Embed Size (px)

Citation preview

IRAQ PRIVATE SECTOR GROWTH AND EMPLOYMENT GENERATION

August 28, 2006

Vegetable Oils in Iraq

This publication was produced for review by the United States Agency for International Development. It was prepared by the joint venture partnership of The Louis Berger Group / The Services Group under Contract # 267-C-00-04-00435-00

Vegetable Oils in Iraq

August 28, 2006

DISCLAIMER The author’s views expressed in this publication do not necessarily reflect the views of the United States Agency for International Development or the United States Government. The IRAQ IZDIHAR project is funded by the United States Agency for International Development (USAID) and implemented by the joint venture partnership of:

International Economic Consulting

THE Louis Berger Group, INC.Engineers Planners Scientists Economists

THE SERVICES GROUP

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

TABLE OF CONTENTS

EXECUTIVE SUMMARY CHAPTER 1: VEGETABLE OILS AND MEAL IN IRAQ

1.1 Vegetable Oil 1.2 Meal 1.3 Soy Oil 1.4 Palm Oil 1.5 Canola Oil 1.6 Sunflower Oil

1 2 2 3 4 5

CHAPTER 2: OILSEED IN IRAQ

6

2.1 Rapeseed - Canola 7 2.2 Sunflower 2.3 Safflower

8 8

CHAPTER 3: CRUSHING OPERATION

9

CHAPTER 4: PURIFICATION PROCESS - REFINING

11

4.1 Fractionation and Hydrogenation 12 CHAPTER 5: DOMESTIC DEMAND FOR VEGETABLE OILS AND FATS CHAPTER 6: COMPETITION

13 15

CHAPTER 7: IMPORT DUTIES CHAPTER 8: CONCLUSIONS

17 18

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

Executive Summary

i

EXECUTIVE SUMMARY Current Status Vegetable oils and fats represent an important food market in Iraq, with a total turnover of and $380 million and 400,000 tons, almost entirely imported from the GCC countries, Turkey, Malaysia, and Indonesia. Seed oil cultivation, crushing facilities, and refining facilities are practically nonexistent in today’s Iraq. Per capita consumption of cooking oil is in keeping with regional values at around 15 kg/year. Vegetable ghee – derived from palm oil – accounts for almost 50% of the market by volume while liquid oil – almost equally split among sunflower oil, palm oil, and soy oil – makes up the other 50%. The state – through the PDS scheme – controls 60% of the total market, creating a major distortion in the mechanism of pricing and distorting supply and demand in the market. The Vegetable Oil Industry in Perspective: Risks and Opportunities

1) Even with the implementation of a more aggressive oilseed plantation program aimed at increasing oilseed production, Iraq will probably remain largely dependent on imports in the medium to long term. Rapeseed (Canola hybrid) looks like the most promising oilseed crop for Iraq, based on data collected by ICARDA in the region. Rapeseed could provide additional income to farmers as a double crop with wheat or as an alternative winter crop.

2) A large scale crushing operation is not currently viable for lack of a strong poultry

industry that could create a high demand for meal. Small mechanical crushing operations seem more appropriate for Iraq, taking into account its limited oilseed production and the current small size of the poultry and aquaculture industries.

3) The current demand for vegetable oil and ghee (manly derived from palm oil) - both

around 200,000 tons per year - confirms the potential for a refining operation. Nevertheless the financial viability of a refining operation depends on:

• Capacity: The ideal capacity should be around 800 TPD, which implies

controlling a 72% share of the fats and oils market in Iraq. A lower capacity – 300/400 TPD – would probably be scarcely competitive with refineries in the Gulf states (Dubai and Saudi Arabia) and Turkey.

• The elimination of the PDS system, currently controlling more than 50% of the market and distorting the price structure.

• A plant with the technology to refine palm, soy, rapeseed, sunflower crude oils and to produce fractionated palm oil for ghee.

4) In particular, the elimination of the PDS appears to be a condition sine qua non, while

a plant with minimal refining capacity lacking the benefits of economies of scale would probably require tariffs on refined vegetable oil imports of around 20% in order to make

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

Executive Summary

ii

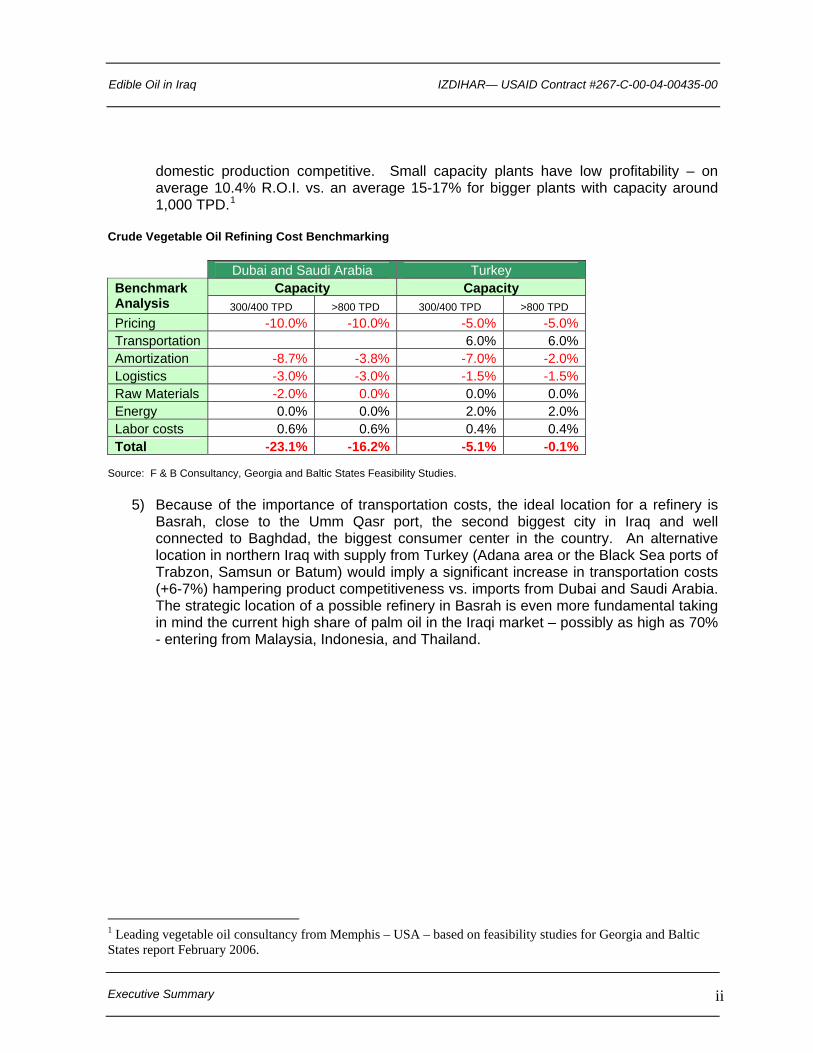

domestic production competitive. Small capacity plants have low profitability – on average 10.4% R.O.I. vs. an average 15-17% for bigger plants with capacity around 1,000 TPD.1

Crude Vegetable Oil Refining Cost Benchmarking

Dubai and Saudi Arabia Turkey Capacity Capacity Benchmark

Analysis 300/400 TPD >800 TPD 300/400 TPD >800 TPD Pricing -10.0% -10.0% -5.0% -5.0% Transportation 6.0% 6.0% Amortization -8.7% -3.8% -7.0% -2.0% Logistics -3.0% -3.0% -1.5% -1.5% Raw Materials -2.0% 0.0% 0.0% 0.0% Energy 0.0% 0.0% 2.0% 2.0% Labor costs 0.6% 0.6% 0.4% 0.4% Total -23.1% -16.2% -5.1% -0.1%

Source: F & B Consultancy, Georgia and Baltic States Feasibility Studies.

5) Because of the importance of transportation costs, the ideal location for a refinery is Basrah, close to the Umm Qasr port, the second biggest city in Iraq and well connected to Baghdad, the biggest consumer center in the country. An alternative location in northern Iraq with supply from Turkey (Adana area or the Black Sea ports of Trabzon, Samsun or Batum) would imply a significant increase in transportation costs (+6-7%) hampering product competitiveness vs. imports from Dubai and Saudi Arabia. The strategic location of a possible refinery in Basrah is even more fundamental taking in mind the current high share of palm oil in the Iraqi market – possibly as high as 70% - entering from Malaysia, Indonesia, and Thailand.

1 Leading vegetable oil consultancy from Memphis – USA – based on feasibility studies for Georgia and Baltic States report February 2006.

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

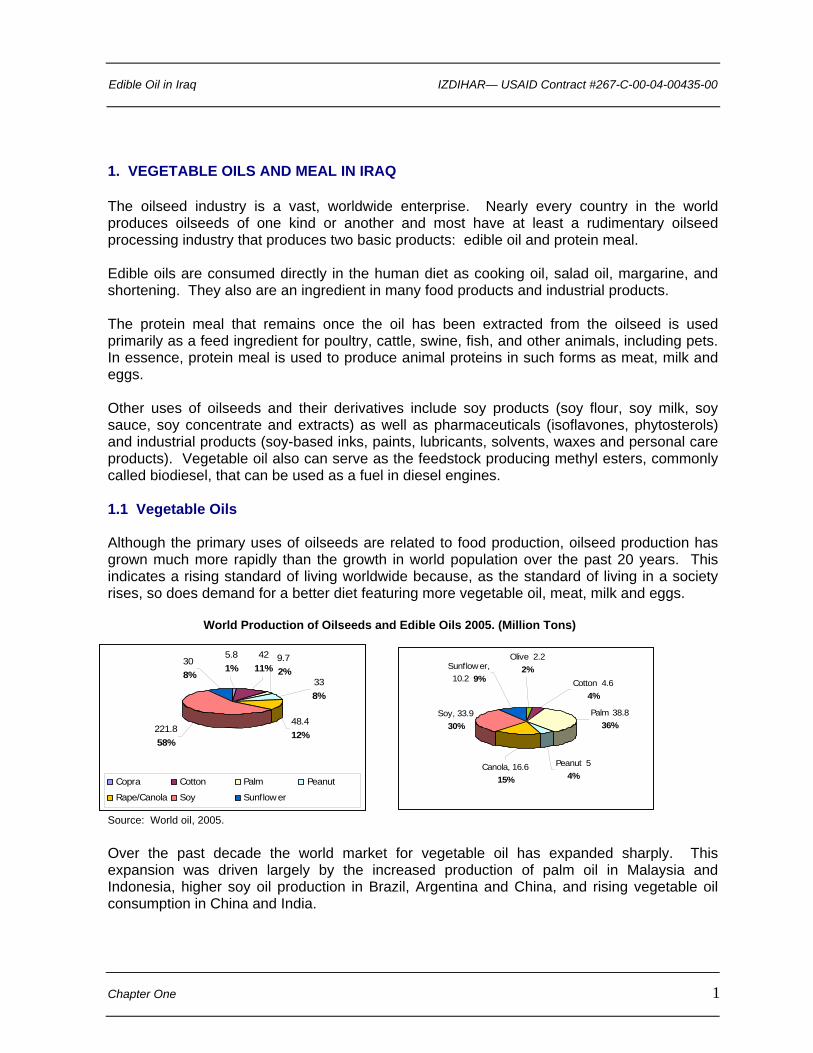

1. VEGETABLE OILS AND MEAL IN IRAQ The oilseed industry is a vast, worldwide enterprise. Nearly every country in the world produces oilseeds of one kind or another and most have at least a rudimentary oilseed processing industry that produces two basic products: edible oil and protein meal. Edible oils are consumed directly in the human diet as cooking oil, salad oil, margarine, and shortening. They also are an ingredient in many food products and industrial products. The protein meal that remains once the oil has been extracted from the oilseed is used primarily as a feed ingredient for poultry, cattle, swine, fish, and other animals, including pets. In essence, protein meal is used to produce animal proteins in such forms as meat, milk and eggs. Other uses of oilseeds and their derivatives include soy products (soy flour, soy milk, soy sauce, soy concentrate and extracts) as well as pharmaceuticals (isoflavones, phytosterols) and industrial products (soy-based inks, paints, lubricants, solvents, waxes and personal care products). Vegetable oil also can serve as the feedstock producing methyl esters, commonly called biodiesel, that can be used as a fuel in diesel engines. 1.1 Vegetable Oils Although the primary uses of oilseeds are related to food production, oilseed production has grown much more rapidly than the growth in world population over the past 20 years. This indicates a rising standard of living worldwide because, as the standard of living in a society rises, so does demand for a better diet featuring more vegetable oil, meat, milk and eggs.

World Production of Oilseeds and Edible Oils 2005. (Million Tons)

Chapter One

1

9.7 2%

33

Source: World oil, 2005. Over the past decade the world market for vegetable oil has expanded sharply. This expansion was driven largely by the increased production of palm oil in Malaysia and Indonesia, higher soy oil production in Brazil, Argentina and China, and rising vegetable oil consumption in China and India.

8%

48.4 12%

5.8 1%

30 8%

42 11%

221.8 58%

Copra Cotton Palm Peanut

Rape/Canola Soy S runflowe

Soy, 33.9 30%

Canola, 16.6 15%

Peanut 5 4%

Palm 38.8 36%

Cotton 4.6 4%

Olive 2.2 2%Sunflow er,

10.2 9%

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

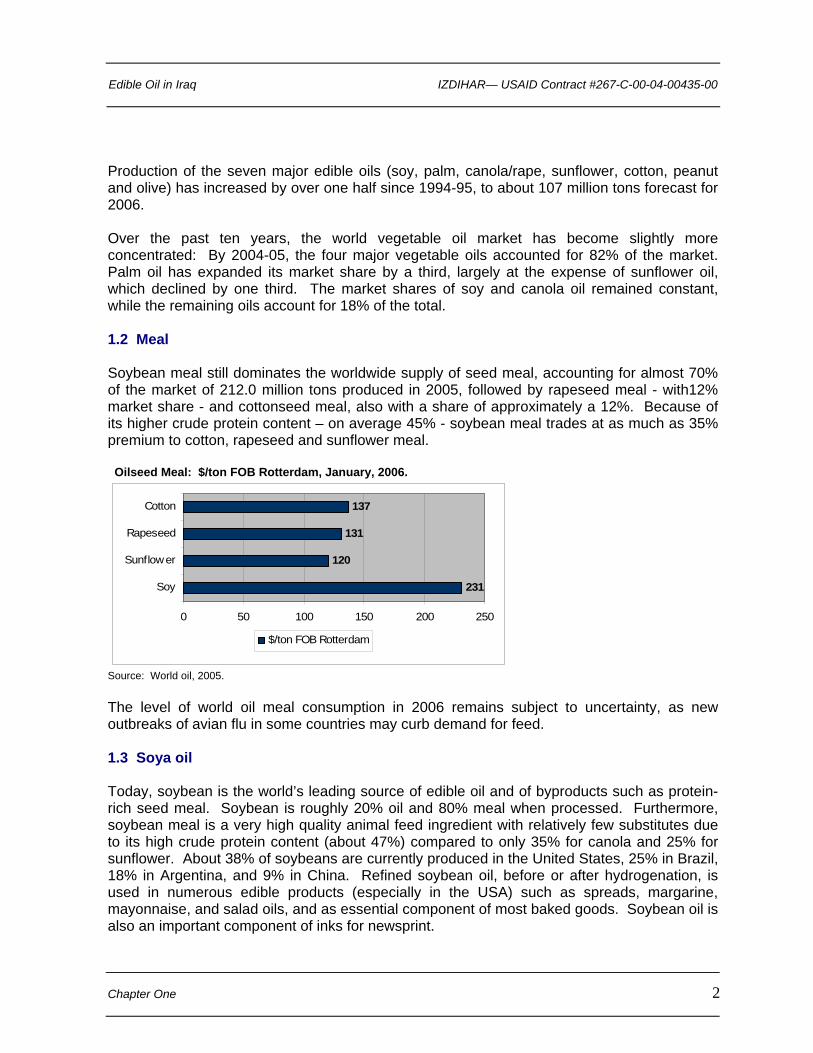

Production of the seven major edible oils (soy, palm, canola/rape, sunflower, cotton, peanut and olive) has increased by over one half since 1994-95, to about 107 million tons forecast for 2006. Over the past ten years, the world vegetable oil market has become slightly more concentrated: By 2004-05, the four major vegetable oils accounted for 82% of the market. Palm oil has expanded its market share by a third, largely at the expense of sunflower oil, which declined by one third. The market shares of soy and canola oil remained constant, while the remaining oils account for 18% of the total. 1.2 Meal Soybean meal still dominates the worldwide supply of seed meal, accounting for almost 70% of the market of 212.0 million tons produced in 2005, followed by rapeseed meal - with12% market share - and cottonseed meal, also with a share of approximately a 12%. Because of its higher crude protein content – on average 45% - soybean meal trades at as much as 35% premium to cotton, rapeseed and sunflower meal. Oilseed Meal: $/ton FOB Rotterdam, January, 2006.

231

120

131

137

0 50 100 150 200 250

Soy

Sunflower

Rapeseed

Cotton

$/ton FOB Rotterdam

Source: World oil, 2005. The level of world oil meal consumption in 2006 remains subject to uncertainty, as new outbreaks of avian flu in some countries may curb demand for feed. 1.3 Soya oil Today, soybean is the world’s leading source of edible oil and of byproducts such as protein-rich seed meal. Soybean is roughly 20% oil and 80% meal when processed. Furthermore, soybean meal is a very high quality animal feed ingredient with relatively few substitutes due to its high crude protein content (about 47%) compared to only 35% for canola and 25% for sunflower. About 38% of soybeans are currently produced in the United States, 25% in Brazil, 18% in Argentina, and 9% in China. Refined soybean oil, before or after hydrogenation, is used in numerous edible products (especially in the USA) such as spreads, margarine, mayonnaise, and salad oils, and as essential component of most baked goods. Soybean oil is also an important component of inks for newsprint.

Chapter One

2

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

Chapter One

3

Soybean meal is the most common protein supplement in the poultry and aquaculture sectors and is widely used in beef rations because of its highly palatable content and moderate level of difficult to digest proteins. On the other hand, it is not highly recommended in high proportions for dairy cows because of the presence of methionine – an amino acid that reduces the rate of lactation. 1.4 Palm oil Since 1994-95, world production of palm oil has expanded rapidly, and surpassed soy oil production in early 2001. Palm oil production is highly concentrated in Malaysia and Indonesia. In Malaysia, production has nearly doubled over the past ten years due to an increase in harvested area. With suitable land for further increases becoming scarce in Malaysia, the expansion has shifted to Indonesia, which has almost tripled its output over the past ten years. The growth in palm groves has been driven by low operating costs compared to competing vegetable oil. Investing in palm trees is capital intensive with a five year lag before production begins, but subsequent costs largely involve the cost of harvesting and on-going fertility. Palm is by far the most productive oil seed in the world: A single hectare may yield 6,000 liters of crude oil. By comparison, soybean generates only 500 and canola approximately 1200 liters/hectare. Palm oil is derived from the fruit, which grows in clusters that may weigh 40 – 50 kilograms. A hundred kilograms of oil seeds typically produce 20 kg of oil. While palms can live 150 years, cultivated palms are generally clear cut or poisoned and replaced at about 25 years old. As soybean oil prices – the benchmark for the vegetable oil commodity market – began to rise in 2001, the spread between palm oil and soybean oil began to widen, increasing the competitiveness of palm oil in world markets. Lower prices have given palm oil a competitive advantage in large oil consuming countries like India and China. Under normal circumstances, palm oil trades at up to $120/ton – approximately 30% below soy oil. Consumer acceptance of palm oil is nevertheless uneven around the world and is mainly used as a food ingredient or for frying and less as a dressing oil. Acceptance of palm oil as cooking and salad oil remains low among consumers except in China, and its consumption usually decreases with increasing purchasing power. In India its share on the total edible oil market has dropped from 31.4% in to only 23.5% in 2005.

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

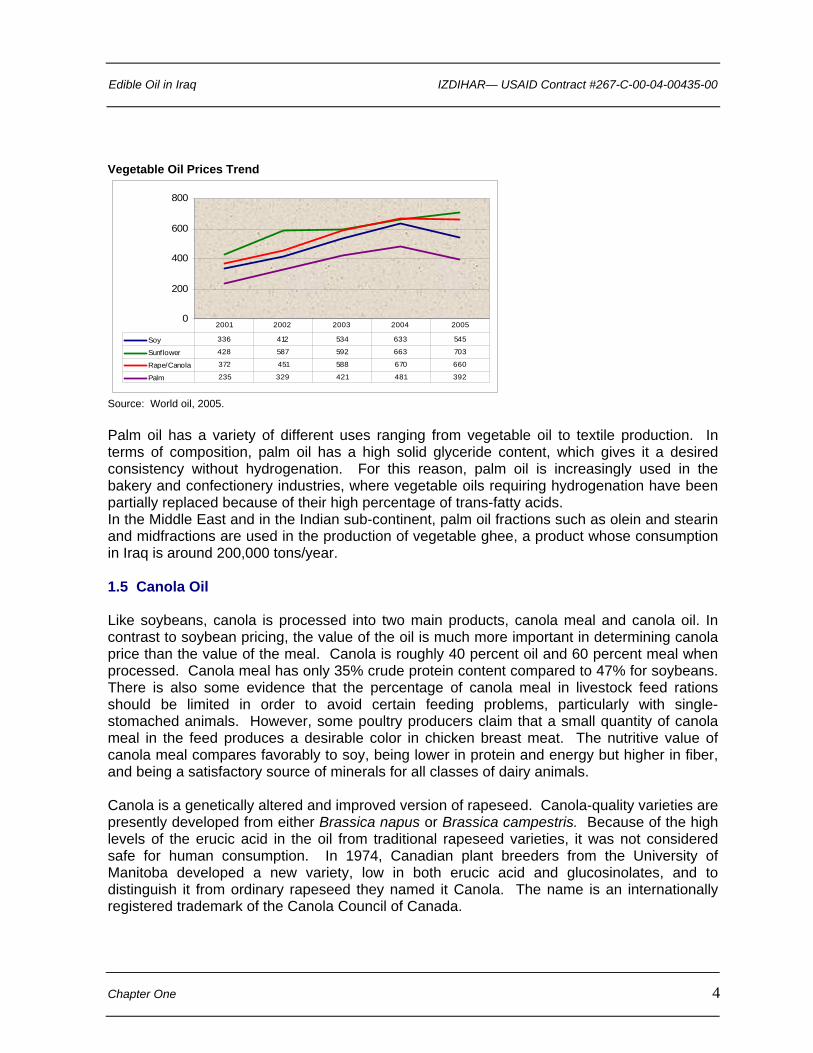

Vegetable Oil Prices Trend

0

200

400

600

800

Soy 336 412 534 633 545

Sunflower 428 587 592 663 703

Rape/Canola 372 451 588 670 660

Palm 235 329 421 481 392

2001 2002 2003 2004 2005

Source: World oil, 2005. Palm oil has a variety of different uses ranging from vegetable oil to textile production. In terms of composition, palm oil has a high solid glyceride content, which gives it a desired consistency without hydrogenation. For this reason, palm oil is increasingly used in the bakery and confectionery industries, where vegetable oils requiring hydrogenation have been partially replaced because of their high percentage of trans-fatty acids. In the Middle East and in the Indian sub-continent, palm oil fractions such as olein and stearin and midfractions are used in the production of vegetable ghee, a product whose consumption in Iraq is around 200,000 tons/year. 1.5 Canola Oil Like soybeans, canola is processed into two main products, canola meal and canola oil. In contrast to soybean pricing, the value of the oil is much more important in determining canola price than the value of the meal. Canola is roughly 40 percent oil and 60 percent meal when processed. Canola meal has only 35% crude protein content compared to 47% for soybeans. There is also some evidence that the percentage of canola meal in livestock feed rations should be limited in order to avoid certain feeding problems, particularly with single-stomached animals. However, some poultry producers claim that a small quantity of canola meal in the feed produces a desirable color in chicken breast meat. The nutritive value of canola meal compares favorably to soy, being lower in protein and energy but higher in fiber, and being a satisfactory source of minerals for all classes of dairy animals. Canola is a genetically altered and improved version of rapeseed. Canola-quality varieties are presently developed from either Brassica napus or Brassica campestris. Because of the high levels of the erucic acid in the oil from traditional rapeseed varieties, it was not considered safe for human consumption. In 1974, Canadian plant breeders from the University of Manitoba developed a new variety, low in both erucic acid and glucosinolates, and to distinguish it from ordinary rapeseed they named it Canola. The name is an internationally registered trademark of the Canola Council of Canada.

Chapter One

4

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

Chapter One

5

The current worldwide production of canola seeds is around 48 million tons; the EU25 are the biggest producer with 15 million tons – a 32% share - followed by China at 13 million tons, and Canada and India with approximately 7 million tons each. Over the past decade, canola oil has positioned itself as a healthy vegetable oil, low in saturated fats, and good for human health. Since 2000 the demand of canola oil increased significantly in EU25 as the European Union sought to reduce its dependency on fossil fuels and quadrupled the production of biodiesel, which now accounts now for some 35% of total canola oil utilization. 1.6 Sunflower Oil Sunflower seeds are approximately 35% oil and 35% meal after the hulling process, which is necessary to reduce the fibrous content of the meal and increase its marketability as stock feed. The crude protein content of sunflower seed meal is lower than soybeans varying between 25% and 32%. The fiber in sunflower meal is hard to digest, and may be a disadvantage when balancing rations for high milk production in calves. Sunflower meal is ALSO less palatable than soybean. Additionally, sunflower meal has a less desirable amino acid profile. Currently the Russian Federation, Ukraine, EU25 and Argentina are the main producers of sunflower seeds: Sunflower seeds production (million tons), 2005

Russia Ukraine EU25 Argentina Total 6 4.4 4.1 4 28.7

Source: USDA Oilseeds: A Summary of Meal and Crude Protein content of Edible Oil Mode value in the world, 2005.

Seeds % oil % cake

CP -crude protein

Average yield oil/ha

Cotton 20% 80% 38% 325Soy 20% 80% 47% 446Canola 40% 60% 35% 1190Palm 20% 5950Sunflower 35% 35% 25% 952

Source: World oil, 2005.

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

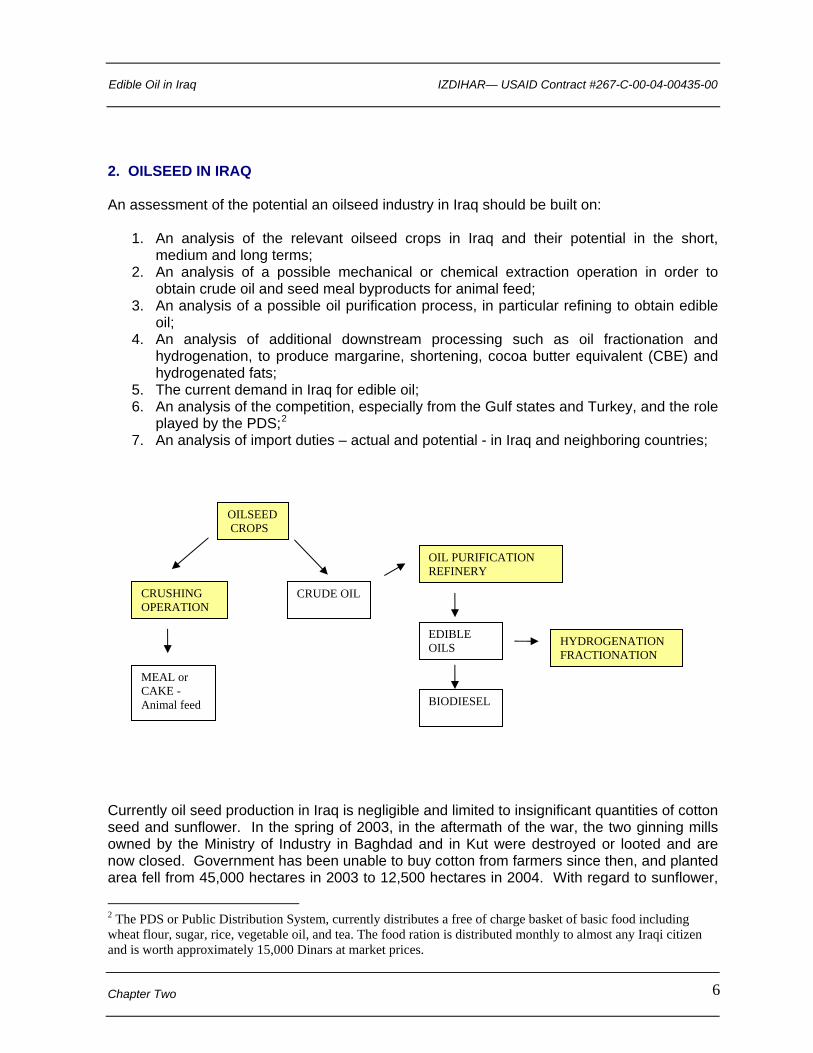

2. OILSEED IN IRAQ An assessment of the potential an oilseed industry in Iraq should be built on:

1. An analysis of the relevant oilseed crops in Iraq and their potential in the short, medium and long terms;

2. An analysis of a possible mechanical or chemical extraction operation in order to obtain crude oil and seed meal byproducts for animal feed;

3. An analysis of a possible oil purification process, in particular refining to obtain edible oil;

4. An analysis of additional downstream processing such as oil fractionation and hydrogenation, to produce margarine, shortening, cocoa butter equivalent (CBE) and hydrogenated fats;

5. The current demand in Iraq for edible oil; 6. An analysis of the competition, especially from the Gulf states and Turkey, and the role

played by the PDS;2 7. An analysis of import duties – actual and potential - in Iraq and neighboring countries;

CRUSHING OPERATION

OILSEED CROPS

OIL PURIFICATION REFINERY

MEAL or CAKE - Animal feed

CRUDE OIL

EDIBLE OILS HYDROGENATION

FRACTIONATION

BIODIESEL

Currently oil seed production in Iraq is negligible and limited to insignificant quantities of cotton seed and sunflower. In the spring of 2003, in the aftermath of the war, the two ginning mills owned by the Ministry of Industry in Baghdad and in Kut were destroyed or looted and are now closed. Government has been unable to buy cotton from farmers since then, and planted area fell from 45,000 hectares in 2003 to 12,500 hectares in 2004. With regard to sunflower,

Chapter Two

6

2 The PDS or Public Distribution System, currently distributes a free of charge basket of basic food including wheat flour, sugar, rice, vegetable oil, and tea. The food ration is distributed monthly to almost any Iraqi citizen and is worth approximately 15,000 Dinars at market prices.

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

Chapter Two

7

the largest production was in 1995 - 42,000 tons - but has since declined to 17,000 tons in 2002 and only 1,000 in 2003. In the year 2005, a total of 17,000 tons were reportedly produced from a cultivated area of 22,000 hectares. No purchase price to farmers was announced by the government through the Vegetable Oil Company. Unlike cereals – especially barley and wheat – which have been the focus of recent comprehensive agricultural studies funded by international donors, oilseed crops have never been studied in Iraq. The only material available stems from ICARDA Oilseed Crops for the Highlands of CWANA (Central and West Asia and North Africa). According to ICARDA researchers the results – in particular those for Iran - seem to be relevant for northern Iraq in the areas with 300 – 500 milliliters of rainfall/year. The ICARDA study offers useful data and recommendations for the possible development of oilseed crops in Iraq, summarized below:

1. Soybeans seem inappropriate for the Iraqi soil and climate;

2. Iraq should analyze primarily the potential of rapeseed – canola – followed by safflower and sunflower. Based on a “similarity analysis” with Iran, rapeseed seems the oilseed crop with the highest potential.

3. Sunflower, although viable in principle, is likely to show low yields and to provide a

meal byproduct too fibrous for the poultry industry which, in theory, should lead the demand for oilseed meal in Iraq.

2.1 Rapeseed - Canola Canola is a cool season crop that requires only moderate moisture – especially at the germinating stage. Canola can be planted either in winter or spring, but winter planting showed much higher yields (2.5 – 3.5 tons/ha vs. only 1.0 tons for spring planting). Canola requires a moderate quantity of water, comparable to wheat, and does well in areas with a seasonal rainfall of 350 – 450 mm. High yield open pollinated canola hybrids such as Hayola 401, Okapi, Orient, SLM-046 have proved successful in dry land conditions and are easily available in the market. Canola is highly resistant to disease and could be cultivated as a double crop with wheat. With regard to meal byproduct, canola compares favorably to soybean meal because of its balanced protein, energy and fiber content. It is strongly indicated for the poultry industry. According to ICARDA’s agronomists, northern Iraq has the potential for planting an estimated 100,000 hectares of canola with minimum yields of 2 tons/ha. Canola profitability at 60% meal and 40% oil would significantly surpass wheat, based on current market prices and taking into account that the two crops have a similar input costs in terms of seed, herbicide, fertilizers, fungicides and insecticides. 3

Wheat and Canola Profitability Simulation

3 Based on commodity quotations of $131/ton for canola meal, $262/ton for canola beans and $180/ton for 1st and 2nd grade flour wheat.

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

Chapter Two

8

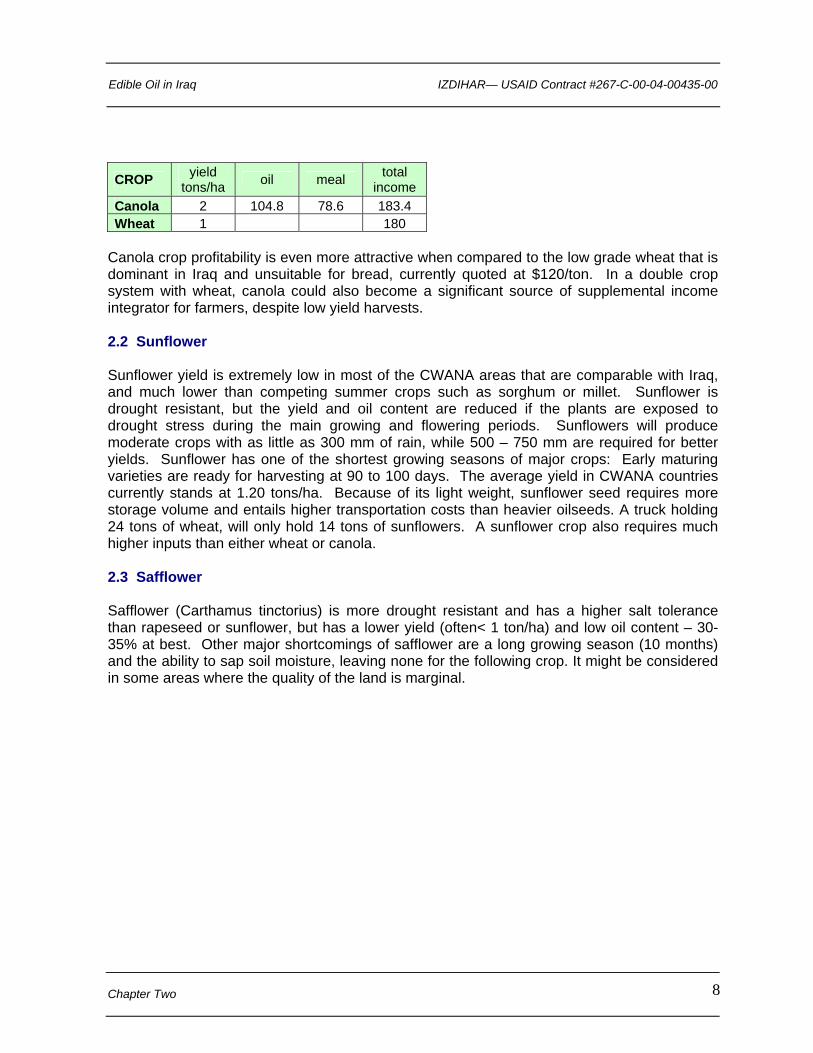

CROP yield tons/ha oil meal total

income Canola 2 104.8 78.6 183.4 Wheat 1 180

Canola crop profitability is even more attractive when compared to the low grade wheat that is dominant in Iraq and unsuitable for bread, currently quoted at $120/ton. In a double crop system with wheat, canola could also become a significant source of supplemental income integrator for farmers, despite low yield harvests. 2.2 Sunflower Sunflower yield is extremely low in most of the CWANA areas that are comparable with Iraq, and much lower than competing summer crops such as sorghum or millet. Sunflower is drought resistant, but the yield and oil content are reduced if the plants are exposed to drought stress during the main growing and flowering periods. Sunflowers will produce moderate crops with as little as 300 mm of rain, while 500 – 750 mm are required for better yields. Sunflower has one of the shortest growing seasons of major crops: Early maturing varieties are ready for harvesting at 90 to 100 days. The average yield in CWANA countries currently stands at 1.20 tons/ha. Because of its light weight, sunflower seed requires more storage volume and entails higher transportation costs than heavier oilseeds. A truck holding 24 tons of wheat, will only hold 14 tons of sunflowers. A sunflower crop also requires much higher inputs than either wheat or canola. 2.3 Safflower Safflower (Carthamus tinctorius) is more drought resistant and has a higher salt tolerance than rapeseed or sunflower, but has a lower yield (often< 1 ton/ha) and low oil content – 30-35% at best. Other major shortcomings of safflower are a long growing season (10 months) and the ability to sap soil moisture, leaving none for the following crop. It might be considered in some areas where the quality of the land is marginal.

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

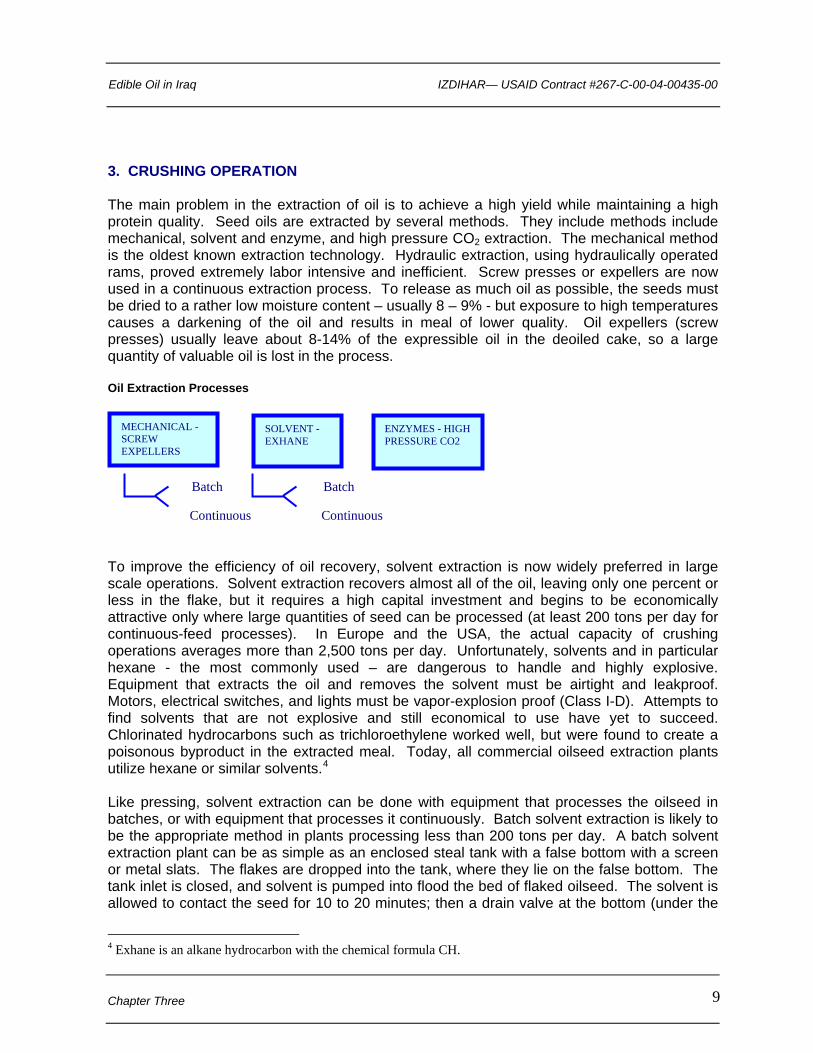

3. CRUSHING OPERATION The main problem in the extraction of oil is to achieve a high yield while maintaining a high protein quality. Seed oils are extracted by several methods. They include methods include mechanical, solvent and enzyme, and high pressure CO2 extraction. The mechanical method is the oldest known extraction technology. Hydraulic extraction, using hydraulically operated rams, proved extremely labor intensive and inefficient. Screw presses or expellers are now used in a continuous extraction process. To release as much oil as possible, the seeds must be dried to a rather low moisture content – usually 8 – 9% - but exposure to high temperatures causes a darkening of the oil and results in meal of lower quality. Oil expellers (screw presses) usually leave about 8-14% of the expressible oil in the deoiled cake, so a large quantity of valuable oil is lost in the process. Oil Extraction Processes

Chapter Three

9

To improve the efficiency of oil recovery, solvent extraction is now widely preferred in large scale operations. Solvent extraction recovers almost all of the oil, leaving only one percent or less in the flake, but it requires a high capital investment and begins to be economically attractive only where large quantities of seed can be processed (at least 200 tons per day for continuous-feed processes). In Europe and the USA, the actual capacity of crushing operations averages more than 2,500 tons per day. Unfortunately, solvents and in particular hexane - the most commonly used – are dangerous to handle and highly explosive. Equipment that extracts the oil and removes the solvent must be airtight and leakproof. Motors, electrical switches, and lights must be vapor-explosion proof (Class I-D). Attempts to find solvents that are not explosive and still economical to use have yet to succeed. Chlorinated hydrocarbons such as trichloroethylene worked well, but were found to create a poisonous byproduct in the extracted meal. Today, all commercial oilseed extraction plants utilize hexane or similar solvents.4

Like pressing, solvent extraction can be done with equipment that processes the oilseed in batches, or with equipment that processes it continuously. Batch solvent extraction is likely to be the appropriate method in plants processing less than 200 tons per day. A batch solvent extraction plant can be as simple as an enclosed steal tank with a false bottom with a screen or metal slats. The flakes are dropped into the tank, where they lie on the false bottom. The tank inlet is closed, and solvent is pumped into flood the bed of flaked oilseed. The solvent is allowed to contact the seed for 10 to 20 minutes; then a drain valve at the bottom (under the

4 Exhane is an alkane hydrocarbon with the chemical formula CH.

Batch

MECHANICAL - SCREW EXPELLERS

SOLVENT - EXHANE

ENZYMES - HIGH PRESSURE CO2

Batch

Continuous

Batch

Continuous

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

Chapter Three

10

false bottom) is opened to complete to extraction. After the final extract has been fully drained, steam is introduced into the bottom to evaporate the solvent out of the flakes. This combination of steam and solvent is subsequently piped out as vapor and condensed, leaving the flakes solvent free. In reality, mechanical and solvent extraction coexist in most crushing factories, since pre-press solvent extraction is widely used for seeds with higher oil content such as canola and sunflower. In pre-press extraction, the seeds are first passed through screw presses which extract most of the oil, and the remaining oil cake is sent to the solvent extractor, where the solvent dissolves the remaining oil (usually 8-9%). For intermediate-scale operations - less than 200 tons per day - the choice is between batch solvent extraction and expeller systems. Batch solvent extraction systems operate more slowly and less efficiently, are more labor intensive, and are dangerous. They use greater quantities of solvent than properly designed continuous systems. Because of these drawbacks, expellers are usually preferred for installations too small for continuous solvent system. The use of high pressure CO2 and enzyme extraction is currently coming into the market, but still used primarily in markets where sophisticated byproducts have a sizeable demand, as in Europe and the USA. In today’s Iraq, the main constraint for an oilseed crushing operation is the limited demand for meal due to the crisis in the poultry industry – a primary target - combined with little demand for protein feed for the aquaculture sector. In the absence of strong meal demand for poultry and aquaculture, no crushing operation would be viable in Iraq. Oilseed meals are in fact important byproducts in crushing operations, accounting for a minimum of 20-25% of the income for sunflower and canola and up to 50-55% for soy seeds. A crushing operation should be put in place only after the refining capacity has been built and demand for the meal exists. In order to establish a solvent extraction crushing operation of 300 tons per day – considered by experts in the sector the minimum economically viable capacity in the Middle East – the domestic poultry industry should grow to at least 80,000 – 100,000 tons per year to create the vital demand. In the meanwhile, the only solution would be to establish small mechanical crushing plant processing 20-25 tons per day, with an investment between $300,000 and $500,000. Such an operation could be designed to process domestically produced seed oils – canola and sunflower.

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

4. PURIFICATION PROCESS – REFINING Oils contain free fatty acids, gummy matter, color pigments, and smelly residue. In some developing countries, poor people may use unrefined raw oil for cooking, but a majority prefers colorless oils with little taste or smell. Therefore, the naturally occurring, undesirable impurities must be removed from the oil during the refining process. Purification is also a necessary step in order to obtain downstream products such as margarine and shortening.5

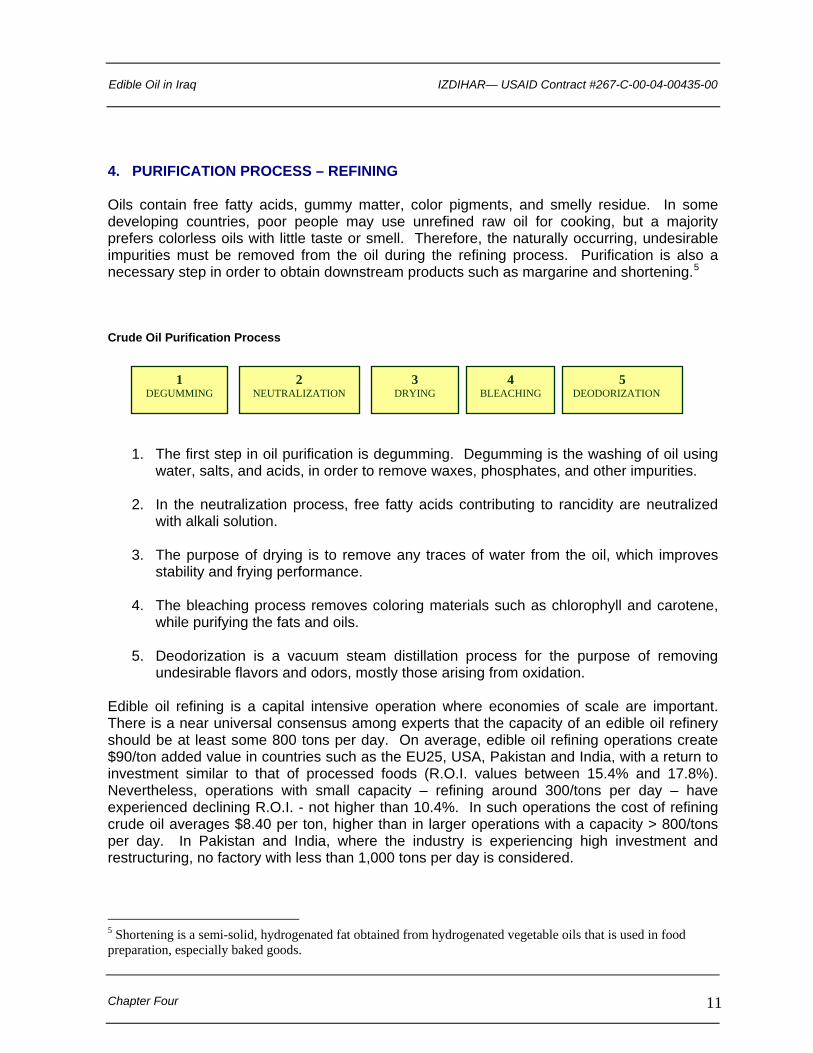

Crude Oil Purification Process

1 DEGUMMING

2 NEUTRALIZATION

3 DRYING

4 BLEACHING

5 DEODORIZATION

1. The first step in oil purification is degumming. Degumming is the washing of oil using water, salts, and acids, in order to remove waxes, phosphates, and other impurities.

2. In the neutralization process, free fatty acids contributing to rancidity are neutralized

with alkali solution.

3. The purpose of drying is to remove any traces of water from the oil, which improves stability and frying performance.

4. The bleaching process removes coloring materials such as chlorophyll and carotene,

while purifying the fats and oils.

5. Deodorization is a vacuum steam distillation process for the purpose of removing undesirable flavors and odors, mostly those arising from oxidation.

Edible oil refining is a capital intensive operation where economies of scale are important. There is a near universal consensus among experts that the capacity of an edible oil refinery should be at least some 800 tons per day. On average, edible oil refining operations create $90/ton added value in countries such as the EU25, USA, Pakistan and India, with a return to investment similar to that of processed foods (R.O.I. values between 15.4% and 17.8%). Nevertheless, operations with small capacity – refining around 300/tons per day – have experienced declining R.O.I. - not higher than 10.4%. In such operations the cost of refining crude oil averages $8.40 per ton, higher than in larger operations with a capacity > 800/tons per day. In Pakistan and India, where the industry is experiencing high investment and restructuring, no factory with less than 1,000 tons per day is considered.

Chapter Four

11

5 Shortening is a semi-solid, hydrogenated fat obtained from hydrogenated vegetable oils that is used in food preparation, especially baked goods.

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

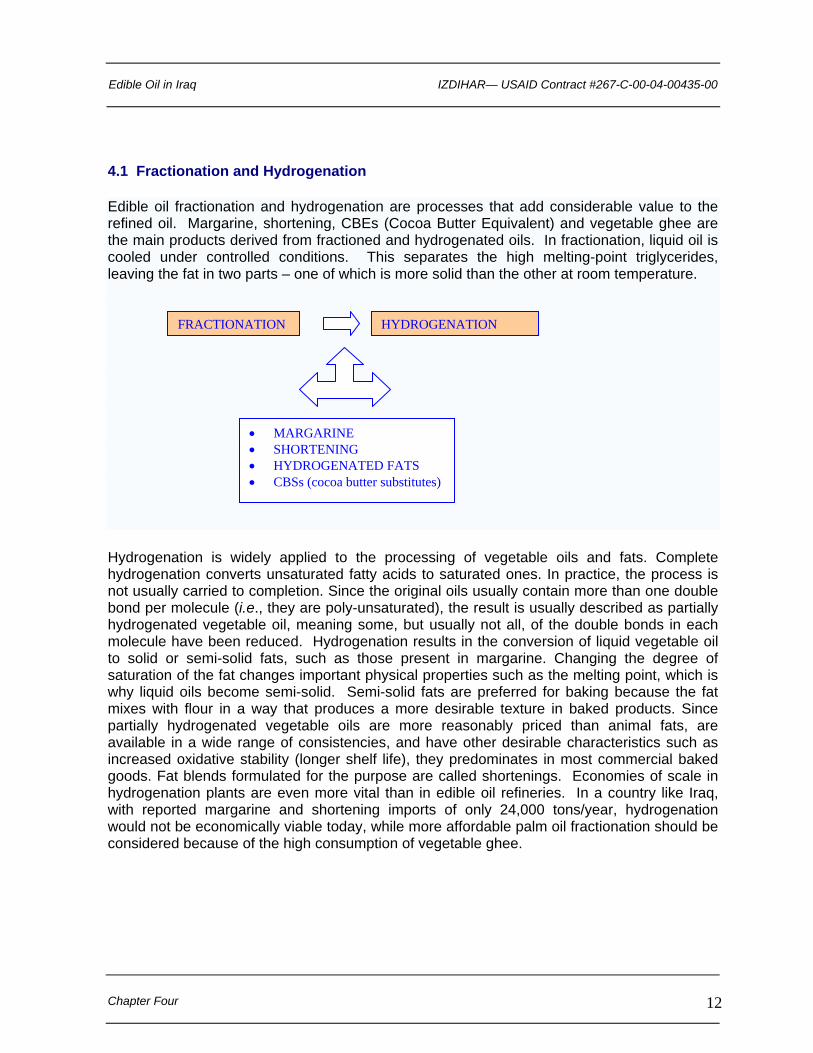

4.1 Fractionation and Hydrogenation

Edible oil fractionation and hydrogenation are processes that add considerable value to the refined oil. Margarine, shortening, CBEs (Cocoa Butter Equivalent) and vegetable ghee are the main products derived from fractioned and hydrogenated oils. In fractionation, liquid oil is cooled under controlled conditions. This separates the high melting-point triglycerides, leaving the fat in two parts – one of which is more solid than the other at room temperature.

Chapter Four

12

FRACTIONATION HYDROGENATION

• MARGARINE • SHORTENING • HYDROGENATED FATS • CBSs (cocoa butter substitutes)

Hydrogenation is widely applied to the processing of vegetable oils and fats. Complete hydrogenation converts unsaturated fatty acids to saturated ones. In practice, the process is not usually carried to completion. Since the original oils usually contain more than one double bond per molecule (i.e., they are poly-unsaturated), the result is usually described as partially hydrogenated vegetable oil, meaning some, but usually not all, of the double bonds in each molecule have been reduced. Hydrogenation results in the conversion of liquid vegetable oil to solid or semi-solid fats, such as those present in margarine. Changing the degree of saturation of the fat changes important physical properties such as the melting point, which is why liquid oils become semi-solid. Semi-solid fats are preferred for baking because the fat mixes with flour in a way that produces a more desirable texture in baked products. Since partially hydrogenated vegetable oils are more reasonably priced than animal fats, are available in a wide range of consistencies, and have other desirable characteristics such as increased oxidative stability (longer shelf life), they predominates in most commercial baked goods. Fat blends formulated for the purpose are called shortenings. Economies of scale in hydrogenation plants are even more vital than in edible oil refineries. In a country like Iraq, with reported margarine and shortening imports of only 24,000 tons/year, hydrogenation would not be economically viable today, while more affordable palm oil fractionation should be considered because of the high consumption of vegetable ghee.

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

Chapter Five

13

5. DOMESTIC DEMAND FOR VEGETABLE OILS AND FATS The consumption of edible oils and fats in Iraq – 15 kg/year per capita – is in line with regional values but different in terms of segmentation: Ghee consumption is still high in Iraq and well established, especially in rural areas. In most of the Gulf countries –exposed to sophisticated packaged goods and marketing – ghee consumption has been partially replaced by butter and margarine. Ghee and vegetable oil consumption is also strongly influenced by the PDS scheme, since the two products are interchangeable in the PDS which guarantees 0.75 liter per capita of one or the other per month. The actual market size of fats and vegetable oils in Iraq is estimated at 405,000 tons, almost entirely imported from Turkey, India, Pakistan, the GCC countries, Europe, Malaysia and Indonesia. Products marketed as vegetable oil account for almost 50% of the market – some 200,000 tons, while the other 50% of the market is made up of products marketed as ghee, but actually they are mostly fractionated palm oils. Ghee is clarified butter or pure butter fat. Its main advantage is that it can be heated to a high temperature without burning. Clarifying involves melting the butter to let all the moisture evaporate. Ghee is widely used in India and the MENA area, since it is more convenient than butter, having a long shelf life even without refrigeration. Ghee made from butter has a sweet, nutty taste – in India is called usli ghee, meaning genuine ghee. More common in Iraq - and less expensive – is vegetable ghee made from saturated vegetables oils which are fractionated or hydrogenated in order to give them a solid consistency. In Iraq, vegetable ghee (known as Vanaspati in India) made from soy oil and palm oil, and flavored and colored to make it look and taste like butter, dominates the market because of its affordability. From a manufacturing standpoint, vegetable ghee derived from palm oil has the great advantage of being produced from fractionated palm oil derivatives – such as palm olein and palm stearin – without the need for hydrogenation. The absence of the hydrogenation process makes the product much cheaper to produce, and explains its growing popularity and acceptance in most of the Middle East, including Iraq, where the ratio of palm oil imports to total edible oils and fats rose from 25% in 1980 to approximately 52% in 2004. However, Iraqi consumers clearly prefer oils from sunflower, corn, and soy for dressing or salads. In 2005, palm oil accounted for 40% of the total vegetable oil imported, followed by sunflower and soy, each with a 30% share of the market. The segmentation more than a real consumer preference, reflects what is made available in the market through the PDS, more than a real consumer preference. Butter consumption is negligible because of the impossibility of keeping it refrigerated, while margarine consumption is limited to industrial use in the pastry and bakery industry. Iraq reportedly imports something around 45,000 – 50,000 tons of margarine, mainly from Turkey (35,000 tons in 2005). 6

6 Report USDA Foreign Agricultural Service number TU6016.

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

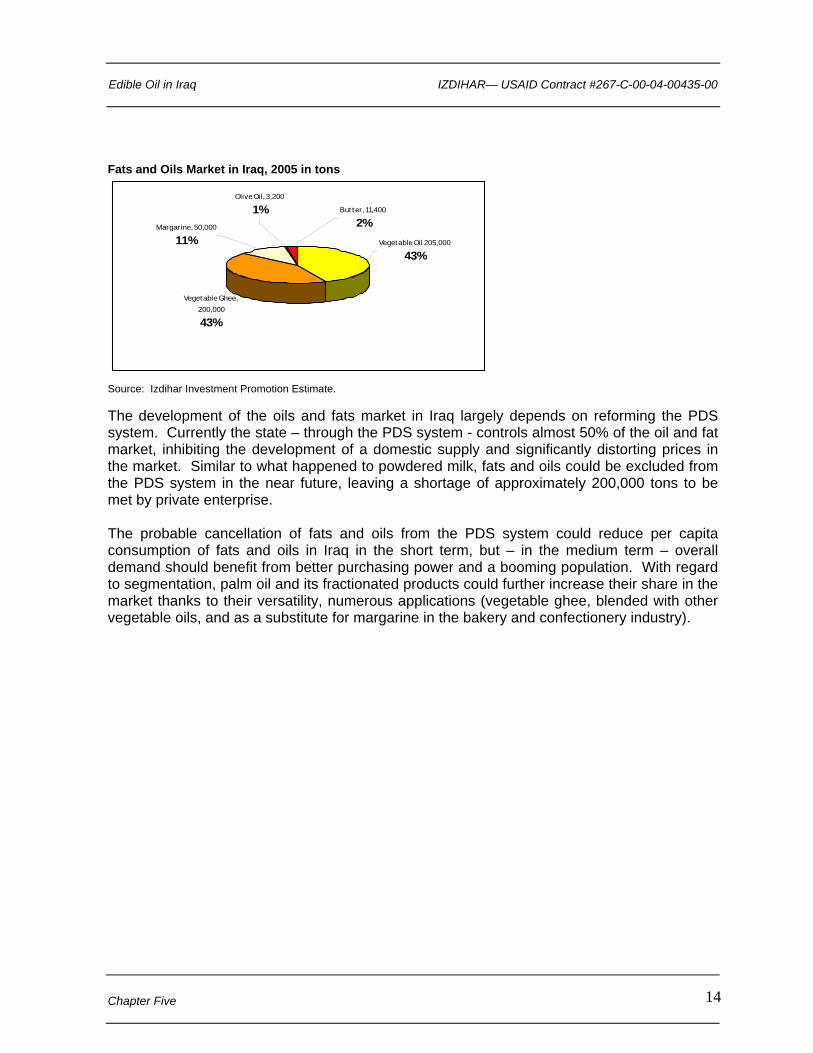

Fats and Oils Market in Iraq, 2005 in tons

Vegetable Ghee, 200,000

43%

Margarine, 50,000

11%

Olive Oil, 3,200

1% But ter, 11,400

2%Vegetable Oil 205,000

43%

Source: Izdihar Investment Promotion Estimate. The development of the oils and fats market in Iraq largely depends on reforming the PDS system. Currently the state – through the PDS system - controls almost 50% of the oil and fat market, inhibiting the development of a domestic supply and significantly distorting prices in the market. Similar to what happened to powdered milk, fats and oils could be excluded from the PDS system in the near future, leaving a shortage of approximately 200,000 tons to be met by private enterprise. The probable cancellation of fats and oils from the PDS system could reduce per capita consumption of fats and oils in Iraq in the short term, but – in the medium term – overall demand should benefit from better purchasing power and a booming population. With regard to segmentation, palm oil and its fractionated products could further increase their share in the market thanks to their versatility, numerous applications (vegetable ghee, blended with other vegetable oils, and as a substitute for margarine in the bakery and confectionery industry).

Chapter Five

14

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

Chapter Six

15

6. COMPETITION Competition in the vegetable fats and oils market in the MENA region is genuinely global. The Middle East and North Africa are important markets for vegetable oil, accounting for 15% of world vegetable oil imports. With regard to Iraq, the underlying facts shaping the competitive environment could be summarized as follows:

1. Competition is widely affected by the government through the PDS distribution system. A considerable percentage of the vegetable fat and oil products in Iraq are imported by the government through auctions not entirely guided by market criteria. Current imports are volatile and erratic, with large orders placed directly with palm oil producer countries such as Malaysia and Indonesia, or in the GCC countries where CPO (crude palm oil) is refined or fractionated.

2. Private imports of vegetable oil are primarily from the GCC countries (55% - 60%) and

from Turkey (mainly sunflower oil, almost 22,000 tons in the year 2005).

3. Turkey is a significant producer of oilseeds (sunflower production in 2006 is expected to be 2.1 million tons) but also a large importer of oilseeds and meals to meet demand from its large poultry industry and its domestic crushing and refining industries. There are about 180 crushing firms in Turkey with a total capacity of more than 4.5 million tons. Some 630 feed mills have an estimated capacity of 15.0 million tons. Turkey also has a large refining capacity, currently about 3.4 million tons, of which some 2.3 million is used to produce liquid oils and the remaining 1.1 million tons for margarine.

4. The competitive profile of the GCC countries – in particular Saudi Arabia and the UAE

– is more refining oriented and increasingly toward palm oil refining, fractionation and hydrogenation. As happens in most of the processed food industries in the GCC, processing units have modern, state-of-the-art technology with high installed capacity. Crushing plant capacity is usually well above 2,000 TPD (tons per day). Most refineries have been designed to process more than 1,500 TPD and none has a capacity < 1,000 TPD.

5. Jeddah-based food giant Savola is the most prominent and active player in the region.

Savola started as a producer of vegetable oils, today is one of the Saudi Arabia’s largest trading conglomerates. It produces a range of foodstuffs, including dairy products, through the Almarai Company. It also owns fast food and supermarket chains and is a major player in the Saudi real estate market. Savola Edible Oils (SEO) holds a 70% market share in Saudi Arabia, and a 26% share in Egypt. Recently the group established a joint ventures in Morocco and Sudan, and has bought a controlling 49% interest in Iranian edible oil giant, Behshair Industrial Company (BIC). This represents an investment of some $75 million, one of the largest strategic initiatives in the Saudi company’s history. BIC holds an estimated 37% share in the Iranian edible oil market, estimated at 1.2 million tons per year in 2005.

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

Chapter Six

16

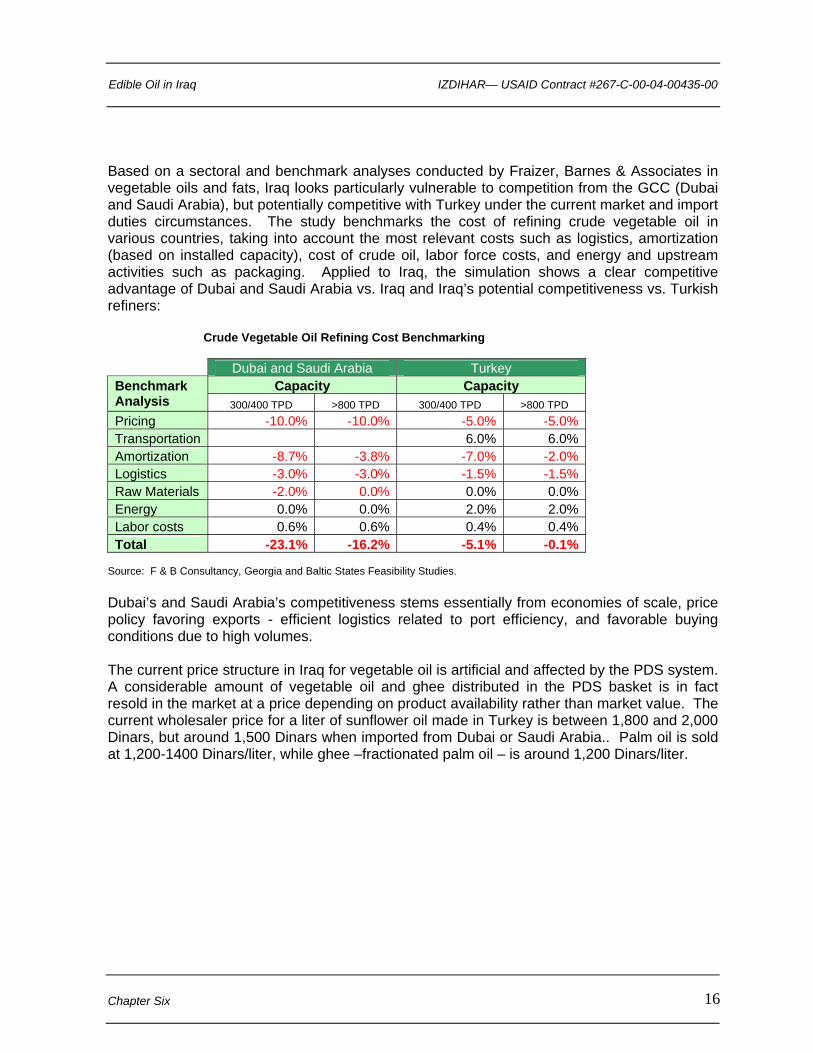

Based on a sectoral and benchmark analyses conducted by Fraizer, Barnes & Associates in vegetable oils and fats, Iraq looks particularly vulnerable to competition from the GCC (Dubai and Saudi Arabia), but potentially competitive with Turkey under the current market and import duties circumstances. The study benchmarks the cost of refining crude vegetable oil in various countries, taking into account the most relevant costs such as logistics, amortization (based on installed capacity), cost of crude oil, labor force costs, and energy and upstream activities such as packaging. Applied to Iraq, the simulation shows a clear competitive advantage of Dubai and Saudi Arabia vs. Iraq and Iraq’s potential competitiveness vs. Turkish refiners: Crude Vegetable Oil Refining Cost Benchmarking

Dubai and Saudi Arabia Turkey Capacity Capacity Benchmark

Analysis 300/400 TPD >800 TPD 300/400 TPD >800 TPD Pricing -10.0% -10.0% -5.0% -5.0% Transportation 6.0% 6.0% Amortization -8.7% -3.8% -7.0% -2.0% Logistics -3.0% -3.0% -1.5% -1.5% Raw Materials -2.0% 0.0% 0.0% 0.0% Energy 0.0% 0.0% 2.0% 2.0% Labor costs 0.6% 0.6% 0.4% 0.4% Total -23.1% -16.2% -5.1% -0.1%

Source: F & B Consultancy, Georgia and Baltic States Feasibility Studies. Dubai’s and Saudi Arabia’s competitiveness stems essentially from economies of scale, price policy favoring exports - efficient logistics related to port efficiency, and favorable buying conditions due to high volumes. The current price structure in Iraq for vegetable oil is artificial and affected by the PDS system. A considerable amount of vegetable oil and ghee distributed in the PDS basket is in fact resold in the market at a price depending on product availability rather than market value. The current wholesaler price for a liter of sunflower oil made in Turkey is between 1,800 and 2,000 Dinars, but around 1,500 Dinars when imported from Dubai or Saudi Arabia.. Palm oil is sold at 1,200-1400 Dinars/liter, while ghee –fractionated palm oil – is around 1,200 Dinars/liter.

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

Chapter Seven

17

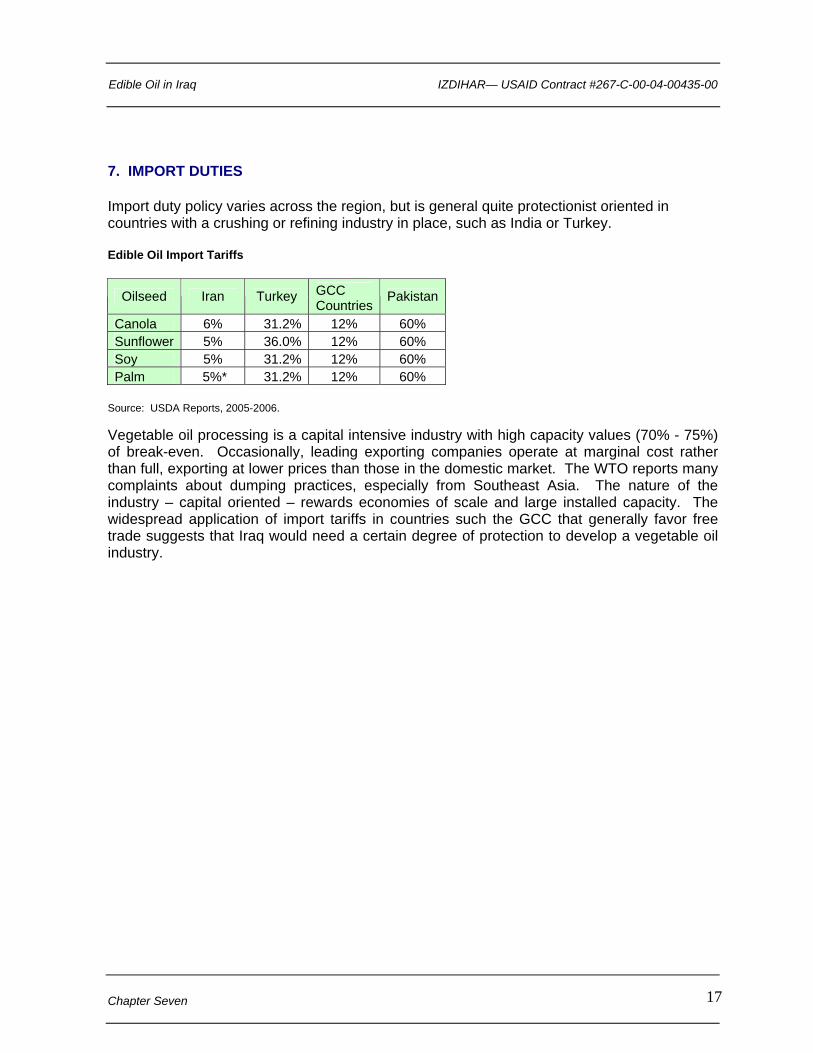

7. IMPORT DUTIES Import duty policy varies across the region, but is general quite protectionist oriented in countries with a crushing or refining industry in place, such as India or Turkey. Edible Oil Import Tariffs

Oilseed Iran Turkey GCC Countries

Pakistan

Canola 6% 31.2% 12% 60% Sunflower 5% 36.0% 12% 60% Soy 5% 31.2% 12% 60% Palm 5%* 31.2% 12% 60%

Source: USDA Reports, 2005-2006. Vegetable oil processing is a capital intensive industry with high capacity values (70% - 75%) of break-even. Occasionally, leading exporting companies operate at marginal cost rather than full, exporting at lower prices than those in the domestic market. The WTO reports many complaints about dumping practices, especially from Southeast Asia. The nature of the industry – capital oriented – rewards economies of scale and large installed capacity. The widespread application of import tariffs in countries such the GCC that generally favor free trade suggests that Iraq would need a certain degree of protection to develop a vegetable oil industry.

Edible Oil in Iraq IZDIHAR— USAID Contract #267-C-00-04-00435-00

Chapter Eight

18

8. CONCLUSIONS

1) Even with the implementation of a more aggressive oilseed plantation program aimed at increasing oilseed production, Iraq will probably remain largely dependent on imports in the medium to long term. Rapeseed (Canola hybrid) looks like the most promising oilseed crop for Iraq, based on data collected by ICARDA in the region. Rapeseed could provide additional income to farmers as a double crop with wheat or as an alternative winter crop.

2) A large scale crushing operation is not currently viable for lack of a strong poultry

industry that could create a high demand for meal. Small mechanical crushing operations seem more appropriate for Iraq, taking into account its limited oilseed production and the current small size of the poultry and aquaculture industries.

3) The current demand for vegetable oil and ghee (manly derived from palm oil) - both

around 200,000 tons per year - confirms the potential for a refining operation. Nevertheless the financial viability of a refining operation depends on:

• Capacity: The ideal capacity should be around 800 TPD, which implies

controlling a 72% share of the fats and oils market in Iraq. A lower capacity – 300/400 TPD – would probably be scarcely competitive with refineries in the Gulf states (Dubai and Saudi Arabia) and Turkey.

• The elimination of the PDS system, currently controlling more than 50% of the market and distorting the price structure.

• A plant with the technology to refine palm, soy, rapeseed, sunflower crude oils and to produce fractionated palm oil for ghee.

4) In particular, the elimination of the PDS appears to be a condition sine qua non, while

a plant with minimal refining capacity lacking the benefits of economies of scale would probably require tariffs on refined vegetable oil imports of around 20% in order to make domestic production competitive. Small capacity plants have low profitability – on average 10.4% R.O.I vs. an average 15-17% of bigger plants with capacity around 1,000 TPD.7

5) Because of the importance of the transportation cost, the ideal location for a refinery is

Basrah, close to the Umm Qasr port, the second biggest city in Iraq and well connected to Bahdad the biggest consumer center in the country. An alternative location in northern Iraq with supply from Turkey (Adana area or the Black Sea ports of Trabzon, Samsun and Bat’um) would imply a significant increase in transportation costs (+6-7%) hampering product competitiveness vs. imports from Dubai and Saudi Arabia. The strategic location of a possible refinery in Basrah is even more fundamental taking in mind the current high share of palm oil in the Iraqi market – possibly as high as 70% - proceeding from Malaysia, Indonesia, and Thailand.

7 Frazier, Barnes & Associates, LLC Memphis feasibility studies Georgia and Baltic States report February 2006.