Embed Size (px)

Citation preview

LA4023 – Taxation Law

Week 1......................................................................................................................................................3What is Tax?......................................................................................................................................................3

Commonwealth Constitution...........................................................................................................................3Tax Definition.................................................................................................................................................3Uniform Tax Scheme......................................................................................................................................3Tax Simplification Project...............................................................................................................................4

Australian Tax System......................................................................................................................................4Who do we tax?...............................................................................................................................................4What do we tax?..............................................................................................................................................7Tax Rates.........................................................................................................................................................7

Week 2......................................................................................................................................................9Income – General Principles.............................................................................................................................9

Income tax formula (s 4-10(3)).......................................................................................................................9Exempt Income..............................................................................................................................................10Non-Assessable Non-Exempt Income...........................................................................................................10Assessable Income........................................................................................................................................10Ordinary Income............................................................................................................................................11

Week 3....................................................................................................................................................14Income from Personal Exertion, Property, Business, & Trading Stocks...................................................14

Income from Personal Exertion.....................................................................................................................14Income from Property...................................................................................................................................17Income from Business...................................................................................................................................19Treating Trading Stock..................................................................................................................................23

Week 4....................................................................................................................................................24Deductions........................................................................................................................................................24

Section 8-1: General deductions....................................................................................................................24S 8-1(1): The Two Positive Limbs................................................................................................................24S 8-2: The Four Negative Limbs...................................................................................................................26

Week 5....................................................................................................................................................31Specific Outright Deductions..........................................................................................................................31

Repairs – s 25-10...........................................................................................................................................31Bad Debts – s 25-35......................................................................................................................................32Carry Forward Losses – Div 36....................................................................................................................33Gifts – Div 30................................................................................................................................................33

Deductions Over Time.....................................................................................................................................33Prepayments..................................................................................................................................................33Borrowing Expenses – s 25-25......................................................................................................................33Depreciation/Uniform Capital Allowance System – Div 40.........................................................................34

Week 6....................................................................................................................................................35Substantiation..................................................................................................................................................35

Who must substantiate?.................................................................................................................................35What records are required?............................................................................................................................35What expenses must be substantiated? S 900-10..........................................................................................35Tax Accounting.............................................................................................................................................37

Week 7....................................................................................................................................................40Capital Gains Tax............................................................................................................................................40

CGT Assets....................................................................................................................................................41

CGT Events...................................................................................................................................................42Capital Gains/Losses.....................................................................................................................................44Indexation and Discounting...........................................................................................................................44Net Capital Gains/Losses..............................................................................................................................46

Week 8....................................................................................................................................................48Superannuation................................................................................................................................................48

Superannuation Regulatory Scheme.............................................................................................................48Taxing Point 1 – When Contributions Are Made..........................................................................................48Taxing Point 2 – Taxation of Super Entities.................................................................................................50Taxing Point 3 – When the Benefit is Paid...................................................................................................50Superannuation Contribution Flow Chart.....................................................................................................53

Termination Payments....................................................................................................................................54Fringe Benefits.................................................................................................................................................55

Taxing Fringe Benefits..................................................................................................................................55Fringe Benefits Taxable Amount..................................................................................................................56

Week 9....................................................................................................................................................59Partnerships.....................................................................................................................................................59

What is a Partnership?...................................................................................................................................59How Partnership Income is Taxed................................................................................................................60Dissolution of Partnerships...........................................................................................................................62

Week 10..................................................................................................................................................63Taxation of Trusts............................................................................................................................................63

What is a Trust?.............................................................................................................................................63Outline of Taxation of a Trust.......................................................................................................................63Anti Tax Avoidance Measures......................................................................................................................68Taxation of a Trust Flow Chart.....................................................................................................................69

Week 11..................................................................................................................................................70Taxation of Companies....................................................................................................................................70

Imputation.....................................................................................................................................................73Benchmark Rule............................................................................................................................................74Franking Deficit Tax.....................................................................................................................................75Companies as Shareholders...........................................................................................................................75

Week 12..................................................................................................................................................76Primary Producers..........................................................................................................................................76

Deferral of Income........................................................................................................................................77Averaging Income Div 392...........................................................................................................................77The Comparison Rate....................................................................................................................................79The Averaging Component s 392-90............................................................................................................80The Averaging Adjustment...........................................................................................................................80Farm Management Deposits..........................................................................................................................80

Week 13..................................................................................................................................................82Tax Collection..................................................................................................................................................82

Commissioner’s Power to Retain Information..............................................................................................82Domestic Collection of Tax..........................................................................................................................83

Tax Evasion, Planning, and Avoidance.........................................................................................................85

2

Week 1

Week 1

What is Tax?

Commonwealth Constitution S 90 – Cth has exclusive powers to impose customs and excise duties

o States and territories are thought to be constrained by this section – definition of excise broad

S 51o Concurrent powero Cth has power to make law in respect of taxation; but so as not to discriminate between

States or parts of States S 109 – Where State and Cth law is inconsistent, Cth law will prevail

o There will be no inconsistency in tax – both taxes must be paid S 81 – Consolidated Revenue Fund (CRF)

o Where tax is collected, it will enter this fundo Once the money enters this fund, the government must pass an Act to take the money

out for spending S 83

o Whether money enters this fund will not determine whether there is a tax

Tax Definition The compulsory extraction of money for public purposes enforceable by law and not a payment

for services rendered Characterisation

o When deciding whether or not it is a tax, the characteristics of the legislation will be considered

o Substance over form Luton v Lessels

Uniform Tax Scheme Only Cth may impose an income tax? Rating Act – set Federal Income Tax rates so high people could not pay both Federal and State

taxes. Assessment Act – giving the Federal Government priority in payment (enforceable under s 109

of the Constitution). Grants Act – reimbursing the states for lost revenue provided they did not raise their own taxes. Arrangements Act – empowering the Federal Government to take over the premises, staff and

records of the various State Tax Offices.

Limits on Federal Legislative Power (from the Constitution) S 51

o The law must be one with respect to taxationo The law must not discriminate between States or parts of States

S 114o The Federal Government may not tax State property

S 55o The law must deal with one subject of tax only

3

Week 1

o Laws imposing taxation shall deal only with the imposition of taxation, and any provision therein dealing with any other matter shall be of no effect.

o Laws imposing taxation, except laws imposing duties of customs or of excise, shall deal with one subject of taxation only.

This is due to s 53 – Bills originating from tax can come only from the House of Reps, the Senate can only accept or reject

State Industries v Commonwealth

Taxing Statutes The Assessment Acts Other – these are separate for fear of breach of s 55 of the Constitution

o Ratings Actso Taxation Administration Acto International Tax Agreement

Tax Simplification Project A project designed to rewrite the 1936 Assessment Act, without changing any policies, with the

purpose of making the act more accessible and easier to understand Both Acts are in force (though they have not finished the rewrite) Resulted in two Assessment Acts

o ITAA 1936o ITAA 1997

Where there is a dash, the section will refer to the 1997 Act

Australian Tax System

Who do we tax? Must be a jurisdiction to impose tax on that entity This will apply to those with a sufficient association with Australia through:

o Residenceo Source of income

Residents will be taxed on world-wide income S 6-5(2) – Ordinary income

Non-residents will only be taxed on Australian sourced income S 6-5(3)

o 6-10(4) – resident, statutory incomeo 6-10(5) – non-resident, including statutory income

Who is a resident?o S 6(1) ITAA 1936

(a) A person, other than a company, who resides in Australia and includes a person:(i) whose domicile is in Australia, unless the Commissioner is satisfied that his permanent place of abode is outside Australia;(ii) who has actually been in Australia, continuously or intermittently, during more than one-half of the year of income, unless the Commissioner is satisfied that his usual place of abode is outside Australia and that he does not intend to take up residence in Australia; or(iii) who is:

4

Week 1

(A) a member of the superannuation scheme established by deed under the Superannuation Act 1990; or(B) an eligible employee for the purposes of the Superannuation Act 1976; or(C) the spouse, or a child under 16, of a person covered by sub-subparagraph (A) or (B).

o Tests – individuals Common Law test

Done on a year to year basis ‘Domicile’ test 183-day rule Superannuation test

Common Law testo Generally used for people entering into Australiao The person must reside in Australia, but residing is not defined in the Act

Tax ruling 98-17 Case law

Has adopted the meaning of where the person dwells permanently or for a considerable time, or where they have settled or it is their usual abode

Master tax guide has many cases – looks at everything across the year Court weighs up:

o Continuityo Routineo Habit of livingo Habit of residingo Physical presence in Australiao How often are visitso Duration of visitso Purpose of visitso Relations in Australiao Note: Nationality is not a significant factor

Federal Commissioner of Australiao Work ties outweigh family ties

o Under this test, residency starts at the date of first arrivalo From that date onwards, world-wide source

Domicile testo A person is a resident of Australia if:o Their domicile is in Australia

Unless the Commissioner is satisfied that the person’s permanent place of abode is outside Australia.

o Domicile is a legal concept according to the Domicile Act 1982 (Cth) and common law rules.

o Categories of Domicile Domicile of Origin Domicile of Choice Domicile of Dependency

o Applegate Was transferred indefinitely to Vanuatu He gave up his Australian flat and rented in Vanuatu Always intended to return to Australia

5

Week 1

He claimed he was a non-resident for the period he was away he should not need to pay income tax

The court said he was a non-resident under the common law test Under the domicile test, he was also found to be a non-resident

o Jenkin Transferred to Vanuatu for three years Returned early due to ill health Court said he was not required to pay income tax for that time under the

Applegate testo IT 2650

Look to the intended and actual stay in the foreign country, and whether that period is substantial

Two years or more is considered substantial Looks to whether they establish a home outside of Australia that is more than

temporary Look to enduring relationship with Australia

183 day ruleo To escape this, must establish that there usual place of abode is outside Australia, and

there is no intention to stay in Australia permanentlyo It is uncertain when a person is actually an Australian resident

For the whole year Case 19 – From the 184th day Groves – Only an Australian resident for the days actually present

Source Source is determined by

o Particular statutory ruleso Common law source rules

Common lawo Nathan v FCT (1918) 25 CLR 183

The ‘source’ of particular income is a ‘practical hard matter of fact’ o ‘Source’ is determined by looking at what a practical person would regard as the ‘real’

source of that income.o SCBT French

Normally where the service is performed is where it’s sourcedo SCBT Mitchum

French is not the only rule – it will not determine where it is sourced All factors must be considered

Common law source ruleso Spotless Services

If they put their money in an Australian bank it would have earned more interest, but they put it in the Cook Islands, who withheld 5%

This meant that they did not have to pay income tax in Australia However, they breached the anti-avoidance rule

Dividend Incomeo Esquire Nomineeso Sourced where the shares are held (now largely govern by s 44 ITAA 1936) o S 44 provides that the source of the dividend is where the profits from which the

dividend is paid were derived.)

6

Week 1

o But s 44 does not permit tracing of those profits back through a chain of companies.

What do we tax? Income tax formula in s 4-10(3)

Income Tax= (Taxable Income × Rate )−Offsets

‘Ordinary’ v ‘Statutory’ Incomeo Whether a particular payment is income “must be determined in accordance with the

ordinary concepts and usages of mankind except in so far as the statute states or indicates an intention that receipts which are not income in ordinary parlance are to be treated as income”.

Per Jordan CJ in Scott (1935) Gross Income:

Gross Income=AllOrdinary Income+ All Statutory Income

o Depends on resident status (see 6-5 and 6-10) Residents – worldwide gross income Non-residents – Australian source gross income

Assessable Income:

Assessable Income = Gross Income – Exempt Income – Non-Assessable Non-Exempt Income Exempt Income – 2 ‘Classes’ (Div 11)

o Income will be exempt if (s 11-1): Income of ‘exempt entities’ (List in s 11-5) Income which is exempt (List in s 11-15)

Non-Assessable Non-Exempt Incomeo Non-assessable, non-exempt income is ordinary or statutory income that is expressly

made neither assessable nor exempt income (see s 6-23).o Income so categorised has no tax affect whatsoever for the receiving taxpayer.

Deductionso Deductions reduce the income on which you are liable to pay tax.o They are expenses you incur in the course of earning your assessable income; or,o Other outgoings specifically made deductible by the Act (e.g. gifts to charities).

Tax Offsets (Rebates and Credits) (Div 13)o Tax offsets reduce tax payableo They do not reduce assessable incomeo Examples

Foreign income tax offsets (‘FITO’s – what were formerly called ‘foreign tax credits’);

Franking credits on dividends; Rebates for family situations (e.g. dependant (invalid and carer) tax offset, low

income rebate); Rebates for some expenses (e.g. medical expenses).

7

Week 1

Tax Rates Rates depend on the taxpayer (individual or company and resident or non-resident) Companies pay tax at a flat rate of 30%

Resident individuals pay on a sliding scale:

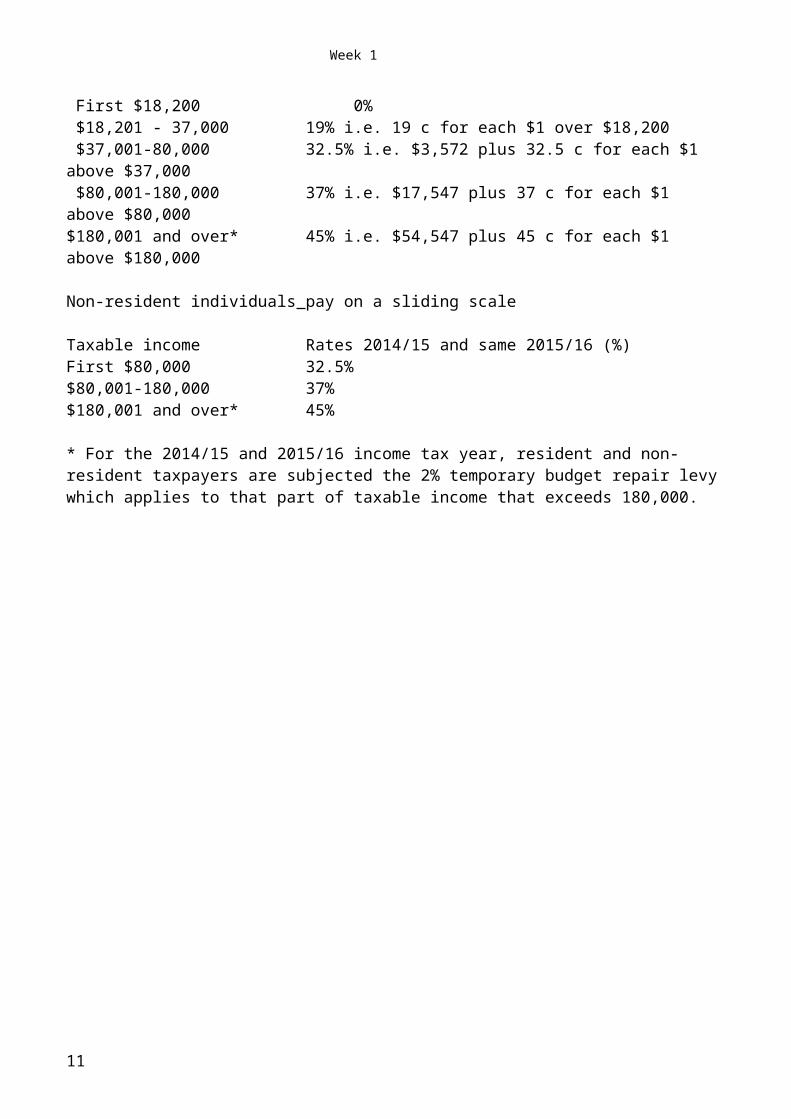

Taxable income Rates 2014/15 and same 2015/16 (%) First $18,200 0% $18,201 - 37,000 19% i.e. 19 c for each $1 over $18,200 $37,001-80,000 32.5% i.e. $3,572 plus 32.5 c for each $1 above $37,000 $80,001-180,000 37% i.e. $17,547 plus 37 c for each $1 above $80,000$180,001 and over* 45% i.e. $54,547 plus 45 c for each $1 above $180,000

Non-resident individuals pay on a sliding scale

Taxable income Rates 2014/15 and same 2015/16 (%)First $80,000 32.5%$80,001-180,000 37%$180,001 and over* 45%

* For the 2014/15 and 2015/16 income tax year, resident and non-resident taxpayers are subjected the 2% temporary budget repair levy which applies to that part of taxable income that exceeds 180,000.

8

Week 2

Week 2

Income – General Principles

Income tax formula (s 4-10(3))

Assessable Income

S 6-1 Diagram showing relationships among concepts in Division 6

9

Week 2

Assessable income includes: All ordinary income (s 6-5); plus, All statutory income (s 6-10); less, Any exempt income (s 6-15); and, Any non assessable non-exempt income

Therefore:

Assessable Income = Gross Income – (Exempt Income + Non-Assessable Non-Exempt Income)Ordinary and Statutory Income

Section s 6-5(1)o Ordinary income is ‘income according to ordinary concepts’.

Section 6-10(2)o Statutory income includes ‘amounts that are not ordinary income but are included in

your assessable income by provisions [in the Act] about assessable income’. What the court have decided is income is income. There are no set or strict rules, though they

have provided guidelines (regular, ordinary, normal etc.) S 6-20 provides a list of what is exempt S 11-5 entities that are exempt, no matter what kind of ordinary or statutory income assessable

Exempt Income Section 6-20(1)-(3)

o Income will be exempt income IF it is made exempt by a provision of the ITAA or another Commonwealth Act.

Section 6-20(4)o An amount that is non-assessable, non-exempt income is NOT exempt income.

Non-Assessable Non-Exempt Income Section 6-23: An amount of ordinary or statutory income is non-assessable non-exempt income

if a provision of the ITAA or another Commonwealth law specifically makes it neither assessable income nor exempt income.

Assessable Income The ITAA does not define the term ‘income’ The ITAA deems some receipts to be ‘income’ for taxation purposes (e.g. non-cash business

benefits, tips and gratuities, post 1985 capital gains etc.) But, apart from that, determining whether a particular receipt is ‘income’ has been largely

determined by the courts

The Courts’ View Whether a particular payment is income must be determined in accordance with the ordinary

concepts and usages of mankind, except in so far as the statute states or indicates an intention that receipts that are not income in ordinary parlance are to be treated as income.

o Per Jordan J in Scott (1935) Whether a particular receipt is income that is taxable in the hands of a taxpayer depends on

whether it is:o Income on ordinary concepts (‘ordinary income’); or

10

Week 2

o Income under some specific statutory provision (‘statutory income’); and

o Whether it has been derived Blake

Statutory Income Receipts that would not be income under ordinary concepts but which are included in income

because some provisions of a taxing statute make them income Examples include:

o S 15-2 (allowances, gratuities etc.)o S 15-15 (income from profit making undertakings or plans)o Capital gains (s 102-5)o Deemed dividends (various sections - including Div 7A)o Balancing adjustments (Div 40)o Recoupments (s 20-20)o Some ETPs

See s 6-25(2) relationship of other income with ordinary income

Income includes Income from personal exertion

o Income from businesso Income from profit-making schemes

Income from property

Ordinary Income Whether an amount is income ‘depends upon its quality in the hands of the recipient’

o FCT v Mc Neil Therefore the receipt must be income in the hands of the taxpayer

o Federal Coke v FCT General Principles1. It must ‘come in’ to the taxpayer (FCT v Cooke and Sherden).2. Not everything which comes in is necessarily income:a. Mutual paymentsb. Windfall gainsc. Capital receipts3. It must be money or something convertible to money.4. It often exhibits characteristics of periodicity, regularity and recurrence.5. Income substitution or compensation payments may be income.6. Illegal, immoral and ultra vires receipts may be income.

It Must ‘Come In’ Generally for an amount to be income, it must ‘come in’ to a taxpayer

o Tennant v Smitho FCT v Cooke and Sherden

It is not just a savingo However, if it is coming regularly it could be a saving

11

Week 2

Not Everything That Comes In is Necessarily Income ‘Mutual payments’

o The Mutuality principle: A taxpayer cannot derive taxable income from payments to him/ herself

Bohemians Club v FTC To be ‘income’, the receipt must arise from a source outside the taxpayer. It

applies particularly to income received by clubs and societies from dealing with their members.

Income from business activities aimed at producing a profit (as opposed to a ‘surplus’) and from non-members is taxable.

Income has to be from an outside source to receive it, i.e. making a purchase and getting a refund for it is not an income because it is your money anyway.

Municipal Mutual Insurance Limited v Hills Bohemians Club v FTC

Paid money to that club as membership, issue was whether excess amount that wasn’t spent for the members was income.

Found not to be income to the club, because the members are the club itself. Therefore the money did not come from outside the club.

o Income of clubs Is the receipt exempt income? If not, the ‘Mutuality Principle’ produces three (3) possibilities:

The receipt is wholly exempt because it comes from members The receipt is wholly taxable because it comes from sources outside the

club The receipt is partly assessable because it comes from the general trading

activities of the club which cannot be sourced to members alone Can be partly assessed – club meals and drinks from the bar, if members are

distinguishable from non-members; however, if they cannot distinguish they will portion it

Gainso The ‘normal proceeds’ of personal exertion, property or business are income –

‘Windfall Gains’ are noto Income = a form of financial ‘gain’o Under tax law, only realised gaino However, not all realised financial gains will be treated as income – courts distinguish

between income and capital gainso Windfall gains

Fall into two main categories Gambling winnings Gifts

Are generally not taxable unless (in the case of gambling proceeds) they are the result of income earning related activity (e.g. a ‘business of gambling’)

Brajkovich Capital receipts

o Our system was designed to tax ‘income’.

12

Week 2

o The concept was based on the trust law distinction between capital and income (the ‘tree’ and the ‘fruit of the tree’ analogy).

o Capital receipts were not taxed (and still are not taxed) unless they are covered by the CGT provisions

o Once it’s classified as capital it is not ordinary income.o The tree is the capital and the fruit is the income

Eisner v Machomber So is it an asset that is purchased for the sole purpose of an investment, to

produce future income?

Cash Or Cash Convertible According to ordinary concepts, to be income the receipt must be in the form of money or

something convertible into moneyo Tennant v Smitho FCT v Cooke & Sherden

This principle is now subject to the contrary intention of parliament found in the ITAA. For contrary intention of parliament, see:

o S 15-2 taxes the ‘value to you’ (subject to the FBT legislation – see s 23L) Does not work in a subjective view, it only works as if it’s a monetary income If it’s a fringe benefit, s 23L means it is non-assessable non-exempt income of

the taxpayer if it is under $300o S 21 deems a money equivalento S 21A deals with ‘non-cash business benefits’

Common Characteristics Periodicity Regularity Recurrence

Income Substitution and Compensation Payments Income substitution payments (key money instead of rent, sign-on fees instead of salary) are

regarded as income Compensation payments take the character of the receipt they replace

o FCT v Meeks Div 20-A specifically makes certain ‘recoupments’ assessable (i.e. as statutory income).

Income from Illegal Activities Assessability of receipts Deductions for outgoings (briefly)

o Under the general lawo Under s 26-54 and s 110-38 – illegal activity outgoingso Under s 26-5 – Fines and penaltieso Under s 26-52 and 26-53 – Bribes

S 167 default assessment

13

Week 3

Week 3

Income from Personal Exertion, Property, Business, & Trading Stocks

Categories of Income Income from personal exertion

o Income from businesso Income from profit-making schemes

Income from propertyo Trading Stock

When you have rewards for service and payments incidental to service, this would be ordinary income; however not payments for restricted rights are not

Income from Personal Exertion Will normally include:

o Salary and wageso Directors’ feeso Payments and prizes received by professional sportspersonso Fees and commissions

Will not include income that is mainly from:o The use of assetso The sale of assetso A business structureo Granting the right to use property

So if paid for work done due to a contractual obligation (employee/sub-contractor), this is ordinary income.

3 situations where it is not as clearo Gift given to you by party you have performed services foro Gift given to you by someone you have not performed services foro Money given to you for giving up something

Underlying principle for all 3 categories:o Is there nexus between service and payment?

Gift given to you by parties you have performed services foro Issue: Was the gift for personal reasons (not ordinary income) or for income earning

activity (ordinary income).o Rule: Gift will be ordinary income if it is a ‘product or incident of employment or a

reward for services rendered’ Hayes

o If there is a strong connection between the payment and the service, then it is more likely to be ordinary income

Scott Harris

o The court will look at all the factors and weigh up (Scott) Relationship of donor-donee What is the character of it in the hands of the receiver Nature of employment Manner the gift was make Was it expected?

14

Week 3

o If it’s one-off, then it is less likely to be ordinary income, if it is regular, then it is more likely to be ordinary income

Harris Also discusses motive of donor Did everyone get that amount Was it determinative of the length and quality of the work

o Ultimate question: Is there a sufficient nexus between gift and income earning activity of recipient?

Yes – ordinary income No – capital To determine this, court will look at factors:

Expected Regular Motive of donor Whether already remunerated Did others get paid? Others

o Note that factors are not definitive, but only help decide the ultimate question

o Can it be traced to some personal relationship? Hayes Scott

Widower Solicitor completed the distribution of the estate after her husband

passed away The widow and the solicitor were friends, so she gave him a gift

afterwards, in spite of the fact that she had already paid him It was not found to be ordinary income

o Supplementary income may constitute income where it is periodic, expected, and relied upon to support family

Dixon He was conscripted to fight in the war and his salary was less than his

ordinary job The employer gave him the difference between his salary and his war

salary The court said this was ordinary income This is because it was still incidental to his employment, it was periodic,

and his family relied on it to live on Also used the replacement principle

Contrast with Harris Ex employee’s got pension at this time Because of high inflation, this did not cover cost of living Employer provided ex employees a lump sum because of this Court found that this was not ordinary income It was for personal reasons It did not depend on the length or quality of their work One off-lump some was considered

Gift by parties you have not performed services foro Voluntary payments may be income

15

Week 3

Moorhouse v Dooland A professional cricketer was entitled to his weekly salary plus talent

money and a collection from the crowd The court was looking as to whether the crowd collection was ordinary

income The court found that it was as it was part of his contract, and he had an

expectation to get this money, periodico Payments made by third parties that are ‘incidental’ to the taxpayer’s employment may

be income Kelly v FTC

Best and Fairest winner AFL would get a cash award Paid by Channel Seven Was this prize ordinary income? The court said yes as it was directly related to the employment, and

caused by the employment, even though it was unexpected and not periodic

Distinction between payment for services and giving up a right/asseto Compensation rule: Compensation assumes the character of the thing for which it is

paid FCT v Meeks Compensation for giving up income will be income Compensation for giving up capital will be capital

o Payments for services v sale of an asset Brent

Taxpayer was a train robber Was paid by a journalist to tell his life story She claimed that when she was receiving the money she was giving up

copyright, and thus it was payment for capital, not ordinary income Copyright does not exist until it is recorded Therefore, the court said that it was ordinary income, as she was being

paid to provide a service – telling the service The copyright was found to belong to the journalist Had she written the story then given it to the newspaper, it would have

been differento Payments for relinquishing rights

Jarrold v Boustead Jarrold was a rugby player and he gave up his amateur status and that

was considered to be capital Therefore, payment for giving up his amateur status was considered to

be capitalo Payments for entering into restrictive covenants

Restrictive covenants = payment for not doing something. These types of agreements would usually be capital.

Higgs v Olivier Made a movie, agreed not to enter into a movie for the next eighteen

months The court said it was capital, as he was giving up his right to make

movies FCT v Woite

16

Week 3

While Woite was working for them, he entered into an agreement not to play for another team

He was not found to be giving up anything Therefore, ordinary income If there is no real restriction, it is not capital

Statutory interventiono Three areas of statutory intervention:

S 15-2 ITAA 1997 Fringe Benefits Tax (FBT) Termination payments

o If it’s not 6-5, it may be 15-2 (value to the taxpayer) Only applies when it is a tax benefit

o Also applies to CGT Whenever something is not 6-5, look to whether it is statutory income

o S 15-2 1) Provides that the value to the taxpayer of any allowances, gratuities,

compensation, benefits, bonuses or premiums provided in respect of employment is assessable to the taxpayer.

2) Since the introduction of FBT (on 1 July 1986), s 15-2 is limited to cash allowances, bonuses etc. paid in relation, directly or indirectly, to any employment or the provision of services.

Fringe Benefitso A fringe benefit is a benefit provided by an employer to an employee in respect of the

employmento S 23L(1) makes fringe benefits non-assessable non-exempt incomeo Fringe benefits are taxed in the employer’s hands and not the employee’s handso At the fringe benefits tax rate – 2013/14: 46.5%, 2014/15: 47%, 2015/16 and 2016/17:

49%, from 2017/18 onward the rate reverts back to 47%o FBT is a loss or outgoing incurred by the employer in gaining or producing assessable

income – so is deductible to the employer. Termination Payments

o Termination payments are any payments received for leaving employment.o Now dealt with under particular statutory provisions which:

Make such payments taxable; but Tax them concessionally (if at all)

Income from Property Interest: What is it?

o Interest is the fruit that flows from the capital (loan) Westminster Bank Case

o Normal Loan: Lender gets right to capital/ principle and interest. Lend $1,000 at a 10% interest. Borrower gets $1,000 and repays $1,000 (capital) and $100 (interest). Lender gets right to $1,000 (capital) and $100 (interest).

Interest: Discounts and premiumso Loan Discount:

Lender gets right to more capital and less interest if any.

17

Week 3

A bill has a face value of $1,000 and is issued at $800. On Borrower gets $800 and on maturity has to repay $1,000. Here $200 will be interest and OI to the financial lender or may capital in other

circumstances o Loan Premium:

On Borrower gets $800 and prepays a premium; the notional principle and interest on the notional loan.

To the lender the premium would be capital unless they are disguised interest. Ask whether it is a genuine premium for capital risk or disguised interest?

If there is a real risk, its capital, if it’s a disguised risk, it’s ordinary income under 6-5

o If it is not ordinary income, it will be statutory income Lomax v Peter Dixon

o The taxpayer was a company who had lent money to Finland before WWII

o There was a high security risk in Finland due to threatso They charged a higher premium due to the risko The court said it was capital as there was a genuine risk of non-

payment Implicit interest

o If an asset is worth $100 and is sold for $120, with the price to be paid in 12 equal installments of $10, is the entire $120 a capital payment for the asset?

See Vestey Debt defeasance arrangements

o You borrow $1,000,000 repayable in 10 years. To get the debt off your books you pay X Ltd $1/2 million now to take over your repayment liability.

o Ask: Is the $1/2 million you saved income? Unilever

If you are in the business of financing, it would be ordinary income Orica

If you are not in the business of financing, then it is not ordinary income, as the argument is that that saving is not a profit, it is a saving

It is an unusual and isolated activity Myer

When you first borrowed this money, did you intend to on sell it to another to make another half a million?

If yes, then it is ordinary income CCT is applied to the original borrower

Rento 6-5 ordinary incomeo Premiums

Prior to Sept 85 not ordinary income because capital Now assessable as CGT event F1

When there is a high demand and low supply for property Potential tenants, because they cannot get a place, would pay the lessor

to accept their application In this regard, when the landlord receives the payment as capital F1 event Payable under CGT

18

Week 3

o Incentive A situation where there is low demand and high supply The difference is the landlord is making payment to a potential tenant to take up

residence in their property When the tenants get that money, what is it to them?

Tax ruling 2631 Cash: ordinary income

o Montgomery Partner in a large firm decided to move the business to a

different building for $30 million over three years Issue was whether the lease incentive was ordinary

income to that partner It was an ordinary incident of the firm’s activity The firm entered into the agreement to get this

inducement Federal court said it was capital Three quarters of the High Court said it was ordinary

income. They applied the Myer principle Consider: Is this a common occurrence in the market at

that moment?o Myer

CGT event H2o S 118-20 Include it as assessable income somewhere else before

H2 applies Non-convertible

S 21A Royalties

o 15-20 statutory income, intellectual property that you are allowed to use and get paid for, and therefore usually be ordinary income

Capital Gainso If you sell your property, you are selling the capital

Income from Business Receipts arising from the normal activities of a business are income according to ordinary

concepts (‘ordinary income’). Two questions arise:

o Is the taxpayer engaged in a ‘business’? o If yes, did the receipt arise from the normal activities of the business?

If ‘yes’ to both, the receipt is prima facie ‘income’. First Issue: Is it a business or a hobby?

o Important differences: Hobby

When you make money from a hobby it is not ordinary income and you can’t claim deductions

If you can prove a hobby is a business then it might be classified as a non-commercial business.

Business An Employee is excluded from the definition of business: s 995-1

o Indicia of a business

19

Week 3

System and Organization: Commerciality; Scale of Activities; Sustained, regular and frequent transactions; Profit Motive; Commercial character of the transactions; Characteristics or quantities of property dealt in; Inherent characteristics of the Taxpayer; and Ancillary matters

o Ferguson Profit motive/intention is important, but it is not necessary in its initial stage It does not matter if never made any money, intention to make money is enough

o Walker Scale of activity is not determinative of whether there is a business Here Walker only had three goats, still a business It does not matter if never made any money, intention to make money is enough

o Stone A javelin thrower was able to turn her javelin throwing skills into a business Received prize money from competitions, government grants, promoting

products, money for speaking appearances Court said she had turned her skill into a business as she sought out those

sponsorships and entered into deals that gave her javelin throwing activity a business flavour

o Brajkovich The normal proceeds of a business depend on:

o The nature and scope of the business Ask: What the taxpayer is in business to do?

o The relationship between the business and the specific receipts in question. Ask: Did the receipt result from some activity that falls within what the taxpayer

is in business to do? Problem areas

o Isolated or one-of transactionso Extraordinary transactionso Realisation of revenue assetso Compensation for cancellation of contractso Treatment of trading stock

20

Week 3

Is the receipt inside or connected to the circle? GP International Pipecoaters

o Company set up by government contract to build pipe coating factory and then use the factory to coat pipes

o Under contract paid two sums: one to build factory, other to coat pipeso Money to coat pipes is ordinary income, but what about money to build factory?o Court said that is also ordinary income, because the reason the business was set up was

to satisfy the government contract, so the scope of the business included both Californian Copper Syndicate

o Made a distinction between mere realisation of an asset (not ordinary income) as opposed to acts that are carrying on the business itself

o Taxpayer was incorporated, and memorandum association says that their main objective was to acquire land which contained copper

o Spent majority of money to buy copper bearing land, did not have sufficient money to extract copper, and never extracted any

o Later sold land to another company, court had to determine whether the receipt was ordinary income

o Was found to be ordinary income as at all times the company’s intention had been to make a profit selling land – never had enough money to extract copper

Scottish Miningo Different from Copper Syndicate because Scottish Mining actually mined land for coalo Exhausted the mineral and then sold the land, but first subdivided and built roads and

other infrastructureo Court held that profit from sale of land was not ordinary income as company was not in

the business of selling land, it was merely realising their capital to its best advantage

21

Week 3

Whitfordo Said would have decided Scottish Mining differently – did not overturn it thougho Group of fisherman created a company and bought land on the beachfront to fisho Land went up in value, and they sold their shares in the company, and the new

shareholders developed the land, subdivided, and sold as residential propertyo Were these sales ordinary income?o Court said company was carrying on the business of land development, so they wereo At the time the new shareholders acquired the company, the intention of the company

changed – now in the business of developing lando Company had also become one in the business of developing and selling land because

the developments were so extensive – gone beyond mere realisation to its best advantage

o Another point is that judges were controversial in taking net approach rather than gross amount with claiming deductions separately

Extraordinary Transactions Myer

o Gains made from extraordinary transactions may be income where they arise from a commercial transaction entered into by a taxpayer with the intention of making a profit

o Where a future right to interest is converted into a personal lump sum, the present lump sum amount will be income as it replaced future interests, which when derived would be treated as income

o Facts Myer lent $80 million to its subsidiary for seven years Subsidiary would then have to pay interest and capital back Myer sold the right to interest, but not the principle to City Bank for $45 million Issue is Myer would not have lent money to a subsidiary had they not been able

to sell the right to the interest Was the $45 million ordinary income? Court said yes, because it was a commercial transaction with a profit making

intent Westfield

o Clarified Myer because it says that the means to make the profit has to be what was intended in entering into the transaction

o Facts Did business by acquiring land, building their shopping centre, then managing it Realised that this wasn’t the best business strategy because they were sinking

capital in land ownership, so they sold the land and were contracted back to build and run the shopping centre

Court said not every profit with the Myer principle is ordinary income The means by which the profit is made must have been their intention at the

time then entered into the transaction At the time they bought the land, they intended on building and running a

shopping centre – the land was capital, it was never intended to be sold to make money

The possibility of selling land is not the same as intention Cooling

o Lease-incentive case

22

Week 3

o That profit making intent must not be insignificant, but it doesn’t have to sole or dominant

o Facts Brisbane law firm in moving into a new building received a lease-incentive Court said that Myer applied Taxpayer argued that they needed a place to run their business, the incentive

was not the sole or dominant reason for entering into the transaction The court said that it was not insignificant, it doesn’t have to be sole or

dominant

Revenue Asset When a business is investing in shares, the investment is likely to be a capital, but where it is a

revenue asset it is likely to be ordinary income Colonial Mutual Assurance

o A mutual life insurance society that invests its funds in stocks and debentureso Adopted the policy of investing in securities was the most effective way of making

money for their businesso Court said that the taxpayer should be assessed on the profit of realising those capital

investmentso An insurance company is undoubtedly carrying on an insurance business and the

investment of funds is as much a part of that business as collecting premiums National Bank of Australia

o Contrast with Colonial Bank of Australia, have to look at circumstanceo Bought shares with the intention of a merger – not about investmento When they sold those shares, it was therefore capital and not revenue assets

Treating Trading Stock The full proceeds of any sales are assessable in the year of sale as a gain from carrying on the

business of trading – s 70-80(1) and s 6-5 The full cost of purchasing trading stock is deductible in the year of purchase – s 70-15;

o Compared to s 8-1 deduct when you incuro S 70-15 says you deduct when you have it on hand

‘On hand’ – when you have the power to dispose of the stock All State Frozen Food

Therefore do not need legal ownership or physical possession, as long as you have the power to dispose of it

Any changes in stock levels over the trading year (opening and closing values) is accounted for by (s 70-35):

o Including in income any excess of closing stock over opening stock; oro Allowing as a deduction any decrease in stock over the period.

The opening stock figure is the same as the previous year’s closing figure (s 70-40); Three alternative bases for valuing closing stock on hand; s 70-45 ITAA97:

o Costo Market selling valueo Replacement value.

23

Week 4

Week 4

Deductions

Section 8-1: General deductions (1) You can deduct from your assessable income any loss or outgoing to the extent that:

o (a) It is incurred in gaining or producing your assessable income; or o (b) It is necessarily incurred in carrying on a * business for the purpose of gaining or

producing your assessable income. Note: Division 35 prevents losses from non-commercial business activities that may contribute

to a tax loss being offset against other assessable income. (2) However, you cannot deduct a loss or outgoing under this section to the extent that:

o (a) It is a loss or outgoing of capital, or of a capital nature; or o (b) It is a loss or outgoing of a private or domestic nature; or o (c) It is incurred in relation to gaining or producing your * exempt income or your *

non-assessable non-exempt income; or o (d) A provision of this Act prevents you from deducting it.

For a summary list of provisions about deductions, see section 12-5. (3) A loss or outgoing that you can deduct under this section is called a general deduction. For the effect of the GST in working out deductions, see Division 27. Note: If you receive an amount as insurance, indemnity or other recoupment of a loss or

outgoing that you can deduct under this section, the amount may be included in your assessable income: see Subdivision 20-A.

S 8-1(1): The Two Positive Limbs You can deduct from your assessable income any loss or outgoing to the extent that:

o It is incurred in gaining or producing your assessable income; ORo It is necessarily incurred in carrying on a business for the purpose of gaining or

producing your assessable income. Note that only businesses can rely on the second limb First limb

o Elements There must be a loss/outgoing expense And it must be connected with the producing of assessable income

o Typically include: Work clothing Tools of trade Technical journals Self-education expenses Home office expenses Motor vehicle expenses Professional association fees

Second limbo Elements

There must be a loss/outgoing expense Must be connected with the carrying on of a business It must be a business (addressed in Week 3) Must be necessary

o Will typically include

24

Week 4

Cost of acquiring trading stock Plant/equipment hire costs Salary/wage costs Expenditure on market research Rental costs Interest and bank charges Advertising expenses FBT Cost of utilities

‘Loss’o Charles Morre

Ran a production company in Perth Each morning would take previous day’s cash to the bank Was held at gunpoint and robbed Court held that this was a loss as taking money to the bank is a necessity and

was the ordinary carrying on of their business Apportionment – ‘to the extend that’ indicates a loss or outgoing may need to be apportioned

o Ronpobin Pino Two types of mixed exp:

Consists undivided items in respect of things/services of which distinct and servable parts are devoted to gain/producing assessable income and other cause.

A single outlay/charge that serves both objects indifferently. ‘Incurred’

o The loss/outgoing must be ‘incurred’ in the year it is claimed as a deduction.o An outgoing is ‘incurred’ when the taxpayer is definitely committed to the outgoing –

this may precede actual payment.o S 26-10 applies to leave payments.o If there is no provision to say when the loss occurred, refer to cases and the facts

‘In’o The connection/nexuso To be deductible, the loss/outgoing must be relevant and incidental to the gaining of

assessable income – that is, there must be a connection between the expenditure and the income production.

Gaining/producing assessable income (first limb) Carrying on a business for the purpose of gaining/producing assessable income

(second limb)o There are a number of different tests in case law

Incidental and Relevant Look to the operations/ activities regularly carried on for the production

income than to purpose in itself. Is it incidental to what they do? Amalgamated Zinc

Essential Character Done separately to incidental and relevant Used when there is an expense that has a private labour to it Is it essentially a business expense, or a private expence? Objective or subjective approach?

o Objective approach – what benefit to you get from it? Cecil Brothers

25

Week 4

Phillipso Subjective

Will only look at subjective approach when something is not right about it

High expense and low gain – the court will then look to the subjective intention of the tax payer

Temporal Connection Courts have adopted not required a particular loss or outgoing to be

matched with the production of a specific amount of assessable income Will only consider timing when there is a pre- and post- business

expense (haven’t started/have finished business) Pre-business expenses are not normally deductible

o Softwood Pulp and Paper Ltd The taxpayer had not yet committed to the project nor

made a definite decision to do soo Griffin Coal Mining Company Ltd v FCT

The expenditure did not relate to their existing business, but to a new source of income

o However, there draws a distinction as to whether they are already committed or not. Where they have committed, they may be deductible

Travel Lodge Papua New Guinea Steele

o Note that there may also be an exception for small business entities seeking advice in establishing their business

Post-business expenses are not normally deductibleo Amalgamated Zinco However, if you can satisfy the following test, then they are:

Whether the ‘occasion for the loss/ outgoing [can be] found in the business operations’ directed to gaining or producing assessable income

Placer Brown Jones

‘Necessarily Incurred’o Courts have interpreted the word ‘necessarily’ liberallyo Snowden & Wilson

Dixon, J ‘Necessarily’ = to be dictated by business ends (what is good for the business)

Fullager, J ‘Necessarily’ = within reason, to be judged by person who is carrying out the business

o This does not mean that the expense must be unavoidable Magna Alloys

S 8-2: The Four Negative Limbs However you cannot deduct a loss or outgoing to the extent that:

o It is a loss or outgoing of capital, or of a capital nature; oro It is a loss or outing of a private or domestic nature; oro It is incurred in relation to gaining or producing your exempt income; or

26

Week 4

o A provision of this Act prevents you from deducting it. The First Negative Limb: Three tests

o Once and for all Vallambrosa Rubber If it is one payment, then it is likely to be capital If it is regular, then it’s revenue

o The ‘enduring benefit’ test British Insulated Is it looking to bring an asset that is lasting in nature? If so, it is likely to be capital

Not necessarily thougho The ‘business entity’ test

Sun Newspapers The starting point If it relates to the business structure, then it is capital If it relates to process, then it is income

Does it simply allow the business to operate? If so, it is process

Three factors that need to be taken into account to determine if it is structure or process

Would the character of the advantage sought be lasting The manner it would be used The means adopted for payment

o If it is capital, it cannot be deducted under s 8-1 There are three alternative options

CGT Specific deductions

o Depreciating asseto Capital expenditure that is not otherwise deductible may be

deductible over 5 years under s 40-880 ITAA 1997.o Called ‘blackhole expenditure’, it covers business capital

expenditure not otherwise taken into account and not denied a deduction under some other provision of the Act.

The Second Negative Limb: Private or Domestic Expenditureo Anything not directly connected to your income-earning activities.

The Third Negative Limb: Expenditures incurred in gaining exempt income or non-assessable non-exempt income

The Fourth Negative Limb: The Act Prevents Deductiono Any expenditure that the Act specifically makes non-deductibleo Examples include:

Business entertainment – Div 32, especially s 32-5. Fines and penalties – s 26-5. Some otherwise deductible education expenses - s 26-20 (HELP/HECS

payments); s 82A (first $250 of other expenditure). Some corporate carry forward losses and bad debt write-offs – Div 165). Excessive payments to associates – Div 7A and s 26-35

Common Types of 8-1 Deduction Travel to or on work

27

Week 4

o Cost of travel ‘on’ work is deductible. Lunney

o Cost of travel to find new employment is not deductible. Maddalena

o Cost of travel to and from work is not deductible; Hayley Exceptions

Itinerant workerso Wiener

On stand-by dutieso Collings

Transport bulky goodso Vogt

Two distinct places of worko S 25-100o One of those workplaces cannot be home

o If claiming motor vehicle expenses, rules apply under div 28 that apply to partnerships and individuals, and the expenses must be substantiated under div 100

Self-Education Expenseso Are deductible if:

If directly relevant to the taxpayer’s current income earning activities. If they enable taxpayer to keep abreast of developments in his/her field

Finn If they will enable the taxpayer to better discharge existing income producing

duties Wilkinson Studdert

If likely to lead to an increase in income Highfield

Linked to other kinds of assessable income Anstis

o Education is not considered capital in nature Hatchett

o If it can be connected to employment then it is not considered private Finn

o S 26-9 prevents from claiming a deduction if it related to rebatable benefitso Where there is HECS, there will be no deduction unless it is a fringe benefit under s 26-

20o In some cases there will be a limit on deduction under s 82Ao Non-Deductable

If designed to enable taxpayer to get employment or to get new employment. If designed to open up a new field of income producing activity. The first $250 of expenses in a ‘prescribed course of education’ (s 82A). Rebatable benefits (s 26-19). HECS payments (s 26-20).

o Deductable Child Care Expenses

o General rule – not deductibleo May be prerequisite but neither incidental or relevant

28

Week 4

o Essential character is private Martin 84ATC 4513

o Now, taxpayers are entitled to a Child Care Benefit - and a Child Care Rebate equal to 50% of the out-of-pocket cost of child care, over the amount of the benefit, up to a maximum of $7,500 per child per annum.

Subdivision 61-1A Home Office Expenses

o Where the taxpayer engages in income producing activity at homeo Must distinguish between

The home as a place of business The home containing an office or private study

o Where the place of business is at home, then can claim both occupancy expenses and running expenses

o Where there is only a home office, then can only claim occupancy expenseso Factors to indicate that it is a place of business

It is clearly indicated as a place of business The area is not suitable for domestic use It is used exclusively/almost exclusively for ordinary business Clients visit this space

o Factors to indicate a study A place of convenience Simply taking home work and completing it at home in this area

o Occupancy expenses Calculated on a floor area basis Must take into account parts of the year that the business is not operating Include

Rent Mortgage interest Rates Insurance premiums

o Running expenses Include

Heating, lighting and cooling expenses Cleaning costs Depreciation, insurance and repairs on equipment Leasing charges on equipment Maintenance costs Telephone expenses Internet expenses

o Note that this will fill main resident exemption when selling the home, will be CGT consequences

Clothingo Generally not deductible unless

Compulsory uniforms Non-compulsory corporate wardrobes

Registered under Div 34 Occupation specific clothing Protective and safety clothing and equipment

o Edwards

29

Week 4

A governor’s wife’s assistant claimed that she was required to dress better and was able to deduct

Can only claim to the extent that it exceeds the previous year or other professional activity

o Mansfield A flight attendant was able to claim moisturiser, air conditioner, and shoes half a

size bigger Entertainment expense

o Generally not deductable under s 8-1 due to div 32 Especially s 32-5

o Exceptions are also found in div 32 Damages and legal expenses

o Generally deductible IF incurred in gaining or producing assessable income;o This can include expenses incurred in defending criminal proceedings related to your

income earning activities;o Unless an outgoing of capital or of a private nature

Broken Hill Theatres John Fairfax PBL Marketing

o But fines and penalties are not deductible – s 26-5o Some legal expenses are specifically deductible (e.g. Borrowing expenses are

deductible under s 25-25.) Interest Payments

o Interest paid on borrowed funds is deductible if the money was borrowed for the purpose of gaining assessable income.

Consider: was the money used for income producing purposes?o The deductibility of interest will usually depend upon the objective use to which the

borrowed funds are applied and not the security provided for the loan Munro (objective test)

o If colourable circumstance the court may consider the subjective purpose and may deny or allow apportionment

Ureo If it is a pre-business expense, consider level of commitment to the business

Steeleo Interest that is a post-business expense may be deductible

Amalgamated Zinco Refinancing principle: If you can deduct using the use these before the finance then

after the refinancing you can continue to deduct the interest expenditure. Roberts v Smith

30

Week 5

Week 5

General deductions (s 8-1 ITAA 1997) This is a general provision under which most deductions are claimed.

Specific deductions (s 8-5 ITAA 1997) Deductions allowed under specific provisions for particular outgoings (eg depreciation)

Note: A number of provisions that deny deductibility where the outgoing might otherwise be deductible (e.g. entertainment expenses)Cannot claim double deductions

Specific Outright Deductions

Repairs – s 25-10 You can deduct expenditure you incur for repairs to premises (or part of premises) or a

depreciating asset that you held or used solely for the purpose of producing assessable income. If you held or used the property only partly for that purpose, you can deduct so much of the

expenditure as is reasonable in the circumstances. You cannot deduct capital expenditure under this section. Elements

o Expenditureo You incuro For repairso To premises or a depreciating asseto Held or used solely or partly

Issueso Is it a repair?o If it is a repair, is it of a capital nature?

Capital if: Addition Improvement Initial repair

Note: If you are unable to get a deduction for repair What is a repair?

o Repair involves restoring an asset to its previous condition without changing its character

W Thomaso Can involve the ‘renewal or replacement of subsidiary parts of a whole” but not

“reconstruction of the entirety’ Lurcott Lindsay

o Extensive works that constitute the acquisition of a new asset are not repairs Lindsay Western Suburbs

o Essential that the asset’s function does not change If the function changes, it is not a repair

o Pre-emptive repairs are deductible Repairs are not limited to rectifying defects that have already become serious Can’t claim a deduction if it results in an improvement

31

Week 5

BP Oil Refinery Deductions can be claimed for work that is done partly (or even) largely to

prevent or anticipate defects or damage or to rectify defects in their early stageso Notional repairs are not deductible

Western Suburbs Cinemas Hypothetically, if there was a repair that could have been done, but you have

gone beyond it, you can’t claim for the cheaper amount that could have been done

This is because you haven’t actually done it If it is a repair, is it of a capital nature?

o Capital if Addition

Did the work result in an expansion of the basic capital structure? Improvement

Did the work make the item significantly functionally better than it was previously?

o Western Suburbs Cinemas Initial repairs

Did the defects exist at the time of acquisition?o W Thomaso Law Shippingo It is irrelevant if the defect was unknown at the time of purchase

o Improvement Use of materials different from the original is not necessarily fatal to the claim

for a deduction (especially if that use involves both advantages and disadvantages)

Ask whether the work improves the value of the asset (from its original state – not from its state of disrepair).

Does the expenditure reduce the likelihood of having to do future repairs?

Bad Debts – s 25-35 To get a deduction for writing-off a bad debt you must show that there was:

o A debt (an existing debt);o That you write off as bad;o In the income year; ando It was included in your assessable income for the income year or for an earlier income

year; oro Be in respect of money that TP lent in the ordinary course of their lending money

business Basically, make an assessment that the money is non-recoverable The debt had to be written off in the same income year as the bad debt Partial Write-offs

o If you get part of what you are owed but have to write off the balance you get a deduction for the part you write off – see s 25-35 (1) and (3)

Recovery of a written-off bad debto The recovered amount (referred to as a ‘recoupment’) is income and taxable in the year

of recovery – see s 25-35(5) Item 4 and ss 20-20(3) and 20-30(1) item 1.4

32

Week 5

Carry Forward Losses – Div 36 Tax losses can only be carried forward and offset against income in a later year

o Can be carried forward indefinitely Carry forward losses are offset first against exempt income (if any) and then against assessable

income. They are offset in the order in which they were incurred The rules differ slightly for corporate tax entities (s 36-17) and other tax entities (s 36-15).

o Corporate tax entities may choose the amount they offset in the later year and may choose a nil amount

Gifts – Div 30 Cannot claim an 8-1 deduction

o Cannot use it to make moneyo Considered private

Specific deduction under div 30o Will only be deductible if they fall within div 30o Individuals giving to hospitals, schools, universities, sports, recreation or cultural

groups, etc. Must be $2 or more, and to certain recipients Must be genuine gifts

o Property must be transferred without any material benefit to the donoro Cyprus Mine Corporation

Deductions Over Time

Prepayments See ss 82KZL-82KZME Advance payments are generally deductible over the life of the benefit or 10 years, whichever

is the lesser (the ‘eligible service period’), unless they are:o ‘Excluded expenditure’ (amounts under $1000 or that are required to be paid by law or

by an order of a court or are salary or wages paid under a contract of service).o Non-business pre-payments by individuals - where the eligible service period is 12

months or less and ends no later than the last day of the next tax year (the ‘12 month rule’)

o Prepaid expenditure by eligible small business entities – the ‘12 month rule’ applies. If the eligible service period exceeds 12 months use the general rule.

Borrowing Expenses – s 25-25 A deduction is permitted for borrowing expenses PROVIDED the loan is used for income

producing purposes. ‘Borrowing expenses’ include loan establishment fees, procuration fees, legal expenses, stamp

duty and loan guarantee insurance etc. They do not include interest – which is separately deductible. Borrowing expenses are generally deducted over the life of the loan or 5 years, whichever is

the LESSER. Unless they amount to $100 or less - when you write them off in the year of expenditure.

33

Week 5

Depreciation/Uniform Capital Allowance System – Div 40 Deduct an amount equal to the decline in value of a depreciating asset (see s 40-25); Which has a limited effective life and which is reasonably expected to decline in value (s 40-

30); Which is held by the economic owner (s 40-40); Beginning when you first use it or have is installed ready for use (the start time – s 40-60); And ending at the end of its effective life (s 40-95). Will not include intangible objects Choice of method to calculate decline in value

o Two choices available Prime cost method:

Asset cost × daysheld365

× 100 %effective life

Assumes a uniform decline in value Diminishing value method:

Base value × days held365

× 200 %effective life

Assumes greater decline in value in early years ‘Base value’ is the cost (in the start time year) and the opening adjustable

value (in subsequent years). The opening adjustable value Effective life

The commissioner determines the effective life, or you can estimate the effective life for your own use

o The choice is made on an asset by asset basis

34

Week 6

Week 6

Substantiation

To be deductible under s 8-1 or a specific deduction provision certain types of outgoing/ loss will need to comply with substantiation rules. The substantiation provisions are contained in Div 900 and for ‘car expenses’, Div 28 ITAA97. Who must substantiate?

Those required to substantiate losses and outgoings are:o S 900-5(1) - an individualo S 900-5(2) - a partnership that includes at least one individualo S 900-5(3) - no other entity.

What records are required? The records differ depending on the type of expenditure involved. Therefore:

o Determine what sort of expenditure you are incurring;o Determine from Div 900 what records are required for that sort of expense.

What expenses must be substantiated? S 900-10

Work Expenses A work expense is a loss or outgoing you incur in producing your salary or wages

o S 900-30(1) To be able to claim a work expense deduction, first must qualify for the deduction under s 8-1,

then must provide the written evidence in s 900-E Must keep records of travel where it includes being away for six or more nights Must retain the records for five years

o S 500-25 900-115 – Written evidence from supplier 900-120 – Depreciation Two exceptions to requirement for record from supplier

o Claim for small items costing less than $10 each and totalling less than $200 in the year of income, you can make a record of your expenses

S 900-125o Expenses too hard to substantiate

S 900-130 No documentary evidence required for

o Total work expenses (including laundry/ excluding travel allowance and meal allowance expenses) are $300 or less – s 900-35

o Laundry expenses to $150 – s 900-40 Does not include dry cleaning

o Work related expenses related to an award transport payment – s 900-45o Domestic travel allowance expenses – s 900-50o Overseas travel allowance expenses – s 900-55o Reasonable overtime meal allowances – s 900-60o Airline crews – s 900-65

35

Week 6

Business Travel Expenses A ‘business travel expense’, in so far as you incur it in producing your assessable income other

than salary or wages [s 900-95(1)]. An expense is a ‘travel expense’ if you incur it for travel that involves you being away from

home for more than one (1) night either inside Australia or overseas [s 900-95(2)]. Conditions of deductibility

o The expense must be deductible anywayo Written evidence is requiredo Travel records may be required

Car Expenses Two methods for calculating car expense deductions (Div 28):

o Cents per kilometre method Limited number of kilometres – 5000 business kilometres Number of kilometres based on reasonable estimate Commissioner determines rate (66c per kilometre 2015-16 income year) Does not need to be substantiated

o Log book method S 28-90(1): each car expense x business use percentage S 28-90(3): business use percentage = business kms

total kms Do it for the first year, and can use the same percentage for the next four years

unless chance in method or business use Substantiation

Log book for at least 12 weeks Odometer records

o Subdivision 28-H Written evidence of expenses Fuel and oil may be substantiated by odometer records Failing to substantiate

o Section 900-195 Commissioner’s Discretion Where taxpayer has not complied with substantiation