Embed Size (px)

Citation preview

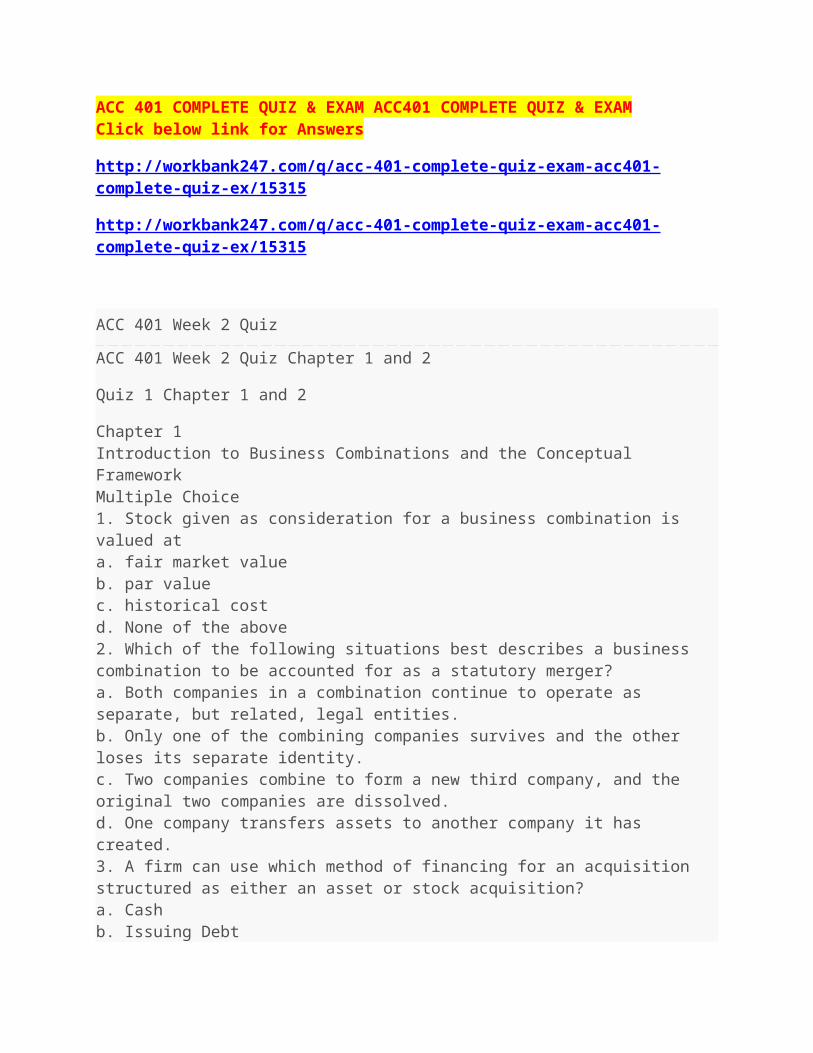

ACC 401 COMPLETE QUIZ & EXAM ACC401 COMPLETE QUIZ & EXAMClick below link for Answers

http://workbank247.com/q/acc-401-complete-quiz-exam-acc401-complete-quiz-ex/15315

http://workbank247.com/q/acc-401-complete-quiz-exam-acc401-complete-quiz-ex/15315

ACC 401 Week 2 Quiz

ACC 401 Week 2 Quiz Chapter 1 and 2

Quiz 1 Chapter 1 and 2

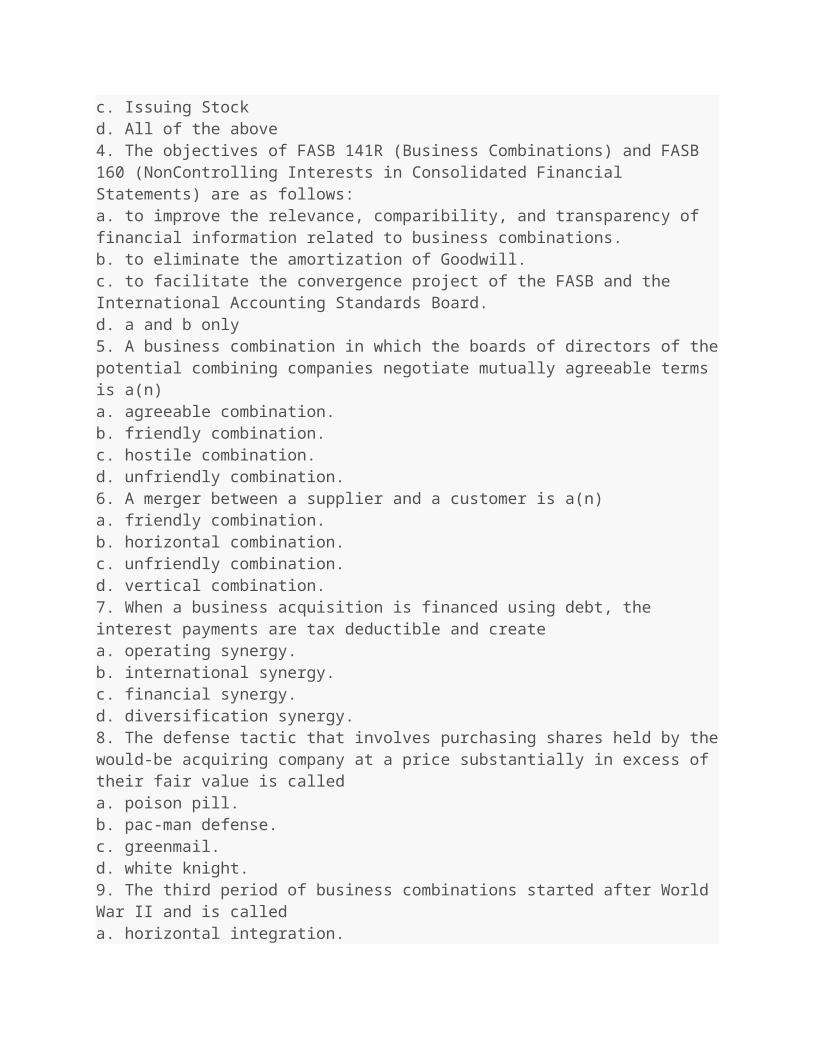

Chapter 1Introduction to Business Combinations and the Conceptual FrameworkMultiple Choice1. Stock given as consideration for a business combination is valued ata. fair market valueb. par valuec. historical costd. None of the above2. Which of the following situations best describes a business combination to be accounted for as a statutory merger?a. Both companies in a combination continue to operate as separate, but related, legal entities.b. Only one of the combining companies survives and the other loses its separate identity.c. Two companies combine to form a new third company, and the original two companies are dissolved.d. One company transfers assets to another company it has created.3. A firm can use which method of financing for an acquisition structured as either an asset or stock acquisition?a. Cashb. Issuing Debtc. Issuing Stockd. All of the above4. The objectives of FASB 141R (Business Combinations) and FASB 160 (NonControlling Interests in Consolidated Financial Statements) are as follows:a. to improve the relevance, comparibility, and transparency of financial information related to business combinations.b. to eliminate the amortization of Goodwill.c. to facilitate the convergence project of the FASB and the International Accounting Standards

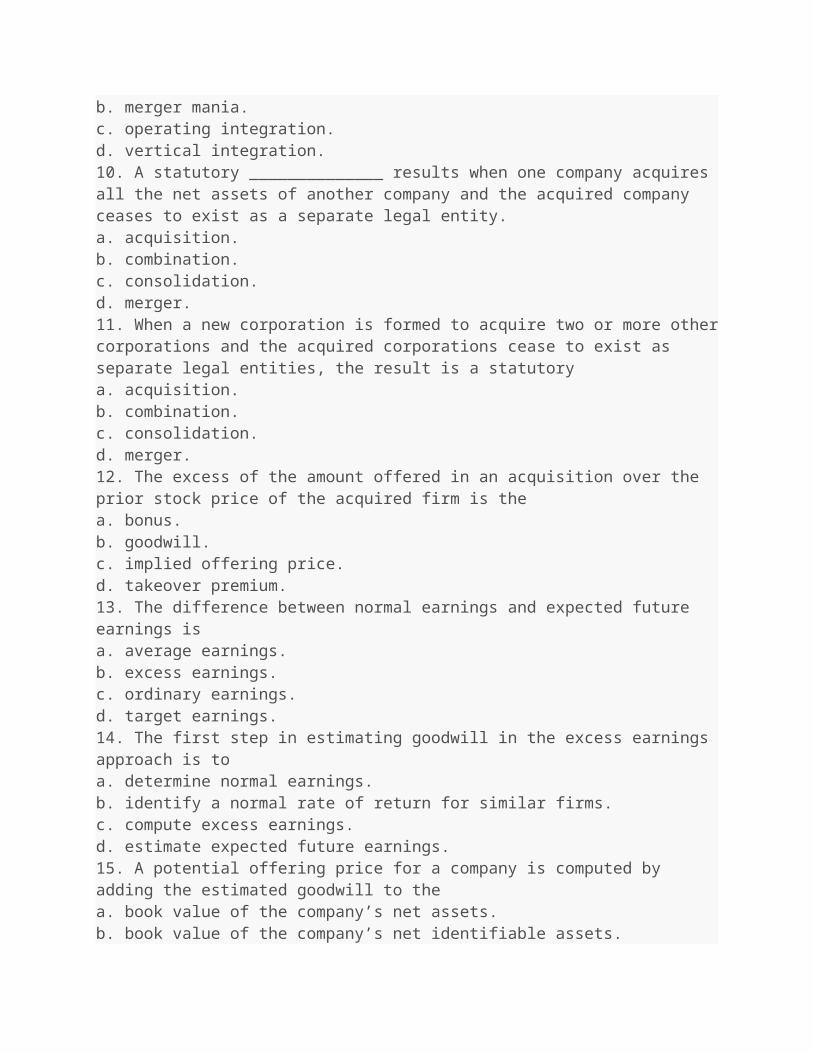

Board.d. a and b only5. A business combination in which the boards of directors of the potential combining companies negotiate mutually agreeable terms is a(n)a. agreeable combination.b. friendly combination.c. hostile combination.d. unfriendly combination.6. A merger between a supplier and a customer is a(n)a. friendly combination.b. horizontal combination.c. unfriendly combination.d. vertical combination.7. When a business acquisition is financed using debt, the interest payments are tax deductible and createa. operating synergy.b. international synergy.c. financial synergy.d. diversification synergy.8. The defense tactic that involves purchasing shares held by the would-be acquiring company at a price substantially in excess of their fair value is calleda. poison pill.b. pac-man defense.c. greenmail.d. white knight.9. The third period of business combinations started after World War II and is calleda. horizontal integration.b. merger mania.c. operating integration.d. vertical integration.10. A statutory ______________ results when one company acquires all the net assets of another company and the acquired company ceases to exist as a separate legal entity.a. acquisition.b. combination.c. consolidation.d. merger.11. When a new corporation is formed to acquire two or more other corporations and the acquired corporations cease to exist as separate legal entities, the result is a statutorya. acquisition.b. combination.

c. consolidation.d. merger.12. The excess of the amount offered in an acquisition over the prior stock price of the acquired firm is thea. bonus.b. goodwill.c. implied offering price.d. takeover premium.13. The difference between normal earnings and expected future earnings isa. average earnings.b. excess earnings.c. ordinary earnings.d. target earnings.14. The first step in estimating goodwill in the excess earnings approach is toa. determine normal earnings.b. identify a normal rate of return for similar firms.c. compute excess earnings.d. estimate expected future earnings.15. A potential offering price for a company is computed by adding the estimated goodwill to thea. book value of the company’s net assets.b. book value of the company’s net identifiable assets.c. fair value of the company’s net assets.d. fair value of the company’s net identifiable assets.16. Estimated goodwill is determined by computing the present value of thea. average earnings.b. excess earnings.c. expected future earnings.d. normal earnings.17. Which of the following statements would not be a valid or logical reason for entering into a business combination?a. to increase market share.b. to avoid becoming a takeover target.c. to reduce risk by acquiring established product lines.d. the operating costs of the combined entity would be more than the sum of the separate entities.18. The parent company concept of consolidation represents the view that the primary purpose of consolidated financial statements is:a. to provide information relevant to the controlling stockholders.b. to represent the view that the affiliated companies are a separate, identifiable economic entity.c. to emphasis control of the whole by a single management.d. to include only a portion of the subsidiary’s assets, liabilities, revenues, expenses, gains, and losses.

19. Which of the following statements is correct?a. Total elimination is consistent with the parent company concept.b. Partial elimination is consistent with the economic unit concept.c. Past accounting standards required the total elimination of unrealized intercompany profit in assets acquired from affiliated companies.d. none of these.20. Under the parent company concept, consolidated net income __________ the consolidated net income under the economic unit concept.a. is the same asb. is higher thanc. is lower thand. can be higher or lower than21. Under the economic unit concept, noncontrolling interest in net assets is treated asa. a liability.b. an asset.c. stockholders’ equity.d. an expense.22. The parent company concept adjusts subsidiary net asset values for thea. differences between cost and fair value.b. differences between cost and book value.c. total fair value implied by the price paid by the parent.d. total cost implied by the price paid by the parent.23. According to the economic unit concept, the primary purpose of consolidated financial statements is to provide information that is relevant toa. majority stockholders.b. minority stockholders.c. creditors.d. both majority and minority stockholders.24. Which of the following statements is correct?a. The economic unit concept suggests partial elimination of unrealized intercompany profits.b. The parent company concept suggests partial elimination of unrealized intercompany profits.c. The economic unit concept suggests no elimination of unrealized intercompany profits.d. The parent company concept suggests total elimination of unrealized intercompany profits.25. When following the parent company concept in the preparation of consolidated financial statements, noncontrolling interest in combined income is considered a(n)a. prorated share of the combined income.b. addition to combined income to arrive at consolidated net income.c. expense deducted from combined income to arrive at consolidated net income.d. deduction from current assets in the balance sheet.26. When following the economic unit concept in the preparation of consolidated financial statements, the basis for valuing the noncontrolling interest in net assets is the

a. book values of subsidiary assets and liabilities.b. fair values of subsidiary assets and liabilities.c. general price level adjusted values of subsidiary assets and liabilities.d. fair values of parent company assets and liabilities.27. The view that consolidated financial statements represent those of a single economic entity with several classes of stockholder interest is consistent with thea. parent company concept.b. current practice concept.c. historical cost company concept.d. economic unit concept.28. The view that the noncontrolling interest in income reflects the noncontrolling stockholders’ allocated share of consolidated income is consistent with thea. economic unit concept.b. parent company concept.c. current practice concept.d. historical cost company concept.29. The view that only the parent company’s share of the unrealized intercompany profit recognized by the selling affiliate that remains in assets should be eliminated in the preparation of consolidated financial statements is consistent with thea. economic unit concept.b. current practice concept.c. parent company concept.d. historical cost company concept.Problems

1-1 Perkins Company is considering the acquisition of Barkley, Inc. To assess the amount it might be willing to pay, Perkins makes the following computations and assumptions.A. Barkley, Inc. has identifiable assets with a total fair value of $6,000,000 and liabilities of $3,700,000. The assets include office equipment with a fair value approximating book value, buildings with a fair value 25% higher than book value, and land with a fair value 50% higher than book value. The remaining lives of the assets are deemed to be approximately equal to those used by Barkley, Inc.B. Barkley, Inc.’s pretax incomes for the years 2009 through 2011 were $470,000, $570,000, and $370,000, respectively. Perkins believes that an average of these earnings represents a fair estimate of annual earnings for the indefinite future. However, it may need to consider adjustments for the following items included in pretax earnings:Depreciation on Buildings (each year) 380,000Depreciation on Equipment (each year) 30,000Extraordinary Loss (year 2011) 130,000Salary Expense (each year) 170,000C. The normal rate of return on net assets for the industry is 15%.

Required:A. Assume that Perkins feels that it must earn a 20% return on its investment, and that goodwill is determined by capitalizing excess earnings. Based on these assumptions, calculate a reasonable offering price for Barkley, Inc. Indicate how much of the price consists of goodwill.B. Assume that Perkins feels that it must earn a 15% return on its investment, but that average excess earnings are to be capitalized for five years only. Based on these assumptions, calculate a reasonable offering price for Barkley, Inc. Indicate how much of the price consists of goodwill.1-2 Pierce Company is trying to decide whether to acquire Hager Inc. The following balance sheet for Hager Inc. provides information about book values. Estimated market values are also listed, based upon Pierce Company’s appraisals.

Hager Inc. Hager Inc.Book Values Market ValuesCurrent Assets $ 450,000 $ 450,000Property, Plant & Equipment (net) 1,140,000 1,300,000Total Assets $1,590,000 $1,750,000Total Liabilities $700,000 $700,000Common Stock, $10 par value 280,000Retained Earnings 610,000Total Liabilities and Equities $1,590,000Pierce Company expects that Hager will earn approximately $290,000 per year in net income over the next five years. This income is higher than the 14% annual return on tangible assets considered to be the industry “norm.”

Required:A. Compute an estimation of goodwill based on the information above that Pierce might be willing to pay (include in its purchase price), under each of the following additional assumptions:(1) Pierce is willing to pay for excess earnings for an expected life of 4 years (undiscounted).(2) Pierce is willing to pay for excess earnings for an expected life of 4 years, which should be capitalized at the industry normal rate of return.(3) Excess earnings are expected to last indefinitely, but Pierce demands a higher rate of return of 20% because of the risk involved.B. Determine the amount of goodwill to be recorded on the books if Pierce pays $1,300,000 cash and assumes Hager’s liabilities.1-3 Pope Company acquired an 80% interest in the common stock of Simon Company for $1,540,000 on July 1, 2011. Simon Company’s stockholders’ equity on that date consisted of:

Common stock $800,000Other contributed capital 400,000Retained earnings 330,000Required:Compute the total noncontrolling interest to be reported in the consolidated balance sheet

assuming the:(1) parent company concept.(2) economic unit concept.1-4 The following balances were taken from the records of S Company:

Common stock (1/1/11 and 12/31/11) $720,000Retained earnings 1/1/11 $160,000Net income for 2011 180,000Dividends declared in 2011 (40,000)Retained earnings, 12/31/11 300,000Total stockholders’ equity on 12/31/11 $1,020,000P Company purchased 75% of S Company’s common stock on January 1, 2011 for $900,000. The difference between implied value and book value is attributable to assets with a remaining useful life on January 1, 2011 of ten years.

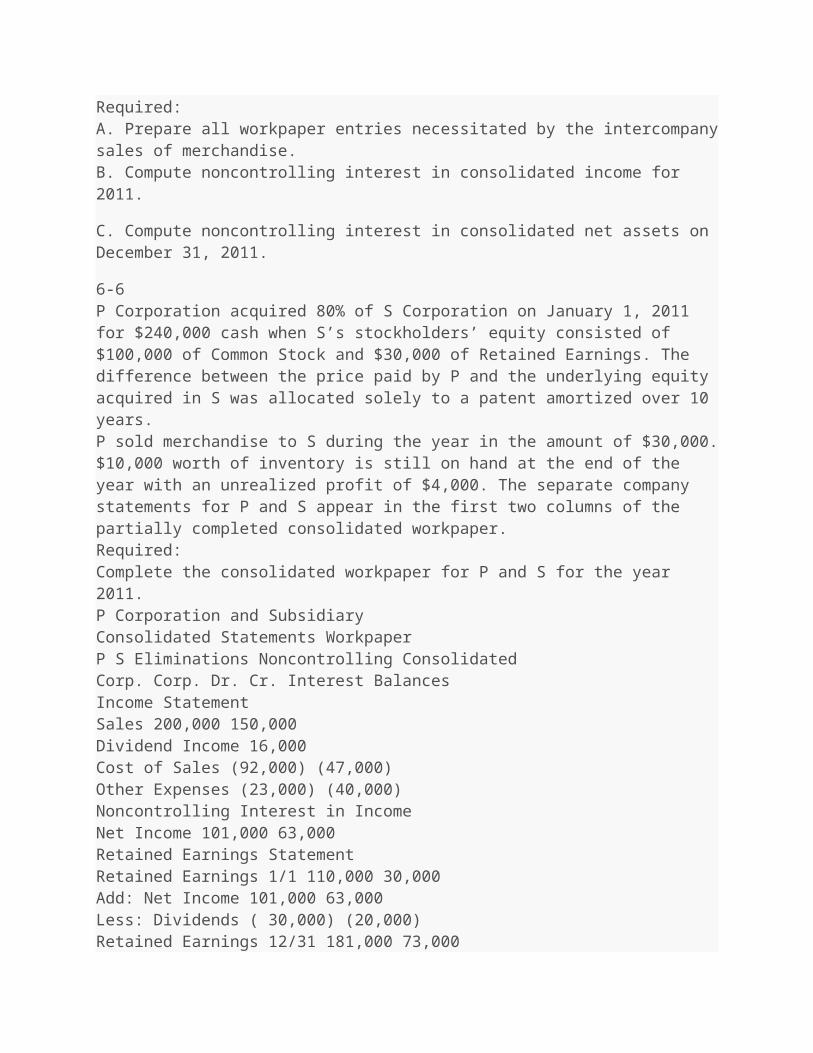

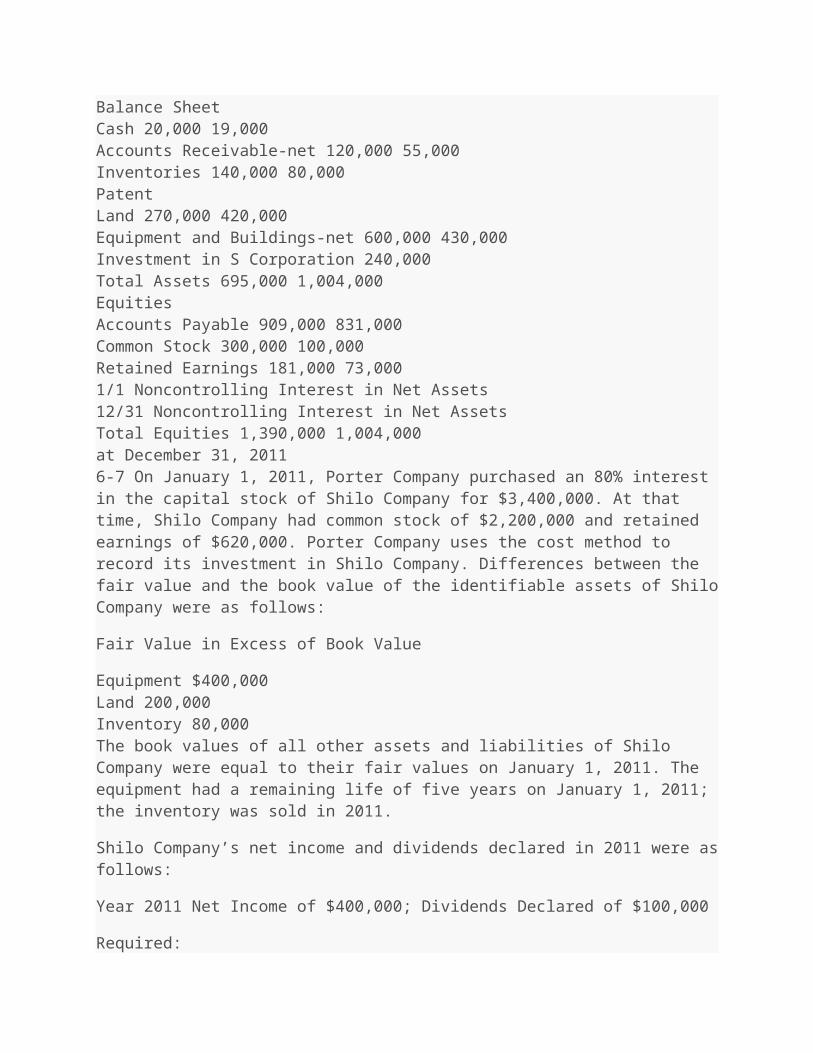

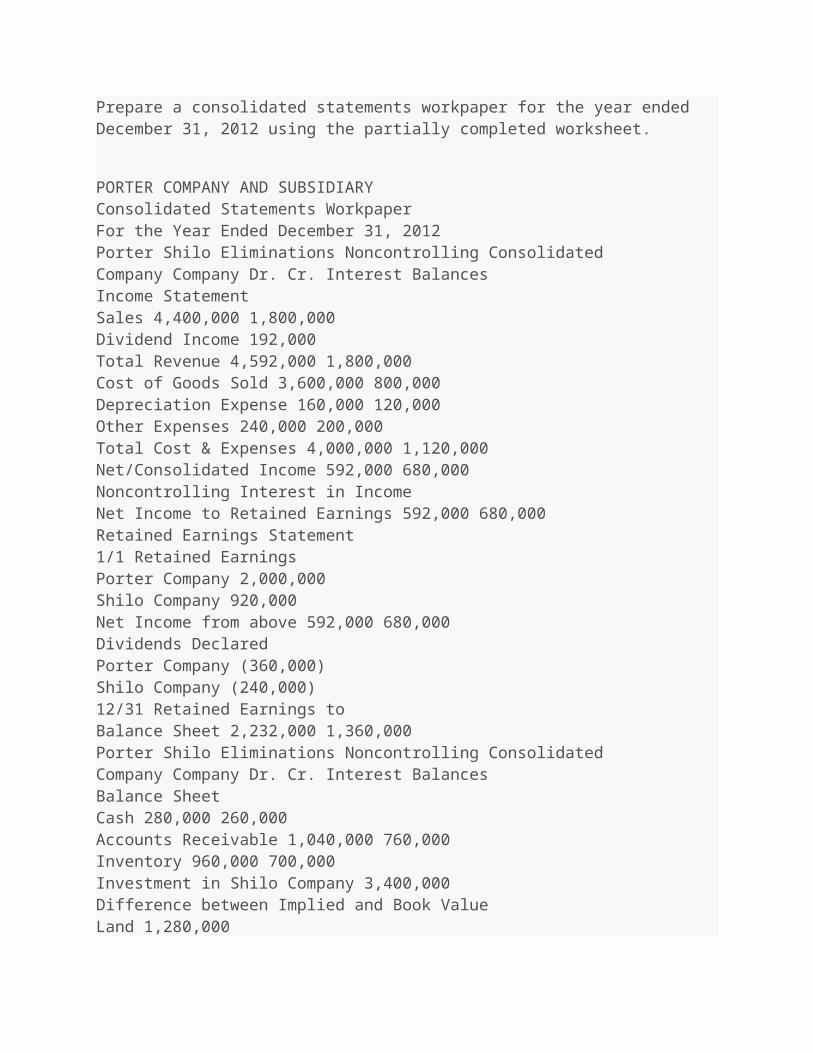

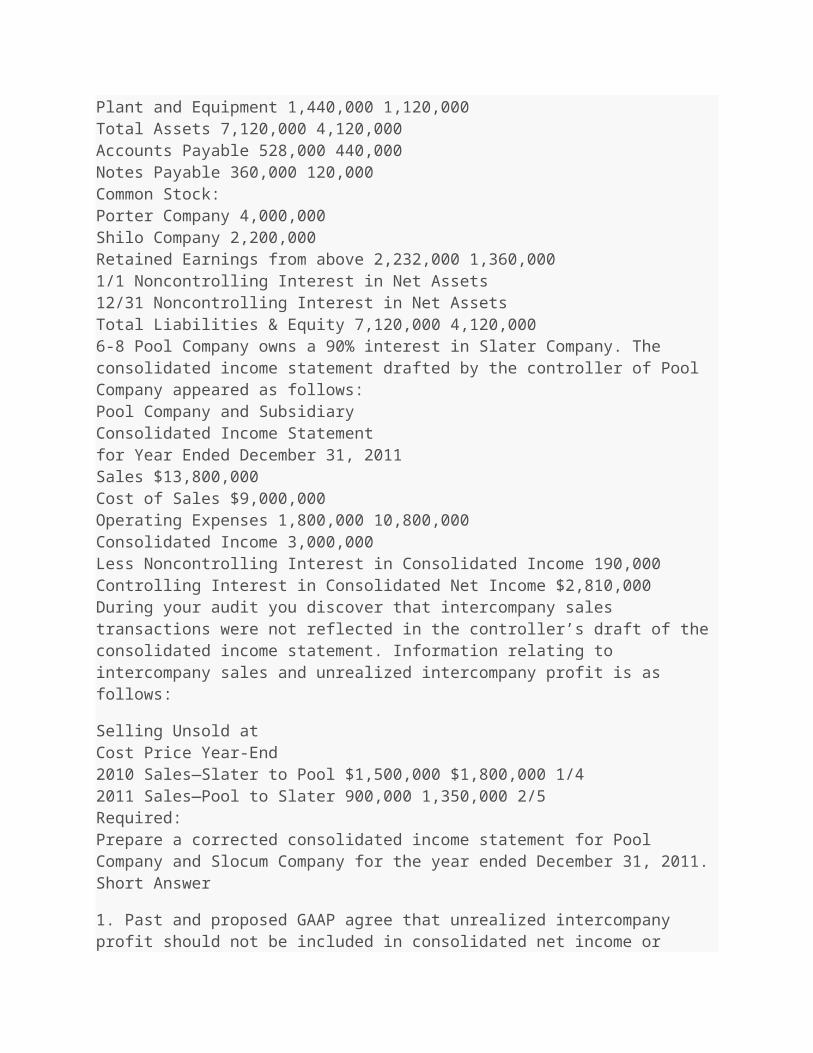

Required:

A. Compute the difference between cost/(implied) and book value applying:1. Parent company theory.2. Economic unit theory.B. Assuming the economic unit theory:1. Compute noncontrolling interest in consolidated income for 2011.2. Compute noncontrolling interest in net assets on December 31, 2011.Short Answer

1. Estimating the value of goodwill to be included in an offering price can be done under several alternative methods. The excess earnings approach is frequently used. Identify the steps used in this approach to estimate goodwill.

2. The two alternative views of consolidated financial statements are the parent company concept and the economic entity concept. Briefly explain the differences between the concepts.

Short Answer Questions in Textbook

1. Distinguish between internal and external expansion of a firm.

2. List four advantages of a business combination as compared to internal expansion.

3. What is the primary legal constraint on business combinations? Why does such a constraint exist?

4. Business combinations may be classified into three types based upon the relationships among the combining entities (e.g., combinations with suppliers, customers, competitors, etc.). Identify and define these types.

5. Distinguish among a statutory merger, a statutory consolidation, and a stock acquisition.

6. Define a tender offer and describe its use.

7. When stock is exchanged for stock in a business combination, how is the stock exchange ratio generally expressed?

8. Define some defensive measures used by target firms to avoid a takeover. Are these measures beneficial for shareholders?

9. Explain the potential advantages of a stock acquisition over an asset acquisition.

10. Explain the difference between an accretive and a dilutive acquisition.

11. Describe the difference between the economic entity concept and the parent company concept approaches to the reporting of subsidiary assets and liabilities in the consolidated financial statements on the date of the acquisition.

12. Contrast the consolidated effects of the parent company concept and the economic entity con-cept in terms of:(a)The treatment of noncontrolling interests.(b)The elimination of intercompany profits.(c)The valuation of subsidiary net assets in the consolidated financial statements.(d)The definition of consolidated net income.13. Under the economic entity concept, the net as-sets of the subsidiary are included in the consolidated financial statements at the total fair value that is implied by the price paid by the parent company for its controlling interest. What practical or conceptual problems do you see in this approach to valuation?

14. Is the economic entity or the parent concept more consistent with the principles addressed in the FASB’s conceptual framework? Explain your answer.

15. How does the FASB’s conceptual framework influence the development of new standards?

16. What is the difference between net income, or earnings, and comprehensive income?

Business Ethics Questions from the Textbook

From 1999 to 2001, Tyco’s revenue grew approximately24% and it acquired over 700 companies. It was widely rumored that Tyco executives aggressively managed the performance of the companies that they acquired by suggesting that before the acquisition, they should accelerate the payment of liabilities, delay recording the collections of revenue, and increase the estimated amounts in reserve accounts.

1. What effect does each of the three items have on the reported net income of the acquired company before the acquisition and on the reported net income of the combined company in the first year of the acquisition and future years?

2. What effect does each of the three items have on the cash from operations of the acquired company before the acquisition and on the cash from operations of the combined company in the first year of the acquisition and future years?

3. If you are the manager of the acquired company, how do you respond to these suggestions?

4. Assume that all three items can be managed within the rules provided by GAAP but would be regarded by many as pushing the limits of GAAP.Is there an ethical issue? Describe your position as: (A) an accountant for the target company and (B) as an accountant for Tyco.

Chapter 2

Accounting for Business Combinations

Multiple Choice

1. SFAS 141R requires that all business combinations be accounted for usinga. the pooling of interests method.b. the acquisition method.c. either the acquisition or the pooling of interests methods.d. neither the acquisition nor the pooling of interests methods.2. Under the acquisition method, if the fair values of identifiable net assets exceed the value implied by the purchase Pratt of the acquired company, the excess should bea. accounted for as goodwill.b. allocated to reduce current and long-lived assets.c. allocated to reduce current assets and classify any remainder as an extraordinary gain.d. allocated to reduce any previously recorded goodwill and classify any remainder as an ordinary gain.3. In a period in which an impairment loss occurs, SFAS No. 142 requires each of the following note disclosures excepta. a description of the facts and circumstances leading to the impairment.b. the amount of goodwill by reporting segment.c. the method of determining the fair value of the reporting unit.d. the amounts of any adjustments made to impairment estimates from earlier periods, if significant.4. Once a reporting unit is determined to have a fair value below its carrying value, the goodwill impairment loss is computed by comparing thea. fair value of the reporting unit and the fair value of the identifiable net assets.b. carrying value of the goodwill to its implied fair value.

c. fair value of the reporting unit to its carrying amount (goodwill included).d. carrying value of the reporting unit to the fair value of the identifiable net assets.5. SFAS 141R requires that the acquirer disclose each of the following for each material business combination except thea. name and a description of the acquiree.b. percentage of voting equity instruments acquired.c. fair value of the consideration transferred.d. Each of the above is a required disclosure6. In a leveraged buyout, the portion of the net assets of the new corporation provided by the management group is recorded ata. appraisal value.b. book value.c. fair value.d. lower of cost or market.7. When the acquisition price of an acquired firm is less than the fair value of the identifiable net assets, all of the following are recorded at fair value excepta. Assumed liabilities.b. Current assets.c. Long-lived assets.d. Each of the above is recorded at fair value.8. Under SFAS 141R,a. both direct and indirect costs are to be capitalized.b. both direct and indirect costs are to be expensed.c. direct costs are to be capitalized and indirect costs are to be expensed.d. indirect costs are to be capitalized and direct costs are to be expensed.9. A business combination is accounted for properly as an acquisition. Which of the following expenses related to effecting the business combination should enter into the determination of net income of the combined corporation for the period in which the expenses are incurred?

Security Overhead allocatedissue costs to the mergera. Yes Yesb. Yes Noc. No Yesd. No No10. In a business combination, which of the following costs are assigned to the valuation of the security?

Professional or Securityconsulting fees issue costsa. Yes Yes

b. Yes Noc. No Yesd. No No11. Par Company and Sub Company were combined in an acquisition transaction. Par was able to acquire Sub at a bargain Pratt. The sum of the fair values of identifiable assets acquired less the fair value of liabilities assumed exceeded the cost to Par. After eliminating previously recorded goodwill, there was still some “negative goodwill.” Proper accounting treatment by Par is to report the amount asa. paid-in capital.b. a deferred credit, which is amortized.c. an ordinary gain.d. an extraordinary gain.12. With an acquisition, direct and indirect expenses area. expensed in the period incurred.b. capitalized and amortized over a discretionary period.c. considered a part of the total cost of the acquired company.d. charged to retained earnings when incurred.13. In a business combination accounted for as an acquisition, how should the excess of fair value of net assets acquired over the consideration paid be treated?a. Amortized as a credit to income over a period not to exceed forty years.b. Amortized as a charge to expense over a period not to exceed forty years.c. Amortized directly to retained earnings over a period not to exceed forty years.d. Recorded as an ordinary gain.14. P Corporation issued 10,000 shares of common stock with a fair value of $25 per share for all the outstanding common stock of S Company in a business combination properly accounted for as an acquisition. The fair value of S Company’s net assets on that date was $220,000. P Company also agreed to issue an additional 2,000 shares of common stock with a fair value of $50,000 to the former stockholders of S Company as an earnings contingency. Assuming that the contingency is expected to be met, the $50,000 fair value of the additional shares to be issued should be treated as a(n)a. decrease in noncurrent liabilities of S Company that were assumed by P Company.b. decrease in consolidated retained earnings.c. increase in consolidated goodwill.d. decrease in consolidated other contributed capital.15. On February 5, Pryor Corporation paid $1,600,000 for all the issued and outstanding common stock of Shaw, Inc., in a transaction properly accounted for as an acquisition. The book values and fair values of Shaw’s assets and liabilities on February 5 were as follows

Book Value Fair ValueCash $ 160,000 $ 160,000Receivables (net) 180,000 180,000

Inventory 315,000 300,000Plant and equipment (net) 820,000 920,000Liabilities (350,000) (350,000)Net assets $1,125,000 $1,210,000What is the amount of goodwill resulting from the business combination?a. $-0-.b. $475,000.c. $85,000.d. $390,000.16. P Company purchased the net assets of S Company for $225,000. On the date of P’s purchase, S Company had no investments in marketable securities and $30,000 (book and fair value) of liabilities. The fair values of S Company’s assets, when acquired, were

Current assets $ 120,000Noncurrent assets 180,000Total $300,000How should the $45,000 difference between the fair value of the net assets acquired ($270,000) and the consideration paid ($225,000) be accounted for by P Company?a. The noncurrent assets should be recorded at $ 135,000.b. The $45,000 difference should be credited to retained earnings.c. The current assets should be recorded at $102,000, and the noncurrent assets should be recorded at $153,000.d. An ordinary gain of $45,000 should be recorded.17. If the value implied by the purchase price of an acquired company exceeds the fair values of identifiable net assets, the excess should bea. allocated to reduce any previously recorded goodwill and classify any remainder as an ordinary gain.b. allocated to reduce current and long-lived assets.c. allocated to reduce long-lived assets.d. accounted for as goodwill.18. P Co. issued 5,000 shares of its common stock, valued at $200,000, to the former shareholders of S Company two years after S Company was acquired in an all-stock transaction. The additional shares were issued because P Company agreed to issue additional shares of common stock if the average post combination earnings over the next two years exceeded $500,000. P Company will treat the issuance of the additional shares as a (decrease in)a. consolidated retained earnings.b. consolidated goodwill.c. consolidated paid-in capital.d. non-current liabilities of S Company assumed by P Company.19. In a business combination in which the total fair value of the identifiable assets acquired over liabilities assumed is greater than the consideration paid, the excess fair value is:

a. classified as an extraordinary gain.b. allocated first to eliminate any previously recorded goodwill, and any remaining excess over the consideration paid is classified as an ordinary gain.c. allocated first to reduce proportionately non-current assets then to non-monetary current assets, and any remaining excess over cost is classified as a deferred credit.d. allocated first to reduce proportionately non-current, depreciable assets to zero, and any remaining excess over cost is classified as a deferred credit.20. The first step in determining goodwill impairment involves comparing thea. implied value of a reporting unit to its carrying amount (goodwill excluded).b. fair value of a reporting unit to its carrying amount (goodwill excluded).c. implied value of a reporting unit to its carrying amount (goodwill included).d. fair value of a reporting unit to its carrying amount (goodwill included).21. If an impairment loss is recorded on previously recognized goodwill due to the transitional goodwill impairment test, the loss should be treated as a(n):a. loss from a change in accounting principles.b. extraordinary lossc. loss from continuing operations.d. loss from discontinuing operations.22. P Company acquires all of the voting stock of S Company for $930,000 cash. The book values of S Company’s assets are $800,000, but the fair values are $840,000 because land has a fair value above its book value. Goodwill from the combination is computed as:a. $130,000.b. $90,000.c. $40,000.d. $0.23. Under SFAS 141R, what value of the assets and liabilities are reflected in the financial statements on the acquisition date of a business combination?a. Carrying valueb. Fair valuec. Book valued. Average valueUse the following information to answer questions 24 & 25.

Pratt Company issued 24,000 shares of its $20 par value common stock for the net assets of Sele Company in business combination under which Sele Company will be merged into Pratt Company. On the date of the combination, Pratt Company common stock had a fair value of $30 per share. Balance sheets for Pratt Company and Sele Company immediately prior to the combination were as follows:

Pratt Sele

Current Assets $1,314,000 $192,000Plant and Equipment (net) 1,725,000 408,000Total $3,039,000 $600,000Liabilities $ 900,000 $150,000Common Stock, $20 par value 1,650,000 240,000Other Contributed Capital 218,000 60,000Retained Earnings 271,000 150,000Total $3,039,000 $600,00024. If the business combination is treated as an acquisition and Sele Company’s net assets have a fair value of $686,400, Pratt Company’s balance sheet immediately after the combination will include goodwill ofa. $30,600.b. $38,400.c. $33,600.d. $56,400.25. If the business combination is treated as an acquisition and the fair value of Sele Company’s current assets is $270,000, its plant and equipment is $726,000, and its liabilities are $168,000, Pratt Company’s financial statements immediately after the combination will includea. Negative goodwill of $108,000.b. Plant and equipment of $2,133,000.c. Plant and equipment of $2,343,000.d. An ordinary gain of $108,000.26. On May 1, 2011, the Phil Company paid $1,200,000 for 80% of the outstanding common stock of Sage Corporation in a transaction properly accounted for as an acquisition. The recorded assets and liabilities of Sage Corporation on May 1, 2011, follow:

Cash $100,000Inventory 200,000Property & equipment (Net of accumulated depreciation) 800,000Liabilities (160,000)On May 1, 2011, it was determined that the inventory of Sage had a fair value of $220,000 and the property and equipment (net) has a fair value of $1,200,000. What is the amount of goodwill resulting from the business combination?a. $0.b. $112,000.c. $140,000.d. $28,000.Use the following information to answer questions 27 & 28.

Posch Company issued 12,000 shares of its $20 par value common stock for the net assets of Sato Company in a business combination under which Sato Company will be merged into Posch

Company. On the date of the combination, Posch Company common stock had a fair value of $30 per share. Balance sheets for Posch Company and Sato Company immediately prior to the combination were as follows:

Posch Sato

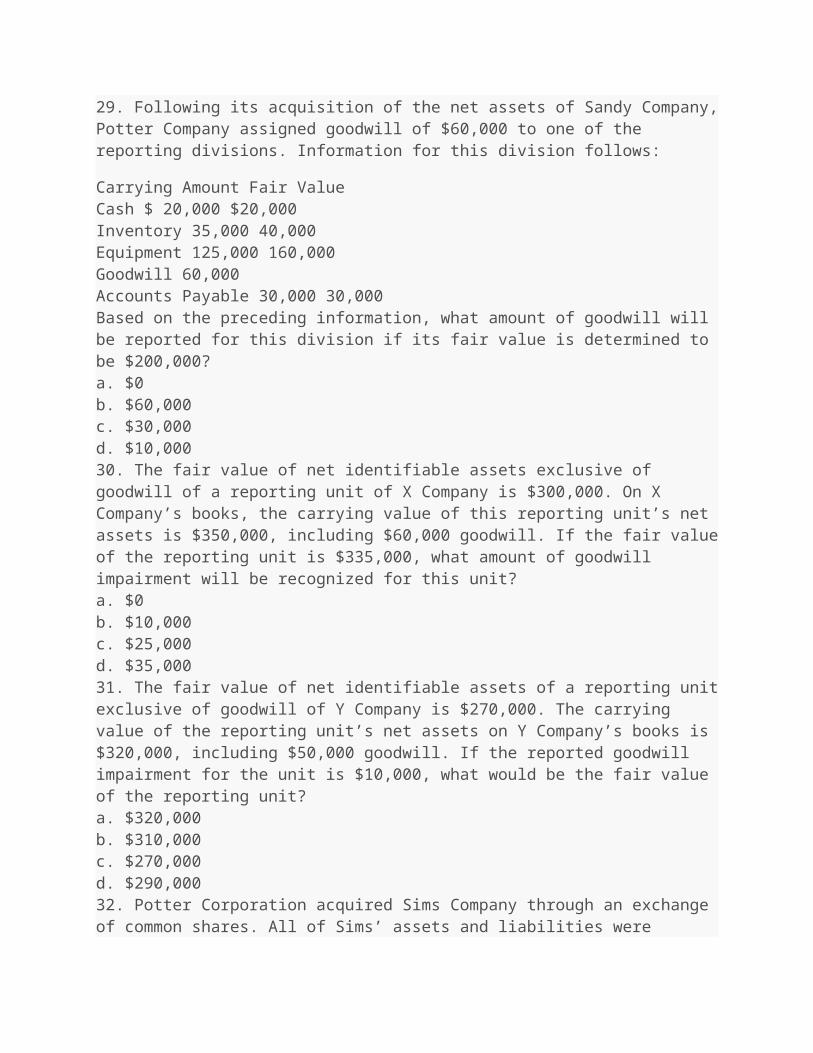

Current Assets $ 657,000 $ 96,000Plant and Equipment (net) 863,000 204,000Total $1,520,000 $300,000Liabilities $ 450,000 $ 75,000Common Stock, $20 par value 825,000 120,000Other Contributed Capital 109,000 30,000Retained Earnings 136,000 75,000Total $1,520,000 $300,00027. If the business combination is treated as an acquisition and Sato Company’s net assets have a fair value of $343,200, Posch Company’s balance sheet immediately after the combination will include goodwill ofa. $15,300.b. $19,200.c. $16,800.d. $28,200.28. If the business combination is treated as an acquisition and the fair value of Sato Company’s current assets is $135,000, its plant and equipment is $363,000, and its liabilities are $84,000, Posch Company’s financial statements immediately after the combination will includea. Negative goodwill of $54,000.b. Plant and equipment of $1,226,000.c. Plant and equipment of $1,172,000.d. An extraordinary gain of $54,000.29. Following its acquisition of the net assets of Sandy Company, Potter Company assigned goodwill of $60,000 to one of the reporting divisions. Information for this division follows:

Carrying Amount Fair ValueCash $ 20,000 $20,000Inventory 35,000 40,000Equipment 125,000 160,000Goodwill 60,000Accounts Payable 30,000 30,000Based on the preceding information, what amount of goodwill will be reported for this division if its fair value is determined to be $200,000?a. $0b. $60,000

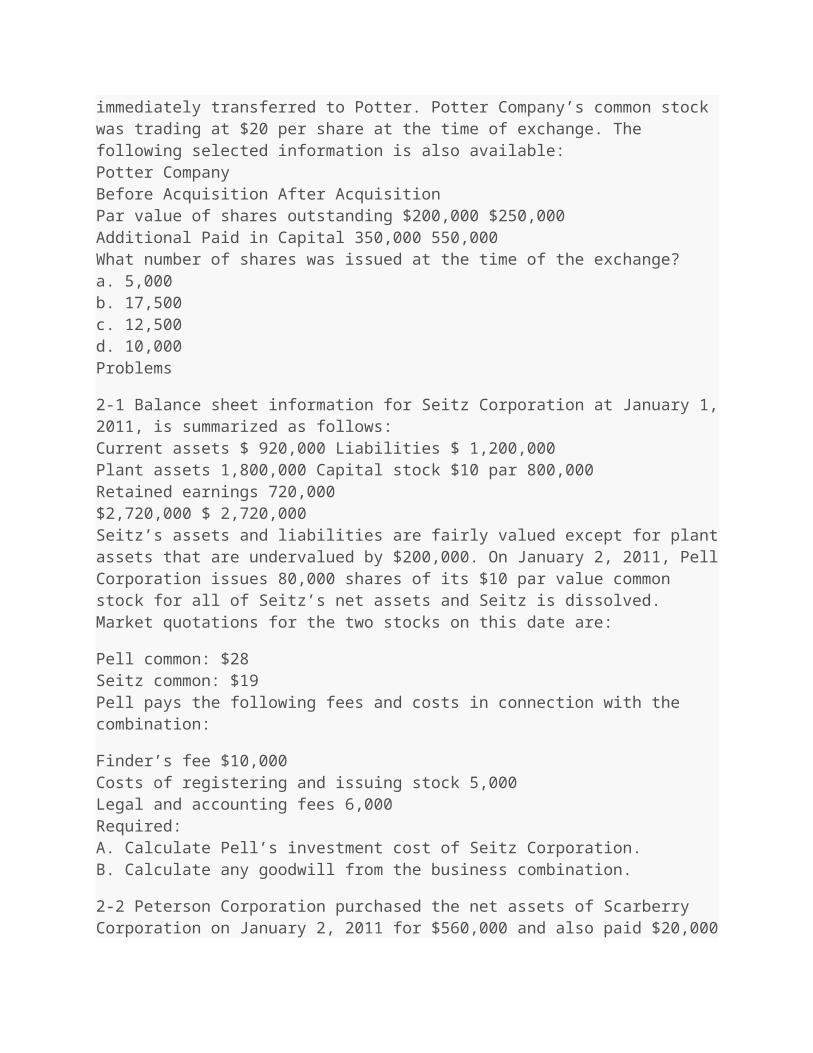

c. $30,000d. $10,00030. The fair value of net identifiable assets exclusive of goodwill of a reporting unit of X Company is $300,000. On X Company’s books, the carrying value of this reporting unit’s net assets is $350,000, including $60,000 goodwill. If the fair value of the reporting unit is $335,000, what amount of goodwill impairment will be recognized for this unit?a. $0b. $10,000c. $25,000d. $35,00031. The fair value of net identifiable assets of a reporting unit exclusive of goodwill of Y Company is $270,000. The carrying value of the reporting unit’s net assets on Y Company’s books is $320,000, including $50,000 goodwill. If the reported goodwill impairment for the unit is $10,000, what would be the fair value of the reporting unit?a. $320,000b. $310,000c. $270,000d. $290,00032. Potter Corporation acquired Sims Company through an exchange of common shares. All of Sims’ assets and liabilities were immediately transferred to Potter. Potter Company’s common stock was trading at $20 per share at the time of exchange. The following selected information is also available:Potter CompanyBefore Acquisition After AcquisitionPar value of shares outstanding $200,000 $250,000Additional Paid in Capital 350,000 550,000What number of shares was issued at the time of the exchange?a. 5,000b. 17,500c. 12,500d. 10,000Problems

2-1 Balance sheet information for Seitz Corporation at January 1, 2011, is summarized as follows:Current assets $ 920,000 Liabilities $ 1,200,000Plant assets 1,800,000 Capital stock $10 par 800,000Retained earnings 720,000$2,720,000 $ 2,720,000Seitz’s assets and liabilities are fairly valued except for plant assets that are undervalued by $200,000. On January 2, 2011, Pell Corporation issues 80,000 shares of its $10 par value

common stock for all of Seitz’s net assets and Seitz is dissolved. Market quotations for the two stocks on this date are:

Pell common: $28Seitz common: $19Pell pays the following fees and costs in connection with the combination:

Finder’s fee $10,000Costs of registering and issuing stock 5,000Legal and accounting fees 6,000Required:A. Calculate Pell’s investment cost of Seitz Corporation.B. Calculate any goodwill from the business combination.

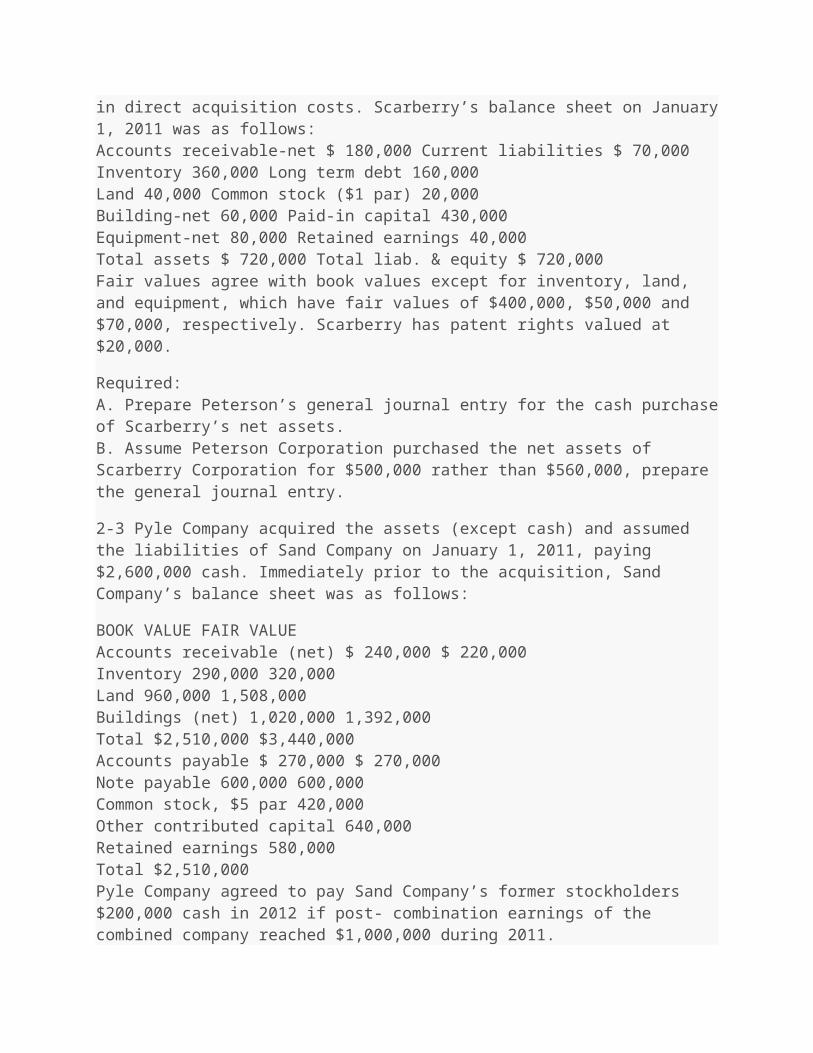

2-2 Peterson Corporation purchased the net assets of Scarberry Corporation on January 2, 2011 for $560,000 and also paid $20,000 in direct acquisition costs. Scarberry’s balance sheet on January1, 2011 was as follows:Accounts receivable-net $ 180,000 Current liabilities $ 70,000Inventory 360,000 Long term debt 160,000Land 40,000 Common stock ($1 par) 20,000Building-net 60,000 Paid-in capital 430,000Equipment-net 80,000 Retained earnings 40,000Total assets $ 720,000 Total liab. & equity $ 720,000Fair values agree with book values except for inventory, land, and equipment, which have fair values of $400,000, $50,000 and $70,000, respectively. Scarberry has patent rights valued at $20,000.

Required:A. Prepare Peterson’s general journal entry for the cash purchase of Scarberry’s net assets.B. Assume Peterson Corporation purchased the net assets of Scarberry Corporation for $500,000 rather than $560,000, prepare the general journal entry.

2-3 Pyle Company acquired the assets (except cash) and assumed the liabilities of Sand Company on January 1, 2011, paying $2,600,000 cash. Immediately prior to the acquisition, Sand Company’s balance sheet was as follows:

BOOK VALUE FAIR VALUEAccounts receivable (net) $ 240,000 $ 220,000Inventory 290,000 320,000Land 960,000 1,508,000

Buildings (net) 1,020,000 1,392,000Total $2,510,000 $3,440,000Accounts payable $ 270,000 $ 270,000Note payable 600,000 600,000Common stock, $5 par 420,000Other contributed capital 640,000Retained earnings 580,000Total $2,510,000Pyle Company agreed to pay Sand Company’s former stockholders $200,000 cash in 2012 if post- combination earnings of the combined company reached $1,000,000 during 2011.

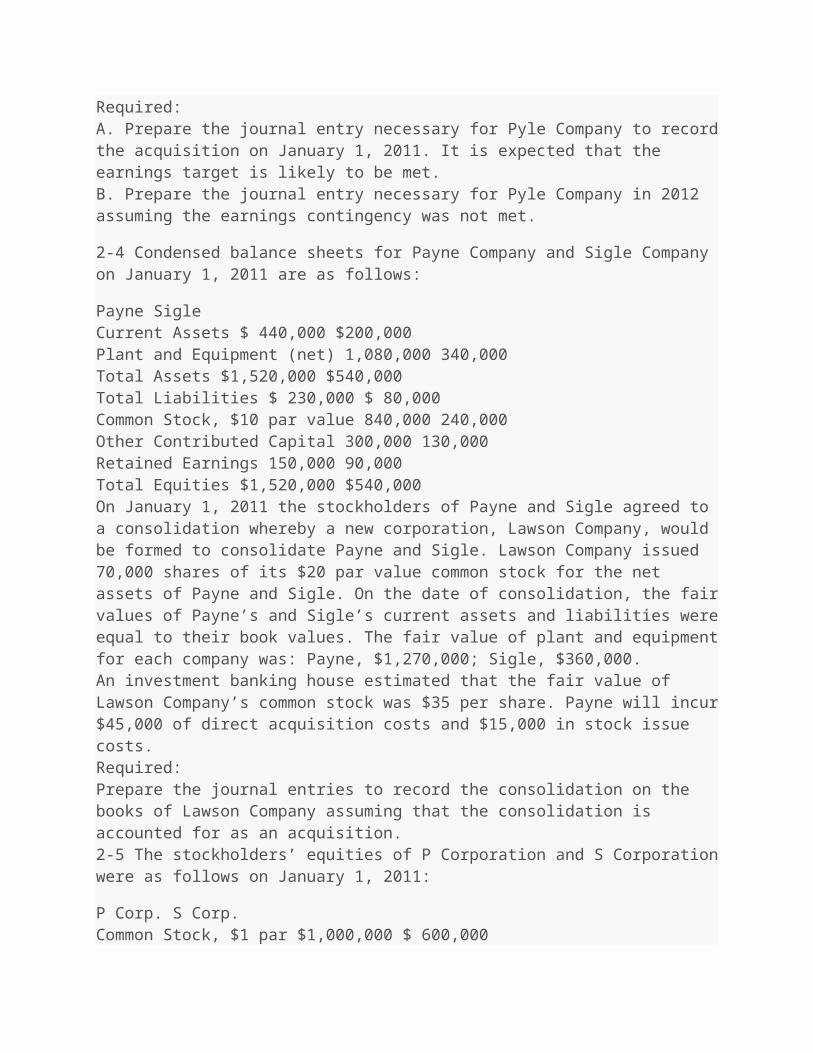

Required:A. Prepare the journal entry necessary for Pyle Company to record the acquisition on January 1, 2011. It is expected that the earnings target is likely to be met.B. Prepare the journal entry necessary for Pyle Company in 2012 assuming the earnings contingency was not met.

2-4 Condensed balance sheets for Payne Company and Sigle Company on January 1, 2011 are as follows:

Payne SigleCurrent Assets $ 440,000 $200,000Plant and Equipment (net) 1,080,000 340,000Total Assets $1,520,000 $540,000Total Liabilities $ 230,000 $ 80,000Common Stock, $10 par value 840,000 240,000Other Contributed Capital 300,000 130,000Retained Earnings 150,000 90,000Total Equities $1,520,000 $540,000On January 1, 2011 the stockholders of Payne and Sigle agreed to a consolidation whereby a new corporation, Lawson Company, would be formed to consolidate Payne and Sigle. Lawson Company issued 70,000 shares of its $20 par value common stock for the net assets of Payne and Sigle. On the date of consolidation, the fair values of Payne’s and Sigle’s current assets and liabilities were equal to their book values. The fair value of plant and equipment for each company was: Payne, $1,270,000; Sigle, $360,000.An investment banking house estimated that the fair value of Lawson Company’s common stock was $35 per share. Payne will incur $45,000 of direct acquisition costs and $15,000 in stock issue costs.Required:Prepare the journal entries to record the consolidation on the books of Lawson Company assuming that the consolidation is accounted for as an acquisition.

2-5 The stockholders’ equities of P Corporation and S Corporation were as follows on January 1, 2011:

P Corp. S Corp.Common Stock, $1 par $1,000,000 $ 600,000Other Contributed Capital 2,800,000 1,100,000Retained Earnings 600,000 340,000Total Stockholders’ Equity $4,400,000 $2,040,000On January 2, 2011 P Corp. issued 100,000 of its shares with a market value of $14 per share in exchange for all of S’s shares, and S Corp. was dissolved. P Corp. paid $10,000 to register and issue the new common shares.

Required:Prepare the stockholders’ equity section of P Corp. balance sheet after the business combination on January 2, 2011.2-6 The managers of Petty Company own 10,000 of its 100,000 outstanding common shares. Swann Company is formed by the managers of Petty Company to take over Petty Company in a leveraged buyout. The managers contribute their shares in Petty Company and Swann Company then borrows $675,000 to purchase the remaining 90,000 shares of Petty Company for $600,000; the remaining $75,000 is used for working capital. Petty Company is then merged into Swann Company effective January 1, 2011. Data relevant to Petty Company immediately prior to the leveraged buyout follow:

Book Value Fair ValueCurrent Assets $ 90,000 $ 90,000Plant Assets 255,000 525,000Liabilities (45,000) (45,000)Stockholders’ Equity $300,000 $570,000Required:A. Prepare journal entries on Swann Company’s books to reflect the effects of the leveraged buyout.B. Determine the balance of each of the following immediately after the merger:1. Current Assets2. Plant Assets3. Note Payable4. Common Stock2-7 On January 1, 2010, Presley Company acquired the net assets of Sill Company for $1,580,000 cash. The fair value of Sill’s identifiable net assets was $1,310,000 on his date. Presley Company decided to measure goodwill impairment using the present value of future cash flows to estimate the fair value of the reporting unit (Sill). The information for these subsequent years is as follows:

Carrying value of Fair ValuePresent value Sill’s Identifiable Sill’s IdentifiableYear of Future Cash Flows Net Assets* Net Assets2011 $1,400,000 $1,160,000 $1,190,0002012 $1,400,000 $1,120,000 $1,210,000* Identifiable net assets do not include goodwill.Required:A: For each year determine the amount of goodwill impairment, if any.B: Prepare the journal entries needed each year to record the goodwill impairment (if any) on Presley’s books.2-8 The following balance sheets were reported on January 1, 2011, for Piper Company and Sieler Company:

Piper SielerCash $ 150,000 $ 30,000Inventory 450,000 150,000Equipment (net) 1,320,000 570,000Total $1,920,000 $750,000Total liabilities $ 450,000 $150,000Common stock, $20 par value 600,000 300,000Other contributed capital 375,000 105,000Retained earnings 495,000 195,000Total $1,920,000 $750,000Required:Appraisals reveal that the inventory has a fair value $180,000, and the equipment has a current value of $615,000. The book value and fair value of liabilities are the same. Assuming that Piper Company wishes to acquire Sieler for cash in an asset acquisition, determine the following cutoff amounts:A. The purchase price above which Piper would record goodwill.B. The purchase price at which Piper would record a $50,000 gain.C. The purchase price below which Piper would obtain a “bargain.”D. The purchase price at which Piper would record $75,000 of goodwill.Short Answer

1. SFAS No. 142 requires that goodwill impairment be tested annually for each reporting unit. Discuss the necessary steps of the goodwill impairment test.

2. Briefly describe the different treatment under SFAS 141 vs. SFAS 141R for the following issues:a. Business definitionb. Acquisitions costs

c. In-process R&Dd. Contingent considerationShort Answer Questions from the Textbook

1. When contingent consideration in an acquisition is based on security prices, how should this contingency be reflected on the acquisition date? If the estimate changes during the measurement period, how is this handled? If the estimate changes after the end of the measurement period, how is this adjustment handled? Why?

2. What are pro forma financial statements? What is their purpose?

3. How would a company determine whether goodwill has been impaired?

4. AOL announced that because of an accounting change (FASB Statements Nos. 141R [ASC 805] and142 [ASC 350]), earnings would be increasing 2002, Veritas Software Corporation’s CFO resigned after claiming to have an MBA from Stanford University. On the other hand, Bausch & Lomb Inc.’s board re-fused the CEO’s offer to resign following a questionable claim to have an MBA. Suppose you have been retained by the board of a company where the CEO has ‘overstated’ credentials. This company has a code of ethics and conduct which over the next 25 years by $5.9 billion a year. What change(s) required by FASB (in SFAS Nos. 141Rand 142) resulted in an increase in AOL’s in-come? Would you expect this increase in earnings to have a positive impact on AOL’s stock price? Why or why not?

Business Ethics Question from TextbookThere have been several recent cases of a CEO or CFO resigning or being ousted for misrepresenting academic credentials. For instance, during February 2006,the CEO of RadioShack resigned by ‘mutual agreement’ for inflating his educational background. During states that the employee should always do “the right thing.”(a) What is the board of directors’ responsibility in such matters?(b) What arguments would you make to ask the CEO to resign? What damage might be caused if the decision is made to retain the current CEO?

ACC 401 Week 3 Quiz

ACC 401 Week 3 Quiz Chapter 3

Quiz 2 Chapter 3

Consolidated Financial Statements—Date of Acquisition

Multiple Choice

1. A majority-owned subsidiary that is in legal reorganization should normally be accounted for using

a. consolidated financial statements.b. the equity method.c. the market value method.d. the cost method.2. Under the acquisition method, indirect costs relating to acquisitions should bea. included in the investment cost.b. expensed as incurred.c. deducted from other contributed capital.d. none of these.3. Eliminating entries are made to cancel the effects of intercompany transactions and are made on thea. books of the parent company.b. books of the subsidiary company.c. workpaper only.d. books of both the parent company and the subsidiary.4. One reason a parent company may pay an amount less than the book value of the subsidiary’s stock acquired isa. an undervaluation of the subsidiary’s assets.b. the existence of unrecorded goodwill.c. an overvaluation of the subsidiary’s liabilities.d. none of these.5. In a business combination accounted for as an acquisition, registration costs related to common stock issued by the parent company area. expensed as incurred.b. deducted from other contributed capital.c. included in the investment cost.d. deducted from the investment cost.6. On the consolidated balance sheet, consolidated stockholders’ equity isa. equal to the sum of the parent and subsidiary stockholders’ equity.b. greater than the parent’s stockholders’ equity.c. less than the parent’s stockholders’ equity.d. equal to the parent’s stockholders’ equity.7. Majority-owned subsidiaries should be excluded from the consolidated statements whena. control does not rest with the majority owner.b. the subsidiary operates under governmentally imposed uncertainty.c. a foreign subsidiary is domiciled in a country with foreign exchange restrictions or controls.d. any of these circumstances exist.8. Under the economic entity concept, consolidated financial statements are intended primarily for the benefit of thea. stockholders of the parent company.b. creditors of the parent company.

c. minority stockholders.d. all of the above.9. Reasons a parent company may pay more than book value for the subsidiary company’s stock include all of the following excepta. the fair value of one of the subsidiary’s assets may exceed its recorded value because of appreciation.b. the existence of unrecorded goodwill.c. liabilities may be overvalued.d. stockholders’ equity may be undervalued.10. What is the method of presentation required by SFAS 160 of “non-controlling interest” on a consolidated balance sheet?a. As a deduction from goodwill from consolidation.b. As a separate item within the long-term liabilities section.c. As a part of stockholders’ equity.d. As a separate item between liabilities and stockholders’ equity.11. Which of the following is a limitation of consolidated financial statements?a. Consolidated statements provide no benefit for the stockholders and creditors of the parent company.b. Consolidated statements of highly diversified companies cannot be compared with industry standards.c. Consolidated statements are beneficial only when the consolidated companies operate within the same industry.d. Consolidated statements are beneficial only when the consolidated companies operate in different industries.12. Pine Corp. owns 60% of Sage Corp.’s outstanding common stock. On May 1, 2011, Pine advanced Sage $90,000 in cash, which was still outstanding at December 31, 2011. What portion of this advance should be eliminated in the preparation of the December 31, 2011 consolidated balance sheet?a. $90,000.b. $54,000.c. $36,000.d. $-0-.Use the following information for questions 13-15.

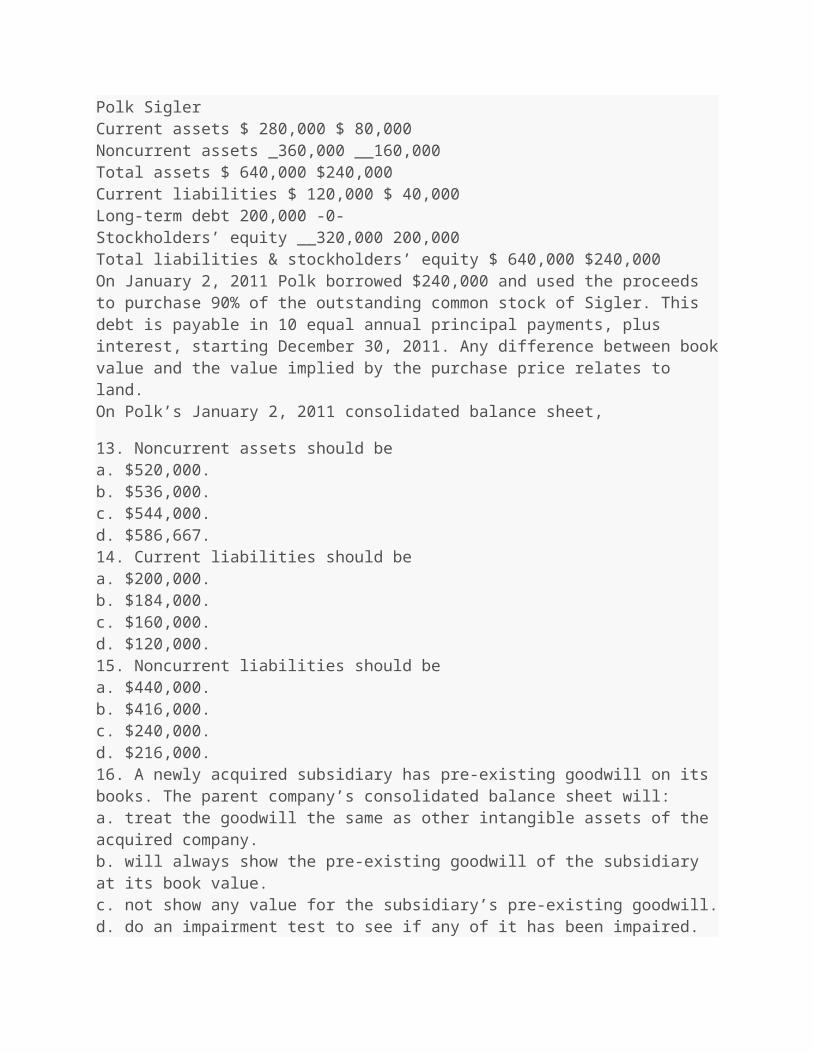

On January 1, 2011, Polk Company and Sigler Company had condensed balance sheets as follows:Polk SiglerCurrent assets $ 280,000 $ 80,000Noncurrent assets _360,000 __160,000Total assets $ 640,000 $240,000

Current liabilities $ 120,000 $ 40,000Long-term debt 200,000 -0-Stockholders’ equity __320,000 200,000Total liabilities & stockholders’ equity $ 640,000 $240,000On January 2, 2011 Polk borrowed $240,000 and used the proceeds to purchase 90% of the outstanding common stock of Sigler. This debt is payable in 10 equal annual principal payments, plus interest, starting December 30, 2011. Any difference between book value and the value implied by the purchase price relates to land.On Polk’s January 2, 2011 consolidated balance sheet,

13. Noncurrent assets should bea. $520,000.b. $536,000.c. $544,000.d. $586,667.14. Current liabilities should bea. $200,000.b. $184,000.c. $160,000.d. $120,000.15. Noncurrent liabilities should bea. $440,000.b. $416,000.c. $240,000.d. $216,000.16. A newly acquired subsidiary has pre-existing goodwill on its books. The parent company’s consolidated balance sheet will:a. treat the goodwill the same as other intangible assets of the acquired company.b. will always show the pre-existing goodwill of the subsidiary at its book value.c. not show any value for the subsidiary’s pre-existing goodwill.d. do an impairment test to see if any of it has been impaired.17. The Difference between Implied and Book Value account is:a. an account necessary for the preparation of consolidated working papers.b. used in allocating the amounts paid for recorded balance sheet accounts that are different thantheir fair values.c. the excess implied value assigned to goodwill.d. the unamortized excess that cannot be assigned to any related balance sheet accounts18. The main evidence of control for purposes of consolidated financial statements involvesa. possessing majority ownershipb. having decision-making ability that is not shared with others.

c. being the sole shareholderd. having the parent company and the subsidiary participating in the same industry.19. In which of the following cases would consolidation be inappropriate?a. The subsidiary is in bankruptcy.b. Subsidiary’s operations are dissimilar from those of the parent.c. The parent owns 90 percent of the subsidiary’s common stock, but all of the subsidiary’s nonvoting preferred stock is held by a single investor.d. Subsidiary is foreign.20. Princeton Company acquired 75 percent of the common stock of Sheffield Corporation on December 31, 2011. On the date of acquisition, Princeton held land with a book value of $150,000 and a fair value of $300,000; Sheffield held land with a book value of $100,000 and fair value of $500,000. What amount would land be reported in the consolidated balance sheet prepared immediately after the combination?a. $650,000b. $500,000c. $550,000d. $375,000Use the following information to answer questions 21 – 23.

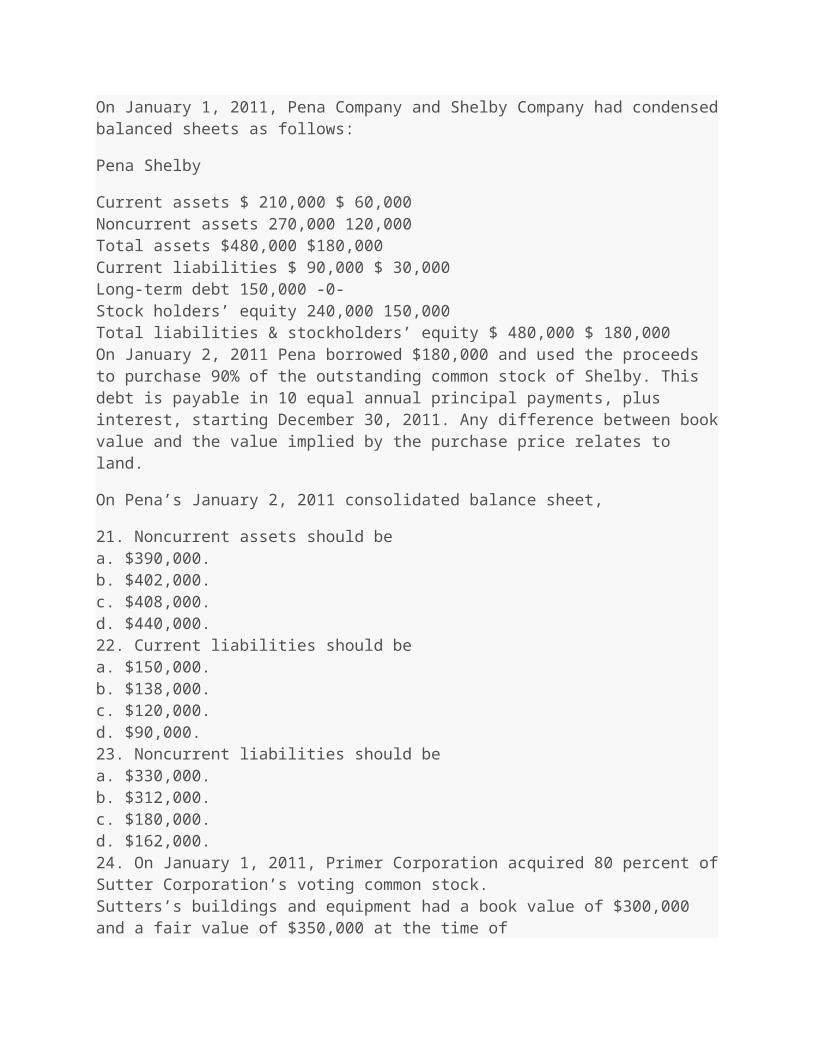

On January 1, 2011, Pena Company and Shelby Company had condensed balanced sheets as follows:

Pena Shelby

Current assets $ 210,000 $ 60,000Noncurrent assets 270,000 120,000Total assets $480,000 $180,000Current liabilities $ 90,000 $ 30,000Long-term debt 150,000 -0-Stock holders’ equity 240,000 150,000Total liabilities & stockholders’ equity $ 480,000 $ 180,000On January 2, 2011 Pena borrowed $180,000 and used the proceeds to purchase 90% of the outstanding common stock of Shelby. This debt is payable in 10 equal annual principal payments, plus interest, starting December 30, 2011. Any difference between book value and the value implied by the purchase price relates to land.

On Pena’s January 2, 2011 consolidated balance sheet,

21. Noncurrent assets should bea. $390,000.b. $402,000.

c. $408,000.d. $440,000.22. Current liabilities should bea. $150,000.b. $138,000.c. $120,000.d. $90,000.23. Noncurrent liabilities should bea. $330,000.b. $312,000.c. $180,000.d. $162,000.24. On January 1, 2011, Primer Corporation acquired 80 percent of Sutter Corporation’s voting common stock.Sutters’s buildings and equipment had a book value of $300,000 and a fair value of $350,000 at the time ofacquisition. At what amount will Sutter’s buildings and equipment will be reported in the consolidatedstatements ?a. $350,000b. $340,000c. $280,000d. $300,000Problems

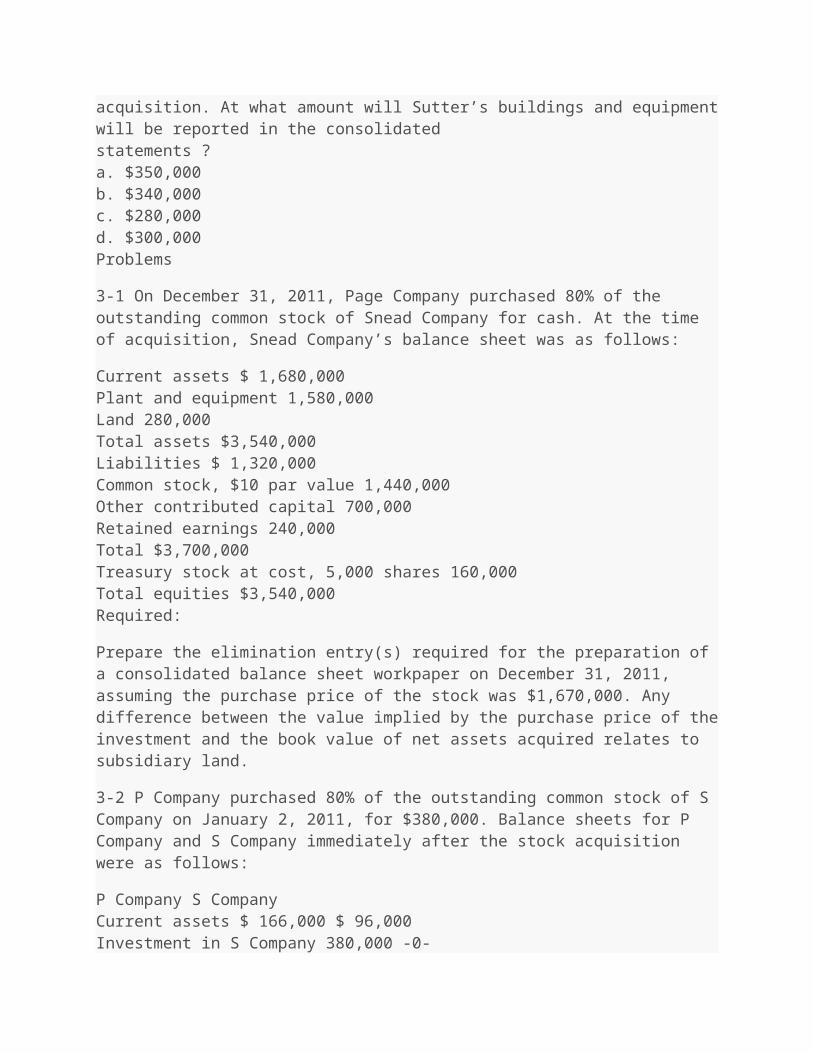

3-1 On December 31, 2011, Page Company purchased 80% of the outstanding common stock of Snead Company for cash. At the time of acquisition, Snead Company’s balance sheet was as follows:

Current assets $ 1,680,000Plant and equipment 1,580,000Land 280,000Total assets $3,540,000Liabilities $ 1,320,000Common stock, $10 par value 1,440,000Other contributed capital 700,000Retained earnings 240,000Total $3,700,000Treasury stock at cost, 5,000 shares 160,000Total equities $3,540,000Required:

Prepare the elimination entry(s) required for the preparation of a consolidated balance sheet workpaper on December 31, 2011, assuming the purchase price of the stock was $1,670,000. Any difference between the value implied by the purchase price of the investment and the book value of net assets acquired relates to subsidiary land.

3-2 P Company purchased 80% of the outstanding common stock of S Company on January 2, 2011, for $380,000. Balance sheets for P Company and S Company immediately after the stock acquisition were as follows:

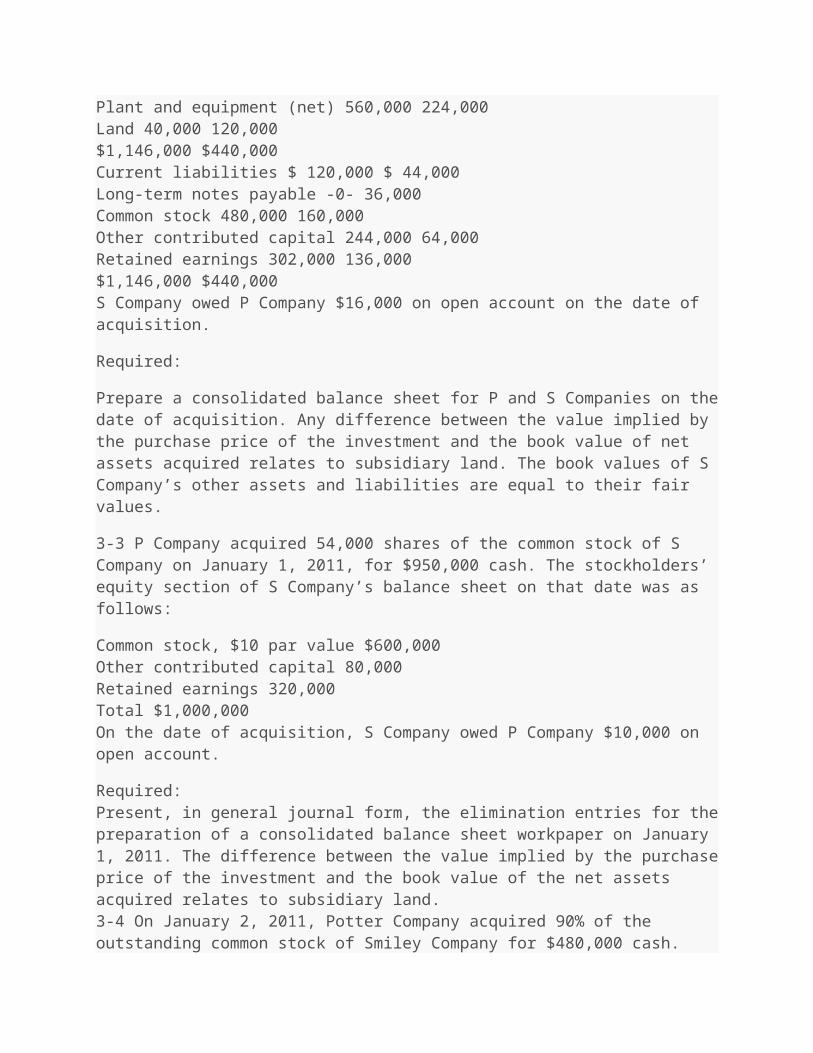

P Company S CompanyCurrent assets $ 166,000 $ 96,000Investment in S Company 380,000 -0-Plant and equipment (net) 560,000 224,000Land 40,000 120,000$1,146,000 $440,000Current liabilities $ 120,000 $ 44,000Long-term notes payable -0- 36,000Common stock 480,000 160,000Other contributed capital 244,000 64,000Retained earnings 302,000 136,000$1,146,000 $440,000S Company owed P Company $16,000 on open account on the date of acquisition.

Required:

Prepare a consolidated balance sheet for P and S Companies on the date of acquisition. Any difference between the value implied by the purchase price of the investment and the book value of net assets acquired relates to subsidiary land. The book values of S Company’s other assets and liabilities are equal to their fair values.

3-3 P Company acquired 54,000 shares of the common stock of S Company on January 1, 2011, for $950,000 cash. The stockholders’ equity section of S Company’s balance sheet on that date was as follows:

Common stock, $10 par value $600,000Other contributed capital 80,000Retained earnings 320,000Total $1,000,000On the date of acquisition, S Company owed P Company $10,000 on open account.

Required:Present, in general journal form, the elimination entries for the preparation of a consolidated balance sheet workpaper on January 1, 2011. The difference between the value implied by the

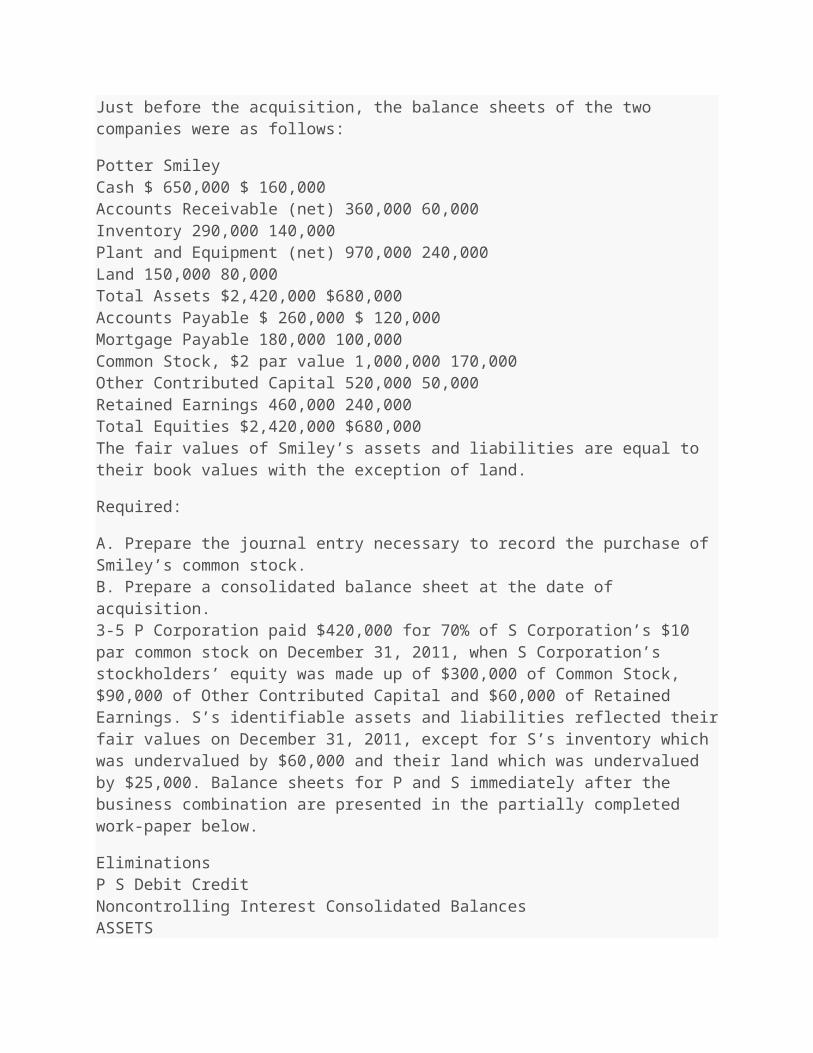

purchase price of the investment and the book value of the net assets acquired relates to subsidiary land.3-4 On January 2, 2011, Potter Company acquired 90% of the outstanding common stock of Smiley Company for $480,000 cash. Just before the acquisition, the balance sheets of the two companies were as follows:

Potter SmileyCash $ 650,000 $ 160,000Accounts Receivable (net) 360,000 60,000Inventory 290,000 140,000Plant and Equipment (net) 970,000 240,000Land 150,000 80,000Total Assets $2,420,000 $680,000Accounts Payable $ 260,000 $ 120,000Mortgage Payable 180,000 100,000Common Stock, $2 par value 1,000,000 170,000Other Contributed Capital 520,000 50,000Retained Earnings 460,000 240,000Total Equities $2,420,000 $680,000The fair values of Smiley’s assets and liabilities are equal to their book values with the exception of land.

Required:

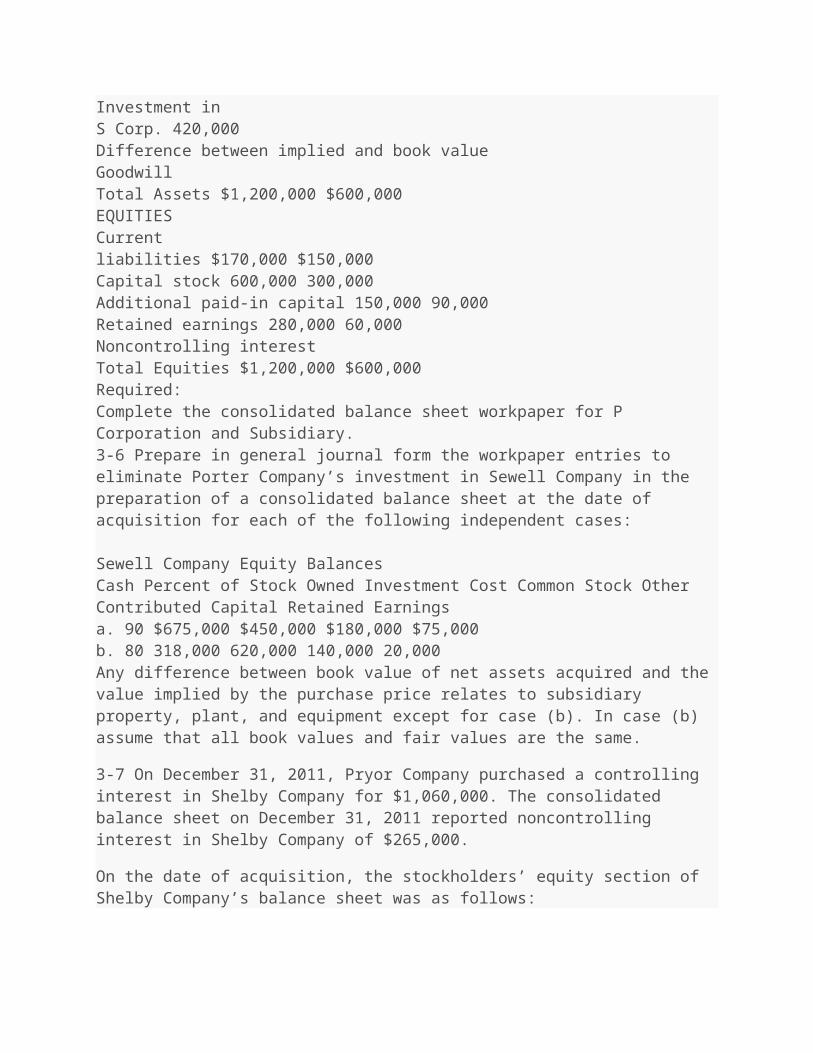

A. Prepare the journal entry necessary to record the purchase of Smiley’s common stock.B. Prepare a consolidated balance sheet at the date of acquisition.3-5 P Corporation paid $420,000 for 70% of S Corporation’s $10 par common stock on December 31, 2011, when S Corporation’s stockholders’ equity was made up of $300,000 of Common Stock, $90,000 of Other Contributed Capital and $60,000 of Retained Earnings. S’s identifiable assets and liabilities reflected their fair values on December 31, 2011, except for S’s inventory which was undervalued by $60,000 and their land which was undervalued by $25,000. Balance sheets for P and S immediately after the business combination are presented in the partially completed work-paper below.

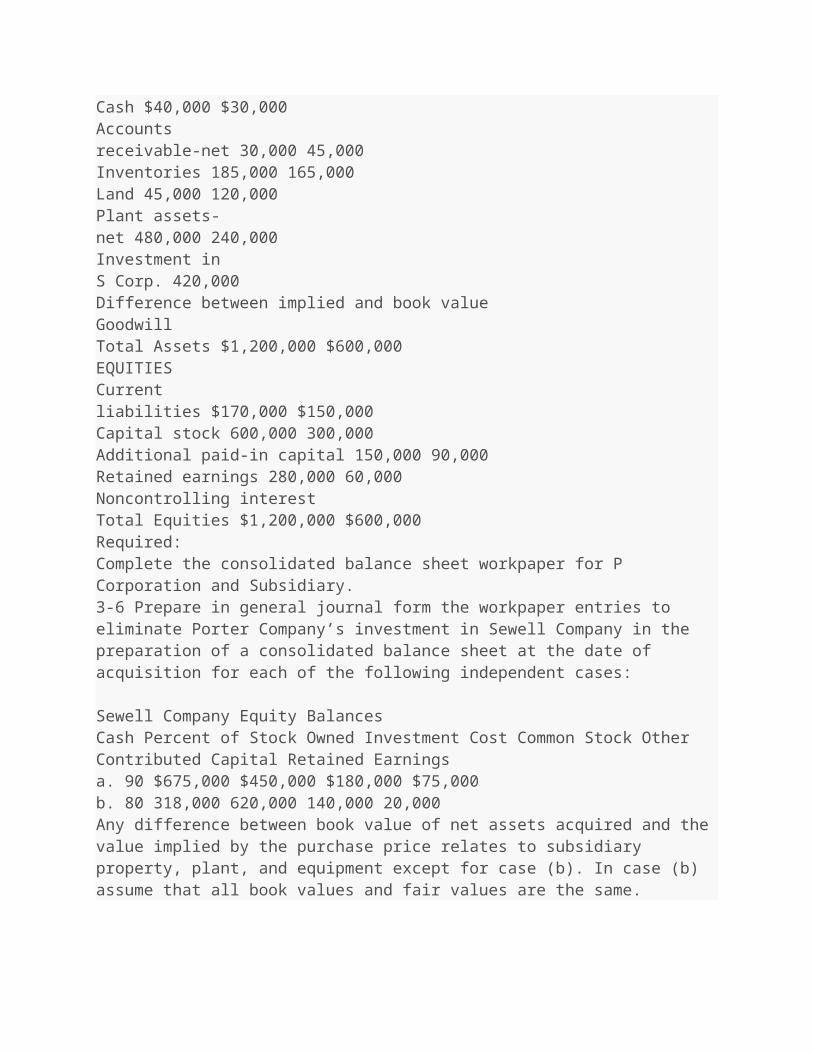

EliminationsP S Debit CreditNoncontrolling Interest Consolidated BalancesASSETSCash $40,000 $30,000Accountsreceivable-net 30,000 45,000Inventories 185,000 165,000

Land 45,000 120,000Plant assets-net 480,000 240,000Investment inS Corp. 420,000Difference between implied and book valueGoodwillTotal Assets $1,200,000 $600,000EQUITIESCurrentliabilities $170,000 $150,000Capital stock 600,000 300,000Additional paid-in capital 150,000 90,000Retained earnings 280,000 60,000Noncontrolling interestTotal Equities $1,200,000 $600,000Required:Complete the consolidated balance sheet workpaper for P Corporation and Subsidiary.3-6 Prepare in general journal form the workpaper entries to eliminate Porter Company’s investment in Sewell Company in the preparation of a consolidated balance sheet at the date of acquisition for each of the following independent cases: Sewell Company Equity BalancesCash Percent of Stock Owned Investment Cost Common Stock Other Contributed Capital Retained Earningsa. 90 $675,000 $450,000 $180,000 $75,000b. 80 318,000 620,000 140,000 20,000Any difference between book value of net assets acquired and the value implied by the purchase price relates to subsidiary property, plant, and equipment except for case (b). In case (b) assume that all book values and fair values are the same.

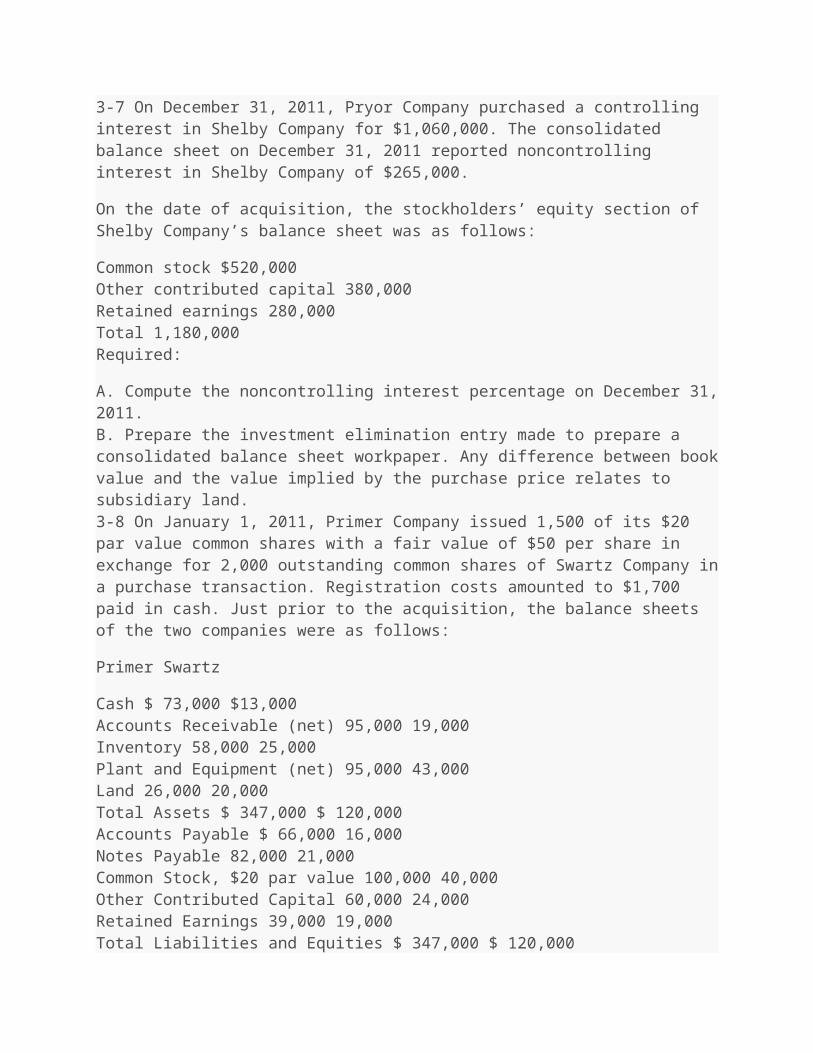

3-7 On December 31, 2011, Pryor Company purchased a controlling interest in Shelby Company for $1,060,000. The consolidated balance sheet on December 31, 2011 reported noncontrolling interest in Shelby Company of $265,000.

On the date of acquisition, the stockholders’ equity section of Shelby Company’s balance sheet was as follows:

Common stock $520,000Other contributed capital 380,000Retained earnings 280,000Total 1,180,000

Required:

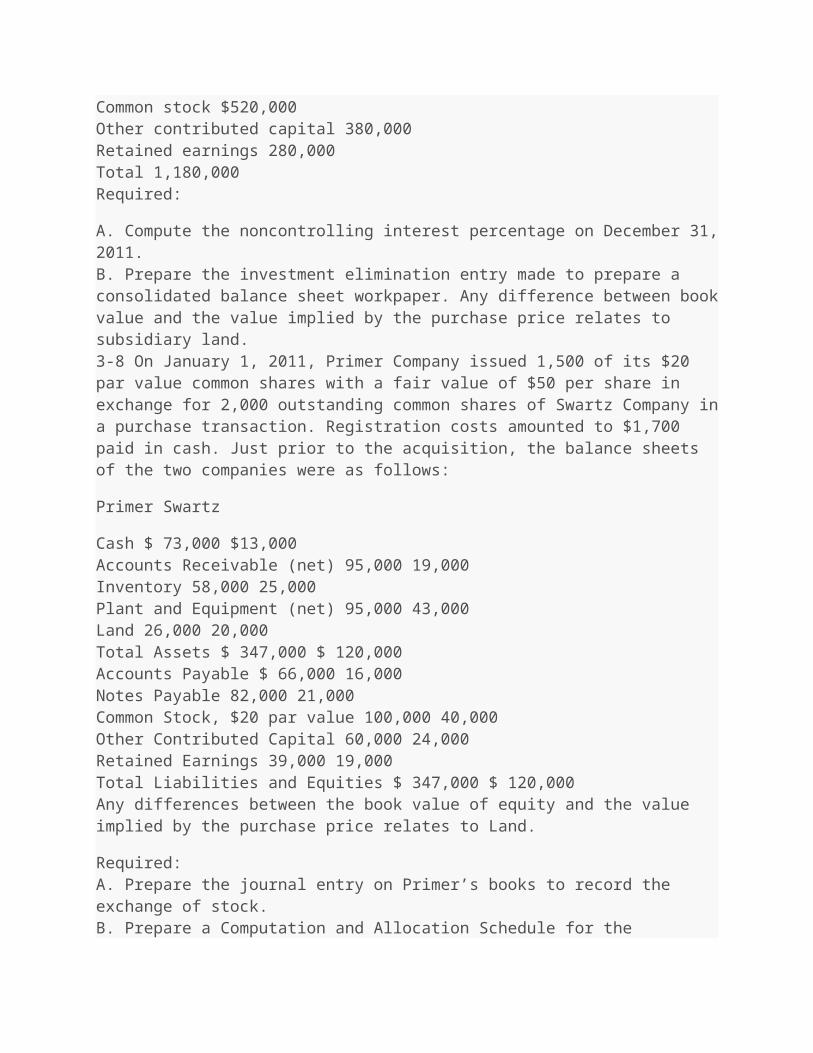

A. Compute the noncontrolling interest percentage on December 31, 2011.B. Prepare the investment elimination entry made to prepare a consolidated balance sheet workpaper. Any difference between book value and the value implied by the purchase price relates to subsidiary land.3-8 On January 1, 2011, Primer Company issued 1,500 of its $20 par value common shares with a fair value of $50 per share in exchange for 2,000 outstanding common shares of Swartz Company in a purchase transaction. Registration costs amounted to $1,700 paid in cash. Just prior to the acquisition, the balance sheets of the two companies were as follows:

Primer Swartz

Cash $ 73,000 $13,000Accounts Receivable (net) 95,000 19,000Inventory 58,000 25,000Plant and Equipment (net) 95,000 43,000Land 26,000 20,000Total Assets $ 347,000 $ 120,000Accounts Payable $ 66,000 16,000Notes Payable 82,000 21,000Common Stock, $20 par value 100,000 40,000Other Contributed Capital 60,000 24,000Retained Earnings 39,000 19,000Total Liabilities and Equities $ 347,000 $ 120,000Any differences between the book value of equity and the value implied by the purchase price relates to Land.

Required:A. Prepare the journal entry on Primer’s books to record the exchange of stock.B. Prepare a Computation and Allocation Schedule for the Difference between book value and value implied by the purchase price.C. Calculate the consolidated balance for each of the following accounts as of December 31, 2011:1. Cash2. Land3. Common Stock4. Other Contributed CapitalShort Answer

1. There are several reasons why a company would acquire a subsidiary’s voting common stock rather than its net assets. Identify at least two advantages to acquiring a controlling interest in the voting stock of another company rather than its assets.

2. A useful first step in the consolidating process is to prepare a Computation and Allocation of Difference (CAD) Schedule. Identify the steps involved in preparing the CAD schedule.

Short Answer Questions from the Textbook

1. What are the advantages of acquiring the majority of the voting stock of another company rather than acquiring all its voting stock?

2. What is the justification for preparing consolidated financial statements when, in fact, it is ap-parent that the consolidated group is not a legal entity?

3. Why is it often necessary to prepare separate financial statements for each legal entity in a consolidated group even though consolidated statements provide a better economic picture of the combined activities?

4. What aspects of control must exist before a subsidiary is consolidated?

5. Why are consolidated work papers used in pre-paring consolidated financial statements?

6. Define noncontrolling (minority) interest. List three methods that might be used for reporting the noncontrolling interest in a consolidated balance sheet, and state which is preferred under the SFAS No. 160[topic 810].

7. Give several reasons why a parent company would be willing to pay more than book value for subsidiary stock acquired.

8. What effect do subsidiary treasury stock holdings have at the time the subsidiary is acquired? How should the treasury stock be treated on consolidated work papers?

9. What effect does a noncontrolling interest have on the amount of intercompany receivables and payables eliminated on a consolidated balance sheet?

10 A.SFAS No. 109and SFAS No. 141R[ASC 740 and805] require that a deferred tax asset or liability be recognized for likely differences between the reported values and tax bases of assets and liabilities recognized in business combinations (for example, in exchanges that are nontaxable to the selling shareholders). Does this decision change the amount of consolidated net income reported in years subsequent to the business combination? Explain.

Business Ethics Question from the Textbook

Part I. You are working on the valuation of accounts receivable, and bad debt reserves for the current year’s annual report. The CFO stops by and asks you to reduce the reserve by enough to increase the current year’s EPS by 2 cents a share. The company’s policy has always been to use the previous year’s actual bad debt percentage adjusted for a specific economic index. The CFO’s suggested change would still be within acceptable GAAP. However, later, you learn that with the increased EPS, the CFO would qualify for a significant bonus. What do you do and why?

Part II. Consider the following: Accounting firm KPMG created tax shelters called BLIPS, FLIP, OPIS, and SOS that were based largely in the Cayman Islands and allowed wealthy clients (there were 186) to create $5 billion in losses, which were then deducted from their income for IRS tax purposes. BLIPS (Bond Linked Issue Premium Structures) had clients borrow from an offshore bank for purposes of purchasing currency. The client would then sell the currency back to the lender for a loss. However, the IRS contends the losses were phony and that there was never any risk to the client in the deals. The IRS has indicted eight former KPMG partners and an outside lawyer alleging that the transactions were shams, illegal methods for avoiding taxes. KPMG has agreed to pay a$456 million fine, no longer to do tax shelters, and to cooperate with the government in its prosecution of the nine individuals involved in the tax shelter scheme. Many argue that the courts have not always held that such tax avoidance schemes show criminal intent because the tax laws permit individuals to minimize taxes. However, the IRS argues that these shelters evidence intent because of the lack of risk.

QuestionIn this case, the IRS contends that the losses generated by the tax shelters were phony and that the clients never incurred any risk. Do tax avoidance schemes indicate criminal intent if the tax laws permit individuals to minimize taxes? Justify your answer.

ACC 401 Week 4 Quiz

ACC 401 Week 4 Quiz Chapter 4

Quiz 3 Chapter 4

Consolidated Financial Statements after Acquisition

1. An investor adjusts the investment account for the amortization of any difference between cost and book value under thea. cost method.b. complete equity method.c. partial equity method.d. complete and partial equity methods.

2. Under the partial equity method, the entry to eliminate subsidiary income and dividends includes a debit toa. Dividend Income.b. Dividends Declared – S Company.c. Equity in Subsidiary Income.d. Retained Earnings – S Company.3. On the consolidated statement of cash flows, the parent’s acquisition of additional shares of the subsidiary’s stock directly from the subsidiary is reported asa. an investing activity.b. a financing activity.c. an operating activity.d. none of these.4. Under the cost method, the workpaper entry to establish reciprocitya. debits Retained Earnings – S Company.b. credits Retained Earnings – S Company.c. debits Retained Earnings – P Company.d. credits Retained Earnings – P Company.5. Under the cost method, the investment account is reduced whena. there is a liquidating dividend.b. the subsidiary declares a cash dividend.c. the subsidiary incurs a net loss.d. none of these.6. The parent company records its share of a subsidiary’s income bya. crediting Investment in S Company under the partial equity method.b. crediting Equity in Subsidiary Income under both the cost and partial equity methods.c. debiting Equity in Subsidiary Income under the cost method.d. none of these.7. In years subsequent to the year of acquisition, an entry to establish reciprocity is made under thea. complete equity method.b. cost method.c. partial equity method.d. complete and partial equity methods.8. A parent company received dividends in excess of the parent company’s share of the subsidiary’s earnings subsequent to the date of the investment. How will the parent company’s investment account be affected by those dividends under each of the following accounting methods?

Cost Method Partial Equity Methoda. No effect No effectb. Decrease No effect

c. No effect Decreased. Decrease Decrease9. P Company purchased 80% of the outstanding common stock of S Company on May 1, 2011, for a cash payment of $1,272,000. S Company’s December 31, 2010 balance sheet reported common stock of $800,000 and retained earnings of $540,000. During the calendar year 2011, S Company earned $840,000 evenly throughout the year and declared a dividend of $300,000 on November 1. What is the amount needed to establish reciprocity under the cost method in the preparation of a consolidated workpaper on December 31, 2012?a. $208,000b. $260,000c. $248,000d. $432,00010. P Company purchased 90% of the outstanding common stock of S Company on January 1, 1997. S Company’s stockholders’ equity at various dates was:1/1/97 1/1/11 12/31/11Common stock $400,000 $400,000 $400,000Retained earnings 120,000 380,000 460,000Total $520,000 $780,000 $860,000The workpaper entry to establish reciprocity under the cost method in the preparation of a consolidated statements workpaper on December 31, 2011 should include a credit to P Company’s retained earnings ofa. $80,000.b. $234,000.c. $260,000.d. $306,000.11. Consolidated net income for a parent company and its partially owned subsidiary is best defined as the parent company’sa. recorded net income.b. recorded net income plus the subsidiary’s recorded net income.c. recorded net income plus the its share of the subsidiary’s recorded net income.d. income from independent operations plus subsidiary’s income resulting from transactions with outside parties.12. In the preparation of a consolidated statements workpaper, dividend income recognized by a parent company for dividends distributed by its subsidiary isa. included with parent company income from other sources to constitute consolidated net income.b. assigned as a component of the noncontrolling interest.c. allocated proportionately to consolidated net income and the noncontrolling interest.d. eliminated.13. In the preparation of a consolidated statement of cash flows using the indirect method of presenting cash flows from operating activities, the amount of the noncontrolling interest in

consolidated income isa. combined with the controlling interest in consolidated net income.b. deducted from the controlling interest in consolidated net income.c. reported as a significant noncash investing and financing activity in the notes.d. reported as a component of cash flows from financing activities.14. On October 1, 2011, Parr Company acquired for cash all of the voting common stock of Stein Company. The purchase price of Stein’s stock equaled the book value and fair value of Stein’s net assets. The separate net income for each company, excluding Parr’s share of income from Stein was as follows:Parr SteinTwelve months ended 12/31/11 $4,500,000 $2,700,000Three months ended 12/31/11 495,000 450,000During September, Stein paid $150,000 in dividends to its stockholders. For the year ended December 31, 2011, Parr issued parent company only financial statements. These statements are not considered those of the primary reporting entity. Under the partial equity method, what is the amount of net income reported in Parr’s income statement?a. $7,200,000.b. $4,650,000.c. $4,950,000.d. $1,800,000.15. A parent company uses the partial equity method to account for an investment in common stock of its subsidiary. A portion of the dividends received this year were in excess of the parent company’s share of the subsidiary’s earnings subsequent to the date of the investment. The amount of dividend income that should be reported in the parent company’s separate income statement should bea. zero.b. the total amount of dividends received this year.c. the portion of the dividends received this year that were in excess of the parent’s share of subsidiary’s earnings subsequent to the date of investment.d. the portion of the dividends received this year that were NOT in excess of the parent’s share of subsidiary’s earnings subsequent to the date of investment.16. Masters, Inc. owns 40% of Fields Corporation. During the year, Fields had net earnings of $200,000 and paid dividends of $50,000. Masters used the cost method of accounting. What effect would this have on the investment account, net earnings, and retained earnings, respectively?a. understate, overstate, overstate.b. overstate, understate, understatec. overstate, overstate, overstated. understate, understate, understateUse the following information in answering questions 17 and 18.

17. Prior Industries acquired a 70 percent interest in Stevenson Company by purchasing 14,000 of its 20,000 outstanding shares of common stock at book value of $210,000 on January 1, 2010. Stevenson reported net income in 2010 of $90,000 and in 2011 of $120,000 earned evenly throughout the respective years. Prior received $24,000 dividends from Stevenson in 2010 and $36,000 in 2011. Prior uses the equity method to record its investment.

Prior should record investment income from Stevenson during 2011 of:a. $36,000b. $120,000c. $84,000d. $48,00018. The balance of Prior’s Investment in Stevenson account at December 31, 2011 is:a. $210,000b. $285,000c. $297,000d. $315,00019. Parkview Company acquired a 90% interest in Sutherland Company on December 31, 2010, for $320,000. During 2011 Sutherland had a net income of $22,000 and paid a cash dividend of $7,000. Applying the cost method would give a debit balance in the Investment in Stock of Sutherland Company account at the end of 2011 of:a. $335,000b. $333,500c. $313,700d. $320,00020. Hall, Inc., owns 40% of the outstanding stock of Gloom Company. During 2011, Hall received a $4,000 cash dividend from Gloom. What effect did this dividend have on Hall’s 2011 financial statements?a. Increased total assets.b. Decreased total assets.c. Increased income.d. Decreased investment account.21. P Company purchased 80% of the outstanding common stock of S Company on May 1, 2011, for a cash payment of $318,000. S Company’s December 31, 2010 balance sheet reported common stock of $200,000 and retained earnings of $180,000. During the calendar year 2011, S Company earned $210,000 evenly throughout the year and declared a dividend of $75,000 on November 1. What is the amount needed to establish reciprocity under the cost method in the preparation of a consolidated workpaper on December 31, 2011?a. $52,000b. $65,000c. $62,000d. $108,000

22. P Company purchased 90% of the outstanding common stock of S Company on January 1, 1997. S Company’s stockholders’ equity at various dates was:1/1/97 1/1/11 12/31/11Common stock $200,000 $200,000 $200,000Retained earnings 60,000 190,000 230,000Total $260,000 $390,000 $430,000The workpaper entry to establish reciprocity under the cost method in the preparation of a consolidated statements workpaper on December 31, 2011 should include a credit to P Company’s retained earnings ofa. $40,000.b. $117,000.c. $130,000.d. $153,000.Use the following information in answering questions 23 and 24.

23. Prior Industries acquired an 80 percent interest in Sanderson Company by purchasing 24,000 of its 30,000 outstanding shares of common stock at book value of $105,000 on January 1, 2010. Sanderson reported net income in 2010 of $45,000 and in 2011 of $60,000 earned evenly throughout the respective years. Prior received $12,000 dividends from Sanderson in 2010 and $18,000 in 2011. Prior uses the equity method to record its investment.

Prior should record investment income from Sanderson during 2011 of:a. $18,000.b. $60,000.c. $48,000.d. $33,600.24. The balance of Prior’s Investment in Sanderson account at December 31, 2011 is:a. $105,000.b. $138,600.c. $159,000.d. $165,000.25. Pendleton Company acquired a 70% interest in Sunflower Company on December 31, 2010, for $380,000. During 2011 Sunflower had a net income of $30,000 and paid a cash dividend of $10,000. Applying the cost method would give a debit balance in the Investment in Stock of Sunflower Company account at the end of 2011 of:a. $400,000.b. $394,000.c. $373,000.d. $380,000.Use the following information to answer questions 26 and 27

On January 1, 2011, Rotor Corporation acquired 30 percent of Stator Company’s stock for $150,000. On the acquisition date, Stator reported net assets of $450,000 valued at historical cost and $500,000 stated at fair value. The difference was due to the increased value of buildings with a remaining life of 10 years. During 2011 Stator reported net income of $25,000 and paid dividends of $10,000. Rotor uses the equity method.

26. What will be the balance in the Investment account as of Dec 31, 2011?a. $150,000b. $157,500c. $154,500d. $153,00027. What amount of investment income will be reported by Rotor for the year 2011?a. $7,500b. $6,000c. $4,500d. $25,00028. On January 1, 2011, Potter Company purchased 25 % of Smith Company’s common stock; no goodwill resulted from the acquisition. Potter Company appropriately carries the investment using the equity method of accounting and the balance in Potter’s investment account was $190,000 on December 31, 2011. Smith reported net income of $120,000 for the year ended December 31, 2011 and paid dividends on its common stock totaling $48,000 during 2011. How much did Potter pay for its 25% interest in Smith?a. $172,000b. $202,000c. $208,000d. $232,000Use the following information to answer questions 29 and 30.

29. On January 1, 2011, Paterson Company purchased 40% of Stratton Company’s 30,000 shares of voting common stock for a cash payment of $1,800,000 when 40% of the net book value of Stratton Company was $1,740,000. The payment in excess of the net book value was attributed to depreciable assets with a remaining useful life of six years. As a result of this transaction Paterson has the ability to exercise significant influence over Stratton Company’s operating and financial policies. Stratton’s net income for the ended December 31, 2011 was $600,000. During 2011, Stratton paid $325,000 in dividends to its shareholders. The income reported by Paterson for its investment in Stratton should be:a. $120,000b. $130,000c. $230,000d. $240,000

30. What is the ending balance in Paterson’s investment account as of December 31, 2011?a. $1,800,000b. $1,900,000c. $1,910,000d. $2,030,000Problems4-1 On January 1, 2011, Price Company purchased an 80% interest in the common stock of Stahl Company for $1,040,000, which was $60,000 greater than the book value of equity acquired. The difference between implied and book value relates to the subsidiary’s land.

The following information is from the consolidated retained earnings section of the consolidated statements workpaper for the year ended December 31, 2011:

STAHL CONSOLIDATEDCOMPANY BALANCES1/01/11 retained earnings $300,000 $1,400,000Net income 220,000 680,000Dividends declared (80,000) (140,000)12/31/11 retained earnings $440,000 $1,940,000Stahl’s stockholders’ equity includes only common stock and retained earnings.

Required:

A. Prepare the workpaper eliminating entries for a consolidated statements workpaper on December 31, 2011. Price uses the cost method.

B. Compute the total noncontrolling interest to be reported on the consolidated balance sheet on December 31, 2011.

4-2 On October 1, 2011, Packer Company purchased 90% of the common stock of Shipley Company for $290,000. Additional information for both companies for 2011 follows:

PACKER SHIPLEYCommon stock $300,000 $90,000Other contributed capital 120,000 40,000Retained Earnings, 1/1 240,000 50,000Net Income 260,000 160,000Dividends declared (10/31) 40,000 8,000Any difference between implied and book value relates to Shipley’s land. Packer uses the cost method to record its investment in Shipley. Shipley Company’s income was earned evenly throughout the year.

Required:

A. Prepare the workpaper entries that would be made on a consolidated statements workpaper on December 31, 2011. Use the full year reporting alternative.

B. Calculate the controlling interest in consolidated net income for 2011.

4-3 On January 1, 2011, Pierce Company purchased 80% of the common stock of Stanley Company for $600,000. At that time, Stanley’s stockholders’ equity consisted of the following:

Common stock $220,000Other contributed capital 90,000Retained earnings 320,000During 2011, Stanley distributed a dividend in the amount of $120,000 and at year-end reported a $320,000 net income. Any difference between implied and book value relates to subsidiary goodwill. Pierce Company uses the equity method to record its investment. No impairment of goodwill is observed in the first year.

Required:

A. Prepare on Pierce Company’s books journal entries to record the investment related activities for 2011.

B. Prepare the workpaper eliminating entries for a workpaper on December 31, 2011.

4-4 Pratt Company purchased 80% of the outstanding common stock of Selby Company on January 2, 2004, for $680,000. The composition of Selby Company’s stockholders’ equity on January 2, 2004, and December 31, 2011, was:1/2/04 12/31/11Common stock $540,000 $540,000Other contributed capital 325,000 325,000Retained earnings (deficit) (60,000) 295,000Total stockholders’ equity $805,000 $1,160,000During 2011, Selby Company earned $210,000 net income and declared a $60,000 dividend. Any difference between implied and book value relates to land. Pratt Company uses the cost method to record its investment in Selby Company.

Required:

A. Prepare any journal entries that Pratt Company would make on its books during 2011 to record the effects of its investment in Selby Company.

B. Prepare, in general journal form, all workpaper entries needed for the preparation of a consolidated statements workpaper on December 31, 2011.

4-5 P Company purchased 90% of the common stock of S Company on January 2, 2011 for $900,000. On that date, S Company’s stockholders’ equity was as follows:

Common stock, $20 par value $400,000Other contributed capital 100,000Retained earnings 450,000During 2011, S Company earned $200,000 and declared a $100,000 dividend. P Company uses the partial equity method to record its investment in S Company. The difference between implied and book value relates to land.

Required:

Prepared, in general journal form, all eliminating entries for the preparation of a consolidated statements workpaper on December 31, 2011.

4-6 Pair Company acquired 80% of the outstanding common stock of Sax Company on January 2, 2010 for $675,000. At that time, Sax’s total stockholders’ equity amounted to $1,000,000. Sax Company reported net income and dividends for the last two years as follows:

2010 2011Reported net income $45,000 $60,000Dividends distributed 35,000 75,000Required:

Prepare journal entries for Pair Company for 2010 and 2011 assuming Pair uses:A. The cost method to record its investmentB. The complete equity method to record its investment. The difference between implied value and the book value of equity acquired was attributed solely to a building, with a 20-year expected life.4-7 Pell Company purchased 90% of the stock of Silk Company on January 1, 2007, for $1,860,000, an amount equal to $60,000 in excess of the book value of equity acquired. All book values were equal to fair values at the time of purchase (i.e., any excess payment relates to subsidiary goodwill). On the date of purchase, Silk Company’s retained earnings balance was $200,000. The remainder of the stockholders’ equity consists of no-par common stock. During 2011, Silk Company declared dividends in the amount of $40,000, and reported net income of $160,000. The retained earnings balance of Silk Company on December 31, 2010 was $640,000. Pell Company uses the cost method to record its investment. No impairment of goodwill was recognized between the date of acquisition and December 31, 2011.

Required:

Prepare in general journal form the workpaper entries that would be made in the preparation of a consolidated statements workpaper on December 31, 2011.