Embed Size (px)

Citation preview

Utah Legislative

Update, March 14, 2007

Phil Powlick, Manager

State Energy Program

Utah Geological Survey

Utah State Energy Program: Who Are We?

• Housed within the Utah Geological Survey– Part of the Utah DNR

• Spin-Off of old UT Energy Office• Promotes energy efficiency and renewable energy in

UT– Anemometer Loans & Wind Resource Characterization– Public Outreach & Education on Renewables & Efficiency– Funds for Local Government Efficiency Upgrades (pilot)– Energy Information for Public and Policy & Program

Development– Certify renewable energy tax credits– New – Revolving Loan Fund for public school efficiency

Background:Utah’s pre-2007 Renewable Tax

Credits

• Income tax credits (personal and corporate) for residential renewable energy systems– Eligible technologies = Wind, Solar PV, Active

& Passive Solar Thermal, Hydro– Credit = 25% of cost up to $2,000 per

residence (lifetime)

Background:Utah’s pre-2007 Renewable Tax

Credits, continued• Income tax credits (personal and

corporate) for commercial renewable energy systems– Eligible technologies = Wind, Solar PV, Active

& Passive Solar Thermal, Hydro, Biomass, Waste Methane

– Credit = 10% of cost up to $50,000 per structure

• Structure could be a building, a turbine, or a solar water pump

Prior Tax Credit Statute Expired on December 31, 2006

• Old statute had 5-year sunset

• Efforts to renew credits for another 5 years stalled in 2006 General Session– Wide support in committee but confusion over

legislating the “flat tax”– Renewal bill dies in last hours of session

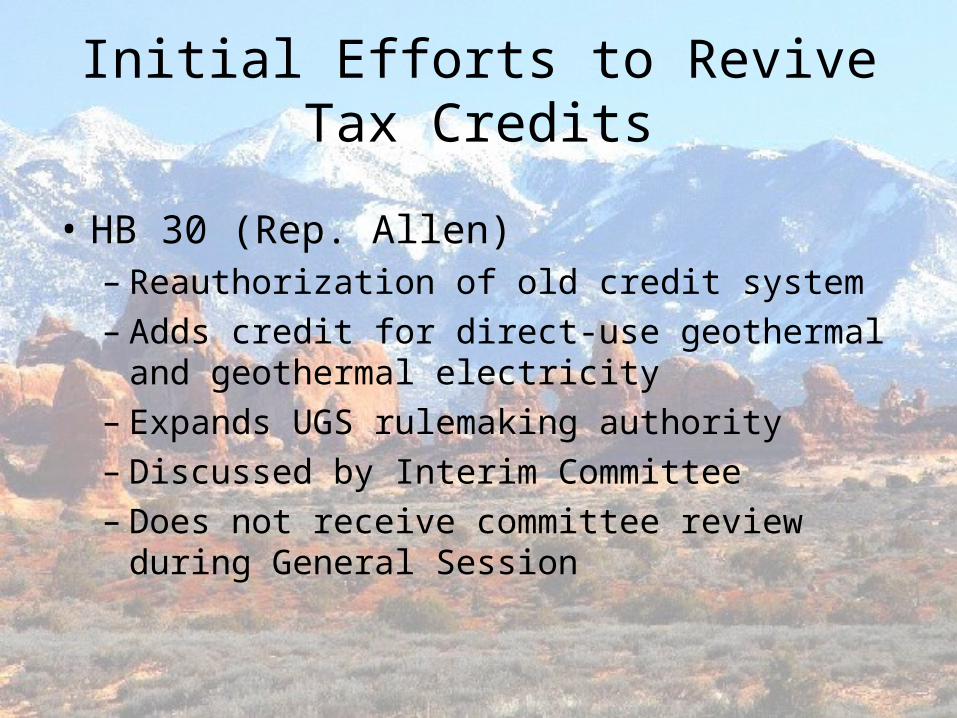

Initial Efforts to Revive Tax Credits

• HB 30 (Rep. Allen)– Reauthorization of old credit system– Adds credit for direct-use geothermal and

geothermal electricity– Expands UGS rulemaking authority– Discussed by Interim Committee– Does not receive committee review during

General Session

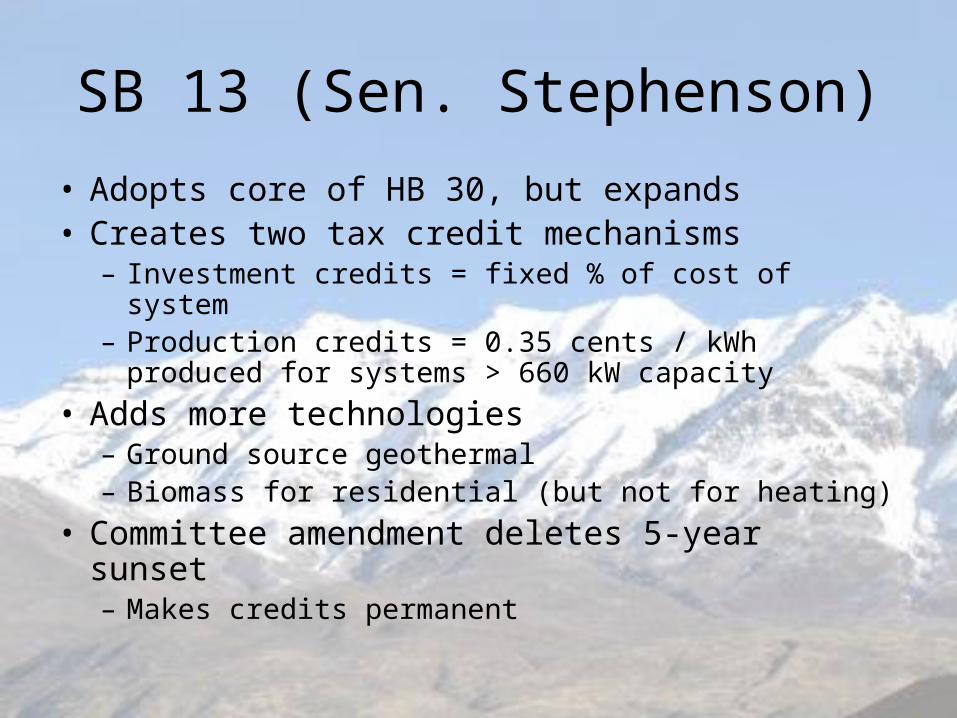

SB 13 (Sen. Stephenson)

• Adopts core of HB 30, but expands• Creates two tax credit mechanisms

– Investment credits = fixed % of cost of system– Production credits = 0.35 cents / kWh produced for

systems > 660 kW capacity

• Adds more technologies– Ground source geothermal– Biomass for residential (but not for heating)

• Committee amendment deletes 5-year sunset– Makes credits permanent

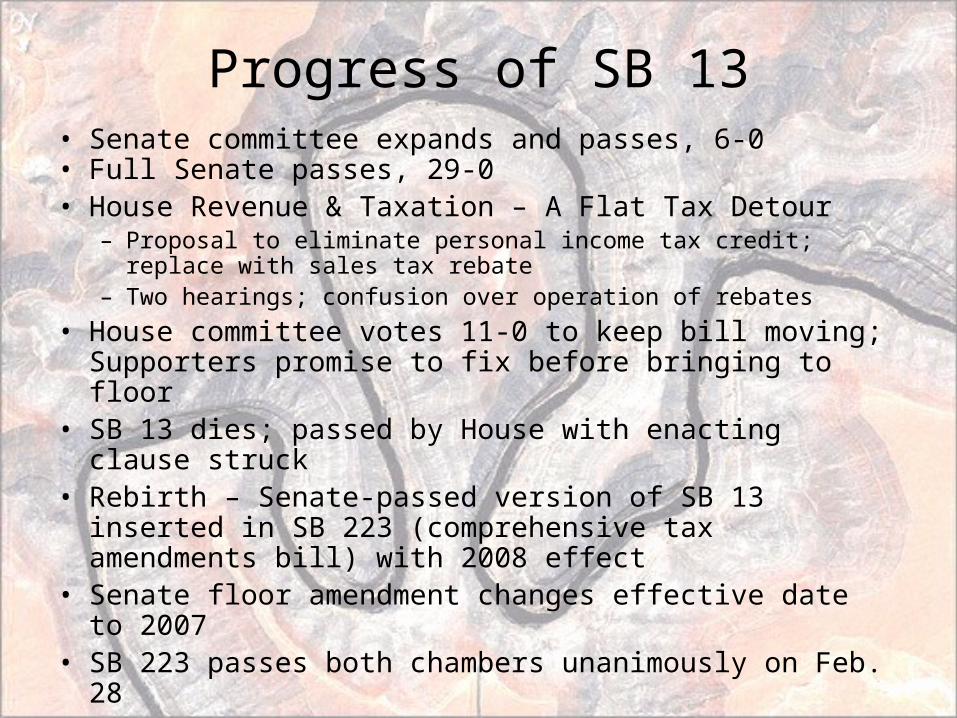

Progress of SB 13• Senate committee expands and passes, 6-0• Full Senate passes, 29-0• House Revenue & Taxation – A Flat Tax Detour

– Proposal to eliminate personal income tax credit; replace with sales tax rebate

– Two hearings; confusion over operation of rebates

• House committee votes 11-0 to keep bill moving; Supporters promise to fix before bringing to floor

• SB 13 dies; passed by House with enacting clause struck

• Rebirth – Senate-passed version of SB 13 inserted in SB 223 (comprehensive tax amendments bill) with 2008 effect

• Senate floor amendment changes effective date to 2007• SB 223 passes both chambers unanimously on Feb. 28

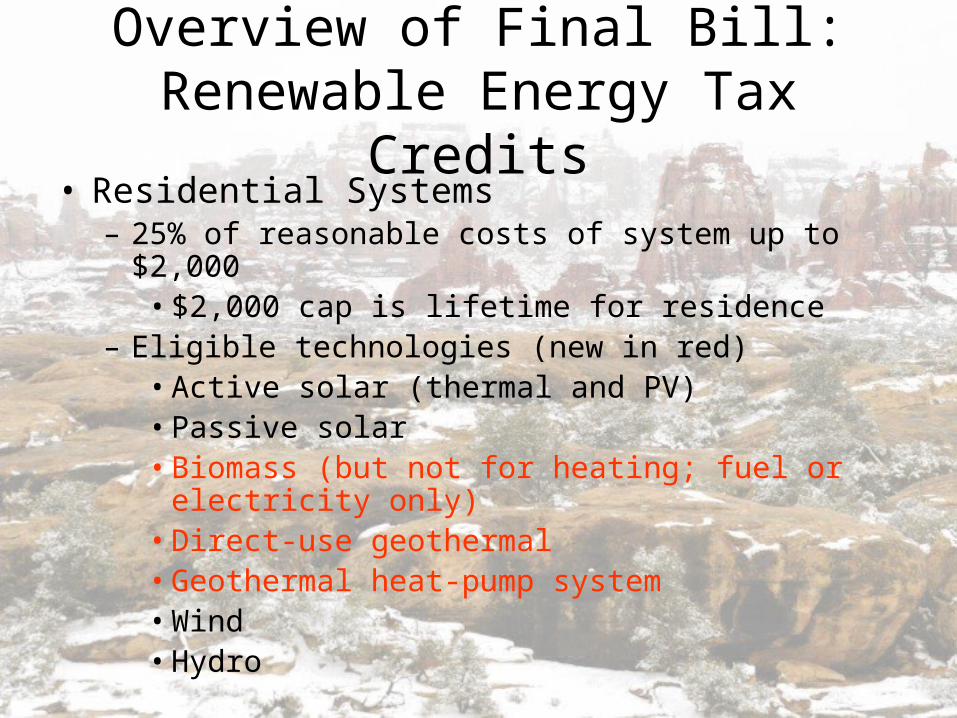

Overview of Final Bill: Renewable Energy Tax Credits

• Residential Systems– 25% of reasonable costs of system up to $2,000

• $2,000 cap is lifetime for residence– Eligible technologies (new in red)

• Active solar (thermal and PV)• Passive solar• Biomass (but not for heating; fuel or electricity

only)• Direct-use geothermal• Geothermal heat-pump system• Wind• Hydro

Overview of Final Bill: Renewable Energy Tax Credits

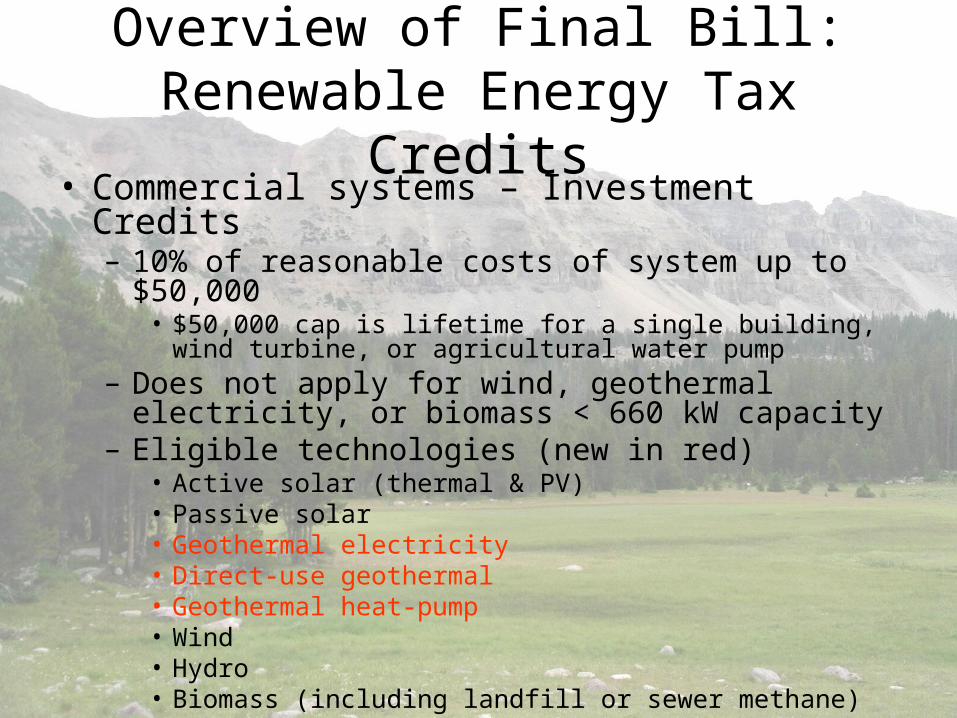

• Commercial systems – Investment Credits– 10% of reasonable costs of system up to $50,000

• $50,000 cap is lifetime for a single building, wind turbine, or agricultural water pump

– Does not apply for wind, geothermal electricity, or biomass < 660 kW capacity

– Eligible technologies (new in red)• Active solar (thermal & PV)• Passive solar • Geothermal electricity• Direct-use geothermal• Geothermal heat-pump• Wind• Hydro• Biomass (including landfill or sewer methane)

Overview of Final Bill: Renewable Energy Tax Credits

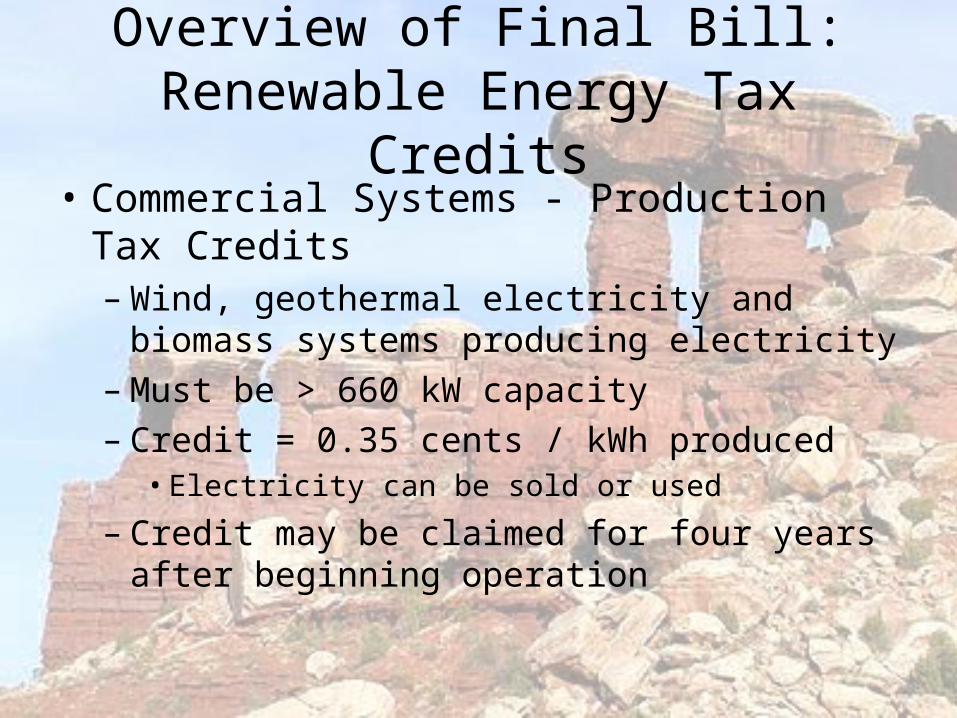

• Commercial Systems - Production Tax Credits– Wind, geothermal electricity and biomass

systems producing electricity– Must be > 660 kW capacity– Credit = 0.35 cents / kWh produced

• Electricity can be sold or used

– Credit may be claimed for four years after beginning operation

Overview of Final Bill: Renewable Energy Tax Credits

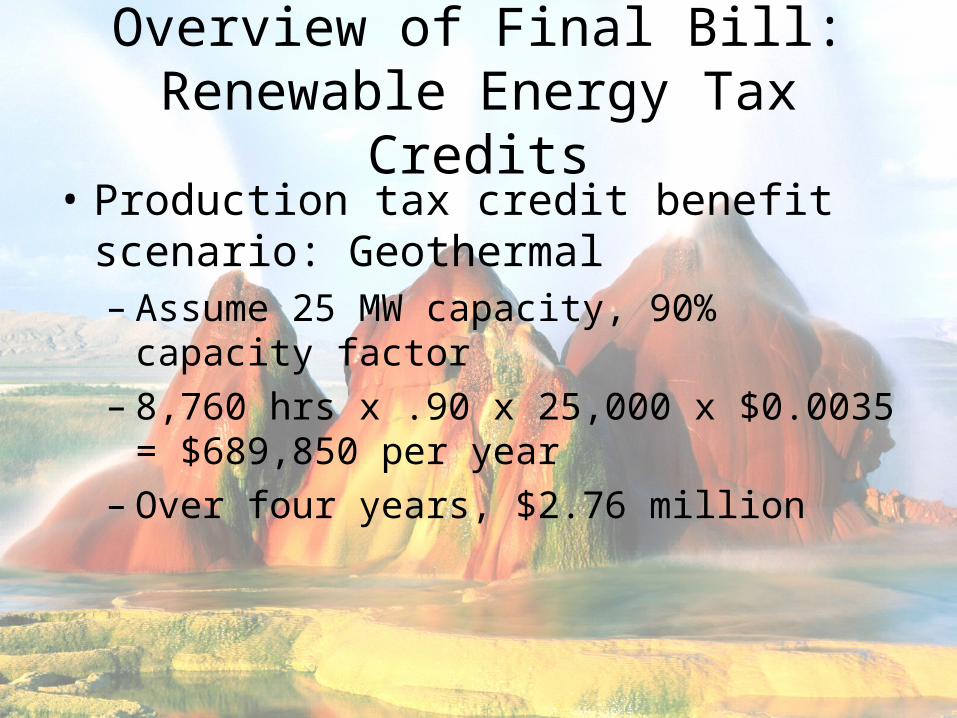

• Production tax credit benefit scenario: Geothermal– Assume 25 MW capacity, 90% capacity factor– 8,760 hrs x .90 x 25,000 x $0.0035 =

$689,850 per year– Over four years, $2.76 million

Overview of Final Bill: Renewable Energy Tax Credits

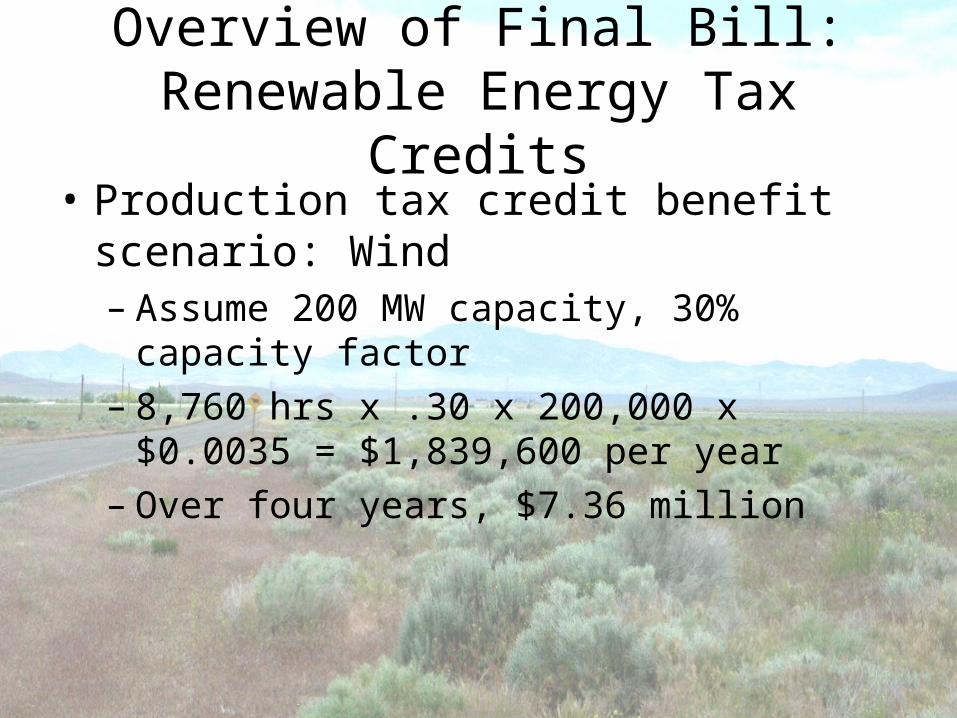

• Production tax credit benefit scenario: Wind– Assume 200 MW capacity, 30% capacity

factor– 8,760 hrs x .30 x 200,000 x $0.0035 =

$1,839,600 per year– Over four years, $7.36 million

Overview of Final Bill: Renewable Energy Tax Credits

• Other final bill features– SEP/UGS to define reasonable cost; may use

capacity based definition– All credits permanently authorized

• No five year sunset• Tax commission to review and report every five

years

– No cap on total amount or cost of credits awarded

– UGS/SEP certifies credit eligibility

Next Steps

• SB 223 awaiting Governor’s signature• UGS will write new rules in next few months

– Defining reasonable costs for systems– Defining eligibility requirements for technologies not

covered by old credits– Rules for claiming production tax credits– Other possible refinements, e.g. installation

requirements, defining eligible equipment, etc.

• Informed public input sought– Look for e-mails announcing