Embed Size (px)

Citation preview

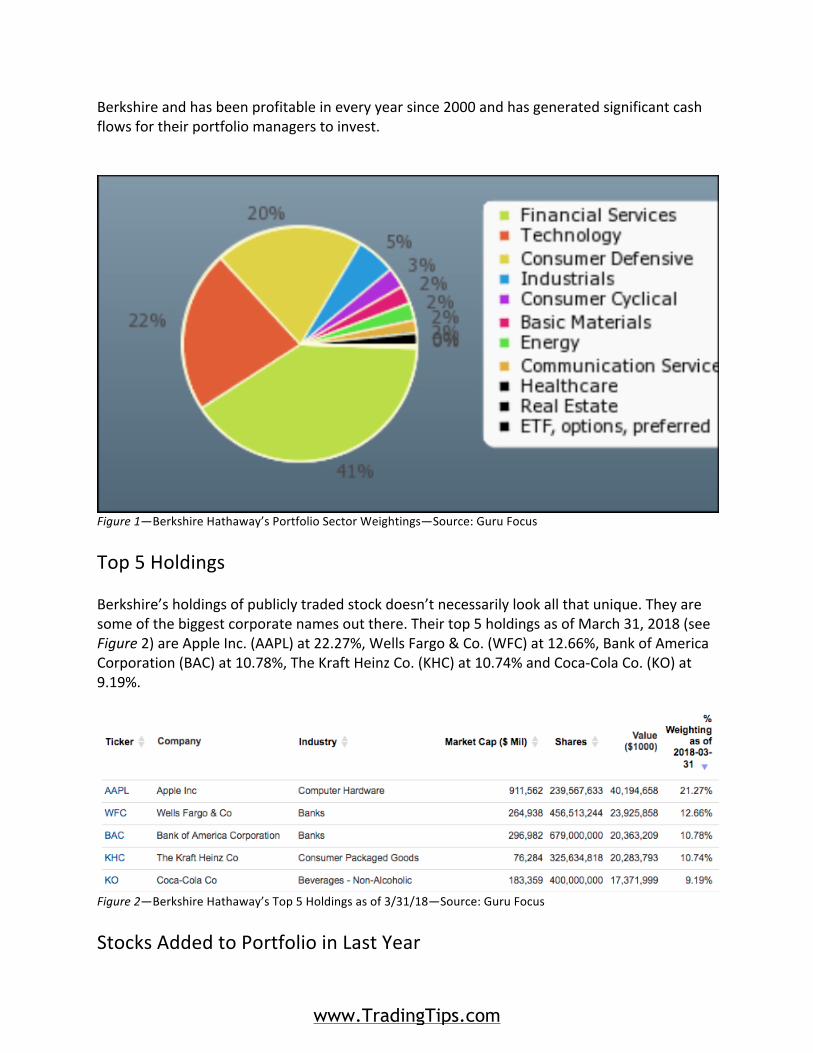

WarrenBuffettisknownasthe“OracleofOmaha”forareason,he’sthemostsuccessfulinvestorinhistory.Currently,he’srankedthirdontheForbestop20billionaire’slistwithanetworthof$84billion.Heisthesonofaformercongressmanandboughthisfirststockattheageof11.Inthisreport,we’regoingtolookatthehistoryofWarrenBuffettandBerkshireHathaway,reviewhisinvestmentphilosophyandanalyze5ofBerkshire’stopholdingsandrecentadditionsforsomeofthebestvalueopportunitiesinthemarket.HistoryWarrenBuffettisknownasastudentofBenjaminGraham,thefatherofvalueinvesting.HewasastudentofGraham’swhileattendingcollegeatColumbia,andthenworkedforGraham-Newmanafterhegraduatedasaninvestmentsalesman.BuffettworkedforGrahamuntilhisretirementandthenstartedapartnershipwithclosefriendsandfamily.BuffettappliedthevalueprinciplesthathelearnedfromGrahamwhenhebeganinvestinginBerkshireHathaway,atextilecompany,in1962.Afterrealizingthatthecompanyneededachangeinmanagement,hebeganpurchasingmoreshares.AfteracquiringBerkshireHathaway,BuffettusedthecompanyasaholdingcompanytobuyNationalIndemnityCompanyandthenuseditscashflowtofinanceotheracquisitions.BuffettiscurrentlythechairmanandCEOofBerkshireHathaway,whichhasownershipinterestin46differentcompanieswithatotalvalueofnearly$190billion.InvestmentPhilosophyBuffett’sinvestmentphilosophycentersonthreebasictenets:lookatthestockasabusiness,usethemarket’sfluctuationstoyouradvantageandseekamarginofsafety.Hewillnotinvestinbusinessesthathedoesn’tunderstandandwon’tconsidercompaniesthathaven’tbeenaroundfor10years.Hefeelsthatacompanythatoffersaqualityproductatagoodpricewithanhonest,reliablemanagementisagoodcompany.Buffettalsocoinedtheterm,“economicmoat.”Thisconcepthasgainedmorebroad-basedappealsinceitwasendorsedbyhimandconjuresupimagerymoatsthatwerebuilttoprotectcastlesfromtheirenemies.Theideaistolookforcompaniesthathaveadurablecompetitiveadvantage.Theadvantagecouldbebasedontheabilitytoproduceatalowercostthantheircompetitors,astrongbrand,barrierstoentry,recurringrevenuestreams,networkeffects,etc.PortfolioSectorWeightingsInFigure1below,you’llseeabreak-downofBerkshireHathaway’sportfolioallocationbysector.Theyareheavilyinvestedinthefinancialservices,technologyandconsumerdefensivesectors.The41percentweightingtofinancialservicesmakessensegivenBerkshire’shistoryofusingcashflowfromonebusinesstoinvestinotherbusinesses.GEICOisafinancialholdingof

www.TradingTips.com

Berkshireandhasbeenprofitableineveryyearsince2000andhasgeneratedsignificantcashflowsfortheirportfoliomanagerstoinvest.

Figure1—BerkshireHathaway’sPortfolioSectorWeightings—Source:GuruFocusTop5HoldingsBerkshire’sholdingsofpubliclytradedstockdoesn’tnecessarilylookallthatunique.Theyaresomeofthebiggestcorporatenamesoutthere.Theirtop5holdingsasofMarch31,2018(seeFigure2)areAppleInc.(AAPL)at22.27%,WellsFargo&Co.(WFC)at12.66%,BankofAmericaCorporation(BAC)at10.78%,TheKraftHeinzCo.(KHC)at10.74%andCoca-ColaCo.(KO)at9.19%.

Figure2—BerkshireHathaway’sTop5Holdingsasof3/31/18—Source:GuruFocusStocksAddedtoPortfolioinLastYear

www.TradingTips.com

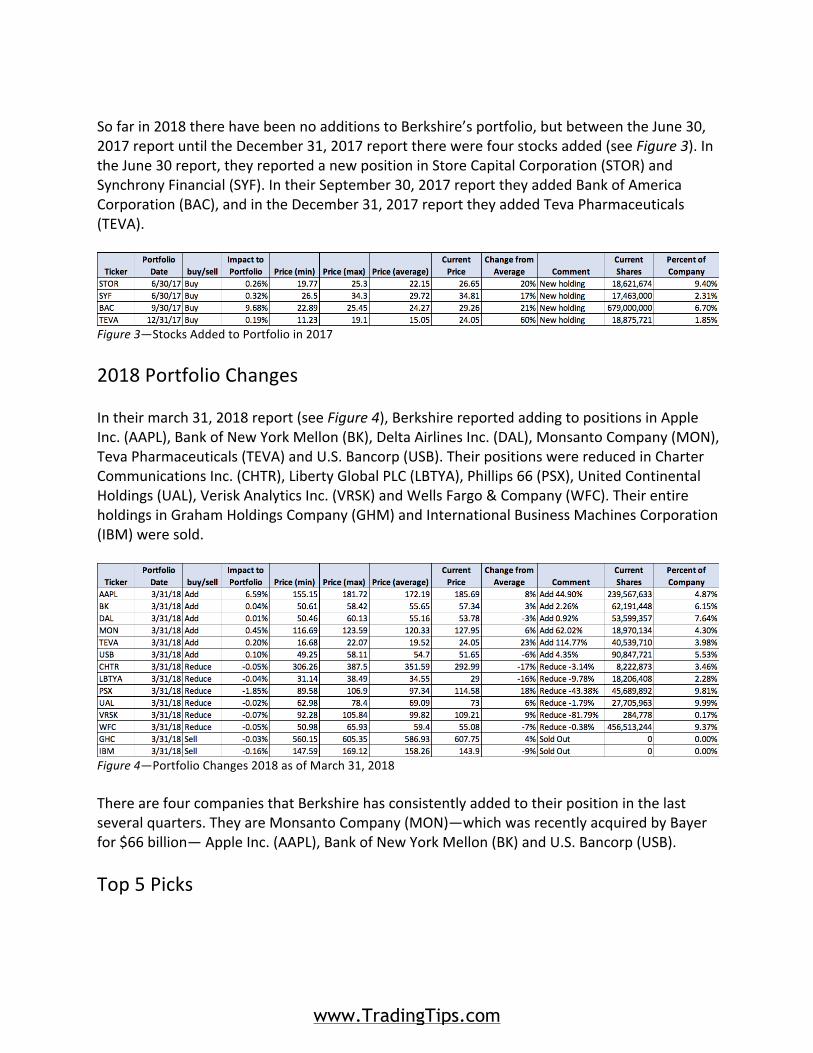

Sofarin2018therehavebeennoadditionstoBerkshire’sportfolio,butbetweentheJune30,2017reportuntiltheDecember31,2017reporttherewerefourstocksadded(seeFigure3).IntheJune30report,theyreportedanewpositioninStoreCapitalCorporation(STOR)andSynchronyFinancial(SYF).IntheirSeptember30,2017reporttheyaddedBankofAmericaCorporation(BAC),andintheDecember31,2017reporttheyaddedTevaPharmaceuticals(TEVA).

Figure3—StocksAddedtoPortfolioin20172018PortfolioChangesIntheirmarch31,2018report(seeFigure4),BerkshirereportedaddingtopositionsinAppleInc.(AAPL),BankofNewYorkMellon(BK),DeltaAirlinesInc.(DAL),MonsantoCompany(MON),TevaPharmaceuticals(TEVA)andU.S.Bancorp(USB).TheirpositionswerereducedinCharterCommunicationsInc.(CHTR),LibertyGlobalPLC(LBTYA),Phillips66(PSX),UnitedContinentalHoldings(UAL),VeriskAnalyticsInc.(VRSK)andWellsFargo&Company(WFC).TheirentireholdingsinGrahamHoldingsCompany(GHM)andInternationalBusinessMachinesCorporation(IBM)weresold.

Figure4—PortfolioChanges2018asofMarch31,2018TherearefourcompaniesthatBerkshirehasconsistentlyaddedtotheirpositioninthelastseveralquarters.TheyareMonsantoCompany(MON)—whichwasrecentlyacquiredbyBayerfor$66billion—AppleInc.(AAPL),BankofNewYorkMellon(BK)andU.S.Bancorp(USB).Top5Picks

www.TradingTips.com

NowthatwehaveanunderstandingofhowWarrenBuffettinvestsandsomeofthecompanieshe’sinvestedin,let’slookatsomeoftheopportunitiesrightnowtoinvestin.HerearethetopfivetradingopportunitiesfromtheportfolioofBerkshireHathaway.1. AppleInc.(AAPL)Price:$185.10DividendYield:1.57%MarketCap:$911.56billionEnterpriseValue:$945.46billionBusinessSummaryAppleInc.designs,manufactures,andmarketsmobilecommunicationandmediadevices,andpersonalcomputerstoconsumers,andsmallandmid-sizedbusinesses;andeducation,enterprise,andgovernmentcustomersworldwide.Thecompanyalsosellsrelatedsoftware,services,accessories,networkingsolutions,andthird-partydigitalcontentandapplications.Apple Inc. was founded in 1977 and is headquartered in Cupertino, California. Earnings&RevenueHistoryInthelast5quartersAAPLhasbeatenboththetoplinerevenueestimatesandthebottomlineearningsestimates.Inthemostrecentquarteritsawyear-overyearrevenueandearningsgrowthandhasafive-yearprojectedearningsgrowthrateof13.76%.AAPLhasgrowntheirearningsinthelast5yearsata6.36%annualgrowthrateandgrewrevenueata7.93%growthrate.Theearningsgrowthrateiswellbelowtheindustryaverageof13.10%andthesectoraveragegrowthrateof11.84%.However,revenueshavegrownatamuchfasterpacethantheindustryat3.57%andsectorat5.08%.ValuationRatiosPrice-to-Earnings(P/E):17.90Price-to-Book(P/B):7.23EnterpriseValuetoEBITDA(EV/EBITDA):11.60ThecurrentP/EratioforAAPLis17.90,whichisslightlyhigherthanthemedianP/Eof15.4overthelast10yearsandislowerthanthemedianvalueof21.22forthecompaniesintheconsumerelectronicsindustry.ItscurrentP/Bishigherthanits10-yearmedianvalueof5.19,whichishigherthanthemedianvalueof1.93forthecompaniesinitsindustry.TheEV/EBITDAisslightlyabovethemedianvalueof9.8butisslightlybelowtheindustrymedianof12.27.Onarelativebasiscomparedtoitsownhistoryandthecurrentvaluesoftheindustry,AAPL’svaluationratiosbetterthanitsownhistoryandprettyclosetothemedianvaluefortheindustry.

www.TradingTips.com

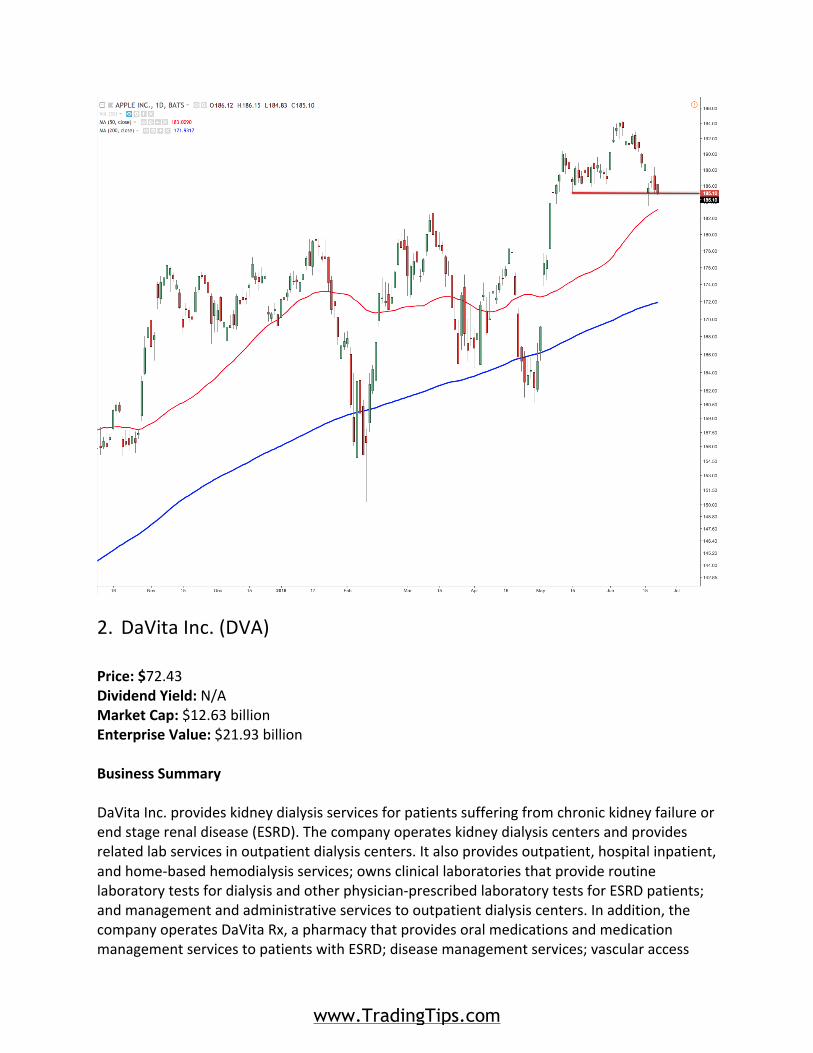

ProfitabilityandGrowthReturnonEquity(ROE):39.93%ReturnonAssets(ROA):14.57%ReturnonCapital(ROC):223.97%3-yearRevenueGrowthRate:13.50%3-yearEBITDAGrowthRate:13%ThecurrentvalueforROEisabovethe10-yearmedianvalueof36.08%butishigherthan96%ofitsindustrywithamedianvalueof6.95.ItsROAisbelowits10-yearmedianvalueof19.79butishigherthan93%oftheindustrywithamedianvalueof3.44%.ItsROCislowerthanits10-yearmedianvalueof364.21butissignificantlyhigherthantheindustrymedianof12.37.AAPLs3-yeargrowthratesareclosetothemedianvalueforthepast10-yearsbutissignificantlyhigherthantheindustry.WhileAAPLsnumbersforprofitabilityandgrowthdon’tnecessarilyjumpoffthepagewhencomparedtoitselfhistorically,whencomparedtoitsindustryitdoesreallywell.PricePerformanceThe52-weekchangeforAAPLis27.50%withthe52-weekhighat$194.20andits52-weeklowat$142.28.ThebetaforAAPLisslightlyhigherthantheS&P500at1.15andits3-monthaveragevolumeis29.73million.AAPLiscurrentlytradingabovebothits50-dayand200-dowsimplemovingaverages.Bothaveragesarerising,whichindicativeofanintermediatetermandlong-termuptrend.Thepricehasexperiencedrecentweaknessasithasnearedthe50-dayat$183,butinthepastfourdayshasheldontoitspreviouslowaround185.41.Ifthatlevelisbroken,theprice’snextlevelsofsupportcomeataround$179andthen$168.Asavalue-orientedinvestor,thelowerpriceandhigheryieldimprovesthelong-termprospectsofaninvestment,allthingsbeingequal.

www.TradingTips.com

2. DaVitaInc.(DVA)Price:$72.43DividendYield:N/AMarketCap:$12.63billionEnterpriseValue:$21.93billionBusinessSummaryDaVitaInc.provideskidneydialysisservicesforpatientssufferingfromchronickidneyfailureorendstagerenaldisease(ESRD).Thecompanyoperateskidneydialysiscentersandprovidesrelatedlabservicesinoutpatientdialysiscenters.Italsoprovidesoutpatient,hospitalinpatient,andhome-basedhemodialysisservices;ownsclinicallaboratoriesthatprovideroutinelaboratorytestsfordialysisandotherphysician-prescribedlaboratorytestsforESRDpatients;andmanagementandadministrativeservicestooutpatientdialysiscenters.Inaddition,thecompanyoperatesDaVitaRx,apharmacythatprovidesoralmedicationsandmedicationmanagementservicestopatientswithESRD;diseasemanagementservices;vascularaccess

www.TradingTips.com

services;clinicalresearchprograms;physicianservices;anddirectprimarycareservices.ThecompanywasformerlyknownasDaVitaHealthCarePartnersInc.andchangeditsnametoDaVitaInc.inSeptember2016.DaVitaInc.wasfoundedin1994andisheadquarteredinDenver,Colorado.Earnings&RevenueHistoryInthelast5quartersDVAhasbeatenboththetoplinerevenueestimatesandthebottomlineearningsestimates.Inthemostrecentquarteritsawyear-overyearearningsgrowth,butrevenuesfell.Ithasafive-yearprojectedearningsgrowthrateof23%.DVAhasgrowntheirearningsinthelast5yearsata4.64%annualgrowthrateandgrewrevenueata5.85%growthrate.Theearningsgrowthrateiswellbelowtheindustryaverageof7.31%andthesectoraveragegrowthrateof8.04%.However,revenueshavealsogrownataslowerratethantheindustryat13.76%andsectorat7.89%.ValuationRatiosPrice-to-Earnings(P/E):33.98Price-to-Book(P/B):2.83EnterpriseValuetoEBITDA(EV/EBITDA):14.68ThecurrentP/EratioforDVAis33.98,whichisalmostdoublethemedianP/Eof18.4overthelast10yearsandisgreaterthanthemedianP/Eof27.31fortheMedicalCareindustry.ItscurrentP/Bislowerthanits10-yearmedianvalueof3.11,whichisclosetotheindustrymedianof2.64.TheEV/EBITDAishigherthemedianvalueof9.2butisbelowtheindustrymedianof15.23.Onarelativebasiscomparedtoitsownhistoryandthecurrentvaluesoftheindustry,DVAsvaluationratiosaremixed.ProfitabilityandGrowthReturnonEquity(ROE):8.13%ReturnonAssets(ROA):2.06%ReturnonCapital(ROC):14.65%3-yearRevenueGrowthRate:-1.20%3-yearEBITDAGrowthRate:8.60%ThecurrentvalueforROEisbelowthe10-yearmedianvalueof18.33%butisslightlyhigherthantheindustrymedianvalueof8.03%.ItsROAisbelowits10-yearmedianvalueof4.51andislowerthantheindustrymedianvalueof3.48%.ItsROCislowerthanits10-yearmedianvalueof63.2%butisslightlylowerthantheindustrymedianof14.91%.DVAs3-yeargrowthratesarebelowmedianvalueforthepast10-yearsandisbelowtheindustryforrevenuegrowthandaboveitforEBITDAgrowth.

www.TradingTips.com

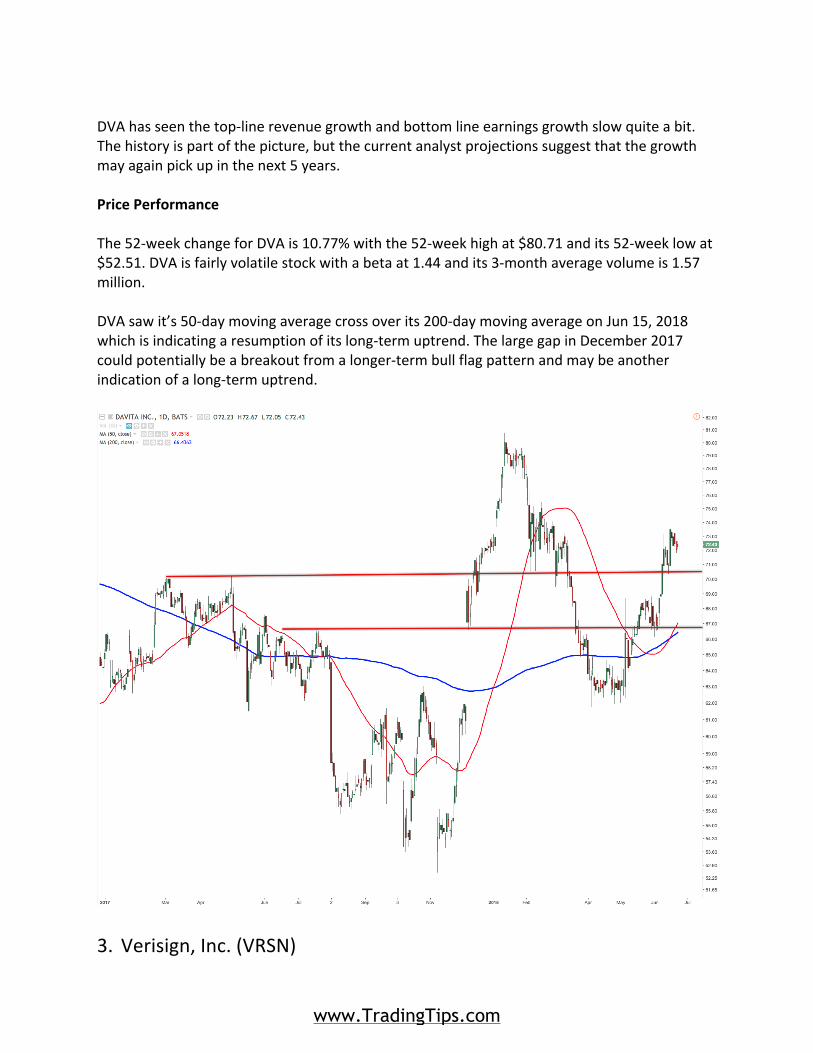

DVAhasseenthetop-linerevenuegrowthandbottomlineearningsgrowthslowquiteabit.Thehistoryispartofthepicture,butthecurrentanalystprojectionssuggestthatthegrowthmayagainpickupinthenext5years.PricePerformanceThe52-weekchangeforDVAis10.77%withthe52-weekhighat$80.71andits52-weeklowat$52.51.DVAisfairlyvolatilestockwithabetaat1.44andits3-monthaveragevolumeis1.57million.DVAsawit’s50-daymovingaveragecrossoverits200-daymovingaverageonJun15,2018whichisindicatingaresumptionofitslong-termuptrend.ThelargegapinDecember2017couldpotentiallybeabreakoutfromalonger-termbullflagpatternandmaybeanotherindicationofalong-termuptrend.

3. Verisign,Inc.(VRSN)

www.TradingTips.com

Price:$139.50DividendYield:N/AMarketCap:$17.17billionEnterpriseValue:$17.23billionBusinessSummaryVeriSign,Inc.providesdomainnameregistryservicesandInternetsecurityworldwide.Thecompanyoffersregistryservicesthatoperatetheauthoritativedirectoryof.com,.net,.cc,.tv,.gov,.jobs,.edu,.name,andotherdomainnames.Itsregistryservicesallowindividualsandorganizationstoestablishtheironlineidentities.Thecompanyalsoprovidesinfrastructureassuranceservices,includingdistributeddenialofserviceprotectionandmanageddomainnamesystemservices.Itservesfinancialinstitutions,software-as-a-serviceproviders,e-commerceproviders,andmediacompaniesthroughdirectsalesandindirectchannels.Thecompanywasfoundedin1995andisheadquarteredinReston,Virginia.Earnings&RevenueHistoryInthelast5quartersVRSNhasbeatenboththetoplinerevenueestimatesandthebottomlineearningsestimates.Inthemostrecentquarteritsawyear-overyearearningsandrevenuegrowth.DVAhasgrowntheirearningsinthelast5yearsata14.52%annualgrowthrateandgrewrevenueata5.93%growthrate.Theearningsgrowthrateisabovetheindustryaverageof8.57%butbelowthesectoraveragegrowthrateof17%.Revenueshavegrownatafasterratethanthesectorat5.09%%butbelowtheindustryat7.88%.ValuationRatiosPrice-to-Earnings(P/E):36.33Price-to-Book(P/B):N/AEnterpriseValuetoEBITDA(EV/EBITDA):21.51ThecurrentP/EratioforVRSNis36.33,whichisabovethemedianP/Eof24.7overthelast10yearsandisslightlyhigherthanthemedianP/Eof33.49fortheInternetContent&Informationindustry.TheEV/EBITDAishigherthanthemedianvalueof14.6andishigherthantheindustrymedianof18.26.Thebookvaluecannotbecalculatedbecauseofthenegativeequityonthebalancesheet.Onarelativebasiscomparedtoitsownhistoryandthecurrentvaluesoftheindustry,VRSNsvaluationratiosaremoderatelyhigh.ProfitabilityandGrowthReturnonEquity(ROE):N/A

www.TradingTips.com

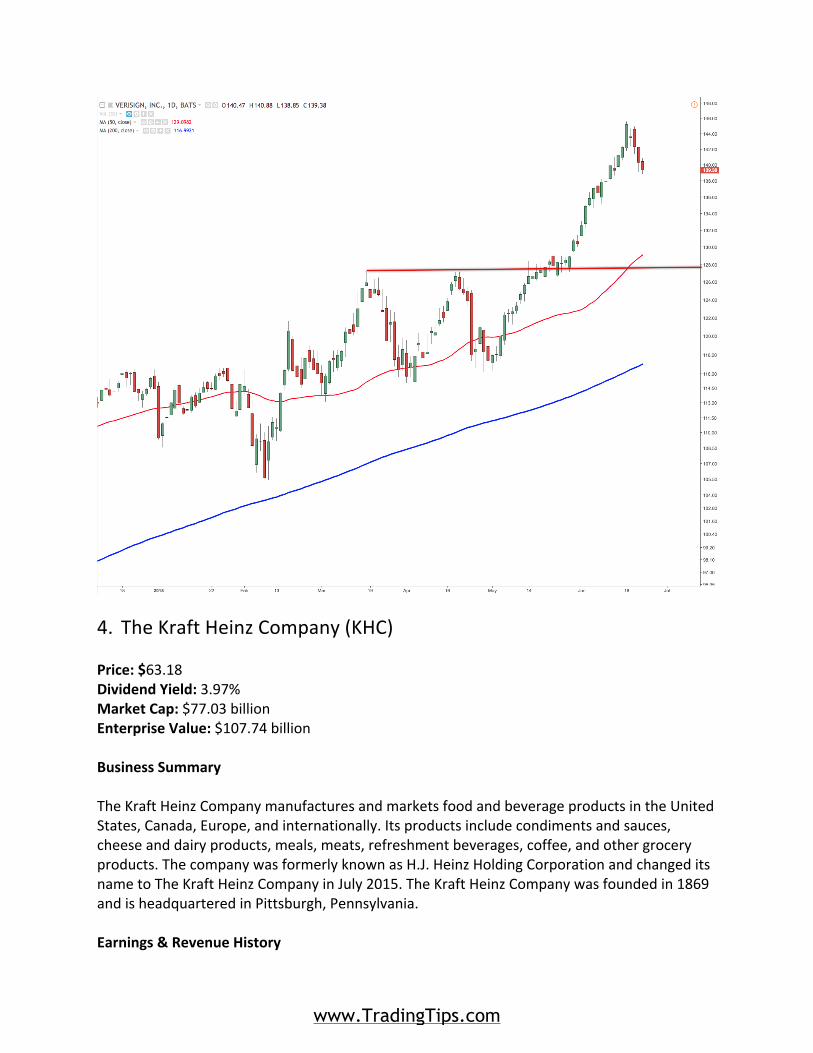

ReturnonAssets(ROA):17.71%ReturnonCapital(ROC):286.9%3-yearRevenueGrowthRate:9.4%3-yearEBITDAGrowthRate:12.10%ThecurrentvalueforROEcannotbecalculatedbecauseofnegativeequityonthebalancesheet.ItsROAisbelowits10-yearmedianvalueof16.83%andissignificantlyhigherthantheindustrymedianvalueof2.54%.ItsROCishigherthanits10-yearmedianvalueof148.95%andhigherthantheindustrymedianof34.22%.DVAs3-yeargrowthratesareslightlybelowthemedianvaluesforthepast10-yearsandisbelowtheindustryforrevenuegrowthandaboveitforEBITDAgrowth.WhiletheROEcan’tbecalculated,itpostshigherreturnsonROAandROC.Forexample,ROAstripsouttheleveragethroughdebtandwillbeequaltoorlessthanROE.PricePerformanceThe52-weekchangeforVRSNis50.04%withthe52-weekhighat$145.57andits52-weeklowat$92.13.DVAisconsideredalowbetastockwithabetaof0.75andits3-monthaveragevolumeis1.07million.VRSNhasperformedextraordinarilywellsofarin2018.Itbrokeoutofamonth-longconsolidationinlateMaytorunnearly$30.Thepriceiswellabovetheuptrending50-dayand200-daymovingaveragesandiscurrentlypullingback.

www.TradingTips.com

4. TheKraftHeinzCompany(KHC)Price:$63.18DividendYield:3.97%MarketCap:$77.03billionEnterpriseValue:$107.74billionBusinessSummaryTheKraftHeinzCompanymanufacturesandmarketsfoodandbeverageproductsintheUnitedStates,Canada,Europe,andinternationally.Itsproductsincludecondimentsandsauces,cheeseanddairyproducts,meals,meats,refreshmentbeverages,coffee,andothergroceryproducts.ThecompanywasformerlyknownasH.J.HeinzHoldingCorporationandchangeditsnametoTheKraftHeinzCompanyinJuly2015.TheKraftHeinzCompanywasfoundedin1869andisheadquarteredinPittsburgh,Pennsylvania.Earnings&RevenueHistory

www.TradingTips.com

Inthelast5quartersKHChasbeatenboththetoplinerevenueestimatesandthebottomlineearningsestimates.Inthemostrecentquarteritsawyear-overyearearningsgrowth,butaslightdecreaseinrevenuegrowth.Thecurrent5-yearprojectedgrowthrateofearningsis6.95%.Thereareno5-yearhistoricalgrowthnumbersbecausethecompanywasbroughtpublicagaininJulyof2015.ValuationRatiosPrice-to-Earnings(P/E):6.99Price-to-Book(P/B):1.16EnterpriseValuetoEBITDA(EV/EBITDA):13.84ThecurrentP/EratioforDVAis6.99,whichisbelowthemedianP/Eof32.17overthelast10yearsandwellbelowthemedianP/Eof20.69forthePackagedFoodsindustry.TheP/BiswellbelowthemedianP/Bof1.74andisbelowthemedianvalueoftheindustryat1.70.TheEV/EBITDAislowerthanthemedianvalueof18.9andishigherthantheindustrymedianof12.61.Onarelativebasiscomparedtoitsownhistoryandthecurrentvaluesoftheindustry,KHCistradingatafairlydiscountedvalue.ProfitabilityandGrowthReturnonEquity(ROE):18.07ReturnonAssets(ROA):9.23%ReturnonCapital(ROC):97.24%3-yearRevenueGrowthRate:-11.10%3-yearEBITDAGrowthRate:18.60%ThecurrentvalueforROEisslightlyaboveitshistoricalmedianvalueof17.83%butissignificantlyabovethemedianvalueforthepackagedfoodsindustryat8.32%.ItsROAisaboveits10-yearmedianvalueof7.34%andissignificantlyhigherthantheindustrymedianvalueof3.80%.ItsROCishigherthanits10-yearmedianvalueof93.22%andhigherthantheindustrymedianof12.67%.DVAs3-yearrevenuegrowthrateisbelowthemedianvaluesforthepast10-yearsandbelowtheindustry.Its3-yearEBITDAgrowthrateishigherthanitsmedianvalueandtheindustrymedianvalue.Whilerevenueshavebeenfalling,thecompanyhasbecomemoreprofitableandhasafairlystrongROE,ROAandROC.PricePerformance

www.TradingTips.com

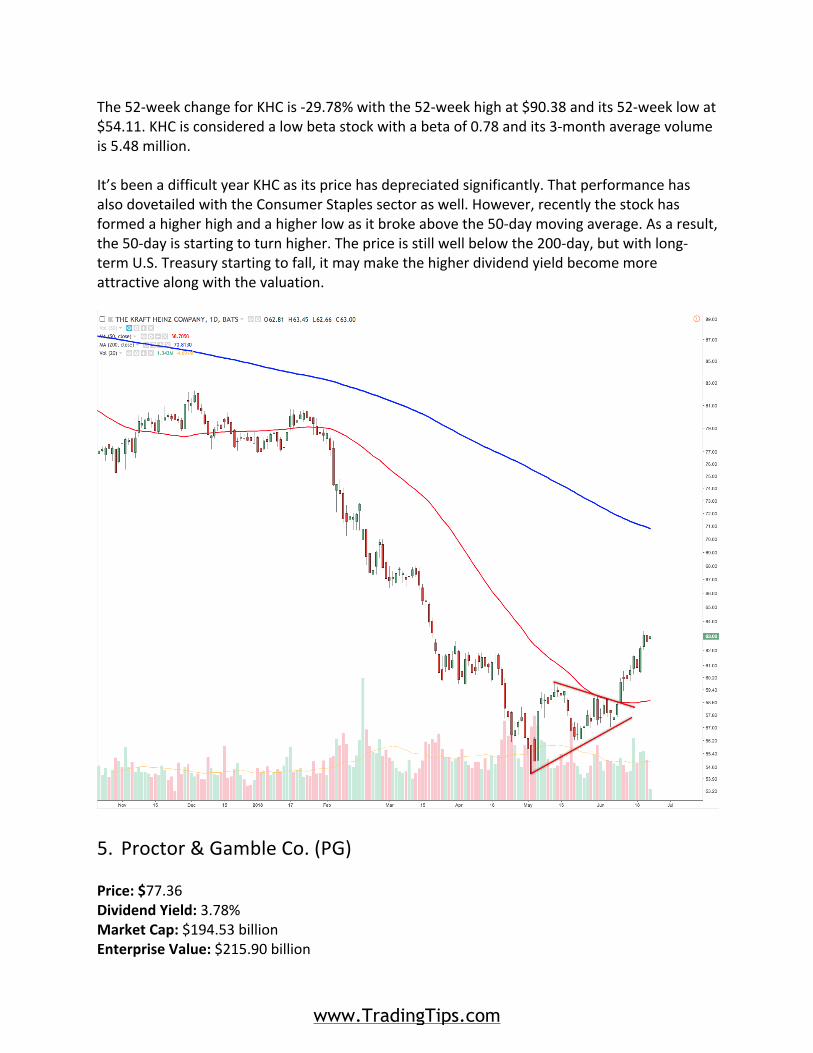

The52-weekchangeforKHCis-29.78%withthe52-weekhighat$90.38andits52-weeklowat$54.11.KHCisconsideredalowbetastockwithabetaof0.78andits3-monthaveragevolumeis5.48million.It’sbeenadifficultyearKHCasitspricehasdepreciatedsignificantly.ThatperformancehasalsodovetailedwiththeConsumerStaplessectoraswell.However,recentlythestockhasformedahigherhighandahigherlowasitbrokeabovethe50-daymovingaverage.Asaresult,the50-dayisstartingtoturnhigher.Thepriceisstillwellbelowthe200-day,butwithlong-termU.S.Treasurystartingtofall,itmaymakethehigherdividendyieldbecomemoreattractivealongwiththevaluation.

5. Proctor&GambleCo.(PG)Price:$77.36DividendYield:3.78%MarketCap:$194.53billionEnterpriseValue:$215.90billion

www.TradingTips.com

BusinessSummaryTheProcter&GambleCompanyprovidesbrandedconsumerpackagedgoodstoconsumersintheUnitedStates,Canada,PuertoRico,Europe,theAsiaPacific,GreaterChina,LatinAmerica,India,theMiddleEast,andAfrica.Thecompanysellsitsproductsthroughmassmerchandisers,grocerystores,membershipclubstores,drugstores,departmentstores,distributors,babystores,specialtybeautystores,e-commerce,high-frequencystores,andpharmacies.TheProcter&GambleCompanywasfoundedin1837andisbasedinCincinnati,Ohio.Earnings&RevenueHistoryInthelast5quartersPGhasbeatenboththetoplinerevenueestimatesandthebottomlineearningsestimates.Inthemostrecentquarteritsseenbothyear-overyearearningsandrevenuegrowth.Thecurrent5-yearprojectedgrowthrateofearningsis6.89%,andthecompanyhasanannualearningsgrowthrateinthelast5yearsof3.42%.Thehistoricalearningsgrowthrateisbelowtheindustryat9.50%andthesectorat7.12%ValuationRatiosPrice-to-Earnings(P/E):20.53Price-to-Book(P/B):3.64EnterpriseValuetoEBITDA(EV/EBITDA):12.51ThecurrentP/EratioforKHCis20.53,whichisabovethemedianP/Eof19.25overthelast10yearsandin-linewiththemedianP/Eof20.69fortheHouseholdandPersonalProductsindustry.TheP/BisabovethemedianP/Bof3.17andisabovethemedianvalueoftheindustryat1.70.TheEV/EBITDAislowerthanthemedianvalueof13.65andlowerthantheindustrymedianof12.61.Onarelativebasiscomparedtoitsownhistoryandthecurrentvaluesoftheindustry,PGistradingnearitsmedianvaluationoverthepast10years.Giventhefairlyhighvaluationforthemarketasawhole,thatmaylookattractivegiventhehighdividendyield.ProfitabilityandGrowthReturnonEquity(ROE):18.02ReturnonAssets(ROA):8.23%ReturnonCapital(ROC):71.84%3-yearRevenueGrowthRate:-2.5%3-yearEBITDAGrowthRate:0.30%ThecurrentvalueforROEisslightlyaboveitshistoricalmedianvalueof17.3%butissignificantlyabovethemedianvaluefortheHouseholdandPersonalProductsindustryat

www.TradingTips.com

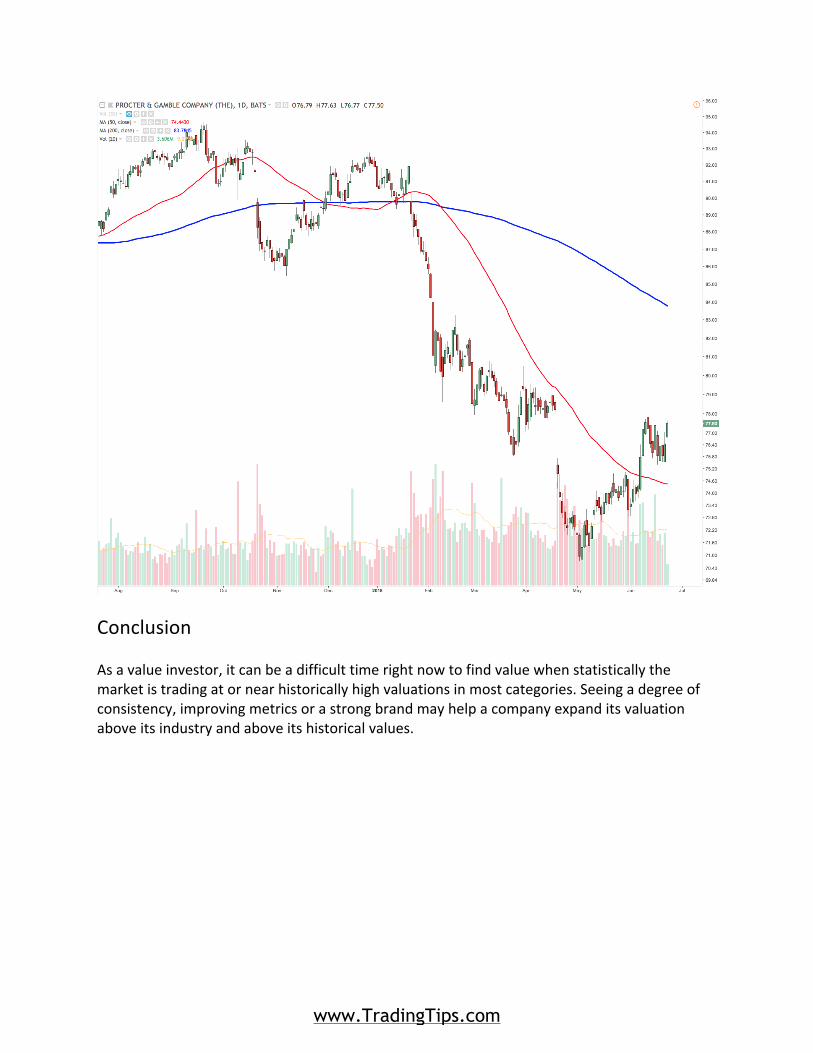

8.32%.ItsROAisslightlybelowits10-yearmedianvalueof8.23%andissignificantlyhigherthantheindustrymedianvalueof3.80%.ItsROCishigherthanits10-yearmedianvalueof68.24%andhigherthantheindustrymedianof12.67%.DVAs3-yearrevenuegrowthrateisbelowthemedianvaluesforthepast10-yearsandbelowtheindustry.Its3-yearEBITDAgrowthrateislowerthanitsmedianvalueandtheindustrymedianvalue.Whilerevenueshavebeenfalling,thecompanyhasmaintainedprofitabilityandhasafairlystrongROE,ROAandROC.PricePerformanceThe52-weekchangeforPGis-14.14%withthe52-weekhighat$94.67andits52-weeklowat$70.73.PGisconsideredalowbetastockwithabetaof0.39andits3-monthaveragevolumeis9.46million.LikemuchoftheConsumerNon-Cyclicalsector,PGhastradedsignificantlylowerin2018andevenhadalargegapfollowingitsearningsinApril.ThepricehasbeguntoreboundsincethebeginningofMayandhasrecentlyhadsomehighervolumeup-days.Therecentstrengthhascarrieditabovethe50-daymovingaverage,buttheaverageisstilldeclining.The200-daymovingaverageisstillwellabovethepriceandisstillreflectingalong-termdowntrend.

www.TradingTips.com

ConclusionAsavalueinvestor,itcanbeadifficulttimerightnowtofindvaluewhenstatisticallythemarketistradingatornearhistoricallyhighvaluationsinmostcategories.Seeingadegreeofconsistency,improvingmetricsorastrongbrandmayhelpacompanyexpanditsvaluationaboveitsindustryandaboveitshistoricalvalues.

www.TradingTips.com