Embed Size (px)

DESCRIPTION

VAT Rules in UK and EU. Impact of Value added tax on the supply chain and how to make the supply chain tax effective using IT solutions

Citation preview

VAT in UK

By Vikas MarwahaManoj Singh

1

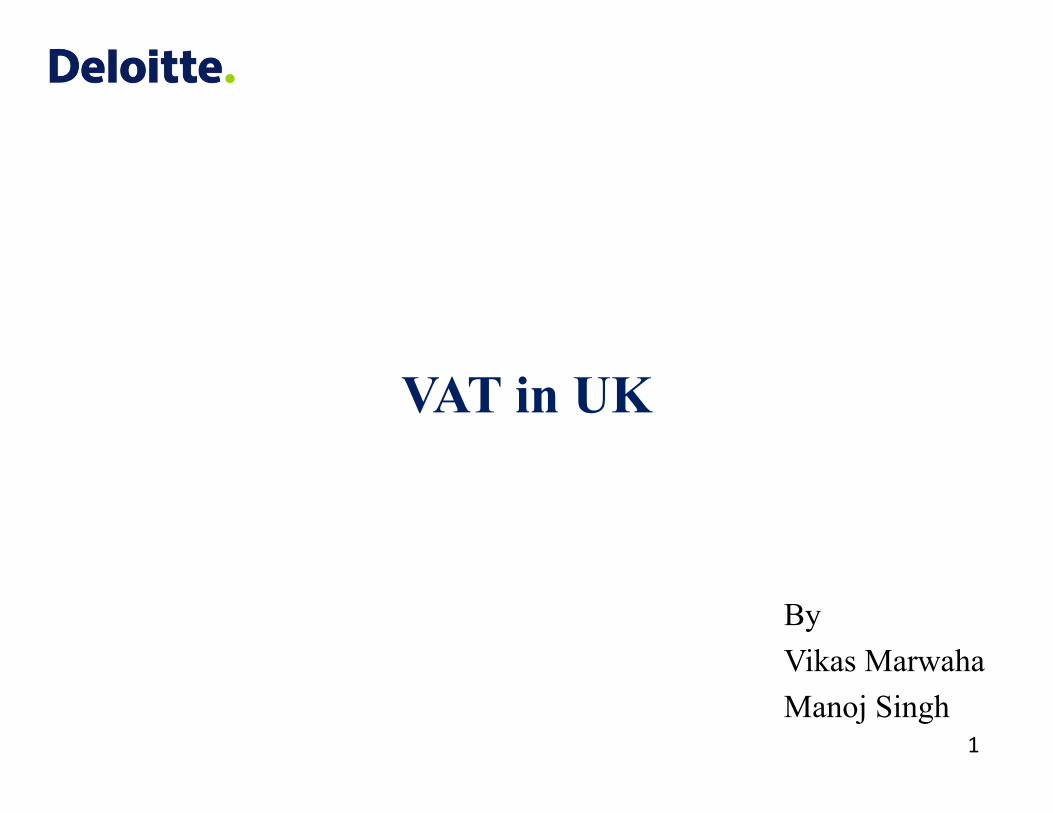

Types of Taxes

Taxes

Indirect tax

VAT

Excise

Others like Customs, Service

tax

Direct tax

Income/Corporate tax

Others like Capital gain tax, Property,

Entitlement

2

Indirect taxes in supply chain

3

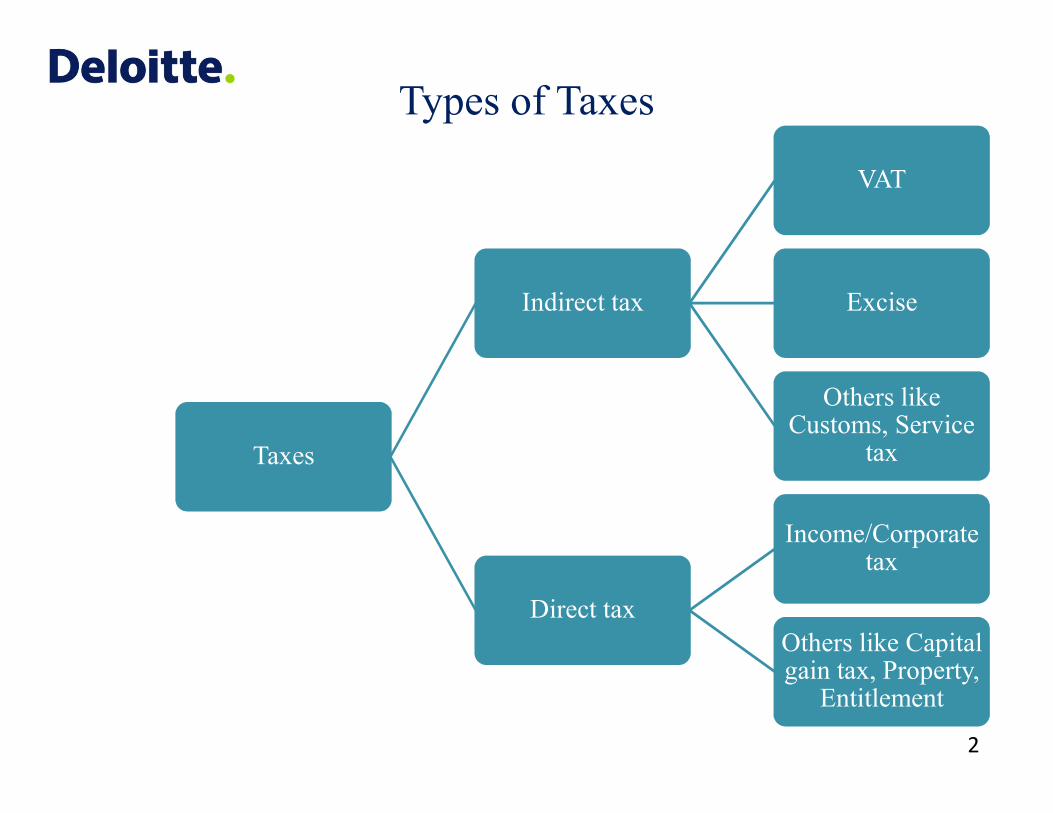

What is VAT?• Collected on business transactions,

imports and acquisitions that VATregistered businesses provide in UK.

• VAT is charged when a VAT-registeredbusiness sells to either anotherbusiness or to a non-businesscustomer.

• Businesses add VAT to the price theycharge when they provide goods andservices.

• Tax on the value added at each stage.4

Tax Credit Method• Input Tax-When a company buys goods or services from

another supplier, VAT is charged on the purchase cost. This isknown as input tax.

• Output Tax-The amount of value added tax a company adds tothe price of its product or service.

• Works on Tax Credit Method: Tax at sales, credit at purchase

• As per this principle,• Input VAT = 3000*(12.5/100) = 375• Output VAT = 4000*(12.5/100) = 500• VAT credit to manufacturer = Input VAT paid

Net VAT to government by manufacturer = 500-375 = 125

5

VAT Calculation Methods

VAT Calculation Methods

Invoice-based credit method (Indirect)• Compute the tax to be imposed at each stage of sales on the entire

sale value• Set-off the tax paid at the earlier stage. (i.e., at the stage of

purchases in set-off)• The differential amount (i.e. Step 2 – Step1) is required to be paid

Subtraction method (Direct)• Determine Value addition as:• Total value of sales• Less: Total value of purchases• (both exclusive of tax)

6

VAT Calculation Formulae

Cases Substraction Method Credit invoice method

No exemption, no zero ratingt1*P1+t2*(P2-P1) +t3*(P3-P2)

t1*P1+[t2*P2-t1*P1]+[t3*P3-t2*P2] = t3*P3

Exemption of the first stage t2*P2+t3*(P3-P2) t2*P2+[t3*P3-t2*P2] = t3*P3

Exemption of the second (middle) stage t1*P1+t3*(P3-P2) t1*P1+t3*P3

Exemption of the third (last) stage t1*P1+t2*(P2-P1) t1*P1+[t2*P2-t1*P1] = t2*P2

Zero rating of the first stage t2*P2+t3*(P3-P2) t2*P2+[t3*P3-t2*P2] = t3*P3

Zero rating of the second (middle) stage t1*P1+0*(P2-P1)+t3*(P3-P2)

t1*P1+[0*P2-t1*P1]+[t3*P3-0*P2]=t3*P3

Zero rating of the third (last) stage t1*P1+t2*(P2-P1)+0*(P3-P2)

t1*P1+[t2*P2-t1*P1]+[0*P3-t2*P2]=0

• Calculations changes with the type ofcalculation methodology and standard/exempt /zero rates condition.

7

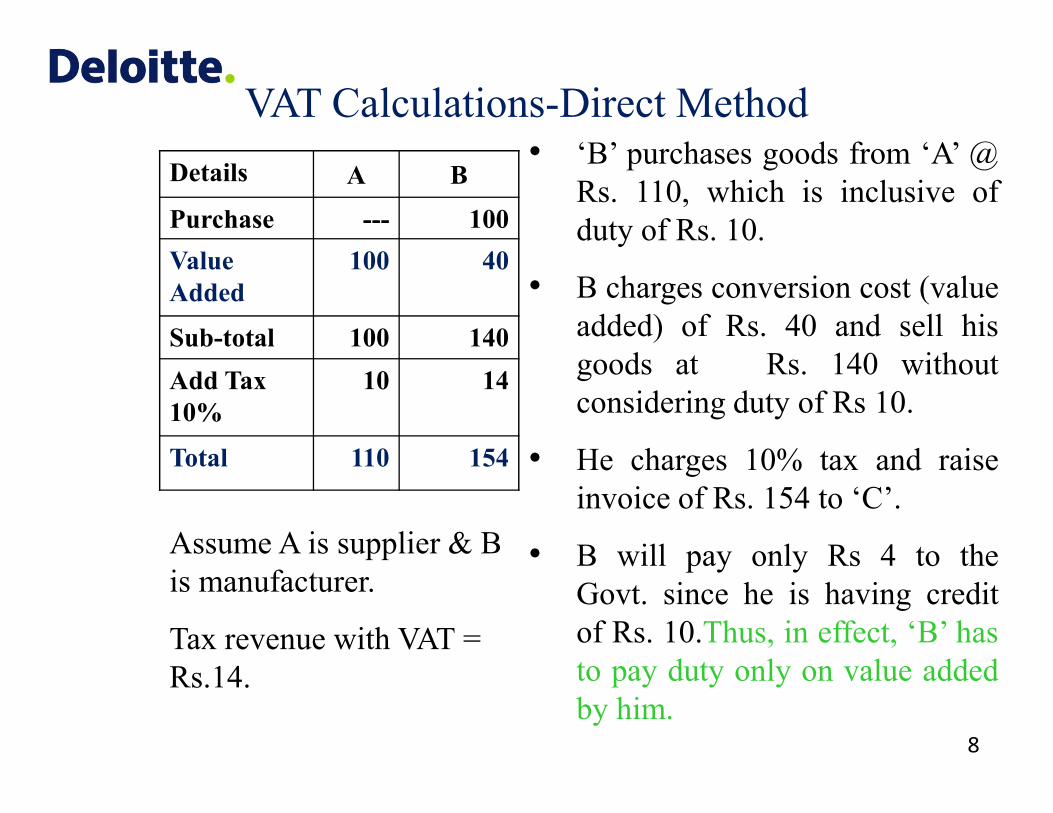

VAT Calculations-Direct MethodDetails A BPurchase --- 100Value Added

100 40

Sub-total 100 140Add Tax 10%

10 14

Total 110 154

Assume A is supplier & B is manufacturer.

Tax revenue with VAT = Rs.14.

• ‘B’ purchases goods from ‘A’ @Rs. 110, which is inclusive ofduty of Rs. 10.

• B charges conversion cost (valueadded) of Rs. 40 and sell hisgoods at Rs. 140 withoutconsidering duty of Rs 10.

• He charges 10% tax and raiseinvoice of Rs. 154 to ‘C’.

• B will pay only Rs 4 to theGovt. since he is having creditof Rs. 10.Thus, in effect, ‘B’ hasto pay duty only on value addedby him.

8

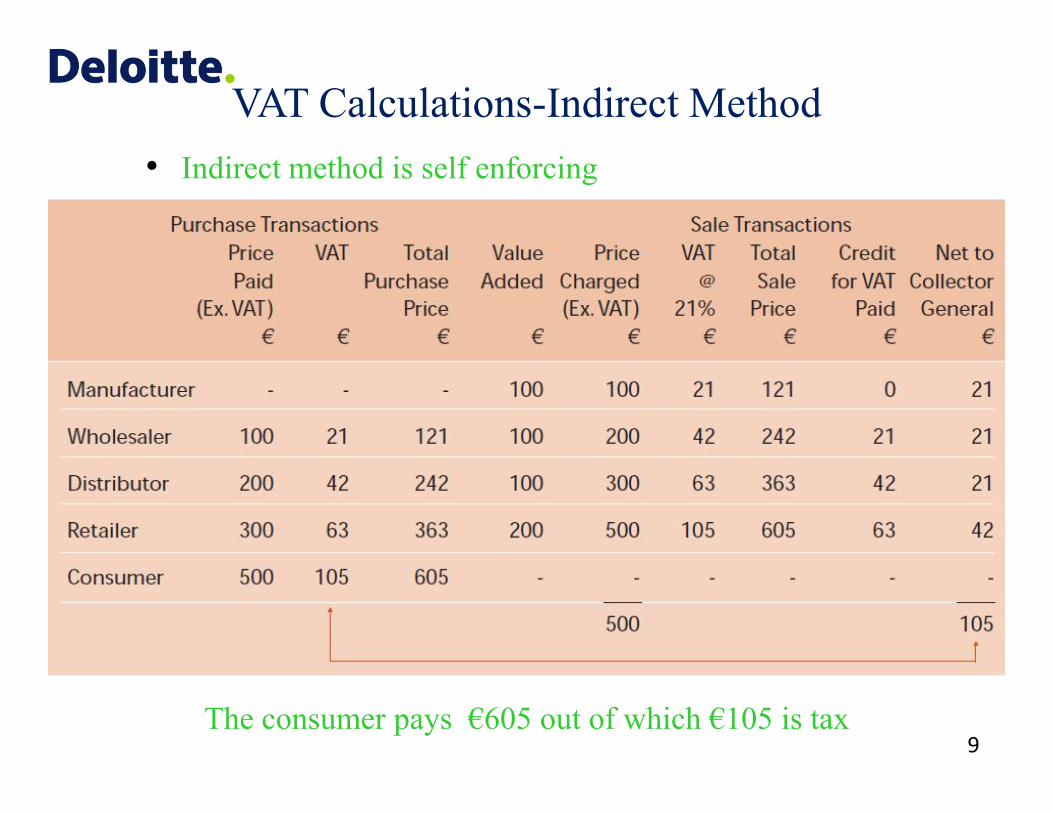

VAT Calculations-Indirect Method

The consumer pays €605 out of which €105 is tax

• Indirect method is self enforcing

9

Distance sales• Distance sales-Refers to goods which are:

Ø Either transported or dispatched to unregistered persons in theState from another EU Member State or from outside the EUthrough another EU Member State.

Ø Transported or dispatched to unregistered persons in anotherEU Member State from UK.

Ø IF distance sales threshold limit exceeds the place the POS iswhere transport ends.

10

Who are required to pay VAT?

• For VAT purposes, the United Kingdom consists of GreatBritain, the Isle of Man and Northern Ireland. It does notinclude the Channel Islands or Gibraltar.

Person who makes taxable supplies above certain value limits (currently £77,000)

Reverse-charge services received by a taxable person

Importation of goods from outside the EU

Unregistered person acquiring goods from another EC member state

Person making distance sales above the limit of £70,000

Voluntary registration is allowed

11

When VAT registration?• A firm has to register for VAT if either:

Ø Sales of non-exempt goods and services for the previous 12months exceed the VAT registration threshold currently£77,000)

Ø Voluntary registration for the businesses with sales below£77,000

Ø However for Intra-Community acquisitions limit is: £70,000Ø For Distance Sales: £70,000

• Companies registered under VAT have to submit their VATreturns to HMRC:Ø As a General rule: QuarterlyØ Monthly If requested by a business that receives regular

repayments

12

Why VAT registration?

• For VAT-registered business:Ø Charge VAT on the goods and services providedØ Reclaim the VAT you paid on goods and services (raw

materials) for your business

• If you are not VAT-registered then you cannot reclaim the VATyou pay when you purchase goods and services.

• If you purchase services or goods before you register for VAT,you may be able to get a VAT credit for them.

• The credit generally applies for services and goods purchasedup to four years prior to VAT registration.

13

Group registration

• Corporate bodies that are under “common control” and areestablished or have a fixed establishment in the UnitedKingdom may apply to register as a VAT group.

• A VAT group is treated as a single taxable person. The groupmembers share a single VAT number and submit a single VATreturn.

• No VAT is charged on supplies made between group members.Group members are jointly and severally liable for all VATliabilities.

14

Criteria for Group Registration

• General Criteria:Ø Each body has its principal or registered office in the UKØ They are under common control

• Special Criteria: If the turnover of the VAT group is over £10million per year and the group is partly owned or managed by athird party:Ø No more than 50 per cent of benefits generated by the business

go to third partiesØ Group uses consolidated accountingØ No third party consolidates the group into its accounts

• The registration is made in the name of the 'representativemember‘

15

Non established businesses• A “non established business” is a business that does not have a

fixed establishment in the United Kingdom

• Must register for VAT if:Ø Goods located in the United Kingdom at the time of supplyØ Intra-Community acquisitions of goodsØ Distance sales of goods to U.K. residents who are not taxable

personsØ Services to which the reverse charge does not apply

16

Destination principle

• VAT is charged based on the place where they are consumed.• It implies that whether the Mr. X purchases raw material locally

or imports it, he has to pay VAT at French rate only.• However, it requires the monitoring of cross-border trade flows

and administrative co-operation.• For trade of goods between two VAT registered businesses in

different EU countriesè Destination principle17

Origin principle

• The origin principle implies the taxation of goods and services where produced, regardless of where they are consumed.

• However, the origin principle introduces the possibility for the tax system to discriminate between domestically produced goods and imports.

• For the dispatch of goods/services to a non registered business or customer in another EU countryè Origin principle

18

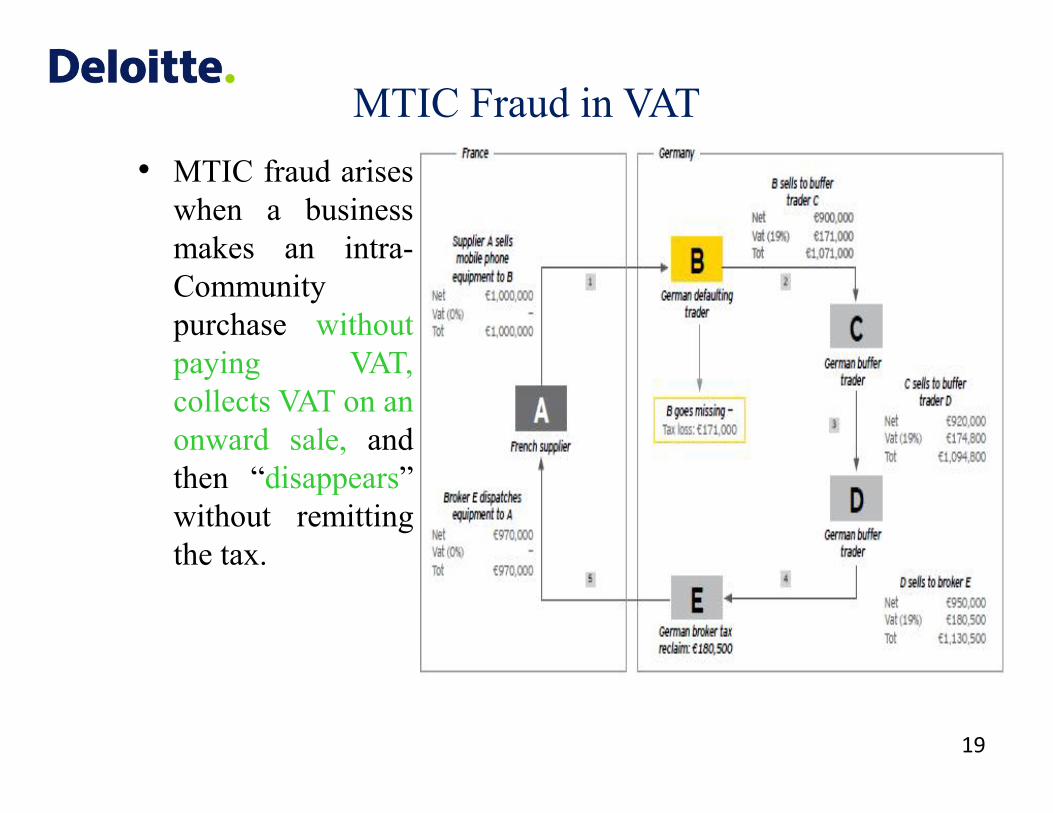

MTIC Fraud in VAT• MTIC fraud arises

when a businessmakes an intra-Communitypurchase withoutpaying VAT,collects VAT on anonward sale, andthen “disappears”without remittingthe tax.

19

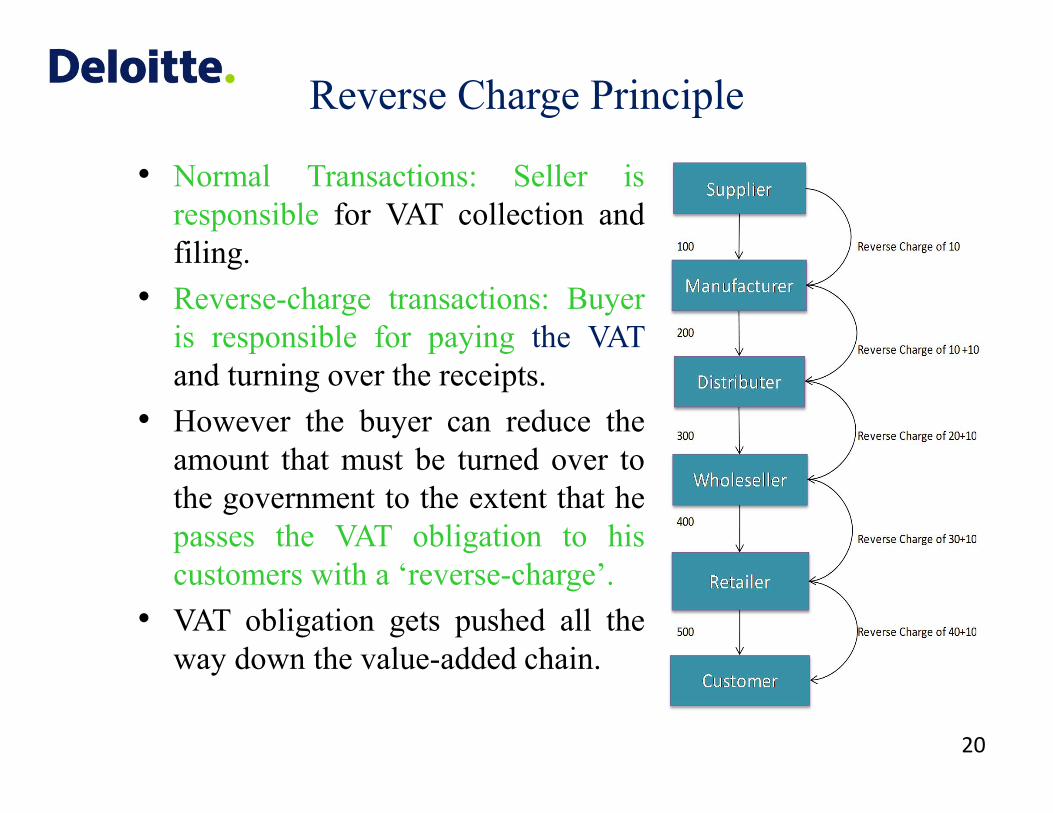

Reverse Charge Principle

• Normal Transactions: Seller isresponsible for VAT collection andfiling.

• Reverse-charge transactions: Buyeris responsible for paying the VATand turning over the receipts.

• However the buyer can reduce theamount that must be turned over tothe government to the extent that hepasses the VAT obligation to hiscustomers with a ‘reverse-charge’.

• VAT obligation gets pushed all theway down the value-added chain.

20

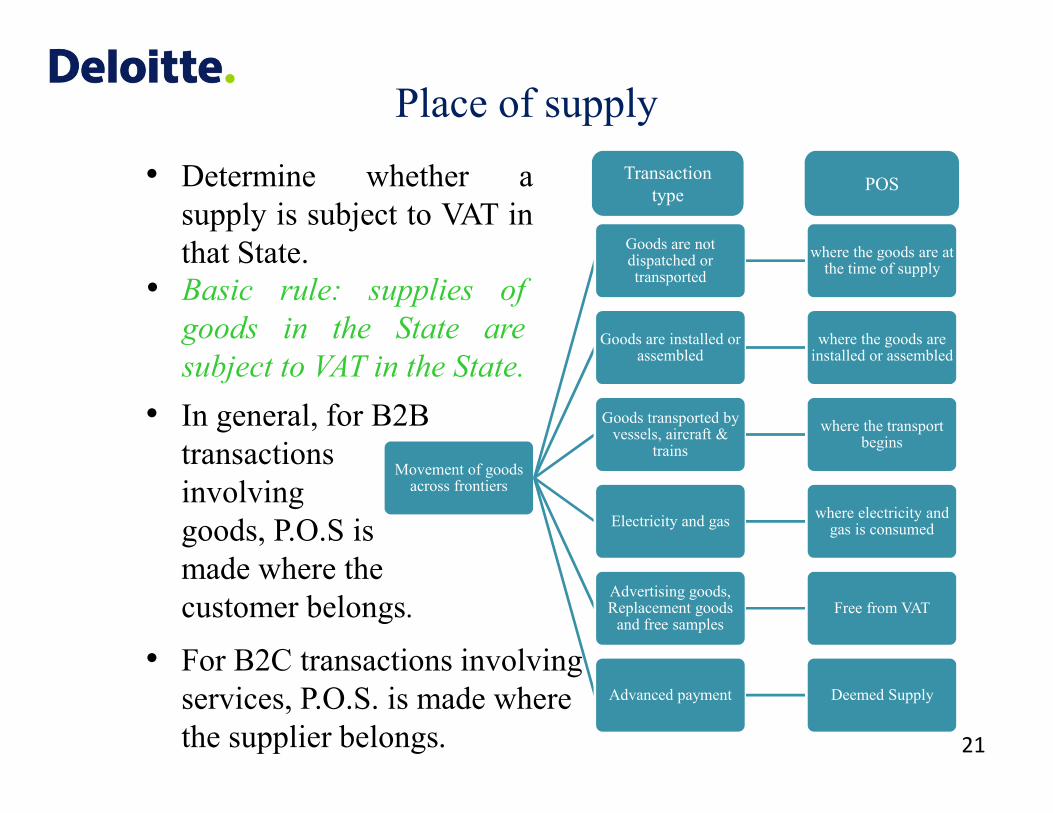

Place of supply• Determine whether a

supply is subject to VAT inthat State.

Movement of goods across frontiers

Goods are not dispatched or transported

where the goods are at the time of supply

Goods are installed or assembled

where the goods are installed or assembled

Goods transported by vessels, aircraft &

trains where the transport

begins

Electricity and gas where electricity and gas is consumed

Advertising goods, Replacement goods

and free samples Free from VAT

Advanced payment Deemed Supply

Transaction type POS

• Basic rule: supplies ofgoods in the State aresubject to VAT in the State.

• For B2C transactions involving services, P.O.S. is made where the supplier belongs.

• In general, for B2B transactions involving goods, P.O.S is made where the customer belongs.

21

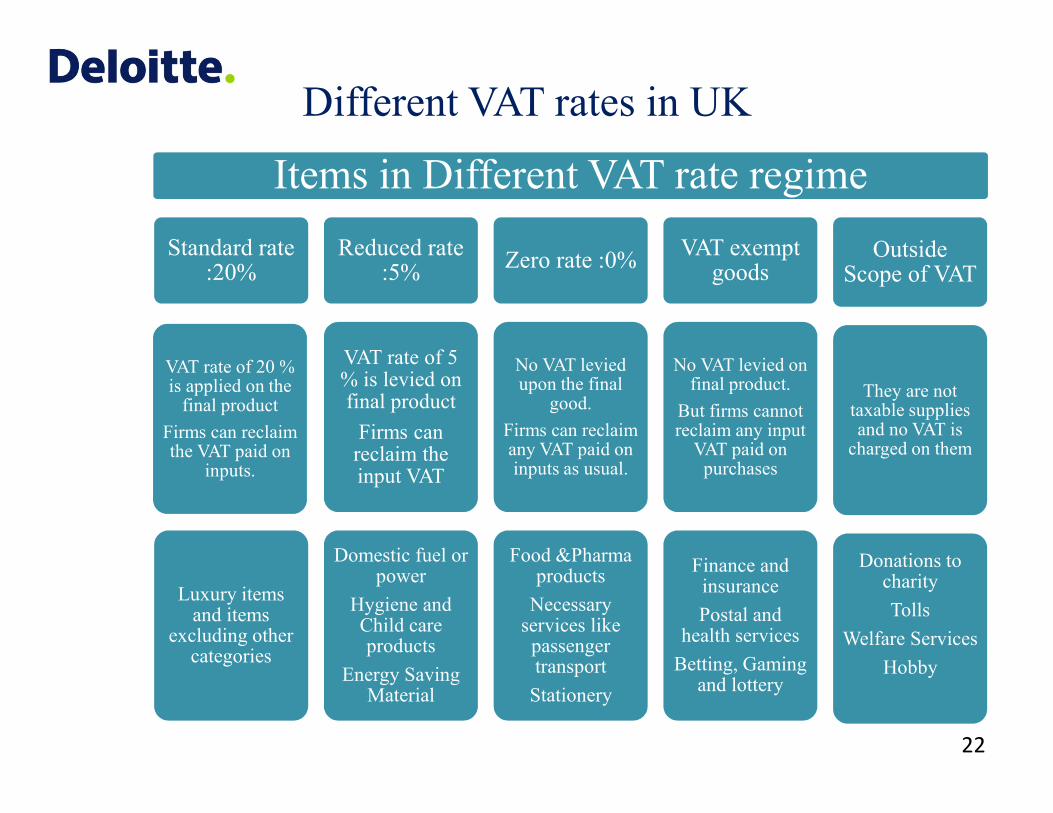

Different VAT rates in UK

Items in Different VAT rate regimeStandard rate

:20%

VAT rate of 20 % is applied on the

final productFirms can reclaim the VAT paid on

inputs.

Luxury items and items

excluding other categories

Reduced rate :5%

VAT rate of 5 % is levied on final product

Firms can reclaim the input VAT

Domestic fuel or power

Hygiene and Child care products

Energy Saving Material

Zero rate :0%

No VAT levied upon the final

good. Firms can reclaim any VAT paid on inputs as usual.

Food &Pharmaproducts

Necessary services like

passenger transport

Stationery

VAT exempt goods

No VAT levied on final product.

But firms cannot reclaim any input

VAT paid on purchases

Finance and insurancePostal and

health servicesBetting, Gaming

and lottery

Outside Scope of VAT

They are not taxable supplies and no VAT is

charged on them

Donations to charityTolls

Welfare ServicesHobby

22

Exempt with credit

• Exempt with credit supplies are effectively treated as if theywere zero-rated, even though they are not within the scope ofVAT.

• No VAT is chargeable, but the supplier may recover relatedinput tax.

• Exempt with credit supplies include services supplied to taxablepersons in the EU and to customers outside the EU.

23

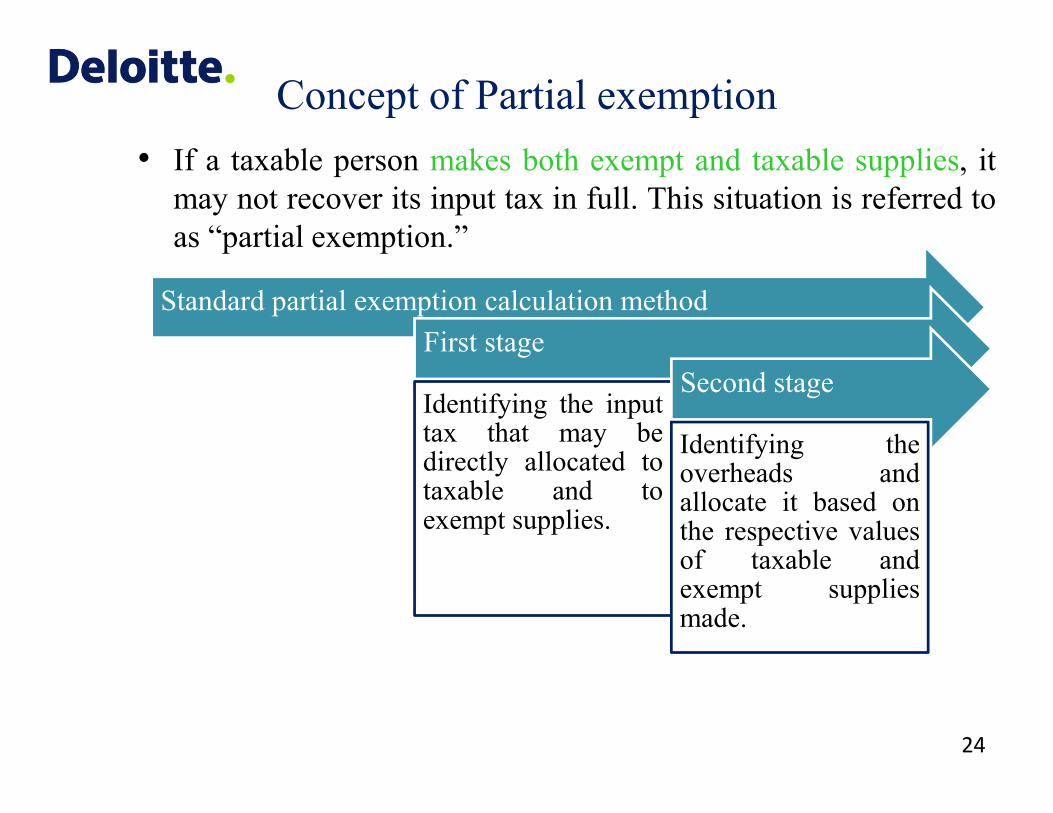

Concept of Partial exemption• If a taxable person makes both exempt and taxable supplies, it

may not recover its input tax in full. This situation is referred toas “partial exemption.”

Standard partial exemption calculation methodFirst stage

Identifying the inputtax that may bedirectly allocated totaxable and toexempt supplies.

Second stage

Identifying theoverheads andallocate it based onthe respective valuesof taxable andexempt suppliesmade.

24

Eligibility of refund (E.U. businesses)• Conditions of Refund:

• Minimum claim amount should be at least £35.• Time limits: The application is to be submitted before 30th

September of a calendar year.

The business is not registered or liable to be registered for VAT in the UK

The business has no residence, seat or permanent establishment in the UK

Businesses don't make any supplies within UK

Carrying out transport services related to the international carriage of goods

Services where the VAT on the supply is payable solely by the person whom they are supplied.

25

VAT recovery on Capital goods• Input tax is deducted in the VAT year in which the goods are

acquired.• However, the amount of input tax recovered for capital goods

must then be adjusted over time.

Land and buildings and related property expenditure valued

at £250,000 or more: adjusted over a

period of 10 years

Computer hardware valued at £50,000 or more: adjusted over

a period of five years

Ships and aircraft valued at £50,000 or more: adjusted over

a period of five years

VAT Recovery on Capital Goods26

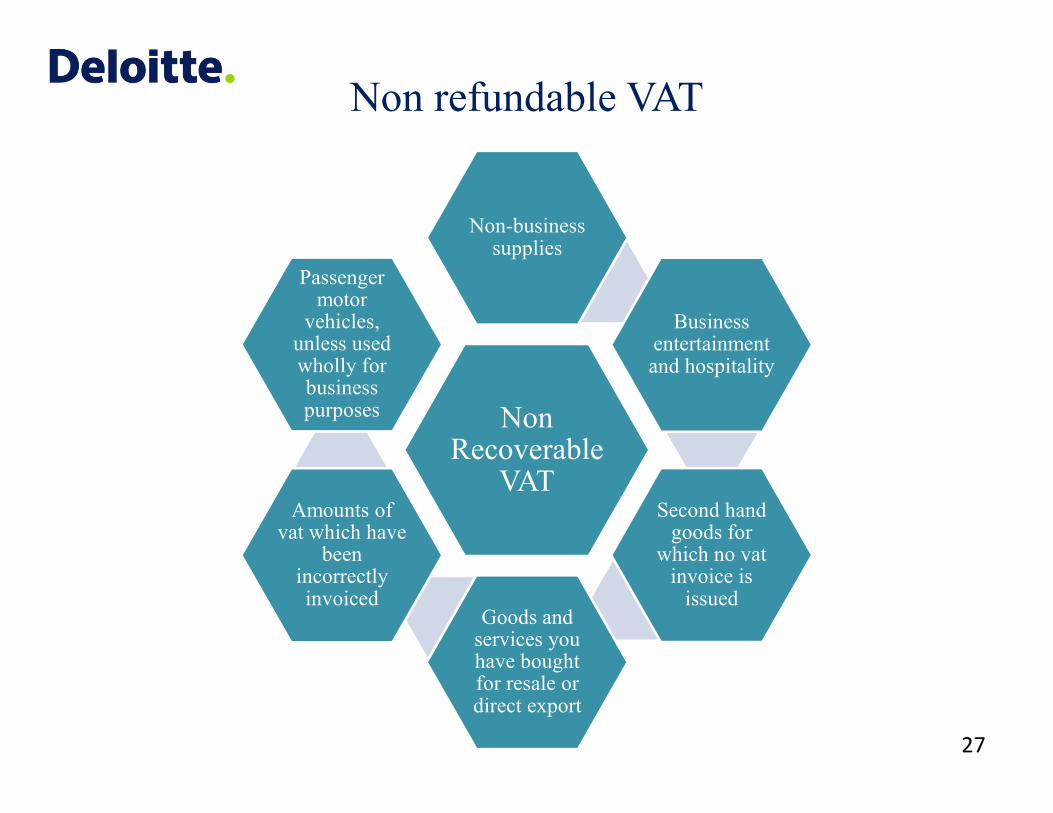

Non refundable VAT

Non Recoverable

VAT

Non-business supplies

Business entertainment and hospitality

Second hand goods for

which no vat invoice is

issuedGoods and

services you have bought for resale or direct export

Amounts of vat which have

been incorrectly invoiced

Passenger motor

vehicles, unless used wholly for business purposes

27

Eligibility of refund (Non E.U. businesses)• Conditions for refund:

• Minimum claim to be made is £16

The business is not registered or liable to be registered for VAT in the UK

The business has no residence, seat or permanent establishment in the UK

Businesses don't make any supplies within UK

Carrying out transport services related to the international carriage of goods

Services where the VAT on the supply is payable solely by the person whom they are supplied.

Claimant’s own country allows similar concessions to UK traders in respect of its own turnover taxes

28

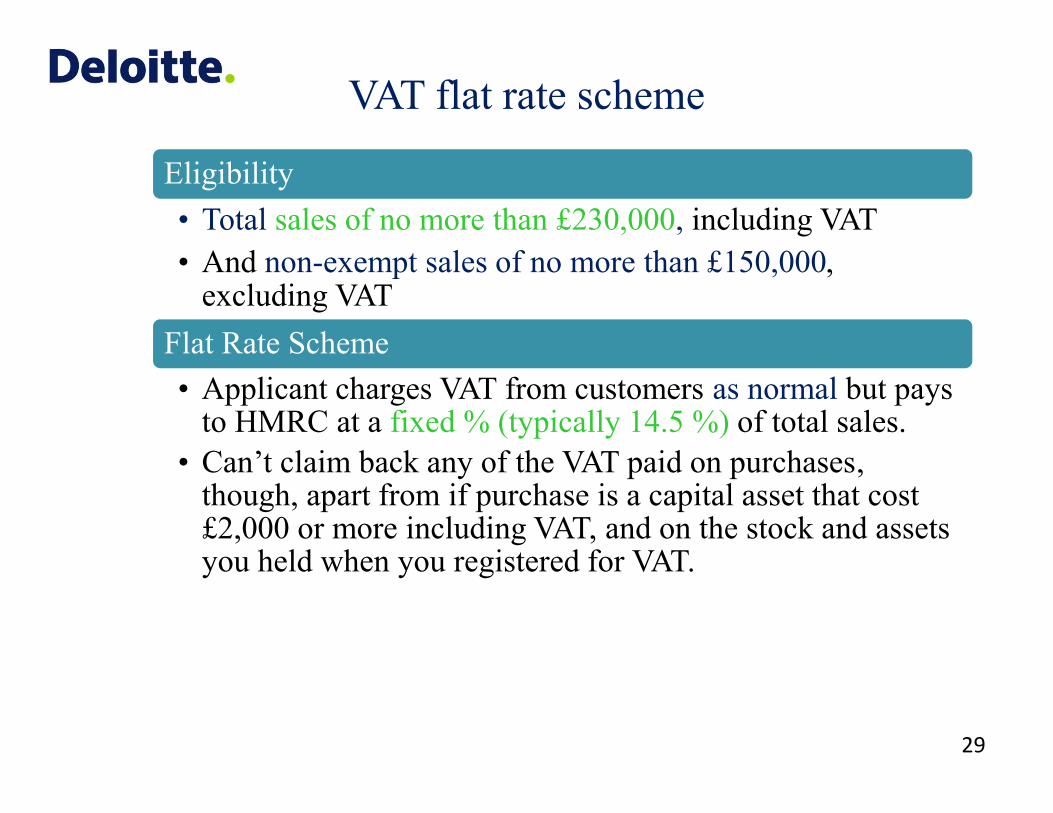

VAT flat rate scheme

Eligibility• Total sales of no more than £230,000, including VAT• And non-exempt sales of no more than £150,000,

excluding VATFlat Rate Scheme• Applicant charges VAT from customers as normal but pays

to HMRC at a fixed % (typically 14.5 %) of total sales.• Can’t claim back any of the VAT paid on purchases,

though, apart from if purchase is a capital asset that cost £2,000 or more including VAT, and on the stock and assets you held when you registered for VAT.

29

Example of benefits from Flat rate scheme

• Mr. X is a consulting engineer earns a total sales of 100000pounds from the client

• He make small purchases of 10000 pounds

• Standard VAT a/c:Ø Input VAT = 2000Ø Output VAT = 20000Ø VAT paid by Mr. X =

18000

• Flat rate schemeØ Flat rate = 14.5 %Ø Total Sales including

VAT = 120000 (This isbecause you chargesclient in normal way)

Ø VAT paid by Mr. X =120000*14.5/100 =17400

Mr. X saves €600 by this schemeAdditionally one can get a 1 % deduction in the first year 30

Cash Accounting Scheme for VAT

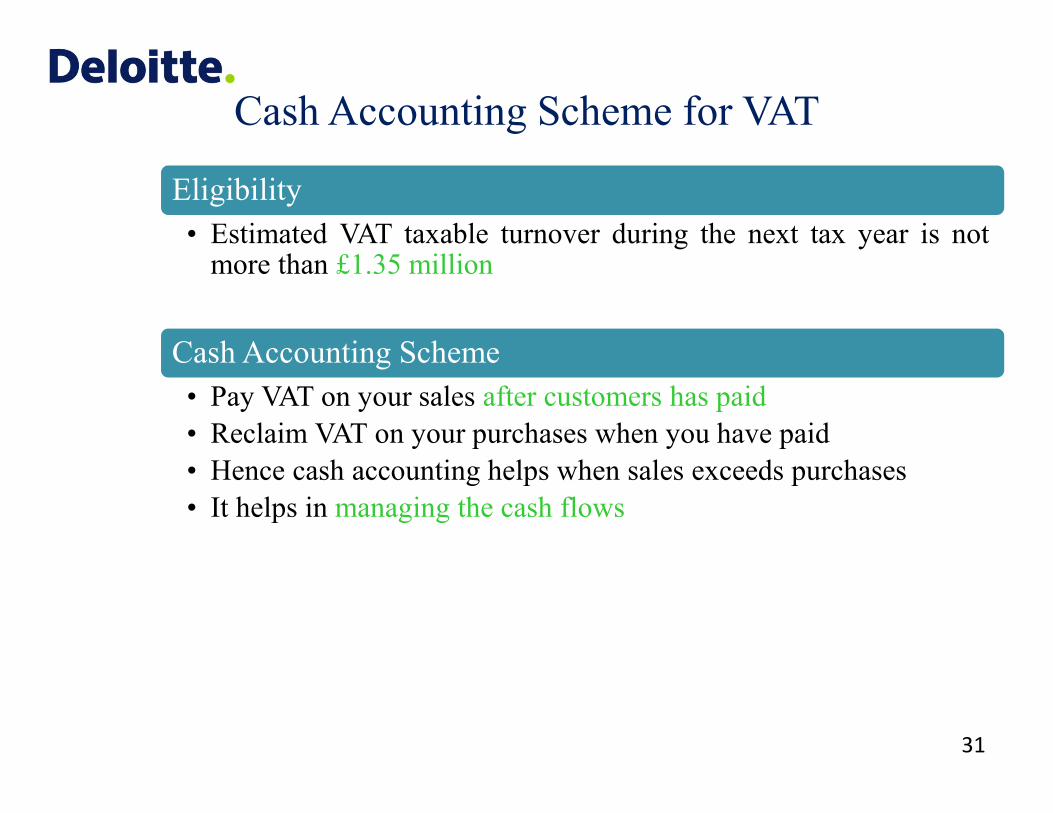

Eligibility• Estimated VAT taxable turnover during the next tax year is not

more than £1.35 million

Cash Accounting Scheme• Pay VAT on your sales after customers has paid• Reclaim VAT on your purchases when you have paid• Hence cash accounting helps when sales exceeds purchases• It helps in managing the cash flows

31

VAT Annual Accounting Scheme

Eligibility• Estimated VAT taxable turnover during the next tax year is not

more than £1.35 million

Annual Accounting Scheme• Helps small businesses by allowing them to submit only one VAT

return annually rather than the normal four• Businesses pay their VAT in nine monthly installments of 10% of

the previous year’s liability. The installments are payable at theend of months 4-12 of the current annual accounting period.

• Alternatively such businesses may choose to pay their VAT inthree quarterly installments of 25% of the previous year’s liabilityfalling due at the end of months 4, 7 and 10.

• The balance of VAT for the year is then due together with the VATreturn two months after the end of the annual accounting period.

32

Standard accounting Annual accounting• Liability to be

paid each monthis known andcertain, cashflow can bemanaged moreeasily

• Simplifiescalculations

• Interimpayments maybe higher thanneeded

Standard Accounting versus Annual Accounting

33

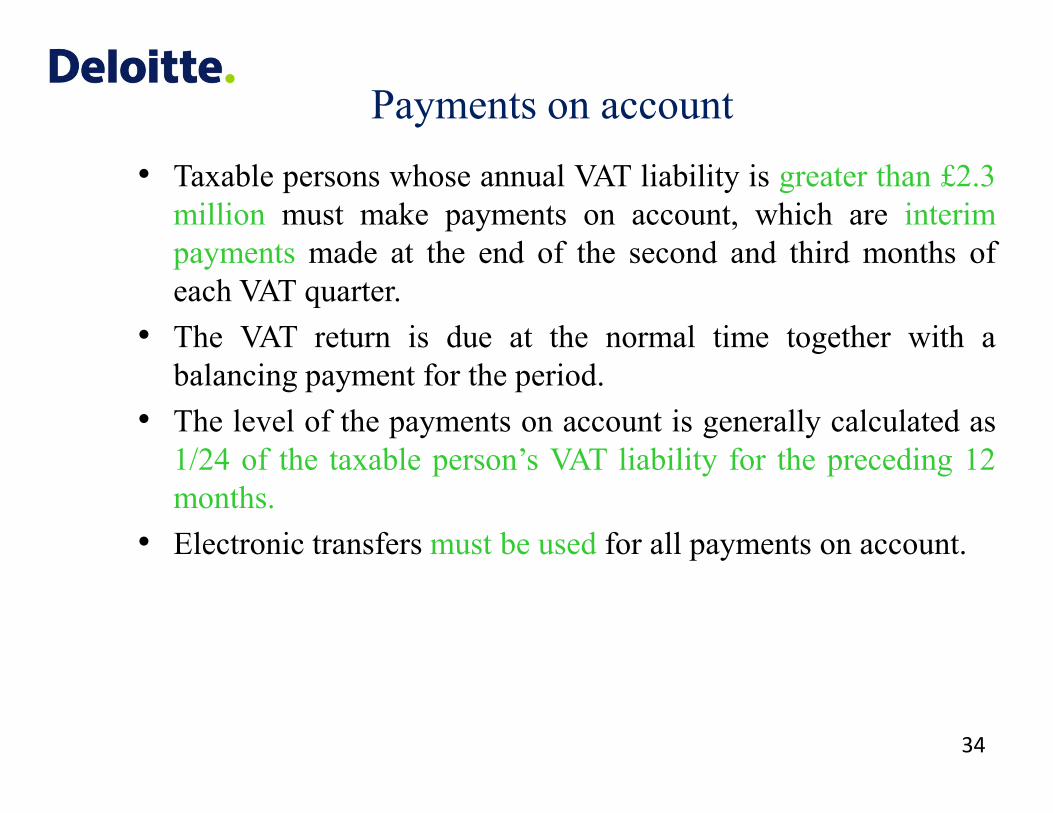

Payments on account• Taxable persons whose annual VAT liability is greater than £2.3

million must make payments on account, which are interimpayments made at the end of the second and third months ofeach VAT quarter.

• The VAT return is due at the normal time together with abalancing payment for the period.

• The level of the payments on account is generally calculated as1/24 of the taxable person’s VAT liability for the preceding 12months.

• Electronic transfers must be used for all payments on account.

34

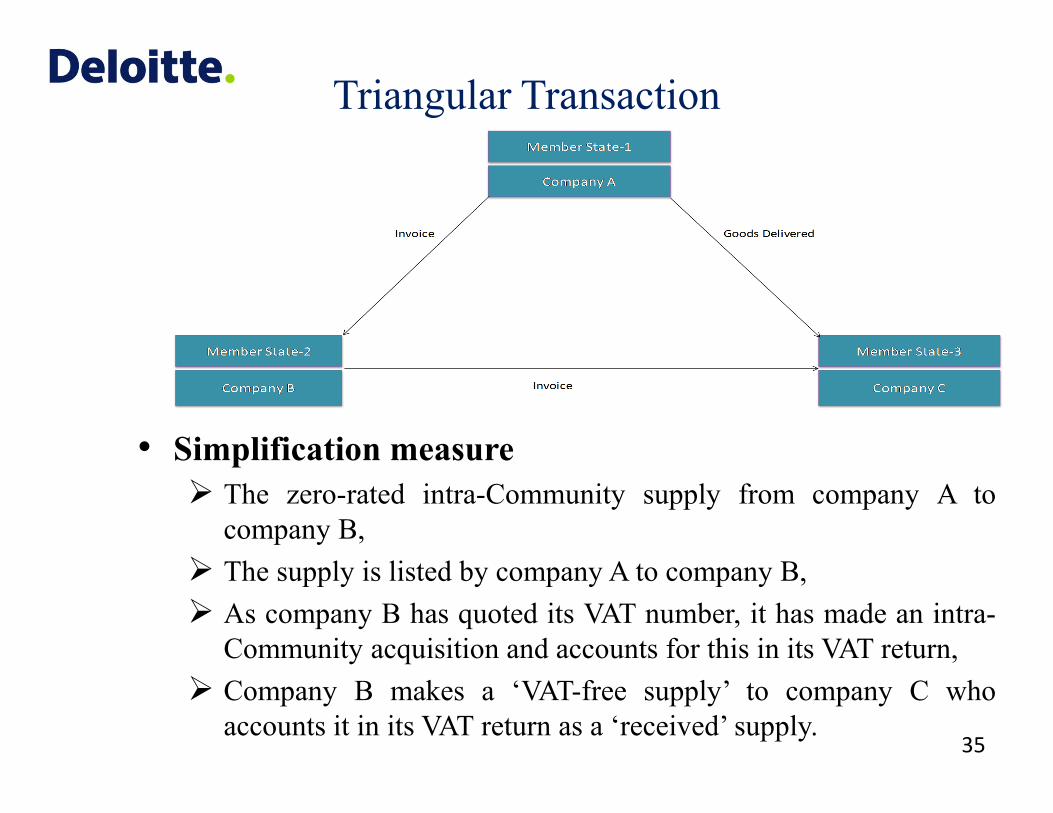

Triangular Transaction

• Simplification measureØ The zero-rated intra-Community supply from company A to

company B,Ø The supply is listed by company A to company B,Ø As company B has quoted its VAT number, it has made an intra-

Community acquisition and accounts for this in its VAT return,Ø Company B makes a ‘VAT-free supply’ to company C who

accounts it in its VAT return as a ‘received’ supply.35

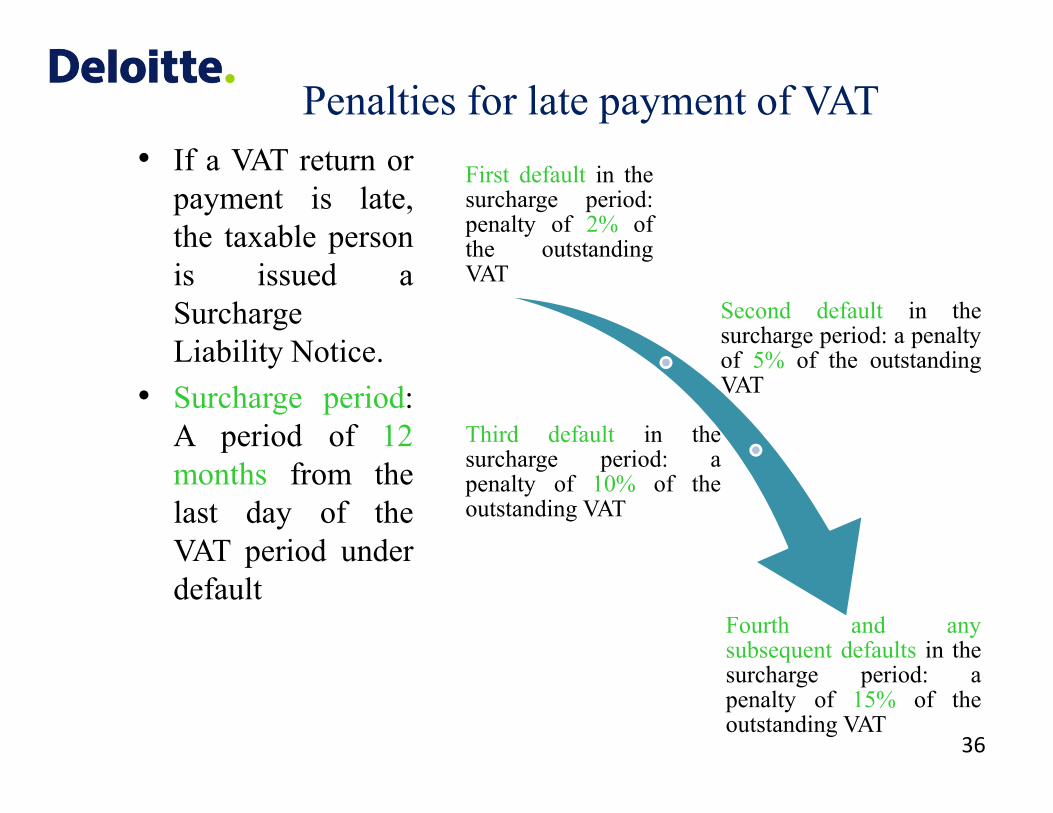

Penalties for late payment of VAT• If a VAT return or

payment is late,the taxable personis issued aSurchargeLiability Notice.

• Surcharge period:A period of 12months from thelast day of theVAT period underdefault

First default in thesurcharge period:penalty of 2% ofthe outstandingVAT

Second default in thesurcharge period: a penaltyof 5% of the outstandingVAT

Third default in thesurcharge period: apenalty of 10% of theoutstanding VAT

Fourth and anysubsequent defaults in thesurcharge period: apenalty of 15% of theoutstanding VAT

36

Flow Chart to determine applicable VAT rate

37

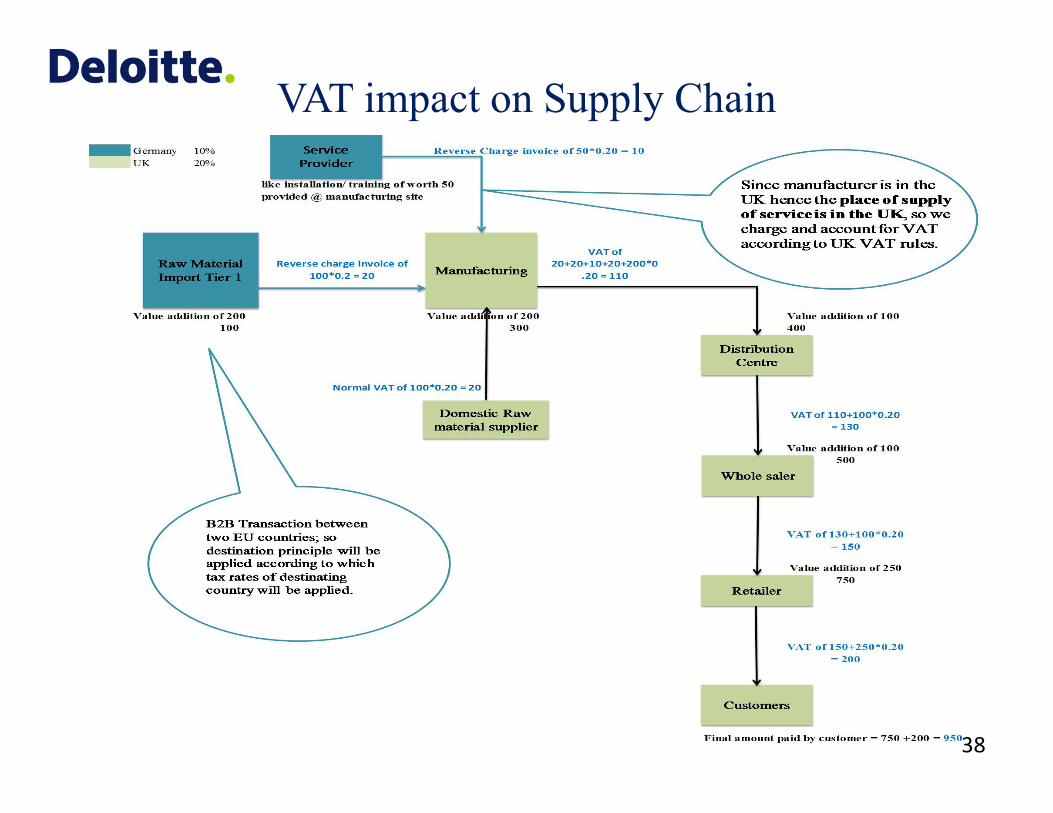

VAT impact on Supply Chain

38

Thank you…

Vikas MarwahaManoj Singh

I. Online VAT Return in UK.

II. Reporting requirements and

procedures.

1

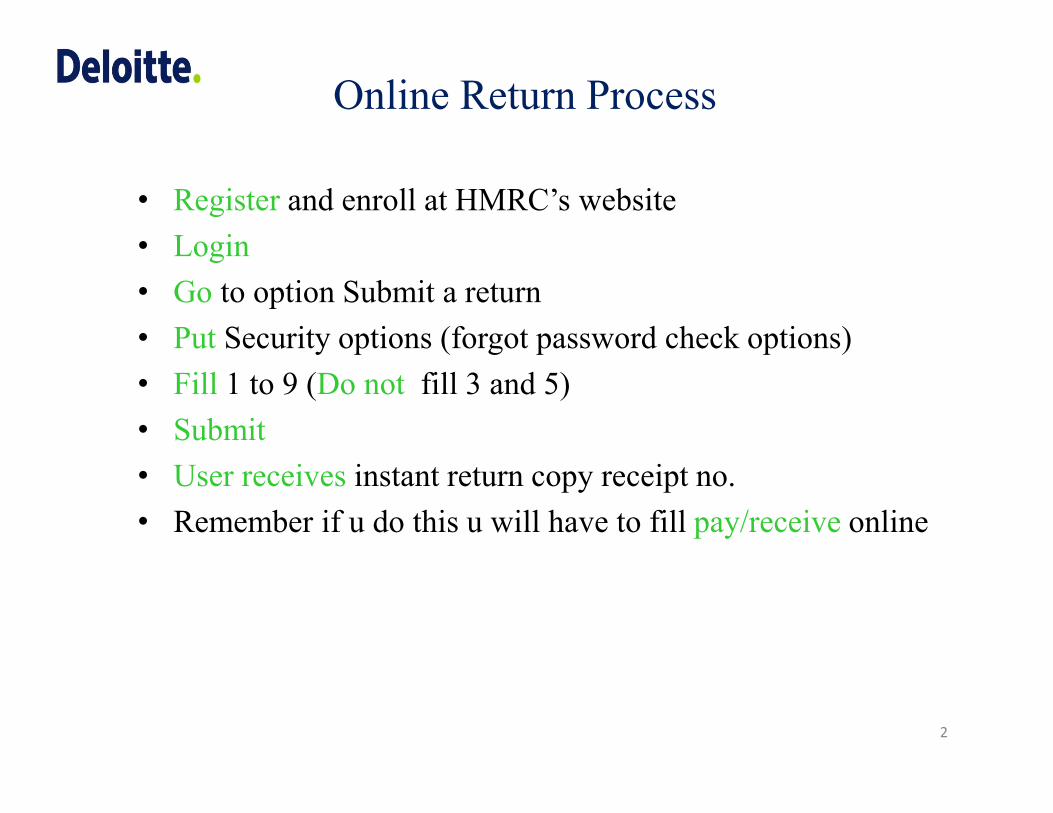

Online Return Process

• Register and enroll at HMRC’s website• Login• Go to option Submit a return• Put Security options (forgot password check options)• Fill 1 to 9 (Do not fill 3 and 5)• Submit• User receives instant return copy receipt no.• Remember if u do this u will have to fill pay/receive online

2

Vat return form, manual filling

3

Vat online return form

4

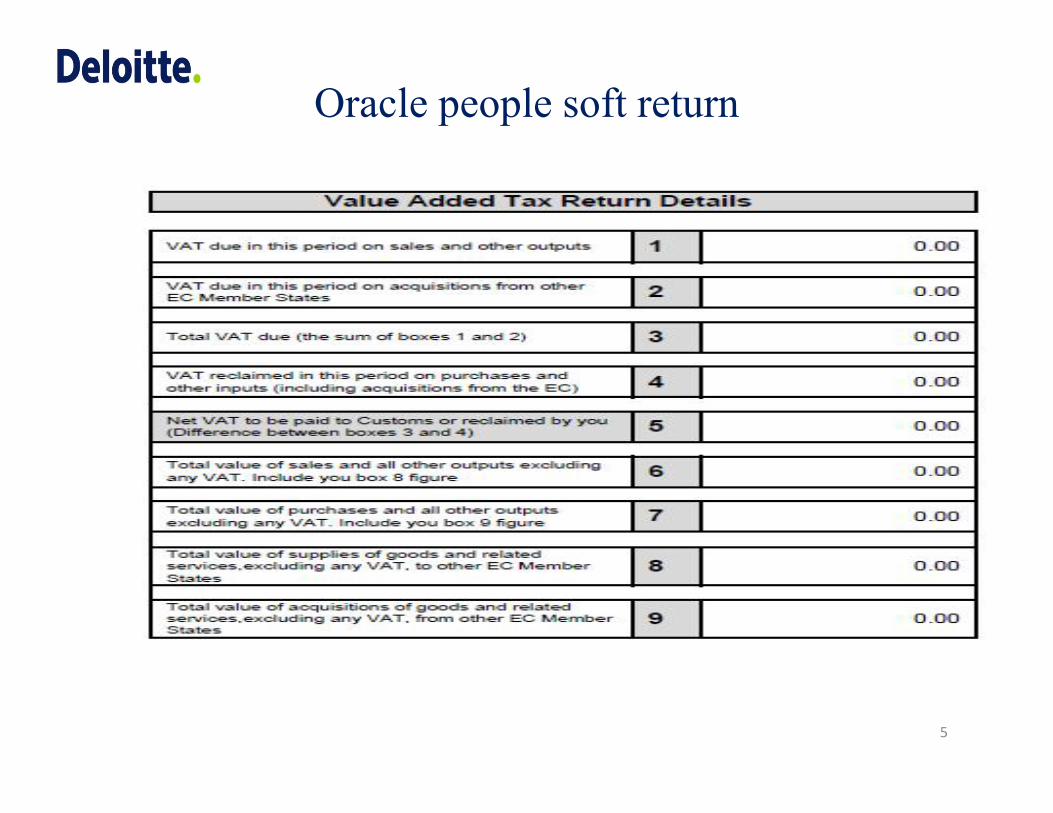

Oracle people soft return

5

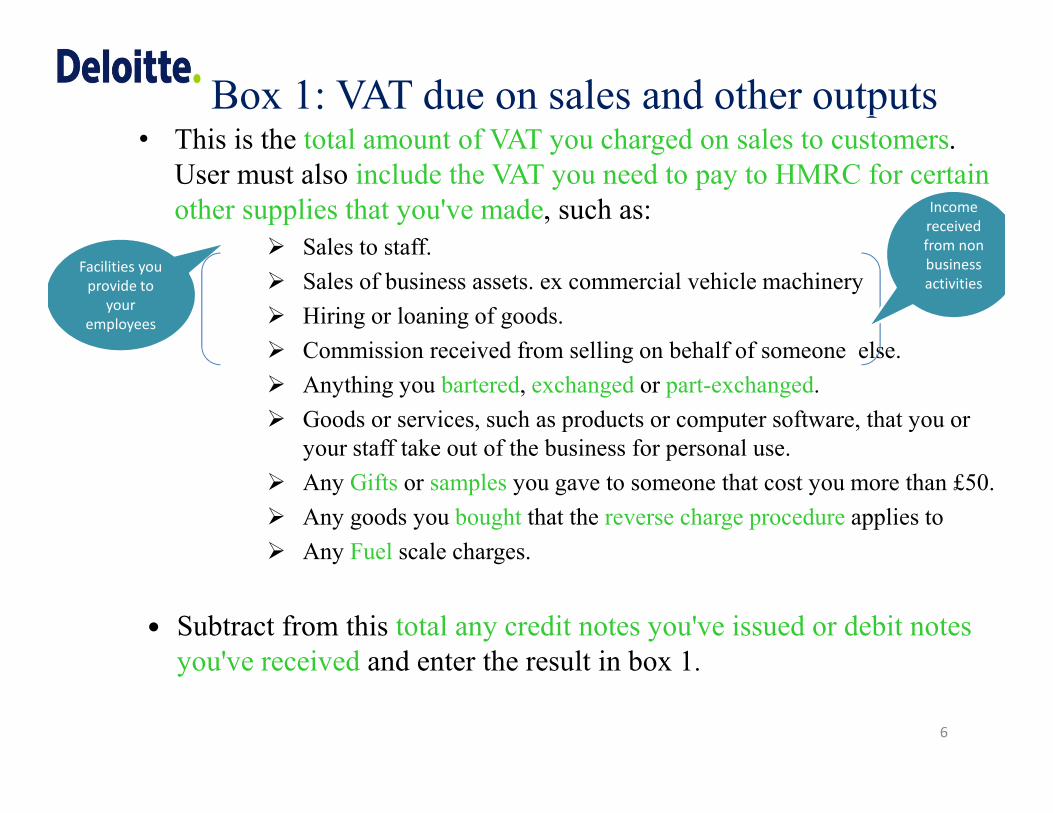

Box 1: VAT due on sales and other outputs• This is the total amount of VAT you charged on sales to customers.

User must also include the VAT you need to pay to HMRC for certain other supplies that you've made, such as:

Ø Sales to staff.Ø Sales of business assets. ex commercial vehicle machineryØ Hiring or loaning of goods.Ø Commission received from selling on behalf of someone else.Ø Anything you bartered, exchanged or part-exchanged.Ø Goods or services, such as products or computer software, that you or

your staff take out of the business for personal use.Ø Any Gifts or samples you gave to someone that cost you more than £50.Ø Any goods you bought that the reverse charge procedure applies toØ Any Fuel scale charges.

� Subtract from this total any credit notes you've issued or debit notes you've received and enter the result in box 1.

Facilities you provide to

your employees

Income received from non business activities

6

Box 2: VAT due from you (but not paid) on acquisitions from other EU countries

• You need to work out the VAT due - but not yet paid by you - on

goods that you buy from other EU countries, and any services

directly related to those goods (such as delivery charges). Put

the figure in box 2.

• You may be able to reclaim this amount, and if so remember to

include this figure in your total in box 4.

7

Box 3: Total VAT due

• This is the total of box 1 and box 2 added together. It is the

amount of VAT that is due to HMRC.

• When you complete your return online, this figure is worked

out automatically for you, based on the information you put in

boxes 1 and 2. You must not enter the total VAT due figure into

box 3 or any other box on your online return.

8

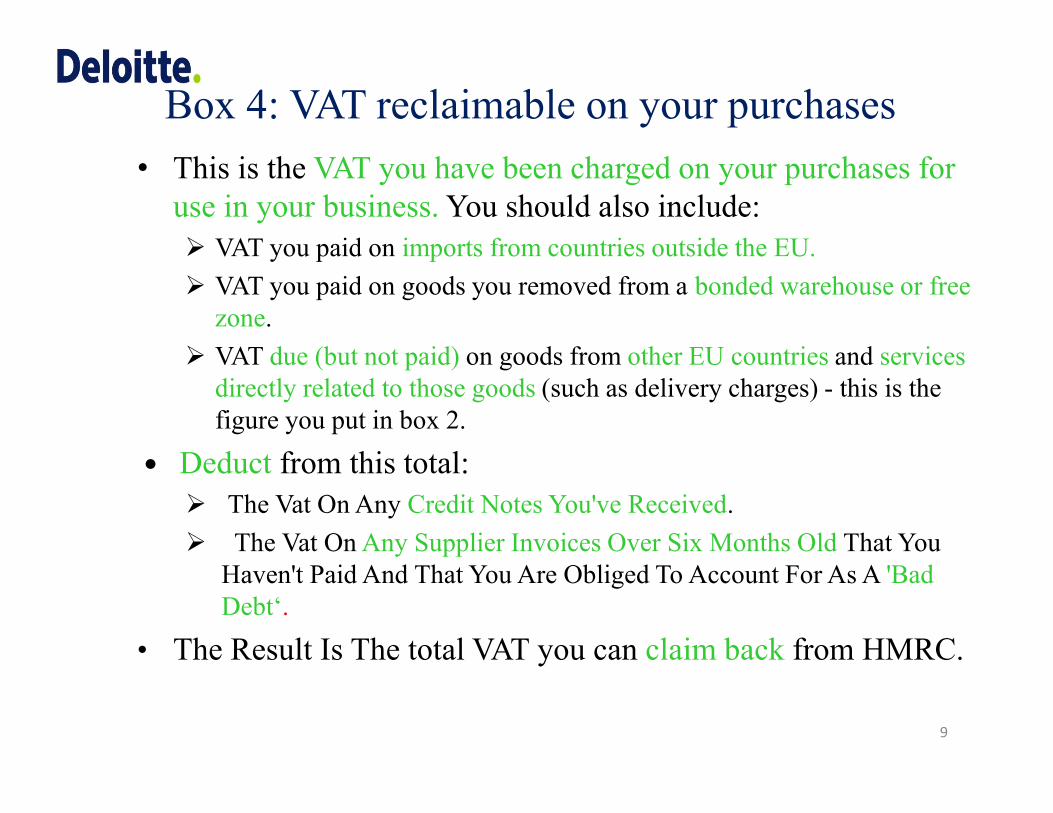

Box 4: VAT reclaimable on your purchases• This is the VAT you have been charged on your purchases for

use in your business. You should also include:Ø VAT you paid on imports from countries outside the EU.Ø VAT you paid on goods you removed from a bonded warehouse or free

zone.Ø VAT due (but not paid) on goods from other EU countries and services

directly related to those goods (such as delivery charges) - this is the figure you put in box 2.

� Deduct from this total:Ø The Vat On Any Credit Notes You've Received.Ø The Vat On Any Supplier Invoices Over Six Months Old That You

Haven't Paid And That You Are Obliged To Account For As A 'Bad Debt‘.

• The Result Is The total VAT you can claim back from HMRC.

9

Box 5: VAT payable or reclaimable

• When you complete your return online, the figure for this box

is worked out automatically for you based on the information

in boxes 3 and 4.

Ø If the amount in box 3 is more than the figure in box 4, you pay

the amount in box 5 to HMRC.

Ø If the amount in box 3 is less than the figure in box 4, you

reclaim the amount in box 5 from HMRC.

Ø If the amount in box 5 is zero, you have no VAT to pay or

reclaim, but you must still submit your return.

10

Box 6: Your total sales excluding VAT

• Enter the total figure for your sales (excluding VAT) for the period, that is, the sales on which you charged the VAT you put in box 1. Additionally, you should also include:Ø Any zero-rated and exempt sales or other supplies you made.Ø Any amount you put in Box 8.Ø Goods or services you have supplied that are subject to the reverse

charge.Ø Goods or services that you have purchased that are subject to the reverse

charge.Ø Exports outside the EU.

� Take off the net amount of any credit notes you issued or debit notes you received.

� Don't include:Ø Loans, dividends and gifts of money.Ø Insurance claims.

� Reverse Charge Sales ListØ If you make reverse charge sales - sales to which a reverse charge is

applied - you must notify HMRC and send in regular Reverse Charge Sales Lists. 11

Box 7: Your total purchases excluding VAT

• Enter the total figure for your purchases (excluding VAT) for

the period, including:

Ø The purchases on which you paid the VAT you put in Box 4.

Ø Anything you bought that the reverse charge procedure applies to.

Ø Any amount you put in Box 9.

• Don't include:

Ø Expenses like salaries and taxes.

Ø Anything outside the scope of VAT like vehicle license's, MOT

certificates and local authority rates

12

Box 8: The total value of goods you supplied to other EU countries

• Put in the total value of goods you supplied to another EU country and services related to those goods (such as delivery charges).

• You may also have to complete an EC Sales List (ESL) for supplies to VAT-registered customers in other EU countries.

• Remember to also include this amount in your Box 6 total.• You should not include in box 8 the value of goods supplied to

customers (including private individuals) who are not registered for VAT where you have not exceeded the 'distance selling' threshold. Each EU country can set its own distance selling threshold which at present £70,000

13

Box 9: The total value of goods you acquired from other EU countries

• Enter the total value of goods you received from VAT

registered suppliers in another EU country and services related

to those goods (such as delivery charges).

• Remember to also include this amount in your Box 7 total.

14

VAT Rules-Traders record requirements

15

Records Required• Following documents are to be maintained and updated on a continuous basis:Ø Business records (bank statements and paying-in slips, accounts books,Ø purchases and sales information)Ø Accounting records(including details of assets, liabilities, income & expenditure).Ø VAT accountØ Copies of all VAT invoices issued and All invoices ReceivedØ Documentation received relating to acquisitions of any goods from other member

StatesØ Copy of documentation issued relating to the transfer, dispatch or transportation

of goods to other member States,Ø Documentation received relating to the transfer, dispatch or transportation of

goods to other member States,Ø Documentation relating to importations and exportations Ø All credit notes, debit notes, or other documents which evidence an increase or

decrease in consideration that are received, and copies of all such documents that are issued.

Ø A copy of any self-billing agreement where he is a customer, party to a self-billing agreement-the name, address and VAT registration number of each supplier with whom he has entered into a self-billing agreement.”

16

Minimum retention periods

S.No. Type of record Minimum period of preservation

1

Sales or service dockets (mainly used by large organisations especially those involved mainly in retail trading e.g. mail order houses). No restriction

2

Copies of orders, delivery notes, dispatch notes, goods returned notes, invoices for expenses incurred by employees. 1 Year

3

Production records, stock records (except those for second hand schemes), job cards, appointment books, diaries, business letters. 1 Year

4Import, export and delivery from warehouse documents. 3 Year

5Daybooks, ledgers, cashbooks, second hand scheme stock books. 3 Year

6Purchase invoices, copy sales invoices, credit notes, debit notes, authenticated receipts. 4 Year

7Daily gross takings records, records related to retail scheme calculations, catering estimates. 4 Year

8Bank statements and paying in books, management accounts, annual accounts. 5 Year

9Electronic Cash Registers (ECR) and Electronic Point of Sale (EPOS) equipment 4 Year

10 Any record containing the VAT account No concession

Minimum retention periods for certain types of record

� Generally all business records that are relevant for VAT must be kept for at least six years. How ever, HMRC may allow to keep some records for a shorter period but not less than:

17

Business and accounting records

• Order and Delivery notes• Relevant business correspondence• Purchase invoice from suppliers• Credit notes• Cash records and till roles• Bank Statements and Pay in slips• Annual accounts/general ledger• Other account books

18

VAT account• Provides the link between business records and VAT Return.• Account shows the cumulative VAT in your sales and purchases

records which are then recorded in VAT account using separate headings for VAT payable and VAT reclaimable/deductible.

• Records under the heading of output tax:Ø The output tax owe on sales.Ø The output tax owe on acquisitions from other EU member states.Ø The tax that is required to be paid on behalf of your supplier under a

reverse charge procedure.Ø Tax that needs to be paid following a correction or error adjustment.Ø Any other adjustment required by VAT rules.

• Records under the heading of input tax:Ø The input tax you are entitled to claim from business purchases.Ø The input tax allowable on acquisitions from other EU member states.Ø Tax that you are entitled to following a correction or error adjustment.Ø Any other necessary adjustment. 19

Adjusting the VAT account• Different adjustment to VAT account:

Ø Allow or receive a credit which includes VAT.

Ø Retail scheme annual adjustment.

Ø Are using an approved estimation procedure like in annual

accounting scheme.

Ø Partial exemption or capital goods scheme adjustment .

Ø Claim for bad debt relief, or

Ø Correct a net error of £2,000 or less made on previous returns.

20

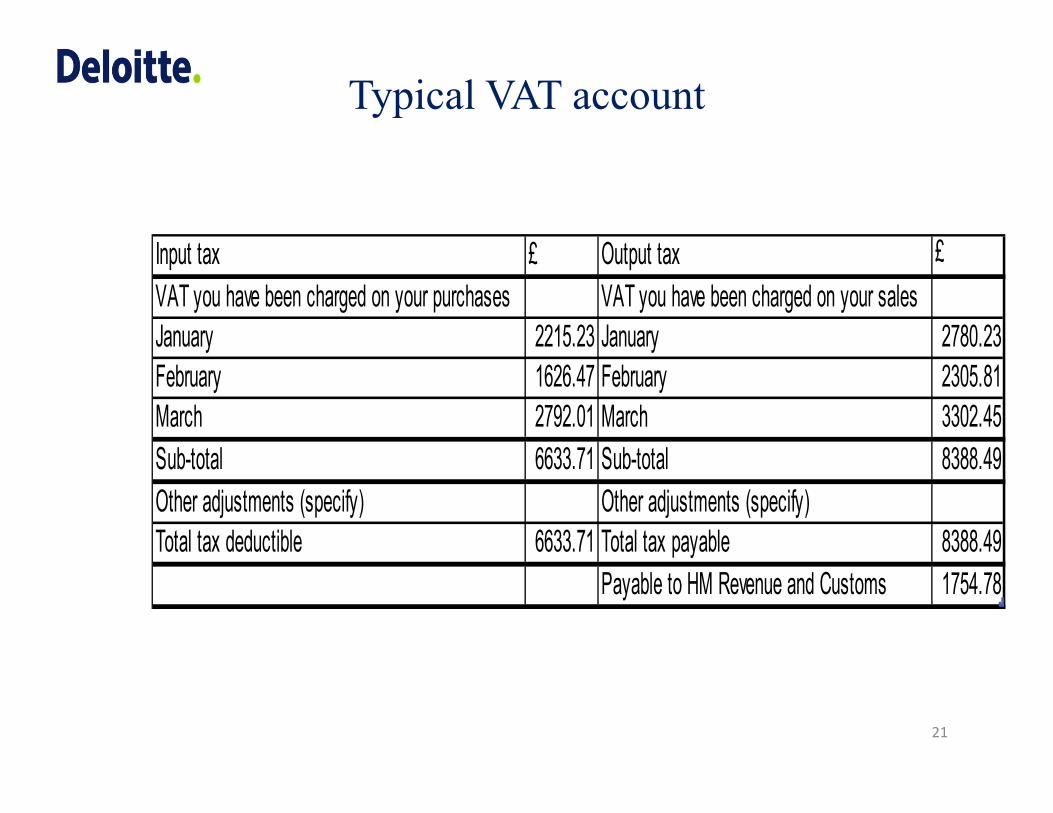

Typical VAT account

Input tax £ Output tax £2VAT you have been charged on your purchases VAT you have been charged on your salesJanuary 2215.23 January 2780.23February 1626.47 February 2305.81March 2792.01 March 3302.45Sub-total 6633.71 Sub-total 8388.49Other adjustments (specify) Other adjustments (specify)Total tax deductible 6633.71 Total tax payable 8388.49

Payable to HM Revenue and Customs 1754.78

21

VAT invoices • Only VAT registered businesses can/must issue a VAT

invoice whenever you supply standard-rate or reduced rate

goods or services to another VAT registered person.

• Normally you must issue a VAT invoice within 30 days of

the date you make the supply.

• There is no requirement to issue a VAT invoice for retail

supplies of less than €250 to unregistered businesses unless

the customer asks for one.

22

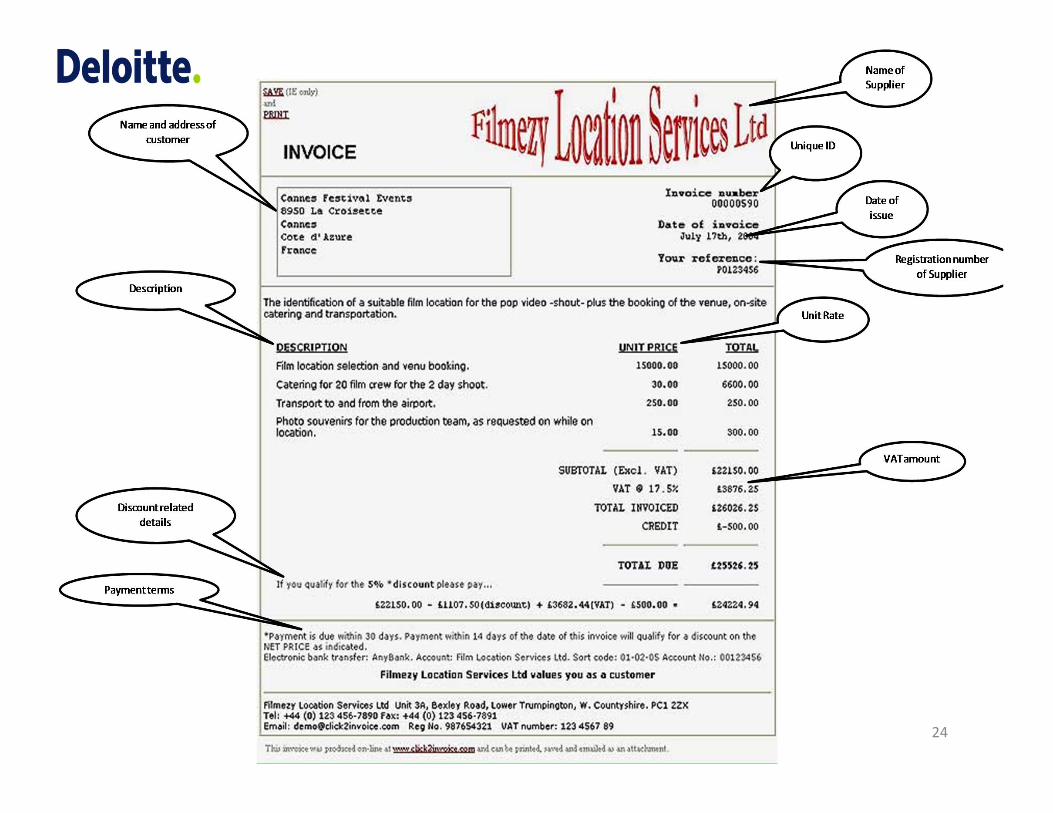

VAT invoices: what they must show• For transaction between one registered person to another registered person:Ø A sequential number based on one or more series which uniquely identifies the

document.Ø The time of the supply .Ø The date of issue of the document (where different to the time of supply) .Ø The name, address and VAT registration number of the supplier .Ø The name and address of the person to whom the goods or services are supplied .Ø A description sufficient to identify the goods or services supplied .Ø For each description, the quantity of the goods or the extent of the services, and

The rate of VAT and the amount payable, excluding VAT, expressed in any currency .

Ø The gross total amount payable, excluding VAT, expressed in any currency .Ø The rate of any cash discount offered .Ø The total amount of VAT chargeable, expressed in sterling .Ø The unit price .Ø The reason for any zero rate of exemption.

• In addition, for Invoices to other EU Member StatesØ The letters ‘GB’ in front of your registration number for cross border supplies .Ø The registration number of the recipient of the supply preceded by the alphabetical

code of the relevant EU Member State.23

24

Concept of time of supply

• The tax point, or time of supply, is the date when a sale is considered to take place for VAT purposes.

• Time of supply for transactions when no VAT invoice is issued

• Time of supply for transactions when VAT invoice is issued

Date full payment received Time of supplyBefore the date the supply takes place The date the payment is receivedOn the day when the supply takes place The date the supply takes placeAfter the date when the supply takes place The date the supply takes place

Date invoice is issued Time of supply (tax point)Before, On or Between 1 and 14 days after the date the supply takes place The date the invoice is issued

15 or more days after the date the supply takes place

The date the supply takes place (unless the supplier has permission from HMRC to move the time of supply to more than 14 days afterwards - in which case it will be the date of the invoice)

25

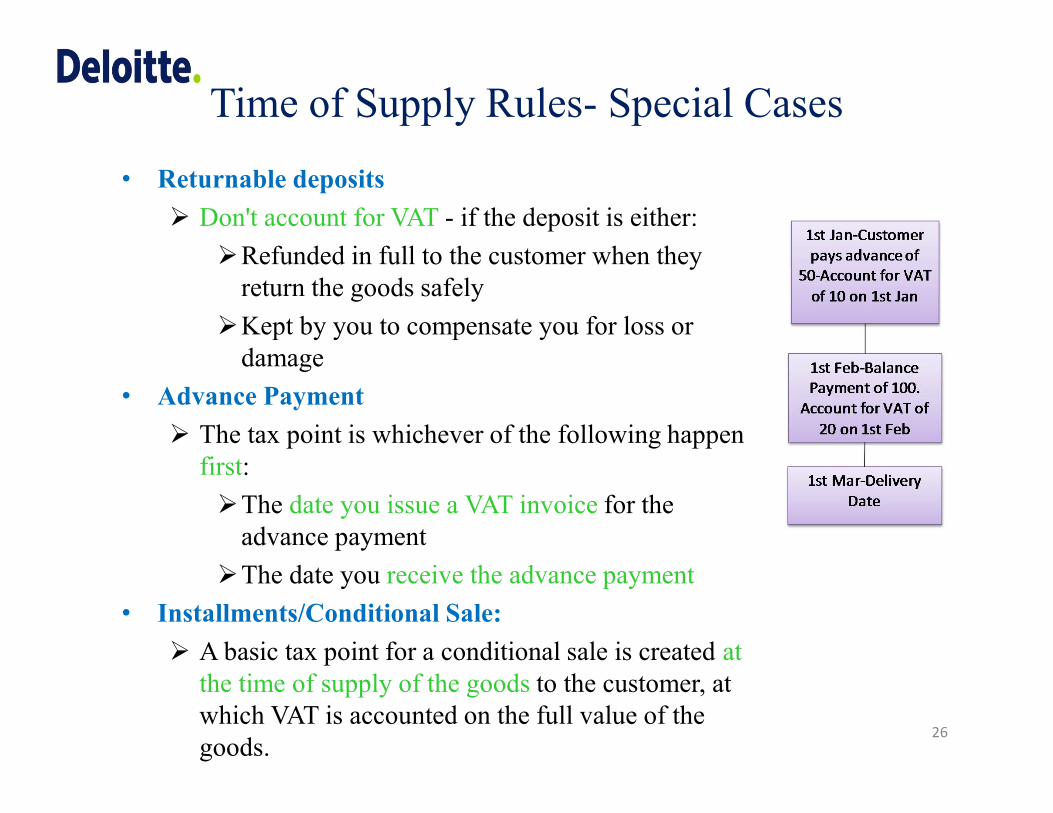

Time of Supply Rules- Special Cases

• Returnable deposits Ø Don't account for VAT - if the deposit is either: ØRefunded in full to the customer when they

return the goods safelyØKept by you to compensate you for loss or

damage• Advance PaymentØ The tax point is whichever of the following happen

first:ØThe date you issue a VAT invoice for the

advance paymentØThe date you receive the advance payment

• Installments/Conditional Sale:Ø A basic tax point for a conditional sale is created at

the time of supply of the goods to the customer, at which VAT is accounted on the full value of the goods.

26

Register of temporary movement of goods to and from other member States.

• For the temporary movements of goods between member states, following records have to be maintained:Ø The date of removal of goods to another member State,Ø The date of receipt of the goods mentioned when they are returned from

the member State.Ø The date of receipt of goods from another member State,Ø The date of removal of the goods when they are returned to the member

StateØ A description of the goods sufficient to identify them.Ø A description of any process, work or other operation carried out on the

goods either in the United Kingdom or in another member State,Ø The consideration for the supply of the goods, andØ The consideration for the supply of any processing, work or other

operation carried out on the goods either in the United Kingdom or another member State.

27

Concept of self-billing

• A self-billing arrangement is where a customer prepares VAT invoices on behalf of their VAT-registered supplier.

• Conditions for self billing:Ø Enter into an agreement with each supplier.Ø Review agreements with suppliers at regular intervals.Ø Keep records of each of the suppliers who let you self-bill

them.Ø Make sure invoices contain the right information and are

correctly issued.

28

Thank You

29

VAT in Netherlands

By Vikas MarwahaManoj Singh

1

VAT Rates

Rates ExampleStandard-19% Most goods and services.Reduced-6% Food and beverage not alcohol, Water,

Pharmaceutical Products, Books, passenger transport, Entertainment.

Zero Rated-0% Export and intra community EU supplies.Exempt Banking/Insurances, property sector ,

medical services, Certain Education.

2

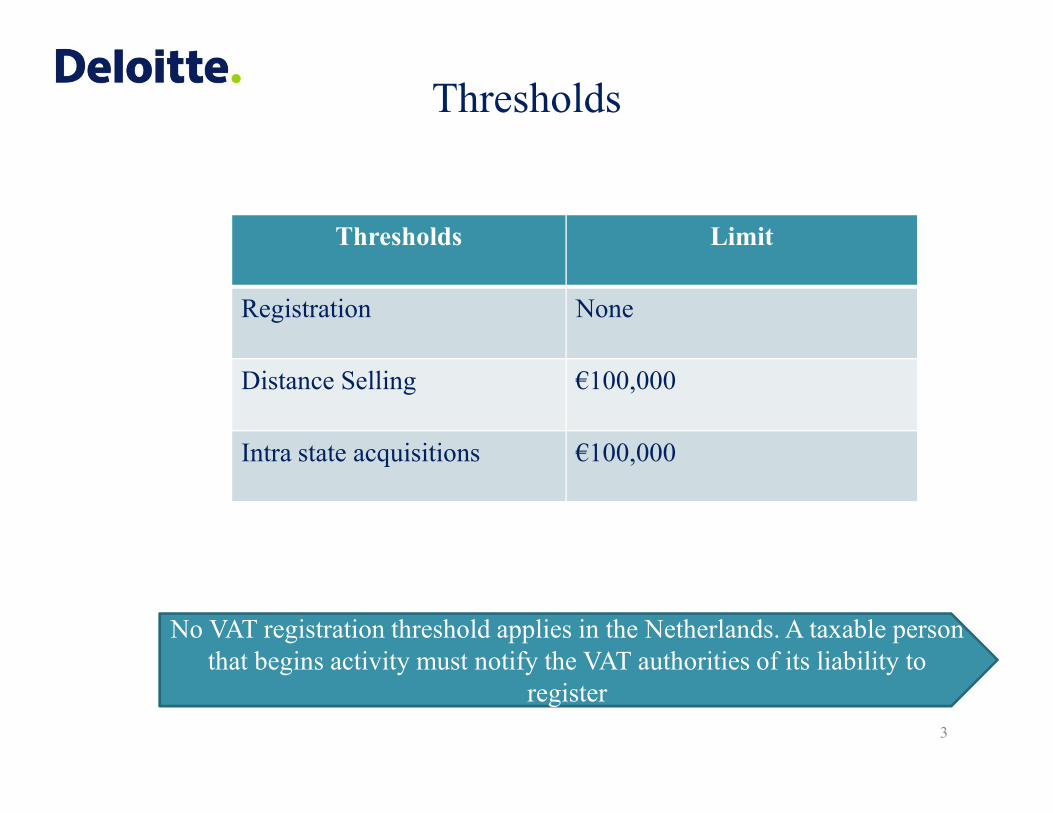

Thresholds

Thresholds Limit

Registration None

Distance Selling €100,000

Intra state acquisitions €100,000

.No VAT registration threshold applies in the Netherlands. A taxable person

that begins activity must notify the VAT authorities of its liability to register

3

Scope of Tax

• VAT applies to the following transactions:

The supply of goods or services made in the Netherlands by a taxable person.

The intra-Community acquisition of goods from another EU member state by a taxable person.

The intra-Community acquisition of goods from another EU member state by a nontaxable legal person in excess of the annual threshold.

Reverse-charge services received by a taxable person and nontaxable legal entities in the Netherlands.

The importation of goods from outside the EU, regardless of the status of the importer.

4

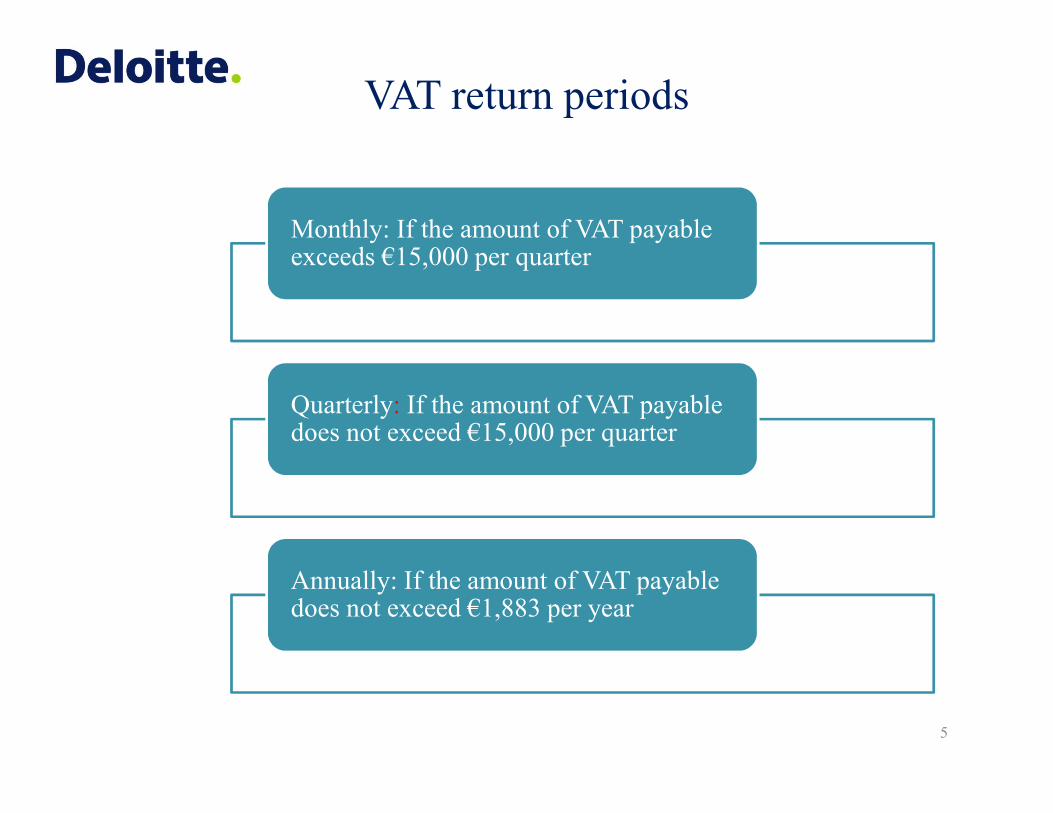

VAT return periods

Monthly: If the amount of VAT payable exceeds €15,000 per quarter

Quarterly: If the amount of VAT payable does not exceed €15,000 per quarter

Annually: If the amount of VAT payable does not exceed €1,883 per year

5

Who are liable

• A taxable person “is any business entity or individual thatmakes taxable supplies of goods or services, or intra-Community acquisitions or distance sales, in the course of abusiness, in the Netherlands”

• Taxable activities also include “carrying on a profession” or the“exploitation of tangible or intangible property in order toobtain income on a continuing basis.”

• Special rules apply to foreign or “non established” businesses.

6

Group Registration

• Taxable persons established in the Netherlands may form a VATgroup if the members are closely bound by “financial, economicand organizational links“. For legal certainty, it is recommendedthat persons meeting the conditions for group registrationinform the Tax Office.

• The effect of VAT grouping is to treat the members as a singletaxable person. As a result, transactions between members ofthe VAT group are disregarded for VAT purposes. Members of aDutch VAT group may file a single VAT return, or membersmay elect to file individually. Each member of a VAT group isjointly and severally liable for all VAT due.

7

Non-established businesses

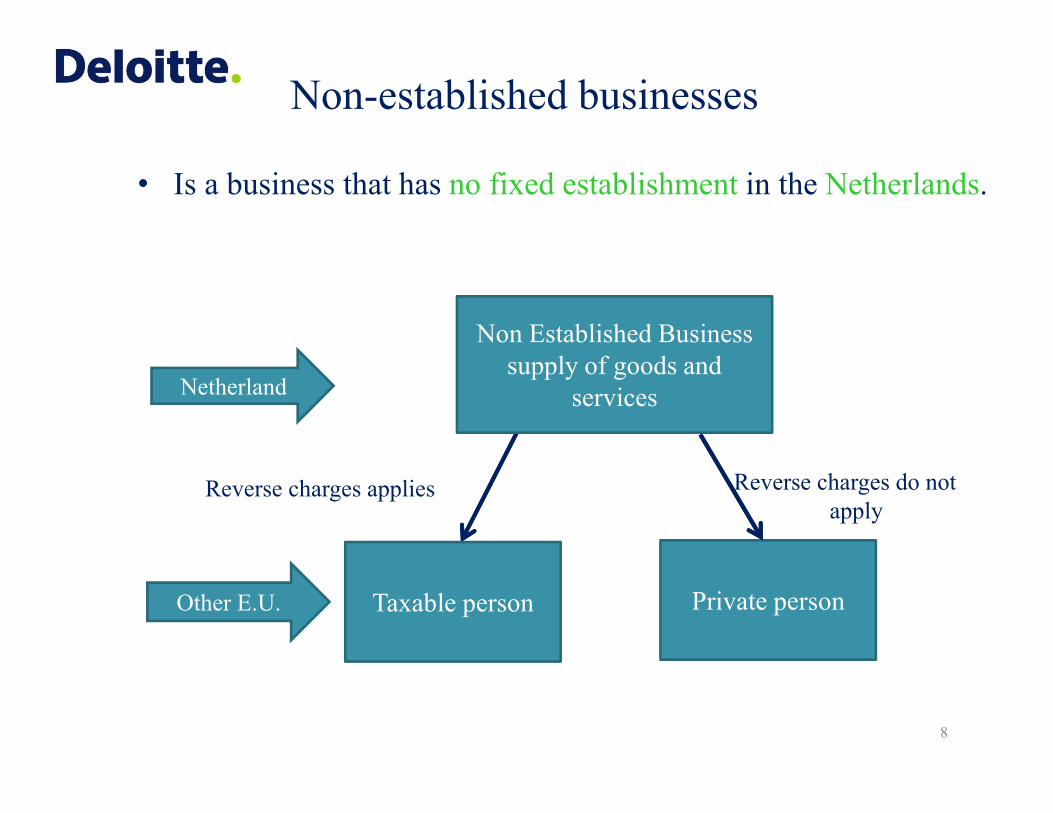

• Is a business that has no fixed establishment in the Netherlands.

Netherland

Private person

Reverse charges applies Reverse charges do notapply

Non Established Business supply of goods and

services

Taxable personOther E.U.

8

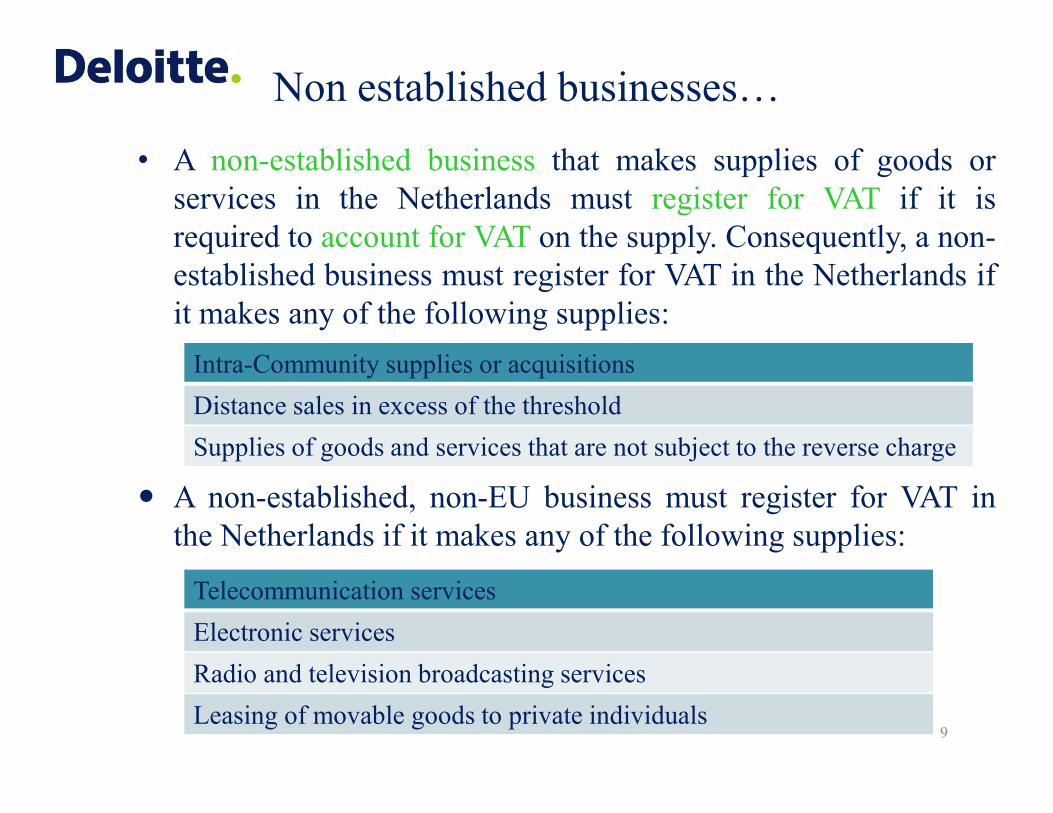

Non established businesses…• A non-established business that makes supplies of goods or

services in the Netherlands must register for VAT if it isrequired to account for VAT on the supply. Consequently, a non-established business must register for VAT in the Netherlands ifit makes any of the following supplies:

� A non-established, non-EU business must register for VAT inthe Netherlands if it makes any of the following supplies:

Intra-Community supplies or acquisitionsDistance sales in excess of the thresholdSupplies of goods and services that are not subject to the reverse charge

Telecommunication servicesElectronic servicesRadio and television broadcasting servicesLeasing of movable goods to private individuals

9

VAT Recovery• Input tax is generally recovered by being deducted from output

tax, which is VAT charged on supplies made.• Input tax includes:

• A valid tax invoice or customs document must be kept in theaccounts to support a claim for input tax.

• Non deductible input tax. Input tax may not be recovered onpurchases of goods and services that are not used for businesspurposes.

VAT charged on goods and services supplied in the Netherlands,VAT paid on imports of goods andVAT self-assessed on the intra-Community acquisition of goods and Reverse-charge services

A maximum limit of €227 annually applies to the value of expenses incurred per employee on which input VAT may be recovered,

10

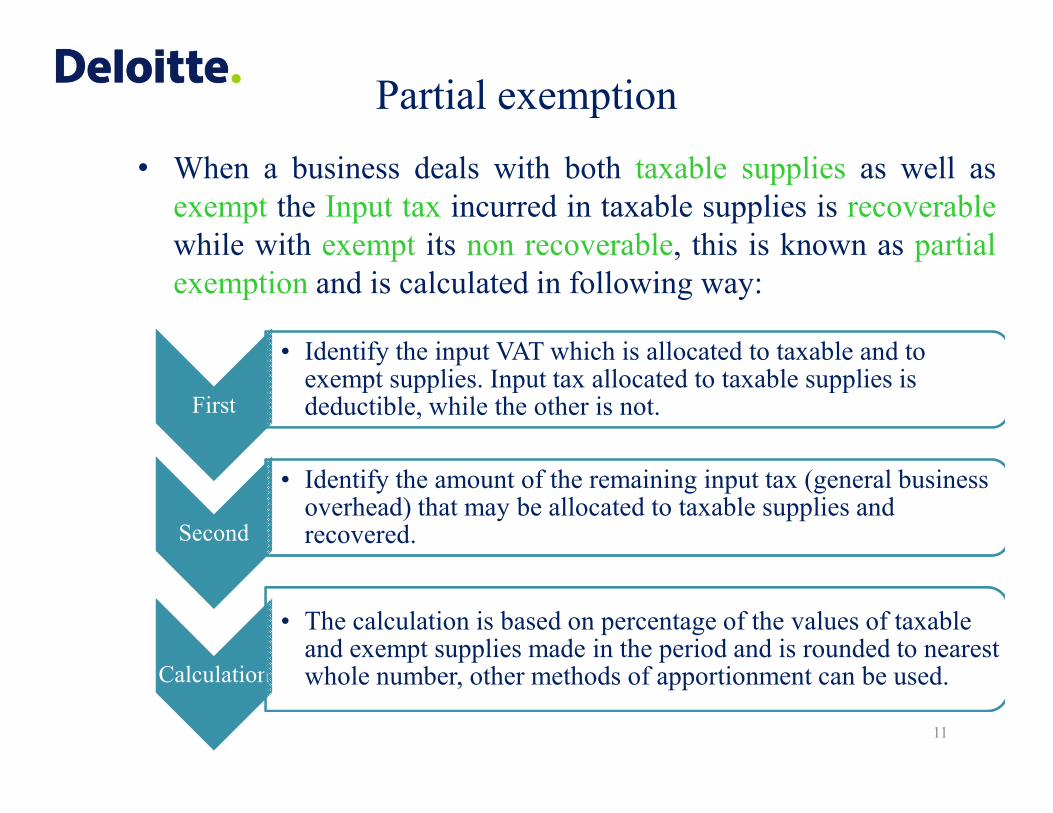

Partial exemption• When a business deals with both taxable supplies as well as

exempt the Input tax incurred in taxable supplies is recoverablewhile with exempt its non recoverable, this is known as partialexemption and is calculated in following way:

First

• Identify the input VAT which is allocated to taxable and to exempt supplies. Input tax allocated to taxable supplies is deductible, while the other is not.

Second

• Identify the amount of the remaining input tax (general business overhead) that may be allocated to taxable supplies and recovered.

Calculation

• The calculation is based on percentage of the values of taxable and exempt supplies made in the period and is rounded to nearest whole number, other methods of apportionment can be used.

11

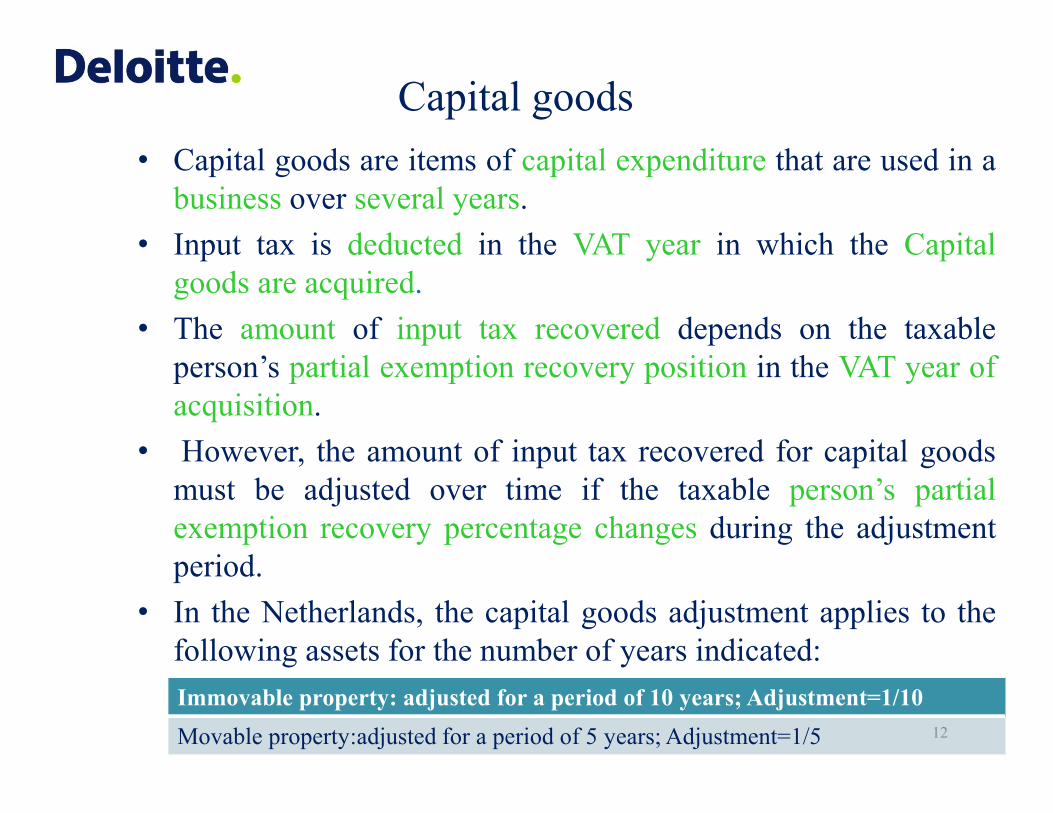

Capital goods• Capital goods are items of capital expenditure that are used in a

business over several years.• Input tax is deducted in the VAT year in which the Capital

goods are acquired.• The amount of input tax recovered depends on the taxable

person’s partial exemption recovery position in the VAT year ofacquisition.

• However, the amount of input tax recovered for capital goodsmust be adjusted over time if the taxable person’s partialexemption recovery percentage changes during the adjustmentperiod.

• In the Netherlands, the capital goods adjustment applies to thefollowing assets for the number of years indicated:Immovable property: adjusted for a period of 10 years; Adjustment=1/10Movable property:adjusted for a period of 5 years; Adjustment=1/5 12

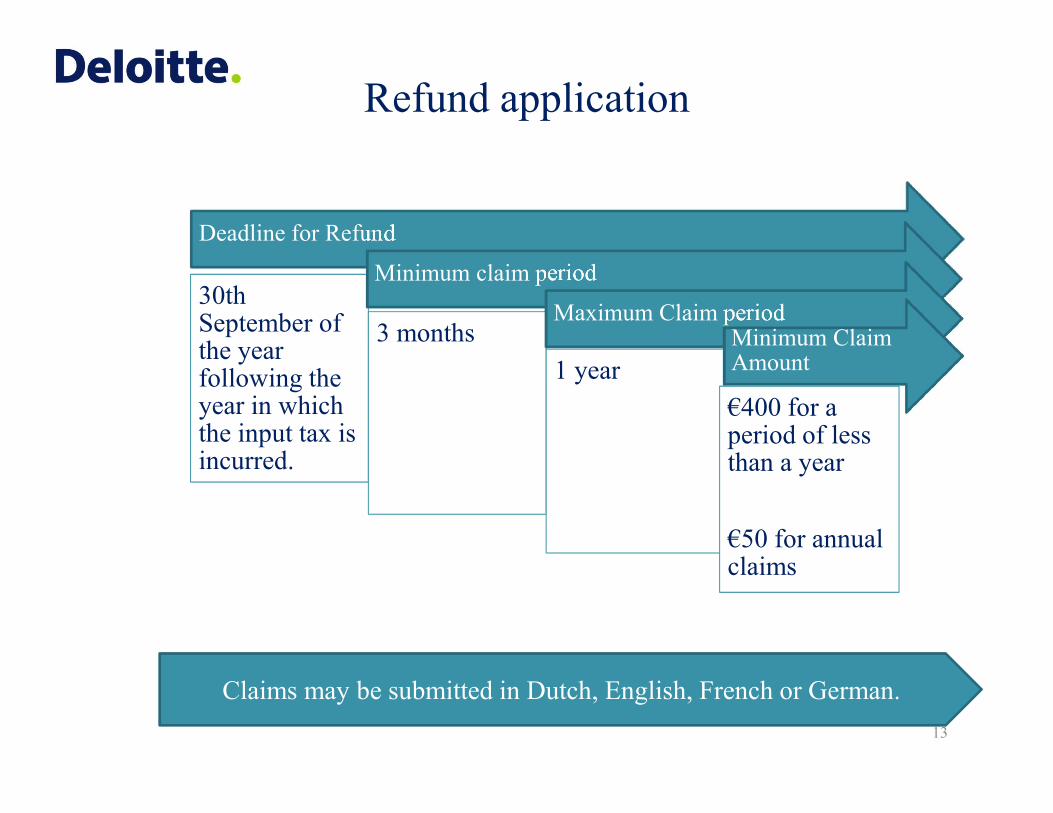

Refund application

Deadline for Refund

30th September of the year following the year in which the input tax is incurred.

Minimum claim period

3 monthsMaximum Claim period

1 yearMinimum Claim Amount

€400 for a period of less than a year

€50 for annual claims

Claims may be submitted in Dutch, English, French or German. 13

Repayment interest

� VAT Refund: Registered person/entity can claim VAT back on the purchases made for the business

• Time limit for Refund: 4 months and 10 days after the date on which the refund claim is submitted.

• In the case of a late refund, the claimant is entitled to interest at the government interest rate in force at the time, in addition to the repayment.

14

Invoicing• VAT invoices:

Ø A taxable person must generally provide a VAT invoice for all taxable supplies made, including exports and intra-Community supplies.

Ø A VAT invoice is required to support a claim for input tax deduction or a refund

Ø Invoices are not automatically required for retail transactions, unless requested by the customer. However, the issuance of invoices for wholesalers is required.

• Retention Period:Ø Taxable persons must retain invoices for 7 years.Ø For real estate, a taxable person must retain the invoice for 10

years.• VAT Credit Note:

Ø A VAT credit note may be used to reduce the VAT charged and reclaimed on a supply. It must be cross-referenced to the original VAT invoice.

15

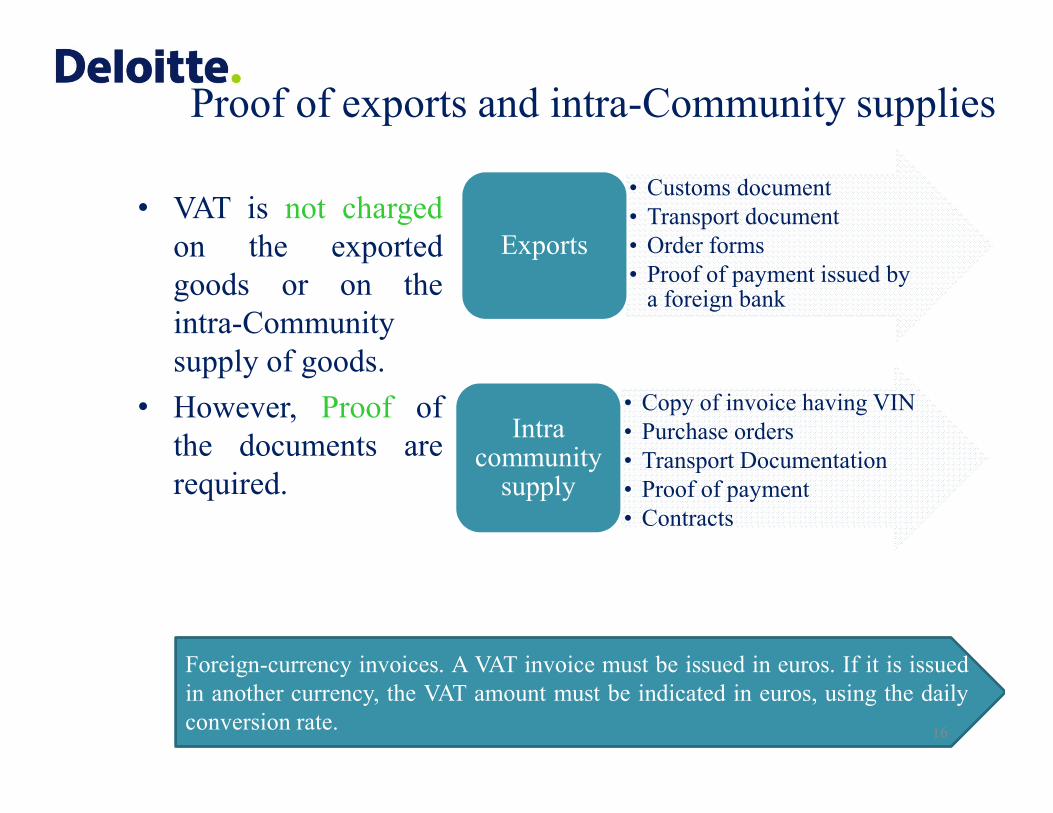

Proof of exports and intra-Community supplies

• VAT is not chargedon the exportedgoods or on theintra-Communitysupply of goods.

• However, Proof ofthe documents arerequired.

• Customs document• Transport document• Order forms• Proof of payment issued by

a foreign bank

Exports

• Copy of invoice having VIN• Purchase orders• Transport Documentation• Proof of payment• Contracts

Intra community

supply

Foreign-currency invoices. A VAT invoice must be issued in euros. If it is issuedin another currency, the VAT amount must be indicated in euros, using the dailyconversion rate. 16

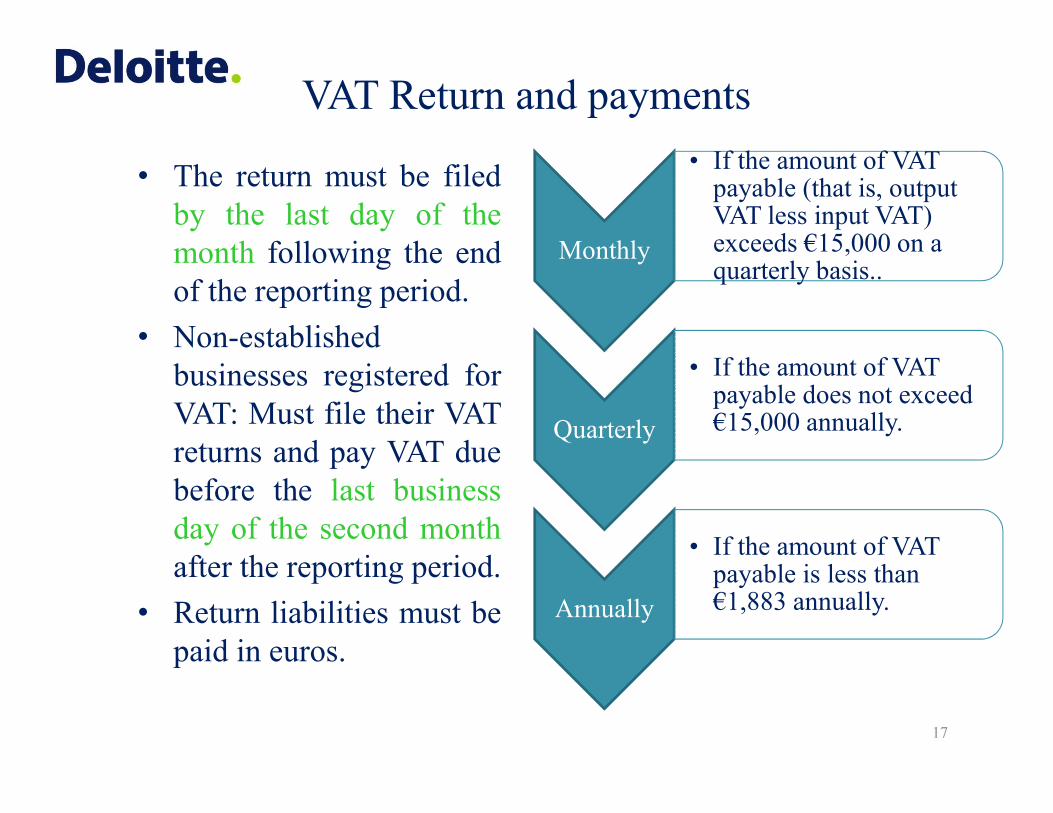

VAT Return and payments

• The return must be filedby the last day of themonth following the endof the reporting period.

• Non-establishedbusinesses registered forVAT: Must file their VATreturns and pay VAT duebefore the last businessday of the second monthafter the reporting period.

• Return liabilities must bepaid in euros.

Monthly

• If the amount of VAT payable (that is, output VAT less input VAT) exceeds €15,000 on a quarterly basis..

Quarterly

• If the amount of VAT payable does not exceed €15,000 annually.

Annually

• If the amount of VAT payable is less than €1,883 annually.

17

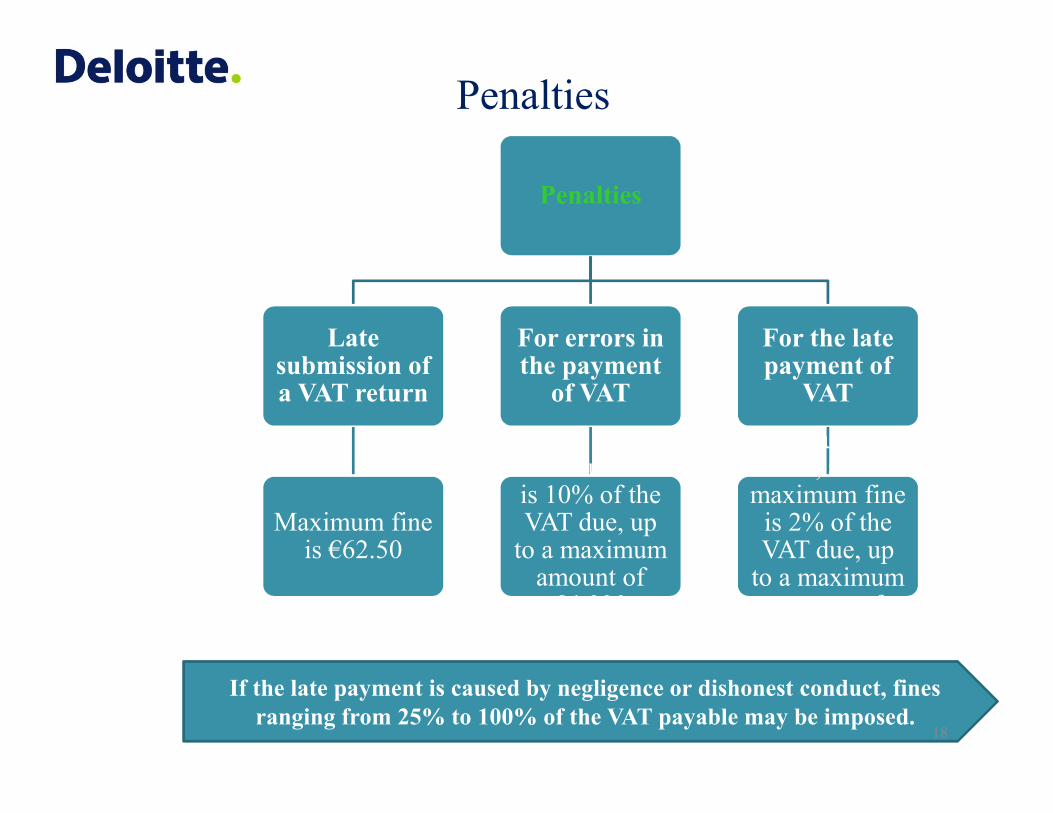

Penalties

Penalties

Late submission of a VAT return

Maximum fine is €62.50

For errors in the payment

of VAT

Maximum fine is 10% of the VAT due, up

to a maximum amount of

€4,920

For the late payment of

VAT

Minimum fine is €50, and the maximum fine

is 2% of the VAT due, up

to a maximum amount of

€4,920.

If the late payment is caused by negligence or dishonest conduct, fines ranging from 25% to 100% of the VAT payable may be imposed.

18

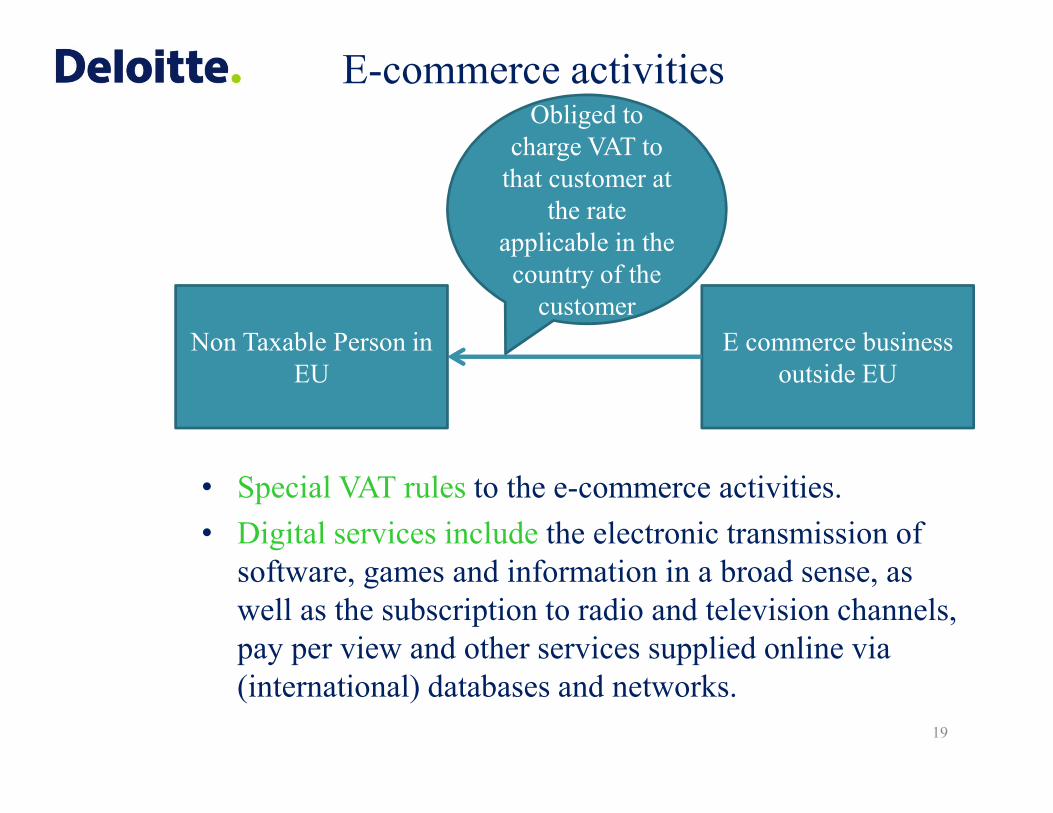

E-commerce activities

• Special VAT rules to the e-commerce activities.• Digital services include the electronic transmission of

software, games and information in a broad sense, as well as the subscription to radio and television channels, pay per view and other services supplied online via (international) databases and networks.

E commerce business outside EU

Non Taxable Person in EU

Obliged to charge VAT to

that customer at the rate

applicable in the country of the

customer

19

Export and Import

mport6

When you purchase goods from outside EU, these goods are subject to VAT at the moment the goods are imported in The Netherlands.When you import goods from a supplier in another EU member state the goods will in general be subject to Dutch VAT.

Export

Import

Supplies of goods to customers outside the EU are in general not subject to VAT. For supply of goods to customers (entrepreneurs) in other EU member states (so called intra community supply) conditionally you are entitled to the 0%-rate.

20

Time of supply• The time when VAT becomes due is called the “time of supply”. • The time of supply for goods is when the goods are delivered. • The time of supply for services is when the service is completed

• In the Netherlands, an invoice must be issued before the 15th day of the month following the month in which the supply takes place. The actual tax point becomes the date on which the invoice is issued.

• However, if no invoice is issued, tax becomes due, at the latest, on the day on which the invoice should have been issued.

• If the purchaser is not a taxable person, the tax becomes due on the date of the supply.

• If the consideration is paid in full, or in part, before the invoice is issued, the actual tax is due on the date on which payment is received (for the amount received).

However, some taxable persons are permitted to account for VAT on a cash basis (cash accounting). If cash accounting is used, the tax point is the date on which the payment is received. 21

Time of Supply…

• If the consideration in installments or makes a prepayment, the supplier must issue an invoice for each installment .The TOS is the date of the invoice.

Prepayments

• The TOS is the 15th day of the month following the month in which the acquisition occurred. If the supplier issues an invoice before this date, the time of supply is when the invoice is issued.

Intra-Community acquisitions

• The TOS is the date of importation or the date on which the goods leave a duty suspension regime. However the payment can be delayed if taxable person applies for postponed accounting where import VAT is reported on person’s VAT return.

Imported goods and postponed accounting

A non-established business must appoint a tax representative resident in the Netherlands to use the postponed accounting facility. 22

Point of supply in services• Whether you owe VAT when rendering these services depends on

whether the services is rendered in Netherlands.

• The following services, amongst others, are excepted from this rule:• Services related to immovable property are considered according

to destination principle.• Services related to culture, sports, education, entertainment are

considered according to destination principle.• Consultancy, advertising and employment services are considered

according to origin principle.• Intra-Community freight transport is considered to take place at

the point where the journey commences. If the customer has a VAT identification number issued by a Member State other than the Netherlands, the point of supply is considered to be in the other Member State.

Services are liable for Dutch VAT only if they are performed in the Netherlands. The basic rule is that services are provided at the place where the supplier is either resident or established.

23

Point of supply in services…• However, if the VAT owed is levied from the buyer of the

services the supplier will not owe any VAT.

• Example-Ø The buyer of the service is an entrepreneur who is based in

the Netherlands or has a permanent establishment in the Netherlands; or

Ø The buyer of the service is a corporate body based in the Netherlands.

If you perform services in the Netherlands as a non-resident entrepreneur, you do not normally have to deal with VAT, because the

levy of VAT is often transferred to the buyer of the service.

If you are a non-resident entrepreneur supplying services in the Netherlands,(as the customer is a private individual;) and you need to

pay VAT yourself.

24

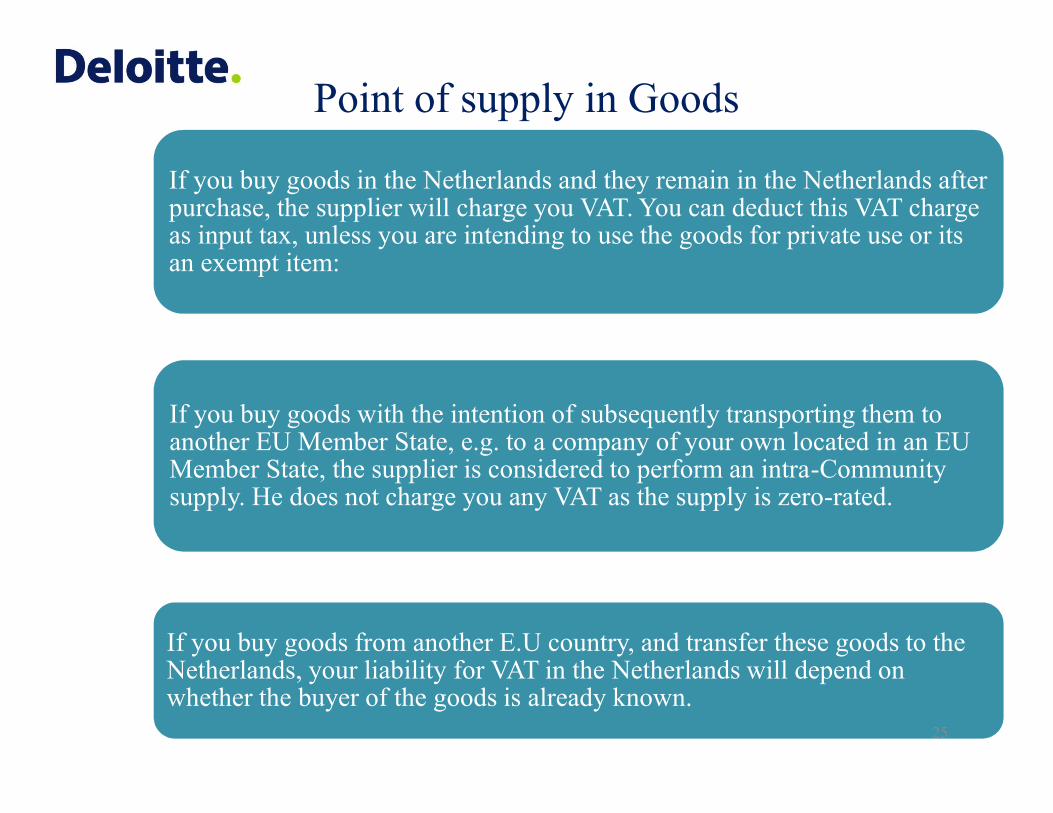

Point of supply in Goods

If you buy goods in the Netherlands and they remain in the Netherlands after purchase, the supplier will charge you VAT. You can deduct this VAT charge as input tax, unless you are intending to use the goods for private use or its an exempt item:

If you buy goods with the intention of subsequently transporting them to another EU Member State, e.g. to a company of your own located in an EU Member State, the supplier is considered to perform an intra-Community supply. He does not charge you any VAT as the supply is zero-rated.

If you buy goods from another E.U country, and transfer these goods to the Netherlands, your liability for VAT in the Netherlands will depend on whether the buyer of the goods is already known.

25

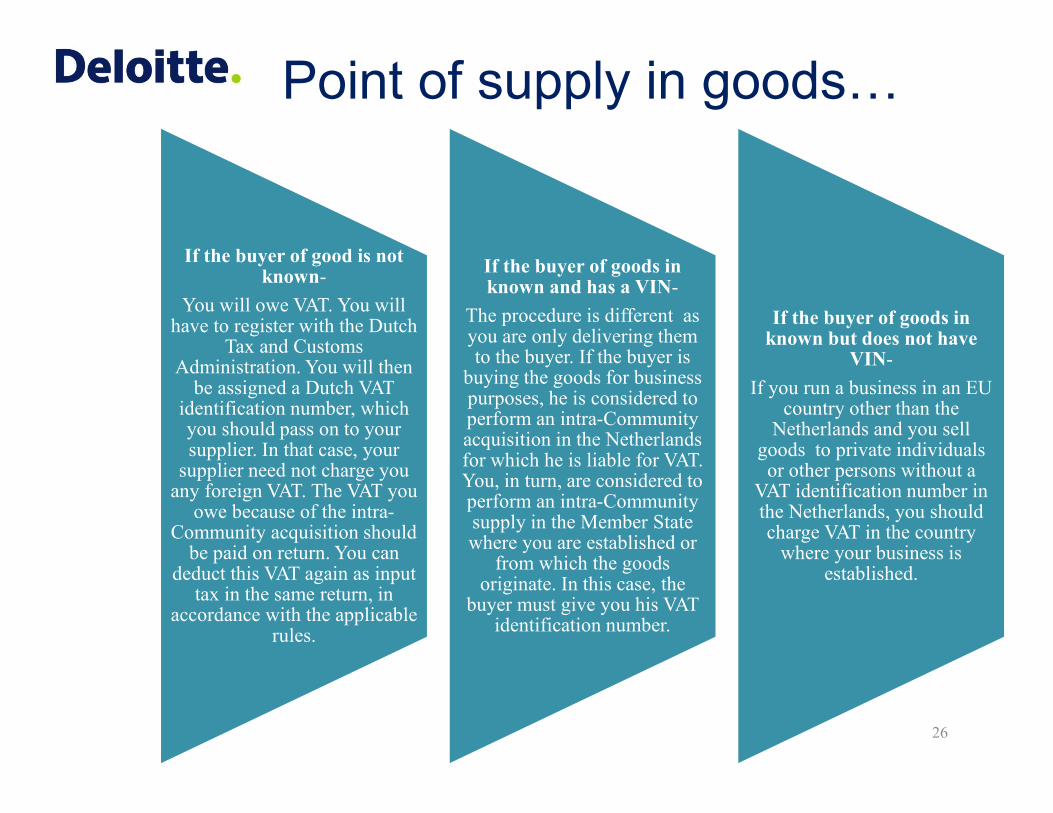

Point of supply in goods…

If the buyer of good is not known-

You will owe VAT. You will have to register with the Dutch

Tax and Customs Administration. You will then

be assigned a Dutch VAT identification number, which you should pass on to your supplier. In that case, your

supplier need not charge you any foreign VAT. The VAT you

owe because of the intra-Community acquisition should

be paid on return. You can deduct this VAT again as input

tax in the same return, in accordance with the applicable

rules.

If the buyer of goods in known and has a VIN-

The procedure is different as you are only delivering them to the buyer. If the buyer is

buying the goods for business purposes, he is considered to perform an intra-Community acquisition in the Netherlands for which he is liable for VAT. You, in turn, are considered to perform an intra-Community supply in the Member State where you are established or

from which the goods originate. In this case, the

buyer must give you his VAT identification number.

If the buyer of goods in known but does not have

VIN-If you run a business in an EU

country other than the Netherlands and you sell

goods to private individuals or other persons without a

VAT identification number in the Netherlands, you should charge VAT in the country

where your business is established.

26

Distance sales

• If you meet the following two conditions, however, you are performing distance sales and should pay VAT in the Netherlands on these sales:– You deliver the goods to the buyer in the Netherlands. You

can do this yourself, but also instruct another business to do this on your behalf. The main point is that the goods were transported by you or at your expense.

– The total amount of the sales to Dutch private individuals or other persons without a VAT identification number during a calendar year should exceed € 100,000.

If you run a business in an EU country other than the Netherlands and you sell goods to private individuals or other persons without a VAT identification number, you should charge VAT in the country where your business is established.

27

A Case in point of supply

• You buy goods in China and import them into the Netherlands. You then transfer the goods to a business of your own in France.

• This means that the import of the goods into the Netherlands is followed by an intra-Community supply.

• You are required to declare the intra-Community supply in the Netherlands, but may at the same time deduct the VAT you were charged on the import transaction.

• You are also required to submit a Declaration of Intra-Community Supplies for the quarter in which you transferred the goods to your own business in France.

• You should state your French firm's VAT identification number in this Declaration.

28

Thank You

29

VAT in PeopleSoft

ByVikas Marwaha

Manoj Singh1

VAT automation through PeopleSoft

Recording

Charging VAT to customers, Paying VAT to suppliers and recording VAT collected VAT paid.

Calculating

Determining recoverable VAT paid on purchases to offset the amount of output VAT that must be sent to VAT authorities.

Accounting

Accounting for and reporting both the VAT paid on purchases and the VAT collected on sales.

2

4P concept for VAT automation

• Determine taxregime.

• Applicabletaxes.

• Tax status andrate.

• Taxable basis.• Calculating

tax amount

Process (Sales/Purchase/

acquisition)

Parties (VAT registered/Not

registered)

Product (Goods/Service)

Places (within EU/outside EU)

3

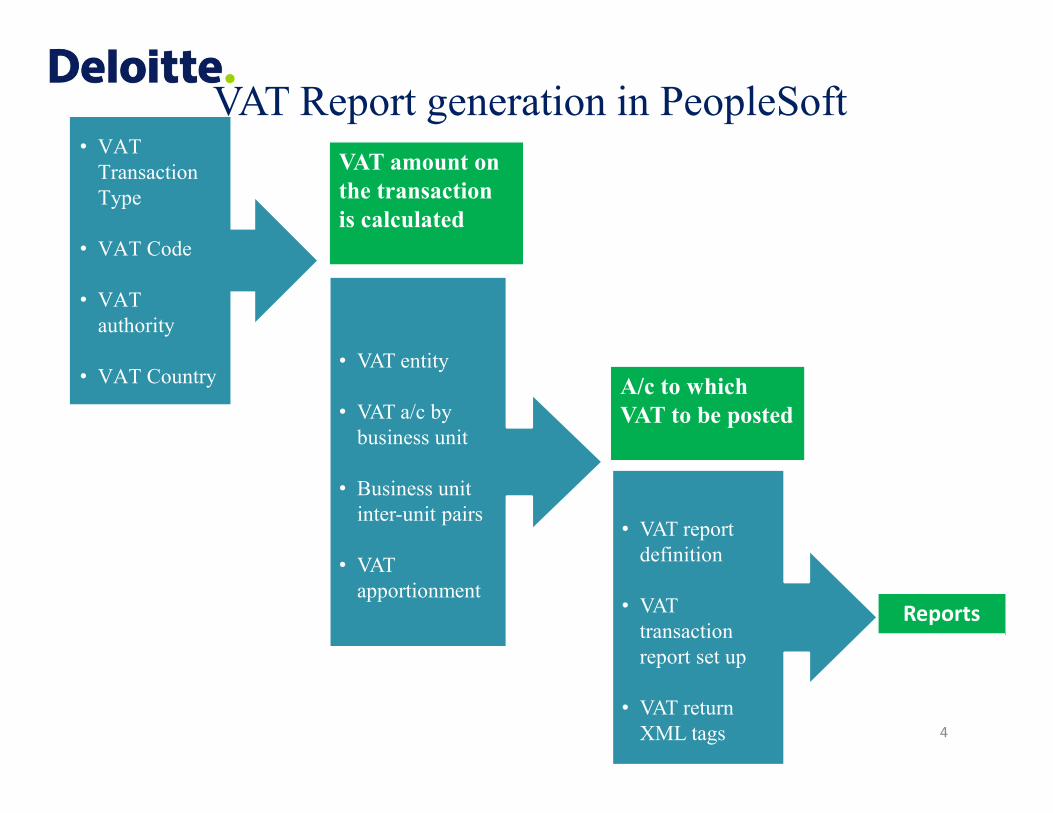

VAT Report generation in PeopleSoft• VAT

Transaction Type

• VAT Code

• VAT authority

• VAT Country• VAT entity

• VAT a/c by business unit

• Business unit inter-unit pairs

• VAT apportionment

VAT amount on the transaction is calculated

• VAT report definition

• VAT transaction report set up

• VAT return XML tags

A/c to which VAT to be posted

Reports

4

VAT configuration in PeopleSoft

Generate VAT reports

Load the VAT transaction table

Define VAT on inter-unit transactions

Establish VAT defaults

Define VAT use types and apportionment

Set up VAT entities

Define VAT countries

Set up VAT authorities and tax codes

Define VAT transaction types

5

Define VAT transaction types

• VAT transaction types areused in VAT report definitionsand accounting to describespecific types of transactions.

• Navigation: Set UpFinancials/Supply Chain,Common Definitions, VATand Intrastat, Value AddedTax, VAT Transaction Type

• VAT transaction types do notcontrol any transactionprocessing. They are usedonly to categorize transactionsfor accounting and reporting.

Write Description and save it.

Define VAT Transaction type

Add new

VAT Transaction Type

Value Added Tax

VAT and Intrastat

Common Definitions

Set Up Financials/Supply Chain

6

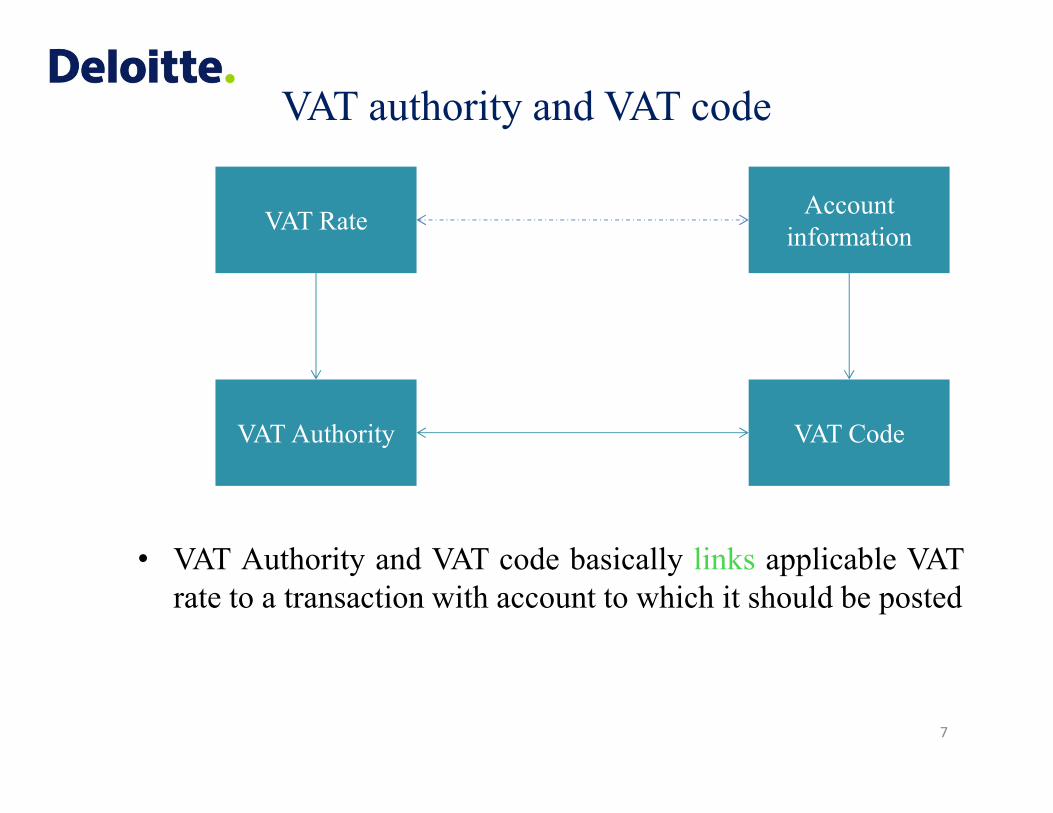

VAT authority and VAT code

• VAT Authority and VAT code basically links applicable VATrate to a transaction with account to which it should be posted

VAT Rate

VAT CodeVAT Authority

Account information

7

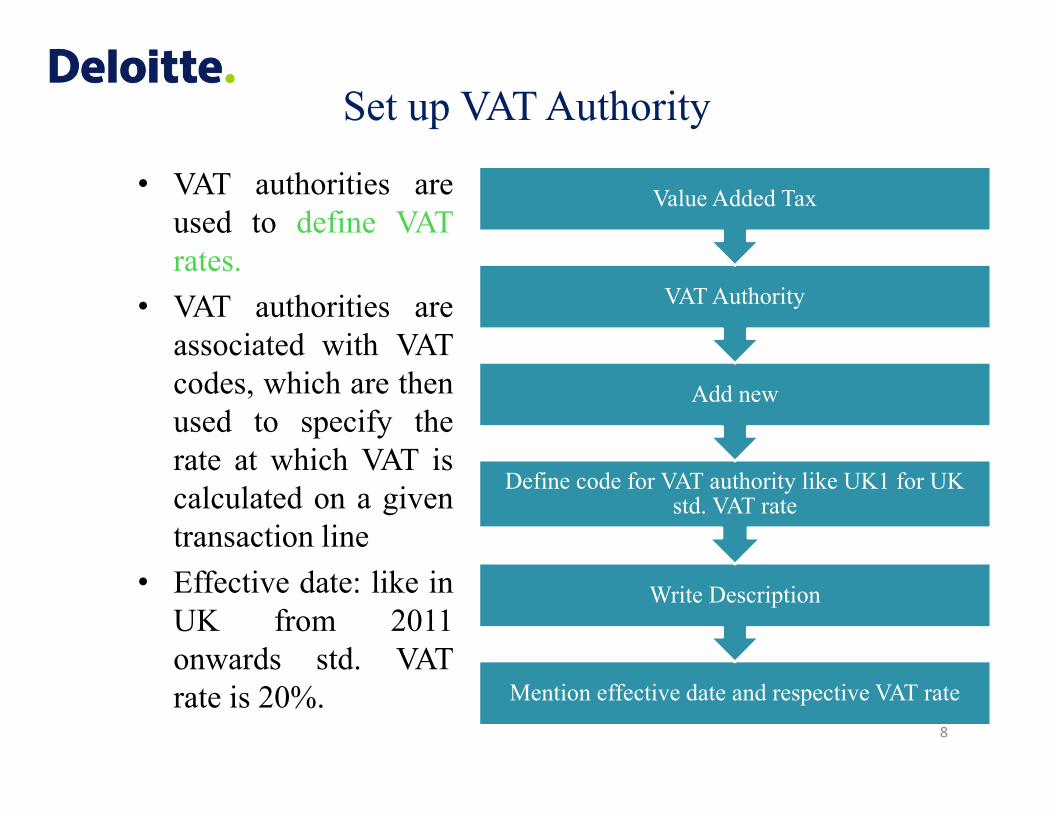

Set up VAT Authority

• VAT authorities areused to define VATrates.

• VAT authorities areassociated with VATcodes, which are thenused to specify therate at which VAT iscalculated on a giventransaction line

• Effective date: like inUK from 2011onwards std. VATrate is 20%. Mention effective date and respective VAT rate

Write Description

Define code for VAT authority like UK1 for UK std. VAT rate

Add new

VAT Authority

Value Added Tax

8

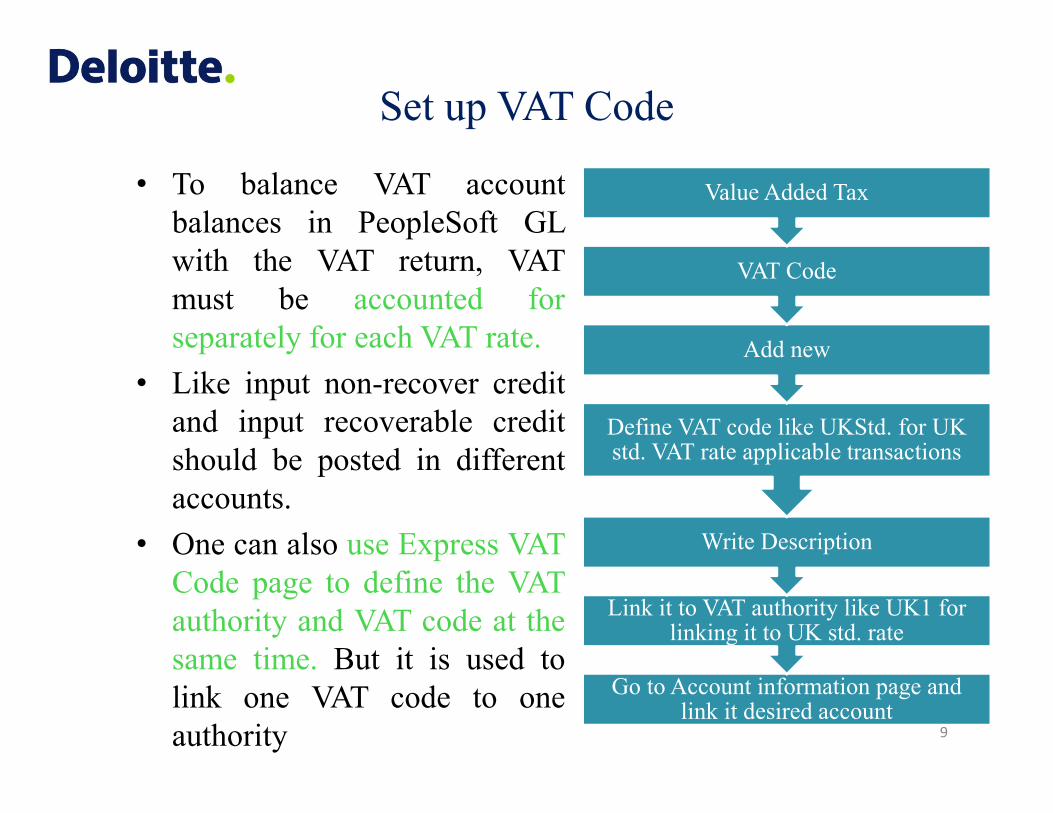

Set up VAT Code

• To balance VAT accountbalances in PeopleSoft GLwith the VAT return, VATmust be accounted forseparately for each VAT rate.

• Like input non-recover creditand input recoverable creditshould be posted in differentaccounts.

• One can also use Express VATCode page to define the VATauthority and VAT code at thesame time. But it is used tolink one VAT code to oneauthority

Go to Account information page and link it desired account

Link it to VAT authority like UK1 for linking it to UK std. rate

Write Description

Define VAT code like UKStd. for UK std. VAT rate applicable transactions

Add new

VAT Code

Value Added Tax

9

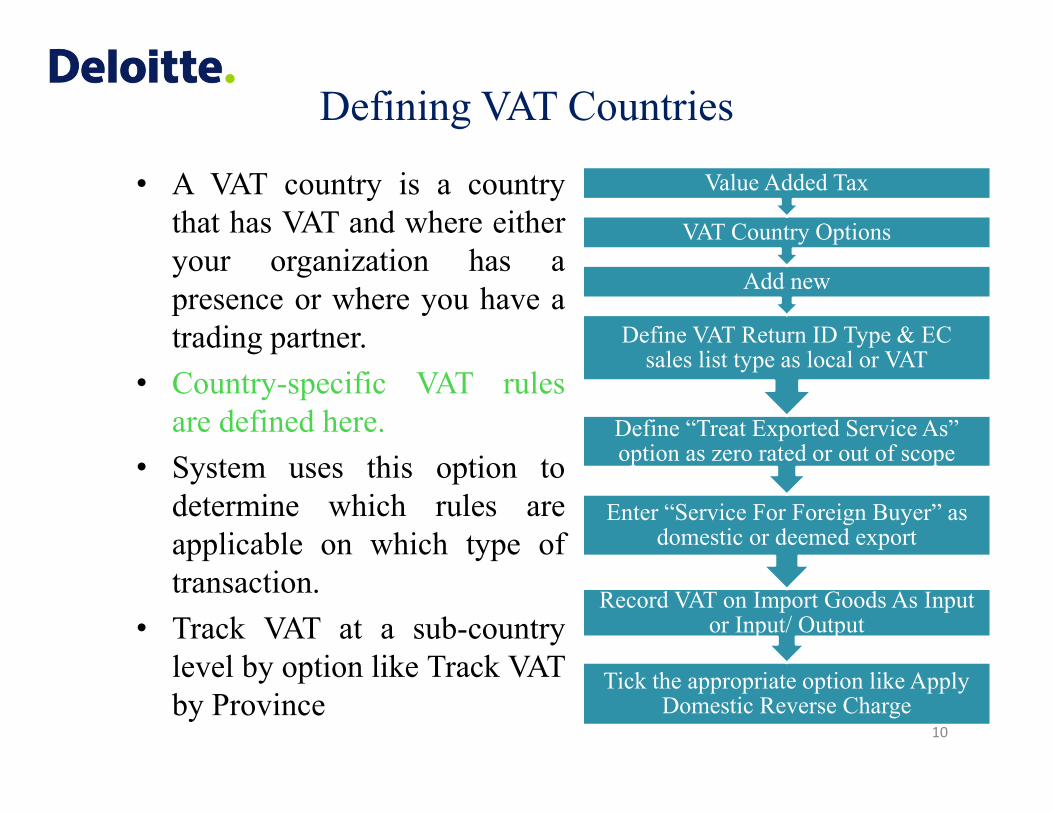

Defining VAT Countries

• A VAT country is a countrythat has VAT and where eitheryour organization has apresence or where you have atrading partner.

• Country-specific VAT rulesare defined here.

• System uses this option todetermine which rules areapplicable on which type oftransaction.

• Track VAT at a sub-countrylevel by option like Track VATby Province

Tick the appropriate option like Apply Domestic Reverse Charge

Record VAT on Import Goods As Input or Input/ Output

Enter “Service For Foreign Buyer” as domestic or deemed export

Define “Treat Exported Service As” option as zero rated or out of scope

Define VAT Return ID Type & EC sales list type as local or VAT

Add new

VAT Country Options

Value Added Tax

10

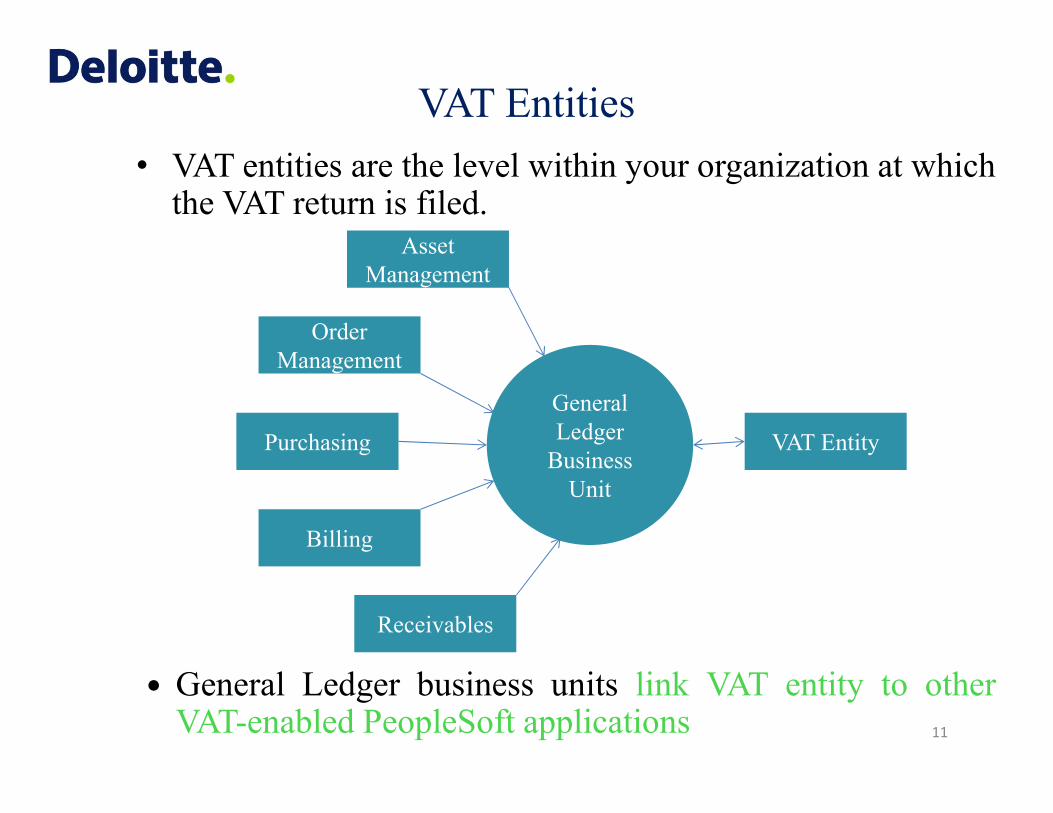

VAT Entities• VAT entities are the level within your organization at which

the VAT return is filed.Asset

Management

Order Management

Billing

Receivables

Purchasing

General Ledger

Business Unit

VAT Entity

� General Ledger business units link VAT entity to otherVAT-enabled PeopleSoft applications 11

Defining VAT entity

• Setting up a VATentity, involvesentering country-specific VATinformation likewhere the VAT entityis registered, andwhether theorganization has beengranted any kind ofexonerations orsuspensions frompaying VAT

Enter name, address in VAT report details

Enter any VAT Exception Details (if any)

Link it to the GL Business Unit/Units

Select the applicable a/c scheme: Cash/Accrual

Enter the VAT R.No. and local VAT ID

Select the country where you are registered

Add new

VAT entity

Value Added Tax

12

Defining VAT Use Types• VAT use is one of the main

determinants in therecoverability of inputVAT.

• Here define the percentageof transaction of taxableand exempt category.

• System allows user todefine the percentagesusing User type or MixedApportionment. In mixedapportionment,percentages are based onmixed-use apportionmentby general ledger businessunit or ChartField.

If mixed apportionment define chartfield

If use type is selected then enter the percentages

Select Use type as mixed apportionment or use type (coefficients for VAT recovery for

France)

VAT Use Type

13

Defining VAT Apportionment• VAT apportionment can be

based on the business unit or the ChartFields to which the purchase or expense is charged.

• The Chartfield can be set as department, division project etc.

• The system actually tracks priority 1 & 2 for a given transaction to carry out the apportionment.

Set the taxable and exempt activity % in the chartfield

Enter the priority values in the chartfield

Set Chartfield priorities

VAT Apportionment

Depart-ment

Project

VAT Apportionment: Track efficiency

and recoverability of Usage

14

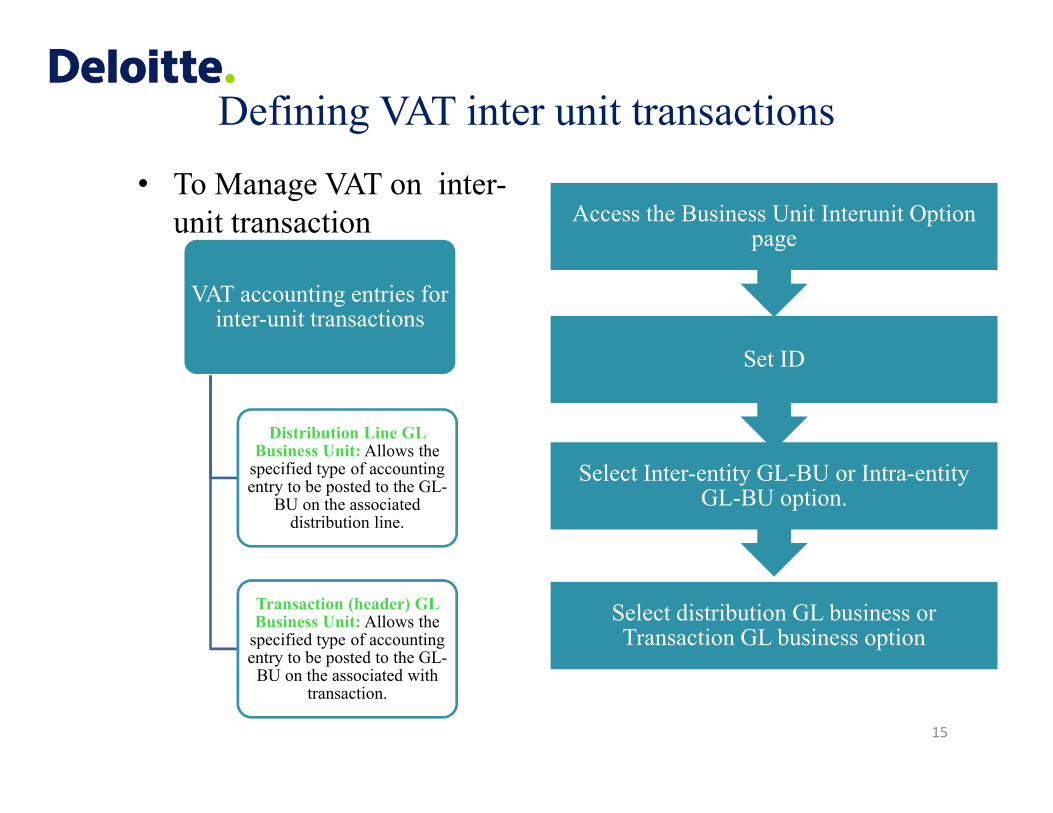

Defining VAT inter unit transactions• To Manage VAT on inter-

unit transaction

Select distribution GL business or Transaction GL business option

Select Inter-entity GL-BU or Intra-entity GL-BU option.

Set ID

Access the Business Unit Interunit Option page

VAT accounting entries for inter-unit transactions

Distribution Line GL Business Unit: Allows the

specified type of accounting entry to be posted to the GL-

BU on the associated distribution line.

Transaction (header) GL Business Unit: Allows the

specified type of accounting entry to be posted to the GL-

BU on the associated with transaction.

15

Loading VAT transaction table• The VAT transaction table

stores the detailed transaction information required for VAT reporting

• It is the primary source of information for all VAT reports.

• For each product, the transaction loader uses a VAT transaction source definition to determine what information to select from which tables. Specify the business unit or units for the process

Specify the PeopleSoft application or applications for which process needs to be

carried out.

Select product/products for which process needs to be carried out.

Select the VAT entity for which VAT transaction data is to be loaded.

Access the VAT Transaction Loader Rqst page

16

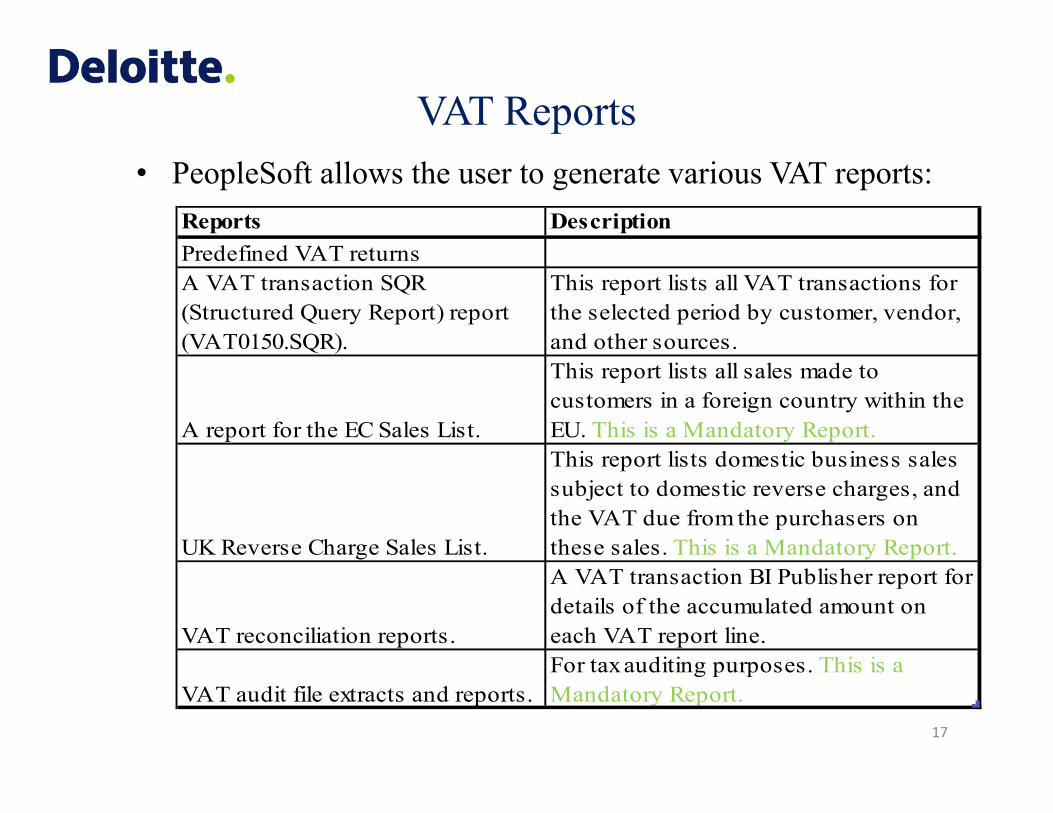

VAT Reports• PeopleSoft allows the user to generate various VAT reports:

Reports DescriptionPredefined VAT returnsA VAT transaction SQR (Structured Query Report) report (VAT0150.SQR).

This report lists all VAT transactions for the selected period by customer, vendor, and other sources.

A report for the EC Sales List.

This report lists all sales made to customers in a foreign country within the EU. This is a Mandatory Report.

UK Reverse Charge Sales List.

This report lists domestic business sales subject to domestic reverse charges, and the VAT due from the purchasers on these sales. This is a Mandatory Report.

VAT reconciliation reports.

A VAT transaction BI Publisher report for details of the accumulated amount on each VAT report line.

VAT audit file extracts and reports.For tax auditing purposes. This is a Mandatory Report.

17

• Thank You

18

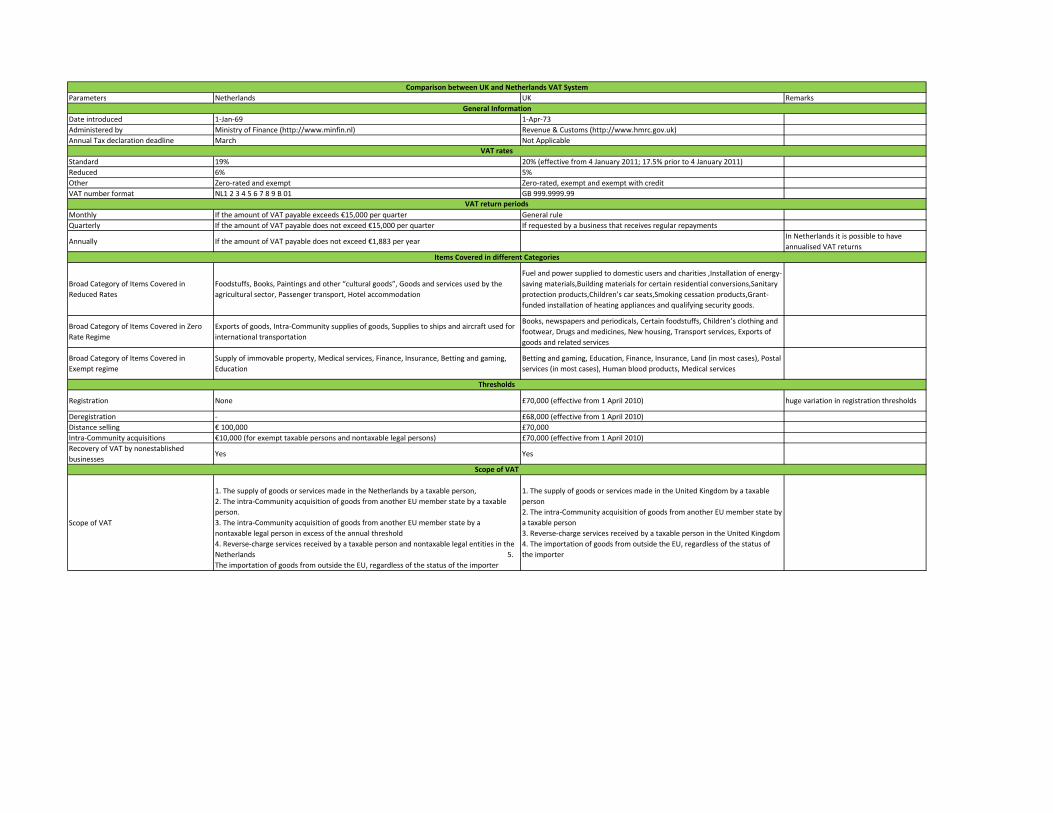

Parameters Netherlands UK Remarks

Date introduced 1-Jan-69 1-Apr-73Administered by Ministry of Finance (http://www.minfin.nl) Revenue & Customs (http://www.hmrc.gov.uk)Annual Tax declaration deadline March Not Applicable

Standard 19% 20% (effective from 4 January 2011; 17.5% prior to 4 January 2011)Reduced 6% 5%Other Zero-rated and exempt Zero-rated, exempt and exempt with creditVAT number format NL1 2 3 4 5 6 7 8 9 B 01 GB 999.9999.99

Monthly If the amount of VAT payable exceeds €15,000 per quarter General ruleQuarterly If the amount of VAT payable does not exceed €15,000 per quarter If requested by a business that receives regular repayments

Annually If the amount of VAT payable does not exceed €1,883 per yearIn Netherlands it is possible to have annualised VAT returns

Broad Category of Items Covered in Reduced Rates

Foodstuffs, Books, Paintings and other “cultural goods”, Goods and services used by the agricultural sector, Passenger transport, Hotel accommodation

Fuel and power supplied to domestic users and charities ,Installation of energy-saving materials,Building materials for certain residential conversions,Sanitary protection products,Children’s car seats,Smoking cessation products,Grant-funded installation of heating appliances and qualifying security goods.

Broad Category of Items Covered in Zero Rate Regime

Exports of goods, Intra-Community supplies of goods, Supplies to ships and aircraft used for international transportation

Books, newspapers and periodicals, Certain foodstuffs, Children’s clothing and footwear, Drugs and medicines, New housing, Transport services, Exports of goods and related services

Broad Category of Items Covered in Exempt regime

Supply of immovable property, Medical services, Finance, Insurance, Betting and gaming, Education

Betting and gaming, Education, Finance, Insurance, Land (in most cases), Postal services (in most cases), Human blood products, Medical services

Registration None £70,000 (effective from 1 April 2010) huge variation in registration thresholds

Deregistration - £68,000 (effective from 1 April 2010)Distance selling € 100,000 £70,000Intra-Community acquisitions €10,000 (for exempt taxable persons and nontaxable legal persons) £70,000 (effective from 1 April 2010)Recovery of VAT by nonestablished businesses

Yes Yes

Scope of VAT

1. The supply of goods or services made in the Netherlands by a taxable person, 2. The intra-Community acquisition of goods from another EU member state by a taxable person. 3. The intra-Community acquisition of goods from another EU member state by a nontaxable legal person in excess of the annual threshold 4. Reverse-charge services received by a taxable person and nontaxable legal entities in the Netherlands 5. The importation of goods from outside the EU, regardless of the status of the importer

1. The supply of goods or services made in the United Kingdom by a taxable person2. The intra-Community acquisition of goods from another EU member state by a taxable person 3. Reverse-charge services received by a taxable person in the United Kingdom4. The importation of goods from outside the EU, regardless of the status of the importer

Thresholds

Scope of VAT

Comparison between UK and Netherlands VAT System

General Information

VAT rates

VAT return periods

Items Covered in different Categories

Parameters Netherlands UK Remarks

Claim Time LimitThe application must cover a period of not less than three consecutive calendar months in one calendar year and not more than one calendar year.

Properly completed applications must be submitted to the Member State of Establishment at the latest on September 30th of the calendar year following the refund year.

Non-refundable VAT

1. Supplies of goods and services that are not used for business purposes;2. Supplies and services acquired or imported in connection with an exempt business activity;3. Food and drinks in restaurants, hotels and cafes;4. Business entertainment in excess of 227 euro a year per person;5. Employee benefits in kind in excess of 227 euro a year per person;6. The VAT on costs for the lease or rental of cars will in practice be limited to an 84% VAT refund (a 16% correction is made for private use).

1. Non-business supplies 2. Supplies which the claimant intends to use for carrying out of an economic activity in the UK or which the claimant intends to export from the UK.3. Business entertainment and hospitality expenses and other expenses on which the recovery of VAT is restricted in the UK.4.Goods and services you have bought for resale.5. Amounts of VAT which have been incorrectly invoiced, or wrongly charged. 6. The purchase or import of passenger motor vehicles, unless used wholly for business purposes;7. Certain second hand goods,for which no tax invoices will be raised.

Minimum Reclaim amount

If the application relates to a period of less than one calendar year but not less than three months, the amount for which application is made may not be less than EUR 400; if the application relates to a period of a calendar year or the remainder of a calendar year, the amount may not be less than EUR 50.

If the application relates to a period of less than one calendar year but not less than three months, the amount for which application is made may not be less than £295; if the application relates to a period of a calendar year or the remainder of a calendar year, the amount may not be less than £35.

Group registration

Taxable persons established in the Netherlands (including fixed establishments) may form a VAT group if the members are closely bound by “financial, economic and organizational links.”

Corporate bodies that are under “common control” and are established or have a fixed establishment in the United Kingdom may apply to register as a VAT group.

Conditions for mandatory registration of non established businesses

1. Intra-Community supplies or acquisitions2. Distance sales in excess of the threshold3. Supplies of goods and services that are not subject to the reverse charge

1. Goods located in the United Kingdom at the time of supply2. Intra-Community acquisitions of goods3. Distance sales of goods to U.K. residents who are not taxable persons4. Services to which the reverse charge does not apply

VAT on capital goods

1. Immovable property: adjusted for a period of 10 years2. Movable property subject to depreciation for income tax purposes: adjusted for a period of five years

1. Land and buildings and related property expenditure valued at £250,000 or more: adjusted over a period of 10 years 2. Computer hardware valued at £50,000 or more: adjusted over a period of five years3. Ships and aircraft valued at £50,000 or more: adjusted over a period of five

VAT Refund/Reclaim Rules

Comparison between UK and Netherlands VAT System