Embed Size (px)

Citation preview

1

1

Valuation of Stocks andCompany Valuation

Capital Budgeting and CorporateObjectives

Professor Ron Kaniel

Simon School of Business

University of Rocheser

2

Overview

Introduction» Stocks and stock markets

» Transactions & Orders

Valuation:» Present Value

» Dividend growth models

Financial ratios» Dividend yields

» P/E multiples

2

3

Common Stock

What does it mean to own common stock?» ownership» residual claimants.

What rights do common shareholders have?» vote at company meetings» dividends» sell their shares

What are the benefits of stock ownership?» dividends» capital gains

Why do firms issue stock?» to finance investments» to acquire other companies» to repurchase debt

4

Preferred Stock: Debt or Equity?

What does it mean to own preferred stock?» ownership

» senior to equity, junior to debt securities in case of default

What rights do preferred shareholders have?» usually no voting rights, except in case of default on dividend

» dividends and other distributions

What are the benefits of preferred stock ownership?» periodic dividend rate, typically cumulative

» capital gains

Why do firms issue preferred stock?» often because of the favorable tax treatment when held by other

firms

3

5

Transactions Involving Stocks

Buy (Long Position) Savings motive Speculative

Sell Liquidity needs Expect stock to decline in value

Short Sell Sell stock without first owning it. Borrow stock from your broker with the promise to return it at some

later date. Sell the borrowed stock. Repurchase it at a later date to return it to your broker. Responsible for all dividends and other distributions while short the

stock.

6

Short selling (in detail)Why Short Sell?

Short Selling is one way of benefiting from a stock that is expected to decline in price.

» Instead of buying today and selling later, the short seller sells today and buys later.

How to Short Sell?

The short-seller (A) finds an existing owner of the shares (B) who is willing and able to lend the shares to A. Once A has negotiated a loan, A can then sell the borrowed shares to any willing buyer (C).

A posts collateral with B. In the US, the standard collateral is cash amounting to 102 per cent of the value of the shares, to be adjusted daily as their value fluctuates.

» Note though that under Federal Reserve Regulation T, in case where B is a U.S. broker/dealer A has to post an additional 50% margin (any long securities can be pledged to satisfy this requirement). Further, broker-dealers may institute higher short sale margin requirements than those imposed by self-regulatory organization rules. e.g., the NASD Rule 2520(d) and NYSE Rule 431(d).

4

7

Short selling (in detail)

A pays B a fee. The fee can be determined by the “rebate” rate, which is the interest that B pays A for use of the cash collateral. For example, if the market rate for cash funds were 5% and the stock loan fee were 1.5% then B would rebate A only 3.5%. (Note that is it possible to have fees that exceed the cash rate, which would result in negative rebate rates).

A pays B any dividends/distributions made to the owners of the shares during the loan.

B has the right to recall the shares from A at any time. Loans are “open” and effectively rolled over each night until either B wants the shares returned or A voluntarily returns them. Given notice of recall, A has three days to return the shares. After this, A can try borrowing the shares from another lender or can “cover” the short position by purchasing the shares.

8

Short selling (in detail)Who are the Participants? The role of B (the lenders) is largely assumed by the big custody banks in the U.S. who act

as intermediaries for large institutional owners like pension funds, mutual funds etc.

Loans of shares can also be made by a broker from his own inventory, from the margin account of another customer, or shares borrowed from another broker. These shares are used to make settlement with the buying broker within three days of the short sale transaction, and the proceeds are used to secure the loan.

Another group that assume the role of B (lenders) consists of the broker-dealers (e.g. Goldman Sachs, Morgan Stanley). These broker-dealers lend from their internal supply of securities held by their market makers and proprietary trading desks, the accounts of institutional customers, and the margin accounts of individual investors.

» Note that Section 8 of the Exchange Act of 1934 prohibits brokers from lending shares held in retail cash or non-margin accounts.

The role of A (the short-sellers) is assumed by a broader group. More obvious examples include:

» Specialists and market makers (for balancing buy orders with sell orders)» Traders of equity options, index futures, equity return swaps and convertible bonds (for

hedging their positions)» Hedge Funds (to execute “arbitrage” strategies)» Speculators

5

9

Short selling (in detail)

The NASDAQ reported that short interest (the number of shares that have already been sold short) around 4.35% days of average daily total share volume at July 2019.

Shorting is subject to many restrictions on the size, price, and types of stocks able to be shorted. For example, you cannot short sell penny stocks (they are non-marginable due to Regulation T) and most short sales need to be done in round lots.

Equity loans can occur for reasons other than short selling. For instance in cases where A borrows from B but then doesn’t short to C, A is treated as the legal owner of the shares and is therefore entitled to the dividends distributed during the course of the loan (which, as previously mentioned, are required to be reimbursed by A to B). This might happen in cases where A values the distribution received more than the reimbursements given (for taxation reasons, for example)

In lending, B forfeits voting rights to A (to C in the case of the short sale). Alternative Uptick Rule: provides that a circuit breaker is triggered with respect

to a stock if the stock’s price declines by 10% or more from prior day’s closing price. At that point short selling is permitted only if its price is above the current national best bid. Once triggered, the circuit breaker remains in effect with respect to the stock for the remainder of the day and the following day.

10

Types of Orders

Market Orders» Buy or sell at the current market price

Limit Order» Buy or sell at a specified price

» Limit by time period

Stop Orders» Stop-loss: Sell if price falls below certain level

» Stop-buy: Buy if price rises above certain level

– Used in conjunction with short selling

6

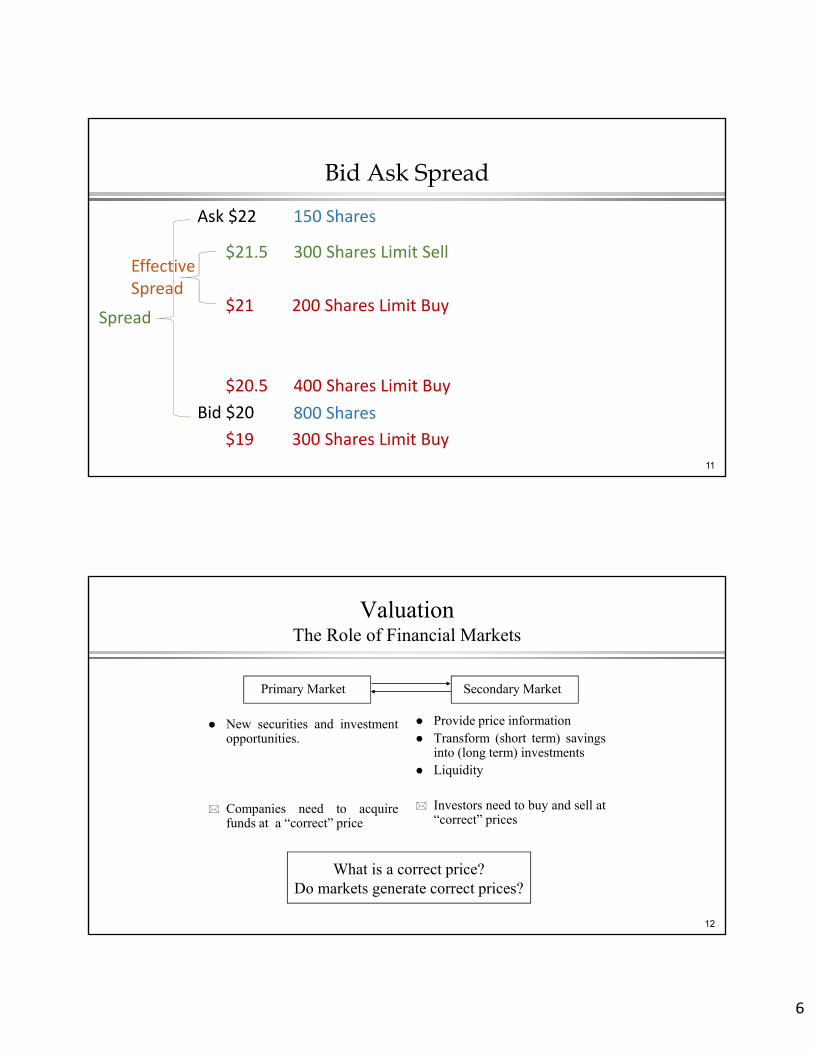

11

Bid Ask Spread

$21.5 300 Shares Limit Sell

$21 200 Shares Limit Buy

$20.5 400 Shares Limit Buy

$19 300 Shares Limit Buy

Ask $22

Bid $20

Spread

EffectiveSpread

150 Shares

800 Shares

12

ValuationThe Role of Financial Markets

Primary Market

New securities and investmentopportunities.

Companies need to acquirefunds at a “correct” price

Secondary Market

Provide price information Transform (short term) savings

into (long term) investments Liquidity

Investors need to buy and sell at“correct” prices

What is a correct price?Do markets generate correct prices?

7

13

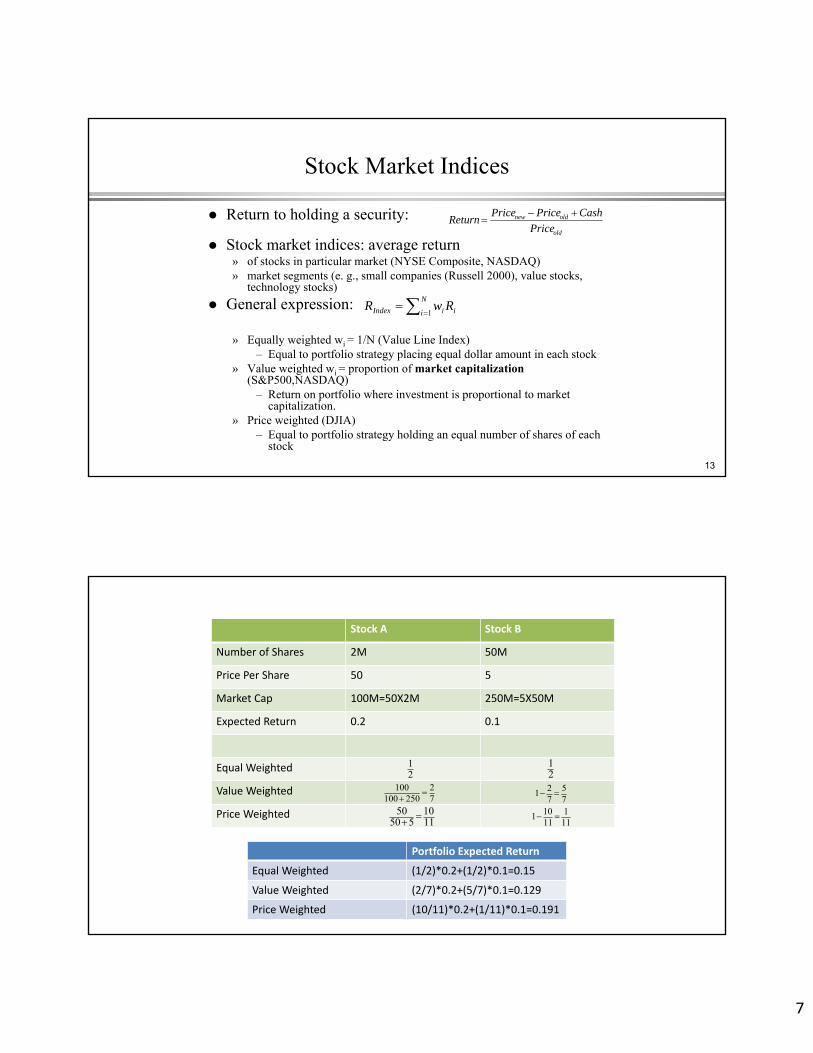

Stock Market Indices

Return to holding a security:

Stock market indices: average return» of stocks in particular market (NYSE Composite, NASDAQ)» market segments (e. g., small companies (Russell 2000), value stocks,

technology stocks)

General expression:

» Equally weighted wi = 1/N (Value Line Index)– Equal to portfolio strategy placing equal dollar amount in each stock

» Value weighted wi = proportion of market capitalization (S&P500,NASDAQ)

– Return on portfolio where investment is proportional to market capitalization.

» Price weighted (DJIA)– Equal to portfolio strategy holding an equal number of shares of each

stock

N

i iiIndex RwR1

old

oldnew

Price

CashPricePriceReturn

Stock A Stock B

Number of Shares 2M 50M

Price Per Share 50 5

Market Cap 100M=50X2M 250M=5X50M

Expected Return 0.2 0.1

Equal Weighted

Value Weighted

Price Weighted

12

12

100 2100 250 7

2 517 7

50 1050 5 11

10 1111 11

Portfolio Expected Return

Equal Weighted (1/2)*0.2+(1/2)*0.1=0.15

Value Weighted (2/7)*0.2+(5/7)*0.1=0.129

Price Weighted (10/11)*0.2+(1/11)*0.1=0.191

8

1515

U. S. Stock Markets

Major U. S. Stock Exchanges New York Stock Exchange (NYSE) American Stock Exchange (AMEX) Over-The-Counter (OTC)

» National Association of Securities Dealers (NASDAQ)U. S. Stock Market:

Stock Index 7/15/2019 7/25/2018 8/28/2017 7/25/16 9/17/2015 2/19/14 2/26/12 4/28/09

Dow Jones Industria 27,334 25,188 21,865 18,571 16,675 16,102 13,900 8,017NASDAQ 8,245 7,884 6,302 5,100 4,894 4,252 3,130 1,674S&P500 3,014 2,827 2,446 2,175 1,990 1,836 1,497 855NYSE Composite* 13,235 12,856 11,792 10,805 10,215 10,296 8,766 5,370Russell 2000 1,580 1,682 1,302 1,213 1,180 1,156 900 473

*The NYSE Composite index was recalculated to reflect a base value of 5,000 as of Dec/31, 2002

Stock Indexes

9

17

Shareholders require a rate of return re for buying a share. They buy for

P0 and sell after one year for P1 and receive dividends D1:

The next buyer also sells after one year:

The same holds for P2. Continuing gives:

Share price = PV of dividends

Why “short-termists” are “long-termists”

PD P

re0

1 1

1

P

D Pr

PD

rD P

re e e1

2 20

1 2 221 1 1

...

111 33

221

0

eee r

D

r

D

r

DP

18

Stock Valuation

Stock Price = PV of future dividends» The price an investor is willing to pay for a share of stock depends upon:

– Magnitude and timing of expected future dividends.

– Risk of the stock.

» The stock’s discount rate, re, is the rate of return investors can expect to earn on securities with similar risk.

» Where are capital gains?

10

19

Another Application:Estimating the required return on equity

Holders of stock receive returns in two forms:» Dividend payouts

» Capital gains (stock price appreciation P1-P0)

– typically larger fraction of returns

» Capital gain reflects growth in future dividend payments

Note:» The expected rate of return is not equal to the dividend yield

» The expression is in terms of the prospective yield, not the historic yield

rDP

P PPe 1

0

1 0

0

20

Assumption: Dividends grow at a constant rate g forever:

Then:

Issues:

» constant growth

The “Constant Growth” Formula

D D g D D g D g D gt tt t

2 1 1 11

01 1 1 1 ( ) ( ) ... ( ) ( ),

rategrowth -return Expected

Shareper Dividend eProspectivPrice Share

...1

1...

)1(

)1(

11

11

211

0

gr

D

r

gD

r

gD

r

DP

et

e

t

ee

11

21

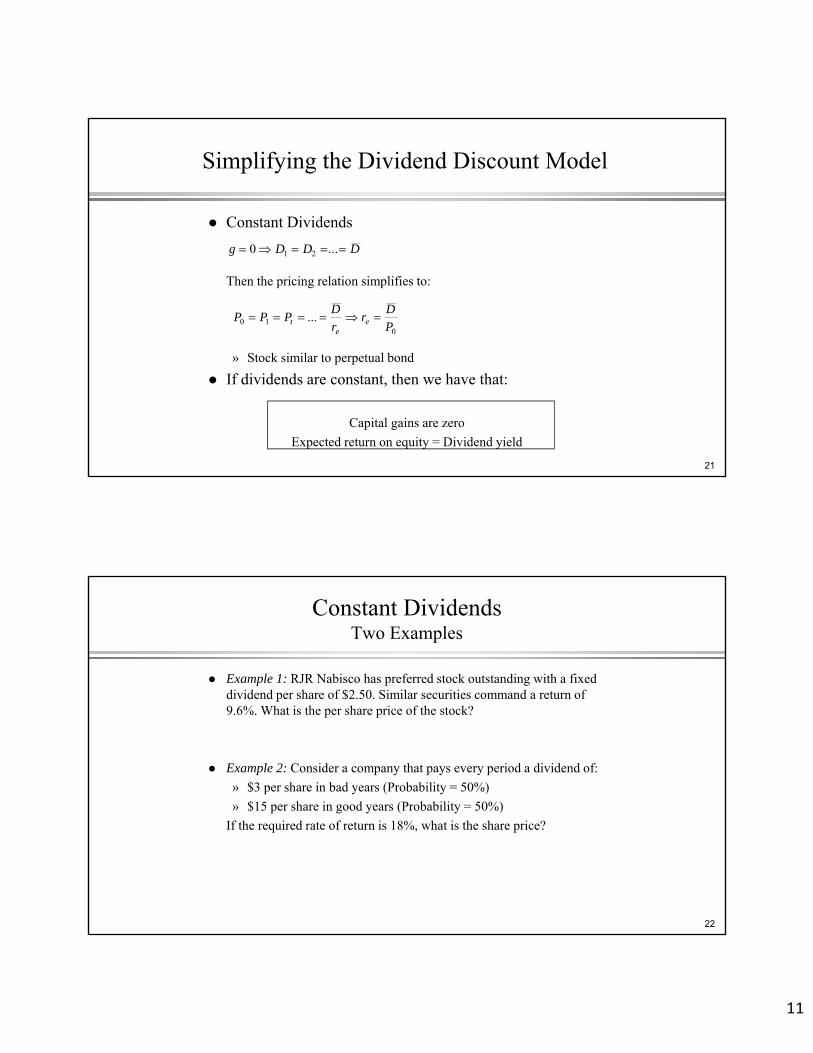

Simplifying the Dividend Discount Model

Constant Dividends

Then the pricing relation simplifies to:

» Stock similar to perpetual bond

If dividends are constant, then we have that:

Capital gains are zero

Expected return on equity = Dividend yield

g D D D 0 1 2 ...

010 ...

P

Dr

r

DPPP e

et

22

Constant DividendsTwo Examples

Example 1: RJR Nabisco has preferred stock outstanding with a fixed dividend per share of $2.50. Similar securities command a return of 9.6%. What is the per share price of the stock?

Example 2: Consider a company that pays every period a dividend of:

» $3 per share in bad years (Probability = 50%)

» $15 per share in good years (Probability = 50%)

If the required rate of return is 18%, what is the share price?

12

23

Valuation with Growing DividendsAn Example: Valuation of XYZ

Consider data for XYZ:

» Number of shares: 856,695

» Market capitalization $46.31m

» Historic dividend $1.60 per share

» Forecasted Dividend: $1.75 per share

– What valuation do you obtain for XYZ, depending on g and r?

24

Valuation of XYZ

Alternative valuations:

Example:

856,695*$1.75=$1.499m

$1.499$37.48

0.09 0.05

forecast

XYZXYZ XYZ

D mMCAP m

r g

Return (re) 3% 4% 5% 6% 7%

7% $37.48 $49.97 $74.96 $149.92 N/A8% $29.98 $37.48 $49.97 $74.96 $149.929% $24.99 $29.98 $37.48 $49.97 $74.9610% $21.42 $24.99 $29.98 $37.48 $49.9711% $18.74 $21.42 $24.99 $29.98 $37.4812% $16.66 $18.74 $21.42 $24.99 $29.98

Growth Rate (g)

13

25

Valuing a BusinessA Hybrid Approach

Sometimes equity analysts have knowledge about the immediate, but not the distant future» Dividend forecasts for immediate future (2-5 years)» Assume constant growth for distant future (>5 years)» How do you change the model?

Dividends

Time

26

Modifying the Constant Growth Model

The formula for a T-year horizon can be written as:

Apply the constant growth model to get the price in period T:

Then the current value of the share is:

P

D

r

P

rt

ett

t T T

eT0 1 1 1

gr

D

gr

DgP

e

T

e

TT

11

gr

D

rr

DP

e

TT

e

Tt

t te

t

1

101

1

1

14

27

Valuing a Business

Consider a company with cash flows from operations of $1 million for the most recent year.

» The company’s cash flows are expected to grow at a rate of 10% for the next 5 years and at a constant rate of 5% thereafter.

» To generate this increase in cash flows, the company is required to reinvest 50% of its cash flows for the first 5 years and 25% of its cash flows thereafter.

» Given the risk of the business, the required rate of return is 15%.

What is the value of the business?

28

Valuing a Business (cont.)

Present value= CF(1)+...+CF(5)=0.48+0.46+0.44+0.42+0.40=2.2

Year 1 Year 2 Year 3 Year 4 Year 5OperatingCash Flows 1.10 1.21 1.33 1.46 1.61New CapitalInvestment -0.55 -0.605 -0.665 -0.73 -0.805Net CashFlow (Div) 0.55 0.605 0.665 0.73 0.805

PresentValue 0.48 0.46 0.44 0.42 0.40

Step 1: Find the present value of the first 5 dividends.

15

29

Valuing a Business (Cont.)

Step 2: Find the present value of the dividends after year 5.

» Value of business at the end of the 5th year.

» Find present value (as of time 0) of this figure.

Step 3: Add result from steps 1 and 2 to get the total present value of the company

30

Expected Returns and the Dividend Growth Model

Use the growth model formula to solve for the required rate of return:

Note that you can synthesize with the previous result,

to show:

Therefore, if dividends grow at a constant rate, then» share prices grow at the same rate:

» yield stays constant:

rD

Pge 1

0

010

01 1 PgPP

PPg

rD

P

P P

Pe 1

0

1 0

0

01 1 PgP

...1

2

0

1 P

D

P

D

16

31

P/E-ratios

Start with basic pricing formula:

Algebra yields:

» Which assumption does one make when arguing that stocks with a low P/E are undervalued?

Some more algebra gives us:

» Implications for re?

Ratio PayoutE

Dd where

gr

dE

gr

DP

ee

1

1110

gr

d

E

P

e

1

0

gP

Edre

0

1

32

Growth Stocks and Value Stocks

Value of stock depends on two components:» Profits generated by assets in place, past capital budgeting

decisions

» Profits generated by growth opportunities in the future

Decompose value of stock:

P/E Ratio

e

ee

r

EdgPPVGO

r

EdgP

r

EP

10

1010

1

1

11

0 1

E

PVGO

rE

P

e

17

33

Historical and Prospective Ratios:

Expected values have to be estimated

Use model to forecast future yields or multiples:

Historic:

Prospective:

Exampled = 0.5, g = 10%, r = 12%

» Prospective: DY=2.0%, PE=25

» Historic: DY=1.81%, PE=27.5

grP

D

gr

d

E

Pe

e

0

1

1

0 ,

01

01

1

1

EgE

DgD

g

gr

P

D

gr

gd

E

P e

e

1

, 1

0

0

0

0

34

Historical Yields and Growth

You can use the expression for the historic yield to infer the growth rate:

Consider the “Alphabet” industry: Yield1Yieldreturn Expected

1 00

00

PD

PDrg e

DEF ABC XYZMCAP ($million) 30.92 40.71 46.31No. of shares 702,500 1,187,000 856,695Share Price $44.01 $34.30 $54.06Dividend p. share $1.35 $1.43 $1.60Dividend Yield 3.07% 4.17% 2.96%EPS $5.03 $3.72 $6.06P/E ratio 8.75 9.22 8.92

18

35

Growth rates in the Industry

Infer growth rate in the “Alphabet” industry

Example:

. . 12%0.12 0.0417

0.0752 7.52%1.0417

Exp retABCg

Expected ReturnsDEF ABC XYZ

9% 5.76% 4.64% 5.87%10% 6.73% 5.60% 6.84%11% 7.70% 6.56% 7.81%12% 8.67% 7.52% 8.78%13% 9.64% 8.48% 9.75%14% 10.61% 9.44% 10.72%15% 11.58% 10.40% 11.69%

Implied growth rates

36

Valuing a Company Using P/E-Multiples

The three steps of using P/E multiples company valuation1 Find sample of comparable companies

2 Compute average of their P/E ratios

3 Multiply earnings by average P/E from step 2.

Example: Value XYZ» Use ABC and DEF as comparables

» Average P/E=(8.75+9.22)/2=8.99

» Estimated value of XYZ share=8.99*$6.06=$54.45

» Market price per share is $54.06 (= 46.31m/856,695)

19

37

Valuation Ratios and Stock Market Outlook

Stock market valuation ratios have been at extreme levels afew years ago by historical standards.

When stock prices are very high relative to indicators offundamental values (such as dividends and earnings), pricestend to fall in the future ...

Consider two measures of fundamental values:– (i) dividend-price ratio (D/P ratio), or dividend yield.– (ii) price-earnings ratio (P/E ratio).

38

Valuation Ratios and Stock Market Outlook (continued)

The dividend-price ratio is measured as previous year’stotal dividends divided by current stock price

» D/P ratios have normally moved in the range from 3% to 7%(with an extreme of much less than 2% a few years ago).

The price-earnings ratio is measured as current stock pricedivided by previous year’s total earnings

» P/E ratios have normally moved in the range 8–20.» Graham and Dodd (1934) said that one should use an average of

earnings of “no less than five years, preferably seven or tenyears”.

20

S&P 500 Dividend/Price and Price/Earnings Ratios

D/P ratio and following returns 1960-2019

21

41

Summary

Stocks and equity securities can be valued by using present value techniques» The discounting horizon does not depend on the investment horizon of

individual investors in the stock market

Investors are compensated through cash dividends and through capital gains» Required returns on equity are generally not equal to the dividend yield, but

to the dividend yield plus the growth rate

P/E-ratios should be used with caution:» Depends on simplifying assumptions