Embed Size (px)

Citation preview

Ghana WT/TPR/S/194Page 44

IV. TRADE POLICIES BY SECTOR

(1) INTRODUCTION

1. Agriculture remains the backbone of Ghana's economy. Cocoa is the dominant cash crop and single most important export product; its output has increased strongly over the past years. The Ghana Cocoa Board has monopoly rights over cocoa exportation. Other cash crops include oil palm, cotton, and coconut. The production of food crops, predominantly on a smallholder basis, has increased in recent years, but is still characterized by low productivity. Forestry and logging account for some 4% of GDP, but are important in terms of merchandise exports. Fisheries also contribute some 4% to GDP, but production is mainly for the national market. The average tariff on agriculture products (major division 1 of ISIC Rev.2) is 15.7%, with maximum tariffs of 20%.

2. The contribution of mining and quarrying to GDP has fallen below 5%, but gold remains Ghana's second most important export product. Other minerals include diamonds, which are mostly produced by small-scale mining operators, bauxite, and manganese. New legislation on the mining subsector entered into force in 2006. Mining rights are subject to fees and royalties; in addition, the state acquires a 10% stake in each mining company at no cost. Mining and quarrying products face an average tariff of 11.2%.

3. Manufacturing activities centre around the processing of agricultural goods, but also include the production of textiles, pharmaceuticals, and electronics. The average tariff on manufacturing products (major division 3 of ISIC Rev.2) is 12.6%; Ghana's tariff displays marked escalation for subsectors such as food and beverages, textiles and apparel, chemicals, and non-metallic products. The resultant high effective protection negatively affects the competitiveness of these products. Activities in the energy subsector remain dominated by state-owned enterprises.

4. Ghana has traditionally been a net importer of services. New legislation has entered into force in the insurance and banking subsectors. Growth rates have been particularly high in transport and communications, while tourism has emerged as an important generator of foreign exchange. Ghana's specific commitments under the GATS cover several service areas, including tourism, financial services, and telecommunications. State-owned enterprises play an important role in postal services and telecommunications; in addition, Ghana's two main commercial seaports are state-owned.

(2) AGRICULTURE, FORESTRY, AND FISHERIES

(i) Overview

5. Ghana's agriculture sector is important in terms of contribution to GDP, employment, and export earnings (Chapter I(1)). The recent good performance of the sector has resulted entirely from strongly growing cocoa production; the GDP shares of other agricultural subsectors have remained either constant (forestry) or have even decreased (fishing, livestock, and other crops). Agriculture is predominantly based on smallholder, familial exploitation, with rudimentary technology for the production of some 80% of total output. It is estimated that over 2.7 million households operate a farm or keep livestock.1 In general, Ghana is a net exporter of agricultural products (Chapter I(3)(i)).

6. The Ministry of Food and Agriculture (MOFA) is responsible for formulating policies in the sector. In line with the Government's overall economic policy and development goals, the main objectives are: food security; production of agricultural raw materials for industry, and agricultural

1 Ministry of Food and Agriculture (2007).

WT/TPR/S/194 Trade Policy ReviewPage 45

commodities for export; and efficient input supply, output processing, and marketing.2 In addition, the Government's objective is to transform Ghana into a leading agri-industrial nation by 2015.

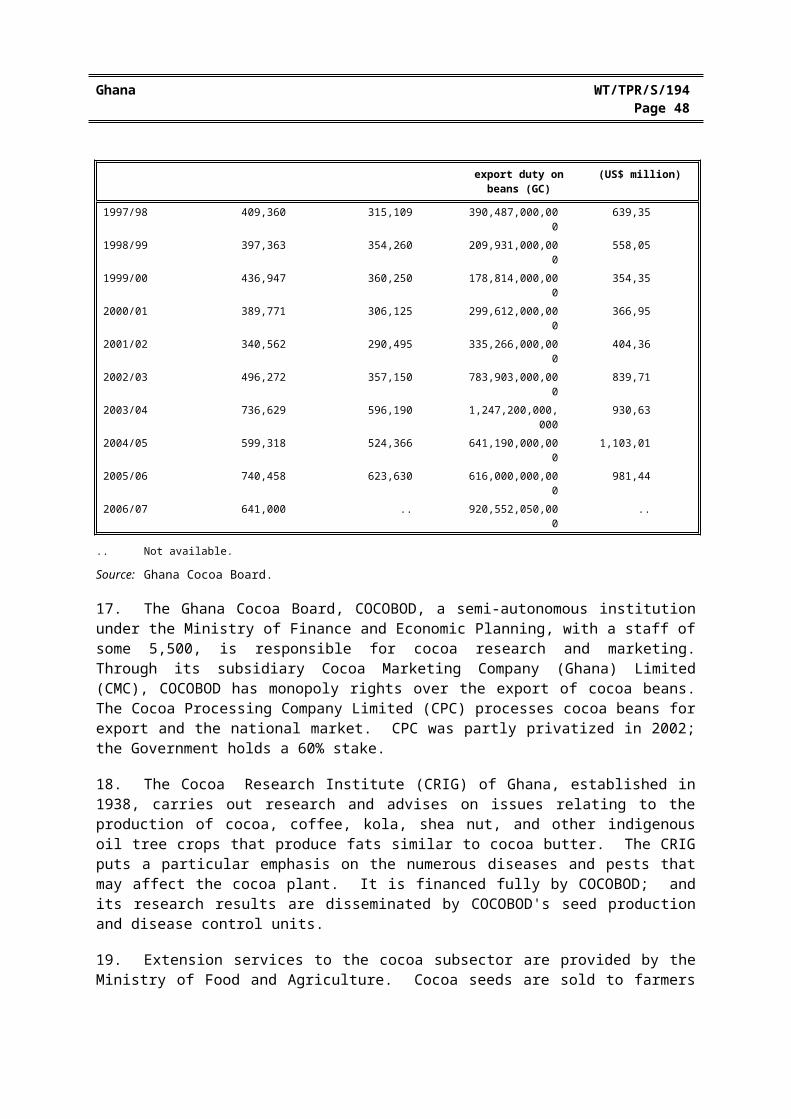

7. Specific objectives and strategies are laid down in the Revised Food and Agricultural Sector Development Policy (FASDEP II).3 The main areas for policy intervention in the sector, as outlined by FASDEP II are: (i) infrastructural development to provide enhanced marketing opportunities, in particular through the construction of feeder roads and storage facilities, and the improvement of irrigation; (ii) the provision of appropriate technology through agricultural research and development; and (iii) the provision of public extension services.

8. Total public expenditure for agriculture was GC 632 billion in 2006, including GC 343 billion of donor support. Ghana's last notification to the WTO Committee on Agriculture, submitted in 2001 indicated that it was not granting export subsidies to agricultural products.4

9. The tariff is the main trade policy instrument in the agriculture sector. The average applied MFN tariff on agriculture products (major division 1 of ISIC Rev.2) is 15.7% (Table AIV.1). Average MFN tariffs are relatively high on meat (20%), live plants (20%), and dairy products (19.5%); while they are lower on oil seeds and oleaginous fruits (9.4%), and fish and fishery products (11.1%). Machinery, plant, apparatus, and spare parts for agricultural purposes are exempt from the payment of import tariffs and value-added tax. In the Uruguay Round, Ghana bound all agricultural tariffs, mainly at a final ceiling rate of 99%; a bound rate of 40% was set on live poultry, milk and cream, wheat, and oil cake, while the rate on tea was bound at 50%.

10. All imports of live plants and animals require a permit issued by the MOFA. SPS measures are under the responsibility of the Directorates of Plant Protection and Regulatory Services, and of Veterinary Services of the MOFA (Chapter III(2)(vi)(b)).

11. Agricultural research is undertaken by numerous public institutions. The Animal Research Institute aims to provide solutions to problems in the livestock industry in Ghana, and advises on livestock policy matters. The Crops Research Institute focuses on breeding and production technologies, crop protection, and water management, mainly in relation to maize, rice, and legumes. Agricultural research is also undertaken by the Oil Palm Research Institute, the Savannah Agricultural Research Institute, the Food Research Institute, the Plant Genetic Resources Centre, the Water Research Institute, and the Soil Research Institute. All these institutions are grouped under the Council for Scientific and Industrial Research (CSIR) and are required to generate at least 30% of their operational budget.

12. About 30% of Ghana's total land area is under cultivation. Much of the agricultural land is "stool land", owned by communal or customary authorities. This may deter investments in agricultural land and limit the availability of credit to farmers due to the lack of collateral. A national land policy and a land administration project, both launched in 1999, attempt to capture the problems associated with land ownership, tenure, and development. New legislation on land administration is also under preparation. As established by the Constitution, foreigners are not allowed to own land in Ghana. However, they may lease land for renewable periods of up to 50 years.

2 Ministry of Food and Agriculture (2002) and (2007).3 Ministry of Food and Agriculture (2007). The initial Food and Agricultural Sector Development

Policy was formulated in 2002.4 WTO document G/AG/N/GHA/2, 21 August 2001.

Ghana WT/TPR/S/194Page 46

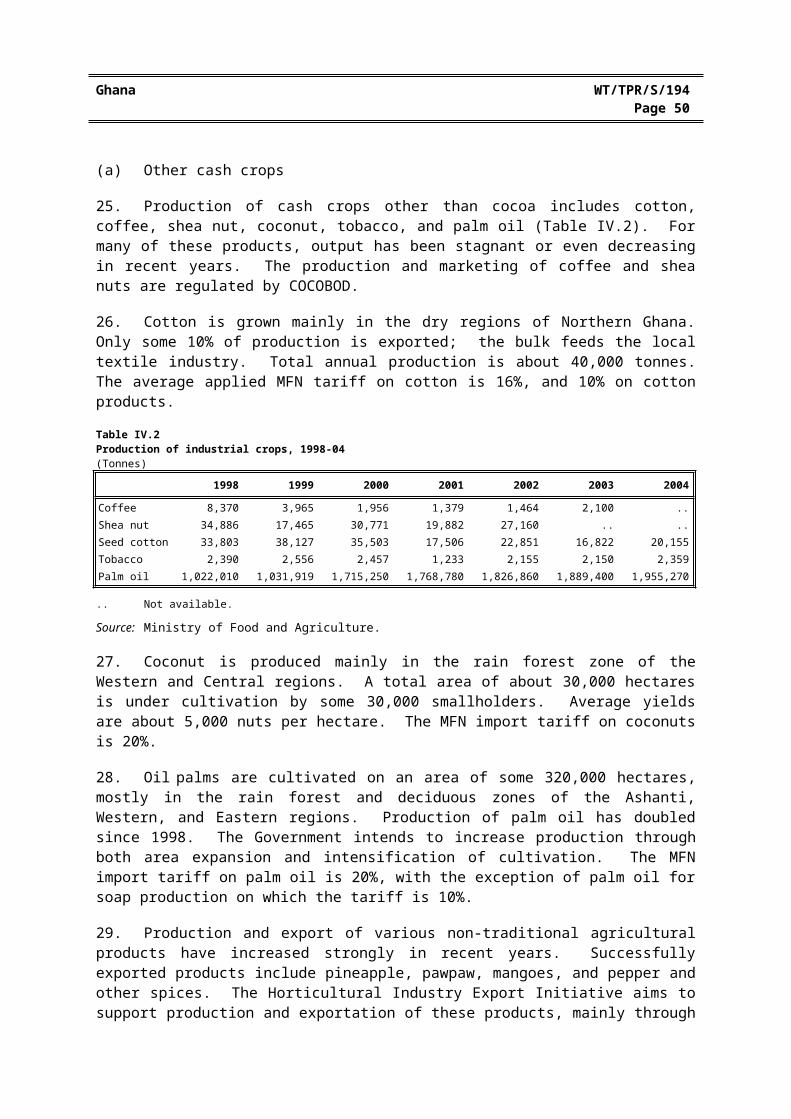

13. Together with other Members, Ghana submitted a negotiation proposal on agriculture in 2003.5 The proposal calls for an exemption of tariff reduction commitments for poor and highly indebted (IDA-only) countries, and guaranteed access to a new special safeguard mechanism for all agricultural products to address emergency situations deriving from import surges and steep price drops.

14. Emergency reserve stocks of maize and rice, which had been managed by private companies under supervision of the National Strategic Buffer Stock, were dissolved in 2005. Since then, the Government encourages the private sector to hold sufficient stocks.

(ii) Key subsectors

(a) Cocoa

15. Cocoa is Ghana's dominant cash crop and single most important export product. In 2006, exports of cocoa butter, powder, beans, paste, and waste totalled US$1,241 million, equivalent to more than 33% of Ghana's merchandise exports. The contribution of cocoa production and marketing to GDP was 8.5% in 2006, up from 4.9% in 1998. The EC is the main export destination for cocoa produced in Ghana.

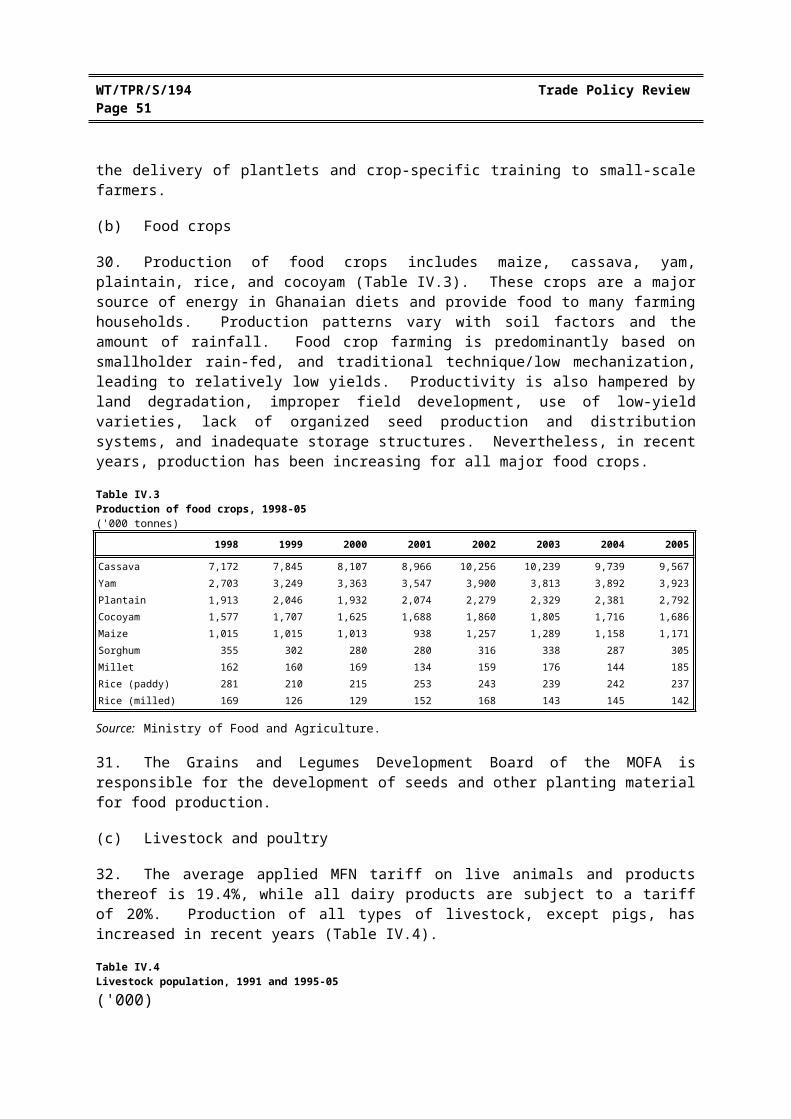

16. Cocoa is cultivated on some 1.6 million hectares in Southern and Central Ghana. About three quarters of output is produced by some 700,000 small-scale farms. Improved agronomic practices and mass spraying have been key factors in boosting cocoa production, leading to record outputs in 2003/04 and 2005/06 (Table IV.1). Fluctuations in cocoa output have mainly been caused by irregular rainfalls and various diseases.

Table IV.1Production and exports of cocoa, 1997-07(Tonnes)

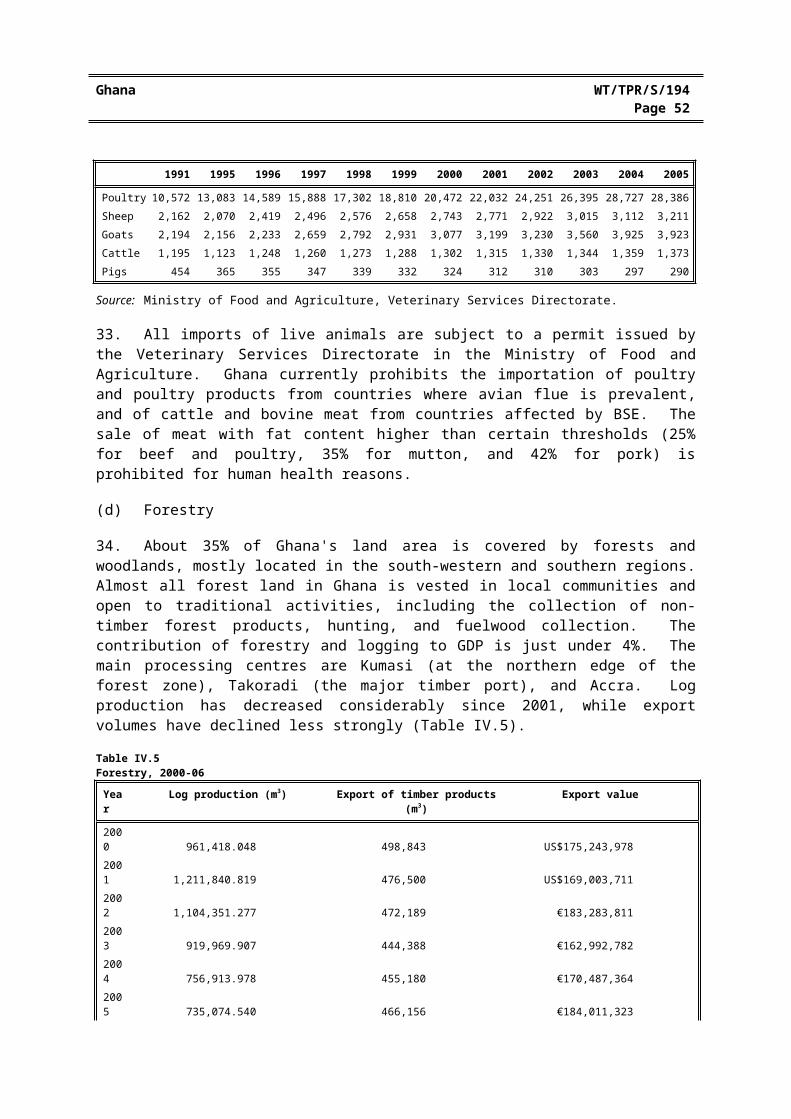

Production Exports Revenue from export duty on beans (GC)

F.o.b. value(US$ million)

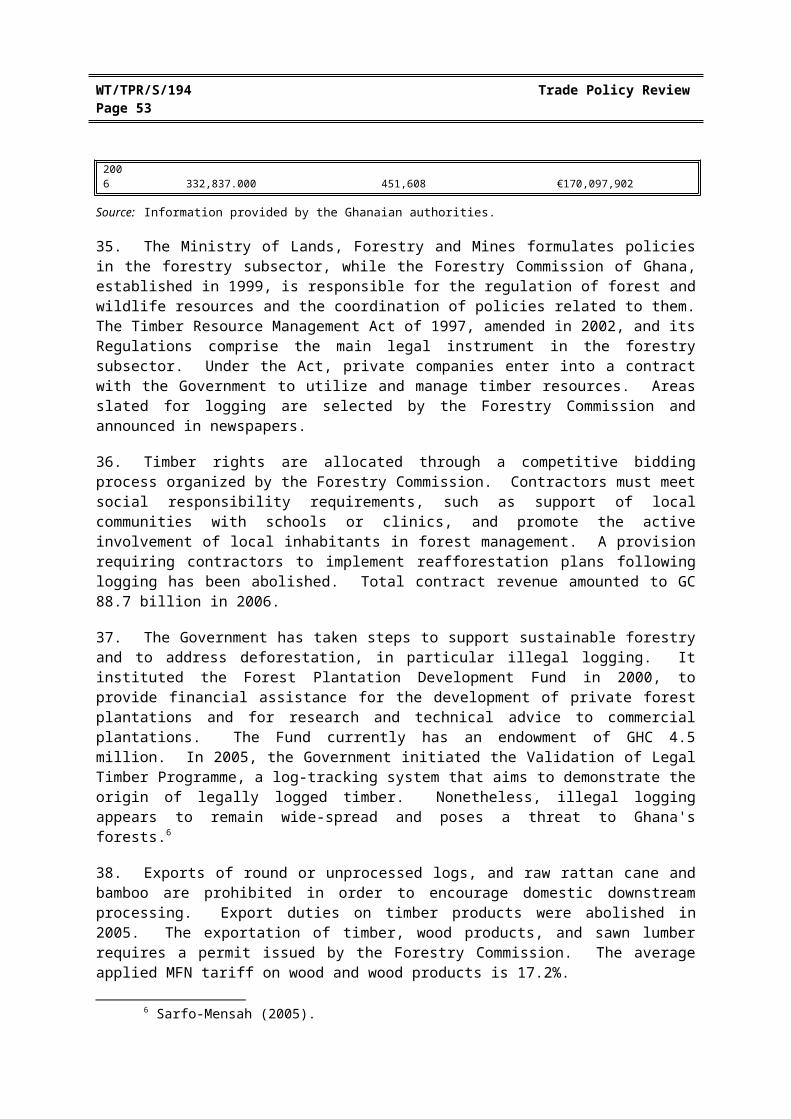

1997/98 409,360 315,109 390,487,000,000 639,351998/99 397,363 354,260 209,931,000,000 558,051999/00 436,947 360,250 178,814,000,000 354,352000/01 389,771 306,125 299,612,000,000 366,952001/02 340,562 290,495 335,266,000,000 404,362002/03 496,272 357,150 783,903,000,000 839,712003/04 736,629 596,190 1,247,200,000,000 930,632004/05 599,318 524,366 641,190,000,000 1,103,012005/06 740,458 623,630 616,000,000,000 981,442006/07 641,000 .. 920,552,050,000 ..

.. Not available.

Source: Ghana Cocoa Board.

17. The Ghana Cocoa Board, COCOBOD, a semi-autonomous institution under the Ministry of Finance and Economic Planning, with a staff of some 5,500, is responsible for cocoa research and marketing. Through its subsidiary Cocoa Marketing Company (Ghana) Limited (CMC), COCOBOD has monopoly rights over the export of cocoa beans. The Cocoa Processing Company Limited (CPC) processes cocoa beans for export and the national market. CPC was partly privatized in 2002; the Government holds a 60% stake.

5 WTO document TN/AG/GEN/5, 29 July 2003.

WT/TPR/S/194 Trade Policy ReviewPage 47

18. The Cocoa Research Institute (CRIG) of Ghana, established in 1938, carries out research and advises on issues relating to the production of cocoa, coffee, kola, shea nut, and other indigenous oil tree crops that produce fats similar to cocoa butter. The CRIG puts a particular emphasis on the numerous diseases and pests that may affect the cocoa plant. It is financed fully by COCOBOD; and its research results are disseminated by COCOBOD's seed production and disease control units.

19. Extension services to the cocoa subsector are provided by the Ministry of Food and Agriculture. Cocoa seeds are sold to farmers by COCOBOD's seed production unit at subsidized prices. Cocoa farmers and producers are exempt from income tax.

20. Only licensed buying companies (LBCs) may engage in internal trade and marketing of cocoa. In October 2000, the government liberalized exports of cocoa, allowing LBCs also to engage in the exportation of cocoa, but this policy was discontinued in 2007. LBC status is granted by COCOBOD; licences have to be renewed annually and are subject to a nominal fee. There are currently 19 LBCs. They purchase cocoa directly from farmers on behalf of COCOBOD and bag it for delivery to COCOBOD at designated take-over centres, on a commission basis. From the centres, CMC takes over the cocoa for export or further processing. The producer price of cocoa is determined by the Producer Price Review Committee (PPRC). Membership of the PPRC includes representatives of cocoa farmers, LBCs, CMC, COCOBOD, the Bank of Ghana, and the Ministry of Finance and Economic Planning.

21. There are five companies engaged in processing cocoa into butter, liquor, cake, and powder, with a combined processing capacity of some 253,000 tonnes. The Government's medium-term objective is to process at least 40% of the cocoa output locally. According to the authorities, tariff escalation in major export markets is a major impediment to domestic processing of cocoa.

22. Ghana imposes a 20% import tariff on cocoa and cocoa products. Cocoa exports are subject to taxes and repatriation of export revenue and its conversion into local currency. The tax rate on exports of cocoa beans is determined annually by the Minster of Finance and Economic Planning; for the crop year 2007/08, it is 11.1% of the f.o.b. price. Government revenue derived from the tax is used entirely to finance COCOBOD's activities: it depends on exports and the tax rate in place, and has varied strongly over the recent years (Table IV.1).

23. All exports of cocoa beans require a fumigation and quality assurance issued by COCOBOD's quality control division (QCD). The QCD fumigates every consignment of cocoa prior to shipment; it also disinfests cocoa storage facilities when deemed necessary. Once quality-graded and fumigated, cocoa may bear the label "Ghana cocoa".

24. Ghana is a member of the International Cocoa Organization.

(a) Other cash crops

25. Production of cash crops other than cocoa includes cotton, coffee, shea nut, coconut, tobacco, and palm oil (Table IV.2). For many of these products, output has been stagnant or even decreasing in recent years. The production and marketing of coffee and shea nuts are regulated by COCOBOD.

26. Cotton is grown mainly in the dry regions of Northern Ghana. Only some 10% of production is exported; the bulk feeds the local textile industry. Total annual production is about 40,000 tonnes. The average applied MFN tariff on cotton is 16%, and 10% on cotton products.

Ghana WT/TPR/S/194Page 48

Table IV.2Production of industrial crops, 1998-04(Tonnes)

1998 1999 2000 2001 2002 2003 2004

Coffee 8,370 3,965 1,956 1,379 1,464 2,100 .. Shea nut 34,886 17,465 30,771 19,882 27,160 .. .. Seed cotton 33,803 38,127 35,503 17,506 22,851 16,822 20,155 Tobacco 2,390 2,556 2,457 1,233 2,155 2,150 2,359 Palm oil 1,022,010 1,031,919 1,715,250 1,768,780 1,826,860 1,889,400 1,955,270

.. Not available.

Source: Ministry of Food and Agriculture.

27. Coconut is produced mainly in the rain forest zone of the Western and Central regions. A total area of about 30,000 hectares is under cultivation by some 30,000 smallholders. Average yields are about 5,000 nuts per hectare. The MFN import tariff on coconuts is 20%.

28. Oil palms are cultivated on an area of some 320,000 hectares, mostly in the rain forest and deciduous zones of the Ashanti, Western, and Eastern regions. Production of palm oil has doubled since 1998. The Government intends to increase production through both area expansion and intensification of cultivation. The MFN import tariff on palm oil is 20%, with the exception of palm oil for soap production on which the tariff is 10%.

29. Production and export of various non-traditional agricultural products have increased strongly in recent years. Successfully exported products include pineapple, pawpaw, mangoes, and pepper and other spices. The Horticultural Industry Export Initiative aims to support production and exportation of these products, mainly through the delivery of plantlets and crop-specific training to small-scale farmers.

(b) Food crops

30. Production of food crops includes maize, cassava, yam, plaintain, rice, and cocoyam (Table IV.3). These crops are a major source of energy in Ghanaian diets and provide food to many farming households. Production patterns vary with soil factors and the amount of rainfall. Food crop farming is predominantly based on smallholder rain-fed, and traditional technique/low mechanization, leading to relatively low yields. Productivity is also hampered by land degradation, improper field development, use of low-yield varieties, lack of organized seed production and distribution systems, and inadequate storage structures. Nevertheless, in recent years, production has been increasing for all major food crops.

Table IV.3Production of food crops, 1998-05('000 tonnes)

1998 1999 2000 2001 2002 2003 2004 2005

Cassava 7,172 7,845 8,107 8,966 10,256 10,239 9,739 9,567 Yam 2,703 3,249 3,363 3,547 3,900 3,813 3,892 3,923 Plantain 1,913 2,046 1,932 2,074 2,279 2,329 2,381 2,792 Cocoyam 1,577 1,707 1,625 1,688 1,860 1,805 1,716 1,686 Maize 1,015 1,015 1,013 938 1,257 1,289 1,158 1,171 Sorghum 355 302 280 280 316 338 287 305 Millet 162 160 169 134 159 176 144 185 Rice (paddy) 281 210 215 253 243 239 242 237 Rice (milled) 169 126 129 152 168 143 145 142

Source: Ministry of Food and Agriculture.

WT/TPR/S/194 Trade Policy ReviewPage 49

31. The Grains and Legumes Development Board of the MOFA is responsible for the development of seeds and other planting material for food production.

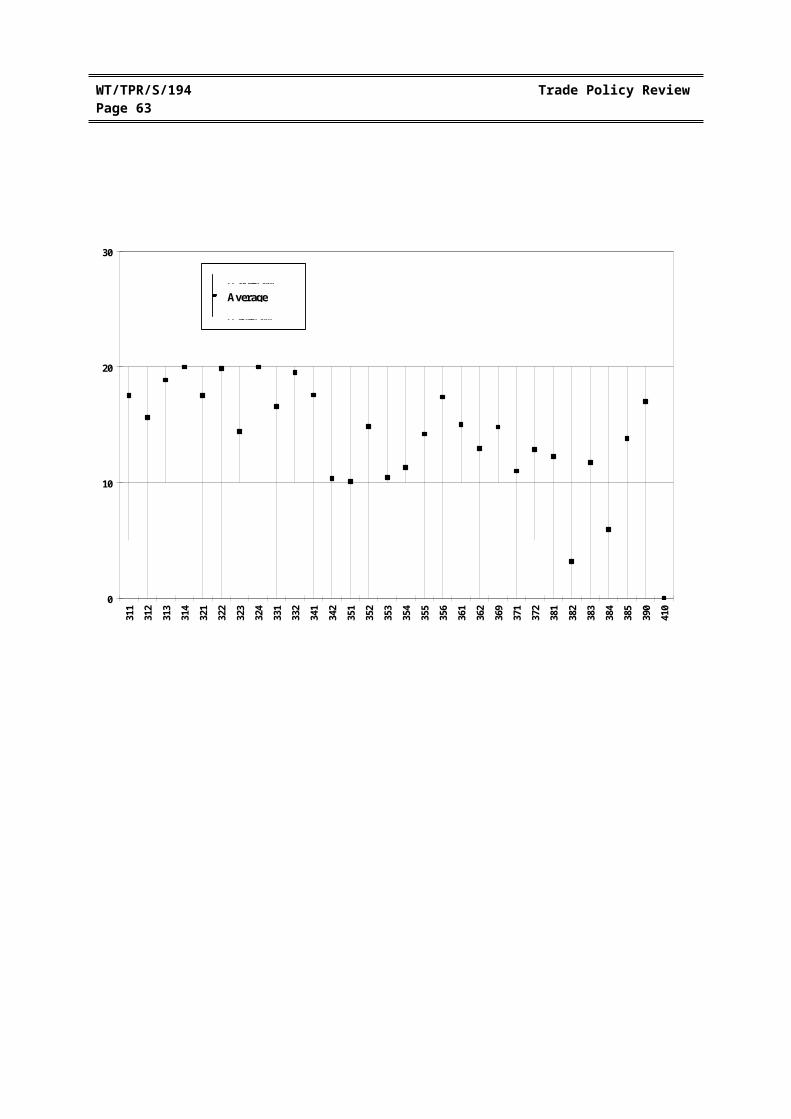

(c) Livestock and poultry

32. The average applied MFN tariff on live animals and products thereof is 19.4%, while all dairy products are subject to a tariff of 20%. Production of all types of livestock, except pigs, has increased in recent years (Table IV.4).

Table IV.4Livestock population, 1991 and 1995-05('000)

1991 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Poultry 10,572 13,083 14,589 15,888 17,302 18,810 20,472 22,032 24,251 26,395 28,727 28,386 Sheep 2,162 2,070 2,419 2,496 2,576 2,658 2,743 2,771 2,922 3,015 3,112 3,211 Goats 2,194 2,156 2,233 2,659 2,792 2,931 3,077 3,199 3,230 3,560 3,925 3,923 Cattle 1,195 1,123 1,248 1,260 1,273 1,288 1,302 1,315 1,330 1,344 1,359 1,373 Pigs 454 365 355 347 339 332 324 312 310 303 297 290

Source: Ministry of Food and Agriculture, Veterinary Services Directorate.

33. All imports of live animals are subject to a permit issued by the Veterinary Services Directorate in the Ministry of Food and Agriculture. Ghana currently prohibits the importation of poultry and poultry products from countries where avian flue is prevalent, and of cattle and bovine meat from countries affected by BSE. The sale of meat with fat content higher than certain thresholds (25% for beef and poultry, 35% for mutton, and 42% for pork) is prohibited for human health reasons.

(d) Forestry

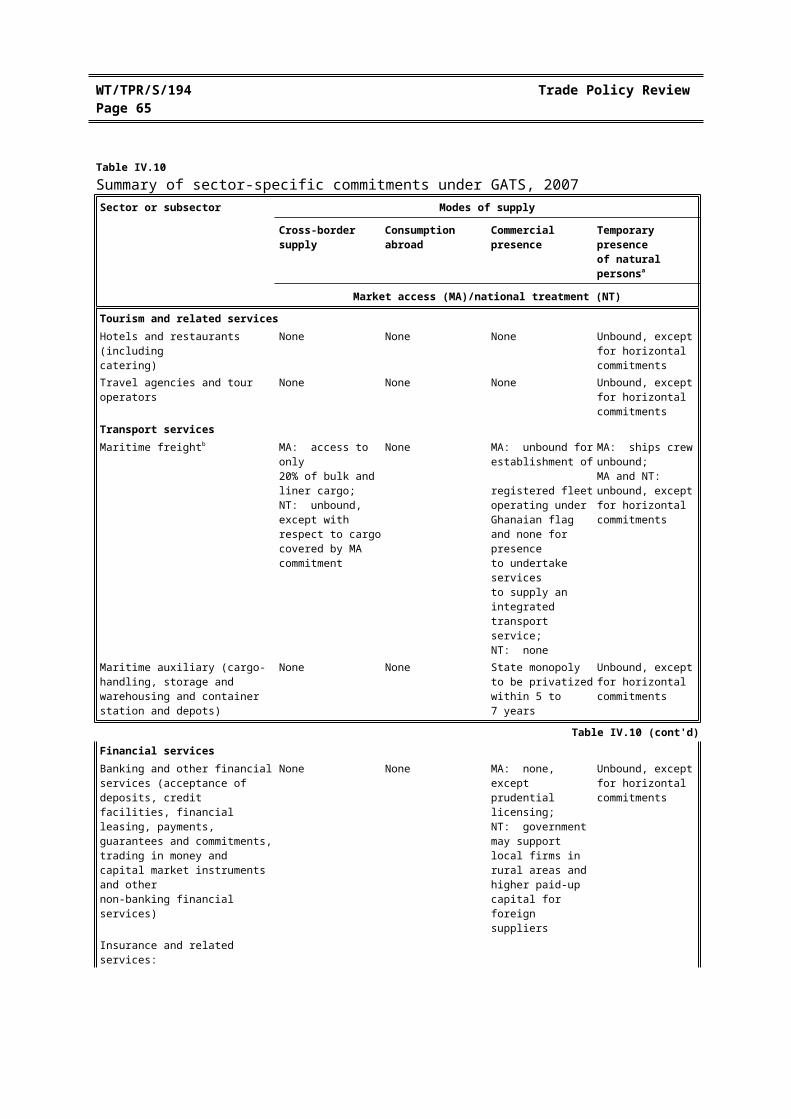

34. About 35% of Ghana's land area is covered by forests and woodlands, mostly located in the south-western and southern regions. Almost all forest land in Ghana is vested in local communities and open to traditional activities, including the collection of non-timber forest products, hunting, and fuelwood collection. The contribution of forestry and logging to GDP is just under 4%. The main processing centres are Kumasi (at the northern edge of the forest zone), Takoradi (the major timber port), and Accra. Log production has decreased considerably since 2001, while export volumes have declined less strongly (Table IV.5).

Table IV.5Forestry, 2000-06

Year Log production (m3) Export of timber products (m3) Export value

2000 961,418.048 498,843 US$175,243,9782001 1,211,840.819 476,500 US$169,003,7112002 1,104,351.277 472,189 €183,283,8112003 919,969.907 444,388 €162,992,7822004 756,913.978 455,180 €170,487,3642005 735,074.540 466,156 €184,011,3232006 332,837.000 451,608 €170,097,902

Source: Information provided by the Ghanaian authorities.

35. The Ministry of Lands, Forestry and Mines formulates policies in the forestry subsector, while the Forestry Commission of Ghana, established in 1999, is responsible for the regulation of forest and wildlife resources and the coordination of policies related to them. The Timber Resource

Ghana WT/TPR/S/194Page 50

Management Act of 1997, amended in 2002, and its Regulations comprise the main legal instrument in the forestry subsector. Under the Act, private companies enter into a contract with the Government to utilize and manage timber resources. Areas slated for logging are selected by the Forestry Commission and announced in newspapers.

36. Timber rights are allocated through a competitive bidding process organized by the Forestry Commission. Contractors must meet social responsibility requirements, such as support of local communities with schools or clinics, and promote the active involvement of local inhabitants in forest management. A provision requiring contractors to implement reafforestation plans following logging has been abolished. Total contract revenue amounted to GC 88.7 billion in 2006.

37. The Government has taken steps to support sustainable forestry and to address deforestation, in particular illegal logging. It instituted the Forest Plantation Development Fund in 2000, to provide financial assistance for the development of private forest plantations and for research and technical advice to commercial plantations. The Fund currently has an endowment of GHC 4.5 million. In 2005, the Government initiated the Validation of Legal Timber Programme, a log-tracking system that aims to demonstrate the origin of legally logged timber. Nonetheless, illegal logging appears to remain wide-spread and poses a threat to Ghana's forests.6

38. Exports of round or unprocessed logs, and raw rattan cane and bamboo are prohibited in order to encourage domestic downstream processing. Export duties on timber products were abolished in 2005. The exportation of timber, wood products, and sawn lumber requires a permit issued by the Forestry Commission. The average applied MFN tariff on wood and wood products is 17.2%.

(e) Fisheries

39. With its 540 kilometres of maritime coastline and 8,520 km2 of inland lakes and rivers, Ghana has a variety of investment opportunities in the fisheries subsector. The subsector comprises marine fisheries, freshwater fisheries, and fish farming. The contribution of fisheries to GDP is 4%, down from 5% in 1998. Total annual fish production has been over 400,000 tonnes in most years (Table IV.6). The average applied MFN tariff on fish and fishery products is 11.1%.

Table IV.6Annual fish production, 1992 and 1995-04(Tonnes)

1992 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Marine 371,000 336,000 378,000 396,000 376,000 333,000 380,000 366,000 290,000 331,412 352,405 Inland 57,000 65,500 74,000 72,000 76,000 89,000 88,000 88,000 88,000 75,450 79,000 Total 428,000 401,500 452,000 468,000 452,900 422,000 468,000 454,000 378,000 406,862 431,405

Source: Ministry of Food and Agriculture, Fisheries Directorate.

40. Artisanal, in-shore, and industrial methods are used in marine fishing. There are nearly 13,000 dugout canoes and about 123,000 fishermen in marine artisanal fisheries; they mainly exploit small pelagic fish. The in-shore fleet consists of some 230 locally built wooden-hulled trawlers that operate from eight landing sites. The industrial fleet is made up of large-sized trawlers, tuna bait boats (pole-and-line) and tuna purse seiners operating from the ports of Tema and Takoradi.

41. The fresh water fishing industry is located mainly along the shores of the Volta Lake, which is the source of about 90% of inland fish production. The main species caught are tilapia, catfish, and

6 Sarfo-Mensah (2005).

WT/TPR/S/194 Trade Policy ReviewPage 51

Volta perch. Inland fishery employs about 80,000 fishers and some 20,000 fish processors. Inland fishery is mainly artisanal: around 17,500 planked canoes are used.

42. Fish farming is relatively new in Ghana, but may represent an option for increasing fish production. There are about 1,000 fish farmers working on over 2,000 ponds with a total surface area of 350 hectares. Both extensive and semi-intensive cultures are practiced, involving tilapia and catfish species. Total annual production is estimated at about 1,200 tonnes.

43. The Fisheries Act of 2002 is the main legal instrument governing the subsector. As established by the Act, ownership of artisanal, semi-industrial or industrial fishing operations is restricted to Ghanaian citizens. Nonetheless, foreigners may engage in fish farming and own up to 50% of vessels engaged in tuna fishing. All operations must be licensed by the Ministry of Fisheries.7

The Fishery Product Regulations (2006) lay down general hygiene provisions for fish and fishery products, including requirements for landing and unloading fishery products, quality assurance, and production conditions.8 Fisheries companies are eligible for the tax and tariff concessions provided in the GIPC Law of 1994 (Chapter III(2)(iii)(d)).

44. The main challenge for fishing is the lack of adequate cold storage facilities at landing sites.9

In addition, weak extension services in some areas, and inadequate supply of good quality fingerlings, pose a problem for fish farming.

(3) MINING AND ENERGY

(i) Mining

45. Ghana is a major producer of gold, diamonds, bauxite, and manganese, with exports of mineral products averaging 35% of total merchandise export earnings (Chapter I(3)(i)). While gold production has been stagnating since 2000, diamond, bauxite, and manganese production has increased significantly (Table IV.7). Silver is also produced, as a by-product of gold, as well as salt. Mining activities are concentrated in the Western, Ashanti, and Central regions. The average applied MFN tariff on mining products (major division 2 of ISIC Rev.2) is 11.4%; the tariff on gold and diamonds is 20%.

Table IV.7Production of major minerals, 1998-05

1998 1999 2000 2001 2002 2003 2004 2005a

Gold (tonnes) 73.75 81.12 76.43 74.07 69.57 70.75 63.20 66.53Diamonds (carats) 822,563 681,576 878,011 1,090,072 963,493 904,089 905,344 1,065,923Bauxite (tonnes) 341,120 355,263 503,825 678,449 683,564 494,716 498,060 606,700Manganese (tonnes) 384,463 638,937 895,749 1,076,666 1,135,828 1,509,432 1,597,085 1,719,589

a Provisional.

Source: Ghana Minerals Commission.

46. After cocoa, gold is Ghana's second most important export product. Gold exports in 2006 amounted to US$1,327 million. Despite stagnating production levels, export income has increased due to rising international gold prices. There are seven operational gold mines in Ghana.

7 Ghana Investment Promotion Centre (2006).8 WTO document G/TBT/N/GHA//4, 11 February 2007.9 Ghana Investment Promotion Centre (2006).

Ghana WT/TPR/S/194Page 52

47. Ghana produces about one million carats of diamonds annually from alluvial deposits; about 85% of its production is industrial diamonds. The bulk of diamond production is by small and medium-scale mines.10 The only large-scale producer, Ghana Consolidated Diamonds, stopped operations in mid-2007. Diamond exports in 2006 amounted to US$31 million.

48. The Ministry of Lands, Forestry and Mines is responsible for formulating policies, while the Ghana Minerals Commission (MINCOM) is the regulatory and main promotional institution. The Environmental Protection Agency is responsible for the formulation of environmental policies, including pollution standards and waste discharge. Pursuant to Article 257(6) of the Constitution, all minerals in their natural state are the property of the Republic of Ghana. The Minerals and Mining Act of 2006 is the main legal instrument in the minerals subsector; regulations under the Act are at the drafting stage (October 2007). The Government has the right of pre-emption over all minerals raised. However, this right has not been used in practice. The Ghana Chamber of Mines represents the collective interests of some 30 major companies involved in mineral exploration, production, and processing. Moreover, it is estimated that some 500,000 people are engaged in small-scale mining.

49. The Minerals and Mining Act provides for various types of mineral rights (Table IV.8). In addition, there are licences for quarrying, salt winning, and sand winning. Non-Ghanaians may not engage in small-scale mining; the minimum investment for foreign companies is US$10 million. Any transfer of mining rights is subject to the approval of the Ministry. A total area of some 30,000 km2, equivalent to about 13% of Ghana's land area, is covered by mineral licences.

Table IV.8Types of mineral rights, 2007

Reconnaissance licence

Prospectinglicence

Mininglease

Restrictedlease

Small scalemininga

Purpose Regional exploration not including drilling and excavation

Search for minerals and evaluation

Extraction of minerals

Building and industrial minerals

Extraction of minerals

Area Blocks of 21 hectares, not exceeding 5,000 contiguous blocks

Not exceeding 750 contiguous blocks

Not exceeding 300 contiguous blocks

.. ..

Duration 12 months, renewable 3 years, renewable with reduction of area to not less than half

30 years or less depending on mine life, renewable

15 years or less depending on mine life, renewable

5 years, renewable

.. Not available.

a Granted to Ghanaians only.

Source: Ghana Minerals Commission.

50. A revised schedule of mineral right fees entered into force in 2005. Royalties vary from 3% to 6% of the gross value of minerals produced. Through royalties, corporate taxes, and pay-as-you-earn payments, the mining subsector contributes significantly to government revenue. In 2005, the subsector's contribution was GC 679.7 billion, equivalent to 11% of income collected by the Internal Revenue Service.

51. Exports of mineral ores require a permit issued by the Minerals Commission. Exports of gold are subject to a foreign exchange surrender and conversion requirement, administered by the Bank of Ghana.

10 Bermúdez-Lugo (2005).

WT/TPR/S/194 Trade Policy ReviewPage 53

52. The state-owned Precious Minerals Marketing Corporation buys gold and diamonds from small-scale miners and resells jewellery and gold products for export. The company, which does not enjoy any specific rights, has an annual turnover of about US$30 million.

53. Mining is the most important target sector for foreign direct investment in Ghana (Chapter I(3)(ii)). Cumulative FDI inflows into the mining sector between 2000 and 2005 amounted to US$2,823 million. There is compulsory state participation in the mineral subsector, whereby the Government acquires a 10% equity in all companies at no cost. The Government also has the option of purchasing an additional 20% equity at a "fair market price", but this has never been exercised.

54. AngloAshanti Gold, Ghana's single largest company and one of the world's leading gold producers, accounts for more than one third of national gold production. The state has reduced its share in this company to 3.4%. Through foreign acquisitions and investments by AngloAshanti Gold, Ghana has become an important mining investor in other African countries such as Guinea, Tanzania, and Zimbabwe.

(ii) Energy

(a) Electricity

55. An estimated 45% to 47% of Ghana's population has access to electricity, including 15% to 17% of the rural population.11 Per capita consumption of electrical energy was estimated at 358 kWh in 2004. Ghana's total installed generation capacity is about 1,800 MW (Table IV.9).12 This comprises the Akosombo hydro-electric power plant (1,040 MW), the Takoradi thermal power station (550 MW), and the Kpong hydro-electric power plant (160 MW). In addition, the Osagyefo power plant is expected to start operations in 2008, adding another 125 MW in March and 60 MW in December. About half of electricity production is consumed by households; commercial and industrial consumers account for the rest. In most years, Ghana is a net exporter of electrical energy. However, low water levels at the Volta dam frequently lead to supply shortages and electricity cuts; and some 25% of electricity production is accounted for by technical and commercial system losses.

56. Electricity, transmission, and distribution are under state monopoly. The state-owned Volta River Authority (VRA), which owns the Akosombo and Kpong dams, is the only major producer of electrical energy in Ghana; it is also responsible for electricity transmission. There are also various smaller private-owned generators producing electricity only for auto-consumption. These independent power producers are not currently permitted to sell electricity, but plans to allow this are under consideration. The VRA was also responsible for power transmission until 2005; since then, the state-owned Ghana Grid Company (GRIDCO) has been in charge of electricity transmission with a view to unbundling the VRA's operations. Two state-owned companies, Electricity Company of Ghana (ECG), and the Northern Electricity Department (NED, a subsidiary of the VRA) are responsible for distribution: ECG delivers power to customers in southern Ghana, and NED supplies northern Ghana.

57. The Ministry of Energy is responsible for formulating policies in the energy subsector. It also supervises the operations of the Ghana National Petroleum Corporation, the Tema Oil Refinery, the Ghana Oil Company, the Bulk Oil Storage and Transportation Company, VRA, GRIDCO, and the Electricity Company of Ghana, all of which are state-owned. The Public Utilities Regulatory Commission (PURC) is an autonomous agency that sets transmission and consumer prices, while the Energy Commission licences operators.

11 University of Ghana, Institute of Statistical, Social, and Economic Research (2005).12 This figure does not include off-grid power plants used e.g. by large mining companies.

Ghana WT/TPR/S/194Page 54

Table IV.9Electricity, 1998-04

1998 1999 2000 2001 2002 2003 2004

Installed electricity generation capacity (MW)Hydro 1,072 1,072 948 971 994 1,002 1,180Thermal 360 360 470 580 580 580 550Total 1,432 1,432 1,418 1,551 1,574 1,582 1,730Electricity generation (GWh)Hydro 3,830.32 5,168.72 6,608.70 6,608.54 5,035.85 3,885.20 5,280.90Thermal 1,182.40 755.59 613.02 1,250.55 2,259.55 201.16 757.84Total 5,012.70 5,924.30 7,222.70 7,859.10 7,295.50 5,900.40 6,038.70Trade in electricity (GWh)Exports 1,386.46 2,254.12 2,896.82 2,866.93 2,674.32 854.23 675.26Imports 573 1,031 864 462 1,146 940 878

Source: Energy Commission of Ghana.

58. The Government has as an objective to increase electrification, particularly in rural areas; it plans to extend electrification to all communities by 2020. Given the high costs of long-distance transmission lines to serve remote rural communities, achieving this objective will require substantial investment in renewable and off-grid electricity.

59. Ghana's electricity grid is connected to Côte-d'Ivoire, Togo, and Benin through high voltage transmission lines, and to Burkina Faso through a low voltage distribution network. A high voltage transmission connection to Burkina Faso is under development. There are also efforts at the ECOWAS level to create a West African power pool, including a regional regulatory body and common standards for maintaining grid stability.13

(b) Petroleum and gas

60. Oil and natural gas production in Ghana remains limited14; most petroleum products are imported, mainly from Nigeria. Various deep-water discoveries of oil and natural gas have been made in the Gulf of Guinea in recent years and have led to an increase in exploration activities. 15 A major offshore oil discovery in Western Ghana was announced by the Kosmos Energy and Tullow Oil groups in June 2007.16 However, these exploration activities have not yet led to major investments in production facilities.

61. Under the Petroleum Law of 1994, the state-owned Ghana National Petroleum Corporation (GNPC) is responsible for procurement, storage, and bulk distribution of petroleum products to retail companies. Ghana's only refinery is the state-owned Tema Oil Refinery, which has an operating capacity of 45,000 barrels per day and runs on crude oil. In March 2006, the private company Arabian Gulf Oil Ltd. announced the construction of a second refinery, with a planned capacity of 200,000 barrels a day.

62. Ghana maintains a fuel subsidy with a view to redistributing income and smoothing out price fluctuations. Total petroleum subsidies amounted to 2.2% of GDP in 2004, 0.4% in 2005, and 1.6% in 2006. According to the authorities, the National Petroleum Authority regularly reviews the formula underlying the subsidy.

13 University of Ghana, Institute of Statistical, Social, and Economic Research (2005).14 The only operational production platform is located in the Saltpond oilfields in Central Ghana.

Production reached its peak in 1978, with some 4,800 barrels per day.15 Ministry of Energy (2003).16 Ghana Home Page, "Jubilation over oil discovery", 19 June 2007. Viewed at:

http://www.ghanaweb.com/GhanaHomePage/NewsArchive/artikel.php?ID=125826 [5 September 2007]

WT/TPR/S/194 Trade Policy ReviewPage 55

63. Thirteen categories of petroleum products are subject to specific tariffs (Chapter III(2)(iii)(a)). Hydrocarbons are subject to export taxes of US$0.09 per litre on aviation turbine kerosene and US$0.03 per litre on gas oil.

64. The Government holds strategic fuel reserves through the state-owned Bulk Oil Storage and Transportation Company. The reserve stocks, consisting of a two-week supply of gas oil and gasoline, are to be used in the event of an interruption in the normal supply of these products.

65. The West African Gas Pipeline Project (WAGP) seeks to supply gas from fields in the Western Delta of Nigeria to Ghana, Benin, and Togo. The Government of Ghana, through the VRA, holds a 16.3% share in the project. Operation of the 678 kilometre pipeline was originally planned to start in December 2006, but, due to construction delays, it is not yet operational. Entry into operation has been rescheduled for April 2008.

(4) MANUFACTURING

66. Ghana has a relatively broad and diverse industrial base, covering aluminium smelting, timber and agricultural processing, brewing, cement manufacture, oil refining, textiles, electronics, and pharmaceuticals. Nonetheless, the contribution of the manufacturing sector to GDP remains modest (Chapter I(1)). In 2003, the year of the most recent industrial census, there were some 23,800 manufacturing companies in Ghana, with nearly 117,000 employees.

67. The average applied MFN tariff on manufactured products (Major division 3 of ISIC Rev.2) is 12.6% (Chart IV.1 and Table AIV.1). Average tariffs are particularly high on footwear (20%), apparel (19.9%), furniture (19.5%), and beverages (18.9%); and low on transport equipment (5.9%) and non-electrical machinery (3.2%). Promotion of agri-industries is one of Ghana's key objectives. However, high prices of certain locally produced agricultural commodities and high tariffs on imports of their equivalents do not favour this objective. Moreover, pronounced tariff escalation, and thereby high effective protection, in industries, including food and beverages, textiles and apparel, chemicals, and non-metallic products, negatively affects the international competitiveness of these goods (Chapter III(2)(iii)(a)).

68. After mining, manufacturing is the main target sector for foreign investors in Ghana. Accumulated foreign investment in manufacturing amounted to US$2.3 billion between 2001 and 2006, generating some 16,400 jobs.17 Nearly 90% of foreign investment projects in manufacturing are located in the Greater Accra area. Specific difficulties encountered by the manufacturing sector include power cuts, and access to and conditions of financing.18

69. The publicly funded Institute for Industrial Research undertakes applied research on industrial process and product technology development; one of its main objectives is to improve agricultural processing machines. The Institute is required to generate at least 30% of its operational budget. Private-sector manufacturers' interests are represented by the Association of Ghana Industries.

70. Manufacturing companies are eligible for the tax and tariff concessions provided by the GIPC Law of 1994 and the benefits provided by the Free Zone Law (Chapter III(2)(iii)(d) and III(3)(v)). In addition, companies located outside Accra and Tema can benefit from locational tax incentives (Chapter III(4)(i)(a)). Upon the request of exporters, the Ghana Standards Board issues a "Mark of Conformity" certifying that goods are compliant with national quality, safety, or health standards.

17 Ghana Investment Promotion Centre (2007).18 Association of Ghana Industries (2007).

Ghana WT/TPR/S/194Page 56

0

10

20

30

311

312

313

314

321

322

323

324

331

332

341

342

351

352

353

354

355

356

361

362

369

371

372

381

382

383

384

385

390

410

Chart IV.1Tariff protection in the manufacturing sector, 2007

Percent

WTO Secretariat calculations, based on data provided by the Ghanaian authorities.

AverageMaximum

Minimum

International Standard Industrial Classification, Revision 2

Source :

311312313314321322323

324331332

341342351352353

Description

Food productionOther food products and animal feedsBeveragesTobacco manufacturingTextilesManufacture of wearing apparel, except footwearLeather products, except footwear and wearing apparelFootwear, except vulcanized rubber or plastic footwearWood and wood products, except furnitureManufacture of furniture and fixtures, except primarily of metalPaper and paper productsPrinting, publishing and allied industriesIndustrial chemicalsOther chemicals, including pharmaceuticalPetroleum refineries

DescriptionManufacture of miscellaneous petroleum and coalproductsManufacture of rubber products n.e.s.Manufacture of plastic products n.e.s.Pottery, china and earthenwareManufacture of glass and glass productsOther non-metallic mineral productsIron and steel basic industriesNon-ferrous metal basic industriesFabricated metal products, except machinery and equipmentNon-electrical machinery including computersElectrical machinery apparatus, appliances and suppliesTransport equipmentProfessional and scientific equipmentOther manufacturing industriesElectrical energy

354

355356361362369371372381

382383

384385390410

WT/TPR/S/194 Trade Policy ReviewPage 57

71. The divestiture programme launched in 1988 has significantly reduced the number of state-owned enterprises; GIHOC Distilleries is the only manufacturing company that remains fully owned by the state; plans to list the company on the stock exchange are under consideration. In addition, the state holds minority shares of between 10% and 40% in PSC Tema Shipyard, Ghana Textile Printing, Bridal Trust International Paints, and GIHOC Pharmaceuticals.

72. Together with other African Members, Ghana submitted two negotiation proposals on market access for non-agricultural goods in 2003.19 The submissions called for the application of a simple and transparent formula that would substantially reduce tariff peaks and tariff escalation and address the special needs of developing countries.

(5) SERVICES

(i) Overview

73. Services constitute a major sector of the economy in terms of contribution to GDP and to employment (Chapter I(1)). Public administration accounts for the largest part, followed by trade, restaurants, and hotels. Individual contributions by other categories of services remain low.

74. Balance-of-payments data indicate that Ghana has traditionally been a net importer of services (Chapter I(3)(i)). In 2005, it exported services worth US$ 1,066 million, while imports of services amounted to US$1,264 million.

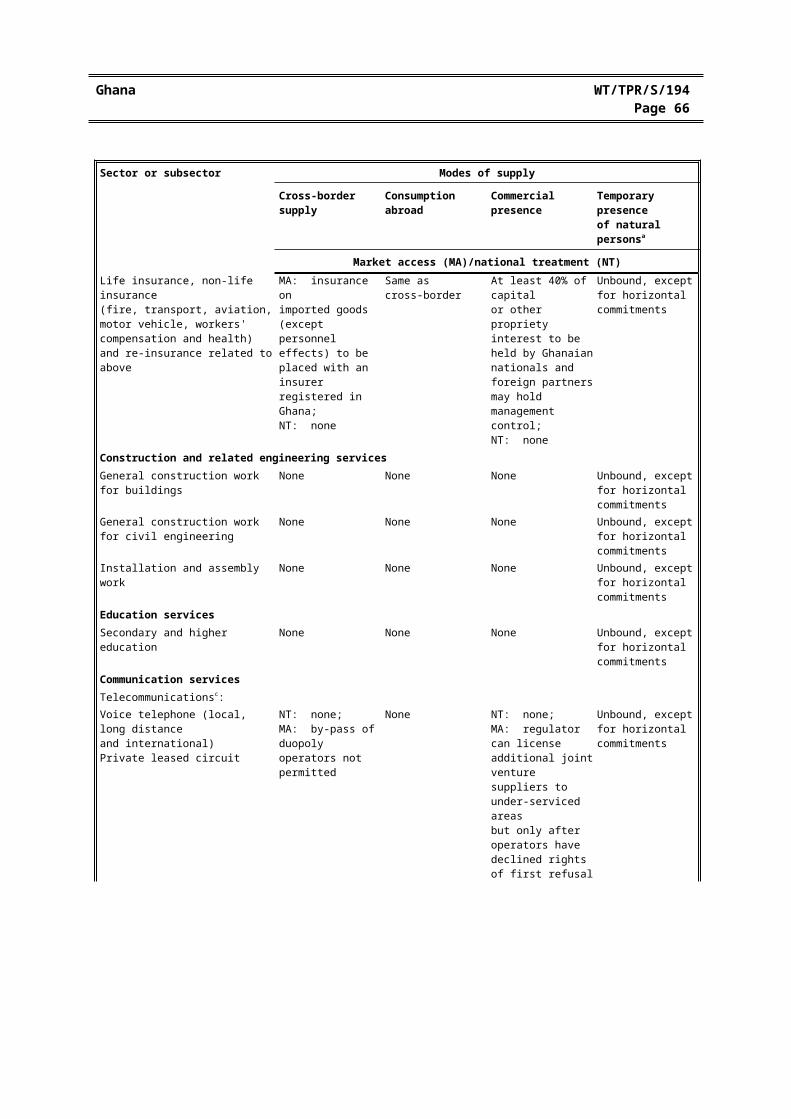

75. Ghana's specific commitments under the GATS cover various subsectors in tourism and related services; maritime transport; construction; education; financial services; and telecommunications (Table IV.10). Ghana has accepted the Fourth and Fifth Protocols to the GATS.

Table IV.10Summary of sector-specific commitments under GATS, 2007Sector or subsector Modes of supply

Cross-bordersupply

Consumptionabroad

Commercialpresence

Temporary presenceof natural personsa

Market access (MA)/national treatment (NT)

Tourism and related servicesHotels and restaurants (including catering)

None None None Unbound, except for horizontal commitments

Travel agencies and tour operators None None None Unbound, except for horizontal commitments

Transport servicesMaritime freightb MA: access to only

20% of bulk and liner cargo;NT: unbound, except with respect to cargo covered by MA commitment

None MA: unbound for establishment of registered fleetoperating under Ghanaian flag and none for presenceto undertake servicesto supply an integrated transport service; NT: none

MA: ships crew unbound; MA and NT: unbound, except for horizontal commitments

Maritime auxiliary (cargo-handling, storage and warehousing and container station and depots)

None None State monopoly to be privatized within 5 to 7 years

Unbound, except for horizontal commitments

Table IV.10 (cont'd)

19 WTO documents TN/MA/W/27, 18 February 2003; and TN/MA/W/40, 11 August 2003.

Ghana WT/TPR/S/194Page 58

Sector or subsector Modes of supply

Cross-bordersupply

Consumptionabroad

Commercialpresence

Temporary presenceof natural personsa

Market access (MA)/national treatment (NT)Financial servicesBanking and other financial services (acceptance of deposits, credit facilities, financial leasing, payments, guarantees and commitments, trading in money andcapital market instruments and othernon-banking financial services)

None None MA: none, except prudential licensing;NT: government may support local firms in rural areas and higher paid-up capital for foreign suppliers

Unbound, except for horizontal commitments

Insurance and related services: Life insurance, non-life insurance(fire, transport, aviation, motor vehicle, workers' compensation and health)and re-insurance related to above

MA: insurance on imported goods(except personnel effects) to be placed with an insurerregistered in Ghana;NT: none

Same as cross-border

At least 40% of capitalor other proprietyinterest to be held by Ghanaian nationals and foreign partners may hold management control;NT: none

Unbound, except for horizontal commitments

Construction and related engineering servicesGeneral construction work for buildings None None None Unbound, except for

horizontal commitments

General construction work for civil engineering

None None None Unbound, except for horizontal commitments

Installation and assembly work None None None Unbound, except for horizontal commitments

Education servicesSecondary and higher education None None None Unbound, except for

horizontal commitments

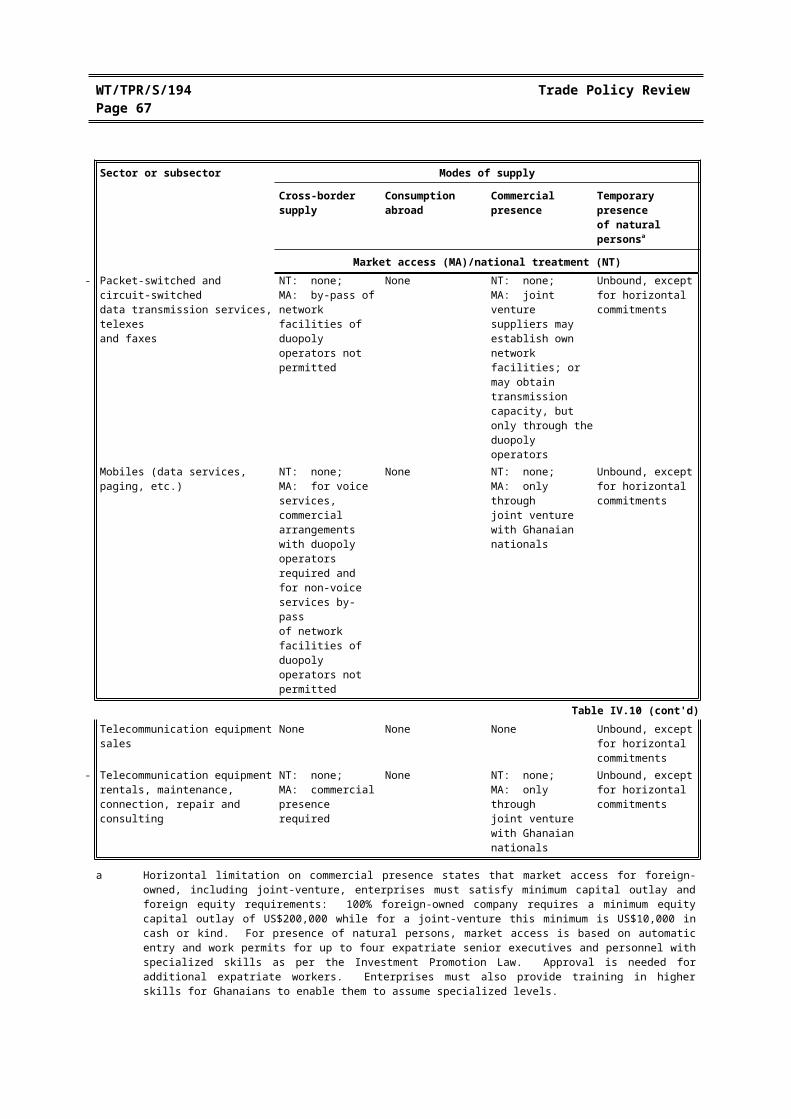

Communication servicesTelecommunicationsc: Voice telephone (local, long distanceand international) Private leased circuit

NT: none;MA: by-pass ofduopoly operators not permitted

None NT: none;MA: regulator can license additional joint venture suppliers to under-serviced areasbut only after operators have declined rights of first refusal

Unbound, except for horizontal commitments

Packet-switched and circuit-switcheddata transmission services, telexesand faxes

NT: none;MA: by-pass of network facilities of duopoly operators not permitted

None NT: none; MA: joint venture suppliers may establish own network facilities; or may obtain transmission capacity, but only through the duopoly operators

Unbound, except for horizontal commitments

Mobiles (data services, paging, etc.) NT: none;MA: for voiceservices, commercial arrangements with duopoly operators required and for non-voice services by-passof network facilities of duopoly operators not permitted

None NT: none;MA: only throughjoint venture with Ghanaian nationals

Unbound, except for horizontal commitments

Table IV.10 (cont'd)

WT/TPR/S/194 Trade Policy ReviewPage 59

Sector or subsector Modes of supply

Cross-bordersupply

Consumptionabroad

Commercialpresence

Temporary presenceof natural personsa

Market access (MA)/national treatment (NT)Telecommunication equipment sales None None None Unbound, except for

horizontal commitments

Telecommunication equipment rentals, maintenance, connection, repair and consulting

NT: none; MA: commercial presence required

None NT: none;MA: only throughjoint venture with Ghanaian nationals

Unbound, except for horizontal commitments

a Horizontal limitation on commercial presence states that market access for foreign-owned, including joint-venture, enterprises must satisfy minimum capital outlay and foreign equity requirements: 100% foreign-owned company requires a minimum equity capital outlay of US$200,000 while for a joint-venture this minimum is US$10,000 in cash or kind. For presence of natural persons, market access is based on automatic entry and work permits for up to four expatriate senior executives and personnel with specialized skills as per the Investment Promotion Law. Approval is needed for additional expatriate workers. Enterprises must also provide training in higher skills for Ghanaians to enable them to assume specialized levels.

b Ghana made an additional commitment to make available on reasonable and non-discriminatory conditions: pilotage, towing and tug assistance, provisioning, fuelling and watering, garbage collection and ballast waste disposal; port captain's services, navigation aids, and fire fighting and ambulance.

c Ghana accepted as additional commitments the regulatory framework outlined in the reference paper. It also listed as an additional commitment that the Government had granted exclusivity to the duopoly operators for five years, and that after this period it would conduct a review of its policy to determine whether to license additional suppliers of such services. This has taken place.

Source: WTO documents.

(ii) Financial services

(a) Banking

76. Ghana's GATS commitments on financial services cover various banking services, including acceptance of deposits, credit facilities, and leasing, and provide for no market-access or national-treatment limitations on cross-border trade and consumption abroad. The only market-access limitation on commercial presence is prudential licensing. National treatment is assured, except that the Government may support local financial institutions in rural areas and apply a higher paid-up capital requirement to foreign suppliers.

77. The Banking Supervision Department of the Bank of Ghana regulates and supervises the subsector. Rules for the establishment of a bank are laid down in the 2004 Banking Act. The minimum capital requirement for setting up a commercial bank is GHC 7 million for Ghanaians and foreigners alike. In the case of foreign ownership, at least 60% of the capital must be brought into Ghana in convertible currency. Applicants must pay a processing fee of GHC 2,000 and an annual licensing fee of GHC 5,000. Applications are subject to an economic needs test. The Act also provides for capital adequacy requirements and a new sanctions regime .

78. As at September 2007, 26 banks were operating in Ghana, of which 14 were foreign-owned and three were state-owned. In addition, there were 126 rural and community banks and 40 non-bank financial institutions. Total assets of the banks amounted to GC 56,276 billion as at end-March 2007, equivalent to 49% of GDP.

79. The ratio of non-performing loans in the banks' total loan portfolio has fallen in recent years, from 20.4% in March 2003 to 6.9% in March 2007.20 The solvency of the banking industry, as measured by the capital adequacy ratio, remains high; as at March 2007, it was at 16.9%, well above the statutory threshold of 10.0%.

20 Bank of Ghana (2007a).

Ghana WT/TPR/S/194Page 60

80. Interest rates are market-determined; the average inter-bank interest rate is currently 12.6%. The spread between deposit and lending rates remains considerable; in December 2006, the maximum saving deposit rate was 9%, while lending rates ranged between 15% and 33.5%.

(b) Insurance

81. The insurance industry is regulated by the National Insurance Commission (NIC), under the Insurance Act of 2006. All insurance companies and brokers must be registered with the NIC and be incorporated in Ghana. The 2006 Act abolished ownership limitations for foreigners in the insurance subsector. Insurance companies are not allowed to engage in any other business, including reinsurance. Moreover, the same company may not supply both life and non-life insurance services. Insurance is compulsory for (i) motor vehicles; (ii) commercial buildings under construction; and (iii) commercial buildings against collapse and natural disasters. The reinsurance arrangements of all direct insurers must be approved by the NIC. Until 2009, all direct insurance companies are obliged to reinsure 20% of their business with Ghana Reinsurance Company. Insurance and reinsurance companies are required to exhaust local capacity before having recourse to foreign-based companies.

82. The minimum capital requirement is equivalent to US$ 1 million for both life and non-life insurance companies. Premiums on motor vehicles are set by the NIC, while all other premiums are market-determined. New insurance products must be approved by the NIC. Ghanaians residing in Ghana may buy insurance abroad only if that type of insurance is not available in Ghana.

83. There are 25 insurance companies, 37 broking companies, and two reinsurance companies. In 2006, total gross premiums were GC 1.15 trillion for non-life insurance, GC 490 billion for life insurance, and GC 285 billion for reinsurance. State Insurance Company (SIC) and Ghana Reinsurance Company are fully state-owned; privatization of SIC through the stock exchange is under consideration. Foreign participation is still de facto limited in Ghana's insurance subsector.

(c) Capital markets

84. The Ghana Stock Exchange (GSE) began trading in corporate equities, bonds, and government securities in 1990. In January 2007, 32 companies were listed. Market capitalization at mid-2007 was around GHC 11,500 million, of which AngloGold Ashanti accounted for some 80%. Many Ghanaian subsidiaries of multinational companies are listed on the GSE.

85. Under the Securities Industry Law of 1993, the Securities and Exchange Commission oversees the GSE, sets listing requirements, and licenses dealers. Its commissioners are appointed by the President of Ghana. Share trading by non-resident foreigners is permitted without prior approval. However, the shares held by any single external resident in a listed company is limited to 10%, and the maximum level of foreign ownership for each firm is 75%.

86. Regulations on the operation of unit trusts and mutual funds, adopted in 2001, lay down operating conditions, reporting requirements and investment rules for various types of trusts and mutual funds.

(iii) Communication

(a) Telecommunication

87. Since Ghana's last TPR in 2001, the telecommunication network has continued to grow, with particularly strong expansion in the mobile market (Table IV.11). As a result, the teledensity was

WT/TPR/S/194 Trade Policy ReviewPage 61

over 27%.21 There are two operators of landline telephone services, Ghana Telecom and Westel. Westel currently deploys only 3,000 lines as against Ghana Telecom's 400,000 lines. Ghana Telecom is fully state-owned, but the Government is seeking an investor for 66.7% of its shares.22 Westel was fully state-owned until October 2007, when 75% of its shares were sold to a Kuwaiti investor. 23 There are five licensed mobile operators of which four (MTN, Tigo, OneTouch, and KASAPA) are providing mobile telephone services.

Table IV.11Telecommunication indicators, 2000-06

2000 2001 2002 2003 2004 2005 2006

Fixed telephones 206,000 249,000 270,000 288,000 372,000 323,000 400,000Mobile telephones 39,000 222,000 383,000 775,000 1,189,000 2,472,000 3,800,000Pay phones 3.291 4.487 4.995 4.995 8.846 11.314 ..

.. Not available.

Source: Ministry of Communication.

88. The Ministry of Communications is responsible for formulating telecom policies. The National Communication Authority (NCA), established in 1996, is in charge of regulating and monitoring the telecom market and issuing licences to operators. The Government formulated a National Telecommunications Policy in 2004; its main objectives are to promote universal access to telephone, internet, and multimedia services by 2010, and to achieve fully open, private, and competitive markets for all telecomm services.24 The Government also intends to increase the use of information and communication technologies, in particular through public investment in areas considered under-served.25

89. The National Communications Regulations of 2003 constitute the legal framework for the telecoms subsector. Enactment of an Electronic Communications Bill has been pending since 2005. The bill contains provisions on licensing, interconnection, and universal services.

90. Ghana endorsed the reference paper on regulatory principles and committed itself to reviewing its duopoly policy after five years to determine whether to license additional suppliers of basic telecommunication services. As a result of the review, the exclusivity licences of the two operators of landline telephone services ended in 2002. Since then, four new licences have been issued to telecom operators.

91. All operators in the telecommunication market require a licence issued by the NCA. Imports of communication equipment require a permit, also issued by the NCA. Individual tariffs are set by operators and subject to approval by the NCA; interconnection charges are negotiated between operators and are also subject to approval by the NCA. In case of disagreement, interconnection charges are set by the NCA.

21 Ministry of Communications (2007).22 A 30% share in Ghana Telecom had been held by a Malaysian investor who decided to withdraw

from the company for reasons of mismanagement.23 Afrique en ligne, "Une compagnie koweïtienne rachète Westel Ghana", 23 October 2007. Viewed at:

http://www.afriquenligne.fr/actualites/economie/une-compagnie-koweitienne-rachete-westel-ghana-2007102311147/ [25 October 2007.]

24 Ministry of Communications (2004).25 Republic of Ghana (2003).

Ghana WT/TPR/S/194Page 62

92. In order to promote universal access to telecommunication services, the Government instituted the Ghana Investment Fund for Telecommunications (GIFTEL) in 2004.26 GIFTEL's primary responsibility is to facilitate investment in information and communication technology in under-served areas; priority is given to projects that seek to increase basic rural connectivity and access to broadband services. To date, GIFTEL has supported the establishment of 77 community information centers and 44 common telecommunication facilities in under-served areas. GIFTEL's operations are financed by contributions from operators who must pay 1% of their net profit; additional resources may be allocated by Parliament. Projects identified by GIFTEL are announced publicly and allocated by open tender.

(b) Postal services

93. The state-owned Ghana Post Company (GPC) provides ordinary postal services throughout the country. As established by the Postal and Courier Services Regulatory Commission Act of 2003, the GPC has exclusive rights to convey letters, postcards, printed matters, and small parcels up to 100 g; all other areas are open to competition. The GPC has the obligation to deliver parcels and letters to any postal address in Ghana within a maximum of three working days (one and a half working days within major urban centers). Its tariffs must be approved by the Postal and Courier Services Regulatory Commission.

94. The GPC competes with private companies for express courier services. There are seven major private courier service providers in Ghana. In addition, various private transport companies are involved in these services. Courier service providers must be licensed by the Postal and Courier Services Regulatory Commission. With a view to addressing increased competition, the GPC has increased its activities in, inter alia, money transfers and sale of prepaid cards and commemorative stamps; establishment of a post bank is under consideration.

(iv) Transport

(a) Land transport

95. Ghana disposes of some 32,300 kilometres of roads, of which about 6,100 kilometres are paved. The Ghana Highway Authority is responsible for the administration, development, and maintenance of trunk roads and related facilities. A Road Sector Development Programme (RSDP) has been implemented by the Ministry of Roads and Transport and its agencies since 2002.

96. Transit traffic to Burkina Faso, Mali, and Niger increased strongly from some 29,000 tonnes in 1998 to over 1 million tonnes in 2003. This rise in transit traffic has come about mainly because of political instability in alternative transit corridors, but has also been further boosted by improvements in Ghana's port operations and hinterland connections as well as by faster clearance procedures for goods in transit.

97. Ghana's rail network comprises mainly a triangular 947 km narrow-gauge system linking Kumasi, Takoradi, and Accra-Tema. The main cargoes are bauxite and manganese. However, rail traffic accounts for only some 2% of freight and passengers land transport. Only parts of the system are operational, and trains from Accra to Kumasi have been suspended. An extension of the rail network to Burkina Faso is being explored.

98. Ghana Railways Corporation is fully state-owned. However, the Government has embarked on a programme to privatize the exploitation of its railways to improve services and efficiency. As

26 Ministry of Communications (2004).

WT/TPR/S/194 Trade Policy ReviewPage 63

part of the privatization efforts, the Ministry of Harbours and Railways has decided to grant a 20-year concession to a private company through a build, operate, and transfer (BOT) arrangement. The arrangement will leave the Government with ultimate control of the railways but operating responsibilities and delivery services will be transferred to the concessionaire, who will pay a fixed annual premium plus a percentage of the revenue.

(b) Air transport

99. Air transport policies in Ghana are formulated by the Ministry of Aviation. The Ghana Civil Aviation Authority (GCAA), a semi-autonomous government agency established in 1986, is responsible for regulating air transportation. In accordance with the Civil Aviation Act of 2004, GCAA's regulatory and management functions were split, transmitting all tasks related to airport management and development to the newly instituted Ghana Airports Company Limited.

100. Ghana is a signatory to the Yamoussoukro Declaration Concerning the Liberalization of Access to Air Transport Markets in Africa. In addition, it has signed bilateral air transport agreements with 47 other countries. These agreements normally cover the first four freedoms of the air: cabotage is restricted to domestic companies.

101. All international flights are handled by Accra's Kotoka Airport, which is served by 25 passenger and five cargo airlines, including international airlines. An expansion of the Kotoka airport was completed in 2003, upgrading its capacity to 2 million passengers per year. The Government hopes that the airport expansion will allow Kotoka to become a regional hub for West Africa. The number of passengers at Kotoko Airport increased to some 900,000 in 2006, up from 592,000 in 2000. There are also domestic airports in Kumasi, Tamale, and Sunyani, and various unpaved airstrips. However, domestic air transport carries less than 5% of total passengers, and thus remains of minor importance.

102. The state-owned company Ghana Airways was liquidated in 2004. Some of its assets were transferred to Ghana International Airlines (GIA), a joint-venture between the Government, which holds 70%, and a U.S.-based investor. The GIA was founded in October 2004 and began operations in 2005. Ghana International Airlines' fleet consists of two leased aircraft serving London.

(c) Water transport

103. The Ghana Ports and Harbour Authority (GPHA), a semi-autonomous agency under the Ministry of Harbours and Railways, owns Ghana's two commercial seaports, at Tema and Takoradi, and various fishing harbours. The two seaports handle over 85% of Ghana's exports and imports; in both ports, cargo handling has grown strongly in recent years (Table IV.12).

104. Port services prices are based on the GPHA's tariff, which must be approved by Government. In recent years, the GPHA's role has shifted from a port operator to a regulator, while the operation of port facilities has increasingly been taken over by private companies licensed by the GPHA; prices for activities such as stevedoring, freight forwarding or cargo clearance are market-determined.

105. The development of Ghana into a maritime hub and shipping gateway to West Africa is a major policy objective. Thus, the Government has initiated various projects to enhance the capacity and efficient operation of Ghana's ports. Planned or ongoing activities include: dredging the port at Tema from a depth of 9.6 meters to 11.5 meters; upgrading the 80 km route between the Tema port and Akosombo; and the construction of new bulk, container and multi-purpose berths at the harbour of Takoradi.

Ghana WT/TPR/S/194Page 64

Table IV.12Cargo traffic, 2000-06('000 tonnes)

2000 2001 2002 2003 2004 2005 2006

Port of TakoradiImportsTotal 1,143 1,151 1,130 1,364 1,455 1,565 1,478Liquid bulk 157 181 155 142 230 174 176Dry bulk 891 849 842 909 889 934 901General cargo 26 43 32 39 49 46 32Bagged cargo 5.7 6.8 20 186 208 327 268Containerized 62 70 70 84 77 83 86ExportsTotal 1,901 2,199 2,262 2,458 2,726 3,071 3,241Dry bulk 1,461 1,799 1,891 2,119 2,329 2,678 2,813Bagged cargo 70 34 13 34 41 27 65Containerized 271 281 294 250 304 324 319Forest products 99 85 64 55 52 40 41Total cargo 3,044 3,350 3,392 3,822 4,181 4,636 4,720

Port of TemaImportsTotal 5,308 5,379 6,020 6,553 7,264 7,959 6,561Liquid bulk 2,064 2,096 2,079 1,963 2,608 2,417 1,266Dry bulk 1,576 1,289 1,258 1,139 1,202 1,052 1,120General cargo 257 311 233 323 530 737 556Bagged cargo 493 724 1,024 1,112 737 1,069 627Containerized 916 958 1,425 1,997 2,185 2,683 2,990ExportsTotal 910 931 819 536 844 1,290 1,117Liquid bulk 291 335 248 215 356 385 152Dry bulk 37 34 38 52 64 51 44General cargo 162 157 159 45 59 108 122Bagged cargo 60 53 28 42 37 40 95Containerized 350 334 344 480 660 704 703Total cargo 6,218 6,310 6,839 7,389 8,108 9,250 7,678

Source: Ghana Ports and Harbours Authority.

106. The Ghana Shipping Act of 2004 governs the registration of ships, while the Ghana Maritime Security Act of 2004 regulates maritime safety and security issues. The Ghana Shipping Act restricts maritime cabotage to domestic companies. The Ghana Maritime Authority (GMA), established in 2004, is responsible for monitoring and regulating activities in the maritime industry. It maintains a shipping register, which contains 298 fishing vessels, 23 cargo vessels, and 43 small craft. Foreigners must form joint-ventures with Ghanaians in order to register. However, the authorities are examining this requirement with a view to allowing more foreigners to register and operate ships in Ghana.

107. The state-owned Volta Lake Transport Company operates cargo and passenger transport services on the Volta Lake and its tributaries. There are plans to create an inland port at Boankra (near Kumasi), with storage facilities for cargo heading to neighbouring landlocked countries.

WT/TPR/S/194 Trade Policy ReviewPage 65

(v) Tourism

108. Tourism is the fourth-largest foreign-exchange earner in Ghana after gold, cocoa, and remittances. Employment in tourism-related activities was estimated at 47,000 direct jobs and 115,000 indirect jobs in 2004.27

109. Ghana's attractions include beaches, festivals, forts and castles, and small wildlife parks. Ghana has also targeted the Afro-American tourist market, promoting special heritage tours (pan-African festivals and Emancipation-day celebrations) and other historical events aimed at the African diaspora.

110. Tourist arrivals and receipts have increased strongly in recent years (Table IV.13). The main sources of tourism are the United States, Nigeria, the United Kingdom, Côte-d'Ivoire, and Germany; Ghanaians based overseas (largely in the United Kingdom and the United States) accounted for 14% of tourist arrivals in 2005.

111. The number of hotel beds in Ghana more than doubled between 1996 and 2006, from 14,000 to over 28,000, reflecting an increase in one-, two-, and three-star accommodation (Table IV.13). There are still only a few hotels with a four-star rating or above. Hotel occupancy rates were around 80% for four- and five-star hotels in 2005 and 2006. The Ghana Tourist Board is in charge of hotel classification, following guidelines issued by ECOWAS.

Table IV.13Tourism basic indicators, 2000-06

2000 2001 2002 2003 2004 2005 2006

Arrivals 399,000 438,833 482,643 530,827 583,821 428,511a 497,129Receipts (US$ million) 386.0 477.8 519.6 602.8 649.4 836.1a 981.3Number of hotels 992 1053 1,169 1,250 1,315 1,344 1,405Number of rooms 13,641 15,453 16,180 17,352 18,079 18,632 19,967Number of beds 17,558 19,648 21,442 22,909 23,538 23,915 28,006

a Change in methodology.

Source: Ghana Tourist Board.

112. An objective of the five-year Strategic Tourism Development Plan is to attract 1 million tourists each year from 2007 and to develop Ghana into an internationally competitive tourist destination. The Plan seeks to improve skills in the hospitality industry and to identify opportunities and programme developments necessary for tourism. The Ghana Tourist Board, as implementing agency of the Ministry of Tourism, carries out promotional activities. It is also responsible for the registration and licensing of tour operators. The Government has divested all of its state-owned hotels; in a few cases, it has kept a minority share.

113. Hotels, guest houses, and other accommodation establishments and tour operators licensed by the Ghana Tourist Board are eligible for certain tariff and tax concessions. As decided by the Ghana Investment Promotion Centre in June 2005, tariff and VAT exemptions are granted on, inter alia, imports of capital and office equipment, furniture, and passenger vehicles. In addition, hotels that have between two and five stars are exempt from corporate tax for five years.

27 Bank of Ghana (2006).

Ghana WT/TPR/S/194Page 66

REFERENCES

Antwi, Yaw Adarwah (2006), Strengthening Customary Land Administration: A DFID/World Bank Sponsored Project in Ghana, Paper presented at the 5th FIG Regional Conference, Accra, 8-11 March 2006.

Antwi-Danso, Wladimir (2007), ECOWAS' ungelöste Aufgaben, Entwicklung und Zusammenarbeit, Frankfurt.

Association of Ghana Industries (2007), AGI Business Climate Survey 2007, Accra.

Bank of Ghana (2005), Annual Report, Accra.

Bank of Ghana (2006), The Tourism Industry and the Ghanaian Economy, Policy Brief, January, Accra.

Bank of Ghana (2007a), Financial Stability Report, Accra.

Bank of Ghana (2007b), Monetary Policy Report – Inflation Outlook and Analysis, Accra.

Bank of Ghana (2007c), Policy Brief – Labour Market Developments 2006, Accra.

Bermúdez-Lugo, Omayra (2005), "The Mineral Industry of Ghana", United States Geological Survey: 2005 Minerals Yearbook. Viewed at: http://minerals.usgs.gov/minerals/pubs/country/2005/ghmyb05.pdf.

Export Development and Investment Fund (2006), Annual Report 2005, Accra.

Ghana Investment Promotion Centre (2007), The GIPC Quarterly Report, January, Accra.

Ghana Investment Promotion Centre (2006), Sector Profile: Fisheries, Accra.

Government of Ghana (2003), National Medium Term Private Sector Development Strategy, Accra.

Ministry of Communications (2004), National Telecommunications Policy, Accra.

Ministry of Communications (2007), Promoting the Information Society in Ghana, Accra.

Ministry of Energy (2003), Brief Profiles of Sector Institutions, Accra.

Ministry of Food and Agriculture (2002), Food and Agriculture Sector Development Policy (FASDEP), September, Accra.

Ministry of Food and Agriculture (2007), Revised Food and Agriculture Sector Development Policy (FASDEP II), Accra.

Ministry of Trade and Industry (2004), Ghana Trade Policy, Accra.

National Development Planning Commission (2005), Growth and Poverty Reduction Strategy (GPRS II) (2006-09), Accra.

Republic of Ghana (2003), The Ghana ICT for Accelerated Development Policy, Accra.

WT/TPR/S/194 Trade Policy ReviewPage 67

Republic of Ghana (2006), The Budget Statement and Economic Policy of the Government of Ghana for the 2007 Financial Year, Accra.

Sarfo-Mensah, Paul (2005), Exportation of Timber in Ghana: The Menace of Illegal Logging Operationms, University of Science and Technology, Kumasi. Viewed at: http://www.feem.it/NR/rdonlyres/7B28B8FB-0D28-4FFC-9527-B966B2A54C02/1462/2905.pdf.

UNCTAD (2006), World Investment Report 2006, Geneva.

University of Ghana, Institute of Statistical, Social, and Economic Research (2005), Guide to Electric Power in Ghana, Legon.

University of Ghana, Institute of Statistical, Social, and Economic Research (2006), The State of the Ghanaian Economy in 2005, Legon.

World Bank (2001), Regional Integration Assistance Strategy for West Africa, Report No. 22520-AFR. Viewed at: http://www-wds.worldbank.org/servlet/WDSContentServer/WDSP/IB/2001/07/27/000094946_01071704015882/Rendered/PDF/multi0page.pdf [17 April 2007].

World Bank (2007), World Development Indicators 2007, Washington D.C.