Embed Size (px)

Citation preview

Vesteda Residential Fund

Business Case and process for obtaining a corporate credit rating

DACT Treasury Beurs13 November 2015

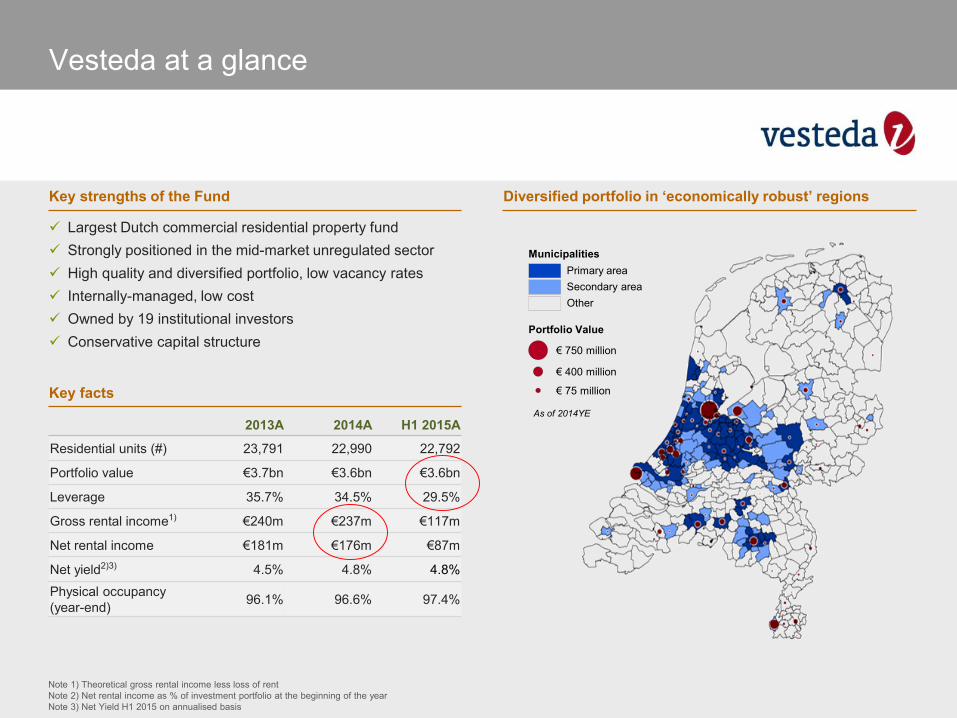

Vesteda at a glance

9 Largest Dutch commercial residential property fund9 Strongly positioned in the mid-market unregulated sector9 High quality and diversified portfolio, low vacancy rates9 Internally-managed, low cost 9 Owned by 19 institutional investors9 Conservative capital structure

2013A 2014A H1 2015A

Residential units (#) 23,791 22,990 22,792

Portfolio value €3.7bn €3.6bn €3.6bn

Leverage 35.7% 34.5% 29.5%

Gross rental income1) €240m €237m €117m

Net rental income €181m €176m €87m

Net yield2)3) 4.5% 4.8% 4.8%Physical occupancy (year-end) 96.1% 96.6% 97.4%

Primary areaSecondary areaOther

Portfolio Value

Municipalities

€ 750 million

€ 400 million

€ 75 million

As of 2014YE

Note 1) Theoretical gross rental income less loss of rent Note 2) Net rental income as % of investment portfolio at the beginning of the yearNote 3) Net Yield H1 2015 on annualised basis

Key facts

Key strengths of the Fund Diversified portfolio in ‘economically robust’ regions

3

Two Storm FrontsAssets and debt funding under pressure

Source: CBS / AFME

Average house prices (EUR)

4

Dutch housing market decline

190

200

210

220

230

240

250

260

270

50%

60%

70%

80%

90%

100%

110%

120%

-21%

Jan-13

Jan-11

Jan-12

Jan-09

+17%

Jan-10

Jan-14

Jan-08

House transaction prices (lhs)Rental price index (rhs)

Rental price index(2008=100)

Drought in Securitisation markets

Housing prices have come down and CMBS market disappeared

Time for Action – Adaptation of the liability side

� Unlock the stranglehold of the CMBS structure

� Deleverage in order to avoid default

� Implement diversification of funding sources

� Generate funding flexibility with ability to tap the most liquid sources/markets

� Create a future proof and scalable debt capital structure

5

Vesteda Treasury long-term target: Creating a reliable funding structure that serves the business at an optimal price

6

2014

Q1 Q2 Q3 Q4

2015

Q1 Q2 Q3 Q4

2013

Q1 Q2 Q3 Q4

2011

Q1 Q2 Q3 Q4

2012

Q1 Q2 Q3 Q4

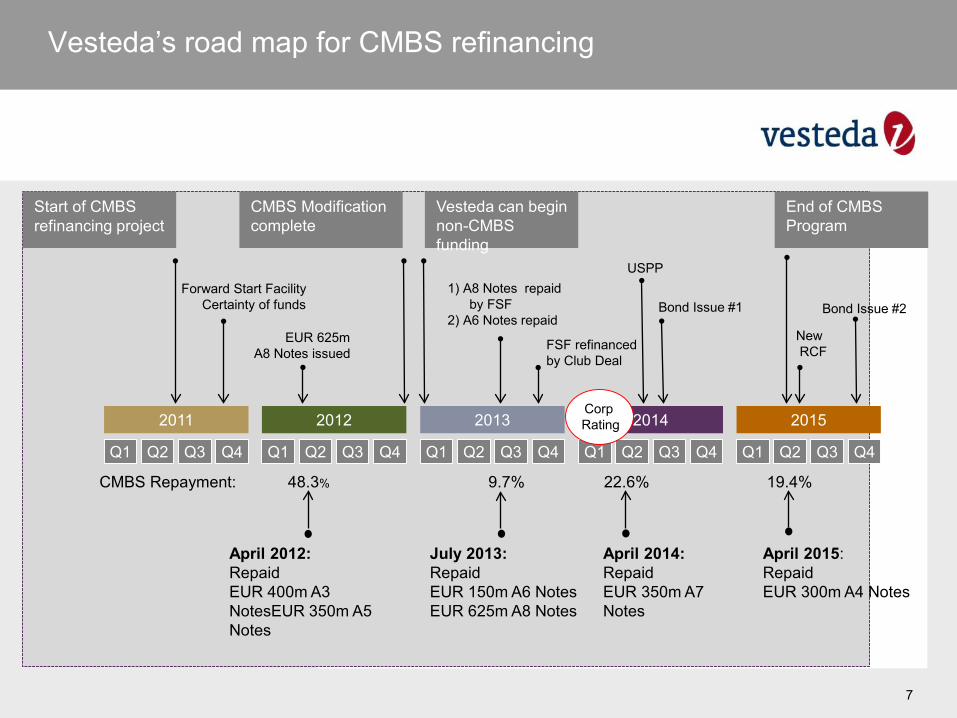

April 2015: RepaidEUR 300m A4 Notes

April 2014: RepaidEUR 350m A7 Notes

July 2013:Repaid EUR 150m A6 NotesEUR 625m A8 Notes

April 2012:RepaidEUR 400m A3 NotesEUR 350m A5 Notes

48.3% 9.7% 22.6% 19.4%CMBS Repayment:

Forward Start Facility Certainty of funds

EUR 625mA8 Notes issued

End of CMBS Program

1) A8 Notes repaidby FSF

2) A6 Notes repaid

FSF refinanced by Club Deal

Vesteda can begin non-CMBS funding

Vesteda’s road map for CMBS refinancing

7

Bond Issue #1

CMBS Modification complete

Bond Issue #2

USPP

NewRCF

Start of CMBS refinancing project

CorpRating

Credit rating research:A combination of work and academic research (VU RT)

8

Idea for a thesis that is linked to a ‘live’ business problem:

� Access: A credit rating might enable access to a larger pool of funding alternatives

� Trade-Off: Analysis of the ‘pros and cons’ of a credit rating (CR)

� Return: Impact on Cost of Capital

Thesis: “What are the relevant strategic considerations, costs and benefits for Vesteda to obtain a Corporate Credit Rating?”

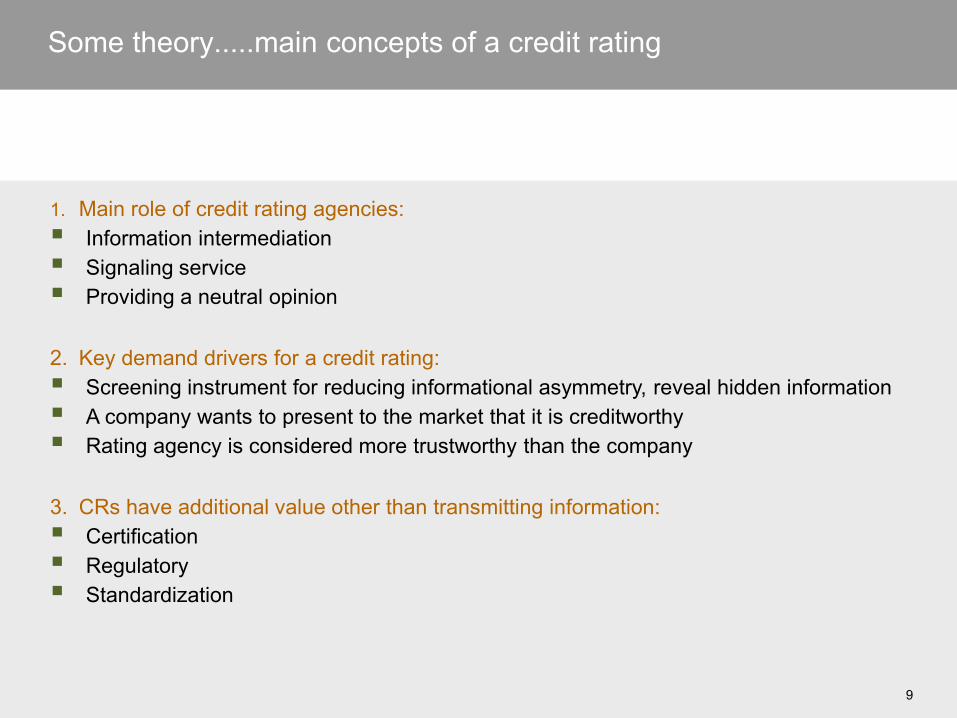

Some theory.....main concepts of a credit rating

9

1. Main role of credit rating agencies:� Information intermediation� Signaling service� Providing a neutral opinion

2. Key demand drivers for a credit rating: � Screening instrument for reducing informational asymmetry, reveal hidden information� A company wants to present to the market that it is creditworthy� Rating agency is considered more trustworthy than the company

3. CRs have additional value other than transmitting information:� Certification � Regulatory� Standardization

The credit rating industry

10

� Worldwide a total of some 150 rating agencies are in operation

� The market share of the top 3 rating agencies is 90%1 or more

40%

35%

16%

10%

S&P Moody's Fitch Other

1) ESMA publication: Credit Rating Agencies’ 2014 market share

A. Legislation: SEC selected Moody's, S&P and (later) Fitch for setting standards in 1930’s

B. Reputation: CRA’s reputation drives on having extensive experience with a wide range of bond issues

C. Economies of scale: Market preference for a small number of rating to facilitate rating comparability and efficiency

Three dominant players

European market share rating agencies

The dominant status of the Top 3 CRAs is a result of:

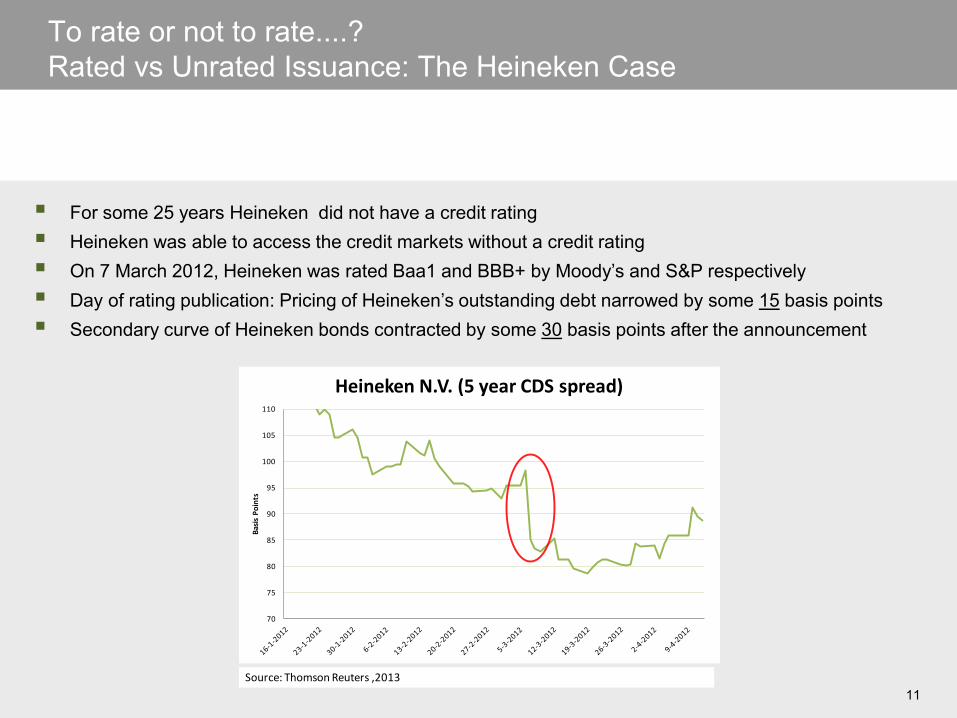

To rate or not to rate....?Rated vs Unrated Issuance: The Heineken Case

11

70

75

80

85

90

95

100

105

110

Ba

sis

Po

ints

Heineken N.V. (5 year CDS spread)

Source: Thomson Reuters ,2013

� For some 25 years Heineken did not have a credit rating� Heineken was able to access the credit markets without a credit rating� On 7 March 2012, Heineken was rated Baa1 and BBB+ by Moody’s and S&P respectively� Day of rating publication: Pricing of Heineken’s outstanding debt narrowed by some 15 basis points� Secondary curve of Heineken bonds contracted by some 30 basis points after the announcement

Selection of rating agenciesTwo rating norm

12

The Two-rating norm � Large and frequent bond issuers mostly obtain multiple credit ratings� Market participants assume that two credit ratings provide additional information� A dual rating facilitates rating-based regulation on a min two-rating condition

A combination of Moody’s and S&P is the preferred standard:� Highest perceived reputation� Provide most standardized investment benchmark � Fitch typically functions as a “third opinion” for large bond issues

Rating agency remunerationRating fees

13

� Example of rating fees based on EUR500M debt issuance in CRA fee structure (2014):

� Standard fee schedule, limited room for negotiation

� Commercial and analyst function strictly separated

Fee schedule 2014 S&P Moody's Fitch

Initial Rating Fee € 54,000 € 30,000 € 66,000

Issuance Fees € 275,000 € 292,500 € 287,500

Surveillance Fee € 53,000 € 75,000 € 66,000

Total Fees € 382,000 € 397,500 € 419,500

Ratings in European Real Estate Sector

14

Observations:

� S&P rates most investment grade European RE

companies in its portfolio (17 ratings)

� Eight companies are single rated by S&P, three are single

rated by Fitch and none are single rated by Moody’s

� In case of dual rating the rating outcome of Moody’s tends

to be one notch lower (split rating) compared to the other

two rating agencies

� VRF’s most direct peer company Deutsche Annington

(Vonovia) only has a single rating by S&P

� The largest European RE companies in terms of issuance

(Unibail, Klepierre, Gecina & Vonovia) are all rated by S&P

Rated RE Company Fitch Moody’s S&P

Atrium BBB- - BBB-

Befimmo - - BBB

British Land BBB+ - -

Citycon

Baa3 BBB-

Cofinimmo - - BBB-

Corio - Baa2 BBB+

Derwent London PLC - - BBB

Deutsche Annington - - BBB

Fonciere des Region - - BBB-

Gecina - Baa2 BBB

Global Switch BBB Baa3 BBB

Goodman European Logistics

Baa3 BBB

Hammerson BBB+ Baa2 -

ICADE - - BBB+

Klepierre - - BBB+

Mercialys - - BBB

PSP Swiss BBB+ - -

Prologis European Properties II - Baa3 BBB

Segro BBB+ - -

Societe Fonciere Lyonnaise - - BBB-

Unibail-Rodamco A - A

Ratings by top 3 agencies in the European real estate sector

Role of the rating advisor

15

� Expertise

� Pre-analysis, applying rating methodology

� Relieving the work load

� Running the process

� Sounding the rating agencies

� Information intermediary

� Capital structuring advice

� Support for annual surveillance

• Notification to rating agencies

• Introductory Meetings

• Potential clarification of issues requested by rating agencies

• Collection of information

• Preparation of Management Presentation

• Management Presentation Meetings

• The rating agencies present their decisions to management of Issuers

• Proceed to public announcement if satisfied, otherwise appeal

WEEK 1-2Preparation

WEEK 2-7Execution

WEEK 8Rating

Meetings

WEEK 9-11Follow Up

Rat

ing

Pro

cess

Ind

icat

ive

Tim

etab

le WEEK 12Rating

Conclusion

Preparation for Rating Meetings

Rating Agency Committee Meeting

Rating AgencyMeetings

Proceed

Rating Assignment

Announcement of Rating

Appeal meeting

Request Rating:Agency assigns

industry rating relationship and

analyst team

Proceed

Selection of a Rating Advisor

Analysis of Potential Rating Outcome

Yes

YesNo

Indicative time line rating process

Initial rating process...min. 12 weeks

S&P methodology VRF rating assessment (high level)

I. VRF Business Risk Profile: • RE industry is classified as a 'low risk' industry• VRF has a 'strong/satisfactory' competitive advantage

profile

II. VRF Financial Risk Profile - Key credit metrics: • Debt service capacity: EBITDA to Interest coverage (ICR)• Leverage: Debt to total of Debt and Equity

Intermediate

Significant

Modest

1,8x

2,0x

2,2x

2,4x

2,6x

2,8x

3,0x

3,2x

3,4x

3,6x

3,8x

4,0x

2013E 2014F 2015F

EBITDA / Interest

Fixed charge cover (x)

Intermediate

Significant

Modest30%

40%

50%

60%

2013E 2014F 2015F

Debt / Debt + Equity

Debt / Debt + Equity

V

RF

Bu

sin

ess r

isk

pro

file

VRF Financial risk profile

Minimal Modest Intermediate Significant Aggressive

Highly

leveraged

Excellent AAA/AA+ AA A+/A A- BBB BBB-/BB+

Strong AA/AA- A+/A A-/BBB+ BBB BB+ BB

Satisfactory A/A- BBB+ BBB /BBB- BBB-/BB+ BB B+

Fair BBB/BBB- BBB- BB+ BB BB- B

Weak BB+ BB+ BB BB- B+ B/B-

Vulnerable BB- BB- BB-/B+ B+ B B-

S&P methodology: Vesteda credit profile

CONSIDERATONS AND KEY TAKEAWAYS5

Credit ratingPossibly added value at a price

19

Obtaining a credit rating implies:

� Restriction of flexibility for changing financial strategy and leverage policy

� Additional risk management aspect: the rating downgrade

� Cost of discipline and transparency

� Two ratings reduce dependency but:

• Risk split-rating

• Increased costs

• Time consuming

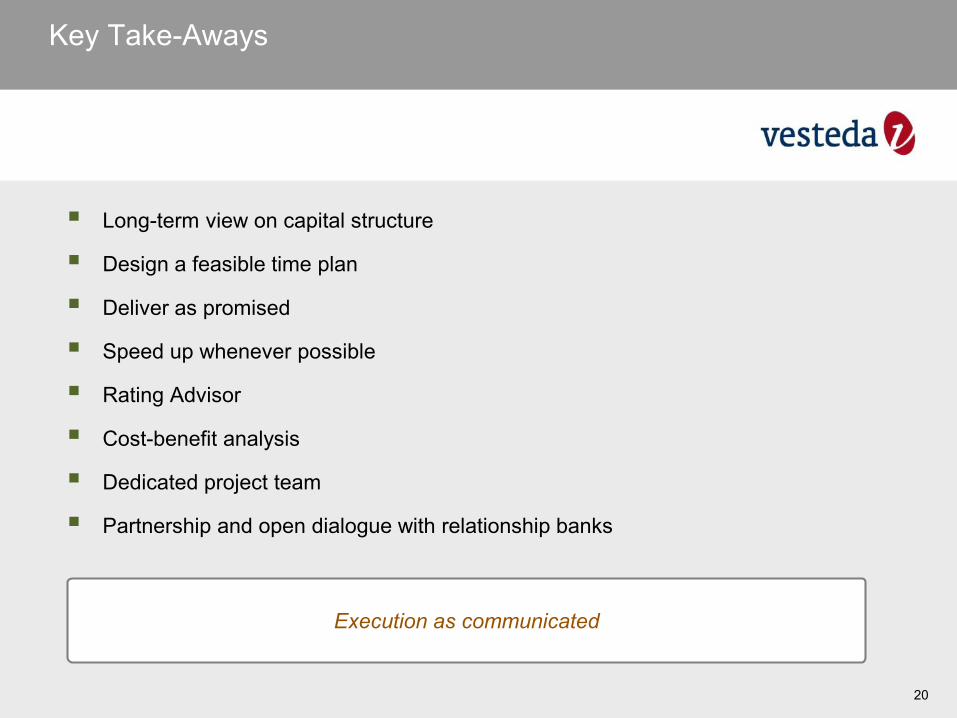

Key Take-Aways

� Long-term view on capital structure

� Design a feasible time plan

� Deliver as promised

� Speed up whenever possible

� Rating Advisor

� Cost-benefit analysis

� Dedicated project team

� Partnership and open dialogue with relationship banks

20

Execution as communicated

21