Embed Size (px)

Citation preview

1

•

Value CreationBaCkground PaPer

2

The Technical Task Force of the International Integrated Reporting Council (IIRC) established a Technical Collaboration Group (TCG) to prepare this Background Paper. The TCG was coordinated by the lead organizations with input from participants from a range of disciplines and countries. This paper reflects the collective views of TCG participants, not necessarily those of their organizations or the IIRC.

The IIRC considered interim findings from the TCG when preparing the Prototype Framework released in November 2012, and considered aspects of this paper in developing its Consultation Draft of the International Integrated Reporting (<IR>) Framework.

The IIRC gratefully acknowledges the contributions made by the following in the drafting of this Background Paper:

lead organiZation Ernst & Young LLP (EY)

Steering CoMMittee Susan Blesener, The Art of Value Pedro Faria, CDP Jonathan Hanks, Incite Sustainability Rowland Hill, Marks & Spencer Bob Massie, New Economics Institute David Matthews, KPMG Tom Rotherham, Hermes EOS Richard Spencer, ICAEW Fraser Thompson, McKinsey Alan Willis, CICA/Independent Joanne Westwood, Vancouver City Savings Credit Union (Vancity) Roger Simnett, University of New South Wales Lois Guthrie, International Integrated Reporting Council Matthew Bell, EY (Australia) Meg Fricke, EY (Australia) Brendan LeBlanc, EY (United States) Benjamin Miller, EY (Canada) Kelly Gilman, EY (South Africa)

Copyright© July 2013 by the International Integrated Reporting Council. All rights reserved. Permission is granted to make copies of this work to achieve maximum exposure provided that each copy bears the following credit line: Copyright© July 2013 by the International Integrated Reporting Council. All rights reserved. Used with permission of the International Integrated Reporting Council. Permission is granted to make copies of this work to achieve maximum exposure.

ISSN: 2052-1723

ContentS

1 Executive Summary

2 About this Background Paper

3 1. Introduction

3 2. Overview of the term “value creation”

9 3. Value creation for <IR> purposes

9 3A Explaining value creation for <IR>11 3B Who assesses value for <IR> purposes?

12 4. Information that enables readers and users of integrated reports to assess value creation

12 4A Information that facilitates an assessment of value creation

13 4B Practical limitations to the communication of value creation

15 5. Examples of communication about value creation

16 Conclusion

1

Value CreationBackground Paper

executive SummaryThisBackgroundPaperexplorestheconceptofvaluecreationforIntegratedReporting<IR>purposes.<IR>isaprocessthatresultsincommunication,mostvisiblyaperiodic“integratedreport”aboutvaluecreationovertheshort,mediumandlongterm1.Theconceptofvaluecreationthereforeliesattheheartof<IR>.TheInternationalIntegratedReportingCouncilhasdevelopedtheConsultationDraftoftheInternational<IR>Framework(DraftFramework)inordertoencouragethetransitionto<IR>.Togetherwiththebusinessmodelandcapitals,valuecreationisoneofthethreefundamentalconceptsidentifiedasunderpinningtherequirementsandguidancesetoutintheDraftFramework.

Althoughorganizationsaimtocreatevalueoverall,resourcesandrelationships,alsoreferredtointheDraftFrameworkasdifferenttypesof“capital”,maybedestroyedordepletedintheprocessofconductingbusinessactivities.Therefore,whenevertheterm“valuecreation”isused,itshouldbeinterpretedtoincludeactualorpotentialvaluedestructionordepletion2.

Valueiscreated,changedordestroyedbyanorganizationthroughitsbusinessmodel.TheBusinessModelBackgroundPaperdefinesthetermbusinessmodelas“thechosensystemofinputs,businessactivities,outputsandoutcomesthataimstocreatevalueovertheshort,mediumandlongterm.”Therefore,withinthecontextof<IR>,theprocessofvaluecreationisexplainedasfollows:Value is created through an organization’s business model, which takes inputs from the capitals and transforms them through business activities and interactions to produce outputs and outcomes that, over the short, medium and long term, create or destroy value for the organization, its stakeholders, society and the environment.

ThecapitalsfromwhichthebusinessmodeltakesinputsareidentifiedintheCapitalsBackgroundPaperasfinancial,manufactured,intellectual,human,socialandrelationship,andnaturalcapital.Thecapitalsrepresentstoresfromwhichvalueisreleasedwhenthecapitalsarecombined,transformedandleveragedthroughanorganization’sbusinessactivitiesandinteractionsinordertoproduceoutputsandoutcomesthatrepresentvaluecreationorvaluedestructionforstakeholdersdependingontheirinterestsandperspectives.

Theprocessoftakinginputsofcapitalandapplying,using,combining,transformingandsometimesdestroyingthemthroughthebusinessmodeltoproduceoutputsandoutcomeshasbothpositiveandnegativeeffectsindividuallyandcollectivelyonthecapitals,ontheorganization,providersofitsfinancialcapital,societyandtheenvironment.Thenatureofthoseeffectsinformsanassessmentofwhether,towhatextent,forwhomandoverwhattimescalesvaluehasbeencreated.Thisinturndependsinpartontheoutcomesfromthebusinessmodelfortheenvironmentandforconsumersandotherstakeholdersaffectedbytheorganization’sactivities(e.g.,competitors,regulatorsandlocalcommunities).

Theassessmentofvaluecreationthereforeinvolvesconsideringtheinterdependenciesbetweenacompany’scompetitivenessandperformanceandthecommunities,stakeholders,supplychainsandnaturalenvironmentitaffectsandonwhichitdraws.Anintegratedreportshouldenableprovidersoffinancialcapitaltoassesswhether,towhatextentandhowanorganization’sbusinessmodelaffectsthewidercontextthatsupportsorthreatensvaluecreation,includingfinancialvalue,intheshort,mediumandlongterm.

1 www.theiirc.org 2 The Capitals Background Paper footnote 7 page 4

2

about this Background PaperThisBackgroundPaperisorganizedintofivesectionsasfollows:

Section1introducesthepaper.

Section2providesanoverviewofsomeofthetheorythatinformsthemeaningofthetermvaluecreation.

Section3explainstheprocessofvaluecreationfor<IR>purposes.Section4considersthetypeofinformationthatislikelytohelpreadersandusersofintegratedreportstoassesswhether,towhatextentandforwhomvaluehasbeencreatedandcancontinuetobecreatedovertheshort,mediumandlongterm.

Section5illustratespracticeoncommunicatingvaluecreationbasedonextractsfromreports.

3

1. introduction 1TheIIRC’sSeptember2011DiscussionPaper,“TowardsIntegratedReporting–CommunicatingValueinthe21stCentury”saidthat<IR>“providesaclearandconciserepresentationofhowanorganizationcreatesvaluenowandinthefuture.”

2Inresponsetothe2011DiscussionPaper73%ofrespondentsagreed,(2%ofwhomagreedwithqualifications),thattheabilityofanorganizationtocreateandsustainvalueovertheshort,mediumandlongtermisappropriateasacentralthemeforthefuturedirectionofreporting3.TheconceptofvaluecreationhasthereforebeenretainedintheConsultationDraftoftheInternational<IR>Framework(theDraftFramework)asoneofthethreefundamentalconceptsunderpinningtherequirementsandguidancesetoutintheDraftFramework.

ThescopeofthisBackgroundPaper3ThisBackgroundPaperrespondstoquestionsandcommentsthatwereraisedinresponsetoandsincepublicationofthe2011DiscussionPaper,inparticulartheneedformoreclarityaboutthetermvaluecreationfor<IR>purposes,towhomvalueaccruesfor<IR>purposesandhowvalueshouldbecommunicatedinanintegratedreport.ThisBackgroundPaperprovidesablendoftheoryandpracticalexamplesintendedtoexplaintheconceptofvaluecreation.TheinformationcontainedinthisBackgroundPaperisneitherexhaustivenorauthoritative.LiketheDraftFrameworkitself,thisBackgroundPaperdoesnotprescribeanidealoruniversallyapplicableapproachtocommunicatingvaluecreation.Rather,itsetsouttheoriesandexamplesthatcanbeusedbyorganizationstotailortheircommunicationofvaluecreationtotheirowncircumstances,reportingneeds,objectivesandaudiences.

4TheexplanationofvaluecreationinthisBackgroundPapershouldbedistinguishedfromthemeaningofvalue.ThisBackgroundPaperdoesnotdefinevalue.Valuehasdifferentmeaningsfordifferentpeopleandindifferentcontextsandthosemeaningsandcontextsarenotexploredhere.ThisBackgroundPaperfocusesonexplainingtheprocessofvaluecreationfor<IR>purposes.5CertainmattersthatareassociatedwiththeconceptofvaluecreationarenotaddressedinthisBackgroundPaperastheyrepresentongoingbodiesofresearchintheirownright,whicharebeyondthescopeofthispaper.Forexample,thepaperdoesnotcoverindetailthedebateaboutwhetherandtowhatextenttheroleofthemoderncorporationistomaximizeshareholdervalueortocreatevalueforthewholeofsociety,nordoesitexaminecreationofintrinsicandextrinsicvalue.Furthermore,thisBackgroundPaperdoesnotseektoreconcilevaluecreationfor<IR>purposeswithotherconceptsofvaluesuchasenterprisevalue,totaleconomicvalue,economicvalueaddedandtotalvalue.Finally,whilstitisrecognizedthatnotionsofvaluecaptureandvalueappropriationarecloselylinkedtotheconceptofvaluecreation,theIIRC’sworkfocusesonvaluecreation.Anexaminationofthewayinwhichandbywhoorwhatcreatedvalueiscapturedorappropriatedisthereforebeyondthescopeofthispaper.

2. overview of the term “value creation”6Valuecreationisawidelyusedterm.Callsforbusinessreportingtofocusmoreonfactors,includingnon-financialfactors,thatcreatelongertermvaluedatebacksomeyears.Forexample,aSpecialCommitteeonFinancialReportingestablishedbytheAmericanInstituteofCertifiedPublicAccountantsin1991recommendedthattheinformationcompaniesshouldprovidetoinvestorsandcreditorsshould“focusmoreonthefactorsthatcreatelongertermvalue4.”

7Althoughthereisnouniversallyagreeddefinitionofthetermvaluecreationorthemannerinwhichitshouldbecommunicated,certainthemesinformthemeaningofthetermgenerally.ThefollowinggeneralthemesaboutvaluecreationemergefromtheliteraturereviewconductedtosupportthedevelopmentofthisBackgroundPaper.ThetenthemesidentifiedinthisBackgroundPaperdonotrepresentacomprehensivelistofallmattersthatinfluencethewayinwhichvaluecreationmaybeunderstood.

3 http://theiirc.org/wp-content/uploads/2012/06/Discussion-Paper-Summary1.pdf 4 http://www.aicpa.org/interestareas/frc/accountingfinancialreporting/enhancedbusinessreporting/pages/jenkinscommittee.aspx

4

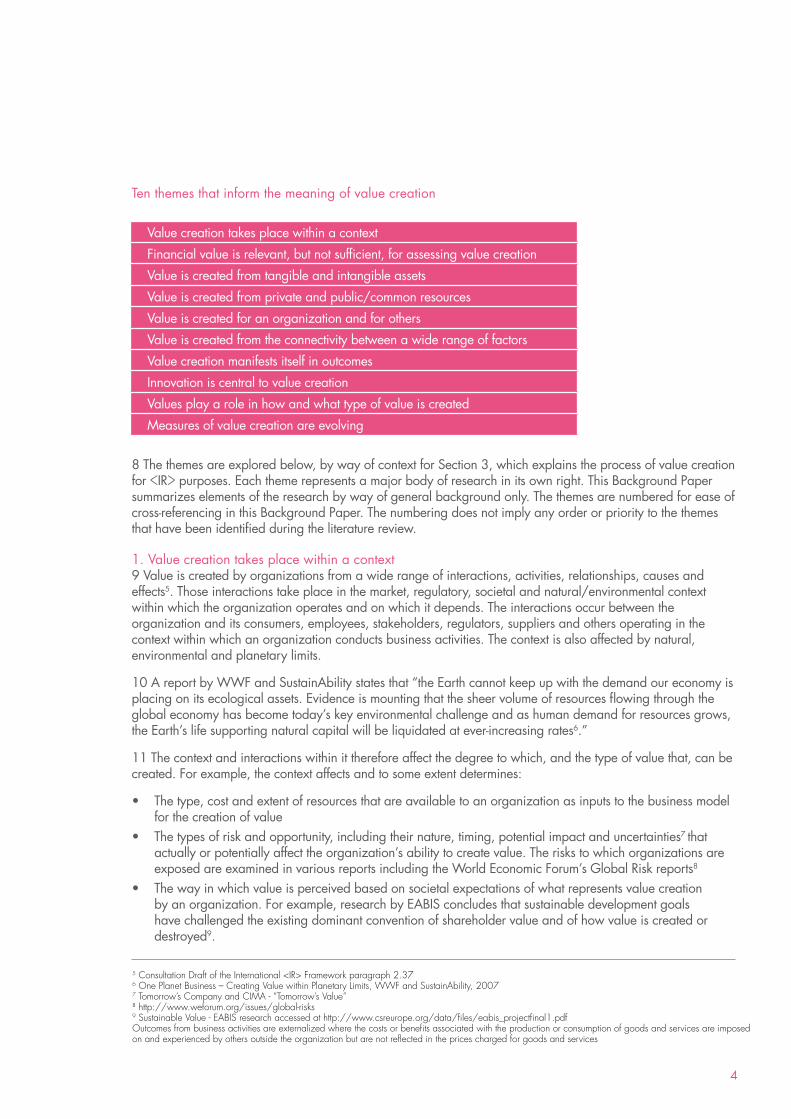

Tenthemesthatinformthemeaningofvaluecreation

8Thethemesareexploredbelow,bywayofcontextforSection3,whichexplainstheprocessofvaluecreationfor<IR>purposes.Eachthemerepresentsamajorbodyofresearchinitsownright.ThisBackgroundPapersummarizeselementsoftheresearchbywayofgeneralbackgroundonly.Thethemesarenumberedforeaseofcross-referencinginthisBackgroundPaper.Thenumberingdoesnotimplyanyorderorprioritytothethemesthathavebeenidentifiedduringtheliteraturereview.

1.Valuecreationtakesplacewithinacontext9Valueiscreatedbyorganizationsfromawiderangeofinteractions,activities,relationships,causesandeffects5.Thoseinteractionstakeplaceinthemarket,regulatory,societalandnatural/environmentalcontextwithinwhichtheorganizationoperatesandonwhichitdepends.Theinteractionsoccurbetweentheorganizationanditsconsumers,employees,stakeholders,regulators,suppliersandothersoperatinginthecontextwithinwhichanorganizationconductsbusinessactivities.Thecontextisalsoaffectedbynatural,environmentalandplanetarylimits.

10AreportbyWWFandSustainAbilitystatesthat“theEarthcannotkeepupwiththedemandoureconomyisplacingonitsecologicalassets.Evidenceismountingthatthesheervolumeofresourcesflowingthroughtheglobaleconomyhasbecometoday’skeyenvironmentalchallengeandashumandemandforresourcesgrows,theEarth’slifesupportingnaturalcapitalwillbeliquidatedatever-increasingrates6.”

11Thecontextandinteractionswithinitthereforeaffectthedegreetowhich,andthetypeofvaluethat,canbecreated.Forexample,thecontextaffectsandtosomeextentdetermines:

• Thetype,costandextentofresourcesthatareavailabletoanorganizationasinputstothebusinessmodelforthecreationofvalue

• Thetypesofriskandopportunity,includingtheirnature,timing,potentialimpactanduncertainties7thatactuallyorpotentiallyaffecttheorganization’sabilitytocreatevalue.TheriskstowhichorganizationsareexposedareexaminedinvariousreportsincludingtheWorldEconomicForum’sGlobalRiskreports8

• Thewayinwhichvalueisperceivedbasedonsocietalexpectationsofwhatrepresentsvaluecreationbyanorganization.Forexample,researchbyEABISconcludesthatsustainabledevelopmentgoalshavechallengedtheexistingdominantconventionofshareholdervalueandofhowvalueiscreatedordestroyed9.

Valuecreationtakesplacewithinacontext

Financialvalueisrelevant,butnotsufficient,forassessingvaluecreation

Valueiscreatedfromtangibleandintangibleassets

Valueiscreatedfromprivateandpublic/commonresources

Valueiscreatedforanorganizationandforothers

Valueiscreatedfromtheconnectivitybetweenawiderangeoffactors

Valuecreationmanifestsitselfinoutcomes

Innovationiscentraltovaluecreation

Valuesplayaroleinhowandwhattypeofvalueiscreated

Measuresofvaluecreationareevolving

5 Consultation Draft of the International <IR> Framework paragraph 2.37 6 One Planet Business – Creating Value within Planetary Limits, WWF and SustainAbility, 2007 7 Tomorrow’s Company and CIMA - “Tomorrow’s Value” 8 http://www.weforum.org/issues/global-risks 9 Sustainable Value - EABIS research accessed at http://www.csreurope.org/data/files/eabis_projectfinal1.pdf Outcomes from business activities are externalized where the costs or benefits associated with the production or consumption of goods and services are imposed on and experienced by others outside the organization but are not reflected in the prices charged for goods and services

5

12Theassessmentofwhether,andtowhatextent,valuehasbeencreatedthereforetakesaccountofcontextualfactorsincluding:resourcescarcity,theincreasingconnectivityoftheglobalizedworldandthewayinwhichcertainoutcomesfrombusinessactivityspilloverintotheenvironmentare“externalized”andareperceivedbysociety.

AccordingtotheOrganizationforEconomicCooperationandDevelopment(OECD),“externalitiesreferstosituationswhentheeffectofproductionorconsumptionofgoodsandservicesimposescostsorbenefitsonotherswhicharenotreflectedinthepriceschargedforthegoodsandservicesbeingprovided.

Pollutionisanobviousexampleofanegativeexternality...Chemicalsdumpedbyanindustrialplantintoalakemaykillfishandplantlifeandaffectthelivelihoodoffishermenandfarmersnearby.

Incontrast,apositiveexternalityorexternaleconomymayarisefromtheconstructionofaroadwhichopensanewareaforhousing,commercialdevelopment,tourism,etc.Theinventionofthetransistorgeneratednumerouspositiveexternalitiesinthemanufactureofmoderntelecommunication,stereoandcomputerequipment.Externalitiesarisewhenpropertyrightscannotbeclearlyassigned.11”

13Accordingtoparagraph2.44oftheDraftFramework,“<IR>takesaccountoftheextenttowhicheffectsonthecapitalshavebeenexternalized(i.e.,thecostsorothereffectsonthecapitalsthatarenotownedbytheorganization).Externalitiesmaybepositiveornegative(i.e.,theymayresultinanetincreaseordecreasetothevalueembodiedinthecapitals).”

2.Financialvalueisrelevant,butnotsufficient,forassessingvaluecreation

14Financialvaluemaybemanifestedinvariousways,includinginanorganization’sstockprice,profits,balancesheetandorganizationalgrowth,anditmaychangeoverdifferenttimeframes.AccordingtoMcKinsey,companiescreatevaluebyinvestingcapitalfrominvestorstogeneratefuturecashflowsatratesofreturnexceedingthecostofthatcapital(i.e.,therateinvestorsrequiretobepaidfortheuseoftheircapital).“Thefastercompaniescangrowtheirrevenuesanddeploymorecapitalatattractiveratesofreturn,themorevaluetheycreate.Inshortthecombinationofgrowthand[returnoninvestmentcapital]drivesvalueandvaluecreation12.”

15However,recentanalyseschallengethenarrowfocusofvaluecreationonfinancialvalueandcontendthatvaluecreationextendsbeyondbenefitsdirectlyassociatedwithfinancialvalueorfinancialcapitalaccretion.Althoughrelevant,itisnotsufficienttoassessvaluecreationonlythroughtheprocessofexchangeinmarketswhichsetspricesandexpressesthequantifiedworthofgoodsandservicesorthroughaccountingconceptsofvalueexpressedinprofitandlossstatements,balancesheetsandorganizationalgrowth.

16Aswellasvaluethatmaybequantifiedinfinancialterms,valuemayalsobemanifestedinutilityvalue,thatisthequalitativeaspectofvalue:valueintheeyesofconsumersandusersthroughitsutilityinmeetinghumanneeds.Utilityvalueisexpressedandrealizedthroughitsconsumption.Utility,thatisthecustomerorstakeholder’sassessmentofworth,isnotderivedfromasinglesourcebutfromthreeoverlappingareas:functionalutility(whattheproductorservicedoes),economicutility(howmuchitcosts)andemotionalutility(howitmakesthecustomerfeel)13.

17SimilarlyBenedicktandOden14,andHermanDaly15refertovaluebeingmanifestedin“qualitativegrowth”,beingtheincreaseinthequalityofgoodsandoutcomesproducedbyaneconomyratherthananincreaseinthequantityofgoodsandservices,whilstofferingthesameorgreateropportunitiesforprofitableinvestment,fullemploymentanddecentwages.

11 OECD Glossary of Statistical Terms accessed 5 February 2013 from http://stats.oecd.org/glossary/ 12 http://www.mckinsey.com/client_service/corporate_finance/latest_thinking/value/the_four_cornerstones 13 “What does value mean and how is it created, maintained and destroyed?” – C Bowman and V Ambrosini, Cranfield School of Management, 2003 14 Better is Better than More, M Benedikt and M Oden, Centre for Sustainable Development Working Paper Series 2011 15 Beyond Growth: The Limits of Sustainable Development, Herman Daly, Boston:Beacon Press 1996

6

3.Valueiscreatedfromtangibleandintangibleassets18Tangibleassetshaveaphysicalformandexistence.Bycontrast,intangibleassetsdonothaveaphysicalpresence.InInternationalAccountingStandard(IAS)38,theInternationalAccountingStandardsBoard(IASB)definesthemasnon-monetaryassets,whicharewithoutphysicalsubstance.Intangibleassetsincludebrands,patents,goodwill,know-how,reputation,theknowledgeheldbyemployeesandthecorporatestrategy.Intangibleassetscontributetothecreationofvaluebyorganizations.

19Increasinglyvalueiscreatedprimarilyfromintangibleratherthanphysicalassets16.Forexample,280chiefexecutiveofficersfromover21countriessurveyedbytheAICPA(AmericanInstituteofCertifiedPublicAccountants)andCIMA(CharteredInstituteofManagementAccountants)concludedthatpeople’sideas,skills,knowledgeandrelationshipsrepresentedtheuniquevalueoftheircompaniesintermsofwhereitcomesfromandhowmuchofitisavailable.Theythereforesupportedtheneedtomeasureandmanagethehumandimensioninordertoachievelongtermsustainablesuccess17.Intangibleassets,suchasgoodreputation,havebeendescribedas“critical,becauseoftheirpotentialforvaluecreationandalsobecausetheirintangiblecharactermakesreplicationbycompetingfirmsconsiderablymoredifficult18.”

20Althoughintangibleassetsarerecognizedforthepurposesofvaluingorganizations,thereisnostandardmethodofaccountingforthem,asthereisforphysicalassets19.Inmanycasestheyarenotreflectedonthebalancesheetdespitecontributingtothefuturesuccessofthecompany20.Arguablythismakesfinancialaccountingincompleteandcontributestothewideninggapbetweenbookandmarketvaluereferredto,forexample,intheSoneconpublication,“WhatIdeasareWorth:TheValueofIntellectualCapitalandIntangibleAssetsintheAmericanEconomy21.”TheSoneconpublicationconcludesthatfortenindustriesitexamined,intangibleassetsrepresentatleast90%ofmarket,notbook,value.The“valuegap”betweenmarketvalueandbookvalueindicatesthatphysicalandfinancialaccountableassetsreflectedonacompany’sbalancesheetcompriseslessthan20%ofthetruevalueoftheaveragefirm.

21Giventheircontributiontovaluecreation,somearguethat“inordertoassistmanagersofbusinessenterprisesandtheirprovidersofcapitalintheirdecision-makingprocesses...guidelines[shouldbedeveloped]fortheidentificationofintangible[assetsandforthe]measurementandsuccessfulmanagementofintangibleswithin...22”organizations.Manythereforecallformeasurement,reportingandmanagementofalloftheassets,tangibleandintangible,thataffecttheabilityofanorganizationtocreatevalue.

4.Valueiscreatedfromprivateandpublic/commonresources22Insomecasesanorganizationdoesnotownorbearadirectchargeforitsuseof,oreffecton,sourcesofcapitalthatareinputtothebusinessmodeltotransformintooutputsandoutcomesthatcreatevalue.Suchsourcesofinputsareoftenknownasthe“globalcommons”or“commonpoolresources”–termsthatrefertoresourcesthatareunowned,unprivatized,unregulated,freeandsharedbyall.Theseincludetheoceansandtheatmosphereandtheenvironmentalgoodsandservicesthattheyprovide,aswellassocietalassetssuchaspublicroadnetworks.

23GarrettHardin’s“TragedyoftheCommons23”recognizesthatthevalueofthecommonsforoneactorinordertomaximizeorcapturehisgaincanresultinnegativeeffectsthataresharedbyall.Forexample,ifthecostofdischargingwasteintothecommonsislessthanthecostofpurifyingthewastebeforereleasingit,thepolluterwillgain(orcapturevalue)butsocietywillbeartheconsequencesandcostsoftheeffectsofthewasteonthecommons.Suchconsequencesandcostsareknownas“externalities”.Externalitiesmayimpactonbothprivateandpublic/commonresources.Varioussolutionshavebeenproposedtomanagecommonresourcesanddealwithexternalities,includinggovernmentintervention,allocationofpropertyrightsandthedevelopmentbycommunitiesoftheirownrulesandmethodsofenforcement24.16 [1] Ocean Tomo LLC report on S&P 500 Components of Value – http://www.oceantomo.com/productsand services/investments/intangible-market-value 17 Rebooting Business: Valuing the Human Dimension, Chartered Global Management Accountant, a joint venture between the AICPA and CIMA 18 Corporate Reputation and Sustained Superior Financial Performance, Peter W Roberts & Grahame R Dowling 19 Accounting for Intangibles: Financial Reporting and Value Creation in the Knowledge Economy - A Research Report for the Work Foundation’s Knowledge Economy Programme by Ricardo Blaug and Rohit Lekhi, Research Republic LLP 20 The Value Relevance and Managerial Implications of Intangibles - Leandro Canibano, Manuel Garcia-Ayuso Covasi and M Paloma Sanchez, March 1999 21 http://www.sonecon.com/docs/studies/Value_of_Intellectual_Capital_in_American_Economy.pdf 22 The Value Relevance and Managerial Implications of Intangibles - Leandro Canibano, Manuel Garcia-Ayuso Covasi and M Paloma Sanchez, March 1999 23 Science, New Series, Vol 162, No 3859 (Dec 13, 1968) 24 The Future of the Commons; Beyond Market Failure and Government Regulation - Elinor Ostrom with contributions from Christina Chang, Mark Pennington and Vlad Tarko - A report for the Institute of Economic Affairs, 2012

7

24Allsolutionsformanagingthecommonsaredependentupontransparency,informationandcommonlanguage.Thisisbecause,inordertomanageandpreservetheirvaluecreatingpotential,decision-makersneedinformationaboutthenatureofthecommonresources,theincentivesanddisincentivesfacingactualandpotentialresourceusers,thescientificandtechnologicalvariablesthataffectcommonresourcesandsoon.

5.Valueiscreatedforanorganizationandforothers25SomeoftheliteratureonvaluecreationreviewedforthisBackgroundPaperreferstothedichotomybetweentwoviewsoftheconstituenciesforwhichanorganizationcreatesvalue.Thefirst,oftenknownas“shareholdervaluetheory”,iswidelyattributedtoMiltonFriedmanin1962.Friedman’sviewdeclaresthepurposeofacompanyasbeingtomaximizeshareholdervalueandtopursuesocialactivitiesonlyaslongastheygenerateprofit.Thesecondview,attributedtoEdwardFreemaninthe1980s,isoftenknownasstakeholdertheoryandstatesthattheobjectiveoforganizationsshouldbetoaugmentthegreatergoodforthemanyandtocreateasmuchvalueaspossibleformultiplestakeholders.Thequestionthereforearisesastowhethervalueshouldbecreatedforshareholdersorformultiplestakeholdersorforboth.

26InMichaelJensen’sreport“ValueMaximization,StakeholderTheoryandtheCorporateObjectiveFunction”,Jensenstatesthatbusinessshouldgetthemostoutofsociety’slimitedresources,whilereturninggreatervaluetosocietysothatthepursuitofstakeholdervalueandahealthyenvironmenthelpsabusinesstomaximizeitsfinancialvalue.TheimplicationofJensen’sworkisthattheinterestsofshareholdersandstakeholdersarenotatodds.Jensenstatesthatanypotentialconflictsbetweenthemshouldberesolvedthroughafocusonlongtermvaluecreation,asthelongtermvalueofacompany“cannotbemaximizedifanyimportantconstituencyisignoredormistreated.Wecannotcreatevaluewithoutgoodrelationswithcustomers,employees,financialbackers,suppliers,regulators,communitiesandsoon25.”

27Increasingly,valuecreationisunderstoodintermsofthevaluethatisappropriatedtotheorganizationfromitsbusinessactivitiesandthevaluethatiscreatedforandcapturedbyothers.In“CreatingSharedValue”MichaelE.PorterandMarkR.Kramerdefinesharedvalueas“creatingeconomicvalueinawaythatalsocreatesvalueforsocietybyaddressingitsneedsandchallenges”.Theydescribesharedvalueas“aconceptthatfocusesontheconnectionsbetweensocietalandeconomicprogress…andthatexpandsthetotalpoolofeconomicandsocialvalue”.Sharedvalueisbasedonthepremisethathavingenvironmentalorsocialissuesthatarenotaddressedcreatesinternalcostsforcompanies(e.g.,wastedenergy,remedialtrainingtocompensateforinadequateeducationsystems),whichconstraintheextentofvaluecreation,destroyvalueor,overthelongerterm,makethebusinessmodelunsustainable.

28Aswellasbeingcreatedforandcapturedbyawiderangeofstakeholders,valueisincreasinglycreatedincollaborationwithothers,includingconsumerswho“armedwithnewtoolsanddissatisfiedwithavailablechoices...wanttointeractwithfirmsandtherebyco-createvalue26.”

6.Valueiscreatedfromtheconnectivitybetweenawiderangeoffactors29Theassessmentofvaluecreationisbasedona“compoundvectorofqualitative,ethical,social,aestheticandpractical27”factors,thewayinwhichtheyinteractandtheoutcomesofthoseinteractionsformultiplestakeholders.AsEdwardFreemannotes,“nostakeholderstandsaloneintheprocessofvaluecreation28.”Therefore,communicatingvaluecreationisnotsimplyaquestionofmergingfinancialandnon-financialinformation.AsErnst&Youngobserves29,acomprehensivepictureofvaluecreationiscommunicatedthroughalignmentbetweenmanyfactorsincludingbusinesspractices,tangibleandintangibleassets,materialfinancialandnon-financialcapitalrisks,thecompany’sstrategy,itsengagementwithmultiplestakeholders,sustainabilityagenda,governancepracticesandfuturegoalsovertheshort,mediumandlongterm.Communicatingvaluecreationalsoinvolvesdescribingthetrade-offsbetweenthevariousinterdependenciesonwhichthevaluecreationprocessdepends,suchasbetweenequityandadvantageandqualityoverquantity30.

25 Michael C. Jensen – Value Maximization, Stakeholder Theory and the Corporate Objective Function, October 2001 – The Monitor Group and Harvard Business School 26 Co-creation Experiences: The next practice in value creation - C.K. Prahalad and Venkat Ramaswamy. Published in the Journal of Interactive Marketing, Volume 18, Number 3, Summer 2004 27 Better is Better than More, M Benedikt and M Oden, Centre for Sustainable Development Working Paper Series 2011 28 The Journal of Business Ethics 2010 96:7-9, R. Edward Freeman - Managing for Stakeholders: Trade offs or Value Creation 29 Insights for Executives - Driving value by combining financial and non-financial information into a single investor grade document 30 Speth (2008) quoted in Better is Better than More

8

30ItisbeyondthescopeofthisBackgroundPapertoexaminethedifferentapproachestothepotentialtrade-offsthatarerequiredtocreatevalue.However,MichaelJensen’swork31isoneexamplethatrecognizestheconceptualdifficultyofmakingtrade-offsbetweenthevariousinterdependentfactorsanddifferentstakeholdersthatcontributeto,orareaffectedby,businessactivitiesaimedatvaluecreation.Jensencharacterizesthedifficultybydescribingthemultipleconstituencieswithcompetingandsometimesconflictinginterests:

“Customerswantlowprices,highqualityandfullservices.Employeeswanthighwages,high-qualityworkingconditionsandfringebenefitsincludingvacations,medicalbenefitsandpensions.Suppliersofcapitalwantlowriskandhighreturns.Communitieswanthighcharitablecontributions,socialexpendituresbycompaniestobenefitthecommunityatlarge,increasedlocalinvestmentandstableemployment32.”

31Inthesecircumstances,Jensensaysthatpotentialconflictsbetweenvarioustrade-offscanberesolvedbysettinganobjectivefunction,representingthecoreofanydecisioncriteriontoguidethewayinwhichtrade-offsbetweendemandsaremadeandenablemanagementtoevaluatedecisions.Inotherwords,reasoneddecisionsabouttrade-offsdependuponaclearobjective.Jensensuggeststhat“theobjectivefunction,theoverridinggoalofthefirmistomaximizetotallongtermfirmmarketvalue…”whichrecognizes“…thepossibilitythatfinancialmarkets,althoughforwardlooking,maynotunderstandthefullimplicationsofacompany’spolicies”untiltheybegintoshowupincashflowsandcustomerandemployeeloyaltyovertime.

7.Valuecreationmanifestsitselfinoutcomes32Theconnectionsandinterdependenciesbetweenthedifferentfactorsthatcontributetothecreationofvalueresultindifferentoutcomesfordifferentstakeholders.Outcomesaredefinedinparagraph2.35oftheDraftFrameworkas“theinternalandexternalconsequences(positiveandnegative)forthecapitalsasaresultofanorganization’sbusinessactivitiesandoutputs.”Thoseoutcomesinformtheassessmentofvaluedependingontheperspectiveofthestakeholdersandtheirdependenceuponthestoresofcapitalaffectedbythevaluecreationprocess.Valuecreationismanifestedinoutcomesfor,orchangesto,thosestoresofcapitalthatresultfromanorganization’sactivities.Thoseoutcomesmaybeaffectedbythewayinwhichanorganizationgovernsenvironmentalandsocialconcernsincreatingvalueforitselfanditsstakeholders33.

33Outcomesarenotalwaysstableandpredictableandtakeplaceovermultipletimeframes.Creationofvalueintheshortormediumtermhasthepotentialtoenhanceordiluteordenythepotentialforvaluecreationinthefuture34.Thereforetheassessmentofvaluecreationisnotnecessarilyconfinedtoaparticulartimeframebuttakesintoaccountthewayinwhichvaluecreatingactivitiesmightaffectfuturevaluecreationpotentialandissuesofintergenerationalequity.

8.Innovationiscentraltovaluecreation34Changestothecontextinwhichorganizationsoperate,includingglobalization,resourcescarcity,demographicalchangesandcompetitionrequirestrategiesthatsecureacompetitiveadvantagefororganizations.Suchstrategiesareaimedatgeneratingandinnovatingnewoutcomesthatdistinguishtheorganizationfromothersinanincreasinglycomplexandcompetitiveenvironmentandthatmaketheorganizationresilientandcapableofadaptingtonewcircumstances.Variousbranchesofresearch35includingresource-basedtheoryandevolutionaryeconomicscontendthatvalueiscreatedormaximizedthroughinnovationthatallowsorganizations“toreconceivetheirsourcesofstrategicadvantageandmasternewmechanismstobuildlastingorsustainablestrength36”andcreativelytorearrangeresourcesinordertocreatenewvalue37.

31 Michael C. Jensen – Value Maximization, Stakeholder Theory and the Corporate Objective Function, October 2001 – The Monitor Group and Harvard Business School 32 Michael C. Jensen – Value Maximization, Stakeholder Theory and the Corporate Objective Function, October 2001 – The Monitor Group and Harvard Business School 33 Sustainable Value Creation Family Business Oct 2012 34 Tomorrow’s Company and CIMA - “Tomorrow’s Value” extract – “Discount rates value future generations less than we value ourselves – but can we be confident of a basis of determining value that may deny our children’s children the joy of nature and the increasing threat we pose to other species?” 35 See for example the work of the Evolutionary Economics Group at http://www.econ.mpg.de/english/research/EVO/discuss.php 36 Sustainable Value Creation Family Business Oct 2012 37 Paul Romer quoted in Better is Better than More

9

9.Valuesplayaroleinhowandwhattypeofvalueiscreated35Whilsttheyaredistinctfromvaluecreation,thereisarelationshipbetweenvaluecreationandvaluessuchasthebeliefs,behaviors,culturalchoicesandphilosophiesembracedbyanorganization.Valuesortheabsenceofvalues,sometimesexpressedincodesofbusinessconduct,canplayaroleindeterminingthewayandextenttowhichanorganizationcreatesandprotectsvalue.

10.Measuresofvaluecreationareevolving36ItisbeyondthescopeofthisBackgroundPapertoexamineandexploretherelativemeritsofthevariouswaysinwhichorganizationsseektomeasureanddescribevaluecreation.However,itisrecognizedthatmeasuresofvaluesuchasEconomicValueAdded,BalancedScorecard,EnterpriseValue,TotalContribution,TotalEconomicValueandTotalValueareemergingasmeansofexpressingvaluecreation.Thesenewmeasuresgobeyondtheexpressionofvaluecreationintermsofmarketvaluationandpricing.Theyseektoreflectthefullcostsandbenefitsoftheoutputsandoutcomescreatedbyanorganization.

3. Value creation for <ir> purposes37Section3Aexplainsvaluecreationfor<IR>and3Bconsiderswhoassessesvalue.3AExplainingvaluecreationfor<IR>38Valuecreationfor<IR>purposesisexplainedasfollows:Value is created through an organization’s business model, which takes inputs from the capitals and transforms them through business activities and interactions to produce outputs and outcomes that, over the short, medium and long term, create or destroy value for the organization, its stakeholders, society and the environment.

Eachpartoftheexplanationisexaminedinmoredetailbelow.

Value is created through an organization’s business model–For<IR>purposesvalueiscreated,changedordestroyedbyanorganizationthroughitsbusinessmodel.TheBusinessModelBackgroundPaperdefinesthetermbusinessmodelas“thechosensystemofinputs,businessactivities,outputsandoutcomesthataimstocreatevalueovertheshort,mediumandlongterm.”

which takes inputs from the capitals–Anorganization’sbusinessmodeltakesinputsorresourcesinoneformoranotherfromthecapitals,identifiedintheCapitalsBackgroundPaperasfinancial,manufactured,intellectual,human,socialandrelationshipandnaturalcapital.Thecapitalsrepresentstoresfromwhichvalueisreleasedwhenthecapitalsarecombined,transformedandleveragedtoproduceoutputsandoutcomesthatrepresentvaluecreationorvaluedestruction,dependingontheperspectivesandinterestsofdifferentstakeholders.Businessinputsmayincluderesourcesintheformofrawmaterials,commonresources,employees,research,ideas,financialcapitaletc.aswellasrelationshipswithsuppliersandotherstakeholders.Inputsmaybeinternalorexternalanddirect(labour,rawmaterialsorcashusedintransactions)orindirect(transportationinfrastructure,regulatoryparametersoreducationoftheworkforce).Inputsarerequiredtoproduce(viaoperationalorotherbusinessprocesses)outputsandoutcomesthatinturncreateordestroyvaluefortheorganization,consumers,theenvironment,providersoffinancialcapitalandothers.

andtransformsthemthroughbusinessactivitiesandinteractions–Takinginputsfromvariousformsofcapitaldoesnotinitselfcreatevalue.Valueiscreatedthroughtheactivitiesbusinessconductsinordertoreleasevaluefrominputsofcapital.Businessactivitiesinvolveusing,combining,applying,processingandtransforminginputsfromthecapitalsintooutputsandoutcomes.Businessactivitiesmayinvolvetheuseofprocesses,tools,technologiesandinnovationtoachieveintendedoutputsandoutcomesidentifiedthroughtheorganization’sstrategyandtargets.Awiderangeofinteractionsoccursthroughthecourseofbusinessactivitiesbothinternallybetweenemployeesandcontractorsandexternallywithsuppliers,consumers,regulators,communitiesandtheenvironment.Valuecreationisassessedinpartbyconsideringtheinteractionsbetweenacompany’scompetitivenessandsuccess,andthecommunitiesandnaturalenvironmentitaffectsandonwhichitdraws.Understandingtheconnectivitybetweeninternalandexternal

10

forcesthatenable,enhanceorfrustratethebusinessmodelisthereforecrucialtoassessingwhethervaluehasinfactbeencreatedordestroyed,andwhetheritislikelytobecreatedinthefuture.

to produce outputs –Throughanorganization’sbusinessactivities,itapplies,uses,consumes,destroysandtransformsdifferenttypesofcapitaltoproduceoutputs,definedintheBusinessModelBackgroundPaperas“thekeyproductsorservicesthatanorganizationproduces,aswellasthewasteorotherby-productsthatcreateorerodevalue...forexample,inthecaseofacarmanufacturer,theoutputisthecar.”Outputsareusuallyplanned,intendedandaimedforthroughacompany’sstrategyandtargets.

and outcomes–Theprocessoftakinginputsfromdifferenttypesofcapitalsandapplying,using,destroyingandtransformingthemthroughthebusinessmodelproducesoutcomesaswellasoutputs.OutcomesaredefinedintheBusinessModelBackgroundPaperas“theinternalandexternalconsequencesforthecapitalsasaresultoftheorganization’sbusinessactivitiesandoutputs.”TheBusinessModelBackgroundPaperstatesthatinthecaseofacarmanufacturer,theoutcomesfortheconsumermaybemobility,safety,reliability,comfortandstatus.Outcomesfromanorganization’sbusinessmodelmaytaketheformofincreasedsales,profit,marketshare,enhancedreputation,bettercommunitylinks,customersatisfaction,declineorenhancementofnaturalenvironment,positiveandnegativeexternalitiesetc.Outcomesfrombusinessactivitythathavenofinancialcounterpartormeansoffinancialmeasurementareasrelevanttovaluecreationasfinancialrevenueandcapital.Therefore,whilsttheyinformandcontributetoit,valuecreationfor<IR>purposesisnotjustassessedbyreferencetooutcomessuchasanorganization’sperformance,stockprice,growth(intheformofreturnoninvestmentcapital)andprofit.Althoughoutcomesfromanorganization’sbusinessmodelarenormallyplannedandintended,notalloutcomescanbepredictedbecauseofthenon-linearinteractionofthewiderangeoffactorsonwhichanorganizationdependsforvaluecreation.Unintendedoutcomesfromthebusinessmodelmaythereforemanifestthemselvesintheshort,mediumorlongtermandmaybepositiveornegative.

that, over the short, medium and long term, create or destroy value–Intendedandunintendedoutcomesfromthebusinessmodelhavebothpositiveandnegativeeffectsindividuallyandcollectivelyonthecapitals,ontheorganization,providersofitsfinancialcapital,onsocietyandtheenvironment.Thoseoutcomesmaymanifestthemselvesovertheshort,mediumorlongterm.Theapplication,use,destructionandtransformation,impactonandinterplaybetweenthecapitalsmaythereforeaffecttheextenttowhichprovidersoffinancialcapitalcanexpectoutcomesintheformoffinancialreturns,aswellastheoutcomesforsocietyintermsoftheaccesstoandbenefitfromthecapitalsandfortheenvironmentintermsofitsenhancementordegradation.Whetherbusinessactivitieshavecreatedordestroyedvaluemaybeimmediatelyevidentormaybecomeapparentovertime.

fortheorganization,itsstakeholders,societyandtheenvironment–Anassessmentofthepositiveandnegativeoutcomesfromthebusinessmodelinformsthedeterminationofwhether,towhatextent,forwhomandoverwhattimescalesvaluehasbeencreatedordestroyed.Whetheroutputsandoutcomesrepresentvaluecreationdependsinpartonthereactionof,oroutcomesfor,consumersandallotherstakeholdersaffectedbytheorganization’sactivities(e.g.,competitors,regulatorsandlocalcommunities)andalsoontheoutcomesfromtheorganization’sbusinessmodelontheenvironment.Anorganization’sabilitytocreatevalueiscloselylinkedtothesupplychains,communitiesandnaturalenvironment,whichmayshareinvaluecreationordestruction.Thewayinwhichallofthoseconstituenciesexperiencetheoutcomesofanorganization’sbusinessmodelinformsanassessmentofwhethervaluehasbeencreated,andforwhom.

11

3BWhoassessesvaluefor<IR>purposes?39Integratedreportsshouldenableprovidersoffinancialcapitaltoassesswhether,towhatextentandhowanorganization’suseof,andoutcomesfor,allofthecapitalsaddstofinancialvalue.

40Paragraph1.6oftheDraftFrameworkdefinestheprimaryintendedaudienceforintegratedreportsandothercommunicationsresultingfromtheprocessof<IR>asprovidersoffinancialcapital.Whilstrecognizingthatarangeofstakeholdersmaybenefitfromintegratedreports,theyarespecificallyintendedtoenableprovidersoffinancialcapitaltogainanunderstandingofhowanorganizationcreatesandsustainsvalueintheshort,mediumandlongterm.Providersoffinancialcapitalequatevaluecreationwiththepotentialforfuturecashflowsandsustainablefinancialreturns,butthisalsotakesintoaccounttheimportanceandlimitationsofdifferentformsofcapitalforvaluecreation.

41ThisBackgroundPaperacknowledgesthatquestionsaresometimesaskedaboutwhethercertainprovidersoffinancialcapitaladequatelyadvancethegoalsofandactasstewardsforindividualswhohaveinvestedwiththem38.Aspectsoftheinstitutionalarrangementsonwhichtherelationshipsbetweenprovidersoffinancialcapitalandcorporationsarebasedhavebeenblamedforagrowinggapbetweeninvestors’financialinterestsandthepublicinterest.Theseinclude:

• Short-termismwhichcanbeimplicatedinmarketfailurebecauselong-durationprojectssufferdisproportionately.

• Agencyandcontractualarrangementsbetweenfinancialactors(e.g.,assetownersandassetmanagers)thatproduceperverseorunintendedoutcomes.

• Failuretotakeintoaccountthevalueofandrelianceoninputsfromnaturalandotherformsofcapitalthatarevulnerable,limitedorexhaustible.

• Definitionsofvaluethatarelimitedonlytoshareholdervalue.

42Theactionsofvariousgovernmental,non-governmentalandotherorganizationsthereforeseektoalignmorecloselyinvestors’long-termfinancialinterestsandcorporatepracticeswiththepublicinterest.

43Investorsalreadycurrentlyplaceavalueoncompanieseitherindirectlyviaanalystreportsandvaluationpredictivemodelingordirectlyfrommarketbidding.<IR>isintendedtoprovidegreaterclarityandinsighttoallowinvestorsmorecomprehensivelytoconsiderthemutualinter-dependencebetweenthelong-termfinancialinterestsoftheultimateownersoffinancialcapital,corporatepracticeandthepublicinterestforthecreationandpreservationofvalue.Certainresearch39arguesthatthepublicinterestandthatofprovidersoffinancialcapitalareservedbyinvestmenttosupportthelongterm,aswellastheshortandmediumterm,continuanceofcapitalsonwhichhumancommunities,economicandenvironmentalsystemsdepend.<IR>canthereforebeseentoencourageamorecomprehensiveconsiderationoftheeffectsthatcorporateandinvestorbehavioranddecision-makinghaveonthepublicinterestbyrequiringabroaderrangeofinformationtobeprovidedincommunicatingcorporateperformanceinanintegratedreport.

44Whilsttheyarenottheprimaryintendedusersofanintegratedreportorothercommunicationsresultingfromtheprocessof<IR>,otherstakeholdersarealsolikelytobenefitfrom<IR>andtohavetheirviewstakenintoaccountbyorganizationswhenpreparingintegratedreports.Thisisbecausethefinancialreturnsonwhichprovidersoffinancialcapitalarefocusedareultimatelydependentuponinter-relationshipsbetweenandincreasesanddecreasesinalltypesofcapitalevenwherefinancialcapitalprovidersarenotaffecteddirectlyorimmediatelybymovementsinthosecapitals.Theconcernsandactionsofstakeholderswithwiderinterestsindifferentcapitalsmayaffectfinancialreturns,andsimilarlytheavailabilityanduseoffinancialcapitalmayaffectothertypesofcapitalinwhichthewiderstakeholdergroupareinterested.

38 Are Institutional Investors Part of the Problem or Part of the Solution? Ben W. Heineman, Jr., Stephen Davis, Center for Economic Development, Yale School of Management 39 Acting in the Public Interest: A Framework for Analysis – ICAEW Market Foundations Initiative,2012

12

4. information that enables readers and users of integrated reports to assess value creation45Integratedreportsshouldcommunicateinformationthatenablesintendedreportuserstoassesswhether,andtowhatextent,valuehasbeencreatedandislikelytobecreatedfortheorganization,soastoaddtofinancialvalue.Inaddition,itmustexplainhowthebusinessmodelaffectswhether,howandtowhatextentvaluehasbeencreatedordestroyedforothers,soastoincreaseordecreasethepoolofcapitalsonwhichtheorganizationcandrawtocreatevalueovertimegivenplanetarylimitsandsocietalexpectations.

46Section4Aconsidersthetypeofinformationthatenablesreadersandusersofintegratedreportstoassessvaluecreation.Thetypeofinformationthatenablessuchassessmentsispotentiallyverywideandmustbebalancedwiththeneedforanintegratedreporttobeconcise.Section4Bthereforediscusseshowtolimitandfocustheinformationthatisreportedaboutvaluecreationandgoesontoconsiderhowinformationshouldbereportedgiventhatstandards,metricsandotherapproachestothecommunicationofcertainaspectsofvaluecreationarenotyetwellestablished.

4AInformationthatfacilitatesanassessmentofvaluecreation47Informationthatislikelytofacilitateanassessmentofwhether,andtowhatextent,valuehasbeencreatedordestroyedincludes:

• Adescriptionofthebusinessmodelincludinginputs,businessactivities,outputsandoutcomesandlinkstotheorganization’sstrategy–Section2CoftheDraftFrameworkandtheBusinessModelBackgroundPaperexplainthetypeofinformationthatshouldbereportedinordertoenableusersofintegratedreportstoassesshowthebusinessmodelcontributestothecreationofvalue.Therelationshipbetweenthebusinessmodelandtheorganization’sstrategyhelpstoexplainthecontext,directionandfocusforthebusinessmodel.

• Performance–Section4FoftheDraftFrameworkdescribesthetypeofinformationthatshouldbeconsideredforcommunicatingperformancefor<IR>purposes.Whilstnotsufficientaloneforanassessmentofvaluecreation,performancecontributestoanunderstandingoftheextenttowhichacompanyhascreatedvaluefromachievementofperformancegoals.

• Whattypeofvaluetheorganizationintendstocreate,how,forwhomandwhy–includingtheorganization’snotionofvalue,theprocessthatisusedforvaluecreation,whatactionsandactivitiesthevaluecreationprocessentails,forwhomtheorganizationaimstocreatevalueandwhy.

• Management’sassessmentofwhethertheintendedvaluehasbeencreated,thatis,whethertheoutputsandoutcomesfromthebusinessmodelareasintendedaccordingtotheorganization’sstrategyandtargets.

• Management’sassessmentofthewayinwhichvariousformsofcapitalhavebeenaffectedbythebusinessmodelsoastocreateordestroyvalue–Businessactivitiesinevitablydrawfromoraddtothecapitals.Overall,inthelongterm,valueforprovidersoffinancialcapitalisunlikelytobecreatedthroughthemaximizationofonecapitalwhiledisregardingtheeffectonothercapitals.Understandingthevariouscapitalstheorganizationusesandaffects,includingtheinterdependenciesandtrade-offsthataremadebetweenthem,isthereforeessentialforassessingwhetherandtowhatextentvaluehasbeencreatedordestroyed.Thecapitalscanalsobeusedtoexpressthetypeofvaluethathasbeencreated.

Wherepossible,informationabouttheextenttowhichcostsorothereffectsonthevariouscapitalshavebeenexternalized(i.e.,thecostsandothereffectsonthecapitalsarepassedonoutsidetheorganizationtosociety,theenvironmentandfuturegenerations)alsoinformsanassessmentofhowoverallincreasesordecreasesinvalueembodiedincapitalsthatarenotownedbytheorganizationaffectsvaluetoprovidersoffinancialcapitalinthelongterm.

• Governance–Informationaboutthestabilityoftheorganization’sgovernancestructurehelpsintendeduserstoassessitsresilienceagainstshorttermdisruptionssoastocontinuetocreatevalue.Informationabouttheorganization’sgovernancestructurealsoinfluencesthelevelofconfidenceintheorganization’sabilitysuccessfullytoimplementitsbusinessmodelandtransparentlyandaccuratelytocommunicateperformance.

13

• Innovationandfutureoutlook,includingthemeasurestaken,andresearchinwhich,theorganizationhasinvestedtoinnovatesoastoensuretheresilienceandefficiencyofthebusinessmodelforvaluecreationovertime.Thiswillincludemanagement’sviewoftheanticipatedeffectonfinancialandothertypesofvalueoftheirpolicies,decisionsandinnovations.

• Stakeholderengagement–Asnotedabove,anorganization’sabilitytocreatevalueiscloselylinkedtothesupplychains,communitiesandconsumers,whichmayshareorbeaffectedbyvaluecreationordestruction.Thereisasymbioticrelationshipbetweenacompany’scompetitivenessandsuccessandthecommunitiesandnaturalenvironmentonwhichitdraws.Theextenttowhichanorganization’sactivitiesandofferingsrepresent“value”dependsinpartonthereactionofconsumersandotherstakeholdersaffectedbytheorganization’sactivities(e.g.,competitors,regulatorsandlocalcommunities).Thosereactions,manifestedinincreasedsales,marketshare,enhancedreputation,bettercommunitylinks,etc.,informfutureiterationsofthebusinessmodel.

• Theexternalcontextinwhichtheorganizationoperates–Anoverviewoftheexternalpolicy,regulatory,societalandenvironmentalcontextinwhichanorganizationoperates,theopportunitiesandrisksitfacesandhowitrespondstotheexternalcontextisimportantforassessingtheresilienceofanorganization’svaluecreationmechanism.Thepolicyandregulatorycontextcanhaveasignificantinfluenceonhow,andtheextenttowhich,theorganizationisabletocreatevalue.Increasingregulationofpollution,wasteandresourcesandchangingapproachestosubsidiescanforcechangestoabusinessmodelandstrategyandthereforeaffectvaluecreation.Regulationandpolicyalsoinfluencethewayinwhichanorganizationpreparescorporatereportsandcommunications.Thegrowingtrendforregulatorstoimposemandatoryreportingrequirementsonsocial,environmentalandgovernanceissuesmayinfluencethewayinwhichanorganizationmeasures,understandsandcommunicatesvaluecreation.

• Valuedriversarecapabilitiesorvariablesresultinginoutcomesthatgiveanorganizationcompetitiveadvantageandoverwhichithassomedegreeofcontrolsoastocreatevalue.Theymayinclude:

• financialdriverssuchaspricingstrategy,operationalefficiency,brandequityandcostofcapital;• non-financialdriverssuchascustomerrelations,societalexpectations,environmentalconcerns,

innovationandcorporategovernance;valuessuchasintegrity,trustandteamworkthatsupportvaluecreation.Valuedriversaloneandincombinationaffectanorganization’sabilitytocreatevalueovertimeoratapointintime.Thetypeandcombinationofrelevantvaluedriversareuniquetoeachorganizationandarethereforelikelytoberelevantfordisclosureinanintegratedreport.

• Connections–Valueiscreatedordestroyedbyorganizationsfromconnectionsbetweenawiderangeoffactorsincludingbusinessactivitiesandthewidersystemandcontextinwhichtheyoperate,includingplanetarylimitsandsocietalexpectations.TheGuidingPrincipleofConnectivityofInformation,whenappliedfor<IR>purposes,encouragescommunicationsthatreflectthedynamicnatureofbusiness,performanceandthewidereconomic,environmental,socialandfinancialsystemswithinwhichthebusinessoperates.Anorganizationshouldthereforereflectinitsdisclosuresaboutvaluecreationtheconnectivitybetweenthevariouspartiesandfactorsthathaveaninterestinthevaluethattheorganizationpurportstohavecreatedorplanstocreateandthevaluethatisatrisk.

4BPracticallimitationstothecommunicationofvaluecreation48Thissectionconsidershowinformationaboutvaluecreationshouldbeidentifiedforcommunicationinanintegratedreport,giventhatanorganizationcannotknowalloftheconnectionsbetweentheiractivities,outcomesandvaluecreationordepletionfordifferentconstituenciesovermultipletimeframes.Thissectionalsoconsidersthewayinwhichinformationaboutvaluecreationmaybeexpressedgiventheabsenceofstandardizedandrecognizedmeasurementapproachesforsometypesofvaluecreationordestruction.

Drawingaboundaryaroundvaluecreation49<IR>shouldcommunicatewhethervaluehasbeencreatedordestroyedfortheorganization,economy,environmentandsocietyonthebasisthatallaspectsofvaluecreation(ordestruction)mayultimatelyimpactanorganization’sownabilitytocreatevalue.However,business(orany)activitycanhaveimpactsfarbeyondthoseanticipatedorcapableofobservationbytheorganizationitself.Thefullextentoftheso-called

14

“butterflyeffect”40andtheconnectionsbetweencorporateactivityandoutcomesandwhethertheycreatevaluecannotbeknownorassessedbyanorganization.Theextenttowhichanorganizationcanassessandcommunicatetheconnectionsbetweentheiractivityandvaluecreationovertimethereforehaspracticallimitations.

50Whenreportingonvalue,anorganizationmaythereforedrawaboundaryaroundelementsandinteractionsthataremostrelevanttotheirbusinessmodelandstrategy,andthereforetothewayinwhichtheorganizationexpectstocreatevalueovertime.Theboundaryshouldbedisclosedtogetherwithanysignificantassumptionsandestimatesmadebymanagementinitsdisclosuresaboutvaluecreation,sothatintendedusersunderstandthelimitationsoftheconnectionsthatitispossiblefortheorganizationtomake,giventhatsomeofthemmightbeoutsideitssphereofknowledge,ormightnotyetbeapparent.

Thetimeframeforconsideringvaluecreationprospects51Similarly,thelengthofthetimeframeoverwhichfuturevaluecreationprospectsareconsideredwillvaryfrombusinesstobusiness.Thetimeframeoverwhichvaluecreationshouldbeconsideredandcommunicatedistheonethatismostappropriateinthecircumstances(whichinsomecaseswillbeshorttermandotherslongerterm).Inotherwords,thefocusshouldbeonthe“appropriate”perspectiveandtimehorizonforcreatingsustainablevaluefortheparticularorganization.

52Whilefocusingonthelongterm,informationonshortandmediumtermprospectsandperformanceofcourseremainsuseful,inparticularasthiswillbecrucialinassessingthelikelihoodofanorganizationattainingitslongtermgoalsandassessingperformanceagainstpreviouslystatedobjectives.Communicationaboutwhenvalueislikelytobecreatedordestroyedmaythereforebeuseful.

Communicatingvaluecreationwithorwithoutquantitativemeasurements53Communicationaboutvaluecreationisnotrestrictedtoinformationthatwilleventuallyfindexpressionasfinancialvalueorasresultsandoutcomesthatcanbemonetized.Informationthatsupportsthecommunicationofvaluecreationcanbeconveyedinquantitativeorqualitativeterms,oracombinationofboth.Inconsideringtherisksandrewardsexpectedfromanorganizationanditscapacitytocreatevalue,providersoffinancialcapitalandotherswillconsiderwhethertheorganizationisusingresourcescost-efficientlyandwithinplanetarylimitsandsocietalexpectations.Therefore,inadditiontoresultsabouthowtheorganizationismakingendsmeetorbalancingbudgets,intendedreportuserswillneedtounderstandtheoutcomesoftheorganization’sbusinessactivitiesforitsstakeholdersandfortheplanetonthebasisthatthoseoutcomesmayaffecttheorganization’sabilitytocreatefuturevalue.

54For<IR>,valuecreationmaybemanifestedinchangestothecapitals.Arguably,valuefor<IR>isequaltothedifferencebetweenthetotalvaluestoredinthecapitalsatthebeginningofthemeasurementperiodorreportingyearandthetotalamountofvaluestoredinthecapitalsattheendoftheperiodorreportingyeartakingintoaccounttheinputs,activitiesandoutputsoftheorganization.Communicationabouteffectsonthecapitalsdoesnotnecessarilyinvolvemeasurementofthemovementsin,orchangesto,thecapitals.AstheCapitalsBackgroundPaperstates,“itisnotanobjectiveof<IR>tomeasureallthecapitalsormovementsinthem.Manyusesofandeffectsonthecapitalsarebest(andinsomecasescanonlybe)reportedintheformofnarrative,ratherthanthroughmetrics.Whereitisnotpracticabletomeasuremovementsinthecapitalsquantitatively,qualitativedisclosuresmaybeusedtoexplainchangesintheavailability,quality,oraffordabilityofcapitalsasbusinessinputsandhowtheirusebytheorganizationenhancesordepletesthem.Insomecasesmonetizationofthesefactorsmay,wherepossible,beappropriate,particularlywherecostsrelatedtoexternalitiesarelikelytobecomeinternalizedasaresultofnewlaws,regulationsandeconomicinstruments.

55TheInternational<IR>Frameworkwillnotprescribemetricstobeusedinanintegratedreportorforthepurposesofmeasuringvalue.However,workconductedbyotherorganizations(e.g.,theGlobalReportingInitiativeandSustainabilityAccountingStandardsBoard,WorldIntellectualCapitalInitiative,EuropeanFederationofFinancialAnalysts,PUMAetc.),mayinformthewayinwhichaspectsofvaluecreationanddestructionarecommunicated.

40 Usually attributed to E. N. Lorenz to describe chaotic behavior in dynamic systems, whereby the smallest change in initial conditions (e.g., a butterfly flapping its wings), may lead to bigger changes in the behavior of the system.

15

5. examples of communication about value creation56Formanycompanies,theirdescriptionofvaluecreationisdepictedholisticallythroughtheirentirereportingandaseparatesectiononvaluecreationisnotclearlydistinguishable.Othercompaniesarelinkingtheirvaluecreationstorytotheirbusinessmodelandthestrategiesthattheyhaveinplacetoensuretheirlongtermsuccess.Thissectionincludeslinkstoextractsfrompublicreportstoillustratethewayinwhichcompaniesareattemptingtocommunicatevaluecreation.Theextractsarenotintendedtorepresentbestpracticeoratemplateforcommunicationofvaluecreation.Rather,theyillustratethecurrentapproachbeingtakenbyselectedorganizationsforcommunicatingaspectsofvaluecreation.

Example5.1SABMillerplcAnnualReportfortheyearended31March2012,p.15,www.sabmiller.comThesepagesofferanoverviewofthecorestrategiesthatthecompanyfollowstocreatevalue.

Example5.2FresnilloplcAnnualReportfortheyearended31March2012,p.3-9&33,www.fresnilloplc.comThesepagesrepresentFresnillo’sdescriptionofitsbusinessmodelandhowitcreatesstakeholdervaluebyspecificallydisclosingthekeyinputsandoutputsandkeystakeholderrelationshipsitdependsonandhowitcreatesvalueforeachstakeholder.

Example5.3AngloAmericanplcSocialDevelopmentReportfortheyearended31December2012,p.24-35,www.angloamerican.comThesepagesexplainhowAngloAmericancreatesvalueforsociety,itshostcountriesanditshostcommunitiesinwhichitoperates,discussingvariousinfrastructureimprovements,localspendingandotherfactorsthatcreatevalueintheareasinwhichitoperates.

Example5.4StandardBankGroupAnnualReportfortheyearended31December2012,p.8,www.standardbank.comThispagerepresentsadepictionofhowStandardBankcreatesfinancialvalue.

Example5.5Vodacom(pty)Limitedfortheyearended31March2013,p.6-7,www.vodacom.comThesepagesrepresentadescriptionofwhatVodacomdoeswiththevalueitcreatesaswellasadiscussiononhowitsabilitytocreatevalueisunderpinnedbydeliveringonitsstrategicprioritiestherebyconnectingitsvalue-addingactivitiestoitsstrategicpriorities.

Example5.6Go-AheadGroupplcAnnualReportfortheyearended30June2012,p.6-7,www.go-ahead.comThesepagesdepictGo-Ahead’sbusinessmodelrepresentedinatablethatlinksthebusinessmodeltohowitgeneratesvalue,alsomentioningtheactionstheyputinplacetobetakeninordertomakeensurethatvalueisgenerated.

Example5.7TataSteelGroupAnnualReportfortheyear2011-2012p.62,www.tatasteel.comThispagedescribesthevaluecreationprocessatTataSteel.

16

Example5.8DanoneGroupRegistrationAnnualFinancialReportFortheyear2011,p.15,www.danone11.danone.comThispageidentifiesupstreamactivityasoneofthesourcesoftheGroup’svaluecreationprocess.

Example5.9GoldFieldsLimitedIntegratedReviewFortheyearended31December2012,p.13www.goldfields.co.zaThediagramonthispagequantifiessharedvaluecreationasanoutputfrom2012.

Conclusion57ThisBackgroundPaperreflectssomeofthetheoryandpracticethatinformsanunderstandingofvaluecreation,aswellasexplainingvaluecreationfor<IR>purposes.Itdoesnotprovideacompleteanswertounderstandingorcommunicatingvaluecreation,butofferstheories,examplesofpractice,adefinitionandguidancethataimtoadvancethinkingaboutvaluecreationandthecommunicationthereofbyorganizations.Justasithastakentimetodevelopandimproveprocesses,language,frameworksandtoolsforreportingotheraspectsofcorporateactivity,newapproacheswillinevitablyemergetoenablereporterstocommunicatereportuserstoassessanddecisionmakerstoactoninformationaboutthewayinwhichorganizationscreatevalue.

58Ultimatelyvalueistobeinterpretedbyreferencetothresholdsandparametersestablishedthroughstakeholderengagementandevidenceaboutthecarryingcapacityandlimitsofresourcesonwhichstakeholdersandcompaniesrelyforwellbeingandprofit,aswellasevidenceaboutsocietalexpectations.Interconnectionsbetweencorporateactivity,societyandtheenvironmentandthepurposeofthecorporationshouldthereforebeunderstoodintermsofwhatthecorporation,societyandtheenvironmentcantolerateandstillsurvive–thatwillbethemaindeterminantofvalue.Thechallengeswillbetoreachagreementatcorporate,nationalandinternationallevelonwhatthosethresholdsandlimitsare,howtheresourceswithinthoselimitsshouldbeallocated,andwhatactionisneededtokeepactivitywithinthoselimitssothatvaluecancontinuetobecreatedovertime.

17

ViSit the eMerging integrated rePorting dataBaSe

http://examples.theiirc.org/