Embed Size (px)

Citation preview

About First Last Name

First Last NameTitle Company Name

Lorem ipsum dolor sit amet, consectetuer adipiscing elit, sed diam nonummy nibh euismod tincidunt ut laoreet dolore magna aliquam erat volutpat. Ut wisi enim ad minim veniam, quis nostrud exerci tation ullamcorper suscipit lobortis nisl ut aliquip ex ea commodo consequat.

Duis autem vel eum iriure dolor in hendrerit in vulputate velit esse molestie consequat, vel illum dolore eu feugiat nulla facilisis at vero eros et accumsan et iusto odio dignissim qui blandit praesent luptatum zzril delenit augue duis dolore te feugait nulla facilisi. Lorem ipsum dolor sit amet, consectetuer adipiscing elit, sed diam nonummy nibh euismod tincidunt ut laoreet dolore magna aliquam erat volutpat.

Ut wisi enim ad minim veniam, quis nostrud exerci tation ullamcorper suscipit lobortis nisl ut aliquip ex ea commodo consequat. Duis autem vel eum iriure dolor in hendrerit in vulputate velit esse molestie consequat, vel illum dolore eu feugiat nulla facilisis at vero eros et accumsan et iusto odio dignissim qui blandit praesent luptatum zzril delenit augue duis dolore te feugait nulla facilisi.

Nam liber tempor cum soluta nobis eleifend option congue nihil imperdiet doming id quod mazim placerat facer possim assum. Lorem ipsum dolor sit amet, consectetuer adipiscing elit.

YOUR BIOGRAPHY GOES HERE

Welcome to…How To Maximize Your Retirement Readiness!

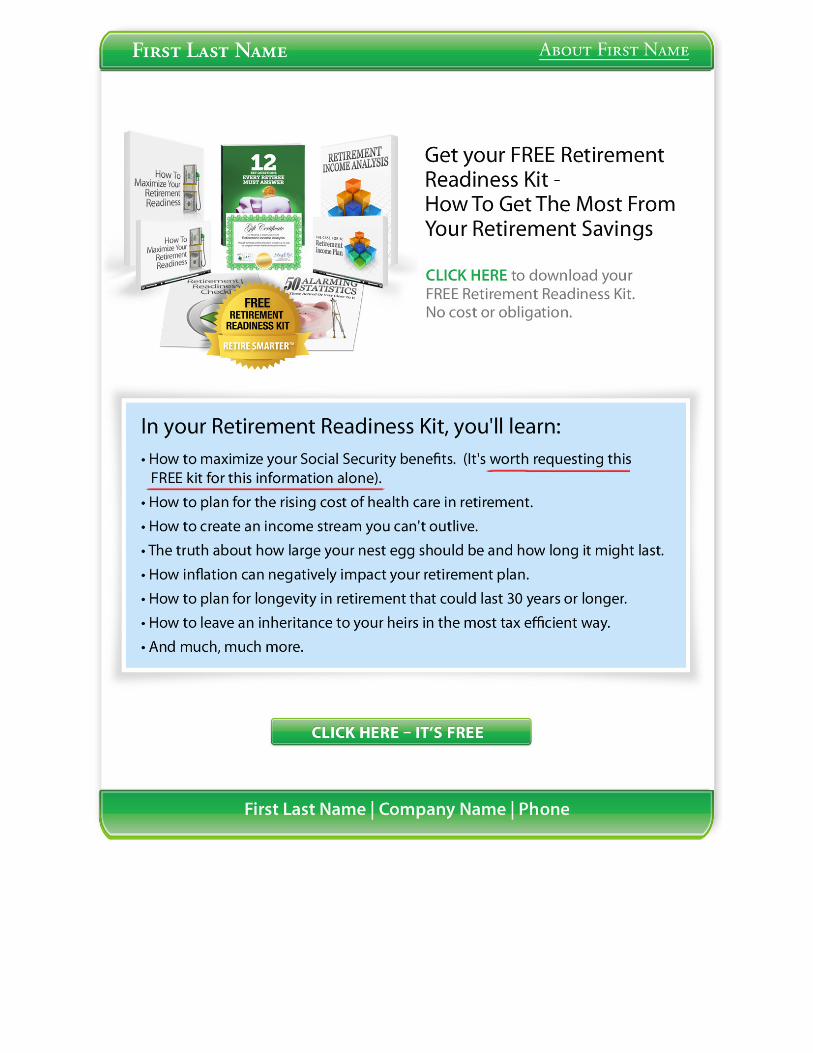

We’ve designed this presentation to help you get the most from your retire-ment savings.

Over the next few minutes, we’ll ask some important questions. Your an-swers will help determine if your financ-es are RETIREMENT READY.

We encourage you to watch again and again, so you’ll know you’re doing every-thing possible to help MAXIMIZE YOUR RETIREMENT!

The face of aging will never be the same again, as 78 million Americans approach-ing retirement transform how we live, work and invest.Source: Merrill Lynch Workplace Insights. The End of Old. 2014.

When it comes to RETIREMENT, it seems 80 is the new 60, and with it comes a whole new set of challenges.Source: UBS Investor Watch. 80 Is The New 60. 4Q 2013

Are you in the majority of Americans wor-ried about not having enough money for retirement?Source: Gallup’s Annual Economy and Per-sonal Finance Poll. April 22, 2014

More than 3 in 5… 61% fear depleting their retirement assets… more than DEATH! Source: Allianz Life Insurance Company. 2013 Reclaiming The Future Study Executive Summary

We feel that NOW is the time to STOP and put your current strategy to the test

to see just how survivable your retirement nest egg really is.

So how do you become “RETIREMENT READY”?

It starts by increasing your knowledge with our 12 Key Questions Every Retiree Must Answer.

You need answers today that are right for you, based on your unique set of circum-stances that take into account the hopes, dreams and goals of the retirement you’ve envisioned.

The 12 Key Questions Action Guide is part of your Retirement Readiness Kit,

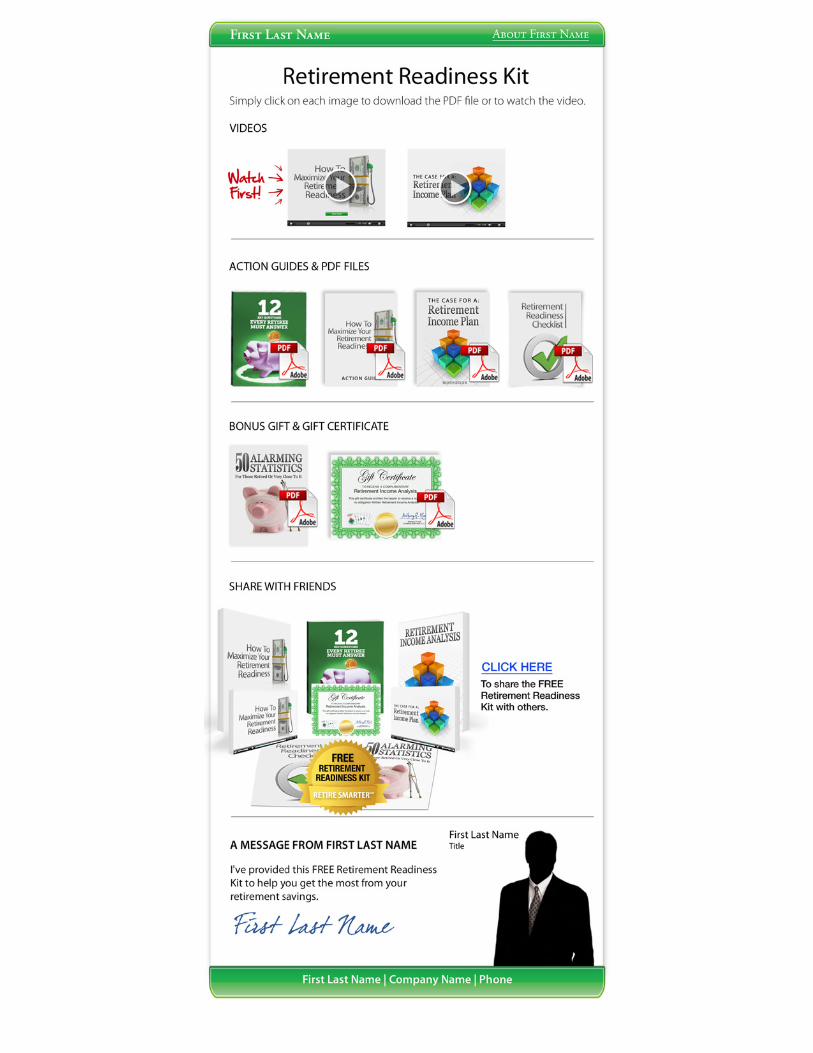

which also includes an invitation to receive a no cost, no obligation Retirement Income Analysis…. prepared just for you.

Why is having a Retirement Income Analy-sis so important? Listen closely…

According to Wells Fargo…those that had a written retirement plan in place…accu-mulate 3x as much in retirement assets as those that don’t.Source: Wells Fargo Study. Middle Class Americans Face A Retirement Shutdown. Oct 23, 2013

Do YOU have a written retirement income plan in place?

Notice, I said INCOME plan….not an INVESTMENT plan.

They’re not the same, and actually, they’re quite different.

An INVESTMENT plan….It’s designed to grow your nest egg in the ACCUMULA-TION phase…before retirement.

A Retirement INCOME plan, however…It’s designed for when you begin DRAWING DOWN your nest egg in the SPENDING phase of your retirement.

Have YOU overlooked this critical planning tool for your retirement?

The switch from a retirement savings plan to a retirement income plan is one of the most challenging aspects of retirement planning.

And why our Retirement Income Analysis can be SO instrumental in helping make that transition.

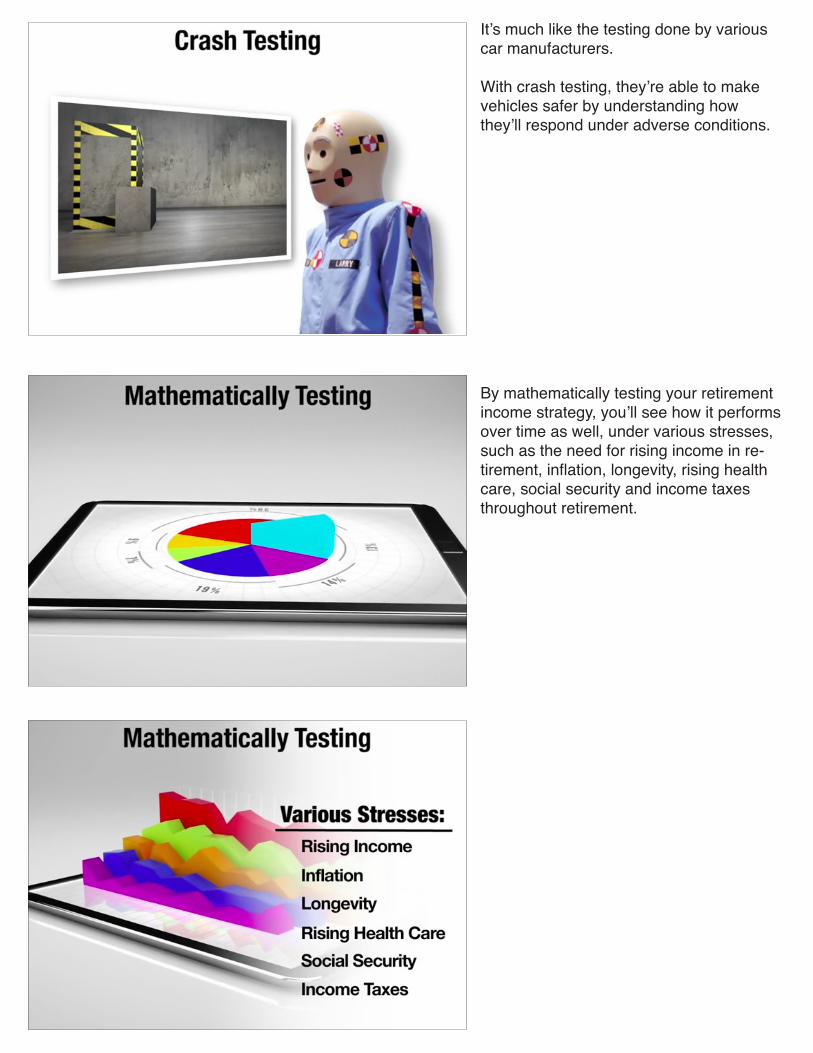

It’s much like the testing done by various car manufacturers.

With crash testing, they’re able to make vehicles safer by understanding how they’ll respond under adverse conditions.

By mathematically testing your retirement income strategy, you’ll see how it performs over time as well, under various stresses, such as the need for rising income in re-tirement, inflation, longevity, rising health care, social security and income taxes throughout retirement.

That testing may expose possible problems with your plan

so you can make the necessary adjust-ments now…

Changes that can help you to get more value from ALL of your retirement accounts.

Do you realize the retirement challenges you have today, that your parents never had to deal with?

Retirement planning for their generation meant a going away party, a Gold watch and a nice pension with a guaranteed pay-check for life.

When you think of YOUR retirement…I’m sure many of these images come to mind, but regardless of what you envision your retirement to be…

To get there…YOU’RE RESPONSIBLE to not only protect the nest egg you’ve worked so hard to accumulate…

But you’ll need to grow those assets

to generate the maximum income…an income stream that will last your lifetime.

Are your worried about the Rising Cost of Health Care?

Today, that tops the list of retirement wor-ries, and even more so among the affluent. Source: Merrill Lynch. 2013 Americans’ Perspectives on New Retirement Realities Study.

Nearly half of high net worth individuals…are “terrified” how rising health care costs could decimate years of retirement plan-ning.Source: Nationwide Financial Survey, May 7, 2012

To be RETIREMENT READY, you should have a meaningful discussion NOW about how to maximize your retirement income

to meet the rising cost of healthcare.

Contrary to marketing and sales pitches that suggest there’s a “MAGIC NUMBER” that will guarantee financial security.

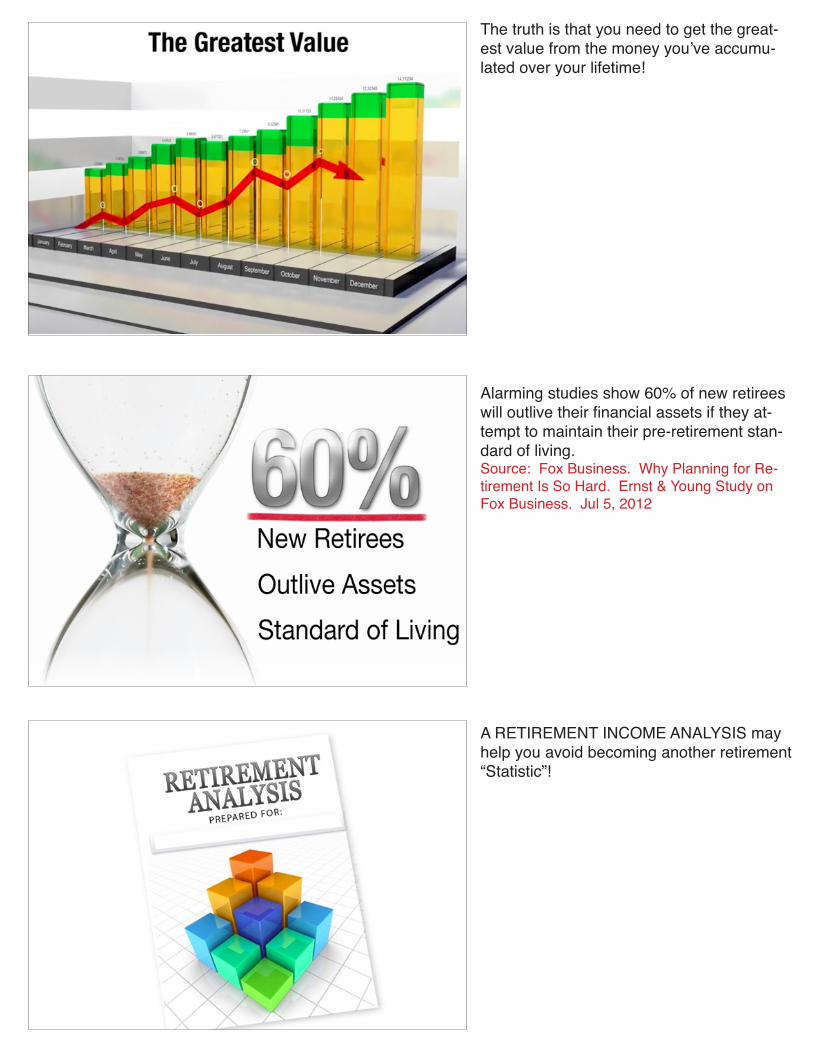

The truth is that you need to get the great-est value from the money you’ve accumu-lated over your lifetime!

Alarming studies show 60% of new retirees will outlive their financial assets if they at-tempt to maintain their pre-retirement stan-dard of living. Source: Fox Business. Why Planning for Re-tirement Is So Hard. Ernst & Young Study on Fox Business. Jul 5, 2012

A RETIREMENT INCOME ANALYSIS may help you avoid becoming another retirement “Statistic”!

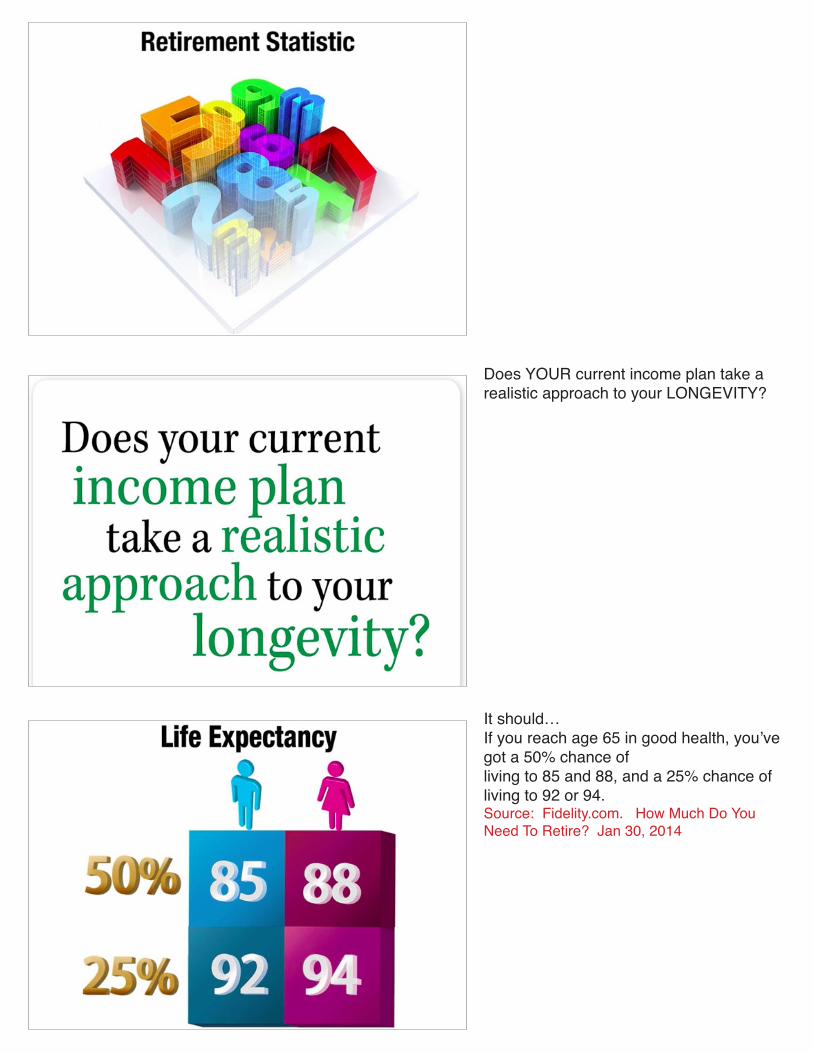

Does YOUR current income plan take a realistic approach to your LONGEVITY?

It should…If you reach age 65 in good health, you’ve got a 50% chance ofliving to 85 and 88, and a 25% chance of living to 92 or 94. Source: Fidelity.com. How Much Do You Need To Retire? Jan 30, 2014

RETIREMENT READINESS is KNOWING your retirement income stream will also last that long…an income stream you can’t outlive.

Do YOU know how much you can safely spend from your nest egg each year, so you don’t run out of money?

Studies show the majority of retirees under-estimate THEIR expenses in retirement,

putting them at risk of outliving their retire-ment savings?Source: The Street.com. Americans Retiring Early, Then Running Out of Money. Nov 11, 2013

RETIREMENT READINESS begins with knowing what your actual expenses in retire-ment might be

AND then testing your strategy to see if your retirement nest egg can safely pro-vide for your needs!

Have YOU built a “cost of living” increase into your retirement income plan?

Today, it’s irresponsible not to include it… You would expect things to cost more in the future, especially with the prospect of higher taxes

and increased healthcare costs.

NOW is the time to get the facts on how these higher costs will impact YOUR retire-ment income planning!

Do YOU know the proper strategy to MAXI-MIZE YOUR Social Security?

Navigating your way through Social Secu-rity so you select the right benefits at the right time is one of the biggest financial decisions you’ll ever make.

Do you know which one of the 567 ways to claim Social Security will maximize the lifetime benefits for you and your spouse? Source: 44 Social Security Secrets All Baby Boomers Need To Know. Laurence Kotlikoff

Have you ever analyzed just how much more money you could get by smart social security planning?You see…

Getting it right could mean tens of thou-sands of additional dollars in retirement.Source: 44 Social Security Secrets All Baby Boomers Need To Know. Laurence Kotlikoff

Making a mistake could cost you up to 72% of your benefits.Source: 44 Social Security Secrets All Baby Boomers Need To Know. Laurence Kotlikoff

Social Security is enormously complex. This is just one of many issues we ad-dress in our Retirement Income Analysis.

The information on Social Security ALONE is reason enough to have a Retirement Income Analysis prepared.

And there’s no cost and no obligation to do it.

To be RETIREMENT READY….

you’ll want to make your money go further by controlling risk, reducing costly fees, and minimizing income taxes throughout retire-ment!

You should also understand how market downturns today are much riskier… now that you depend on your nest egg to provide your retirement income!

The lessons learned from the financial wake up call of the recent recessions,

has amplified the dangers and the very real risks of aggressive investment strategies.

And to complete your RETIREMENT READINESS, you’ll also want to know the most tax efficient method to transfer any assets left over to your heirs.

The challenges facing today’s retirees are numerous. And this is where we’d like to help.

If you’ve hit 45, 55, 65, even 75 years of age,

whether you’re retired or close to it… we’d like to help in your goal of becoming RE-TIREMENT READY.

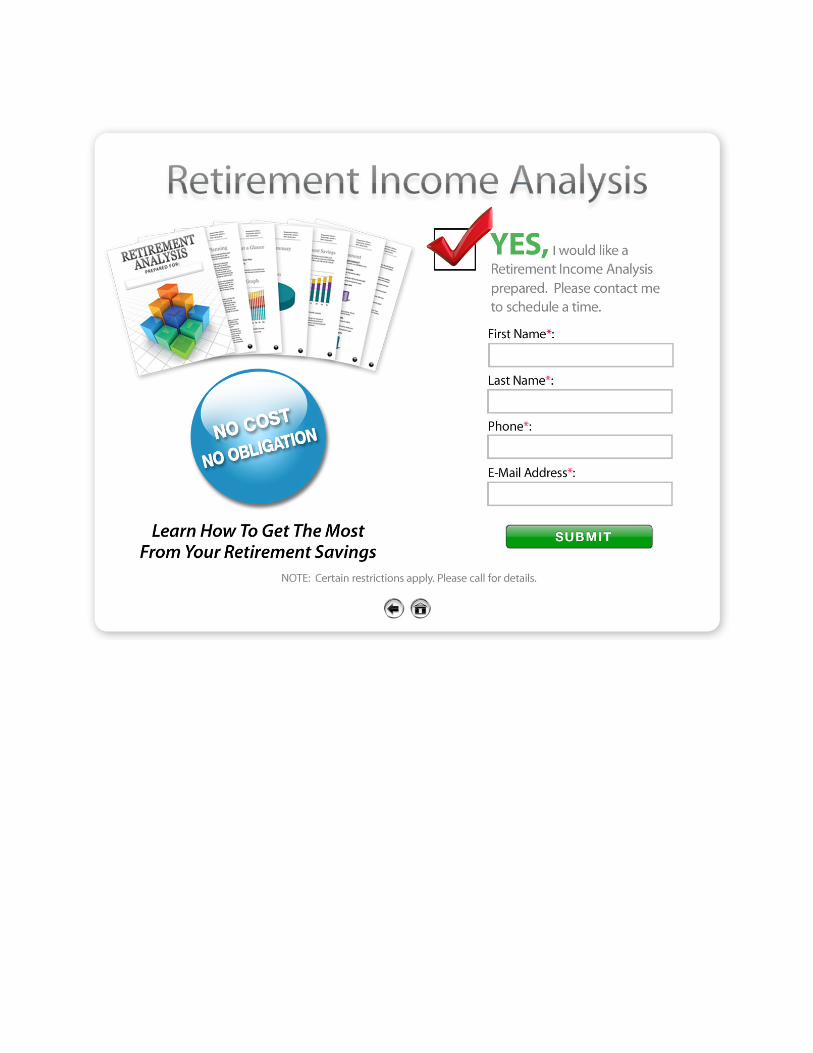

Would YOU benefit from a personalized Retirement Income Analysis?

We believe…YES.

Here are 6 ways both pre and post retirees tend to benefit.

FIRST: It will help simplify the issues critical to your retirement, the risks you face, the challenges that lie ahead and the prepara-tions you’ll need to make.

SECOND: It will help simplify your transi-tion from a retirement SAVINGS plan to a retirement INCOME plan.

THIRD: You’ll see the results of testing your current plan to verify if it will survive throughout retirement and if not, make the necessary adjustments!

FOURTH: You’ll examine potential outcomes of various “what if” scenarios, along with the pros and cons of the trade offs you must consider.

FIFTH: You’ll have a plan that harnesses all of your resources working together all aligned to help you to maximize your retire-ment.

AND SIXTH: You’ll have a process in place to act as a guide to course correct as circum-stances warrant and changes are needed.

In addition, you’ll have CLARITY about your retirement by having specific answers tai-lored just for you…to The 12 Key Questions Every Retiree Must Answer.

In a moment, you’ll be given an opportunity to receive a Retirement Income Analysis, but first, it’s your turn…

We’d love to hear your thoughts about this presentation.

Welcome to…The Case For A Retirement Income Plan.

Over the next few minutes, we’ll focus on 3 things…

First…why you need a Retirement Income Plan…Second…why sooner is much better than later.And third…what’s involved in putting it together.

With people living longer,

health care costs rising,

pensions disappearing

and people embracing longer, more active lifestyles,

retirees today need to be a lot more deliberate about making their money last.

Will you have enough to live the retirement life you’d like?

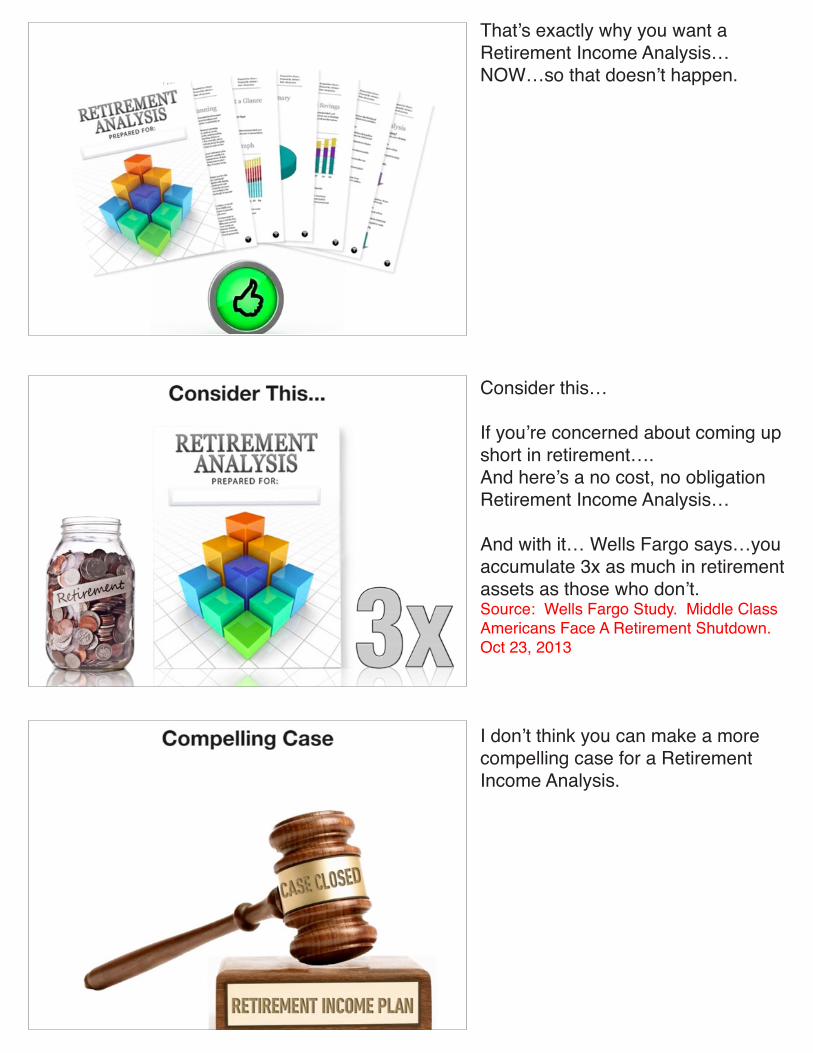

Studies show…People with retirement income plans in place…make better decisions.

And in addition, they have more income in retirement as well.Source: Forbes. Why The Stakes Are Higher With Retirement Income Planning Than Retirement Savings. April 10, 2014

70% of those with a written plan are confident they’ve saved enough for retirement

compared to just 44% without a plan.Source: Wells Fargo Study. Middle Class Americans Face A Retirement Shutdown. Oct 23, 2013

The biggest fear for pre and post retirees is they haven’t socked enough away

and they’re fearful of running out of money in retirement.Source: You’ll Never Run Out of Money In Retirement. The Motley Fool. Feb 22, 2014.

That’s exactly why you want a Retirement Income Analysis…NOW…so that doesn’t happen.

Consider this…

If you’re concerned about coming up short in retirement….And here’s a no cost, no obligation Retirement Income Analysis…

And with it… Wells Fargo says…you accumulate 3x as much in retirement assets as those who don’t.Source: Wells Fargo Study. Middle Class Americans Face A Retirement Shutdown. Oct 23, 2013

I don’t think you can make a more compelling case for a Retirement Income Analysis.

Why should you have one prepared for you?I can think about at least 3x as many reasons.Source: Wells Fargo Study. Middle Class Americans Face A Retirement Shutdown. Oct 23, 2013

Still not convinced…

Here’s just one…of the many areas we address in your Retirement Income Analysis.

Social Security…For most 65 and older…

It represents the largest source of income in your nest egg…Source: US News & World Report. The 4 Most Important Sources of Retirement Income. March 22, 2012.

Representing 38% of your income in retirement.Source: Social Security Basic Facts. www.ssa.gov. April 2, 2014.

Smart Social Security Planning has never been more important…

• 51% of workers have no private pension today

• 34% have no savings set aside for retirement.

Source: Social Security Basic Facts. www.ssa.gov. April 2, 2014.

In the other video in your Retirement Readiness Kit,

How To Maximize Your Retirement Readiness…

you learned they’re 567 ways to claim social security.Source: 44 Social Security Secrets All Baby Boomers Need To Know. Laurence Kotlikoff

Now before you think you know the 1 best way that will maximize your lifetime benefits…

Consider this… For a couple, age 62, there are over 100 million combinations of months for each of the two spouses to take benefits.Source: 44 Social Security Secrets All Baby Boomers Need To Know. Laurence Kotlikoff

And if you think the Social Security administration is there to help.

Think again.

The Social Security Handbook has 2,728 separate rules governing your benefits.Source: 44 Social Security Secrets All Baby Boomers Need To Know. Laurence Kotlikoff

Yet they provide you with ZERO employees to advise you on the best strategy. Source: 44 Social Security Secrets All Baby Boomers Need To Know. Laurence Kotlikoff

Hey…It’s me again. Yep…down here in the corner. Trust me when I say…This one decision about your Social Security is one of the most important decisions you’ll ever make regarding your retirement…Here’s why…

If you get it right…it could mean tens of thousands of additional dollars in retirement income.Source: 44 Social Security Secrets All Baby Boomers Need To Know. Laurence Kotlikoff

Make a mistake and you risk losing up to 72% of your benefits.Source: 44 Social Security Secrets All Baby Boomers Need To Know. Laurence Kotlikoff

With potentially 10’s of thousands of dollars at stake…

How confident are you NOW

that you’ve got the expertise to make the right decision on your own?

With 567 ways, 100 million combintations, 2,728 rules, and so much at stake, Source: 44 Social Security Secrets All Baby Boomers Need To Know. Laurence Kotlikoff

arriving at the right social security claiming strategy for many looks an awful lot like this…Source: 44 Social Security Secrets All Baby Boomers Need To Know. Laurence Kotlikoff

It’s your Social Security…but what you don’t know CAN hurt you.

And this is just ONE of many issues we address…

But…as you’re about to see, having a Retirement Income Analysis prepared SOONER is much better than LATER...And here’s WHY.

Let’s assume you’re flying from Los Angeles to New York City, but they’ve only put enough fuel onboard to get you somewhere over Chicago.

When would be the best time to address that shortfall?

When you’re 30,000 feet in the air, somewhere over Chicago, two-thirds of the way to your desingation, but you’re out of fuel… Or would it be better to address it while you’re still on the ground in LA before you take off?

The answer is pretty obvious., isn’t it?

Well…When would be the best time to address a retirement shortfall?

When you’re two-thirds of the way into your retirement, and you’ve depleted your nest egg and run out of money, but you could easily live another 10 or 15 years….

Or would it be better to address it while you’re still working, before you retire, or shortly after you retirement, so you’ve got plenty of time to course correct and make adjustments along the way.

The answer is just as obvious, isn’t it?

Whether your already retired or very close to it…

NOW is the time

to have a Retirement Income Analysis prepared just for you…

based on your unique set of circumstances,

that takes into account the hopes, dreams and goals of the retirement you envision.

Your Retirement Income Analysis

is created with one goal in mind…To help you get the most from your retirement savings.

Well, hopefully at this point, you’re sold on the need to have a Retirement Income Analysis and you agree that having it prepared SOONER is much better than LATER. So let’s walk through and explain the process of creating it.

Here are the 6 steps we’ll go through with you in preparing your complimentary Retirement Income Analysis.

Step 1: We’ll ask you to articulate what your portfolio is intended to do, and describe what you’d like your ideal retirement to be… This way we both understand the real purpose of your retirement income planning!

Does the retirement you envision include any of these activities?

Step 2: We will help you to inventory all of your assets, savings and investments into one simple to understand report.

In order to create a sustainable Retirement Income Plan, we’ll help you understand the pros and cons of each of your assets such as these.

Step 3: We’ll help you calculate to see what your expenses in the retirement YOU envision…might be.

Some expenses will increase in retirement, while others may decrease, but we’ll bring these into clear focus, in addition to addressing rising health care costs and how to plan for it.

Step 4: We’ll total up your income in retirement from all sources to get a clear retirement income picture.

In retirement, you’ll likely have several sources of income such as these…and we’ll detail it all in one easy to understand report.

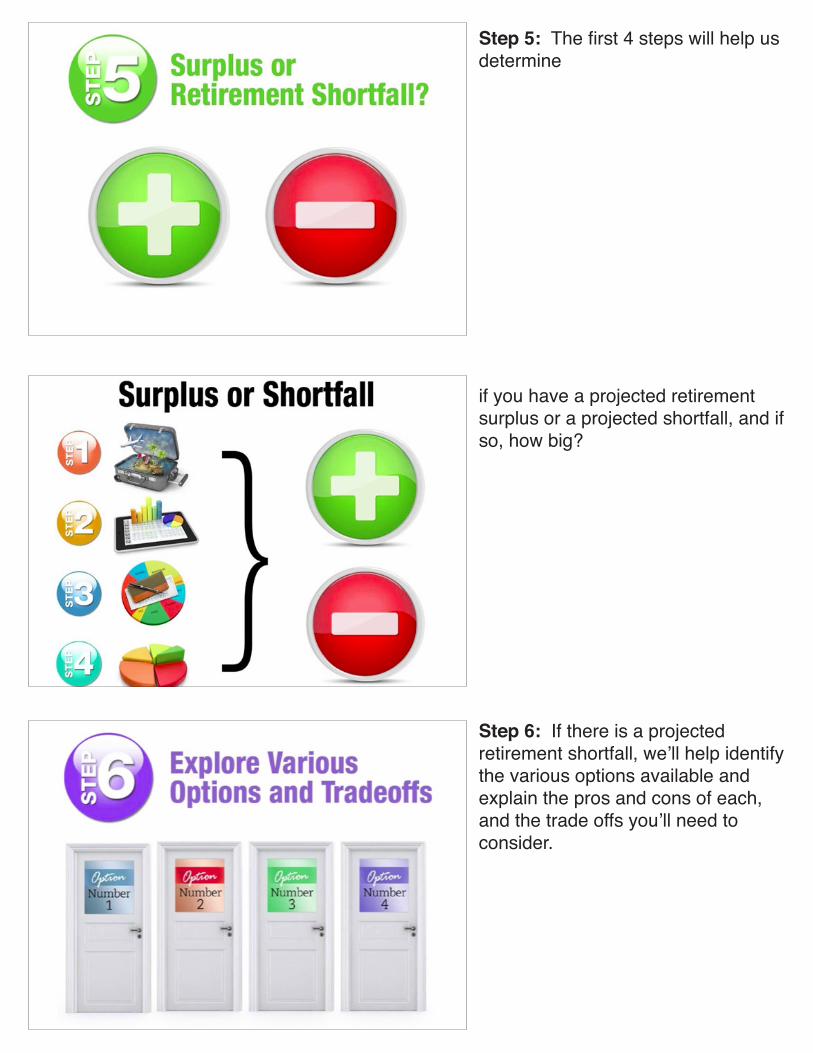

Step 5: The first 4 steps will help us determine

if you have a projected retirement surplus or a projected shortfall, and if so, how big?

Step 6: If there is a projected retirement shortfall, we’ll help identify the various options available and explain the pros and cons of each, and the trade offs you’ll need to consider.

Would you benefit from a Retirement Income Analysis?

Since there is no cost and no obligation, you really have nothing to lose,

but quite possibly much to gain….How much?

According to Wells Fargo….3x as much.

We’d like to invite you NOW to receive a no cost, no obligation Retirement Income Analysis prepared just for you.