Embed Size (px)

Citation preview

-Well-positioned in the Americas Well positioned in the Americas

Mark Mullin CEO Americas

New York City – December 2009

Key messages

o The US market is the largest market in the world and AEGON is a top player

o We have transformed the organization to simplify the business

– Capture synergies

– Economies of scale

– Share best practices

o We are focused in key attractive markets of life and retirement

o We have a strong franchise that is positioned to win

Local knowledge. Global power. 2

Our ambition

“To be a leader in helping customers secure their financial futures”

o Rebalance capital allocation

o Improve growth and returns

…resulting in sustainable profitable growth

o Reduce financial markets risks

o Manage AEGON as an international company

Local knowledge. Global power. 3

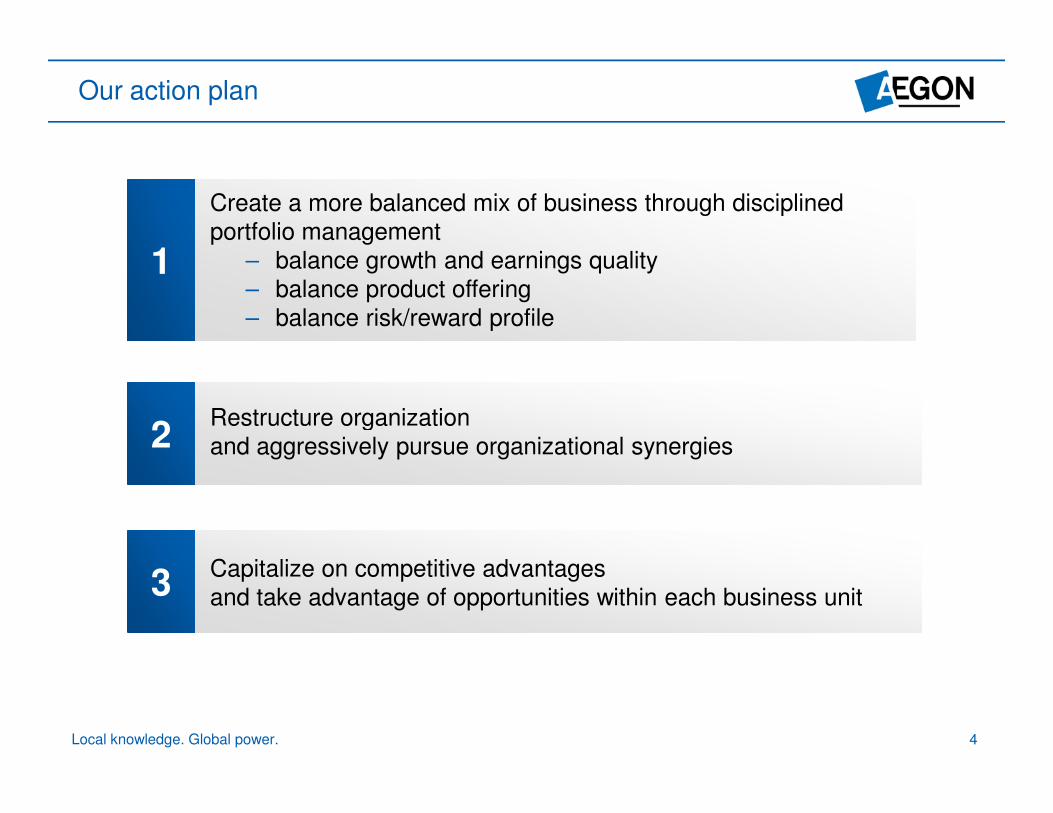

Restructure organization

Our action plan

1

Create a more balanced mix of business through disciplined

portfolio management

– balance growth and earnings quality

– balance product offering

– balance risk/reward profile

Restructure organization

and aggressively pursue organizational synergies 2

3 Capitalize on competitive advantages

and take advantage of opportunities within each business unit

Local knowledge. Global power. 4

Retirement Pensions

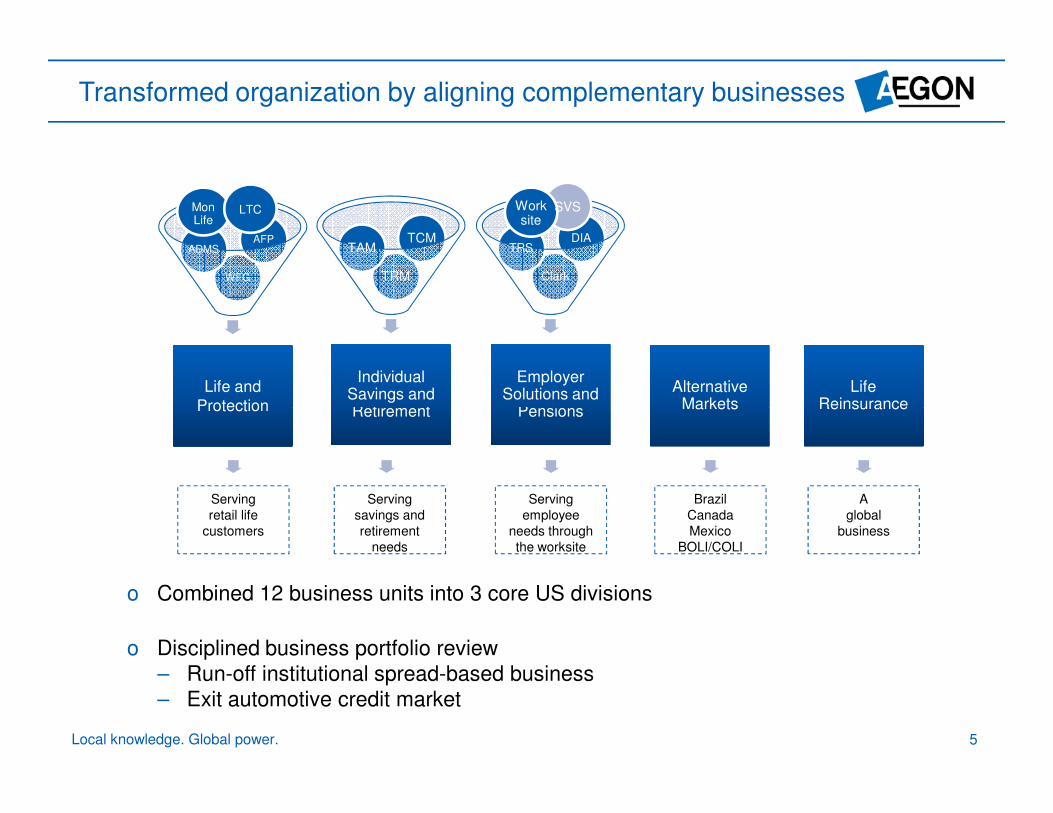

Transformed organization by aligning complementary businesses

Mon Work SVS LTC Life site

AFP TCM DIA ADMS TAM TRS

WFG TRM Clark

Individual Employer Life and Alternative Life Savings and Solutions and

Protection Protection Markets Markets Reinsurance Reinsurance Retirement Pensions

Serving Serving Serving Brazil A

retail life savings and employee Canada global

customers retirement needs through Mexico business

needs the worksite BOLI/COLI

o Combined 12 business units into 3 core US divisions

o Disciplined business portfolio review

– Run-off institutional spread-based business

– Exit automotive credit market

Local knowledge. Global power. 5

Leading in the US life and retirement market

o Largest life insurance and pension market in the world

o Industry fundamentals and demographic attractiveness have both improved

o Our competitive advantages and distribution capabilities position us as a leader in

each business unit

#5 in both term and universal life

#7 in DC providers by assets

#10 in total individual annuity sales

Life

and

Protection

Employer

Solutions and

Pensions

Individual

Savings and

Retirement

Serving the life cycle needs of our customers

*Life and annuity rankings based on LIMRA data. Rankings for ES&P based on independent study and includes Synthetic GICs

Local knowledge. Global power. 6

si nificant economies of o Service excellence and

Capitalizing on competitive advantages and opportunities

Life and Protection

Employer Solutions and

Pensions

Individual Savings and Retirement

o

o

o

Market is underserved

and under-protected

Low cost provider with

significant economies of g

scale

Track record of success

in recruiting and

building effective

distribution

o Growing reliance on

worksite distributed

products

o Service excellence and

award winning

innovative participant

programs

o Total retirement

outsourcing solutions

o Greater awareness of

retirement needs

o One-stop shopping for

protection,

accumulation and

retirement income

solutions

o Continue to attract top

tier talent and increase

penetration of broker

dealer channel

Strong Transamerica brand

Local knowledge. Global power. 7

Q&A

For questions please contact Investor Relations +31 70 344 8305

P.O. Box 85 2501 CB The Hague The Netherlands

Local knowledge. Global power. 8

Appendix – Fulfilling our ambition

Local knowledge. Global power. 9

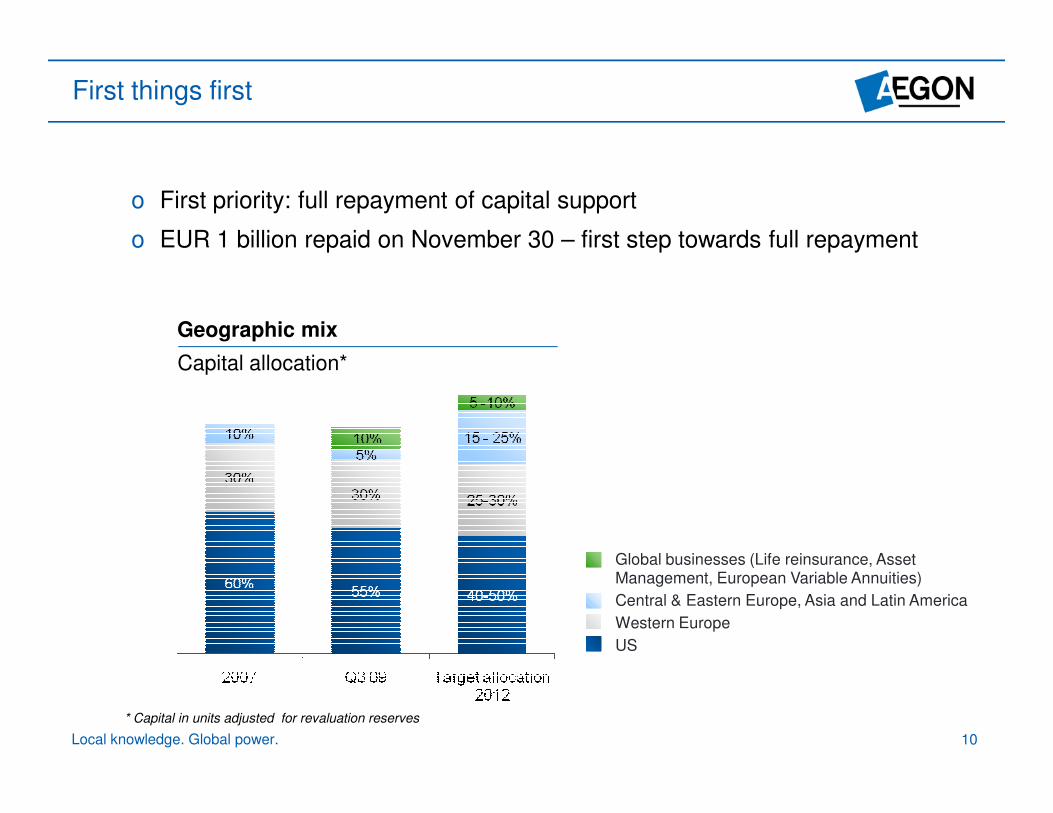

First things first

o First priority: full repayment of capital support

o EUR 1 billion repaid on November 30 – first step towards full repayment

Geographic mix

Capital allocation*

Global businesses (Life reinsurance, Asset Management, European Variable Annuities)

Central & Eastern Europe, Asia and Latin America

Western Europe

US

* Capital in units adjusted for revaluation reserves

Local knowledge. Global power. 10

Im rove rowth and return from existin business

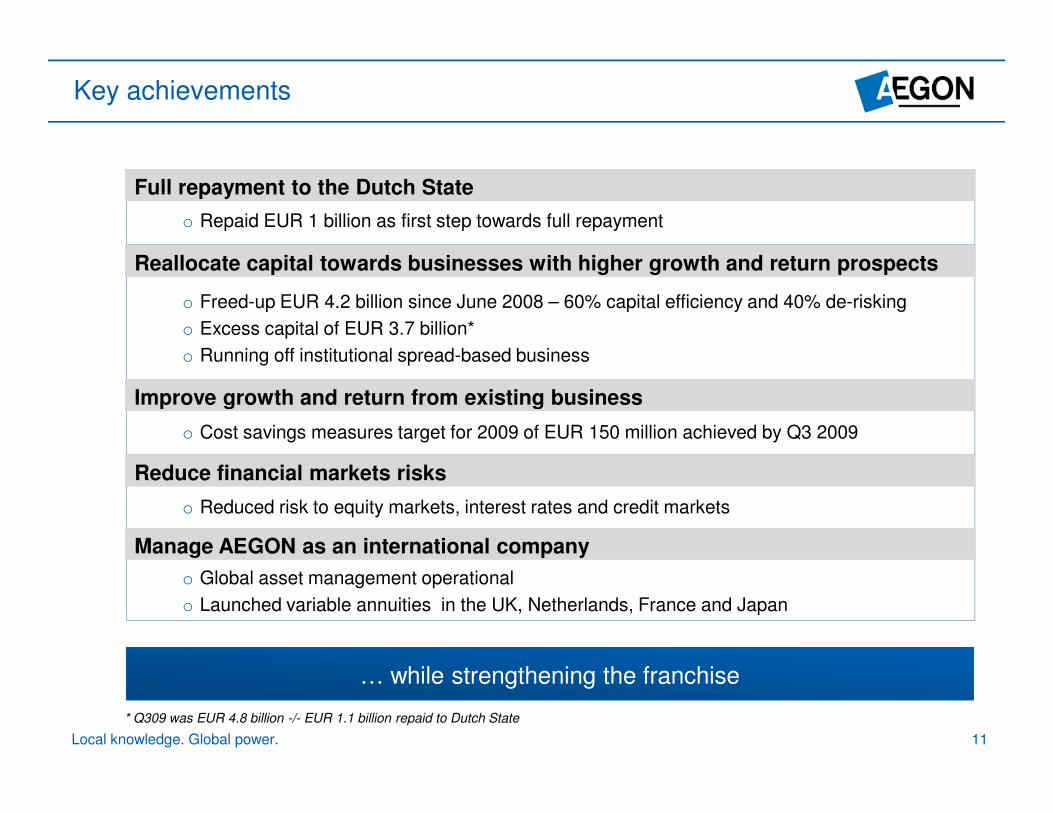

Key achievements

o Freed-up EUR 4.2 billion since June 2008 – 60% capital efficiency and 40% de-risking

o Excess capital of EUR 3.7 billion*

o Running off institutional spread-based business

o Repaid EUR 1 billion as first step towards full repayment

Full repayment to the Dutch State

Improve growth and return from existing business

Reallocate capital towards businesses with higher growth and return prospects

o Cost savings measures target for 2009 of EUR 150 million achieved by Q3 2009

o Global asset management operational

o Launched variable annuities in the UK, Netherlands, France and Japan

… while strengthening the franchise

o Reduced risk to equity markets, interest rates and credit markets

Reduce financial markets risks

Manage AEGON as an international company

p g g

* Q309 was EUR 4.8 billion -/- EUR 1.1 billion repaid to Dutch State

Local knowledge. Global power. 11

illing

am

bitio

nP

en

sio

Fu

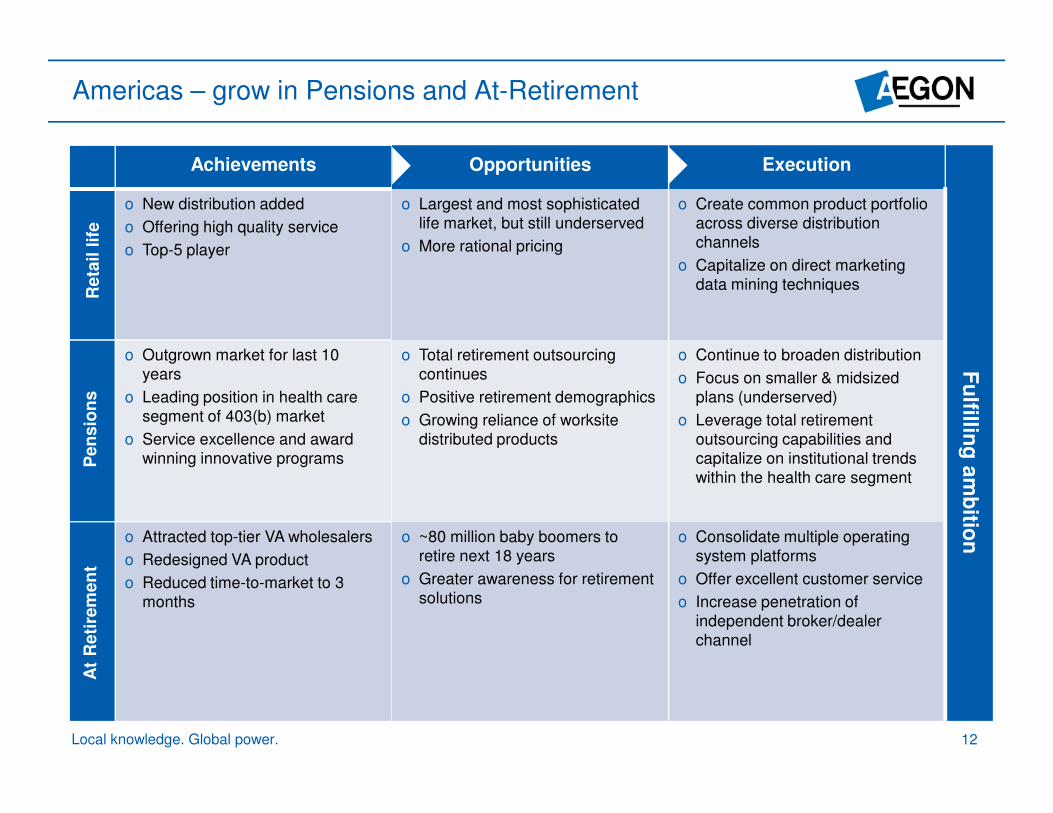

lsAmericas – grow in Pensions and At-Retirement

Achievements

Reta

il l

ife

o New distribution added

o Offering high quality service

o Top-5 player

ns

o Outgrown market for last 10

years

o Leading position in health care

segment of 403(b) market

o Service excellence and award

winning innovative programs

o Attracted top-tier VA wholesalers

o Redesigned VA product

o Reduced time-to-market to 3

months

Pen

sio

nA

t R

eti

rem

en

t

Opportunities Execution

o Largest and most sophisticated

life market, but still underserved

o More rational pricing

o Create common product portfolio

across diverse distribution

channels

o Capitalize on direct marketing

data mining techniques

o Total retirement outsourcing

continues

o Positive retirement demographics

o Continue to broaden distribution

o Focus on smaller & midsized

plans (underserved)

Fu

lf

o Growing reliance of worksite

distributed products

o Leverage total retirement

outsourcing capabilities and

capitalize on institutional trends

within the health care segment

o ~80 million baby boomers to

retire next 18 years

o Greater awareness for retirement

solutions

o Consolidate multiple operating

system platforms

o Offer excellent customer service

o Increase penetration of

independent broker/dealer

channel

filling

am

bitio

n

Local knowledge. Global power. 12

illing

am

bitio

nP

en

sio

o Outstandin roduct line

Fu

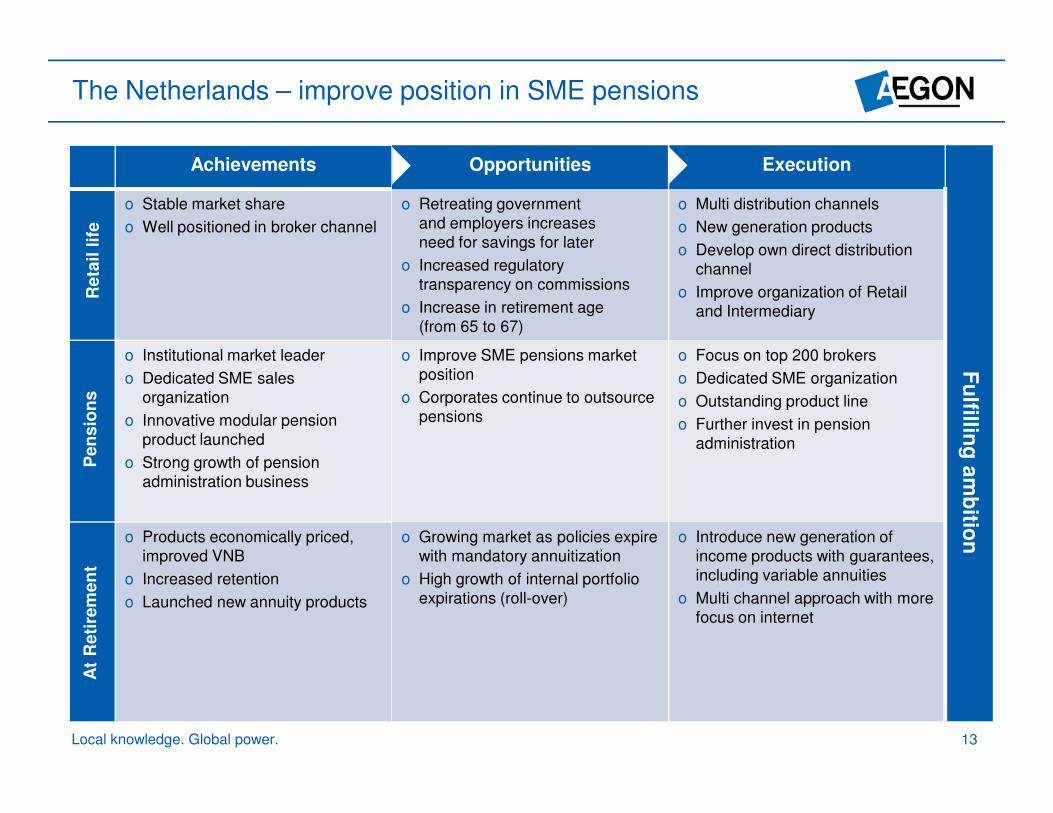

lsThe Netherlands – improve position in SME pensions

Achievements

Reta

il l

ife

o Stable market share

o Well positioned in broker channel

ns

o Institutional market leader

o Dedicated SME sales

organization

o Innovative modular pension

product launched

o Strong growth of pension

administration business

o Products economically priced,

improved VNB

o Increased retention

o Launched new annuity products

Pen

sio

nA

t R

eti

rem

en

t

Opportunities Execution

o Retreating government

and employers increases

need for savings for later

o Increased regulatory

transparency on commissions

o Increase in retirement age

(from 65 to 67)

o Multi distribution channels

o New generation products

o Develop own direct distribution

channel

o Improve organization of Retail

and Intermediary

o Improve SME pensions market

position

o Corporates continue to outsource

o Focus on top 200 brokers

o Dedicated SME organization

o Outstanding product line

Fu

lf

pensions g p

o Further invest in pension

administration

o Growing market as policies expire

with mandatory annuitization

o High growth of internal portfolio

expirations (roll-over)

o Introduce new generation of

income products with guarantees,

including variable annuities

o Multi channel approach with more

focus on internet

filling

am

bitio

n

Local knowledge. Global power. 13

illing

am

bitio

nP

en

sio

Fu

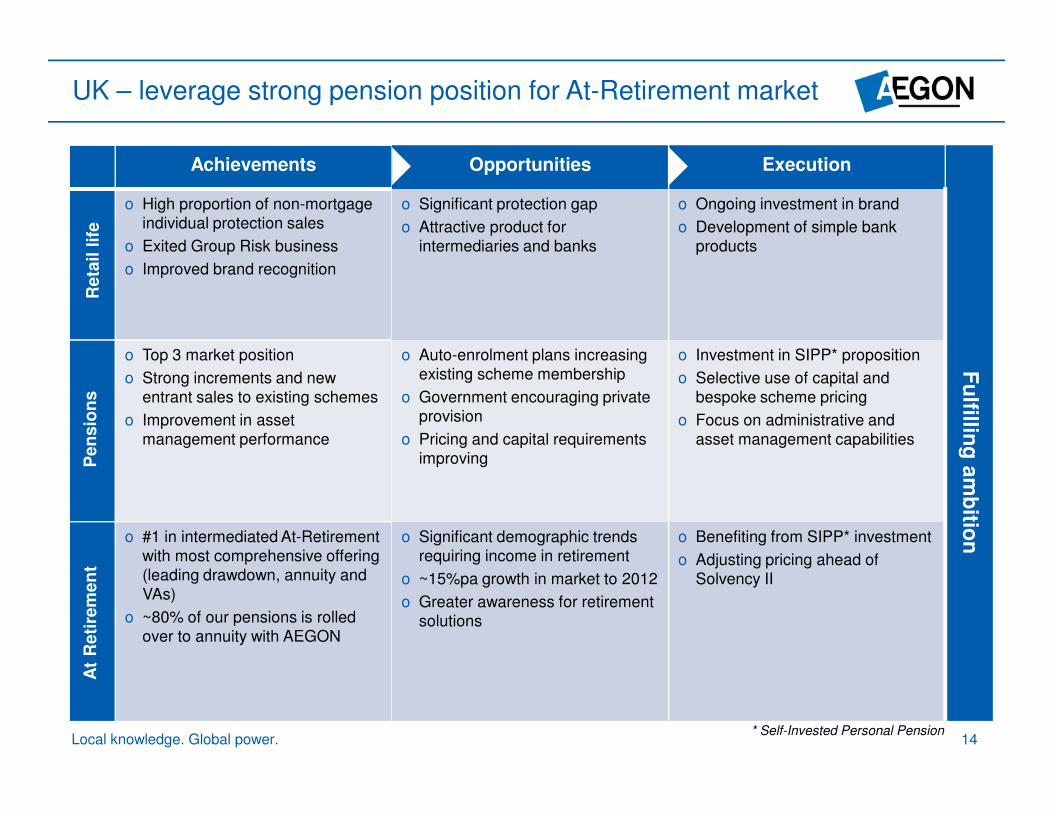

lsUK – leverage strong pension position for At-Retirement market

Achievements

Reta

il l

ife

o High proportion of non-mortgage

individual protection sales

o Exited Group Risk business

o Improved brand recognition

ns

o Top 3 market position

o Strong increments and new

entrant sales to existing schemes

o Improvement in asset

management performance

o #1 in intermediated At-Retirement

with most comprehensive offering

(leading drawdown, annuity and

VAs)

o ~80% of our pensions is rolled

over to annuity with AEGON

Pen

sio

nA

t R

eti

rem

en

t

Opportunities Execution

o Significant protection gap

o Attractive product for

intermediaries and banks

o Ongoing investment in brand

o Development of simple bank

products

o Auto-enrolment plans increasing

existing scheme membership

o Government encouraging private

o Investment in SIPP* proposition

o Selective use of capital and

bespoke scheme pricing

Fu

lf

provision

o Pricing and capital requirements

improving

o Focus on administrative and

asset management capabilities

o Significant demographic trends

requiring income in retirement

o ~15%pa growth in market to 2012

o Greater awareness for retirement

solutions

o Benefiting from SIPP* investment

o Adjusting pricing ahead of

Solvency II

filling

am

bitio

n

* Self-Invested Personal Pension Local knowledge. Global power. 14

illing

am

bitio

nP

en

sio

Fu

lsCentral & Eastern Europe – profitable growth

Achievements

Reta

il

o Top 3 in Poland and Hungary

o Introduced innovative products in

Czech Republic and Slovakia

o Start-ups in Romania and Turkey

ns

o Strong asset management

performance

o High growth in pension fund

members to 2.1 million currently

o Out-performance of asset

management Pen

sio

nA

t R

eti

rem

en

t

Opportunities Execution

o Market ready for new type of life

products

o Roll-out of household insurance

throughout region

o Launching new products,

developed with US expertise

o Leverage on Hungarian

household knowledge – one

administrative platform

o Add new ‘lottery’ members in

Poland

o Favorable demographics

o Develop Pension Advisor channel

(tied)

o Capitalize on banking and broker

Fu

lf

relationships

o Asset management out-

performance

o First retirees from private pension

funds will enter to the market

in 2-3 years

o New product developed

(regulated)

o Direct distribution

filling

am

bitio

n

Local knowledge. Global power. 15

illing

am

bitio

nS

pai

Fu

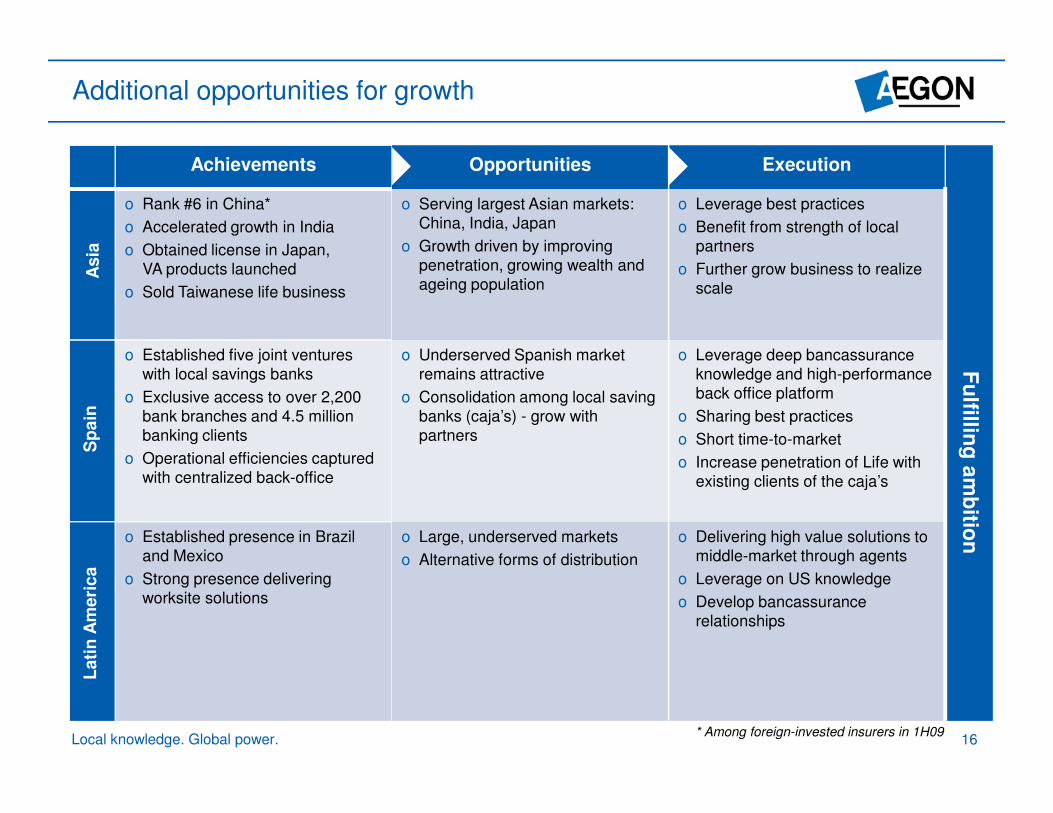

lAdditional opportunities for growth

Achievements

Asia

o Rank #6 in China*

o Accelerated growth in India

o Obtained license in Japan,

VA products launched

o Sold Taiwanese life business

n

o Established five joint ventures

with local savings banks

o Exclusive access to over 2,200

bank branches and 4.5 million

banking clients

o Operational efficiencies captured

with centralized back-office

o Established presence in Brazil

and Mexico

o Strong presence delivering

worksite solutions

Sp

ain

Lati

n A

meri

ca

Opportunities Execution

o Serving largest Asian markets:

China, India, Japan

o Growth driven by improving

penetration, growing wealth and

ageing population

o Leverage best practices

o Benefit from strength of local

partners

o Further grow business to realize

scale

o Underserved Spanish market

remains attractive

o Consolidation among local saving

o Leverage deep bancassurance

knowledge and high-performance

back office platform

Fu

lf

banks (caja’s) - grow with

partners

o Sharing best practices

o Short time-to-market

o Increase penetration of Life with

existing clients of the caja’s

o Large, underserved markets

o Alternative forms of distribution

o Delivering high value solutions to

middle-market through agents

o Leverage on US knowledge

o Develop bancassurance

relationships

filling

am

bitio

n

* Among foreign-invested insurers in 1H09 Local knowledge. Global power. 16

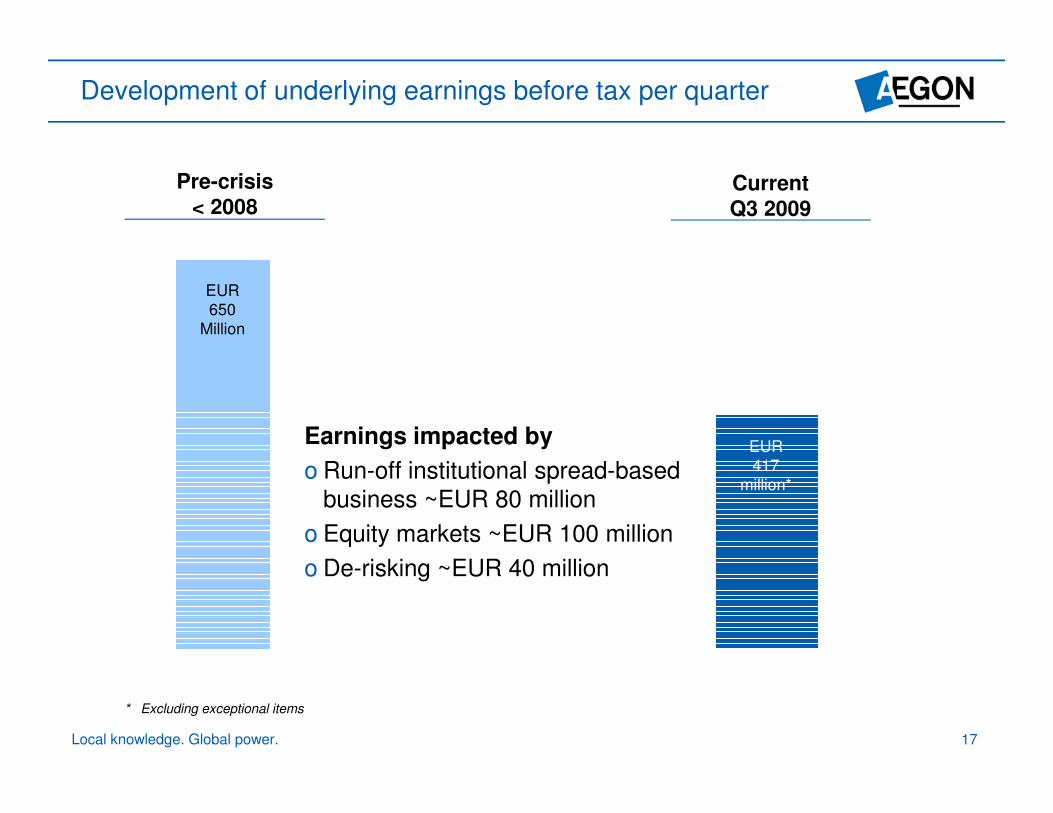

Development of underlying earnings before tax per quarter

Pre-crisis Current < 2008 Q3 2009

EUR

650

Million

Earnings impacted by

o Run-off institutional spread-based

business ~EUR 80 million

o Equity markets ~EUR 100 million

o De-risking ~EUR 40 million

EUR

417

million*

* Excluding exceptional items

Local knowledge. Global power. 17

Mrk

et

imp

act

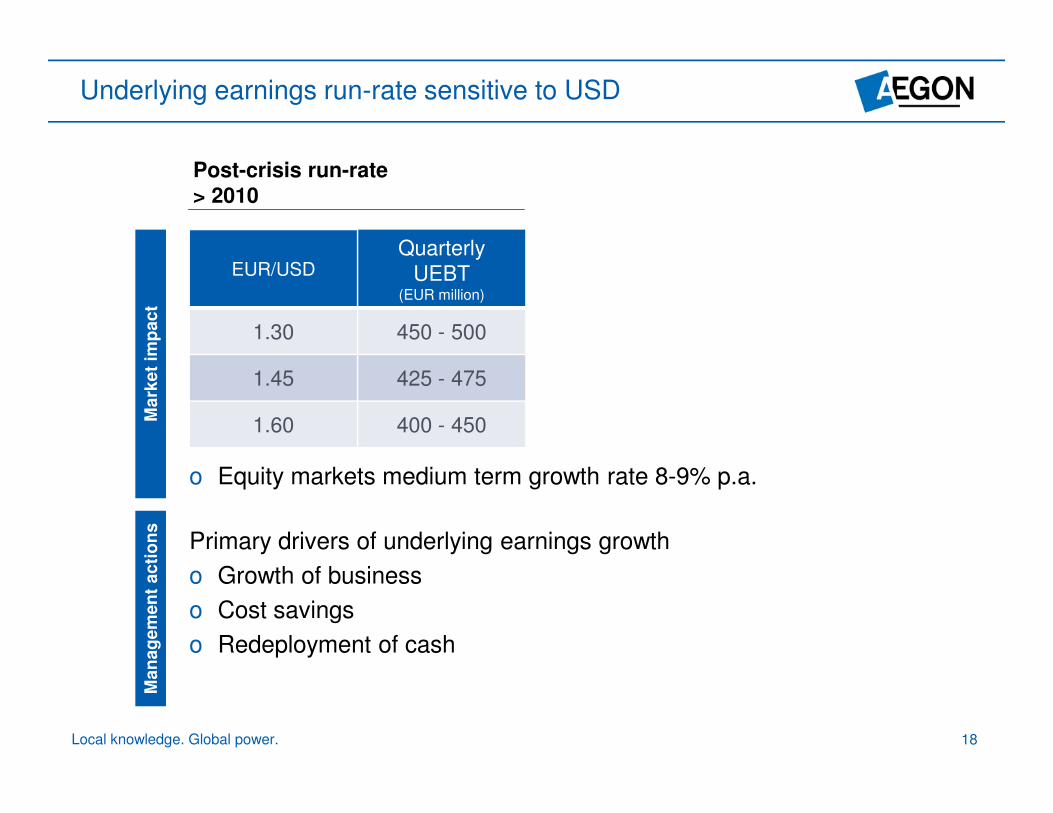

Underlying earnings run-rate sensitive to USD

Post-crisis run-rate

> 2010

EUR/USD Quarterly

UEBT (EUR million)

1.30 450 - 500

1.45 425 - 475

ark

et

imp

act

18 Local knowledge. Global power.

1.60 400 - 450

Primary drivers of underlying earnings growth

o Growth of business

o Cost savings

o Redeployment of cash

MM

an

ag

em

en

t acti

on

s

o Equity markets medium term growth rate 8-9% p.a.

o a e o equ y pos ons comp e e en

Reduced financial markets risks

o Risk transfer through reinsurance

o Macro-hedge related to retail variable annuity portfolio

o Run-off of Institutional spread-based business

o Product redesign (Variable Annuities)

S l f it iti l t d d 2007

Americas

The Netherlands

Local knowledge. Global power. 19

o Reduced risk profile of investment portfolio

o Sale of credit derivatives (tranched credit protection)

o Sale of equity positions completed end 2007

o Interest rate risk almost completely hedged

o 50% of equity exposure embedded in guarantees hedged

o Exit Taiwan – reduced long-term interest sensitivity

Investments

Other countries

– Launched VA in UK NL France Ja an

Manage AEGON as an international company

o Global asset management operational

o Variable Annuities:

– Use product competencies from US and UK to growth markets

– Hedging centralized in the US

– European platform in Dublin

– Launched VA in UK, NL, France, Japan , , p,

o European data center in Edinburgh

Local knowledge. Global power. 20

Appendix - Americas

Local knowledge. Global power. 21

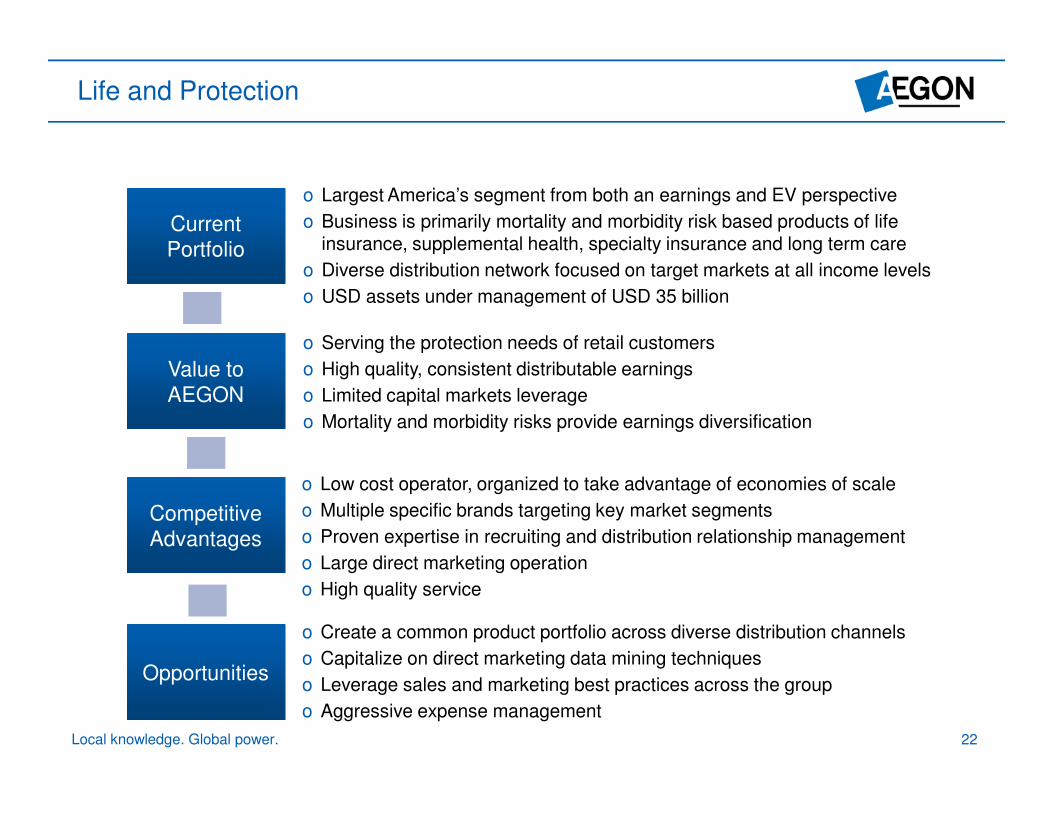

Life and Protection

Current

Portfolio

Value to

AEGON

Opportunities

Competitive

Advantages

o Largest America’s segment from both an earnings and EV perspective

o Business is primarily mortality and morbidity risk based products of life insurance, supplemental health, specialty insurance and long term care

o Diverse distribution network focused on target markets at all income levels

o USD assets under management of USD 35 billion

o Serving the protection needs of retail customers

o High quality, consistent distributable earnings

o Limited capital markets leverage

o Mortality and morbidity risks provide earnings diversification

o Low cost operator, organized to take advantage of economies of scale

o Multiple specific brands targeting key market segments

o Proven expertise in recruiting and distribution relationship management

o Large direct marketing operation

o High quality service

o Create a common product portfolio across diverse distribution channels

o Capitalize on direct marketing data mining techniques

o Leverage sales and marketing best practices across the group

o Aggressive expense management

Local knowledge. Global power. 22

AEGON

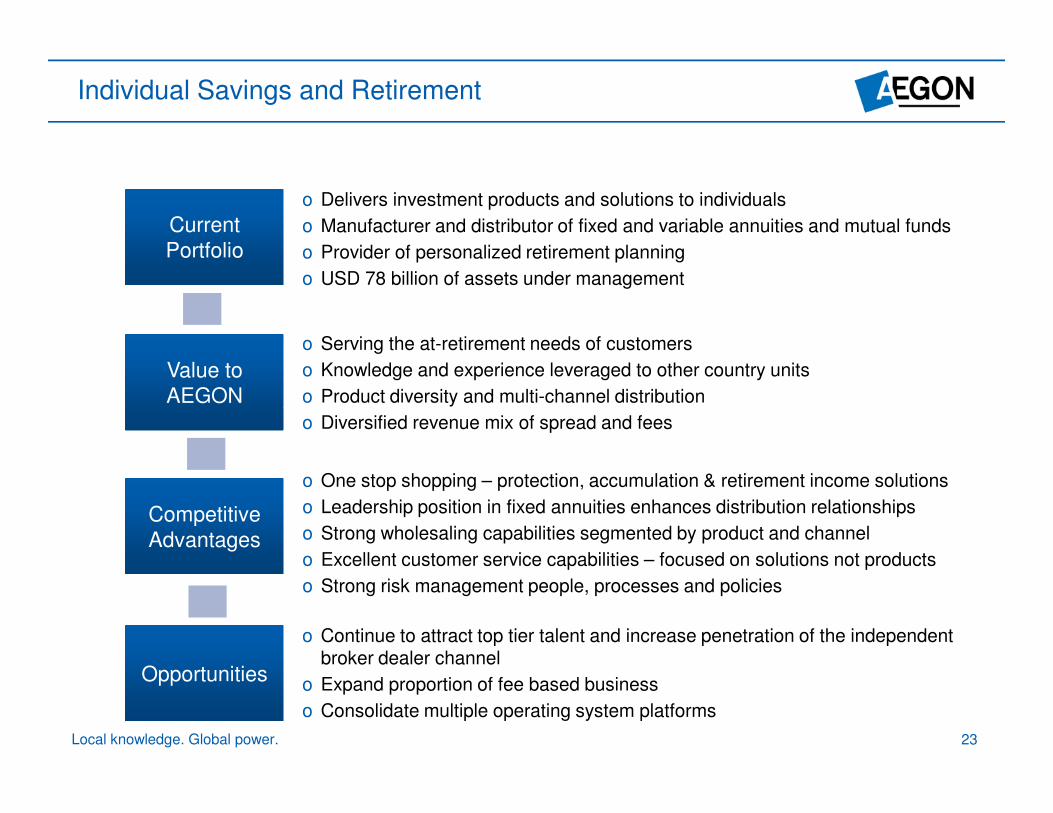

Individual Savings and Retirement

Current

Portfolio

Value to

AEGON

Opportunities

Competitive

Advantages

o Delivers investment products and solutions to individuals

o Manufacturer and distributor of fixed and variable annuities and mutual funds

o Provider of personalized retirement planning

o USD 78 billion of assets under management

o Serving the at-retirement needs of customers

o Knowledge and experience leveraged to other country units

o Product diversity and multi-channel distribution

o Diversified revenue mix of spread and fees

o One stop shopping – protection, accumulation & retirement income solutions

o Leadership position in fixed annuities enhances distribution relationships

o Strong wholesaling capabilities segmented by product and channel

o Excellent customer service capabilities – focused on solutions not products

o Strong risk management people, processes and policies

o Continue to attract top tier talent and increase penetration of the independent broker dealer channel

o Expand proportion of fee based business

o Consolidate multiple operating system platforms

Local knowledge. Global power. 23

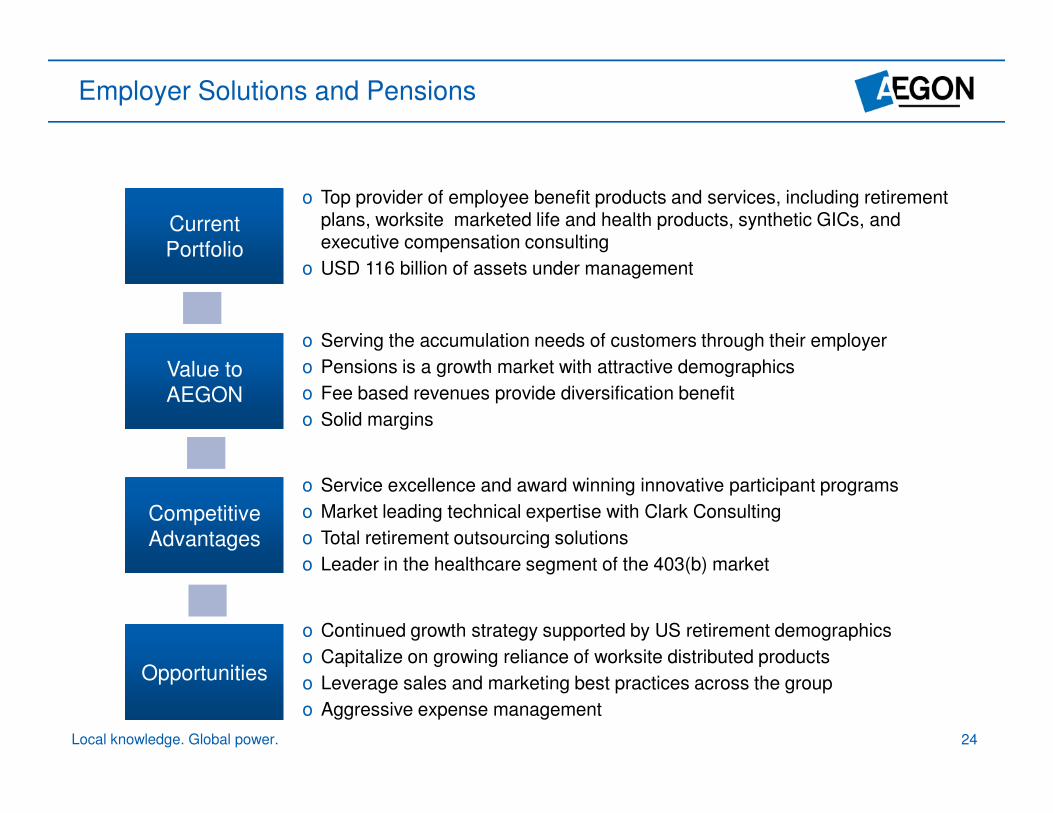

Employer Solutions and Pensions

Current

Portfolio

Value to

AEGON

Opportunities

Competitive

Advantages

o Top provider of employee benefit products and services, including retirement plans, worksite marketed life and health products, synthetic GICs, and executive compensation consulting

o USD 116 billion of assets under management

o Serving the accumulation needs of customers through their employer

o Pensions is a growth market with attractive demographics

o Fee based revenues provide diversification benefit

o Solid margins

o Service excellence and award winning innovative participant programs

o Market leading technical expertise with Clark Consulting

o Total retirement outsourcing solutions

o Leader in the healthcare segment of the 403(b) market

o Continued growth strategy supported by US retirement demographics

o Capitalize on growing reliance of worksite distributed products

o Leverage sales and marketing best practices across the group

o Aggressive expense management

Local knowledge. Global power. 24

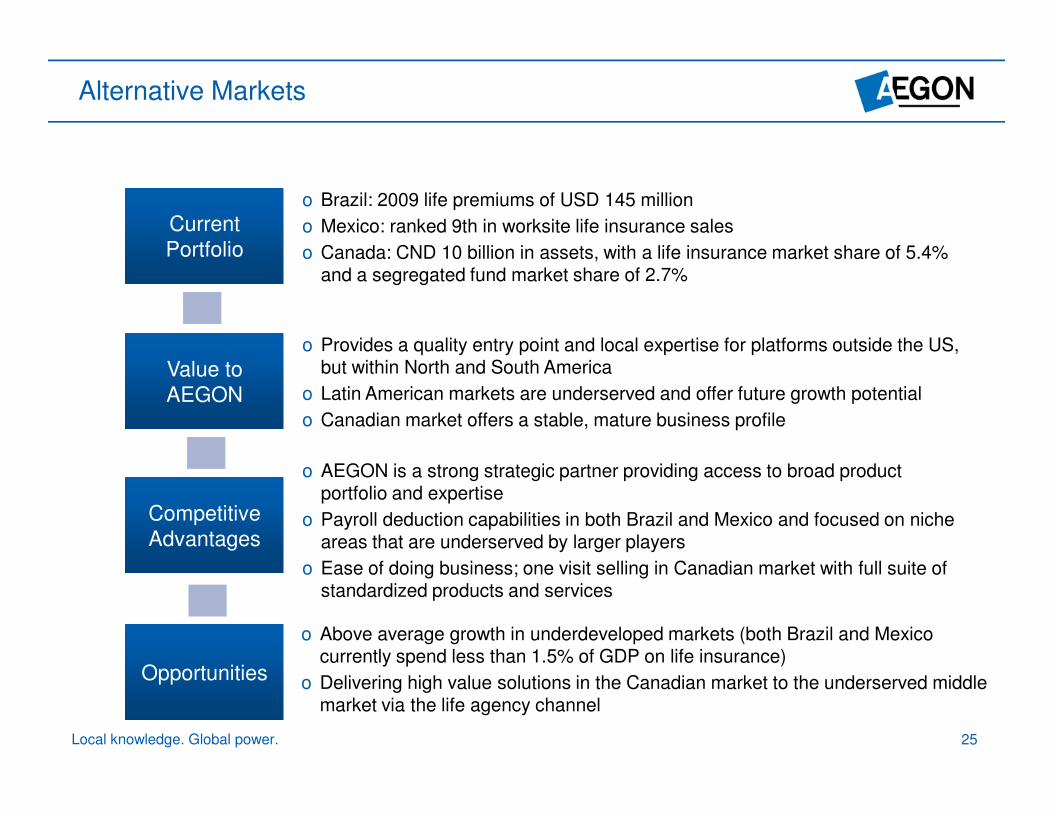

Alternative Markets

Current

Portfolio

Value to

AEGON

Opportunities

Competitive

Advantages

o Brazil: 2009 life premiums of USD 145 million

o Mexico: ranked 9th in worksite life insurance sales

o Canada: CND 10 billion in assets, with a life insurance market share of 5.4% and a segregated fund market share of 2.7%

o Provides a quality entry point and local expertise for platforms outside the US, but within North and South America

o Latin American markets are underserved and offer future growth potential

o Canadian market offers a stable, mature business profile

o AEGON is a strong strategic partner providing access to broad product portfolio and expertise

o Payroll deduction capabilities in both Brazil and Mexico and focused on niche areas that are underserved by larger players

o Ease of doing business; one visit selling in Canadian market with full suite of standardized products and services

o Above average growth in underdeveloped markets (both Brazil and Mexico currently spend less than 1.5% of GDP on life insurance)

o Delivering high value solutions in the Canadian market to the underserved middle market via the life agency channel

Local knowledge. Global power. 25

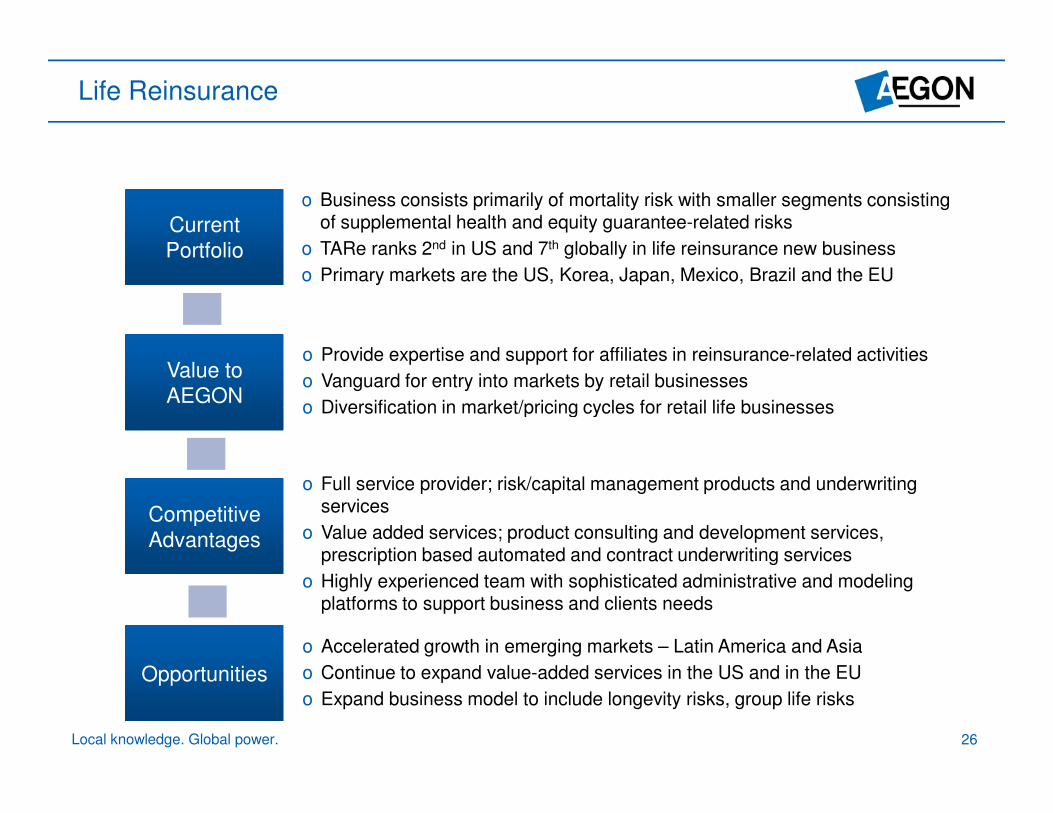

AEGON

Life Reinsurance

Current

Portfolio

Value to

AEGON

Opportunities

Competitive

Advantages

o Business consists primarily of mortality risk with smaller segments consisting of supplemental health and equity guarantee-related risks

o TARe ranks 2nd in US and 7th globally in life reinsurance new business

o Primary markets are the US, Korea, Japan, Mexico, Brazil and the EU

o Provide expertise and support for affiliates in reinsurance-related activities

o Vanguard for entry into markets by retail businesses

o Diversification in market/pricing cycles for retail life businesses o Diversification in market/pricing cycles for retail life businesses

o Full service provider; risk/capital management products and underwriting services

o Value added services; product consulting and development services, prescription based automated and contract underwriting services

o Highly experienced team with sophisticated administrative and modeling platforms to support business and clients needs

o Accelerated growth in emerging markets – Latin America and Asia

o Continue to expand value-added services in the US and in the EU

o Expand business model to include longevity risks, group life risks

Local knowledge. Global power. 26

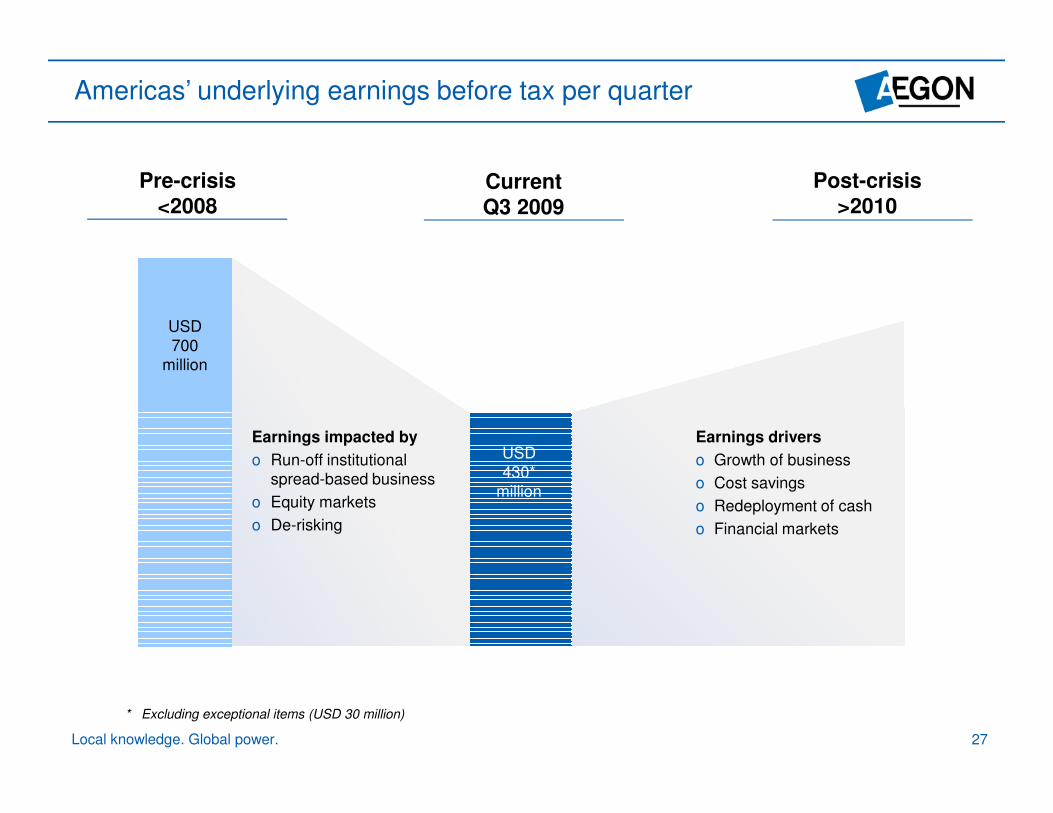

Americas’ underlying earnings before tax per quarter

Pre-crisis Current Post-crisis

<2008 Q3 2009 >2010

USD

700

Earnings impacted by

o Run-off institutional

spread-based business

o Equity markets

o De-risking

USD

430*

million

Earnings drivers

o Growth of business

o Cost savings

o Redeployment of cash

o Financial markets

million

* Excluding exceptional items (USD 30 million)

Local knowledge. Global power. 27

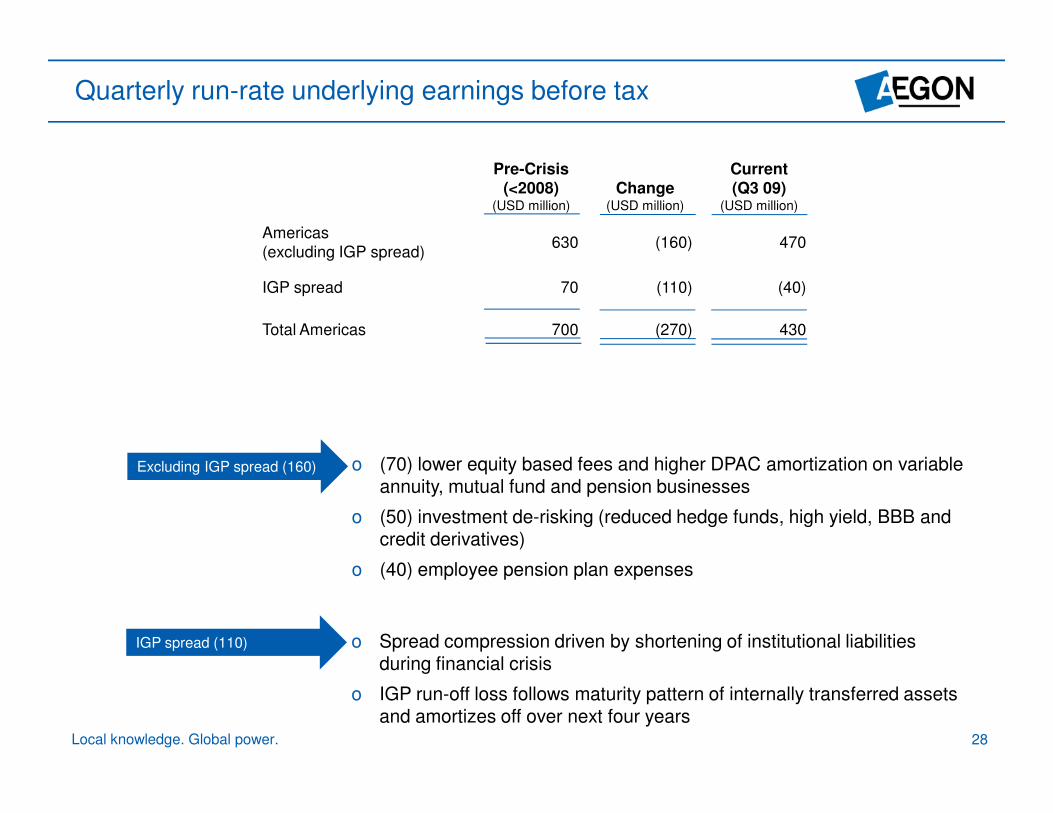

Quarterly run-rate underlying earnings before tax

Pre-Crisis Current (<2008) Change (Q3 09)

(USD million) (USD million) (USD million)

Americas 630 (160) 470

(excluding IGP spread)

IGP spread 70 (110) (40)

Total Americas 700 (270) 430

Excluding IGP spread (160) o (70) lower equity based fees and higher DPAC amortization on variable annuity, mutual fund and pension businesses

o (50) investment de-risking (reduced hedge funds, high yield, BBB and credit derivatives)

o (40) employee pension plan expenses

IGP spread (110) o Spread compression driven by shortening of institutional liabilities during financial crisis

o IGP run-off loss follows maturity pattern of internally transferred assets and amortizes off over next four years

Local knowledge. Global power. 28

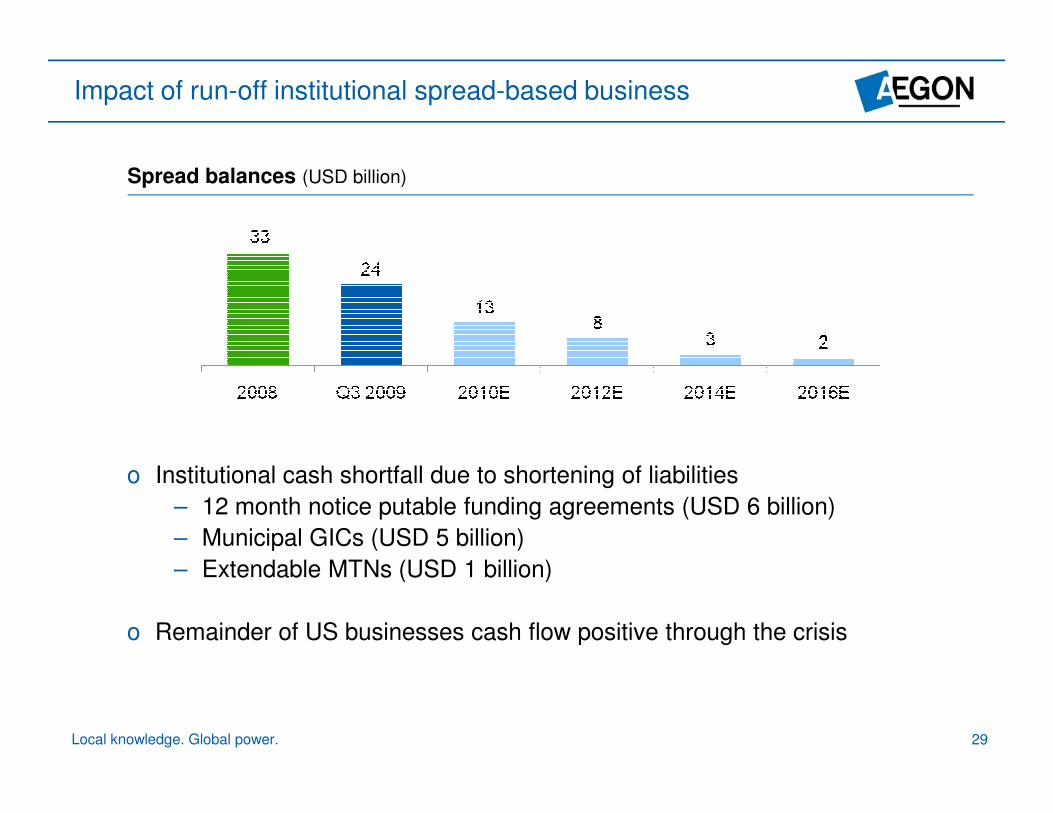

Impact of run-off institutional spread-based business

Spread balances (USD billion)

o Institutional cash shortfall due to shortening of liabilities

– 12 month notice putable funding agreements (USD 6 billion)

– Municipal GICs (USD 5 billion)

– Extendable MTNs (USD 1 billion)

o Remainder of US businesses cash flow positive through the crisis

Local knowledge. Global power. 29

exchan e for cash

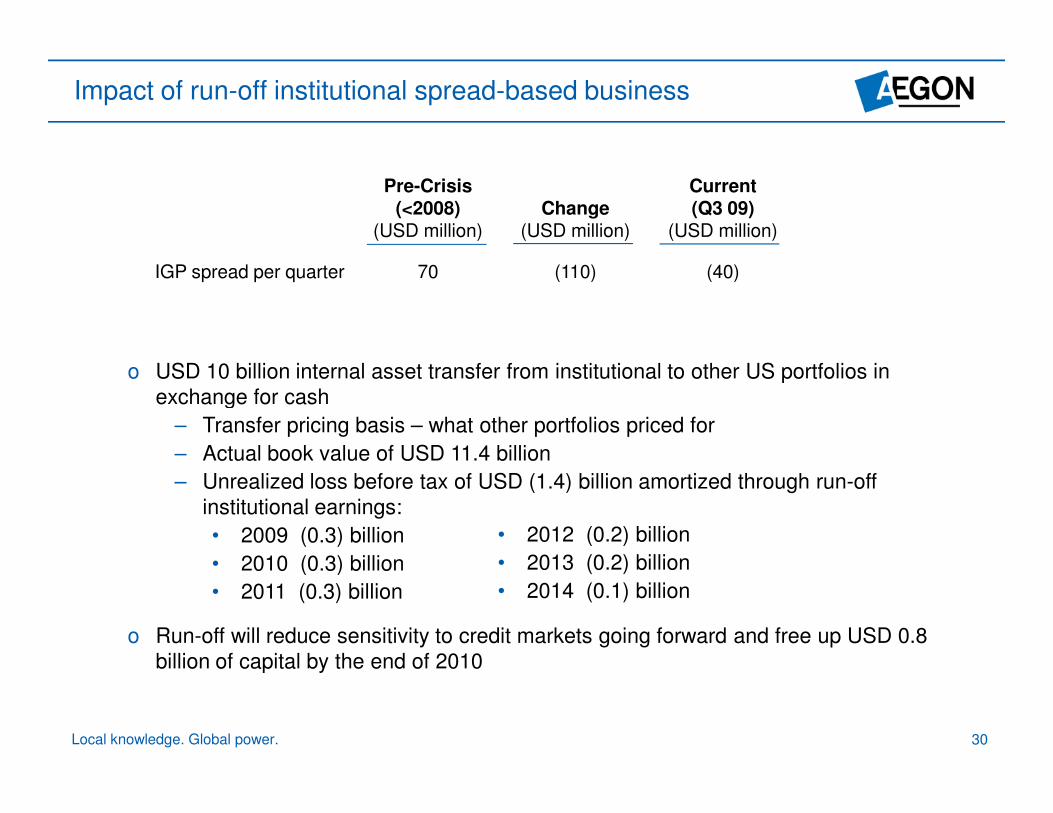

Impact of run-off institutional spread-based business

Pre-Crisis Current (<2008) Change (Q3 09)

(USD million) (USD million) (USD million)

IGP spread per quarter 70 (110) (40)

o USD 10 billion internal asset transfer from institutional to other US portfolios in

exchange for cash g

– Transfer pricing basis – what other portfolios priced for

– Actual book value of USD 11.4 billion

– Unrealized loss before tax of USD (1.4) billion amortized through run-off

institutional earnings:

• 2009 (0.3) billion • 2012 (0.2) billion

• 2010 (0.3) billion • 2013 (0.2) billion

• 2011 (0.3) billion • 2014 (0.1) billion

o Run-off will reduce sensitivity to credit markets going forward and free up USD 0.8

billion of capital by the end of 2010

Local knowledge. Global power. 30

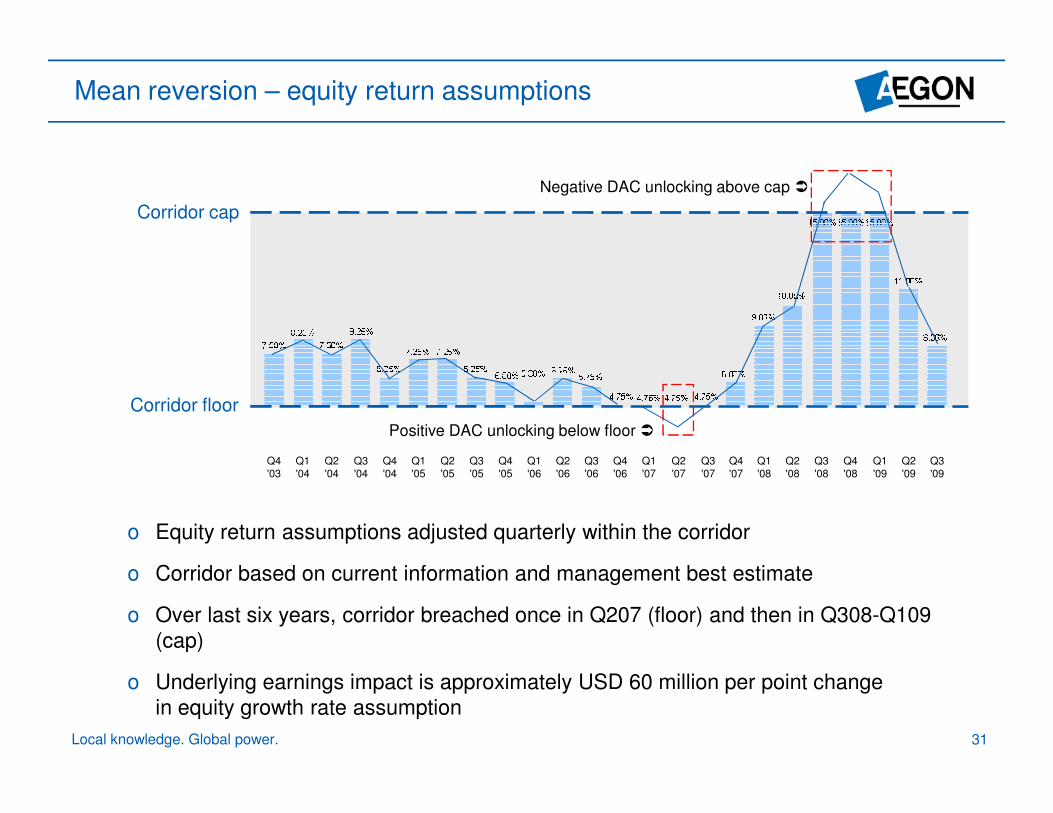

Mean reversion – equity return assumptions

Negative DAC unlocking above cap �

Corridor cap

Corridor floor Corridor floor

Positive DAC unlocking below floor �

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 '03 '04 '04 '04 '04 '05 '05 '05 '05 '06 '06 '06 '06 '07 '07 '07 '07 '08 '08 '08 '08 '09 '09 '09

o Equity return assumptions adjusted quarterly within the corridor

o Corridor based on current information and management best estimate

o Over last six years, corridor breached once in Q207 (floor) and then in Q308-Q109

(cap)

o Underlying earnings impact is approximately USD 60 million per point change

in equity growth rate assumption

Local knowledge. Global power. 31

–

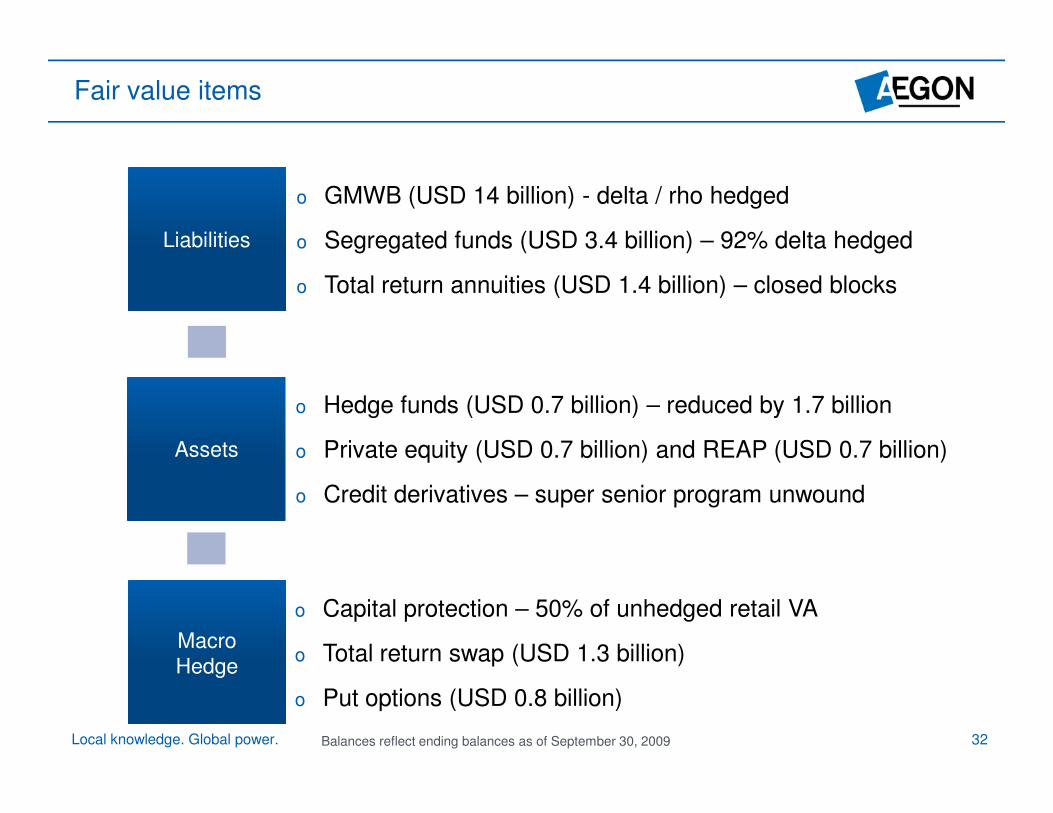

Fair value items

Liabilities

Assets

Macro

Hedge

Local knowledge. Global power.

o GMWB (USD 14 billion) - delta / rho hedged

o Segregated funds (USD 3.4 billion) – 92% delta hedged

o Total return annuities (USD 1.4 billion) – closed blocks

o Hedge funds (USD 0.7 billion) – reduced by 1.7 billion reduced by 1.7 billion o Hedge funds (USD 0.7 billion)

o Private equity (USD 0.7 billion) and REAP (USD 0.7 billion)

o Credit derivatives – super senior program unwound

o Capital protection – 50% of unhedged retail VA

o Total return swap (USD 1.3 billion)

o Put options (USD 0.8 billion)

Balances reflect ending balances as of September 30, 2009 32

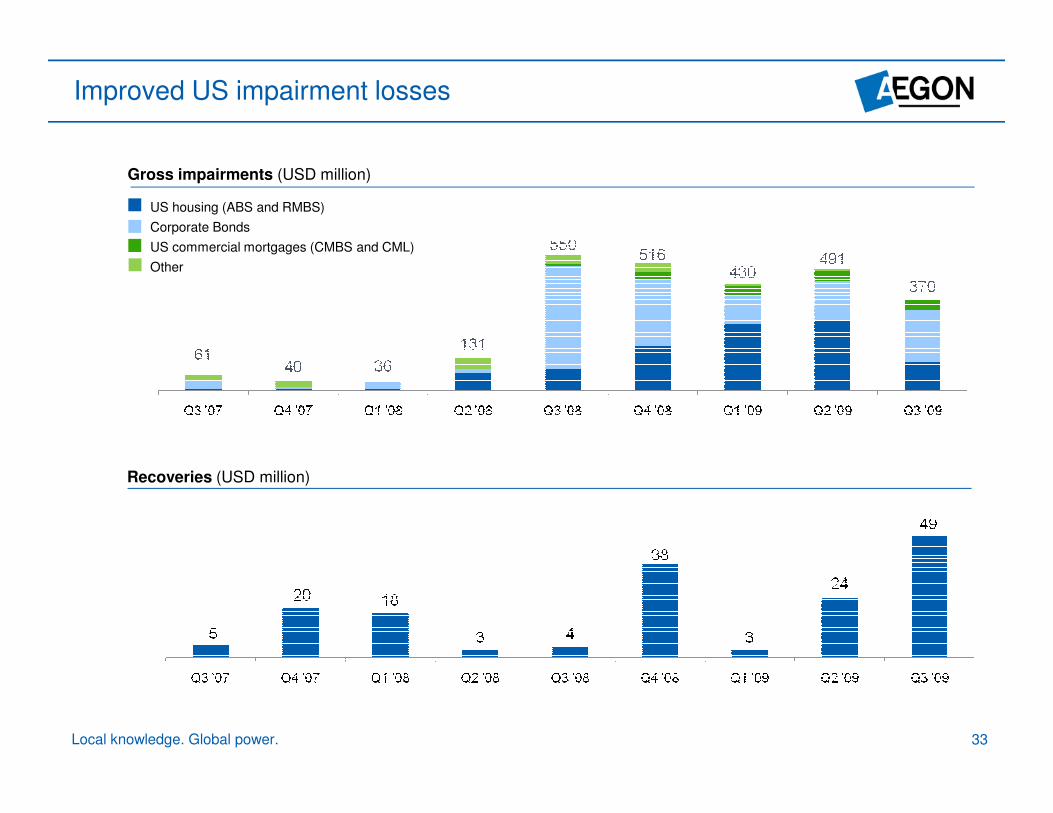

Improved US impairment losses

Gross impairments (USD million)

US housing (ABS and RMBS)

Corporate Bonds

US commercial mortgages (CMBS and CML)

Other

Recoveries (USD million)

Local knowledge. Global power. 33

o yn e c so Variable life insurance

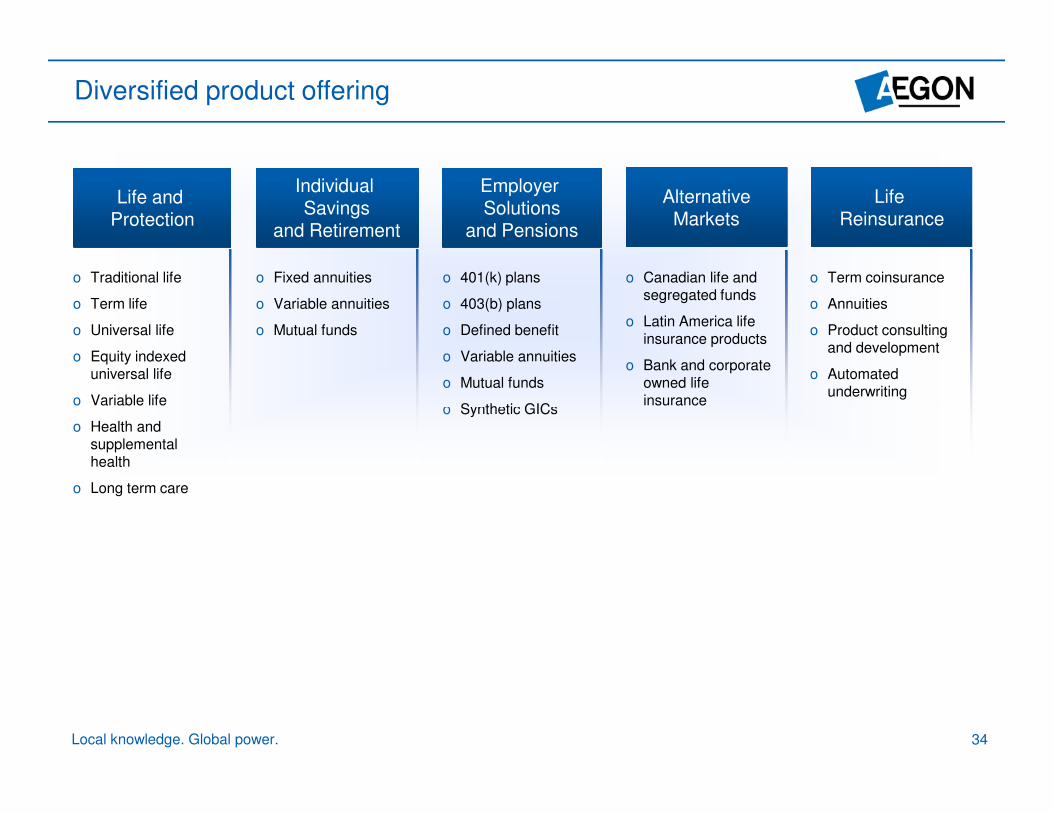

Diversified product offering

Life and Protection

Individual Savings

and Retirement

Employer Solutions

and Pensions

Alternative Markets

Life Reinsurance

o Traditional life

o Term life

o Universal life

o Equity indexed universal life

o Variable life

o Fixed annuities

o Variable annuities

o Mutual funds

o 401(k) plans

o 403(b) plans

o Defined benefit

o Variable annuities

o Mutual funds

S th ti GIC

o Canadian life and segregated funds

o Latin America life insurance products

o Bank and corporate owned life insurance

o Term coinsurance

o Annuities

o Product consulting and development

o Automated underwriting

Local knowledge. Global power. 34

o Health and supplemental health

o Long term care

o Synthetic GICs

o ome serv ceartners o Worksite ecialists

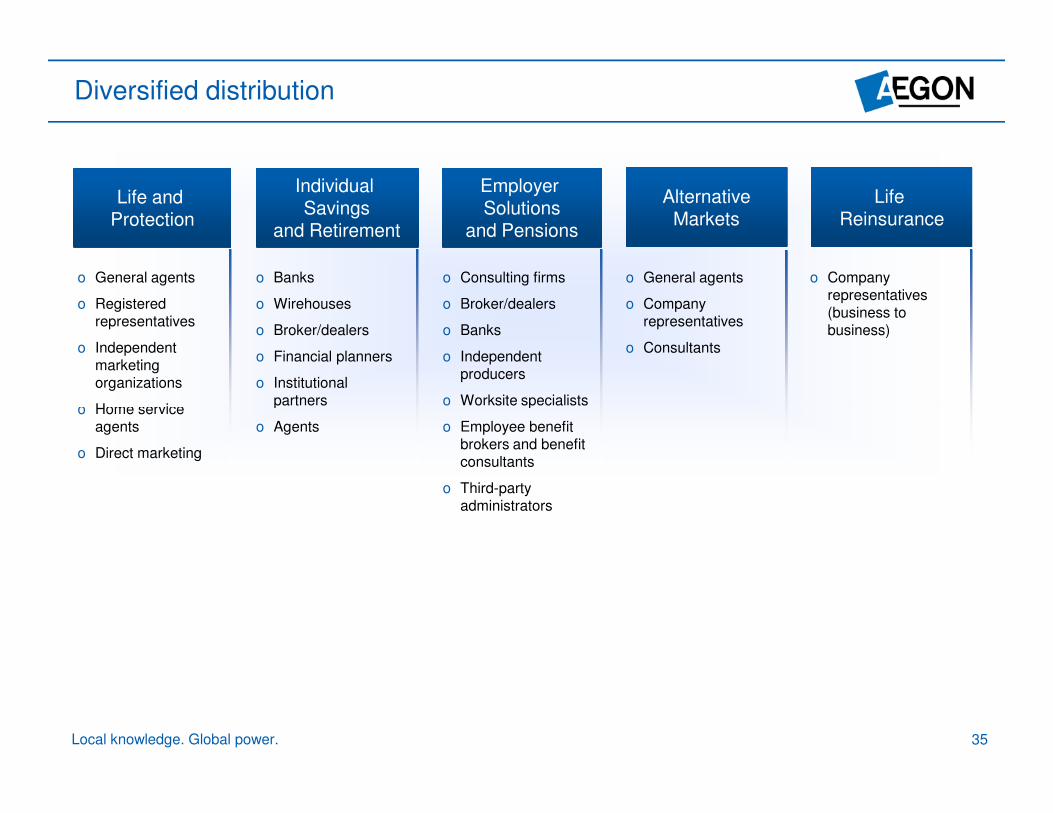

Diversified distribution

Life and Protection

Individual Savings

and Retirement

Employer Solutions

and Pensions

Alternative Markets

Life Reinsurance

o General agents

o Registered representatives

o Independent marketing organizations

H i

o Banks

o Wirehouses

o Broker/dealers

o Financial planners

o Institutional partners

o Consulting firms

o Broker/dealers

o Banks

o Independent producers

o Worksite specialists

o General agents

o Company representatives

o Consultants

o Company representatives (business to business)

Local knowledge. Global power. 35

o Home service agents

o Direct marketing

p

o Agents

sp

o Employee benefit brokers and benefit consultants

o Third-party administrators

Appendix – Q3 2009 results

Local knowledge. Global power. 36

Highlights

o Return to profit

o Repayment of EUR 1 billion core capital to Dutch State (November 30, 2009)

o Further strengthened capital position

o Revaluation reserves improve by EUR 3.3 billion

o Profitable sales and net deposits, evidence of strong franchise

o Continued execution of strategy

Local knowledge. Global power. 37

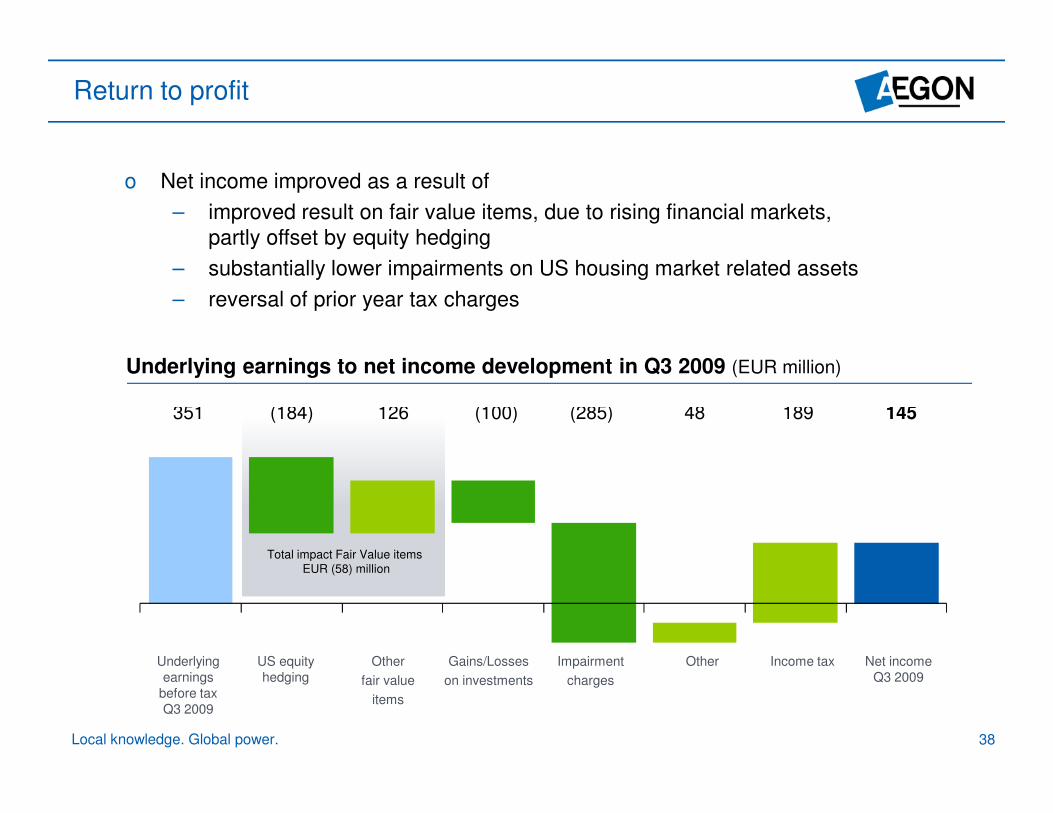

351 (184) 126 (100) (285) 48 189 145

Return to profit

o Net income improved as a result of

– improved result on fair value items, due to rising financial markets,

partly offset by equity hedging

– substantially lower impairments on US housing market related assets

– reversal of prior year tax charges

Underlying earnings to net income development in Q3 2009 (EUR million)

(184) 126

Total impact Fair Value items

EUR (58) million

351 (100) (285) 48 189 145

Underlying US equity Other Gains/Losses Impairment Other Income tax Net income

earnings hedging fair value on investments charges Q3 2009

before tax items

Q3 2009

Local knowledge. Global power. 38

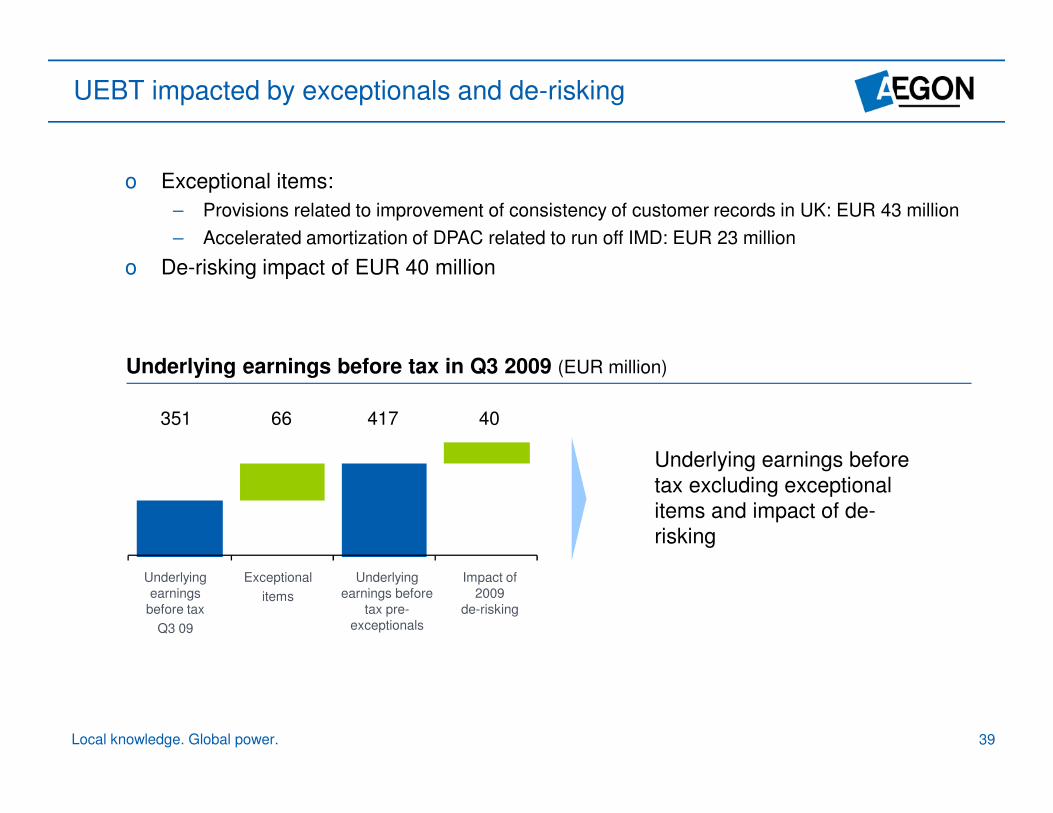

UEBT impacted by exceptionals and de-risking

o Exceptional items:

– Provisions related to improvement of consistency of customer records in UK: EUR 43 million

– Accelerated amortization of DPAC related to run off IMD: EUR 23 million

o De-risking impact of EUR 40 million

Underlying earnings before tax in Q3 2009 (EUR million)

351 66 417 40

Underlying earnings before

tax excluding exceptional

items and impact of de-

risking

Underlying

earnings

before tax

Q3 09

Exceptional

items

Underlying

earnings before

tax pre

exceptionals

Impact of

2009

de-risking

Local knowledge. Global power. 39

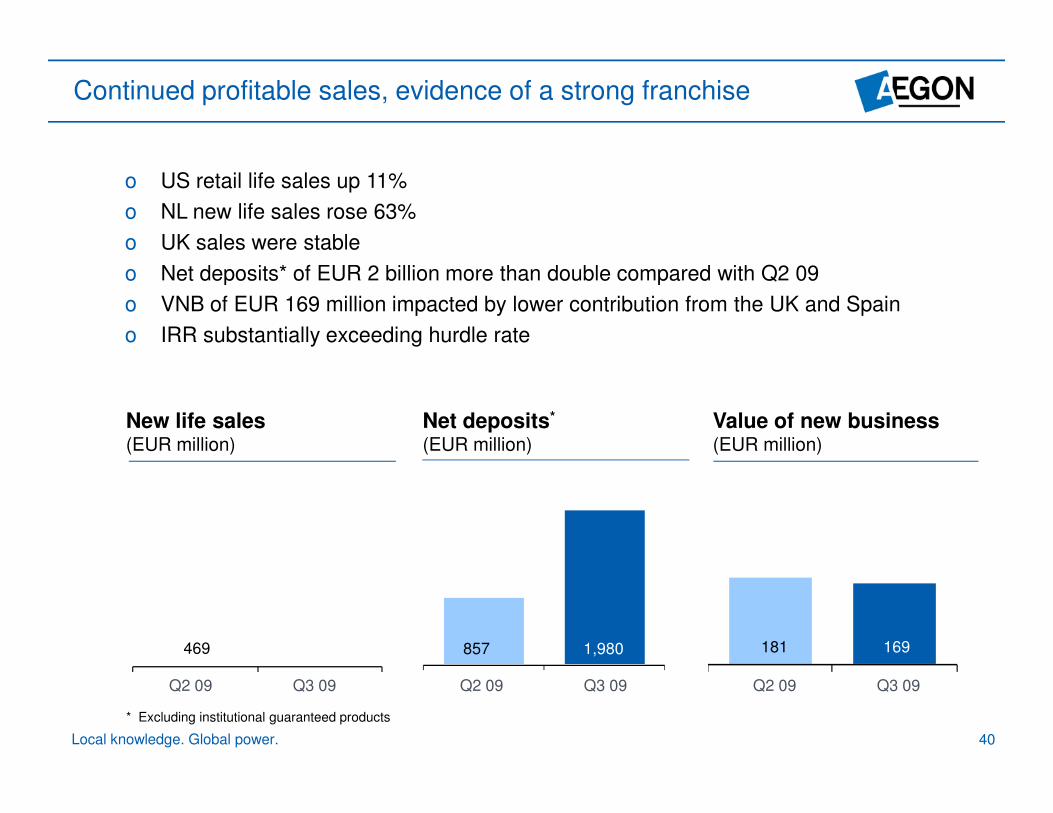

Continued profitable sales, evidence of a strong franchise

o US retail life sales up 11%

o NL new life sales rose 63%

o UK sales were stable

o Net deposits* of EUR 2 billion more than double compared with Q2 09

o VNB of EUR 169 million impacted by lower contribution from the UK and Spain

o IRR substantially exceeding hurdle rate

New life sales Net deposits* Value of new business (EUR million) (EUR million) (EUR million)

469

Local knowledge. Global power.

* Excluding institutional guaranteed products

Q2 09 Q3 09 Q2 09 Q3 09 Q2 09 Q3 09

40

857 1,980 181 169

-400

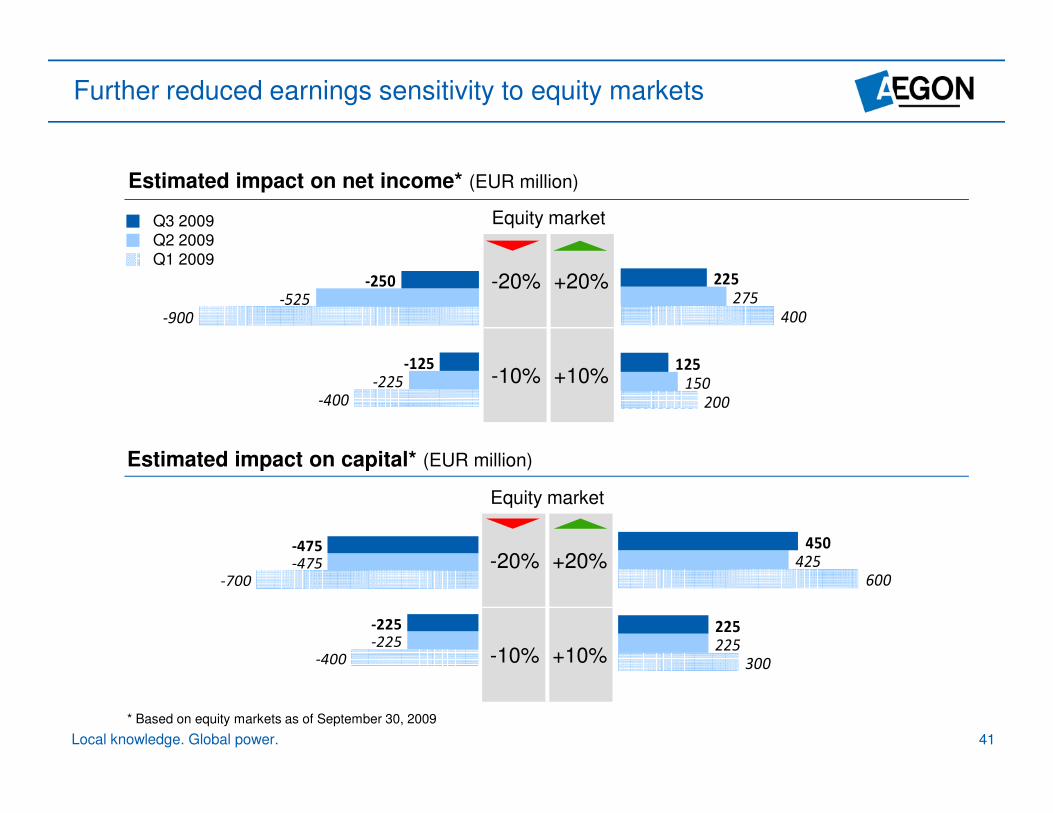

Further reduced earnings sensitivity to equity markets

Estimated impact on net income* (EUR million)

Q3 2009 Equity market Q2 2009

Q1 2009

-250 -20% 225 +20% 275 -525

400 -900

-125 125 -10% +10% -225 150

-400 200 200

Estimated impact on capital* (EUR million)

Equity market

450 -475

+20% 425 -475 -20% 600 -700

-225 225

-225 225 +10% -400 -10% 300

* Based on equity markets as of September 30, 2009

Local knowledge. Global power. 41

Q2 ital

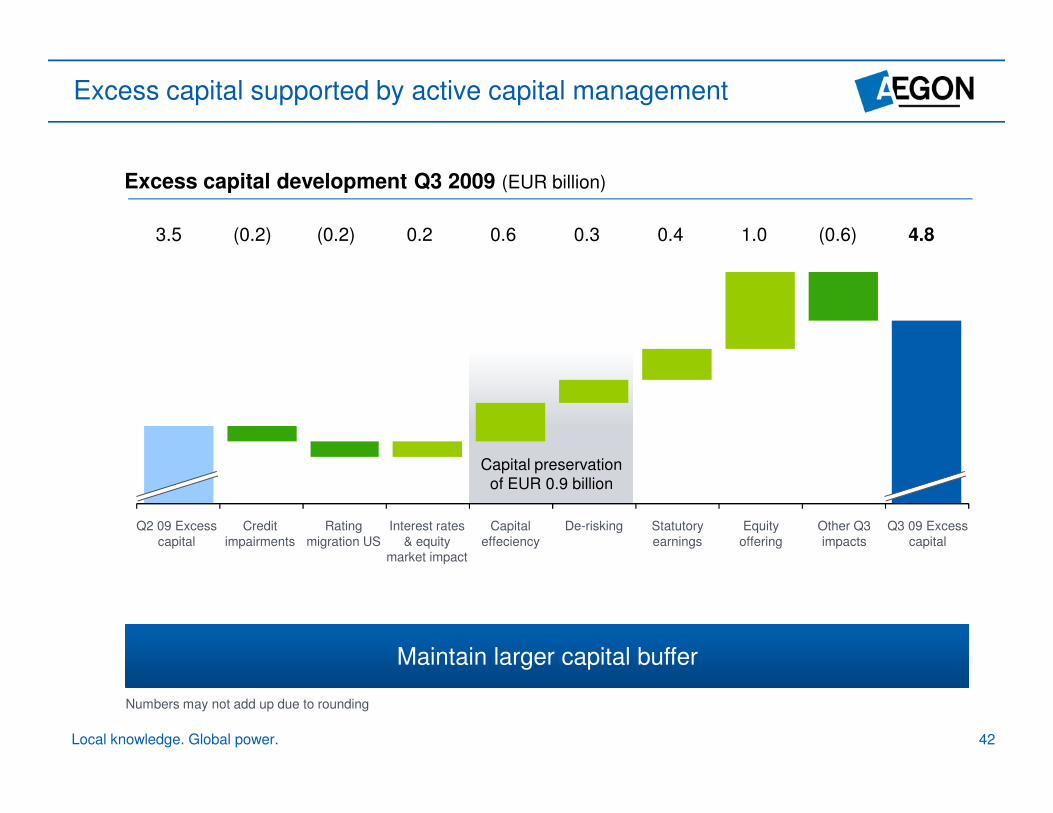

Excess capital supported by active capital management

Excess capital development Q3 2009 (EUR billion)

3.5 (0.2) (0.2) 0.2 0.6 0.3 0.4 1.0 (0.6) 4.8

Capital preservation

of EUR 0.9 billion

Q2 09 Excess Credit Rating Interest rates Capital De-risking Statutory Equity Other Q3 Q3 09 Excess

capital impairments migration US & equity effeciency earnings offering impacts capital market impact

Maintain larger capital buffer

Numbers may not add up due to rounding

Local knowledge. Global power. 42

. o e-r s ng

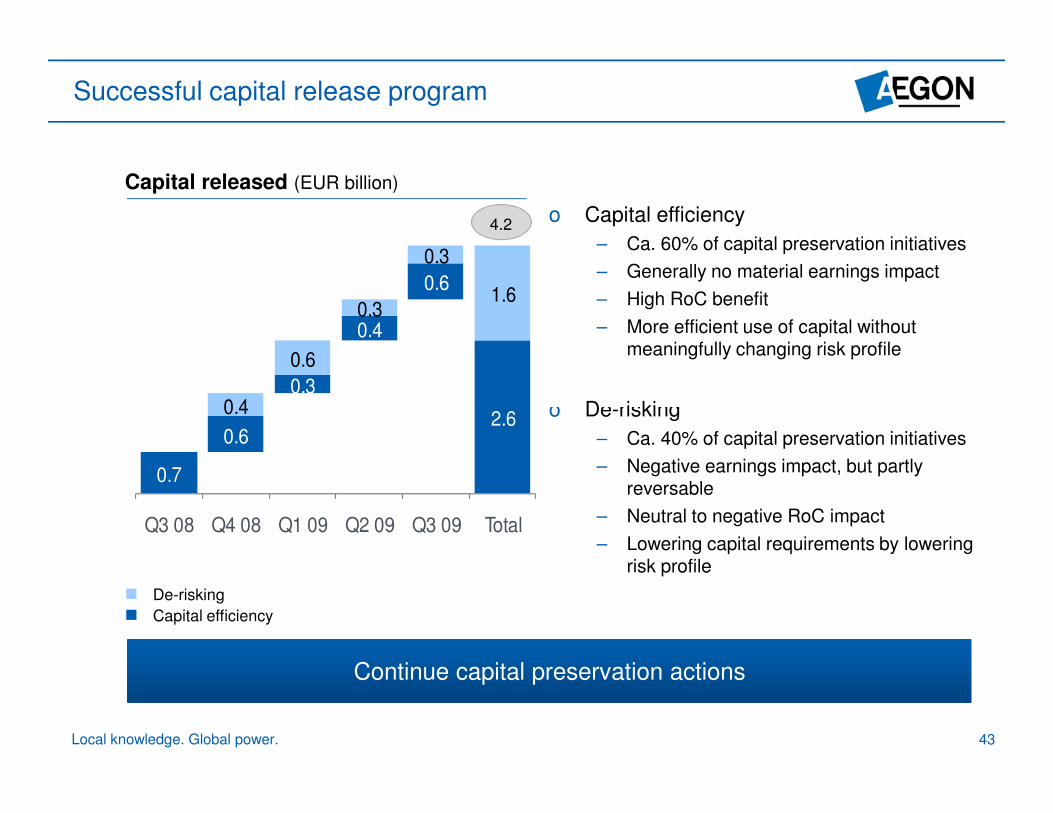

Successful capital release program

Capital released (EUR billion)

0.3

0.4

0.6

0 4

0.6

0.3

0.3

1.6

4.2 o Capital efficiency

– Ca. 60% of capital preservation initiatives

– Generally no material earnings impact

– High RoC benefit

– More efficient use of capital without meaningfully changing risk profile

D i ki

� De-risking

� Capital efficiency

0.7

0.6 2.6

0.4

Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Total

o De-risking

– Ca. 40% of capital preservation initiatives

– Negative earnings impact, but partly reversable

– Neutral to negative RoC impact

– Lowering capital requirements by lowering risk profile

Continue capital preservation actions

Local knowledge. Global power. 43

. . . . . . . . .

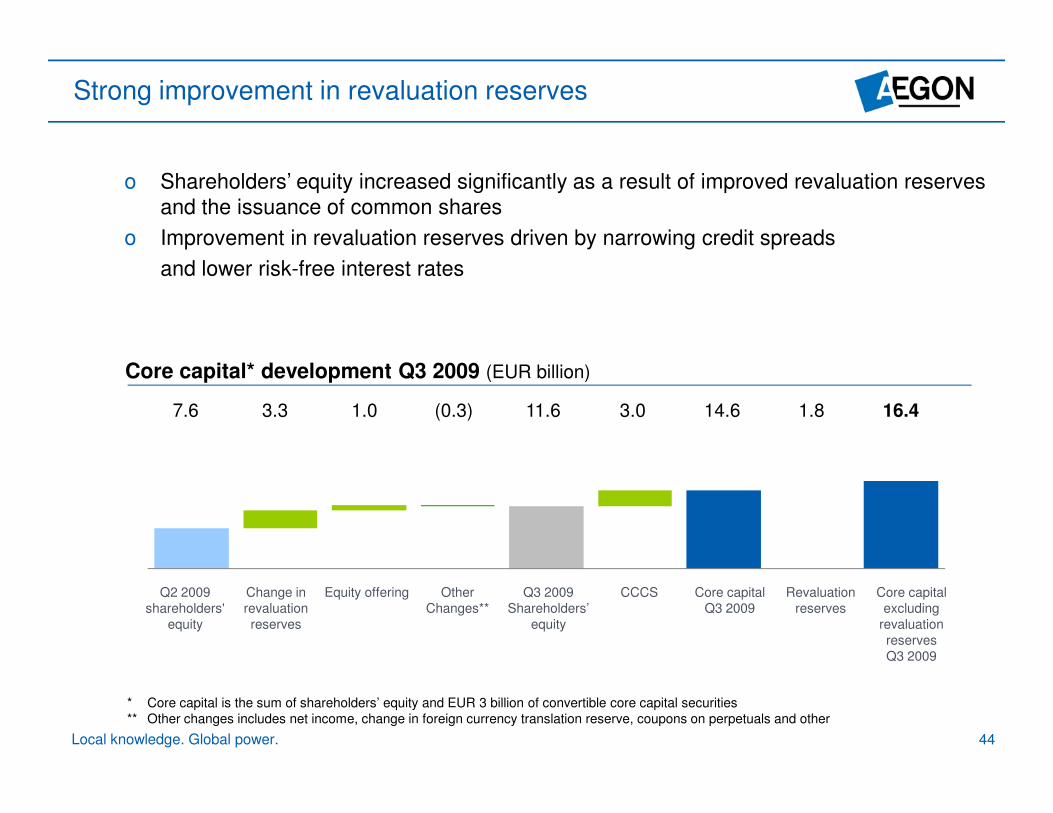

Strong improvement in revaluation reserves

o Shareholders’ equity increased significantly as a result of improved revaluation reserves

and the issuance of common shares

o Improvement in revaluation reserves driven by narrowing credit spreads

and lower risk-free interest rates

Core capital* development Q3 2009 (EUR billion)

7 6 7.6 3 3 3.3 1.0 1 0 (0 3) (0.3) 11.6 11 6 3.0 3 0 14.6 14 6 1 8 1.8 16 4 16.4

Q2 2009 Change in Equity offering Other Q3 2009 CCCS Core capital Revaluation Core capital

shareholders' revaluation Changes** Shareholders’ Q3 2009 reserves excluding

equity reserves equity revaluation

reserves

Q3 2009

* Core capital is the sum of shareholders’ equity and EUR 3 billion of convertible core capital securities

** Other changes includes net income, change in foreign currency translation reserve, coupons on perpetuals and other

Local knowledge. Global power. 44

Disclaimer

Forward-looking statements

The statements contained in this presentation that are not historical facts are forward-looking statements as defined in the US Private Securities Litigation Reform

Act of 1995. The following are words that identify such forward-looking statements: aim, believe, estimate, target, intend, may, expect, anticipate, predict, project,

counting on, plan, continue, want, forecast, goal, should, would, is confident, will, and similar expressions as they relate to our company. These statements are

not guarantees of future performance and involve risks, uncertainties and assumptions that are difficult to predict. We undertake no obligation to publicly update

or revise any forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which merely reflect company

expectations at the time of writing. Actual results may differ materially from expectations conveyed in forward-looking statements due to changes caused by

various risks and uncertainties. Such risks and uncertainties include but are not limited to the following:

o Changes in general economic conditions, particularly in the United States, the Netherlands and the United Kingdom;

o Changes in the performance of financial markets, including emerging markets, such as with regard to:

- The frequency and severity of defaults by issuers in our fixed income investment portfolios; and

- The effects of corporate bankruptcies and/or accounting restatements on the financial markets and the resulting decline in the value of equity and

debt securities we hold;

o The frequency and severity of insured loss events;

o Changes affecting mortality, morbidity and other factors that may impact the profitability of our insurance products;

o Changes affecting interest rate levels and continuing low or rapidly changing interest rate levels; interest rate levels and continuing low or rapidly changing interest rate levels; o Changes affecting

o Changes affecting currency exchange rates, in particular the EUR/USD and EUR/GBP exchange rates;

o Increasing levels of competition in the United States, the Netherlands, the United Kingdom and emerging markets;

o Changes in laws and regulations, particularly those affecting our operations, the products we sell, and the attractiveness of certain products to our consumers;

o Regulatory changes relating to the insurance industry in the jurisdictions in which we operate;

o Acts of God, acts of terrorism, acts of war and pandemics;

o Effects of deliberations of the European Commission regarding the aid we received from the Dutch State in December 2008;

o Changes in the policies of central banks and/or governments;

o Litigation or regulatory action that could require us to pay significant damages or change the way we do business;

o Customer responsiveness to both new products and distribution channels;

o Competitive, legal, regulatory, or tax changes that affect the distribution cost of or demand for our products;

o Our failure to achieve anticipated levels of earnings or operational efficiencies as well as other cost saving initiatives; and

o The impact our adoption of the International Financial Reporting Standards may have on our reported financial results and financial condition.

Further details of potential risks and uncertainties affecting the company are described in the company’s filings with Euronext Amsterdam and the US Securities

and Exchange Commission, including the Annual Report on Form 20-F. These forward-looking statements speak only as of the date of this document. Except as

required by any applicable law or regulation, the company expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any

forward-looking statements contained herein to reflect any change in the company’s expectations with regard thereto or any change in events, conditions or

circumstances on which any such statement is based.

Local knowledge. Global power. 45