Embed Size (px)

Citation preview

WAVELET-BASED LEADING INDICATORS OF INDUSTRIALACTIVITY IN BRAZIL

PAULO PICCHETTI

Fundação Getúlio Vargas �EESP/IBRE

Abstract. The search for business cycles leading indicators in the economet-rics literature has considered a large set of statistical methods. The maindi¤erence among these methodologies can be considered the treatment of theevident non-stationarity of the data. While a very large class of models isbased on some sort unit-root type stochastic trend, others try to incorporate amore formal probabilistic structure for regime shifts and yet another large classof models considers di¤erent �lters and decompositions aimed to reveal andanticipate major turns in economic activity. Data on the Brazilian economyis particularly characterized by relatively short time-series, while containingsigni�cant structural changes, seriously weakening the performance of theseclasses of models. An alternative set of decompositions, based on Waveletsand Multi-Resolution Analysis [Priestley (1996), Percival and Walden (2000)]have been providing a very promising alternative to the analysis of time-seriesbased on time-scales that expose their changing behavior across time, both in-dividually and in terms of correlations with each other [Ramsey and Lampart(1998)]. Wavelet covariances between series are estimated on di¤erent timescales, thus allowing the whole sample to be retained in the analysis, even inthe presence of structural changes. A leading indicator for Brazilian industrialactivity is constructed upon these results. Another contribution of this paperwill be to re-construct a set of survey data available on di¤erent frequenciesto make it compatible with the series it will try to anticipate.

Keywords: Business cycles, Brazilian industrial production, Leading indi-cators, Wavelets, Structural time-series models

JEL: C32, C42, C53, E32, E47

1. Introduction

Surveys on expectations of industrial activity are mainly motivated by the needto obtain leading indicators of activity cycles. How the di¤erent surveyed aspectsrelate to actual industrial production in the future is a very active topic of research,both at the theoretical and applied levels. Traditional methods for dynamical corre-lation between historical data on variables representing expectations and variablesrepresenting actual realizations that can be associated with these expectations pro-vide results which are both highly relevant and interesting. Some shortcomings ofthis type of analysis are fundamentally linked to the nature of the non-stationarityof the available data. Speci�cally, with historical data highly characterized by struc-tural breaks and outliers, �rst-di¤erencing methods on the time domain are usuallyincapable of inducing stationarity. Likewise, traditional methods for frequency do-main decomposition and coherence analysis between this kinds of variables alsoproduces results whose usefulness is considerably limited.

1

2 PAULO PICCHETTI

In this context, Lucas (1981) stresses that the importance of looking at co-movements between variables: "Technically, movements about trends in GDP inany country can be well described by a stochastically disturbed di¤erence equationof very low order. These movements do not exhibit uniformity of either periodor amplitude... Those regularities which are observed are in the co-movementsamong di¤erent series. ... The central �nding, of course, is the similarity of allcycles with one another, once variation in duration was controlled for, in the sensethat each cycle exhibits about the same pattern of co-movements as do the others."Harding and Pagan (2000), however, consider a fundamental issue concerning theimplementation of this idea: "How exactly could Lucas conclude that there is nouniformity in temporal movements in output and yet be con�dent that there areuniform co-movements ? ... The academic literature has mostly identi�ed co-movements with covariances, and then estimated the latter with a sample periodthat includes many cycles. Hence, it is assumed that the co-movements are thesame across cycles."Wavelet decompositions can be employed to capture these co-movements between

economic series at the �ner detail of di¤erent time-scales. Insofar as covariancesare regularly estimated averaging several di¤erent frequencies, it seems highly de-sirable to isolate these associations. The objective of this paper is to decomposeseries on expectations based on di¤erent time-scales, and assess how each of thesecomponents relate dynamically the equivalent components in actual industrial pro-duction measures. This decomposition is based on wavelet coe¢ cients which havebeen widely used in a series of applications across di¤erent �elds, including econom-ics. Section 3 below very quickly summarizes some of the main concepts neededto understand and interpret the results here, and provides additional referencesfor details on aspects of both theory and implementation. Section 2 describes thedata, Section 4 shows the results. In section 5 we build a leading indicator forindustrial activity based on expectations from survey data. Section 6 discusses theimplications for growth-cycle analysis, and Section 7 concludes.

2. Data Description

The main variable for measuring industrial activity is the monthly industrialproduction index calculated by Instituto Brasileiro de Geogra�a e Estatística �PIM/IBGE. This series has been calculated since the mid-seventies, and has urde-gone periodic methodological revisions. The last of these revisions established newweights at the �rm and sectoral levels, and was made compatible with the previousmethodology going back to January 1991. Data is available on di¤erent regionaland sectoral aggregations, but here we concentrate at the whole-industry level forall regions, i.e., the most aggregated version. Future research may contemplate�ner resolutions at both dimensions.Our analysis will decompose the time-scale relationships between this main vari-

able and di¤erent indicators from survey data provided by Sondagem Conjunturalda Indústria de transformação �Sondagem/FGV, calculated by Fundação GetúlioVargas in Brazil since the mid-sixties. Sondagem/FGV surveys the general per-formance related to the most relevant products at the �rm level. While some ofthe items on the questionnaire relate to �rm-speci�c measures (such as employmentlevel and capacity utilization), others such as demand, output, stocks and prices are

WAVELET-BASED LEADING INDICATORS OF INDUSTRIAL ACTIVITY IN BRAZIL 3

taken at the speci�c product level. In order to make the sample periods compatiblewith PIM/IBGE, we will consider data from January 1991 until March 2008.More speci�cally, the variables in our analysis are:

� Global Demand Level� Inventory Levels� Capacity Utilization� Expected Production� Expected Employment

Inventory Levels and Capacity Utilization are surveyed in relation to the time ofthe response, whereas all other variables are qualitative measures of three-monthahead expectations. Capacity Utilization is the only quantitavely measured vari-able, on a 0�100 scale. All other variables are indexes representing the net resultof qualitative questions, such as Inventory Levels above, equal, or below a desirednumber, Expected Production less, equal or above the current value, etc. Raw dataat the �rm level are weighted according to each respondent �rm�s gross receipts,the only exception being the Expected Employment variable, which is weightedaccording to each �rm�s number of employees. Data at the sectoral and regionallevels are accordingly weighted with respect to industry-wide and country-wide sig-ni�cances to compose the aggregate measures which will be used in this study.Data for these variables from Sondagem/FGV is also available with �ner resolu-tions in terms of industrial sectors and regions, mostly in consistence with data forPIM/IBGE, warranting the kind of further research outlined above.

2.1. Frequency Compatibility. Data on Sondagem Industrial is gathered byFGV since 1966 , �rst on a quarterly basis, and more recently (since mid-2005) ona monthly basis. We reconstruct the series on a monthly basis for the whole sampleperiod (beginning on january 1991) in order to make it compatible with monthlydata from PIM/IBGE, the variable for which we seek a leading indicator. Themethodology is to estimate the components of a structural model (Harvey(1989)),and treat the months between quarterly observations as missing values. The formu-lation of the structural model in state-space and the estimation of its componentsby the Kalman Filter easily allows the estimation of these missing values. Thestate-space representation of the structural model is

yt = �t + t + �t; �t � NID(0; �2�)�t+1 = �t + �t + �t; �t � NID(0; �2�)�t+1 = �t + �t; �t � NID(0; �2�)

t =

[s=2]Xj=1

jt

j;t+1 = jt cos�j + �jt sin�j + !jt; !jt; !

�jt � NID(0; �2!)

�j;t+1 = � jt sin�j + �jt cos�j + !�jt; j = 1; : : : ; [s=2]

where [s=2] is the largest integer of the seasonal frequency divided by two, and�j =

2�js ; j = 1; : : : ; [s=2]. This choice of speci�cation for the seasonal component

t is based on considerations by Durbin and Koopman (2001).For one of the variables (NUCI) these model was estimated both in the univariate

context and the bi-variate, where an alternative measurement of the same variable

4 PAULO PICCHETTI

(NUCI-CNI) is available on a monthly basis for the whole sample period. The latterapproach has the advantage of more e¢ cient estimation of the missing data, giventhat the state components of the structural model are usually correlated. Insofaras the results from both approaches were very similar, the univariate model wasused to provide the complete monthly observations for all the series in Sondagem.

3. Building Blocks for Wavelet Decompositions

Wavelet theory has been developing for a long time, and has relatively recentlybeen consolidated in a single �eld of theoretical and applied research, with a fastgrowing literature (Percival and Walden(2000)). Economic applications of themethod are still far behind traditional time-series and �ltering methods, but aregrowing very rapidly (Ramsey(2000,2002), Crowley(2007)). A good introductionto the current literature on wavelets and its applications to economics is Crow-ley(2007). Here we only attempt a rapid introduction, to put the methodology incontext and to help the interpretation of the results.Wavelets transforms are analogous to Fourier transforms in the sense that the

original series is projected on a set of basis functions, which are related to di¤erentfrequencies. However, the main limitation to Fourier analysis is the requirement ofa stationary time-series, which are unable to represent interesting economic time-series exhibiting stochastic trends, structural breaks, outliers, and changing vari-ance. Wavelets provide a new set of basis functions which are �exible enough torepresent these features commonly found in economic data, decomposing the orig-inal series across di¤erent time-scales. These time-scales are related to the inverseof di¤erent frequencies intervals.With data sampled at discrete points in time, we concentrate on the Discrete

Wavelet Transform (DWT) methods. Initially, for a series fytg of T = 2J obser-vations (J being the number of time-scales represented), we can obtain a vector ofwavelet coe¢ cients represented as

W = [w1; w2; : : : ; wJ ; vJ ]0

where each wj is T=2j vector of coe¢ cients associated with variations within ascale of length �j = 2j�1, and vj is a T=2J vector of coe¢ cients associated withaverages os a scale of length 2J = 2�J . These coe¢ cients are obtained by theexpression

w =Wy

where W is a T � T orthonormal matrix de�ning the DWT. Details of di¤erent al-gorithms for implementing this matrix can be found in Percival and Walden (2000).With these estimated coe¢ cients, the series yt has a multiresolution analysis

(MRA) representation given by

yt = SJ +JXj=1

Dj;t; t = 1; : : : ; T

where Dj = W0

jwj ; j = 1; : : : ; J and SJ = V0

JVJ de�ne the j-th level "waveletdetail" associated with variations in yt at scale �j . While the individual waveletcoe¢ cients are normally referred to as "atoms", their sums over each time-scale arenamed "crystals", and summarize the behavior of the series at the correspondinglevel or time-scale. In the context of our monthly frequency dataset ranging fromJanuary 1991 through March 2008, we are able to estimate crystals for six di¤erente

WAVELET-BASED LEADING INDICATORS OF INDUSTRIAL ACTIVITY IN BRAZIL 5

time-scales. The monthly resolutions for the time-scales corresponding to crystalsD1�D6 are, respectively {[2-4], [4-8], [8-16], [16-32], [32-64], [64-128]}. Each ofthese will be interpreted according to the usual analysis of time-series componentsin terms of seasonality and cycles. The smooth component SJ represents the long-term trend of the series which does not necessarily conforms to periodic behavior.Here, we utilize a variation of the DWT known as the Maximal Overlap Discrete

Wavelet Transform (MODWT). Details for the algorithms employed can be foundin Percival and Walden (2000). The motivation is summarized by:

� whereas sample size is restricted to T = 2J observations in DWT, it canhave any number of observations in MODWT,

� in multiresolution analysis, the wavelet details can be perfectly aligned intime with the original series, which is not the case in DWT, and

� the MODWT wavelet variance estimator is asymptotically more e¢ cientcompared to the estimator based on DWT.

This last item is particularly important for the analysis conducted here sincewe use the estimated wavelet variances for calculating the wavelet cross-correlationbetween a pair of series. This cross-correlation in wavelet analysis is the analogue ofthe coherence in Fourier analsyis. Formally, the wavelet cross-correlation betweena pair of series Yt = [y1;t; y2;t] for di¤erent leads/lags � is de�ned as

�Y;� (�j) = Y;� (�j)

�1(�j)�2(�j)

where Y (�j) is the wavelet covariance of between the series in Yt on time-scale�j and the denominator represents the product of the wavelet standard-deviationsof both series on the same time-scale. Again, details of the estimation for thesestatistics can be found in Percival and Walden (2000).In what follows, we use these results to base our analysis on the lag/lead rela-

tionships between variables of sondagem and the industrial production index on ascale-by-scale basis.

4. Results

Decomposing the PIM/IBGE by the MODWT produces a set of wavelet coef-�cients that can be better understood visually. One of the ways they are usuallydepicted can be seen on Figure 1.

Figure 1

The absolute magnitude of the estimated coe¢ cients at each point in time, and ateach of the six time-scales considered, is represented by a darker colour. therefore,

6 PAULO PICCHETTI

the relative darkness of each decomposition relates to the relative importance ofthat level of time-scale at that point in time for explaining the observed variationin the series. The generalization of this type of analysis compared to a standardFourier frequency-domain decomposition is clearly seen in this real-world example,since the contribution of di¤erent frequencies for the total variation of the series isnot constant across time.Another yet more powerful visual tool is the evolution of the MRA elements

compared to the actual observed series in the sample period, as seen on Figure 2.

1992 1994 1996 1998 2000 2002 2004 2006 200860

80

100

120

140PIM

50

100

150

SJ0

10

0

10

D1

10

0

10

D2

10

0

10

D3

5

0

5

D4

5

0

5

D5

1992 1994 1996 1998 2000 2002 2004 2006 20085

0

5

D6

Figure 2

Crystal D1 captures the random behavior on the short time-scale, analogous to theestimated residuals in standard time-series models. The seasonal pattern of theseries is characterized by variations which are neither monotonic inside each year,nor constant across di¤erent years. Crystals D2 and D3 are associated with thisimportant behavior of the analyzed series. Cristals D4-D6 are associated with longertime-scales variability, usually related to cycles. The relative estimated waveletvariances of these di¤erent time-scales can be seen in Figure 3.

WAVELET-BASED LEADING INDICATORS OF INDUSTRIAL ACTIVITY IN BRAZIL 7

0 1 2 3 4 5 6100

101

102

LevelW

avel

et V

aria

nce

P IM

Figure 3

For the industrial production index, the greatest wavelet variance is estimated atlevel 3 �in relation to the seasonal time-scale, while short-time scales variances arerelatively bigger than the ones associated to the longer time-scales.Similar estimations are conducted to the survey data series, the graphical results

of which can be seen on the appendix. In what follows, we focus on the wavelet cross-correlations between the series in the survey data and the industrial productionindex.

4.1. Global Demand Level. Estimated crystals for global demand level are dy-namically correlated to industrial production at all time-scales. Whereas it posi-tively leads and lags at the J4 throuth J6 time-scales, at the main seasonal time-scale(J3) it positively lags and negatively leads. In other words, at the approximatelyhalf-year resolution, a larger output increases the percepetion of the global demandlevel, but this increased demand perception is associated with a smaller output atthe seasonal frequency.

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J1

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J2

6 5 4 3 2 1 0 1 2 3 4 5 60.5

0

0.5J3

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J4

6 5 4 3 2 1 0 1 2 3 4 5 60

0.5

1J5

6 5 4 3 2 1 0 1 2 3 4 5 60

0.5

1J6

Global D emand Lev el

Figure 4

8 PAULO PICCHETTI

This suggests that in this time-scale, a current increase in the perception of demandtends to anticipate production, leading to a smaller output �ve to six months ahead.

4.2. Inventory Levels. Inventories are only correlated to output at the longertime-scales, positively leading and lagging it.

6 5 4 3 2 1 0 1 2 3 4 5 60.5

0

0.5J1

6 5 4 3 2 1 0 1 2 3 4 5 60.5

0

0.5J2

6 5 4 3 2 1 0 1 2 3 4 5 60.5

0

0.5J3

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J4

6 5 4 3 2 1 0 1 2 3 4 5 60

0.5

1J5

6 5 4 3 2 1 0 1 2 3 4 5 60

0.5

1J6

Inv entory Lev els

Figure 5

Inventories below the optimal level (associated with increases in the values of thesevariables) lead to greater future output, but not as strongly as greater realizedoutput are associated with inventories below the optimal level. This suggests aninteresting asymmetry concerning the planning and management of inventories.

4.3. Capacity Utilization. At the longer time-scales, capacity utilization signif-icantly and positively leads and lags industrial output, as expected.

WAVELET-BASED LEADING INDICATORS OF INDUSTRIAL ACTIVITY IN BRAZIL 9

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J1

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J2

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J3

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J4

6 5 4 3 2 1 0 1 2 3 4 5 60

0.5

1J5

6 5 4 3 2 1 0 1 2 3 4 5 60

0.5

1J6

C apac ity Lev el U tiliz ation

Figure 6

At the J3 seasonal frequency, bigger levels of capacity utilization are associatedwith smaller output at future periods beginning around 4 months. This suggestsan interesting pattern of changes in the intra-year allocation of production, relatedto decisions justifying anticipations in planned output.

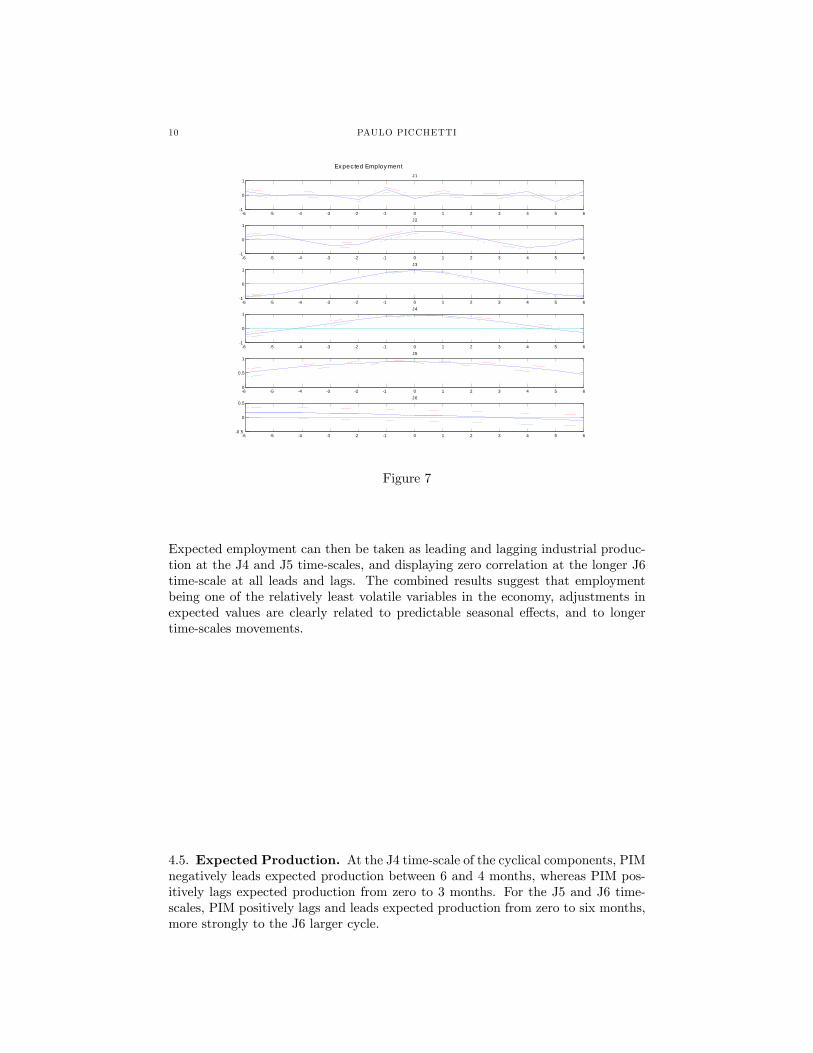

4.4. Expected Employment. For the seasonal component J3, correlations arenear perfect (close to 1) at zero lags, and close to -1 at the six-months lags and leads,indicating a perfect forecast for the peaks and troughs of the seasonal frequencybetween production and expected employment. For the cycles components J4 andJ5, correlations are also close to one at the zero lead/lag, and present a symmetricaldeclining pattern towards the leads and lags directions.

10 PAULO PICCHETTI

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J1

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J2

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J3

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J4

6 5 4 3 2 1 0 1 2 3 4 5 60

0.5

1J5

6 5 4 3 2 1 0 1 2 3 4 5 60.5

0

0.5J6

Expec ted Employ ment

Figure 7

Expected employment can then be taken as leading and lagging industrial produc-tion at the J4 and J5 time-scales, and displaying zero correlation at the longer J6time-scale at all leads and lags. The combined results suggest that employmentbeing one of the relatively least volatile variables in the economy, adjustments inexpected values are clearly related to predictable seasonal e¤ects, and to longertime-scales movements.

4.5. Expected Production. At the J4 time-scale of the cyclical components, PIMnegatively leads expected production between 6 and 4 months, whereas PIM pos-itively lags expected production from zero to 3 months. For the J5 and J6 time-scales, PIM positively lags and leads expected production from zero to six months,more strongly to the J6 larger cycle.

WAVELET-BASED LEADING INDICATORS OF INDUSTRIAL ACTIVITY IN BRAZIL 11

6 5 4 3 2 1 0 1 2 3 4 5 60.5

0

0.5J1

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J2

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J3

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J4

6 5 4 3 2 1 0 1 2 3 4 5 61

0

1J5

6 5 4 3 2 1 0 1 2 3 4 5 60

0.5

1J6

Expec ted Produc tion

Figure 8

As in the case of capacity utilization, these results suggest interesting patternsof intra-year allocation of output, isolating this e¤ect from the longer time-scalesstrong positive correlations. Of all the survey-based variables considered here,expected production is the natural candidate for anticipating actual output. Nextsection provides a methodology for implementing this idea in the context of the�ner time-scale resolution.

5. Constructing a Leading Indicator using Expected Production

The survey measure of expected production is traditionally used as a leadingindicator for actual future industrial production. Quantitatively, we can estimatefuture production using currently available information on both actual and surveymeasures through a dynamic linear model of the form:

PIMt =

pXi=1

�iPIMt�i +

pXi=1

�iEPt�i + �t

The estimated parameters for a dynamic speci�cation chosen by the Schwarz In-formation Criteria, along with their associated standard errors (in parentheses) areshown in Table 1 below.

12 PAULO PICCHETTI

Table 1Estimated Coe¢ cients

PIMt�20:285(0:071)

PIMt�30:188(0:072)

PIMt�40:213(0:073)

PIMt�50:253(0:072)

ExpProdt�10:203(0:041)

ExpProdt�20:096(0:043)

ExpProdt�5�0:076(0:036)

ExpProdt�60:072(0:032)

R2 0:93Q-stat 0:795

The coe¢ cient of multiple linear determination shows a high value, in accor-dance with the range usually obtained in this class of dynamic linear models. ThePortmanteau-test statistic for residual auto-correlation up to six lags shows no signof dynamic speci�cation problems.Whereas this result represent dynamic relationships across all time-scales simul-

taneously, we attempt to assess potential gains in estimating particular dynamicrelations for each of the estimated time-scale crystals, both for actual industrialproduction and the survey expected variable. Figure 9 compares the estimatedcrystals for industrial production and expected production for each of the time-scales considered.

1995 2000 20052.5

0.0

2.5

D6t_PIMD6t_EP

1995 2000 2005

2

0

2

D5t_PIMD5t_EP

1995 2000 2005

5

0

5

D4t_PIMD4t_EP

1995 2000 2005

20

0

20

D3t_PIMD3t_EP

1995 2000 2005

10

10

D2t_PIMD2t_EP

1995 2000 200510

0

10

D1t_PIMD1t_EP

WAVELET-BASED LEADING INDICATORS OF INDUSTRIAL ACTIVITY IN BRAZIL 13

Figure 9

There is a clear dynamical association at each time-scale, which can be estimatedby:

PIM [TSj ]t =

pXi=1

�iPIM [TSj ]t�i +

pXi=1

�iEP [TSj ]t�i + �t

TSj = SJ0; D1�D6:Particular dynamical speci�cations are chosen again on basis of optimal informationcriteria. The corresponding statistics are now presented for each particular time-scale in table 2:

Table 2Estimated Coe¢ cients

SJ0 D1 D2 D3 D4 D5 D6

PIMt�14:876(0:054)

�2:442(0:058)

1:531(0:066)

2:869(0:072)

4:192(0:068)

4:471(0:068)

5:292(0:056)

PIMt�2�9:893(0:259)

�3:564(0:136)

�2:550(0:113)

�3:698(0:223)

�7:609(0:280)

�8:228(0:307)

�11:860(0:268)

PIMt�310:806(0:514)

�3:659(0:190)

2:179(0:165)

2:446(0:348)

7:729(0:501)

7:846(0:583)

14:475(0:524)

PIMt�4�6:819(0:529)

�2:769(0:192)

�1:818(0:160)

�0:860(0:343)

�4:757(0:491)

�3:928(0:589)

�10:195(0:527)

PIMt�52:411(0:282)

�1:372(0:138)

0:745(0:107)

1:743(0:263)

0:867(0:316)

3:943(0:271)

PIMt�6�0:381(0:061)

�0:369(0:059)

�0:256(0:056)

�0:309(0:061)

�0:655(0:057)

ExpProdt�10:242(0:119)

0:521(0:074)

0:169(0:028)

�0:507(0:141)

�1:471(0:136)

ExpProdt�20:946(0:105)

0:236(0:090)

�0:389(0:097)

2:833(0:318)

ExpProdt�30:772(0:344)

1:155(0:114)

0:397(0:168)

�2:895(0:424)

ExpProdt�4�1:141(0:266)

1:075(0:100)

0:254(0:090)

1:646(0:337)

ExpProdt�50:706(0:116)

0:662(0:067)

�0:104(0:053)

0:627(0:151

�0:485(0:150)

ExpProdt�6�0:168(0:022)

0:258(0:031)

0:137(0:026)

0:061(0:030)

�0:149(0:030)

R2 0:99 0:97 0:98 0:99 0:99 0:99 0:99Q-stat 0:814 1:013 0:981 0:813 1:957 1:835 0:875

Once again, the auto-correlation tests for the residuals of each equation show no

signs of dynamic misspeci�cations, while the linear association measure shows anear-perfect �t for each of the equations.The leading indicator is now constructed summing all the individual estimated

components of the MRA, and then compared to the �tted values of the previous

14 PAULO PICCHETTI

model (averaging the time-scales). Figure 10 compares the actual industrial pro-duction index to both series of �tted values throughout the sample period, as wellas the estimated residuals for both models.

1995 2000 2005

75

100

125

fitted_averagefitted_MRAPIM

1995 2000 200510

5

0

5

10 residuals_averageresiduals_MRA

Figure 10

Clearly, the magnitude of the residuals from the model averaging the time-scalesis signi�cantly and consistently bigger than the residuals from the MRA approach.As a simple exercise, the RMSE for one-step ahead forecasts during the last 12months of the sample period is 3.71 for the previous model, compared with 0.58 forthe prediction based on individual time-scales. In conclusion, there are substantialgains in precision by building a leading indicator based on the MRA approach.

6. Implications for Cycles Analysis

The Brazilian economy underwent a series of signi�cant shocks and structuralmodi�cations during the past two decades, which mainly coincides with the sampleperiod in our analysis. The characterization of standard business-cycles in thiscontext with the available data is troublesome (Chauvet (2002)). However, shiftingthe attention to the annual growth rate of industrial production, a growth-cycleregularity seems to apply, as can be seen in Figure 11.

WAVELET-BASED LEADING INDICATORS OF INDUSTRIAL ACTIVITY IN BRAZIL 15

2 .5

0.0

2.5

5.0

7.5

10 .0

2

1

0

1

2

1995 2000 2005

PIM 12months(year_ t)/12months(year_t1)D5D6

Figure 11

Measured on the left scale is the percent variation of the twelve-month accumulatedPIM index over the previous twelve-month period. On the right scale, we measurethe estimated D5 and D6 wavelet crystals from the MODWT decomposition. Thecombined e¤ect of the D5 and D6 crystals appears to match the major turningpoints of the accumulated industrial production over the sample period. While theD5 crystal overall dynamics is very similar to the industrial production growth cycle,the D6 crystal �related to a longer time-scale �seems to reinforce it. Given thehigh dynamic correlation of the estimated crystals for the survey-based expectedproduction and actual industrial output pointed out in the previous section, itappears that the wavelet decomposition o¤ers good insights for predicting growth-cycle turning points.

7. Conclusions and Further Research

Correlations at di¤erent time-scales between survey-based expectations and in-dustrial production show a set of interesting dynamic relationships between thesevariables. The expected production variable was used to construct a leading in-dicator for actual output, and the information at the �ner resolution of di¤erenttime-scales provides encouraging improvements over the results obtained throughthe usual methodologies using information corresponding only to time variation.These �ndings provide a considerable incentive to extend this kind of analysisalong di¤erent dimensions. First, the same kind of leading indicator methodol-ogy can be tried to relate survey-based expectations to actual future realizationsof other important variables such as employment. Second, the survey data fromSondagem/FGV employed here was aggregated accross di¤erent sectors providingindustry-wide measures, but these variables are also available for di¤erent sectors,strati�ed consistently with the industrial output measured by PIM/IBGE. There-fore, the usual heterogeneity considerations motivating the analysis disagreggatedby sectors apply to the methodologies considered here, with potential bene�ts for

16 PAULO PICCHETTI

interpretation of the relationships, as well as construction of leading indicators. Fi-nally, on the methodology side, the wavelet transform comprises nowadays a largeamount of alternative speci�cations and estimation algorithms, and so additionalresearch is by all means necessary to gain an understanding on the relative meritsof these alternatives.

8. References

Abberger, K. (2007): IFO Survey on Employment Plans: Sectoral Evaluation,in Handbook of Survey-Based Business Cycle Analysis.

Chauvet, M. (2002): The Brazilian Business Cycle and Growth Cycle, RevistaBrasileira de Economia.

Crowley, P. (2007): A Guide to Wavelets for Economists, Journal of EconomicSurveys, Vol. 21, No.2.

Durbin, J. and Koopman, S. J. (2001): Time Series Analysis by State Space Meth-ods, Oxford University Press.

Gençay R., Selçuk, F. and Whitcher, B. (2002): An Introduction to Wavelets andOther Filtering Methods in Finance and Economics, Academic Press.

Harding, D. and Pagan, A. (2000): "Knowing the Cycle", in Backhouse, R. andSalanti, A., Macroeconomics and the Real World. Volume 1: Econometric Tech-niques and Macroeconomics, Oxford University Press.

Harvey, A. (1989): Forecasting, structural time series models and the Kalman�lter, Cambridge University Press.

Lucas, R. (1981): "Methods and Problems in Business Cycle Theory", in R.E.Lucas, Studies in Business Cycles Theory, Cambridge, MIT Press.

Mallat, S (1989) A Theory for Multiresolution Signal Decomposition: The WaveletRepresentation. IEEE Transactions on Pattern Analysis and Machine Intelligence,Vol. 11, No. 7.

Percival, D.B and Walden, A.T. (2000), Wavelet Methods for Time-Series Analysis,Cambridge University Press.

Priestley, M. (1996): Wavelets and time-dependent spectral analysis, Journal ofTime-Series Analysis.

Ramsey, J. (2000): The contribution of wavelets to the analysis of economic and�nancial data. In B. Silverman and J. Vassilicos (eds.), Wavelets: The Key toIntermittent Information, Volume Wavelets: the key to intermittent information.New York: Oxford University Press.

Ramsey, J. (2002) Wavelets in Economics and Finance: Past and Future. Studies

WAVELET-BASED LEADING INDICATORS OF INDUSTRIAL ACTIVITY IN BRAZIL 17

in Nonlinear Dynamics & Econometrics, Vol. 6, No. 3.

Ramsey, J. and Lampart, C. (1998): The Decomposition of Economic Relationshipsby Time Scale Using Wavelets, Studies in Nonlinear Dynamics and Econometrics.

Whitcher, B., Guttorp, P. and Percival, D. (1999) Mathematical background forwavelet estimators of cross-covariance and cross-correlation. Technical Report 38,National Research Center for Statistics and the Environment, Boulder, Seattle,USA.

9. Appendix �MODWT decompositions of the Survey Data

1992 1994 1996 1998 2000 2002 2004 2006 20080

50

100

150Global Demand Level

80

100

120

SJ0

10

0

10

D1

10

0

10

D2

20

0

20

D3

20

0

20

D4

20

0

20

D5

1992 1994 1996 1998 2000 2002 2004 2006 200820

0

20

D6

Figure A1

1992 1994 1996 1998 2000 2002 2004 2006 200860

80

100

120I nvent ory Levels

80

90

100

SJ0

5

0

5

D1

10

0

10

D2

20

0

20

D3

20

0

20

D4

10

0

10

D5

1992 1994 1996 1998 2000 2002 2004 2006 200810

0

10

D6

Figure A2

18 PAULO PICCHETTI

1992 1994 1996 1998 2000 2002 2004 2006 200860

70

80

90Level of Capacit y Ut ilizat ion

70

80

90

SJ0

2

0

2

D1

2

0

2

D2

5

0

5

D3

5

0

5

D4

2

0

2

D5

1992 1994 1996 1998 2000 2002 2004 2006 20085

0

5

D6

Figure A3

1992 1994 1996 1998 2000 2002 2004 2006 200850

60

70

80

90Cap. Ut il. Level Const ruct ion Mat er ials

60

80

100

SJ0

5

0

5

D1

5

0

5

D2

5

0

5

D3

5

0

5

D4

5

0

5

D5

1992 1994 1996 1998 2000 2002 2004 2006 20085

0

5

D6

Figure A4

1992 1994 1996 1998 2000 2002 2004 2006 200850

100

150Expect ed Employment

80

100

120

SJ0

10

0

10

D1

10

0

10

D2

20

0

20

D3

10

0

10

D4

10

0

10

D5

1992 1994 1996 1998 2000 2002 2004 2006 20085

0

5

D6

Figure A4

WAVELET-BASED LEADING INDICATORS OF INDUSTRIAL ACTIVITY IN BRAZIL 19

1992 1994 1996 1998 2000 2002 2004 2006 200850

100

150

200Expect ed Product ion

115

120

125

SJ0

20

0

20

D1

50

0

50

D2

50

0

50

D3

10

0

10

D4

5

0

5

D5

1992 1994 1996 1998 2000 2002 2004 2006 20085

0

5

D6

Figure A5