Embed Size (px)

Citation preview

1

Vision for Industry

Cognex Corporation

Project Group Members:

Britt Fisher [email protected]

Bryan McCalister [email protected]

Chris Nelson [email protected]

Ray O’Connor [email protected]

Taylor Pettigrew [email protected]

2

Table of Contents:

Executive Summary 8 Business and Industry Analysis 10

Company Overview 17

Industry Overview 19

Five Forces Model 24

Rivalry of Existing Firms 25

Industry Growth Rate 25

Concentration of Competitors 27

Differentiation 29

Learning Economies 29

Excess capacity 30

Exit Barriers 31

Conclusion 31

Threat of New Entrants 31

Economies of Scale 32

First Mover Advantage 34

Legal Barriers 35

Conclusion 36

Threat of Substitute Products 37

Customers’ Willingness to Switch 38

Conclusion 39

Bargaining Power of Customers 39

3

Price sensitivity of Customer 40

Relative Bargaining Power-Customer 40

Customer Switching Cost 41

Conclusion 42

Bargaining Power of Suppliers 42

Price sensitivity of Supplier 43

Relative Bargaining Power-Supplier 43

Conclusion 43

Industry Analysis 44

Superior Product Quality 44

Superior Product Variety 45

Superior Customer Service 46

R&D 47

Investment in Brand Image 48

Value Creation Analysis 49

Superior Customer Service 49

Superior Product Variety 53

R&D 53

Superior Product Quality 54

4

Conclusion 56

Formal Accounting Analysis 56

Key Accounting Policies 57

Goodwill 58

Research and Development 60

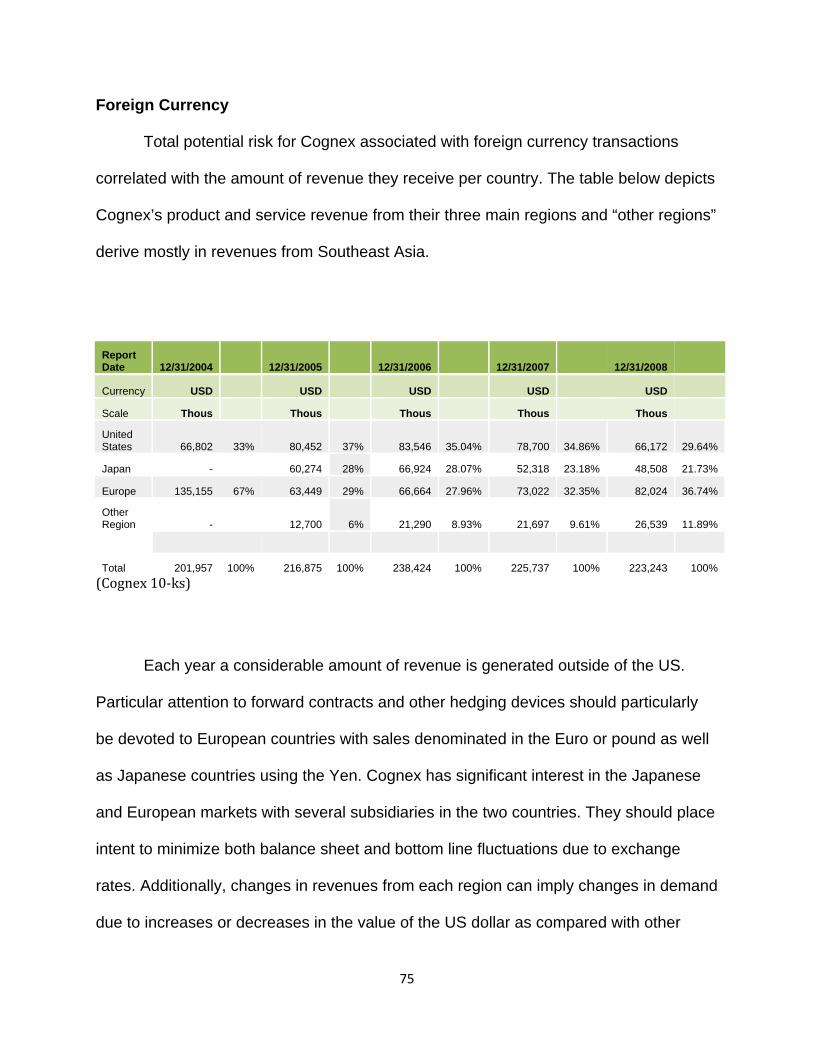

Foreign Currency 62

Accounting Flexibility 65

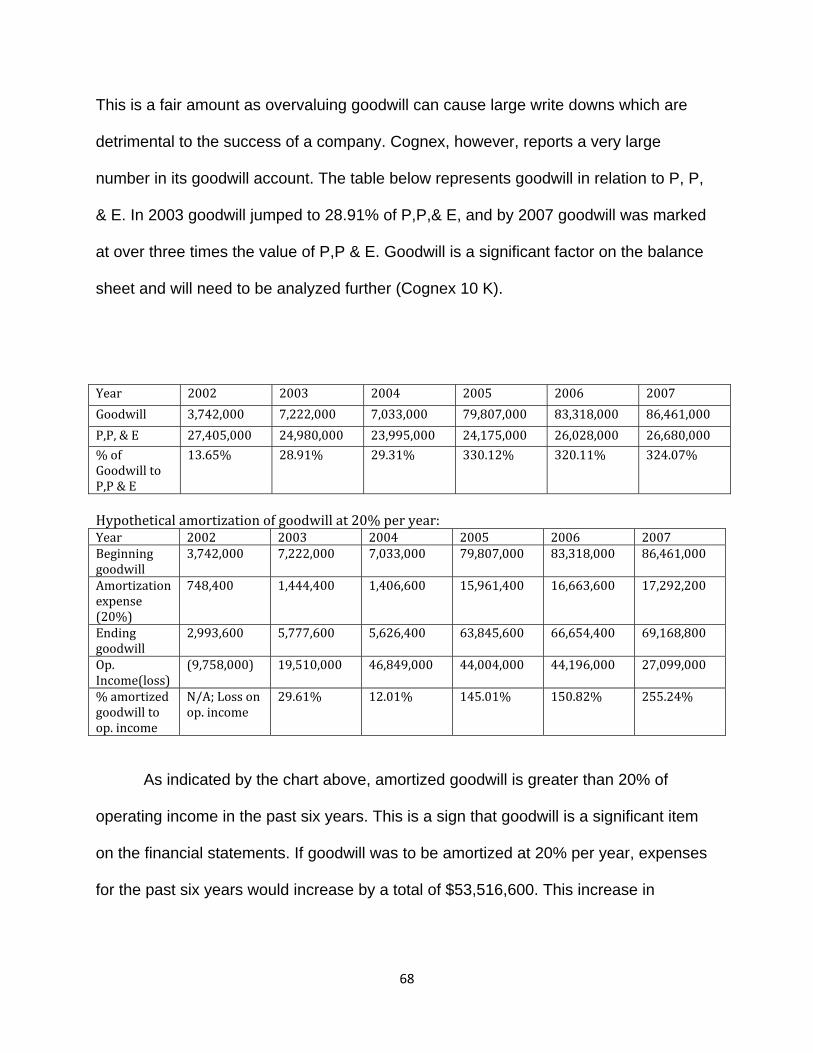

Goodwill 66

Research and Development 68

Foreign Currency 69

Evaluate Accounting Strategy 70

Goodwill 70

Research and Development 72

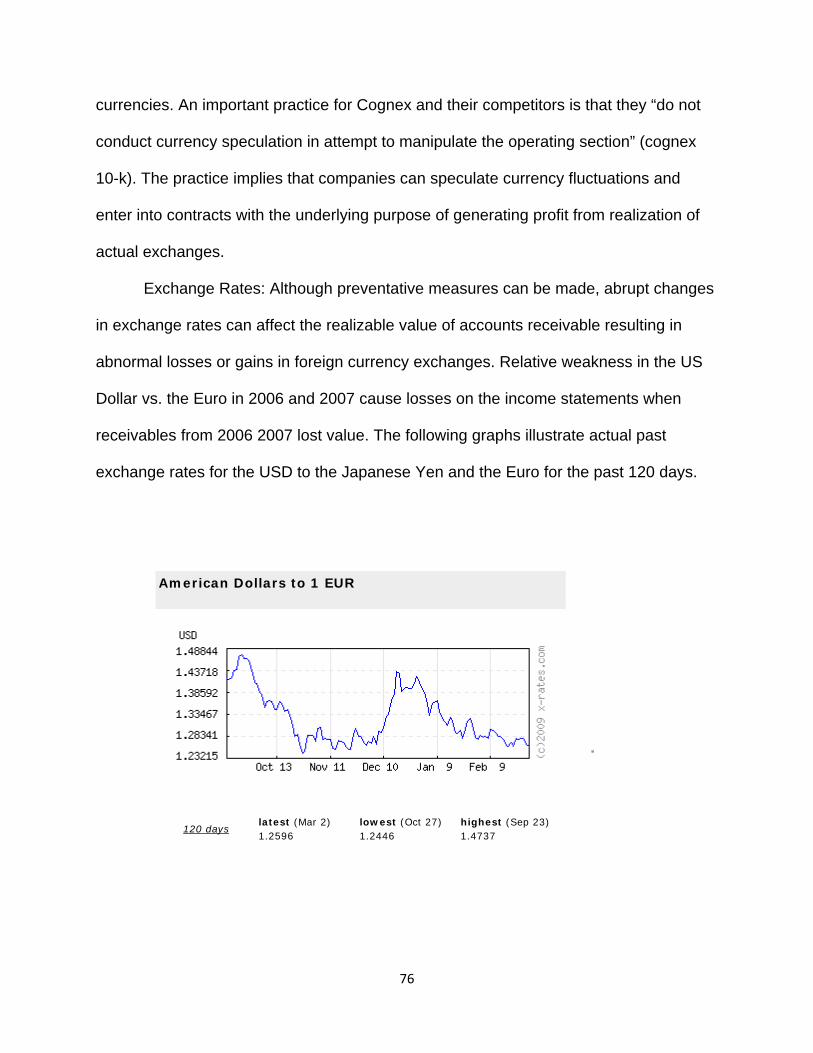

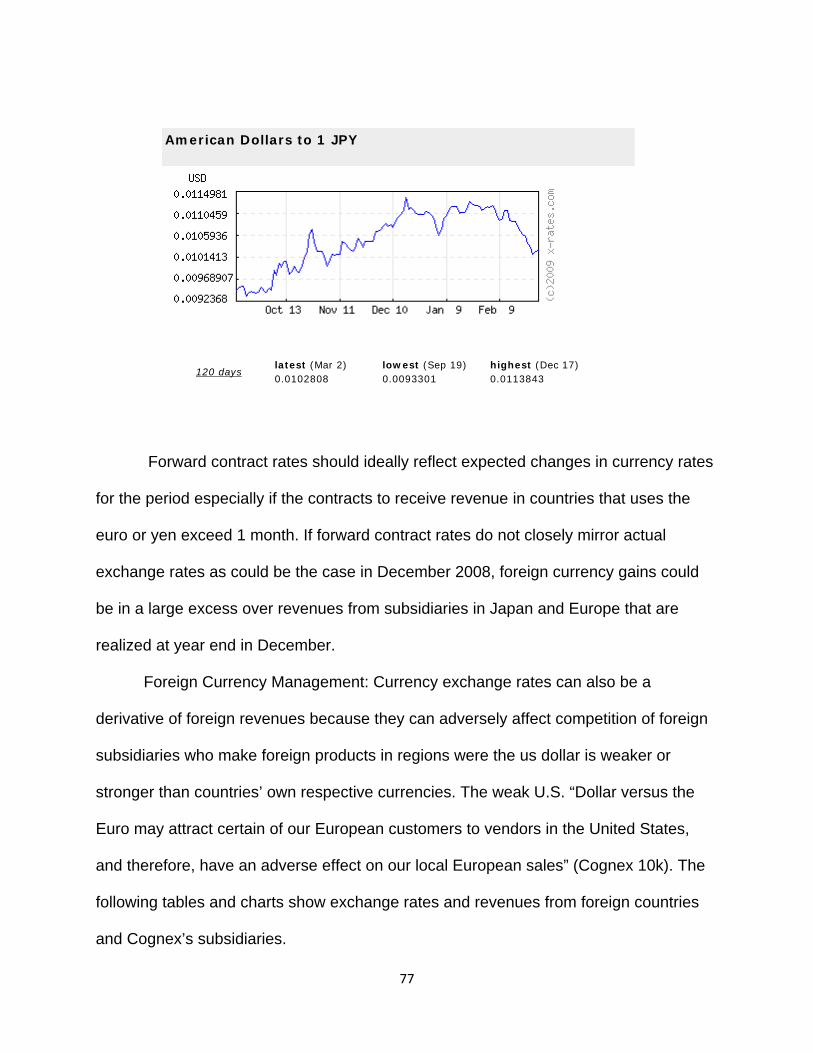

Foreign Currency 74

Qualitative Disclosure 81

Goodwill 81

Research and Development 83

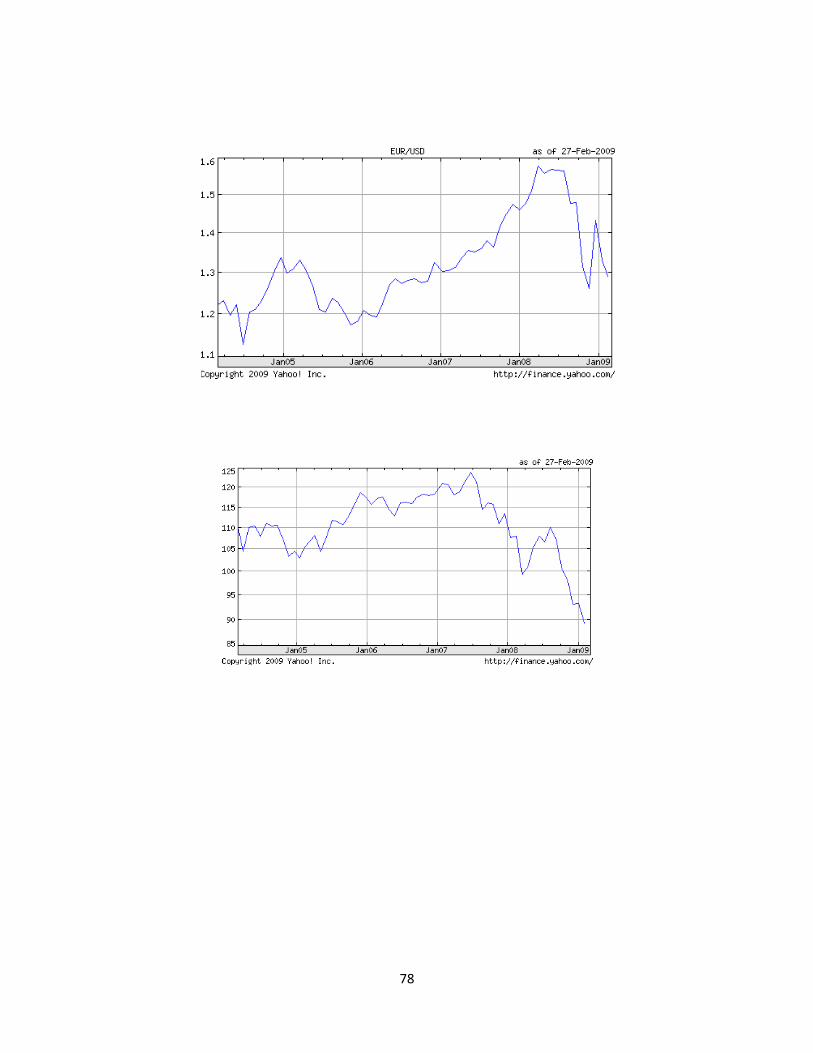

Foreign Currency 83

Conclusion 85

Quantitative Analysis 85

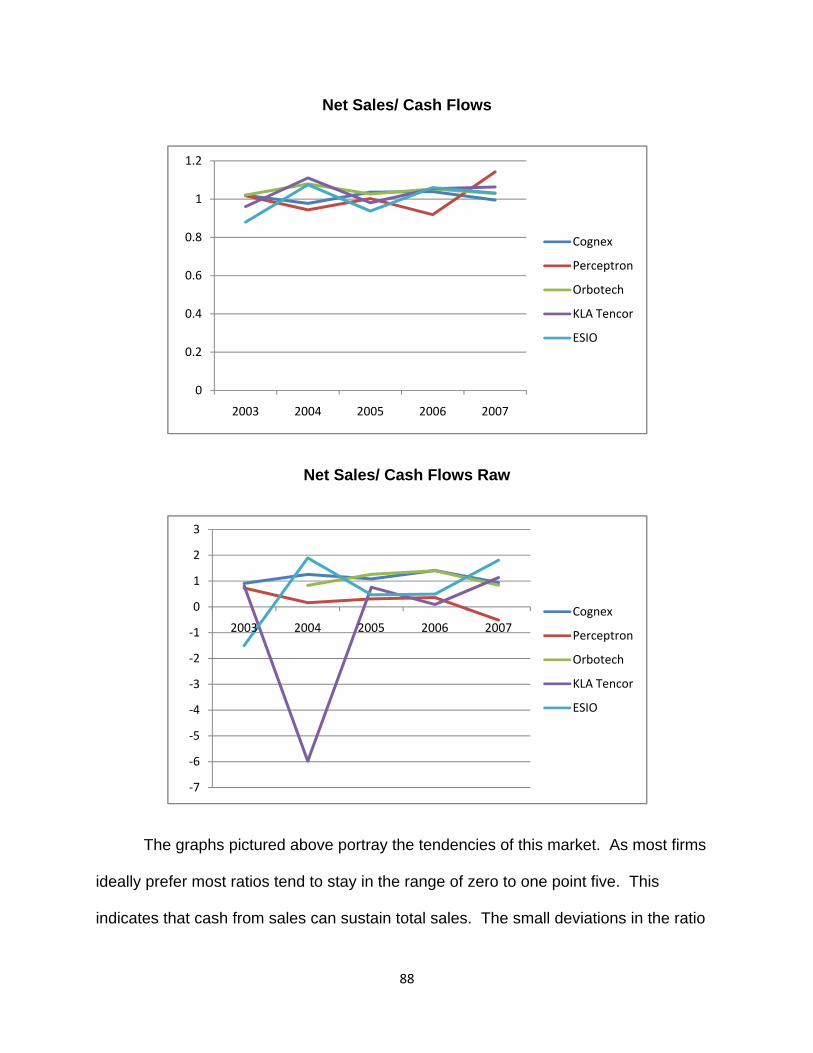

Revenue Manipulation Diagnostics 86

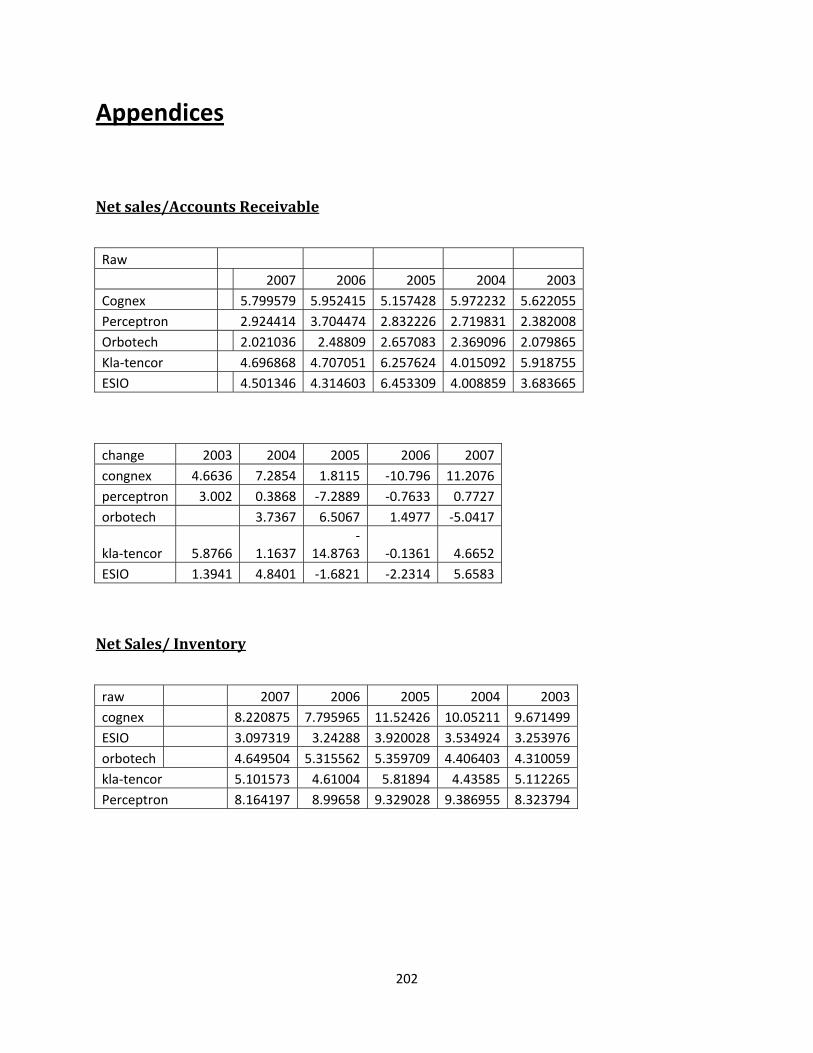

Net sales/cash from sales 86

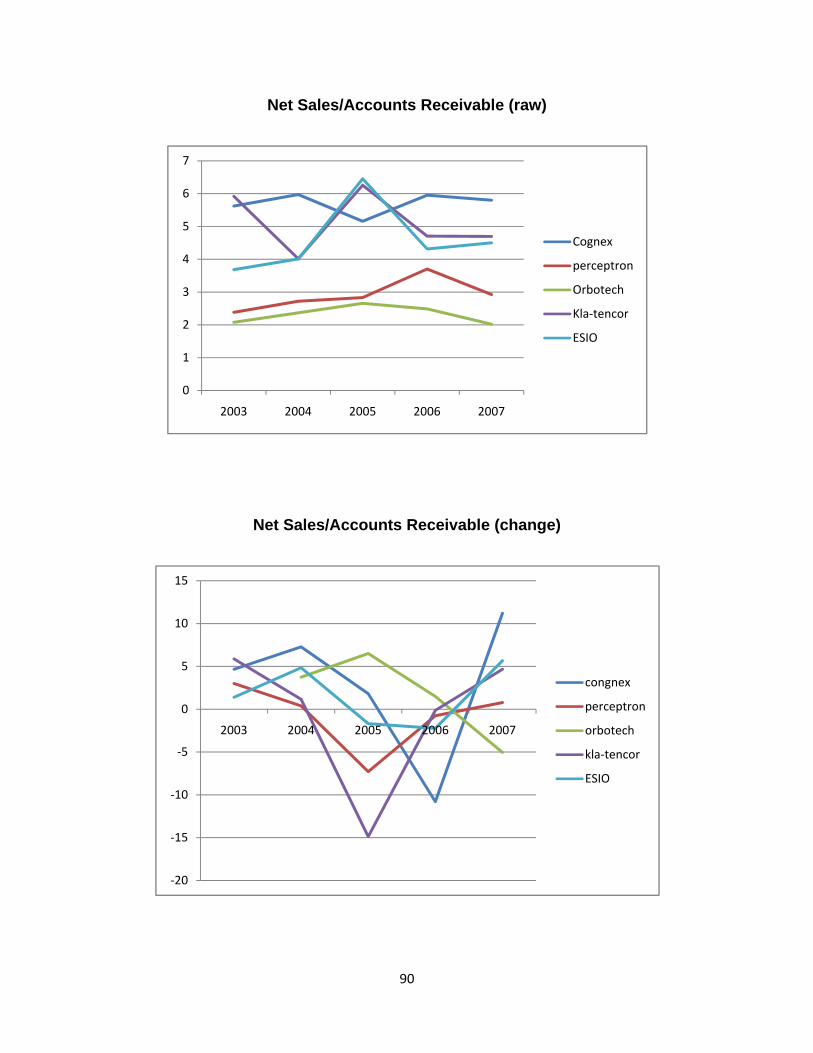

Net sales/accounts receivable 88

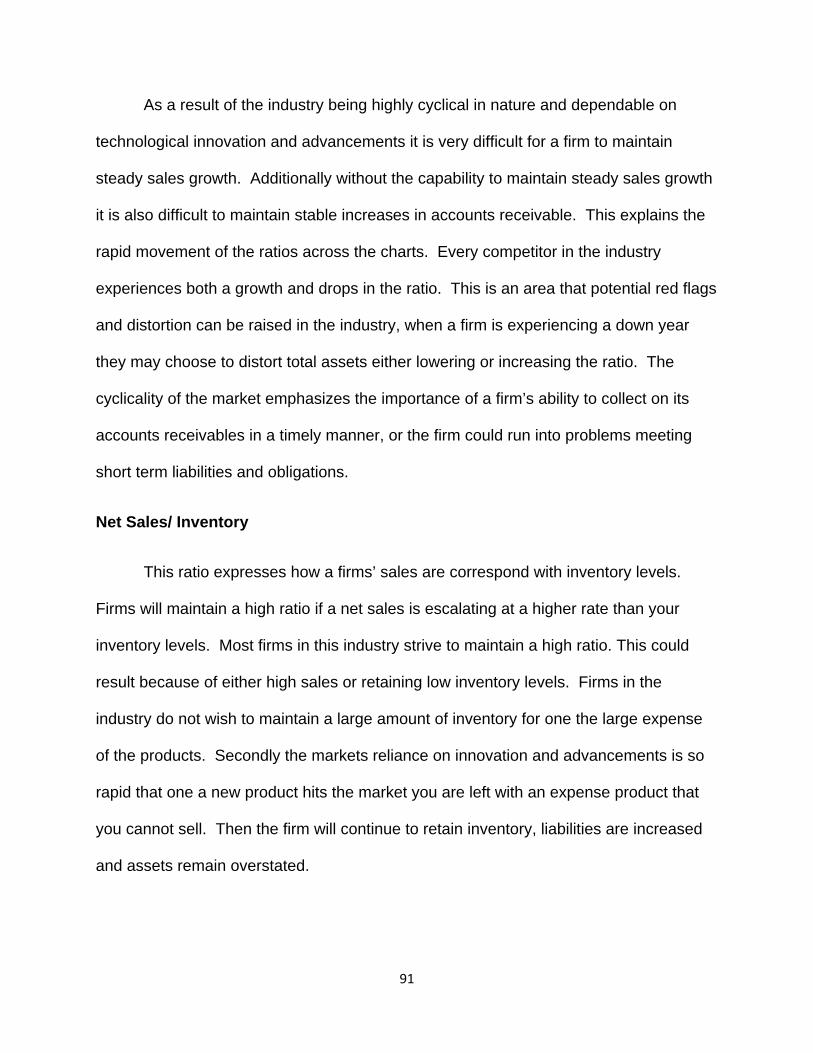

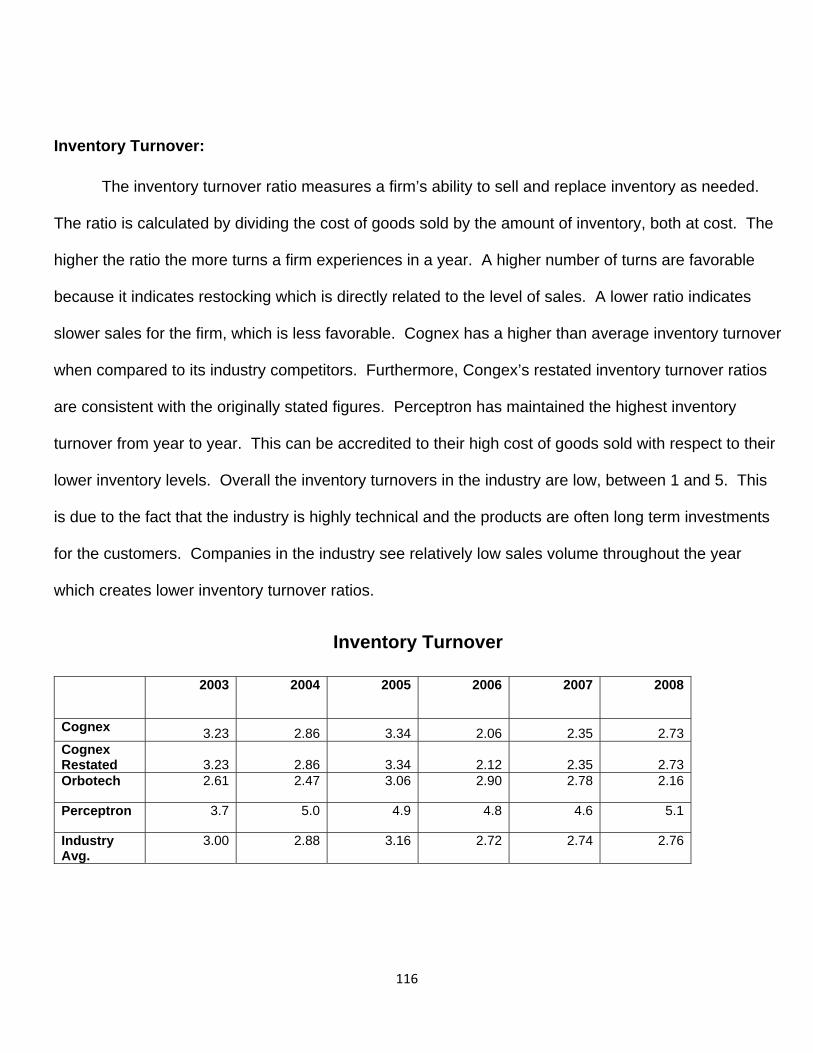

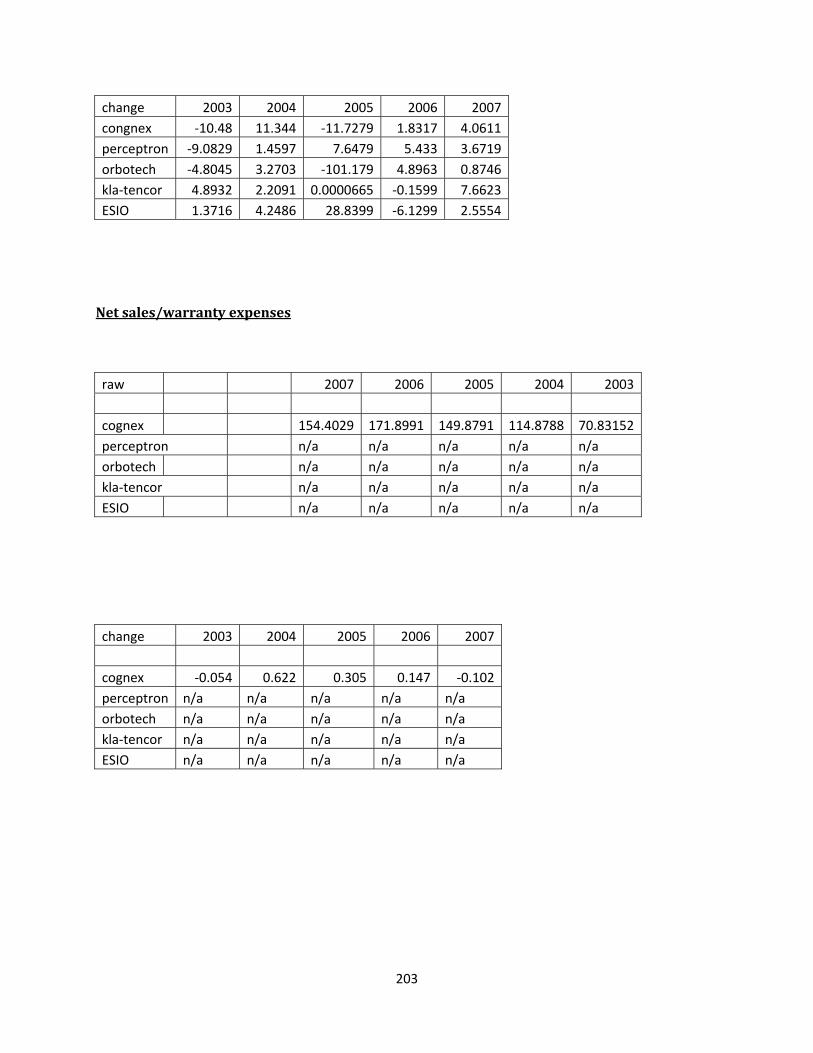

Net sales/ inventory 90

5

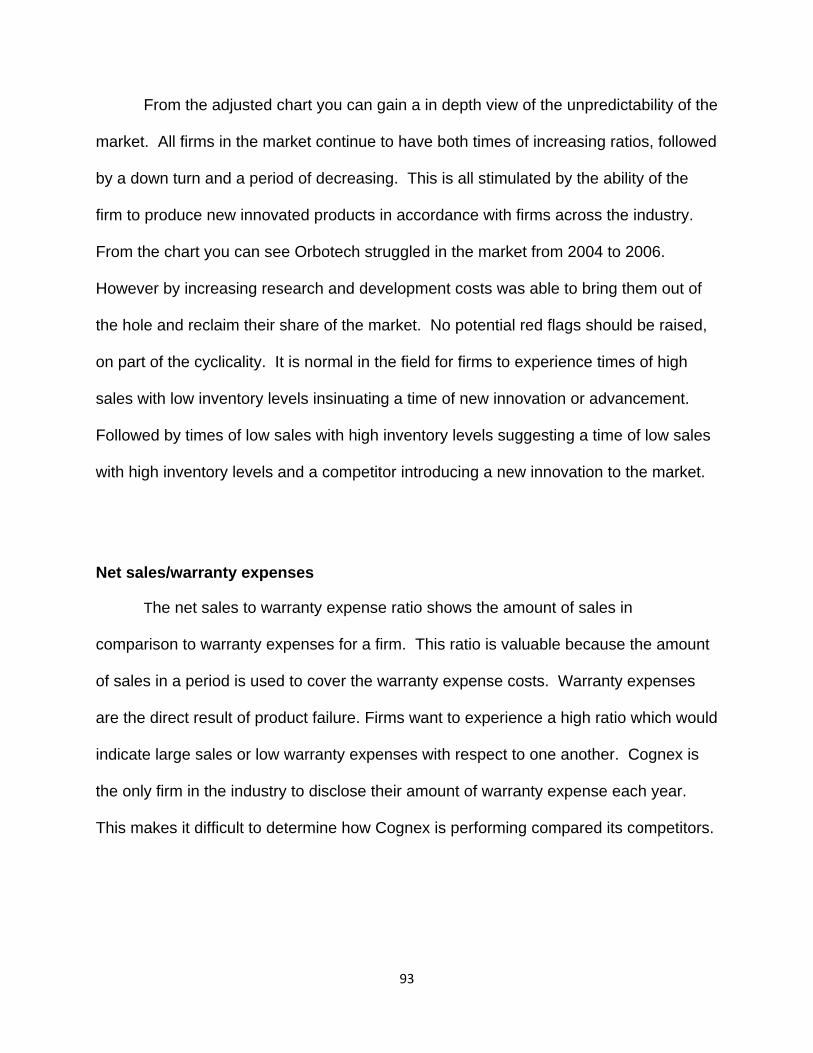

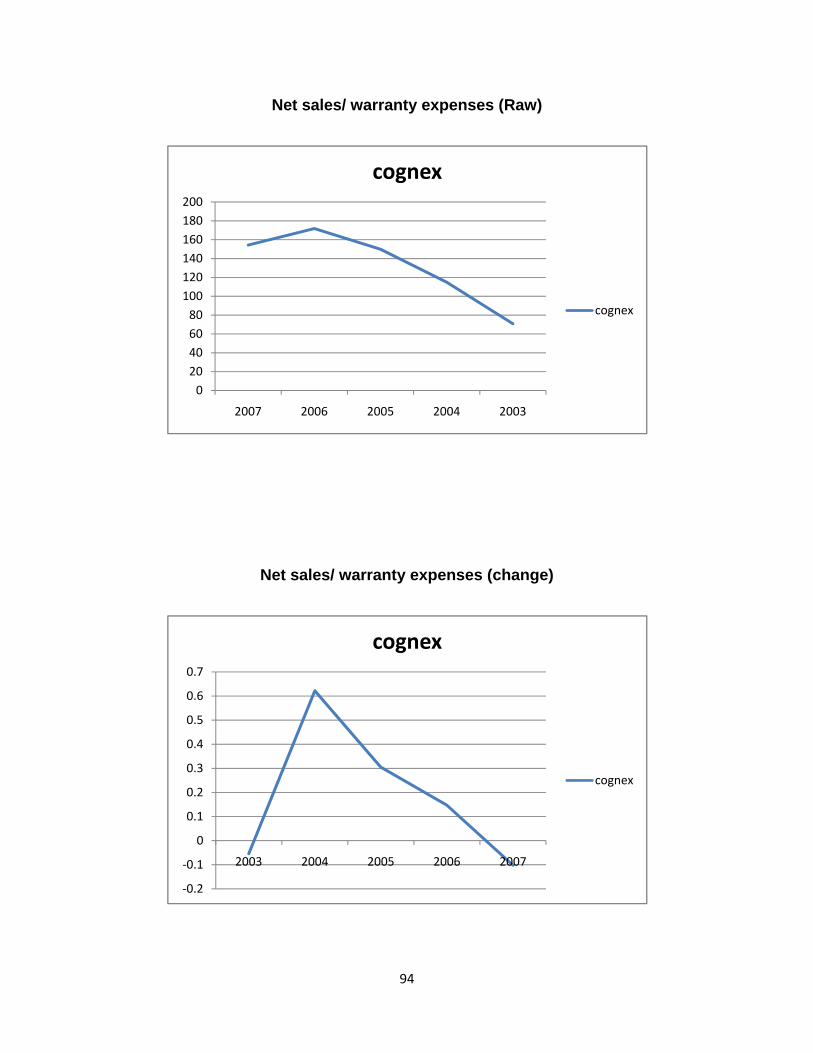

Net sales/warranty expense 92

Conclusion 94

Expense Manipulation Diagnostics 95

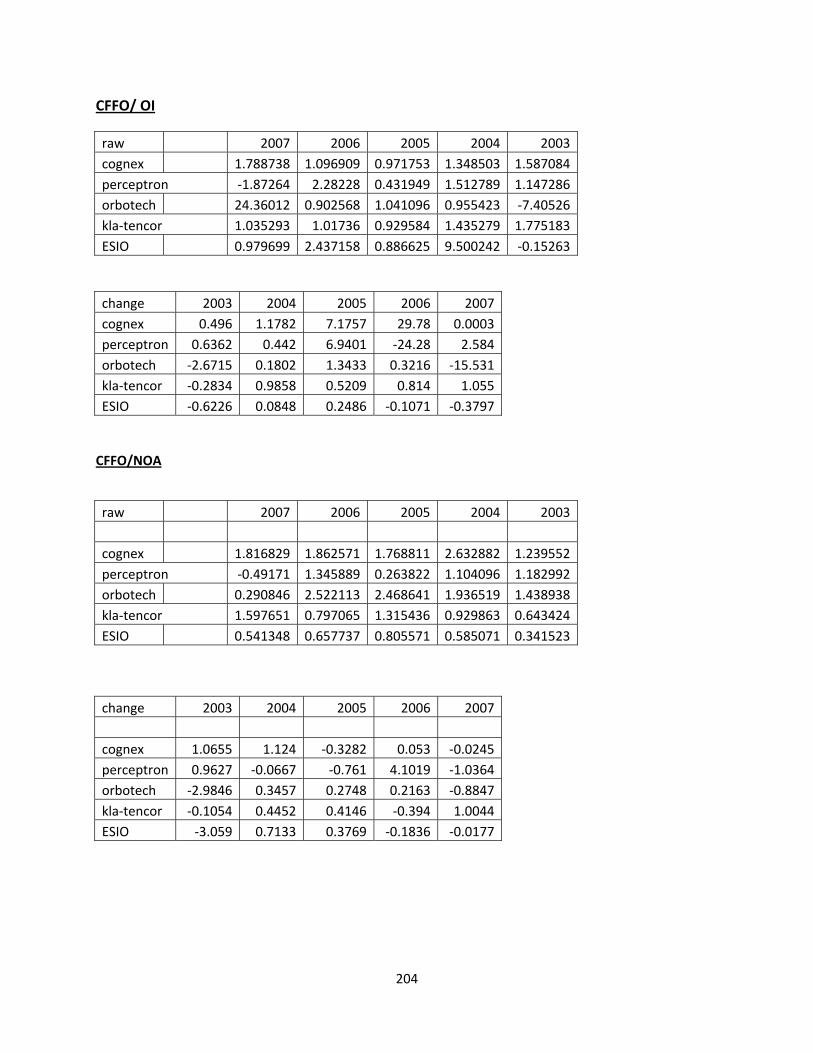

Cash flow from operations/operating income 95

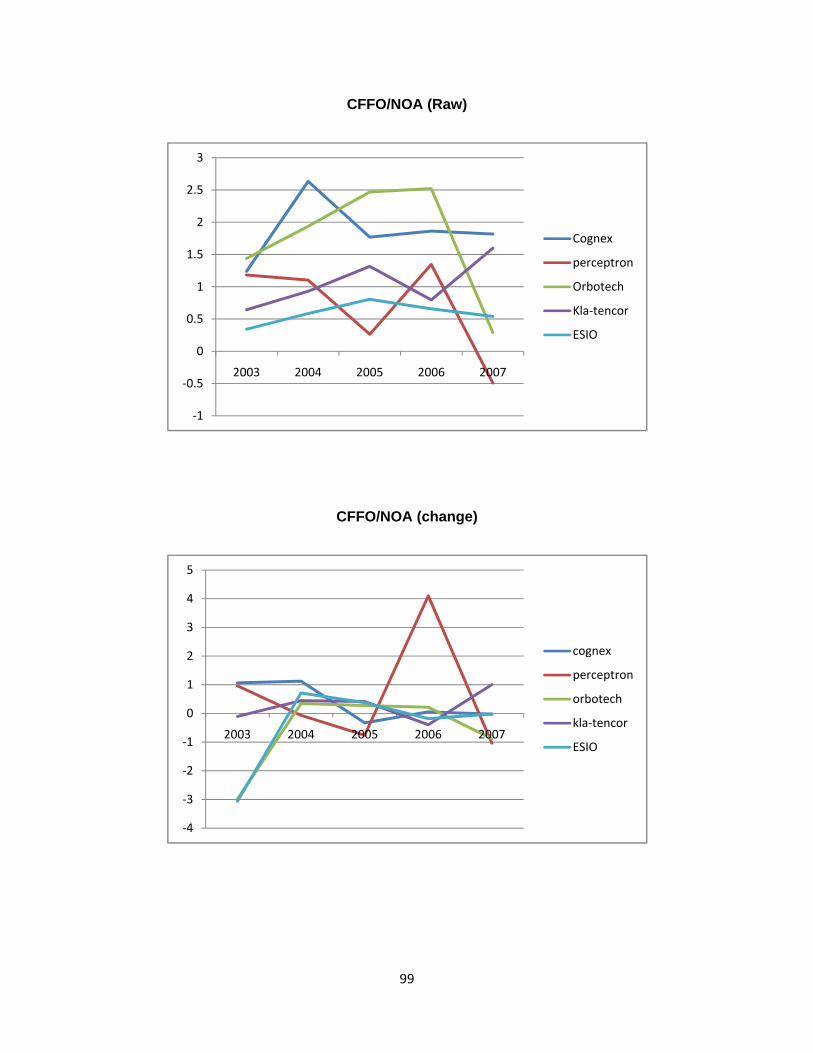

Cash flow from operations/net operating assets 97

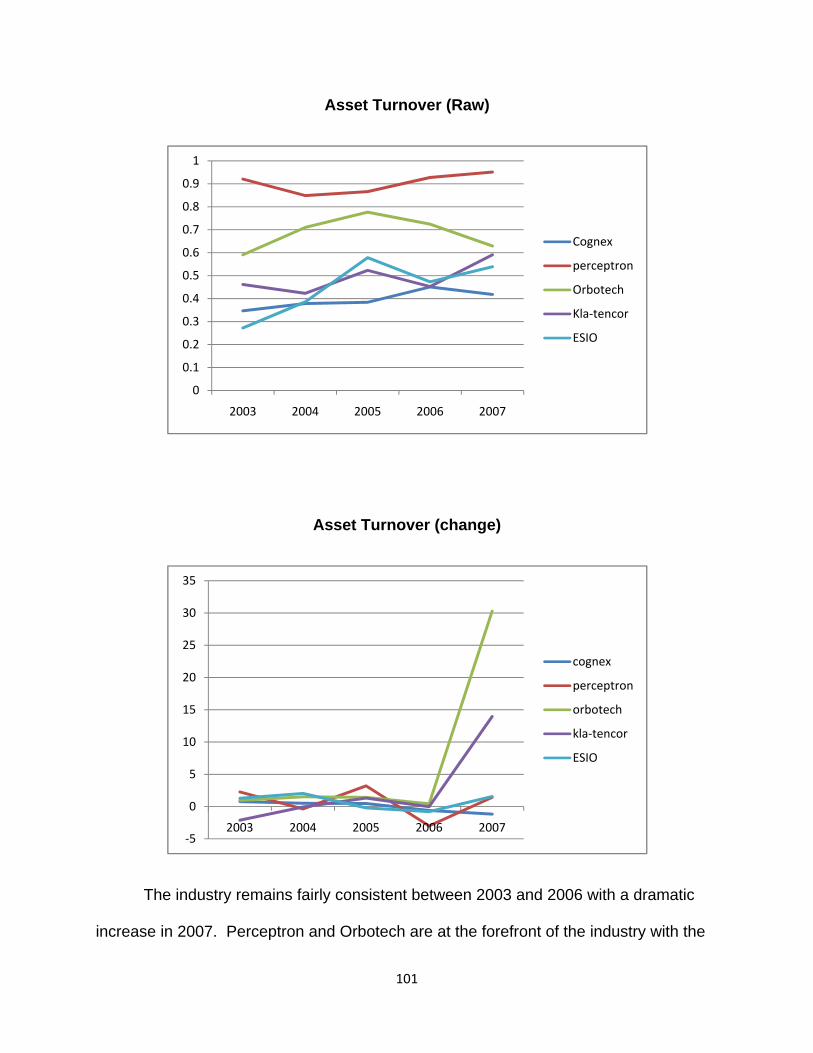

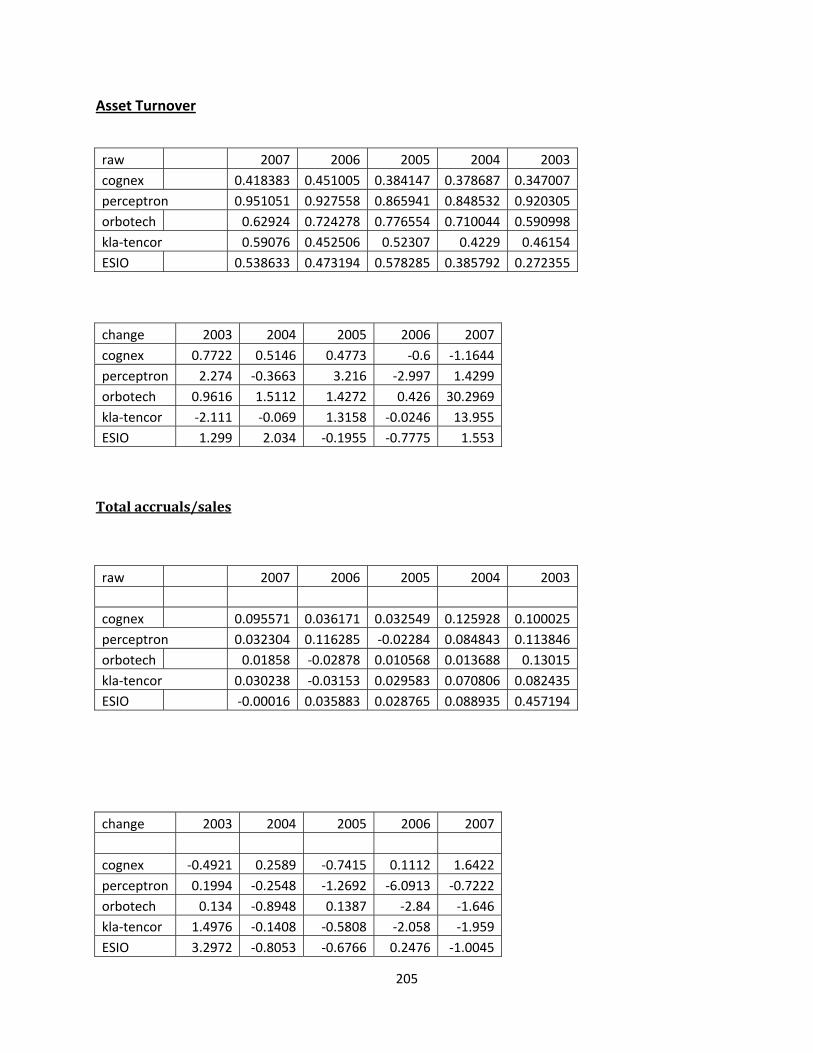

Asset turnover 99

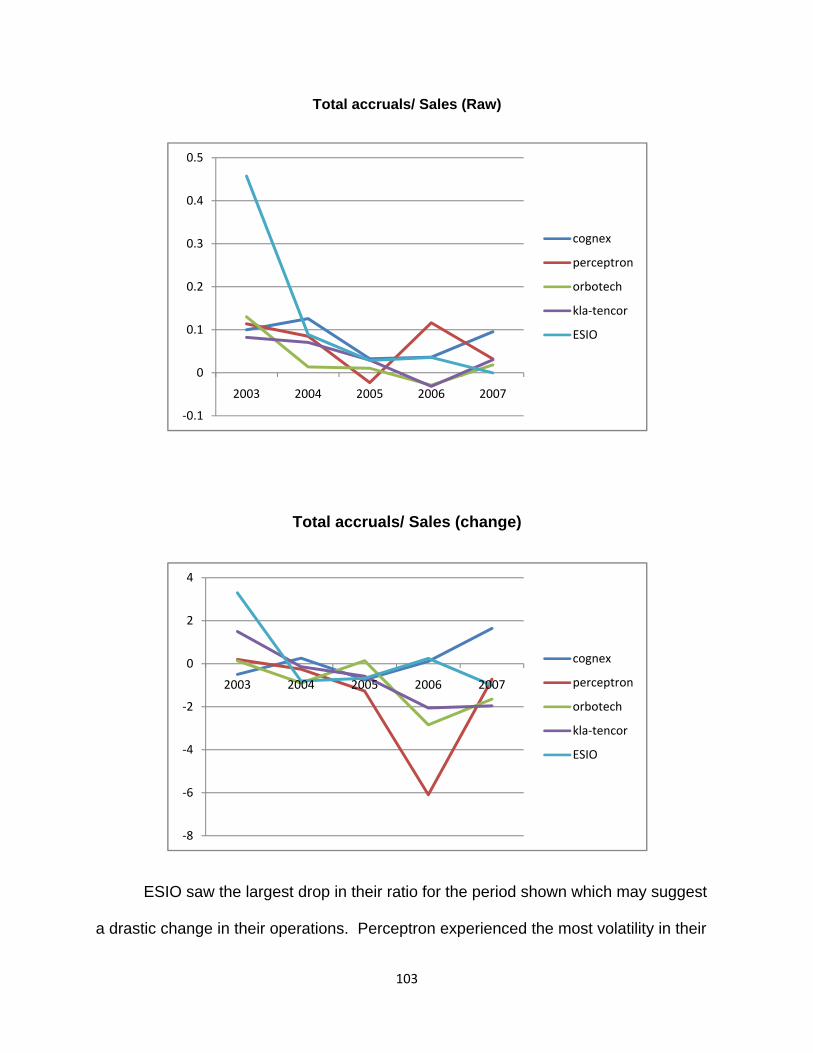

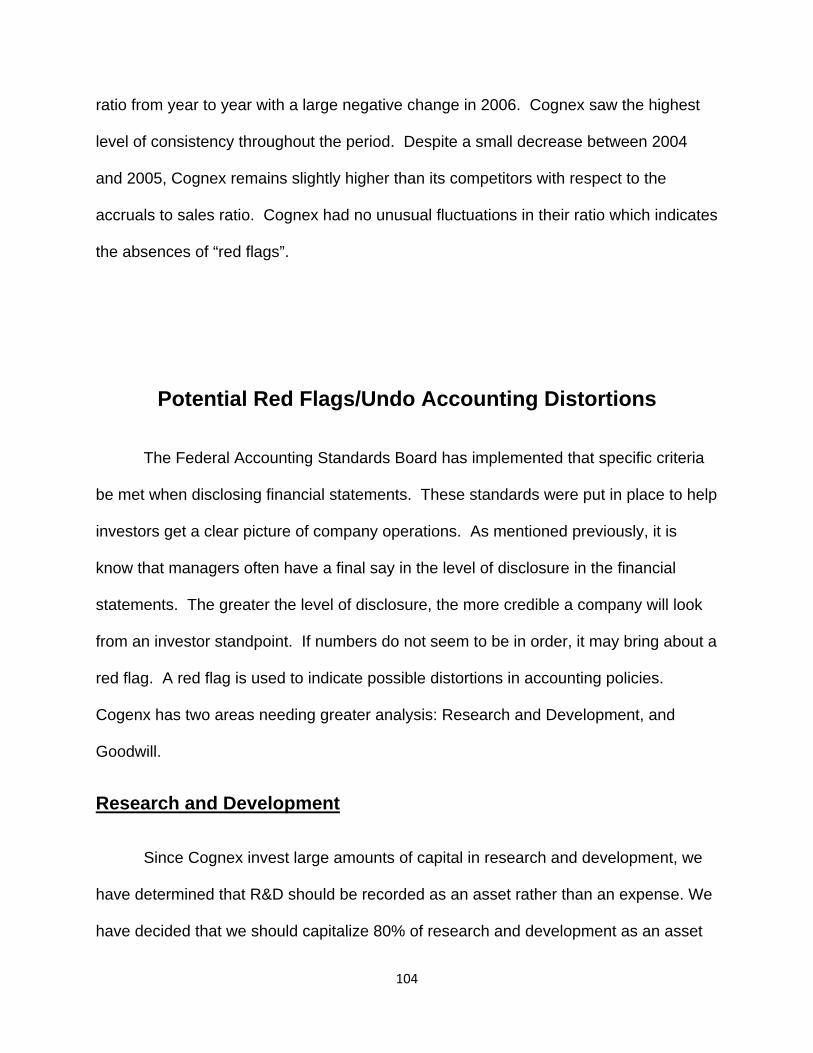

Total Accruals/sales 101

Potential Red Flags/Undo Accounting Distortions 103

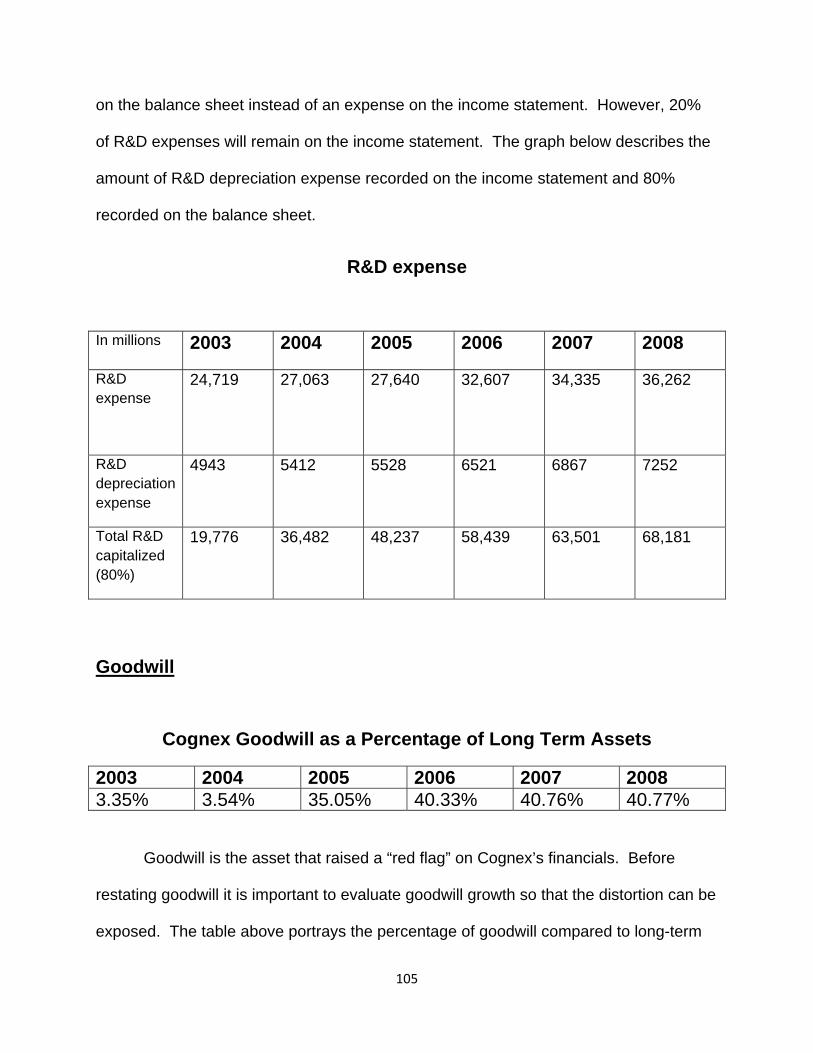

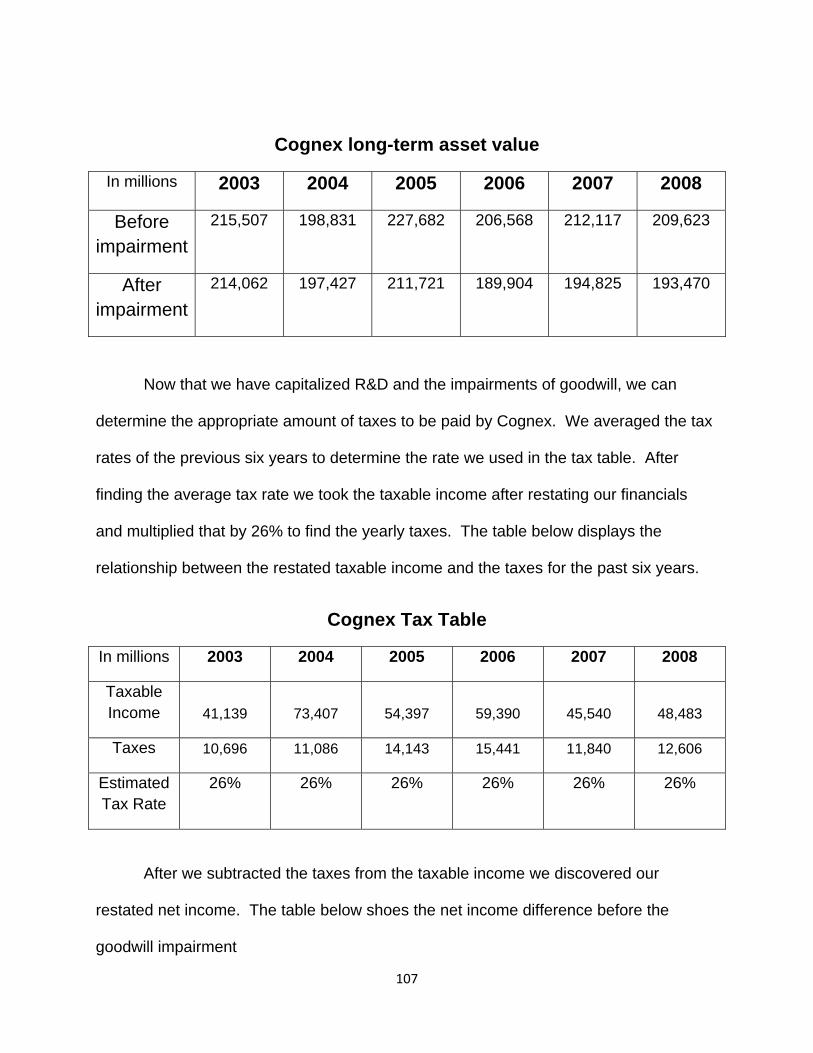

Research and Development 103

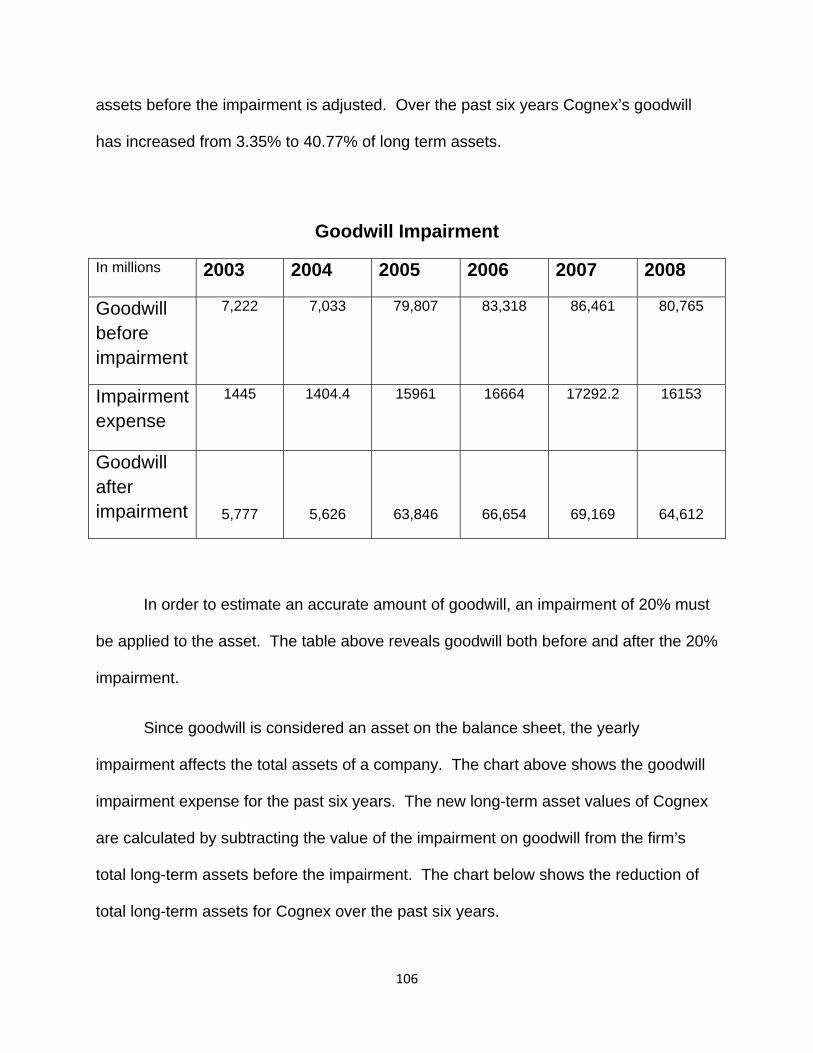

Goodwill 104

Restated Income Statement 108

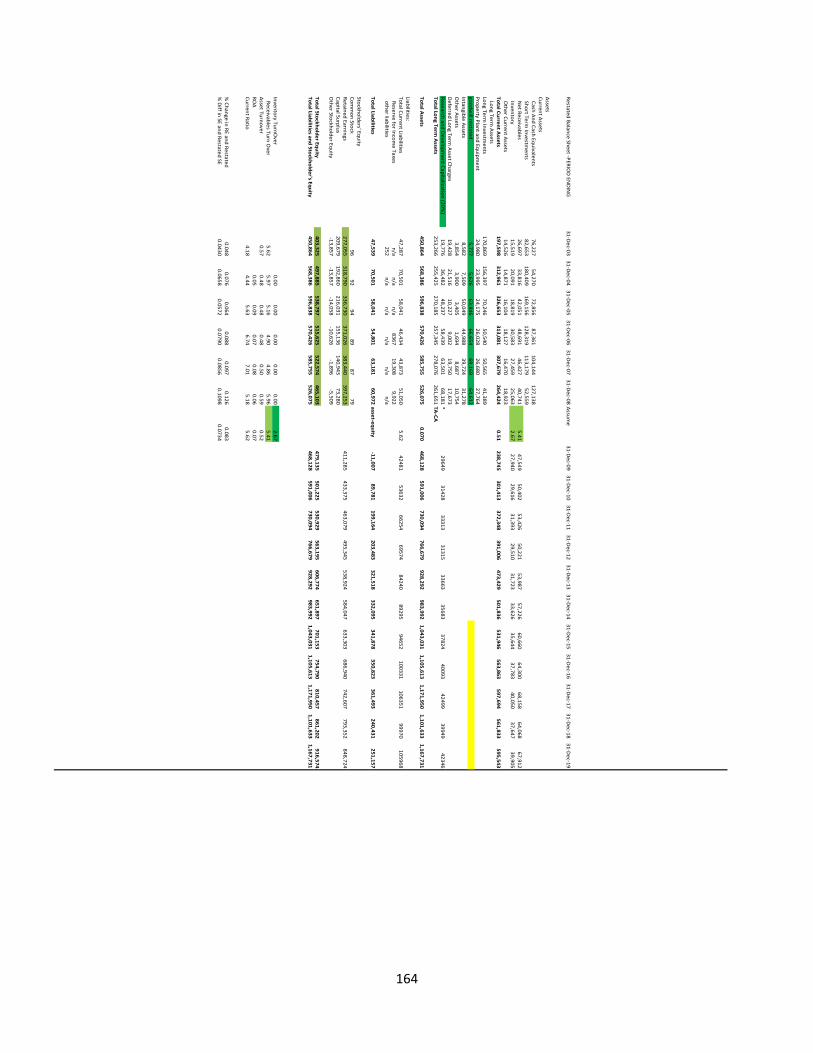

Restated Balance Sheet 109

Financial Analysis, Forecasting Financials, and Cost of Capital Estimation 110

Financial Analysis 110

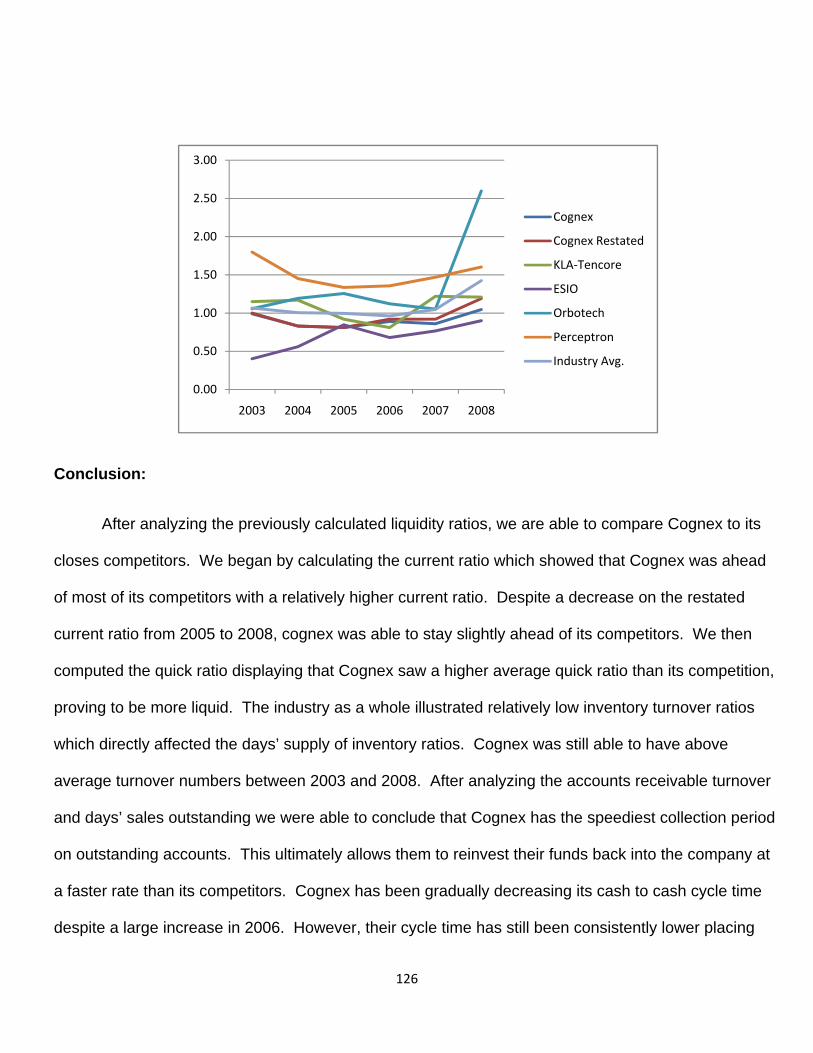

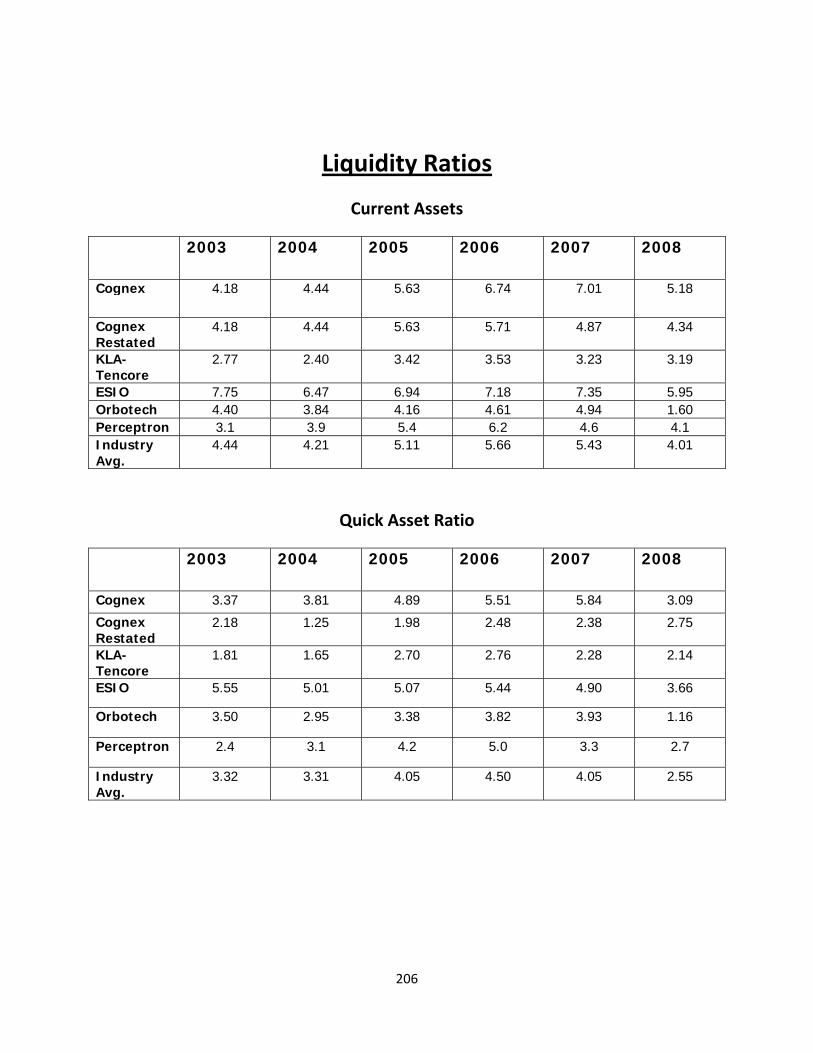

Liquidity Ratio Analysis 111

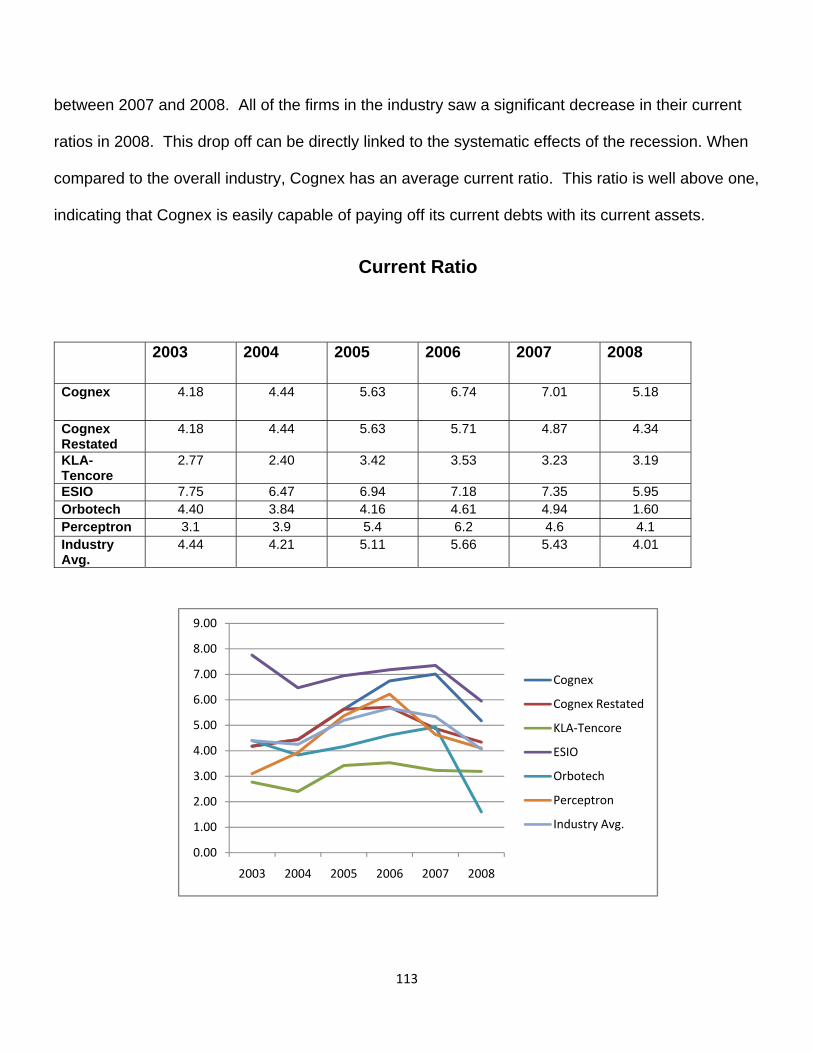

Current Ratio 111

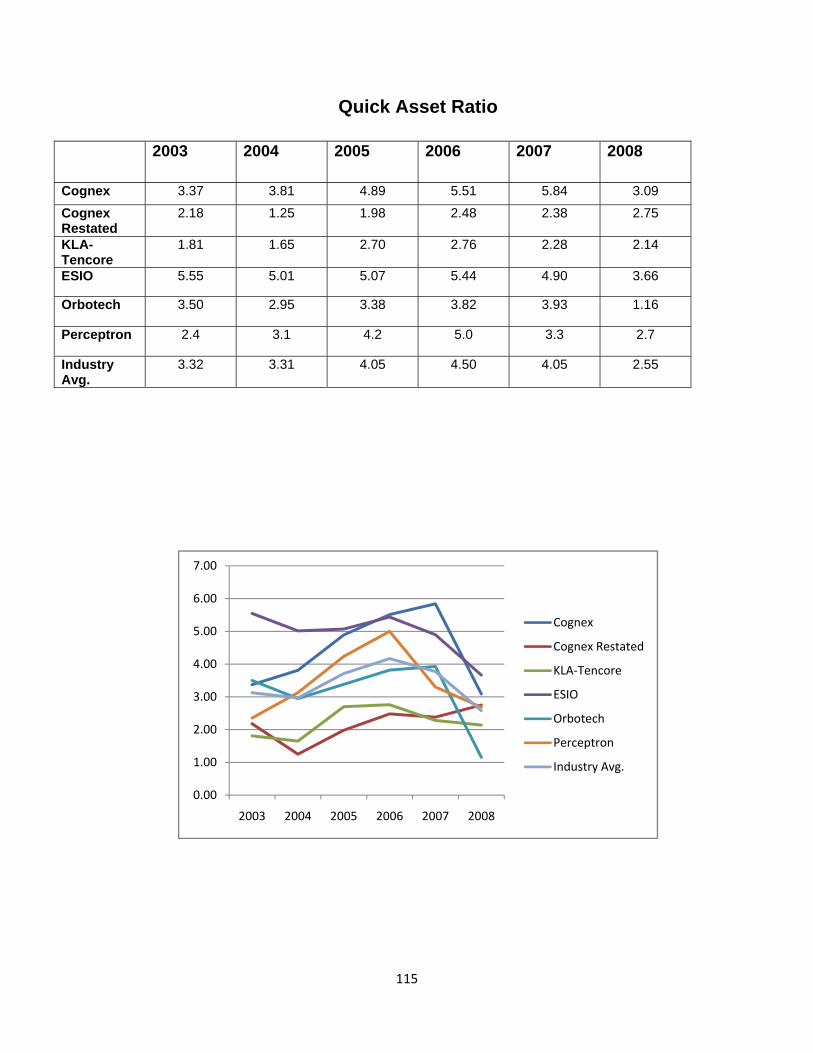

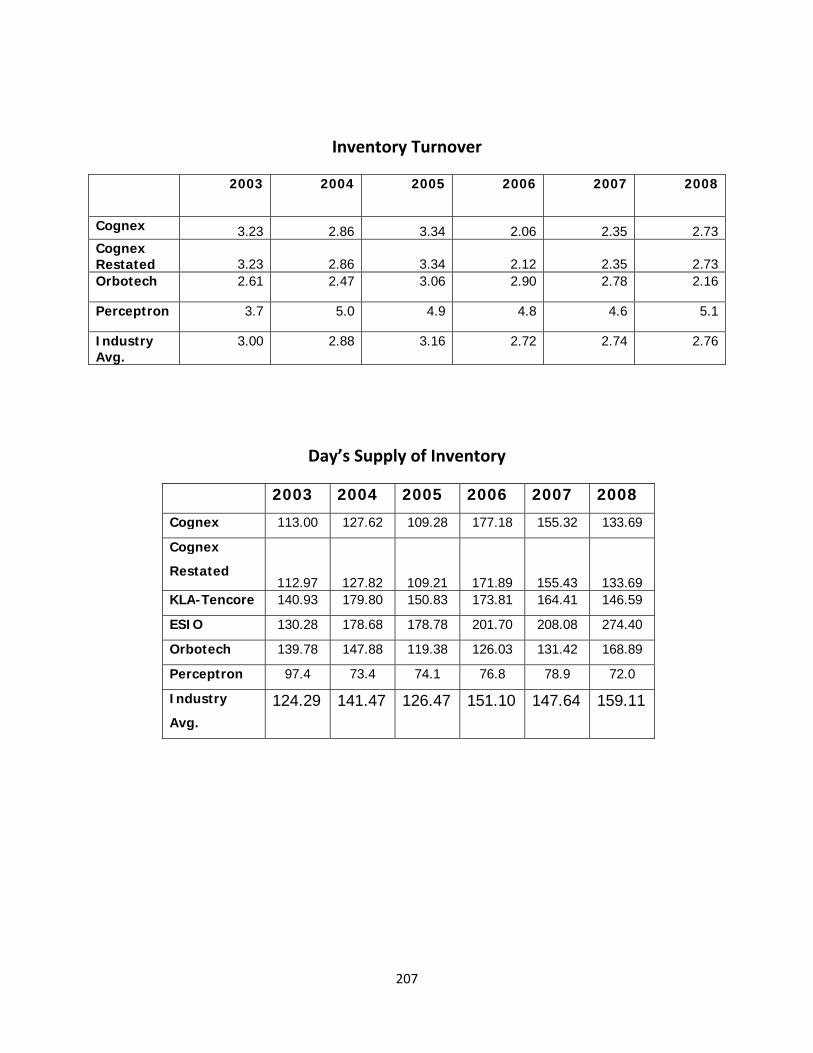

Quick Asset Ratio 113 Inventory Turnover 115

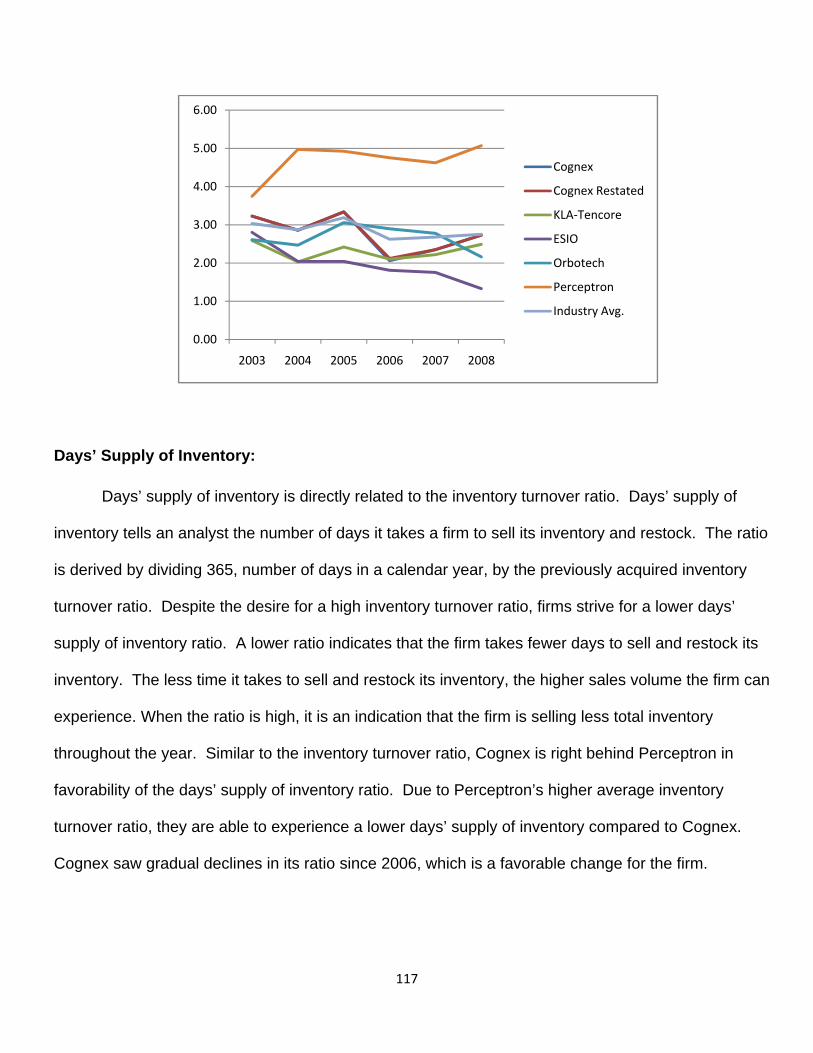

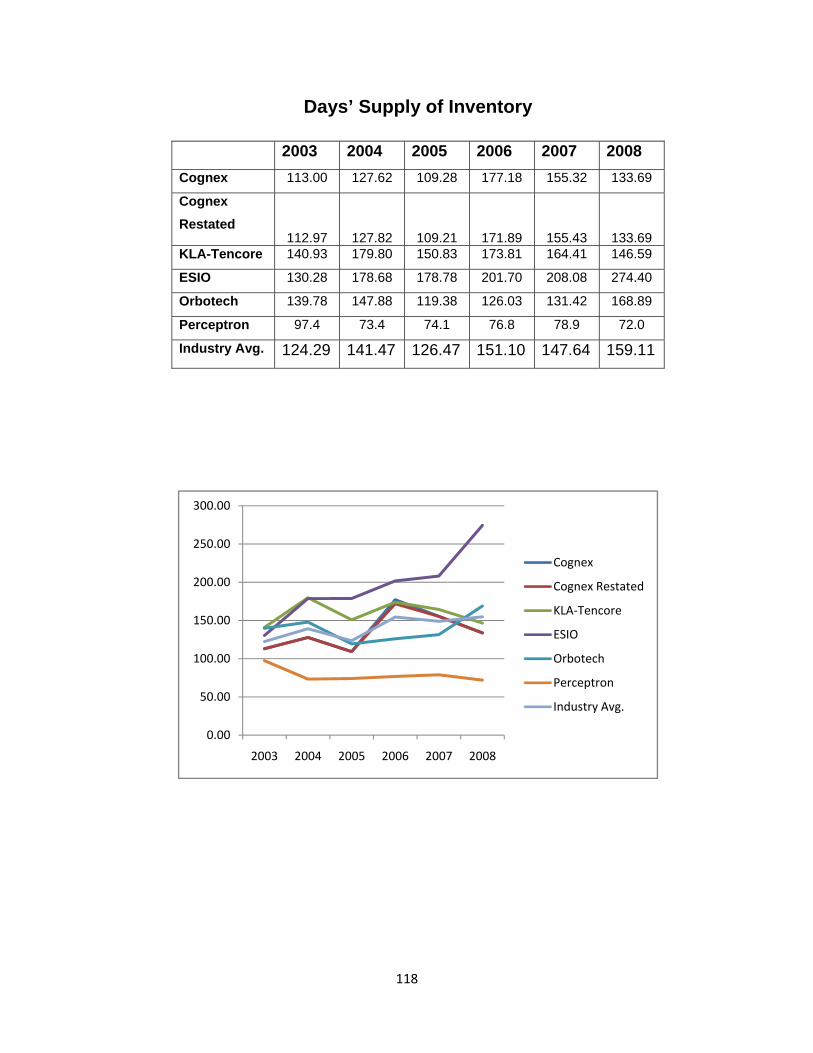

Days Supply Inventory 116

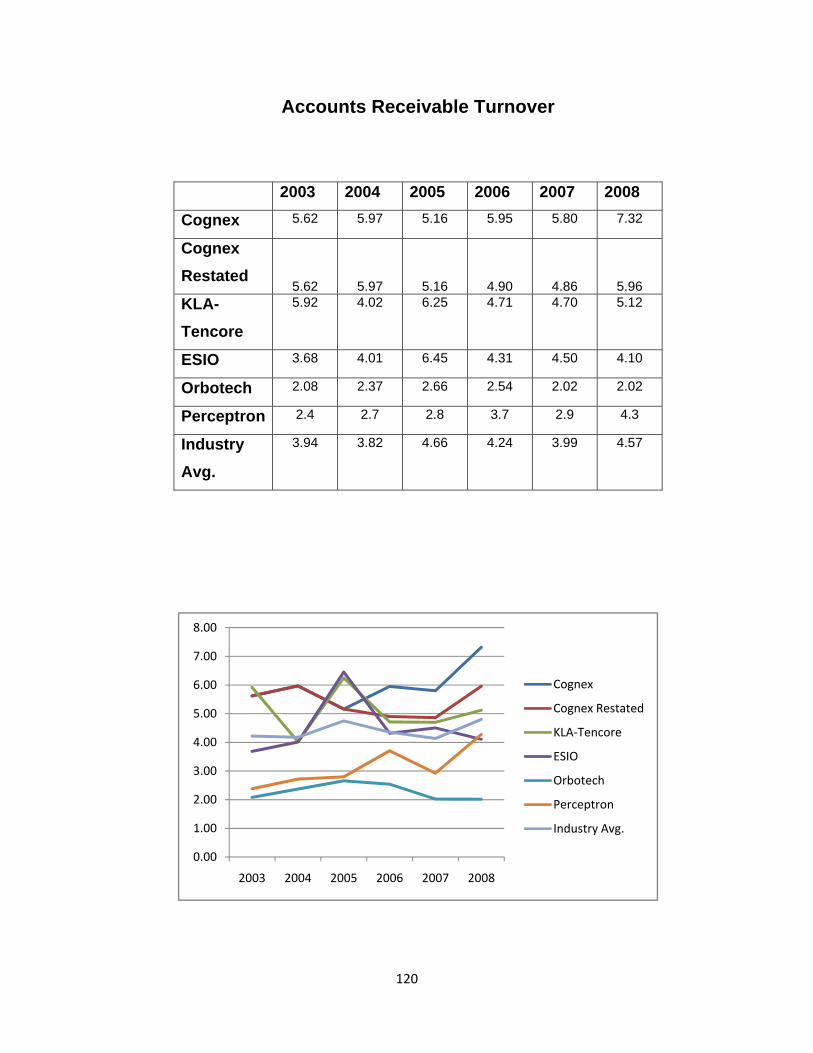

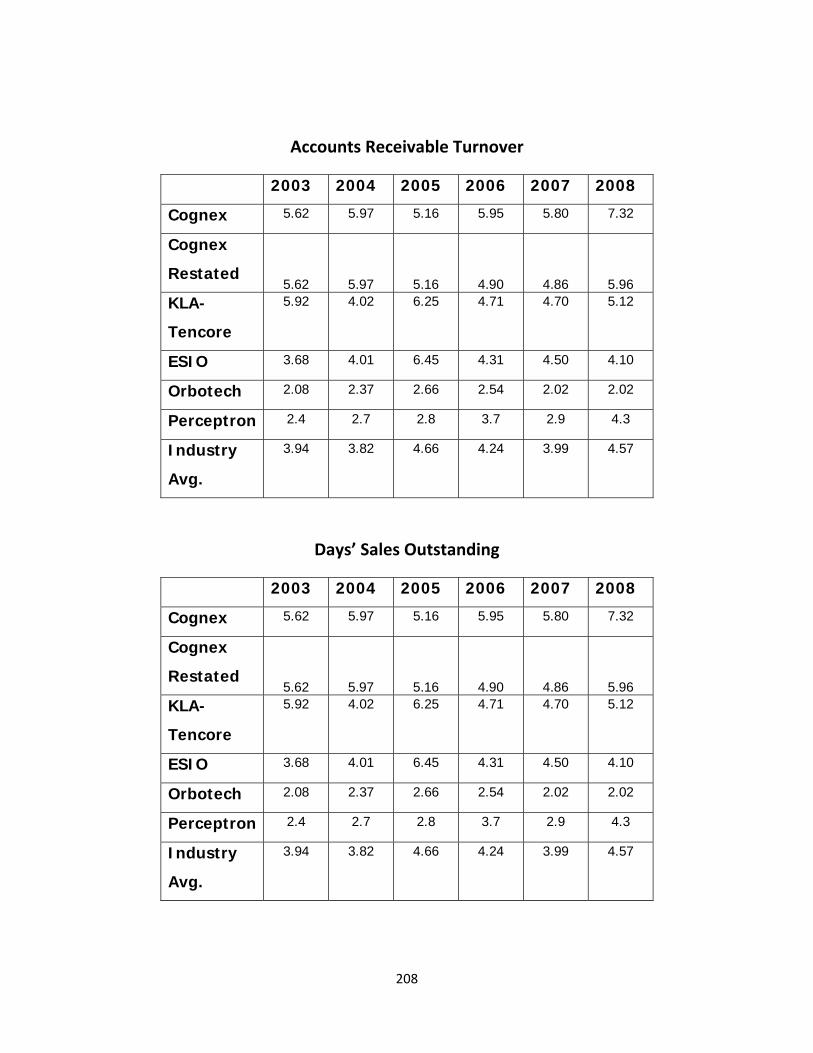

Accounts receivable turnover 118

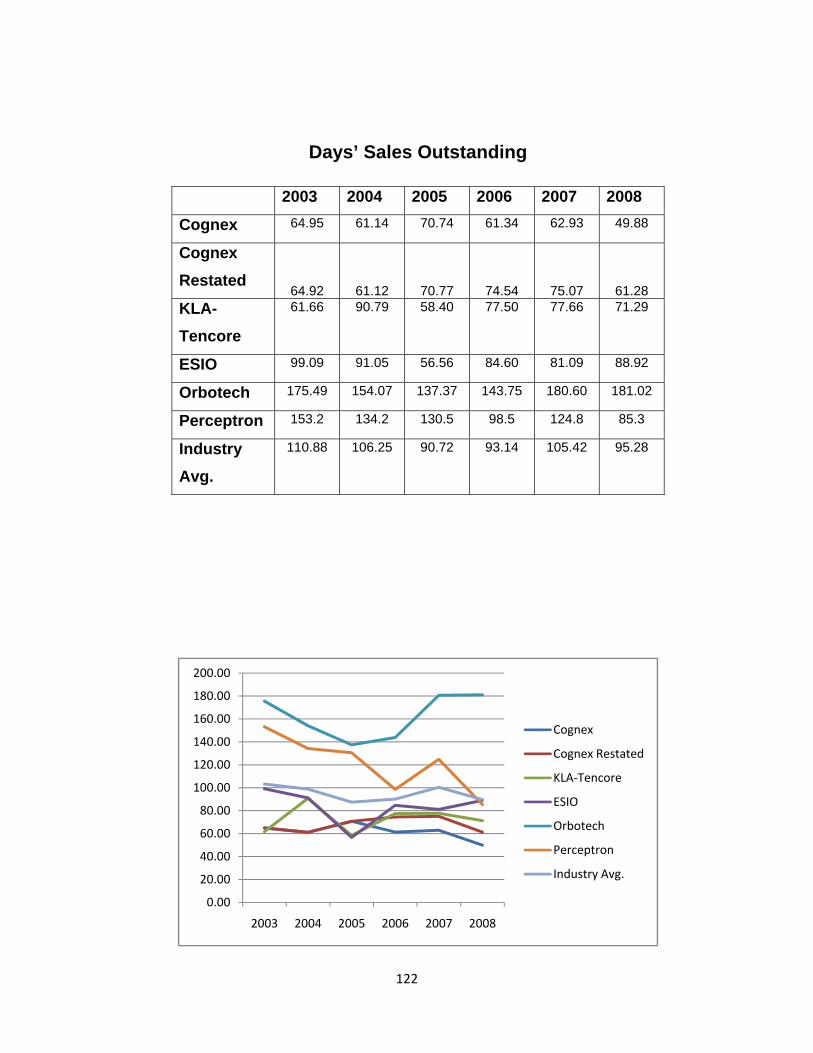

Days Sales Outstanding 119

6

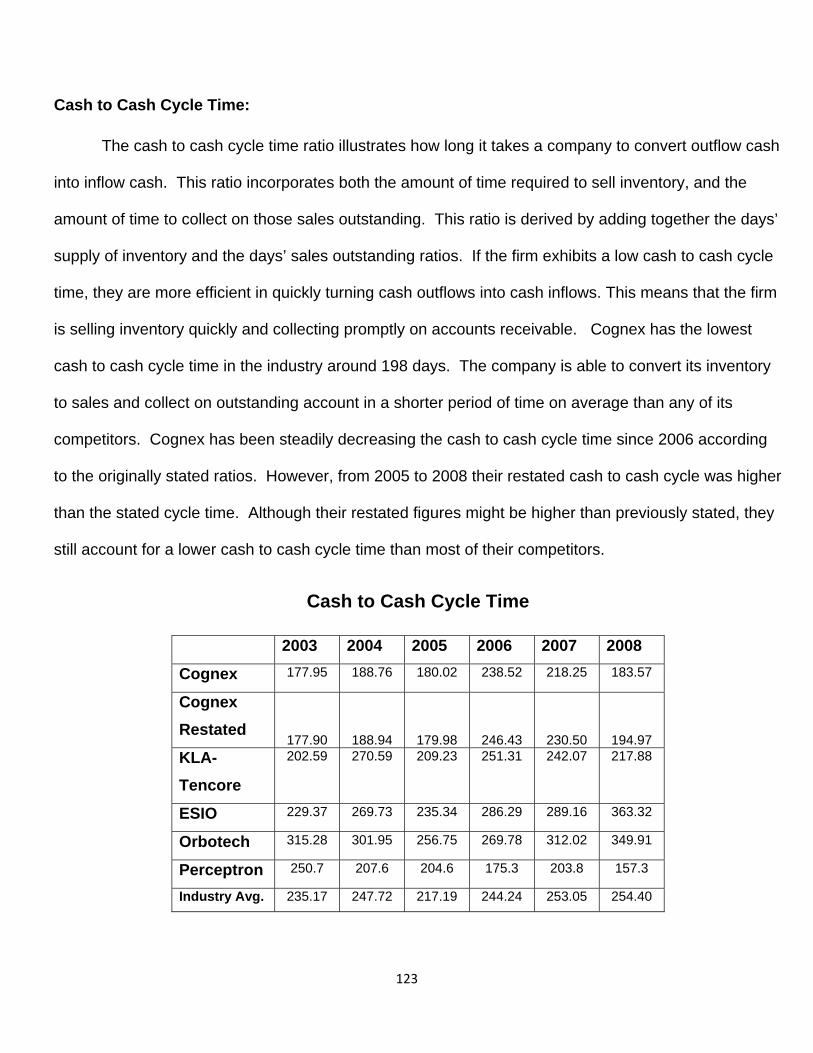

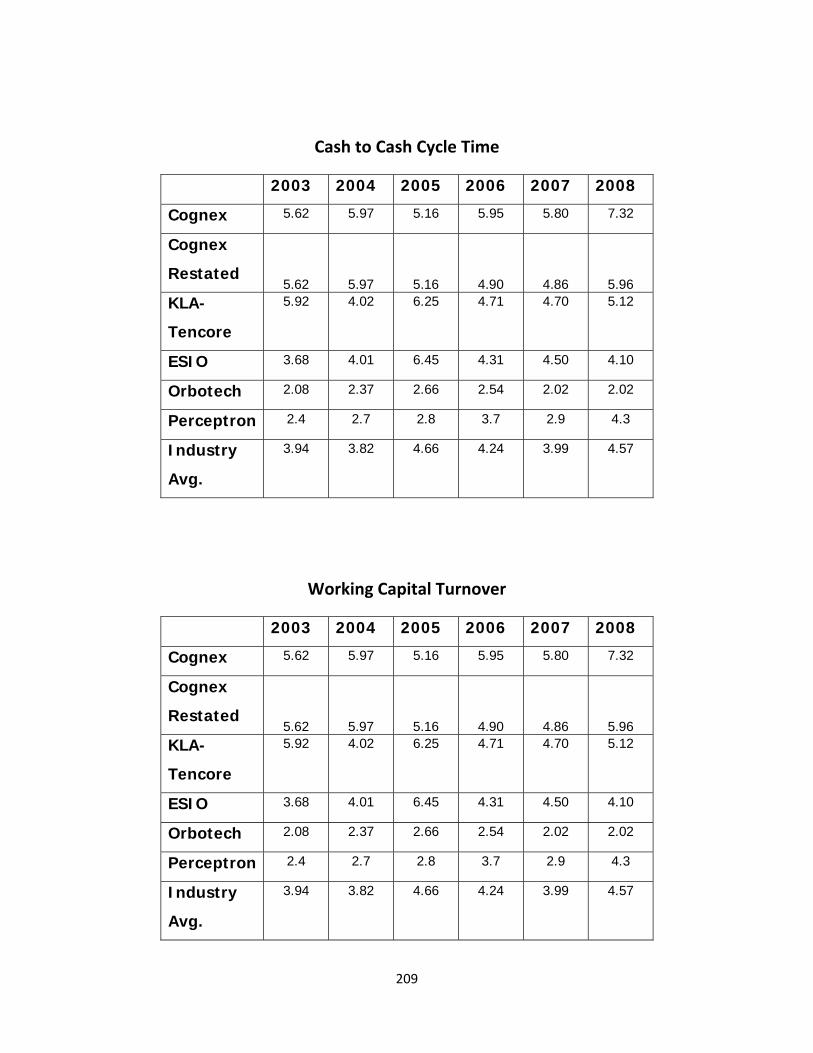

Cash to Cash Cycle 122

Working Capital Turnover 123

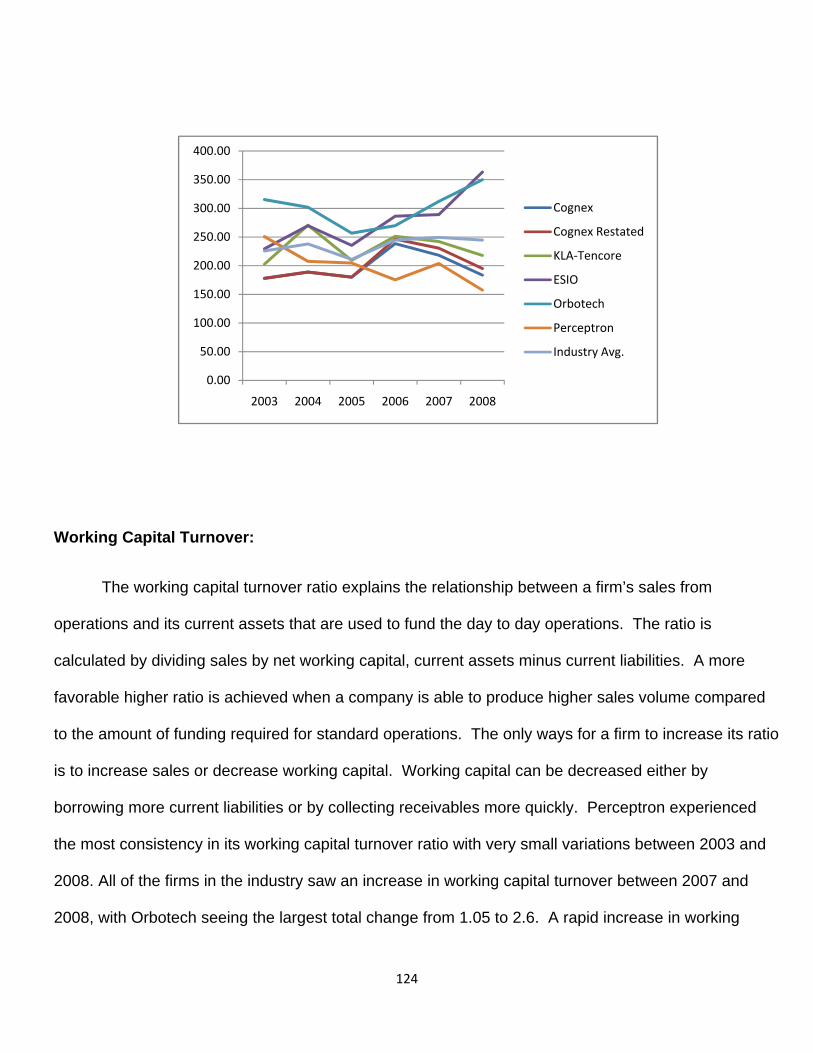

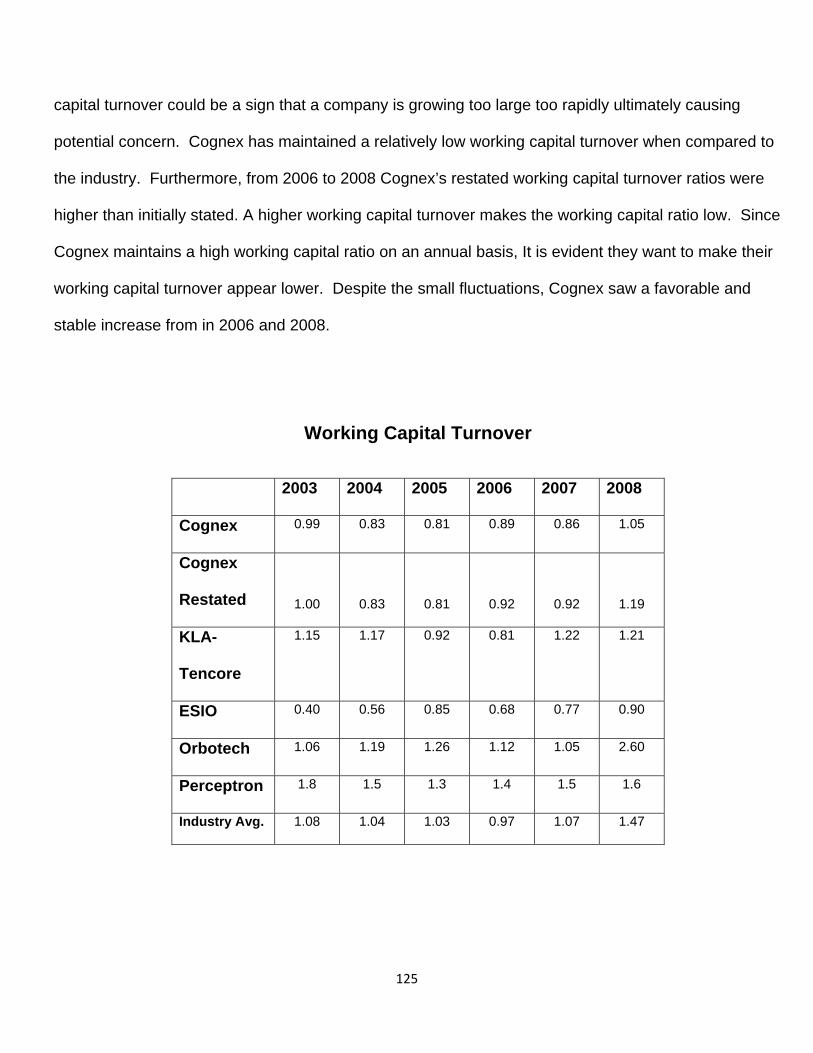

Conclusion 125

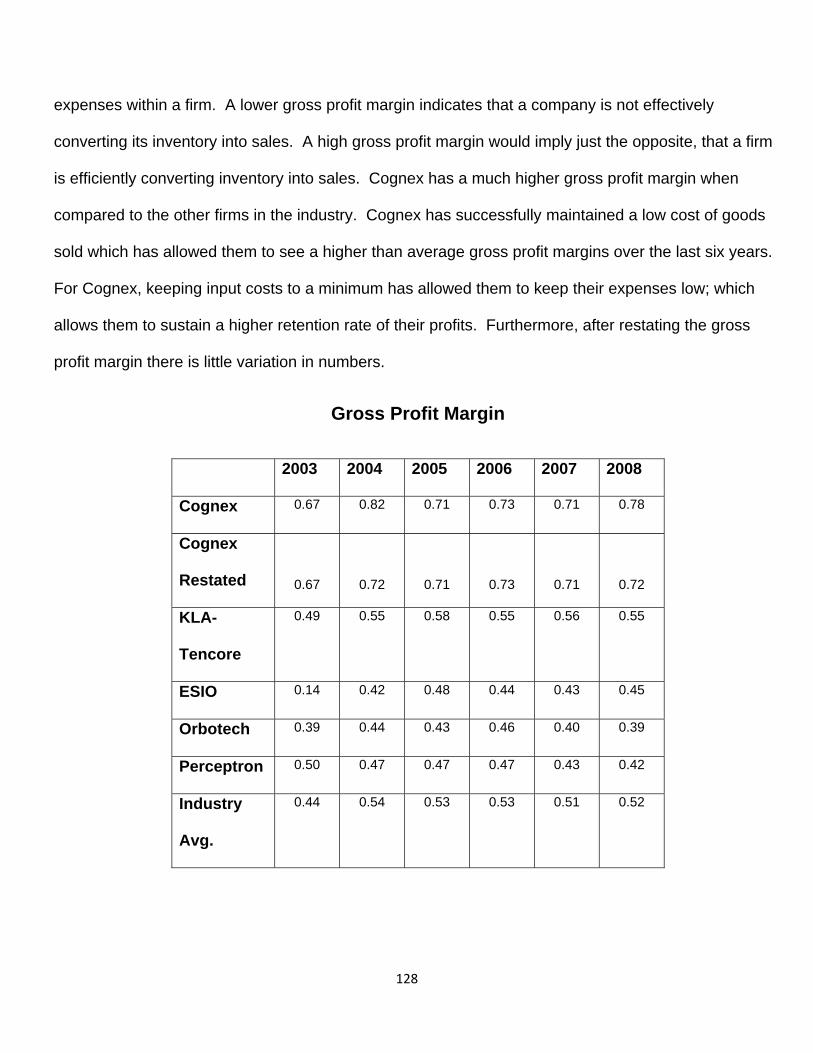

Profitability Ratio Analysis 126

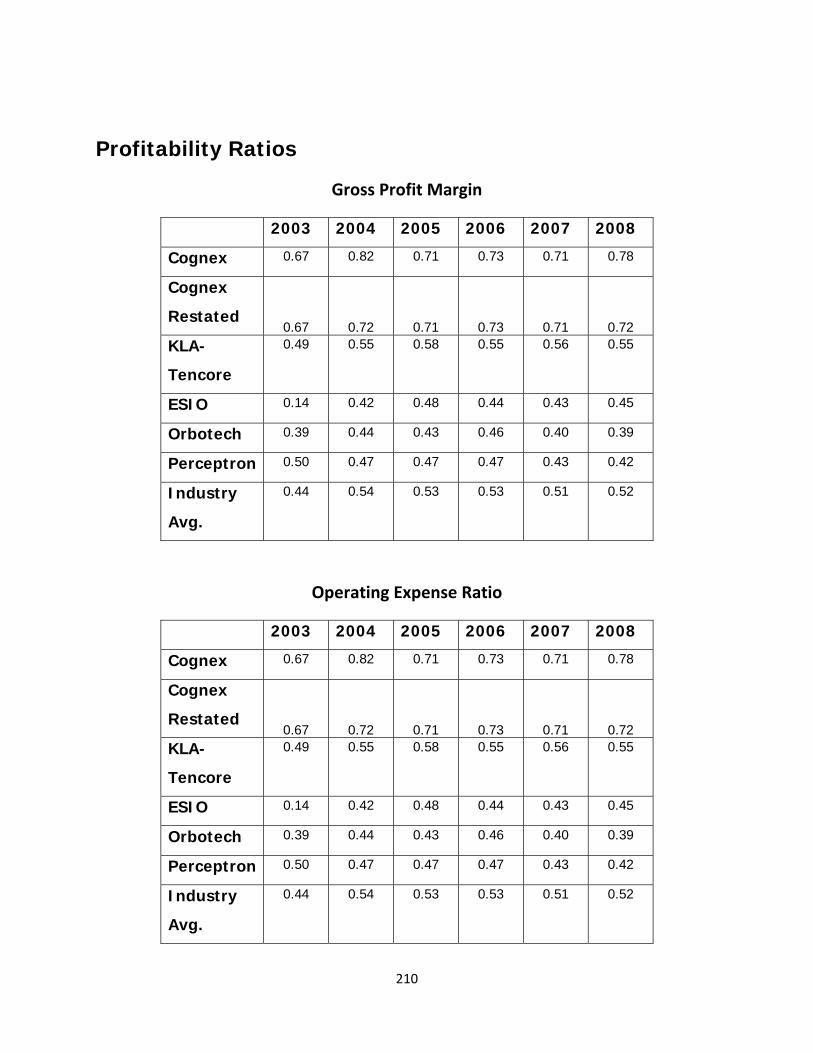

Gross Profit Margin 126

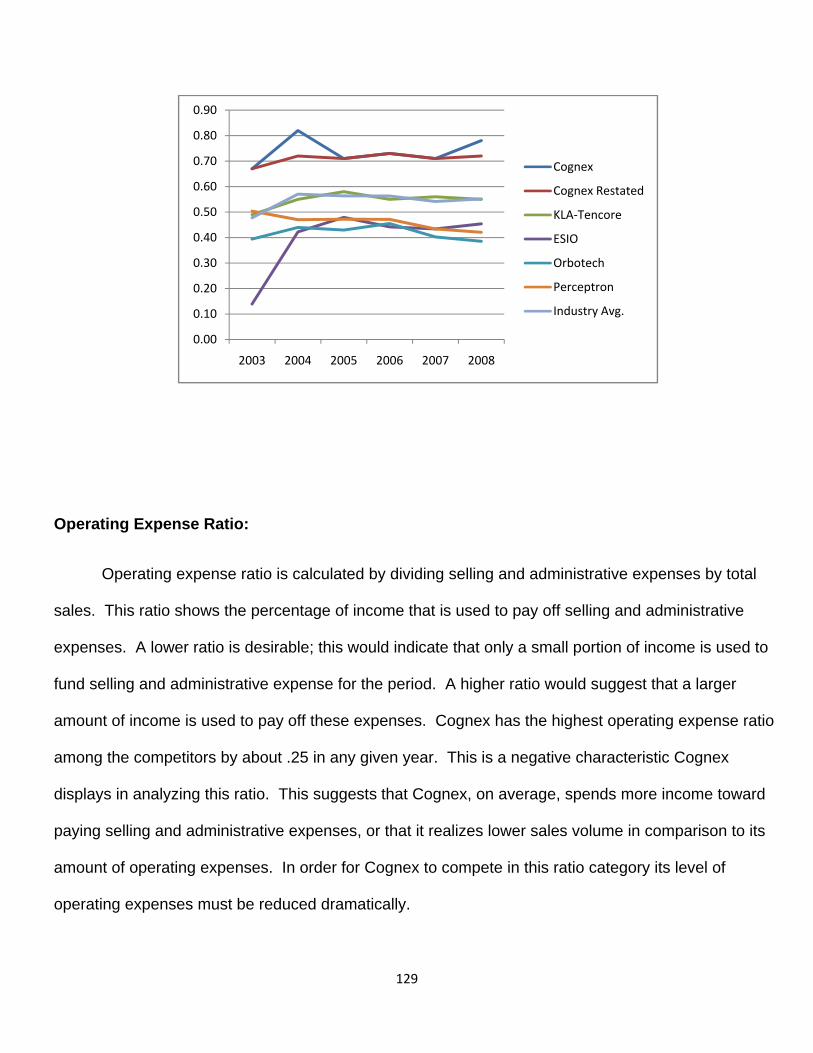

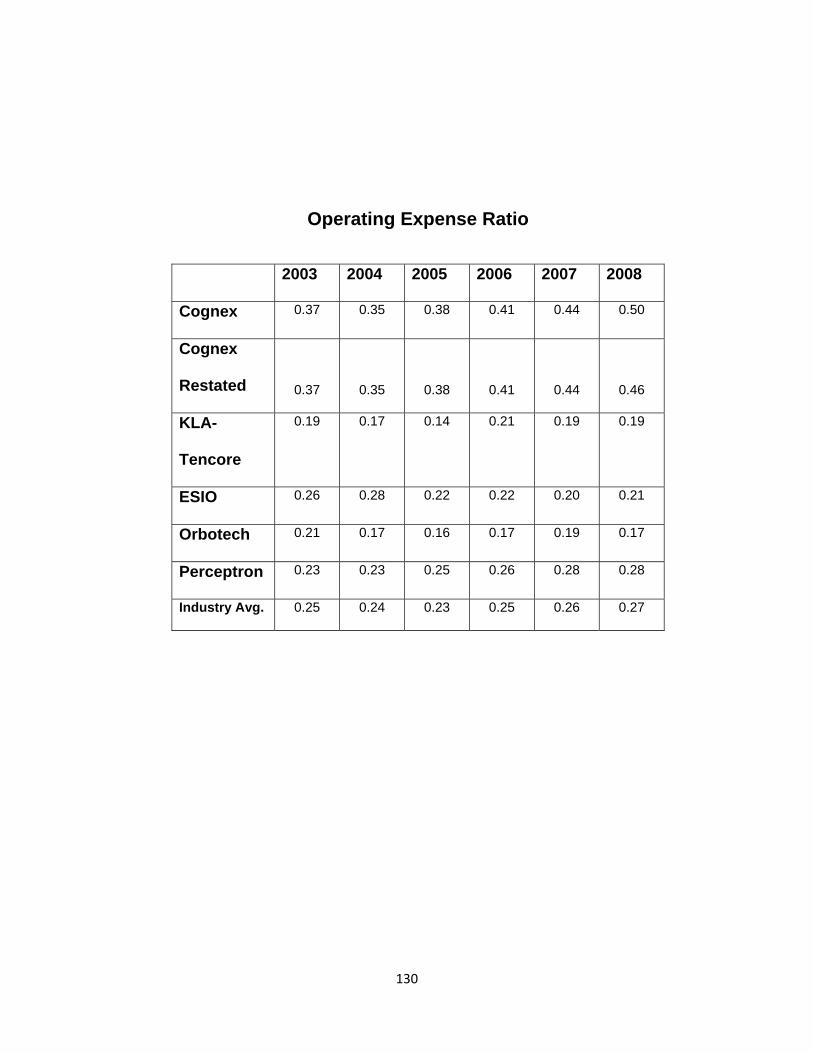

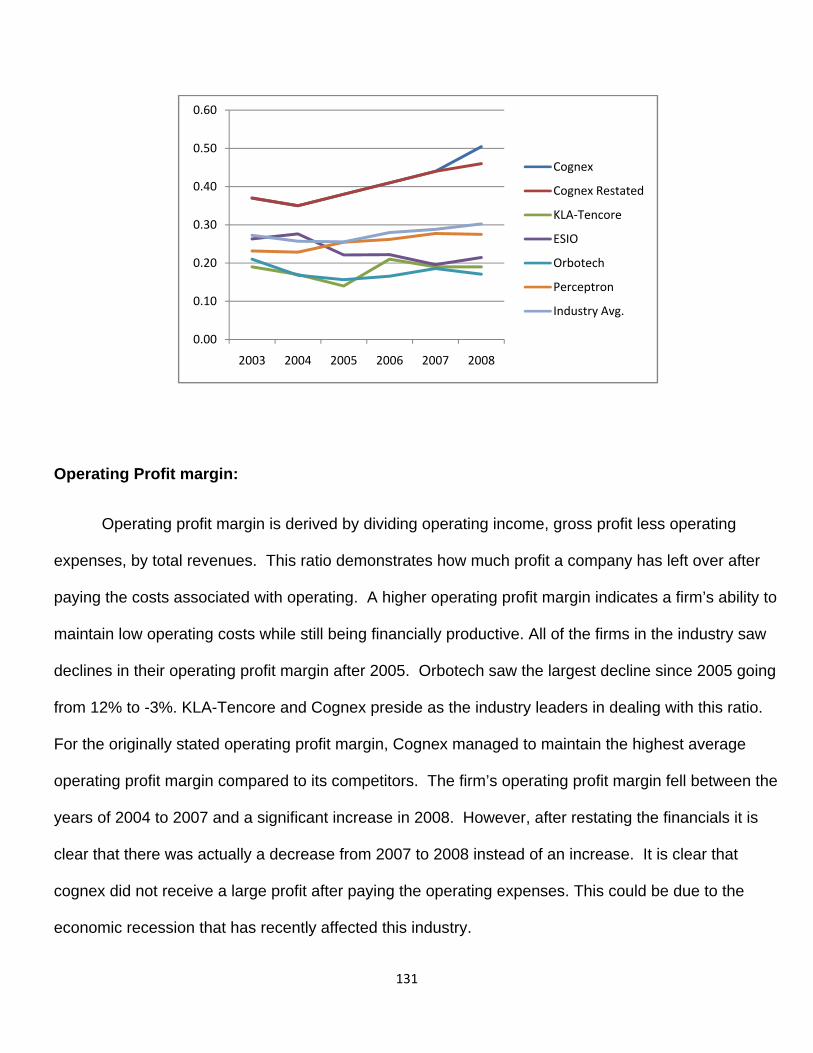

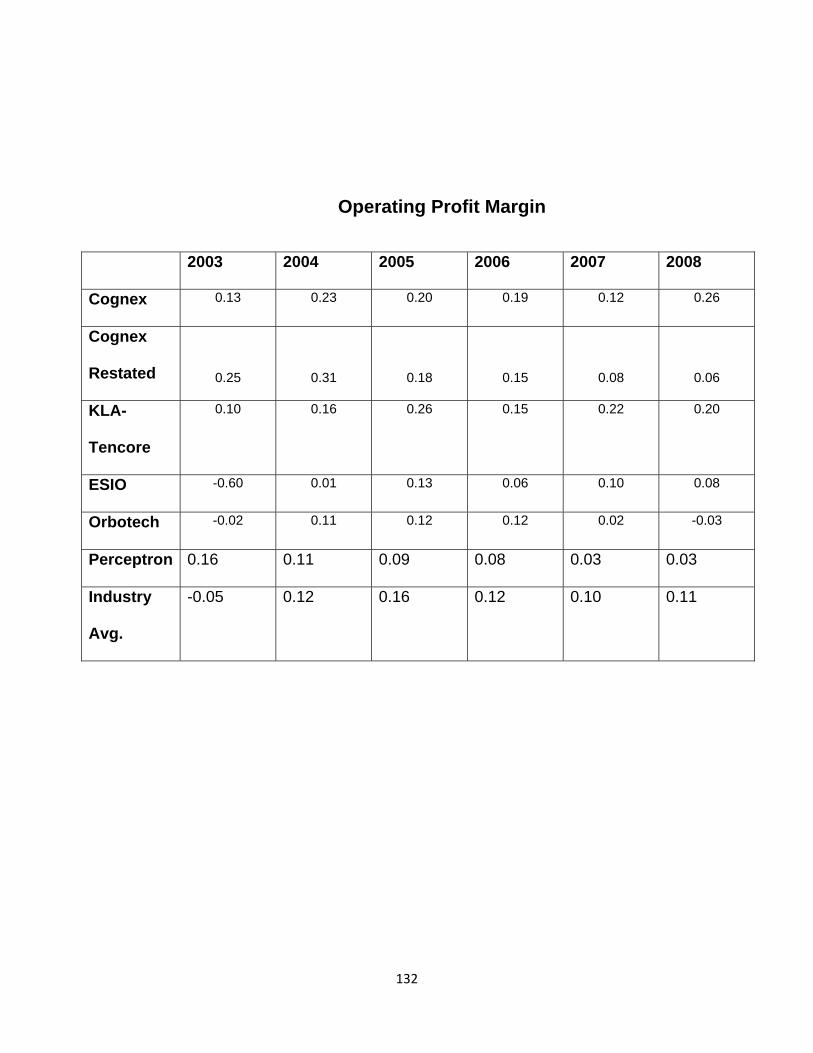

Operating expense ratio 128

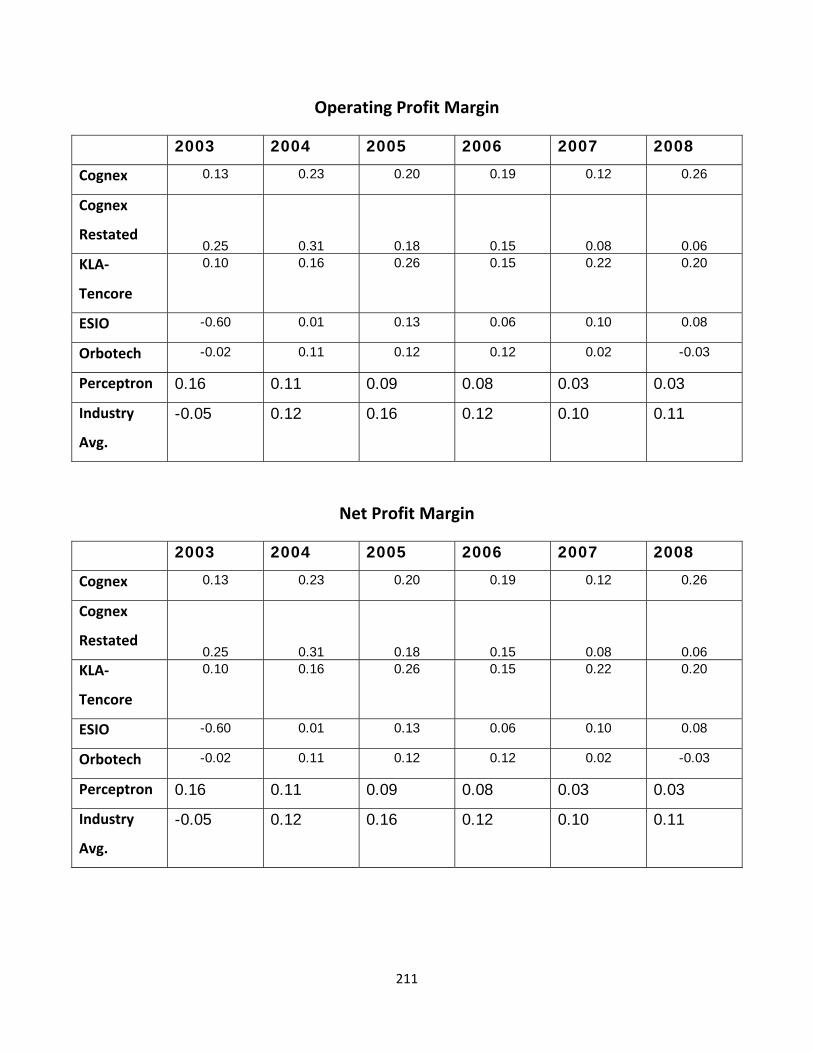

Operating profit margin 130

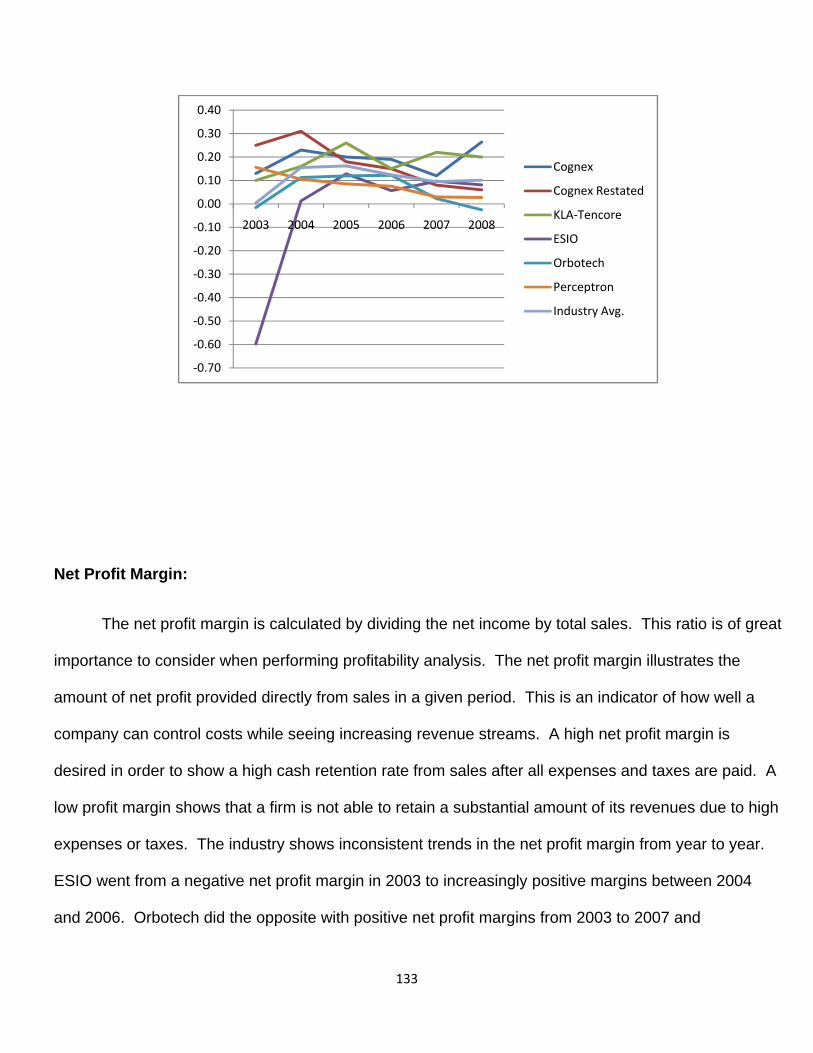

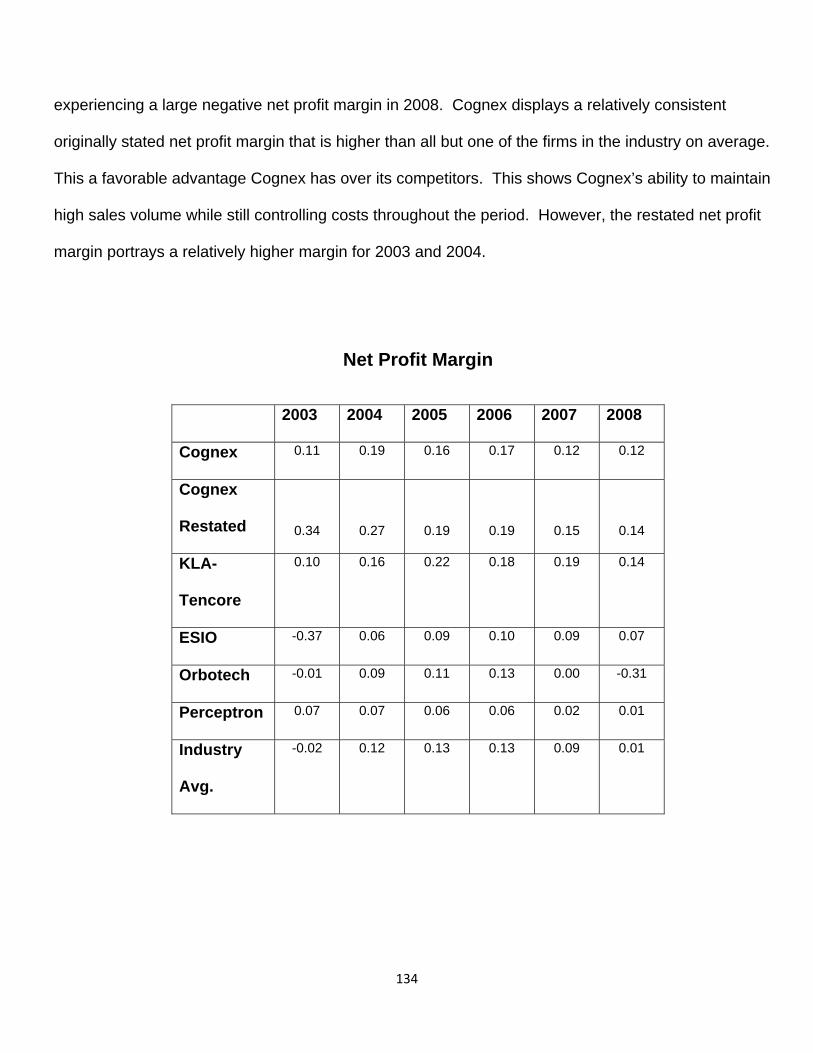

Net Profit Margin 132

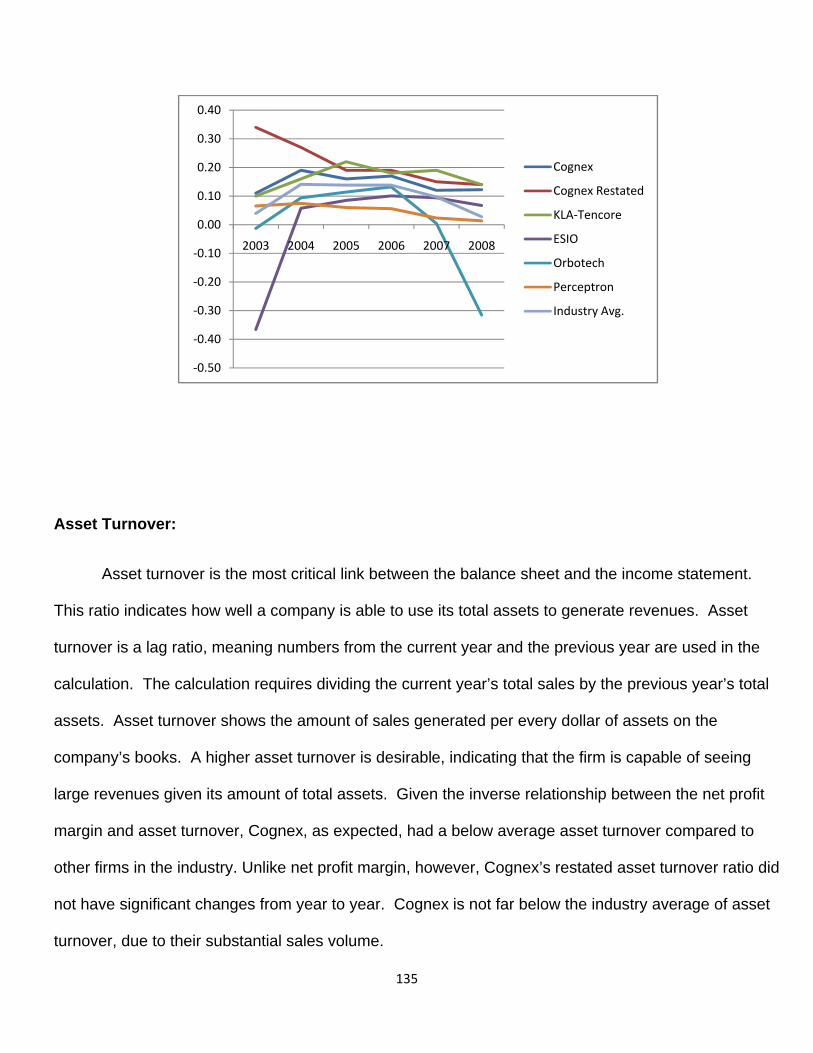

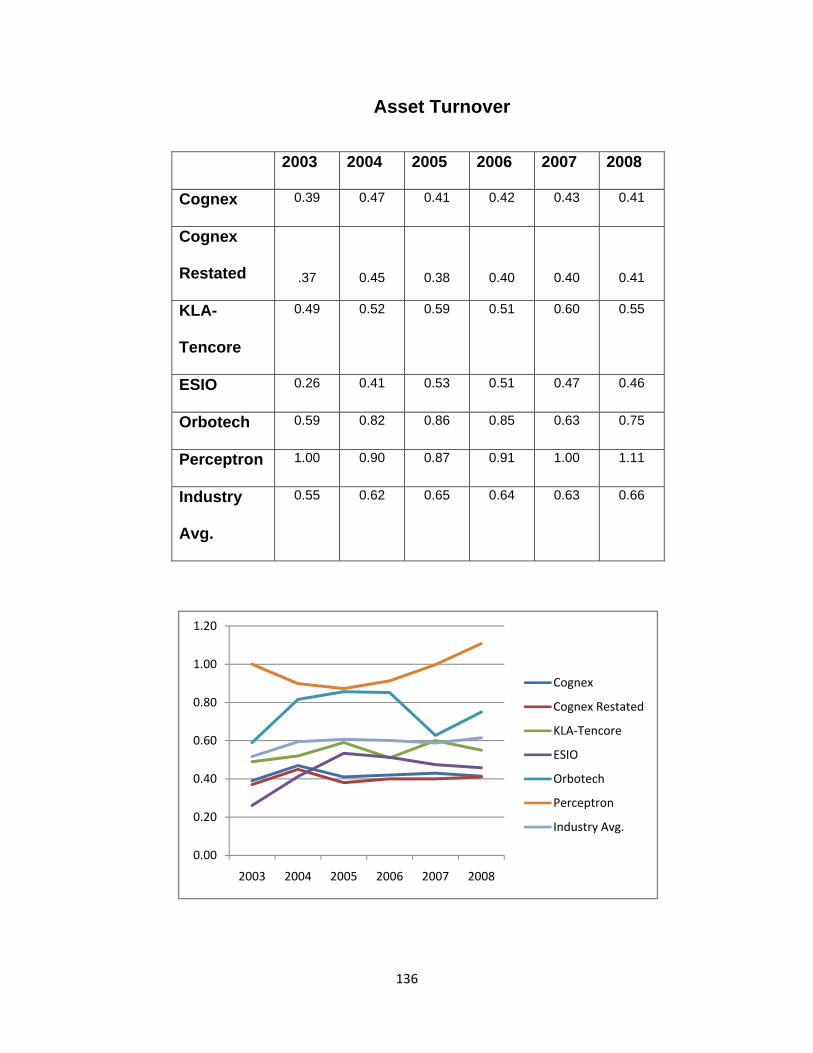

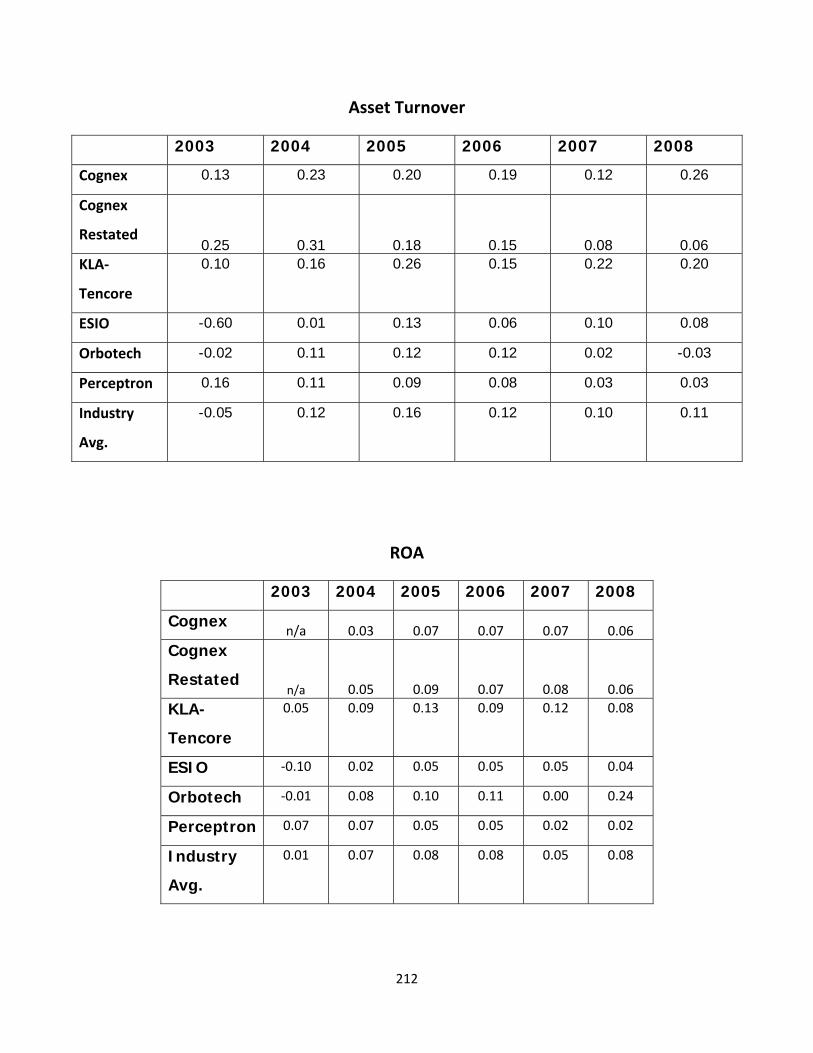

Asset Turnover 134

ROA 136

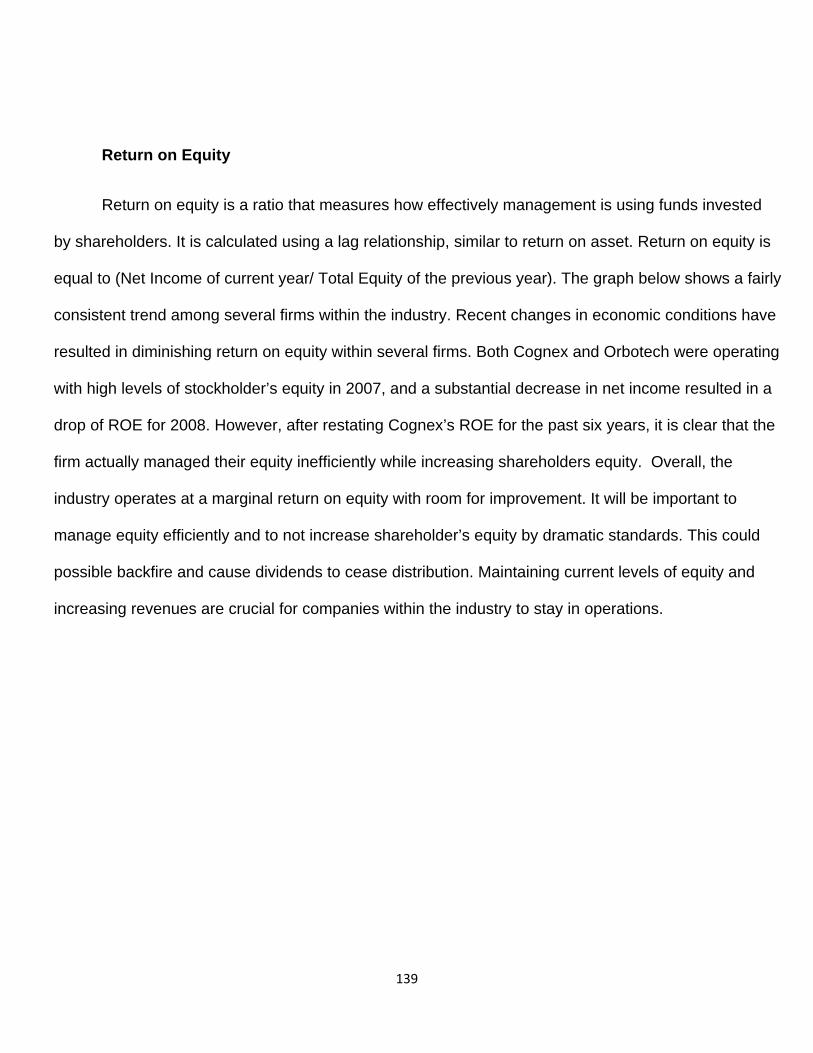

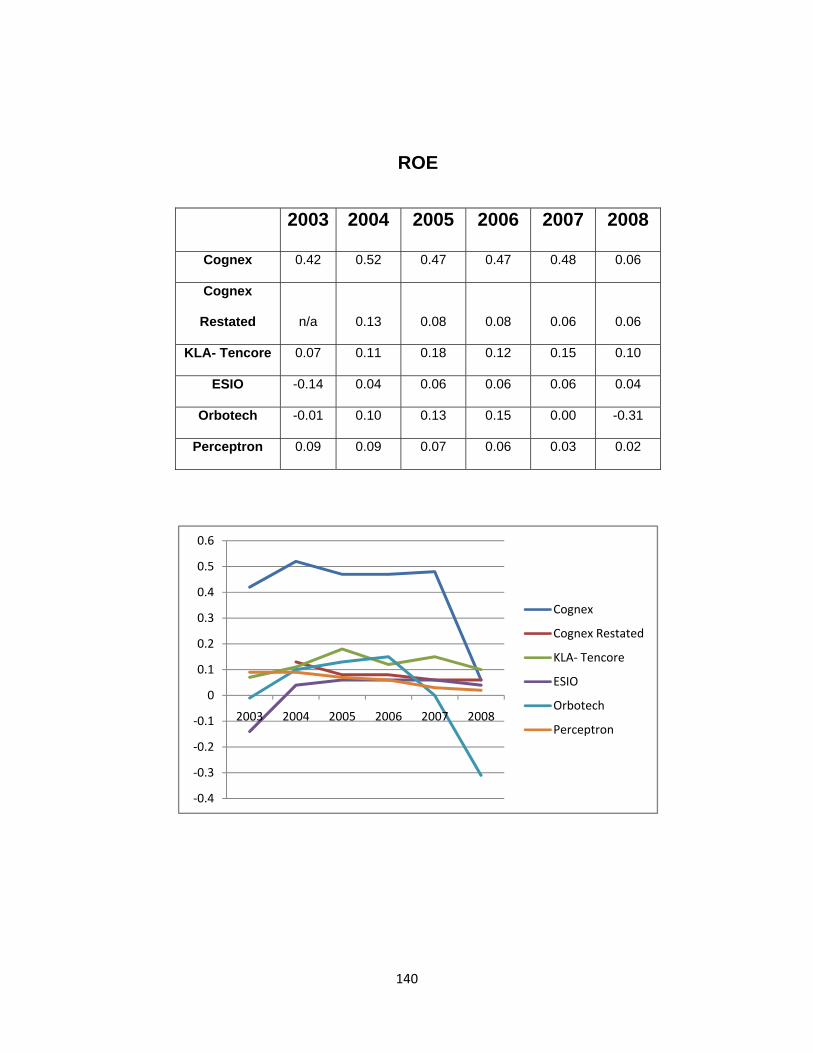

ROE 138

Conclusion 140

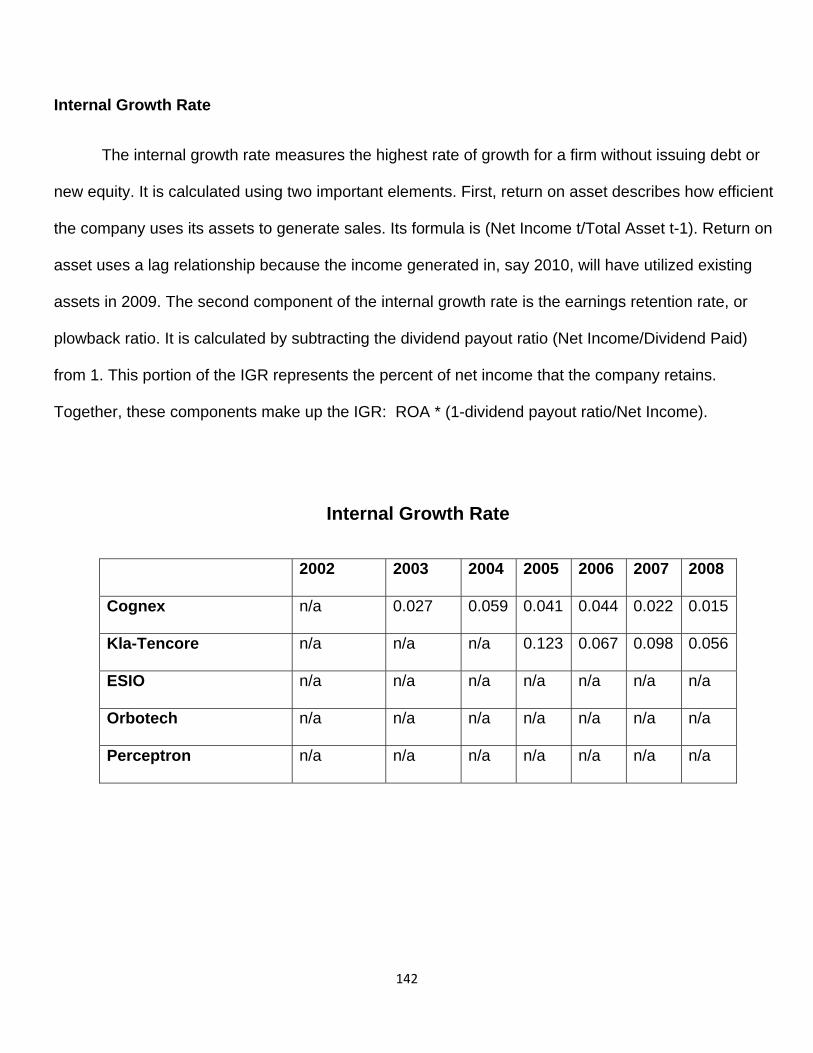

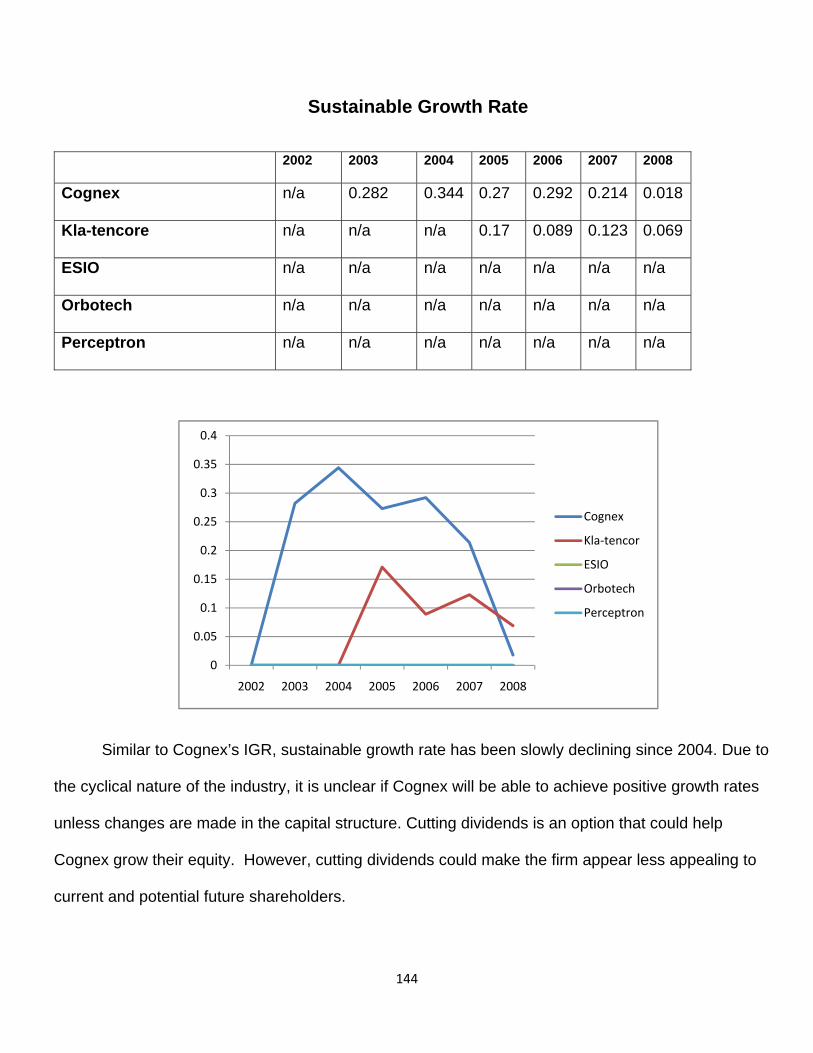

Growth rate Ratios 140

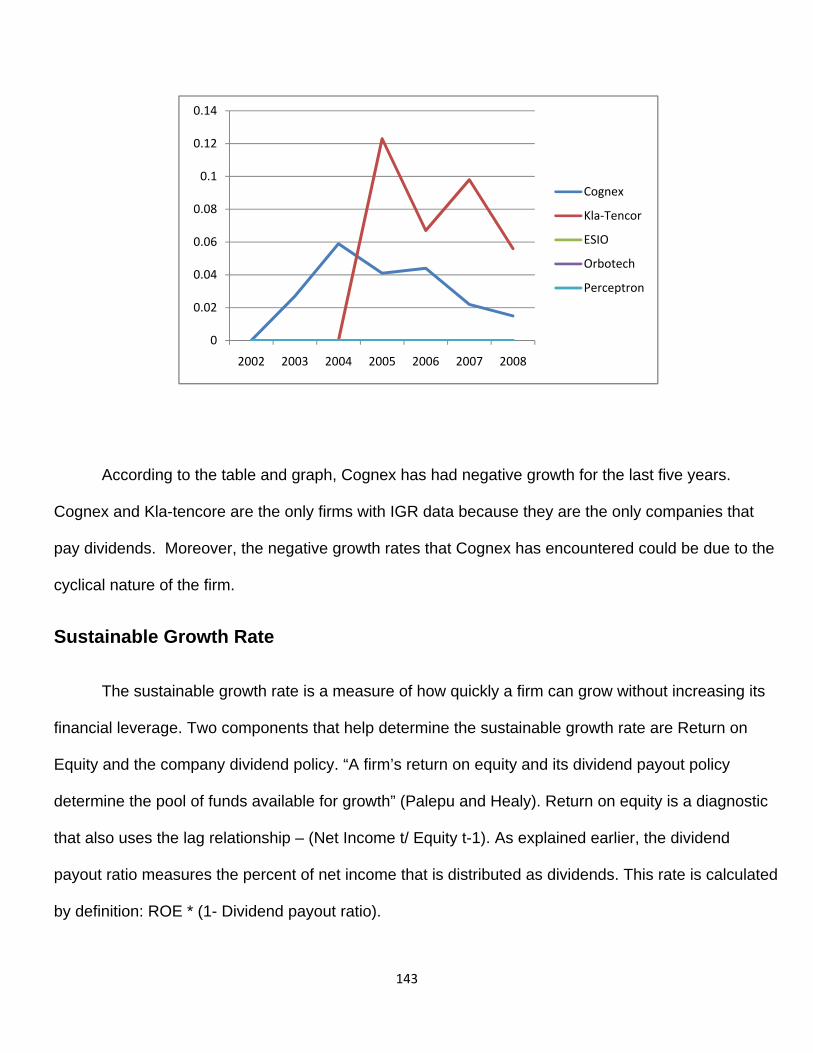

Internal growth rate 141

Sustainable growth rate 142

Conclusion 144

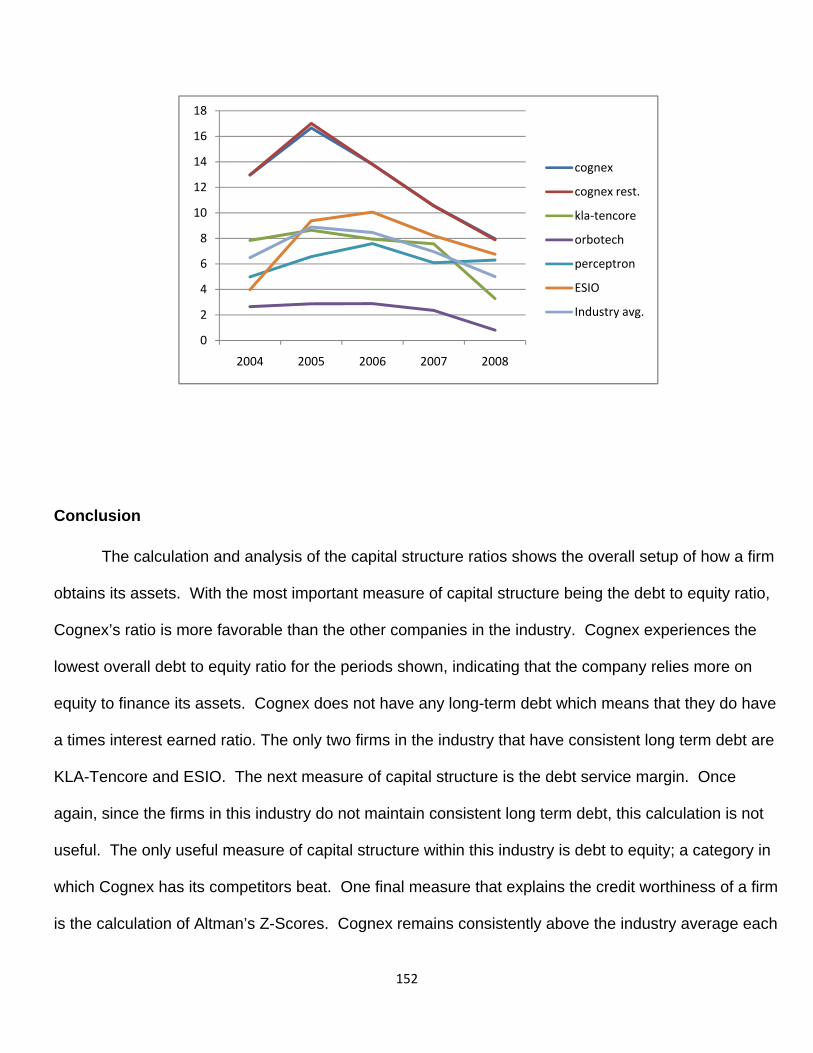

Capital Structure Analysis 144

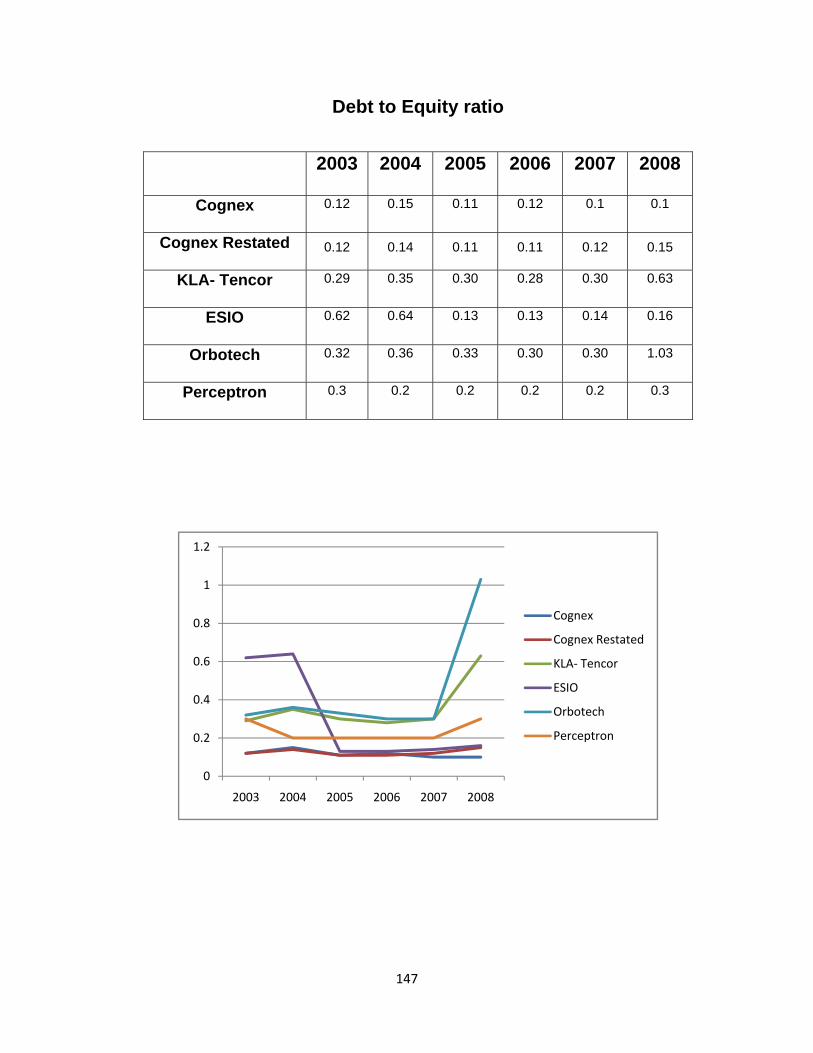

Debt to Equity ratio 145

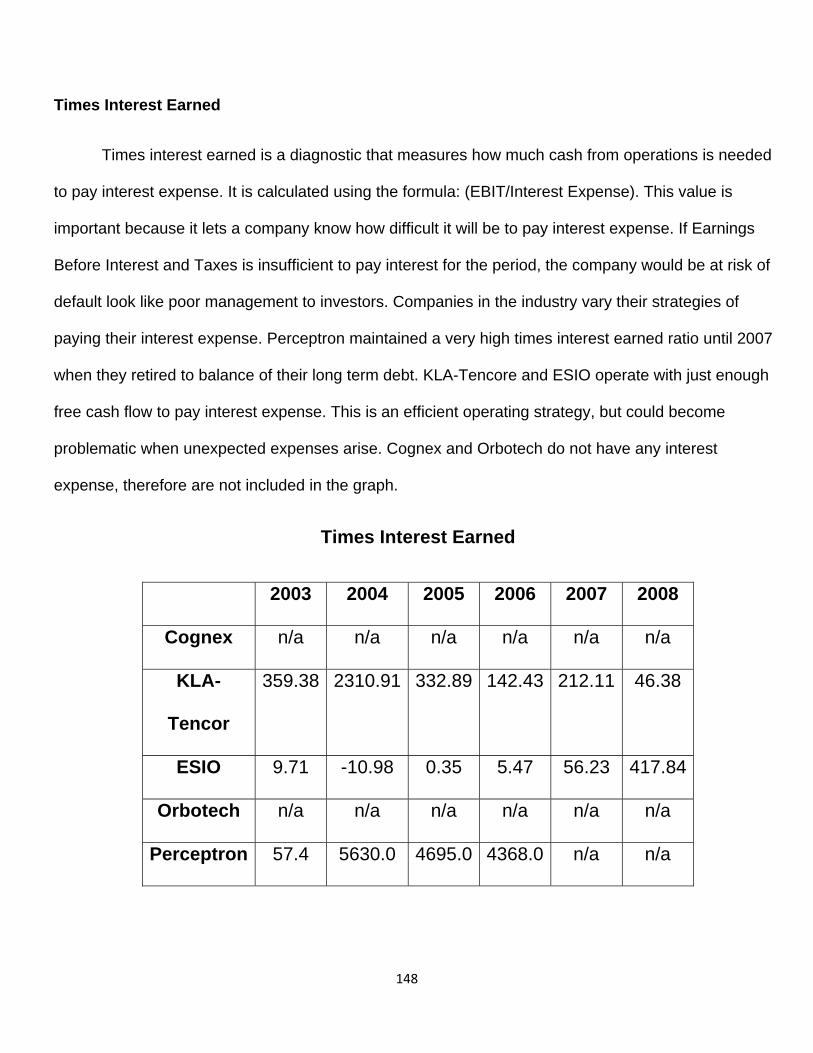

Times interest Earned 147

7

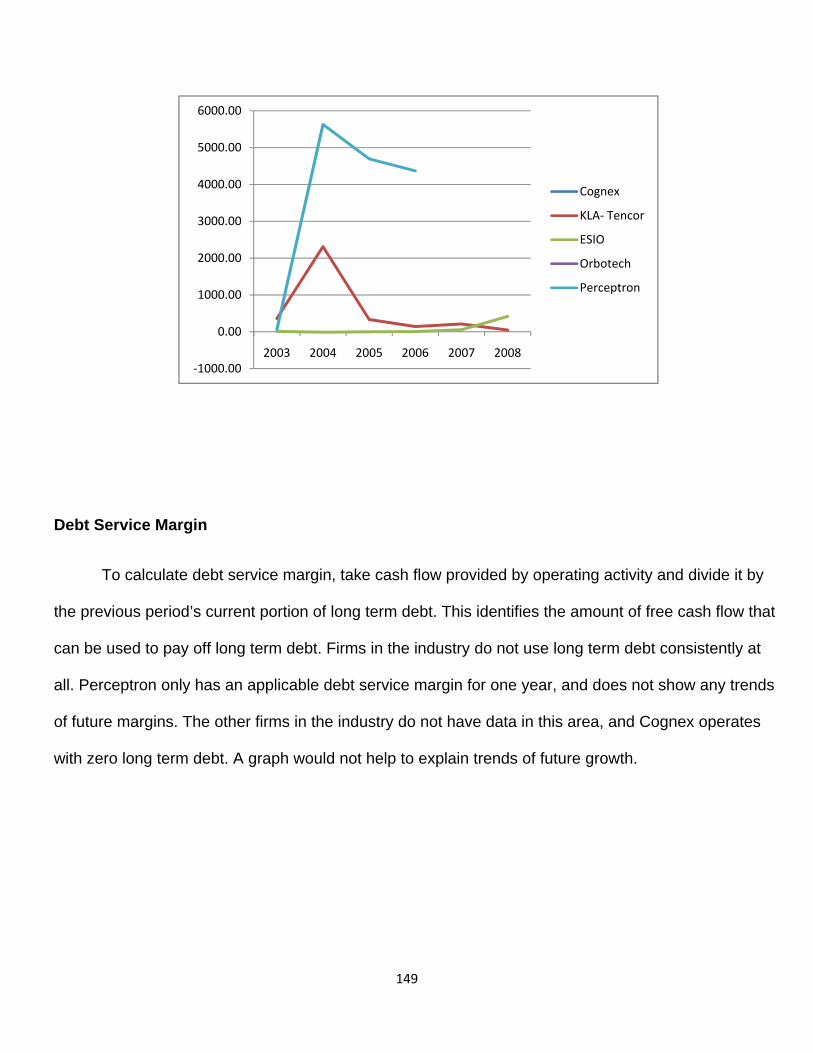

Debt Service margin 148

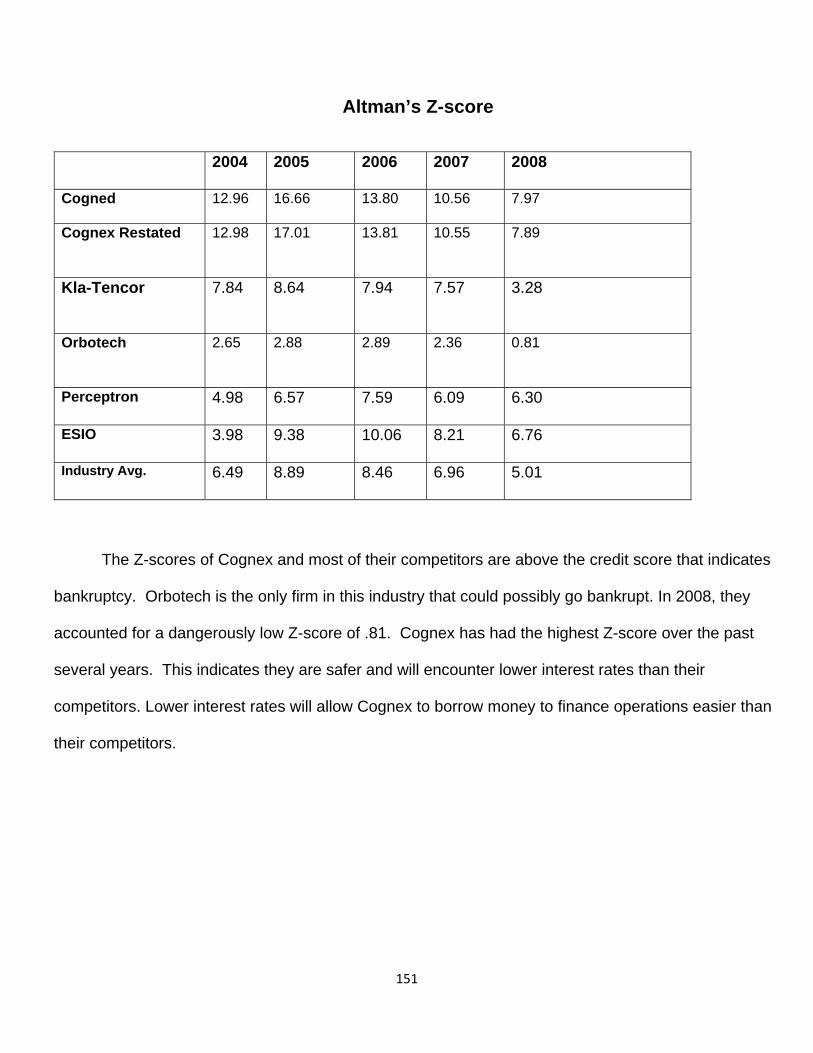

Z-score 149

Conclusion 151

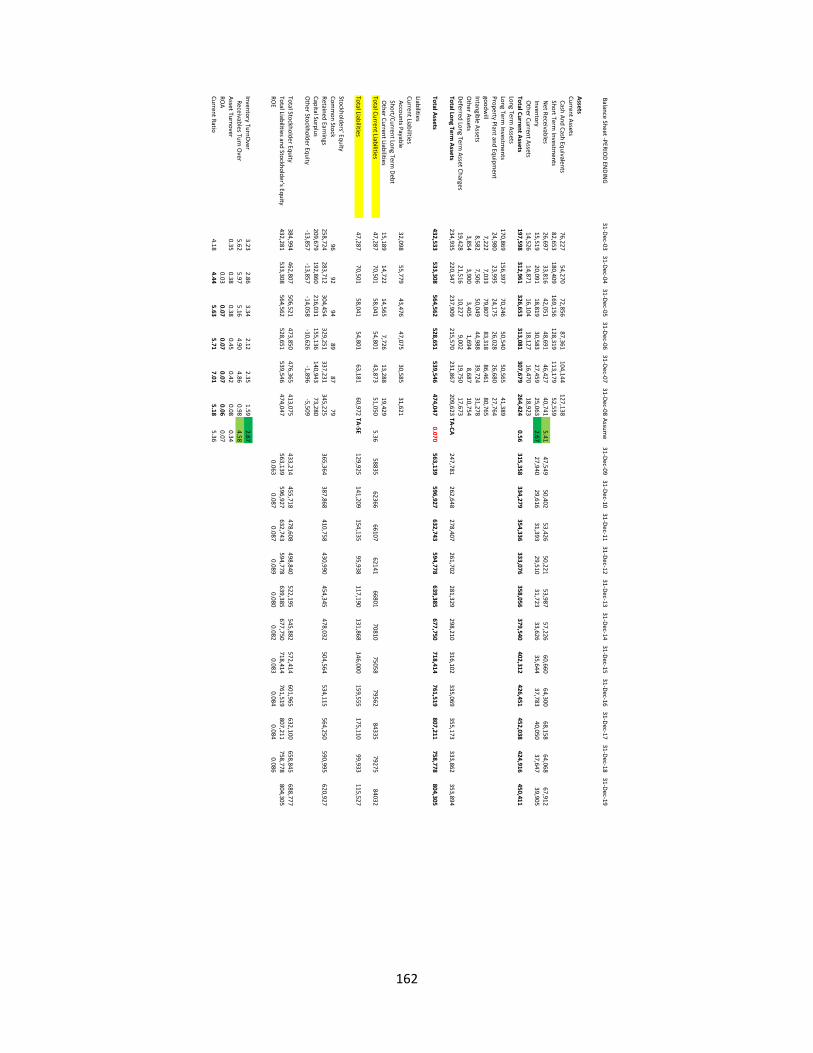

Financial Statement Forcasting 152

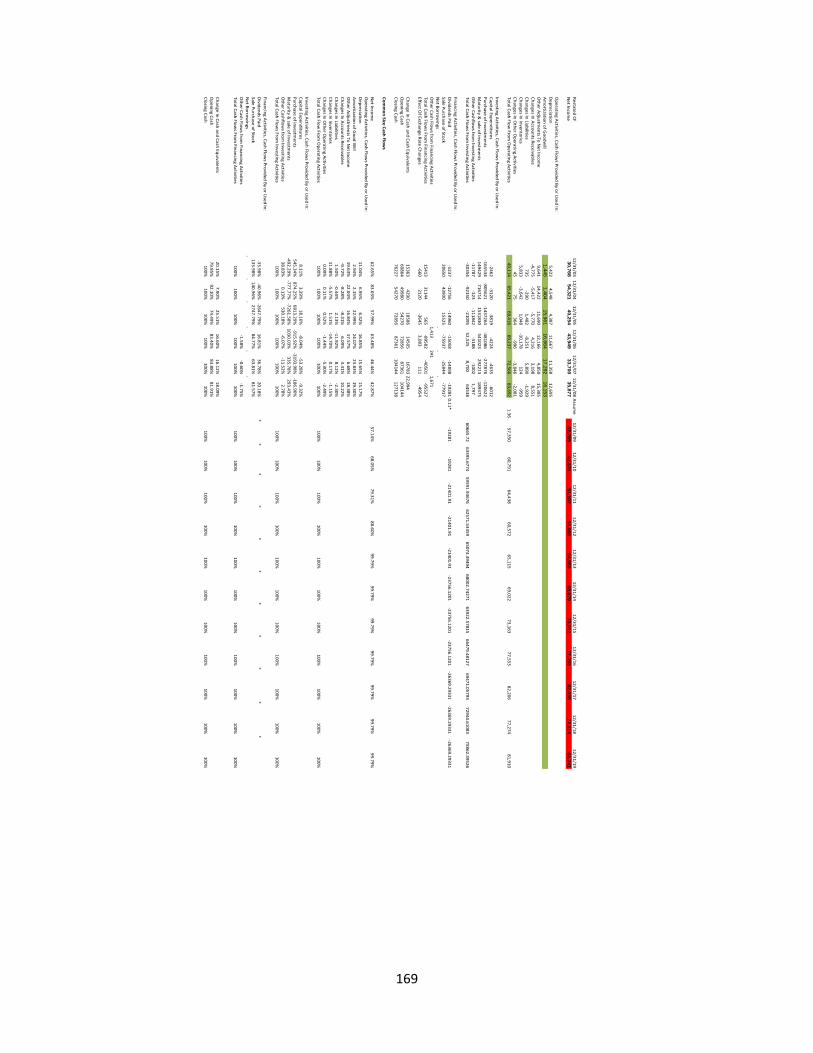

Income Statement 152 Income Statement (Restated) 157 Balance Sheet 159 Balance Sheet (Restated) 162 Statement of Cash Flows 164 Statement of Cash Flows (Restated) 167

Estimating Cost of Capital

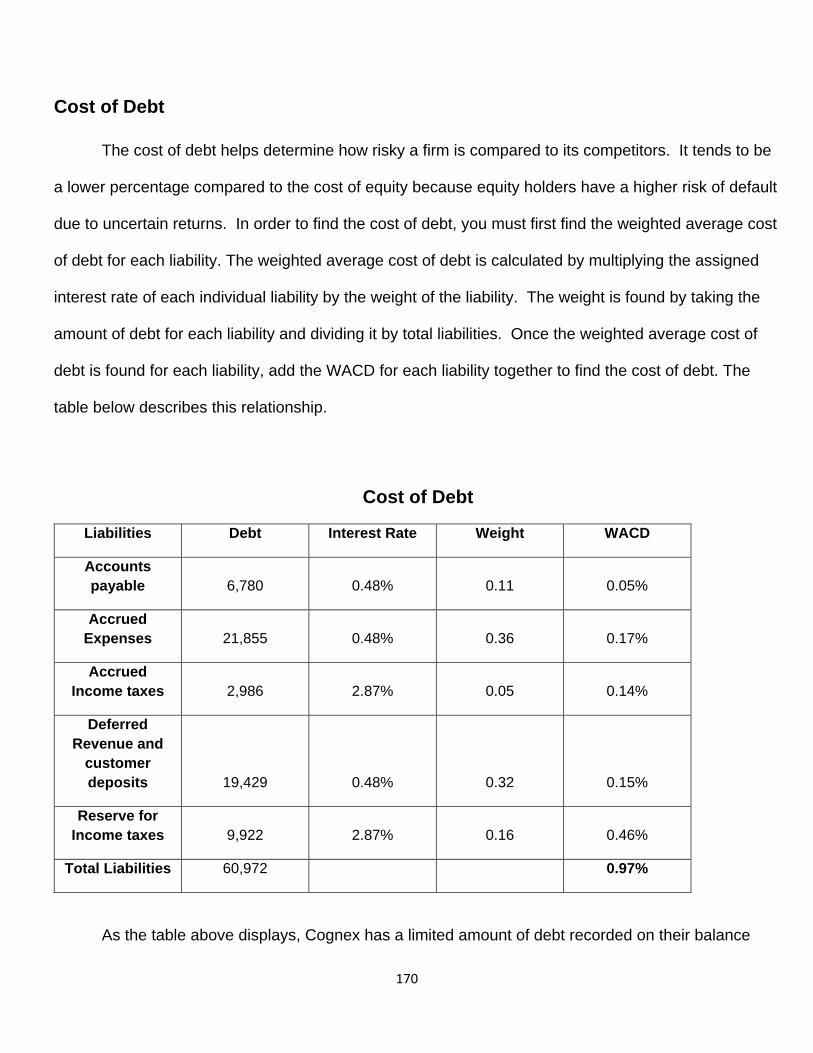

Cost of Debt 169

Cost of Equity 170

Size Adjusted 173

Alternative Cost of Equity 173

Weighted average cost of capital 174

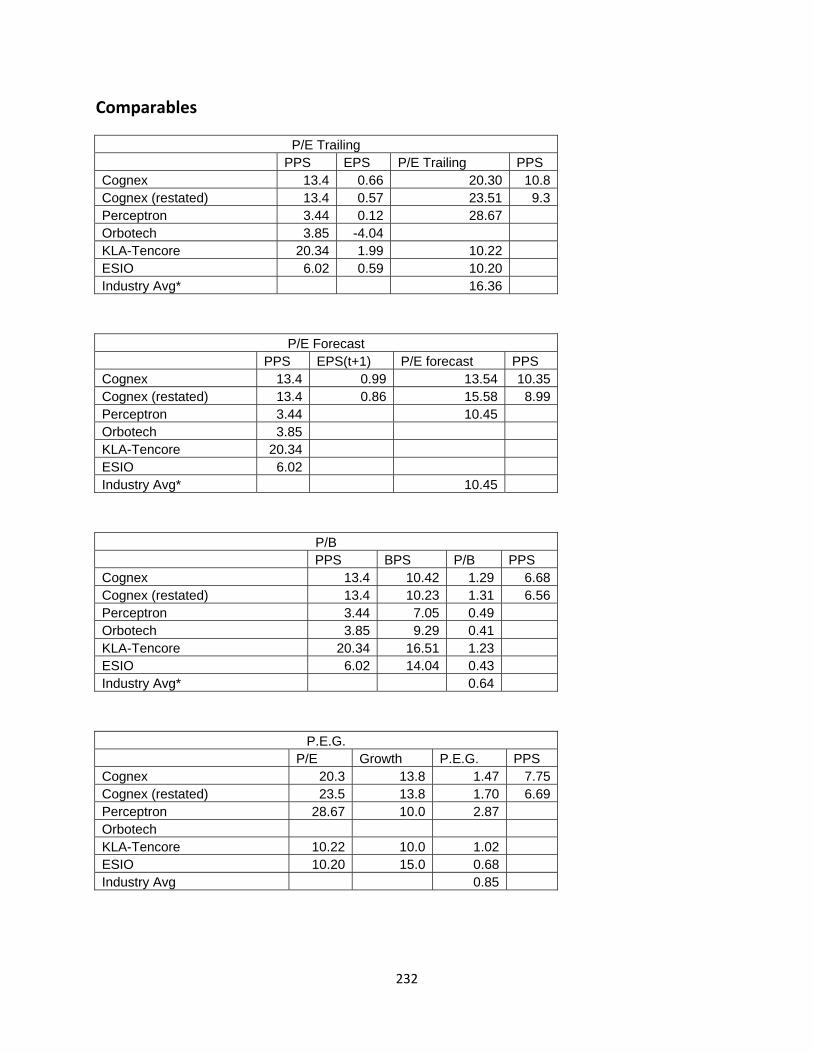

Method of Comparables 175

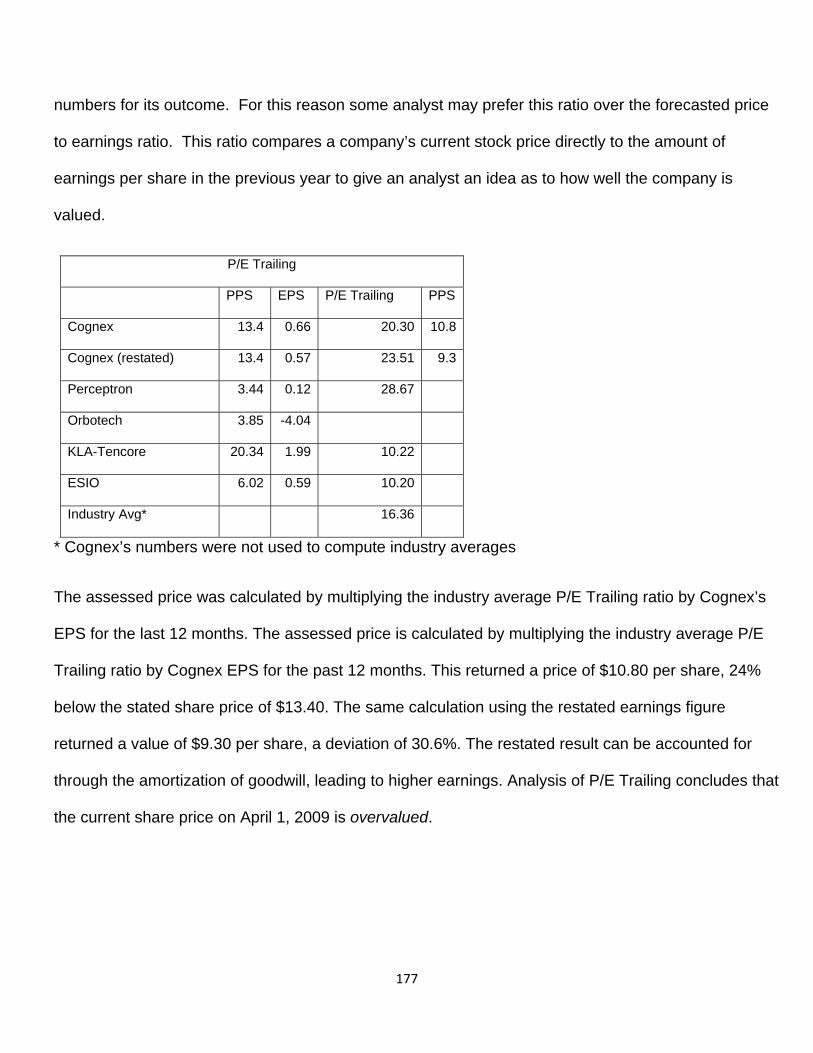

P/E Trailing 175

P/E Forecast 177

P/B 178

PEG 179

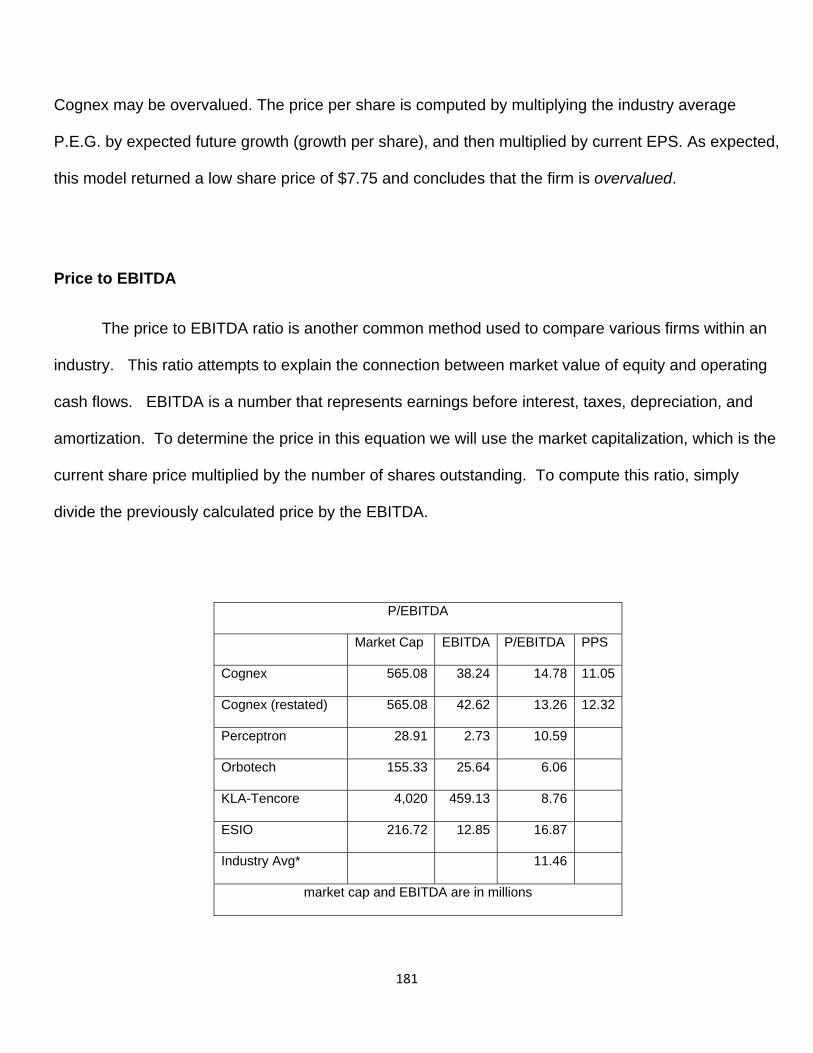

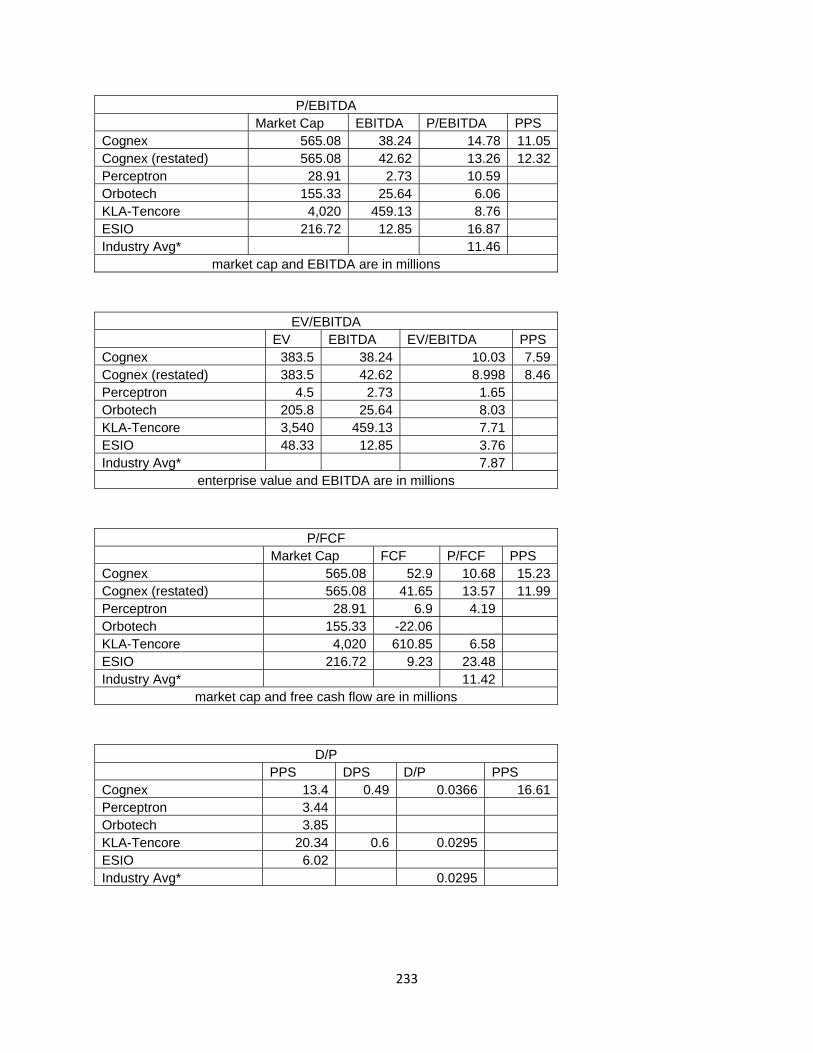

P/EBITDA 180

8

EV/EBITDA 181

P/FCF 182

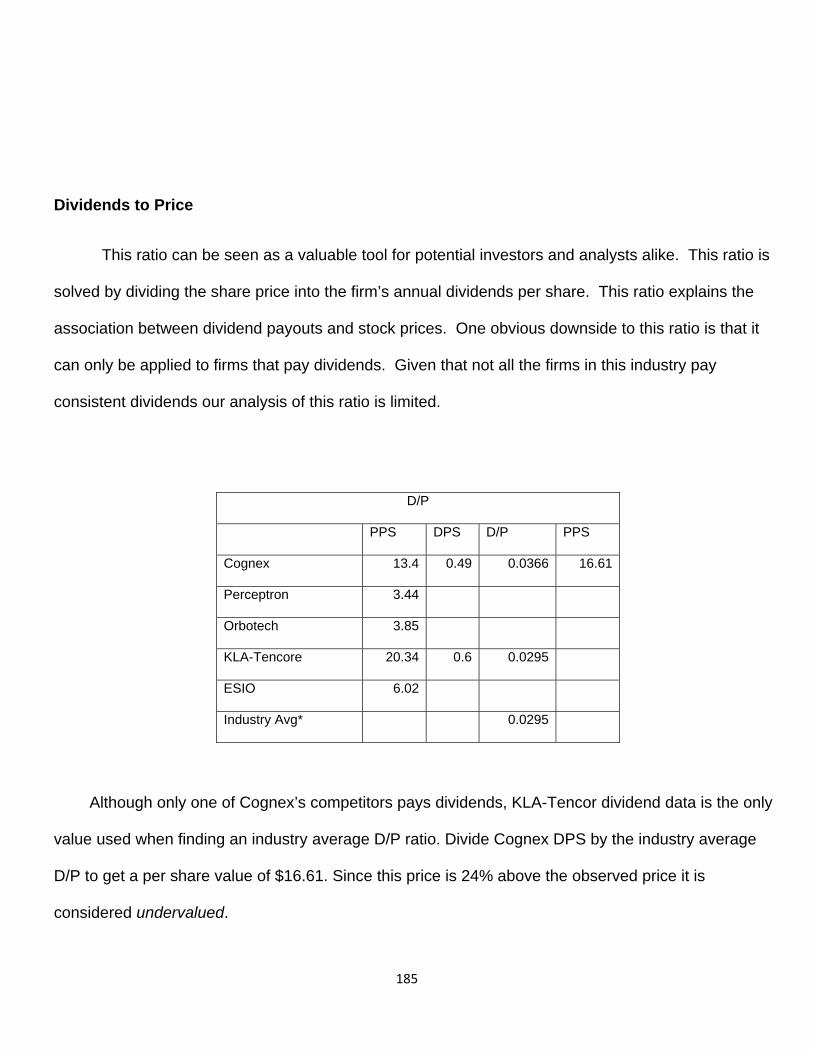

D/P 184

Conclusion 185

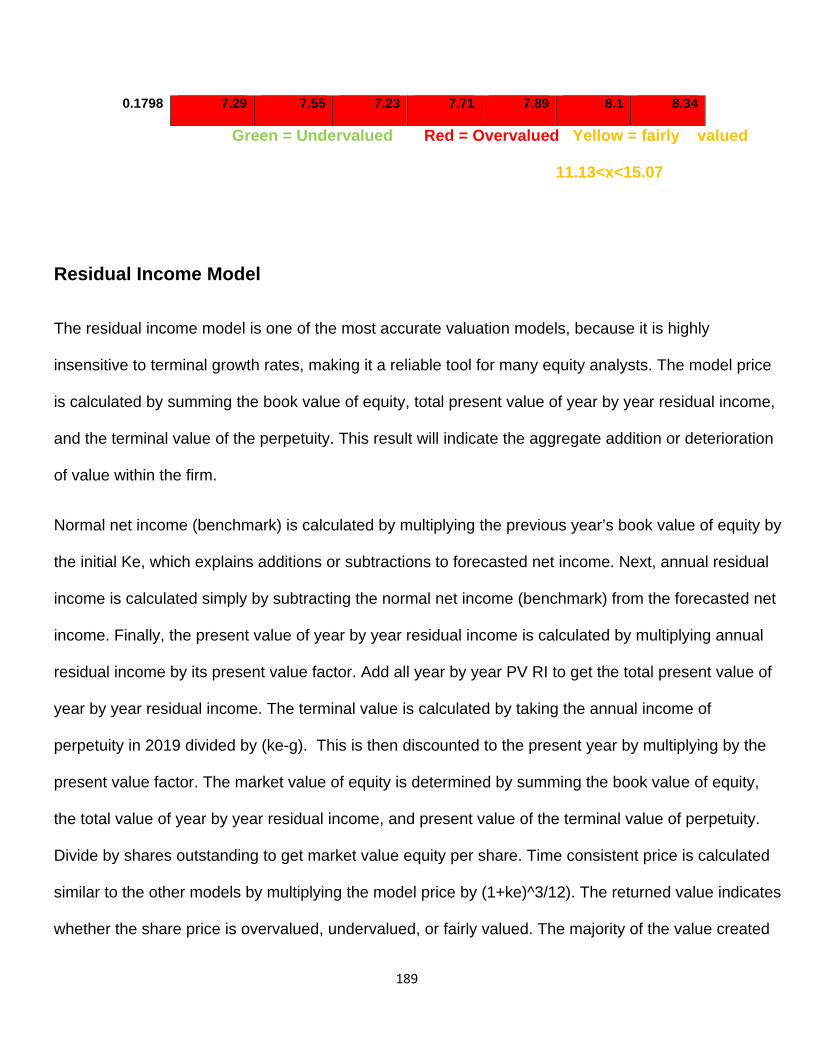

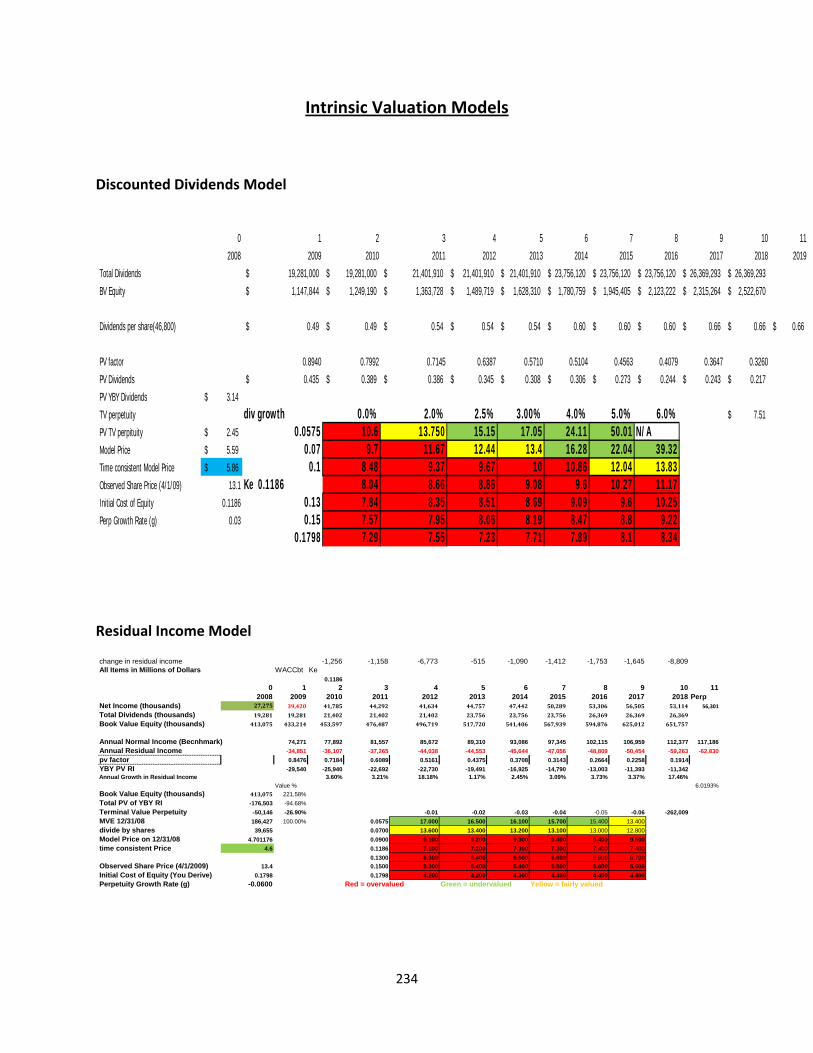

Intrinsic Valuation Models 186

Discounted Dividends Model 186

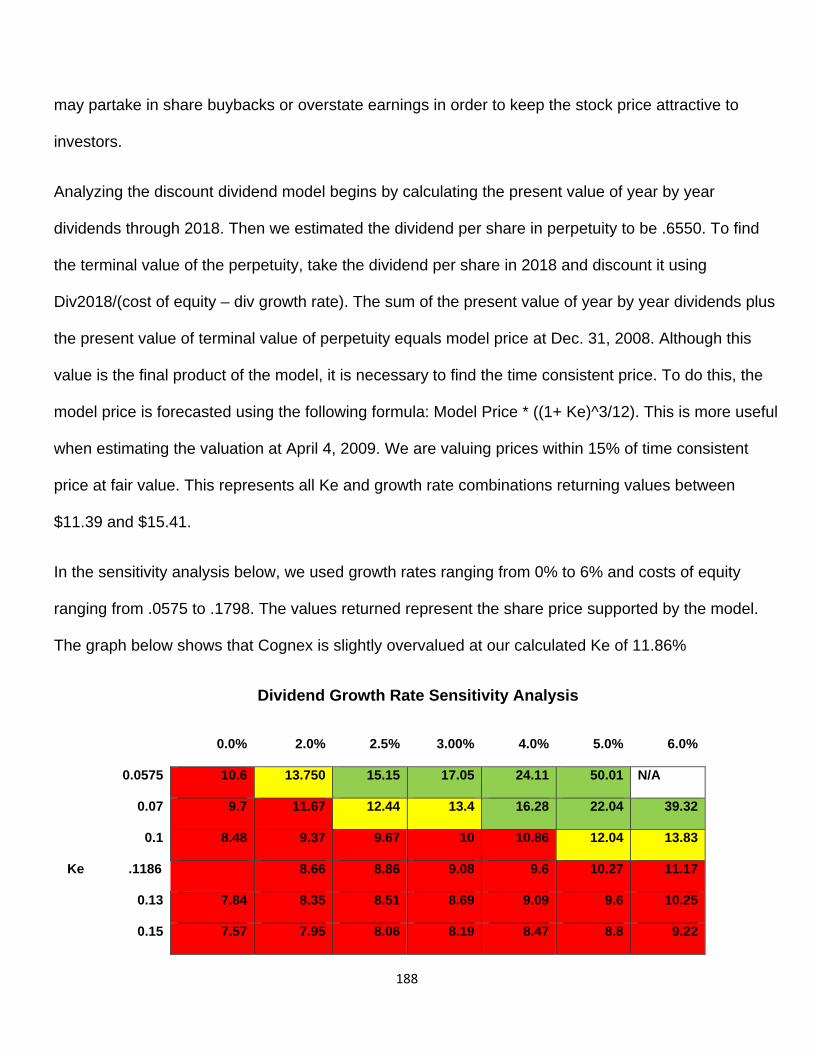

Residual Income Model 188

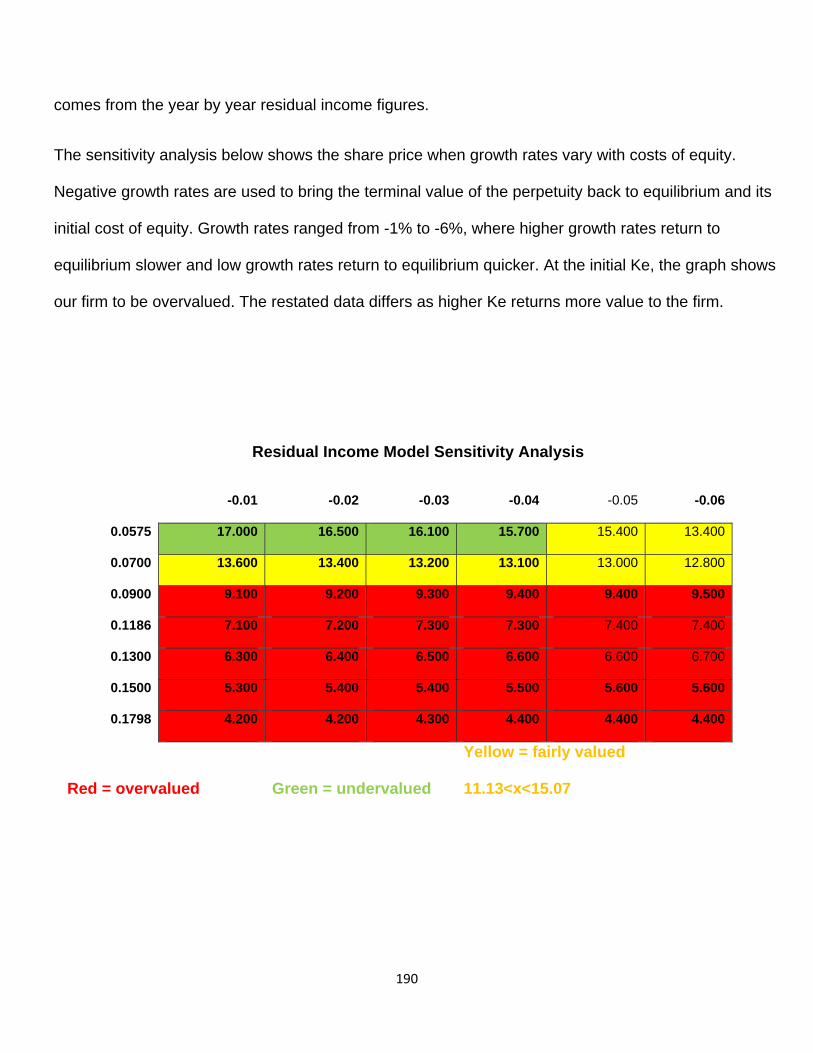

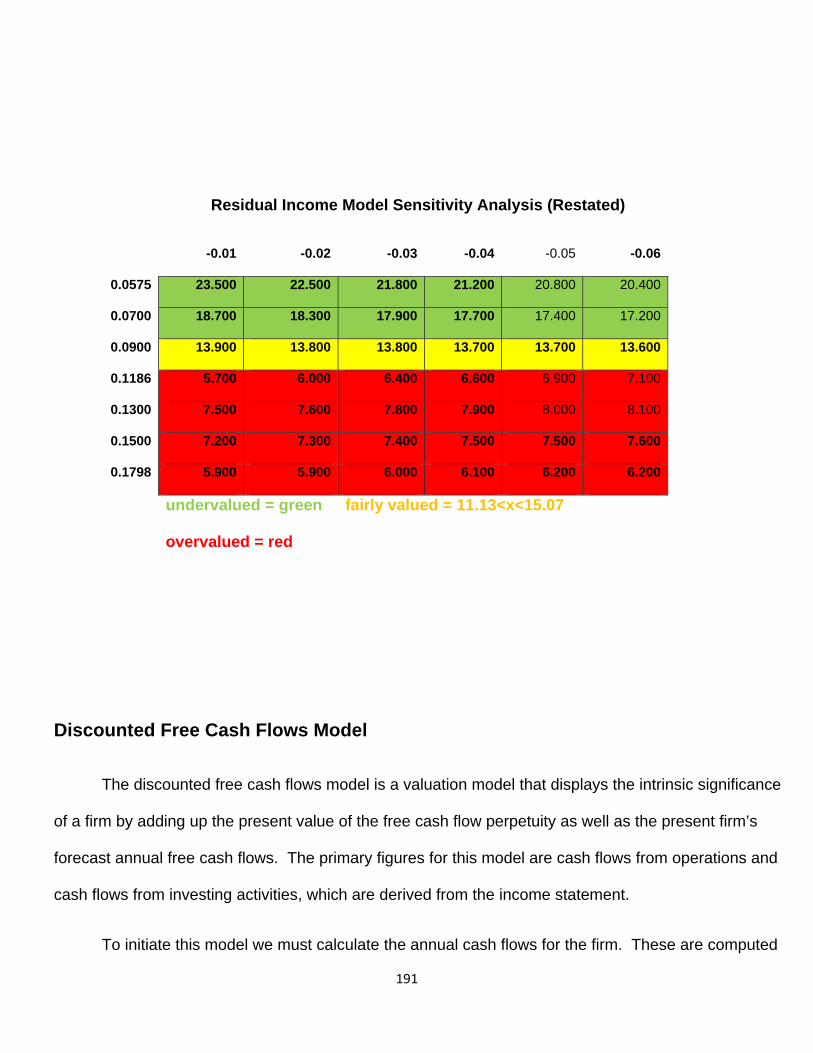

Residual Income Model Restated 190

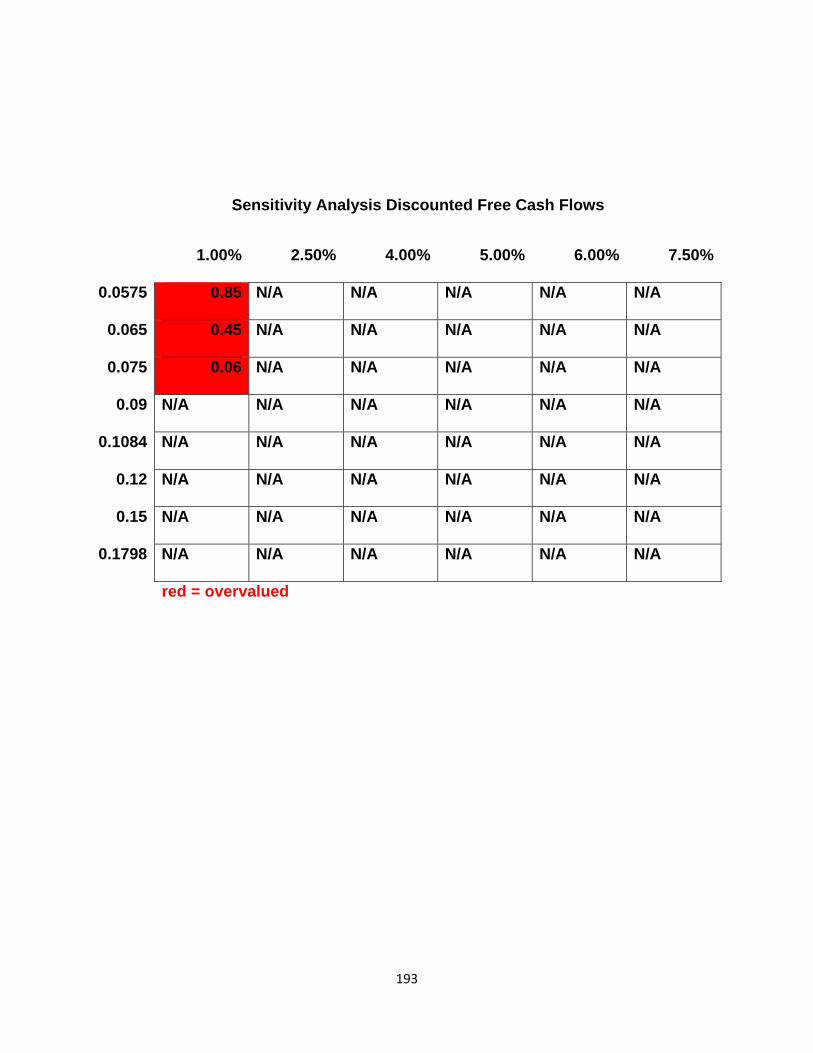

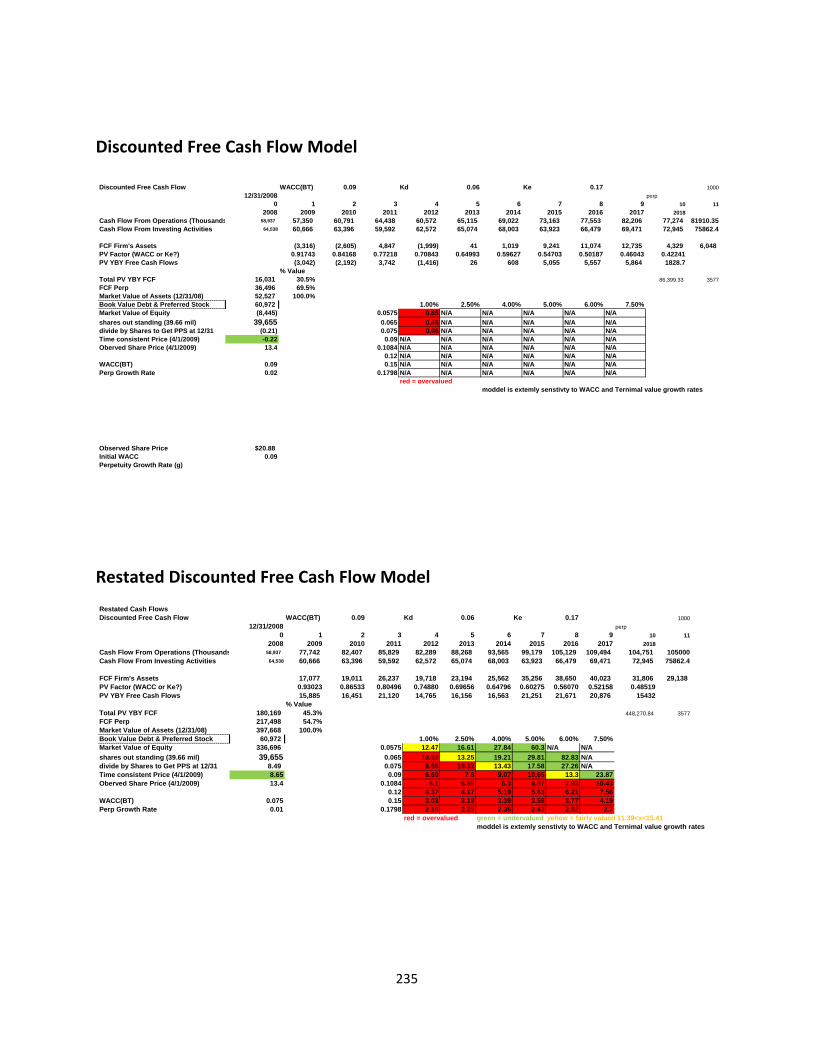

Discounted Free Cash Flows Model 190

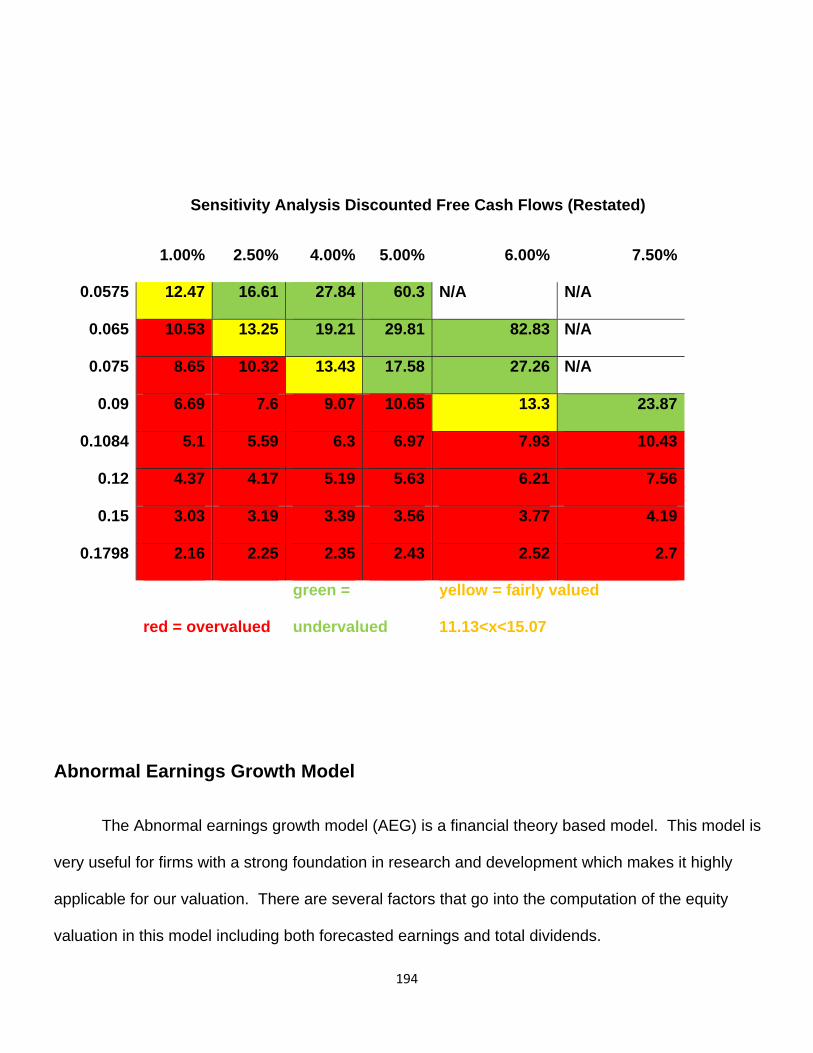

Discounted Free Cash Flows Model Restated 193

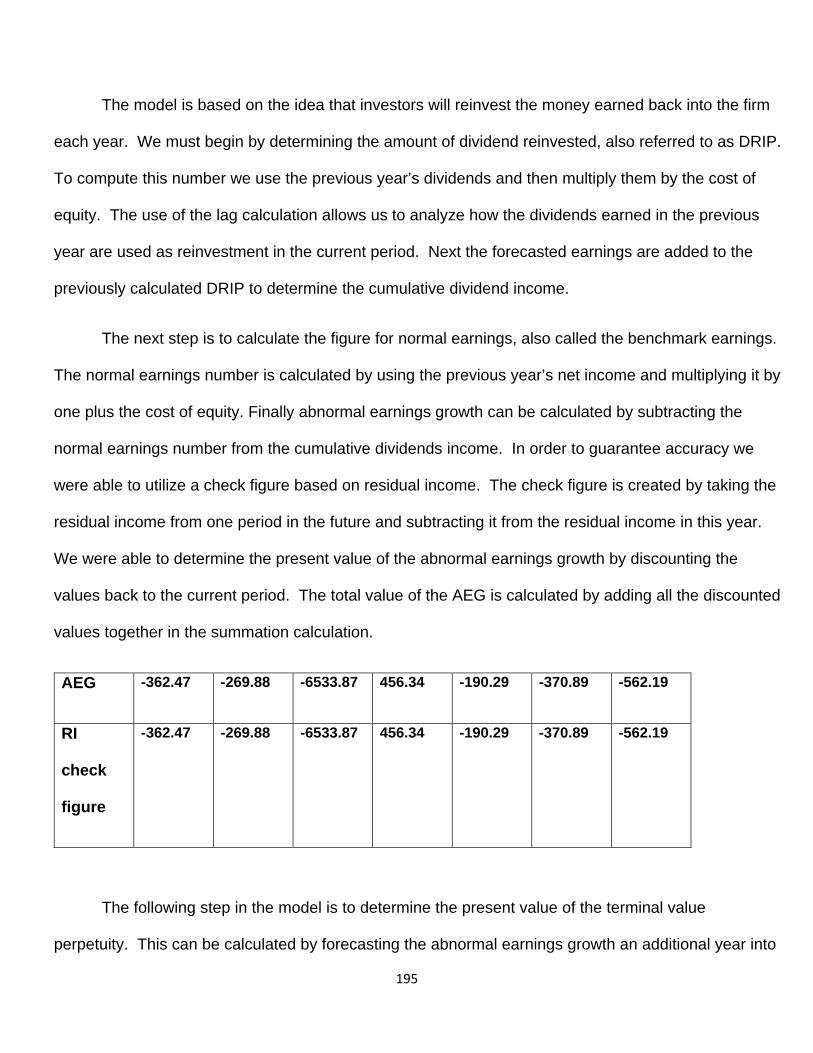

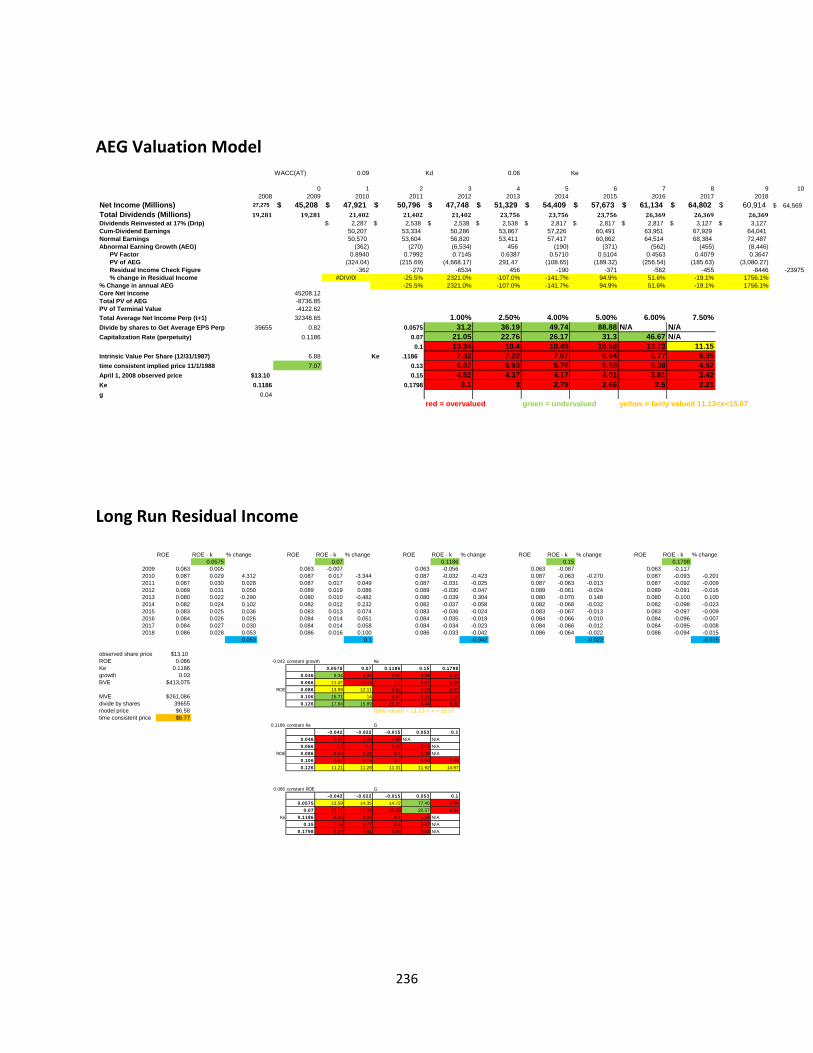

AEG Model 193

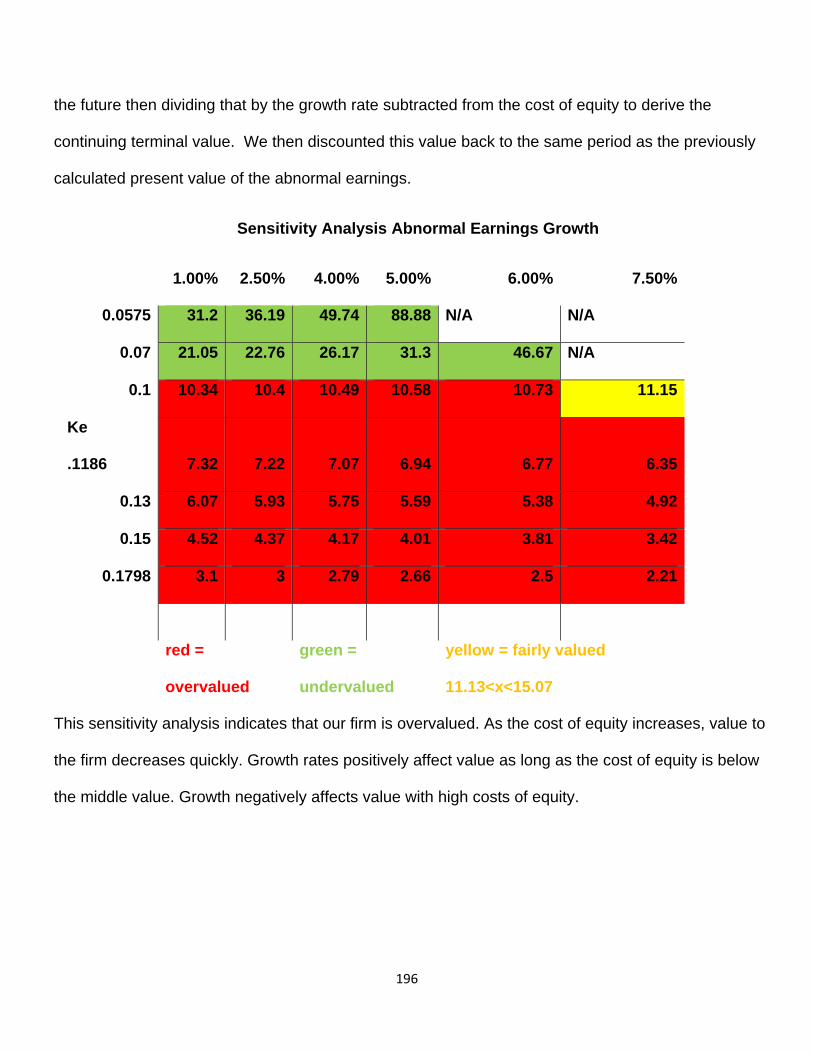

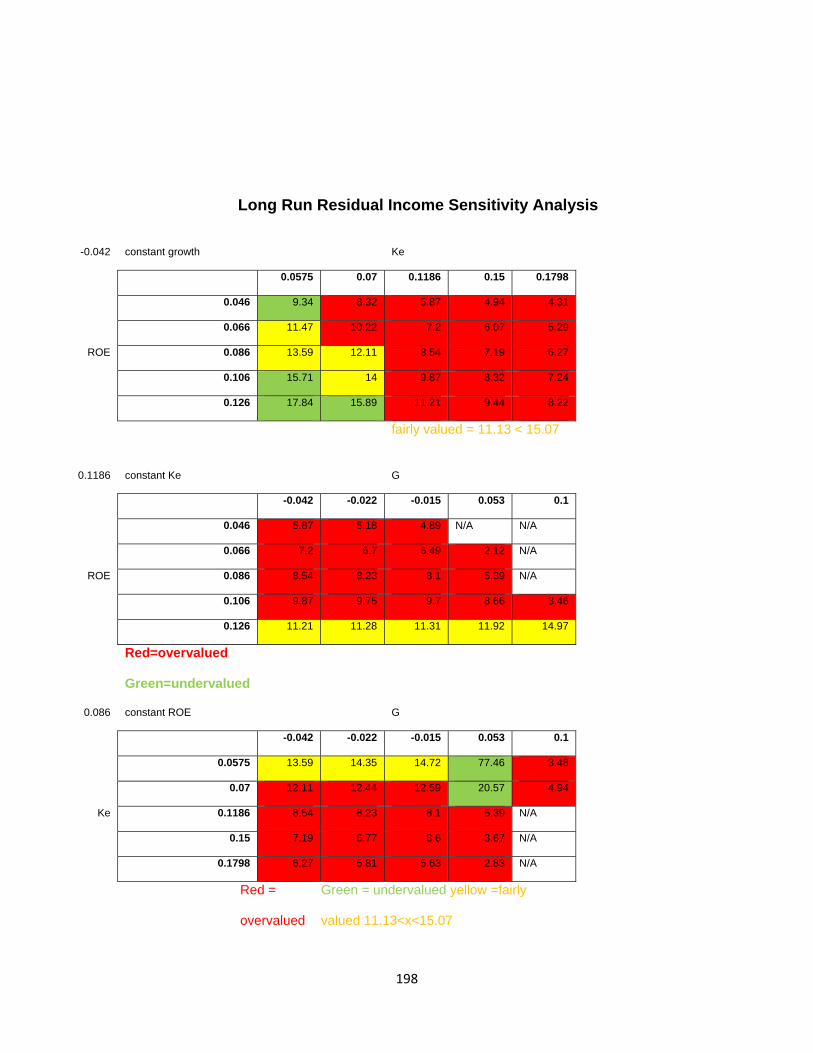

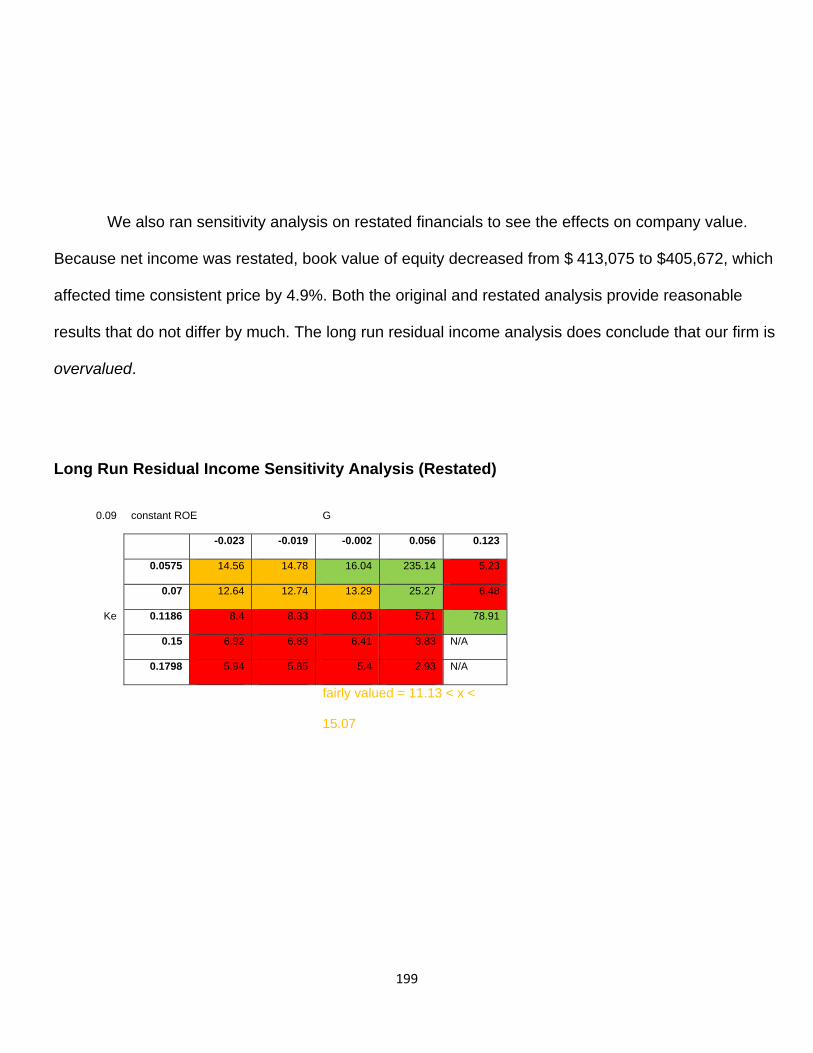

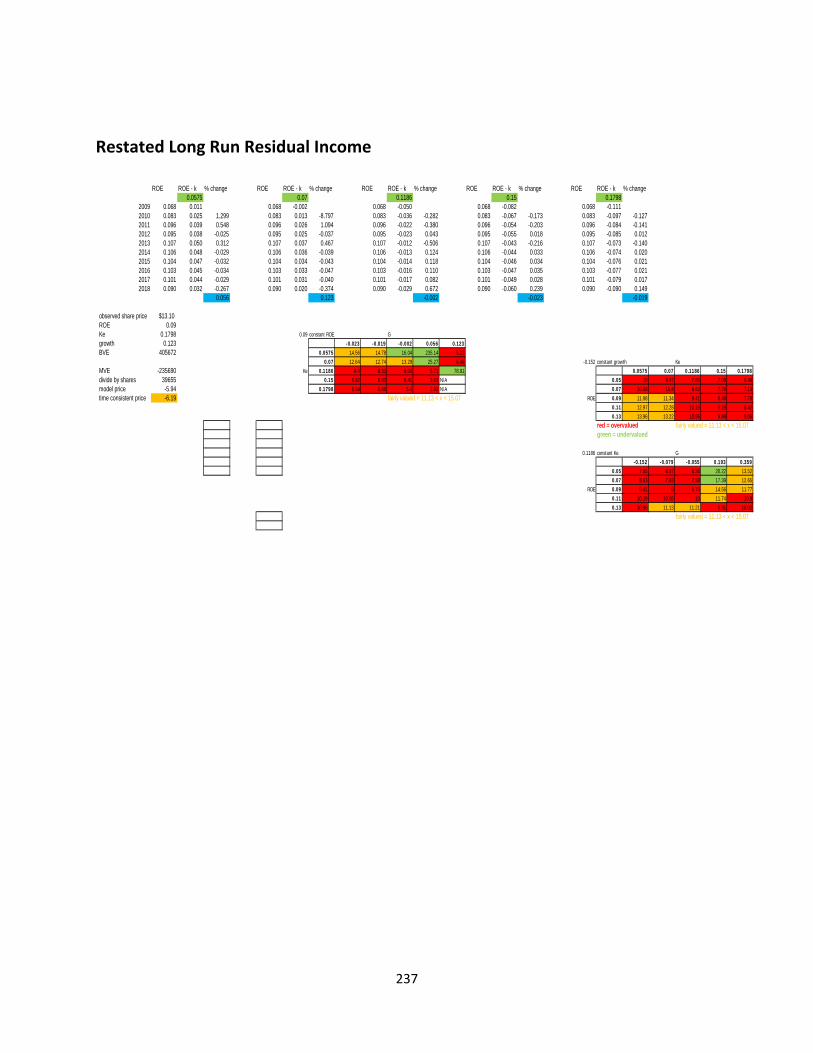

Long Run Residual Income Model 196

Long Run Residual Income Model Restated 198

Analyst Recommendation 199

Appendices 201

References 237

9

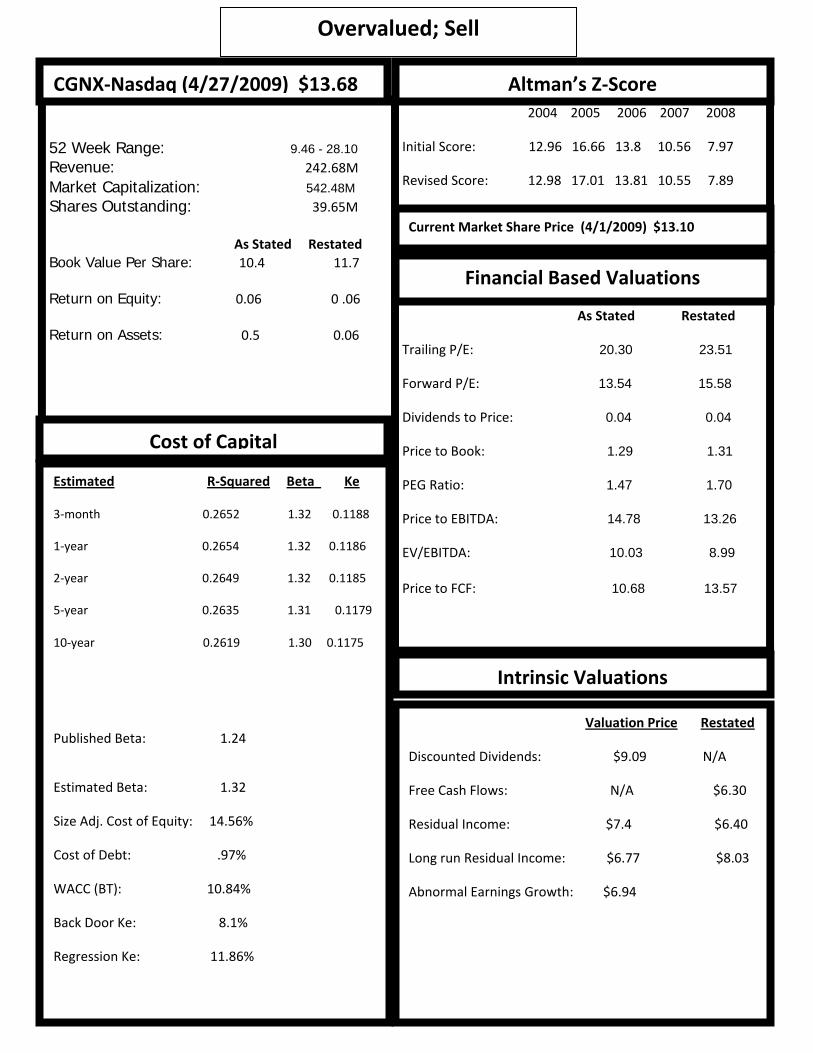

52 Week Range: 9.46 - 28.10 Revenue: 242.68M Market Capitalization: 542.48M Shares Outstanding: 39.65M

As Stated Restated Book Value Per Share: 10.4 11.7 Return on Equity: 0.06 0 .06 Return on Assets: 0.5 0.06

2004 2005 2006 2007 2008

Initial Score: 12.96 16.66 13.8 10.56 7.97

Revised Score: 12.98 17.01 13.81 10.55 7.89

As Stated Restated

Trailing P/E: 20.30 23.51

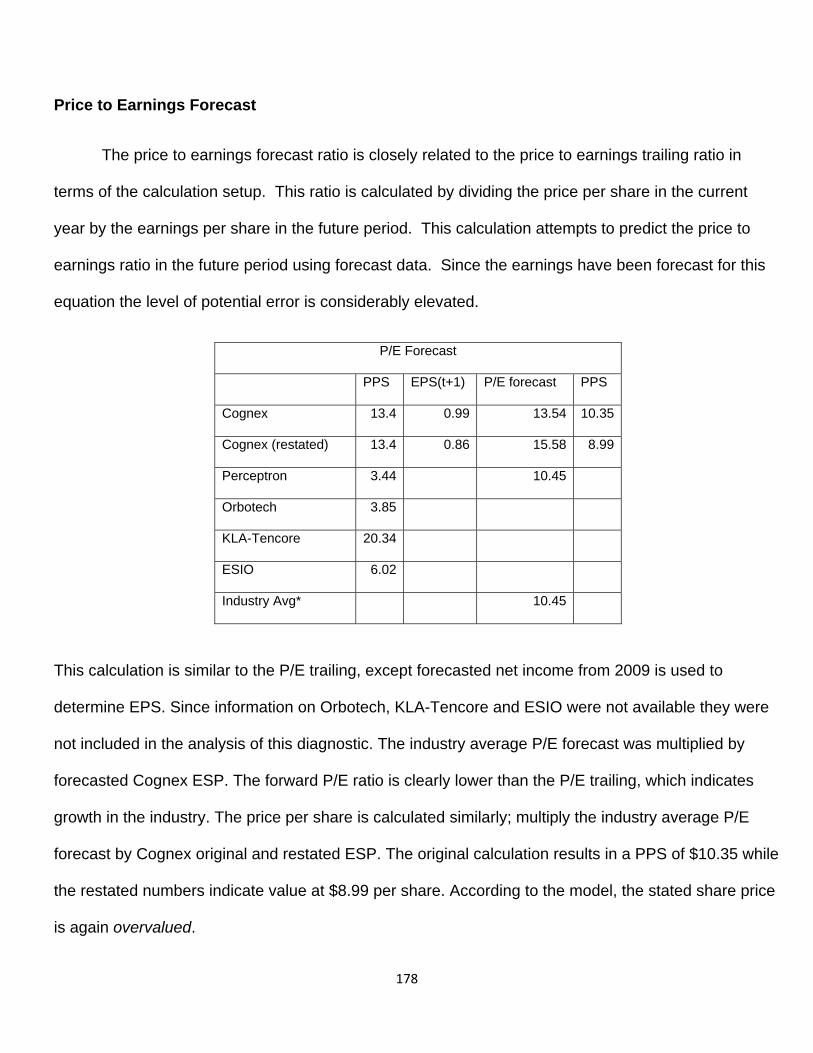

Forward P/E: 13.54 15.58

Dividends to Price: 0.04 0.04

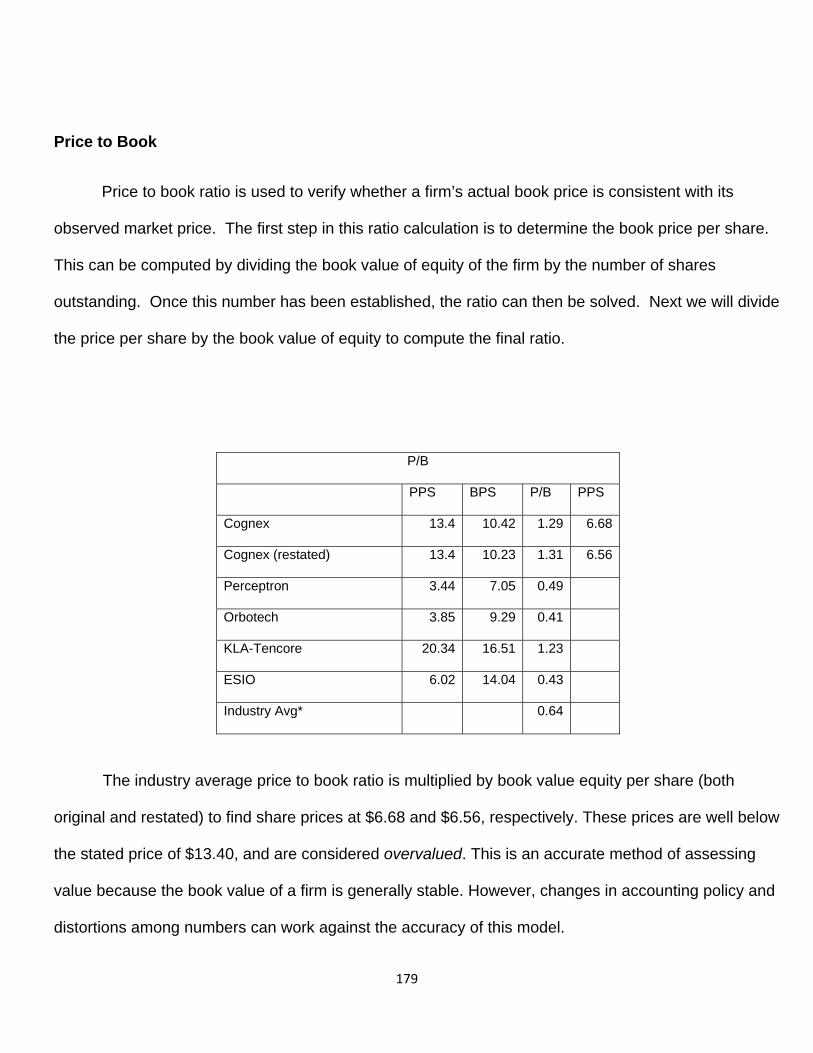

Price to Book: 1.29 1.31

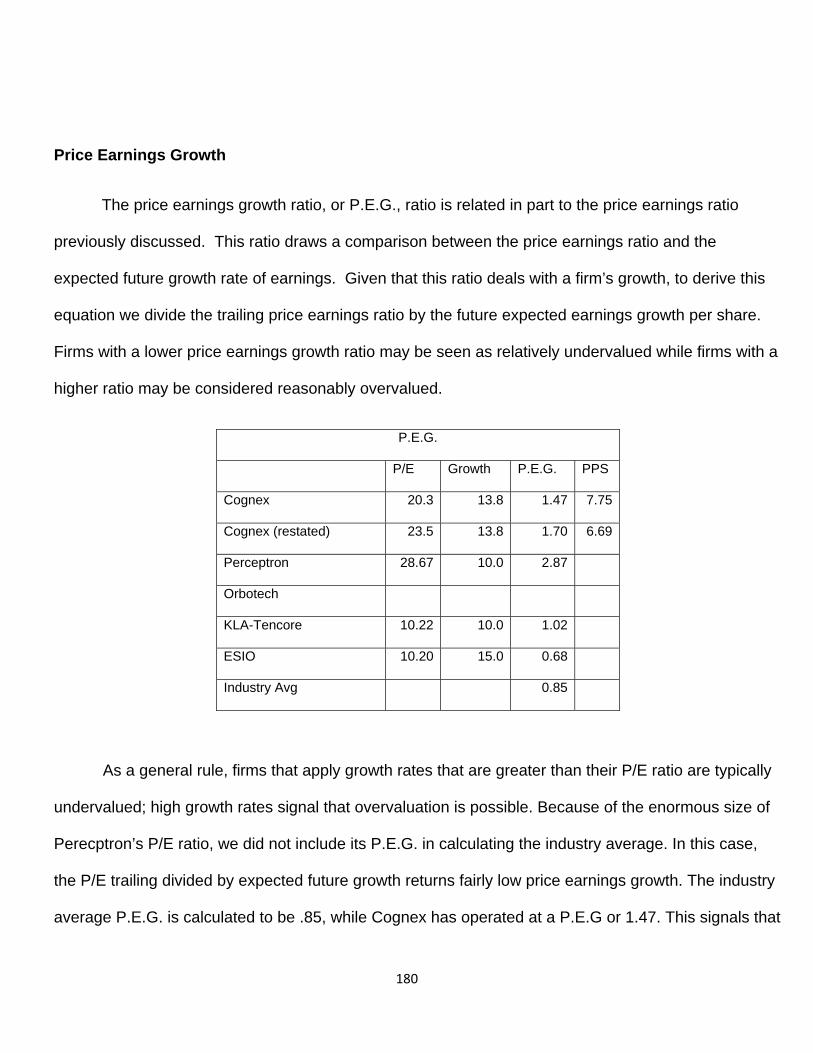

PEG Ratio: 1.47 1.70

Price to EBITDA: 14.78 13.26

EV/EBITDA: 10.03 8.99 Price to FCF: 10.68 13.57

CGNX‐Nasdaq (4/27/2009) $13.68 Altman’s Z‐Score

Current Market Share Price (4/1/2009) $13.10

Financial Based Valuations

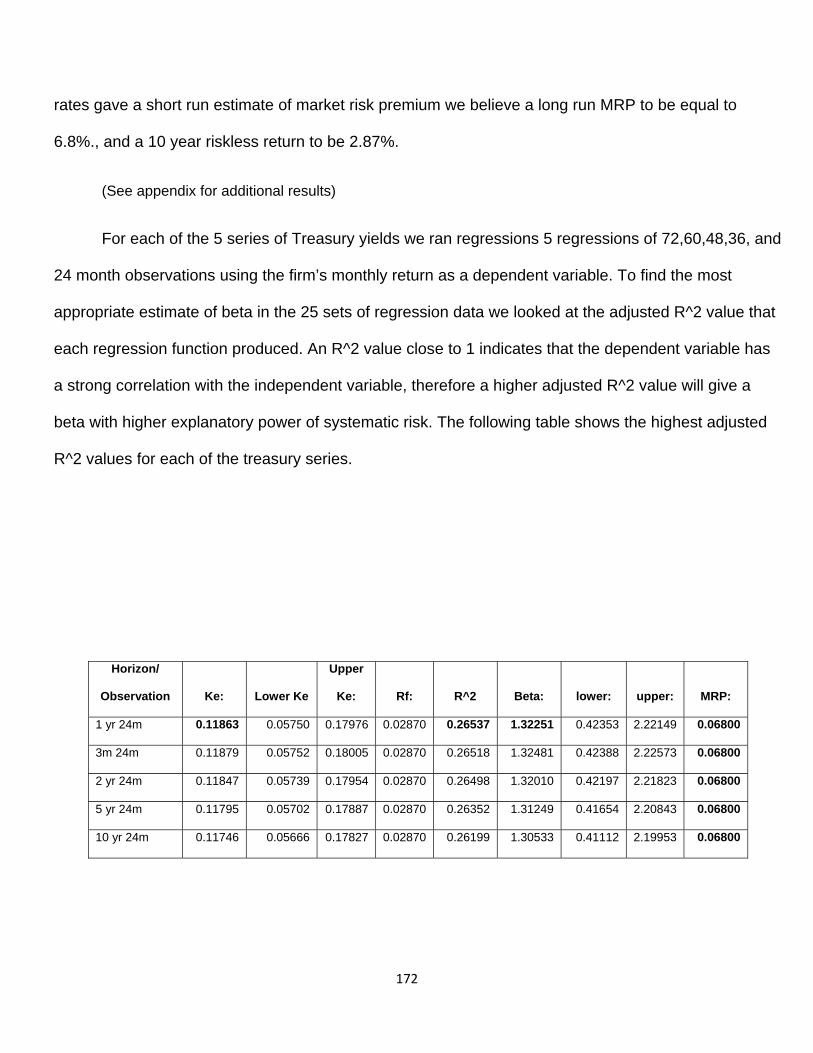

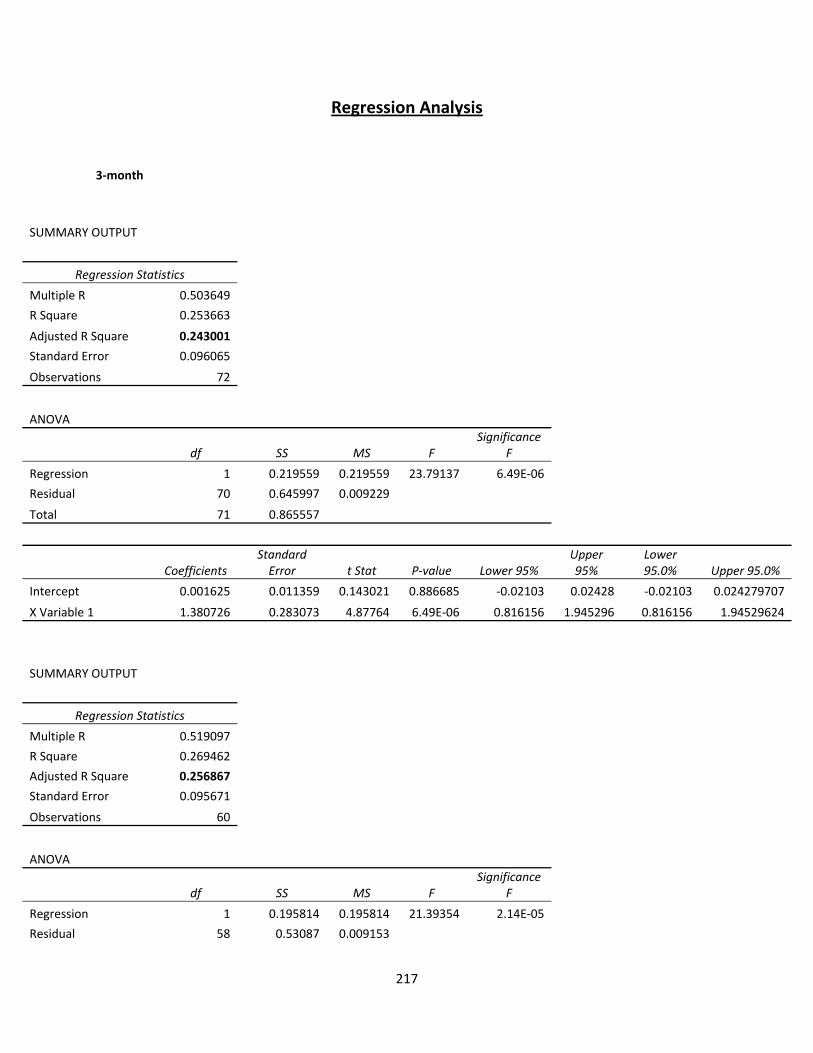

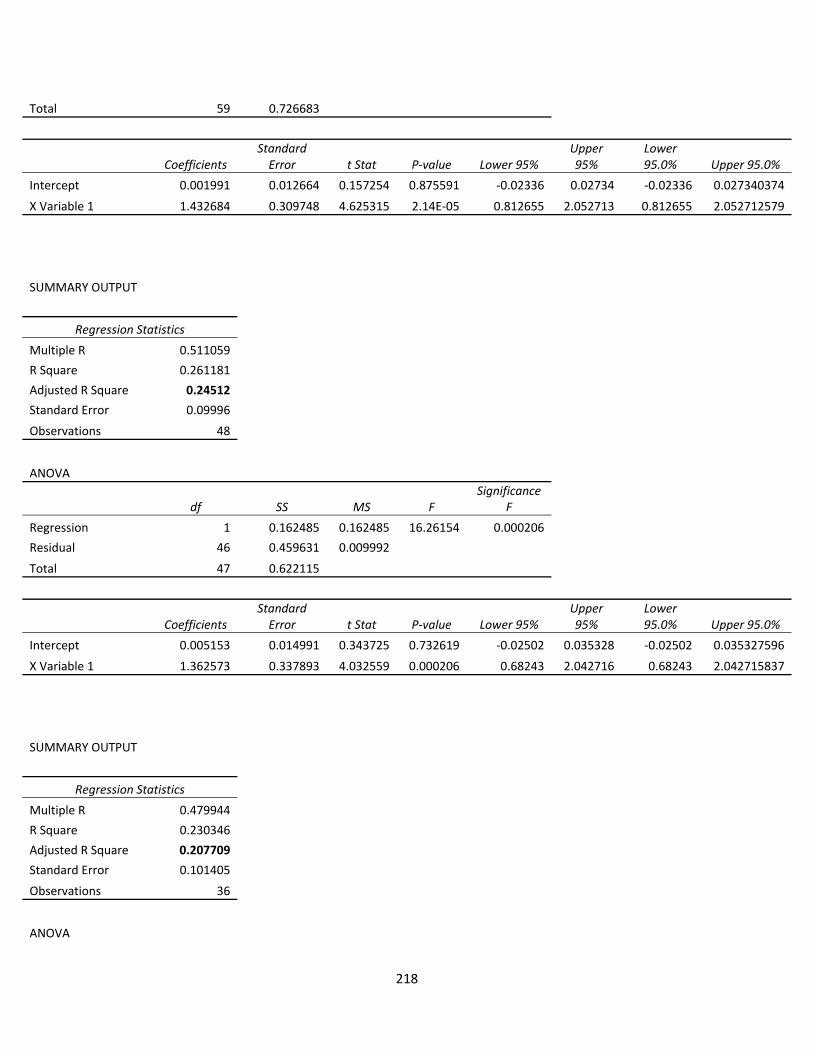

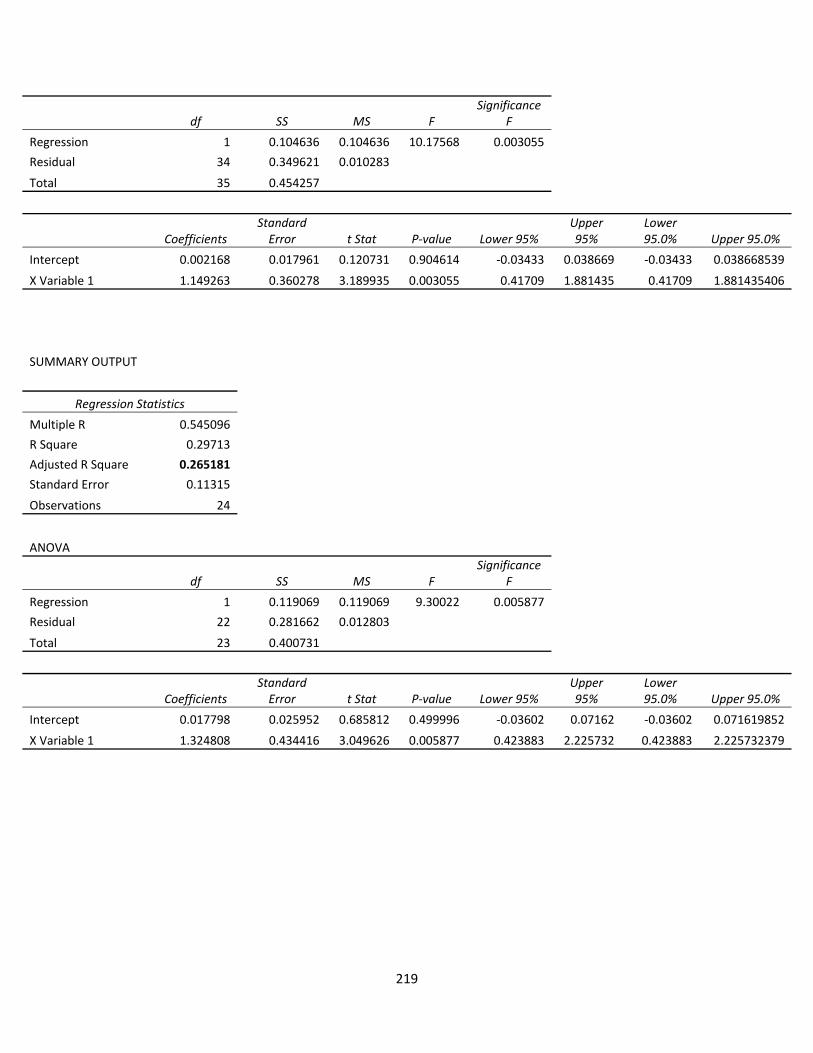

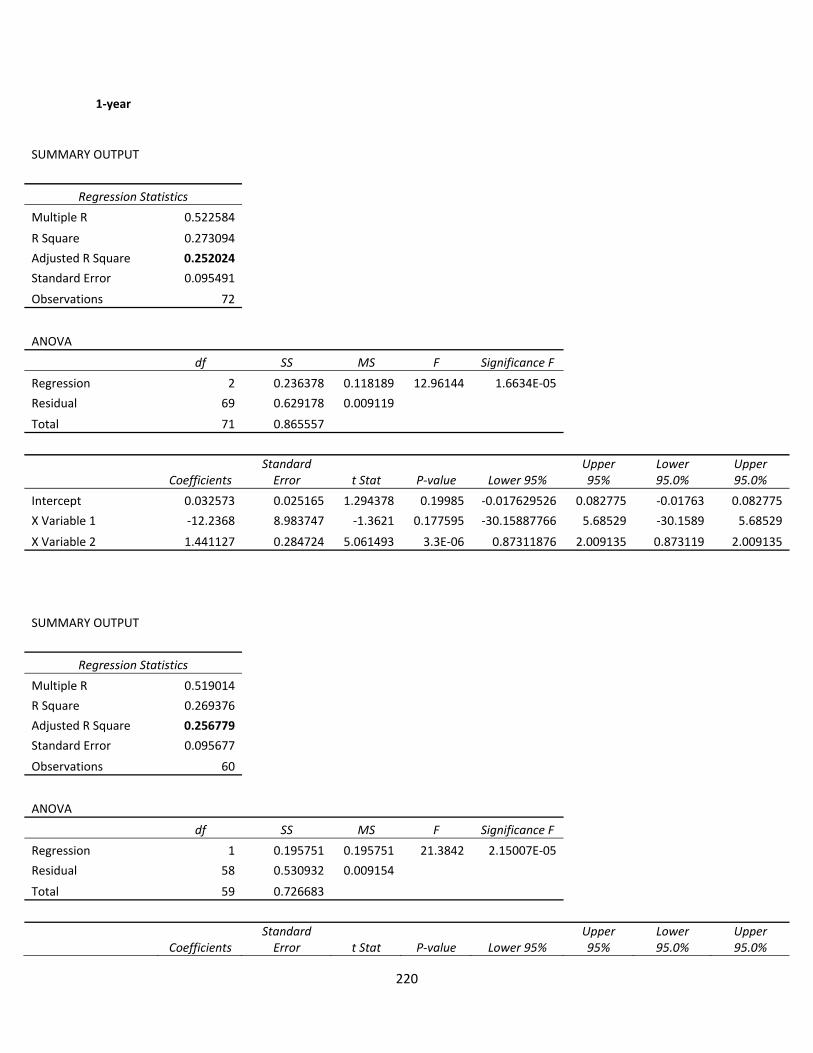

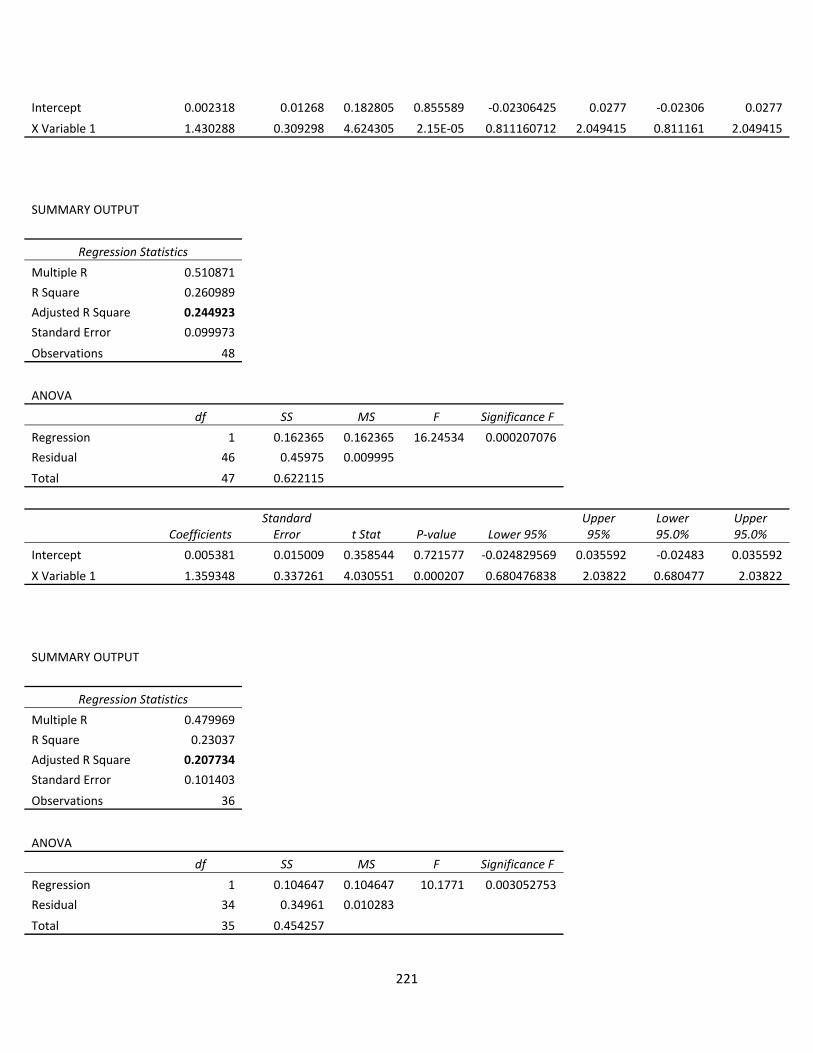

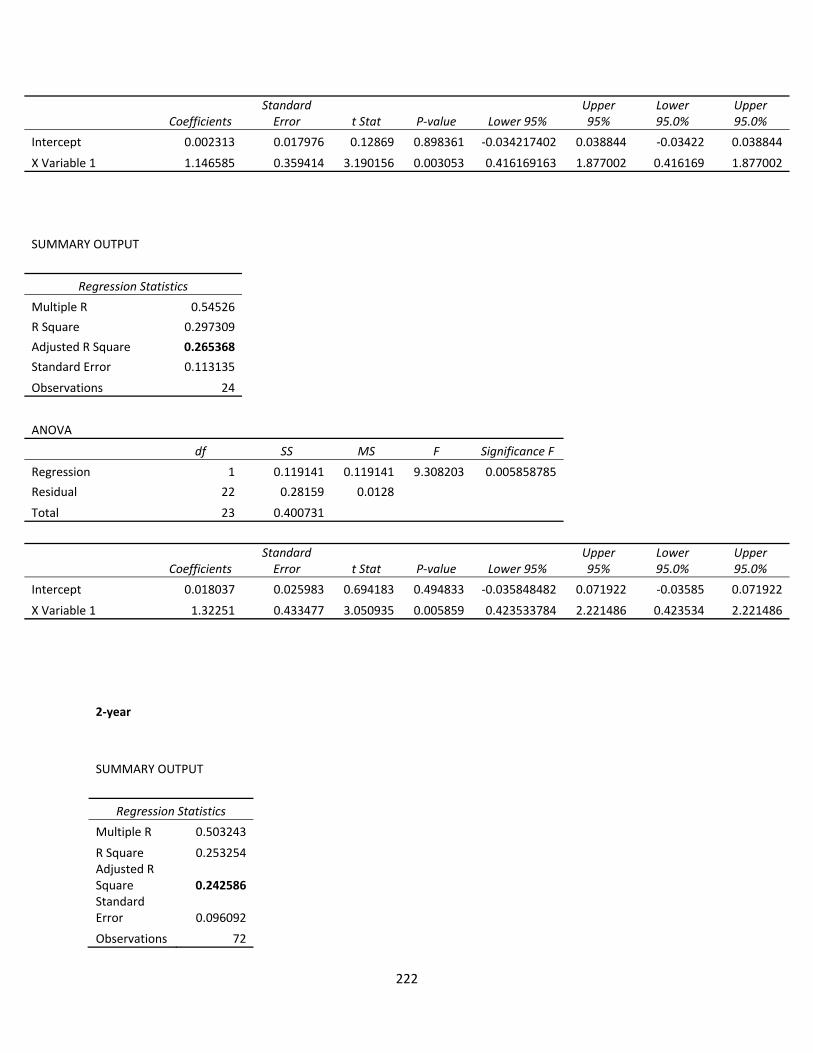

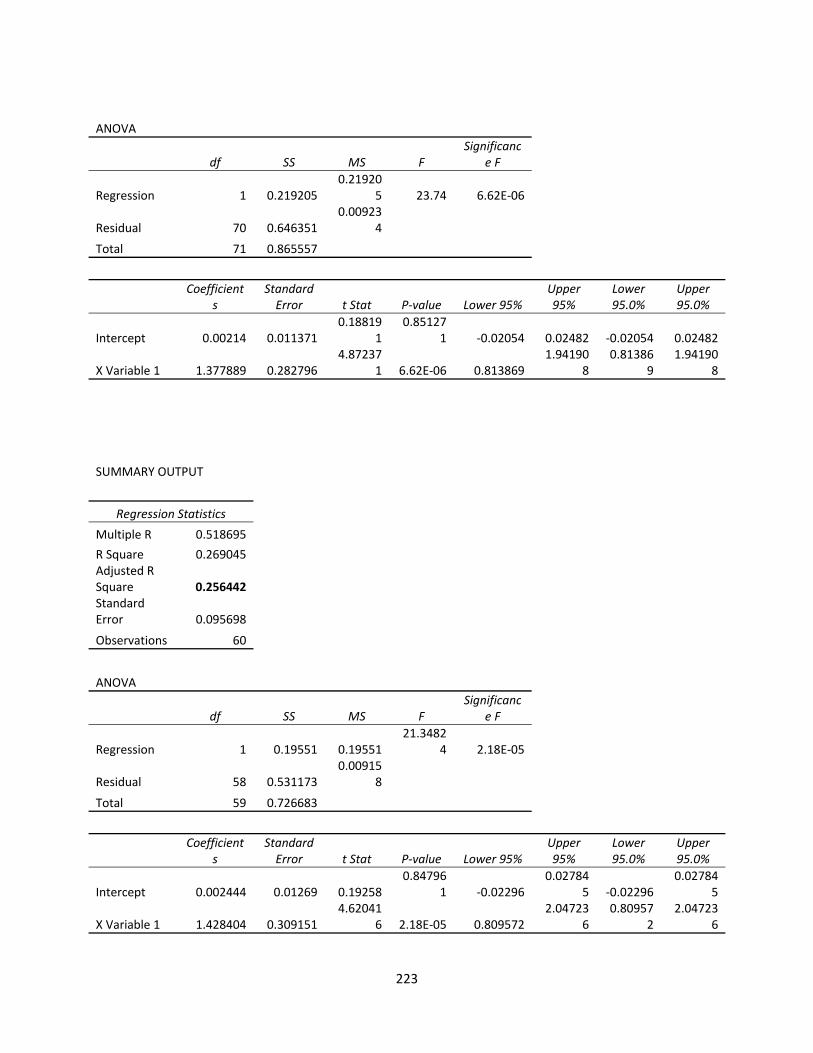

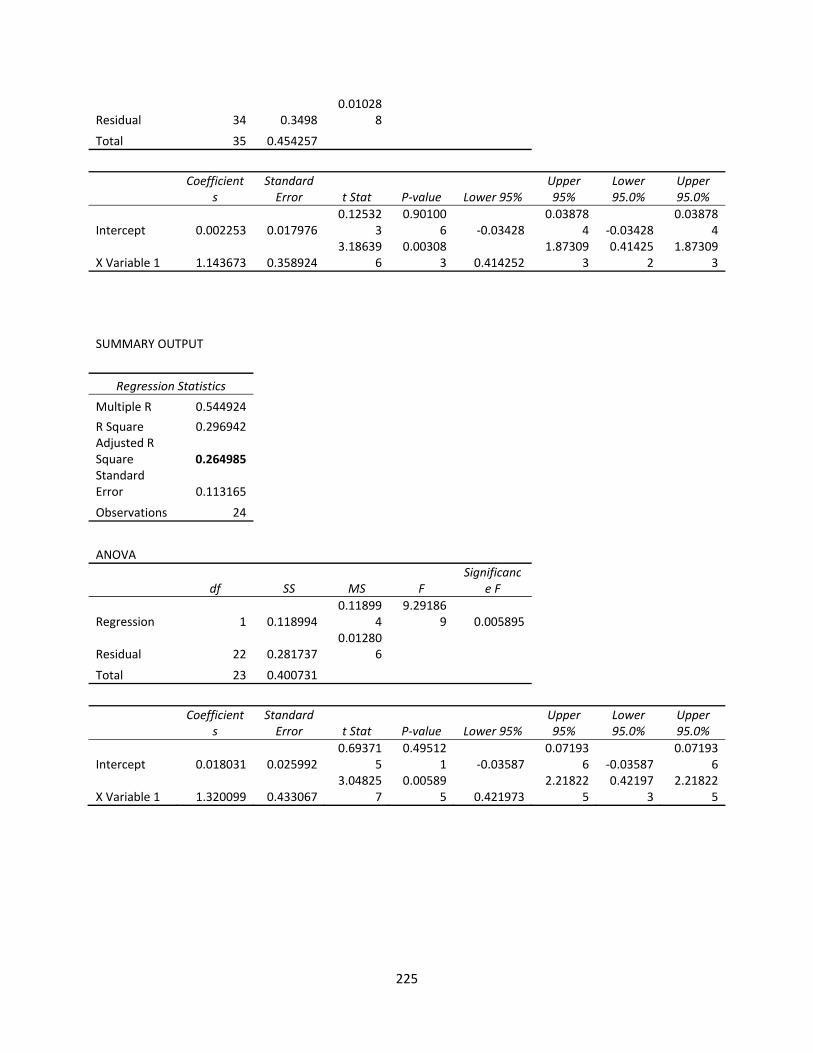

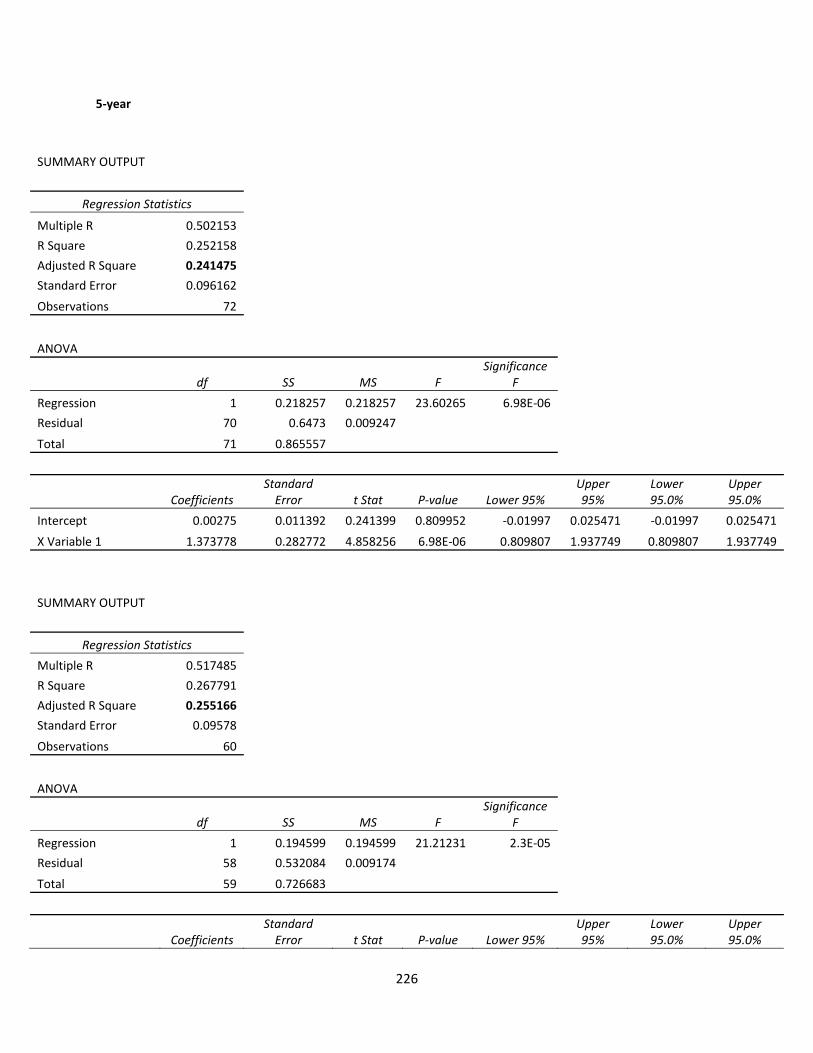

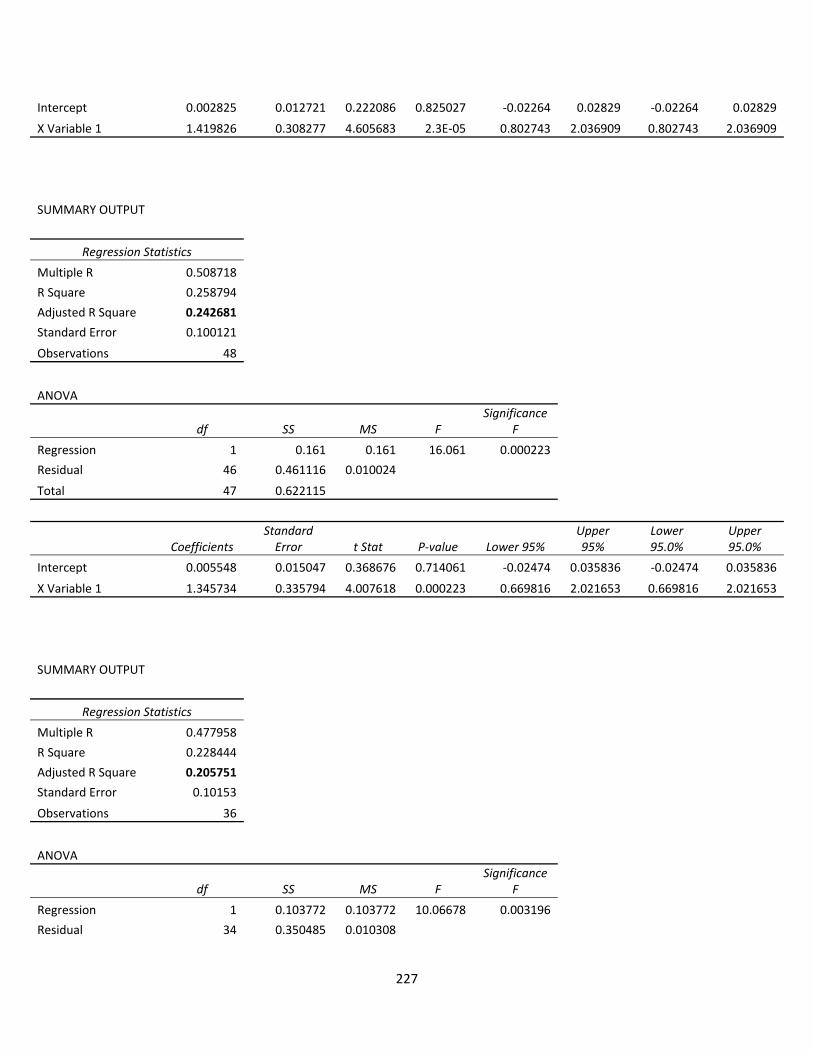

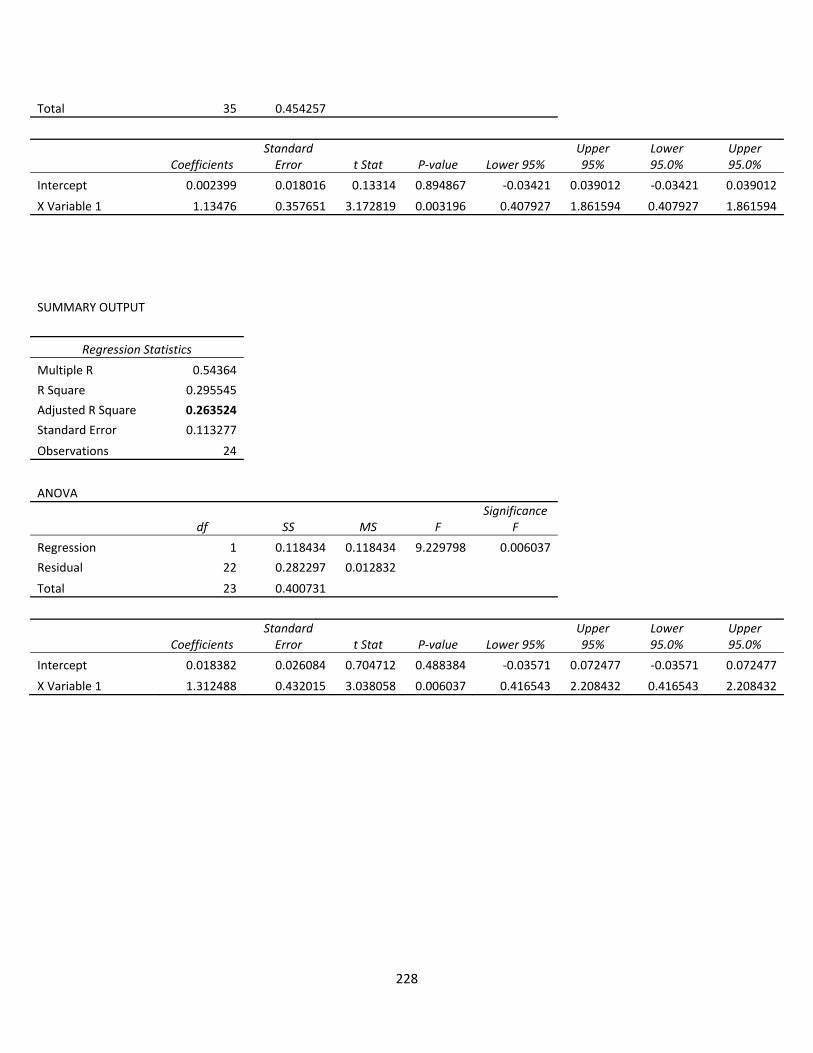

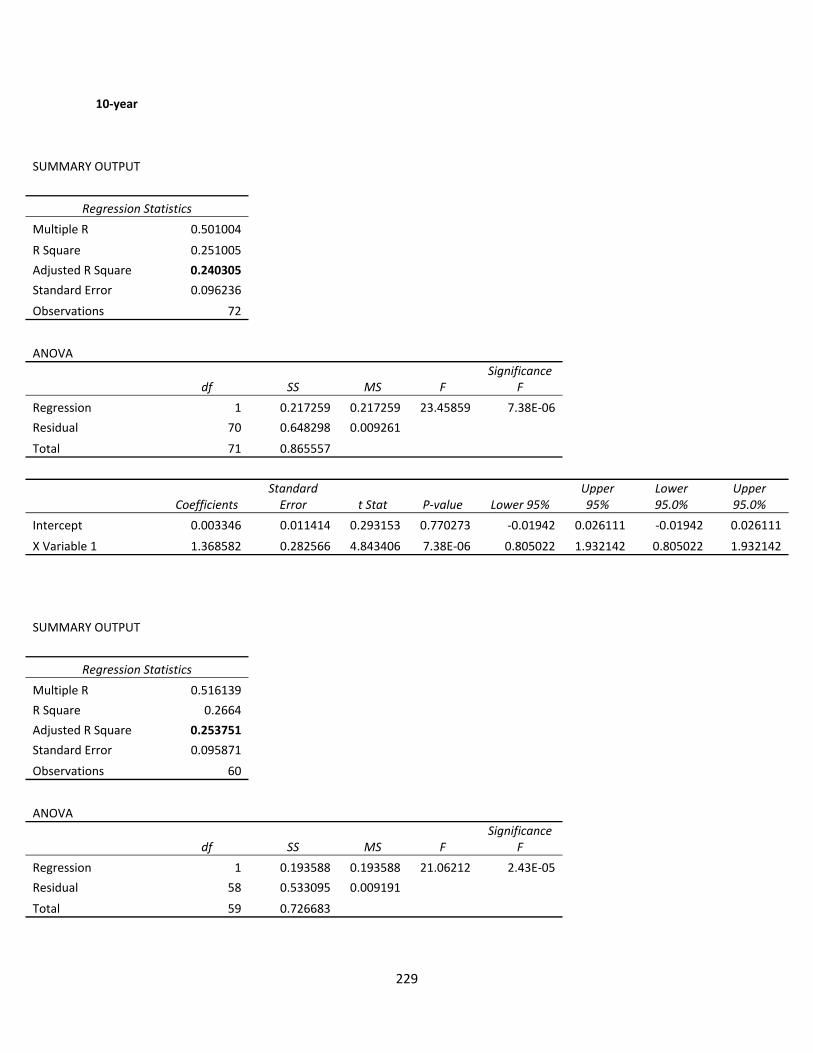

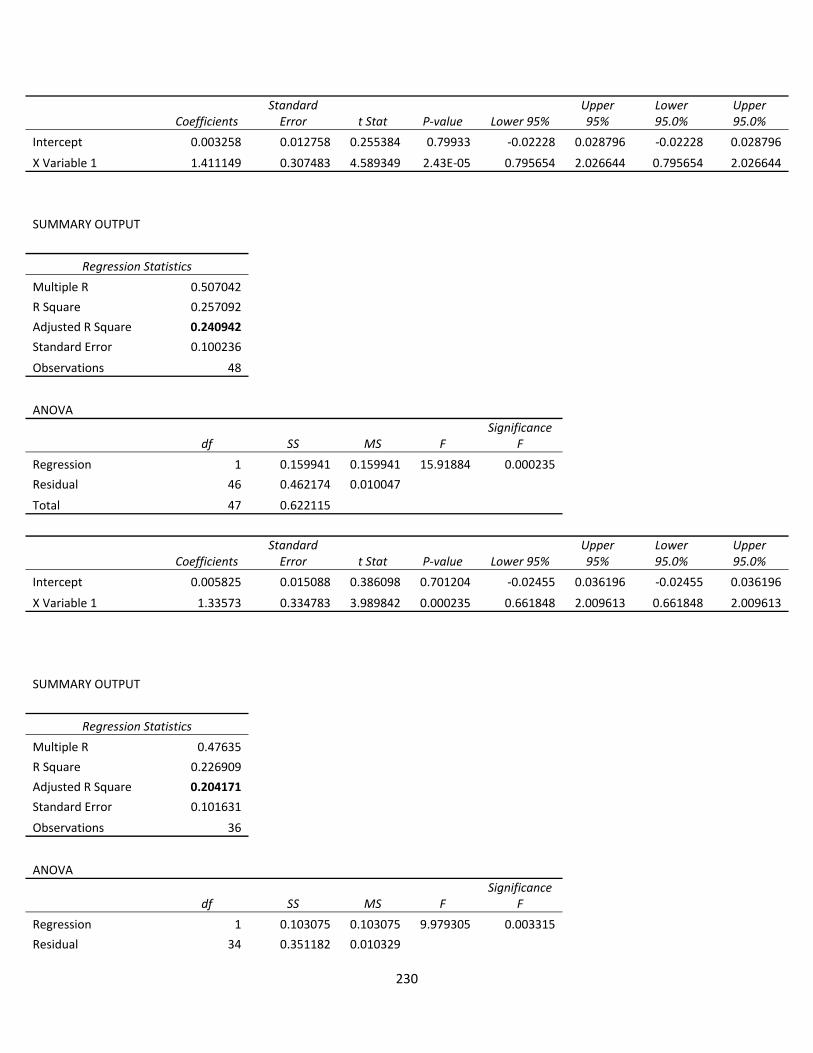

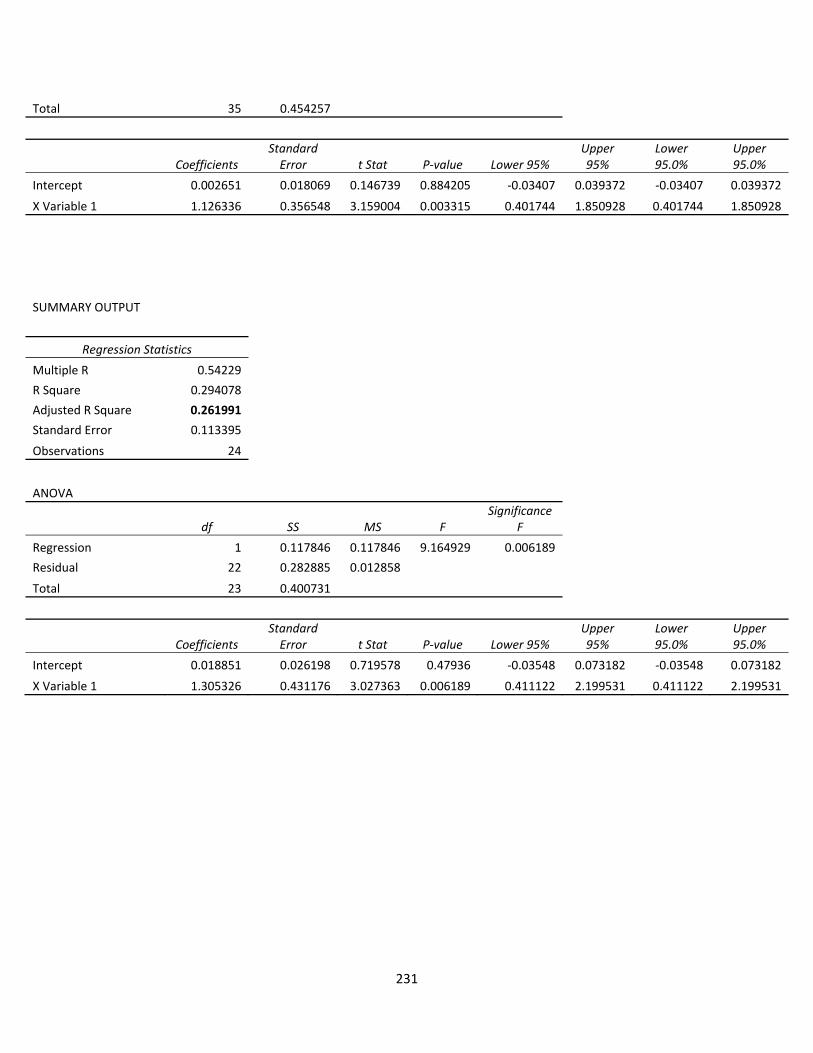

Estimated R‐Squared Beta Ke

3‐month 0.2652 1.32 0.1188

1‐year 0.2654 1.32 0.1186

2‐year 0.2649 1.32 0.1185

5‐year 0.2635 1.31 0.1179

10‐year 0.2619 1.30 0.1175

Published Beta: 1.24

Estimated Beta: 1.32

Size Adj. Cost of Equity: 14.56%

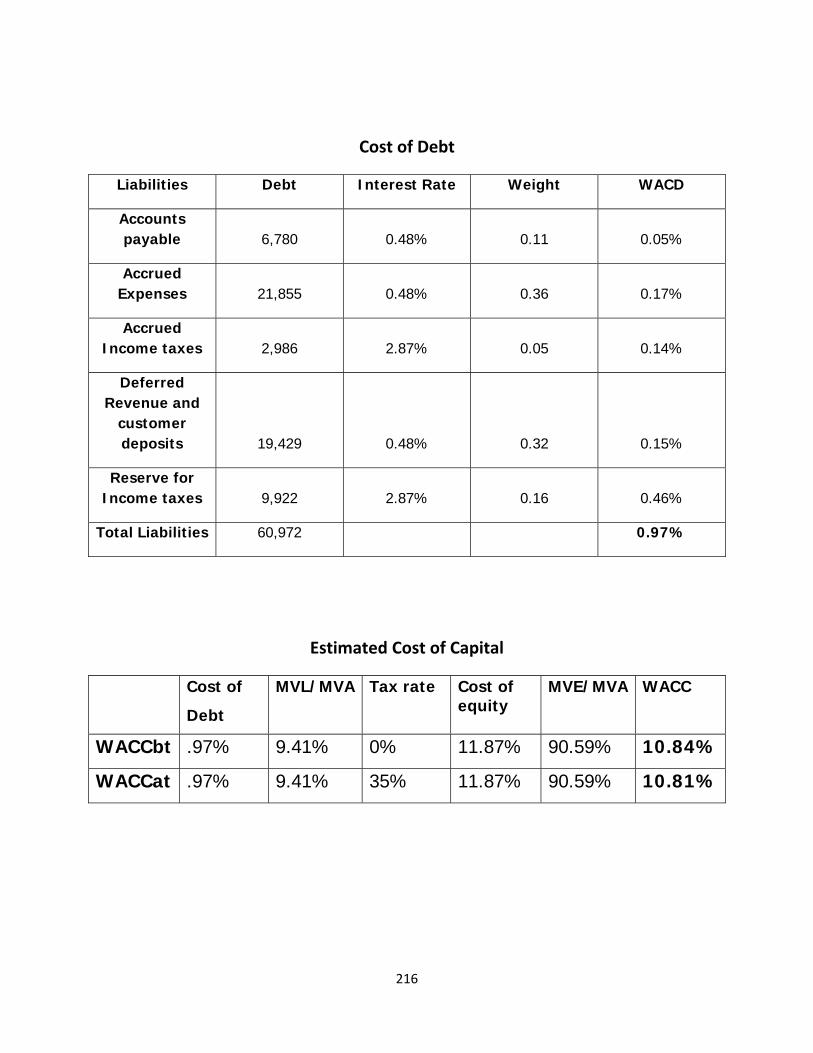

Cost of Debt: .97%

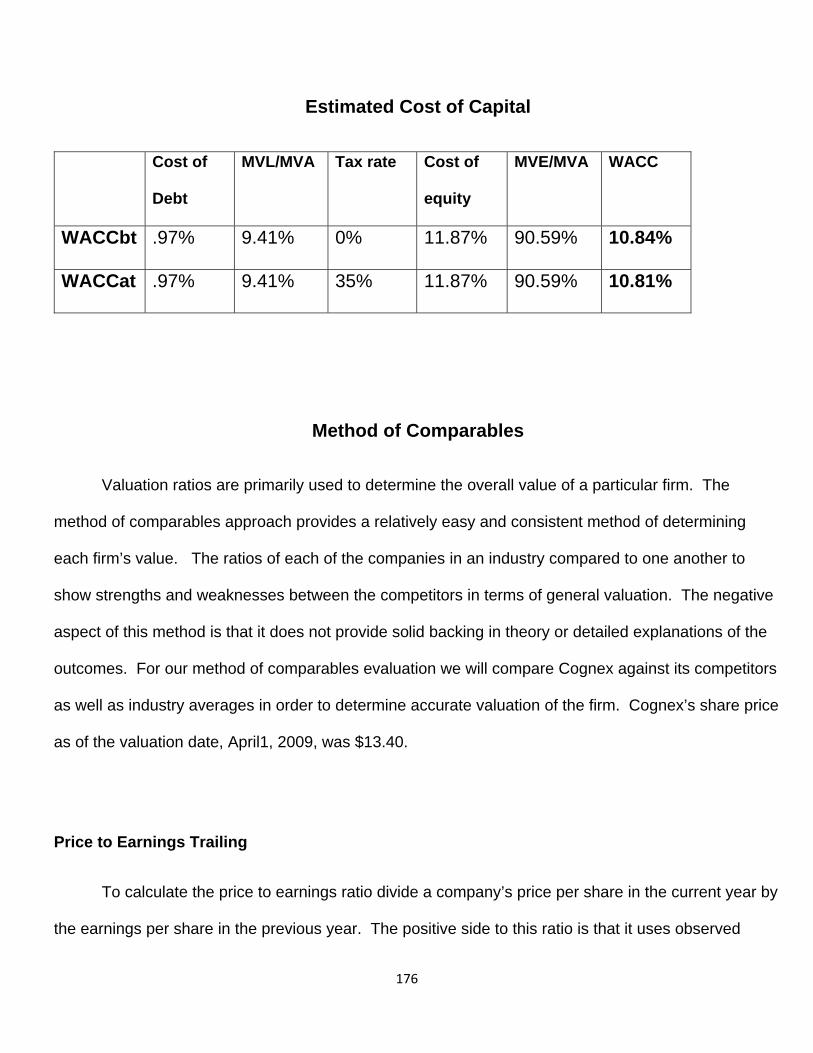

WACC (BT): 10.84%

Back Door Ke: 8.1%

Regression Ke: 11.86%

Cost of Capital

Intrinsic Valuations

Valuation Price Restated

Discounted Dividends: $9.09 N/A

Free Cash Flows: N/A $6.30

Residual Income: $7.4 $6.40

Long run Residual Income: $6.77 $8.03

Abnormal Earnings Growth: $6.94

Overvalued; Sell

10

11

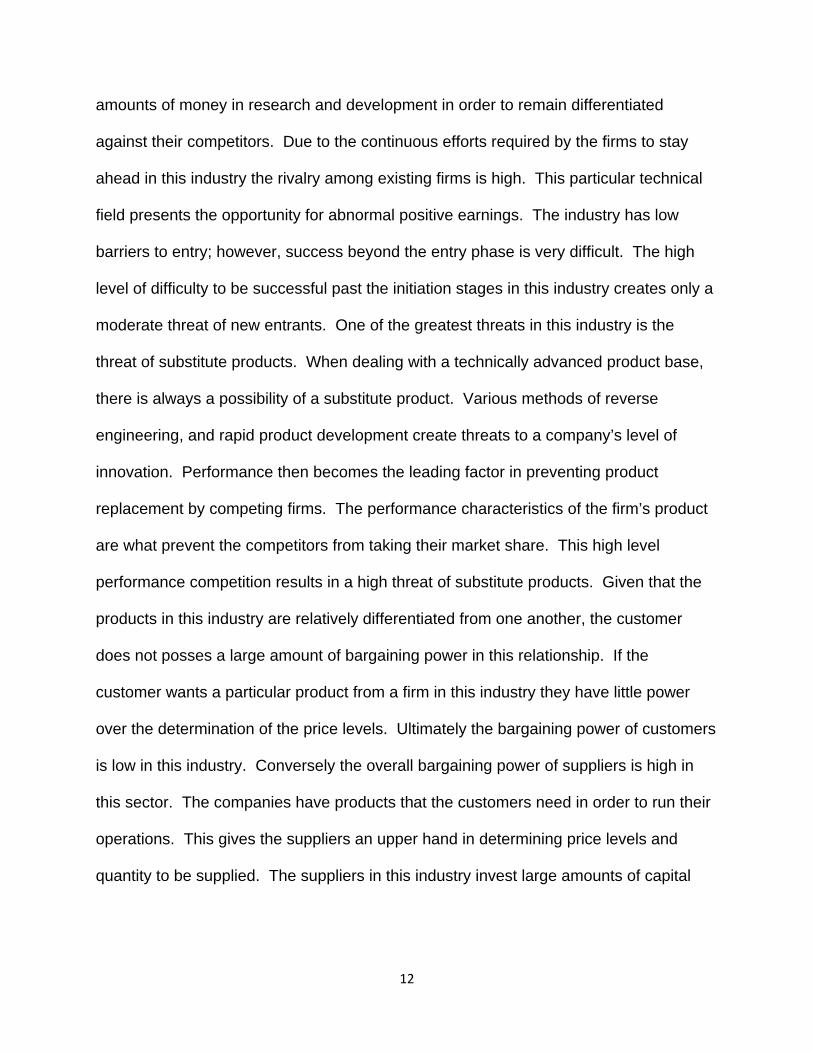

Executive Summary

Industry Analysis

Created in 1981 Cognex is the largest provider in machine vision software, vision

systems, vision sensors, and surface inspection systems utilized in manufacturing

automation. The company is headquartered in Natick, Massachusetts with offices in

twenty countries including North America, Japan, Latin America, Asia and Europe.

Cognex has the largest global presence of any firm in the industry. In the machine

vision industry Cognex competes directly with KLA-Tencor, Perceptron, Orbotech, and

Electro Scientific Industries Inc (ESIO). Each of the firms are fairly different in terms of

geographic location, primary business focus, and competitive advantages.

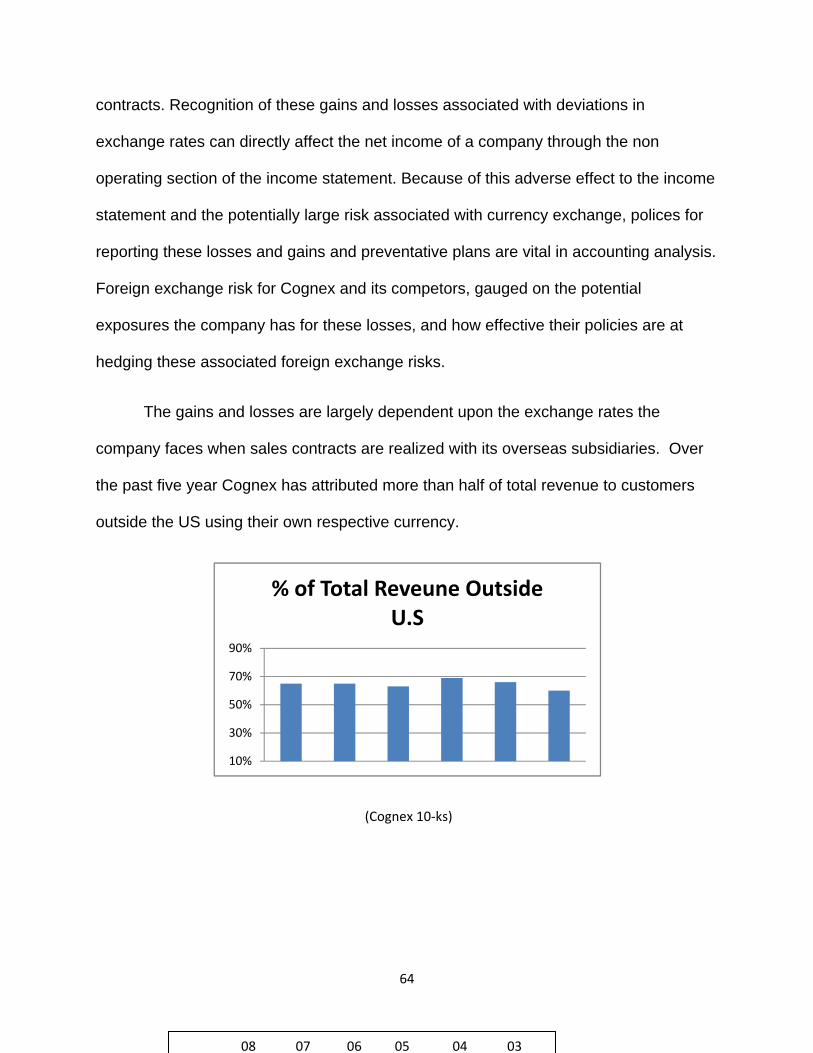

Since the firms in this industry are dealing with a global client base, they rely

heavily on product differentiation in order to stay ahead of their competitors. The only

way to stay ahead of the curve in the industry is to be at the forefront of technical

innovation. Dealing with a highly technical product, the firms must all invest large

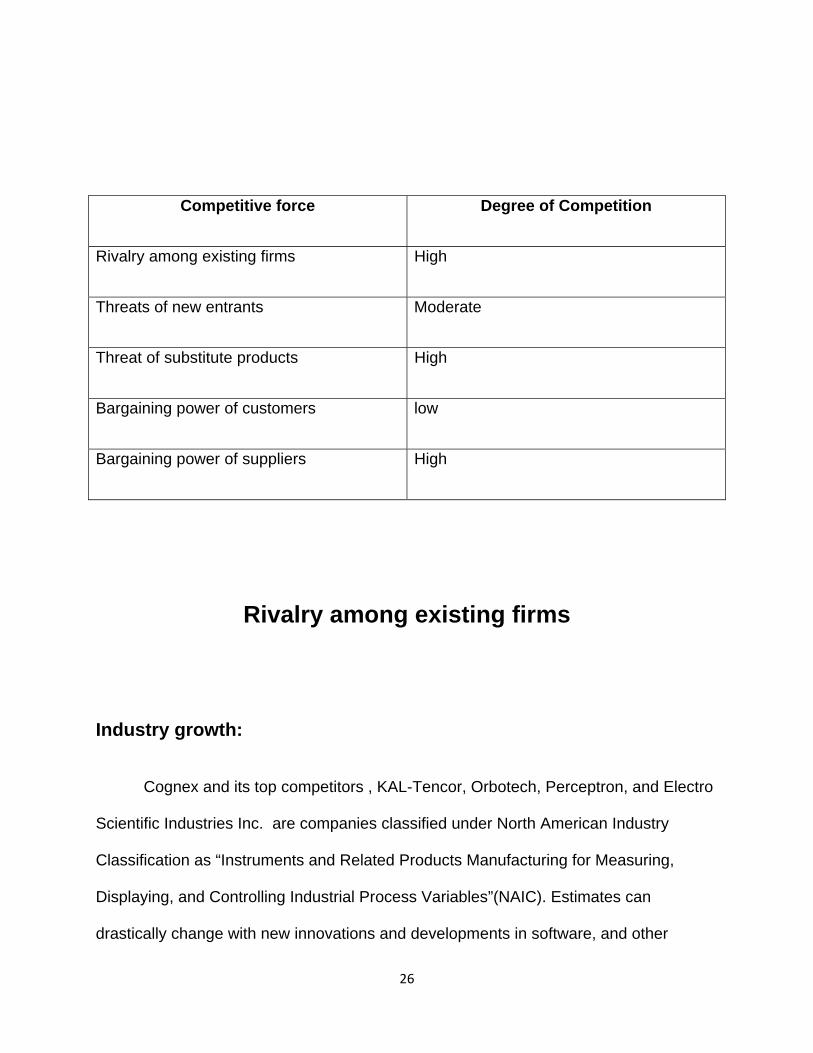

Competitive force Degree of Competition

Rivalry among existing firms High

Threats of new entrants Moderate

Threat of substitute products High

Bargaining power of customers Low

Bargaining power of suppliers High

12

amounts of money in research and development in order to remain differentiated

against their competitors. Due to the continuous efforts required by the firms to stay

ahead in this industry the rivalry among existing firms is high. This particular technical

field presents the opportunity for abnormal positive earnings. The industry has low

barriers to entry; however, success beyond the entry phase is very difficult. The high

level of difficulty to be successful past the initiation stages in this industry creates only a

moderate threat of new entrants. One of the greatest threats in this industry is the

threat of substitute products. When dealing with a technically advanced product base,

there is always a possibility of a substitute product. Various methods of reverse

engineering, and rapid product development create threats to a company’s level of

innovation. Performance then becomes the leading factor in preventing product

replacement by competing firms. The performance characteristics of the firm’s product

are what prevent the competitors from taking their market share. This high level

performance competition results in a high threat of substitute products. Given that the

products in this industry are relatively differentiated from one another, the customer

does not posses a large amount of bargaining power in this relationship. If the

customer wants a particular product from a firm in this industry they have little power

over the determination of the price levels. Ultimately the bargaining power of customers

is low in this industry. Conversely the overall bargaining power of suppliers is high in

this sector. The companies have products that the customers need in order to run their

operations. This gives the suppliers an upper hand in determining price levels and

quantity to be supplied. The suppliers in this industry invest large amounts of capital

13

into research and development, and for this reason they have a vast amount of control

over the bargaining power.

Accounting Analysis

To get a true picture of a firm and its operations, it is necessary to study its

financial records and disclosure policies. GAAP requires a minimum level of disclosure

for all firms, which aims to prevent misleading the public. Although this requires

companies to state details about their operations, it leaves room for managers to over or

understate specific line items in an attempt to make the company look more profitable to

investors. A firm with detailed disclosure within their 10-K will look trustworthy and

credible in its operations. However, firms providing only a minimum level of disclosure

present concerns for those wanting to invest. It is important to analyze details within the

accounting disclosure and identify “red flags” if necessary.

The first step in accounting analysis is to identify key success factors. Some key

success factors for Cognex and its industry are research and development, product

differentiation, superior quality, global distribution and value creation for the customer.

To properly value the firm, these key success factors must be linked to the key

accounting policies. The key accounting policies that most directly affect Cognex’s key

success factors include research and development, goodwill and foreign currency risk.

The amount of detail in the disclosure of the mentioned key success factors will either

support the financial statements or expose distortions.

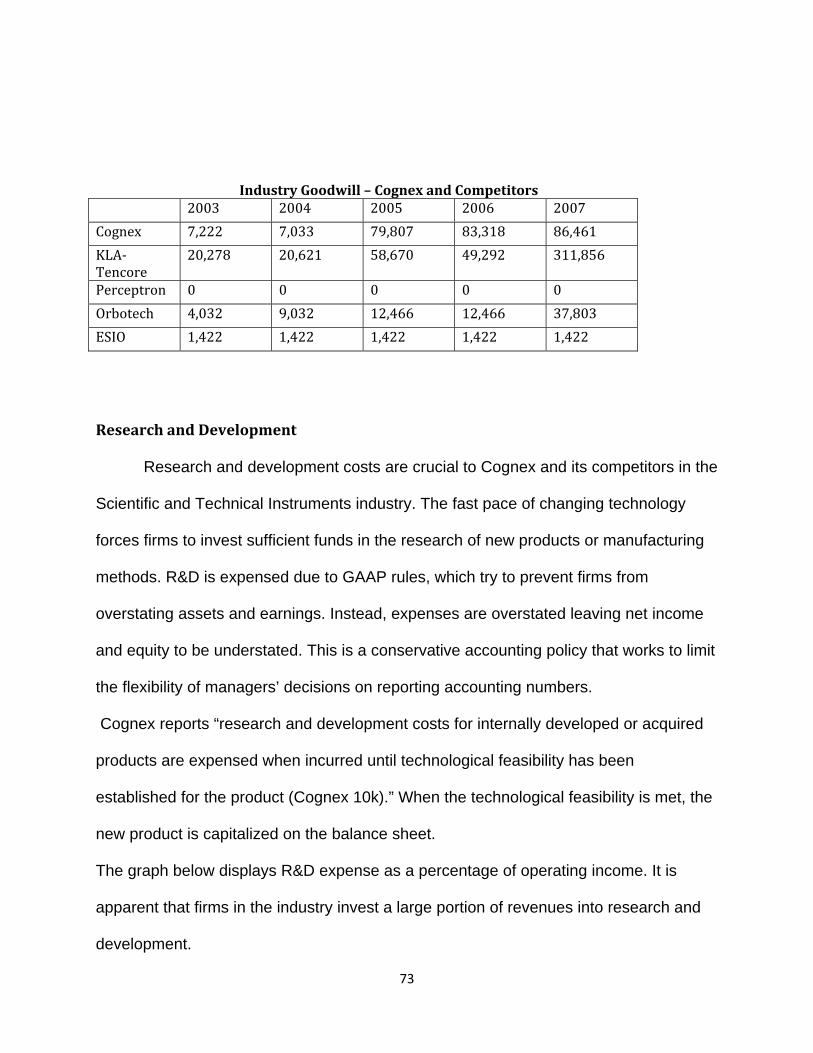

Goodwill is a major operation of many companies and can be manipulated on the

balance sheet. Before 2005 Cognex had a relatively small amount of goodwill on its

14

books, but after several acquisitions in 2005 and 2006 the goodwill account amounted

to almost 15% of total assets. Moderate levels of disclosure only tell part of the story.

The aggressive accounting for goodwill needed to be further analyzed to get a truly

transparent picture of how goodwill is accounted for. This is evidence of a type 2

accounting distortion and is identified by a “red flag”. In order to present a more

reasonable estimate of goodwill, 20% of the account was amortized. This decreased the

value of assets and added an amortization expense to the income statement, helping to

present a better overall picture of firm operations.

The research and development account was also identified as a type 2

accounting distortion and needed to be altered. Cognex does not provide much

disclosure within research and development, signaling another red flag. A similar

approach was used to reduce the enormous R&D expenses piling up on the income

statement; 20% of R&D was capitalized to reduce expenses to a reasonable amount.

Disclosure of foreign currency risk is moderate. The company 10-K states that it

uses financial instruments to hedge against this risk, but does not go into detail about

the measures used. It does state that it hedges using forward contracts among other

instruments. This type 1 accounting distortion was further examined in order to see

exactly how foreign currency risk affected Cognex. Overall Cognex moderate disclosure

with goodwill and R&D, but the aggressive accounting strategy showed that several line

items needed to be restated.

15

Financial Analysis, Cost of Capital Estimation, and Forecasting

In order to thoroughly evaluate a firm, it is necessary to go through extensive

financial analysis including ratio analysis, estimating the cost of capital, and forecasting

financials. Examining each of these aspects of the firms will provide a more in-depth

view of how well the firm is functions on an annual basis.

Firms and analysts alike often times use ratios to draw simplistic comparisons

between their performance and the performance of their competitors. The primary

types of ratio analysis classifications are liquidity analysis, profitability analysis, and

capital structure analysis. Liquidity ratios are used to explain how easily a firm can pay

its short term debt obligations. These ratios are used to discuss the overall financial

health of the firms. Analysts may use the liquidity ratios to develop a general idea as to

the level of risk within a particular firm. As a broad generalization the higher the ratios

the more safety a firm exhibits. Cognex was able to maintain average to above average

ratios throughout the liquidity analysis section. The company was also able to produce

industry leading numbers in the working capital turnover ratio. Profitability ratios explain

how successfully a firm can generate revenues in excess of their expenses. The

profitability ratios will allow analysts to understand what expenses are incurred from the

general operations as well as the revenues produced to cover those expenses. Cognex

performed exceptional with the analysis of the profitability ratios. The firm was able to

display consistent industry leading results in most of the ratio categories. The ratios in

which they did not lead to industry were still consistent and promising providing no

cause for concern. The final classification of financial ratio analysis is capital structure

ratios. Capital structure ratios are used to help understand the overall structure of

16

leverage for each firm as well as to aide in determining credit ratings. A firm can

finance its assets by either utilizing debt financing or equity financing. Firms that rely

more heavily on equity financing are easily capable of paying off their liabilities and

interest as it becomes due. Companies that utilize more debt financing are seen as

higher risk endeavors. Several of the capital structure ratios are unable to be computed

consistently in this industry due to the trend of firms holding no long term debt. The

debt to equity ratio is the most useful ratio when dealing with the Scientific and

Technological Instruments industry. A lower ratio is favorable in this category

suggesting that a company is more dependent upon equity financing than debt

financing. Cognex was once again at the forefront of the industry with persistently low

and consistent ratio results.

In order to create an effective Prospective analysis we needed to forecast the

income statement balance sheet, and stament of cash flows in both nominal and

restated terms. The most important forecast needed to determine our net income each

period ending was expected sales growth. We concluded that sales would continue to

rise in a cycle like pattern at 6% then effectively drop in year 2012. Cost of goods sold

remained at a steady retrospective average of 71% of revenue so we assumed this

could be applicable to future forecasts as well. Other forecast could be represented as

a % of sales to ultimately arrive at a forecasted net income. To connect the income

stamen to the balance sheet a return on assets average was used to forecast our total

assets through year 2019. Retained earnings can be forecasted through a net income

amount less forecasted dividends, and the net change in retained earrings was sued to

forecast our book value in equity. CFFO was forecasted as a % of OI for both restated

17

and nominal. We concluded that dividends were not a well forecasted as a function of

NI and created a growth that was more representative of past pay outs.

Using a CAPM method were r able to attain what we felt to be the most

reasonable estimate of Kd at 11.86, although we did calculate other estimates such as

the back door and size adjusted. Our estimate of Kd equated to .97 . Such a low

estimate is not out of the ordinary because of Cognex’s low amounts of reported long

term Liabilities. Next using estimates of Kd and Ke we were able to find our WACC at

10.84 before tax and 10.81 after tax.

Valuation

The last step in the equity valuation analysis is to estimate a current market

share price. We used several techniques to achieve this. First, we studied trends of

financial ratios through the method of comparables. This technique compares financial

ratios of companies with similar cash flow and business operation. The other valuation

method used involves intrinsic valuation models, a much more sophisticated approach.

It is almost impossible to predict current market price down to the penny, so we decided

to use a range of +/- 15% in share price to determine whether the firm is overvalued,

undervalued, or fairly valued.

We began the valuation analysis using the method of comparables. Competitor’s

ratios were averaged against Cognex’s to determine proper valuation. It is important to

exclude outliers when calculating industry averages, as these can adversely affect the

credibility of the conclusion. Of the 8 comparables used, 5 concluded Cognex is

18

overvalued, 2 concluded fairly valued, and one concluded undervalued. It is apparent

that through the method of comparables Cognex is determined to be overvalued.

The intrinsic valuation models offer a more accurate estimate of value because

they offer more insight into the detail of company operations, as opposed to industry

comparison. Data from our forecasted financial statements was discounted to get a

present value. We also used sensitivity analysis to see how different growth rates and

costs of capital affected current share price. We then determined if the firm was

overvalued, undervalued, or fairly valued based on a 15% margin of error. All of the

models conclude that the current market price of Cognex is overvalued. The only

drawback to the intrinsic models is that they rely on estimates, not concrete numbers.

Company Overview

History

Cognex is a firm providing vision and sensor systems, and specializes in

Industrial Optical Character Recognition System (IOCR). These systems are “capable

of reading, verifying, and assuring the quality of letters, number and symbols marked

directly on parts and components.” (cognex.com) This application reduces downtime

and improves existing quality control systems. Cognex began by servicing typewriter

manufacturers to ensure the quality of detail in the product. This unique system has

proven effective today, as Cognex serves the capital equipment market for

semiconductors and electronic tools, discrete factory automation, and surface

inspection.

19

The two divisions Cognex operates in are: Modular Vision Systems (MVS), and

Surface Inspection Systems. The MVS segment uses a variety of handheld cameras

strategically placed along the assembly line or throughout the assembly process.

These cameras will then analyze the orientation, size, and appearance of the product.

The diagnostics are then transferred to an easy to use interface monitor. This vision

software allows a firm to analyze the efficiency of the assembly process and increases

the speed and precision of product defect detection. This is very important to a firm

mass producing products, in order to identify problems early. These processes help to

improve product quality, customer satisfaction, and maintain the brand image. This

division is responsible for 87% of total company revenue. (cognex 10-k)

The second segment Cognex operates in is the Web and Surface Inspection

System, which makes up 13% of sales. The Web and Surface Inspection systems and

the Smart View software uses cameras in addition to lighting and imaging software to

detect and classify defects in metals, paper, plastics, non-wovens, and glass

(cognex.com). This software allows firms to guarantee perfection on flat and irregular

surfaces. The optical lenses can be easily installed with little or no downtime. Cognex

customers are located in three markets: semiconductor and electronic capital

equipment, surface inspection, and discrete factory automation. (cognex 10-k)

Fundamentals

Research, development, and engineering (R,D, & E) is extremely important to

Cognex. It is important to improve existing products as well as develop new techniques

to improve product performance. Failure to develop new products and respond to

20

technological changes could affect Cognex adversely through loss of profit and market

share. Cognex currently invests 15% of sales in research, development and

engineering. This has allowed Cognex to develop several new products to help sustain

its market share.

Industry Overview

The industry in which Cognex operates is Scientific and Technical Instruments.

Cognex and its top competitors , KAL-Tencor, Orbotech, Perceptron, and Electro

Scientific Industries Inc. are companies classified under North American Industry

Classification as “Instruments and Related Products Manufacturing for Measuring,

Displaying, and Controlling Industrial Process Variables”(NAIC). Firms in this industry

design, manufacture, and market the technical tools that serve manufacturing

companies today. These products are used in process and control devices, precise

measurement and signal processing, and other technologically advanced machinery.

The industry has seen extensive growth as a result of a technology boom in the 1980’s.

Machine vision, wafer identification and surface inspection systems are three general

applications this industry specializes in. This industry is very cyclical in nature due to

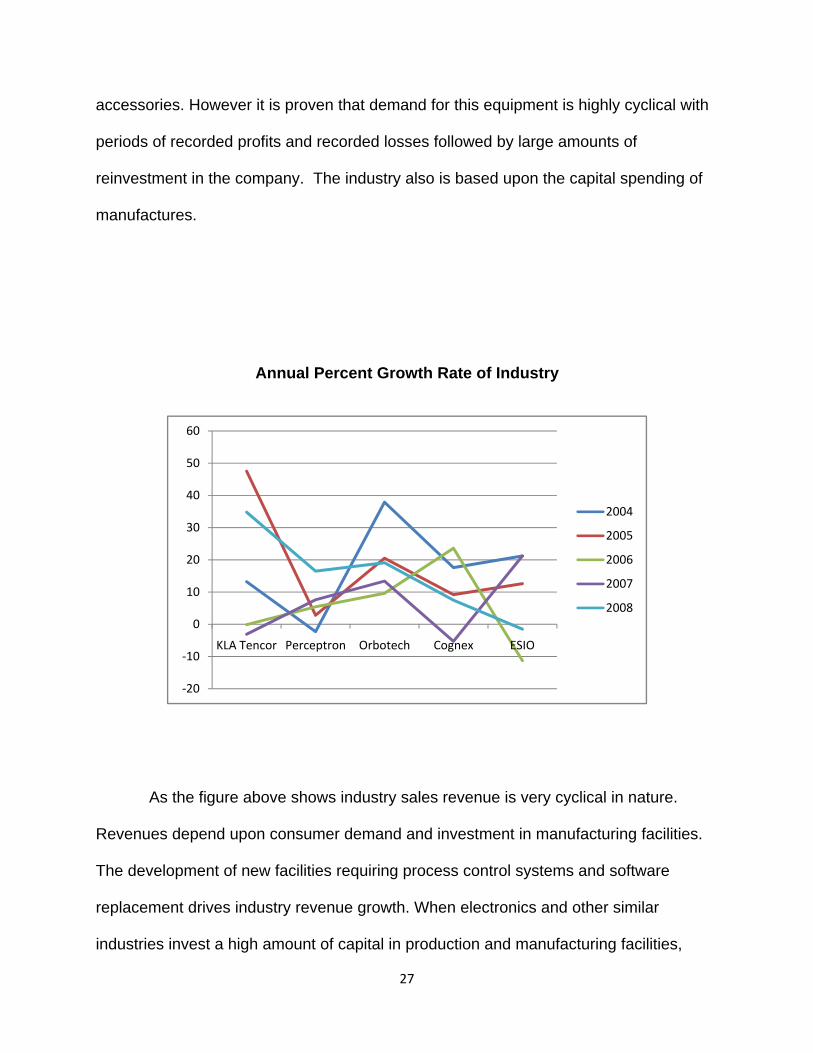

the heavy reliance on technological innovations and advancements. The chart below

demonstrates the size of each firm in the industry based on sales. It also demonstrates

the amount of the firm’s sales in comparison to the industries total sales.

21

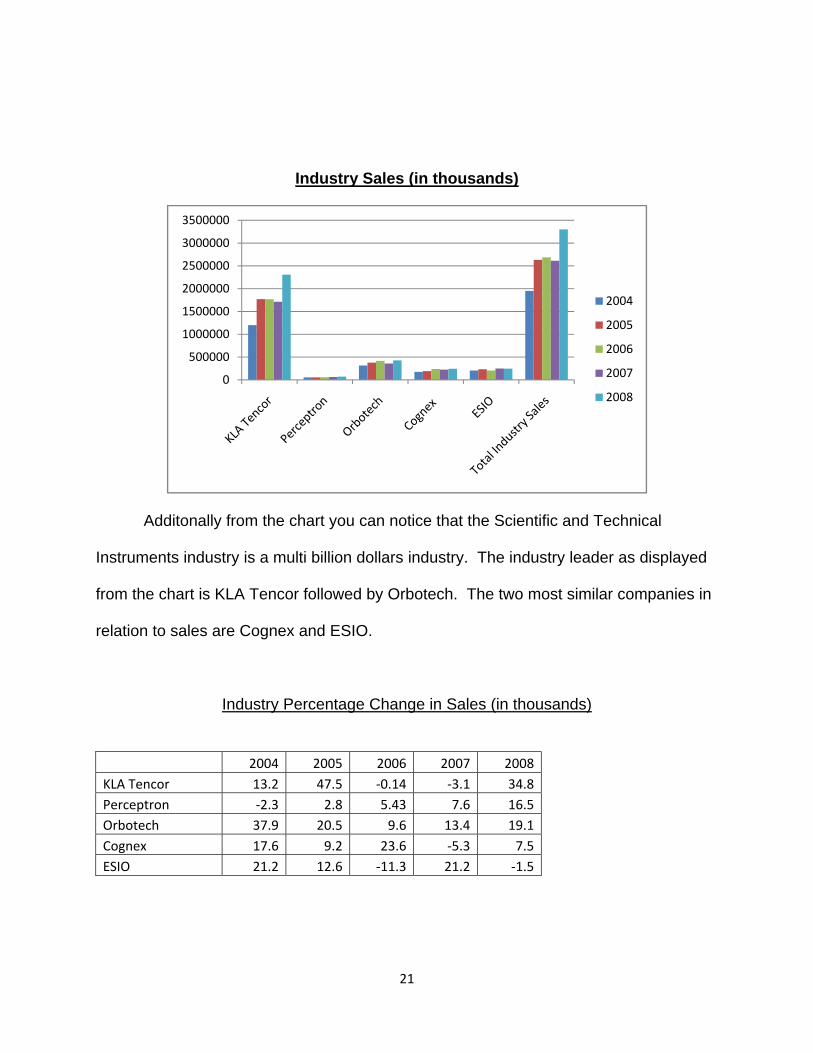

Industry Sales (in thousands)

Additonally from the chart you can notice that the Scientific and Technical

Instruments industry is a multi billion dollars industry. The industry leader as displayed

from the chart is KLA Tencor followed by Orbotech. The two most similar companies in

relation to sales are Cognex and ESIO.

Industry Percentage Change in Sales (in thousands)

2004 2005 2006 2007 2008KLA Tencor 13.2 47.5 ‐0.14 ‐3.1 34.8Perceptron ‐2.3 2.8 5.43 7.6 16.5Orbotech 37.9 20.5 9.6 13.4 19.1Cognex 17.6 9.2 23.6 ‐5.3 7.5ESIO 21.2 12.6 ‐11.3 21.2 ‐1.5

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

2004

2005

2006

2007

2008

22

From the chart above you can observe the cyclicality of the market. Every year one or

two firms excelled from the previous year while one or two others fell. This is due to

firm’s new innovations and technological advancements giving them a competitive

advantage.

Machine Vision

“Machine vision integrates image capture systems with digital input/output

devices and computer networks to control manufacturing equipment such as robotic

arms.” (machinevision.co.uk). Cognex, Perceptron, Orbotechm and ESIO mainly

participate in this industry. Machine vision equipment was first used in the early 1950’s

as a military application to research artificial intelligence. This technology proved itself to

be practical and effective, drawing some of the world’s highest profile institutions to

conduct further research. In the late 1960’s and into the 1970’s Massachusetts Institute

of Technology (MIT) developed the first machine vision application that would soon

prove to drive an entire industry. The competitors in this industry began pouring money

into Research and Development in an attempt to perfect machine vision processes and

develop new revenue streams. In the 1980’s it was apparent that firms applying

machine vision would become part of an extremely lucrative industry. Manufacturers

began installing applications involving industrial cameras to monitor and control

production operations. Many firms in the semiconductor industry were among those to

adopt the new technology, driving machine vision firms to continue expanding to service

23

new markets and increase market share. The 1990’s to current have been some of the

fastest growing years for this industry, as demand for automation and quality increase

consistently.

Wafer Identification

Many firms particularly KLA Tencor competes in this industry. KLA is heavily

impacted by the semiconductor industry. “KLA‐Tencor's primary market is the

semiconductor industry.” (KLA Tencor 10‐K) The increase in technology has lead to an

extensive demand for smaller, more powerful computer chips.

Semiconductors, small pieces that make up integrated circuits (IC’s), were some of the

components that felt this demand the most. As production increased, it became more

important to track and identify product defects. Systems were designed to take the small

semiconductors (also known as wafers) and scan each product into a computer system

for analysis.

Wafer identification systems read numbers and characters through bar codes.

This enables firms to track their products and ensure a timely production process. The

wafer ID systems use optical lenses and lasers to “see, read and record” wafers

throughout the production process.http://news.thomasnet.com/fullstory/460005

).“Integrated lensing and lighting capabilities provide flexibility required to read code

consistently throughout various stages of production that subject wafer to changes in

appearance, such as contrast and color modifications.”

(http://findarticles.com/p/articles/mi_m0EIN/is_2005_June_28/ai_n14701699)

24

Surface inspection systems

Surface inspection is the main industry Cognex, Peceptron, KLA Tecnor, ESIO,

and Orbotech mainly compete in. All of the firms inspect Surface inspection systems

scan products for constant quality control evaluation. These systems serve a wide

variety of firms including those who produce metals, paper, plastics, and non-wovens.

Lenses and 360 degree cameras are used to monitor and control the production

process the many products. It is imperative for these firms to identify defects in their

products before costly value-added processes are added to the production phase. This

is especially important for automobile manufacturers, one of the largest consumers of

surface inspection equipment.

Conclusion

The increasing availability of industrial systems stimulated the need for new

technology, pushing R&D efforts ever higher throughout the Scientific and Technical

Instruments industry. This new machinery thus increased quality control standards

across the world. Constant demand on improved production capacity and minimal

product defects has allowed manufacturing firms to purchase equipment to meet these

zero tolerance standards. It is important for firms in this industry to be aware of both

25

customer and supplier perspectives in order to stay afloat in a competitive market

(Frost). Although some markets (ie. Surface inspection equipment) show strength in the

near future, the industry as a whole cannot say the same. Technology related

purchases by firms increased consistently from 2002 through 2008; in 2008 technology

purchases by firms and governments increased by 8% (Forrester Research). However,

according to

Forrester Research, a drop of 3% in technology purchases is expected in 2009

(Forrester Research). Overall the industry has shown extensive growth in the past

decade, but companies that strive to continue their operations will depend on constant

investment in research and development (xbitlabs.com). (WSJ)

Five Forces Model

The five forces model allows a company to analyze what effects the individual

firm in relation to the industry. Using this model will allow the firm to better compete in

the industry. Additionally can establish the amount of success and profitability the firm

will realize. The model analyzes the following five issues: Rivalry among existing firms,

threat of new entrants, threat of substitute products, bargaining power of customers,

and bargaining power of suppliers. The first three of these forces are used to analyze

profits of an industry based on competition, while the latter two describe relationship of

power between input and output markets (suppliers and consumers). The model is

picture below:

26

Competitive force Degree of Competition

Rivalry among existing firms High

Threats of new entrants Moderate

Threat of substitute products High

Bargaining power of customers low

Bargaining power of suppliers High

Rivalry among existing firms

Industry growth:

Cognex and its top competitors , KAL-Tencor, Orbotech, Perceptron, and Electro

Scientific Industries Inc. are companies classified under North American Industry

Classification as “Instruments and Related Products Manufacturing for Measuring,

Displaying, and Controlling Industrial Process Variables”(NAIC). Estimates can

drastically change with new innovations and developments in software, and other

27

accessories. However it is proven that demand for this equipment is highly cyclical with

periods of recorded profits and recorded losses followed by large amounts of

reinvestment in the company. The industry also is based upon the capital spending of

manufactures.

Annual Percent Growth Rate of Industry

As the figure above shows industry sales revenue is very cyclical in nature.

Revenues depend upon consumer demand and investment in manufacturing facilities.

The development of new facilities requiring process control systems and software

replacement drives industry revenue growth. When electronics and other similar

industries invest a high amount of capital in production and manufacturing facilities,

‐20

‐10

0

10

20

30

40

50

60

KLA Tencor Perceptron Orbotech Cognex ESIO

2004

2005

2006

2007

2008

28

firms don’t need to capture others sales revenue to increase their market share. This

allows smaller firms to capture the industries excess capacity and grow within the

industry (Palepu & Healy).

Concentration :

Although a large number of firms compete in this industry, size does not ensure

dominance among firms with less than 50 million in annual revenue (Hardin).Firms with

smaller amounts of revenue are large in number and survey customers on a global

scale.

The smaller number of firms can be attributed to companies specializing their

efforts toward a specific industry. An industry with the vast amount of smaller

companies can still compete on prices and production level with larger firms because

their products and services can be tailored to specific manufacturing systems.

Particular company growth also depends to the extent that their firm specifically targets

markets. Large companies that compete in the industry may only have a fraction of

their sales revenue from inspection devices or controlling devices, while smaller firms

derive much more of their revenue from these devices and systems. Displayed below

the percentage of market share each of the main competitors of the industry maintain:

29

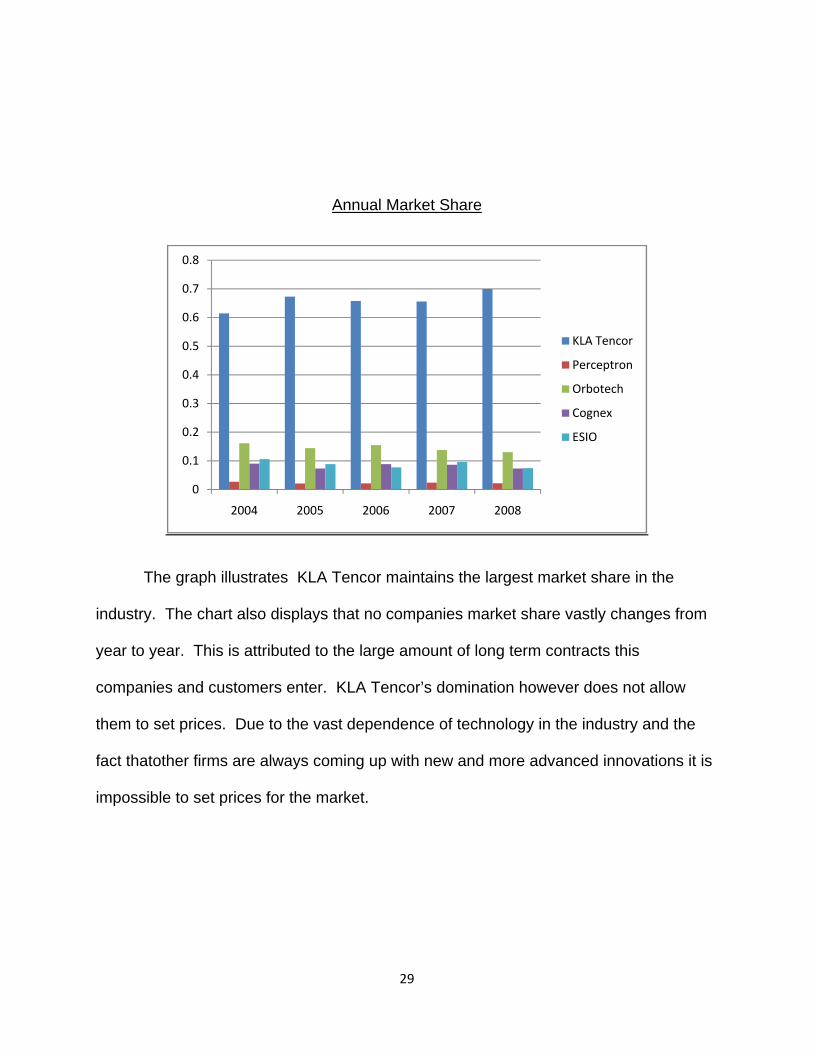

Annual Market Share

The graph illustrates KLA Tencor maintains the largest market share in the

industry. The chart also displays that no companies market share vastly changes from

year to year. This is attributed to the large amount of long term contracts this

companies and customers enter. KLA Tencor’s domination however does not allow

them to set prices. Due to the vast dependence of technology in the industry and the

fact thatother firms are always coming up with new and more advanced innovations it is

impossible to set prices for the market.

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

2004 2005 2006 2007 2008

KLA Tencor

Perceptron

Orbotech

Cognex

ESIO

30

Differentiation:

Firms can differentiate their products in a number of ways by focusing their

attention on specializing in the process control industry or by focusing on the products

themselves. Each instrument is fairly specialized which can help firms avoid head on

completion. Since most of the industry serve global end users, head on competition can

be somewhat avoided because their products and services are so specialized.

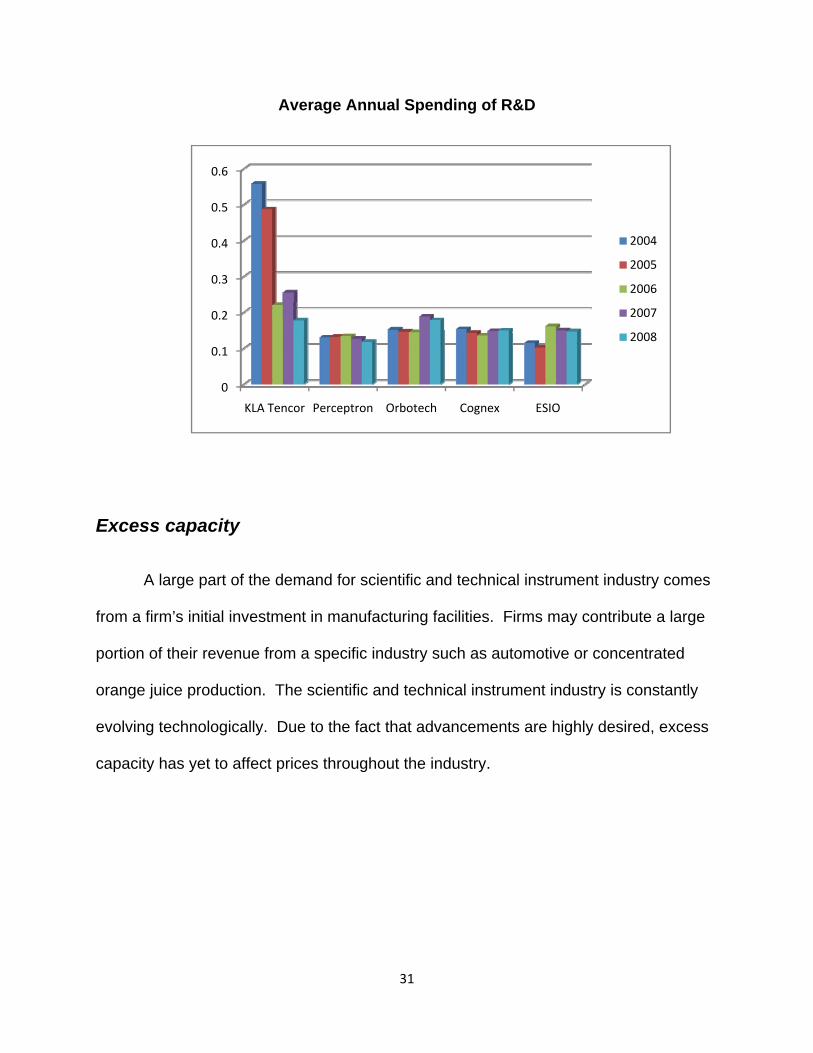

Learning economies

The process control industry has a steep learning curve and it is a necessity for

competing firms to spend time and money in research and development to create the

best product for their end user. Allowing the firm to capture a better hold of the market .

Companies in the industry spent on an industry average 2.3 billion in 2008 alone.

(Mergent online). Compared to the industry sales revenue firms will spend more on

research and development when industry revenues are gaining. The graph below

illustrates the cumulative average annual spending on R&D for firms competing in this

industry. From the chart pictured below you can see that while KLA Tencor is the

industry leader it also is the leader in allocation to Research and Development. You

also can distinguish that Perceptron the lowest performer in sales is also the firm that

allots the least amount to Research and Development. Every firm in the industry does

continue to increase the amount of funds allocated to Research and Development, even

in years when sales drop. This steady inflow of cash results in constant innovation and

advancement, which is a necessity in the industry.

31

Average Annual Spending of R&D

Excess capacity

A large part of the demand for scientific and technical instrument industry comes

from a firm’s initial investment in manufacturing facilities. Firms may contribute a large

portion of their revenue from a specific industry such as automotive or concentrated

orange juice production. The scientific and technical instrument industry is constantly

evolving technologically. Due to the fact that advancements are highly desired, excess

capacity has yet to affect prices throughout the industry.

0

0.1

0.2

0.3

0.4

0.5

0.6

KLA Tencor Perceptron Orbotech Cognex ESIO

2004

2005

2006

2007

2008

32

Exit Barriers

The scientific and technical instrument industry requires highly specialized

assets, resulting in high exit barriers. As a result specialized assets being highly ill-

liquid, it deters many firms from leaving the industry.

Conclusion

The rivalry among existing firms is highly competitive. The competitive nature of

the industry can be based upon the fact it is highly based upon differentiation. The

reliance on differentiation makes switching costs high, as well as exit barriers. The

industry is also highly competitive due to the fact of the high growth rate it has

experienced in the past several years. As the industry continues to grow, the

innovations and advancements do as well giving the industry even more growth

potential.

The Threat of New Entrants

The scientific and technical instruments market offers a great possibility for

earning abnormal profits. There are few barriers to enter into the market increasing the

competition between firms. The threat of new entrants in the market is relatively

moderate. However entering the market and being successful in the market do not go

hand in hand. Some of the factors that will determine whether a firm will enter the

industry and the amount they will invest are economies of scale, first mover advantage,

33

and access to channels of distribution and relationships, and the legal barriers. Upon

analyzing these factors the threat of new entrants in moderate throughout the industry.

Economies of Scale

In the scientific and technical instruments market there are small economies of

scale. The industry does require a large amount of capital invested in PPE and

Research and Development initially. This does not alleviate all the danger of entering

a new market however, “either way new entrants will at least initially suffer from a cost

disadvantage in competing with existing firms” (Palepu & Healy). However a large

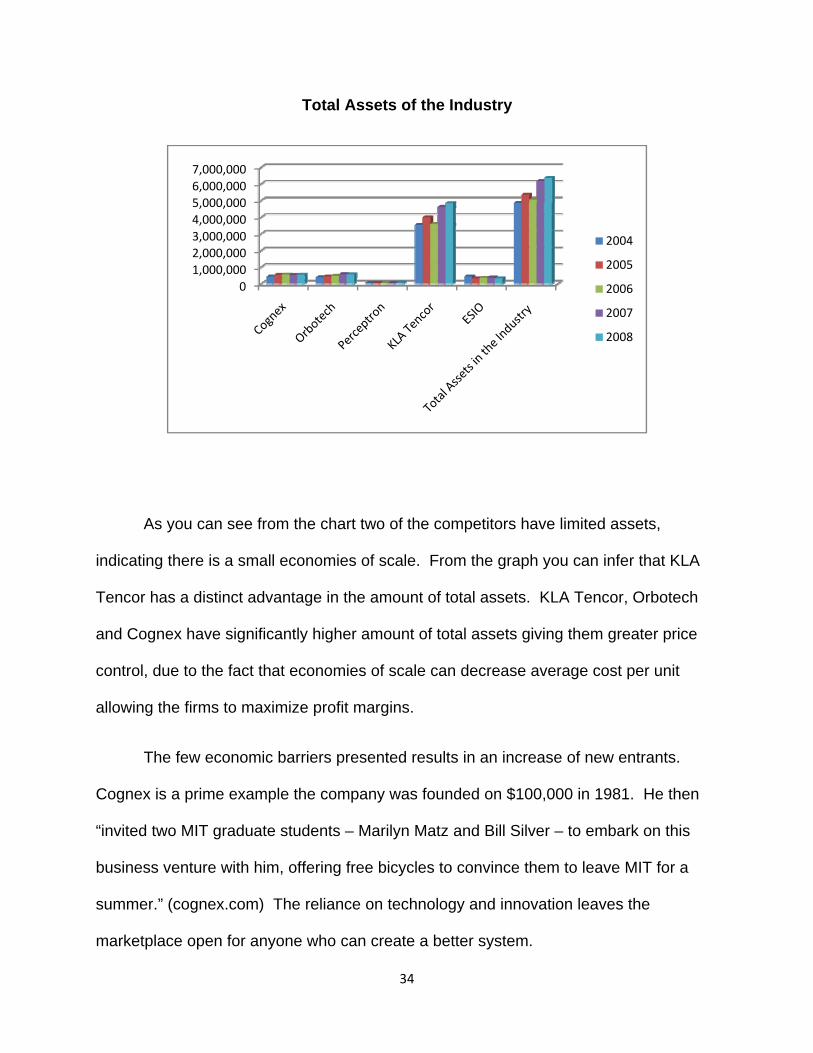

amount of current assets gives firms a greater advantage to increase their market

share. The chart displayed below presents the total assets for Cognex and its top three

competitors for the previous five years

34

Total Assets of the Industry

As you can see from the chart two of the competitors have limited assets,

indicating there is a small economies of scale. From the graph you can infer that KLA

Tencor has a distinct advantage in the amount of total assets. KLA Tencor, Orbotech

and Cognex have significantly higher amount of total assets giving them greater price

control, due to the fact that economies of scale can decrease average cost per unit

allowing the firms to maximize profit margins.

The few economic barriers presented results in an increase of new entrants.

Cognex is a prime example the company was founded on $100,000 in 1981. He then

“invited two MIT graduate students – Marilyn Matz and Bill Silver – to embark on this

business venture with him, offering free bicycles to convince them to leave MIT for a

summer.” (cognex.com) The reliance on technology and innovation leaves the

marketplace open for anyone who can create a better system.

01,000,0002,000,0003,000,0004,000,0005,000,0006,000,0007,000,000

2004

2005

2006

2007

2008

35

Due to the ease of entering the industry firms are forced to decrease the cost of

products and enter a worldwide distribution system. The industry as a whole resulted to

globalizing their distribution strategically locating distribution system worldwide. Cognex

and Orbotech experience few barriers to achieve greater economies of scale, largely

due to the amount of outsourcing available. In conclusion we conclude that the

economies to scale are moderate, making it possible for new entrants to enter the

marketplace. However the fact that firms may enter does not indicate success.

First Mover Advantage

First entrants of an industry maintain a certain amount of advantage over new

entrants. New firms attempting to achieve market share may find themselves behind

established firms because “first movers might be able to set industry standards, or enter

into exclusive arrangements with suppliers of cheap raw materials”(Papelu & Healy).

In a technological dependent economy, first movers in the industry will possess

previously established contracts with suppliers and customers. All of the firms in the

industry have previously established contracts with suppliers of cheap raw materials.

Additionally the extremely high price of these products makes switching costs high,

therefore giving a firm a first mover advantage. This makes it extremely difficult for new

entrants to gain an advantage over previously established firms. This however does not

lower the threat of new entrants, due to the fact there are constant technological

advancements in the industry.

36

Distribution Access

Possible problems for new entrants into the industry can arise with channels of

distribution. There is “limited capacity in the existing distribution channels and high

costs of developing new channels” (Palepu & Healy). Currently globalized countries

can maintain a large competitive advantage and a large portion of the market share in

comparison to new entrants attempting to compete in a much smaller market share.

Cognex and their main competitors all currently operate globally. For example Cognex

is currently established in “52 countries worldwide,”(cognex.com) as well as KLA‐Tencor

maintains a significant presence throughout the United States, Europe and Asia. (KLA Tencor).

Orbotech also operates mainly out of Israel and the Middle East. This indicates that

previously established firms in this industry maintain a competitive advantage through

prior established distribution networks. This may limit new entrant’s ability to distribute

to existing markets, since these consumers currently are brand loyal.

Legal Barriers

In the electronic inspection and monitoring instruments market one very essential

aspect is to protect intellectual property rights. Firms are successful protecting this

information through trademarks and patents. Cognex currently attains “264 patents and

trademarks.” (10-k) One competitor Perceptron possess “27 patents” and

trademarks.(10-k) New entrants can find it extremely difficult to gain market share in

currently occupied markets, because of these stringent patent and trademark

requirements. In order for obtain superior product quality new entrants are often times

obligated to acquire products from a single source provider. The other option is to

37

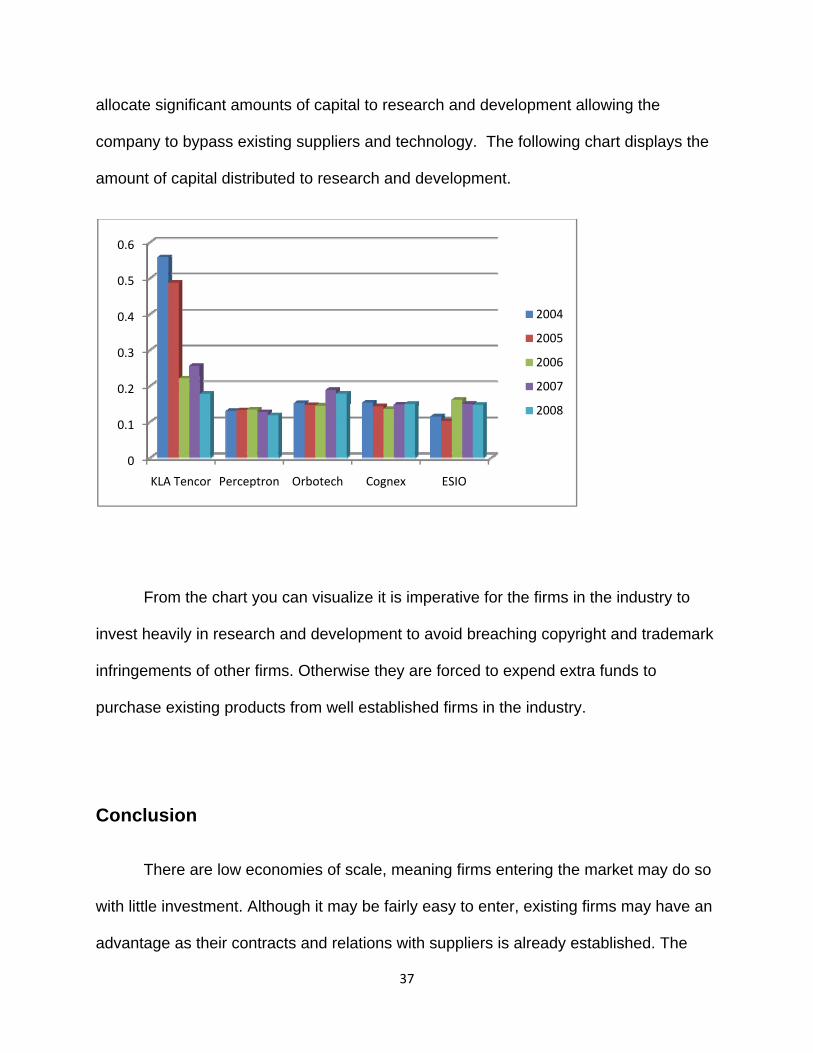

allocate significant amounts of capital to research and development allowing the

company to bypass existing suppliers and technology. The following chart displays the

amount of capital distributed to research and development.

From the chart you can visualize it is imperative for the firms in the industry to

invest heavily in research and development to avoid breaching copyright and trademark

infringements of other firms. Otherwise they are forced to expend extra funds to

purchase existing products from well established firms in the industry.

Conclusion

There are low economies of scale, meaning firms entering the market may do so

with little investment. Although it may be fairly easy to enter, existing firms may have an

advantage as their contracts and relations with suppliers is already established. The

0

0.1

0.2

0.3

0.4

0.5

0.6

KLA Tencor Perceptron Orbotech Cognex ESIO

2004

2005

2006

2007

2008

38

cost of developing new distribution channels also poses a problem for firms entering the

market. Several legal barriers have also made it difficult for new firms to establish

themselves. Every firm in the industry uses patents, trademarks and long term contracts

to protect themselves from firms attempting to increase their market share.

The scientific and technical instruments market is a very accessible market to

enter with low capital. But however legal barriers and the emphasis and new

technological advances can make it difficult for new entrants to be successful. Currently

established distribution markets and brand loyalty give long-standing firms a competitive

advantage. Contracts, copyrights, and trademarks can also allow initial firms a first

mover advantage.

Threat of Substitute Products

In the scientific and technical instruments market, there are various motivations

to substitute a product for a different one. One of the factors affecting substitution is

price. Price is very relative in the relation of substitutes because products in the

industry are very expensive they are not everyday goods. Performance additionally

plays a large role in the substitution process. The most important element of this

industry is the ability to ensure perfection among produced products.

Due to the mass quantity of firms that would desire a electronic inspection and

monitoring of this nature many have been produced to attempt to mimic the task,

allowing for a variety of products in the market. As technology advances devices for

39

manufacturing monitoring can become more universal and less specialized. Less

specialized products have a higher threat of substitute products.

Performance is absolutely vital to ensure success in the market. In the industry

there is an elevated demand for smaller, faster, and more efficient products allowing

several substitutes to be created. This constantly evolving industry allows a vast

amount of consumers to play an active role in the market. Consequently, firms in the

industry must be able to emphasize both on price and performance. Although some will

sacrifice performance in order to cut price most consumers are not. However a superior

performance and superior price can force consumers to acquire a more affordable

product.

Costumers Willingness to Switch

In an industry dominated by technological innovation, differentiation, and

constant improvements substitute products are viable in the industry. Firms are

constantly endowing capital in order to create new advancements. Most products and

technology are protected by legal copyrights, and patents. Reverse engineering allows

for similar products to be produced quickly. The industry is an active market that allows

consumers to find the most effective product at an agreed upon price.

40

Conclusion

Price is fairly consistent throughout the industry, as most firms are willing to pay

a high price for a premium product. The products in this industry are highly specialized

and differentiated leading to a low customer willingness to switch. Additionally halting

customers to switch is the long life of the product, every company in the industry offers

various types of warranty programs additionally to keep the product operating properly

and at full satisfaction of the consumer.

Bargaining Power of Customers

To determine the actual bargaining power of a firm’s customer base, analysts

begin by examining the core markets the firm operates in and to whom they sell their

products. The scientific and technical instruments market operates in three specific

markets: semiconductor and electronic capital equipment, surface inspection, and

discrete factory automation. The original equipment manufacturers (OEM) who produce

semiconductor and electronic capital equipment are major customers in this market.

Other industries these products are present are in the automotive, consumer products,

electronics, food and beverage, medical devices, pharmaceutical, packaging, solar, and

glass. The discrete automation manufacturing market supplies manufacturers of several

industries. They include: automotive, consumer electronics, food, beverage, health care,

pharmaceutical and aerospace industries. The customers of the surface inspection

market include firms that manufacture metals, paper, non-wovens, plastics, and glass.

41

Firms in these industries purchase this equipment from authorized third party dealers or

a direct sales force. Due to the wide variety of the product specifications and growing

customer needs, it is important that firms maintain strong customer relations.

Price Sensitivity - Customer

Just as external relationships are crucial, it is also important to examine price

sensitivity in order to establish a fair market price. “The importance of the product to the

buyers’ own product quality also determines whether or not price becomes the most

important determinant of the buying decision”(Palepu & Healy). Customers in this

industry rely strongly on their brand image; therefore many are willing to pay a premium

on capital equipment to ensure the quality of their products. Patents are often used to

protect intellectual property used in developing products in this industry. For example,

Cognex has approximately 264 patents while their competitor Perceptron, accounts for

27. Due to the high specification of the products in the industry customers have low

price sensitivity.

Relative Bargaining Power - Customer

The relative bargaining power with respect to customers is “the cost to each party

of not doing business with the other party” (Palepu & Healy). In other words, the more

firms and alternative products that the customers have to choose from the more

customers have bargaining power over suppliers. In this case, the customer base within

42

the industry has a demand for highly specialized products that meet their needs. Firms

in this industry have bargaining power over their customers because these products are

essential to their business and there business operating effectively. However, the loss

of any customer or potential orders could adversely affect business operations. Every

firm in the industry has its large customer base and additionally a small customer base.

These larger customer bases in general account for a much large percentage of sales

than do the smaller customers. Due to the nature of this industry, relative bargaining

power over customers is considered to be moderate.

Customer Switching Cost

Switching cost refers to how easily customers can switch from one product to

another. Although this is a concern in some industries where products are easily

substituted, this industry proves otherwise. The fact that firms in the industry rely on

differentiation, switching costs are particularly high. The firms in this industry produce

technology that many customers find essential for their business, limiting their ability to

seek alternative products. Additionally the price of the products being considered a

exclusive good make it difficult to switch from product to product, without a significant

loss of capital Therefore, customer switching cost in this industry are high.

43

Conclusion

The scientific and technical instruments industry is a highly differentiated market,

resulting in a very low quantity of substitutable products. Additionally the high price of

the products also makes it very hard to switch, without losing large amounts of

investment.

Bargaining Power of Suppliers

Several of the concepts used to determine the ultimate power of customers are

also incorporated when analyzing the sensitivity of price between firms and their

suppliers. Depending on the size, number and proximity of suppliers, prices can

fluctuate to a great extent. If not controlled adequately, high prices from suppliers can

result in large operation costs. In industries where many suppliers operate, bargaining

power of the purchasing firm is high. In contrast, in an industry with one or few

suppliers there is little to none bargaining power. Cognex and orbotech conclude that

they are firms that obtain components from single source suppliers (Cognex and

Orbtech 10-ks). KLA Tencor, ESIO, and Perceptron also have contracts with suppliers

make the products exclusively available to the individual firm. Due to the lack of

alternative suppliers, these single source suppliers can simply set a price that firms

must consent to.

44

Price Sensitivity – Supplier

As mentioned previously, the number of suppliers can greatly influence the cost

of operations for a business. In an industry that is greatly dependent on differentiation,

the number of suppliers is already limited to firms. Cognex, KLA Tencor, Orbotech,

Perceptron, and ESIO furthermore have a single supplier contracts, prohibiting some

suppliers from supplying any other firms. This can greatly limit firm’s ability to find an

alternative low cost provider.

Relative Bargaining Power – Supplier

In a differentiated market where there are a limited number of supplying firms,

the bargaining power is generally fixed. As a result, firms tend to enter into long term

contracts with their suppliers in order to keep costs relatively stable, and because they

simply have no other means of acquiring equipment. These long term contracts,

coupled with a small number of suppliers makes it difficult for firms to find alternative

low cost options. Therefore, suppliers in this industry have low relative bargaining power

over firms.

Conclusion

Suppliers in the industry are limited due to the contracts and differentiated products.

Additionally the high switching costs lowers the amount of power they maintain over

buyers. These conditions make it very difficult for the firms in the industry to look

45

around for other alternatives. The industry is not affected to market fluctuations, as well

as inflation because of the long term contracts they enter with the firms.

Industry analysis

Superior product quality:

Firms can compete on a product that; lowers the cost of inspection and detection,

produces accuracy and serves their industry closer than the competitors. Vision devices

in highly automated production lines need to be able to provide guidance, identification,

and inspection at a high speed and register moving elements accurately and reliably.

Accurate and reliable detection can ensure that the original product manufacture has a

finished good that is on par with their quality standards. Deviations of quality in

production can cause unnecessary loss of productivity and other costs to

manufacturers. KLA Tencor offers superior products quality by guaranteeing

“extensive refurbishment, testing, and certification minimize investment risks,

while increasing equipment value. As well as Cognex, Orbotech, Perceptron, and

ESIO that all offer extensive warranty and guarantees to ensure superior product

quality. Some firms have been able to lower costs of inspection with specific products.

Technological advances have allowed some vision systems to become more general, in

that they don’t require as much specialization to perform a wide array of operations.

46

Superior product variety:

Visual systems allow firms to detect orientation, identify, to inspection, or

measure dimensions. Not all firms in any market are the same or use the same

production process. The larger deviation between firms is the products that they

produce. In order to be successful in the vision inspection market you must be able to

inspect and ensure perfection on a variety of products that are a variety of sizes,

shapes, materials, and even color. The visual identification tools available can pinpoint

the exact location and orientation of a variety of products. For example id scanners can

be used in warehouses, supermarkets, food and beverage industries and consumer

packaging. KLA Tencor who specializes in wafer identification, while Cognex and

Orbotech use a system called surface inspection systems. Defects do come in all

shapes and sizes. Some markets may have a defect in the printing department; others

may have one in a manufacturing department. Ideally you would need to be able to

inspect every department in the manufacturing process from beginning to end. While at

the same time they must be able to inspect and guarantee perfection in a wide variety of

products. These products can serve a multiple amounts of industries such as wood,

metals, papers, nonwovens, plastics and glass, automotive, consumer products,

electronics, food and beverage, medical devices, pharmaceutical, packaging and solar.

Available technology can even assist with products in automation and determine the

dimensions of a product that does not possess a defined shape. By allowing firms to

inspect every aspect of their product, you allow those firms to guarantee perfection back

47

to their customers, heavily increasing their market share. As well as presenting this

firms with a more marketable product. Electronic inspection devices do not come in only

one shape or size. There is a wide variety of products offered to enable any

manufacture to incorporate them into a current line with little disturbance in current

production.

Superior customer service:

Due to evolving nature of automated assembly lines customer service is a necessity

among firms. Automated lines depend on essentially all products running smoothly so if

detection devices or software are on the failing, production capabilities can be

hampered. Companies in this industry provide training for their clients on several

different technological levels from beginner to advance. This advanced training can add

considerable amounts of value to a firm. Additionally this training can prevent a wide

variety of problems from occurring after the product is installed, and when these

problems do occur the provided training can aid in ensuring a rapid repair. This will

reduce the amount of revenue lost by manufacturing lines being halted. This

educational material is more often than not free of charge to customers. Firms will send

out a magnitude of informational software and literature along with several trainers

permit a hands on approach. Around the clock customer service call centers are

available from Cognex, KLA Tencor, Orbotech, Perceptron, and ESIO. Operated by

highly trained and intelligent individuals guaranteeing your product will be operational

48

twenty four hours a day. These first-class customer service plans can improve client’s

perception of the industry and the market, and will refrain customers from substituting

your product for another due to small predicaments with the product. The large

customer based served by the industry includes the food industry, electronics, printing,

textiles, glass, packaging and many others. These industries cannot afford to have

production lines shut down for extended periods of time and therefore rely on these

products to be successful.

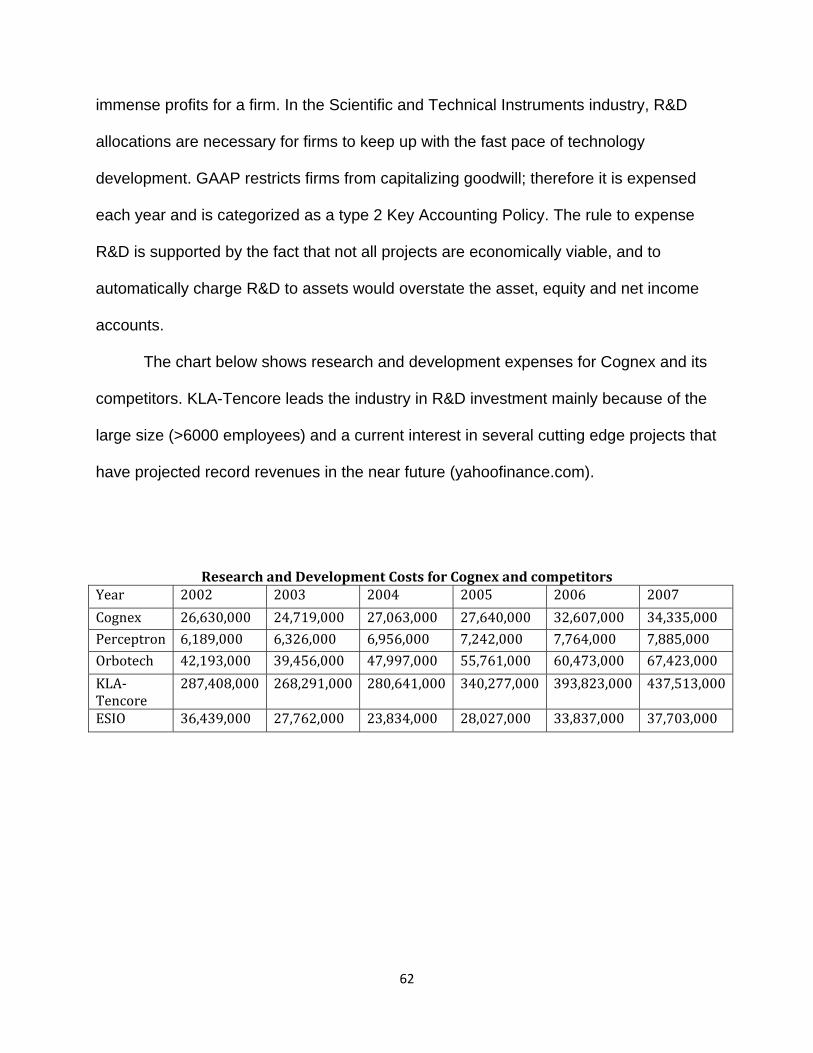

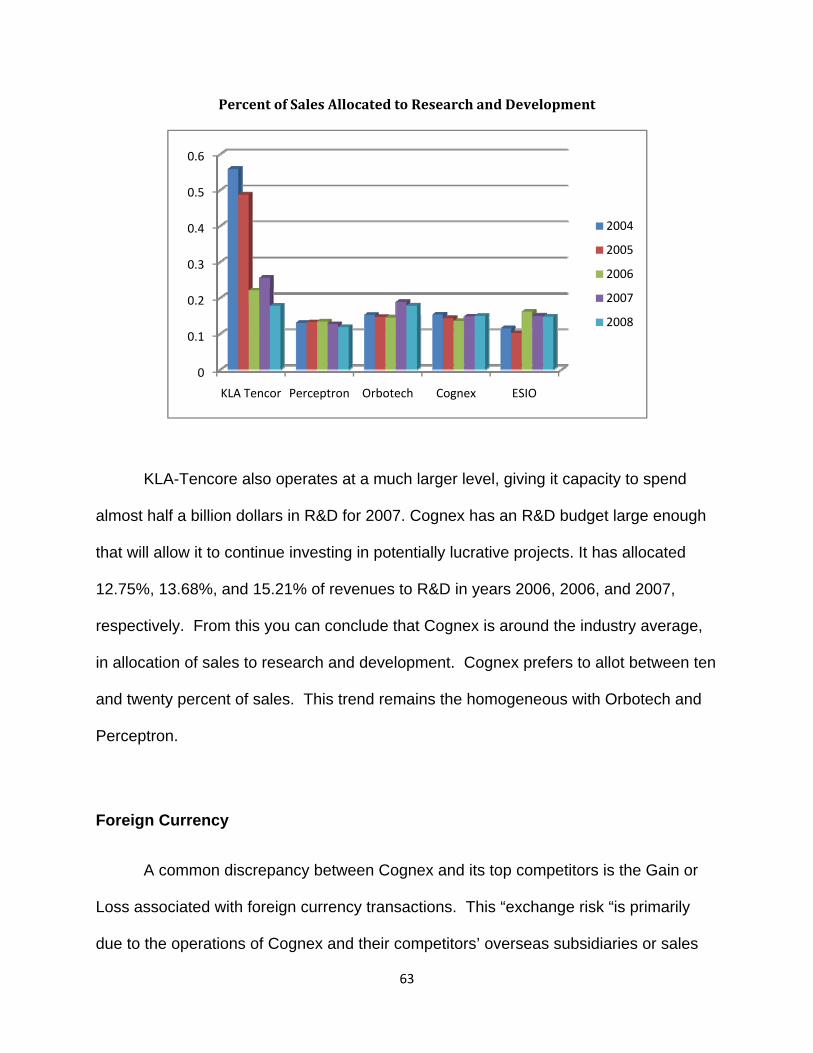

Research and Development

In order for firms to keep pace with the industry’s accelerating learning curve,

they must spend substantial amounts of capital on R&D. Kla-Tencor stated in their

annual report “that continued and timely development of new products and

enhancements to existing products are necessary to maintain a competitive position”

(KLA-TENCOR 10-K). Therefore, firms in this industry must invest a percentage of

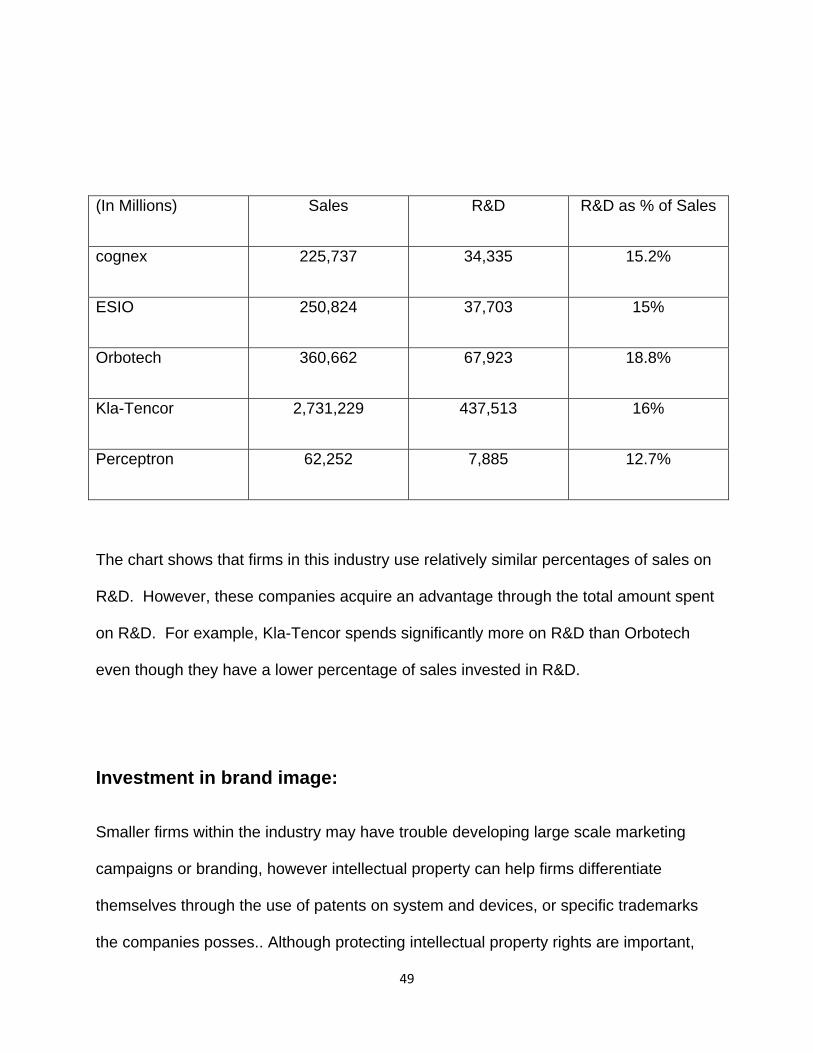

sales in research and development to remain effective. The chart below provides

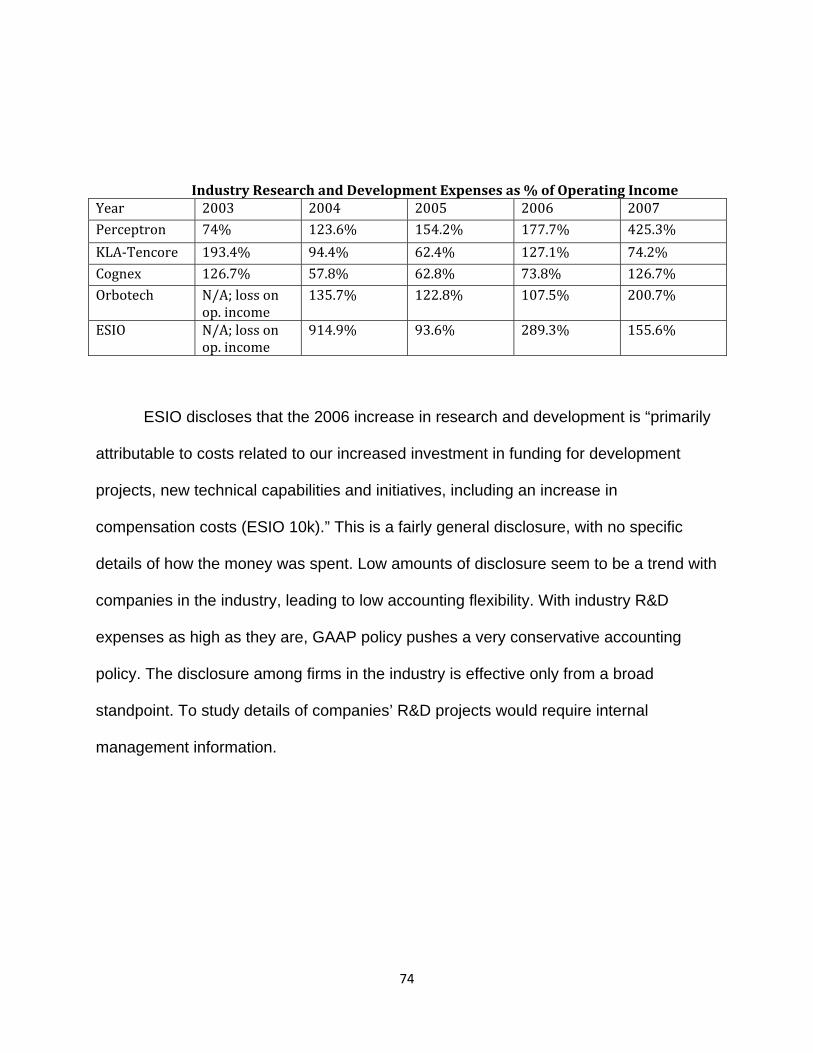

information about net sales and R&D of rival firms in this industry.

49

The chart shows that firms in this industry use relatively similar percentages of sales on

R&D. However, these companies acquire an advantage through the total amount spent

on R&D. For example, Kla-Tencor spends significantly more on R&D than Orbotech

even though they have a lower percentage of sales invested in R&D.

Investment in brand image:

Smaller firms within the industry may have trouble developing large scale marketing

campaigns or branding, however intellectual property can help firms differentiate

themselves through the use of patents on system and devices, or specific trademarks

the companies posses.. Although protecting intellectual property rights are important,

(In Millions) Sales R&D R&D as % of Sales

cognex 225,737 34,335 15.2%

ESIO 250,824 37,703 15%

Orbotech 360,662 67,923 18.8%

Kla-Tencor 2,731,229 437,513 16%

Perceptron 62,252 7,885 12.7%

50

their functionally is to protect “technological expertise and develop new and better

technologies”(kla-Tencor). Additionally firms invest in advertising to get the frims name

more familiar with the public. KLA Tencor invests on average 4.58 million dollars a year

in advertising while Cognex invests 1.74 million a year in advertising. However firms

hoping to build off of their core competencies need to have products that end-users can

associate with, especially if companies serve the market.

Value Creation analysis

Superior customer service

With new products evolving daily in the scientific and technical industry there

remains a lot of room for inexperience on the job. Manufactures that integrate new

systems, however do not offer employees adequate training and education in the field

will not be successful. Without proper training employees will run into an ample

amount of technical problems resulting in delays in production and manufacturing lines.

They also will not be able to guarantee precision and flawless work, which will greatly

damage their products image, and not to mention market share and profits Behind all

of these vision professionals lies a wealth of support resources, including live, online,

and video-based training; online conferencing; software downloads; our searchable web

knowledge base; and worldwide technical support . Firms such as Intel and Applied

Materials are spending less on capital equipment due to the current economic situation.

51

It is more important than ever for customers to maintain relationships with their

suppliers. (WSJ)

Workshops and Seminars

Before purchasing a product, there is a large array of workshops available in

order to acquire prior information about the product to make sure it will be the right

purchase. These workshops are available worldwide and open to the public. There

are additionally seminars available on the internet to provide easily accessible

information to any consumer worldwide. These seminars are available for all of the

leading technological progress available to purchase.

Installation

With the purchase of a Cognex system, you are provided with a world class

installation team to apply the products to your current manufacturing process “they

adapt automatically and never need adjustment”. (Cognex.com) This installation is not

only quick and effective customers are not forced to change a manufacturing process in

order to fulfill to criteria to make the product effective. This amounts to little or no delays

in manufacturing process. With the professional installation Cognex offers a wide

variety of training programs for customers.

Training

52

The mass amounts of training programs offered, greatly increase companies

chances of succeeding. After installation a highly trained and experienced employee

will come educate, and prepare you for your product. You will be instructed with

directions on use of the product, but also with information on how to repair any

malfunctions. As well as a wide variety on in class training programs that can be

attended, that “most are free-of-charge* and we provide many different vehicles to help

you learn more about how to improve your process through machine vision

inspections..” (Cognex.com) These classes will provide not only educational

information about the product, but also provides a hands on approach to allow students

to master the product. Training programs are also provided on the web, if you are not

able to make it to a class room session, giving full accessibility to knowledge of the

product. This allows manufacturers to cross train employees, providing producers with

a much more efficient manufacturing process.

Online Meeting Rooms

In Cognex’s online meeting rooms you are able to communicate with other

customers around the world allowing customers to entertain others with questions they

might have previously had, or to give each other advice about new equipment. There

are two online meeting rooms available to anyone with the internet anywhere in the

world. These rooms have a capacity to accommodate anyone, allowing all customers

the same amenities.

Smartlist

53

This program allows customers to email each other with questions. Smartlist will

allow you to see other customers sharing the same products and services you are

currently enjoying as well as other products you may be interested in the future.

24 Hour Customer Service

Customer service representatives are available twenty four hours a day, three

hundred and sixty five days a year. All customer service representatives are trained

with knowledge of all current programs and products offered in the line. These

representatives can be contacted through a variety of ways including over the phone,

email, and via online chat. These services stations are located worldwide in able to

prevent a language barrier of any kind. As opposed to Orbotech whom only provides

five worldwide centers. (Orbotech.com)

In an industry that is continually increasing the amount of knowledge it takes to

be successful, everyone will need a helping hand. At Cognex “Customers are our

number one priority, and listening to them is always the first step. Cognex sales

engineers and application specialists are located around the world, to provide

assistance wherever and whenever needed.” (Cognex.com) The wide array of

customer service and training available anyone can become a knowledgeable Cognex

customer.

54

Superior Product Variety

In the scientific and technical industry all competitors are endlessly competing on

product size and quality. Cognex strives to make their product smaller and more widely

available for all areas of the product line, and for numerous markets. Currently Cognex

services the “automotive, the medical, the solar, the semiconductor and electronic, the

pharmaceuticals, the paper, plastics, nonwovens web inspection, the food and

beverage, packaging, the metal and glass surface inspection, and general

manufacturing markets” (Cognex.com). These markets all require different products in

order for them to be successful, currently Cognex reinvested $34,335,000 into research

and development in order to meet this needs of its customers. With more advanced

products being introduced to current customers, it is also very available to other markets

similar in nature. By offering more advanced products and numerically a greater

number Cognex can greatly improve its market share. Cognex presently is the number

“one in the widest product range, providing robust and cost effective solutions to every

application.” (Cognex.com) By producing a wide variety of products Cognex is able to

offer numerous products at different prices to accommodate any and all consumers.

Research and Development

In the scientific and technical instruments industry it is vital to respond to new

technological transformations within the industry. Cognex states that “the failure to

develop new products could result in a loss of market share and decrease revenues and

profits” (Cognex 10-k). Cognex has increased the amount of revenue used for R&D

55

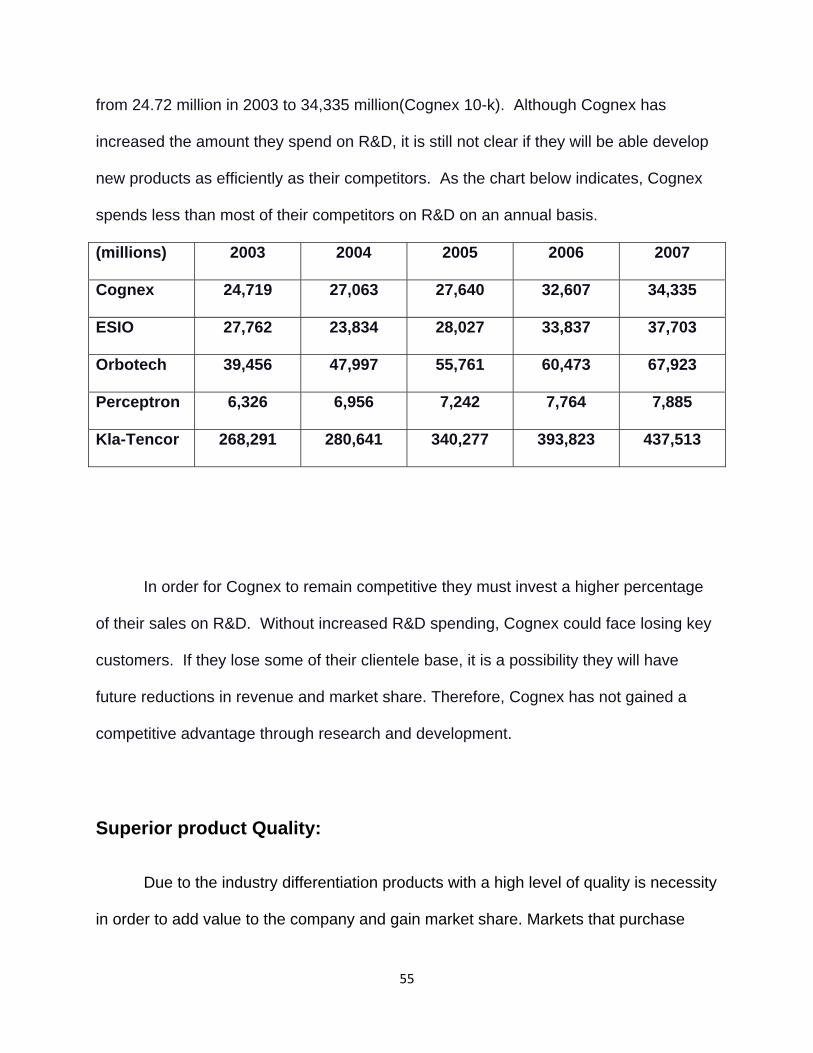

from 24.72 million in 2003 to 34,335 million(Cognex 10-k). Although Cognex has

increased the amount they spend on R&D, it is still not clear if they will be able develop

new products as efficiently as their competitors. As the chart below indicates, Cognex

spends less than most of their competitors on R&D on an annual basis.

(millions) 2003 2004 2005 2006 2007

Cognex 24,719 27,063 27,640 32,607 34,335

ESIO 27,762 23,834 28,027 33,837 37,703

Orbotech 39,456 47,997 55,761 60,473 67,923

Perceptron 6,326 6,956 7,242 7,764 7,885

Kla-Tencor 268,291 280,641 340,277 393,823 437,513

In order for Cognex to remain competitive they must invest a higher percentage

of their sales on R&D. Without increased R&D spending, Cognex could face losing key

customers. If they lose some of their clientele base, it is a possibility they will have

future reductions in revenue and market share. Therefore, Cognex has not gained a

competitive advantage through research and development.

Superior product Quality:

Due to the industry differentiation products with a high level of quality is necessity

in order to add value to the company and gain market share. Markets that purchase

56

Cognex vision systems require that products satisfy their manufacturing process needs

in order for them to be able to realize their own products. Products that provide a

greater degree of accuracy, especially for the electronics industry, are more sought after

because they insure that the manufacturing process is running according to plan without

expensive delays in production. Congenx provides for this necessity by providing

products that cater to a need of accurate and reliable measurements and inspections.

Identification and inspection systems for industries such as the electronics industry

require high-speed and accurate detection of defects in minute components “Cognex’s

In-Sight® 1720 series wafer ID reader quickly and reliably reads codes”(Cognex 10-k),

although this may seem as industry standard Cognex has devoted much of their time

and effort into developing better products for the electronics markets, “In 2000 sales to

semiconductor and electronics capital equipment manufactures represented

approximately 61% of the companies’ total revenue”(Cognex 10-k). Cognex has been

leading machine vision technologies and is able to capture sales from companies who

need specific solutions. Cognexs’ innovative tool PatMax®, enabled companies to

detect defects in hard to identify surfaces such as reflective solar panels with better

accuracy (Cognex.com).Tools such PatMax® as can lower the cost of inspection by

reducing expensive returns and new materials. Further development of In-Sight®

product lines and other lines has helped Cognex develop industry specific solutions that

maximize accuracy. Further devotion to accuracy and vision technologies in their

products can lead Cognex to further increase their market share and help gain a

competitive advantage over firms competing in similar markets. Cognex also has the

capacity to produce generalized goods that can sevrve a basic amount of functions

57

Conclusion

To create value within a firm customer service, superior product quality, research

and development, and product variety are all necessities. Cognex has a market full of

competitors. This means that the product lines must be flexible enough to serve any

industry. The variety of products firms offer can determine whether or not they are

flexible enough to become a major force in the industry. Product quality is very

important as consumer firms have a zero tolerance on defective products. The training,

online meeting rooms and 24 hour customer service are some intangibles that create

value for Cognex.

Formal Accounting Analysis

Introduction

The accounting procedure is a very important operation in business. It reports

how a firm accounts for its transactions, and in turn, helps to establish a value for the

firm. Due to the fact, that most of the numbers are either exposed to some degree of

manipulation or error there is need for a method to standardize this distortion.

Consequently it is required for companies to follow the Generally Accepted Accounting

Principles.

However even thought this practice was created and is enforced by the United

States Government under the Sarbanes Oxaley Act, there is still room for error. This

allows firms to still manipulate numbers in whatever they deem necessary. One

practice of manipulation is by deflating or inflating net income. By inflating net income

58

firms are able mislead investors by presenting a more profitable firm. Additionally by

deflating net income a firm is able to reduce tax expenses or deceive competitors.

These practices are legal under the GAAP principles, and therefore elevate the

importance for a system to recognize these instances.

In order to locate the manipulation an accounting analysis is used using six

steps. These steps evaluate a firm’s accounting quality. Step one is to identify principal

accounting policies. This involves identifying key success factors and potential risks in

an industry. Step two is to assess accounting flexibility. The flexibility of the accounting

policies can have a significant impact on the reported financial performance of a firm

(Palepu & Healy). Step three is to evaluate accounting strategy. After the flexibility of

the policies are examined, it is necessary to assess accuracy and bias within the

reporting. Step four evaluates the quality of disclosure. GAAP establishes minimum

criteria for disclosure, but company managers have final discretion when reporting

financial statements. Step five is to identify potential red flags within the financial

statements. These are indicators that analysts should examine to assess the accuracy

of the reports. The final step is to undo any accounting distortions. If any numbers

appear to be inaccurate, analysts should restate the reports in order to reduce distortion

as much as possible (Palepu & Healy).

Key Accounting Policies

Cognex key success factors include product differentiation, superior quality,

global distribution and value creation for the customer. The prior factors are a firms

type one Key Accounting Policies that allow you to analyze the key success factors in

59

relation to disclosure. These success factors are driven by the accounting of day to day

business operations. Different accounting policies create different images of firms,

depending how management decides to report the financials. This creates the

opportunity for management to distort financial statements in order to hide potentially

negative information or create a false image.

Secondly the type two policies that refers to distortion. These distortions can

occur in areas regarding research and development, goodwill, defined pension plans,

foreign currency risk, and operating and capital leases. GAAP allows managers to use

the most appropriate accounting techniques because of managements’ “superior

knowledge of the business to determine how best to report the economies of key

business events” (Palepu & Healy). It is important to analyze each area where there is a

potential for distortion in order to create a true and accurate picture of the firm and its

industry.

Goodwill

A major operation of many firms is acquiring subsidiaries and smaller companies

to increase market share and implement new technology. When a new firm is acquired,

it is assigned a price at market value. However, many companies purchase subsidiaries

for an amount in excess of their fair market value. This additional amount paid above

market value is referred to as goodwill. Goodwill is located on the balance sheet as an

intangible asset. It refers to the extra “value” obtained by the structure of a business’s

operations. Cognex has two units to which it reports goodwill, the Modular Vision

System Division (MVSD) and the Surface Inspection Systems Division (SISD).

Currently, the MSVD reports a goodwill value of $83,328,000 and the SISD reports

60

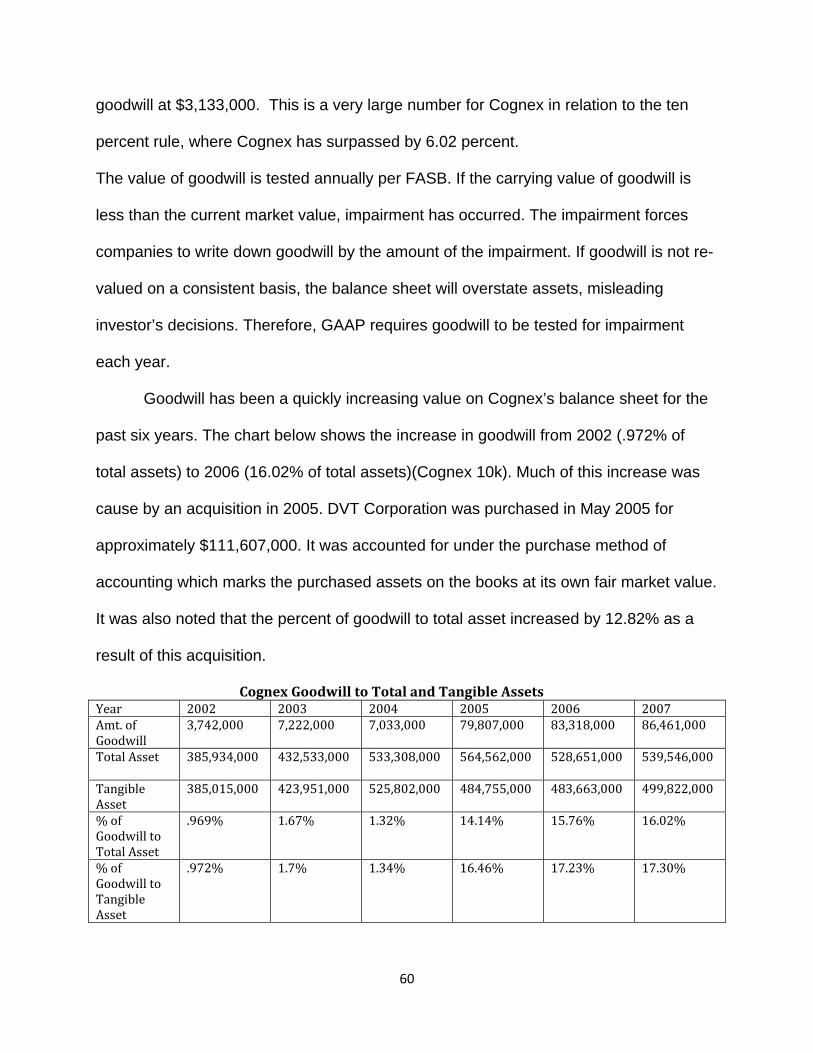

goodwill at $3,133,000. This is a very large number for Cognex in relation to the ten

percent rule, where Cognex has surpassed by 6.02 percent.

The value of goodwill is tested annually per FASB. If the carrying value of goodwill is