Embed Size (px)

Citation preview

VEC Tutorial

Dean Fantazzini

Dipartimento di Economia Politica e Metodi Quantitativi

University of Pavia

Overview of the Lecture

1st A review of Johansen’s approach for cointegration

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 2

Overview of the Lecture

1st A review of Johansen’s approach for cointegration

2nd An empirical example: the long run Phillips curve

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 2-a

Overview of the Lecture

1st A review of Johansen’s approach for cointegration

2nd An empirical example: the long run Phillips curve

3rd An empirical example: Italian Treasury bills interest rates

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 2-b

Overview of the Lecture

1st A review of Johansen’s approach for cointegration

2nd An empirical example: the long run Phillips curve

3rd An empirical example: Italian Treasury bills interest rates

4th An empirical example: A model for the Danish Economy

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 2-c

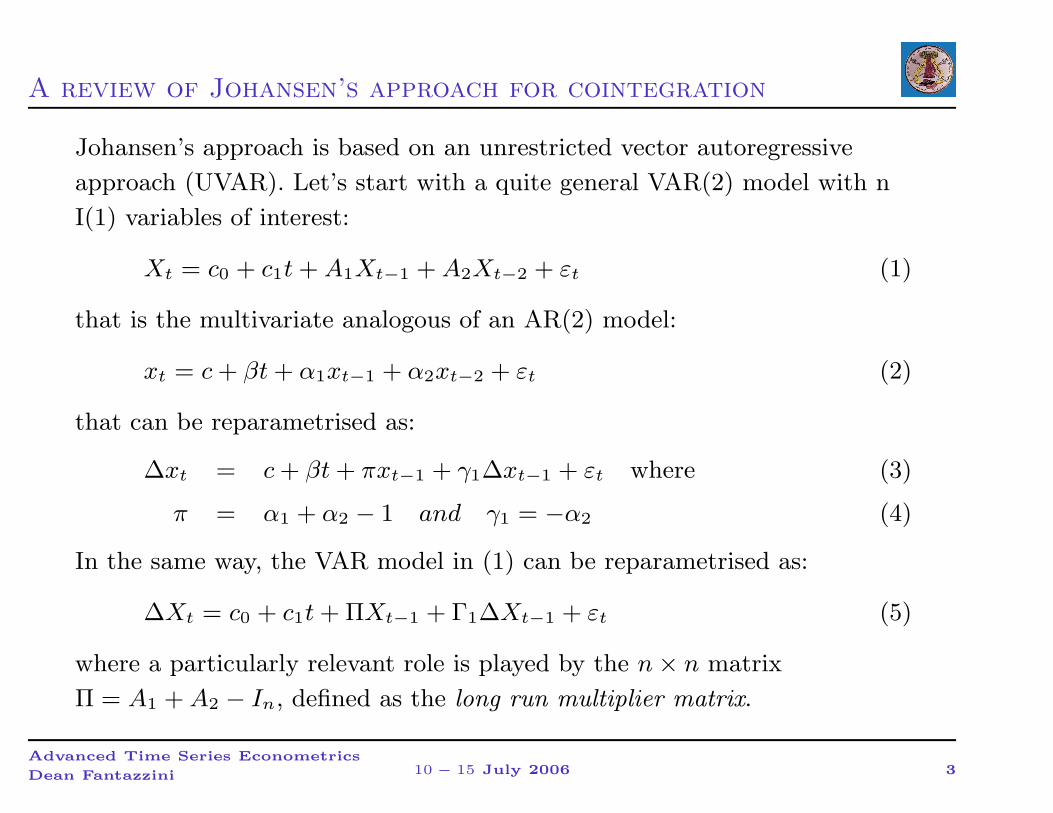

A review of Johansen’s approach for cointegration

Johansen’s approach is based on an unrestricted vector autoregressive

approach (UVAR). Let’s start with a quite general VAR(2) model with n

I(1) variables of interest:

Xt = c0 + c1t + A1Xt−1 + A2Xt−2 + εt (1)

that is the multivariate analogous of an AR(2) model:

xt = c + βt + α1xt−1 + α2xt−2 + εt (2)

that can be reparametrised as:

∆xt = c + βt + πxt−1 + γ1∆xt−1 + εt where (3)

π = α1 + α2 − 1 and γ1 = −α2 (4)

In the same way, the VAR model in (1) can be reparametrised as:

∆Xt = c0 + c1t + ΠXt−1 + Γ1∆Xt−1 + εt (5)

where a particularly relevant role is played by the n × n matrix

Π = A1 + A2 − In, defined as the long run multiplier matrix.

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 3

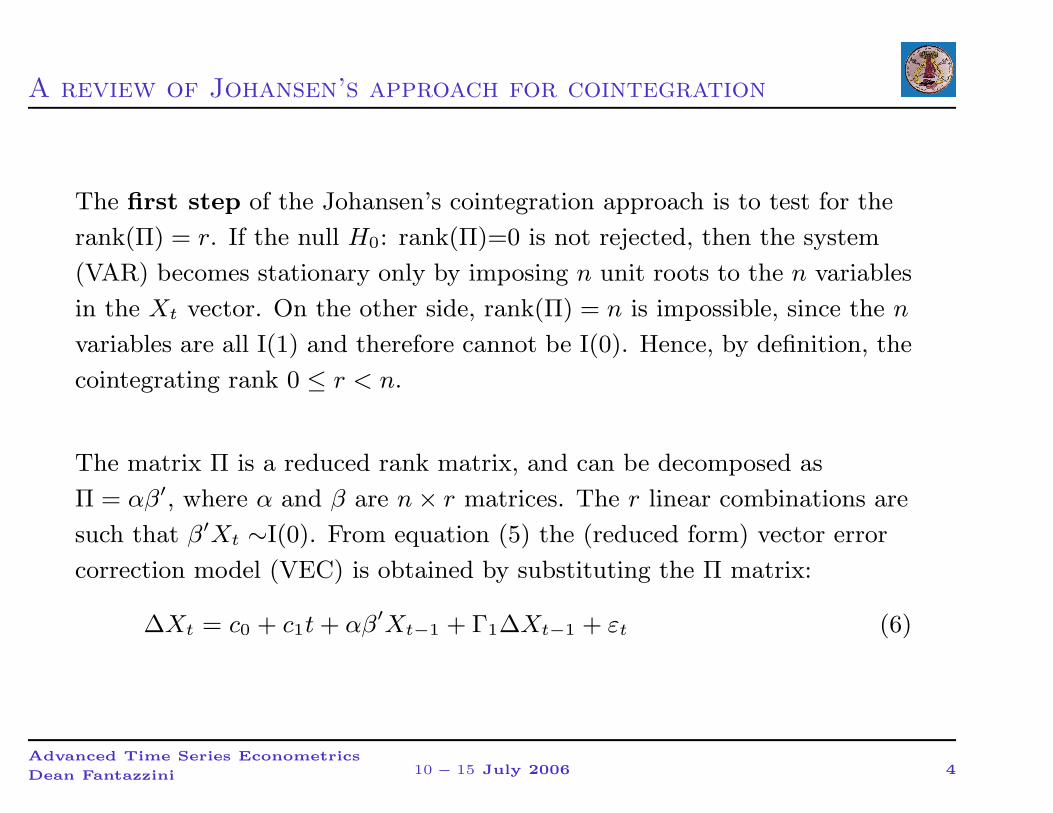

A review of Johansen’s approach for cointegration

The first step of the Johansen’s cointegration approach is to test for the

rank(Π) = r. If the null H0: rank(Π)=0 is not rejected, then the system

(VAR) becomes stationary only by imposing n unit roots to the n variables

in the Xt vector. On the other side, rank(Π) = n is impossible, since the n

variables are all I(1) and therefore cannot be I(0). Hence, by definition, the

cointegrating rank 0 ≤ r < n.

The matrix Π is a reduced rank matrix, and can be decomposed as

Π = αβ′, where α and β are n × r matrices. The r linear combinations are

such that β′Xt ∼I(0). From equation (5) the (reduced form) vector error

correction model (VEC) is obtained by substituting the Π matrix:

∆Xt = c0 + c1t + αβ′

Xt−1 + Γ1∆Xt−1 + εt (6)

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 4

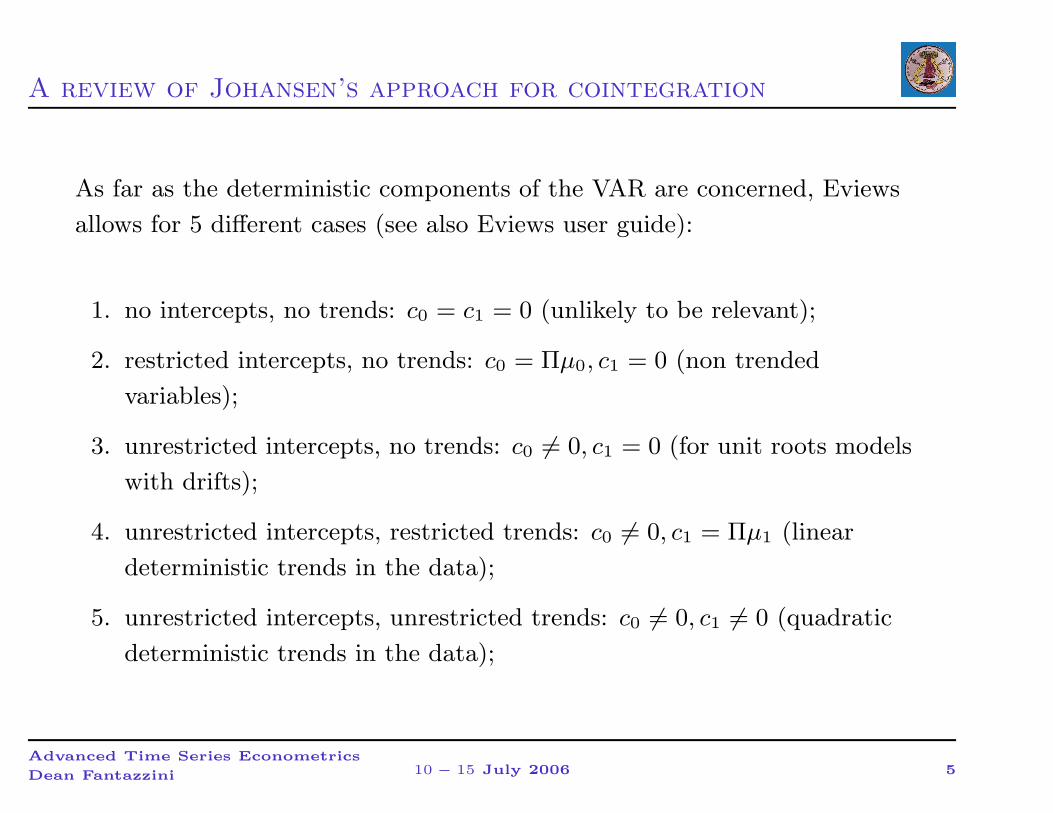

A review of Johansen’s approach for cointegration

As far as the deterministic components of the VAR are concerned, Eviews

allows for 5 different cases (see also Eviews user guide):

1. no intercepts, no trends: c0 = c1 = 0 (unlikely to be relevant);

2. restricted intercepts, no trends: c0 = Πµ0, c1 = 0 (non trended

variables);

3. unrestricted intercepts, no trends: c0 6= 0, c1 = 0 (for unit roots models

with drifts);

4. unrestricted intercepts, restricted trends: c0 6= 0, c1 = Πµ1 (linear

deterministic trends in the data);

5. unrestricted intercepts, unrestricted trends: c0 6= 0, c1 6= 0 (quadratic

deterministic trends in the data);

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 5

A review of Johansen’s approach for cointegration

The null hypothesis of the trace test is Hr : rank(Π) = r against the

alternative hypothesis of (trend)-stationarity: Hn : rank(π) = n (full

rank). The trace statistic is also a loglikelihood ratio statistic, and the

appropriate critical values for all the five cases are reported by Eviews.

−→ To determine the number of cointegrating relations r, subject to the

assumptions made about the trends in the series, we can proceed

sequentially from r = 0 to r = n − 1 until we fail to reject.

The first row in the upper table tests the hypothesis of no cointegration,

the second row tests the hypothesis of one cointegrating relation, the third

row tests the hypothesis of two cointegrating relations, and so on, all

against the alternative hypothesis of full rank, i.e. all series in the VAR are

stationary.

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 6

A review of Johansen’s approach for cointegration

After the value of r is estimated, the second step is to identify β. When r

= 1, there are no problems: the normalization (one) restriction for the

parameter of what the economic theory suggests is the dependent variable

yields a unique estimate up to a scaling parameter. However, when r > 1,

the problem of identification arises. The appropriate procedure would be

to estimate the cointegrating relationships subject to a priori restrictions

from the economic theory.

Suppose there are r cointegrating relations and β is a n × r matrix, then

we need at least r restrictions (including the normalization restriction) on

each of the r cointegrating relationships. The exact identification of the

whole cointegrating parameters requires r × r restrictions.

Remember: the source of these identifying restrictions is usually from a

priori theory. As far as the role of theory in providing these restrictions are

discussed in Pesaran (1997).

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 7

An empirical example: the long run Phillips curve

−→ We want to estimate the long run Phillips curve, that is the long run

relationship between real wage growth and (logs of) the unemployment

rate.

Open the workfile Phillips.WF1. You find the following variables (yearly

data):

Variable Description

lu log of Italian unemployment rate 1960-1999

dlw difference in logs of wages 1961-1999

dlp difference in logs of prices 1961-1999

dlwp difference in logs of real wages 1961-1999

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 8

An empirical example: the long run Phillips curve

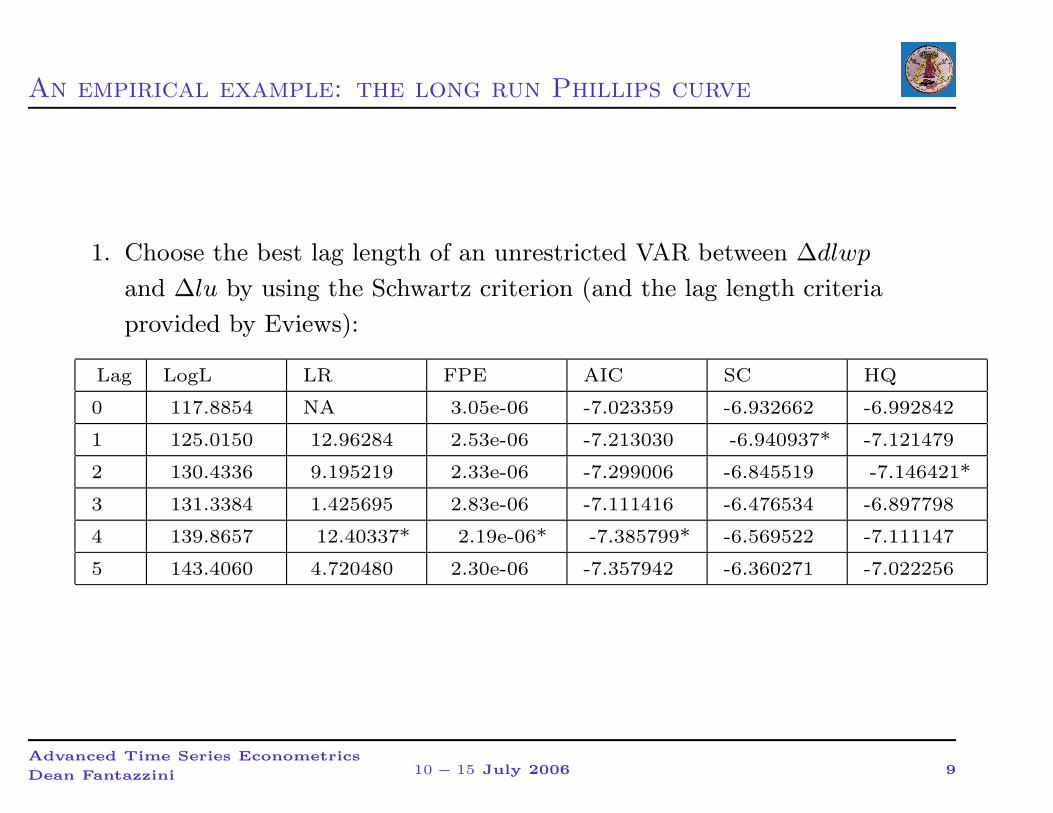

1. Choose the best lag length of an unrestricted VAR between ∆dlwp

and ∆lu by using the Schwartz criterion (and the lag length criteria

provided by Eviews):

Lag LogL LR FPE AIC SC HQ

0 117.8854 NA 3.05e-06 -7.023359 -6.932662 -6.992842

1 125.0150 12.96284 2.53e-06 -7.213030 -6.940937* -7.121479

2 130.4336 9.195219 2.33e-06 -7.299006 -6.845519 -7.146421*

3 131.3384 1.425695 2.83e-06 -7.111416 -6.476534 -6.897798

4 139.8657 12.40337* 2.19e-06* -7.385799* -6.569522 -7.111147

5 143.4060 4.720480 2.30e-06 -7.357942 -6.360271 -7.022256

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 9

An empirical example: the long run Phillips curve

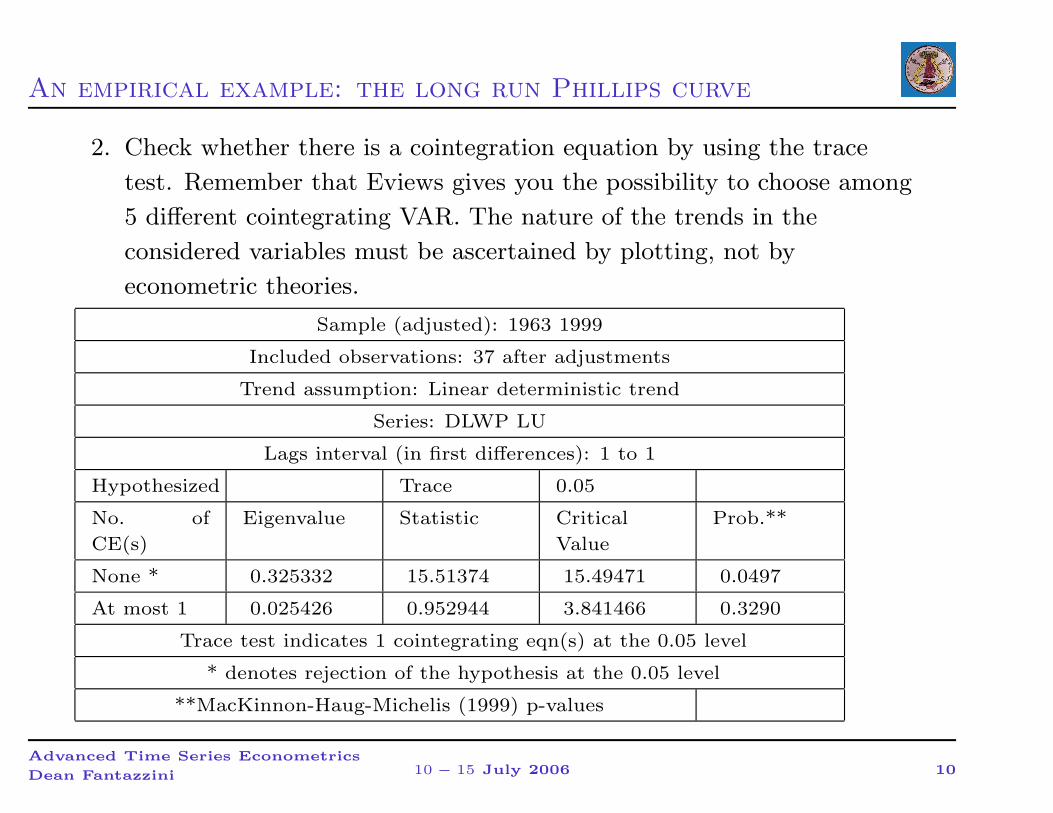

2. Check whether there is a cointegration equation by using the trace

test. Remember that Eviews gives you the possibility to choose among

5 different cointegrating VAR. The nature of the trends in the

considered variables must be ascertained by plotting, not by

econometric theories.

Sample (adjusted): 1963 1999

Included observations: 37 after adjustments

Trend assumption: Linear deterministic trend

Series: DLWP LU

Lags interval (in first differences): 1 to 1

Hypothesized Trace 0.05

No. of

CE(s)

Eigenvalue Statistic Critical

Value

Prob.**

None * 0.325332 15.51374 15.49471 0.0497

At most 1 0.025426 0.952944 3.841466 0.3290

Trace test indicates 1 cointegrating eqn(s) at the 0.05 level

* denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 10

An empirical example: the long run Phillips curve

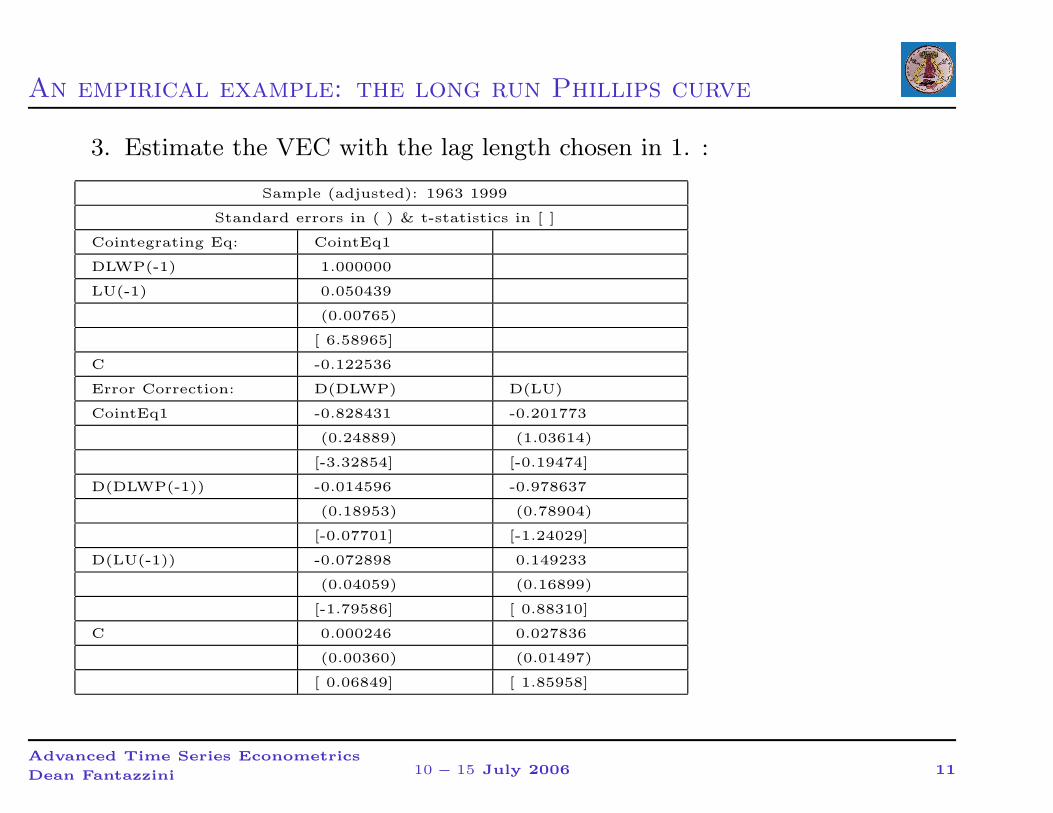

3. Estimate the VEC with the lag length chosen in 1. :

Sample (adjusted): 1963 1999

Standard errors in ( ) & t-statistics in [ ]

Cointegrating Eq: CointEq1

DLWP(-1) 1.000000

LU(-1) 0.050439

(0.00765)

[ 6.58965]

C -0.122536

Error Correction: D(DLWP) D(LU)

CointEq1 -0.828431 -0.201773

(0.24889) (1.03614)

[-3.32854] [-0.19474]

D(DLWP(-1)) -0.014596 -0.978637

(0.18953) (0.78904)

[-0.07701] [-1.24029]

D(LU(-1)) -0.072898 0.149233

(0.04059) (0.16899)

[-1.79586] [ 0.88310]

C 0.000246 0.027836

(0.00360) (0.01497)

[ 0.06849] [ 1.85958]

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 11

An empirical example: the long run Phillips curve

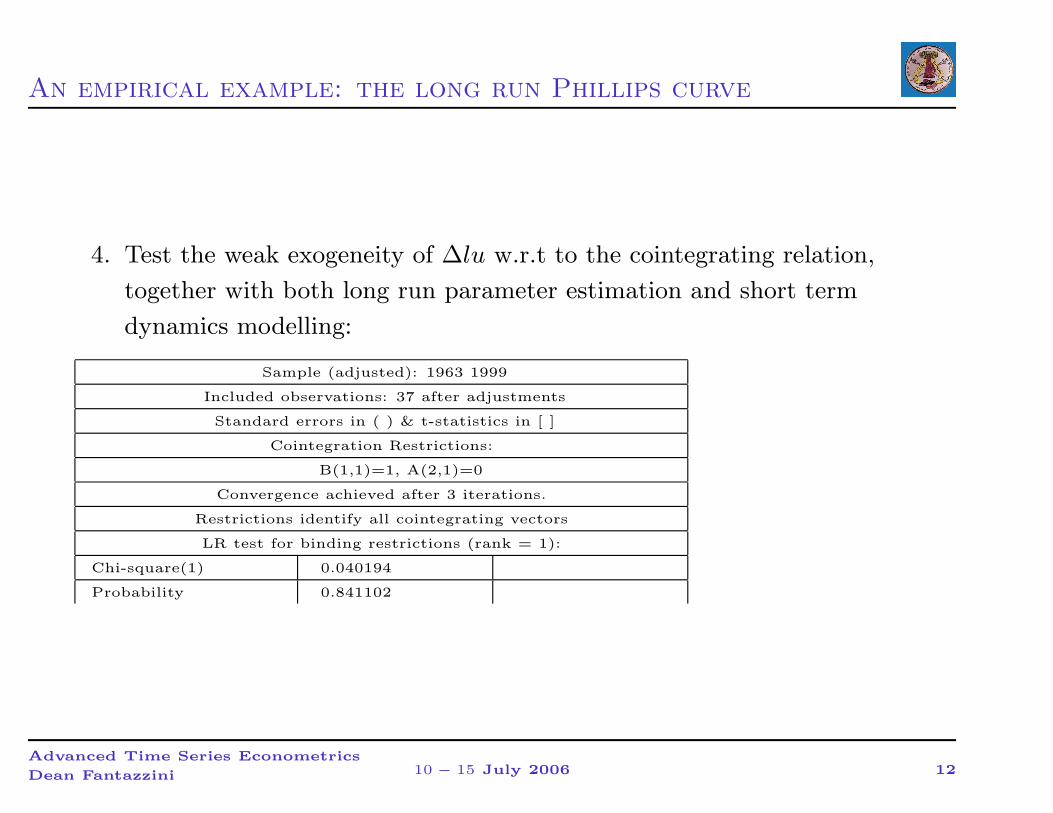

4. Test the weak exogeneity of ∆lu w.r.t to the cointegrating relation,

together with both long run parameter estimation and short term

dynamics modelling:

Sample (adjusted): 1963 1999

Included observations: 37 after adjustments

Standard errors in ( ) & t-statistics in [ ]

Cointegration Restrictions:

B(1,1)=1, A(2,1)=0

Convergence achieved after 3 iterations.

Restrictions identify all cointegrating vectors

LR test for binding restrictions (rank = 1):

Chi-square(1) 0.040194

Probability 0.841102

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 12

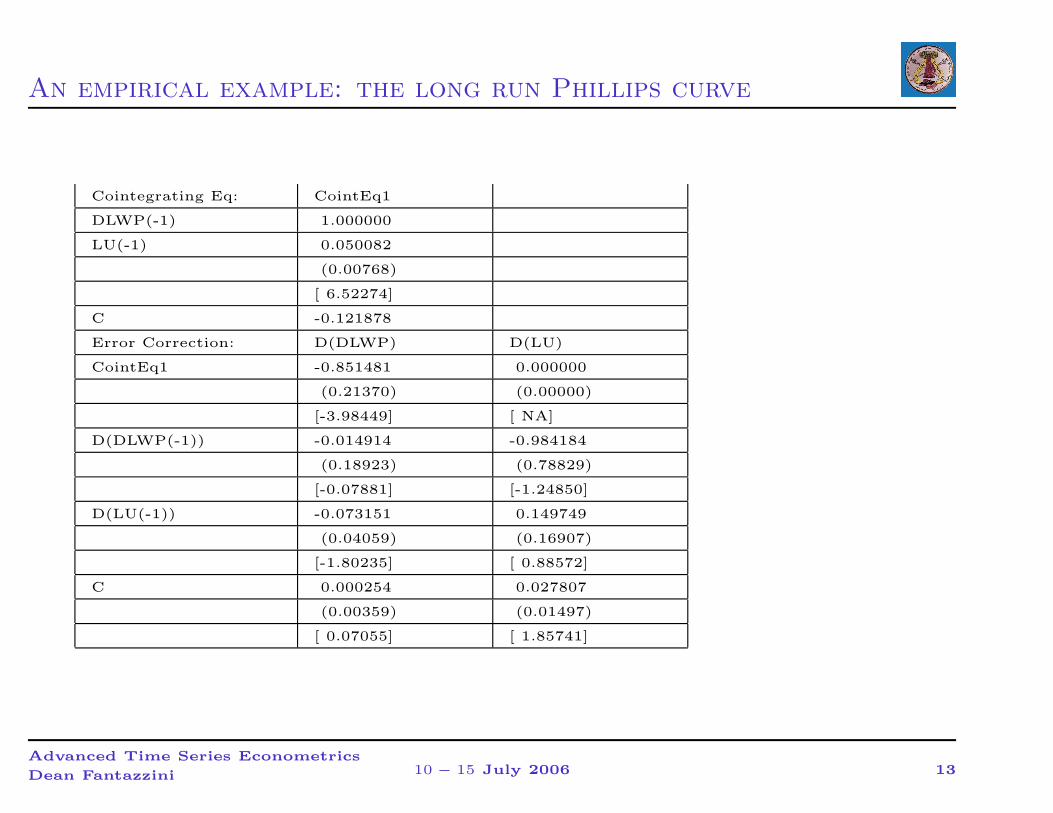

An empirical example: the long run Phillips curve

Cointegrating Eq: CointEq1

DLWP(-1) 1.000000

LU(-1) 0.050082

(0.00768)

[ 6.52274]

C -0.121878

Error Correction: D(DLWP) D(LU)

CointEq1 -0.851481 0.000000

(0.21370) (0.00000)

[-3.98449] [ NA]

D(DLWP(-1)) -0.014914 -0.984184

(0.18923) (0.78829)

[-0.07881] [-1.24850]

D(LU(-1)) -0.073151 0.149749

(0.04059) (0.16907)

[-1.80235] [ 0.88572]

C 0.000254 0.027807

(0.00359) (0.01497)

[ 0.07055] [ 1.85741]

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 13

An empirical example: the long run Phillips curve

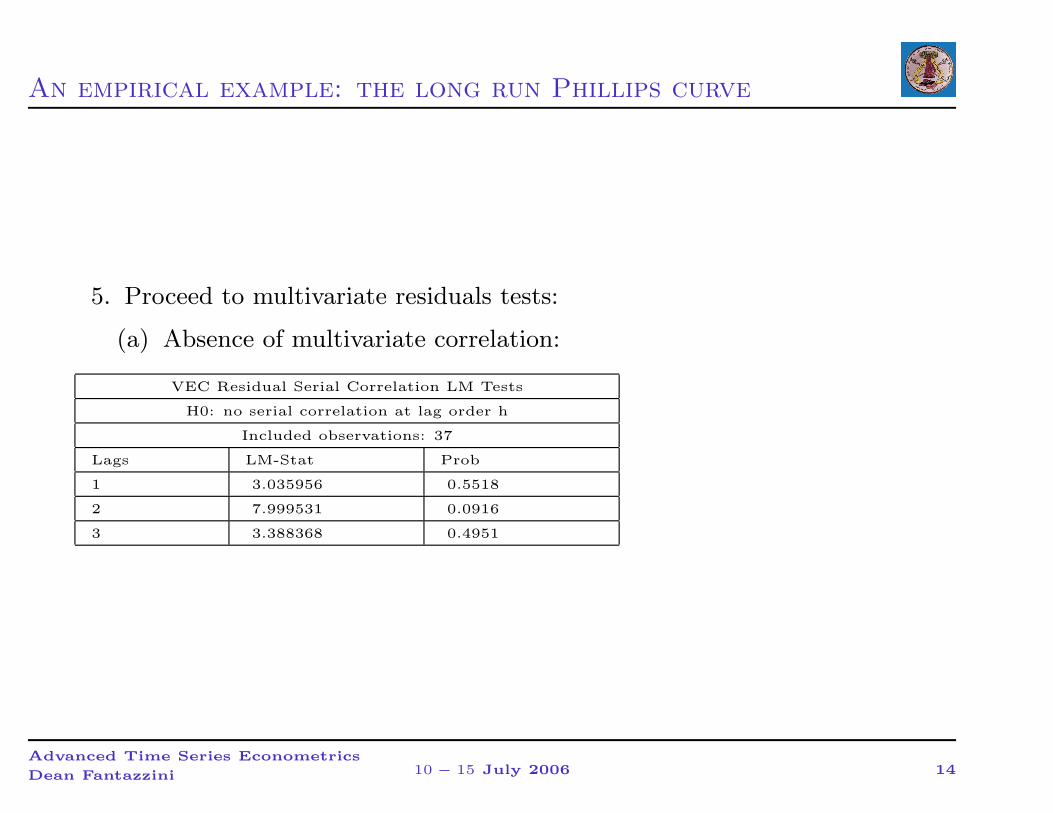

5. Proceed to multivariate residuals tests:

(a) Absence of multivariate correlation:

VEC Residual Serial Correlation LM Tests

H0: no serial correlation at lag order h

Included observations: 37

Lags LM-Stat Prob

1 3.035956 0.5518

2 7.999531 0.0916

3 3.388368 0.4951

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 14

An empirical example: the long run Phillips curve

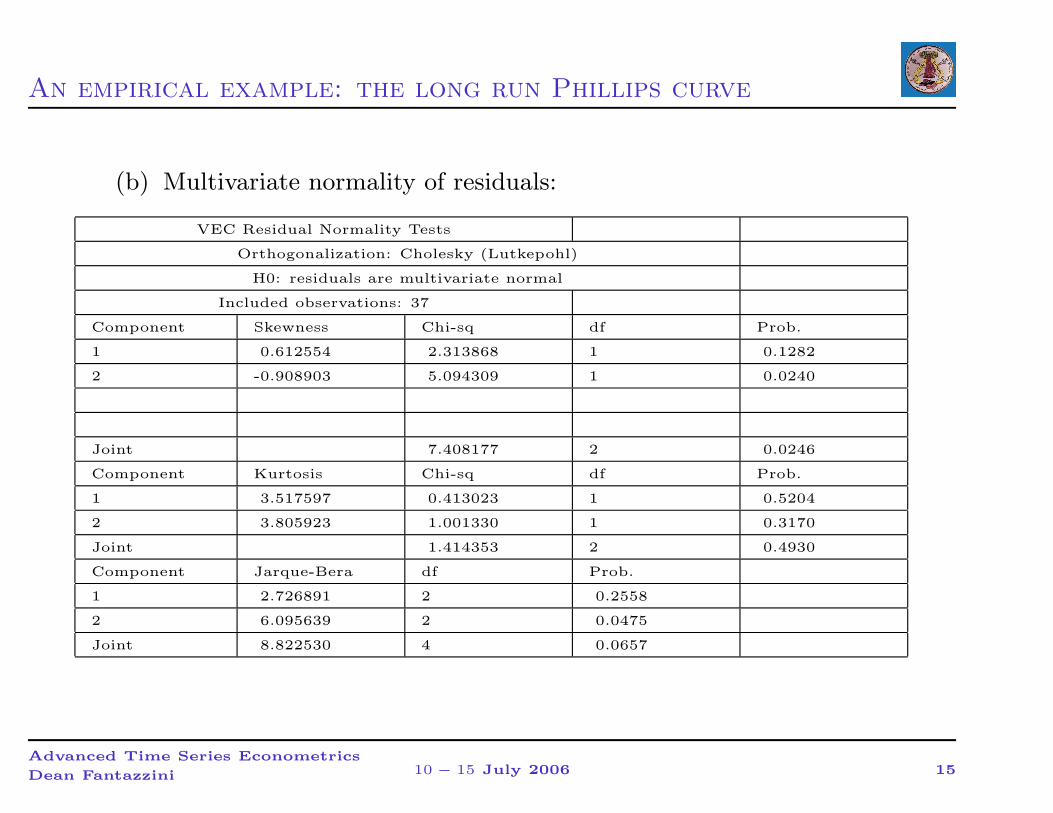

(b) Multivariate normality of residuals:

VEC Residual Normality Tests

Orthogonalization: Cholesky (Lutkepohl)

H0: residuals are multivariate normal

Included observations: 37

Component Skewness Chi-sq df Prob.

1 0.612554 2.313868 1 0.1282

2 -0.908903 5.094309 1 0.0240

Joint 7.408177 2 0.0246

Component Kurtosis Chi-sq df Prob.

1 3.517597 0.413023 1 0.5204

2 3.805923 1.001330 1 0.3170

Joint 1.414353 2 0.4930

Component Jarque-Bera df Prob.

1 2.726891 2 0.2558

2 6.095639 2 0.0475

Joint 8.822530 4 0.0657

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 15

An empirical example: the long run Phillips curve

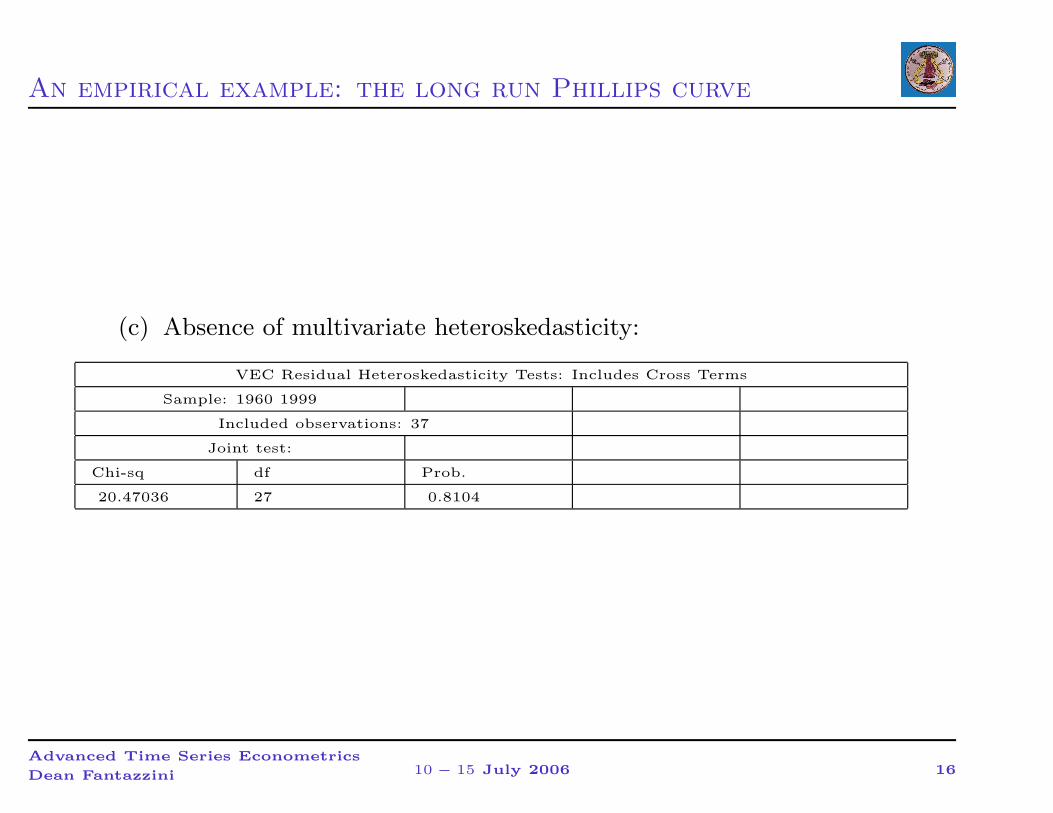

(c) Absence of multivariate heteroskedasticity:

VEC Residual Heteroskedasticity Tests: Includes Cross Terms

Sample: 1960 1999

Included observations: 37

Joint test:

Chi-sq df Prob.

20.47036 27 0.8104

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 16

An empirical example: Italian Treasury bills interest rates

−→ Another example can be drawn from Italian Treasury bills interest

rates.

Open the file termine.wf1. We have 3, 6, 12 month bills. Repeat all the

steps you did with the Phillips curve example, remembering that there

should be 2 cointegration relationships: 1) Between the 3 and 12 months

Treasury bills; 2) Between the 6 and 12 months Treasury bills.

The 12 months Treasury bill should be weak exogenous.

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 17

An empirical example: A model for the Danish Economy

−→ The following program replicates example 2.4.1 (pp.23-28) from

Johansen (1995) Likelihood-based Inference in Cointegrated Vector

Auto-regressive Models, Oxford University Press.

’replicate example 2.4.1 (pp.23-28)

’Johansen (1995) Likelihood-based Inference in Cointegrated

’Vector Auto-regressive Models, Oxford University Press

’change path to program path

%path = @runpath

cd %path

’create workfile

wfcreate denmark q 1974:1 1987:3

’fetch data from database

’data downloaded from johansen’s website at

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 18

An empirical example: A model for the Danish Economy

’http://www.math.ku.dk/ sjo/data/data.html

fetch(d=var dat) lrm lry ibo ide

’create centered seasonal dummies

for !i=1 to 3

series d!i = @seas(!i) - 0.25

next

’estimate unrestricted VAR

var var1.ls 1 2 lrm lry ibo ide @ c d1 d2 d3

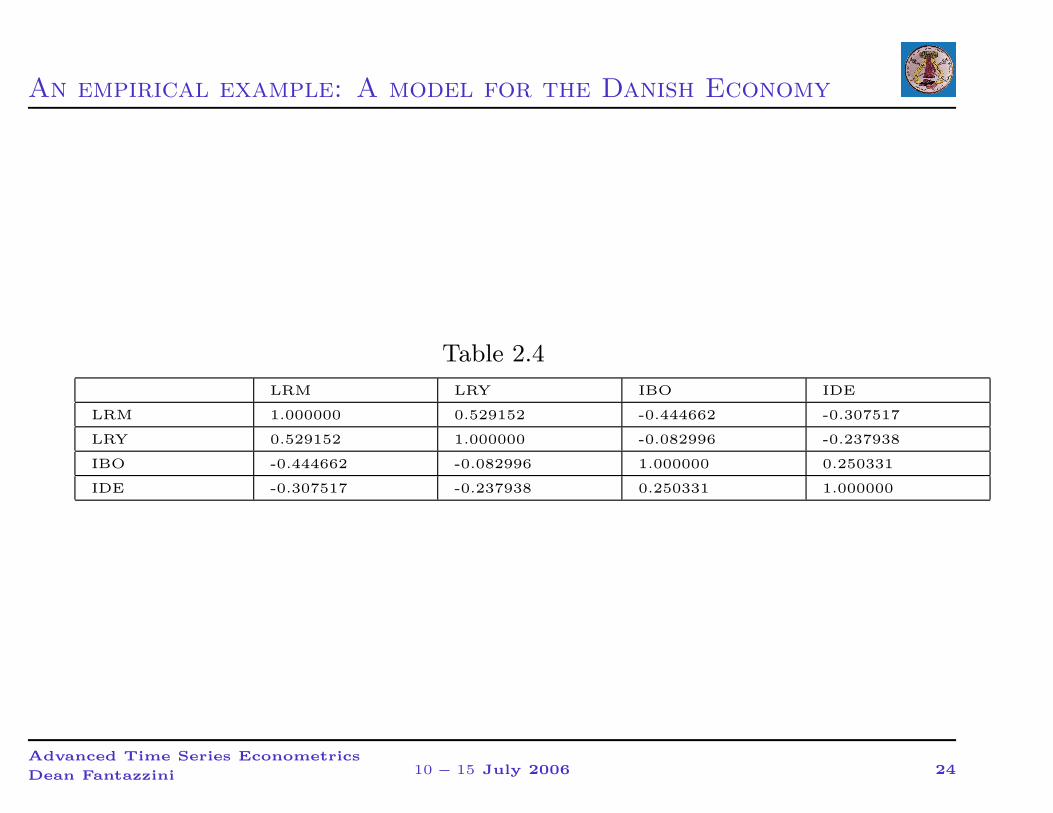

’replicate residual correlation matrix Table 2.4 (p.24)

freeze(tab24) var1.residcor

show tab24

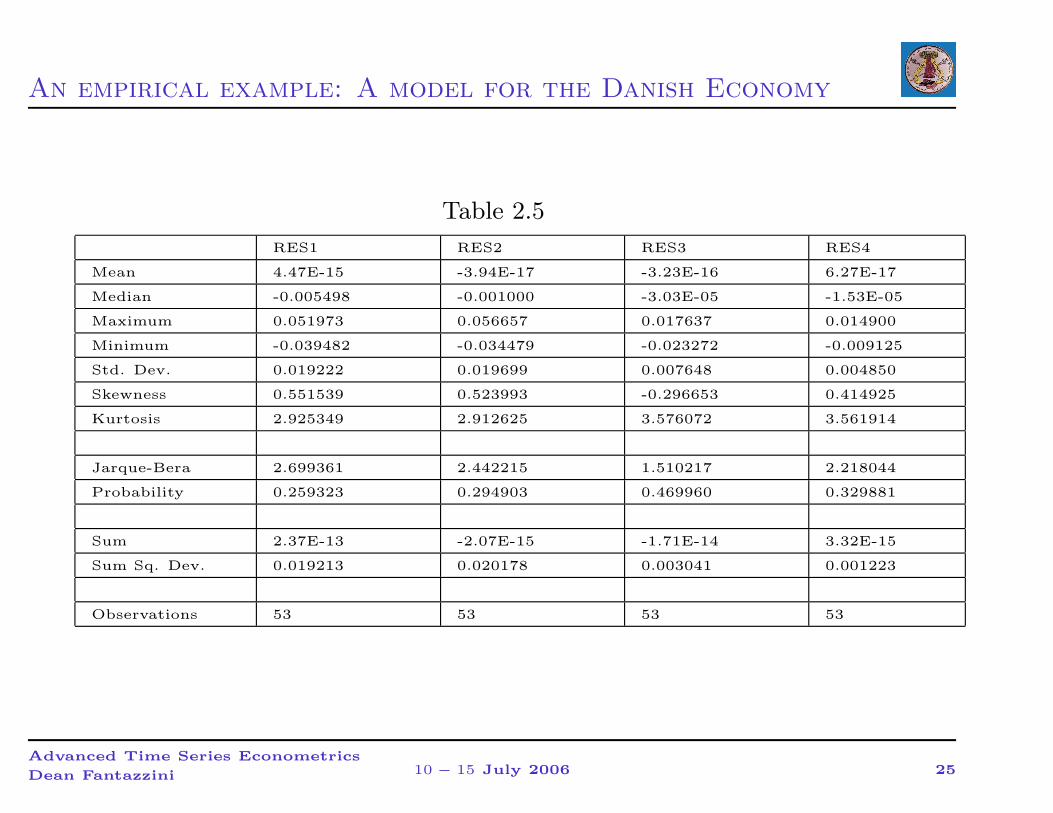

’replicate univariate residual diagnostics Table 2.5 (p.25)

’note that Johansen reports *excess* kurtosis relative to 3.0

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 19

An empirical example: A model for the Danish Economy

’also JB statistic does not match; why?

var1.makeresid(name=gres) res1 res2 res3 res4

freeze(tab25) gres.stats

show tab25

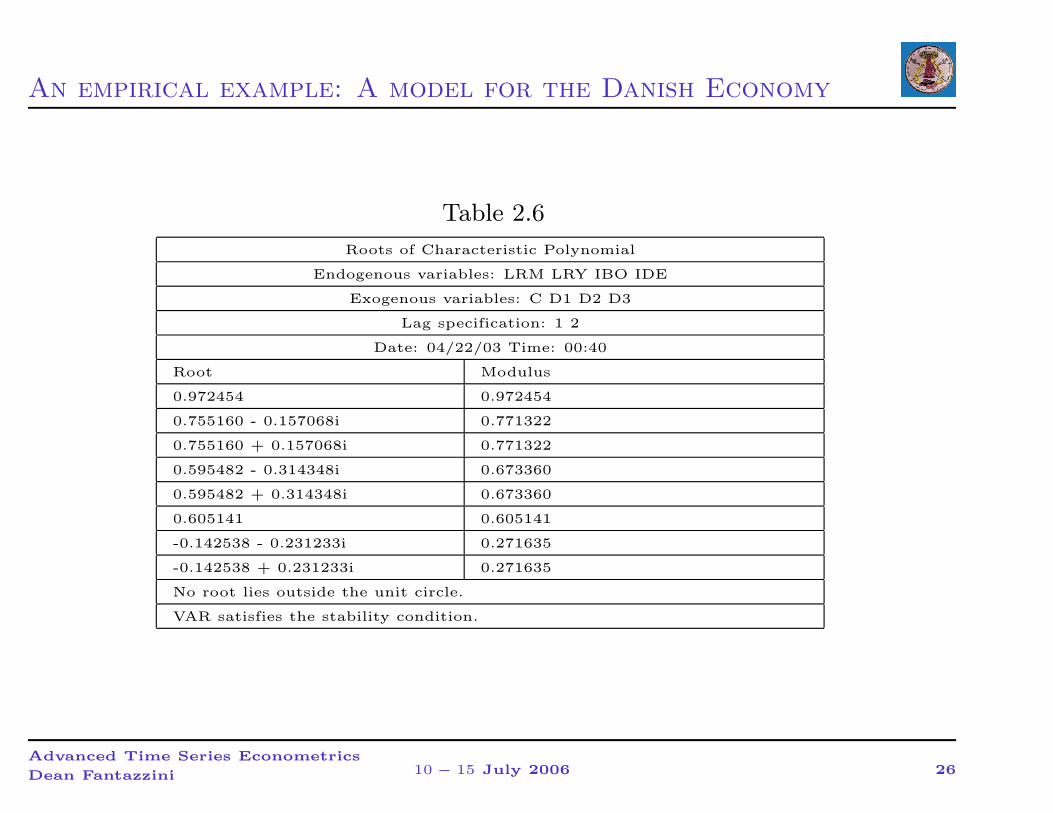

’replicate roots in Table 2.6 (p.25)

freeze(tab26) var1.arroots

show tab26

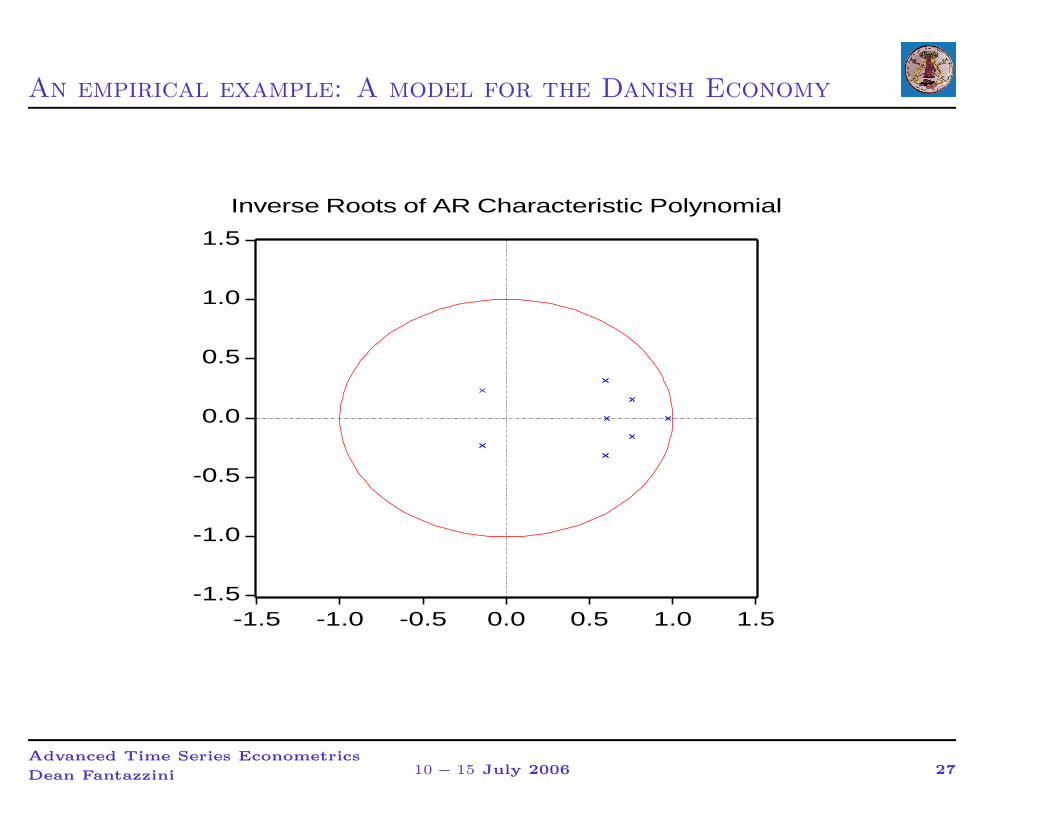

’show roots in unit circle

freeze(gra26) var1.arroots(graph)

show gra26

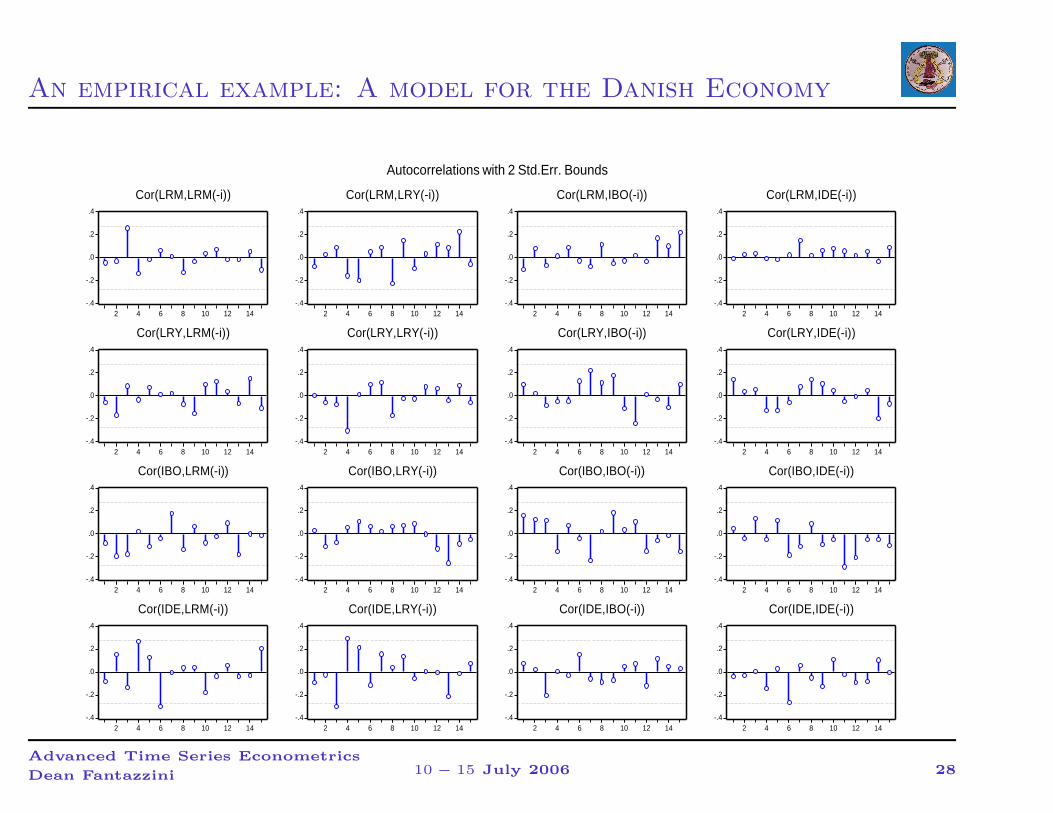

’replicate auto-correlation functions Fig 2.3 (p.28)

’note that eviews graph is transpose of Fig 2.3

freeze(fig23) var1.correl(15,graph)

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 20

An empirical example: A model for the Danish Economy

fig23.options size(4,2)

fig23.align(4,1,1)

show fig23

−→ You should get these results:

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 21

An empirical example: A model for the Danish Economy

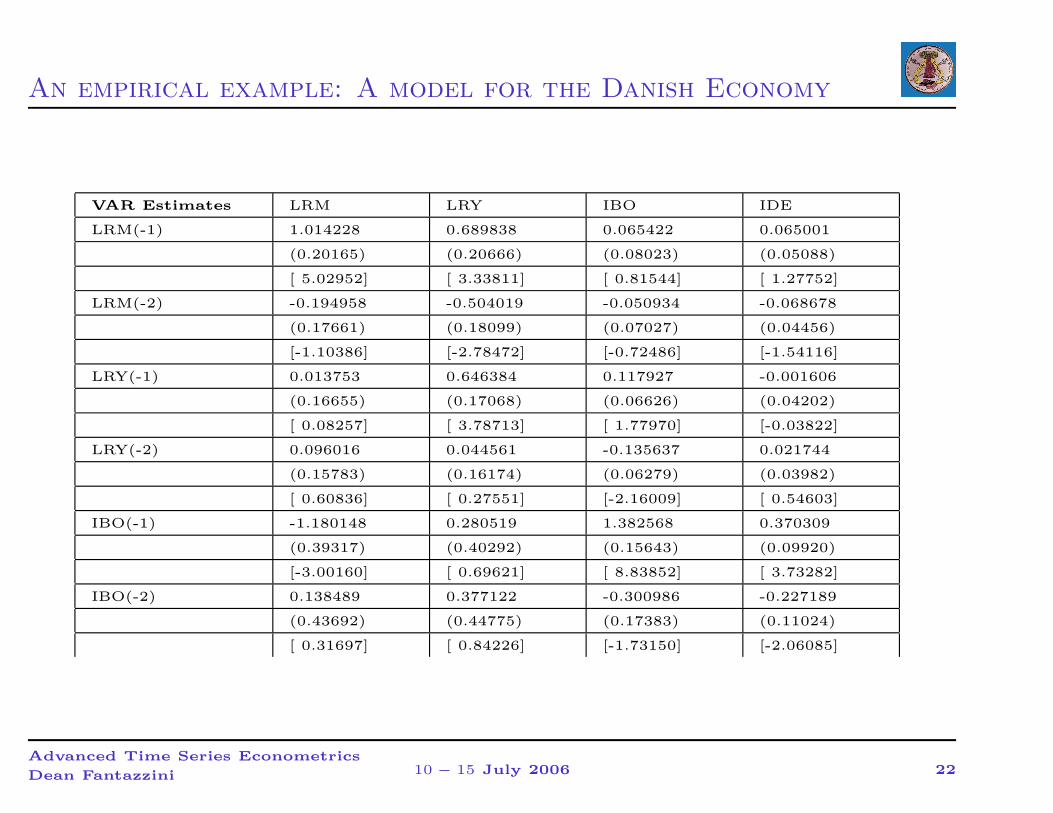

VAR Estimates LRM LRY IBO IDE

LRM(-1) 1.014228 0.689838 0.065422 0.065001

(0.20165) (0.20666) (0.08023) (0.05088)

[ 5.02952] [ 3.33811] [ 0.81544] [ 1.27752]

LRM(-2) -0.194958 -0.504019 -0.050934 -0.068678

(0.17661) (0.18099) (0.07027) (0.04456)

[-1.10386] [-2.78472] [-0.72486] [-1.54116]

LRY(-1) 0.013753 0.646384 0.117927 -0.001606

(0.16655) (0.17068) (0.06626) (0.04202)

[ 0.08257] [ 3.78713] [ 1.77970] [-0.03822]

LRY(-2) 0.096016 0.044561 -0.135637 0.021744

(0.15783) (0.16174) (0.06279) (0.03982)

[ 0.60836] [ 0.27551] [-2.16009] [ 0.54603]

IBO(-1) -1.180148 0.280519 1.382568 0.370309

(0.39317) (0.40292) (0.15643) (0.09920)

[-3.00160] [ 0.69621] [ 8.83852] [ 3.73282]

IBO(-2) 0.138489 0.377122 -0.300986 -0.227189

(0.43692) (0.44775) (0.17383) (0.11024)

[ 0.31697] [ 0.84226] [-1.73150] [-2.06085]

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 22

An empirical example: A model for the Danish Economy

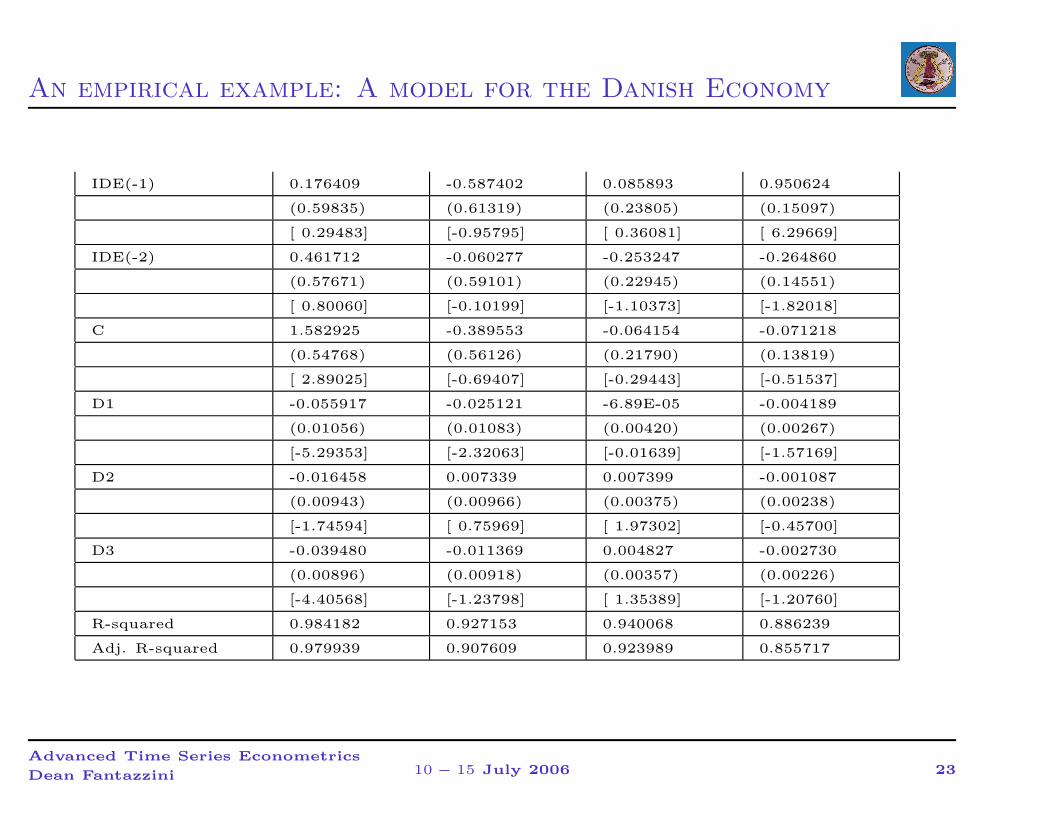

IDE(-1) 0.176409 -0.587402 0.085893 0.950624

(0.59835) (0.61319) (0.23805) (0.15097)

[ 0.29483] [-0.95795] [ 0.36081] [ 6.29669]

IDE(-2) 0.461712 -0.060277 -0.253247 -0.264860

(0.57671) (0.59101) (0.22945) (0.14551)

[ 0.80060] [-0.10199] [-1.10373] [-1.82018]

C 1.582925 -0.389553 -0.064154 -0.071218

(0.54768) (0.56126) (0.21790) (0.13819)

[ 2.89025] [-0.69407] [-0.29443] [-0.51537]

D1 -0.055917 -0.025121 -6.89E-05 -0.004189

(0.01056) (0.01083) (0.00420) (0.00267)

[-5.29353] [-2.32063] [-0.01639] [-1.57169]

D2 -0.016458 0.007339 0.007399 -0.001087

(0.00943) (0.00966) (0.00375) (0.00238)

[-1.74594] [ 0.75969] [ 1.97302] [-0.45700]

D3 -0.039480 -0.011369 0.004827 -0.002730

(0.00896) (0.00918) (0.00357) (0.00226)

[-4.40568] [-1.23798] [ 1.35389] [-1.20760]

R-squared 0.984182 0.927153 0.940068 0.886239

Adj. R-squared 0.979939 0.907609 0.923989 0.855717

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 23

An empirical example: A model for the Danish Economy

Table 2.4

LRM LRY IBO IDE

LRM 1.000000 0.529152 -0.444662 -0.307517

LRY 0.529152 1.000000 -0.082996 -0.237938

IBO -0.444662 -0.082996 1.000000 0.250331

IDE -0.307517 -0.237938 0.250331 1.000000

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 24

An empirical example: A model for the Danish Economy

Table 2.5

RES1 RES2 RES3 RES4

Mean 4.47E-15 -3.94E-17 -3.23E-16 6.27E-17

Median -0.005498 -0.001000 -3.03E-05 -1.53E-05

Maximum 0.051973 0.056657 0.017637 0.014900

Minimum -0.039482 -0.034479 -0.023272 -0.009125

Std. Dev. 0.019222 0.019699 0.007648 0.004850

Skewness 0.551539 0.523993 -0.296653 0.414925

Kurtosis 2.925349 2.912625 3.576072 3.561914

Jarque-Bera 2.699361 2.442215 1.510217 2.218044

Probability 0.259323 0.294903 0.469960 0.329881

Sum 2.37E-13 -2.07E-15 -1.71E-14 3.32E-15

Sum Sq. Dev. 0.019213 0.020178 0.003041 0.001223

Observations 53 53 53 53

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 25

An empirical example: A model for the Danish Economy

Table 2.6

Roots of Characteristic Polynomial

Endogenous variables: LRM LRY IBO IDE

Exogenous variables: C D1 D2 D3

Lag specification: 1 2

Date: 04/22/03 Time: 00:40

Root Modulus

0.972454 0.972454

0.755160 - 0.157068i 0.771322

0.755160 + 0.157068i 0.771322

0.595482 - 0.314348i 0.673360

0.595482 + 0.314348i 0.673360

0.605141 0.605141

-0.142538 - 0.231233i 0.271635

-0.142538 + 0.231233i 0.271635

No root lies outside the unit circle.

VAR satisfies the stability condition.

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 26

An empirical example: A model for the Danish Economy

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

-1.5 -1.0 -0.5 0.0 0.5 1.0 1.5

Inverse Roots of AR Characteristic Polynomial

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 27

An empirical example: A model for the Danish Economy

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(LRM,LRM(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(LRM,LRY(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(LRM,IBO(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(LRM,IDE(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(LRY,LRM(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(LRY,LRY(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(LRY,IBO(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(LRY,IDE(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(IBO,LRM(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(IBO,LRY(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(IBO,IBO(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(IBO,IDE(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(IDE,LRM(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(IDE,LRY(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(IDE,IBO(-i))

-.4

-.2

.0

.2

.4

2 4 6 8 10 12 14

Cor(IDE,IDE(-i))

Autocorrelations with 2 Std.Err. Bounds

Advanced Time Series Econometrics

Dean Fantazzini 10 − 15 July 2006 28