Embed Size (px)

Citation preview

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Walmart Neighborhood Market:

March 2016

Doing Business in Bentonville

Leon Nicholas, SVP and Knowledge Officer

Laura Kennedy, Director

Assessing Its Prospects in a Changing Landscape

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Copyright © 2016 Kantar Retail. All Rights Reserved.

501 Boylston St., Suite 6101, Boston, MA 02116

T: +1 (617) 912 2828

No part of this material may be reproduced or transmitted in any form or by any means, electronic or

mechanical, including photography, recording, or any information storage and retrieval system now

known or to be invented, without the express written permission of Kantar Retail.

The printing of any copies for backup is also strictly prohibited.

Disclaimers

The analyses and conclusions presented in this seminar represent the opinions of Kantar Retail. The

views expressed do not necessarily reflect the views of the management of the retailer(s) under

discussion.

This seminar is not endorsed or otherwise supported by the management of any of the companies

covered during the course of the workshop or within the following slides.

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

3

Agenda: Assessing Neighborhood Market’s Prospects

Source: Kantar Retail research and analysis

Shopper

Assortment

Prototype

Competition: Spotlight on Publix

Conclusion and Supplier To-Dos

‒ Add or delete points as

needed by inserting or

deleting rows

‒ Align with the image

‒ Reach out to creative for

assistance if needed

Replace w/

topical image or

reach out to

creative

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Neighborhood Market’s Expansion Will Continue 4

Source: Company presentation and reports, Kantar Retail analysis

Sales (USD millions) Stores

“I am really excited about what we can do with Neighborhood Markets. But we have got to

fix some of these basic things and then we can get into them.” –Greg Foran, October 2015

About 35% of WMT’s U.S. sales added through 2020 will be from small formats

Closed 102 12,000

square foot NMKTs, 24

“traditional”

Note: Neighborhood Market store closures in January 2016 occurred before the end of the fiscal year and are accounted for in 2015. Sales impact is accounted for beginning in 2016.

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Establishing “Development” Leadership

Neighborhood Market has equal footing with Supercenter in ops structure

5

Judith McKenna

Chief Operating Officer,

Walmart US

As COO, now also oversees all

Walmart associates in addition

to leading small format strategy

and the Development Team

Previously EVP strategy and

international dev. for WMT

International (M&A, real estate,

format development)

Before, COO and CFO of

ASDA; as COO, oversaw

logistics, eCommerce, financial

services

Source: Company reports, Kantar Retail research and analysis

“Ignore [Neighborhood

Markets] at our peril” –Judith McKenna, June 2015

Julie Murphy

EVP, Neighborhood

Markets, Walmart US

Previously EVP and

President, Walmart West;

divisional SVP; and various

store operations positions

Replaced Mike Moore in

May 2015—Moore now

oversees Supercenters

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Julie Murphy

EVP, Neighborhood Markets,

Walmart US

Looking for More Autonomy for Merchants

Neighborhood Market structure has focused on ops

6

Steve Bratspies

Chief Merchant

Lea Jepson

Senior Director, Merchandising,

Small Formats

15-20+ reports,

and growing

PLUS: Market managers for

each district exclusively

focused on NMKTs

Larry Mahoney

SVP, Logistics

Marc Lieberman

VP, Small

Formats

Brian Hooper

VP, Real Estate

Small Formats

David Norman

SVP, Ops West

Glenda Fleming

SVP, Ops East

Regional VPs

Regional VPs

Source: Company reports, Kantar Retail research and analysis

Jesica Duarte

VP, Neighborhood

Market

Development

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

7

Fill-in Trips

Fresh

Fuel

Pharmacy

Pickup

Retooling Neighborhood Market

“There are opportunities for us to significantly update and improve things like

space allocations; adjacencies; ambience; navigation; and flow in both of our

formats. We’re working on this now” –Greg Foran, April 2015

Source: Kantar Retail research and analysis

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016 © Kantar Retail 2016

8

Shopper

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

68% 62%

9%

17%

3% 10%

28%

60%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Ja

n-0

7

Ma

r-0

7

Ma

y-0

7

Ju

l-0

7

Se

p-0

7

No

v-0

7

Ja

n-0

8

Ma

r-0

8

Ma

y-0

8

Ju

l-0

8

Se

p-0

8

No

v-0

8

Ja

n-0

9

Ma

r-0

9

Ma

y-0

9

Ju

l-0

9

Se

p-0

9

No

v-0

9

Ja

n-1

0

Ma

r-1

0

Ma

y-1

0

Ju

l-1

0

Se

p-1

0

No

v-1

0

Ja

n-1

1

Ma

r-1

1

Ma

y-1

1

Ju

l-1

1

Se

p-1

1

No

v-1

1

Ja

n-1

2

Ma

r-1

2

Ma

y-1

2

Ju

l-1

2

Se

p-1

2

No

v-1

2

Ja

n-1

3

Ma

r-1

3

Ma

y-1

3

Ju

l-1

3

Se

p-1

3

No

v-1

3

Ja

n-1

4

Ma

r-1

4

Ma

y-1

4

Ju

l-1

4

Se

p-1

4

No

v-1

4

Ja

n-1

5

Ma

r-1

5

Ma

y-1

5

Ju

l-1

5

Se

p-1

5

No

v-1

5

Ja

n-1

6

Walmart/Walmart Supercenter

Walmart.com

Neighborhood Market*

9

Neighborhood Market Needs to Recapture Trips

Amazon.com

Percent Shopped Walmart during Past Four Weeks, by Format

Analysis for Neighborhood Market is limited to states in which Neighborhood Market had a presence as of January 2016

Source: Kantar Retail ShopperScape® , January 2007- January 2016

Continued decline in Supercenter penetration, despite stores added

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

10

‒ Compared to Supercenter

shoppers, Neighborhood Market

shoppers…

Live in denser market areas

Are younger

More likely to be Hispanic,

African American

NMKT’s Shoppers Are Younger than the Supercenter’s

Shopper Profile: Past 4-Week Shoppers

Walmart SC Walmart NMKT

Annual HH Income

<$25k 27% 26%

$25k-$49.9k 27% 27%

$50k-$74.9k 18% 19%

$75k-$99.9k 11% 12%

$100k+ 17% 17%

Mean income $58,180 $58,720

Locale*

Rural 17% 9%

Small Town 21% 13%

Large Town 13% 15%

Suburban 36% 43%

Urban/City 13% 21%

Kids in HH Yes 28% 29%

No 73% 71%

Generation

Gen Y 20% 25%

Gen X 31% 32%

Boomers 38% 34%

Seniors 11% 9%

Mean age 49.3 46.8

Race/Ethnicity

White Non-Hispanic 68% 59%

Black Non-Hispanic 14% 17%

Hispanic 13% 17%

Analysis limited to states in which Neighborhood Market was present as of January 2016

Note: highlighting indicates significant difference between column percentages (95% confidence level)

Source: Kantar Retail ShopperScape®, January-December 2015

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

11

NMKT and Supercenter Shoppers Overlap

Cross-Shopping Between Walmart Banners (among past four week shoppers of retailers)

Analysis limited to states in which Neighborhood Market was present as of January 2016

Source: Kantar Retail ShopperScape®, January 2011-December 2015

Though over time NMKT shoppers become less likely to cross-shop the SC

73% 75%

67% 65% 64%

4% 5% 7% 8%

10%

2011 2012 2013 2014 2015

NMKT shopped SC SC shopped NMKT

2011-2015 % Change: -12% 2011-2015 % Change: +136%

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Describes experience

at NMKT

Describes experience

at Supercenter

Knowing that I'm paying a low price 59% 68%

Feeling like I got a "good deal" 57% 64%

Ability to get in and out quickly 53% 36%

Fast checkout 52% 45%

Store is clean and looks nice 49% 35%

Specific items I want being in-stock 46% 63%

Availability of high-quality fresh foods (e.g., meat, produce) 41% 51%

Availability of my favorite national brand products 39% 43%

Can get everything I need across a variety of categories 37% 31%

Availability of high-quality private label brands 30% 29%

Store associates are available and helpful if I need them 28% 23%

Good variety of pre-prepared "to-go" foods available 25% 26%

Fun and pleasant shopping experience 25% 24%

Offers unique products I can't find elsewhere 16% 15%

Ability to use the retailer's app on my smartphone while in the store to

make the shopping trip easier 14% 12%

Offers "meal solutions" to help me figure out what to buy/cook 13% 13%

Wide variety of organic products available 11% 13%

Opportunities to engage with products in the store (e.g., through

sampling stations, interactive displays, etc.) 4% 12%

12

For Shoppers, NKMT Beats Supercenter on Efficiency

Source: Kantar Retail ShopperScape®, May 2015

How Shoppers Describe the Shopping Experience at Walmart, by Format (among past four-week shoppers of each retailer)

Green=

NMKT is

better

Orange=

WMSC is

better

Legend

But lacks on some key convenience measures

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Describes experience

at NMKT

Describes experience

at Supercenter

Knowing that I'm paying a low price 59% 68%

Feeling like I got a "good deal" 57% 64%

Ability to get in and out quickly 53% 36%

Fast checkout 52% 45%

Store is clean and looks nice 49% 35%

Specific items I want being in-stock 46% 63%

Availability of high-quality fresh foods (e.g., meat, produce) 41% 51%

Availability of my favorite national brand products 39% 43%

Can get everything I need across a variety of categories 37% 31%

Availability of high-quality private label brands 30% 29%

Store associates are available and helpful if I need them 28% 23%

Good variety of pre-prepared "to-go" foods available 25% 26%

Fun and pleasant shopping experience 25% 24%

Offers unique products I can't find elsewhere 16% 15%

Ability to use the retailer's app on my smartphone while in the store to

make the shopping trip easier 14% 12%

Offers "meal solutions" to help me figure out what to buy/cook 13% 13%

Wide variety of organic products available 11% 13%

Opportunities to engage with products in the store (e.g., through

sampling stations, interactive displays, etc.) 4% 12%

13

For Shoppers, NKMT Beats Supercenter on Efficiency

Source: Kantar Retail ShopperScape®, May 2015

How Shoppers Describe the Shopping Experience at Walmart, by Format (among past four-week shoppers of each retailer)

Green=

NMKT is

better

Orange=

WMSC is

better

Legend

But lacks on some key convenience measures

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Extremely/somewhat

important when shopping

Describes experience

at NMKT

PPT Diff

(Actual – Ideal)

Knowing that I'm paying a low price 86% 59% -27.1

Availability of high-quality fresh foods 85% 41% -43.9

Feeling like I got a "good deal" 83% 57% -25.8

Fast checkout 81% 52% -29.5

Store is clean and looks nice 81% 49% -32.6

Can get everything I need across a variety of categories 81% 37% -44.0

Specific items I want being in-stock 80% 46% -33.5

Ability to get in and out quickly 78% 53% -25.5

Availability of my favorite national brand products 70% 39% -31.1

Store associates are available and helpful if I need them 68% 28% -40.0

Fun and pleasant shopping experience 64% 25% -39.1

Availability of high-quality private label brands 52% 30% -22.3

Offers unique products I can't find elsewhere 42% 16% -25.4

Good variety of pre-prepared "to-go" foods available 38% 25% -12.9

Wide variety of organic products available 34% 11% -22.5

Opportunities to engage with products in the store (e.g.,

through sampling stations, interactive displays, etc.) 28% 4%

-23.6

Offers "meal solutions" to help me figure out what to buy/cook 26% 13% -12.5

Ability to use the retailer's app on my smartphone while in the

store to make the shopping trip easier 20% 14%

-6.6

14

Overall, Big Gaps Between Expectations and NMKT’s

Delivery of Fresh, Service, Variety

Source: Kantar Retail ShopperScape®, May 2015

Ideal Shopping Experience vs. Experience at Neighborhood Market (among past four-week Neighborhood Market shoppers)

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016 © Kantar Retail 2016

15

Assortment

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

16

Fill-in Trips

Fresh

Fuel

Pharmacy

Pickup

Recapturing the Fill-In Trip

Source: Kantar Retail research and analysis

Redirecting the “mass” model

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

17

Food Merchandise Ladder

Source: Kantar Retail store visits and analysis, 2016

Half as many SKUs at Neighborhood Market, but higher proportion of

smaller sizes

Fill-in Trips

Mustard

Assortment:Neighborhood Market Supercenter

% Private Label 22% 23%

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Non-Edible Grocery Ladder: Paper Towels

SKU culling, more thoughtful pack sizes at NMKT

18

Source: Kantar Retail store visits and analysis

Fill-in Trips

Paper Towels

Assortment:Neighborhood Market Supercenter

% Private Label 28% 28%

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

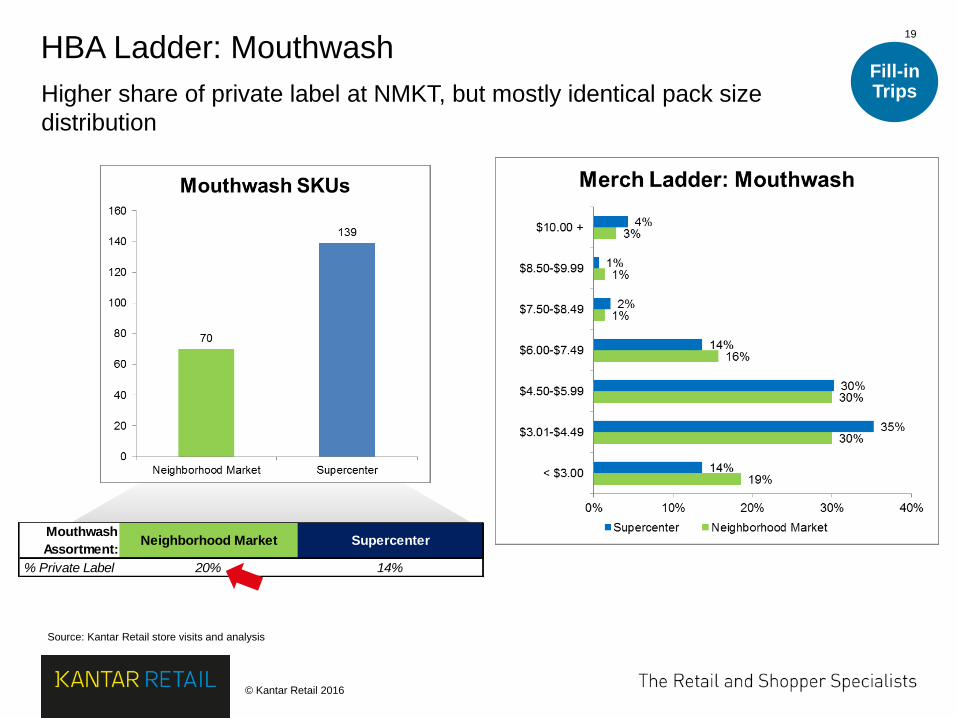

HBA Ladder: Mouthwash

Higher share of private label at NMKT, but mostly identical pack size

distribution

19

Fill-in Trips

Source: Kantar Retail store visits and analysis

Mouthwash

Assortment:Neighborhood Market Supercenter

% Private Label 20% 14%

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Private Label Initiatives Crystallize at NMKT

Elevating brand, emphasizing quality; central to operating model

20

Best

Basic

Fill-in Trips

Source: Kantar Retail store visits

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

21

Adult Beverages Are a Trip Driver

Clear fill-in, quick trip role; create excitement Fill-in Trips

Creating excitement,

solutions

Source: Kantar Retail store visits

Shelf guidance for

types of beer,

suggested food

pairings for wine

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Co-merchandising Encourages Routine, Impulse Solutions 22

Fill-in Trips

Moving fresh

through the store

Source: Kantar Retail store visits

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

23

General Merchandise Becoming a Better Complement

Using Pickup to extend the aisle Fill-in Trips

Source: Kantar Retail store visits

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016 © Kantar Retail 2016

24

Prototype

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Go-Ahead Prototype Floor Plan

Walnut St., Rogers, AR

25

Including self-

checkouts

Drinks To Go

station

Source: Kantar Retail store visits, company reports

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

26

Rogers Prototype Store Revolves Around Fresh

Low sightlines, layout give full view of perishables on entry Fresh

Source: Kantar Retail store visits

“We’ve seen fresh penetration expand in this store

[prototype] relative to its peers.” –Greg Foran, November 2015

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

27

Meat Moves Up Front, Produce Artfully Displayed Fresh

Source: Kantar Retail store visits

“We’re encouraged by our newest prototype,

which features better sightlines and displays.” –Greg Foran, November 2015

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Deli and Bakery Elevate Fresh, Quick Trip Message 28

Fresh

“All Neighborhood Markets… will open up with a bakery and a deli because we

absolutely believe that’s important in the future” –Judith McKenna, April 2015

Source: Kantar Retail store visits

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Stores Within the Store Add Meaning to Assortment

Tapping into special health needs, young families

29

Fill-in Trips

Source: Kantar Retail store visits

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

Grocery Pickup Is Expanding to NMKT

Online grocery could be key cog in quick-trip message

30

Pickup

• Curbside grocery pickup

now available in 20

markets, across Walmart

formats; adding another

20 in 2016

• Features drive-up kiosks

for calling up an order

and parking spaces

where orders can be

loaded

Marketing in-store

reminds shoppers of

online grocery option

Source: Kantar Retail store visits

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016 © Kantar Retail 2016

31

Competition: Spotlight on Publix

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

32

Recapturing the Fill-In Trip in the Portfolio

NMKT

Pressure continues on “mass” model

Source: Kantar Retail research and analysis

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

33

Neighborhood Market’s Supermarket Competitive Set

Varies by Region

Top Grocery Retailers Also Shopped by Neighborhood Market Shoppers, by Region

West

Walmart/WMSC 59%

Costco 46%

Safeway 33%

Trader Joe’s 32%

Albertsons 28%

WinCo Foods 23%

Southwest

Walmart/WMSC 75%

Kroger 31%

Albertsons 30%

Sam’s Club 28%

Sprouts 22%

H-E-B 21%

Northeast

Walmart/WMSC 64%

Food Lion 30%

ALDI 27%

Sam’s Club 21%

Kroger 20%

Trader Joe’s 17%

Central

Walmart/WMSC 83%

Sam’s Club 35%

ALDI 32%

Hy-Vee 20%

Kroger 15%

Whole Foods 13%

Southeast

Walmart/WMSC 74%

Publix 61%

Winn-Dixie 39%

Sam’s Club 25%

ALDI 20%

Costco 15%

Source: Kantar Retail ShopperScape®, January-December 2015

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

34

Fill-in Trips

Fresh

Fuel

Pharmacy

Pickup

Where Can NMKT Learn from Competitors?

Keeping in mind NMKT’s points of focus “When we are up against

someone who is really

good at running

supermarkets, frankly

our fresh offering has

not been on par with

what it takes to win.” –Greg Foran, October 2015

Source: Kantar Retail research and analysis

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

35

Source: Aggdata, Kantar Retail analysis

Case Study: Neighborhood Market vs. Publix

March 2015, Tampa, FL

40% are within

2 miles of a Publix

Charlotte

Miami

Jacksonville

Atlanta

Lakeland

(rest of Florida)

Among the Neighborhood

Markets in the six states

Publix has a presence…

53% are within

5 miles

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

36

‒ March 2015, Tampa, FL

‒ Basket of 12 fresh items, 16

grocery items, 12 HBA items

‒ Neighborhood Market was

less expensive in all three

sub-baskets

Biggest differential in fresh

Only three items cheaper at

Publix overall

‒ No Rollbacks, 3 sale items at

Publix

Neighborhood Market vs. Publix: A Price Comparison

Source: Kantar Retail store visits

Segment Product Brand NMKT Publix Index

(Publix-NMKT)

Raspberries - - $2.78 $4.49 162

Bread 100% Whole Wheat (Whole Grain) Arnold $2.98 $4.29 144

Chicken breast Perfect Portions Fresh Perdue $6.98 $8.99 129

Hot dogs Bun-sized premium beef franks Oscar Mayer $3.98 $4.99 125

Tomatoes Cherry Campari $2.48 $2.99 121

Apples Granny Smith - $1.67 $1.99 119

Bananas - - $0.59 $0.69 117

Cheese Provolone Land O' Lakes $3.98 $4.39 110

Butter Salted - 4 sticks Land O' Lakes $3.96 $4.29 108

Bacon Black label original Hormel $4.78 $4.99 104

Orange Juice Homestyle, Some Pulp Tropicana $3.98 $3.99 100

Grapes Green - $2.98 $1.99 67

Glass Cleaner Regular Windex $2.83 $3.99 141

Ice Cream

French Vanilla, Cardboard cartoon, tub - black

label Breyers $3.94 $5.49 139

Cereal Corn Flakes Kellogg's $2.98 $3.99 134

Canned Tuna Chunk Light, packed in water, can Starkist $0.75 $0.99 132

Pasta (dry) Angel Hair Barilla $1.38 $1.69 122

Diapers Little Snugglers - size 2 Huggies $8.97 $10.49 117

Soap Pads Steel Wool pads - Lemon S.O.S. $1.88 $2.19 116

Foil Heavy Duty Aluminum Foil Reynold's $5.92 $6.79 115

Soda Cans - fridge pack Coca-Cola Classic $4.48 $4.99 111

Soup Chicken Noodle Campbell's $0.88 $0.97 110

Infant Formula Sensitive, for Fussiness and Gas, with Iron Similac $24.98 $26.99 108

Dog Food Adult Complete Nutrition Pedigree $12.97 $13.99 108

Ketchup Plain, Squeeze bottle - inverted Heinz $2.22 $2.39 108

Wipes Disinfecting Wipes, Fresh Scent Clorox $4.63 $4.79 103

Laundry Soap 64 loads Tide $11.97 $11.99 100

Baby Food

plastic jar - strained Peas "All Natural", 2nd

foods Gerber $1.08 $1.07 99

Hand Soap Crisp Cucumber and Melon Softsoap $0.98 $1.79 183

Vitamins Gummy Vites, Complete - natural flavor Lil Critters $3.98 $5.49 138

Floss Satin Complete - mint Oral B $2.27 $2.99 132

Hair Coloring Colorsilk - Beautiful Revlon $2.97 $3.79 128

Razors Women's - Hydro Silk, 3 Razors, 5 blades Schick $9.97 $12.49 125

Antiobiotic

Ointment Plus Pain Relief antibiotic cream, tube Neosporin $4.44 $5.39 121

Mouthwash Cool Mint Listerine $5.97 $6.99 117

Diaper Cream Rapid Relief Diaper Rash Cream - Blue tube Desitin $5.27 $5.89 112

Painkiller Ibuprofen, 200 Mg Advil $5.94 $6.29 106

Shampoo Dandruff Shampoo - Classic Clean

Head and

Shoulders $7.26 $7.49 103

Eye Makeup

Remover Oil-Free, blue bottle (liquid) Neutrogena $6.47 $6.49 100

Shaving Gel Extra Moisture Gel, with Vit. E Edge $2.97 $2.55 86

Total $150.35 $170.44 113

NMKT Publix

Index

(Publix-

NMKT)

Fresh basket 42.44$ 50.08$ 118

Grocery 91.86$ 102.80$ 112

HBA 58.49$ 67.64$ 116

Total 150.35$ 170.44$ 113

March 2015 Results

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

37

Within Categories, Publix’s Average Prices Are Higher Too

What is the price differential worth to shoppers?

Source: Kantar Retail store visits and analysis

NMkt Publix NMkt Publix NMkt Publix

% Private

Label26% 18% 9% 13% 11% 13%

Retailer Merch Ladders

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

38

But Publix Is Strong in the Perimeter and in Service

Fresh is throughout the store, cross-merchandising guides the shopper

Source: Kantar Retail store visits

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

39

‒ Perishables, fresh continue to elevate

Investment on the rise as shoppers demand it

‒ Driving differentiation with departments

Greater importance on categories and merchandising

placement

‒ Keying on digital, not just eCommerce

Online grocery will become a more important factor

‒ The wild card: Lidl

Where price and assortment will be center stage

Source: Kantar Retail research and analysis

Competition Will Necessarily Go Beyond Price

New thinking, new innovation driving differentiation in marketplace

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016 © Kantar Retail 2016

40

Conclusion and Supplier To-Dos

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

41

Is Walmart Differentiating This Format?

A closer look at the “Neighborhood” message

Selection

emphasizes local ties

“Available at your local

Supercenter and

Neighborhood Market”

Some attention to local connection,

distinguishing the store… …Marketing largely remains parallel

with the Supercenter

Ad is the same as at the

Supercenter Source: Kantar Retail store visits

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

42

Neighborhood Market’s Prospects: To-Dos for Suppliers

Source: Kantar Retail research and analysis

‒ Add or delete points as

needed by inserting or

deleting rows

‒ Align with the image

‒ Reach out to creative for

assistance if needed

Replace w/

topical image or

reach out to

creative 1

Resources: • Evaluate your team size and structure, including roles in category

management, supply chain, analytics, and marketing.

• Capitalize on expertise already in your company around BIC

supermarkets and other small formats (e.g., drug).

• Include these teams in joint business planning.

2

Differentiation: • Build merchandising skills outside the pallet, selling off the shelf.

• Dedicate resources to assortment and endcap planning for this format.

• Craft solutions at Neighborhood Market that are different from the

Supercenter, especially focused on to-go and fill-in trip missions.

3

Prototype-driven growth: • Target merchandising that orients around fresh and perishables.

• Develop an online grocery and broader assortment Pickup strategy to

build baskets and send the convenience message.

• Link solutions with services to highlight the convenience message.

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

At this two-day workshop, our Walmart and Sam’s Club experts will dig into the retailers’ efforts to

significantly evolve their propositions for a rapidly changing and demanding shopper base, and will

deliver implications for suppliers’ business planning and growth opportunities.

Kantar Retail

Walmart & Sam's Club Workshop

© Kantar Retail 2016

Apr 5-6, 2016 Bentonville, AR

You’ll walk away from this Workshop with:

‒ Forecasts for Walmart’s store expansion and sales

growth heading into the end of the decade

‒ Insights into where Walmart is investing to drive

relevance and what the retailer will demand from

suppliers as investments continue to pressure profits

‒ Understanding of the extent, purpose, and plausibility of

Sam’s current member and merchandise evolution

through 2020

Featuring Kantar Retail Experts:

Laura Kennedy, Director

David Marcotte, SVP

Leon Nicholas, SVP & Knowledge Officer

Sara Al-Tukhaim, Director

Tim Campbell, Jr. Analyst

Page Title 8.80

Lower content limit 7.03

Bottom margin 7.86

Content start 6.08

© Kantar Retail 2016

For further information please refer to

KantarRetailiQ.com

Contact:

Laura Kennedy

Director

T: +1 (617) 912 2851

@LauraWK_KR

@kantarretail

Leon Nicholas

SVP and Knowledge Officer

T: +1 (617) 912 2871

@leonnicholas7

![LETTERS OF THOMAS BOYLSTON ADAMS TO WILLIAM SMITH … · 2015. 2. 25. · 1917.] Letters of Thomas Boylston Adams. 83 LETTERS OF THOMAS BOYLSTON ADAMS TO WILLIAM SMITH SHAW,i 1799-1823](https://img.pdfslide.net/doc/110x75/60c2fe4bae365105fe6d301c/letters-of-thomas-boylston-adams-to-william-smith-2015-2-25-1917-letters.jpg)