Embed Size (px)

Citation preview

1

Vale’s Performance in 1Q17

Ricardo Teles / Agência Vale

Rio de Janeiro, April 27th, 2017

2 Ag

en

da“This presentation may include statements that present Vale's expectations about

future events or results. All statements, when based upon expectations about the

future and not on historical facts, involve various risks and uncertainties. Vale

cannot guarantee that such statements will prove correct. These risks and

uncertainties include factors related to the following: (a) the countries where we

operate, especially Brazil and Canada; (b) the global economy; (c) the capital

markets; (d) the mining and metals prices and their dependence on global

industrial production, which is cyclical by nature; and (e) global competition in the

markets in which Vale operates. To obtain further information on factors that may

lead to results different from those forecast by Vale, please consult the reports

Vale files with the U.S. Securities and Exchange Commission (SEC), the

Brazilian Comissão de Valores Mobiliários (CVM), the French Autorité des

Marchés Financiers (AMF) and in particular the factors discussed under

“Forward-Looking Statements” and “Risk Factors” in Vale’s annual report on Form

20-F.”

“Cautionary Note to U.S. Investors - The SEC permits mining companies, in their

filings with the SEC, to disclose only those mineral deposits that a company can

economically and legally extract or produce. We present certain information in

this presentation, including ‘measured resources,’ ‘indicated resources,’ ‘inferred

resources,’ ‘geologic resources’, which would not be permitted in an SEC filing.

These materials are not proven or probable reserves, as defined by the SEC, and

we cannot assure you that these materials will be converted into proven or

probable reserves, as defined by the SEC. U.S. Investors should consider closely

the disclosure in our Annual Report on Form 20-K, which may be obtained from

us, from our website or at http://http://us.sec.gov/edgar.shtml.” Dis

clai

mer

3 Ag

en

da

1. Vale’s performance in 1Q17

2. Capital expenditures

3. Capital structure

4. Business segment performance

Agen

da

4

Vale’s performance in

1Q17

5

Fe Pellets Ni Cu Coal

Record production performance in iron ore

and coal

Production highlights 1Q17

Total: 86.2 Mt

Carajás: 36.0 Mt

Total: 12.4 Mt Total: 71.4 kt

VNC: 10.2 kt

Total: 109.0 kt

Salobo: 42.6 kt

Mozambique: 2.4 Mt

&

%

Quarterly record%

&

% &

5

Record for a first quarter&

6

45%

14%

18%

10%

7%

3%4%

China Other AsiaEurope BrazilNorth America Middle EastRest of the World

Seasonally lower sales volumes led to lower

q-o-q revenues

Highlights 1Q17

Net operating revenues of US$ 8.515

billion

Revenues were 8.1% lower vs. 4Q16

mainly due to seasonally lower sales

volumes of Ferrous Minerals

59% sales to Asia and 10% domestic

sales

Ferrous Minerals accounted for 76%

of revenues

Base Metals accounted for 19% of

revenues

Net operating revenues by destination

in 1Q17

6

7

5.632

5.115

0.703

0.213

0.121 0.148

4Q16 Sales volumes

Higher costs

FX Expenses 1Q17

Lower costs achieved driven by lower sales

despite exchange rate and inflation

Highlights

Total costs and expenses decreased

by US$ 517 million

COGS was impacted by higher price-

related cost factors such as the

leasing of pellet plants, royalties, feed

purchased from third-parties and higher

bunker oil prices

Higher costs were partially offset by

lower expenses

Costs and expenses 1Q17 vs. 4Q16

US$ billion

7

8

1.935

4.7224.308

1Q16 4Q16 1Q17

EBITDA impacted by seasonally lower

volumes and higher prices

Highlights 1Q17

Overall EBITDA increased 123% vs.

1Q16; and decreased 9% vs. 4Q16

EBITDA decreased driven by seasonally

lower sales volumes (US$ 828 million)

partially offset by higher prices (US$ 672

million)

Iron ore sales volumes were planned to

take into account the build-up of

inventory due to blending activities

EBITDA, q-o-q

123%

US$ billion

8

9

Capital expenditures

10

Steady reduction of investments

Highlights 1Q17

Total capex was US$ 1.113 billion in 1Q17,

decreasing US$ 210 million vs. 4Q16

Ferrous Minerals and Base Metals business

segments represented 57% and 38% of

sustaining capex

Base Metals sustaining will be higher in

2017 due to the transition to a single furnace

operation in Sudbury and the Air Emission

Reduction project

Project and sustaining capex

US$ million

913

588 587

497735

526

1Q16 4Q16 1Q17

Growth projects Sustaining

1,323

1,113

10

1,410

11

4.2 4.03.7

2017E 2018E 2019E

Vale’s capex guidance excluding

investments in Fertilizers segment

US$ billion

Note: BRL/USD exchange rate of BRL/USD 3.37 from 2017 onwards

11

12

S11D continued its successful ramp-up,

advancing according to plan

Highlights

88% of combined physical

progress in 1Q17 with 98%

progress at the mine site and

80% at the logistic

infrastructure sites

The duplication of the

railway reached 66%

physical progress with 367

km duplicated

Onshore expansion reached

89% physical progress

12

S11D Mine – In operation

13

Capital structure

14

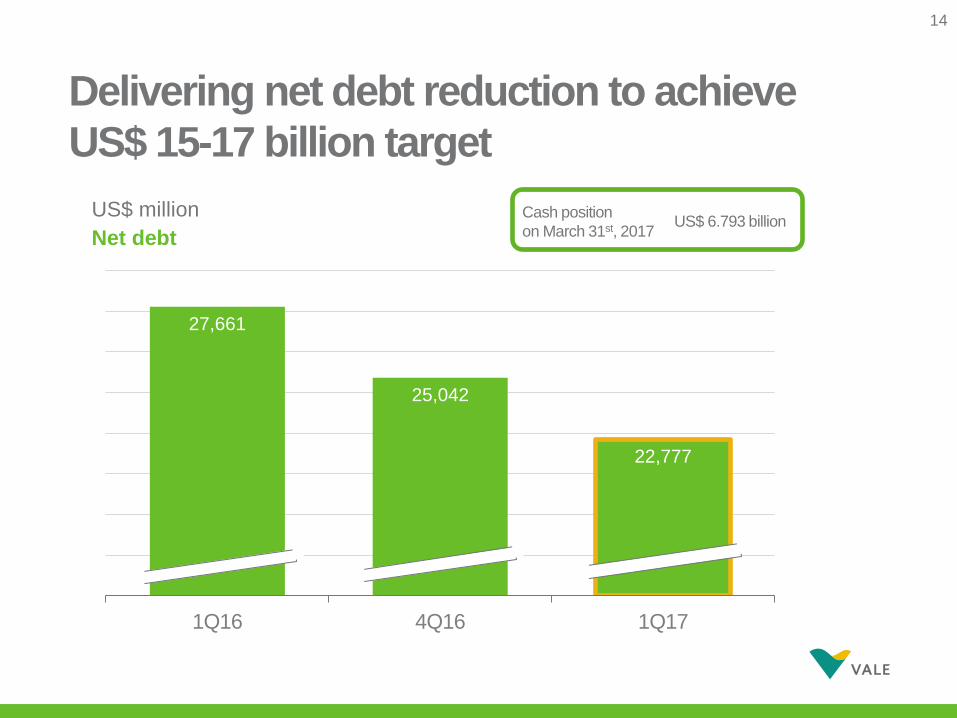

27,661

25,042

22,777

1Q16 4Q16 1Q17

US$ 6.793 billion

Delivering net debt reduction to achieve

US$ 15-17 billion target

14

Net debt

Cash position

on March 31st, 2017

US$ million

15

4.03.8

3.0

2.1

1.6

1Q16 2Q16 3Q16 4Q16 1Q17

A significant improvement in Net Debt /

EBITDA ratio

Net debt / LTM1 EBITDA Ratio

1 LTM – last twelve months, excluding non-recurring items.

Net debt in

1Q17:

US$ 22.777

billion

Cash position in

1Q17:

US$ 6.793 billion

Average maturity:

8.0 years

Average cost of

debt:

4.71% per annum

15

16

0.83.1 3.5 3.9

17.6

28.9

2017 2018 2019 2020 2021onwards

Gross debt

Cash balance will be used to implement a liability

management program to reduce Gross Debt in 2017

Gross debt amortization schedule1

1 As of March 31st, 2017. Does not include accrued charges.

US$ billion

61% of our debt settlement will occur

after 2020

16

31,470

29,322 29,570

1Q16 4Q16 1Q17

Gross debt

US$ million

17

We concluded the equity transaction with

Mitsui in March 2017

1 Very Large Ore Carriers2 Total value of transaction is US$ 2.5 billion with US$ 1.25 billion in cash and the remainder in Mosaic’s shares; the deal was announced in December 2016

and is expected to be completed late 2017 as conditions precedent are fulfilled

17

US$ billion

Reference

US$ 1 billion

10 VLOCs¹

El Hatillo

Araucária

Ferroalloys in

Europe

Oil and gasconcessions

CADAM

2011-2012

US$ 2.6 billion

GoldstreamI

VLI

Log-In

Fosbrasil

Tres Valles

Norsk

Hydro

2013

US$ 6.0 billion

Goldstream II

Belo Monte stake

2015

US$ 3.0 billion

8 VLOCs¹

MBR preferredshares

2016

US$ 1.3 billion

Goldstream III

3 VLOCs1

Fertilizers2

Paragominas

Capesizes

2017

US$ 3.2 billion

Global

Coal –

Mitsui

Equity

Aluminumassets

18

Business segment

performance

19

Ferrous Minerals EBITDA was practically in line with

4Q16, despite seasonally lower sales volumes

4,109 3,967

584

84 51

774

138

5 75 115

EBITDA 4Q16

Price FX Bunker Volume Commercial initiatives

CFR Freight Sales

Unit costs Others EBITDA 1Q17

US$ million, 4Q16 vs. 1Q17

US$ 183M

19

201 Ex-ROM

1Q17 cash break-even cost landed in China

for iron ore and pellets

14.7

14.2

2.6

0.6 2.9

2.4

32.6

2.1

30.5

3.8 34.4

C1 cash cost¹ Freight Royalties & expenses

Distribution Moisture Quality EBITDA breakeven

iron ore fines

Pellet adjustment

EBITDA breakeven (pellets &

fines)

Sustaining Iron ore & pellets cash breakeven

Cost landed in China

US$/t, 1Q17

20

21

Cash cost1 in BRL remained at low levels

despite inflationary pressures

54.6

50.0

46.9 46.347.5

46.1

42.2

44.846.1

0.73.0

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

1 2015 figures were adjusted to the new allocation criteria, as reported in the 4Q15, and include acquisition costs of third party purchased ore

-15.6%

R$/tNon-recurring costs

21

-2.9%

22

Price realization continued to improve in

1Q17

85.6 86.7

75.8

1.9

0.5

4.1 2.1 0.1

3.2

4.1

6.8

AveragePlatts

1Q17 (dmt)

Quality Premium / discount and commercial conditions

Provisionalprices in

prior quarter¹

Laggedprices

Current Provisionalprices

in currentquarter²

CFR reference price (dmt)

Adjustmentfor

FOB sales

Moisture Vale CFR/FOB price

(wmt)³

Impact of pricing system adjustments

1 Adjustment as a result of provisional prices booked in 4Q16 at US$ 74.6/t.2 Difference between the weighted average of the prices provisionally set at the end of 1Q17 at US$ 77.9/t based on forward curves and US$ 85.6/t from the 1Q17 IODEX.3 Vale price is net of taxes.

US$/t, 1Q17

+ 1.1 US$/t

22

23

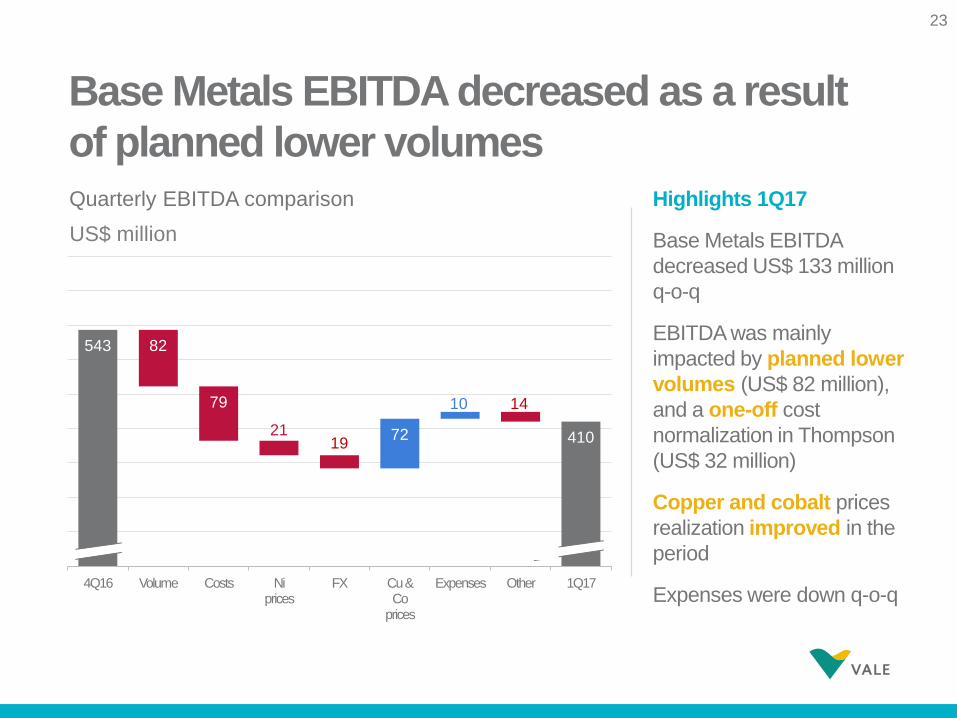

543

410

82

79

2119

72

10 14

4Q16 Volume Costs Ni prices

FX Cu & Co

prices

Expenses Other 1Q17

Base Metals EBITDA decreased as a result

of planned lower volumesHighlights 1Q17

Base Metals EBITDA

decreased US$ 133 million

q-o-q

EBITDA was mainly

impacted by planned lower

volumes (US$ 82 million),

and a one-off cost

normalization in Thompson

(US$ 32 million)

Copper and cobalt prices

realization improved in the

period

Expenses were down q-o-q

Quarterly EBITDA comparison

US$ million

23

24

Coal production cost per ton through Nacala

decreased driven by the quarterly production record

24

900

1,585

2,434

1Q16 4Q16 1Q17

Moatize coal production

000’ t

168.0

97.883.9

1Q16 4Q16 1Q17

Moatize production cost through Nacala

US$/t

25

Additional

information

26

Non-recurring costs

Evolution of iron ore fines cash cost, freight

and expenses

12.313.5

14.7

0.9

1Q16 4Q16 1Q17

C1 Cash Cost FOB Port1 Freight

US$/t

11.3

13.214.2

1Q16 4Q16 1Q17

Expenses2 & Royalties

4.0

3.5

2.5

1.3

1Q16 4Q16 1Q17

1 Ex-ROM and ex-royalties; all figures as per new managerial allocation changes, as reported in 4Q15, and include acquisition costs of third party

purchased ore.2 Net of depreciation.3 Positive one-off impact of insurance recoveries of US$ 85 million in 1Q17.

+20.5% +25.7% -5.0%

26

Positive one-off impact3

27

Iron ore pricing systems

Provisional - prior quarter Lagged

Current Provisional - current quarter

4.84.1

4Q16 1Q17-1.3

-2.1

4Q16 1Q17

1.0

-0.1

4Q16 1Q17

1.7

-3.2

4Q16 1Q17

Pricing system breakdown Impact of pricing mechanisms

US$/t

27

10% 10%

45% 49%

45% 41%

4Q16 1Q17

Lagged

Current

Provisional

28

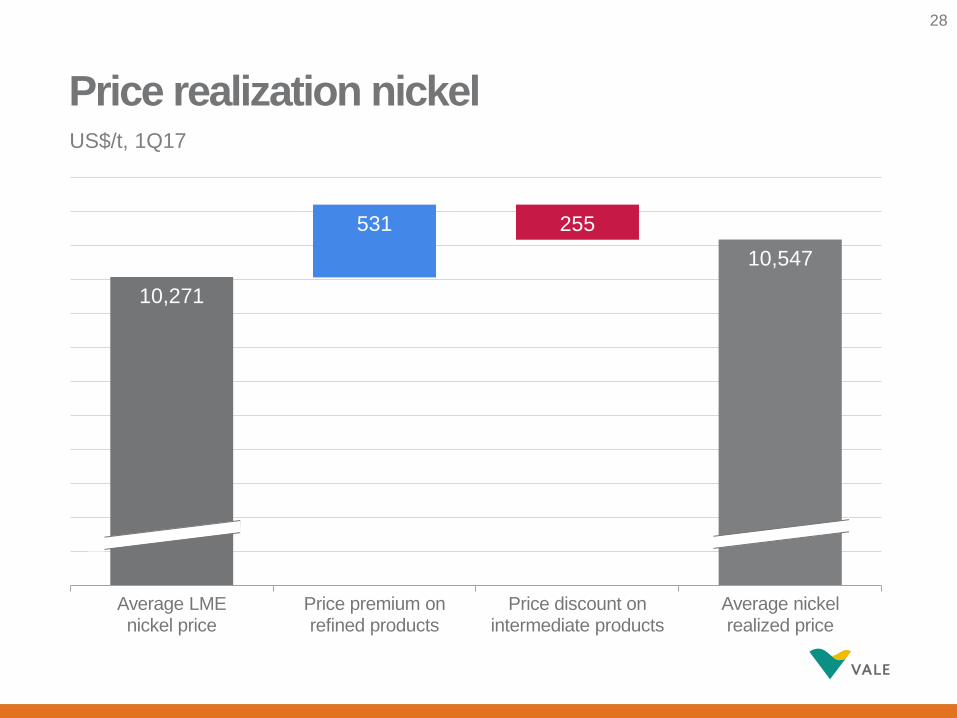

Price realization nickel

10,271

10,547

531 255

Average LME nickel price

Price premium on refined products

Price discount on intermediate products

Average nickel realized price

28

US$/t, 1Q17

29

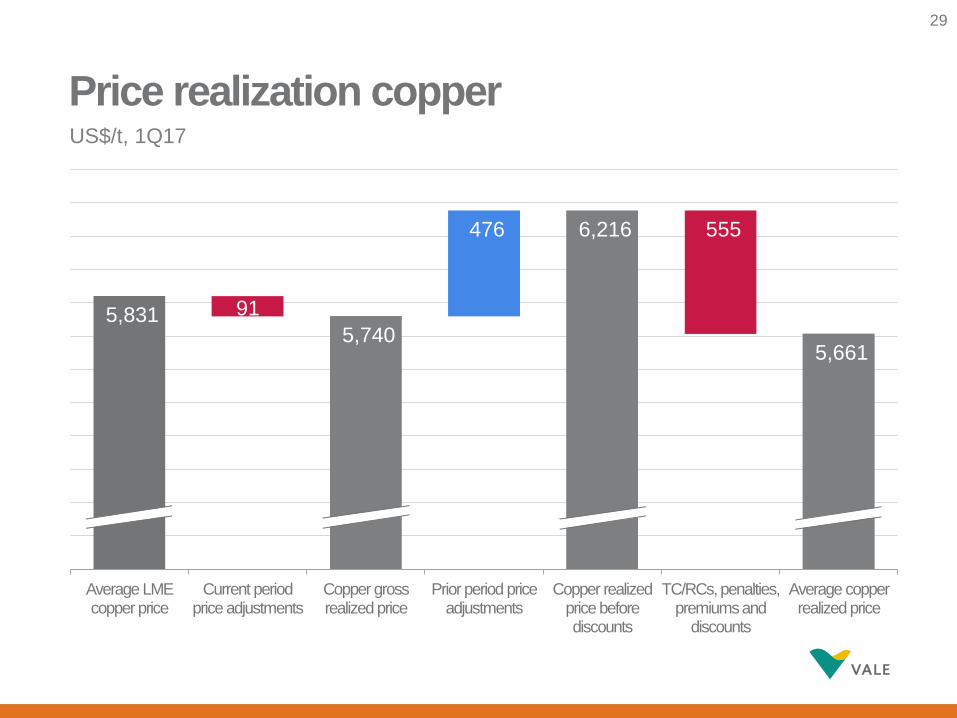

Price realization copper

5,831 5,740

6,216

5,661

91

476 555

Average LME copper price

Current period price adjustments

Copper gross realized price

Prior period price adjustments

Copper realized price before discounts

TC/RCs, penalties, premiums and

discounts

Average copper realized price

US$/t, 1Q17

29

30

Unit cost of sales per operation, net of by-

product credits1

Operation (US$ / t) 1Q17 4Q164 1Q164

North Atlantic Operations2 (nickel) 6,699 5,125 4,008

PTVI2 (nickel) 6,821 5,770 6,636

VNC3 (nickel) 11,232 11,375 13,691

Onça Puma (nickel) 9,341 9,204 8,064

Sossego (copper) 2,941 3,207 2,692

Salobo (copper) 1,406 589 923

1 North Atlantic figures includes Clydach and Acton refining costs.2 Prior periods restated to include royalties, freight and other period costs.3 Unit cash cost restated for periods prior to 1Q17 to exclude pre-operating and other operating expenses.4 We realigned our unit cash cost of sales methodology in 1Q17 to include all freight, royalty and other costs reported as cost of goods sold and to exclude other

operating expenses and pre-operating expenses for certain operations. Considering the previous criteria, the unit cash cost figures in prior periods would be: North

Atlantic, US$ 3,412/t and US$ 3,218/t in 4Q16 and 1Q16, respectively; PTVI, US$ 5,695/t and US$ 5,806/t in 4Q16 and 1Q16, respectively; VNC, US$ 11,017/t

and US$ 12,711/t in 4Q16 and 1Q16, respectively.

30

31

Price realization – metallurgical coal from

Mozambique

168.2 165.2 165.2

8.1 0.9 9.1

4.2 0.6

7.9

Averagereference price

1Q17

Quality Current Lagged price index

Lagged pricequarterly

benchmark

Freightdifferential

Others Valeprice

US$/t, 1Q17

31

Impact of pricing system adjustments

32

Price realization – thermal coal from

Mozambique

82.4

68.2

14.0

1.0 0.9 0.1 2.0

Averagereference price

1Q17

Quality Current Lagged price index

Freight margin Others Vale price

US$/t, 1Q17

32

Impact of pricing system

adjustments

33

73%

21%

5%

USD Hedge to USD BRL Others

73%

23%

3%

USD BRL EUR Others

Debt position breakdown by currency

Debt position breakdown by currency

(before hedge)

Debt position breakdown by currency

(after hedge)

33

34