Embed Size (px)

Citation preview

Warwick Actuarial Conference

Roger EdwardsProducts DirectorBright Grey

It’s about time we got it right!

Do you know what

consumer focus is?

Is it really possible to innovate?

Innovation

That’s a daft idea…..

We couldn’t do that because……

My only concern is that…..

The Reassurers won’t let us do

that….

Innovation

Taking a risk?

Short term

Sales

Profit/Share price

Tactics

Safety in similarity

Long term

Strategy

R&D

Innovation

New product lines

Innovation

• Are we designing products for consumers or our distribution channels?

• Bells and whistles that let our consultants get one up on the competition or benefits of real value to the consumer?

• Features that research well with consumers don’t always research well with distributors

Do you really talk to your customers?

Talking to customers

• Talk to consumers – how many of us do this enough?

• Product testing• Trial areas• FMCG tactics

Research

Session one – research concept

Refine session

Session two – research concept

Refine session

Session three – research concept

Marketable proposition

What do consumers think about protection?

• Building lifestyle pictures

• They do recognise the need

• Income is the foundation stone

What do consumers think about protection?

• Confusing• Don’t trust it• Don’t understand it• Too much small print• Jargon• Not convinced it will

pay out

What do consumers need from protection?

• Consumers want money and help if something goes wrong in their lives but they don’t know what will go wrong

• To know that it will pay out

Happy customers

• Financial • Debt repayment• Family security = income

replacement

Happy customers

Financial • Death

• Debt repayment• Family security = income

replacement• Major life changing

illness• Debt repayment• Family security = income

replacement• Prolonged illness

• Family security = income replacement

Happy customers

• Financial • Debt repayment• Family security = income

replacement

• Non-financial• Health/well-being• Recovery help

Happy customers

• Non-financial• Health/well-being –

rewards for staying healthy?

• Access to early diagnosis

• Recovery help• Counselling• Lifestyle advice

Happy customers

• Financial • Debt repayment• Family security = income

replacement• Non-financial

• Health/well-being• Recovery help

• Clarity• What is NOT included• Easy to understand• Little medical jargon

Happy customers

• Clarity• Chatty language• No jargon• No medical jargon• What is covered• What is NOT covered• No small print• No surprises

Summary

• Financial • Debt repayment• Family security = income

replacement• Non-financial

• Health/well-being• Recovery help

• Clarity• What is NOT included• Easy to understand• Little medical jargon

Product

Financial • Death

• Debt repayment• Family security = income

replacement• Major life changing

illness• Debt repayment• Family security = income

replacement• Prolonged illness

• Family security = income replacement

Life cover?

Critical illness?

Income protection?

Product

• Death• Debt repayment• Family security = income

replacement Life cover?

Fits bill

Probably should sell more income benefit – value for money

Product

• Major life changing illness

• Debt repayment• Family security = income

replacement

Critical illness?

Complex to explain definitions

Gaps

Windfalls

Product

• Prolonged illness• Family security = income

replacementIncome protection?

Idea meets needs but:

Complex

Don’t know what you’ll pay or what you’ll get

Language - communication

IP

Whole

of L

ifeLTA

FIBCICTPD

Where now?

PTD

PMI

Where now?

“Buy one get one free”

“In the event that you procure one item, as defined by the appropriate boxed quantity and confirmed by the electronic point of sale supervisor, we will assist you in the procurement of a second item, as defined by the appropriate boxed quantity, for no charge, that is, no monetary transaction, as defined by an exchange of currency, would be needed”

Communications

• Communication has got to be simple• How do retailers sell financial services?

Claims tidal wave - solutions

Critical illness is easy to understand

“If you get one of the illnesses on the list and you get a stack of cash”

“If you get one of the illnesses on the list and it meets a quite complex medical definition then you get a stack of cash”

What IFAs want?

IFAs say tighter CI definitions better than losing guaranteeBy Sonia Speedy

IFAs would rather see definitions on guaranteed critical-illness policies continually tightened than lose them altogether, according to research by Legal & General. L&G's survey of 400 IFAs found that new-generation CI cover products should be based on today's model rather than "radical" new designs. Fifty-seven per cent of the IFAs offer only guaranteed premiums to clients while 42 per cent offer both guaranteed and reviewable rates.

ABI - Definition creep• Any malignant tumour characterised by the uncontrolled

growth and spread of malignant cells and invasion of tissue. The term cancer includes leukaemia and Hodgkin’s disease, but the following are excluded:• All tumours which are histologically described as pre-malignant, as

non-invasive or as cancer-in-situ• Any skin cancer other than invasive malignant melanoma• All forms of lymphoma in the presence of any Human

Immunodeficiency Virus• Kaposi’s Sarcoma in the presence of Human Immunodeficiency Virus• All tumours of the prostate unless histologically classified as having a

Gleason score greater than 6 or having progressed to at least TNM classification T2N0M0

• All tumours of the bowel unless progressed to and measured by some meaningless medical measure

• All tumours of the liver unless progressed to and measured by some other meaningless medical measure

Communications

• Many articles state that the female market should be targeted more. Nowhere in these articles does it ever say how to do this.

• Suggestions of articles in females glossies.• The female network

Traditional triggers

Modern triggers

So what does this mean for current product developments?

The future of critical illness cover

Concerns• Medical

advancements• Claims tidal wave• Non disclosure

What consumer need is critical illness cover

meeting?

What consumer need is critical illness meeting?

Income replacement?

Debt repayment?

Mortgage repayment?

Lifestyle adjustment?

Compensation for life

changing events?

Evolution – Reviewable definitions

• The public don’t trust our existing small print

• Now we expect them to accept variable small print?

• Could only work with independent body who agrees when something can be changed

The CIC Plan

NEW – Reviewable

Definitions

Evolution – Severity underpin

• Retains existing problems at an individual definition level

• Expectations – “I’ve still got cancer”

• More small print to explain

The CIC Plan

NEW – Severity

Underpin

Evolution – Tiered benefits

• Split between severe and mild illnesses

• More complex medical definitions

• More to explain• Chance of making

the wrong decision

The CIC Plan

NEW – Tiered

benefits

Challenges

• More complexity• More explanation

required• More small print• More declined claims

Evolution – acceptable guaranteed product

The CIC Plan

• Bin angioplasty, CABG and other heart surgeries• Introduce age limit of 65• Introduce cover limit - £250,000

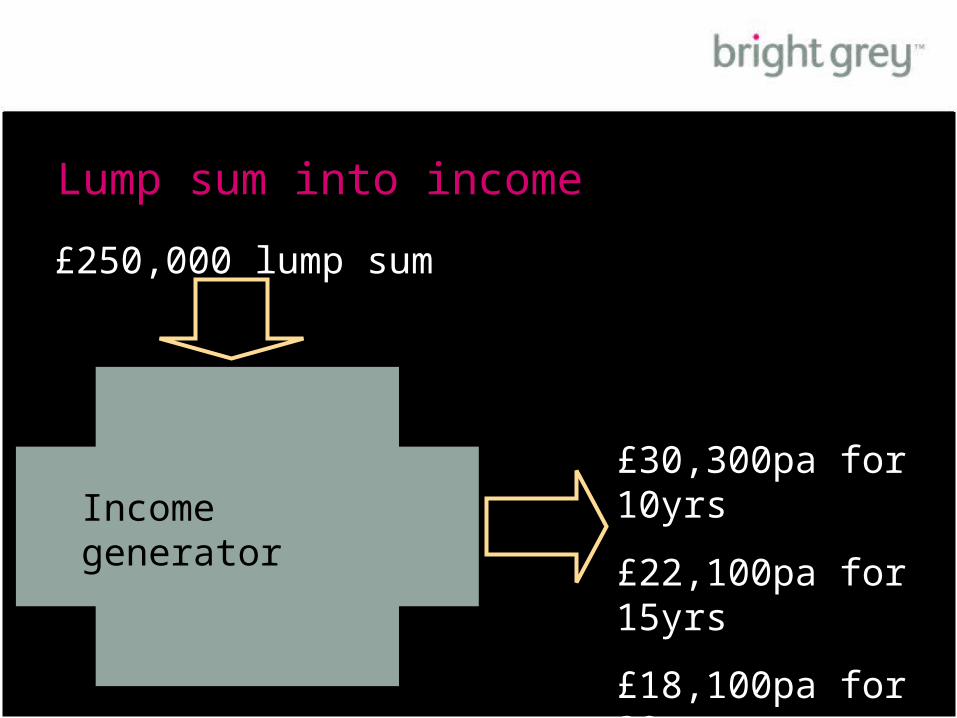

Lump sum into income

£250,000 lump sum

£30,300pa for 10yrs

£22,100pa for 15yrs

£18,100pa for 20yrs

£15,700pa for 25yrs

Income generator

Whatever we do with CI – people

need more income protection!

Summary

• Design propositions for the consumer, get buy in from the distributor, give them the tools to sell

• Think beyond the “financial bit” – what is the whole end to end proposition

• Research, research, research, test, test, test• Include communication and service innovation• Design a product based on the needs of the

person buying it