Embed Size (px)

Citation preview

Vimo SEWA – Health Insurance

SEWA VIMOSEWA

Our Approach

• SEWA aims to provide total social security to its members.

• We observed that lack of risk financing for health risks was pulling our members back into the vicious cycle of poverty.

• SEWA has an extensive health program and insurance makes it an integrated health intervention.

The Products

• It’s a medical reimbursement plans on lines of a regular medi-claim policy

• The coverage limits are up to Rs.2000 to Rs. 6000, as per the schemes chosen

• Minimum age of entry – 03 months

• Maximum age of entry - 55 Years

• Coverage is available up to 70 years of age

The Products

• 24 Hour Hospitalization is the minimum criterion to make a claim

• Conditions like fractures and cataract covered without hospitalization

• Pre existing disease are covered after one year of policy.

• Documents needed – Doctor’s prescription, Hospital bills, medicine bills etc.

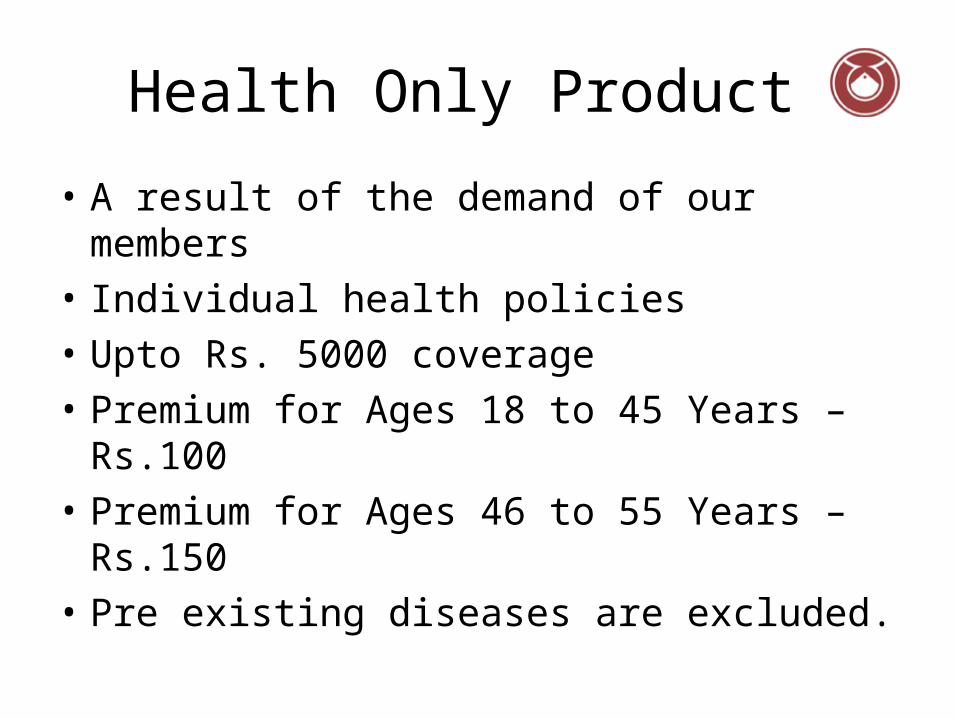

Health Only Product

• A result of the demand of our members

• Individual health policies

• Upto Rs. 5000 coverage

• Premium for Ages 18 to 45 Years – Rs.100

• Premium for Ages 46 to 55 Years – Rs.150

• Pre existing diseases are excluded.

Claims process

• In house claims settlement through a claims settlement committee comprising of qualified doctors, insurance experts and grass root representatives.

• In Ahmedabad city we follow the prompt reimbursement system

• In rest of the areas, we do the normal health claim reimbursement

Normal Health Claim settlement

The member makes the claim by sending all the relevant documents to the vimo office through Aagewaans/ partner organization or directly

The claims are scrutinized by the internal claims committee including doctors

The claims can be approved or rejected or recommended for a revisit due to lack of relevant documents

The rejected and revisit claims are sent back to members, in case of revisit the claim is made again with proper documents

Approved claims are sent to the insurance partner which settles it within 7 days

The member receives the amount

The Prompt Reimbursement The Member falls ill and is admitted to a network hospital

The member informs the Aagewaan

Aagewaan visits the hospital, after 24 hour hospitalization, and meets the member and the doctors

She makes an assessment of documents, history of the claimant, estimates the costs as per the information provided

Presents the facts at Vimo Office

The claim is promptly analyzed by the claims committee and if approved the amount is released

The Aagewaan delivers the amount to the Member in hospital

Advantages of the Model

• The integrated approach – Health + Insurance, special focus since 2007

• Helps SEWA’s health program to identify geographical locations as well as health issues to focus on

• The insured members also get SEWA’s preventive as well as curative health interventions and trainings

Advantages of the Model • Better customer service – Claims approval rate –

90 %

• Helps us to identify the primary illnesses that are preventable like fever, diarrhea, gastro related diseases, about 30 % claims arise out of these diseases

• This information has triggered an action research where we are trying to analyze the impact of preventive health care for primary illnesses and its impact on claims ratios.

• Benefits of an integrated insurance package, all round protection.

Advantages of the Model

• Our in-house claim settlement capacity helps us to quickly respond to the members claims

• The prompt reimbursement system has taken off the burden of arranging cash as short notice for our members

• Average Turn around time is 9 Days for normal claims in Ahmedabad city.

• Its been observed that backed by an insurance policy more women seek health facilities

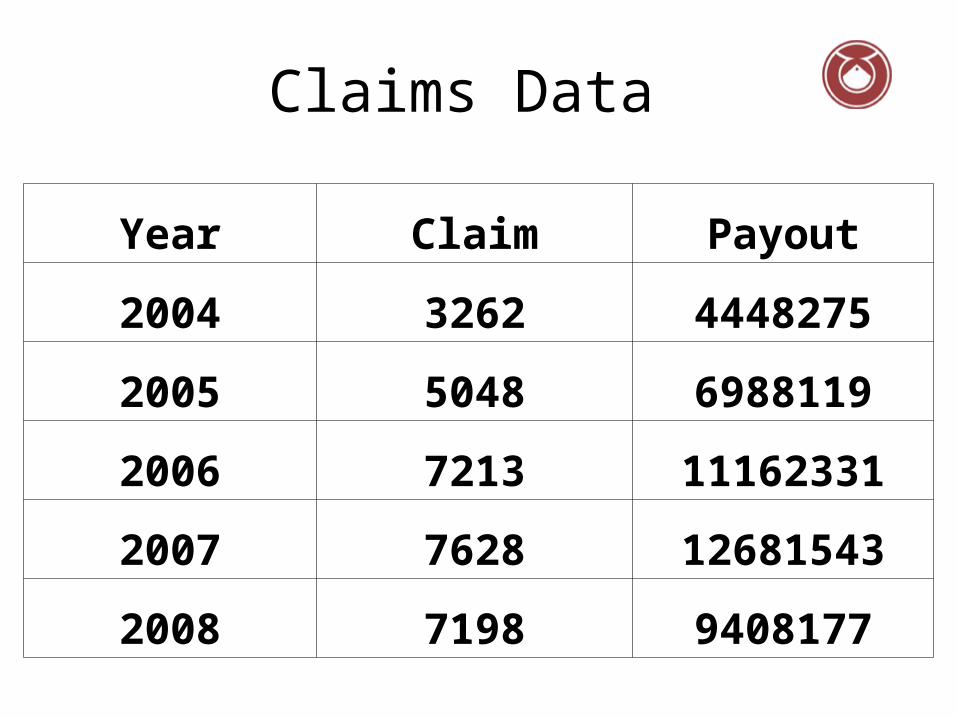

Claims Data

Year Claim Payout

2004 3262 4448275

2005 5048 6988119

2006 7213 11162331

2007 7628 12681543

2008 7198 9408177

Challenges

• High Claims Ratio – Our claims ratios have been high.

• 2007 – 116 %, 2008 – 112 %

• The rural members tend to subsidize our urban members

• Urban Area claim ratio - 172 %

• Rural claim ratios – 70 %

• Need for differential pricing

Challenges

• Education and awareness amongst members to utilize these services.

• High distribution costs.

• Fraudulent claims.

• Affordability and limited coverage.

• Moral Hazards

• Unregulated health sector.

Future Plans

• Covering maternity • Active involvement in RSBY• Propose to increase health coverage at least up

to Rs. 5000 for all members• To offer policies with a family floater

Thanks!