Embed Size (px)

Citation preview

1

APRIL 2014

This publication was produced for review by the United States Agency for International Development. It was prepared by RTI International

Value Chain Assessment Annex 2. Construction Industry Assessment Local Enterprise and Value Chain Enhancement (LEVE) Project

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 1

TABLE OF CONTENTS ABBREVIATIONS...................................................................................................... 2

1. INTRODUCTION ................................................................................................. 3

2. METHODOLOGY ................................................................................................ 3

3. CONSTRUCTION INDUSTRY PROFILE ............................................................ 5

3.1 Port-au-Prince and Cap-Haïtien .................................................................. 5

3.2 Industry Structure ........................................................................................ 6

3.3 Defining Value Chains & Subsectors ......................................................... 8

3.4 Stimulating Employment ........................................................................... 20

3.5 Developing the Workforce......................................................................... 25

4. VALUE CHAIN SELECTION ASSESSMENT ................................................... 26

4.1 Building Value Chains ............................................................................. 27

4.2 Infrastructure Value Chains .................................................................... 32

4.3 Value Chain Selection for Corridors ...................................................... 37

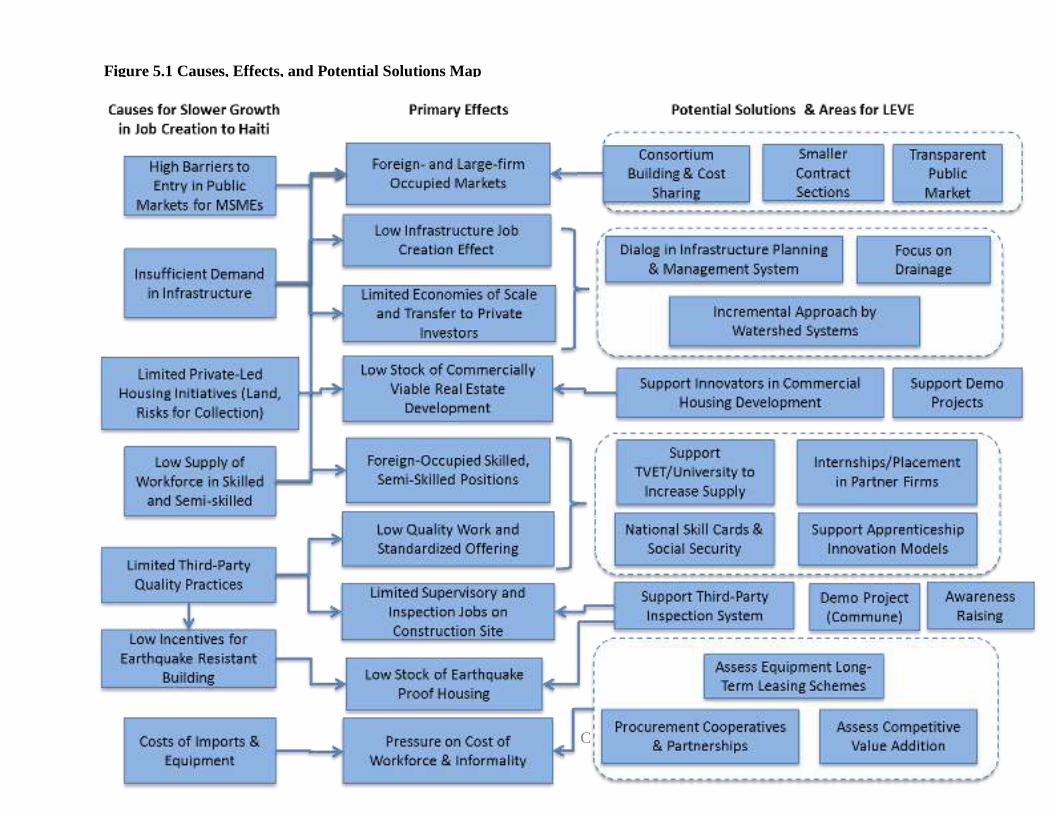

5. UPGRADING STRATEGIES ............................................................................. 40

5.1 Causal Model ........................................................................................... 40

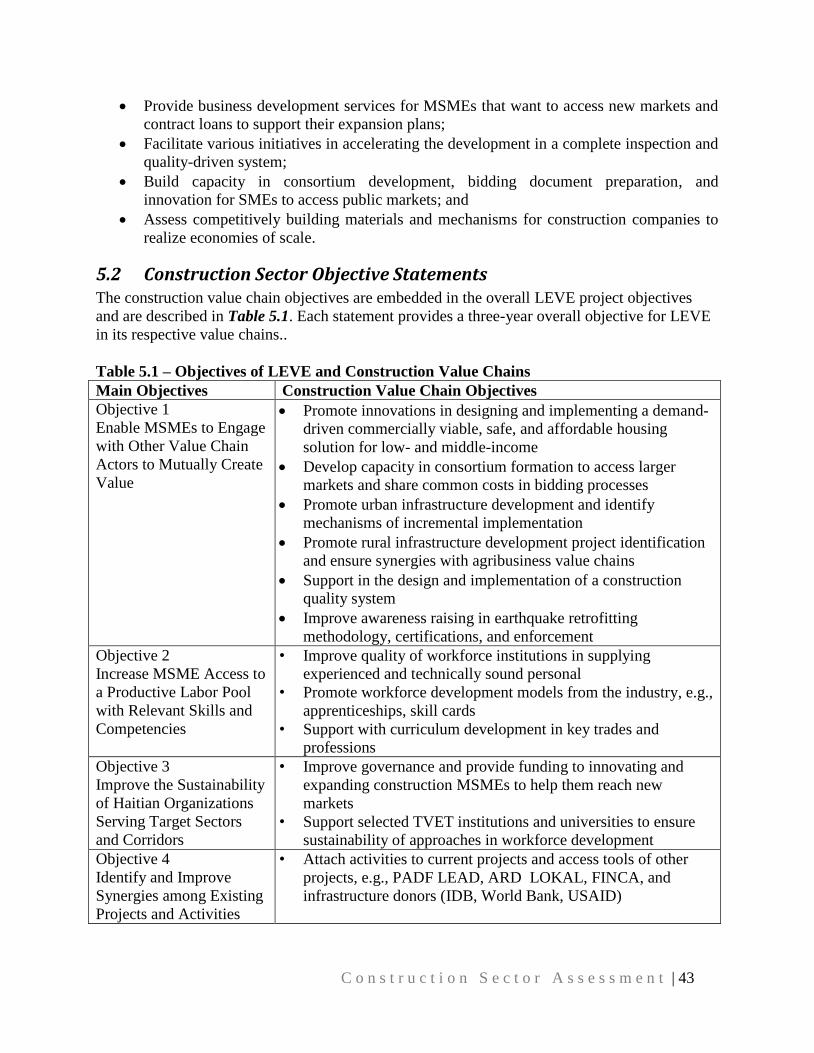

5.2 Construction Sector Objective Statements ........................................... 43

5.3 Value Chain Upgrade Strategies ............................................................ 44

5.4 Corridor Upgrade Strategies .................................................................. 54

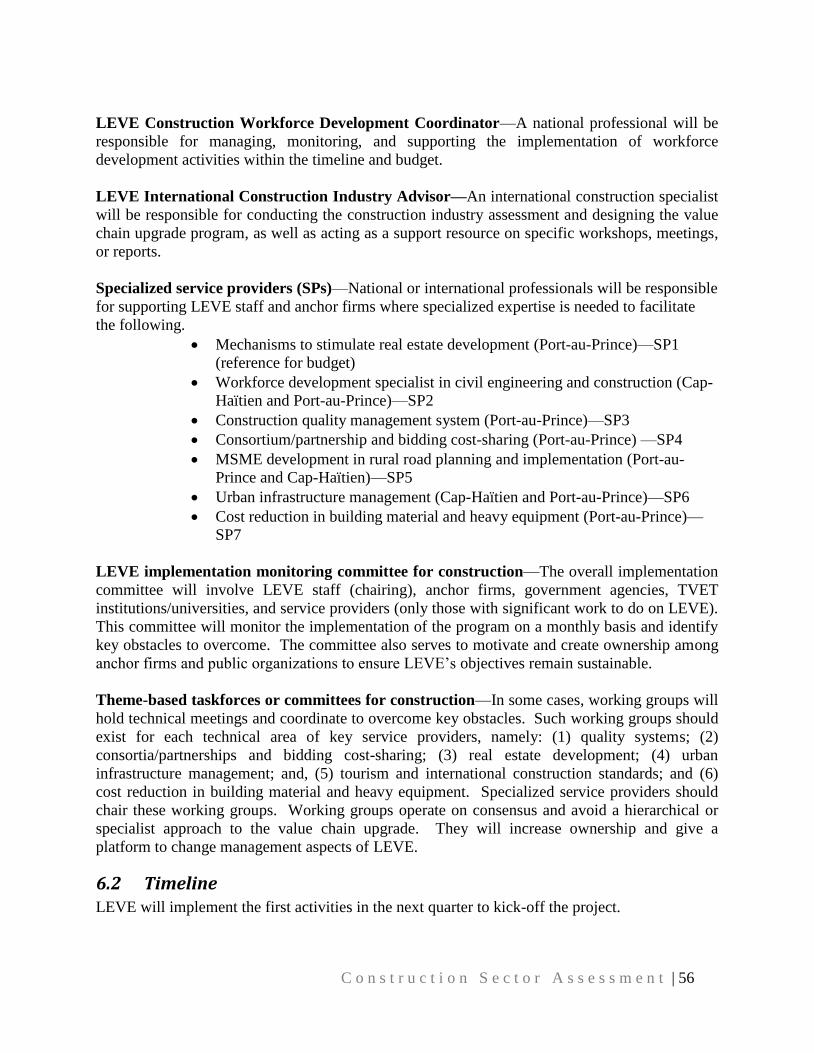

6. IMPLEMENTATION PLAN ............................................................................... 55

6.1 Organization ............................................................................................ 55

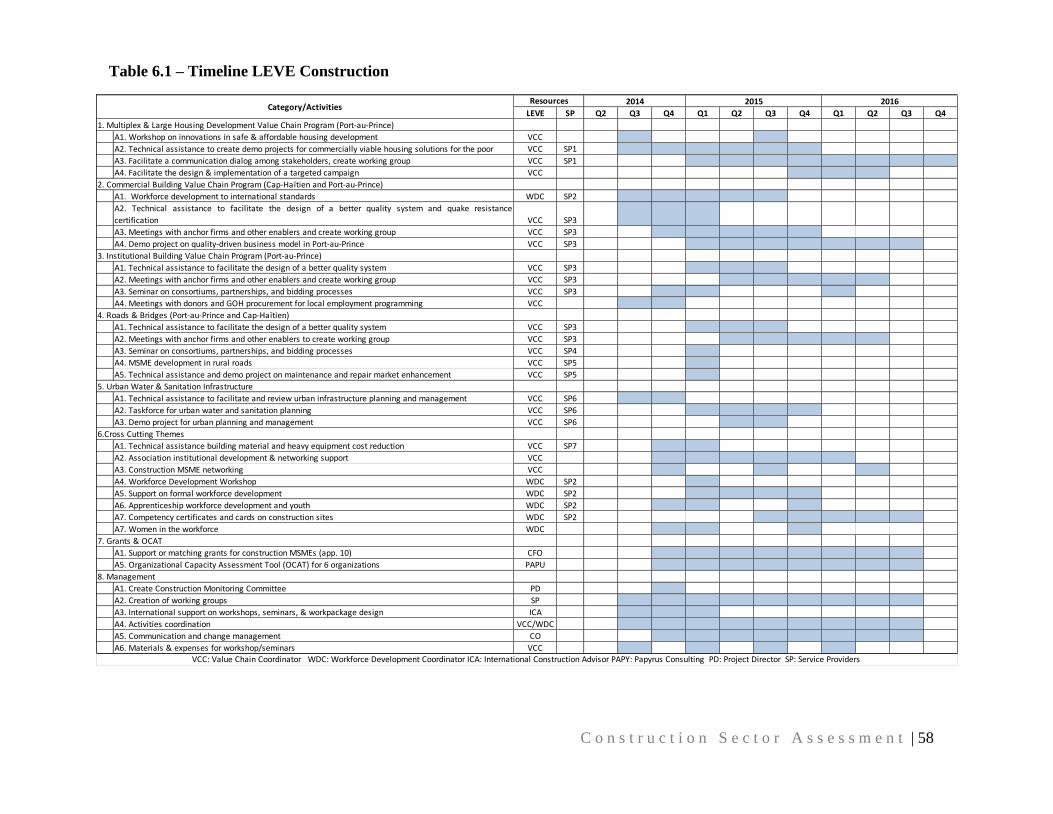

6.2 Timeline .................................................................................................... 56

REFERENCES ......................................................................................................... 59

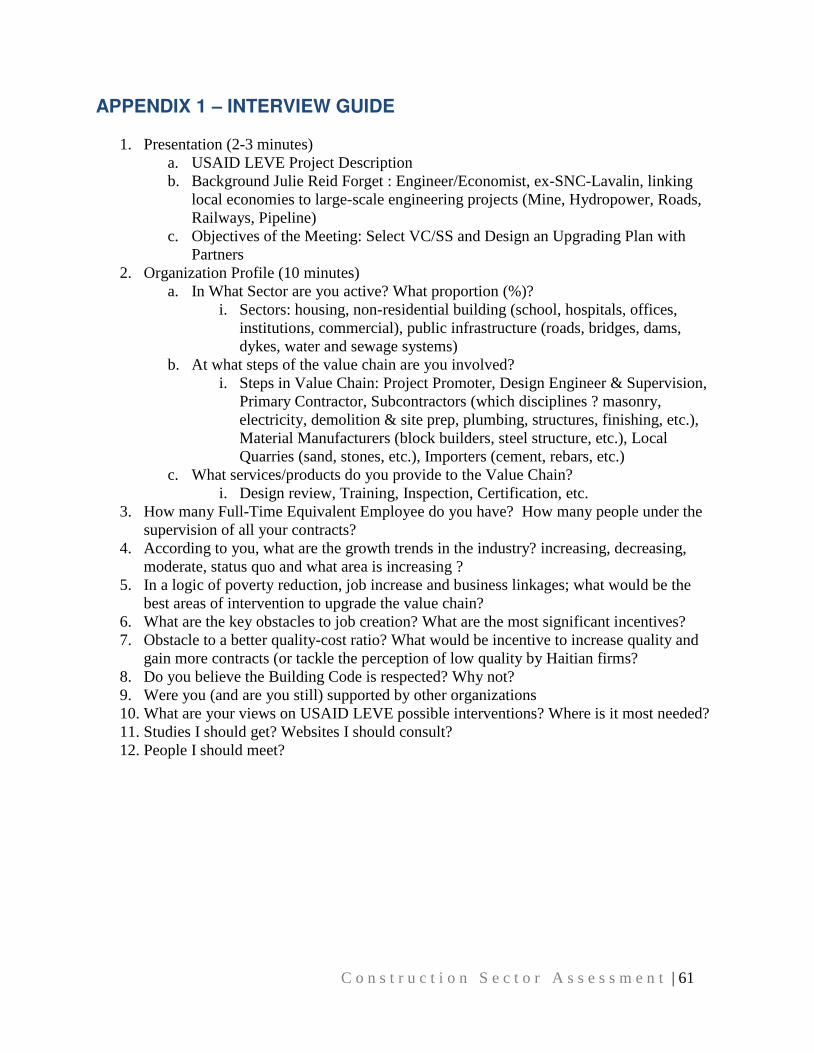

APPENDIX 1 – INTERVIEW GUIDE ........................................................................ 61

APPENDIX 2 – CONTACT LIST .............................................................................. 62

APPENDIX 3 – BUILDING VALUE ADDED PROCESS ......................................... 64

APPENDIX 4 – INFRASTRUCTURE VALUE ADDED PROCESS .......................... 65

APPENDIX 5 – DETAILED CONSTRUCTION WORKFORCE DEMAND ............... 66

APPENDIX 6 – DETAILED VC ASSESSMENT MATRICES ................................... 69

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 2

ABBREVIATIONS AHEC Construction Enterprise Association of Haiti APRODBP Association of Building Block and Paving Producers ATH Haitian Tourist Association BEB Bureau of Building Evaluation CAD Computer-Assisted Design CH Cap-Haïtien CIAT Interministerial Committee for Regional Planning CINA National Cement Manufacturer CO Communication Officer DINEPA National Direction of Potable Water and Sanitation EPCM Engineering, Procurement, Construction, and Management GIS Geographic Information System GoH Government of Haiti HTG Haitian Gourde HVAC Heating, Ventilation, and Air Conditioning ICA International Construction Advisor IDB Inter-American Development Bank LEAD Leveraging Effective Application of Direct Investment for Haiti LEVE Local Enterprise Value Chain Enhancement MTPTC Ministry of Public Work, Transport and Communication MPCE Ministry of Planning and External Cooperation MSME Micro, Small, and Medium Enterprises MTPTC Ministry of Public Work, Transport, and Communication OCAT Organizational Capacity Assessment Tool MSMEs Micro, Small and Medium Enterprises PAP Port-au-Prince PNLH National Policy for Housing QA/QC quality assurance/quality control TVET Technical Vocational Education Training UCLBP Public Building and Housing Coordination Unit USAID United States Agency for International Development VCC Value Chain Coordinator VF Vorbe & Fils WB World Bank WDC Workforce Development Coordinator

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 3

1. INTRODUCTION The United States Agency for International Development’s (USAID’s) Local Enterprise and Value Chain Enhancement (LEVE) project is a carefully crafted blueprint to expand opportunities for Haiti’s micro, small, and medium enterprises (MSMEs) in key agribusiness, textile/apparel, and construction value chains, generating employment for Haitian men, women, youth, and vulnerable populations in priority corridors of Port-au-Prince, Saint-Marc, and Cap-Haïtien. There are four key objectives to LEVE. Objective 1—Enable MSMEs to Engage with Other Value Chain Actors to Mutually Create Value drives the growth and sustainable competitiveness of Haitian MSMEs by expanding the sales and investments of lead firms in targeted sectors, deepening supply and value chain relationships within the value chains, and fostering market opportunities for entrepreneurial MSMEs. Objective 2—Increase MSME Access to a Productive Labor Pool with Relevant Skills and Competencies focuses on productivity, addressing workforce-related constraints in key sectors and generating more and better employment opportunities, particularly for vulnerable populations. These substantive efforts are supported by Objective 3—Improve the Sustainability of Haitian Organizations Serving Target Sectors and Corridors, which builds capacity for sustainability, enabling a set of strong business service providers and workforce training institutions to support ongoing, self-propelled growth and upgrading at all levels of these industries. Objective 4—Identify and Improve Synergies among Existing USAID Activities will put emphasis on intra- and cross-donor project collaboration activities that provide leverage, reducing friction resulting from overlaps, accelerating start-up by using existing research and analysis, and amplifying impact by leveraging financial and other resources from complementary programs and initiatives. This report is solely concerned with the value chains in the construction sector. It includes an overview of the construction industry in Port-au-Prince and Cap-Haïtien and results of the value chain assessment and lays out an upgrading plan for several value chains. This work provides USAID LEVE with sound analytics of the construction sector in Cap-Haïtien and Port-au-Prince to prepare detailed implementation plans of value chain activities, which will start in May 2014. Sections 1 to 4 present the state of the construction sector and the selection of the value chains most appropriate for interventions based on a competitiveness framework developed for this purpose. Sections 5 and 6 propose the implementation plans to upgrade the selected value chains over the course of USAID LEVE. The program will be designed to meet the four project objectives, including the cross-cutting aspects of economic development, namely, the business enabling environment, business development services and other support services, access to financing, and formalization of MSMEs. 2. METHODOLOGY The LEVE team will follow research-backed methodologies for demand-driven workforce development linked with value chain upgrading in the construction industry in Port-au-Prince and Cap-Haïtien. The assessment process was based on the Rapid Value Chain Assessment Methodology, developed by Tetra Tech International Development, using various set of factors to evaluate the potential for upgrading a value chain. To obtain reliable primary sources of data, the team consulted with industry stakeholders, with the goal of identifying potential partnerships with anchor firms, workforce development leaders, agents of change/innovators, or expanding

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 4

and innovative MSMEs. The consultation process was participatory to ensure that consultants would appropriately integrate the views and concerns of the stakeholders, find common ground, and prepare a work plan that will remain ambitious while mitigating risks of change management. More than 35 interviews were conducted with the industry stakeholders in Port-au-Prince and Cap-Haïtien between March 12 and April 4 with the objective of:

Presenting LEVE’s objectives and explaining the value chain approach; Collecting information about their role in the value chain (supplier, contractor, promoter,

regulatory agency); Identifying their involvement in subsectors and value chains; Assessing competitive growth areas; Understanding the constraints and opportunities of the industry by subsector or value

chain; Identifying quality issues, earthquake awareness, foreign-occupied markets, workforce

development; Identifying potential solutions to address constraints; and Brainstorming areas of collaboration with LEVE.

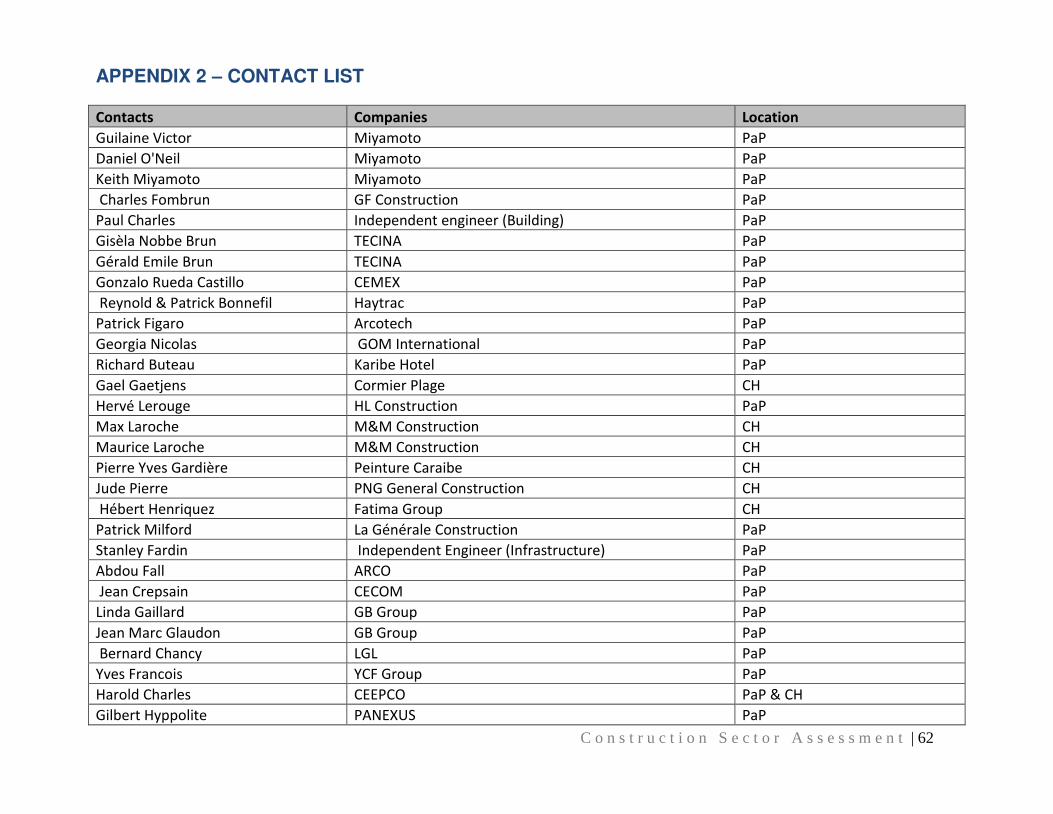

To ensure that information was collected in a consistent manner, the LEVE construction team designed an interview guide to ask open-ended and fundamental questions (Appendix 1), and the list of contacts visited are listed in Appendix 2 Categories of construction sector stakeholders visited included the following.

Client or construction project promoters (3 private, 2 public) Services, e.g., real estate developer, banks, insurance companies (3 real estate

developers) Engineering design, study, and supervision firms (4) Lead contractors (3 large; 5 medium; 2 small) Subcontractors by trade, e.g., site preparation, masonry, electricity, plumbing, finishing

(2) Building material distributors and manufacturers (4 large) Technical training institutions (1) Associations (3) Government officials, e.g., laboratory, permitting, bid requirements (3)

At least two to three stakeholders from each of these categories were met to cross-reference information, and ongoing stakeholder consultations were conducted to explore in greater detail key identified issues will be conducted in workshops/seminar formats at the start of implementation. The team actively searched for anchor firms that will generate new opportunities for MSMEs. LEVE is looking for those opportunities that will stimulate Haitian entrepreneurs to address value chain constraints with for-profit solutions and build capacity in Haiti’s education and training institutions to provide the skills required by Haitian businesses. In the stakeholder

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 5

engagement process, we identified various key MSMEs, associations, or education institutions that either would benefit from direct or indirect capacity development support or could act as a service provider or change agent for the industry. This mutual support will have a direct effect in supporting the expansion and the professionalization of key actors of the value chains via increased business linkages, business opportunities, and ultimately, job creation. Finally, synergies between programs were assessed and areas of mutual collaboration were identified. 3. CONSTRUCTION INDUSTRY PROFILE

3.1 Port-au-Prince and Cap-Haïtien

Demand for construction projects is always high in developing countries due to rapid population growth and significant donor investment in infrastructure meant to attract foreign direct investment or national private sector initiatives. In this regard, Haiti is somewhat different; the recent earthquake had a “boom-bust” effect on the construction industry1. Due to insufficient national capacity to respond to the reconstruction needs, foreign firms addressed the supply gap in expertise and the necessary workforce. Surprisingly, four years after the earthquake, foreign firms still occupy key market segments such as buildings, roads, and bridges, where foreign expertise is not required. Although significantly more investment is required to undertake post-earthquake reconstruction, donor aid is now being reduced. With that reduction, large construction projects could have reached a plateau in Port-au-Prince, though the numbers of medium-size and small construction projects are still growing. In terms of infrastructure development, although the debt relief truly helped the Government of Haiti’s (GOH’s) to reduce the cost of debt, borrowing capacity is still limited and interest rates are high. This can refrain the undertaking of major public infrastructure development. Consequently, the construction industry cannot rely on public works as a major source of growth, except for projects such as road paving, schools, and hospitals, which traditionally grow at a steadier rate. In most developing countries, public work infrastructure is a key job creator for the construction industry sector. For Cap-Haïtien, the situation is somewhat different. The construction industry is significantly less developed there than in Port-au-Prince and most mid- to large-size projects are not performed by Cap-Haïtien firms. However, unlike in Port-au-Prince, sources of growth in Cap-Haïtien are clear and significant. There are over 700 new hotel rooms planned for construction in 2014, as the international airport nears completion, linking Cap-Haïtien to the USA and Canada. Resorts along Cormier Beach and in Cap-Haïtien are expanding to prepare for the additional tourists expected to visit the Citadel Laferrière and Sans-Souci Palace. The industrial park is also expecting new industrial tenants, which could stimulate more housing development for employees; however, entrepreneurs are still doubtful when this could happen and will wait until the Korean SAE-A Trading, the largest enterprise, and other smaller companies are clearer about their expansion plans.

1 A boom bust effect is known in large-scale projects, as the local effect of a large demand, that the local economy cannot take, and the ensuing vacuum once the project is more advanced and completed. This is typical of mining projects in underdeveloped economies. There is inflation and immigration for some years, followed by deflation and emigration.

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 6

Cap-Haïtien does not have a complete construction industry. Apart from distributors and manufacturers of building materials like M&M Construction and CEMEX, respectively, there are no engineering design firms and lead contractors to undertake projects larger than churches and schools. Most often, firms from Port-au-Prince or the Dominican Republic bring along key management staff, skilled labor and hire what unskilled labor they can locally. However, even among the unskilled local labor force, firms are challenged to find employees with sufficient construction experience and end up hiring from Port-au-Prince at higher costs (per diems and lodging).

3.2 Industry Structure

The construction industry is divided in two subsectors: buildings and infrastructure. These two subsectors do not generally have the same value addition process and expertise and are not occupied by the same organizations. Buildings from single-floor houses all the way to skyscrapers have similar construction steps, but the complexity increases with the number of floors or with the design itself. In addition to design complexity, there is also project management complexity in larger-scale projects. Thus, the more costly and complex the building, the larger the contractor that will execute the contract. As for the infrastructure subsector, each type of infrastructure calls for a different type of engineering expertise, and firms tend to be more specialized in that subsector.

For both subsectors, building materials and equipment will often come from the same suppliers, as all of those projects require concrete and rebar. On average, building materials can represent 50 to 70% of the total cost of a construction project, creating significant profit margin pressure on the contractor.2 Unfortunately, building material is not significantly cheaper in Haiti. The following building materials are produced (or finished) in Haiti:

Building blocks Cobblestone/sett Steel bars (cutting and assembling/welding) Cement (packaging) Quarrying (sand, aggregates)

The steel mill (Acierie d’Haïti) once operated by GB Group is no longer producing rebar. This is all imported and then cut and welded in Haiti. Moreover, cement production from CINA and Cemex is limited to packaging in Port-au-Prince, and in Cap-Haïtien, cement is imported already packaged from the Dominican Republic. These enterprises also attempt to increase their sales by providing concrete pre-mixed, which ensures greater quality results than manual production of concrete.

2 Construction and Civil Engineering : Approach and Data Requirements, Operational Guide, Draft version, International Comparison Program, 2011, http://siteresources.worldbank.org/ICPINT/Resources/270056-1255977254560/6483625-1314373178597/ICP-OG_Construction_Draft.pdf

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 7

Another key cost driver is heavy machinery (5 to 15% of the total cost of construction projects) ,3 which is imported via firms like Haytrac. Leasing is too expensive for longer term projects, but remains particularly popular for short-term use. After three months, leasing loses any advantage over purchasing. Haytrac is developing a lease-buy longer term contract, which is available in other Caribbean islands, but not yet in Haiti. The cost of the workforce usually makes up between 15 and 30% of the total costs of a project.4 Approximately 80% of the workforce is unskilled, while the remainder is semi-skilled (electrical; heating, ventilation, air conditioning [HVAC]; masonry; plumbing), skilled (civil engineering technicians), and very skilled (civil engineers), as well as procurement officers, cost controllers, and senior project directors. Typically, the masonry team stays permanently on the construction site, while other trades are periodically present at times when they are installing electrical, plumbing, and HVAC systems, etc. The industry is characterized by a mixed formal and informal system. Most senior and skilled jobs at the top of the pyramid are for formal, full-time employees of construction companies. However, for management at the construction site, companies traditionally use a foreman (called contremaître in Haiti) to manage the workforce and delivery of materials on site. The foreman supplies most of the workforce, especially masonry work and is responsible to lead, organize and pay most employees. The lead contractor remains accountable for the project, but delegates some of the human resources functions. This contremaître with his team can be viewed as an unregistered MSME, paying no taxes, effectively lowering short-term costs of labor for lead contractors. Other construction firms believe this traditional system is very costly in supervision, as the contremaîtres are not accountable for their work and do very little training of labor. In addition, the contremaître model of project management might reduce the level of specialization and thus quality. It remains unclear what proportion of companies use the informal model over the formal model. Lately, Haiti has seen the emergence of formal MSMEs specializing in the electrical, plumbing, and HVAC trades, as in most developing countries. In the formal model, the MSMEs are formally contracted by the lead contractor, instead of being informally hired by the Contremaître, acting as an intermediate, potentially reducing the direct professional fees the MSME can obtain from direct contracting with lead contractor. Informal models are still prevalent because Haitian construction firms face significant building material and equipment costs and have limited power to negotiate better prices. Thus, there is extensive negative pressure on labor costs and quality standards to maximize profits. Demand for the sector comes primarily from the housing market, which is relatively steady. The non-residential market is less steady, except for school and hospital construction, but represents higher returns. Thus, most firms are focused on these larger buildings. For most stakeholders, customers in the non-residential building market are more experienced and less emotionally attached to the design. They are thus more likely to trust the construction company regarding the overall management of the project. On the contrary, in residential building markets, customers are less experienced in construction projects and tend to frequently ask for various changes, as they are emotionally attached to the construction project. Public infrastructure has the most volatile demand and calls for high specialization levels, most of which cannot be addressed by

3 Ibid 4 Ibid

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 8

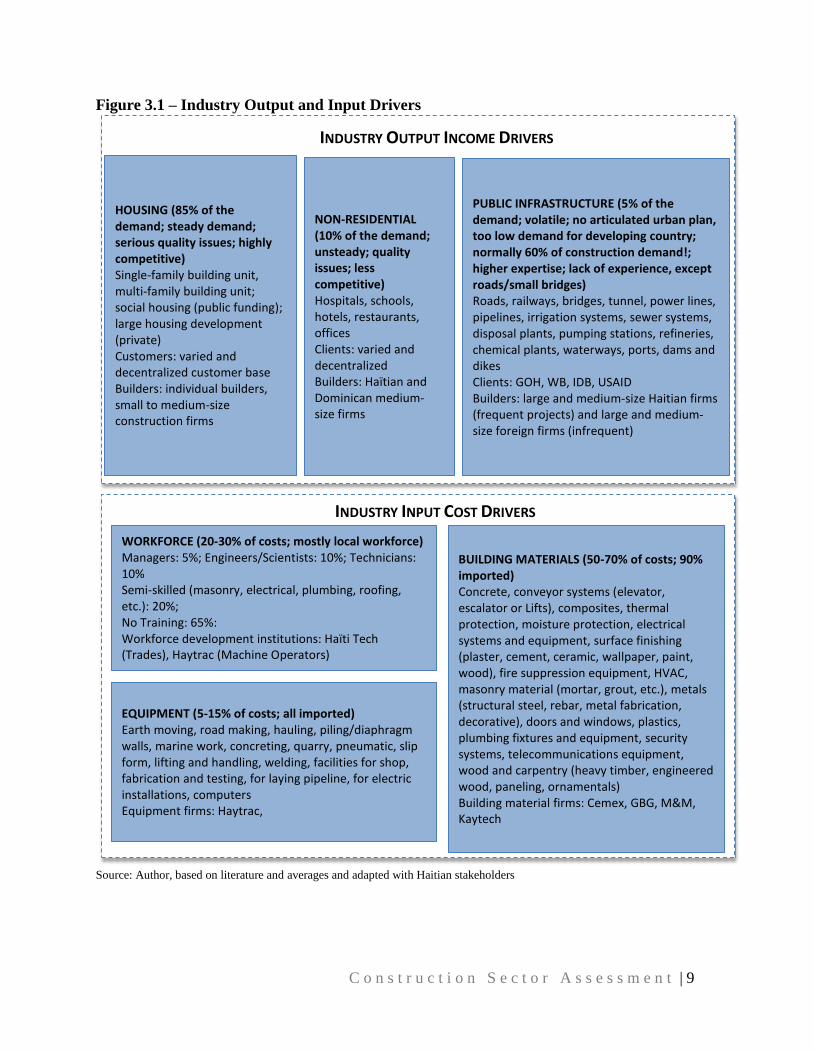

Haitian firms. Figure 3.1 illustrates the basic input and output drivers of the Haiti construction sector.

Supply on the other hand is characterized by the high proportion of costs in raw or manufactured material, rather than in equipment or workforce. Workforce remains a significant cost driver, though its proportion might not justify the very low wage in the industry (200 HTG/day). The cost of equipment is normally a relatively lower proportion of total costs than raw material and workforce, but that assumes a functioning equipment market, which is not the case in Haiti. Stakeholders voiced their concerns over very high costs of equipment, including the leasing market. There is an industry consensus that construction material and equipment costs should be brought down.

3.3 Defining Value Chains & Subsectors

The Haitian construction sector will be divided into two subsectors for the purposes of this assessment: building and infrastructure. The building subsector includes residential, commercial, and institutional building types. Stakeholders in the building subsector will vary depending upon the value of the building being constructed, the level of specialized work involved, and the demand. The infrastructure subsector includes roads and bridges, water and sanitation, and complex civil works. Again, the level of complexity increases as the level of expertise increases and demand decreases. Airports or hydropower dams are often undertaken by international foreign firms, which execute these projects all over the world.

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 9

Figure 3.1 – Industry Output and Input Drivers

Source: Author, based on literature and averages and adapted with Haitian stakeholders

BUILDING MATERIALS (50-70% of costs; 90%

imported) Concrete, conveyor systems (elevator,

escalator or Lifts), composites, thermal

protection, moisture protection, electrical

systems and equipment, surface finishing

(plaster, cement, ceramic, wallpaper, paint,

wood), fire suppression equipment, HVAC,

masonry material (mortar, grout, etc.), metals

(structural steel, rebar, metal fabrication,

decorative), doors and windows, plastics,

plumbing fixtures and equipment, security

systems, telecommunications equipment,

wood and carpentry (heavy timber, engineered

wood, paneling, ornamentals) Building material firms: Cemex, GBG, M&M,

Kaytech

WORKFORCE (20-30% of costs; mostly local workforce) Managers: 5%; Engineers/Scientists: 10%; Technicians:

10% Semi-skilled (masonry, electrical, plumbing, roofing,

etc.): 20%;

No Training: 65%: Workforce development institutions: Haïti Tech

(Trades), Haytrac (Machine Operators)

EQUIPMENT (5-15% of costs; all imported) Earth moving, road making, hauling, piling/diaphragm

walls, marine work, concreting, quarry, pneumatic, slip

form, lifting and handling, welding, facilities for shop,

fabrication and testing, for laying pipeline, for electric

installations, computers Equipment firms: Haytrac,

-

INDUSTRY OUTPUT INCOME DRIVERS

HOUSING (85% of the

demand; steady demand;

serious quality issues; highly

competitive) Single-family building unit, multi-family building unit;

social housing (public funding); large housing development

(private) Customers: varied and

decentralized customer base Builders: individual builders,

small to medium-size

construction firms

NON-RESIDENTIAL

(10% of the demand;

unsteady; quality

issues; less

competitive) Hospitals, schools,

hotels, restaurants,

offices Clients: varied and

decentralized Builders: Haïtian and

Dominican medium-

size firms

PUBLIC INFRASTRUCTURE (5% of the

demand; volatile; no articulated urban plan,

too low demand for developing country;

normally 60% of construction demand!;

higher expertise; lack of experience, except

roads/small bridges)

Roads, railways, bridges, tunnel, power lines,

pipelines, irrigation systems, sewer systems,

disposal plants, pumping stations, refineries,

chemical plants, waterways, ports, dams and

dikes Clients: GOH, WB, IDB, USAID Builders: large and medium-size Haitian firms

(frequent projects) and large and medium-

size foreign firms (infrequent)

INDUSTRY INPUT COST DRIVERS

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 10

3.3.1 Subsector 1: Building

In building either a small house or a large multi-story structure, the construction follows similar value chains. What differentiates the value chains from one another are the type of project promoter, the level of technical and management complexity of projects and the consistency of the demand, hereafter explained:

Project developers—An individual home owner brings different requirements than a real estate

developer, whether a private commercial developer, a public institution developer, or an industrial developer. The individual owner has a generally low understanding of the construction process, as a family might build 1 to 2 houses in a lifetime, whereas a real estate developer is a professional customer who knows exactly what to ask of a contractor when undertaking a construction project. Similarly, while commercial and institutional buildings are almost identical, commercial and institutional customers do not contract construction firms the same way. The former will contract professional firms based on personal contacts and previous experiences. The latter selects contractors and professionals based on a tender process that requires a significant investment from the bidders.

Technical and project management complexity—A one-floor house might have the least-complex construction process, while multi-story buildings are more complex. On one end of the spectrum, housing development is accessible to most of the sector stakeholders and remains the most open value chain of the building subsector, as it is informal and occupied by small and medium firms. On the other end of the spectrum, complex industrial buildings or large-scale building projects offer a more limited market, whereby only foreign or very large firms are capable of handling the project management and complexity of design. Industrial buildings require more specialized infrastructure construction capacity. In that view, larger and more specialized firms will tend to occupy complex value chains, whereas micro- or small firms tend to occupy more accessible markets like housing or smaller multi-story buildings.

Consistency of demand—Large, complex development projects are less numerous than individual housing, multiplex housing developments, or commercial and institutional buildings. The market with unsteady demand tends to be occupied by foreign firms, which have access to larger (exporting their services) and more specialized markets. This explains the predominance of firms from the Dominican Republic on larger projects in Haiti and the presence of firms from industrialized countries in highly specialized work.

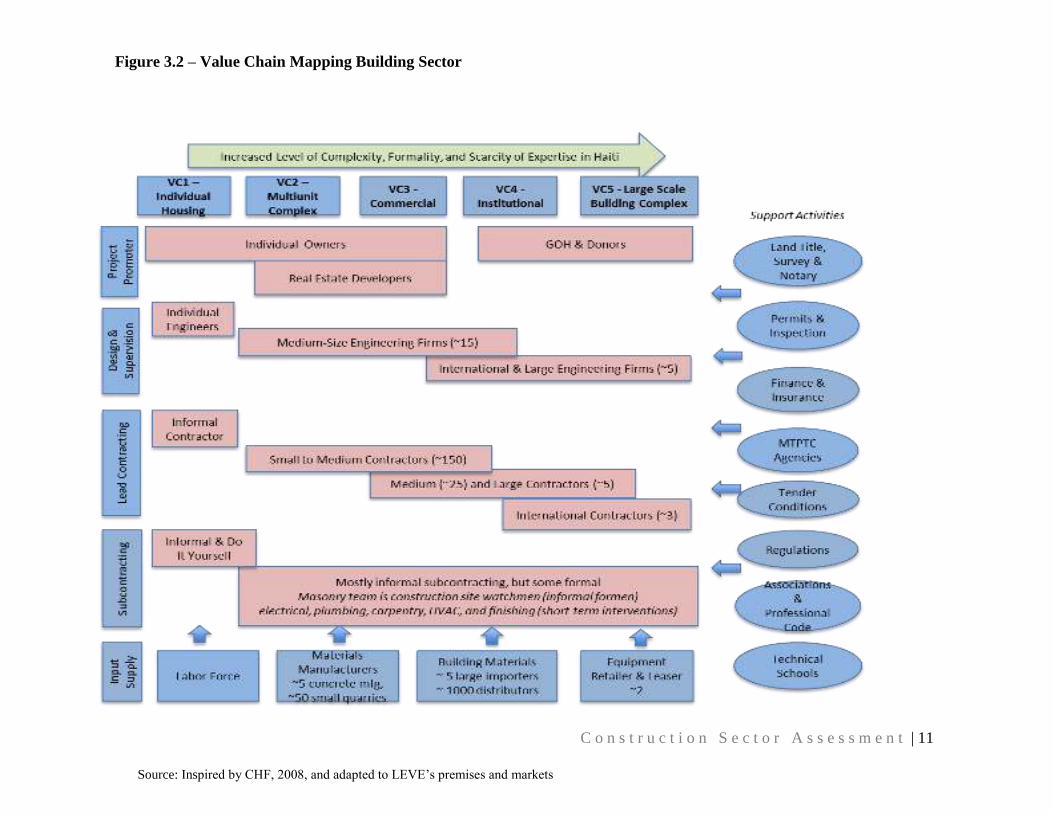

Figure 3.2 maps out the value chains in the building subsector.5 On the top are the proposed value chains; on the left, the cycle of a building construction project; on the bottom, the input factors; and on the right, the supporting services. In the middle are the size and types of stakeholders. Value chains are presented in order of complexity, formality, and scarcity of expertise. Table 3.1 describes the key features of each value chain considered for assessment for the LEVE Project.

5 Adapted from Value Chain Tools for Market-Integrated Relief : Haiti’s Construction Sector., Guided Case Studies in Value Chain Development for Conflict-Affected Environments, microREPORT #93

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 11

Figure 3.2 – Value Chain Mapping Building Sector

Source: Inspired by CHF, 2008, and adapted to LEVE’s premises and markets

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 12

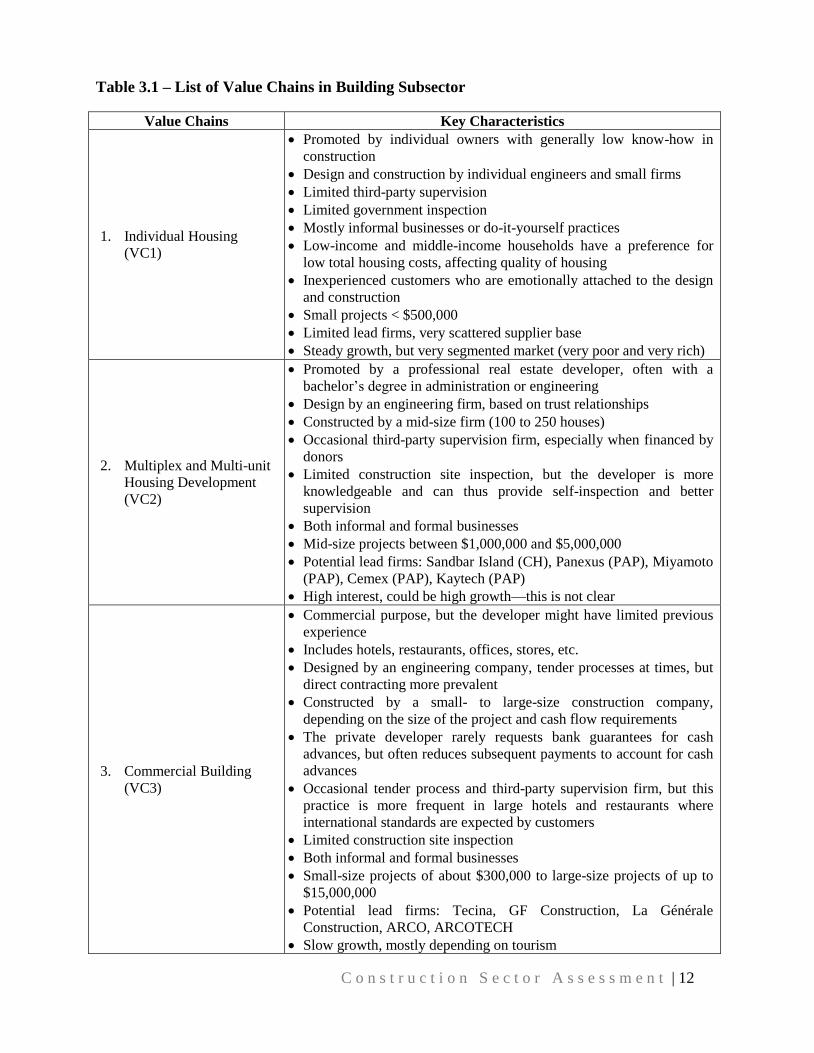

Table 3.1 – List of Value Chains in Building Subsector

Value Chains Key Characteristics

1. Individual Housing (VC1)

Promoted by individual owners with generally low know-how in construction

Design and construction by individual engineers and small firms Limited third-party supervision Limited government inspection Mostly informal businesses or do-it-yourself practices Low-income and middle-income households have a preference for

low total housing costs, affecting quality of housing Inexperienced customers who are emotionally attached to the design

and construction Small projects < $500,000 Limited lead firms, very scattered supplier base Steady growth, but very segmented market (very poor and very rich)

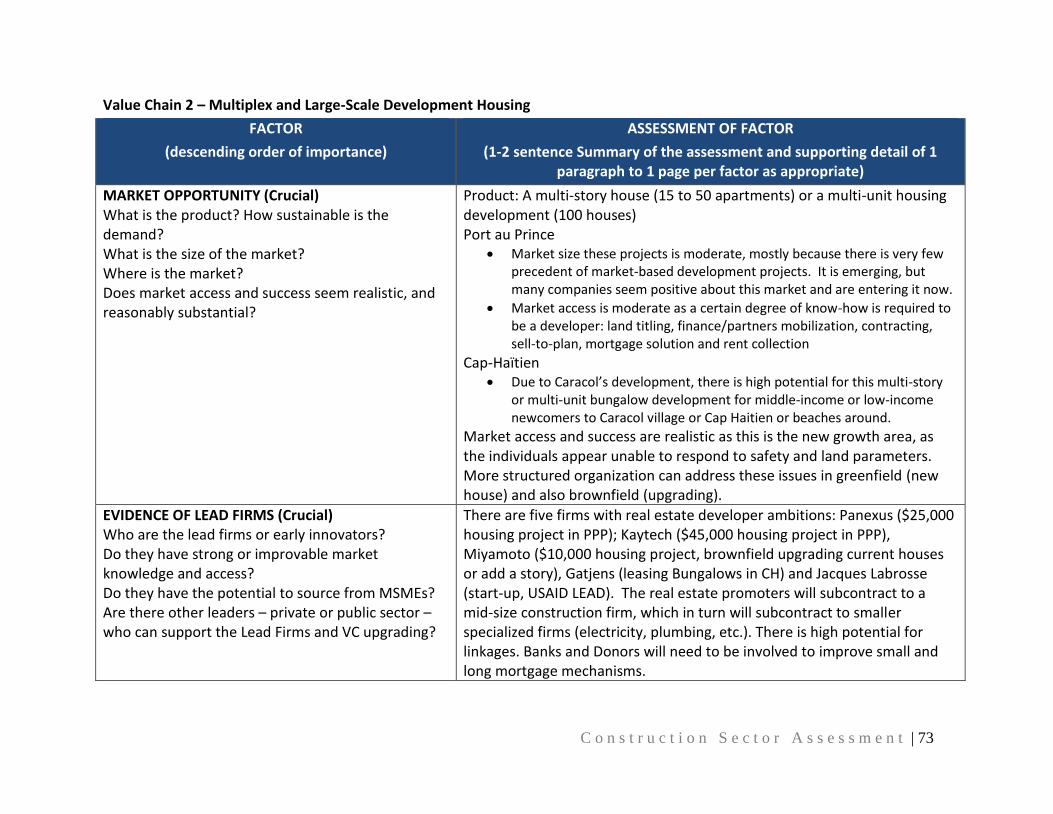

2. Multiplex and Multi-unit Housing Development (VC2)

Promoted by a professional real estate developer, often with a bachelor’s degree in administration or engineering

Design by an engineering firm, based on trust relationships Constructed by a mid-size firm (100 to 250 houses) Occasional third-party supervision firm, especially when financed by

donors Limited construction site inspection, but the developer is more

knowledgeable and can thus provide self-inspection and better supervision

Both informal and formal businesses Mid-size projects between $1,000,000 and $5,000,000 Potential lead firms: Sandbar Island (CH), Panexus (PAP), Miyamoto

(PAP), Cemex (PAP), Kaytech (PAP) High interest, could be high growth—this is not clear

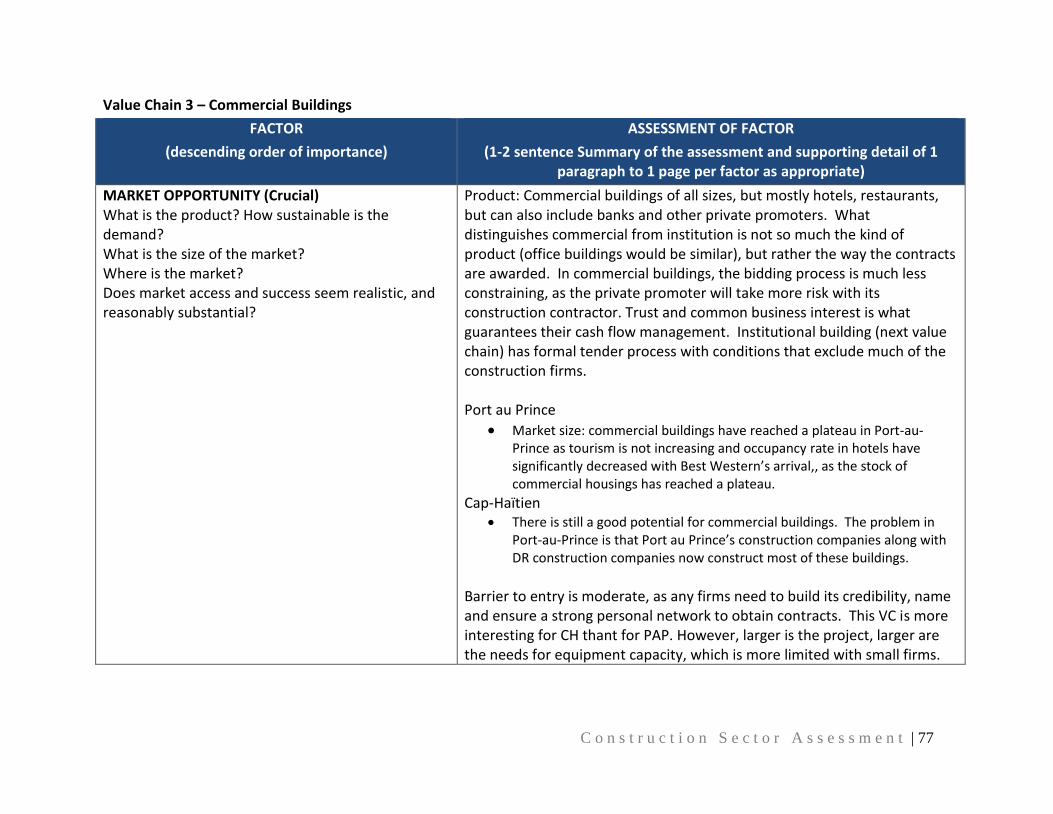

3. Commercial Building (VC3)

Commercial purpose, but the developer might have limited previous experience

Includes hotels, restaurants, offices, stores, etc. Designed by an engineering company, tender processes at times, but

direct contracting more prevalent Constructed by a small- to large-size construction company,

depending on the size of the project and cash flow requirements The private developer rarely requests bank guarantees for cash

advances, but often reduces subsequent payments to account for cash advances

Occasional tender process and third-party supervision firm, but this practice is more frequent in large hotels and restaurants where international standards are expected by customers

Limited construction site inspection Both informal and formal businesses Small-size projects of about $300,000 to large-size projects of up to

$15,000,000 Potential lead firms: Tecina, GF Construction, La Générale

Construction, ARCO, ARCOTECH Slow growth, mostly depending on tourism

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 13

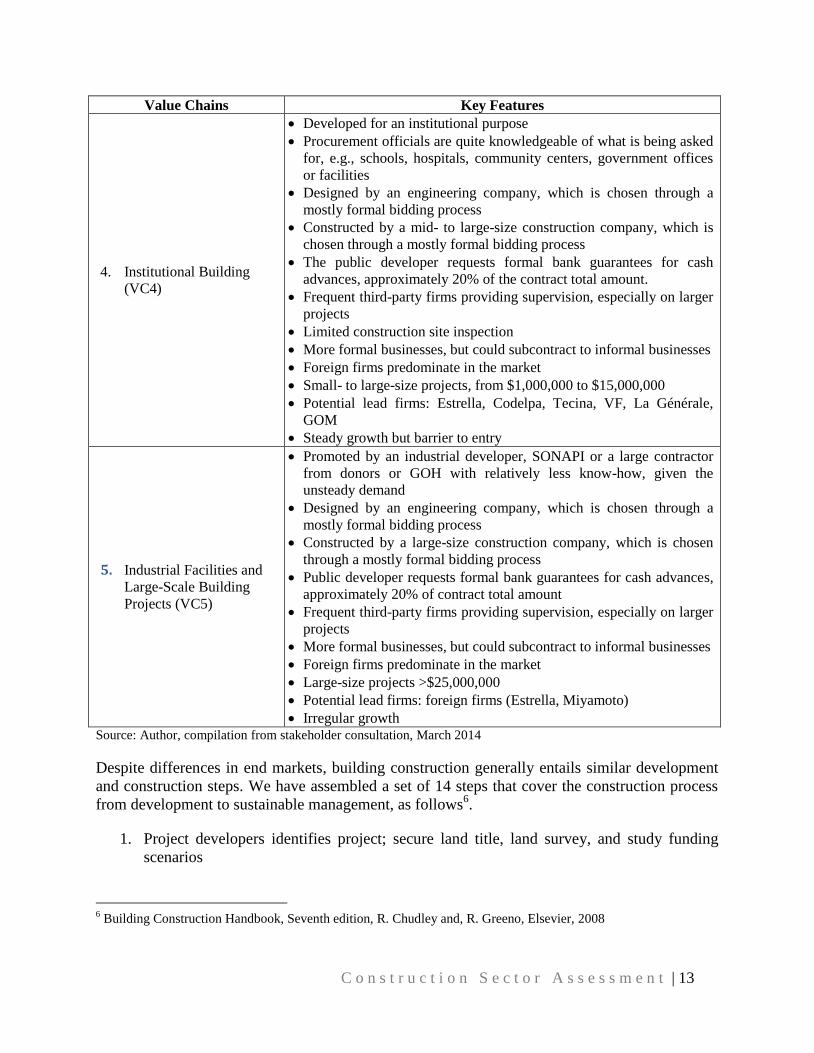

Value Chains Key Features

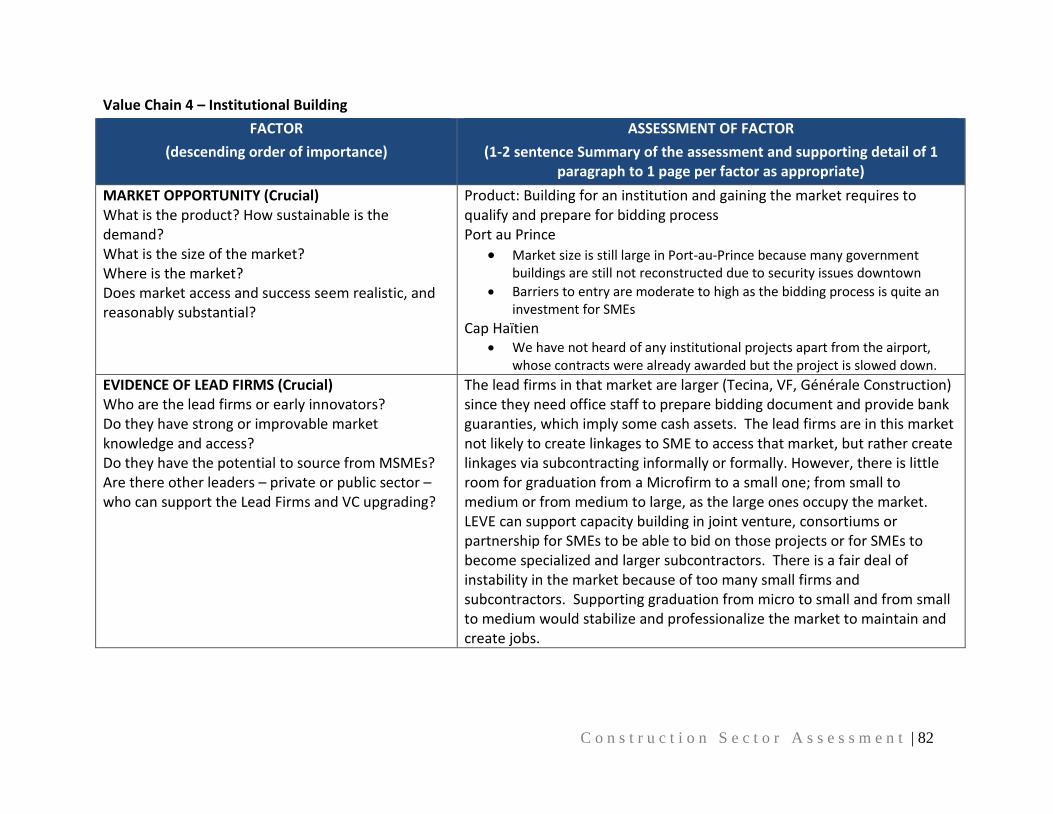

4. Institutional Building (VC4)

Developed for an institutional purpose Procurement officials are quite knowledgeable of what is being asked

for, e.g., schools, hospitals, community centers, government offices or facilities

Designed by an engineering company, which is chosen through a mostly formal bidding process

Constructed by a mid- to large-size construction company, which is chosen through a mostly formal bidding process

The public developer requests formal bank guarantees for cash advances, approximately 20% of the contract total amount.

Frequent third-party firms providing supervision, especially on larger projects

Limited construction site inspection More formal businesses, but could subcontract to informal businesses Foreign firms predominate in the market Small- to large-size projects, from $1,000,000 to $15,000,000 Potential lead firms: Estrella, Codelpa, Tecina, VF, La Générale,

GOM Steady growth but barrier to entry

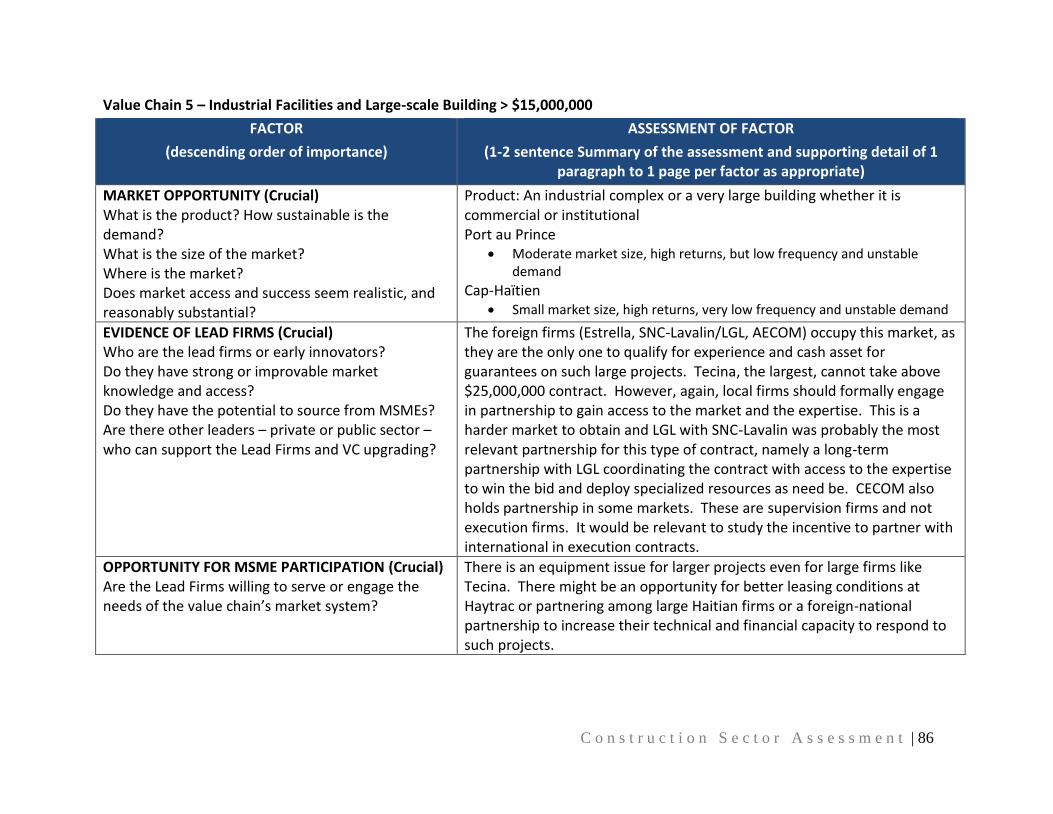

5. Industrial Facilities and Large-Scale Building Projects (VC5)

Promoted by an industrial developer, SONAPI or a large contractor from donors or GOH with relatively less know-how, given the unsteady demand

Designed by an engineering company, which is chosen through a mostly formal bidding process

Constructed by a large-size construction company, which is chosen through a mostly formal bidding process

Public developer requests formal bank guarantees for cash advances, approximately 20% of contract total amount

Frequent third-party firms providing supervision, especially on larger projects

More formal businesses, but could subcontract to informal businesses Foreign firms predominate in the market Large-size projects >$25,000,000 Potential lead firms: foreign firms (Estrella, Miyamoto) Irregular growth

Source: Author, compilation from stakeholder consultation, March 2014

Despite differences in end markets, building construction generally entails similar development and construction steps. We have assembled a set of 14 steps that cover the construction process from development to sustainable management, as follows6.

1. Project developers identifies project; secure land title, land survey, and study funding scenarios

6 Building Construction Handbook, Seventh edition, R. Chudley and, R. Greeno, Elsevier, 2008

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 14

2. Project developer contracts a design engineering/architecture firm for project concept and, if acceptable to the promoter, detailed engineering plans

3. Project developer secures funding and insurance packages

4. Project developer obtains construction permit

5. Project developer with the assistance of the design firm select lead contractor and hire a third-party supervision firm (often the designer)

6. Lead contractor starts subcontracting process (staff mobilization) and procurement strategy.

7. Lead contractor or subcontractor starts demolition, earthwork, and site preparation.

8. Municipality or third party office inspects.

9. Lead contractor or subcontractor builds foundations.

10. Municipality or third party office inspects.

11. Lead contractor or subcontractor mounts rough framing, electrical systems, and plumbing.

12. Municipality or third party office inspects the construction.

13. Lead contractor or subcontractor issues the certification of occupancy if all inspections confirm compliance with building code.

14. Lead contractor ensures adequate project management.

It is important to underscore that the quality assurance/quality control (QA/QC) system for building construction in Haiti is minimal at best. In addition, there has been limited donor funding to improve the QA/QC system, even post-earthquake, forfeiting an opportunity to fundamentally shift the way the construction industry is managed. As a result, access to safer housing for lower income households has not been increased, and construction companies are not monitored in providing these households with safe and quality housing that complies with building codes.

The mayor’s office has the authority for inspections but does not have capacity to provide systematic inspections on each construction site. The Bureau of Building Evaluation (Bureau d’Évaluation des Bâtiments [BEB]), created in the aftermath of the earthquake under the Direction of Public Works at Ministry of Public Work, Transport, and Communication (Ministere des Travaux Publics, Communication, et Transportation [MTPCT]) has created protocols, and the Cabinet issued the building code in 2013. This Bureau did significant capacity building to evaluate the stock of housing and to inspect new housing and is designing protocols within the permitting cycles so that when the building permit is issued, the construction company is presented with an inspection plan.

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 15

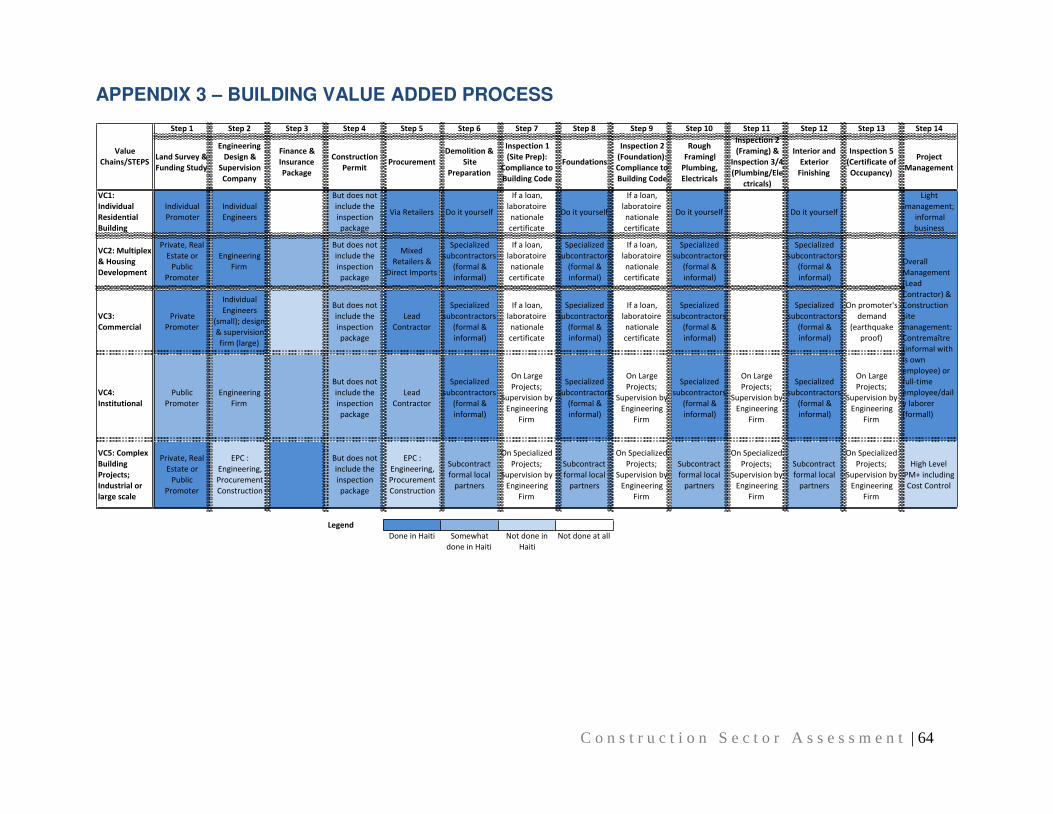

Appendix 3 presents a summary matrix presenting the building value chains, the steps in the chains, and some detailed characteristics at each step of the chains.

3.3.2 Subsector 2: Infrastructure

The infrastructure subsector is less established than the building subsector. The key problem is the level of expertise required to address the variability in project types and demand. Apart from roads and bridges, where demand is steady, all other value chains within this subsector are costly, and government and donor hesitation to allocate significant funding to infrastructure tempers demand. Haitian firms have not developed as much as they could have in this area, and foreign firms are systematically performing better than Haitian firms, except in the road and bridge market, where VF construction and HL are large enough to comply with the bidding rules.

The differentiation factors are also slightly distinct from those in the building sector. What varies between one value chain and another, for instance, is not the project developer, which is most of the time the government or a public-private partnership. The fact that infrastructure projects are financed by public funds has a significant impact on the structure of the industry, which ends up subjected to a cumbersome and constraining bidding process that tends to favor experienced firms with the capacity to provide cash advance guarantees (typically 20% of the total amount of the project). And as with the building subsector, the same factors of complexity in project management and expertise along with the consistency of demand also apply in the infrastructure subsector.

The key differentiation factors in the infrastructure value chains follow.

Final end products—Final products are very different. Infrastructure generally includes transportation, energy, and water domains. Transport usually includes roads, bridges, overpasses, railways, and airports. Energy includes hydropower plants, transmission lines, oil & gas infrastructure, pipelines, and other power sources. Water includes irrigation, water canals, drainage and sanitation, and watershed management.

Technical and project management complexity—Roads are simpler projects than hydropower dams. Levels of expertise and complexity in management vary extensively between infrastructure projects. As a result, larger and more specialized firms will tend to occupy complex value chains, whereas small or medium firms tend to occupy more accessible markets like road and bridges.

Consistency of demand—Large complex infrastructure projects are less frequent than roads and bridges or irrigation projects. As a result, this market tends to be occupied by foreign firms that have access to a larger market to develop the level of specialization required, either from their home base (US or Brazil) or because they export their services all over the world (French for irrigation, Canada for hydropower, Japan for seismic design, etc.). This is one of the reasons the Dominican Republic dominates larger road projects and industrialized countries take on highly specialized work in Haiti.

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 16

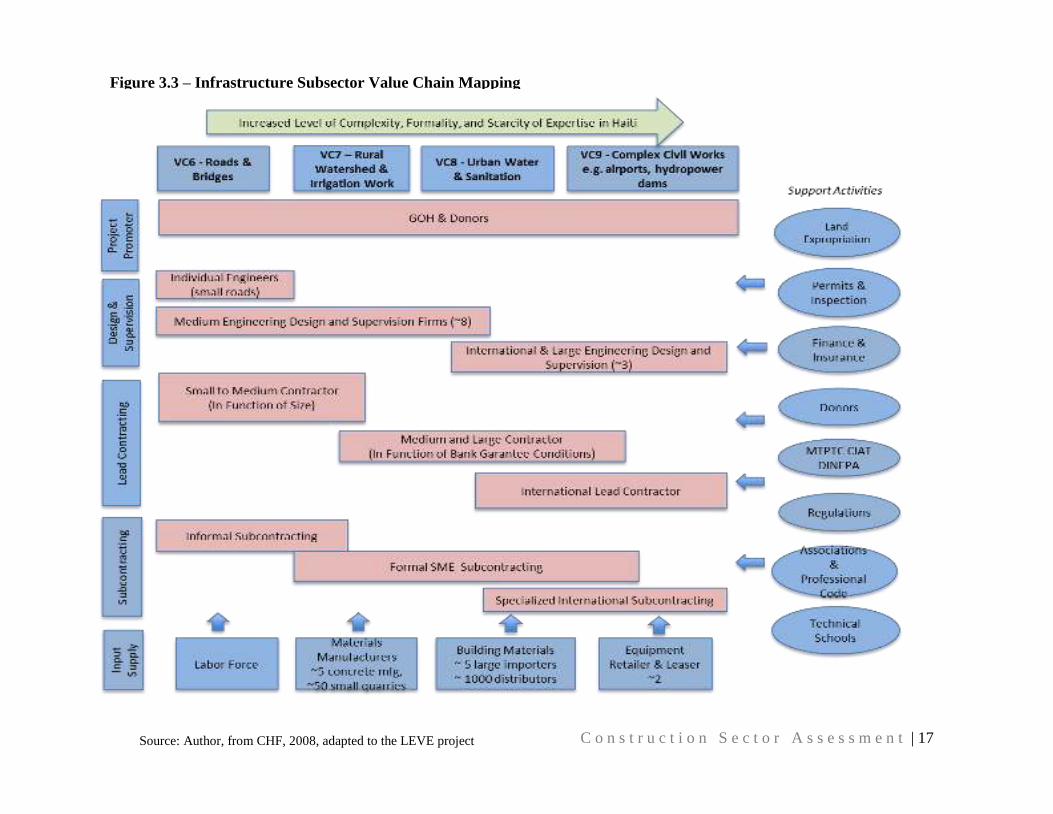

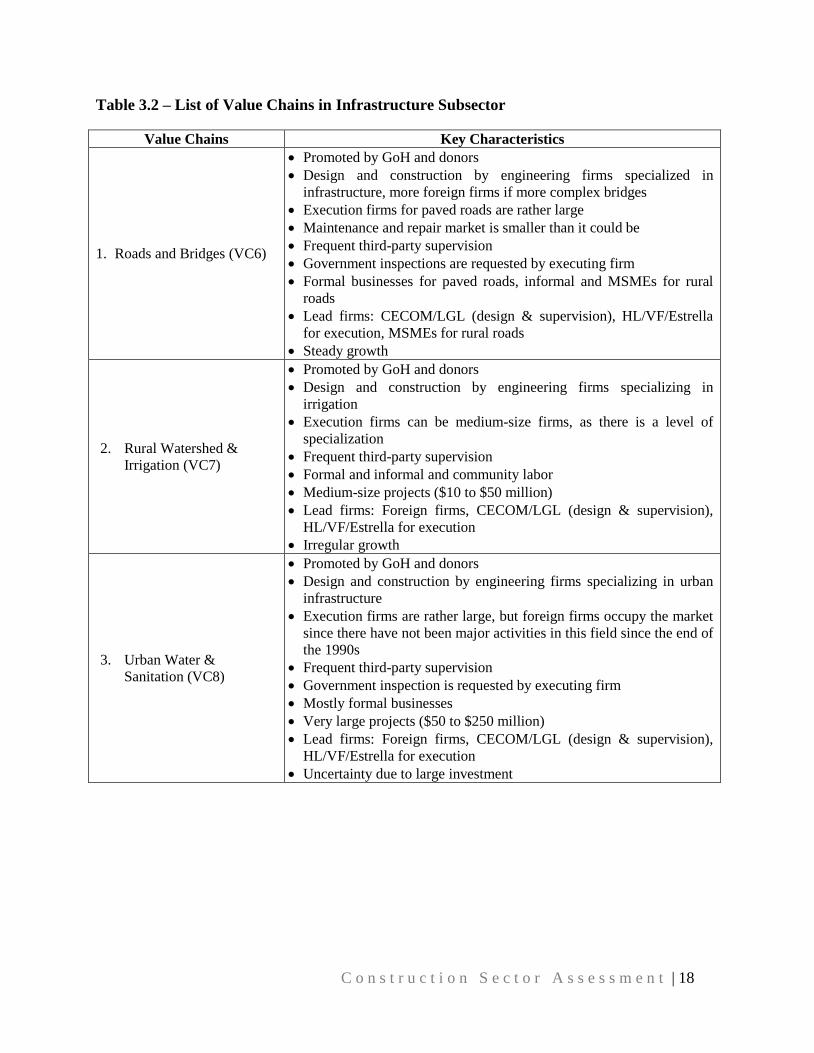

Figure 3.3 illustrates the infrastructure subsector. On the top are the proposed value chains; on the left, the cycle of an infrastructure project; on the bottom, the input factors; and on the right, the supporting services. In the middle are the size and types of stakeholders. Value chains are presented in order of complexity, formality, and scarcity of expertise in Haiti. Table 3.2 describes the key features of each value chain considered for assessment for LEVE in the infrastructure subsector.

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 17

Figure 3.3 – Infrastructure Subsector Value Chain Mapping

Source: Author, from CHF, 2008, adapted to the LEVE project

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 18

Table 3.2 – List of Value Chains in Infrastructure Subsector

Value Chains Key Characteristics

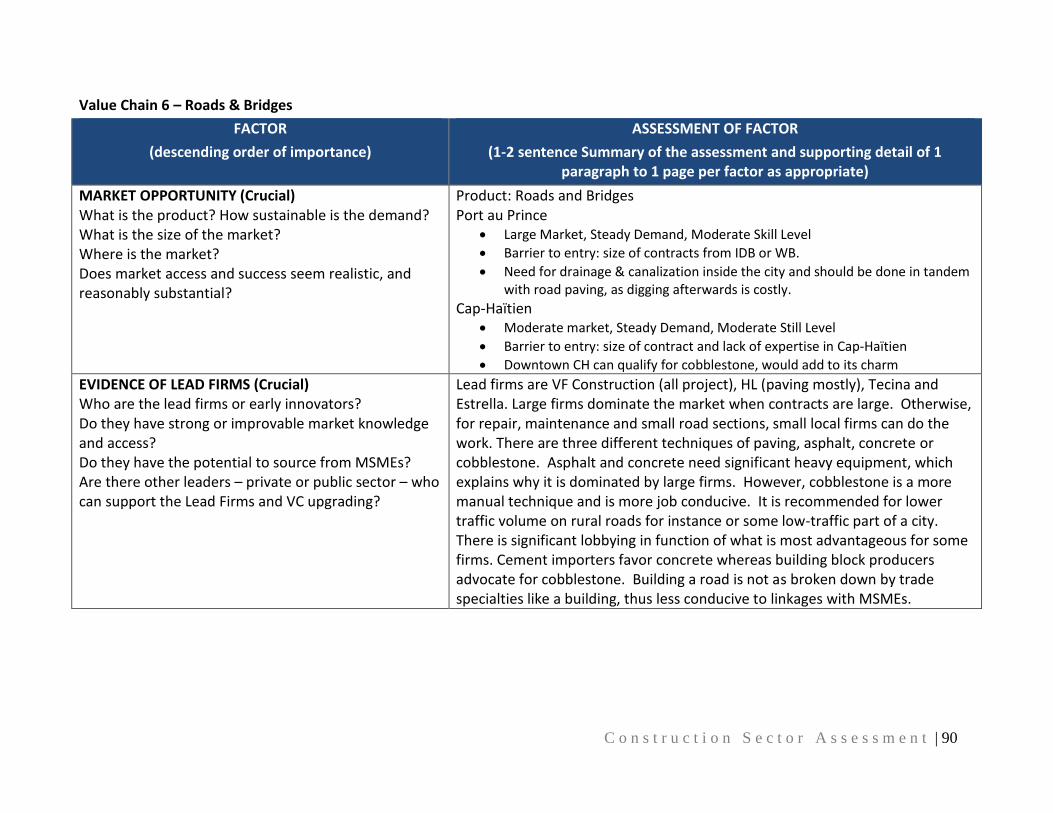

1. Roads and Bridges (VC6)

Promoted by GoH and donors Design and construction by engineering firms specialized in

infrastructure, more foreign firms if more complex bridges Execution firms for paved roads are rather large Maintenance and repair market is smaller than it could be Frequent third-party supervision Government inspections are requested by executing firm Formal businesses for paved roads, informal and MSMEs for rural

roads Lead firms: CECOM/LGL (design & supervision), HL/VF/Estrella

for execution, MSMEs for rural roads Steady growth

2. Rural Watershed & Irrigation (VC7)

Promoted by GoH and donors Design and construction by engineering firms specializing in

irrigation Execution firms can be medium-size firms, as there is a level of

specialization Frequent third-party supervision Formal and informal and community labor Medium-size projects ($10 to $50 million) Lead firms: Foreign firms, CECOM/LGL (design & supervision),

HL/VF/Estrella for execution Irregular growth

3. Urban Water & Sanitation (VC8)

Promoted by GoH and donors Design and construction by engineering firms specializing in urban

infrastructure Execution firms are rather large, but foreign firms occupy the market

since there have not been major activities in this field since the end of the 1990s

Frequent third-party supervision Government inspection is requested by executing firm Mostly formal businesses Very large projects ($50 to $250 million) Lead firms: Foreign firms, CECOM/LGL (design & supervision),

HL/VF/Estrella for execution Uncertainty due to large investment

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 19

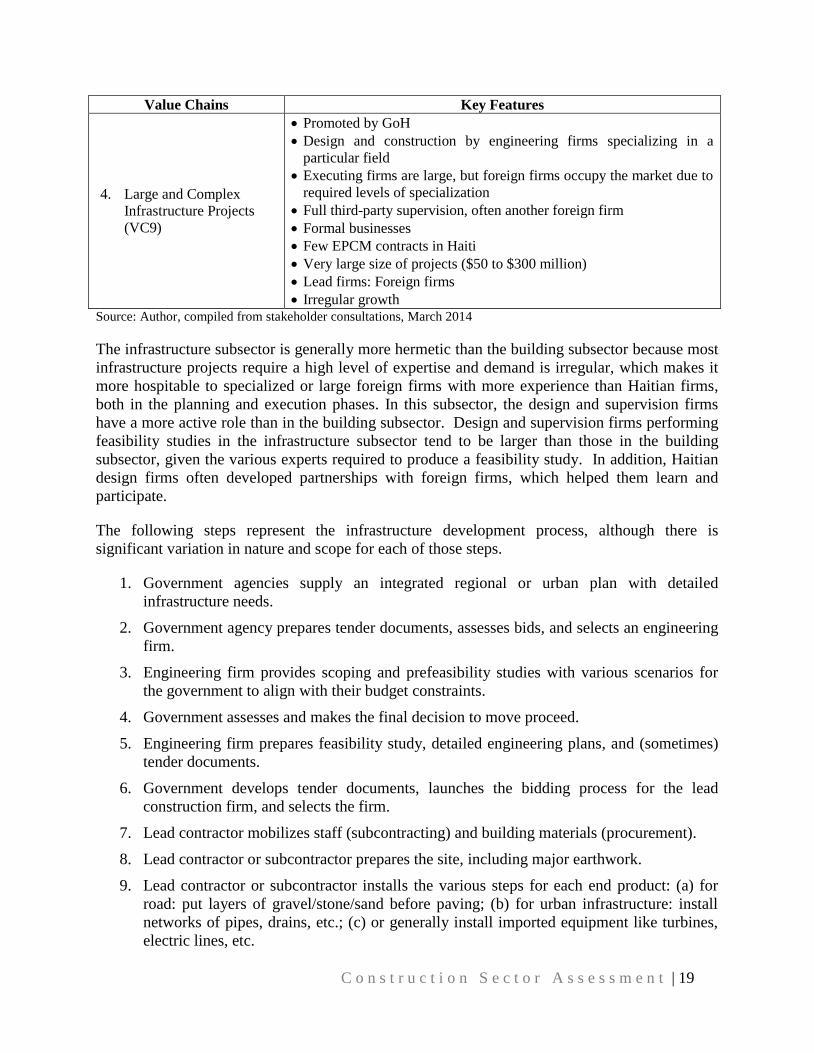

Value Chains Key Features

4. Large and Complex Infrastructure Projects (VC9)

Promoted by GoH Design and construction by engineering firms specializing in a

particular field Executing firms are large, but foreign firms occupy the market due to

required levels of specialization Full third-party supervision, often another foreign firm Formal businesses Few EPCM contracts in Haiti Very large size of projects ($50 to $300 million) Lead firms: Foreign firms Irregular growth

Source: Author, compiled from stakeholder consultations, March 2014

The infrastructure subsector is generally more hermetic than the building subsector because most infrastructure projects require a high level of expertise and demand is irregular, which makes it more hospitable to specialized or large foreign firms with more experience than Haitian firms, both in the planning and execution phases. In this subsector, the design and supervision firms have a more active role than in the building subsector. Design and supervision firms performing feasibility studies in the infrastructure subsector tend to be larger than those in the building subsector, given the various experts required to produce a feasibility study. In addition, Haitian design firms often developed partnerships with foreign firms, which helped them learn and participate.

The following steps represent the infrastructure development process, although there is significant variation in nature and scope for each of those steps.

1. Government agencies supply an integrated regional or urban plan with detailed infrastructure needs.

2. Government agency prepares tender documents, assesses bids, and selects an engineering firm.

3. Engineering firm provides scoping and prefeasibility studies with various scenarios for the government to align with their budget constraints.

4. Government assesses and makes the final decision to move proceed.

5. Engineering firm prepares feasibility study, detailed engineering plans, and (sometimes) tender documents.

6. Government develops tender documents, launches the bidding process for the lead construction firm, and selects the firm.

7. Lead contractor mobilizes staff (subcontracting) and building materials (procurement).

8. Lead contractor or subcontractor prepares the site, including major earthwork.

9. Lead contractor or subcontractor installs the various steps for each end product: (a) for road: put layers of gravel/stone/sand before paving; (b) for urban infrastructure: install networks of pipes, drains, etc.; (c) or generally install imported equipment like turbines, electric lines, etc.

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 20

10. Third party engineering supervision is present throughout the project to ensure that the quality of the design is respected.

11. Lead contractor ensures adequate project management.

A summary matrix presenting the value chains, the steps in the chains, and various characteristics can be found in Appendix 4.

3.4 Stimulating Employment

The construction industry is not a saturated market. Anyone can see there is still significant work to be done at all levels in Haiti. It is generally a competitive industry with many suppliers seeking to access opportunities and demand significantly constrained by the investment climate of Haiti. The construction sector should be supported in improving the supply (quality and ability to access public and larger markets) and stimulating the demand (promote innovations and improve planning and coordination). According to the industry stakeholders and consulted experts, there are eight most-effective ways to generate employment in the construction sector, as follow: 1. Alleviate barriers to entry in public markets. 2. Increase incentives to construct quality and earthquake resistant buildings and infrastructure

to better compete against foreign firms and, by doing so, create inspection-related jobs. 3. Stimulate demand in infrastructure, where numbers of jobs are proportionately lower than in

most developing countries. 4. Promote innovations for commercially driven real estate housing development. 5. Support innovators in their expansion plans to create employment in new business areas. 6. Improve strategies to reduce costs of materials and heavy equipment. 7. Encourage better alignment between supply and demand for MSMEs to enter key markets. 8. Develop the workforce to match the needs of the market to minimize hiring from abroad (see

Section 3.5).

3.4.1 Alleviate Barriers to Entry in Public Markets

Large Haitian firms or foreign firms generally dominate public markets, because MSMEs do not meet basic qualification requirements to enter the market. A key consequence is not only reduced mobility among firms hoping to graduate to larger public markets, but also a diminished competition level among qualifying firms, potentially increasing the profit margins by qualifying firms. Key barriers to entry for MSMEs are as follows. Level of expertise required in the (re)construction of complex work. This argument is valid

for complex civil engineering work like hydropower dams, airports, and industrial parks, which are rarely needed in a smaller country’s development. Most countries contract specialized firms that are likely to be from abroad for these types of projects. If the government determines that these civil works projects will reoccur soon or need repair and maintenance, there would be a strong argument for requiring know-how transfer to Haitian partners. For instance, if new small hydropower dams are to be built in the near future, the know-how transfer is important. In any case, maximizing know-how transfer in the parameters of a project is always a best practice for developing nations. The client should however be ready to spend additional time for training and quality control.

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 21

The perception that Haitian firms will not construct to building codes and earthquake resistant constructions. The building code was adopted in 2012 with great efforts from MTPTC and its constituents, the BEB and the National Laboratory (Laboratoire Nationale). Very few hard copies are in circulation, but it is available o-line. In recent months, MTPTC trained significant numbers of masonry foremen to increase the awareness of earthquake-resistant construction. Although the MTPTC is making serious efforts, the construction industry continues to operate as it did before the earthquake, profit seeking by applying downward pressure on labor and material costs. Because Haiti is a lower income economy, private sector clients are reluctant to pay for quality and safety in the short run, even if the maintenance and repair costs will be lower in the long run. There are rare exceptions of clients ready to invest in a supervising engineering firm to conduct quality control.

The inability of Haitian firms to provide guarantees for cash advances.7 Tenders for public works, though of high interest to entrepreneurs, are not readily accessible by MSMEs, often because of their size and complexity. Only 5 to 10 lead Haitian contractors out of 100 have the capability to respond to large public tenders. The key challenges for Haitian firms are the numbers of years of experience for project managers or lead engineers and the requirements to provide guarantees of cash assets for the equivalent amount of the cash advance planned in the contract. In developed economies, export agencies or insurance companies provide these guarantees to the commercial banks. For the Haitian construction sector, this infrastructure does not exist, and the industry stakeholders have been advocating for developing a guarantee fund that would be pooled for all users and provided by a Haitian bank or donor, but it has not yet implemented. In most countries, the building of a consortium is the best way to address cash flow management, since partner entrepreneurs can pool equipment, workforce, and cash assets on the project. Development banks have standardized procurement policies,8 and significant advocacy would be required to change these terms.

Paperwork or lack of experience in preparing bid documents. Many stakeholders admitted that bidding documents were a deterrent, as some did not build expertise in that regard and are reluctant to allocate resources to do so. Despite other constraints, this might be a problem of perception. Most construction firms have standard documents for bidding as well as set-up processes and just need to adapt these for this new request for proposals (RFP). The investment is thus not completely recurrent.

3.4.2 Increase Incentives for Quality and Earthquake-Resistant Buildings

As stressed in previous sections, the lack of incentives to design and construct quality and earthquake-resistant buildings is a serious problem. Despite the trauma households experienced in 2010, homebuilders still compromise on more water-based concrete and reduced use of rebar, since their clients do not have sufficient income to have their houses constructed to building

7 Stakeholders were especially concerned with advance payment guarantees, which consist of a deposit to the bank of between 20 to 30% of the total value of a contract to ensure that the client’s advance payment will be used for starting that contract and nothing else. A bid bond is less (3 to 5%) of the total amount and consists of paying the client, if the bidder won and cannot commence the work. A performance bond (or completion bond) is a contract providing protection to the client, if the contractor becomes insolvent or cannot complete the work. For instance, with the IDB or World Bank, it is possible to use an advance payment guarantee as an alternative to performance bonds, but both tools serve an equivalent purpose and present approximately the same burden for contractors. The bid bond is more systematic in most contracts. 8 Prequalification for Procurement of Works and User’s Guide, The Inter-American Development Bank, 2011

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 22

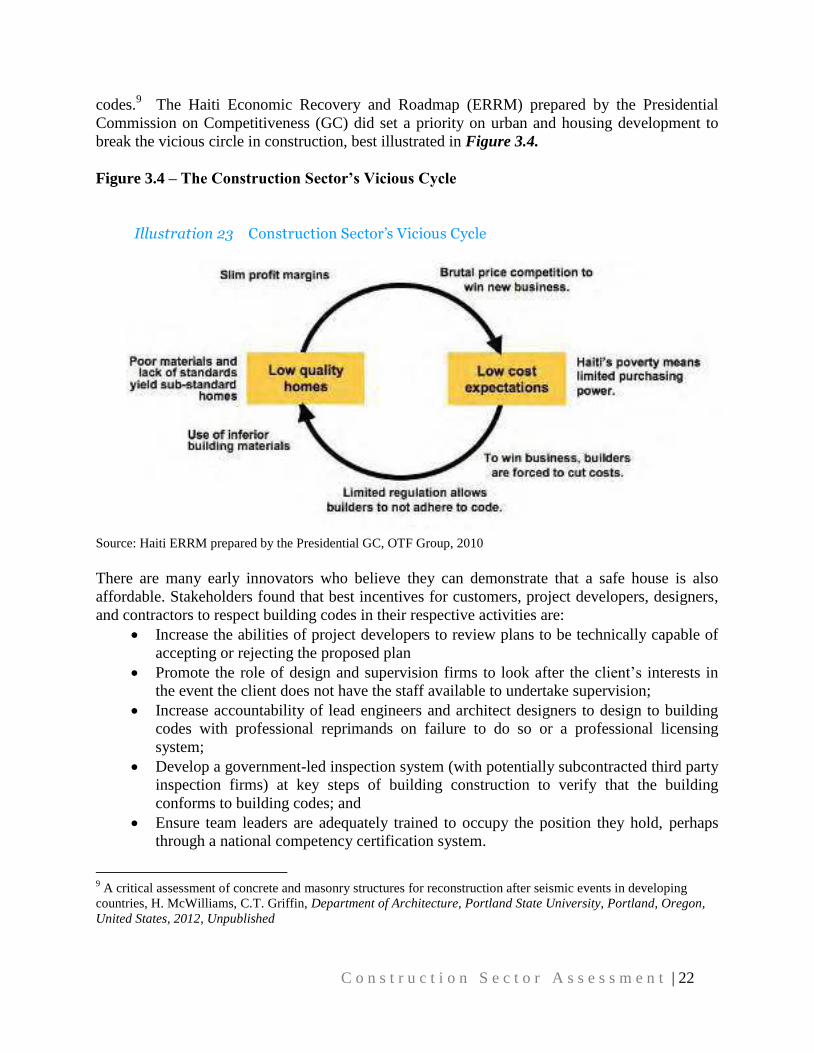

codes.9 The Haiti Economic Recovery and Roadmap (ERRM) prepared by the Presidential Commission on Competitiveness (GC) did set a priority on urban and housing development to break the vicious circle in construction, best illustrated in Figure 3.4. Figure 3.4 – The Construction Sector’s Vicious Cycle

Source: Haiti ERRM prepared by the Presidential GC, OTF Group, 2010 There are many early innovators who believe they can demonstrate that a safe house is also affordable. Stakeholders found that best incentives for customers, project developers, designers, and contractors to respect building codes in their respective activities are:

Increase the abilities of project developers to review plans to be technically capable of accepting or rejecting the proposed plan

Promote the role of design and supervision firms to look after the client’s interests in the event the client does not have the staff available to undertake supervision;

Increase accountability of lead engineers and architect designers to design to building codes with professional reprimands on failure to do so or a professional licensing system;

Develop a government-led inspection system (with potentially subcontracted third party inspection firms) at key steps of building construction to verify that the building conforms to building codes; and

Ensure team leaders are adequately trained to occupy the position they hold, perhaps through a national competency certification system.

9 A critical assessment of concrete and masonry structures for reconstruction after seismic events in developing countries, H. McWilliams, C.T. Griffin, Department of Architecture, Portland State University, Portland, Oregon, United States, 2012, Unpublished

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 23

These various systems take years to put in place, but the industry stakeholders are convinced a change is urgently needed to gain more public markets and also to ensure safety in the country with the next earthquake. LEVE should facilitate the elaboration of an action plan among key enablers with realistic short-term and mid-term objectives. Quality building will enhance the reputation of Haitian firms, helping them access additional markets and create jobs. In addition, inspection skills will be developed, and jobs will be created.

3.4.3 Stimulate Demand in Infrastructure

Surprisingly, Port-au-Prince’s reconstruction did not result in significant urban infrastructure development. The overall costs of urban infrastructure development in water and sanitation in Port-au-Prince are probably well above $1 billion. Even smaller sections, like the water basin of Tabarre and environs, cost more than $200 million, which is almost the entire IDB yearly budget for Haiti. The very high costs of urban infrastructure will require creativity not only in funding patterns, but also in the city’s priority system. If the overall reconstruction of urban infrastructure takes 10 to 15 years, it is essential that the first 5 years be focused on the most pressing aspects. Stakeholders believed that the best thing LEVE could do to create jobs was to stimulate the urban infrastructure demand and ensure a role in the construction for Haitian firms. There is also a vision (Pillar I from the Private Sector Forum10) to try to bring foreign direct investment in infrastructure projects, and this should be considered as another strategy to stimulate the demand.

3.4.4 Promote Commercially Viable Safe and Affordable Housing

Development

Since the earthquake, the housing value chain especially witnessed donor-supplied housing development projects for relief purposes, or government-led social housing projects. These projects were developed after a catastrophe and thus could not have been privately led housing developments. There is still a great need for social housing development projects, which should be promoted in line with the master plan from the Ministry of Planning and External Cooperation (Ministère de la Planification et de la Coopération Externe [MPCE]) for Port-au-Prince11 along with the National Policy for Housing (Politique Nationale du Logement et de l’Habitat [PNLH]) recently developed by the Public Building and Housing Coordination Unit (UCLBP).12 The Private Sector Forum also articulated significant necessary reforms in Pillar IV of the report13 to encourage private investment in housing. However, to truly address the shortage of housing in Port-au-Prince, it is also important that commercially viable solutions emerge to supply various segments of the market. Innovative manufacturers are developing housing for low- to middle-income households, while others are looking at retrofitting the current stock of housing by adding additional floors in a safe and affordable manner. This will call for creativity, and many developing nations can provide good practices to promote private sector provision of low-income housing. For instance, Cemex in Mexico has been a pioneer and could provide that expertise to

10 Vision and Roadmap for Haiti Prepared by the Private Sector Economic Forum Final Draft Version, March 23, 2010 11 Cité administrative de Port-au-Prince, Lignes directrices d’aménagement, Gouvernement de la République d’Haïti, Ministère de la Planification et de la Coopération Externe, Août 2012. 12Politique Nationale du Logement et de l’Habitat (PNLH), UCLBP, 2013 13 Ibid

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 24

Haiti.14. Market studies on housing markets in Haiti were performed in 2010 at USAID.15. LEVE could gather information and share it in a user-friendly format to various innovators in real estate development.

3.4.5 Support Expansion of Innovators

Entrepreneurship in Haiti is a real blessing, as many developing countries cannot boast of this comparative advantage. During the course of the assessment, at least 10 to 15 MSMEs had viable business ideas and capital. Some needed support in commercialization of their business ideas, and others needed governance support. With the help of LEVE’s small fund and the Organizational Capacity Assessment Tool (OCAT), MSMEs will be directly or indirectly supported to create job opportunities in Port-au-Prince and Cap-Haïtien.

3.4.6 Reduce Costs of Building Materials and Heavy Equipment

Haitian firms are importing most of their building materials, except for basic concrete components that are extracted in Haiti. In terms of heavy machinery, firms need to acquire from retailers in Haiti, or hold an expensive leasing agreement. If Haitian firms can reduce the costs of material and heavy machinery (almost 75% of construction costs), there will be a direct effect on additional employment and profit. Stakeholders expressed their disappointment toward unfavorable taxation or tariff schemes between importers and value addition manufacturers, which to them completely discourage the industry from doing value addition. Infant industry protective schemes existed (and still do) in the Dominican Republic, but not in Haiti. In addition, there is a bargaining power issue between small construction firms and large importers. There might be ways to realize economies of scales through association networks or cooperatives to increase economies of scale on building materials and heavy equipment.

3.4.7 Encourage Better Alignment between Supply and Demand for MSMEs

MSMEs are left out of most public markets, even where they actually have the technical and managerial capacities to operate. MSMEs are still challenged by informality, which can be a requirement to work with larger lead contractors, as taxations increase labor costs of formal firms. This informality is a barrier in itself, as the firm cannot publicly market its services and, at worst, cannot become a contractor for the public market. In the construction industry, the public market represents a higher proportion of the demand than other economic sectors because the GOH and donors sponsor many segments of its demand, such as schools, hospitals, public offices, roads and bridges, and all infrastructure projects. The private market is more open to MSMEs, but at times informality will prevent the MSME from truly making a name and obtaining new clients. MSMEs should be key suppliers of mid- to small-size schools, hospitals, unpaved and paved roads and bridges, maintenance and repair contracts, small to mid-size buildings and small to mid-size infrastructure works. Encouraging better conditions for MSME will increase the supply, potentially reduce costs, and consequently, stimulate the demand.

14 “A Value Chain Framework For Affordable Housing in Emerging Countries,” Bruce Ferguson, Global Urban Development, Volume 4 Issue 2, November 2008, and 14 Housing Demand in Port-au-Prince, FS Share, Chemonics International, USAID, 2011. 15 Housing for Haiti’s Middle ClassPost-Earthquake Diagnosis and Strategy Final Report 29 September 2010 September 2010, by Nathan Associates Inc. for review by USAID.

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 25

3.5 Developing the Workforce

3.5.1 Characteristics of a Project-Based Industry

The construction sector in most countries suffers from a chronic workforce development deficit because it is a project-based industry with a very short-term outlook on workforce development. Apart from the core team of engineers, technicians, and administrators who have full-time positions, the bulk of the workforce is subcontracted, and the lead contractors do not expect to provide training and supervision of the workforce. This reality is key to understand that training in the construction sector does not take place within firms, as is the case for sectors that are significantly less project-based, such as manufacturing or hotels and accommodation, or for industries that hire on a permanent basis. In this context, countries must find ways to increase workforce capabilities despite this project-based mentality through regulated requirements on engineers, technicians, and presence on a construction site.

Haiti also has two key problems with regard to workforce development. First, most construction companies are not specialized because the market is very competitive and small. If a company specializes in one market, it will succeed only if the company takes a good chunk of the market and if the market has steady demand. Otherwise, there will be too much down time and the company will not be able to grow. The small size of the market creates a culture of subsistence, like in agriculture. To minimize its business risk, the construction firm does many different types of work (housing, institutional buildings, and roads) and also different types of trades (masonry, electricity, plumbing, finishing, etc.). The constraint created by this lack of specialization is that the firms are not building experience in the same field, hence they are not increasing skills to the highest level possible. Second, these small, informal subcontractors are still used today, even by very large formal firms, in order to decrease costs of labor, primarily by avoiding the 30% profit taxes that would result from using a formal subcontractor. It is likely that this informal sector aggravates the skills shortage in the industry, as informal firms have significantly less control over project demand. They suffer from even more volatility than the lead construction firms and the formal subcontractors, which in turn, can market their services out in the open and get more business. This dependence and volatility makes investing in the workforce risky and unlikely.

Increasing skill in the construction industry is very important, as it acutely affects the safety of building and infrastructure construction in the country, which has just experienced the trauma of a devastating earthquake. As of now, there have been no efficient remedies to the low-cost low-quality building mentality, because Haitian customers are not ready to pay for quality and safety. One way to resolve this issue is a supply-driven mentality change to convince customers that the costs are not much higher if they think more long term.

By upgrading the workforce, numerous newcomers in the industry at all levels will have learned good practices and promote them. Customers and suppliers with new capable workforce can bring about this shift in mentality.

3.5.2 Industry Demand

The sector suffers from a skills deficit, especially in project management and in the semi- and specialized needs of the industry. Good indicators for understanding the skilled labor shortage

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 26

are the presence of foreigners occupying positions in the sector and several construction skill assessments found online regarding construction.16 The most serious issues expressed by the industry regarding their role in the value chains are as follows.

Estate development—There is currently no formal training in Haiti to develop multiplex and multi-unit housing development. It is relevant to have workforce developed in Haiti in these areas, since private investors from abroad react to risks and instabilities in a different way than private investors from Haiti.

Design and supervision—Engineers and architects are well trained in Haiti (even better than in the Dominican Republic according to many), but there is a shortage of well-trained Haitians in areas such as geographic information system (GIS) and computer-assisted design (CAD) drawings, as most Haitian schools still teach with drawing tables.

Production of input material—Most building materials are imported, but concrete, a significant input in any construction project, is mixed in Haiti. Quality of production is uneven, and there is a lack of standardization, which usually is symptomatic of a lack of supervision or lack of incentive to buy premixed concrete. Supervisors are most likely insufficiently trained or receive cost-cutting pressure to add more water than cement. Normally a technical degree in civil engineering is required for supervisory functions as a good grasp of the physical aspects of concrete and structure is essential.

Heavy machinery—The operation of machines is being done more and more by Haitians, primarily trained at the HayTrac training facilities, but there is still significant work to be done, especially in maintenance and repair of the machines, which require trained mechanics.

Execution—The industry complained of the poor project management skills of Haitian employees, particularly on construction sites. Usually, technical training does not include project management, as the private firm usually provides the project management. In Haiti, given the pressure on cost, no one is currently being trained in project management as construction site managers (typically a three-year degree as a technician in civil engineering) or foremen (typically one year of training in a special trade like masonry, electricity, plumbing).

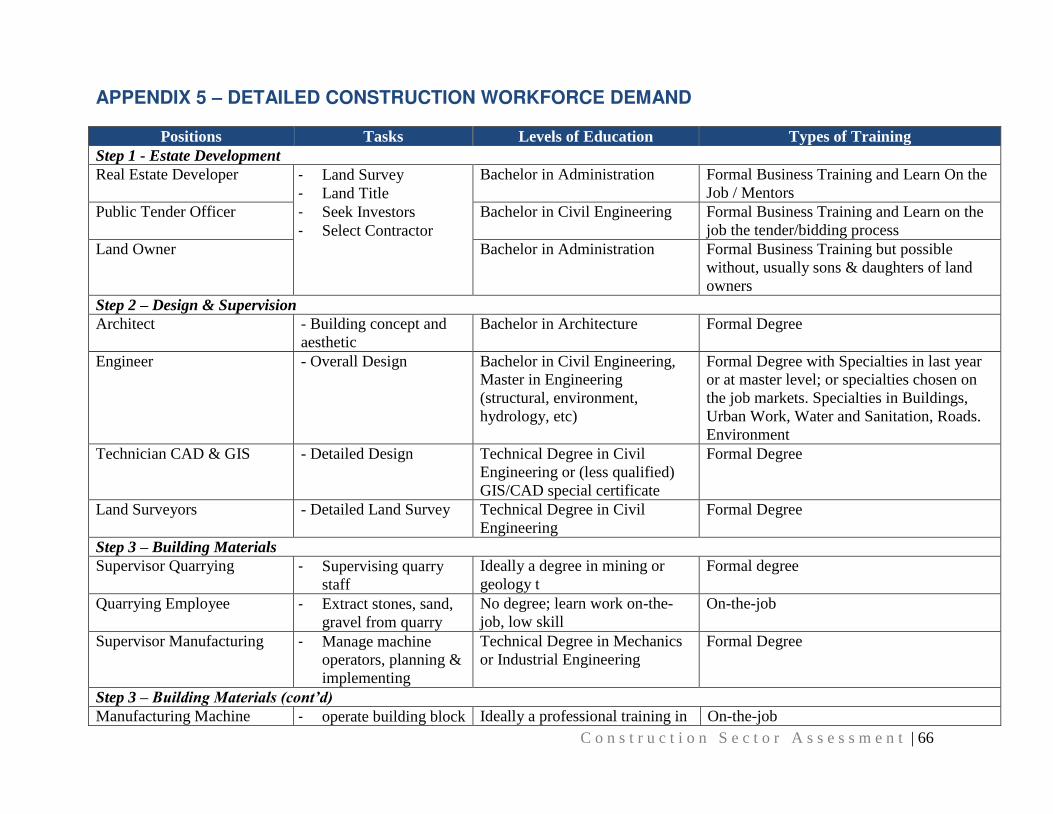

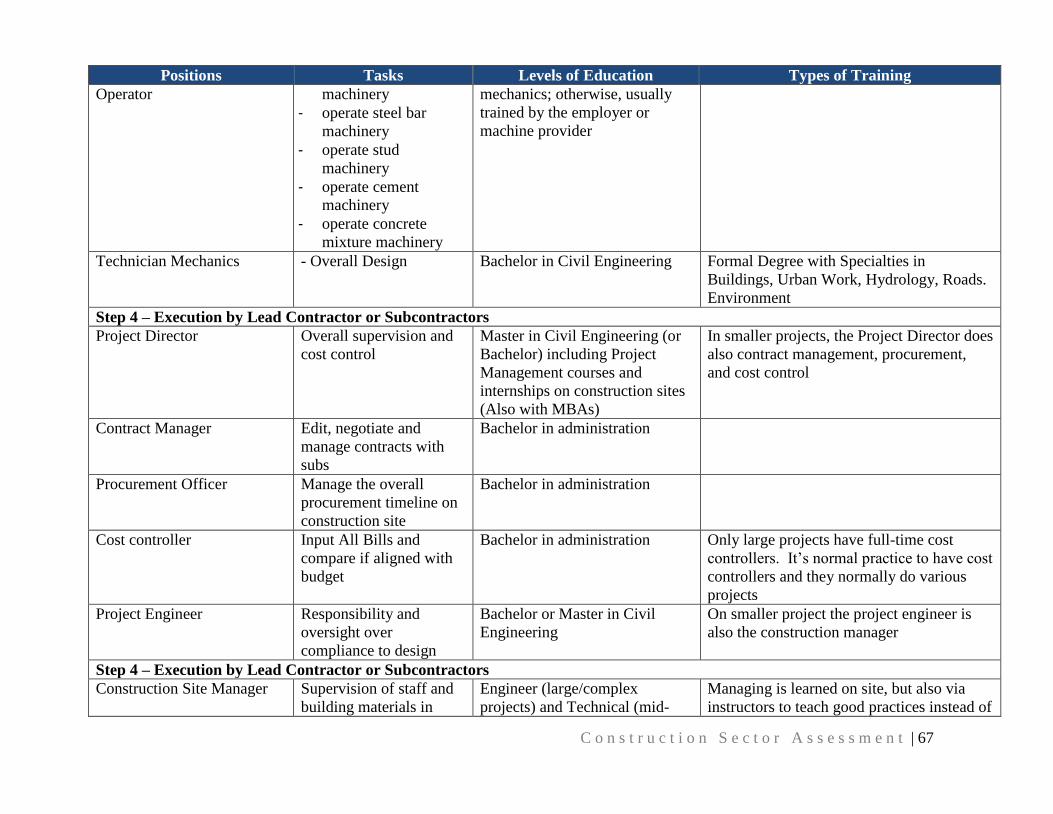

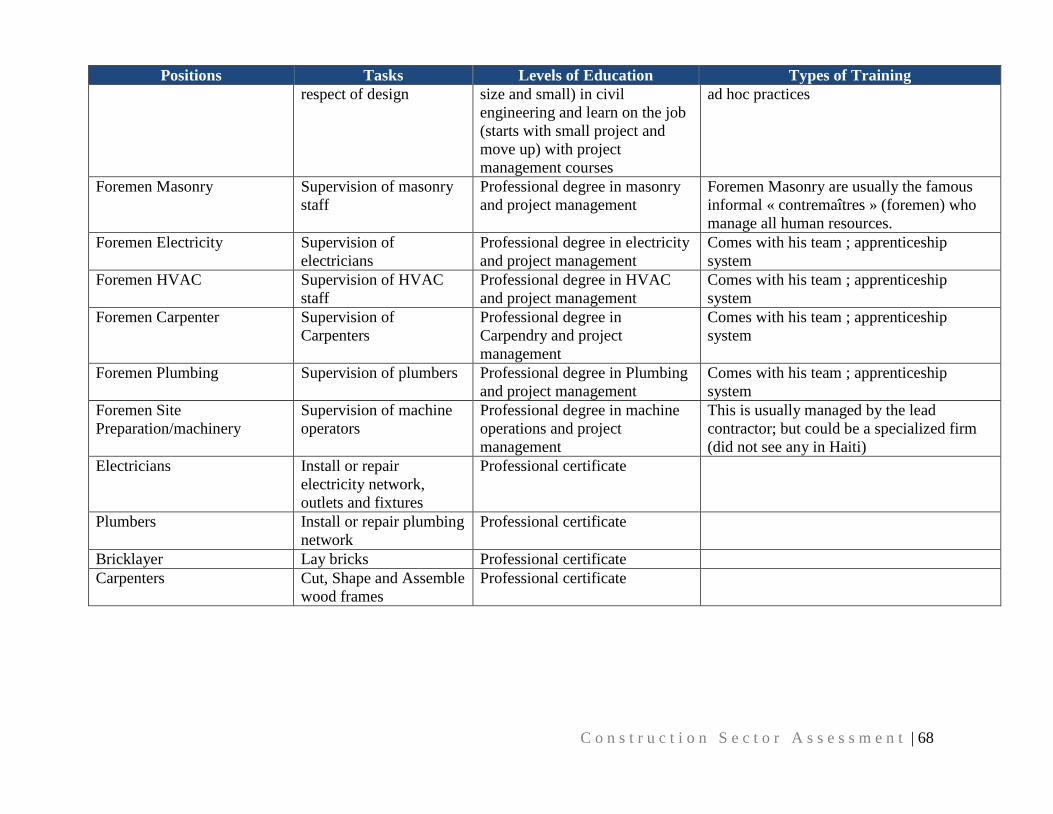

The industry demand for skills is detailed in Appendix 5, but more details on the industry supply and the misalignment of both will be detailed in the workforce development report for the three sectors.

4. VALUE CHAIN SELECTION ASSESSMENT The process of value chain selection assessment is important for many international development projects seeking a particular focus on value chain upgrade approaches. The choice relies on important criteria of market opportunities, competitiveness, presence of lead firms, potential for 16 Rwanda Skills Survey 2012, Construction Sector Report, Rwandan Development Board and Human Resource and Skill Requirements in the Building, Construction and Real Estate Services, A Report, National Skill Development Corporation (NSDC), India, 2010.

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 27

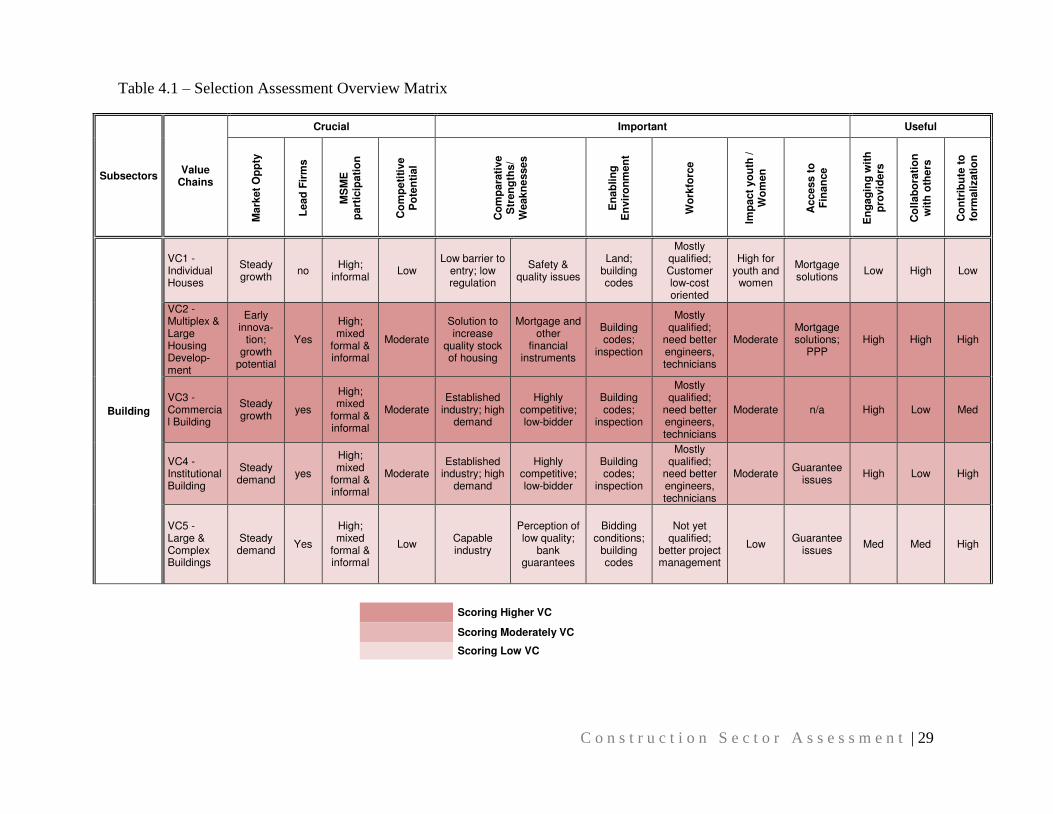

linkages to MSMEs, enabling environment baseline conditions, and the like. This section provides a summary analysis at the subsector level, and detailed assessment matrices are provided in Appendix 6 for each value chain. A summary matrix is presented in Table 4.1 to provide an overview of the value chain selection process and support the following argumentation for selection of specific value chains. In lighter red are the value chains for which the crucial and important criteria are less convincing, whereas in darker red are the value chains for which crucial and important criteria are more convincing. There are also regional variations between Cap-Haïtien and Port-au-Prince summarized in last section.

4.1 Building Value Chains

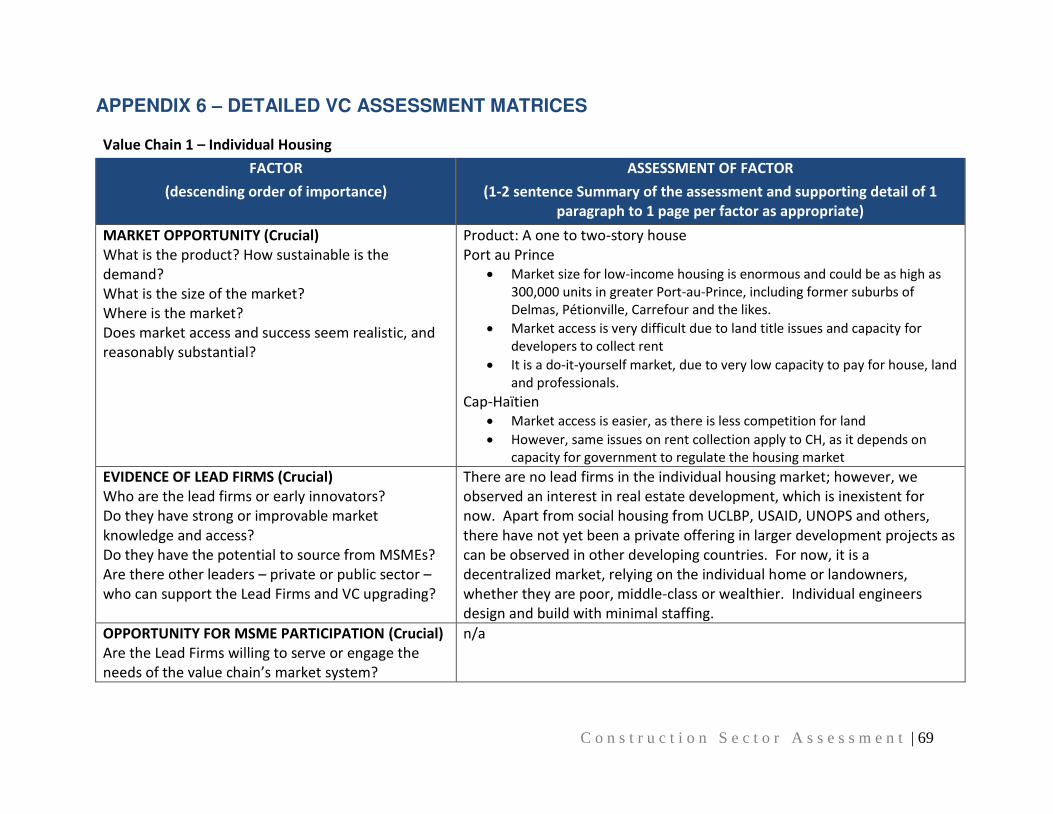

There are three value chains (multiplex housing development, commercial buildings, and institutional buildings) that are more conducive to value chain upgrading because they meet crucial and important criteria, while the two other value chains (individual housing and industrial complex buildings) are not good candidates for upgrading because of their very challenging structure. The factors that justify that selection are as follows. Market opportunity (crucial) —Of all value chains, individual housing (VC1) has the largest volume and potentially the highest demand of all value chains, followed by the multiplex housing development (VC2) and the institutional building (VC4). The real estate housing development projects currently proposed on the market are innovative, and developers are enthusiastic about market opportunities for middle-income houses ($25,000 to $45,000) and low-income houses (brownfield17 $10,000). Nonetheless, significant financial obstacles must be overcome. The commercial building value chain (VC3) is very competitive yet it is currently stagnating due to high investment in tourism in the last two years. The occupancy rates at other hotels have dropped to 60% since the Best Western opened in 2013, which is symptomatic of a slowdown in the commercial buildings in Port-au-Prince, according to many stakeholders. However, in Cap-Haïtien, it’s the opposite: the commercial building sector (VC3) is more attractive than the institutional market, since the international airport will be completed soon and will attract customers from the US/Canada and elsewhere. The Northern Tourist Association has a clear plan and strong mobilization of its stakeholders.18 As for large complex facilities (VC5) in Cap-Haïtien and Port-au-Prince, demand for additional industrial complex construction is very uncertain. Elections this fall are also slowing down investment, according to some, but not significantly, according to others. Many believe business conditions are better now than ever in the last decades. Lead firms (crucial)—All value chains have lead firms, except individual housing (VC1), which is characterized by a highly unstructured value chain, with not even some association networks such as owners’ associations, tenants’ associations, real estate associations, or

17 Brownfield in construction jargon stands for repair, overhaul, and expansion of an already existing construction. In this case, low-income households could pay for a safety and expansion upgrade for approximately $10,000. Adding floors could contribute to the densification of Port-au-Prince and ensure earthquake-proof structures. 18 “Pour une Meilleure Exploitation des Opportunités Touristiques de la Région du Nord (Vision du Secteur Hôtelier)”, Comité de Direction Régional Nord de l’Association Touristique d’Haïti & ATH NORD, TechnoServe/HIFIVE

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 28

cooperative housing projects. Apart from social housing projects from UCLBP, that value chain has almost no handle to pull on in order to upgrade it. However, given the inter-linkages of firms with subsistence construction practices,19 upgrading other value chains should have spillover effects on the individual housing value chain. Indeed, the multiplex and large housing development value chains (VC2) could innovate in providing new housing stock and inspiring some individual engineers in the market to propose such houses to their clientele. New manufacturers recently arrived in Port-au-Prince (Kaytech, Veerhouse Voda, YCF, etc.) to seek buyers for their technical solutions, whether they are individual owners or real estate developers. The commercial (VC3) and institutional (VC4) value chains have many lead firms, but the former has more room for MSMEs than the latter, due to the latters’ requirements in the bidding process. Thus, lead firms in the commercial sector are actually smaller than in the institutional building value chain. In the institutional building market, larger firms are more active, as are even Dominican firms, due to the banking guarantee constraint (see Enabling environment, below). Foreign firms or the largest Haitian firms lead the last value chain, large complex buildings (VC5), and even more important constraints close this market to MSMEs. MSME participation (crucial) —The network of MSMEs in the building subsector is significant. The most open market with the most possibilities for MSMEs to expand is in the commercial building value chain (VC3), since there is no bidding process blocking access to market for MSMEs. In the individual housing market (VC1), there are micro- and small firms that could graduate to access the commercial building market. The other value chains (VC2, real estate housing projects; VC4, institutional buildings; and VC5, large complex buildings), although closed off to MSME as lead contractors, are nonetheless open to them as formal or informal subcontractors. MSMEs are found in specialized markets such as electrical systems, plumbing, HVAC, and finishing, because they do not require permanent presence on the construction site. MSMEs in those value chains have high potential for upgrade, since their clients have high incentives to see them strengthened.

19 As described in a previous section, subsistence construction refers to the organizational behavior to occupy all markets to ensure stable income and minimize risks of falling idle and, worst, out of business.

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 29

Subsectors Value

Chains

Crucial Important Useful

Ma

rket

Op

pty

Le

ad

Fir

ms

MS

ME

p

art

icip

ati

on

Co

mp

eti

tive

Po

ten

tial

Co

mp

ara

tive

Str

en

gth

s/

Weakn

esses

En

ab

lin

g

En

vir

on

men

t

Wo

rkfo

rce

Imp

act

yo

uth

/

Wo

men

Access t

o

Fin

an

ce

En

ga

gin

g w

ith

p

rov

iders

Co

llab

ora

tio

n

wit

h o

the

rs

Co

ntr

ibu

te t

o

form

alizati

on

Building

VC1 - Individual Houses

Steady growth

no High;

informal Low

Low barrier to entry; low regulation

Safety & quality issues

Land; building codes

Mostly qualified; Customer low-cost oriented

High for youth and

women

Mortgage solutions

Low High Low

VC2 - Multiplex & Large Housing Develop-ment

Early innova-

tion; growth

potential

Yes

High; mixed

formal & informal

Moderate

Solution to increase

quality stock of housing

Mortgage and other

financial instruments

Building codes;

inspection

Mostly qualified;

need better engineers, technicians

Moderate Mortgage solutions;

PPP High High High

VC3 - Commercial Building

Steady growth

yes

High; mixed

formal & informal

Moderate Established

industry; high demand

Highly competitive; low-bidder

Building codes;

inspection

Mostly qualified;

need better engineers, technicians

Moderate n/a High Low Med

VC4 - Institutional Building

Steady demand

yes

High; mixed

formal & informal

Moderate Established

industry; high demand

Highly competitive; low-bidder

Building codes;

inspection

Mostly qualified;

need better engineers, technicians

Moderate Guarantee

issues High Low High

VC5 - Large & Complex Buildings

Steady demand

Yes

High; mixed

formal & informal

Low Capable industry

Perception of low quality;

bank guarantees

Bidding conditions;

building codes

Not yet qualified;

better project management

Low Guarantee

issues Med Med High

Scoring Higher VC

Scoring Moderately VC

Scoring Low VC

Table 4.1 – Selection Assessment Overview Matrix

C o n s t r u c t i o n S e c t o r A s s e s s m e n t | 30