Embed Size (px)

Citation preview

April 11, 2018

Washington Area Economy: Performance and Outlook

Mark C. White, Ph.D.Deputy Director

Center for Regional AnalysisSchar School of Policy and Government

George Mason University

Presentation to:

Greater Washington Association of Financial Professionals

1

Agenda

• Broad economic trends

• The Washington regional economy

• Emerging trends in federal employment

• Ongoing challenges

2

U.S. Gross Domestic Product

Source: Bureau of Economic Analysis (Seasonally Adjusted, Chained 2009 Dollars )

2010 2011 2012 2013 2014 2015 2016 2017

$13,000

$13,500

$14,000

$14,500

$15,000

$15,500

$16,000

$16,500

$17,000

$17,500

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0Quarterly Change Real GDP (Billions)

%

2017 +2.3%

125

130

135

140

145

150

0

50

100

150

200

250

300

350

400

2012 2013 2014 2015 2016 2017 2018

Month-to-Month Change (000s) Total (Millions)

US Payroll Jobs

Source: Bureau of Labor Statistics (Seasonally Adjusted), GMU Center for Regional Analysis

2016-2017

2.17 M

Mar+103K

Since 2010 +18M

The Washington Regional Economy

5

GDP Trends since 2001

6

90

95

100

105

110

115

120

125

130

135

140

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

20

01

GD

P*=

10

0

Washington-Arlington-Alexandria, DC-VA-MD-WV MSA

United States

Source: US Bureau of Economic Analysis, *2009 Chained Dollars

0

2

4

6

8

10

12

5.7 – DC4.1 – U.S.4.0– SMD

3.6– MSA2.7 – NVA

Unemployment Rates in the WMSABy Sub-State Area

Source: Bureau of Labor Statistics (Region - Not Seasonally Adjusted, US – Seasonally Adjusted)

Annual Job Change - Washington MSA

2,800

2,850

2,900

2,950

3,000

3,050

3,100

3,150

3,200

3,250

3,300

3,350

-10

10

30

50

70

90

110

2012 2013 2014 2015 2016 2017 2018

MOTYC Non-Farm Jobs

Source: Bureau of Labor Statistics (Not Seasonally Adjusted), GMU Center for Regional Analysis

February-18 Total: 3,278 K

000’s 000’s

Feb 17-Feb 18

+44.8 K

15 Largest Job MarketsJob Change: Feb 2017 – Feb 2018

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Washington +1.4%

Source: Bureau of Labor Statistics (Not Seasonally Adjusted), GMU Center for Regional AnalysisSource: Bureau of Labor Statistics (Not Seasonally Adjusted), GMU Center for Regional Analysis

10

Professional & Business Services drive the regional economy

Source: US Bureau of Labor Statistics, Current Employment Statistics

1.7%

1.9%

2.1%

2.3%

4.8%

4.8%

6.4%

8.3%

9.8%

10.4%

11.1%

13.6%

23.0%

0% 5% 10% 15% 20% 25%

Manufacturing

Wholesale Trade

Transportation & Utilities

Information

Financial Activites

Construction

Other Services

Retail Trade

Leisure & Hospitality

State & Local Government

Federal Government

Education & Health Services

Professional & Business Services

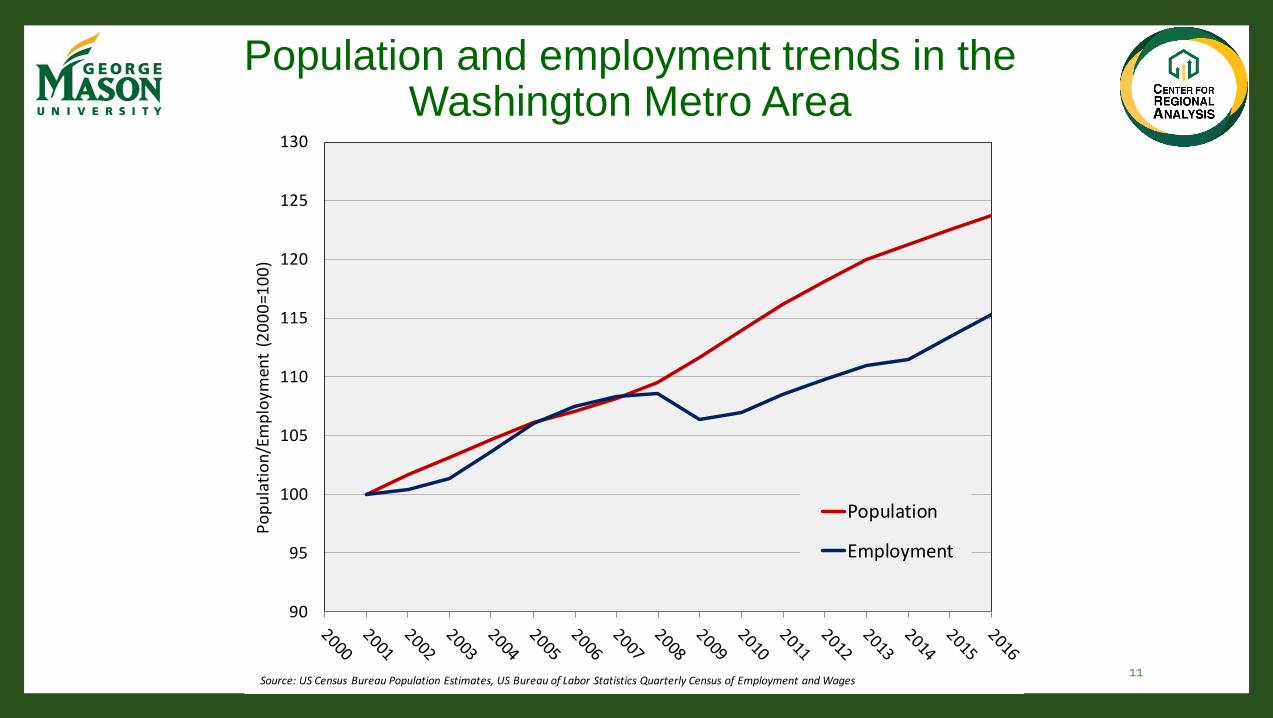

Population and employment trends in the Washington Metro Area

Source: Bureau of Labor Statistics (Not Seasonally Adjusted), GMU Center for Regional Analysis11

90

95

100

105

110

115

120

125

130

Po

pu

lati

on

/Em

plo

ymen

t (2

00

0=1

00

)

Population

Employment

Source: US Census Bureau Population Estimates, US Bureau of Labor Statistics Quarterly Census of Employment and Wages

Job Change by SectorFeb 2017 – Feb 2018

Washington MSA

-0.2

-0.7

3.4

0.1

2.7

4.1

4.7

0.1

9.7

3.3

-6.6

7.6

16.6

-10 -5 0 5 10 15 20

Manufacturing

Wholesale Trade

Transp. & Util.

Information

Financial

Construction

Other Services

Retail Trade

Leisure & Hosp.

State & Local Govt

Federal Govt.

Educ & Health Svcs

Prof. & Bus. Svcs

(000s) Total = 44,800

Source: Bureau of Labor Statistics (Not Seasonally Adjusted), GMU Center for Regional Analysis

(Ranked by Size in 2017)

The DC Metro is a leader in Cyber-security

13

1,740

1,970

2,170

2,270

2,360

2,360

2,430

2,460

3,030

3,110

3,200

3,400

3,560

7,380

13,520

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000

DenverSt. Louis

BaltimoreSF-Oakland

PhoenixCharlotte

AtlantaPhiladelphiaLos Angeles

BostonMinneapolis

ChicagoDallas

New YorkWashington

Information Security Analysts (SOC 15-1122) by metro area, 2017

Source: U.S BLS Occupational Employment Statistics (May 2017) and GMU Center for Regional Analysis

The Economic Influence of the Federal Government

14

Federal GovernmentWashington MSA

345

350

355

360

365

370

375

380

385

390

-20

-15

-10

-5

0

5

10

15

20

25

30

2010 2011 2012 2013 2014 2015 2016 2017 2018

MOTYC

TotalJobs

(000s)

Source: Bureau of Labor Statistics (Not Seasonally Adjusted), GMU Center for Regional Analysis February-18 Total: 362K

(000s)

Feb 17-Feb 18

-6,600

Federal Procurement in the Washington MSA1980-2017 (Fiscal Years)

0

10

20

30

40

50

60

70

80

90

75.0

$ Billions

TOTAL = $1,388.5 Billion 79.976.3

69.1 71.1

Source: US Census, Consolidated Federal Funds Report and USAspending.gov

71.2

82.477.6

Professional & Business ServicesWashington MSA

620

640

660

680

700

720

740

760

780

-15

-10

-5

0

5

10

15

20

25

2010 2011 2012 2013 2014 2015 2016 2017 2018

MOTYC

Total Jobs

(000s)

Source: Bureau of Labor Statistics (Not Seasonally Adjusted), GMU Center for Regional Analysis

February-17Total: 752.4K

Feb 16-Feb 17

+16.6K

Professional and Business Services Employment and Federal Employment in Washington, DC Metro Area Compared to the

Previous Year, 2012-2018

18

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

2012 2013 2014 2015 2016 2017 2018

Mo

nth

ove

r th

e Y

ea

r E

mp

loy

me

nt

Ch

an

ge

(0

00

s)

Prof. & Business Services Federal

Source: US Bureau of Labor Statistics, Current Employment Statistics

Additional ongoing challenges

19

Long commutes diminish quality of life

20

Source: US Census Bureau, 2016 American Community Survey, Table S08025.5%

7.2%

7.6%

9.1%

9.3%

10.7%

11.2%

11.6%

12.2%

13.3%

13.8%

14.1%

14.5%

17.2%

17.8%

21.8%

0% 5% 10% 15% 20% 25%

Minneapolis

Detroit

Phoenix

United States

Dallas

Miami

Houston

Philadelphia

Seattle

Los Angeles

Boston

Chicago

Atlanta

SF-Oakland

Washington

New York

Proportion of workers with travel time to work of 60 or more minutes

100

150

200

250

300

350

400

450

500

Median House Sales PriceWashington MSA

$400 KFeb 2018

Source: Metropolitan Regional Information Systems (MRIS), GMU Center for Regional Analysis

(000s)(000s)

The region has experienced net domestic out-migration since 2013

22

• This trend started sooner in places like Arlington-Alexandria and suburban Maryland.

• People move here for jobs, then choose a place to live in the region.• Many factors cause them to

consider other metro areas

• Note the continued importance of Int’l migration to the region’s continued growth

49,016 49,169 47,790 48,651 47,832 44,882 42,616

37,183 39,715 39,358

41,048

45,41045,606

44,760

23,8646,843

3,143

-23,209-31,483 -31,492

-21,543

-40,000

-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

-40,000

-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

2010-2011 2011-2012 2012-2013 2013-2014 2014-2015 2015-2016 2016-2017

Total P

op

ulatio

n C

han

ge

Po

pu

lati

on

Ch

ange

Elements of population change in the Washington, DC Metro Area

Net Domestic Migration

Net Int'l Migration

Natural Increase

Total Change

Source: US Census Bureau, Population Estimates Program, V2017

The DC Metro Area’s Immigrant Workforce

23

0%

5%

10%

15%

20%

25%

30%

35%

Less than HighSchool

High schooldiploma/GED

Associates degree orSome College

Bachelors Degree Graduate orProfessional Degree

Per

cen

tag

e o

f P

op

ula

tio

n

Educational Attainment, Non Citizen, Foreign Born Workers MWCOG Region

Non Citizen Foreign Born Workers MWCOG Workforce

Source: US Census Bureau ACS 2016, GMU Center for Regional Analysis

The DC Metro Area’s Immigrant Workforce

24

Majority of immigrants have been here 10 years or more

25

0.2% 0.5% 1.5%

8.4%

22.2%

48.3%

17.2%

1.8%0%

10%

20%

30%

40%

50%

60%

before 1960 1960-1969 1970-1979 1980-1989 1990-1999 2000-2009 2010-2014 2015 or later

Year of Entry, Non Citizen Foreign Born WorkersMWCOG Region

Source: US Census Bureau ACS 2016, GMU Center for Regional Analysis