Embed Size (px)

Citation preview

Ethical Behavior and Theory in Accounting

Dawn ChurchETH/557May 4, 2015Matthew Homa

Highlights of Today’s PresentationToday’s presentation will provide information on

the following topics:

Ethics, ethical theory, and the basis of ethical theory.

The primary ethical issues and challenges in accounting and auditing.

The ethical theories of egoism, utilitarianism, deontological ethics, the categorical imperative, and virtue ethics.

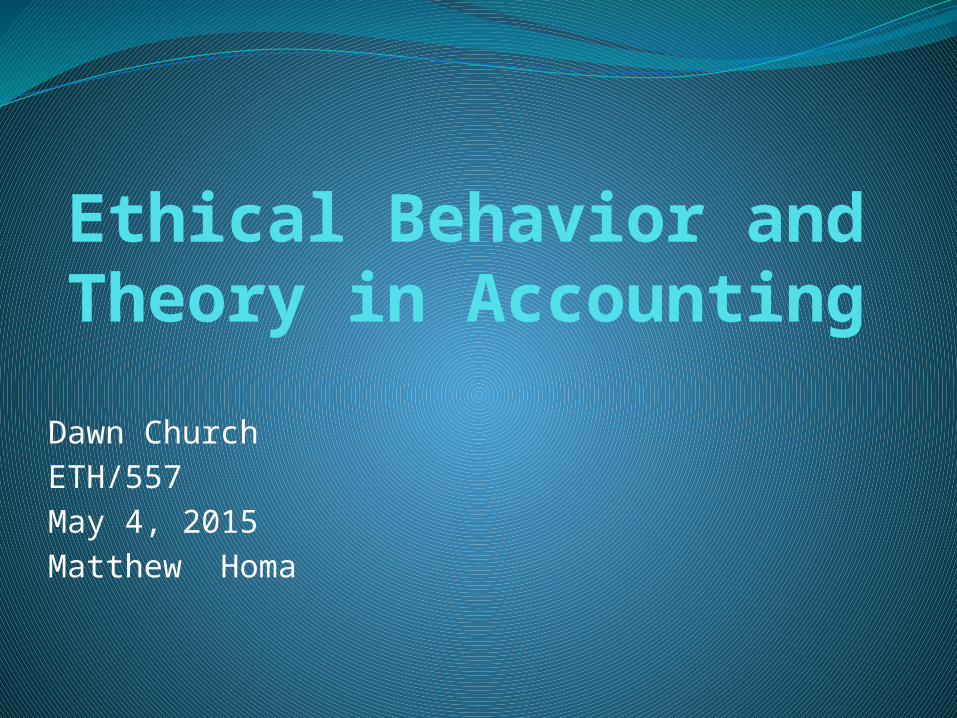

What is Ethics?

(IESE Business School, 2010).

What is Ethics?Ethics is defined as a set or theory, of moral

principles or values.Ethics focuses on dealing with what is good

or bad, right or wrong, and a person’s duties or obligations.

Ethics can be the set of principles held by an individual or a group.

Ethical beliefs contain two parts, a subject (the action) and a predicate (description of subject)

Ethical beliefs are usually based on human actions (Duska, 2011).

Ethics Theory- Why Study Ethics?Reasons why studying ethics is important:

1. Some beliefs a person holds may not be adequate because of the complexity of the issue.

2. Sometimes there are multiple ethical beliefs involved in one situation.

3. Some people's beliefs and values are not adequate.

4. Studying ethics allows individuals the chance to deepen their understanding of why our opinions are worth holding.

5. Identify the ethical practices that can be applied to different actions and situations (Duska, 2011).

The Basis of Ethical TheoryThe basis of ethical theory is the idea that to

justify an action, we have to examine all the reasons in favor of and against the action.

To examine the reasons to base our justification of an action, we need to ask questions (Duska, 2011).

Ask questions such as: Is the action good for me?Is the action good for society, or will it harm society?Is the action fair or just?Does the action violate anyone's rights?Have I made a commitment? (Duska, 2011).

Primary Ethical Challenges in Accounting and Auditing

Challenges that accountants and auditors face:

General disclosures

Determining and disclosing asset values

Consulting roles (Duska, 2011).

General DisclosuresThere is a fine line between disclosing

unneeded information and withholding information.

How do accountants decide what information to disclose?

They ask the following questions:Does the information persuade people to act in

a specific way?Is it harmful to the person getting the

information?Does it benefit the person giving the

information? (Duska, 2011).

Asset Valuation and ConsultingVarious methods of asset valuation that can

mislead financial statement users by altering the data.

Valuation can be based on:Asset cost at the time of the purchaseWhat the asset could be sold for currently

Consulting services are a challenge because they open the accountant up to conflicts of interest (Duska, 2011).

Ethical TheoriesFive ethical theories:

1. Utilitarianism2. Egoism3. Deontological Ethics4. Categorical Imperative5. Virtue Ethics (Duska, 2011).

UtilitarianismFocuses on the question of whether the

action benefits the people more than it harms them.

Takes into consideration the impact had by everyone, including the individual.

An individual’s self-interests are cast aside.All actions recommended are done to

enhance the good of the largest number of people (Duska, 2011).

EgoismFocuses on whether the action is good for

ourselves. Concerns of oneself take priority over

what might be best for others. Does not consider what is fair to all

human beings, but focuses on the belief that people should act in their best interest (Duska, 2011).

Deontological EthicsFocus on fairness.Fairness takes priority over any

consequences the actions would have.The overall key points to this theory are a

focus on fairness, rights, commitments, and doing the right thing.

People cannot think only of their own wants and desires. They must think of others (Duska, 2011).

Categorical ImperativeGoes along with deontological theory.Focus on people being treated fairly.There is also a focus on leading by example.

If you want others to act ethically, then you must also act ethically.

This theory shows that all people are equal are must abide by the same rules (Duska, 2011).

Virtue Ethics

Focus on character traits that are acknowledged across cultures.

There is a focus on reaching the end goal or purpose to achieve full potential.

Focus is on virtues and moral character and not on duties, rules, or consequences.

The emphasis has been taken away from the consequences of the actions, and looks at the kind of person who is doing the action (Gregory B. Sadler, 2011).

How Ethical Theories Relate to Accounting and Auditing

Utilitarianism leans towards companies that provide goods and services while doing the least harm, and condemns companies that cause more harm than benefit to others.

Egoism creates complications because there are going to be times within your career when you are not the best person to help a client. You have to make the decision to send them to another accountant, and by doing so you will lose their business. Doing this is not the best decision for you, but it is the best decision for the client (Duska, 2011).

How Ethical Theories Relate to Accounting and Auditing Cont.

Deontological ethics applies to accountants and auditors because they have to maintain a fair and consistent relationship with all their clients. They must also ensure that they are following through with their commitments. If they do not do this, clients will lose trust in them, and it will be difficult for them to find new clients.

Categorical Imperative relates to auditors because if they are upholding a high moral standard, they will encourage the people working for them, as well as their clients, to do so as well (Duska, 2011).

How Ethical Theories Relate to Accounting and Auditing Cont.

Virtue Ethics applies to accountants because it says that they should be all they can be in their profession. They should be the best accountant possible by being truthful, avoiding harming others, following through on commitments, and having integrity.

There are times when a decision will involve multiple theories, and this will often cause a conflict about which theory to follow (Duska, 2011).

Conclusion

Ethics focuses on dealing with what is good or bad, right or wrong, and a person’s duties or obligations (Duska, 2011).

Ethics, in general, is made up of smaller parts that all work together to build the moral fabric of society. (Carlton University, 2015).

ReferencesCarlton University. (2015). [Drawing of the elements

of ethics] Ethics. Retrieved from https://www.pinterest.com/pin/567172146795006005/

Duska, R. (2011). Accounting Ethics (2nd ed.). Retrieved from The University of Phoenix eBook Collection.

Gregory B. Sadler. (2011). Five Ethical Theories: Bare Bones for Business Educators [PowerPoint slides]. Retrieved from http://www.academia.edu/1702607/Five_Ethical_Theories_Bare_Bones_for_Business_Educators.

References IESE Business School. (2010). [Drawing of a

cartoon depicting a manager telling an employee not to do the ethical thing] What Business does Ethics Have in Business. Retrieved from http://blog.iese.edu/dgdw/2010/11/12/what-business-does-ethics-have-in-business/