Embed Size (px)

Citation preview

Wells Fargo 9th Annual Pipelineand MLP Symposium

Wells Fargo 9th Annual Pipelineand MLP Symposiumand MLP Symposiumand MLP Symposium

Barry E. DavisPresident and CEO

Barry E. DavisPresident and CEO

1

President and CEOCrosstex Energy

President and CEOCrosstex Energy

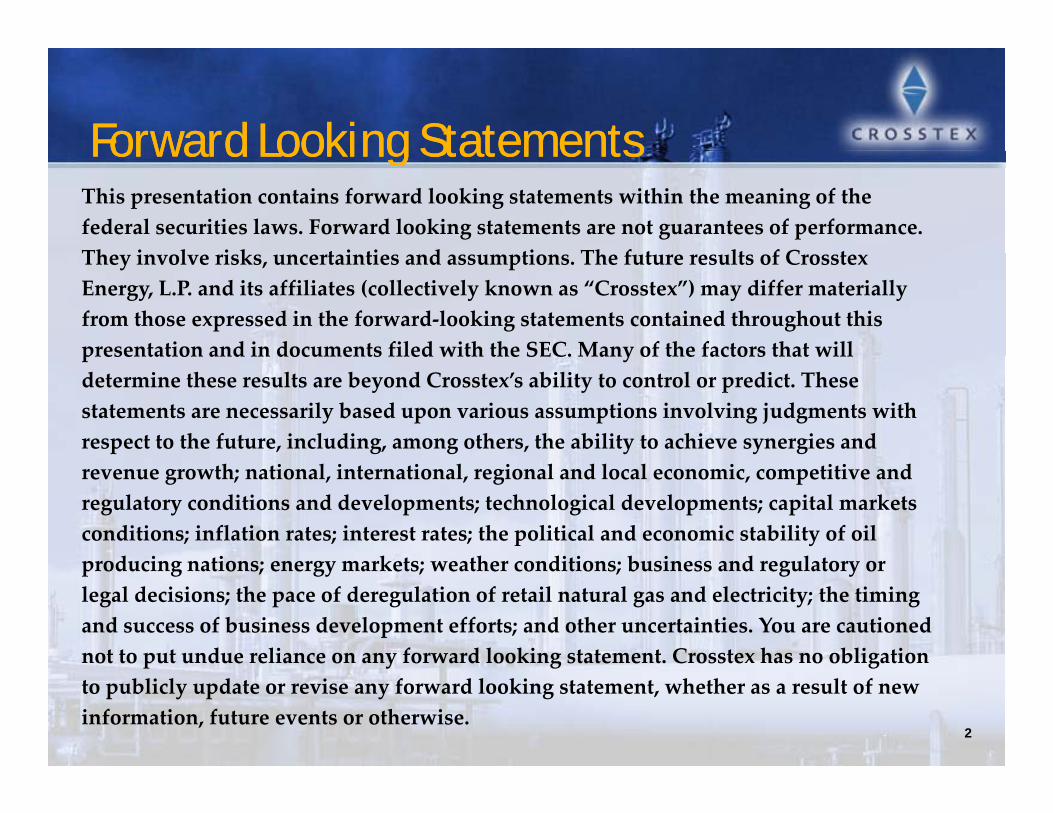

Forward Looking StatementsForward Looking StatementsForward Looking StatementsForward Looking StatementsThis presentation contains forward looking statements within the meaning of the federal securities laws. Forward looking statements are not guarantees of performance. Th i l i k t i ti d ti Th f t lt f C tThey involve risks, uncertainties and assumptions. The future results of Crosstex Energy, L.P. and its affiliates (collectively known as “Crosstex”) may differ materially from those expressed in the forward‐looking statements contained throughout this presentation and in documents filed with the SEC. Many of the factors that willpresentation and in documents filed with the SEC. Many of the factors that will determine these results are beyond Crosstex’s ability to control or predict. These statements are necessarily based upon various assumptions involving judgments with respect to the future, including, among others, the ability to achieve synergies and revenue growth; national, international, regional and local economic, competitive and regulatory conditions and developments; technological developments; capital markets conditions; inflation rates; interest rates; the political and economic stability of oil odu i atio e e y a ket eathe o ditio bu i e a d e ulato y oproducing nations; energy markets; weather conditions; business and regulatory or

legal decisions; the pace of deregulation of retail natural gas and electricity; the timing and success of business development efforts; and other uncertainties. You are cautioned not to put undue reliance on any forward looking statement. Crosstex has no obligation

2

ot to put u due e ia ce o a y o wa d oo i g state e t. C osste as o ob igatioto publicly update or revise any forward looking statement, whether as a result of new information, future events or otherwise.

Strategically Positioned for Strategically Positioned for Performance and GrowthPerformance and GrowthPerformance and GrowthPerformance and GrowthWell positioned assets

Access to full midstream value chain

Strong organizational capabilities

Financially strong with access to capitalFinancially strong with access to capital

Poised to take advantage of the macro environmentg

Focused on long‐term, high‐return growth projects

3Resumption of dividends and distributions

We We SpanSpan the Value Chainthe Value Chain

id i f d

Focused Midstream CompanyFocused Midstream Company Diversity of ServicesDiversity of Services

Over 2 800 miles of natural gas gathering

We We SpanSpan the Value Chainthe Value Chain

Midstream energy services company focused

on full value chain

Assets strategically located in key producing

Over 2,800 miles of natural gas gathering

and transmission pipeline

9 natural gas processing plants

areas and market regions

Focus on Barnett and Haynesville shale plays

3 fractionators

Over 450 miles of NGL pipeline

2 4 MM barrels of NGL storage capacity2.4 MM barrels of NGL storage capacity

Transmission Lines

Natural Gas Consumers

Gathering, Dehydration & Compression NGL Transportation &

Fractionation

4Wellhead Processing , Conditioning & Treating

NGL Markets

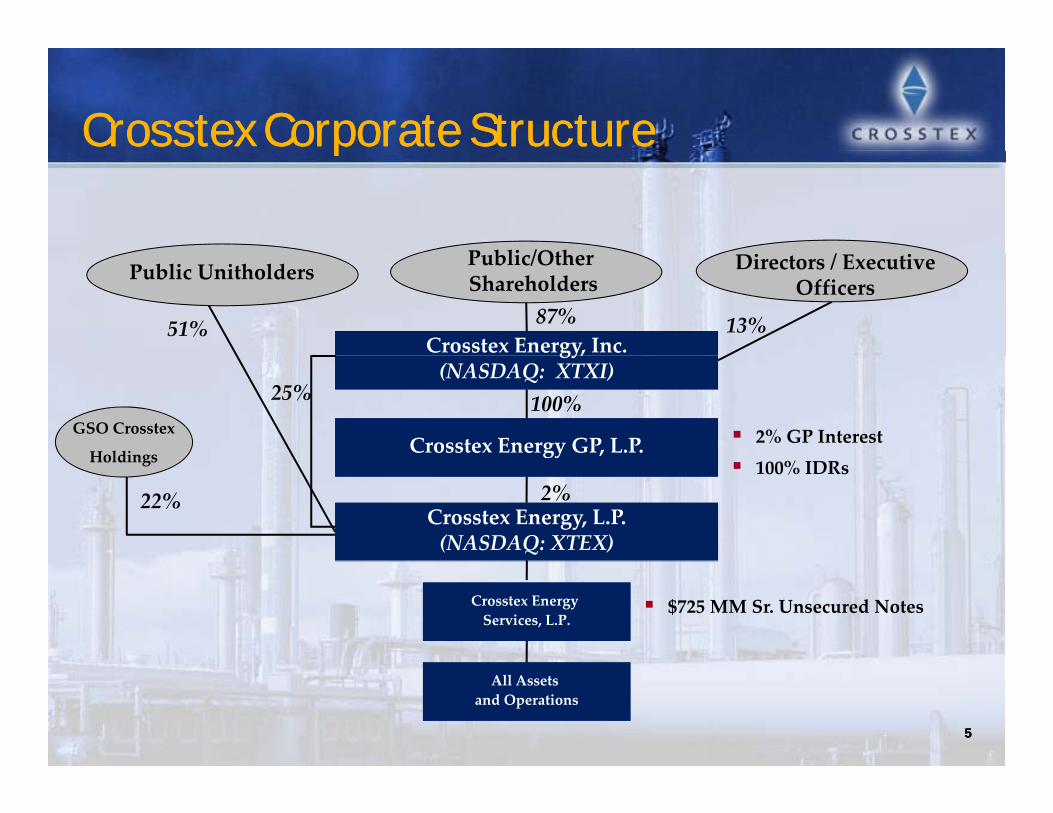

Crosstex Corporate StructureCrosstex Corporate Structure

P bli /Oth

pp

Public/OtherShareholdersPublic Unitholders

51%Crosstex Energy, Inc.Crosstex Energy, Inc.

Directors / Executive Officers

87% 13%

Crosstex Energy GP, L.P.Crosstex Energy GP, L.P.

100%2% GP Interest

gy,(NASDAQ: XTXI)

gy,(NASDAQ: XTXI)

25%GSO Crosstex

Holdings gy100% IDRs

2%Crosstex Energy, L.P.(NASDAQ: XTEX)Crosstex Energy, L.P.(NASDAQ: XTEX)

22%

Holdings

Crosstex Energy Services, L.P.

Crosstex Energy Services, L.P.

$725 MM Sr. Unsecured Notes

5

All Assets and OperationsAll Assets

and Operations

5

Strategically Positioned Assets Strategically Positioned Assets Strategically Positioned Assets Strategically Positioned Assets North Texas

~780 miles of pipeline3 processing plants3 processing plants

Processing & NGLs ~440 miles of NGL pipeline

LIG ~2,100 miles of pipeline2 processing plants

440 miles of NGL pipeline4 processing plants

2 fractionation facilities

$352010 Guidance ($MM)

$111 (50%)

$35 (16%)

6

$74 (34%)

NTX LIG PNGL

North TexasNorth Texas

7

NTX: Strategically Positioned in the NTX: Strategically Positioned in the Barnett ShaleBarnett ShaleBarnett ShaleBarnett Shale

Fossil CreekFossil Creek

Benbrook

Well Positioned Assets (current capacity) :

NTPL – 375 MMcfd

NTX Gathering Assets – 1 Bcfd +

Azle plant – 50 MMcfdNorth Texas Gathering Systems

8

Goforth plant – 30 MMcfd

Silvercreek plant – 200 MMcfd

SystemsNorth Texas Pipeline

Processing Plant

NTX: New Long Term Gathering NTX: New Long Term Gathering AgreementsAgreementsNorth Texas Expansion Project 1:

N 10 t t t N TX V l it t f t l t 50

AgreementsAgreements

New 10 yr. transport agreement on N.TX Volume commitment of at least 50

MMBtu/d

Expected capital of less than $10 million cashExpected capital of less than $10 million cash

Expected annual run‐rate cash flow of approximately $8 million

System expected in operations first quarter 2011 y p p q

North Texas Expansion Project 2:

$25 million, 15‐mile expansion project supported by volumetric commitments$ , p p j pp y

Seven‐mile low‐pressure pipeline, eight‐mile high‐pressure pipeline and

compressor station in southwest Tarrant County

Peak flow rate in 2012 expected to be more than 100 MMBtu/d

System expected in operation first quarter 2011 9

Barnett Shale Volume / Undeveloped Barnett Shale Volume / Undeveloped Location ProjectionLocation ProjectionLocation ProjectionLocation Projection

Barnett Volume Projection(PIRA 2/10 Fcst)* Approximate number of undeveloped locations remaining as of April 1, 2009

10,000

12,000

(PIRA 2/10 Fcst) pp p g p

6,000

8,000

MMCFD

17K*

22K*

2,000

4,000

M

11K*

‐

J‐90

J‐91

J‐93

J‐94

J‐96

J‐97

J‐99

J‐00

J‐02

J‐03

J‐05

J‐06

J‐08

J‐09

J‐11

J‐12

J‐14

J‐15

J‐17

J‐18

Hi h B L

10Source: Netherland, Sewell & Associates, Inc.

High Base Low

LIGLIG

11

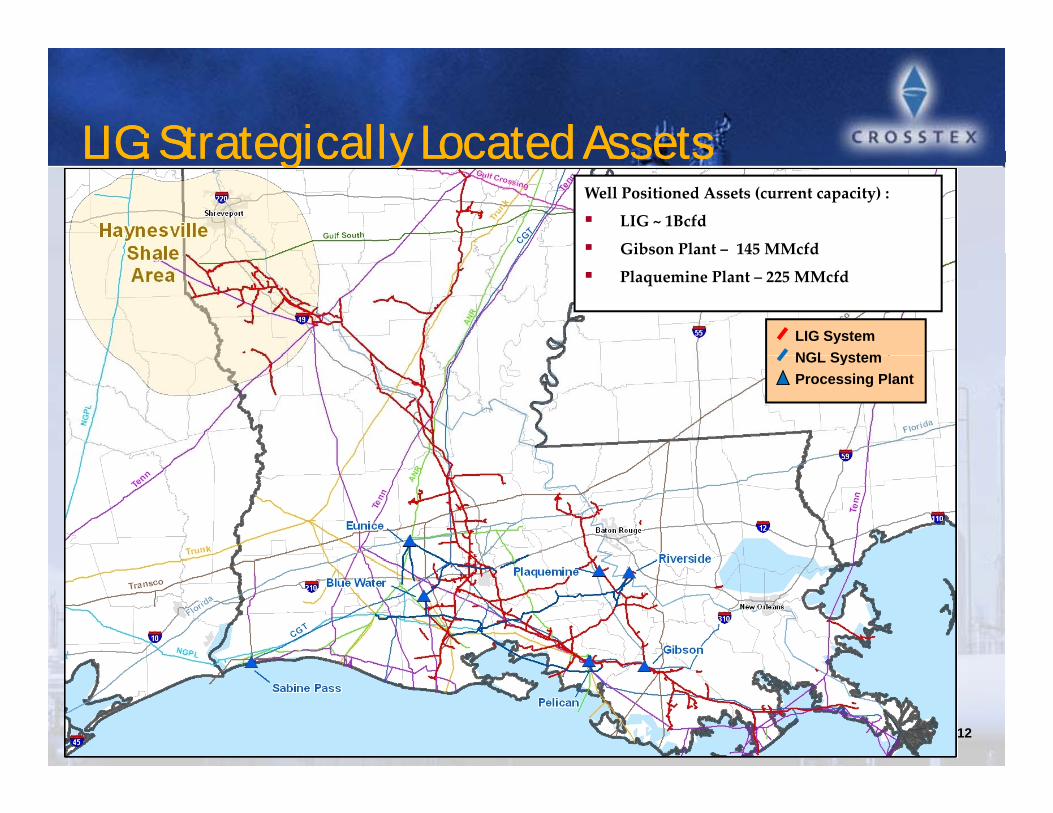

LIG: Strategically Located AssetsLIG: Strategically Located AssetsLIG: Strategically Located AssetsLIG: Strategically Located AssetsWell Positioned Assets (current capacity) :

LIG ~ 1Bcfd

Gibson Plant – 145 MMcfd

LIG System NGL System

Gibson Plant 145 MMcfd

Plaquemine Plant – 225 MMcfd

NGL System Processing Plant

12

LIG: Strong Execution LIG: Strong Execution Haynesville OpportunitiesHaynesville OpportunitiesHaynesville OpportunitiesHaynesville Opportunities

Haynesville ProjectsCapacity MMcf/d Avg. Contract

I S i T t l C t t d THaynesville Projects In Service Total Contracted Term

N. LIG Contracted Projects

Red River Project Q3 2007 240 240 5 yr

North LIG Expansion Phase I Q4 2008 35 35 10 yr

North LIG Expansion Phase II Q2 2009 100 100 10 yr

Black Lake Interconnect Phase III – Part I Q4 2009 35 35 3 yr

Red River Amine Unit (120 MMcf/d Capacity) Q4 2009 3 yr

Black Lake Interconnect Phase III – Part II Q2 2010 25 25 1.5 yrBlack Lake Interconnect Phase III Part II Q2 2010 25 25 1.5 yr

LIG Phase IV Expansion‐ Part I Q3 2010 30 30 5 yr

Total Contracted 465 465Wtd. Avg. Life

5 yearsy

13

Processing and NGL’sProcessing and NGL’s

14

PNGL: Strategically Located Assets PNGL: Strategically Located Assets PNGL: Strategically Located Assets PNGL: Strategically Located Assets

Truck and rail from Marcellus, Bakken, Eagle Ford, Permian Basin

Well Positioned Assets (current capacity) :

Eunice – 1.2 Bcf/d; 50,000 Bbls/d

15

; ,

Pelican – 600 MMcf/d

Sabine – 300 MMcf/d

Riverside ‐ 20,000 Bbls/d

PNGL: Eunice PNGL: Eunice FracFrac RestartRestartPNGL: Eunice PNGL: Eunice FracFrac RestartRestartRestarting 15,000 Bbls/d of existing 36,000 Bbls/d frac

Capex ‐ $9.3MM with op income contribution of $3.3MM annually

Economics supported by volume commitments and expense savings

Project will connect Plaquemine fractionation into our NGL system

Upside – additional capacity to bring liquids from other plays

16

Growth Opportunities Growth Opportunities

17

Shale OpportunitiesShale OpportunitiesShale OpportunitiesShale OpportunitiesShale OpportunitiesShale OpportunitiesShale OpportunitiesShale OpportunitiesKey Macro Trends:• Crude/gas ratio driving focus to wet

Montana Thrust Belt

Williston Basin

Gammon

Cody

AppalachianMichigan

Devonian (Ohio)

driving focus to wet gas/crude opportunities• Continued low gas prices could impact dry

Hilliard-Baxter Mancos

Hermosa

Mancos

Excello-

Antrim

New

AppalachianBasin

MichiganBasin

IllinoisBasin

ForestCity BasinPiceance

Basin

Unita Basin

GreaterGreenRiverBasin

Marcellus

Utica

prices could impact dry gas development •Producers sale of undivided property i te e t i etu fo

LewisPierre

Barnett

WoodfordFayetteville

Mulky Albany

Chattanooga

Conasauga

Valley andRidge Province

Black WarriorBasin

Floyd-NealTexas-

Louisiana

Arkoma Basin

Cherokee Platform

AnadarkoBasin

Ardmore Basin

Permian

Palo DuroBasin Bend

RatonBasin

San JuanBasin

MarfaBasin

Paradox Basininterest in return for drilling carry has provided near‐term growth cap ex for drilling

Barnett-Woodford

Pearsall-Eagle Ford

EagleFord

Haynesville- Bossier

Ridge ProvinceLouisiana-Mississippi Salt Basin

Ft. WorthBasinMaverickSub-Basin

Rio GrandeEmbayment

Basindrilling• Lack of NGL infrastructure (RM transport and fractionation) will be

Basins Shale Gas Plays Shallowest / Youngest Deepest / Oldest

fractionation) will be key for continued development

18Source: EIA

Growth, Focus and PrioritizationGrowth, Focus and PrioritizationGrowth, Focus and PrioritizationGrowth, Focus and PrioritizationGrowth, Focus and PrioritizationGrowth, Focus and PrioritizationGrowth, Focus and PrioritizationGrowth, Focus and Prioritization

Company’s strategic advantages include:E f ti ti ith il d b– Excess fractionation with rail and barge access

– NGL market knowledge through PNGL– Experience with large shale developmentsp g p– Regional experience (i.e., Texas and Louisiana)– Producer relationships/customer service

Targeted areas include:– Emerging shale plays focusing on wet gas/crude– NGL opportunities utilizing existing infrastructure– Large scale gathering, processing and take‐away

19

Financial OverviewFinancial Overview

20

CurrentCurrent Financial FocusFinancial FocusCurrentCurrent Financial FocusFinancial Focus

Maintaining strong liquidity position for flexibility– No near term debt maturities– Over $300 million available on revolver

Deleveraging balance sheet

Improving cash flows

Focusing on high return investmentsFocusing on high return investments

21

Conservative Financial GuidelinesConservative Financial GuidelinesConservative Financial GuidelinesConservative Financial GuidelinesFund organic growth and strategic opportunities with internal cash flows and a balanced mix of debt and equityflows and a balanced mi of debt and equity

Maintain a balanced contract mix and an active commodity price hedging program consistent with risk management guidelines

N l i h d i i i i f ki– No speculative hedging positions, no compensation for takingpositions

– Utilization of product‐specific swaps

Maintain adequate liquidity to manage business cash flow requirements, margin requirements and business risks

Maintain a conser ati e capital structure and le erage ratiosMaintain a conservative capital structure and leverage ratios– Achieve a ratio of Debt/EBITDA of 4.0x

22

Operating Income Summary & Operating Income Summary & Operating Income Mix ($ MM)Operating Income Mix ($ MM)Operating Income Mix ($ MM)Operating Income Mix ($ MM)

2008 2009 2010 (3)

$100

$120

$140 NTX G&T NTX Fee Based NTX Commodity Based

North Texas $103 $113 $111

LIG $82 $80 $74$‐

$20

$40

$60

$80

2006 2007 2008 2009 2010

PNGL (1) $12 $23 $35

Shared Services & Other ($14) ($14) ($13)$50

$60

$70

$80

$90

LIG Mktg. & Trans. LIG Fee Based LIG Commodity Based

Total Continuing Operations $183 $202 $207 ….

Discontinued Operations(2) $91 $50 $0$‐

$10

$20

$30

$40

$50

2007 2008 2009 2010

Total $274 $252 $207

(1) Includes impact of Eunice lease buy‐out in 2009 and Intracoastal acquisition‐‐ $2 MM $20

$25

$30

$35

$40

$45

PNGL Fee Based PNGL Commodity Based

impact in 2009 and $13 MM impact in 2010

(2) Includes contributions from sold assets (STX, Miss, Ala, Treating, Seminole interest,

Arkoma, and ETX)

(3) 2010 represents mid‐point of guidance 23$‐

$5

$10

$15

$20

2007 2008 2009 2010

Gross Gross Margin By Contract Type Margin By Contract Type Gross Gross Margin By Contract Type Margin By Contract Type

2008 (1) 2009 (1)

Non‐commodity based margins have increased from ~68% in 2008 to greater than 81% in 2010 (in Guidance)

2010 (Guidance)

15%

G& T Fee POL Proc Margin

13%

9%

G& T Fee POL Proc Margin

14%

5%

G& T Fee POL Proc Margin

58%

10%

17%

66%

12%

65%

16%

YTD 09/30/10

G& T Fee POL Proc Margin

11%

12%

24

63%14%

(1) Excludes Discontinued Operations

Guidance for 2010Guidance for 2010Total Year 2010

Low HighNet income $ (41) $ (10)

Guidance for 2010Guidance for 2010

Depreciation and amortization 113 113

Stock‐based compensation 6 6

LOC Fees & Interest 80 79

Taxes and other 2 2

Adjusted EBITDA $ 160 $ 190Adjusted EBITDA $ 160 $ 190

Taxes and other $ (3) $ (3)

LOC Fees & Interest $ (80) $ (79)

Maintenance capital expenditures $ (12) $ (10)

Distributable cash flow $ 62 $ 96

Growth Capital $ 35 $ 35

Key Assumptions for Forecast

Weighted Average Liquids Price ($/gallon) $ 0.80 $ 1.09

Crude ($/Bbl) $ 69.37 $ 94.52

Natural Gas ($/MMBtu) $ 6.00 $ 5.00

Natural Gas Liquids to Gas Ratio 149 9% 245 0%

25

Natural Gas Liquids to Gas Ratio 149.9% 245.0%

XTEX Distribution per Unit $ 0.30

XTXI Dividends per Share $ 0.10 25

AppendixAppendix

26

Reconciliation to Net IncomeReconciliation to Net IncomeReconciliation to Net IncomeReconciliation to Net IncomeNet Income to DCF Reconciliation: Years Ended($ in millions) December 31

2009 2008(Unaudited)( )

Net income (loss) attributable to Crosstex Energy, L.P. $ 104 $ 11 Depreciation, amortization and impairments (1) 132 163 Stock‐based compensation 9 11 Interest expense, net (2) 130 105 L ti i h t f d bt 5Loss on extinguishment of debt 5 ‐Gain on sale of property (184) (51)Taxes and other 8 6

Adjusted EBITDA 204 245 ‐ ‐

Interest (2)(3)(4) (121) (83)Cash taxes and other (5) (3) (3)Maintenance capital expenditures (11) (18)Distributable cash flow $ 68 $ 141

(1) Excludes minority interest share of depreciation and amortization of $290 and $286K for the year ended 2009 and the year ended 2008 respectively. Includes depreciation, amortization and impairments related to discontinued operations of $10.7 and $26.4 million for the year ended 2009 and the year ended 2008 respectively.

(2) Includes interest expense allocated to discontinued operations of $34.9 and $30.0 million for the year ended 2009 and the year ended 2008, respectively.

(3) Excludes $4.3 million of debt issuance cost amortization, and $5.2 million of senior secured note make‐whole and call premium paid‐in‐kind interest resulting from repayment of such notes from the proceeds of asset sales for the year ended 2009

27 27

resulting from repayment of such notes from the proceeds of asset sales, for the year ended 2009.

(4) Excludes noncash interest rate swap mark to market of ($797K) for the year ended 2009, and $22.1 million for the year ended 2008.

(5)Includes Seminole Adjustment of $39 million for the year ended 2008.