Embed Size (px)

Citation preview

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166

For your personal interest and information. These News Abstracts are compiled by the DBTG Secretariat from direct sources. Publications including Fairplay (FP),and various international agencies, as well as the research division of Clarkson and Fearnleys. They cover a wide range of issues of direct and indirect relevance to dry bulk terminal operators as well as the aims and activities of the DBTG.

Hello and welcome to the selection of news extracts for March 2017. March was a busy month for me, not least because of the DBTG Spring meeting in Gijon and all that is required to prepare for such an event - a report follows below.

Ahead of the Gijon meeting, we held an Executive Committee meeting at which the date and location for the next DBTG meeting was decided. I am pleased to announce that it will be held on the 9th/10 th of November in Punta del Este, Uruguay.

I am currently working on some other items to compliment the meeting in Uruguay so please keep an eye out for updates and more news on this over the coming weeks.

Gijon also saw us welcome Ership as a new Member and Firefly AB as an Associate Member. Ership are a Madrid based company which operates in many areas of the industry and Firefly provide spark detection, fire and dust explosion protection systems. Both are very welcome and both attended Gijon.

Up-coming over the next few weeks I am hoping to visit more Members and some of

our partner organisations. To do this I will be in Mexico later in April and early May from where I can visit our partners in the USA.

As I am sure I have mentioned before, in November last year I produced an information brochure about DBTG. This was done as a way of letting potential Members know what DBTG is and what it does. If anyone would like copies to hand to potential Members please do let me know.

Finally, as always, if there is anything contained in this Newsletter that you would like to discuss further, please don’t hesitate to contact me.

Nic Ingle - Executive [email protected]

DIARY DATES Singapore Maritime week, 22nd/28th April,

Singapore Breakbulk Europe, 24th/26th April, Antwerp Sea Asia, 25th /27th April, Singapore

IN THIS ISSUE

Gijon Report AAPA Latin America Shipping Matters Economy/Finance/Trade Commodities Terminals/Ports Ballast Water Management Freight Markets

1www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166

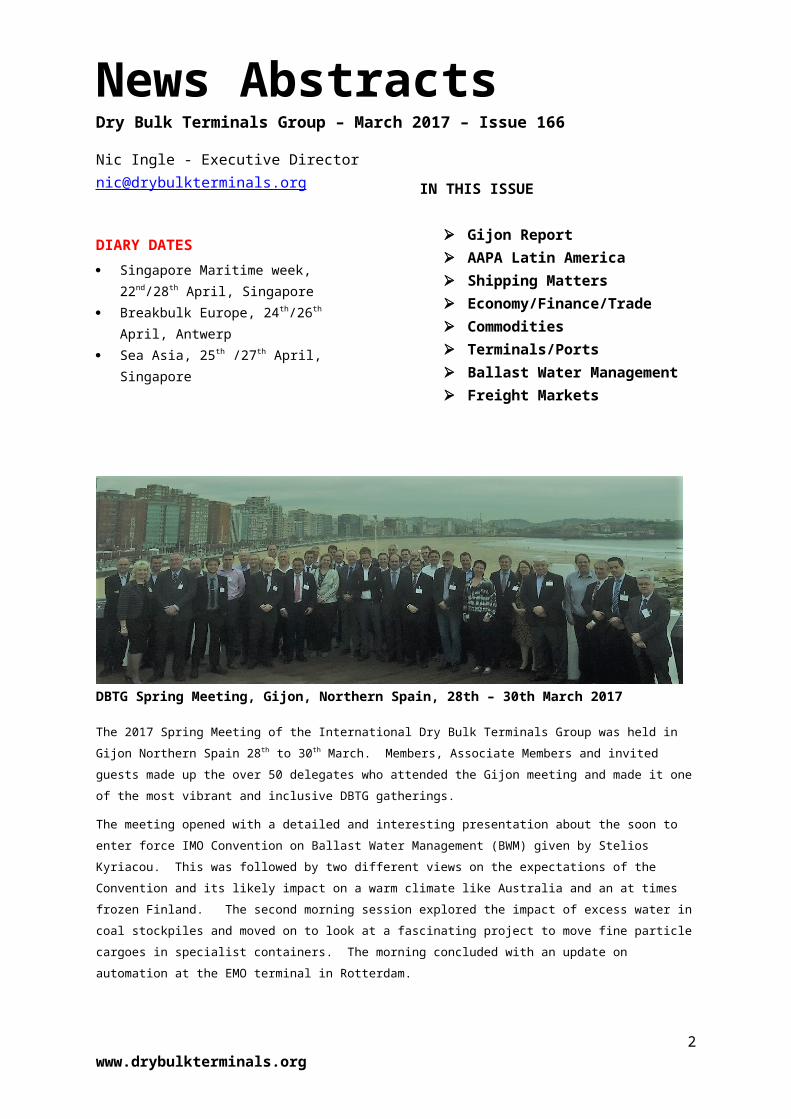

DBTG Spring Meeting, Gijon, Northern Spain, 28th – 30th March 2017

The 2017 Spring Meeting of the International Dry Bulk Terminals Group was held in Gijon Northern Spain 28 th to 30th

March. Members, Associate Members and invited guests made up the over 50 delegates who attended the Gijon meeting

and made it one of the most vibrant and inclusive DBTG gatherings.

The meeting opened with a detailed and interesting presentation about the soon to enter force IMO Convention on Ballast

Water Management (BWM) given by Stelios Kyriacou. This was followed by two different views on the expectations of the

Convention and its likely impact on a warm climate like Australia and an at times frozen Finland. The second morning

session explored the impact of excess water in coal stockpiles and moved on to look at a fascinating project to move fine

particle cargoes in specialist containers. The morning concluded with an update on automation at the EMO terminal in

Rotterdam.

A DBTG meeting would not be complete without a terminal tour and following lunch delegates visited the EBHI terminal

and toured the recently expanded Port of Gijon. The EBHI terminal is a DBTG Member and our local host and Executive

Committee Member Amalio Alvarez explained the unique aspects of his operations and detailed some of the issues they

face every day.

The second day explored a variety of environmental issues including filtration ponds and educational initiatives that engage

the community to explain port operations as well as systems that significantly decrease dust and reduce spillage. A capital

expenditure project to replace a ship unloader was also detailed. Health and Safety was then covered with a frank

explanation of some serious incidents and accidents experienced by employees of some Members, as was a serious

ship/shore crane impact accident. The day moved on to a freight and commodity market report from Susan Oatway of

Drewry and concluded with a HR exercise which ivolved all present.

The next meeting will be held in Punta del Este in Uruguay on the 9th and 10th of November 2017 – see you all there!

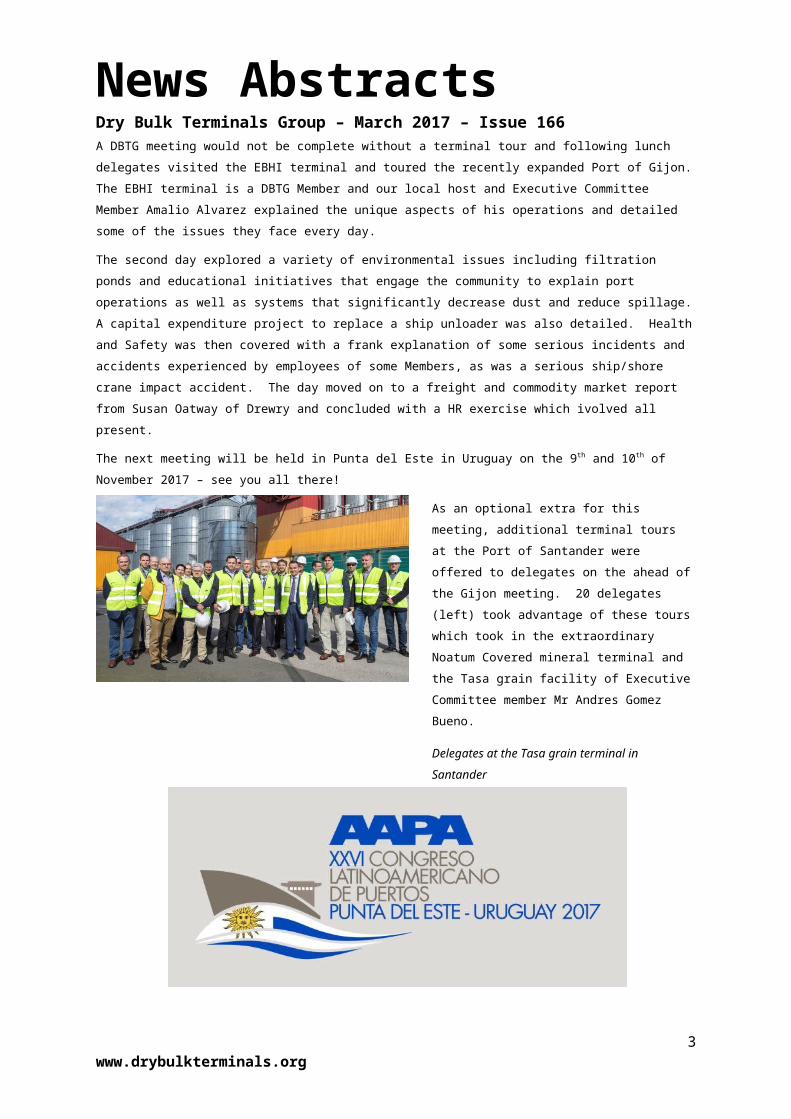

As an optional extra for this meeting, additional

terminal tours at the Port of Santander were offered

to delegates on the ahead of the Gijon meeting. 20

delegates (left) took advantage of these tours which

took in the extraordinary Noatum Covered mineral

terminal and the Tasa grain facility of Executive

Committee member Mr Andres Gomez Bueno.

Delegates at the Tasa grain terminal in Santander

2www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166

LATIN AMERICAN PORTS SET SAIL IN PUNTA

The Congress -annually gathering 400 industry leaders- will take place in the Uruguayan city of Punta del Este, one of the

most exclusive and sophisticated destinations in South America.

Latin American ports and industry service providers are getting ready for their next annual summit which will be held from

November 6th to 9th at the Conrad Hotel in Punta del Este, Uruguay.

The Congress is organized by the American Association of Port Authorities (AAPA) and the Administración Nacional de

Puertos of Uruguay (ANP).

In preparation for the event, a delegation consisting of

Rafael Díaz-Balart, AAPA Latin American Coordinator;

Alicia Abelenda, ANP Deputy General Manager; Ana

María Copello, ANP National and International

Relations Chief and Zulma Dinelli, International

Coordinator of the Latin American Congress, visited

different locales throughout the city in order to

develop an outstanding and high-level agenda of

activities, which has become the standard for the

organizers.

During the first technical inspection of the eastern city, the delegation held meetings with authorities of the Maldonado

Department, directors of the Conrad Hotel and businessmen of the region in order to conduct a detailed survey of all the

tourist and business attractions offered by the host city of the 26th Latin American Congress of Ports.

For this edition, the following institutions, port authorities and companies have already confirmed their support: Jan de

Nul, Boskalis, Van Oord, Firefly AB, Dredging International, Port of Corpus Christi, Port of Valparaíso (Chile), BEDESCHI Spa,

Tideland Signal Corp., Port of Arica (Chile), South Point Engineering, Port of Rosario (Argentina), Force Technology, Port of

Quequén (Argentina), Berenguer Ingenieros, Aplia and Grupo Lindley.

HOST CITY:

Punta del Este, internationally known as “the Pearl of Uruguay”, is located only 130 kilometers (80 miles) away from

Montevideo on a long peninsula of sand, woodlands and rocks that gives the city its name. It is one of the most important

tourist destinations in the country, and a synonym for the international jet set, good life and good taste.

MORE INFORMATION:

3www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166Those interested in receiving further information about the Congress can write to [email protected]. More

details on the event’s progress will be available soon on the website www.aapalatinoamerica.com.

ABOUT THE AAPA:

Founded in 1912 and headquartered in Alexandria, Virginia (USA), the American Association of Port Authorities (AAPA) is

the institution which represents the deep water public ports of the United States, Canada, Latin America and the

Caribbean.

The AAPA promotes the common interests of the port community and provides leadership in the areas of trade,

transportation, environment and other issues related to port development and operations.

It is also dedicated to increase public, media and especially government entities’ awareness of the essential role played by

ports in the global transportation system.

It has an extensive offering of education and training programs, conducts extensive research on the port industry, and

provides contact services and information to professionals in the sector.

Consisting of approximately 500 members, the AAPA includes most of the deep water public ports in the Western

Hemisphere, numerous fluvial ports, port operators and private terminals.More information: www.aapa-ports.org

ABOUT THE ANP:

Created in July 21st, 1916 as the highest port authority in Uruguay, the Administración Nacional de Puertos (ANP) is a decentralized entity that, in collaboration with the Ministry of Transport and Public Works, has responsibility for the administration, maintenance and development of the public ports of Montevideo, Nueva Palmira, Colonia, Juan Lacaze, Fray Bentos, Paysandú and Salto.

The Port Law #16.246 of 1992 assigned to the ANP control of realizing the national port system and promoting the decentralization of the Republic’s ports, guaranteeing the coordination of activities taking place in them and ensuring that services are offered in a system of full and open competition. More information: www.anp.com.uy

4www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166

SHIPPING MATTERS

S Korean cargo ship Stellar Daisy vanishes in South Atlantic – BBC 1st April

A huge South Korean cargo ship which had 24 people on

board has gone missing in the South Atlantic.

Two Filipino sailors found on a life raft were rescued,

AFP reported, citing a Uruguayan navy spokesman.

On Friday, a crew member sent a text saying the 312m-

long (1024ft) Stellar Daisy freighter was taking on water.

The Uruguayan navy alerted merchant ships in the area,

which began a search. A navy spokesman said they had

reported a strong smell of fuel.

The two people rescued had been found by commercial

ships aiding the search, Yonhap news agency said.

"A search operation is continuing for the 22 people," a

South Korean foreign ministry official told Reuters.

South Korea also requested assistance in the search

from Brazil and Uruguay, the official said.

The ship, a Very Large Ore Carrier (VLOC) with a capacity

of 260,000 tonnes, was being operated by a South

Korean company but was flagged to the Marshall

Islands, and had 16 Filipinos and 8 South Koreans on

board.

It had departed from Brazil, reports said.

Golden Ocean delays 10 newbuilds, returns to the black in Q4 – SMN 1st March

Golden Ocean has delayed the delivery of 10

newbuildings and agreed price cuts of $15.3m in total.

In its full year financial results Golden Ocean said that all

newbuilds due to be delivered in Q4 2016 were delayed

until Q1 this year, while all its other newbuildings due to

be delivered this year had been postponed till the first

quarter of 2018.

“In aggregate the company has achieved price

reductions of $15.3m for its remaining ten newbuildings

through negotiations with the yards,” Golden Ocean

said.

According to the company’s website it had six capsize

newbuilds remaining scheduled for delivery in 2017

from New Times Shipbuilding in China. The agreements

are subject to approval by the shipyard’s refund banks.

Golden Ocean reported a full year net loss of $127.7m

for 2016 compared to a loss of $220.8m in the previous

year. In the fourth quarter of 2016 the company

returned to the black with a net profit of $6.5m

compared to a $26.7m in the corresponding quarter a

year earlier.

“Our results improved in the fourth quarter, and better

rates will also have a positive impact on our results for

the first quarter of 2017,” said Birgitte Ringstad Vartda,

ceo of Golden Ocean Management.

“Against this market backdrop, we continued to execute

on our strategic plan by achieving further deferrals of

vessel deliveries and securing price reductions related to

the deferred newbuildings.”

Pacific Basin 2016 losses widen to $86.5m on low rates – SMN 1st March

Pacific Basin Shipping saw its 2016 net loss widen to

$86.5m from $18.5m previously as record low dry bulk

market conditions significantly undermined its ability to

5www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166generate satisfactory results and revenue slid 14% to

$1.09bn from $1.26bn previously.

The company’s core dry bulk business generated a net

loss of US$87.6m compared to a net loss of $34.7m in

2015. "2016 was an extremely poor year for dry bulk

shipping. Average market rates were even weaker than

in 2015, dragged down in the first quarter by rates not

seen for 45 years," chairman David Turnbull said in a

stock market statement.

However it added that "conditions improved over the

remainder of the year, and sentiment in the industry is

recovering".

While Pacific Basin again outperformed the market in

terms of vessel earnings and generated positive

operating cash flow, given the weak market, it still

produced a significant net loss.

Pacific Basin ceo Mats Berglund said: "Freight rates were

undermined at the start of the year by the general

seasonal slowdown in demand, lingering oversupply of

dry bulk tonnage and reduced movements of coal."

He noted that freight earnings then improved over the

remainder of the year, benefitting from increased South

American grain exports in the second quarter and

stronger US grain exports in the second half, as well as

growth in trades such as cement into North America.

Berglund said Chinese industrial activity was significantly

down at the start of the year, but improvements from

March onwards drove a revival in the iron ore and coal

trades and minor bulks such as logs, cement and copper

concentrates in the remainder of the year.

"In this difficult environment, we generated average

handysize and hupramax daily TCE earnings of $6,630

and $6,740 per day net, outperforming the BHSI and BSI

indices by 34% and 14% respectively," Berglund pointed

out.

Looking ahead, Berglund said: "2017 has started

stronger than last year, and we believe the worst of the

current market cycle is behind us and that supply-side

corrections have begun to lay the foundations for an

eventual market improvement.

"We believe 2017 will be better than 2016," he said,

however Berglund reiterated that the group still expects

"continued uncertain markets in 2017 and will continue

to conduct our business efficiently and safely while

astutely combining ships and cargoes to maximise our

margins".

Berglund continued the usual mantra that market

recovery needs lower net growth in the global dry bulk

fleet. He noted however that negligible new minor bulk

ship ordering and non-delivery of some existing

newbuilding orders should help alleviate the situation

somewhat in the next few years.

Pacific Basin is also joining other shipping related firms

such as maritime law firm Ince & Co in moving out of

costly offices in downtown Hong and will be relocating

to more cost-effective premises in Wong Chuk Hang

outside of the central business district in May.

Shipping and refiners in catch-22 over 0.5% sulphur rule – SMN 2nd March

The 0.5% fuel sulphur content cap regulation by the IMO

is less than three years away from the enforcement date

of 1 January 2020, leaving the refining and shipping

industries caught in a catch-22 situation.

The problem with the 0.5% sulphur cap regulation is

indeed a textbook conundrum for refiners (the fuel

suppliers), and shipowners (the fuel buyers), caught in a

quandary whereby suppliers are unable to commit on

how much to produce as buyers do not know how much

is needed, vice versa.

In July this year, the IMO will meet and present a more

detailed roadmap, with help from independent research

and consultancy organisation CE Delft, on how the fuel

sulphur regulation should be appropriately implemented

6www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166in order to ensure a smooth transition and mitigate

disruption to the market, according to Sushant Gupta,

director - Asia Pacific, refining and chemicals research,

Wood Mackenzie.

“The IMO could possibly be looking at a phased

introduction of the regulation rather than instant

compliance,” Sushant believed.

Heavy fuel oil (HFO), which is high in sulphur content

and considered the bane for environmentalists, is the

traditional source of energy to power ships. In 2016,

global demand for high-sulphur HFO stood at almost

70% of overall bunker fuels, including the low-sulphur

marine gas oil (MGO), or distillates, with below 0.5%

sulphur content.

The switch to burning MGO is an option for shipowners

to be in compliant with the IMO regulation, and two

other alternatives are installing abatement technology

such as scrubbers or using LNG as fuel. The use of LNG

as fuel, however, is considered a distant option due to

the global lack of LNG bunkering infrastructure, not to

mention a great deal of uncertainty regarding supplies.

“Installing scrubbers may be an economically attractive

option. Although there is an initial investment, shippers

can expect a high rate of return of between 20-50%

depending on investment cost, MGO-fuel oil spread and

ships’ fuel consumption,” Gupta said.

“Despite attractive returns, penetration rate for

scrubbers could be limited by access to finance,

scrubber manufacturing capacity, dry-dock space and

technological uncertainties. The shipping industry is

traditionally slow to move, but in this case, early

adopters may hugely benefit,” he said.

Wood Mackenzie forecast that the retrofitting or

installation of scrubbers will not pick up substantially

until 2020 due to the costly investments ranging from

$5-10m per vessel. Analyst McQuilling Services said in a

recent industry note that players with difficult access to

financing for a scrubber can look to potential

cooperation with trading companies as alternatives to

banks and investors.

Scrubber manufacturer DuPont Clean Technologies

estimated that up to 25% of the world’s fleet would be

fitted with abatement technology by 2025, and in the

run up to 2020 between 500 to 2,000 additional ships

will retrofit with scrubbers.

“Switching to MGO is a more costly solution. In full

compliance, we expect shippers to try to pass the cost to

consumers and freight rates from the Middle East to

Singapore could increase by up to $1 a barrel,” Gupta

said.

JBC Energy, a boutique oil market research company,

also noted that tonne-kilometres and freight rates for

dirty tankers are likely to receive a boost with the 0.5%

sulphur regulation. The research firm sees potential for

crude runs to have additional upside resulting from the

specification switch, while the need to optimise the

global distribution of HFO should unlock extra demand

for dirty freight.

“On top of that, requirements for floating storage of low

and high sulphur residue streams are expected to be an

additional pillar of support for freight rates over the

crucial period from 2019 through 2021,” JBC Energy

said.

In terms of demand, Wood Mackenzie’s data showed

that MGO sales are currently at approximately 700,000-

800,000 barrels per day (bpd), and they are forecast to

skyrocket to 2.8m bpd by 2020. Demand levels for HFO,

on the other hand, are at around 3.2m bpd and are

projected to plunge to 700,000 bpd by 2020.

Gupta pointed out that the change in supply landscape

would then create a dilemma for scrubber users who

would question if there will be enough HFO to burn if

refiners significantly restrict the sale of the high-sulphur

product as they reap higher margins from selling MGO.

7www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166Refiners also have their worries that any extra

production of MGO would be stranded if the more ships

equipped with scrubbers continue to consume the less

costly HFO.

“The options for refiners and ship operators will depend

on the course of action decided by each of them. At the

end of the day, the shipping industry and refineries need

to communicate and find middle ground, and time,

unfortunately, is running out,” Gupta said.

Environmental regs in focus from IMO sec-gen Lim at Panama Maritime XIII opening – SMN 14th March

On Sunday IMO secretary general Kitack Lim

inaugurated the Panama Maritime XIII World

Conference and Exhibition, the largest event of the

maritime industry in Latin America as the country’s Ship

Registry is celebrating its centenary.

“I wish to congratulate the great achievement of

Panama in celebrating 100 years of ship registry and the

major contribution it represents to the maritime sector,

together with the country’s support to the work of the

IMO, tangible with the large number of ratifications of

the conventions adopted by the organisation,”

expressed Kitack Lim.

“For IMO, 2016 was another of considerable progress on

many key areas of our work. Amongst the highlights

were the agreement on year 2020 for a global reduction

of the sulphur content of ships’ fuel oil; adopting a

mandatory requirement for ships to collect and report

data on the fuel and a road map to develop a

comprehensive strategy for reducing greenhouse gas

emissions from ships.

“It was also the year of ratification of the Ballast Water

Management Convention that triggered the entry into

force of that important instrument later this year,” Lim

said.

“The shipping industry is searching for ways to prosper

in the current climate…and while some sectors have

been hit harder than others, the overall picture has not

been good.”

However, “the IMO continues to work towards common

global standard and to enhance efficiency of maritime

trade and to pursue better regulation and listening to

the needs of the maritime industry,” Lim told the

attendees from the shipbuilding sector, from bunker and

port industries, from shipyards, classification societies,

service providers, auxiliary maritime suppliers with the

most important leaders of the maritime industry of

Panama and experts from more than 50 countries.

Panama Maritime is held every two years and is

organised by the Panama Chamber of Shipping the

Panamanian Maritime Law Association with the

collaboration of the Panama Maritime Authority (AMP)

and the Panama Canal Authority (ACP). This year the

Organising Committee president was Ms. Flor Torrijos, a

lawyer from the InterMaritime Group and representing

the Panama Maritime Law Association.

At the end of the opening ceremony, an award was

made to relevant industry players amongst them, the

award given to the Panama Canal Administrator, Jorge L.

Quijano, who was chosen as the "Maritime Personality

of the Year".

The conference was initiated Monday with

presentations from Jorge Barakat, Minister of Maritime

Affairs and the award-winning. Quijano, followed by

speakers from the presidents of the Shipowners'

Association of South Korea and Greece, representatives

of companies such as Oldendorff Carriers, Wärtsilä

North America, Chemoil Corp and many others as the

conference extends to Wednesday.

8www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166Cyprus back into shipping – SMN 23rd March

Cyprus is back. Decisive reforms, prudent fiscal

management, hard work and the peoples' determination

have seen the country exit earlier than expected from

the economic adjustment programme instigated by the

its creditors.

“We can proudly – once more – connect Cyprus to

growth and potential. The Cypriot economy is emerging

stronger and stands ready to face current challenges,

utilising its full potential,” the country’s president Nicos

Anastasiades declared in New York on 22 March.

He said the state has gained access to lending with

interest rates which are now at historically low levels, as

a result of continuous upgrading of the economy by

international rating agencies. The banking sector has

also now been restructured and recapitalised mostly

through private funds, becoming smaller with more

effective management and supervision and the shipping

and tourism sectors are again flourishing.

Addressing the Capital Link Invest in Cyprus Forum,

Anastasiades said: “Already in 2015 the Cyprus economy

had recorded a positive growth rate of 1.7%. For 2016

growth was at 2.8%, one of the highest in the European

Union. Most importantly this growth rate is expected to

stay at this level for the next few years.”

Anastasiades said that despite the economic difficulties

faced, Cyprus’ comparative advantages “not only remain

intact, but have been further enhanced and expanded,

setting them apart from most investment destinations”.

He said Cyprus has one of the lowest and most

competitive corporate tax rates in Europe at 12.5%,

“deeming it an attractive investment destination, and a

highly competitive centre for international businesses,

offering a platform for operations and preferential

access to markets like Europe, Middle East, North Africa

and Asia”.

Marios Demetriades, Cyprus’ communication & works

minister, said shipping is an invaluable asset for Cyprus

with significant political and economic advantages.

“Despite the international adverse economic conditions,

the Cyprus shipping sector has managed to maintain its

competitiveness and grow further," he said.

Demetriades said Cyprus “managed to maintain a high

quality fleet through the implementation of all

internationally applicable safety, security and

environmental protection standards”.

“Currently, Cyprus shipping offers a wide range of fiscal

and economic incentives, including competitive ship

registration costs and annual tonnage taxes, ensuring

the fleet's worldwide competitiveness,” he said. “On the

logistics side, Cyprus fulfils all criteria to become a trade

hub in the region, due to its strategic location. This

particularly applies in relation to the latest

developments in the energy sector in Eastern

Mediterranean and the need of companies to be based

out of a stable country in the region like Cyprus.”

Andreas Hadjiyiannis, president of Cyprus Sea Lines and

of the Cyprus Union of Shipowners (CUS), said the CUS is

“committed to the further development and growth of

the Cyprus flag and to Cyprus attracting more business

and investment to the wide range of opportunities that

our country offers”.

Columbia Shipmanagement managing director Andreas

Hadjipetrou said the fact the company is headquartered

in Limassol shows “Cyprus can be a hub for international

shipping businesses to grow”. He noted “it is estimated

20% of the global third-party ship management fleet is

controlled from Cyprus employing around 4,500 highly

qualified personnel and 55,000 seafarers.”

Hadjipetrou said: “Historically the governments have

been supportive of the maritime cluster and this has

resulted in the innovative tonnage tax system and

superb local expertise.”

9www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166

Nowhere to go? Fiji bans dirty bulker DL Marigold after expulsion from NZ – SMN 8th March

Fiji has banned the bulker DL Marigold from entering its

waters after it was expelled from New Zealand over

“severe” bio-fouling on its hull.

The Korean-owned, 2012-built, bulker had planned to

head to Fiji for hull cleaning after it was expelled by New

Zealand’s Ministry of Primary Industries (MPI) on

Sunday.

Biosecurity Authority of Fiji ceo Xavier Khan was

reported as saying it had issued an inspection certificate

to local agents Campbell Shipping that DL Marigold

would not be allowed into Fijian waters to clean its hull.

Divers in New Zealand had found the ship to have dense

fouling of barnacles and tube worms on its hull and

other underwater surfaces.

Khan said the bio-fouling on the vessel could introduce

invasive species into Fijian waters. "This will never be

allowed as it would be very devastating for the Fijian

marine and aquatic species."

The DL Marigold had planned to call in Fiji on 10 March

specifically to have its hull cleaned before returning to

New Zealand to finish discharging its cargo of palm oil

expeller.

New Zealand authorities said the vessel would not be

allowed back in its waters until its hull had been

thoroughly cleaned.

The latest move by the Fijian authorities to ban the DL

Marigold from entering its waters would appear to leave

the vessel in limbo.

Panama Canal sets new daily tonnage record in February – SMN 10th March

The Panama Canal set a new daily tonnage record in

February 2017 of 1.18m Panama Canal tonnes (PC/UMS)

with a total of 1,180 vessels through both the expanded

and original locks.

The previous record was established in January 2017

when the canal recorded a daily tonnage average of 1.16

PC/UMS.

February is the third-consecutive record-breaking month

for the Panama Canal. In December 2016 and January

2017, the waterway set monthly tonnage records after

transiting 35.4m PC/UMS and 36.1m PC/UMS,

respectfully.

“These records are evidence of the maritime industry’s

growing adoption of the expanded canal,” said Panama

Canal administrator Jorge L. Quijano. “As the new lane

continues to reshape global maritime trade and its true

impact becoming more and more apparent, we will

continue to offer new growth opportunities to our

customers and cargo destinations around the world.”

Eight months since the inauguration [of the new locks],

approximately 850 neo-panamax vessels have transited

the new locks, and 53% of containerised cargo transiting

the waterway is using the expanded canal. In addition,

11 new liner services have been re-routed to take

advantage of the economies of scale the canal offers. As

the impact of the expansion becomes more evident, this

number is expected to increase.

Further, LPG and LNG vessels, as well as bulk carriers,

tankers and vehicle carriers have transited the expanded

canal since it became operational last June 2016.

10www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166And in April 2017, the first neo-panamax cruise ship,

capable of carrying up to 4,000 passengers, will transit

the new locks.

China steel and coal production cuts give dry bulk freight a boost – SMN 10th March

Freight rates might never be the same – at least as

compared to last year’s doldrums - and instead are

looking to push to new highs. It may be some way off

the “boom-time” highs but the Baltic Dry Index (BDI)

pushed past the 1,000-point level, its steepest climb

since mid-February 2017.

By Wednesday, the BDI had climbed to 1,045 points up

6% since Monday’s 979 points – a positive trend when

compared to the low of 300-400 points in the

corresponding period of last year.

Perhaps the higher rates stemmed from market

optimism set in motion by higher commodity prices

especially on iron ore and coal. Both commodities seem

to be gearing up for higher rates as market direction

from China becomes clearer after the National People’s

Congress meeting last week.

During the meeting, the Chinese authorities pledged

further capacity cuts in steel and coal production of 50m

tonnes and 150m tonnes respectively. The Chinese

government also adopted an infrastructure spending

package to keep its economy growing at around 6.5% or

higher for 2017.

The plan is for RMB800bn ($116bn) of investment in

construction of rail networks in the country followed

RMB1.8trn infrastructure spending on road and

waterways projects.

On this basis, FIS expects China to import more coal due

to the production constraints in the country. Moreover,

the stricter environmental protection measures may

prompt the Chinese mills to import higher grade iron ore

to reduce emissions.

With higher imports, the outlook for dry bulk looks

promising for the rest of the year, and “some traders

have suggested we may well be seeing higher levels for

capesizes in the coming days,” said an FIS broker.

HSH Nordbank rejects latest restructuring proposal for Rickmers Maritime – SMN 13th March

HSH Nordbank has rejected the latest restructuring

proposal for Rickmers Maritime from financial advisor

Ferrier Hodgson.

Following the rejection by SGD100m noteholders of a

proposed financial restructuring last December the

further restructuring proposals had been sought for the

embattled Singapore shipping trust.

Rickmers Trust Management (RMT) said they met with

major creditor HSH Nordbank on 7 March to see if the

senior lender’s financial advisor Ferrier Hodgson secured

a “credible alternative restructuring proposal” to

restructure the notes.

“The senior lender informed the Trustee-Manager that

its financial adviser’s proposed restructuring proposal

for the restructuring of the notes was not acceptable to

the senior lender,” RMT said in a statement.

11www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166HSH Nordbank advised RMT to formulate a revised

restructuring proposal. No further discussions on a

restructuring proposal are ongoing between HSH

Norbank and Ferrier Hodgson, with the restructuring of

the notes likely to be further delayed.

The Trust is now seeking debt forgiveness on its existing

loans from the senior lender, which has “indicated it

maybe willing” given similar agreement from

noteholders and other unsecured lenders with recovery

that would be higher than the winding-up of the Trust.

“In all other cases, the senior lender indicated it would

support an orderly winding-up of the Trust,” RTM said.

“Further to the above, the Trustee-Manager is currently

in discussions with its advisers to formulate a new

framework for restructuring the liabilities of the Trust

and intends to present such new restructuring proposal

to its creditors and noteholders when it has been

finalized.”

Greek fleet grows by 3.5m gt in 2016 – SMN 17th March

The Greek shipping community has long slammed the

Athens government for not taking advantage of the

potential the maritime industry offers to the struggling

Greek economy and the latest overview of the Greek

fleet adds weight to the argument.

Despite the on-going tax issues and the country’s

economic woes the growth of the Greek-controlled

armada continues at a pace and at the beginning of

March stood at record levels.

The fleet of ships over 1,000 gt 1 March comprised

4,084 ships of 329m dwt and 192.4m gt, just seven

vessels more than a year ago, but some 8.16m dwt and

3.52m gt more.

The figures include 196 vessels of 20.6m dwt and

12.34m gt, on order from shipyards around the globe

according to data compiled for the 30th consecutive

year by the London-based Greek Shipping Cooperation

Committee (GSCC).

However, the home flag fleet has decreased in all

categories and according to data provide to the GSCC

shipowners’ body by IHS Markit, the Greek flag flies over

747 ships, of 75.21m dwt and 43.71m gt, a significant

loss of 62 ships, 3.74m dwt and 2.34m gt over the 12

months.

In fact, the Greek flag is the third choice of home owners

with the fleet registered under some 41 flags all told, led

by the Marshall Islands which gained 74 ships in the 12

months to March, ahead of Liberia which gained 31

ships. Cyprus gained 13 ships, and Malta four overall

with, like the Greek, a decrease for all other flags.

Notably, Greek parent companies represent 25.2% of

the world tanker fleet and 16.2% of the ore and bulk

fleet. Overall, the Greek owned fleet comprises 7.6% of

the world’s ships, 13.7% of gt and 16.2% of dwt.

Average age of the Greek-controlled fleet in ship terms

increased slightly but, nevertheless, continues to be 2.9

years below the world average age standing at 10.3

years. It is 8.7 years in terms of gt and 8.6 years in dwt

terms.

When it comes to classification, LR's Greek fleet

comprises 834 ships (856 ships in 2016); ABS: 768 ships

(779 in 2016); ClassNK: 744 ships (732 in 2016); BV: 688

ships (681 in 2016); DNV GL: 668 ships, down from 702

ships in 2016 and RINA 191 ships, a gain over the year of

26 ships. When it comes to the Greek flag fleet, LR has

223 ships (261 in 2016); ABS 207 ships (211 in 2016);

DNV GL 117 ships (130 in 2016); RINA 80 ships (78 in

2016); BV 66 ships, (77 in 2016) and ClassNK 20 ships,

down five from a year ago.

Dry bulk freight market seizes the day – SMN 17th March

12www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166Riding high on wave of market optimism, freight rates

have entered an upwards phase as result of seasonally

high demand for steel and iron ore in China. The bullish

market is prompting freight market participants to seize

the moment and capitalize on the flow of steel

production in China.

As a result of the surging demand, the Baltic Dry Index

rocketed from very low to quite low (1,147 points) on

Wednesday, spurred on by the three-day consecutive

gains made in capesize rates. By Thursday it had hit a

three-month high climbing to 1,172 points.

“Early talk of C5 rates slipping caused a brief pause from

paper buyers but Atlantic strength added more fuel to

the fire as the trading progressed,” said an FIS FFA

broker explaining the capesize market’s rise on Tuesday.

Capesize rates increased by $607 or 5% day-on-day on

Tuesday to $14,250 from Monday’s starting position of

$13,643, followed by an even greater stride of 10% day-

on-day rise on Wednesday to $15,764.

Despite the high demand for raw materials, uncertainty

may lie ahead if China enacts a policy of stricter safety

regulations and environmental protection measures.

The country’s policymakers have extended restrictions

on sintering output in Tangshan by a further three days,

having an immediate, if temporary effect on the

seaborne import of iron ore due to reduced production

of the Tangshan mills.

China’s policy-makers have also sent mixed signals on

the coal market without clearly specifying whether they

will revert back to a 276-working day ‘working year’, a

decision expected in mid-March 2017. Instead, they

announced that the country will continue to reduce

150m mt of coal this year. However, the statement did

not distinguish between thermal and coking coal and the

impact on coking coal supply remains ambiguous.

It was a different story on the Panamax market where

rates scaled back to $9,248 on Wednesday, down by 5%

from the starting point of $9,697 recorded on Monday.

“We witnessed further declines today on panamax

paper as the build-up of tonnage on TA/FH business

brought with it another sharp decline in the index,” said

an FIS FFA broker based in Asia. According to the broker,

many panamax sellers have adopted a cautious attitude

in lieu of the firmer capesize market.

Panamax sellers continued to apply some pressure to

the front of the curve with April and Q2 sold off to

$9650 and $9450 before bouncing back somewhat,

leaving the prompt months looking relatively flat

towards the week’s end.

Supramax rates too remained virtually flat, trading from

$9,151 to $9,171 on Wednesday while handysize rates

saw steady growth from $7,340 on Monday to $7,413 on

Wednesday.

As we approach the end of quarter, perhaps we should

remember the words of the great poet Horace who

opined "Seize the day, put very little trust in tomorrow”

perhaps a fitting epithet for judging the freight market’s

current situation against its future prospects.

2017 a year of retrenchment rather than improvement: Moore Stephens – SMN 22nd March

2017 for shipping will be a year of retrenchment rather

than improvement, according to what most respondents

believed in a regular survey conducted by Moore

Stephens, with shipping confidence holding steady in

the three months to end-February 2017.

Apart from anticipated job losses, respondents generally

felt that competition was running at very high levels,

while other familiar concerns included vessel

overtonnage and geopolitical uncertainty.

In the three months ended 28 February 2017, the

average confidence level expressed by respondents was

5.6 out of 10, unchanged from the previous survey in

13www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166November 2016, according to international accountant

and shipping adviser Moore Stephens.

Owners were the only main category to show an

improved level of confidence, up from 5.4 to 5.6.

Confidence on the part of charterers was down from its

all-time survey high of 6.8 to 5.9, while that of managers

fell from 6.4 to 6. Confidence levels in the broking

sector, meanwhile, dropped from 5.6 to 4.6.

Confidence was up in Europe and North America, from

5.4 to 5.5 and 5.9 to 6.1 respectively, but down from 5.7

to 5.6 in Asia.

One respondent commented: “If owners can maintain

their discipline and resist the blandishments of shipyards

desperate for business, there is hope that 2018 will see

a return of market equilibrium, in which continued

scrapping remains a key element.” Another, meanwhile,

noted: “The current state of most shipping markets,

coupled with the weakness of banks, means that

conditions should be more attractive for alternative

lenders.”

Demand trends overtook competition as the factor

expected to influence performance most significantly

over the next 12 months, followed by finance costs and

tonnage supply. “Competition is so intense at the

moment that you either accept what is offered or a

competitor will take the cargo,” said one respondent.

The number of respondents expecting higher rates in

the tanker market over the next 12 months fell by eight

percentage points to 25%, while the number anticipating

lower tanker rates rose from 24% to 28%.

In the dry bulk sector, there was a three-percentage-

point rise to 44% in the numbers anticipating higher

rates. One respondent, however, remarked: “The dry

bulk freight market will continue to be tough, with

returns not much above breakeven.”

In container shipping, the numbers expecting higher

rates rose from 27% to 31%, while there was a three-

percentage-point fall, to 18%, in those anticipating lower

container ship rates.

Richard Greiner, Moore Stephens partner, shipping &

transport, said: “The issues facing the industry include

an oversupply of ships and insufficient demolition.

Freight markets are dragging along the bottom in many

sectors, with net rate sentiment in the tanker market

being particularly low. Add to this the expectation of

higher ship finance costs, the mounting costs of

regulation, the threat of cyber-crime and projected

increases in operating costs and it is evident that

shipping will not be a picnic for the foreseeable future.”

Dry bulk freight: where next for the commodities upcycle? – SMN 24th March

The shine came off the commodities rebound this week,

as the price of iron ore fell 4% on Wednesday (from a

high above $90 per tonne this month) as traders

anticipated a reduction of Chinese steel demand.

If the downward correction persists, the question will be

how much freight rates are affected and move with the

price move or whether the freight market can continue

to defy bearish sentiment. To judge from the early

results, the price fall was a signal for more fixing as the

week came to a close.

14www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166

The capesize 5TC index slid by 4% since Monday from

$18,080 to $17,292 on Wednesday. The price decline

reflected the lacklustre fixing activity during the week as

well as lower seaborne iron ore demand.

The fall is awkwardly timed since the start of Q2 should

be the start of higher seasonal demand as construction

activity intensifies in China, prompting more imports of

iron ore. It is likely that the restocking had gone too well

during first quarter – bringing port inventory levels to

over 130m tonnes.

In addition, heavy weather conditions off Australian

loadports also disrupted capesize shipping activities on

the Western Australia to Qingdao route. As such, the

Pilbara Ports Authority issued a cyclone warning at Port

Dampier on Wednesday.

“The passing cyclone not only slowed down activity but

created an air of uncertainty which some felt would lead

to continued negative sentiment,” added the FIS FFA

broker.

However by Thursday, capesize paper rates had

rebounded. In the early session there was little physical

data to justify the move but by the afternoon details of

better fixtures hit the airwaves. The Pacific was quieter

thanks to the cyclone but the transatlantic remained

very solid with the trip out via Brazil particularly firm.

Panamax freight rates have also been gaining ground

steadily and might see further upturn, driven on by

robust soyabean demand in China. For instance, the

panamax TC average began the week at $8,875 before

closing at $8,998 on Wednesday, booking a gain of $123.

“With the emergence of a few more Atlantic cargoes,

lending further support to the panamax market and the

index flattening out, we saw continued appetite from

buyers across the curve.” said the FIS FFA broker.

It’s possible that panamax freight rates could see

continued support into the middle of Q2 due to the

strong agribulk demand from China.

Meanwhile, supramax freight rates remained virtually

unchanged through the week, recording $9,245 on

Monday then $9,289 on Wednesday. In contrast,

handysize freight rates saw steady gains throughout the

week, posting $7,573 on Wednesday from a starting

point of $7,499 on Monday. Despite the gains in smaller

and midsize ships, the overall Baltic Dry Index (BDI)

dipped by 10 points to 1,190 points on Wednesday.

Whether China’s steel demand rally will sputter out

remains to be seen, but as the proverb goes; “a journey

of a thousand miles begins with a single step”, thus it

may be too early to judge which way the market will go

in the near term.

Prepare for challenges to stay relevant, say maritime leaders – SMN 31st March

Maritime leaders today called for the industry to

proactively prepare for future challenges to not only

remain competitive and relevant in today’s volatile

market environment, but to also future-proof the

industry.

Speaking at a briefing session ahead of the Sea Asia 2017

conference and exhibition in April, the four industry

leaders pointed out the importance of investing in

solutions now to ensure companies are well-placed to

navigate future headwinds such as regulation changes,

while better understanding the impact of technology.

René Piil Pedersen, chairman for the International

Committee of the Singapore Shipping Association (SSA),

said despite challenges in 2016, this year is looking to be

a better year for the industry, with projected growth of

two to four per cent in container shipping demand as

well as growing demand in bulk and tanker segments.

15www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166“The container industry is not out of the woods yet, but

we are seeing most trades being in better balance after

record-low freight rates in 2016. This could lead to a

more sustainable industry in 2017 supported by the

increased consolidation activity. In the bulk segment,

there is optimism while the coming year’s newbuilding

program will be decisive for the tanker segment” said

Pedersen.

Digitalisation also presents a huge opportunity for the

industry, according to Pedersen.

“Digitalisation can give companies the possibility to

engage with customers in a way that creates more value

to the customers, just as Big Data can be used to

operate assets more efficiently. Two to three years ago,

you’d see a container booking take two hours, whereas

today it takes minutes, and in the next few years, it will

likely take seconds.

“With the growing focus on e-commerce and digital

solutions, SMEs and consumers who were not directly

linked to the global supply chains, now have the

opportunity to connect, giving companies the

opportunity to address consumer needs in a more direct

and efficient way than ever before,” he said.

Tan Beng Tee, assistant chief executive (development) of

the Maritime and Port Authority of Singapore (MPA)

emphasised the importance of industry players keeping

an eye on the future, especially with the fast pace of

technology adoption.

“The advent of digitalisation will help improve processes

in the industry but it will also disrupt the way you do

business. With this in mind, there is a need for us to be

prepared and start thinking about the new business

models that will arise as a result of digitalisation in the

industry.

“Another area we need to start focusing on is the skills

of our workforce. Shipping is a traditional and

documents intensive industry. This will no longer be the

case in the future with blockchain coming into the

market. New skills will be required and we will need to

start equipping our workforce with cross-disciplinary

skills such as IT literacy and data analytics,” said Tan.

The panellists also discussed the importance of solid risk

management as the industry anticipates major structural

changes with new mega-alliances, mergers and

acquisitions, in addition to an increasingly demanding

regulatory environment and compliance issues.

K Murali Pany, managing partner at Joseph Tan Jude

Benny (JTJB) LLP, stressed that companies must re-

evaluate their business models with a view to invest in

risk management.

With more regulatory changes coming such as the

Ballast Water Management Convention and the low

sulphur cap by 2020, Pany said compliance with these is

key to risk management.

“In line with this, companies need to have and invest in

more stringent and stronger risk management

programmes. The key to this is setting up the right

procedures, protocols and technological structures,” he

said.

Marcus Hand, editor of Seatrade Maritime News, said

these are some of the discussions that will be taking

place at Sea Asia 2017, including conversations around

the implications of disruptive and innovative technology

for the future of shipping.

“In addition to market challenges, the industry will need

to prepare itself for the wave of technological change

that has already begun to take place. Industry players

need to look ahead and see how they can leverage

current opportunities in the industry, while at the same

time ensuring they have proper safeguards ready to

tackle barriers in the future.

“This year’s edition of Sea Asia 2017 will explore some of

these opportunities and barriers, and it will provide an

international platform for maritime leaders to come

16www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166together and share with one another insights on how

they can shape the course of the global maritime

industry.

“With more than 16,000 people expected to come for

this year’s Sea Asia, we are looking forward to fruitful

discussions that can further propel the industry

forward,” said Hand.

Bronka trials containerised bulk solution – PSM 15th March

The testing of a new container for bulk cargo is being

tested at the container terminal of the Multipurpose Sea

Cargo Complex (MSCC) Bronka.

Designed by Yuna Llc, the container and its technology

aim to allow it to be transported efficiently by rail,

accumulate bulk cargo in the port and tranship bulk

cargoes without the construction of a specialised

terminal.

“The project is attractive because to use this

development there is no need for additional

investments in the infrastructure of the port and crane

equipment,” commented Aleksei Shukletsov, executive

director of Fenix LLC – the investor and operator of

MSCC Bronka.

He added: “For example, it can be used for fertilizers.

This experience is very important for Bronka, as an

advanced innovative platform, since it lets develop the

technologies and open up new opportunities for the

Russian market of transport and logistics services.”

The container meets the requirements of Russian

Railways and is compatible with standard container

handling equipment.

The amount of dry bulk shipload depends on the

number of containers, area available for stacking and

the depth at berths.

A positive of the containers are the environmental

aspect, it will allow eco-friendly ports to handle cargoes

of high pollution risk without damage to the

environment.

MSCC Bronka is a new deepwater port of Saint-

Petersburg, its Phase 1 capacity is 1.45m TEU and

260,000 units of Ro-Ro cargoes.

In the future, the MSCC Bronka expansion will help

increase the facility's container throughput to 1.9m TEU

Cyber risks of increased automation – PSM 29th March

With increasing automation of systems and equipment,

expect a marked uptick in the number of cyber attacks

on ports, a security specialist has warned.

Speaking at Navis World, Darich Runyan, senior director,

information security at Virginia Port Authority, said the

increasing public awareness of automation uptake in

terminals leaves the sector vulnerable to hackers.

“We are underprepared for what’s out there in terms of

cyber threats. As we see more press about terminals

going online and being automated we are going to see

more uptake of cyber attacks,” he said. “The more we

automate, the more dependent we are on data

therefore the integrity of the data is paramount.” -

The internet has lowered the entry barrier for hackers

and since 2010 there has been a significant increase in

attacks on automation. The majority of these attacks

come from external sources.

One weak point is external vendors that plug into

operational systems, yet don’t support encryption or

even passwords. “When an engineer comes in and plugs

into a crane that can be a breach of your network,” said

Mr Runyan.

If a terminal has been compromised it may not even

know until months after the breach, he continued.

“When an attacker comes in there is a lot of planning

and scoping. Then comes reconnaissance and scanning.

The third step is exploitation. This all takes time –

17www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166hackers can start a year or so before they actually attack

and it can take months to detect.”

Mr Runyan advises that ports implement a number of

strategies, including adhering to the principal of least

privilege – never let anyone know more than they need

to do their job; whitelisting of applications; proper

configuration management – knowing what’s on every

machine; and implementing identity management.

He recommended that ports deploy the CIS diagnostic

critical controls for corporate networks: “Just

implementing 50% of these will reduce over 90% of

attacks.” He also advised that ports undertake exercises

to test resilience and implement a user awareness

campaign. “The users are the weakest link".”

He added that cyber security must be initiated from the

top down: “Sites that are successfully deploying have

CISOs that report directly to the CEO.”

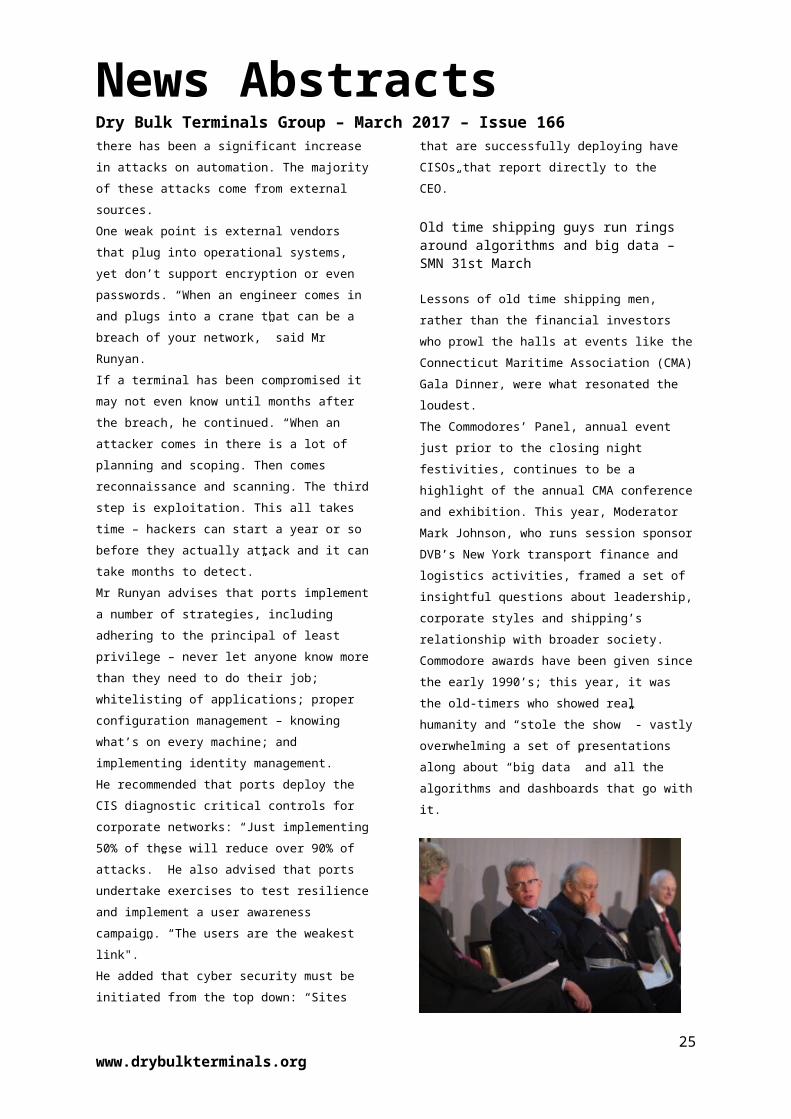

Old time shipping guys run rings around algorithms and big data – SMN 31st March

Lessons of old time shipping men, rather than the

financial investors who prowl the halls at events like the

Connecticut Maritime Association (CMA) Gala Dinner,

were what resonated the loudest.

The Commodores’ Panel, annual event just prior to the

closing night festivities, continues to be a highlight of

the annual CMA conference and exhibition. This year,

Moderator Mark Johnson, who runs session sponsor

DVB’s New York transport finance and logistics activities,

framed a set of insightful questions about leadership,

corporate styles and shipping’s relationship with

broader society. Commodore awards have been given

since the early 1990’s; this year, it was the old-timers

who showed real humanity and “stole the show” - vastly

overwhelming a set of presentations along about “big

data” and all the algorithms and dashboards that go

with it.

Throughout the session, the CMA’s 2005 Commodore, C

Sean Day, who spent time as a banker crafting shipping

companies before linking up with the Teekay Group,

talked about the harmonies among seafarers, the

corporate purpose and the value of the equity. “If you

treat seafarers with respect, it’s better for everyone,” he

said.

The CMA’s 2017 Commodore, Jack Noonan, honored

several hours later, talked about how financial value was

preserved because the company’s “platform”,

buttressed by the company’s people, remained in place

during the difficult times for Chembulk Tankers (which

he leads) and its then parent, Berlian Laju Tankers.

The CMA’s 1995 Commodore, Gregory

Hadjieleftheriadis, one of four of Eletson Corporation’s

founding partners, talked about his roots as a sea

captain and how forming a tanker company was a logical

progression. “If you have everything else the money will

come and find you,” he said referring to providing a

good service and treating staff with respect.

In stark contrast to the investment mentality often on

display at industry conventions, the now retired

Hadjieleftheriadis said, “You have to provide a service,

irrespective of the market conditions need to provide it

in all conditions. ” He added: “This will establish you as

someone who the client will come back to… again and

again. This philosophy was the driver behind our

company.”

During his remarks, he added that Eletson outfitted

vessels with holding tanks for ballast and waste tanks in

the 1980’s - more than 20 years prior to the onset of the

present BWT-mania and discussions about shore

reception facilities.

18www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166Jack Noonan, during his dinner speech, summarized the

ying and the yang of modern business and old time

shipping, telling the 600 plus dinner guests, “I now sit in

the corner office, but I was once a seafarer.”

Courage Marine narrows 2016 loss to $18m – SMN 30th March

Dry bulk firm Courage Marine managed to halve losses

for 2016 to $17.8m from $36.8m previously even though

revenue decreased by 32% to $4.5m from $6.7m in 2015

as impairments did not take such a big chunk out of the

results as the year before.

Courage blamed the decrease in the group’s revenue

mainly on the drop in revenue in the key marine

transportation business as demand for vessel chartering

and freight rate remained low throughout most of 2016.

Operating losses were also reduced because less vessels

were being operated during the year due to the weak

operating environment.

The marine transportation business generated revenue

of $3.6m 46% down from $6.6m in the previous

corresponding period as low demand for commodities in

the Greater China Region in recent years has adversely

impacted the demand for vessel chartering in the dry

bulk market throughout most part of 2016, Courage

said.

"In addition, the oversupply of vessels has put extra

pressure on freight rate in dry bulk market... The

sluggish demand for vessel chartering and hence low

utilisation rate of the group’s vessels, together with low

freight rate were the main causes that led to the decline

of the operation’s revenue," the group said.

The marine transportation business recorded an

operating loss of $3.3m although this was an

improvement on the $5.2m loss recorded in 2015, due

to lower operating costs as fewer vessels were

chartered out and the disposal of two loss-making

vessels.

However, impairment charges of $10.8m had to be

taken on the fair value of two vessels Zorina and Heroic,

held by the group, although this was an improvement

over the $20.7m charge the year before.

Looking ahead, Courage said: "The board is of the view

that the operating environment of the group’s marine

transportation business will continue to be difficult in

the near term.

"It has therefore decided to shift its focus to plan to

progressively put more emphasis on the property

holding and investment, investment holding and

merchandise trading segments, which are expected to

make positive contributions to the group in terms of

revenue and profitability and boost overall results in

future.”

World's largest containership delivered to Mitsui OSK Lines – SMN 28th March

The world’s largest containership, the MOL Triumph, has

been delivered to Mitsui OSK Lines (MOL) from Samsung

Heavy Industries.

At 400 meters in length and 58.8 meters in width, MOL

Triumph is currently the world’s largest containership.

And with a capacity of 20,170 TEU, the vessel is the first

20,000 TEU-class containership deployed in THE

Alliance’s Asia to Europe trade via the FE2 service.

MOL’s newest vessel is the first of a fleet of six 20,000

TEU-class containerships for the company, the second of

which is due to be delivered in May 2017.

19www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166

Junichiro Ikeda, president and ceo of MOL said: “The

MOL Group is honoured to unveil this new vessel, which

is the largest containership in the world. The vessel is

equipped with various new sustainable technologies to

provide more efficient fuel consumption and improved

environmental performance.”

The new 20,000 TEU-class containerships are equipped

with various highly advanced energy-saving technologies

including low friction underwater paint, high efficiency

propeller and rudder.

The vessel has also been designed with the retrofit

option to convert to LNG fueled ship in view of the

implementation of the International Maritime

Organisation’s new regulation to limit SOx emission in

marine fuels which will come into effect in 2020.

MOL Triumph will set off on her maiden voyage from

Xingang in April 2017 and will sail to Dalian, Qingdao,

Shanghai, Ningbo, Hong Kong, Yantian and Singapore.

She will then transit through the Suez Canal and

continue on to Tangier, Southampton, Hamburg,

Rotterdam and Le Havre. She will then call at Tangier

and Jebel Ali on the way back to Asia.

Eco-friendly ultramax pair joins U-Ming fleet – SMN 29th March

A pair of eco-friendly ultramax bulk carriers, Asian

Summit and Asian Prominence, have joined U-Ming

Marine Transport Corporation’s fleet following a

christening and delivery ceremony held on Tuesday at

Japan’s Oshima Shipbuilding yard.

The two 62,466-dwt ships are the second and third of

the ultramax series built for Taiwan’s U-Ming by the

Japanese shipyard.

At present, there are three more new vessels being

ordered and under construction by Oshima Shipbuilding

and they are expected to be delivered by 2019.

The new ultramaxes Asian Summit and Asian

Prominence are tested to achieve fuel saving of at least

25%, and the CO2 emissions of the ships have exceeded

the IMO Energy Efficiency Design Index (EEDI) reference

value by 32%.

U-Ming has also installed ballast water treatment

system onboard the ships, ahead of the IMO Ballast

Water Management Convention set to enter into force

in September 2017.

U-Ming currently owns and operates 48 vessels

including dry bulk carriers of capesizes, post-panamaxes,

kamsarmaxes, panamaxes, ultramaxes and supramaxes.

Baltic Exchange outlines changes to dry bulk shipping indices – SMN 29th March

The Baltic Exchange has outlined changes to its indices

reflecting the growth in sizes of vessels.

Following a successful trial of dual reporting for a 58,000

dwt Supramax

Index since 31 July 2015 the Baltic will cease publishing

the 52,000 dwt assessments from 3 April and contracts

based on the 52,000 dwt suprmax will be settled based

on a derived formula.

In the panamax sector dual reporting fro the Baltic

Panamax Index will start on 24 April based on the larger

82,000 dwt TESS panamax.

20www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166

The Baltic has also set out proposal to use a Imabari

38,200 dwt geared bulker for a new vessel benchmark to

cover the handysize size sector.

The Baltic said the changes were designed to reflect

changes in the dry bulk shipping fleet and cargo flows.

“These are important changes that are at various points

in our ongoing development cycle. All the amendments

have made following extensive consultations with the

market,” said Mark Jackson, ceo of the Baltic Exchange.

“It is important to note that all these amendments are

designed to reflect vessel fixtures and cargo flows as

required by the International Organization of Securities

Commissions (IOSCO). IOSCO requires financial and

commodity Index providers to demonstrate through

data that their indices are a true reflection of the

underlying market.”

Queen Mary 2 to act as a centrepiece for Britain's first maritime trade mission to China – SMN 28th March

As the day the UK triggers Article 50 to start its

departure from the European Union, this Wednesday,

David Dingle, chairman of Maritime UK and also chair of

Carnival UK will be hosting Chinese government officials

and business leaders aboard Queen Mary 2 in Shanghai

for a lunch to showcase the UK’s shipping capabilities.

Dingle is part of a Maritime UK and UK Government will

three-day trade mission to Shanghai taking place

between 28-30 March, aimed at boosting maritime ties

between the UK and China.

Attended by senior industry and government leaders

from both countries, including shipping and ports

minister, John Hayes MP, and trade minister, Mark

Garnier MP, the mission has been timed to coincide with

Cunard’s Queen Mary 2 calling in Shanghai.

The vessel will be used to promote the UK’s world-

leading maritime position, and boost trade and

investment between the two countries.

“The UK and China are two of the world’s leading

maritime and trading powers, and our mission is

designed to further strengthen relations between our

two countries,” said Dingle.

“On Wednesday the Prime Minister will trigger Article

50. More than any industry, maritime has a unique role

to play in making Brexit a success. As Britain goes out

into the world, determined to increase exports and sign

ambitious trade deals, we have a unique responsibility

to make ‘Global Britain’ a reality, and are ready to do

so,” added Dingle.

The trade and investment relationship between the UK

and China has deepened over recent years, and during

the visit Maritime UK and the Department for

International Trade will be collaborating with the

Chinese government to identify new maritime trade and

investment opportunities for both the UK and China.

“A significant number of world-leading British maritime

companies are already working with China and we are

looking forward to opening new chapters in these

relationships, and beginning others,” said Dingle.

Last month Carnival Corp. & plc, Fincantieri and China

State Shipbuilding Corp (CSSC) advanced their plans to

build cruise ships in Shanghai for the Chinese market by

21www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166signing a binding memorandum of agreement for two

newbuilds with an option for four more.

The deal, subject to several conditions, is valued at

approximately $1.5bn for the first two ships. The ships

will be built at Shanghai Waigaoqiao Shipbuilding (SWS),

a CSSC Group facility with the first delivery expected in

2023.

Following the Shanghai visit, the Maritime UK chairman

and Minister Hayes will visit Hong Kong to meet with the

Hong Kong Shipowners Association.

Directly supporting 500,000 jobs, the maritime industry

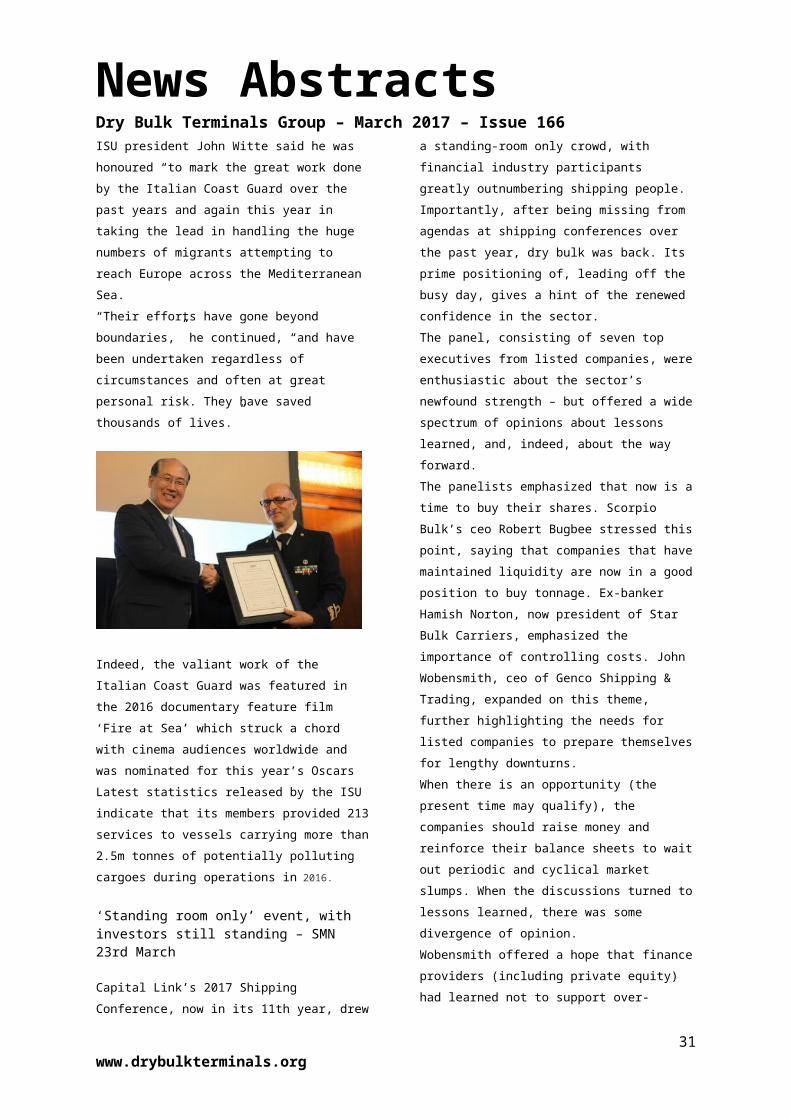

Italian Coast Guard honoured for Med migrant rescue work – SMN 24th March

IMO secretary-general Lim Ki-tack this week presented

the International Salvage Union (ISU) Meritorious

Service Award to the Italian Coast Guard, in recognition

of what were described as its “extraordinary efforts” in

handling the Mediterranean migrant crisis.”

The award was received by the service’s head of plans

and operations department, Nicola Carlone, at the ISU’s

annual Associate Members’ Day Conference in London.

ISU president John Witte said he was honoured “to mark

the great work done by the Italian Coast Guard over the

past years and again this year in taking the lead in

handling the huge numbers of migrants attempting to

reach Europe across the Mediterranean Sea.

“Their efforts have gone beyond boundaries,” he

continued, “and have been undertaken regardless of

circumstances and often at great personal risk. They

have saved thousands of lives.”

Indeed, the valiant work of the Italian Coast Guard was

featured in the 2016 documentary feature film ‘Fire at

Sea’ which struck a chord with cinema audiences

worldwide and was nominated for this year’s Oscars

Latest statistics released by the ISU indicate that its

members provided 213 services to vessels carrying more

than 2.5m tonnes of potentially polluting cargoes during

operations in 2016.

‘Standing room only’ event, with investors still standing – SMN 23rd March

Capital Link’s 2017 Shipping Conference, now in its 11th

year, drew a standing-room only crowd, with financial

industry participants greatly outnumbering shipping

people.

Importantly, after being missing from agendas at

shipping conferences over the past year, dry bulk was

back. Its prime positioning of, leading off the busy day,

gives a hint of the renewed confidence in the sector.

The panel, consisting of seven top executives from listed

companies, were enthusiastic about the sector’s

newfound strength – but offered a wide spectrum of

opinions about lessons learned, and, indeed, about the

way forward.

The panelists emphasized that now is a time to buy their

shares. Scorpio Bulk’s ceo Robert Bugbee stressed this

point, saying that companies that have maintained

liquidity are now in a good position to buy tonnage. Ex-

banker Hamish Norton, now president of Star Bulk

Carriers, emphasized the importance of controlling

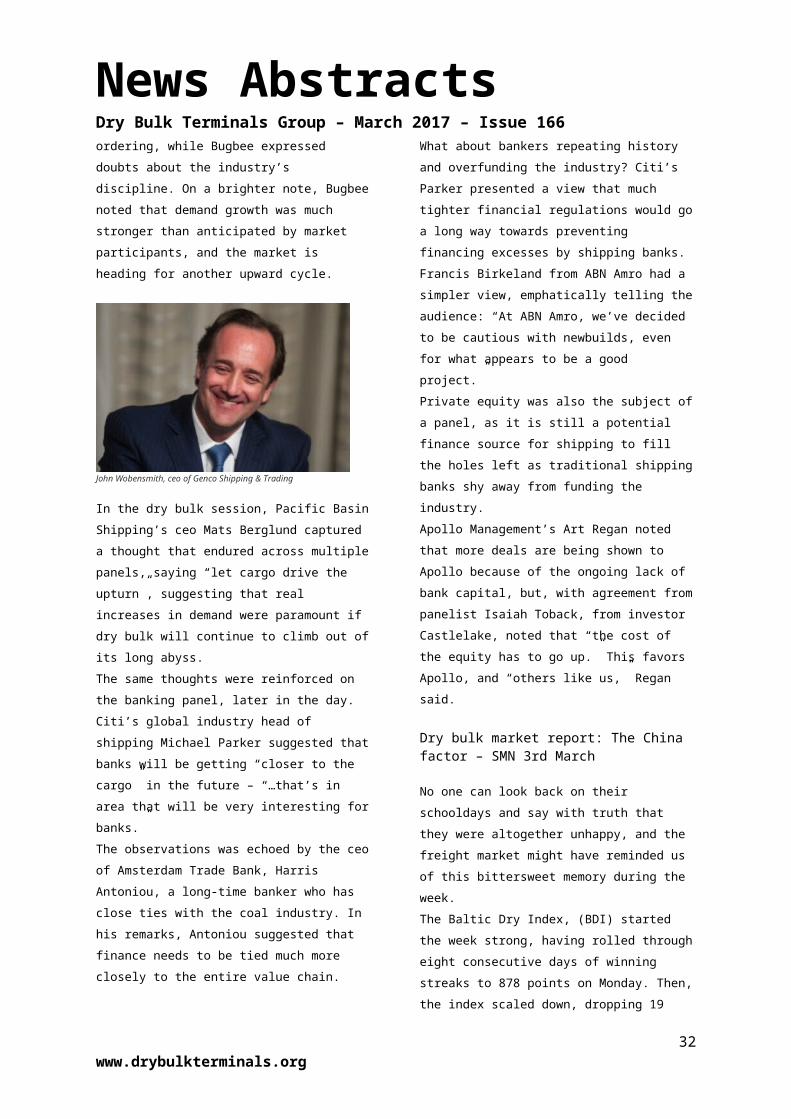

costs. John Wobensmith, ceo of Genco Shipping &

Trading, expanded on this theme, further highlighting

the needs for listed companies to prepare themselves

for lengthy downturns.

When there is an opportunity (the present time may

qualify), the companies should raise money and

reinforce their balance sheets to wait out periodic and

cyclical market slumps. When the discussions turned to

lessons learned, there was some divergence of opinion.

Wobensmith offered a hope that finance providers

(including private equity) had learned not to support

over-ordering, while Bugbee expressed doubts about

22www.drybulkterminals.org

News AbstractsDry Bulk Terminals Group – March 2017 – Issue 166the industry’s discipline. On a brighter note, Bugbee

noted that demand growth was much stronger than

anticipated by market participants, and the market is

heading for another upward cycle.

John Wobensmith, ceo of Genco Shipping & Trading

In the dry bulk session, Pacific Basin Shipping’s ceo Mats

Berglund captured a thought that endured across

multiple panels, saying “let cargo drive the upturn”,

suggesting that real increases in demand were

paramount if dry bulk will continue to climb out of its

long abyss.

The same thoughts were reinforced on the banking

panel, later in the day. Citi’s global industry head of

shipping Michael Parker suggested that banks will be

getting “closer to the cargo” in the future – “…that’s in

area that will be very interesting for banks.”

The observations was echoed by the ceo of Amsterdam

Trade Bank, Harris Antoniou, a long-time banker who

has close ties with the coal industry. In his remarks,

Antoniou suggested that finance needs to be tied much

more closely to the entire value chain.

What about bankers repeating history and overfunding

the industry? Citi’s Parker presented a view that much

tighter financial regulations would go a long way

towards preventing financing excesses by shipping

banks. Francis Birkeland from ABN Amro had a simpler

view, emphatically telling the audience: “At ABN Amro,

we’ve decided to be cautious with newbuilds, even for

what appears to be a good project.”

Private equity was also the subject of a panel, as it is still

a potential finance source for shipping to fill the holes

left as traditional shipping banks shy away from funding

the industry.

Apollo Management’s Art Regan noted that more deals

are being shown to Apollo because of the ongoing lack