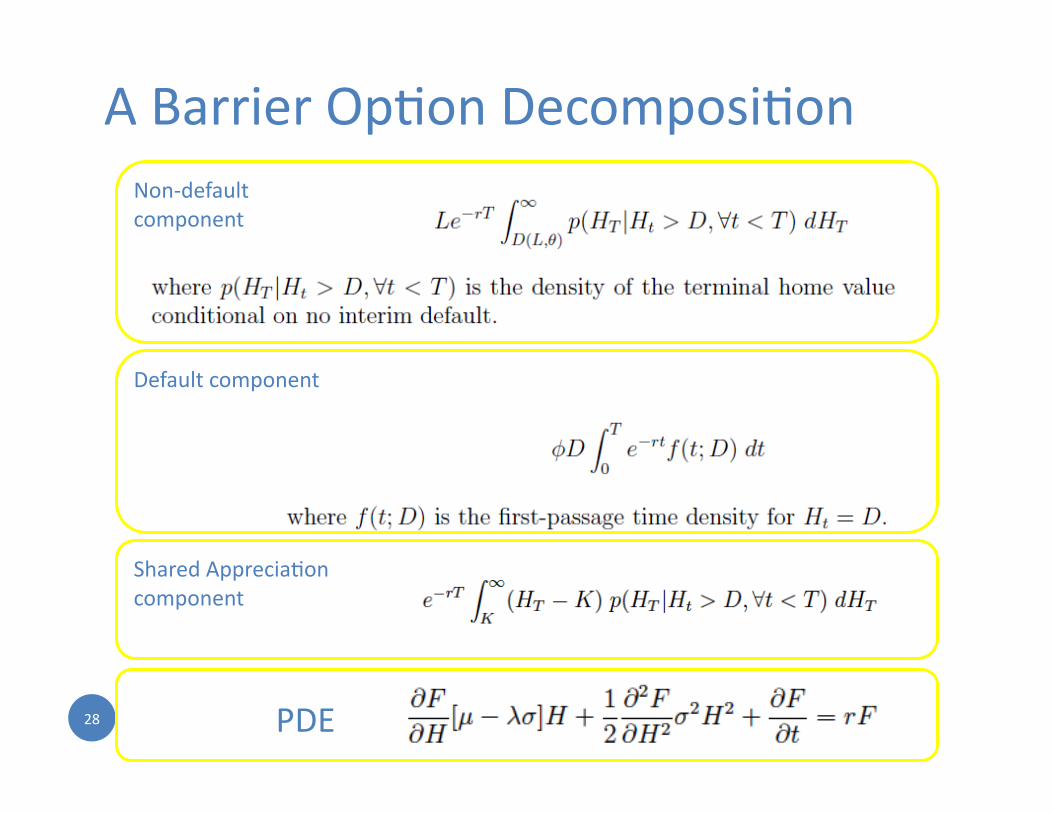

A Barrier OpGon DecomposiGon Non-‐default component

Default component

Shared AppreciaGon component

PDE

h?p://algo.scu.edu/~sanjivdas/ 29

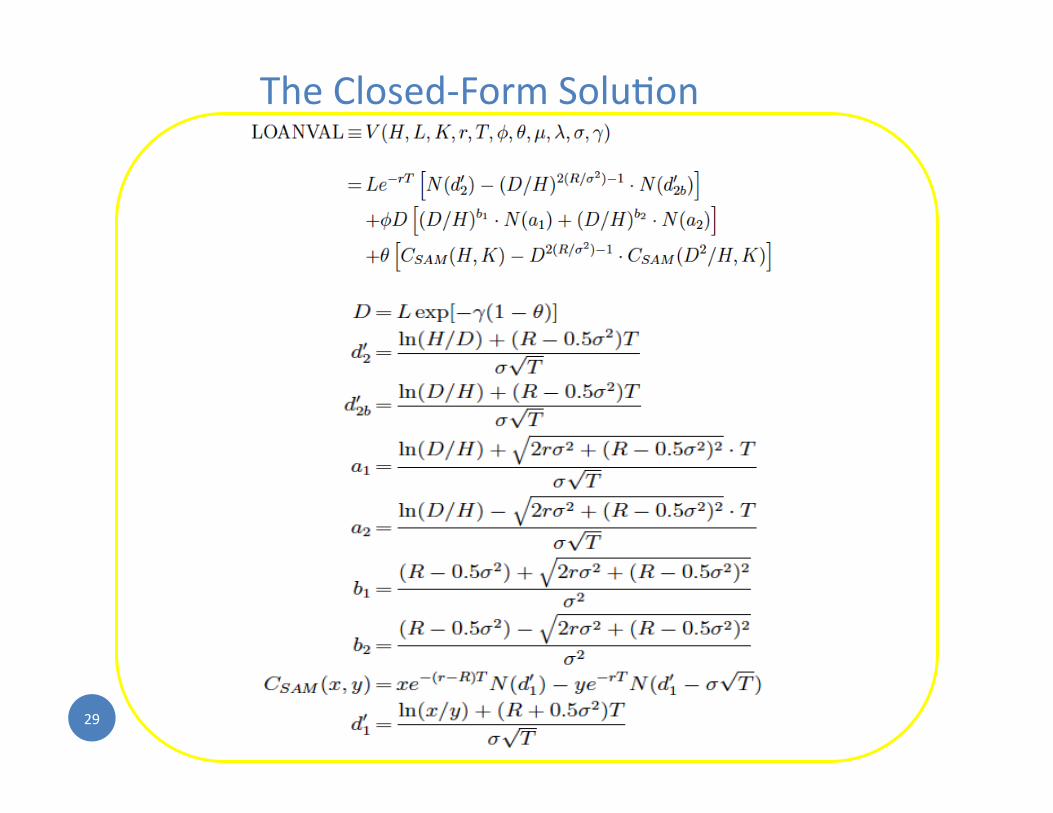

The Closed-‐Form SoluGon

h?p://algo.scu.edu/~sanjivdas/ 30

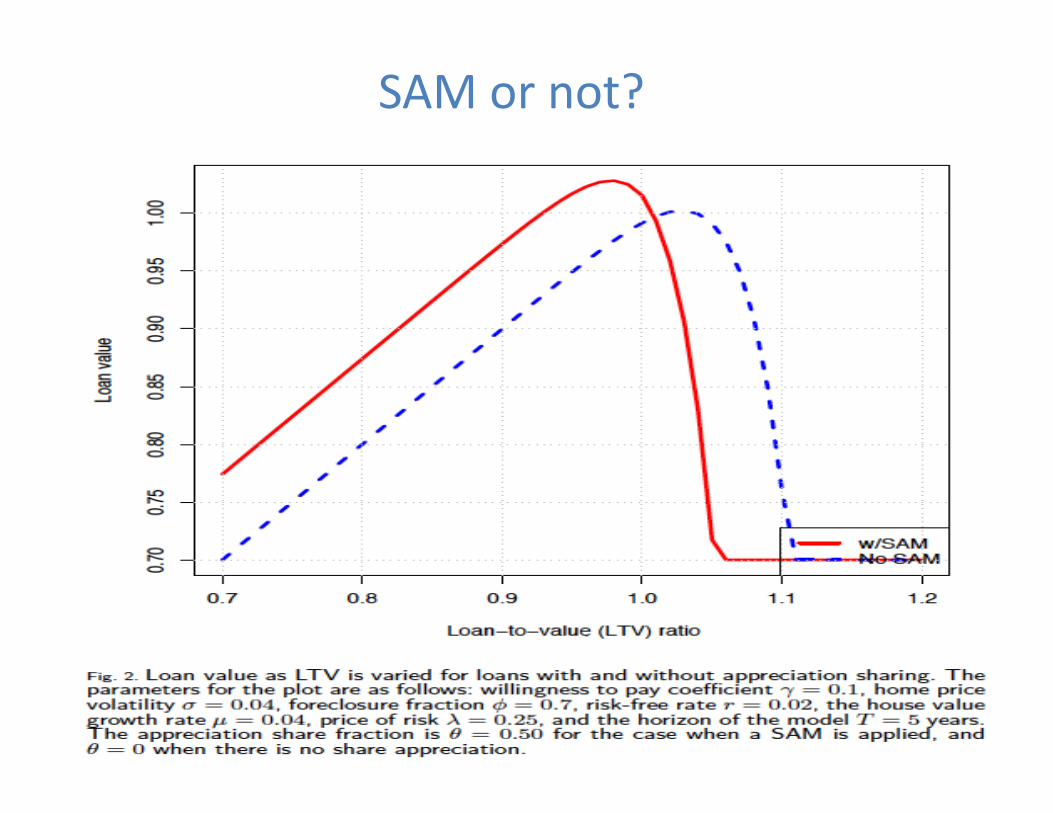

SAM or not?

MANAGING SYSTEMIC RISK BY ANALYZING NETWORKS USING R

THE MIDAS PROJECT @IBM

Topic 2

Paper: “Unleashing the Power of Public Data for Financial Risk Measurement, RegulaGon, and Governance” (with Mauricio A. Hernandez, Howard Ho, Georgia Koutrika, Rajasekar Krishnamurthy, Lucian Popa, Ioana R. Stanoi, Shivakumar Vaithyanathan) IBM Almaden)

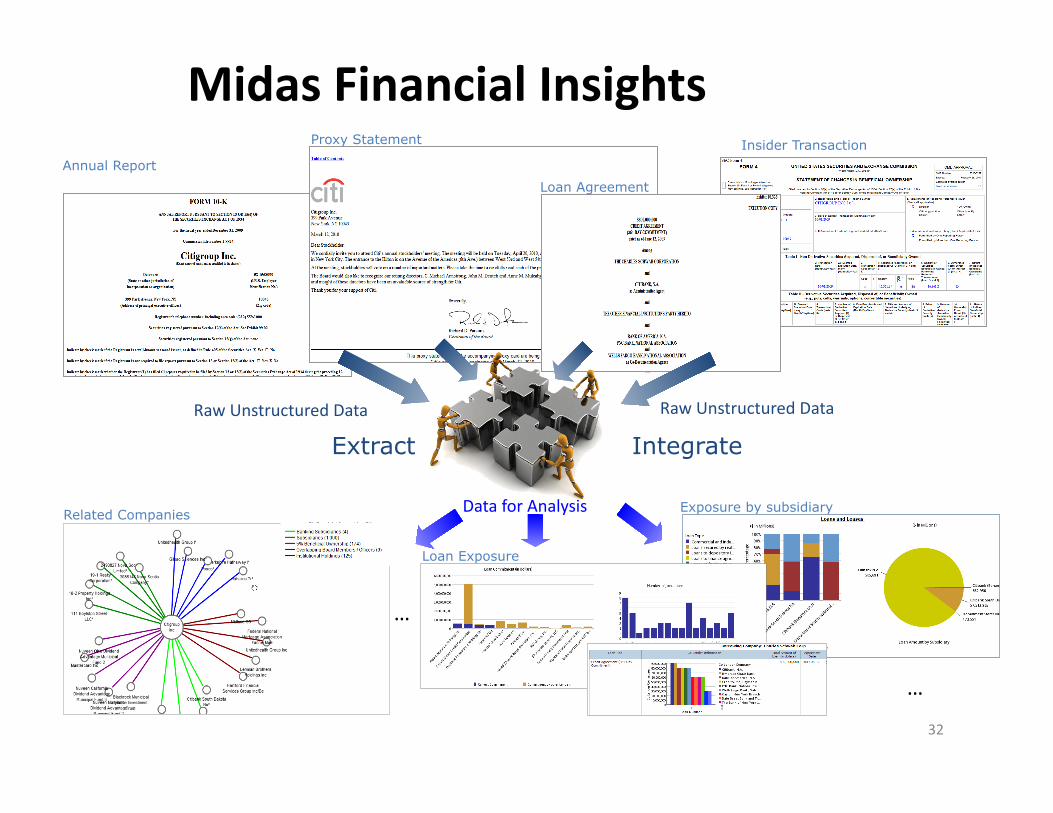

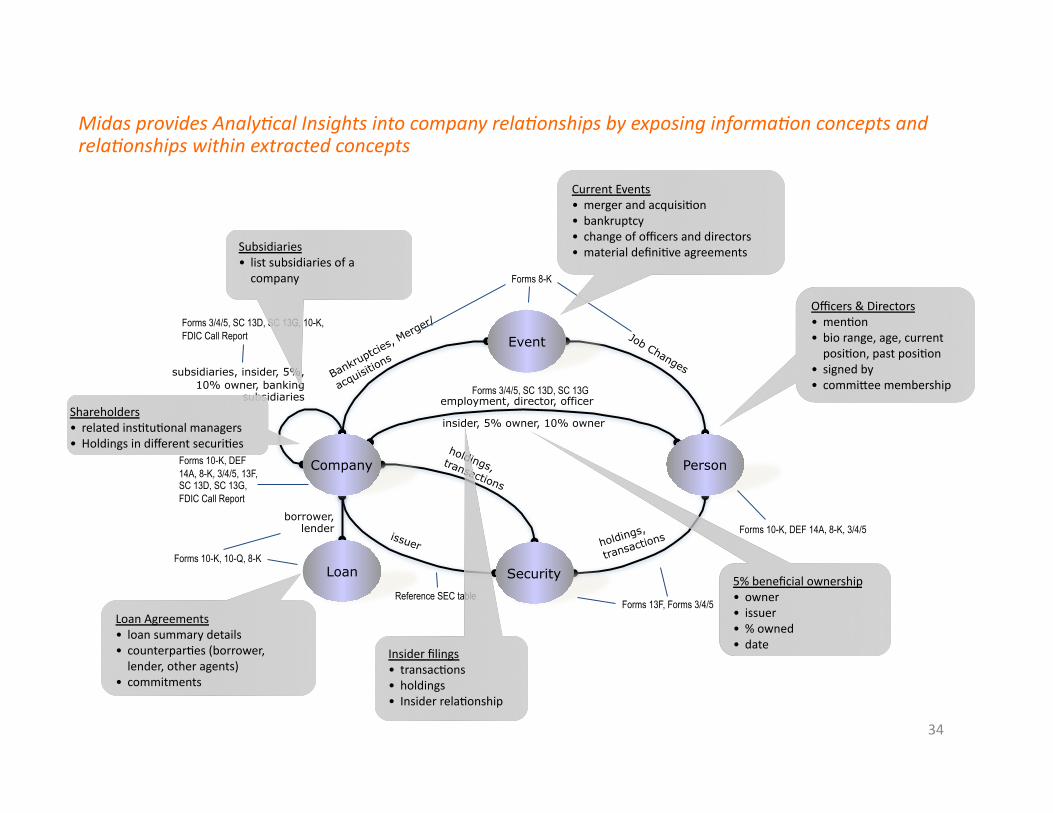

Midas Financial Insights

32

Annual Report

Proxy Statement Insider Transaction

Loan Agreement

Extract Integrate

Related Companies

Loan Exposure

Exposure by subsidiary

…

…

Raw Unstructured Data

Data for Analysis

Raw Unstructured Data

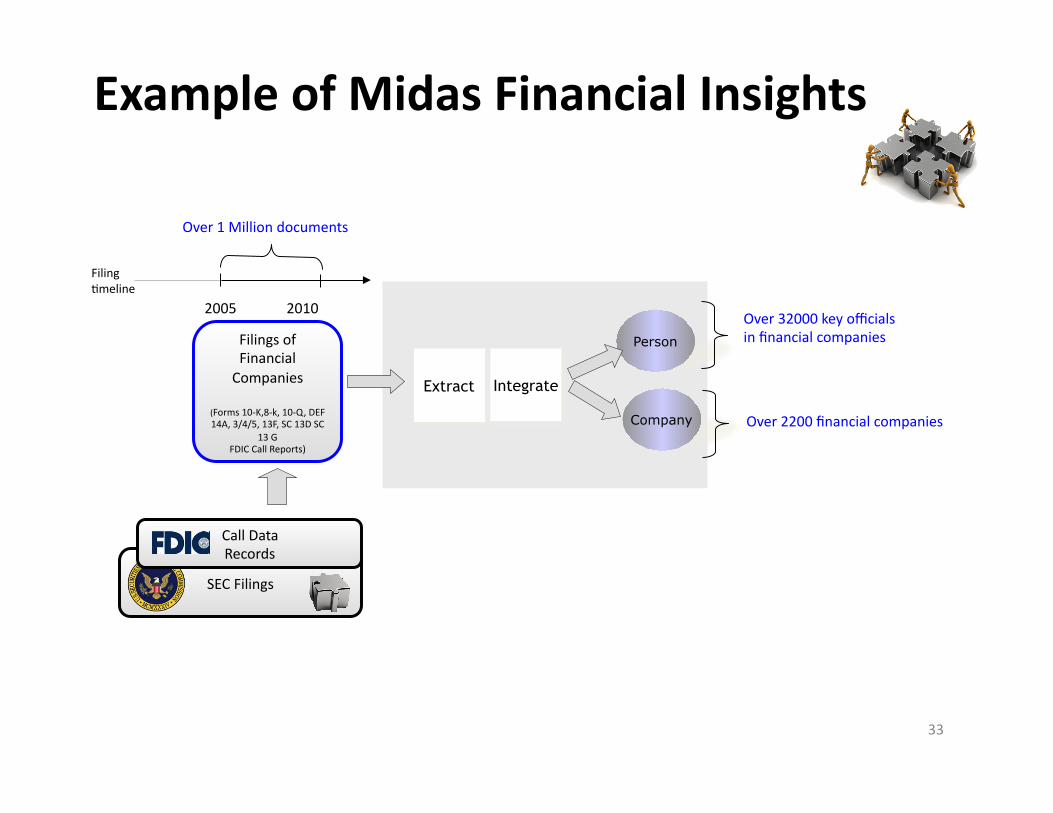

Example of Midas Financial Insights

33

Company

Person

Extract Integrate

Over 2200 financial companies

Over 32000 key officials in financial companies

SEC Filings

Over 1 Million documents

2005 2010

Filing Gmeline

Filings of Financial Companies

(Forms 10-‐K,8-‐k, 10-‐Q, DEF 14A, 3/4/5, 13F, SC 13D SC

13 G FDIC Call Reports)

Call Data Records

34

employment, director, officer

insider, 5% owner, 10% owner

holdings,

transactions

Event

Company Person

Security Loan

subsidiaries, insider, 5%, 10% owner, banking

subsidiaries

borrower, lender

Forms 8-K

Forms 10-K, DEF 14A, 8-K, 3/4/5

Forms 10-K, DEF 14A, 8-K, 3/4/5, 13F, SC 13D, SC 13G, FDIC Call Report

Reference SEC table Forms 13F, Forms 3/4/5

Forms 3/4/5, SC 13D, SC 13G, 10-K, FDIC Call Report

Forms 3/4/5, SC 13D, SC 13G

Forms 10-K, 10-Q, 8-K

5% beneficial ownership • owner • issuer • % owned • date

Shareholders • related insGtuGonal managers • Holdings in different securiGes

Subsidiaries • list subsidiaries of a company

Current Events • merger and acquisiGon • bankruptcy • change of officers and directors • material definiGve agreements

Loan Agreements • loan summary details • counterparGes (borrower, lender, other agents)

• commitments

Insider filings • transacGons • holdings • Insider relaGonship

Officers & Directors • menGon • bio range, age, current posiGon, past posiGon

• signed by • commi?ee membership

Midas provides Analy8cal Insights into company rela8onships by exposing informa8on concepts and rela8onships within extracted concepts

35

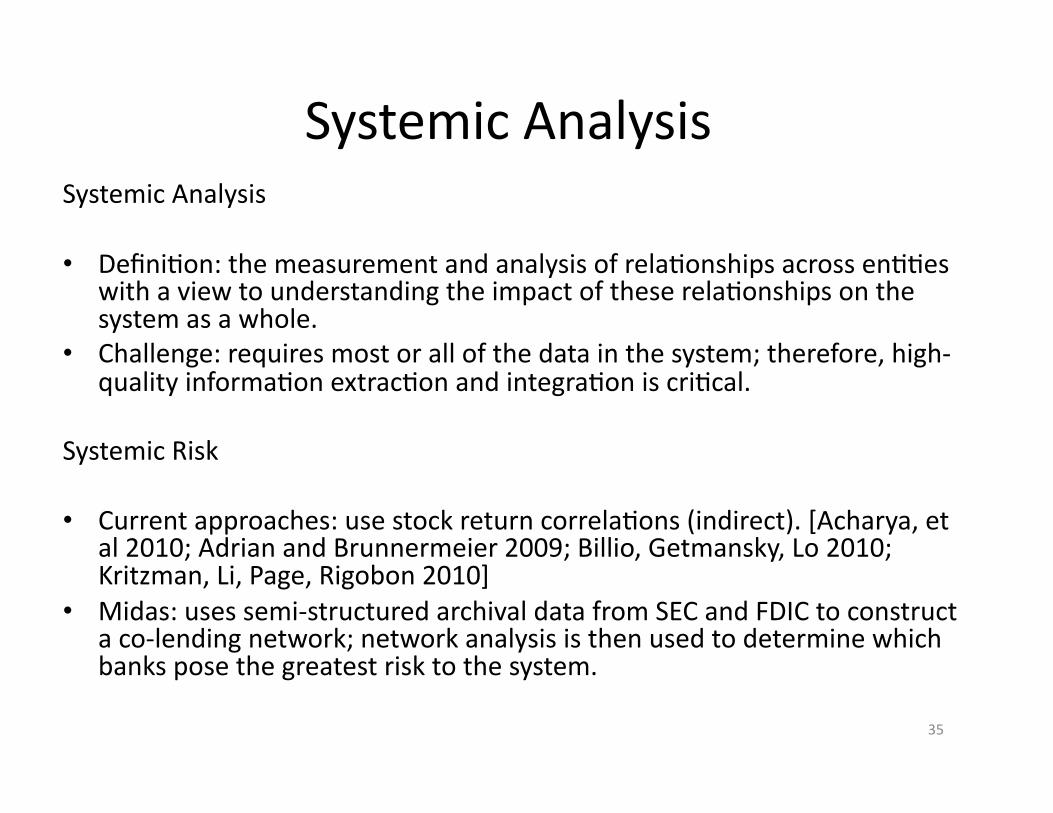

Systemic Analysis Systemic Analysis

• DefiniGon: the measurement and analysis of relaGonships across enGGes with a view to understanding the impact of these relaGonships on the system as a whole.

• Challenge: requires most or all of the data in the system; therefore, high-‐quality informaGon extracGon and integraGon is criGcal.

Systemic Risk

• Current approaches: use stock return correlaGons (indirect). [Acharya, et al 2010; Adrian and Brunnermeier 2009; Billio, Getmansky, Lo 2010; Kritzman, Li, Page, Rigobon 2010]

• Midas: uses semi-‐structured archival data from SEC and FDIC to construct a co-‐lending network; network analysis is then used to determine which banks pose the greatest risk to the system.

36

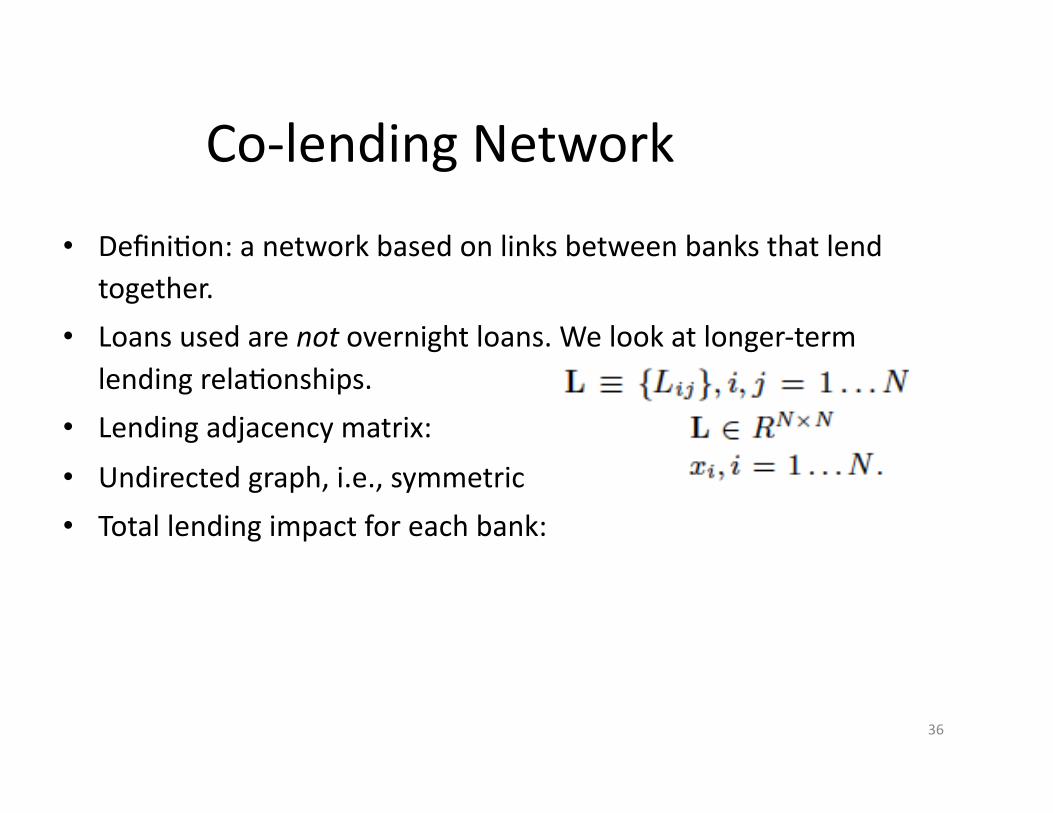

Co-‐lending Network

• DefiniGon: a network based on links between banks that lend together.

• Loans used are not overnight loans. We look at longer-‐term lending relaGonships.

• Lending adjacency matrix:

• Undirected graph, i.e., symmetric

• Total lending impact for each bank:

37

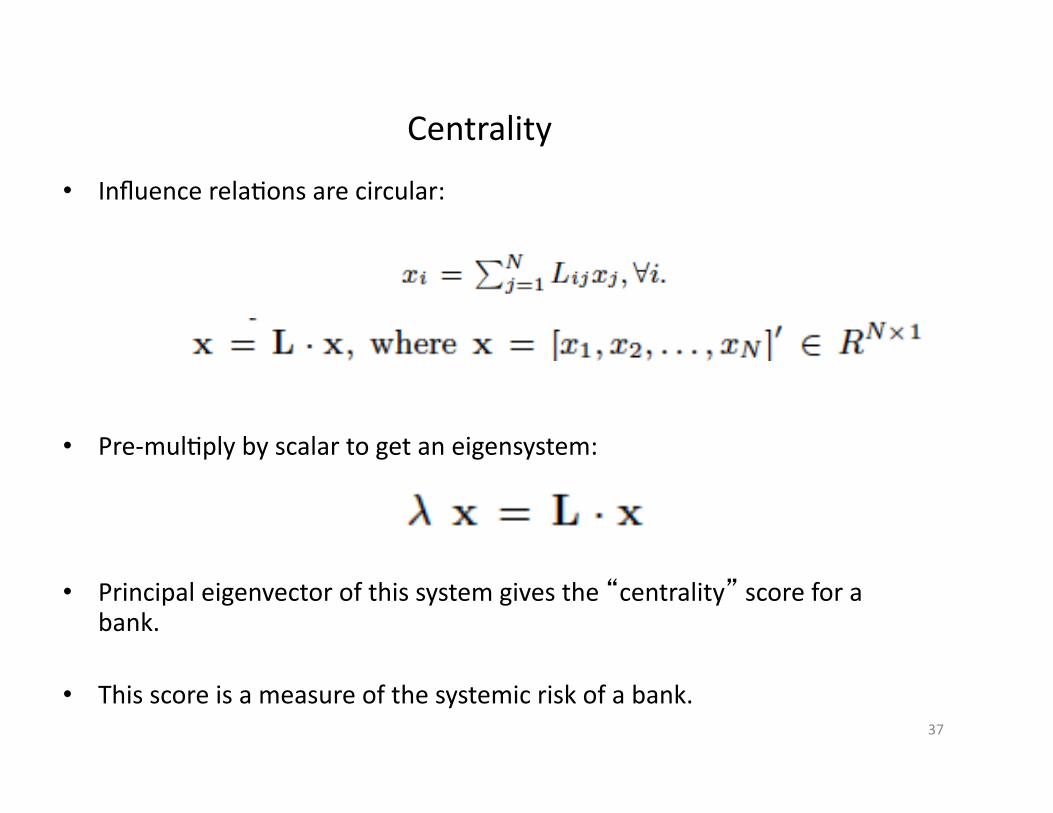

Centrality

• Influence relaGons are circular:

• Pre-‐mulGply by scalar to get an eigensystem:

• Principal eigenvector of this system gives the “centrality” score for a bank.

• This score is a measure of the systemic risk of a bank.

38

Data

• Five years: 2005—2009.

• Loans between FIs only. • Filings made with the SEC.

• No overnight loans. • Example: 364-‐day bridge loans, longer-‐term credit arrangement, Libor

notes, etc.

• Remove all edge weights < 2 to remove banks that are minimally acGve. Remove all nodes with no edges. (This is a choice for the regulator.)

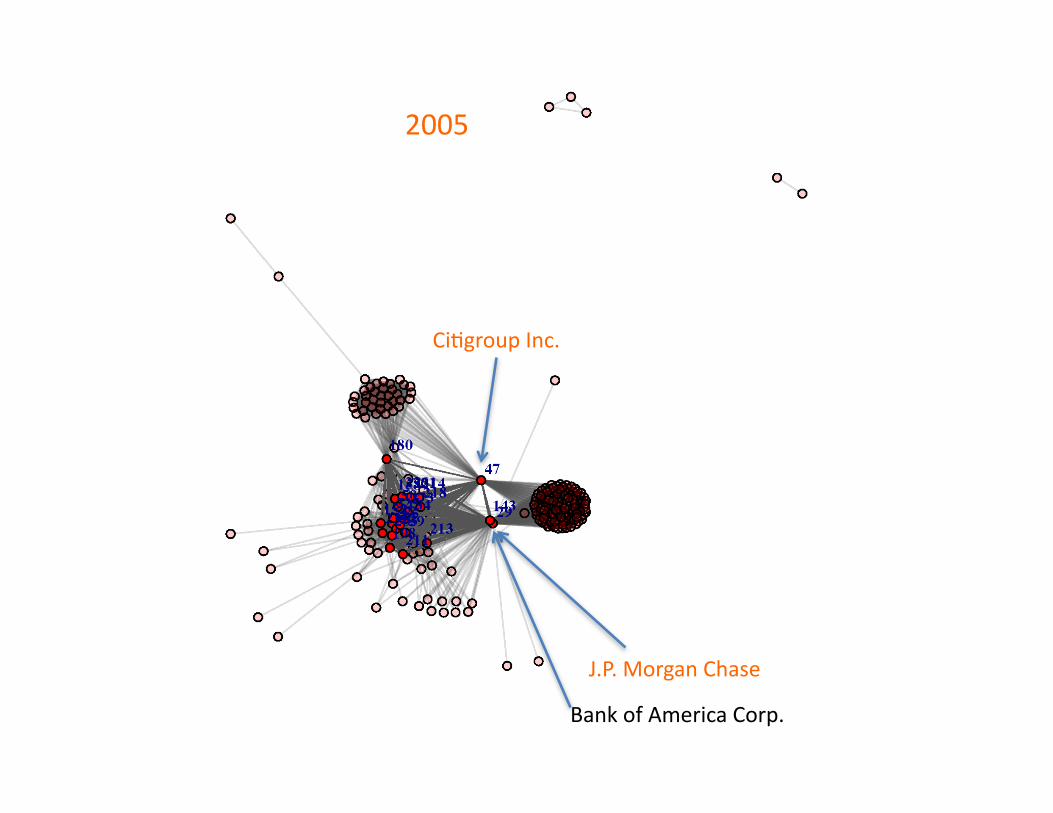

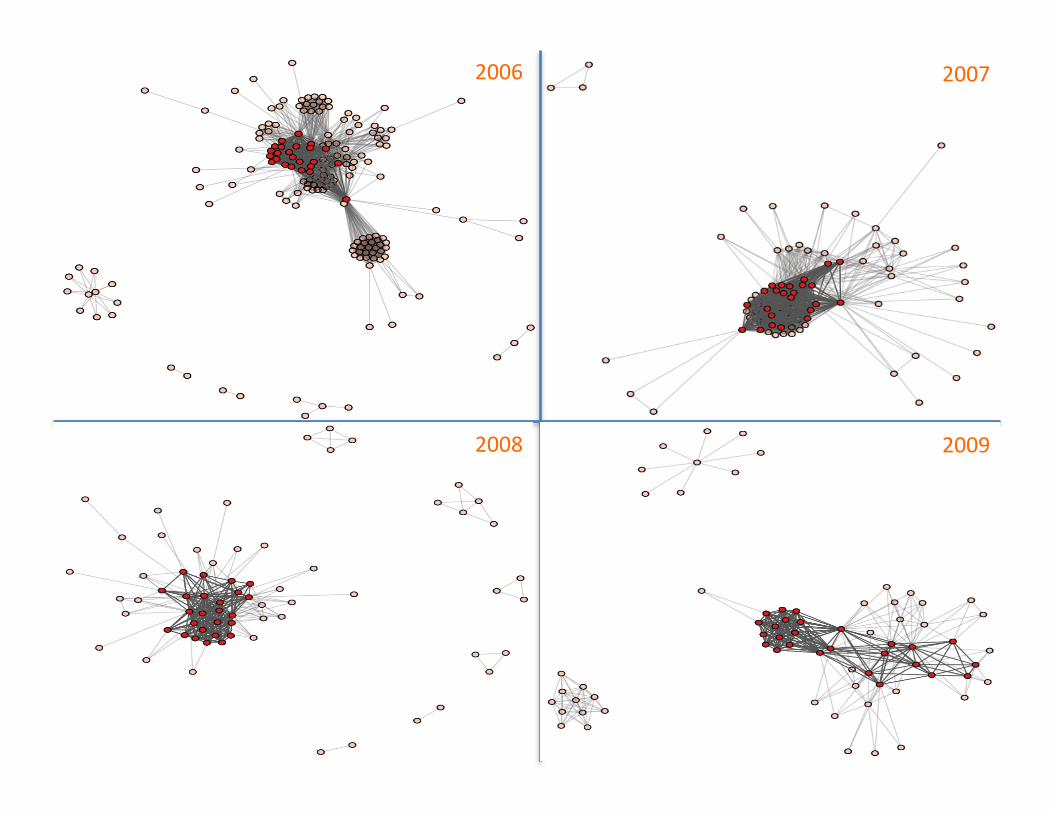

2005

CiGgroup Inc.

J.P. Morgan Chase

Bank of America Corp.

42

2006 2007

2008 2009

43

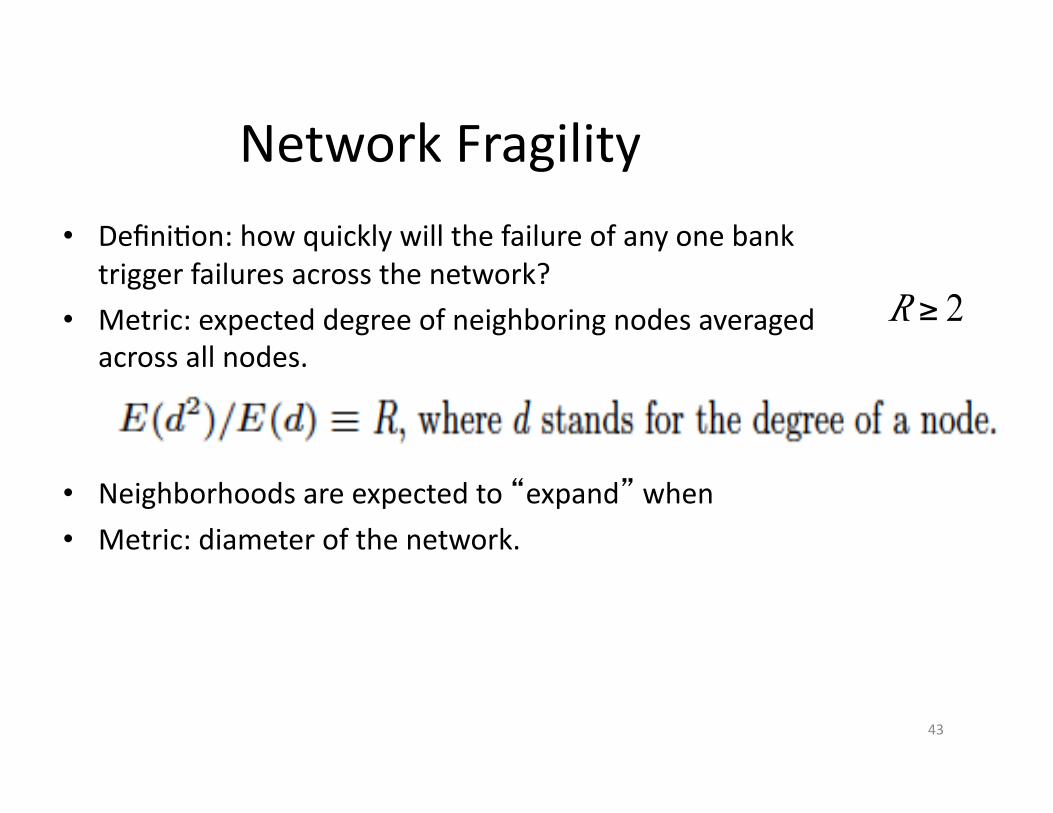

Network Fragility

• DefiniGon: how quickly will the failure of any one bank trigger failures across the network?

• Metric: expected degree of neighboring nodes averaged across all nodes.

• Neighborhoods are expected to “expand” when • Metric: diameter of the network.

44

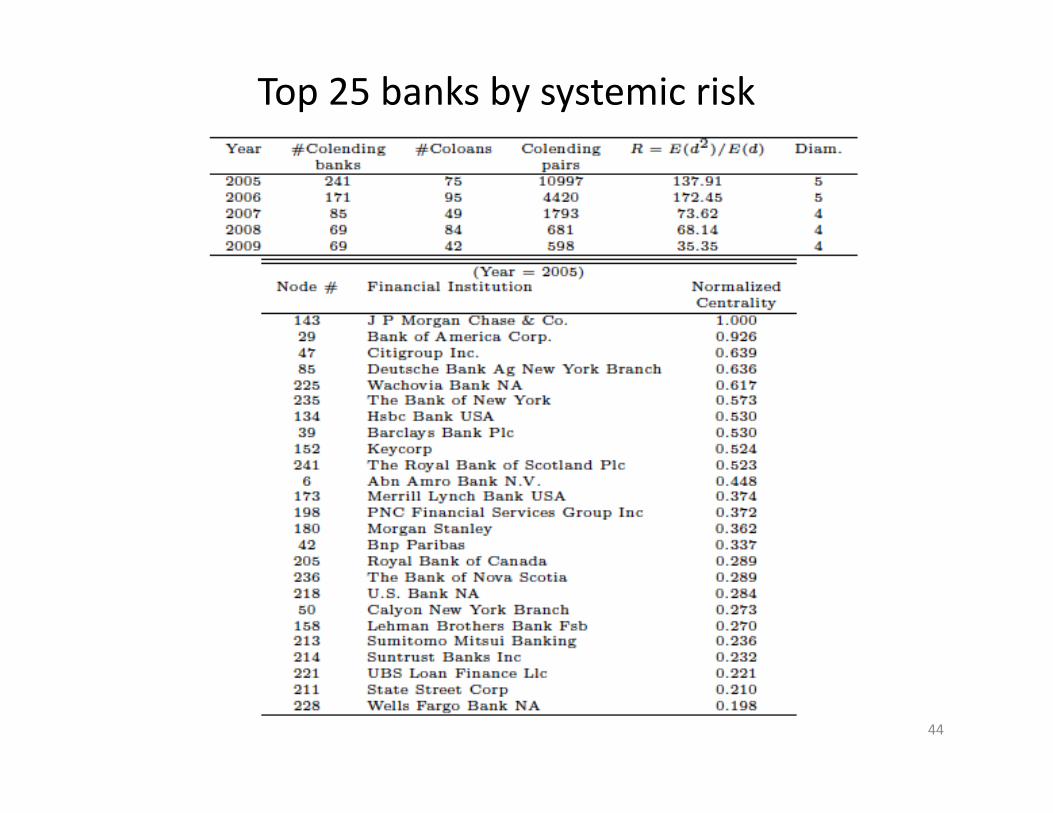

Top 25 banks by systemic risk

PORTFOLIO OPTIMIZATION USING R

Topic 3

The research papers for this work are on my web page – just google it. h?p://algo.scu.edu/~sanjivdas/research.htm/

1. Das, Markowitz, Scheid, and Statman (JFQA 2010), “PorOolio OpGmizaGon with Mental Accounts”

2. Das & Statman (2008), “Beyond Mean-‐Variance: PorOolio with Structured Products and non-‐Gaussian returns.”

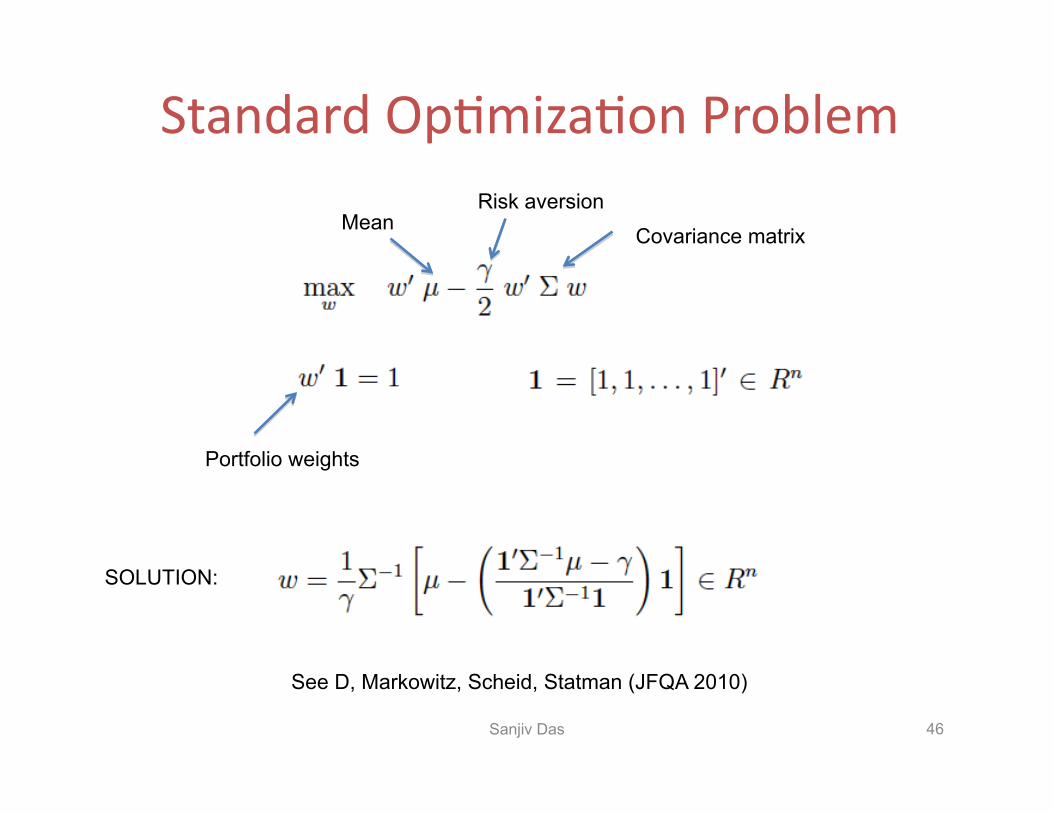

Standard OpGmizaGon Problem

Sanjiv Das 46

Mean Covariance matrix Risk aversion

Portfolio weights

SOLUTION:

See D, Markowitz, Scheid, Statman (JFQA 2010)

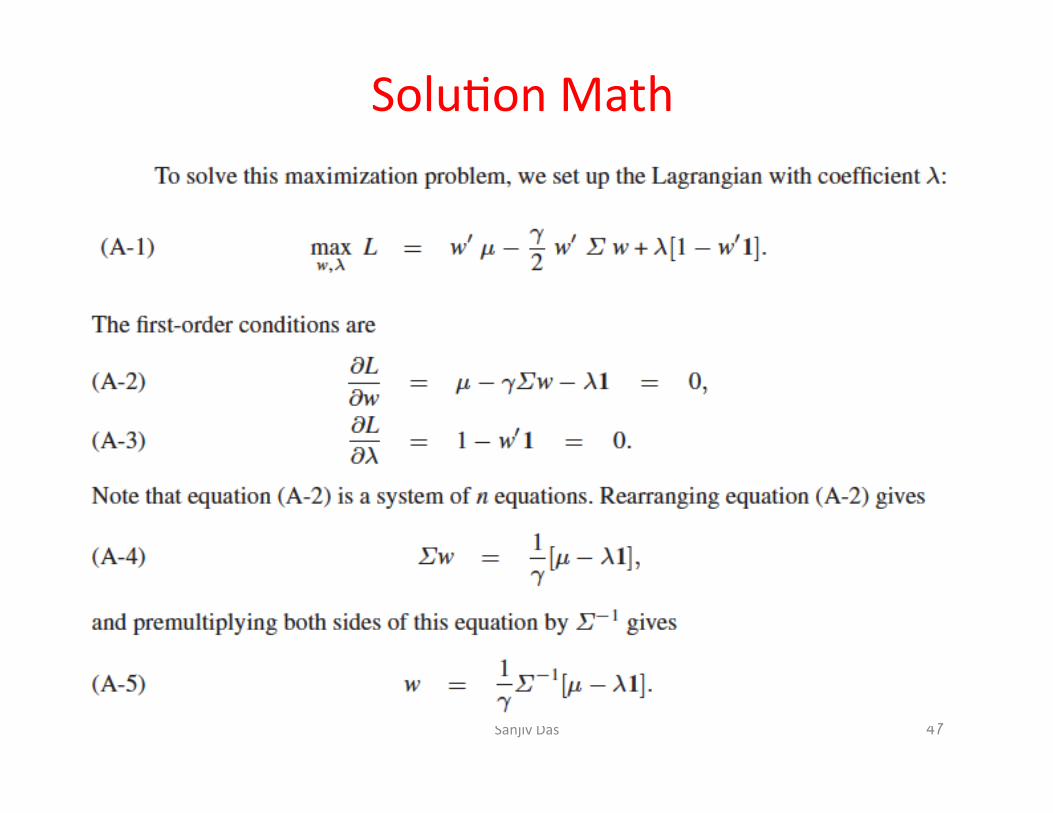

SoluGon Math

Sanjiv Das 47

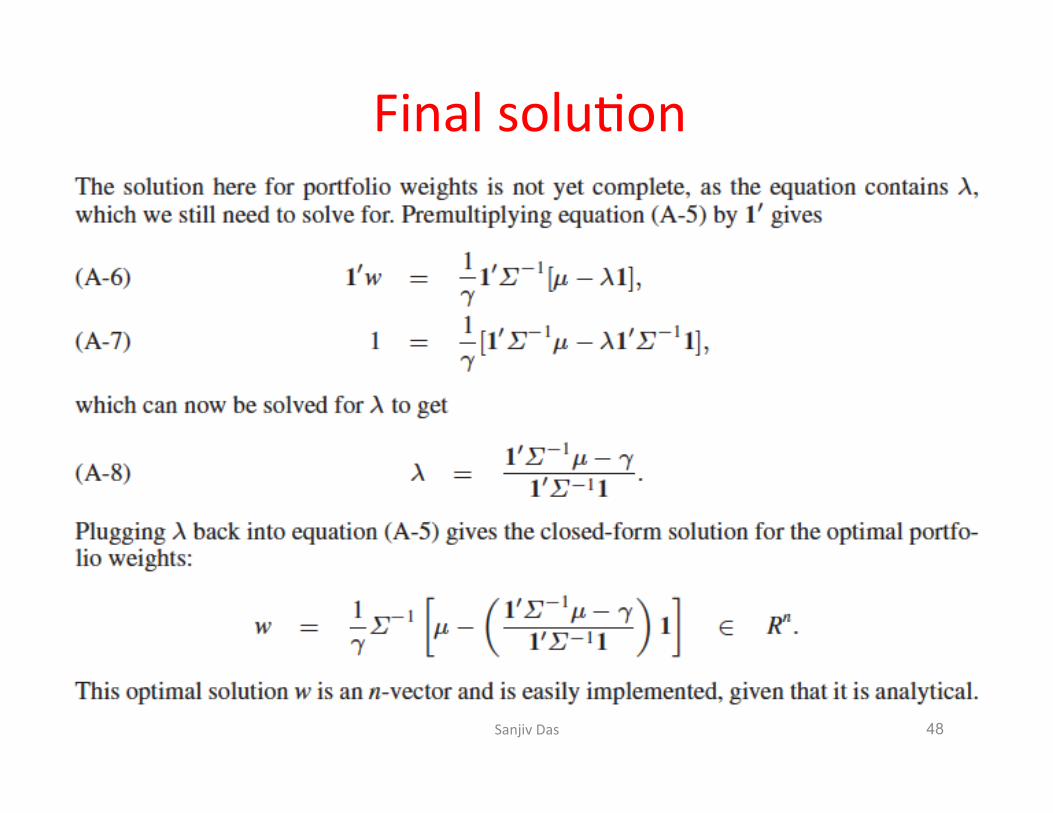

Final soluGon

Sanjiv Das 48

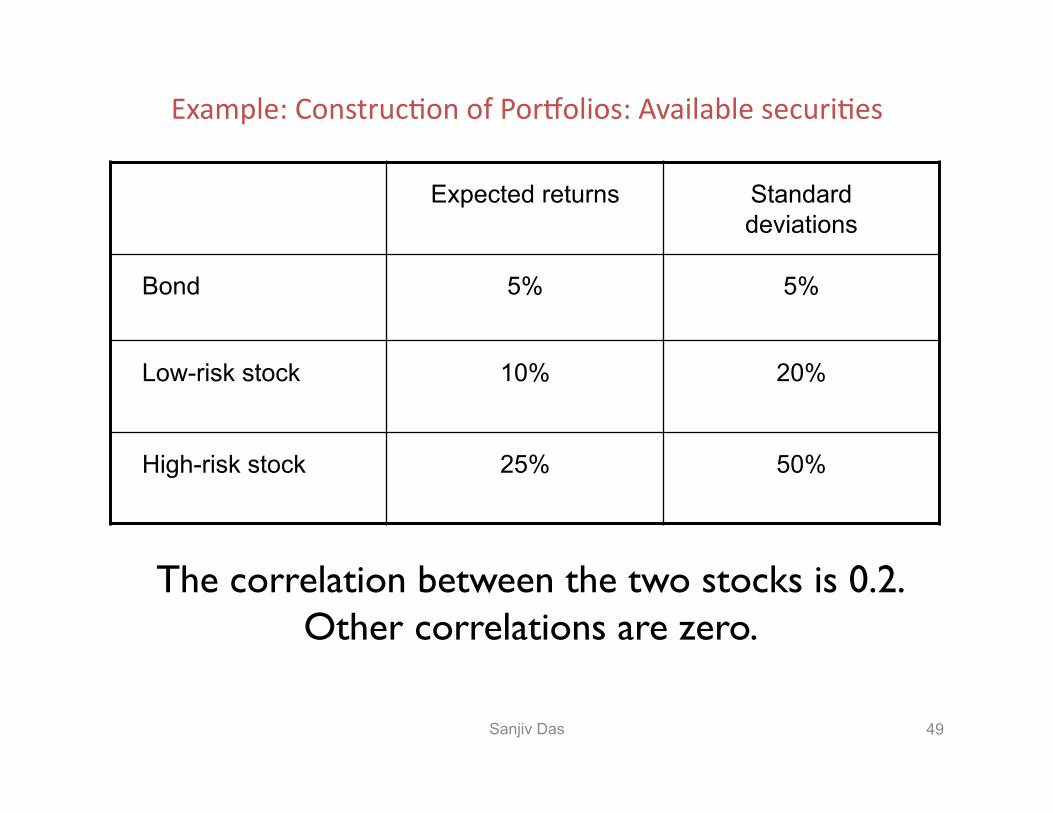

Example: ConstrucGon of PorOolios: Available securiGes

Expected returns Standard deviations

Bond 5% 5%

Low-risk stock 10% 20%

High-risk stock 25% 50%

Sanjiv Das 49

The correlation between the two stocks is 0.2. Other correlations are zero.

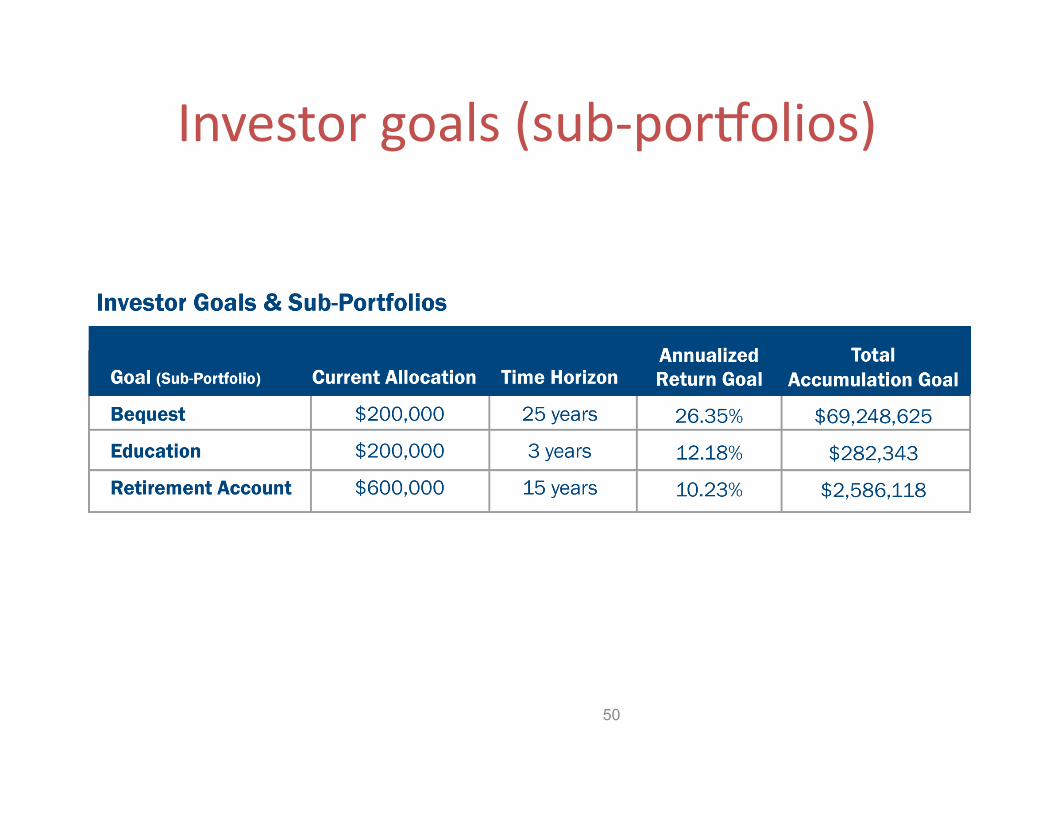

Investor goals (sub-‐porOolios)

50

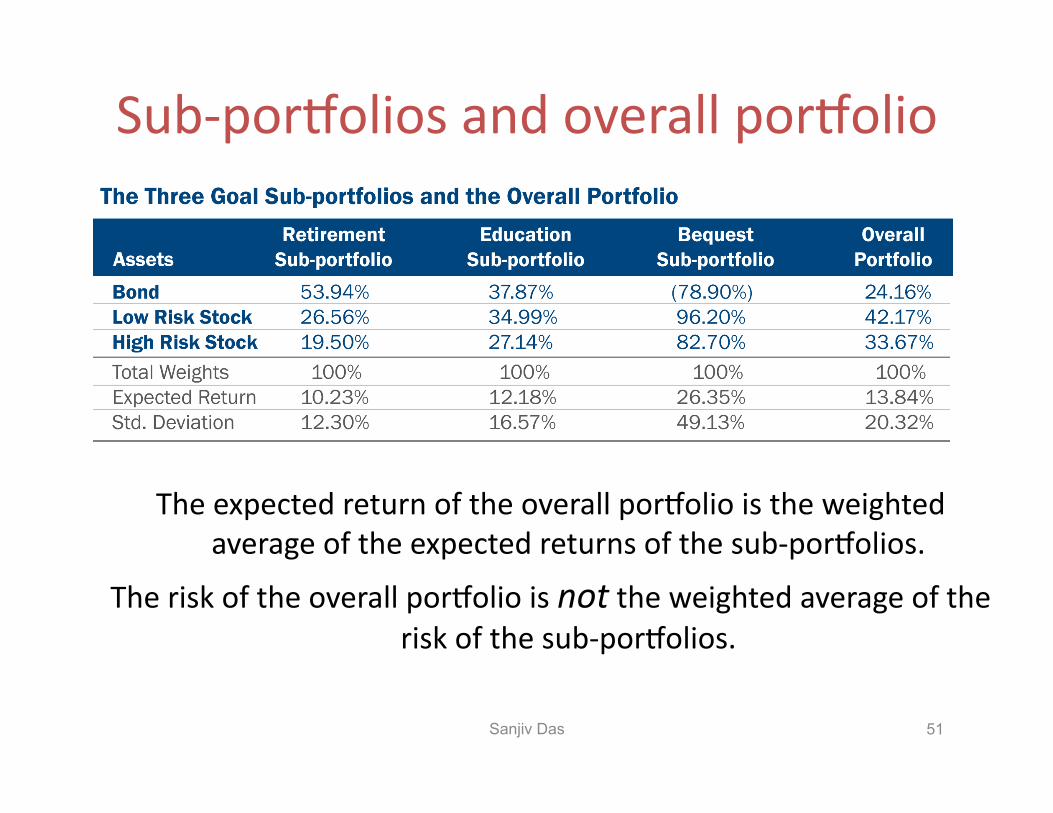

Sub-‐porOolios and overall porOolio

The expected return of the overall porOolio is the weighted average of the expected returns of the sub-‐porOolios.

The risk of the overall porOolio is not the weighted average of the risk of the sub-‐porOolios.

Sanjiv Das 51

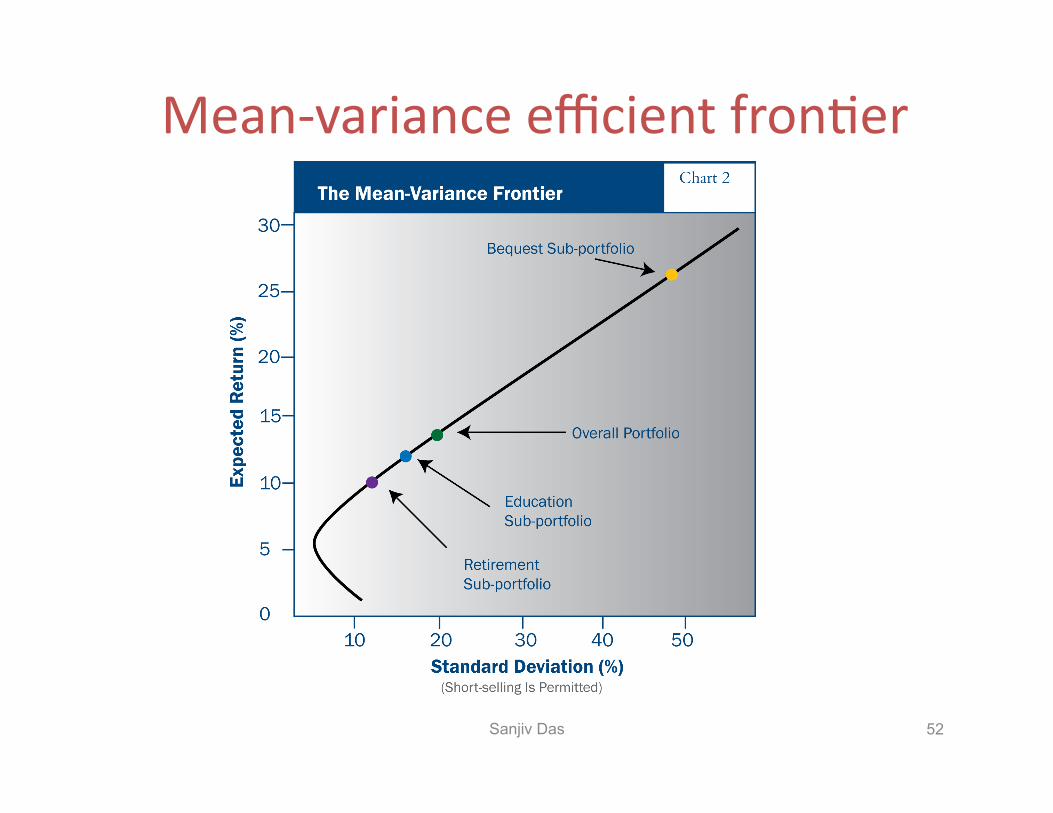

Mean-‐variance efficient fronGer

Sanjiv Das 52

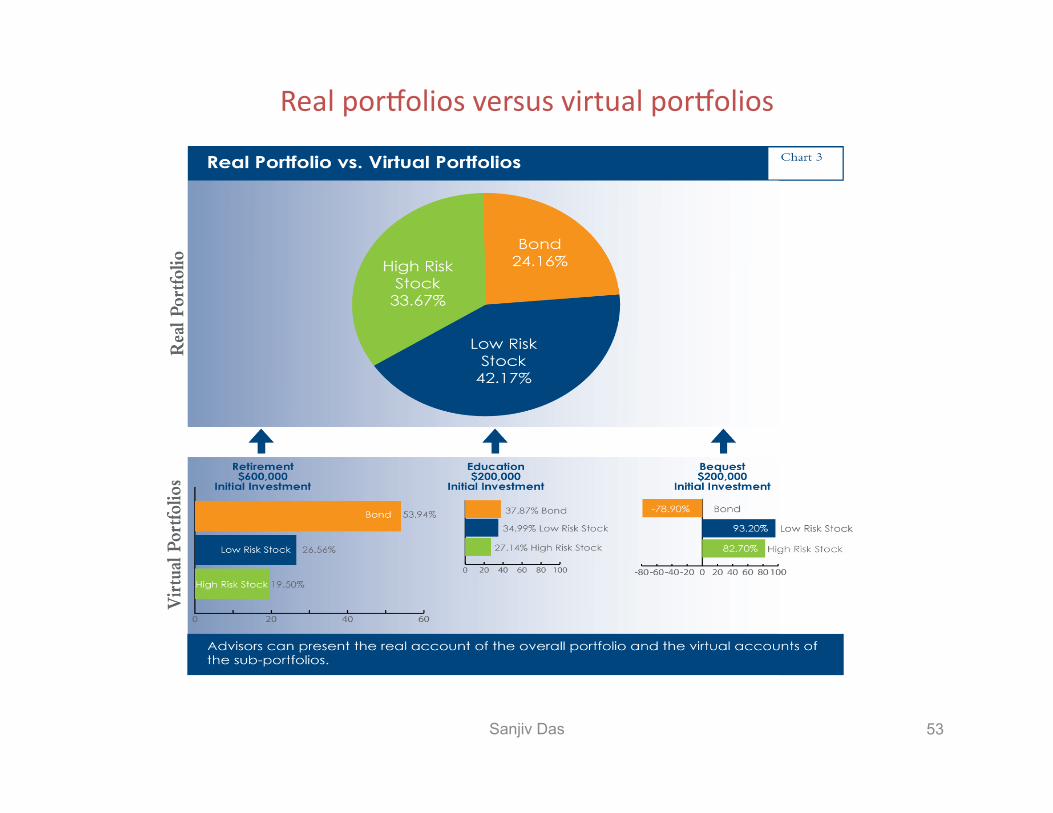

Real porOolios versus virtual porOolios

Sanjiv Das 53

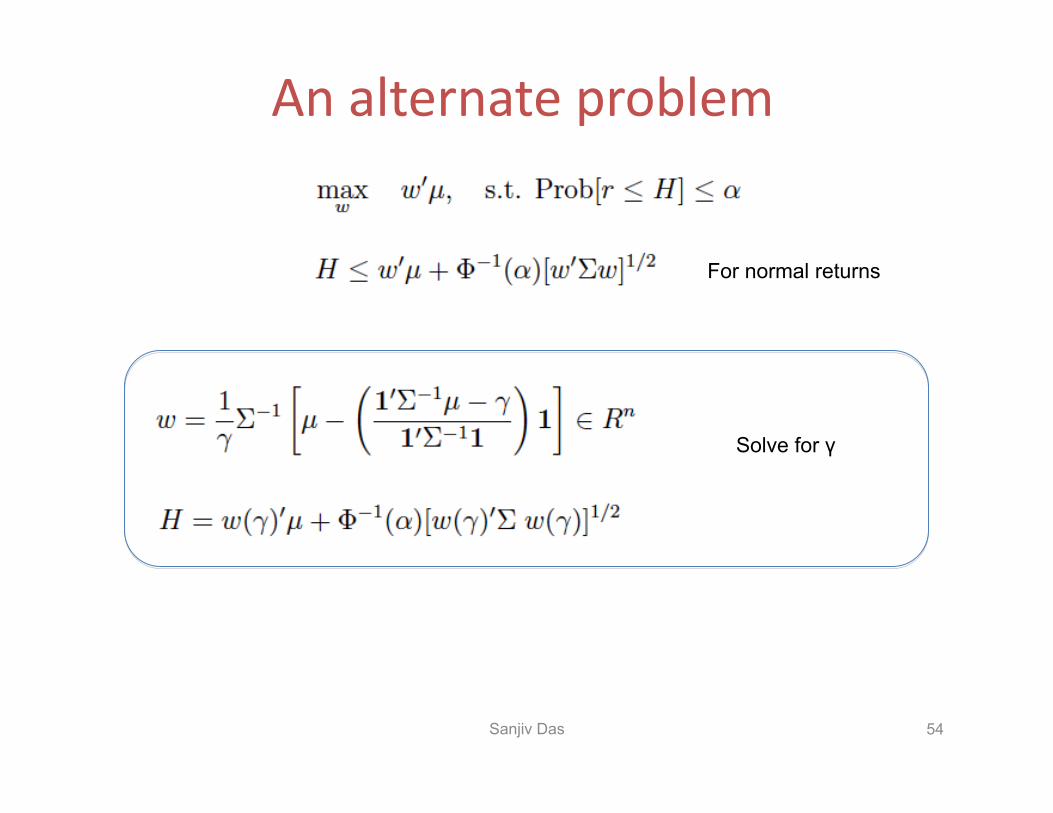

An alternate problem

Sanjiv Das 54

For normal returns

Solve for γ

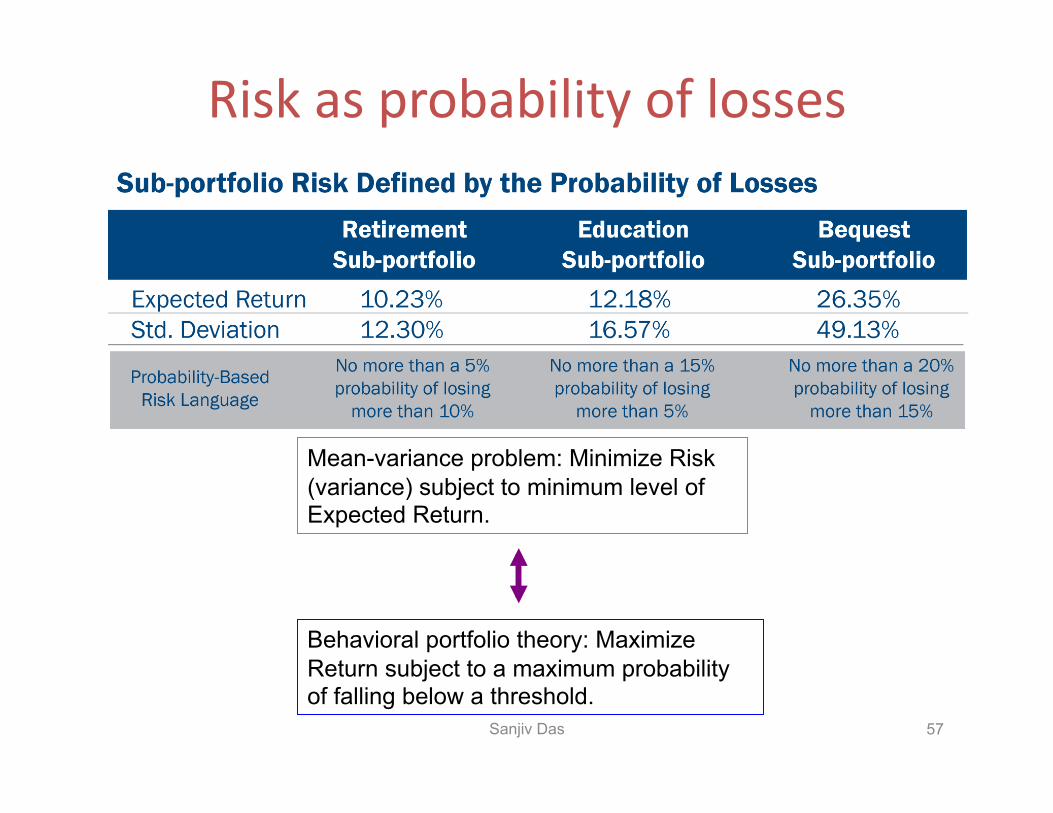

Risk as probability of losses

Sanjiv Das 57

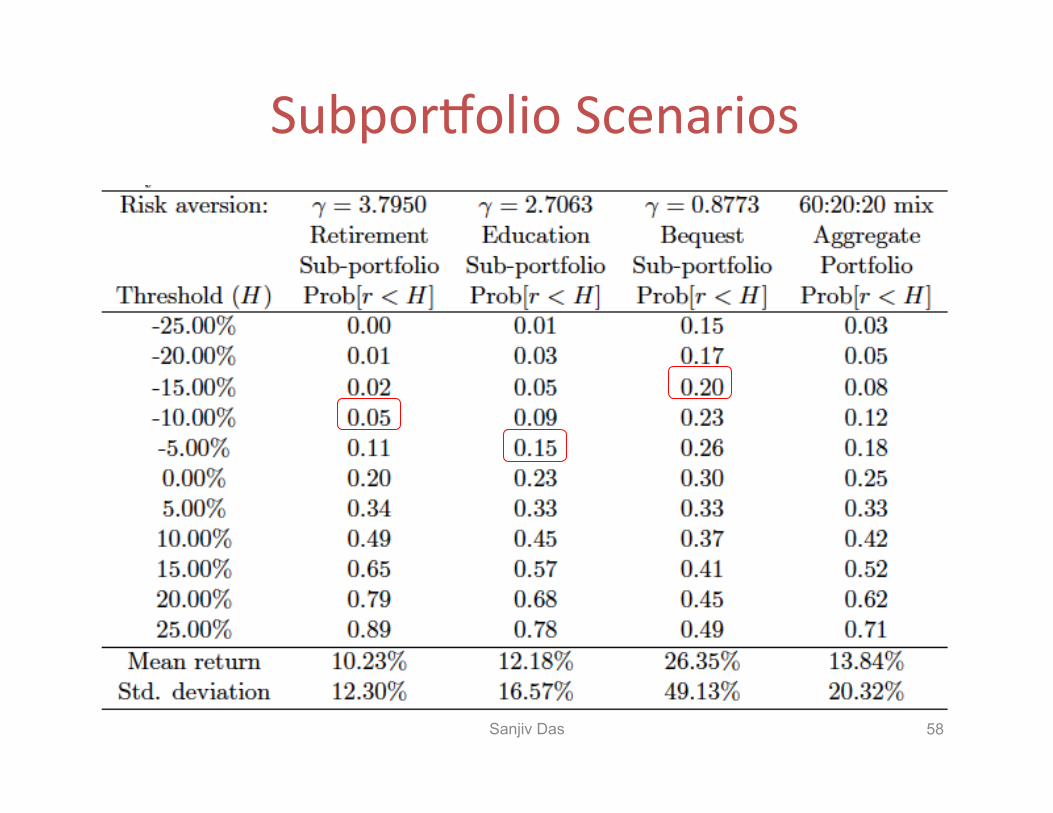

Mean-variance problem: Minimize Risk (variance) subject to minimum level of Expected Return.

Behavioral portfolio theory: Maximize Return subject to a maximum probability of falling below a threshold.

SubporOolio Scenarios

Sanjiv Das 58

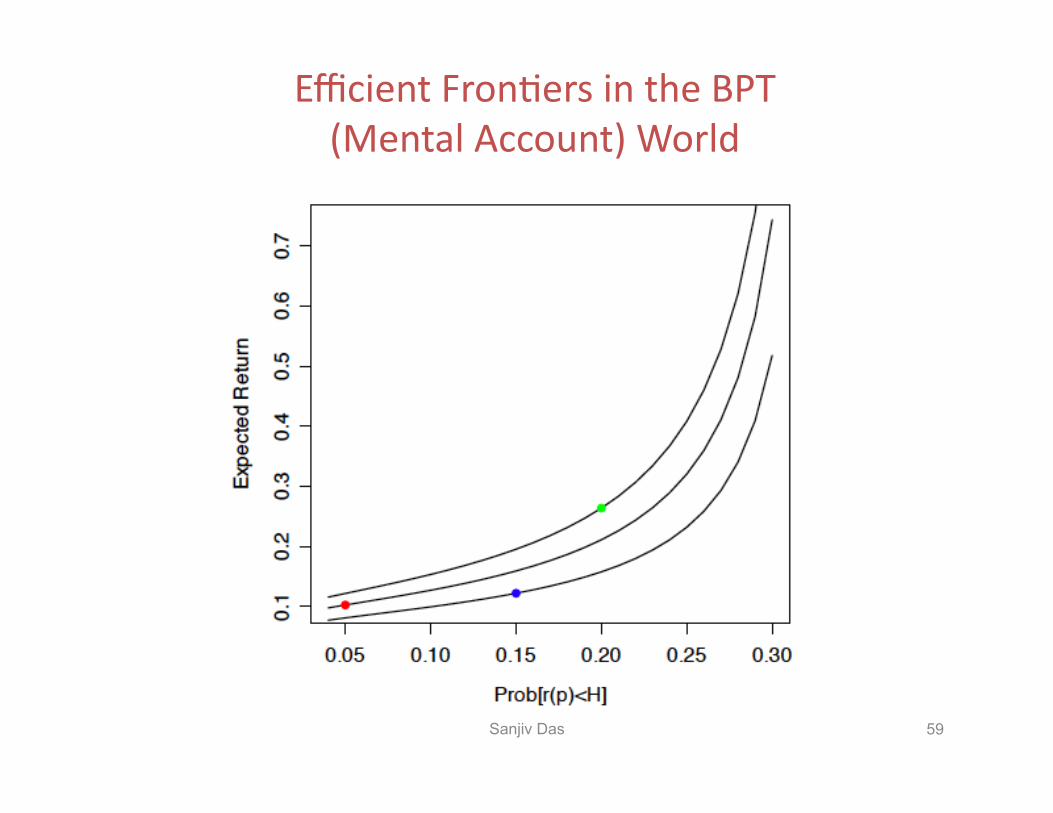

Efficient FronGers in the BPT (Mental Account) World

Sanjiv Das 59

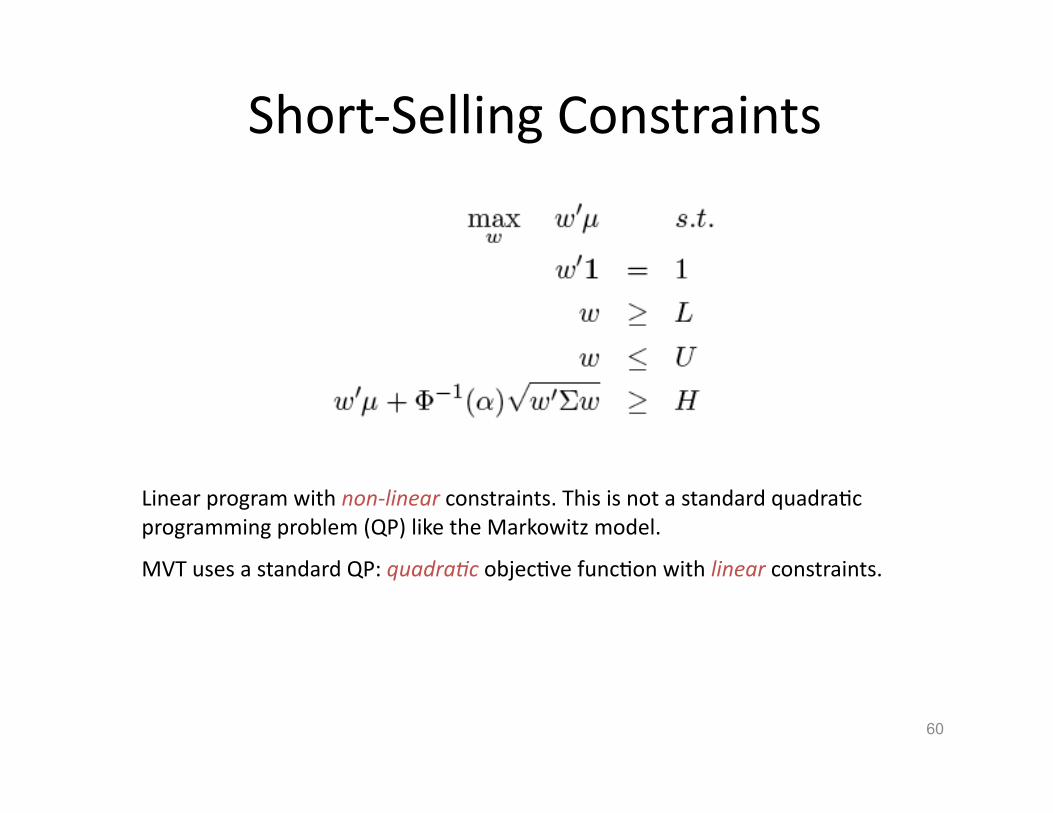

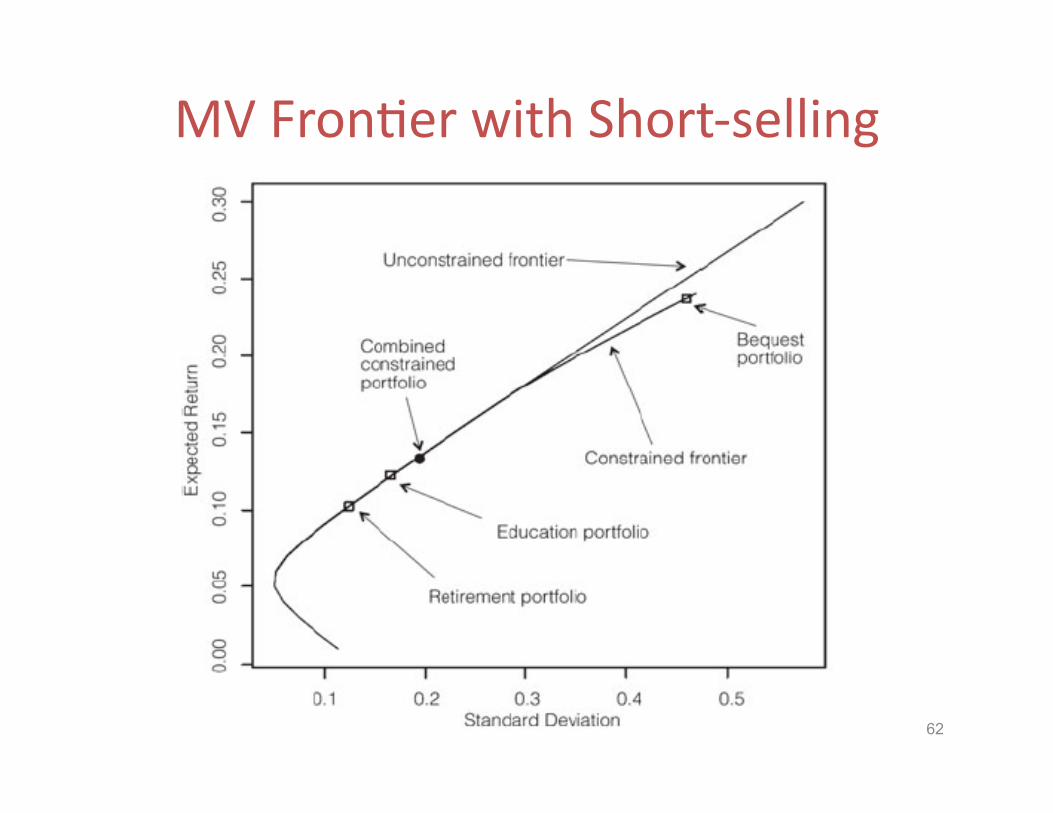

Short-‐Selling Constraints

60

Linear program with non-‐linear constraints. This is not a standard quadraGc programming problem (QP) like the Markowitz model.

MVT uses a standard QP: quadra8c objecGve funcGon with linear constraints.

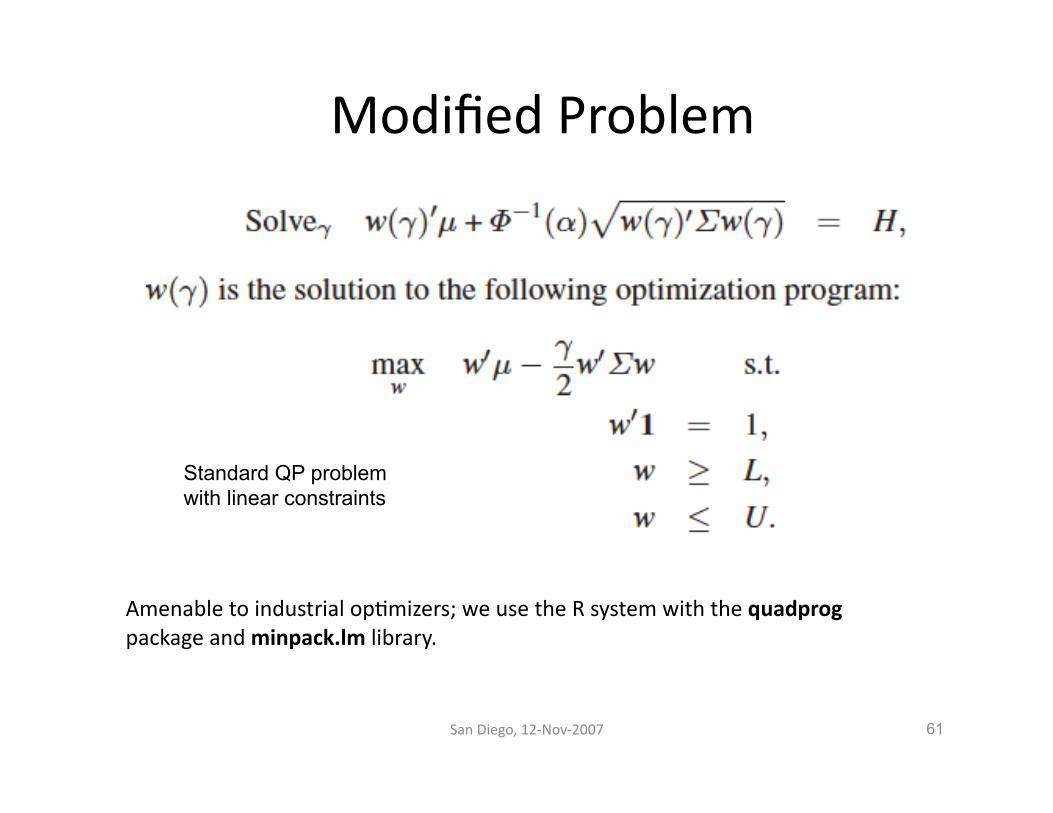

Modified Problem

San Diego, 12-‐Nov-‐2007 61

Standard QP

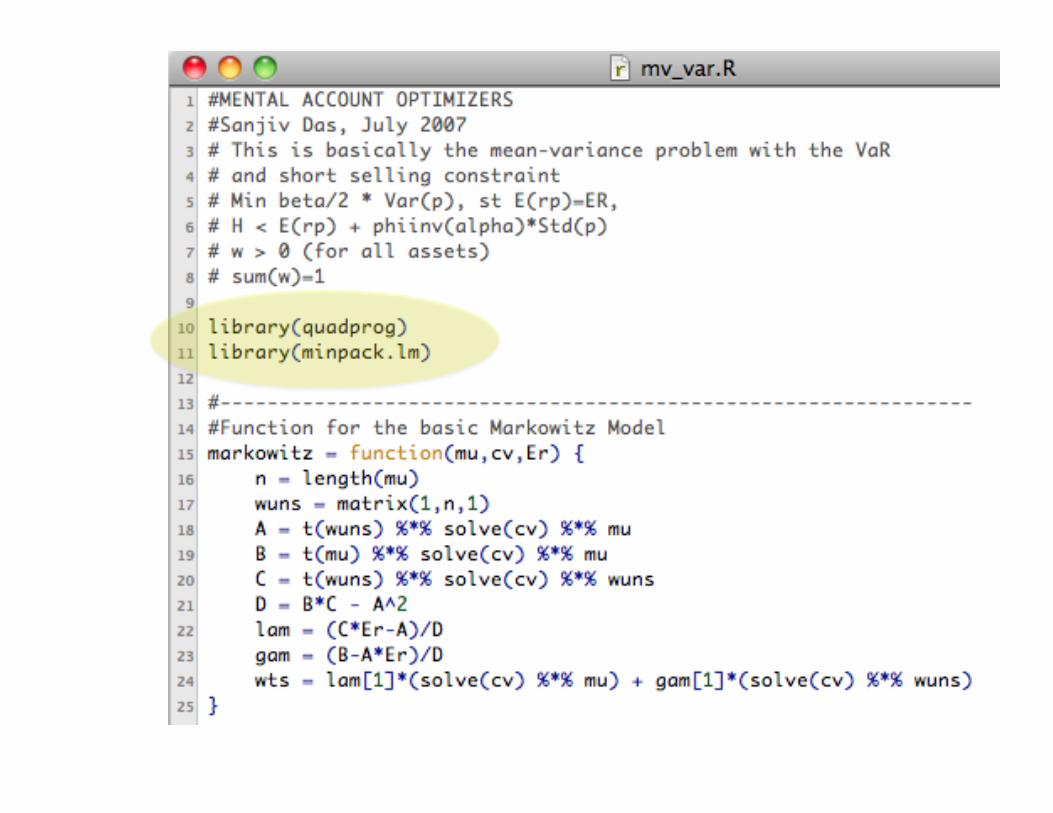

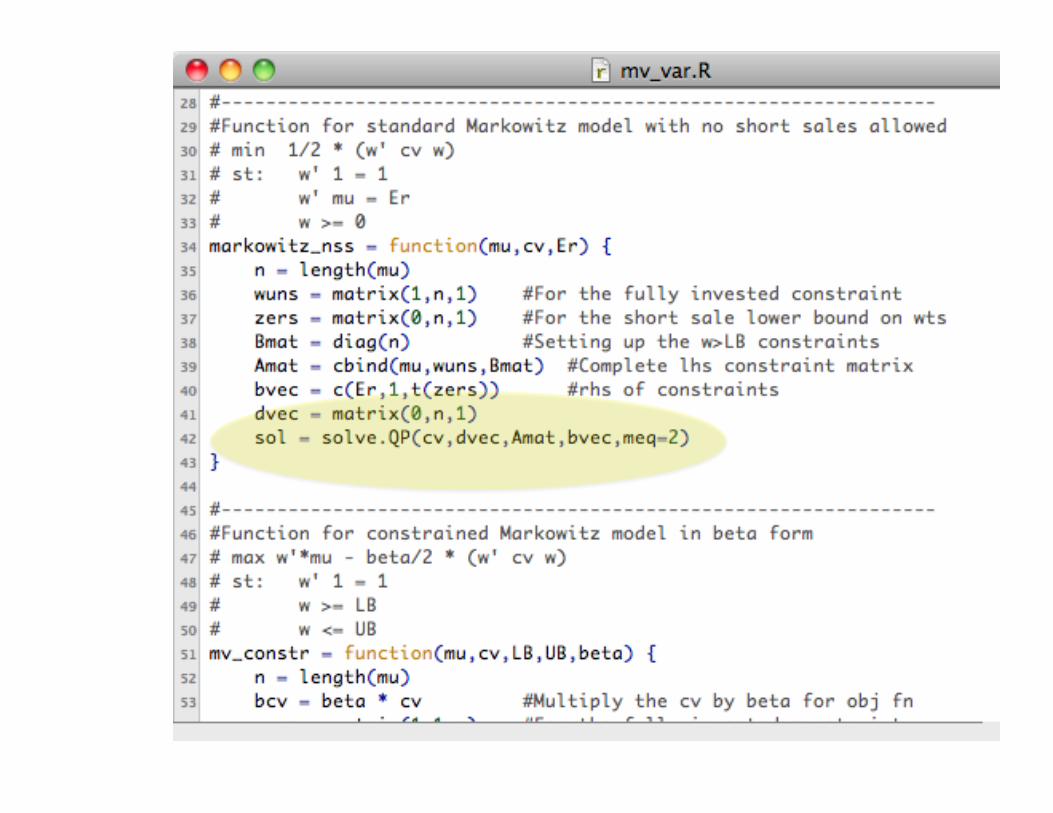

Amenable to industrial opGmizers; we use the R system with the quadprog package and minpack.lm library.

Standard QP problem with linear constraints

MV FronGer with Short-‐selling

Sanjiv Das 62

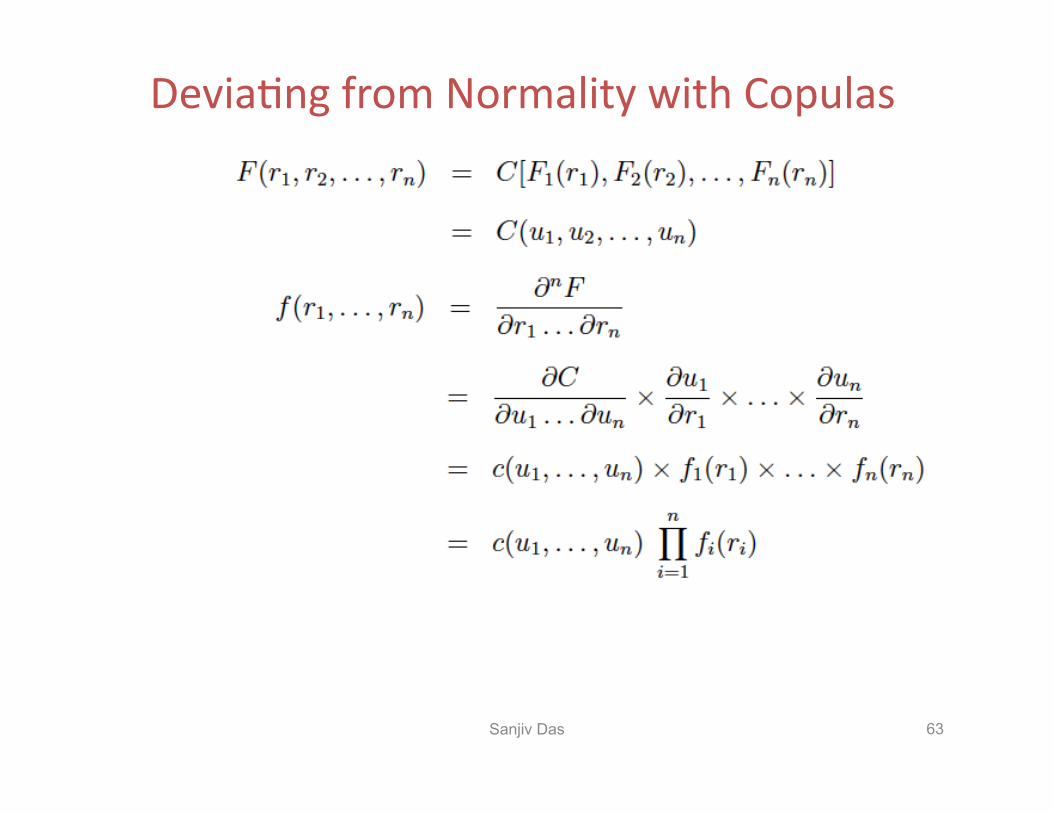

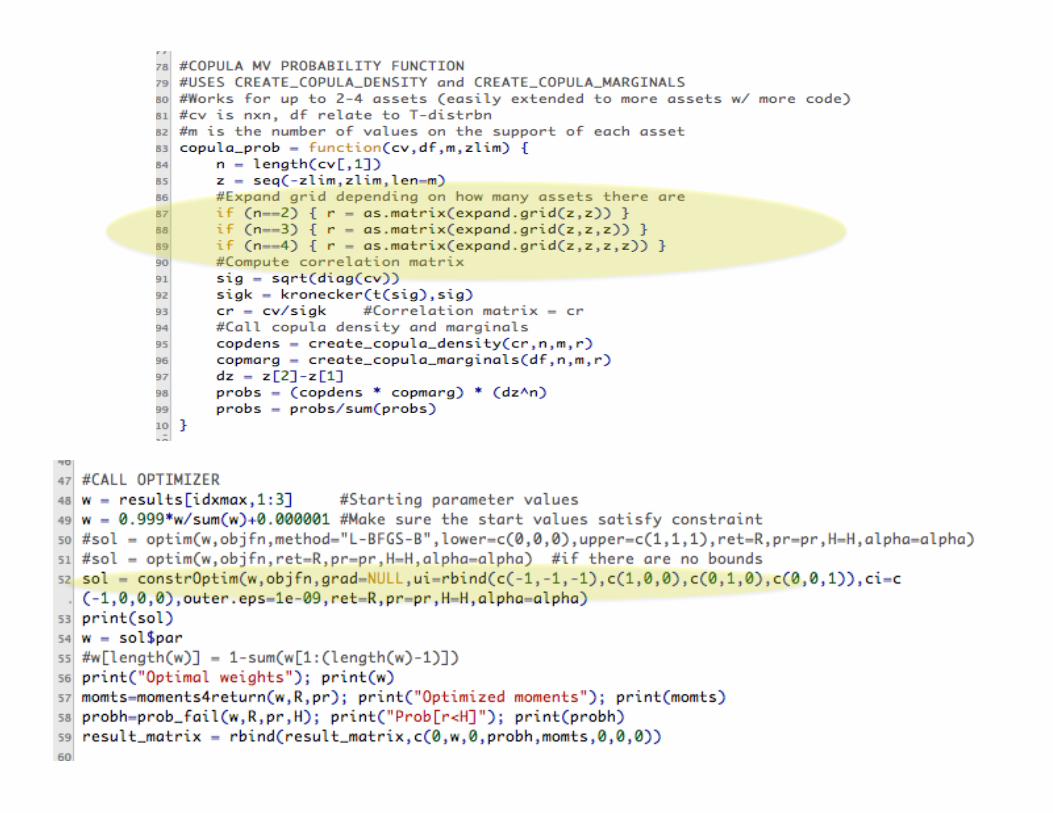

DeviaGng from Normality with Copulas

Sanjiv Das 63

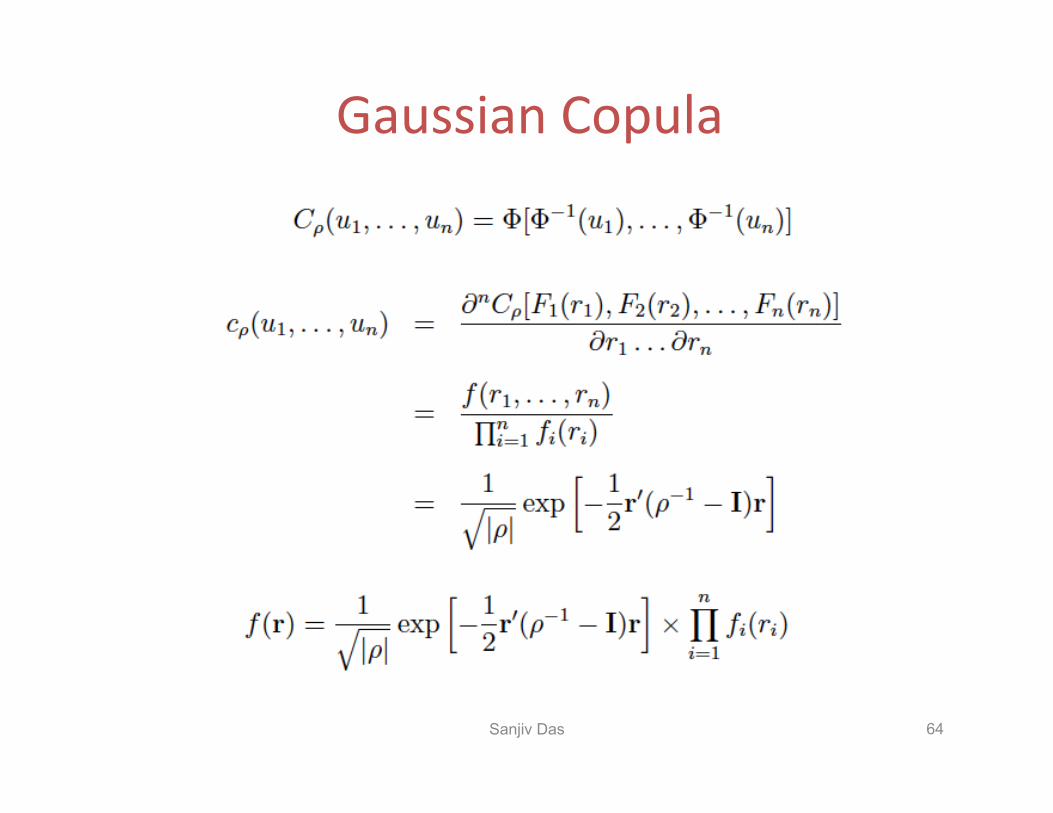

Gaussian Copula

Sanjiv Das 64

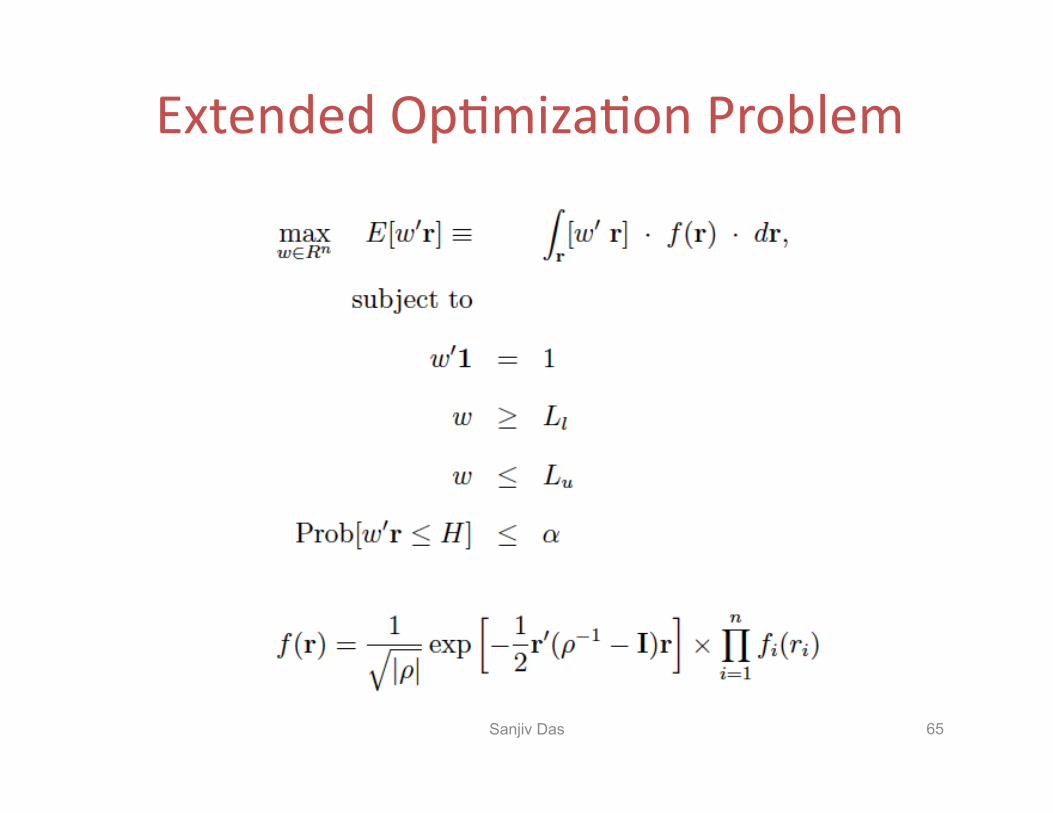

Extended OpGmizaGon Problem

Sanjiv Das 65

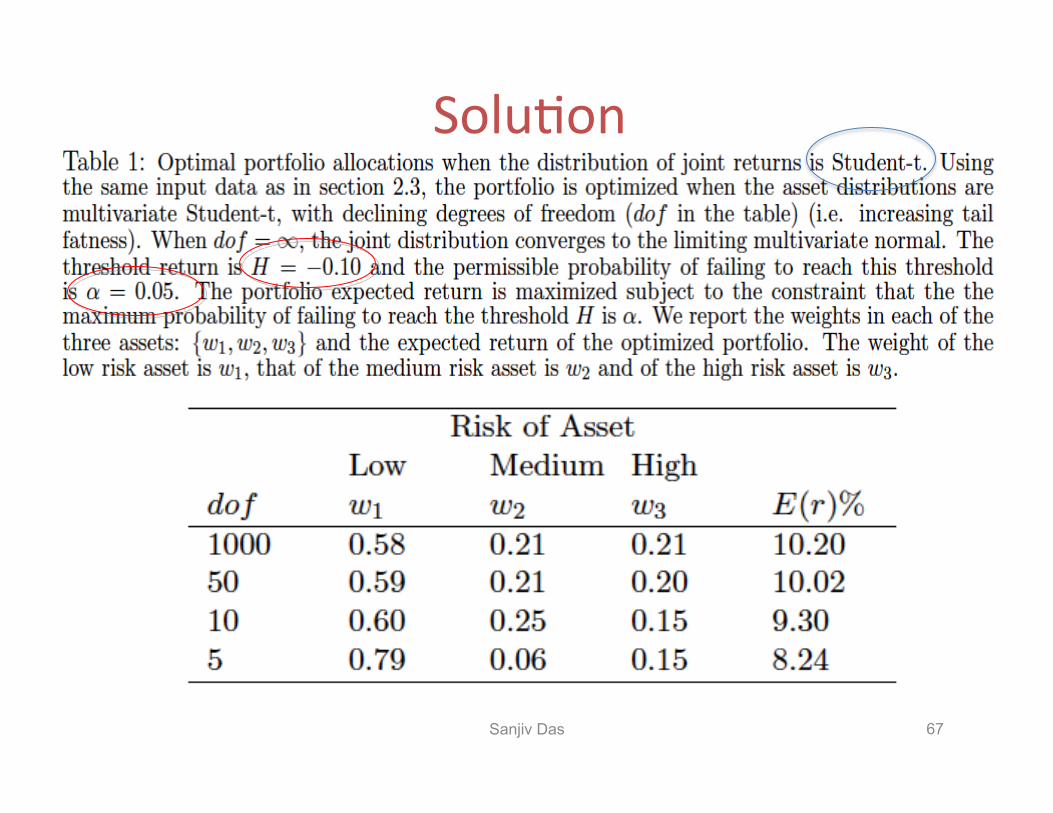

SoluGon

Sanjiv Das 67

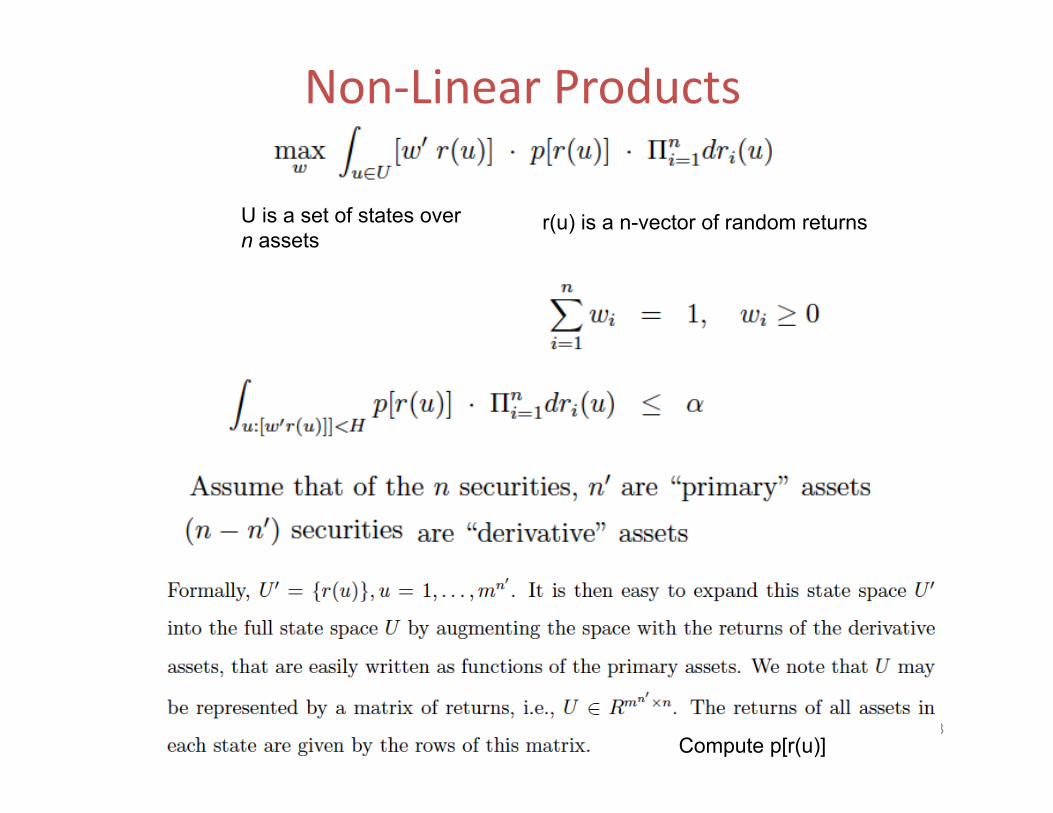

Non-‐Linear Products

Sanjiv Das 68

U is a set of states over n assets

r(u) is a n-vector of random returns

Compute p[r(u)]

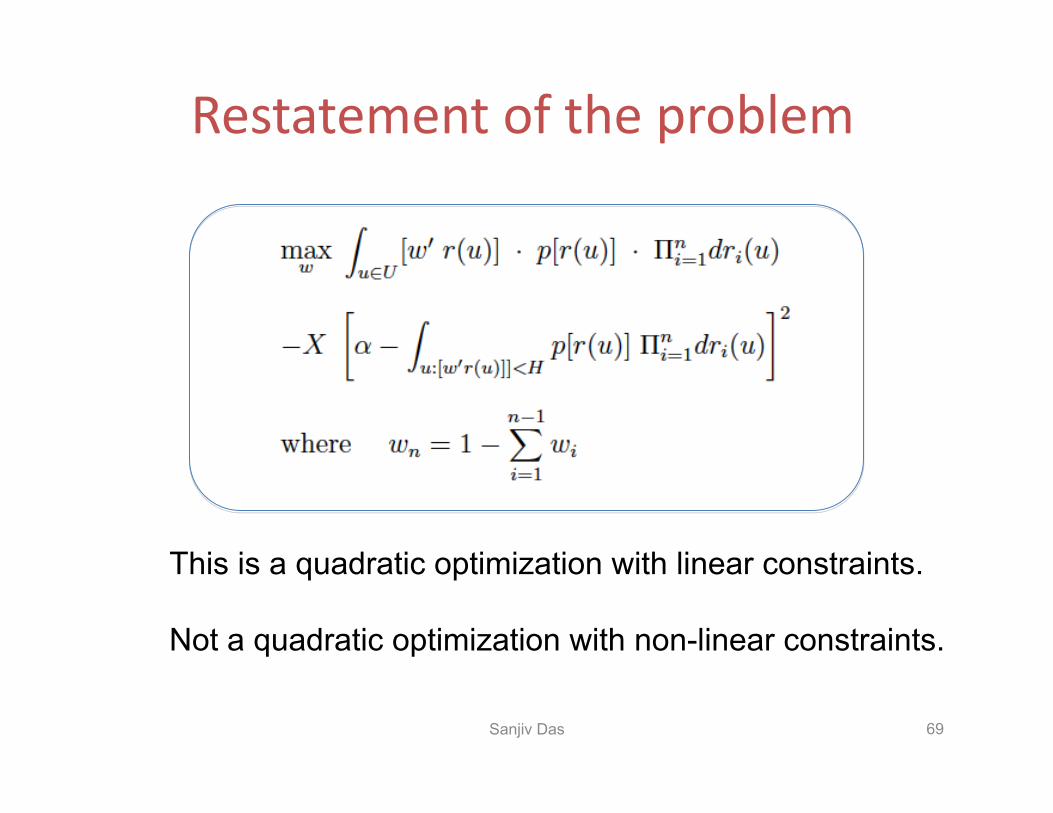

Restatement of the problem

Sanjiv Das 69

This is a quadratic optimization with linear constraints.

Not a quadratic optimization with non-linear constraints.

Introducing Structured Products

Sanjiv Das 70

Can we improve the risk-adjusted returns in a portfolio by using puts and calls?

Derivatives are very risky.

And so ….

Are puts opGmal?

Sanjiv Das 71

No, they add very little value to the portfolio.

But …

Puts are needed when the threshold return is high

Sanjiv Das 72

For high thresholds the investor cannot get an acceptable portfolio without puts.

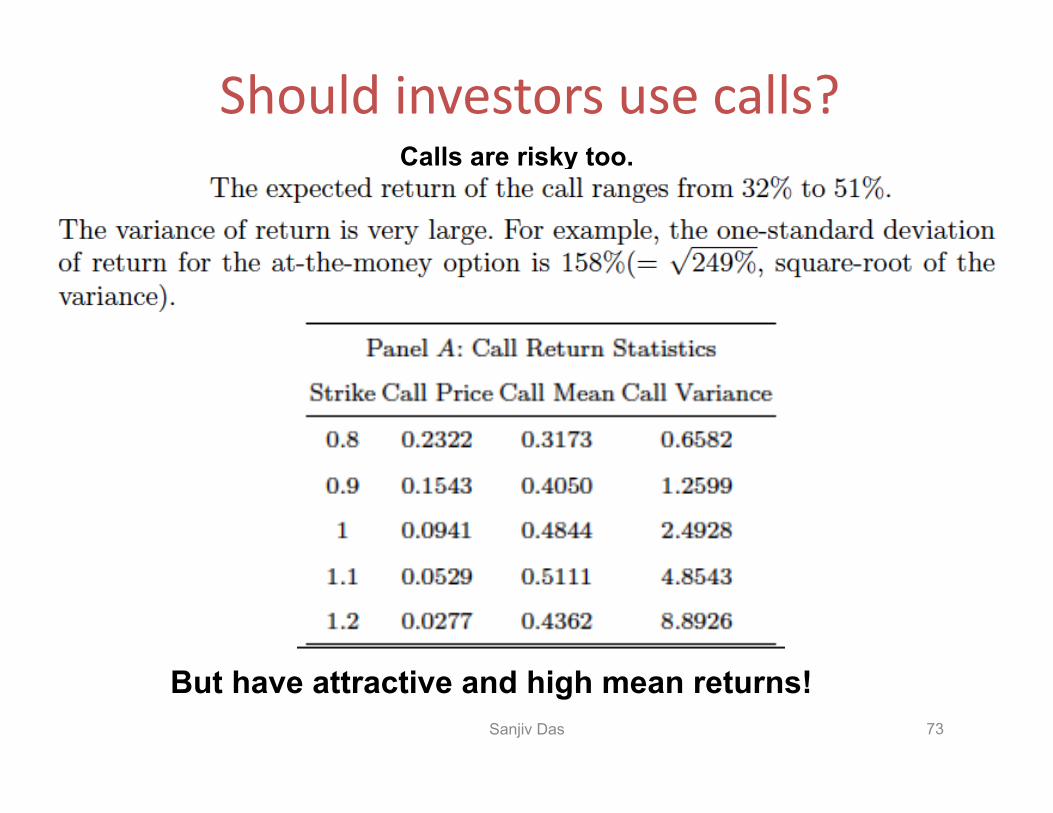

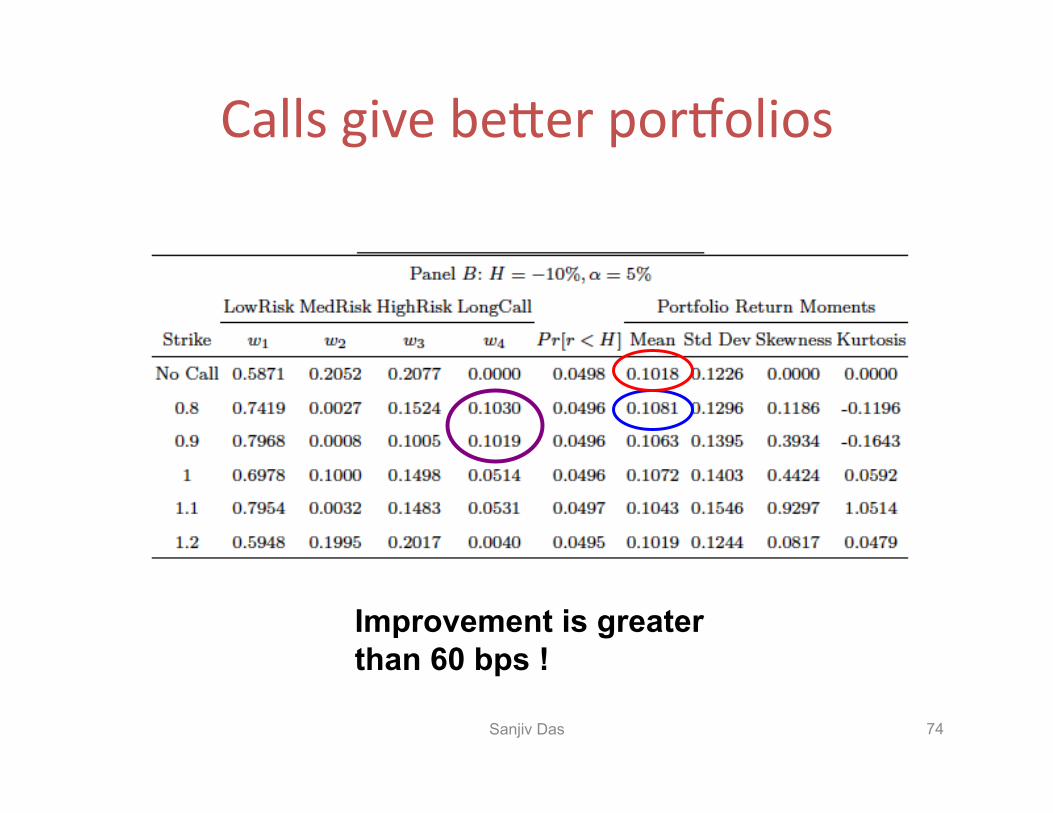

Should investors use calls?

Sanjiv Das 73

Calls are risky too.

But have attractive and high mean returns!

Calls give be?er porOolios

Sanjiv Das 74

Improvement is greater than 60 bps !

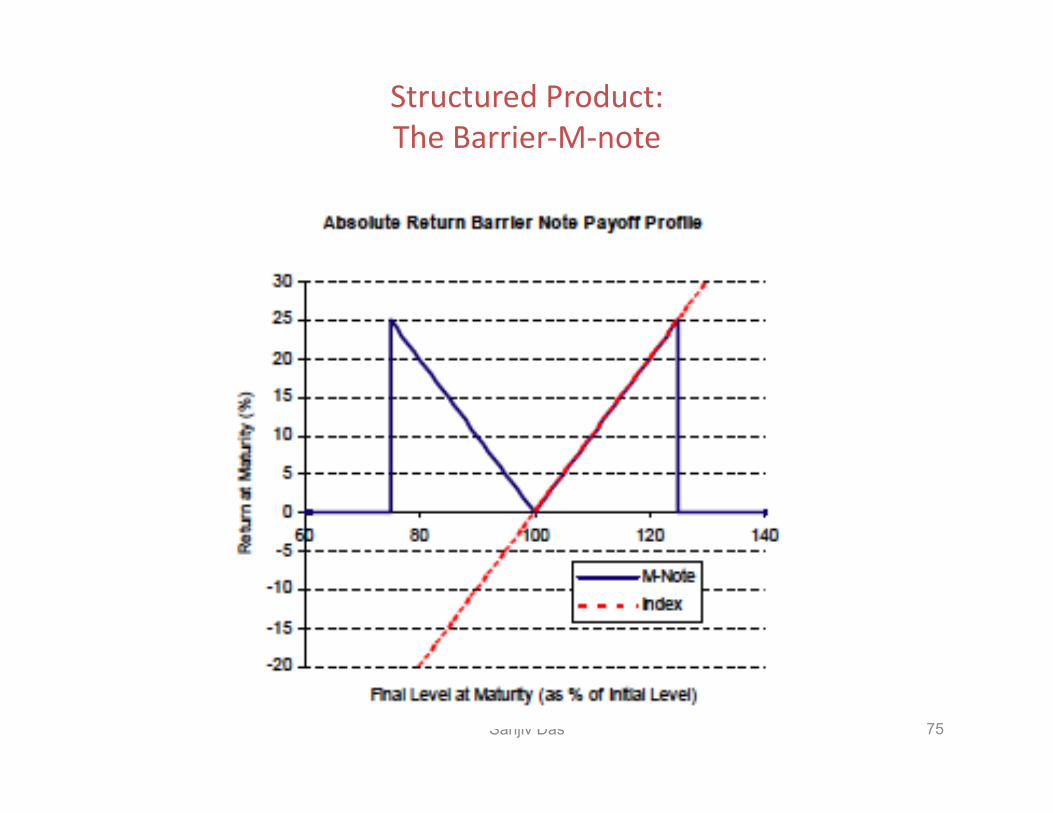

Structured Product: The Barrier-‐M-‐note

Sanjiv Das 75

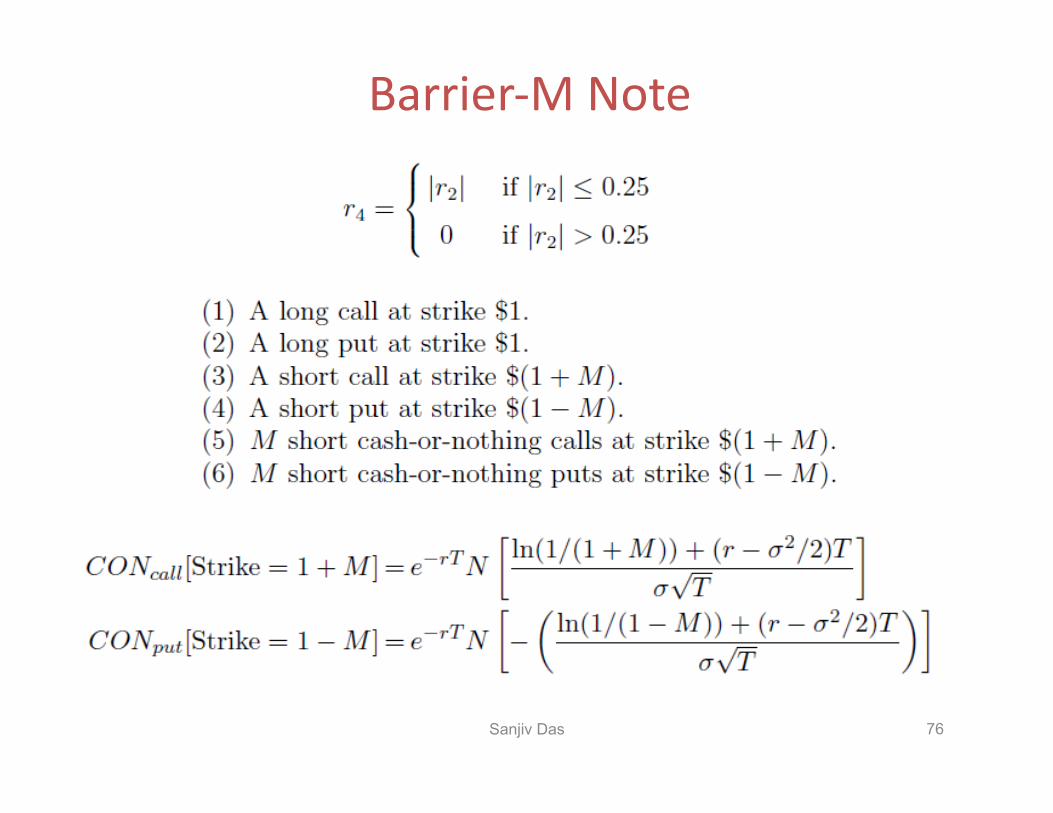

Barrier-‐M Note

Sanjiv Das 76

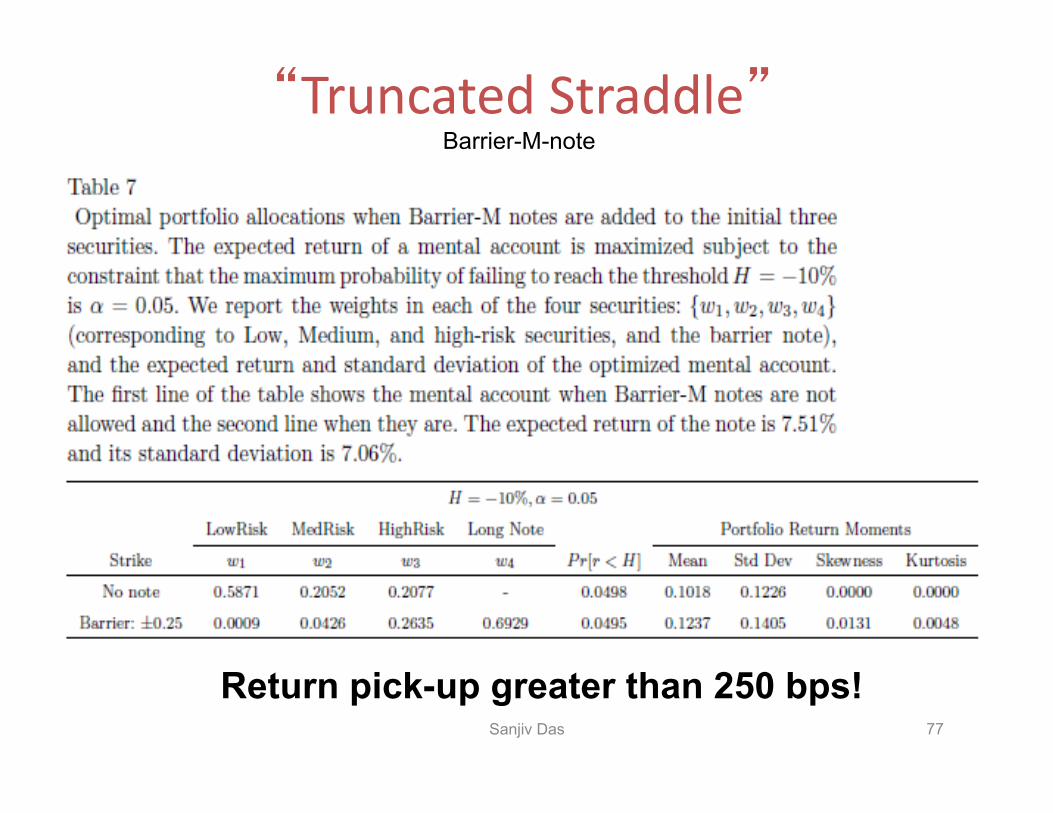

“Truncated Straddle”

Sanjiv Das 77

Return pick-up greater than 250 bps!

Barrier-M-note

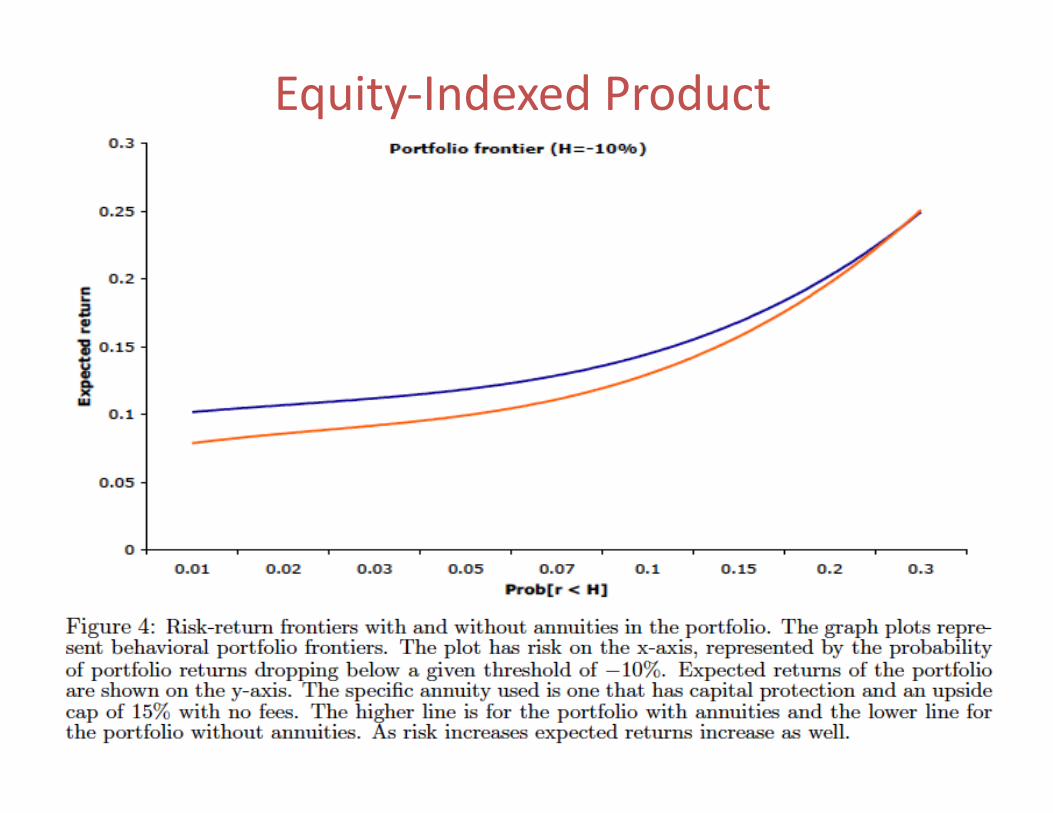

Equity-‐Indexed Product

Sanjiv Das 78

Conclusion • Investors find it easier to think in terms of mental accounts or sub-‐porOolios

when trying to reach their separate financial goals.

• Behavioral porOolio theory deals with maximizing return subject to managing the risk of loss. This problem has a mathemaGcal mapping into mean-‐variance opGmizaGon, yet is much more general.

• Even with short-‐selling prohibited, the loss from sub-‐porOolio opGmizaGon is smaller than the loss from misesGmaGng investor preferences.

• ReporGng performance by sub-‐porOolio enables investors to track their goals be?er.

• Goal-‐based opGmizaGon enables choosing porOolios even when normality is not assumed.

• Goal-‐based opGmizaGon provides a framework for including structured products in investor porOolios.

Sanjiv Das 79

The research papers for this work are on my web page – just google it. h?p://algo.scu.edu/~sanjivdas/research.htm/

1. Das, Markowitz, Scheid, and Statman (JFQA 2010), “PorOolio OpGmizaGon with Mental Accounts”

2. Das & Statman (2008), “Beyond Mean-‐Variance: PorOolio with Structured Products and non-‐Gaussian returns.”

PEDAGOGICAL USES FOR R USING THE WEB

Topic 4

h?p://sanjivdas.wordpress.com/

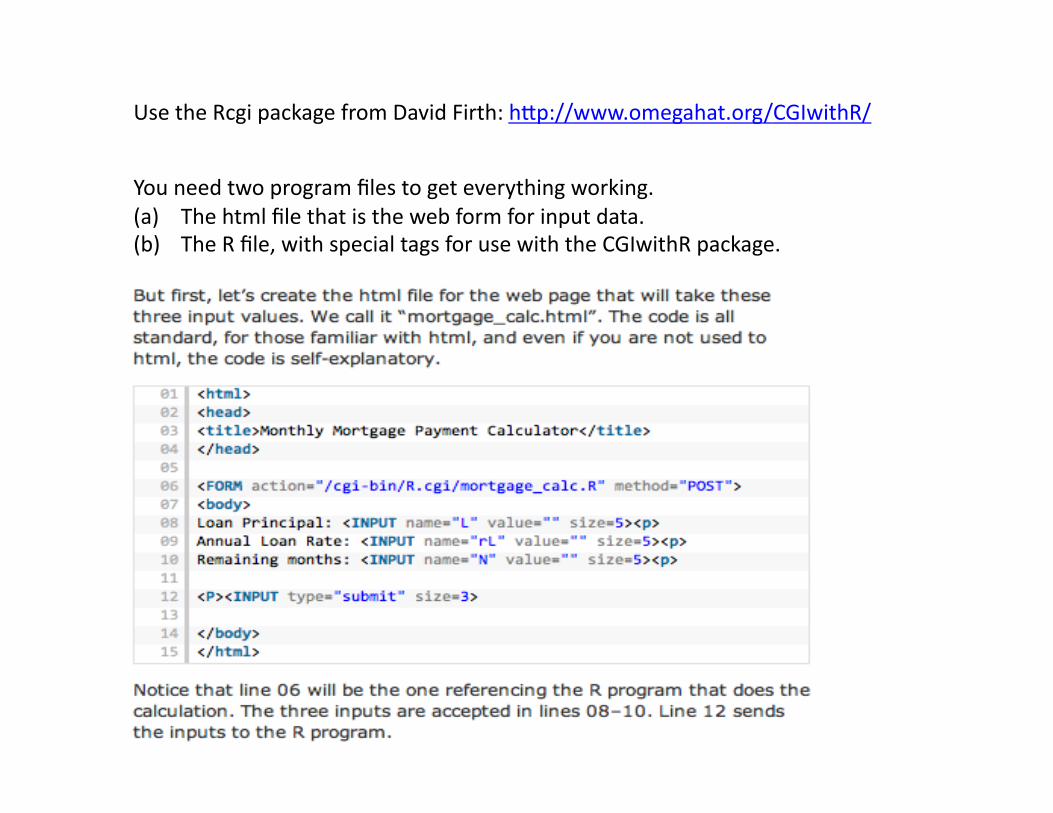

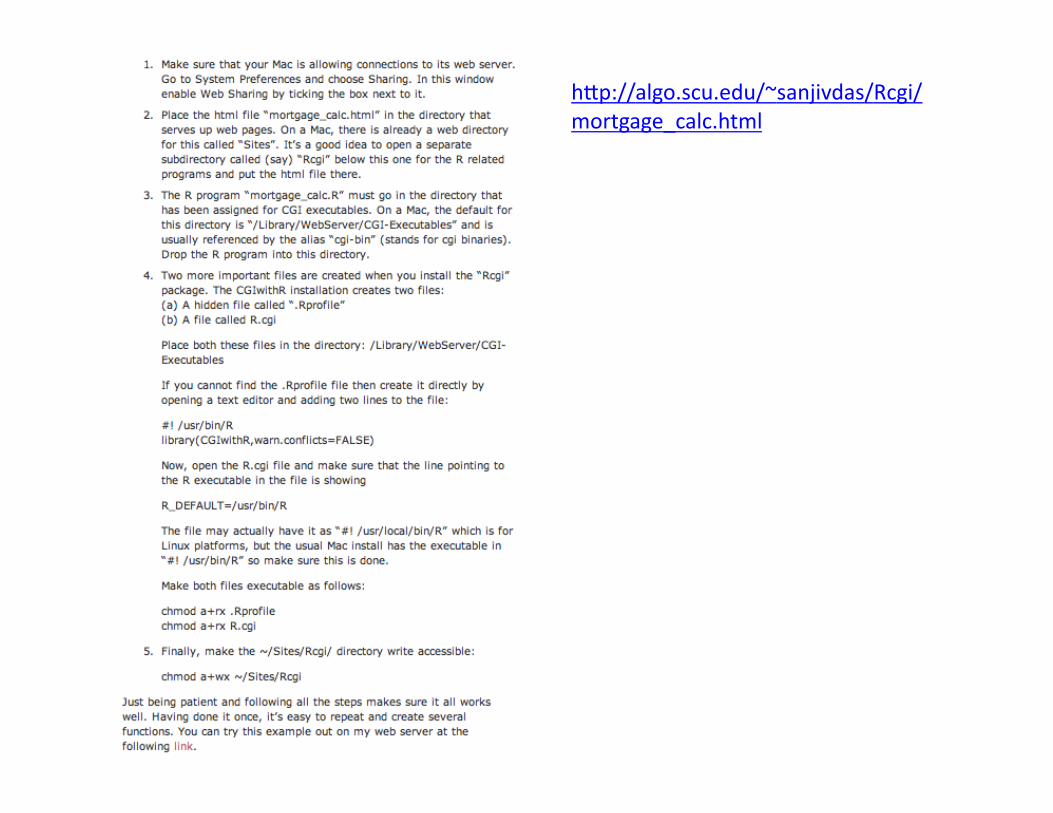

Use the Rcgi package from David Firth: h?p://www.omegahat.org/CGIwithR/

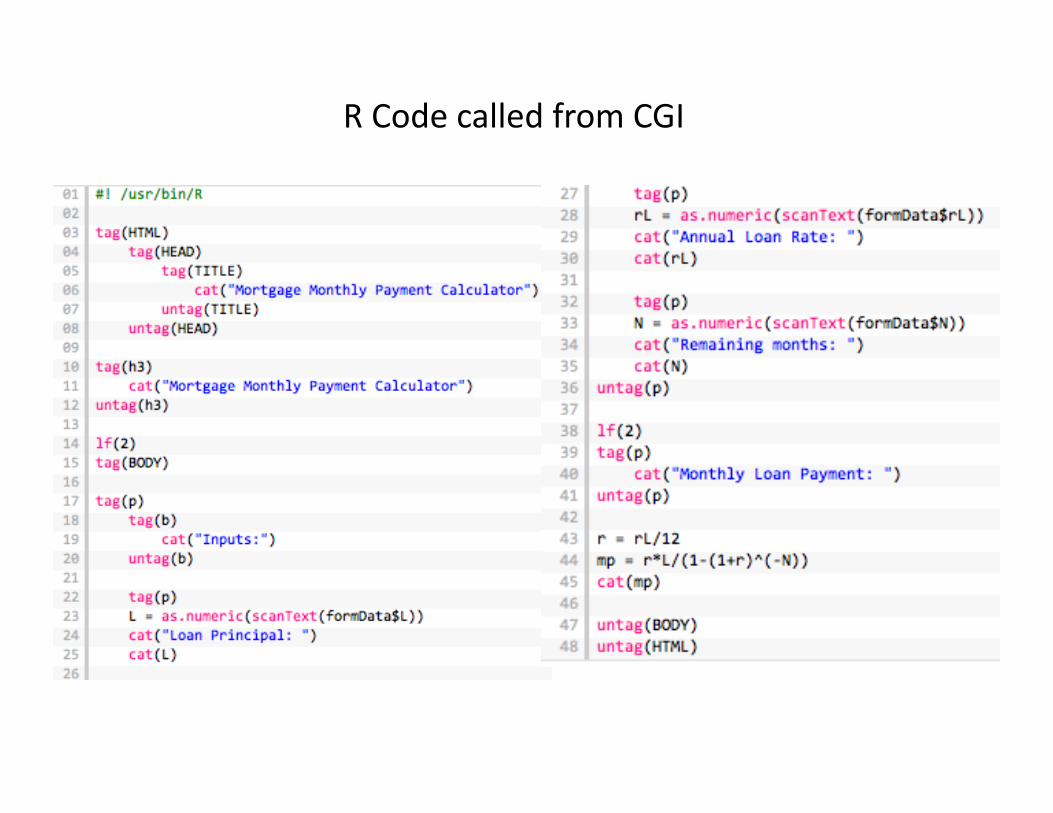

You need two program files to get everything working. (a) The html file that is the web form for input data. (b) The R file, with special tags for use with the CGIwithR package.

R Code called from CGI

h?p://algo.scu.edu/~sanjivdas/Rcgi/mortgage_calc.html

High-performance computing (parallelR)

Calling C from R

Lattice dynamic optimization

Network modeling

Optimization

High-dimensional distributions with copulas

Web functions

Q?