Embed Size (px)

Citation preview

UTICA Summit IV Canton, Ohio

Petrochemicals and More: Sustainable Benefits of Utica Energy

October 11, 2016

Downstream Economics Joe Eddy, President/CEO

Eagle Manufacturing Company

WhygrowthofGas,OilandCoalaresoimportanttoourfuture

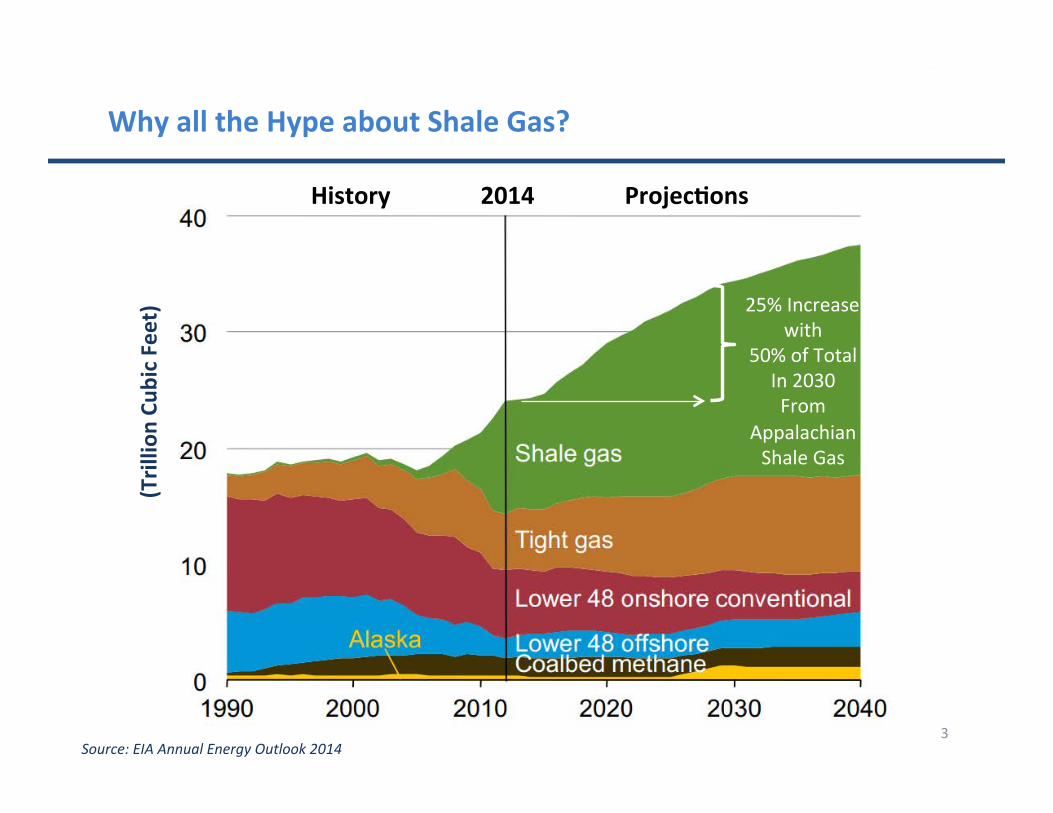

WhyalltheHypeaboutShaleGas?

3Source:EIAAnnualEnergyOutlook2014

(Trillio

nCu

bicFeet)

History2014ProjecHons

25%Increasewith

50%ofTotalIn2030From

AppalachianShaleGas

Marcellus,U@caandDevonianShaleunderlieouren@rearea(sodoothershaleforma@ons!!!!)Devonianat2000to5000’deepMarcellusat5000to7000’deepU@caat8000to9000’deep

AppalachianBasin

MarcellusRegionGasProducHonGrowth

• 2007at1.2BCFD• 2016atover18BCFD• 2020projover20BCFD• NGLnowover450,000Bbl/day• Drilling,FrackingTechniquesImprove• ReservoirDefini@onImproves(oil/gas)

MarcellusShaleIQImproves• AvgProduc@vity/WellIncreasing• 2011at2MMCFD,2016at12MMCFD• LongerLaterals=MoreFracStages• ProlificWellstes@ngover20MMCFD• ReturnonInvestmentImproves(pricing)• InfrastructureBuildoutCon@nues

U.S.EnergyInforma@onAdministra@on|DrillingProduc@vityReport

Ohio’sUHcaRegionGasProducHonGrowth

UHcaShaleIQImproves

• 2012Produc@onat160MMCFD• [email protected]• [email protected]• Drilling,FrackingTechniquesImprove• ReservoirDefini@onImproves(oil/gas)

• AvgProduc@vity/WellIncreasing• 2011at1.0MMCFD,2016at8MMCFD• LongerLaterals=MoreFracStages• ProlificWellsTes@ngover50MMCFD• ReturnonInvestmentImproves

U.S.EnergyInforma@onAdministra@on|DrillingProduc@vityReport

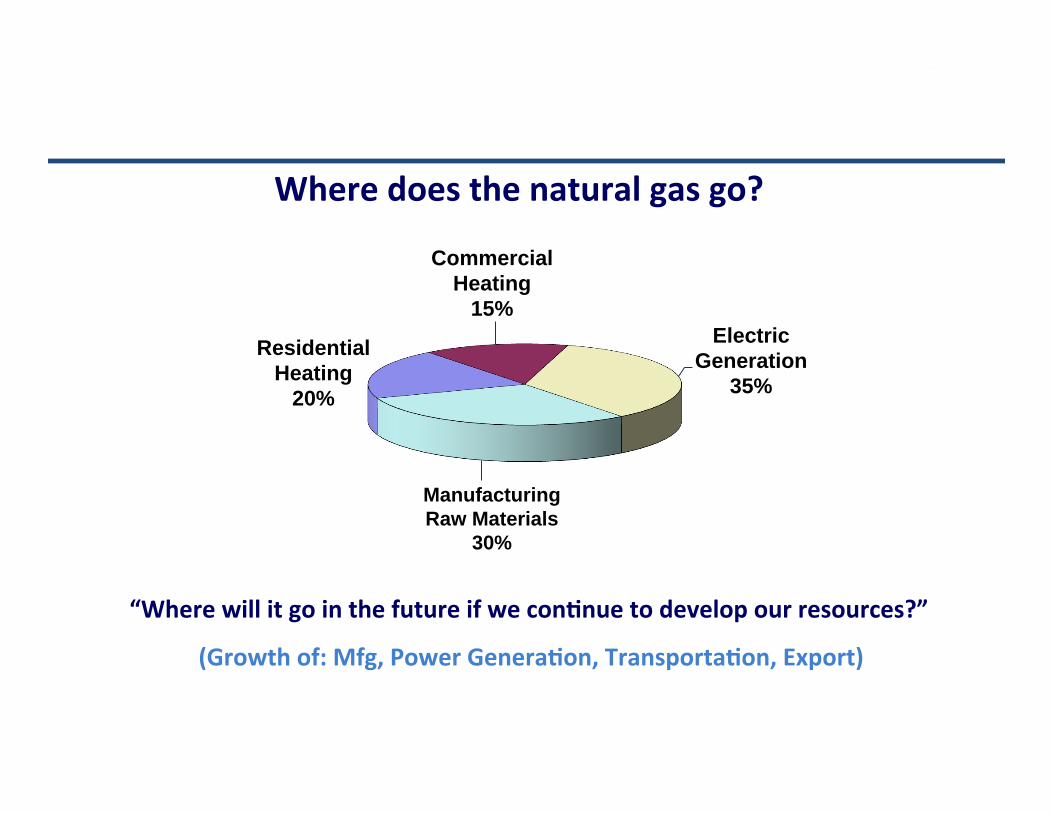

Wheredoesthenaturalgasgo?

Residential Heating

20%

Commercial Heating

15% Electric

Generation 35%

Manufacturing Raw Materials

30%

“WherewillitgointhefutureifweconHnuetodevelopourresources?”

(Growthof:Mfg,PowerGeneraHon,TransportaHon,Export)

Dry Gas

Methane

Consumers or Industry Gas Processing Plant

Wellhead Gas

Wet Gas

NGL Fractionation & Storage

LPG Light Naphtha (pentanes)

Pipeline Distribution System

Ethane NGLs Ethane

Propane Butane Pentane

Cracker

Shale Gas Value Chain – The Downstream Segment

• The Midstream buildout positions the basin for Downsteam Development

The Midstream Segment – Fractionating NGL’s Creating Opportunity for Downstream Expansion

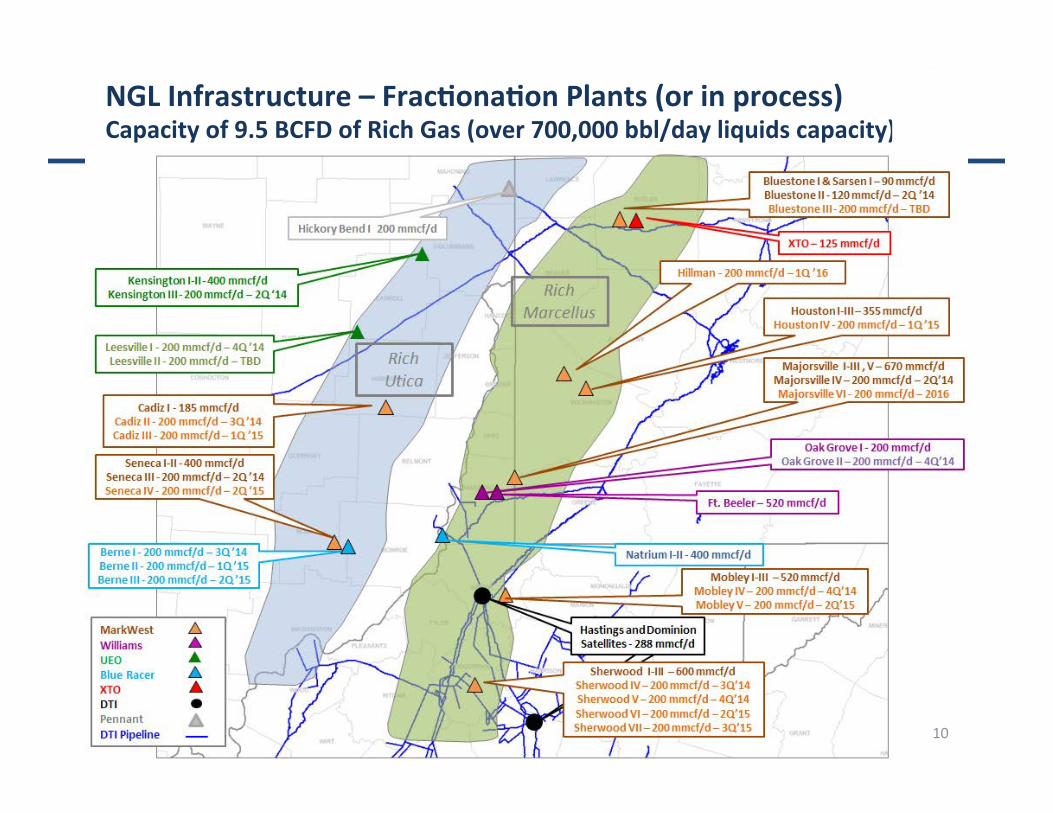

NGLInfrastructure–FracHonaHonPlants(orinprocess)Capacityof9.5BCFDofRichGas(over700,000bbl/dayliquidscapacity)

10

11

EthaneBalance–Only3thingstodowithEthane1.MoveawaybyPipeline(below)2.RejectintoGas(BTU),3.Consumeitlocally–Crackit

12

INEOSInsight–1of8newDragonClassshipsmoving27,000cubicmeterseach(226Mbbl)EthaneFromMarcusHookTerminalto2IneosCrackersinNorwayandSweden(3800miles)(SunocoLogis@csMarinerEastpipeline300milesfromWesternPA,extintoOhio)

13

PTTGlobalChemical

ShellChemical

ProposedAppalachianStorageHubPipelineRoute(methane,ethane,ethylene,propane,propylene,chlorine)

RegionalExtrac6on-Consump6onStrategy

BraskemASCENT

KanawhaValley

Canton

14

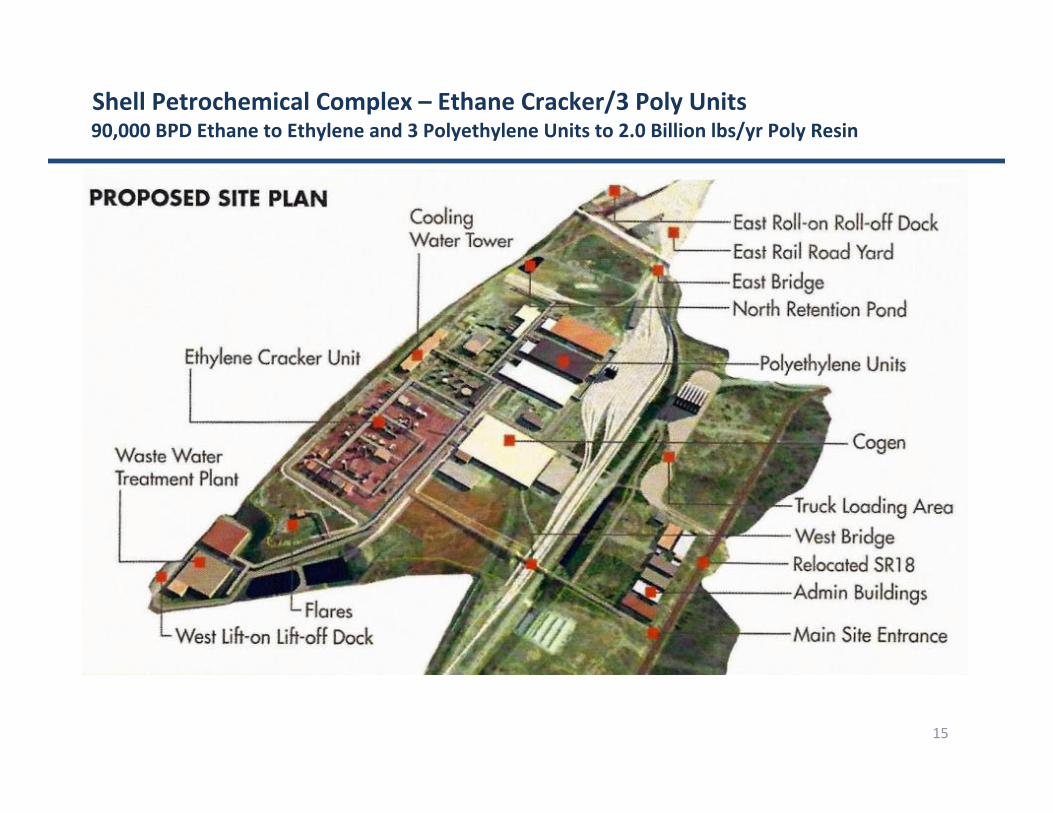

ShellChemicalPetrochemicalComplex–SiteWorkMonaca,PA($7.0BillionInvestment)

15

90,000BPDEthanetoEthyleneand3PolyethyleneUnitsto2.0Billionlbs/yrPolyResinShellPetrochemicalComplex–EthaneCracker/3PolyUnits

Dry Gas

Methane

Consumers or Industry Gas Processing Plant

Wellhead Gas

Wet Gas

NGL Fractionation & Storage

LPG Light Naphtha (pentanes)

Pipeline Distribution System

Ethane NGLs Ethane

Propane Butane Pentane

Cracker

Shale Gas Value Chain – The Downstream Segment

• The real “Value Proposition” keeping the ethane here and cracking it into ethylene

Ethane Cracker Plant (also cracks propane and butane)

Nat

ural

Sha

le G

as

Ethane

Methane

Propane

Butane

Ammonia

Methanol

Ethylene

Propylene

N-Butylene

Isobutylene

Market Sectors

Apparel and Accessories

Beverages and Tobacco Products

Chemicals

Computer and Electronics

Fabricated Metal Products

Food and Kindred Products

Leather and Allied Products

Machinery, Except Electrical

Nonmetalic Mineral Products

Paper

Petroleum and Coal Products

Pharmaceuticals

Plastics and Rubber Products

Primary Metal Manufacturing

Printed Matter and Related Products

Textile and Fabrics

Textile Mill Products

Transportation Equipment

Wood Products

Product Categories

Fertilizers

Adhesives

Alkyd Resins

Solvents

Corrosion Inhibitors

Textiles

Inks, Adhesives

Shampoos, Detergents, Soaps

Paints

Coatings

Pipes, Hoses, Wire Coating

Coolant, Antifreeze

Films, Packaging, Bottles

Paint Remover

Plastics

Tires and Rubber

Lubricant Additives

Solvent, Industrial Cleaners Source: PwC and TopLine Analytics

Shale Gas Value Chain-Downstream

• Ethane, Propane, Butane downstream of cracker • Focus on Ethane to Ethylene to Polyethylene Stream

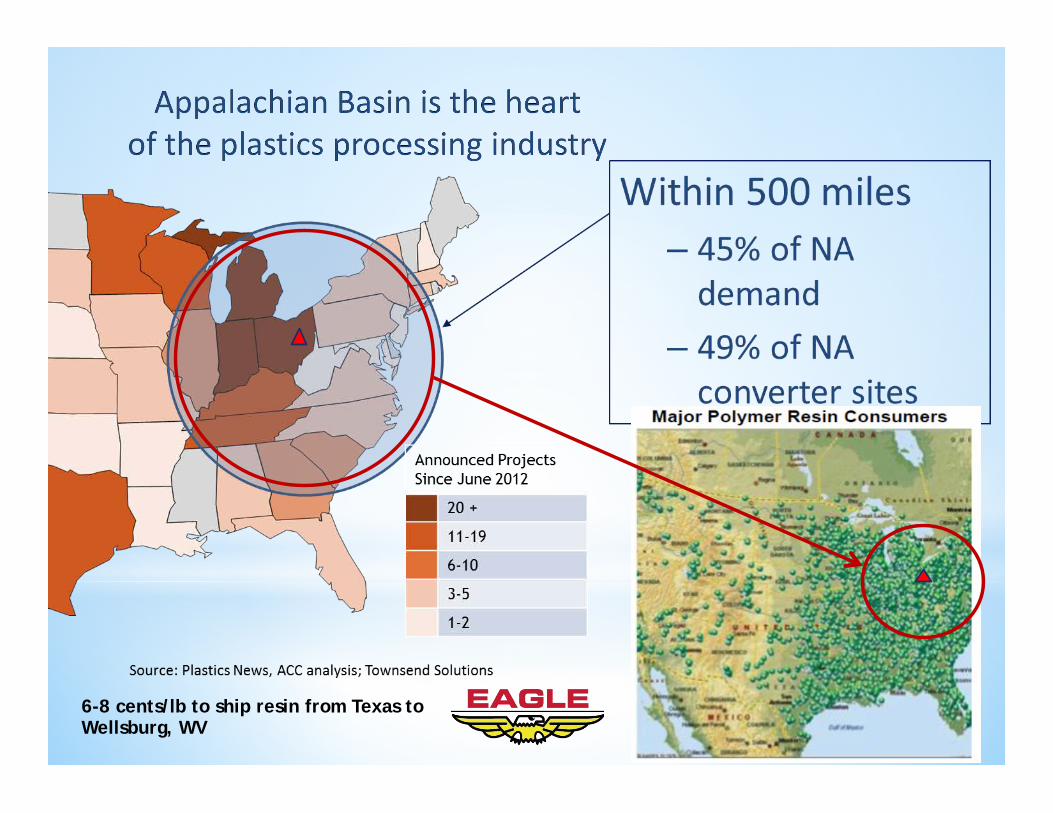

6-8 cents/lb to ship resin from Texas to Wellsburg, WV

Tri-StateShaleSummit• Government

– DOE(NETL)– StateofWestVirginia

October 13, 2015

ProposedEthaneDemand/EthyleneSupply(Crackers)

Canton

100MileRadius 80%

North American HDPE Capacity with announced additions

Source: IHS Chemical

Current NA HDPE Capacity = 20 Billion lb/yr Total HDPE Additions = 7 Billion lb/yr

N/A Poly Resin Capacity Increase by Company (Current N/A PE capacity = 44 B lbs = 20M Mt)

Source: IHS Chemical

Added capacity will support, secure & stabilize plastics processing industry growth

HDPE Pricing vs. Feedstock Pricing

Source: IHS Chemical

Poly Prices remain stable with nat gas, ethane and ethylene remaining low, supporting cracker margins and economics, especially if converting ethylene to polyethylene at same plant (ethane 2010 at $.90/gal, 2016 at <$.15/gal)

Downstream - Plastics Processing Industry

Resin Suppliers

Acetal – Acrylics

ABS – Alkyds Alloys – Blends

--------------------------------

Polyethylene --------------------------------

Barrier Resins Cellulosics

Diallyl Phthalates Engineered Plastics

Epoxies Fluoropolymers

Melamine Nitrile Resins

Nylon/PVC/Urea Silicone/Phenolics

Polycarbonates Polyester/Polystyrene

Polypropylene Polyurethanes

Additive Suppliers

Accelerators Antistats

Antioxidants Blowing Agents

Colorants Conductive

EMI Shielding Filters

Flame Retardants Inhibitors Lubricants Plasticizers Stabilizers

Processors

Custom Captive

Rotational Molding Injection Molding

Blow Molding Structural Foam IM

------------------------------- Blown / Cast Film

Coaters Pultrusion

Thermoforming Calendering

Compression Molding Reaction Molding Transfer Molding

Distributors Compounders Direct Sales

Enduser Market Home Indust Gov Export

Industrial Safety Environmental

Building & Construction Material Handling

Agricultural ------------------------------------------------------------------------------------

Appliances Auto/Transportation Telecommunications

Computers/Electronics/Elect Furniture

Food Processing Recreation/Toys Textiles/Flooring

Recycling

Post Consumer Post Industrial

Distributors Direct Sales

Machinery Suppliers

Extruders

Injection Molding BlowMolding

Compression Presses Transfer Presses

Thermoforming Machines Molds/Dies

Auxillery Equipment Liquid/Solids Dispensing

Plotters Gravimetric Systems

Process Controls Silos/Transfer Systems

A Plastic Processing Model – Eagle Mfg Company ___________________________________________________________

• Current Capacity: 20 million lb/HDPE/Year

• Facility: 800,000sf w/250,000sf dedicated to plastics (in WV)

• Resin Storage: 2 million lbs, plus 2 rail sidings (20 rail cars-4 mil lbs)

• Products: Over 400 Eagle plastic product models

• Employees: 195 w/60 dedicated to plastics production Quick Review: 1. Processing Equipment

2. Poly Products – Eagle & Region 3. Value Chain Example –

One Cracker Supports 100 Eagle Equivalent Operations

Plastics Processing – Eagle Manufacturing Company Extrusion Blow-Molding

Plastics Processing – Eagle Manufacturing Company

Structural Foam Injection Molding

Injection Molding Rotational Molding

Eagle Polyethylene Products

Other Plastic Products made in our area Over 1000 Plastic Processors - 1,000’s of Products

Poly Foam Building, Packing & Insulation Materials

Vinyl Windows, Doors, Siding

Kitchen/Bath Fixtures

Tool & Die Makers

Urethanes

Plastic Pipe Cooling Towers

Bottles, Jars, Caps & Lids Food Containers

Shale Gas Value Chain-Plastics Model Economics Ethane to Ethylene to Polyethylene-vs-Pipeline Out of Region

• Estimated 20:1 value added ratio of downstream economy (jobs, tax base, future economic development)

Pipeline Ethane Pipeline 100,000 BPD = 36.0 Million Bbl/yr 100 Direct/425 Indir Jobs = $27.8 Million/yr Total Value Added: $330 Million/yr

INPUT – OUTPUT: Ethane Ethylene Polyethylene Poly Products

Based upon: 100,000 BPD ethane at $.20/gal, cracker/reactor net output of 2.0 billion lbs/yr polyethylene, plus 20% value for addl products (ethylene, propylene, butylene, butadiene), ethylene at $.40/lb, direct jobs at $65,000/yr, indirect jobs at 4.25x direct at $50,000/yr, polyethylene at $.65/lb, poly product wholesale value of $1.90/lb, Value Added=Material Output Value + Labor Costs, # of processors based on 50 at 24 million lb/yr, TVA=Total Value Added

36 M bbl/yr 2.5 B lb/yr 2.0 B lb/yr 2.0 B lb/yr $302 M/yr ($1.0 B/yr) $1.30 B/yr $3.80 B/yr

Value Added $330M/yr

Cracker Reactors Plastics

Processors

Fractionation

Markets 100+425 Jobs

350+1,575 Jobs 100+425 Jobs 4,000+18,000 Jobs

$1.43 B/yr $4.96 B/yr TVA = $6.39 B/yr

Value Added Ratio: 1.0/1.0 4.33/1.0 15.0/1.0 19.4/1.0

Same Plant

Update: 10/10/16

Material Value Material Volume

Labor Costs $27.8 M/yr $101.5 M/yr $129.3 M/yr $1.16 B/yr

Key Takeaways:

• Marcellus & Utica are most prolific, productive, profitable shales

• At forefront of shale gas development (10% or less)

• Regional Extraction-Consumption Strategy (App Storage Hub) -Lowers Risk for Additional Crackers/Chemical Buildout in the Basin

-Improves National Security-reduces threat from weather or terrorism in Gulf Coast (Mt Belvieu System)

-Creates Regional Supply-Demand based Pricing Hub (improves value across chain)

-Secures, Stabilizes Plastic Industry with local Supply and much reduced Freight Costs

• Value Proposition is in cracking ethane into ethylene regionally

• Local Ethylene and Polyethylene create major downstream mfg expansion

• Realize an estimated 20:1 Value Added Ratio, economic development worth billions

• What to Do? Engage, Embrace, Educate and Endure with the Industry

Cracker Reactors Plastics

Processors

Fractionation

Markets

100+425 Jobs

350+1575 Jobs 100+425 Jobs 4,000+18,000 Jobs

25,000 Industry Jobs $1.4 Billion/Yr Payrolls $6.4 Billion/Yr TVA